UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended June 30, 20222023

OR

☐

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______ to _______

Commission File Number 000-56115

Woodbridge Liquidation Trust

(Exact name of registrant as specified in its charter)

Delaware

| | 36-7730868

|

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

201 N. Brand Blvd., Suite M

Glendale, California | | 91203

|

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (310) 765-1550

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s)

| Name of each exchange on which registered |

None

| N/A | N/A |

Securities registered pursuant to Section 12(g) of the Act:

Class A Liquidation Trust Interests

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | Large accelerated filer ☐ | Accelerated filer ☐ |

| | Non-accelerated filer ☐☒ | Smaller reporting company ☒ |

| | | Emerging growth company ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestingattestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 762(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

At December 31, 2021,2022, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the registrant’s shares of Class A Liquidation Trust Interests held by non-affiliates of the registrant was approximately $104.76$28.60 million based upon the average bid and ask price of $9.16.$2.50. As of December 31, 2021,2022, there were approximately 11.44 million shares of Class A Liquidation Trust Interests held by non-affiliates.

APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY

PROCEEDINGS DURING THE PRECEDING FIVE YEARS:

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. ☒�� Yes ☐ No

DOCUMENTS INCORPORATED BY REFERENCE

None

Table of Contents

| | | Page |

| Part I | | |

| Item 1. | | 1 |

| Item 1A. | | 1821 |

| Item 1B. | | 2629

|

Item 1C.

| Cybersecurity

| 29

|

| Item 2. | | 2629

|

| Item 3. | | 2730 |

| Item 4. | | 3035 |

| |

| |

| Part II |

| |

| Item 5. | | 3136 |

| Item 6. | | 32

37 |

| Item 7. | | 3338 |

| Item 7A. | | 4147 |

| Item 8. | | 4147 |

| Item 9. | | 4147 |

| Item 9A. | | 4247 |

| Item 9B. | | 4247 |

| Item 9C. | | 4247 |

| | | |

| Part III | | |

| Item 10. | | 4348 |

| Item 11. | | 4651 |

| Item 12. | | 5258 |

| Item 13. | | 5359

|

| Item 14. | | 5562 |

| | | |

| Part IV | | |

| Item 15. | | 5663 |

CAUTIONARY NOTE ABOUT FORWARD-LOOKING STATEMENTS

The Woodbridge Liquidation Trust (the “Trust”) is a Delaware statutory trust. It was formed on February 15, 2019, the effective date (the “Plan Effective Date”) of the First Amended Joint Chapter 11 Plan of Liquidation dated August 22, 2018 of Woodbridge Group of Companies, LLC and Its Affiliated Debtors (the “Plan”). The Trust was formed to implement the terms of the Plan. The Plan was confirmed by the United States Bankruptcy Court for the District of Delaware (the “Bankruptcy Court”) on October 26, 2018 in the jointly administered chapter 11 bankruptcy cases (the “Bankruptcy Cases”) of Woodbridge Group of Companies, LLC and its affiliated chapter 11 debtors (collectively, the “Debtors”), Case No. 17-12560 (JKS).

In this Annual Report on Form 10-K (“Annual Report”), all beneficial interests in the Trust, including both Class A Liquidation Trust Interests (“Class A Interests”) and Class B Liquidation Trust Interests (“Class B Interests”), are collectively referred to as “Liquidation Trust Interests.”

The material terms of the Plan which relate to holders of Liquidation Trust Interests (the “Interestholders”) are described in this Annual Report, as well as in the Disclosure Statement for the First Amended Joint Chapter 11 Plan of Liquidation of The Woodbridge Group of Companies, LLC and Its Affiliated Debtors (the “Disclosure Statement”). The Disclosure Statement was approved by the Bankruptcy Court on August 22, 2018 and was distributed or made available to creditors of the Debtors and other parties in interest pursuant to Section 1125 of Title 11 of the United States Code (the “Bankruptcy Code”).

A copy of the Plan is referenced as Exhibit 2.1 to this Annual Report. A copy of the order of the Bankruptcy Court confirming the Plan is referenced as Exhibit 99.1 hereto.

Statements Regarding Forward-Looking Statements. This Annual Report, and other filings by the Trust with the U.S. Securities and Exchange Commission (“SEC”), or written statements made by the Trust in press releases or in other communications, oral or written, may contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, as codified in Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act” and, together with the Securities Act, the “Acts”). Such statements include, without limitation, financial guidance and projections and statements with respect(other than historical facts) that address future plans, goals, expectations, activities, events or developments. The Trust has tried, where possible, to expectation of future financial condition, changes in net assets in liquidation, cash flows, plans, targets, goals, objectives, performance, and termination and dissolution of the Trust. Such forward-looking statements also include statements that are preceded by, followed by, or that include theuse words such as “anticipates”, “if”, “believes,” “estimates,” “plans,” “expects,” “intends,” “is anticipated,” “will continue,” “project,” “may,” “could,” “would,”“forecasts”, “initiative, “objective”, “goal, “projects”, “outlook”, “priorities”, “target”, “evaluate”, “pursue”, “seek”, “potential”, “continue”, “designed”, “impact”, “may”, “could”, “would”, “should”, “will” and similar expressions and all other statements that are not historical facts. All suchto identify forward-looking statements. Forward-looking statements are based on the Trust’s current expectations and involveare subject to substantial risks, uncertainties and uncertaintiesother factors, many of which may cause actual results to differ materially from those set forth in such statements.are beyond our control and not of all of which can be predicted by the Trust. Such risks and uncertainties include the amount of sales proceeds, timing of sales of real estate assets, amount of funds needed for warrantyconstruction defect and other claims, punch list items and holding costs of the single-family homes, amount of general and administrative costs, the number and amount of successful litigations and/or settlements and the ability to recover thereon, the amount of funding required to continue litigations, the continuing impact of the COVID-19 pandemic and other global health issues, interest rates, adverse weather conditions in the regions in which properties to be sold are located, inflation, domestic and global economic and political conditions, changes in tax and other governmental rules and regulations applicable to the Trust and its subsidiaries, and other risks identified and described in “Item 1A. Risk Factors” of this Annual Report. Accordingly, the Trust cannot guarantee that any forward-looking statements will be realized, as actual results may differ materially from those identified or implied in any forward-looking statement. These risks and uncertainties are beyond the ability of the Trust to control, and in many cases, the Trust cannot predict the risks and uncertainties that could cause its actual results to differ materially from those indicated by the forward-looking statements.

In connection with the “safe harbor” provisions of the Acts, the Trust has identified and is disclosing important factors, risks and uncertainties that could cause its actual results to differ materially from those projected in forward-looking statements made by the Trust, or on the Trust’s behalf. (See “Item 1A. Risk Factors” of this Annual Report.) These cautionary statements are to be used as a reference in connection with any forward-looking statements. The factors, risks and uncertainties identified in these cautionary statements are in addition to those contained in any other cautionary statements, written or oral, which may be made or otherwise addressed in connection with a forward-looking statement or contained in any of the Trust’s subsequent filings with the SEC. Because of these factors, risks and uncertainties, the Trust cautions against placing undue reliance on forward-looking statements. Although the Trust believes that the assumptions underlying forward-looking statements are currently reasonable, any of the assumptions could be incorrect or incomplete, and there can be no assurance that forward-looking statements will prove to be accurate. Forward-looking statements speak only as of the date on which they are made. Except as may be required by law, the Trust does not undertake any obligations to modify, update or revise any forward-looking statement to take into account or otherwise reflect subsequent events, corrections in or revisions of underlying assumptions, or changes in circumstances arising after the date that the forward-looking statement was made.

The Trust and its wholly-owned subsidiary Woodbridge Wind-Down Entity LLC (the “Wind-Down Entity”) were formed pursuant to the Plan. The purpose of the Trust is to prosecute various causes of action owned by the Trust (the “Causes of Action”), to litigate and resolve claims filed against the Debtors, to pay allowed administrative and priority claims against the Debtors (including professional fees), to receive cash from certain sources and, in accordance with the Plan, to make distributions of cash to Interestholders subject to the retention of various reserves and after the payment of Trust expenses and administrative and priority claims. The Trust has no other purpose. Sources and potential sources of cash include the net proceeds from settlements of various Causes of Action, remittances of cash distributed from the Wind-Down Entity, “Fair Fund” recoveries from the SEC, and assets forfeited to the U.S. Department of Justice by former owners and principals of the Debtors (“Forfeited Assets”).

The purpose of the Wind-Down Entity is, through its subsidiaries (the “Wind-Down Subsidiaries” and, with the Wind-Down Entity, the “Wind-Down Group”), to develop (as applicable), market, and sell the real estate assets owned by the Wind-Down Subsidiaries to generate cash to be remitted to the Trust after the payment of Wind-Down Group expenses and subject to the retention of various reserves. The Trust, the Remaining Debtors (as defined in Section B of this Item 1) and the Wind-Down Group are collectively referred to in this Form 10-KAnnual Report as the “Company.”

Most of the Debtors filed for chapter 11 bankruptcy protection in December 2017 (certain other Debtors filed cases on later dates). During the Bankruptcy Cases, the major constituencies reached agreements on several matters, including new management for the Debtors, the manner and timing of the liquidation of the Debtors’ assets, and relative priorities to such distributions among creditors. Certain of these agreements were embodied in the Plan, which was confirmed in October 2018 and became effective on February 15, 2019. Under the Plan, holders of certain claims against the Debtors received Class A Interests, which became registered pursuant to Section 12(g) of the Exchange Act on December 24, 2019.

The Trust will be terminated upon the first to occur of (i) the making of all distributions required to be made and a determination by the Liquidation Trustee that the pursuit of additional Causes of Action held by the Trust is not justified or (ii) February 15, 2024. However, the Bankruptcy Court may approve an extension of the term if deemed necessary to facilitate or complete the recovery on, and liquidation of, the Trust’s assets.

During the year ended June 30, 2023, the Company concluded that its liquidation activities would not be completed by February 15, 2024, the current outside termination date of the Trust, for a number of reasons. First, there have been significant delays in certain legal proceedings where the Company is the plaintiff as more fully described in "Item 3. Legal Proceedings". Second, a construction defect claim has been asserted against one of the Wind-Down Subsidiaries by the buyer of one of the subsidiary’s single-family homes. The subsidiary has tendered the claim to its insurance carrier. At this time, the amount of the liability exposure, if any, has not been determined and it is not known if the subsidiary has any exposure in excess of its insurance coverage. The subsidiary is investigating the claim, including the extent and causes of the alleged damage and the identification of other potentially responsible persons. Based on the foregoing, the Company currently projects a revised estimated completion date for the Company’s operations of approximately March 31, 2026.

The Company is required to file a motion with the Bankruptcy Court to extend the termination date of the Trust beyond February 15, 2024. The motion is required to be filed within six months before February 15, 2024. The Company expects that the motion will be filed as required and that the Bankruptcy Court will grant the motion as the extension is needed to pursue additional Trust actions that are expected to yield additional proceeds to the Trust and to address the construction defect claim.

The Trust is administered by a Liquidation Trustee. The Liquidation Trustee is authorized, subject to the oversight of a six-member supervisory board (the “Supervisory Board”), to carry out the purposes of the Trust. The Wind-Down Entity iswas initially managed by a three-member board of managers (the “Board of Managers”), one of whom iswas the chief executive officer.Chief Executive Officer. The Board of Managers was reduced to two members following the effectiveness of the Chief Executive Officer’s resignation on December 31, 2022, and was reduced to one person on April 29, 2023, following the sale of the last single-family home and the resignation of Richard Nevins.

Pursuant to the Plan and the Liquidation Trust Agreement of the Trust (as amended, the “Trust Agreement”), a copy of which is referenced as Exhibits 3.2, 3.3 and 3.4 to this Annual Report, distributions to Interestholders are net of any costs and expenses incurred by the Trust, including in connection with administering the Trust and litigating or otherwise resolving the various Causes of Action and disputed claims. Amounts withheld from distribution may include cost of collecting, administering, distributing, and liquidating the Trust assets such as fees and expenses of the Liquidation Trustee, reserves for contingent liabilities, premiums for directors’ and officers’ insurance, and fees and expenses of attorneys and consultants. Furthermore, cash received from the Wind-Down Group is net of the payment of Wind-Down Group expenses and the retention of reserves by the Wind-Down Group.Group for contingent liabilities, including potential construction defect claims.

Distributions will be made by the Trust only to the extent that the Trust has sufficient net assets (over amounts retained for contingent liabilities and future costs and expenses, among other things) to make such payments in accordance with the Plan and the Trust Agreement. No distribution is required to be made to any Interestholder unless such Interestholder is to receive in such distribution at least $10.00. If the Trust mails a distribution check to an Interestholder and the Interestholder fails to cash the check within 180 calendar days, or if the Trust mails a distribution check to an Interestholder and such check is returned to the Trust as undeliverable and is not claimed by the Interestholder within 180 days, then the Interestholder may not only lose its right to the amount of that distribution, but also may be deemed to have forfeited its right to any reserved and future distributions under the Plan.

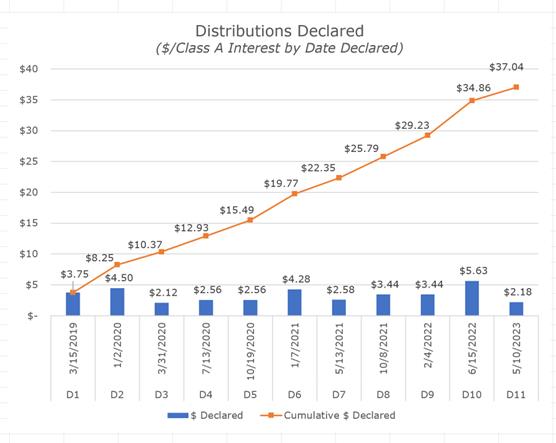

Distributions will be made at the sole discretion of the Liquidation Trustee in accordance with the provisions of the Plan and the Trust Agreement. Since the Plan Effective Date, the Liquidation Trustee and the Supervisory Board have authorized teneleven cash distributions to the holders of Class A Interests.On August 3, 2023, at the recommendation of the Liquidation Trustee, the Trust suspended the making of additional Trust distributions pending the result of the investigation of a construction defect claim asserted against one of the Wind-Down Subsidiaries by the buyer of one of the subsidiary's single-family homes.

Part I

Item 1. Business (Continued)

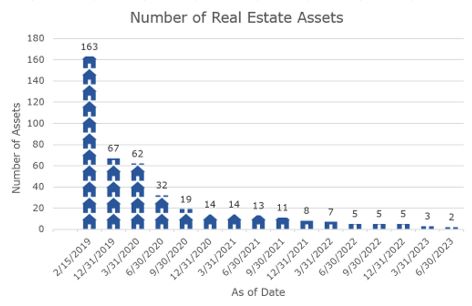

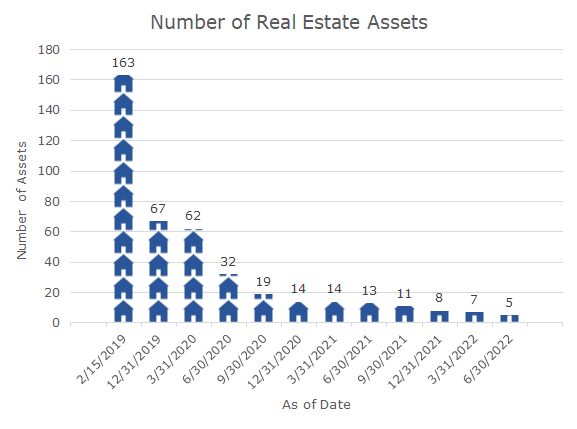

Since its inception, the Wind-Down Entity has made substantial progress toward completion of its liquidation activities and is nearing the end of the liquidation of itshas liquidated all but two real estate portfolio.assets with a net carrying value of approximately $0.77 million. Holders of Liquidation Trust Interests are advised that future distributions from the Trust, if any, will be limited. Once the Company’s remaining real property assets have been liquidatedlimited and the net proceeds resulting therefrom, net of reserves, have been distributed, further distribution(s) will be solelymaterially reliant on future recoveries from litigation, net of accrued liquidation costs, including amounts for potential construction defect claims, which are uncertain and the amount and timing of which, if any, are difficult to determine.

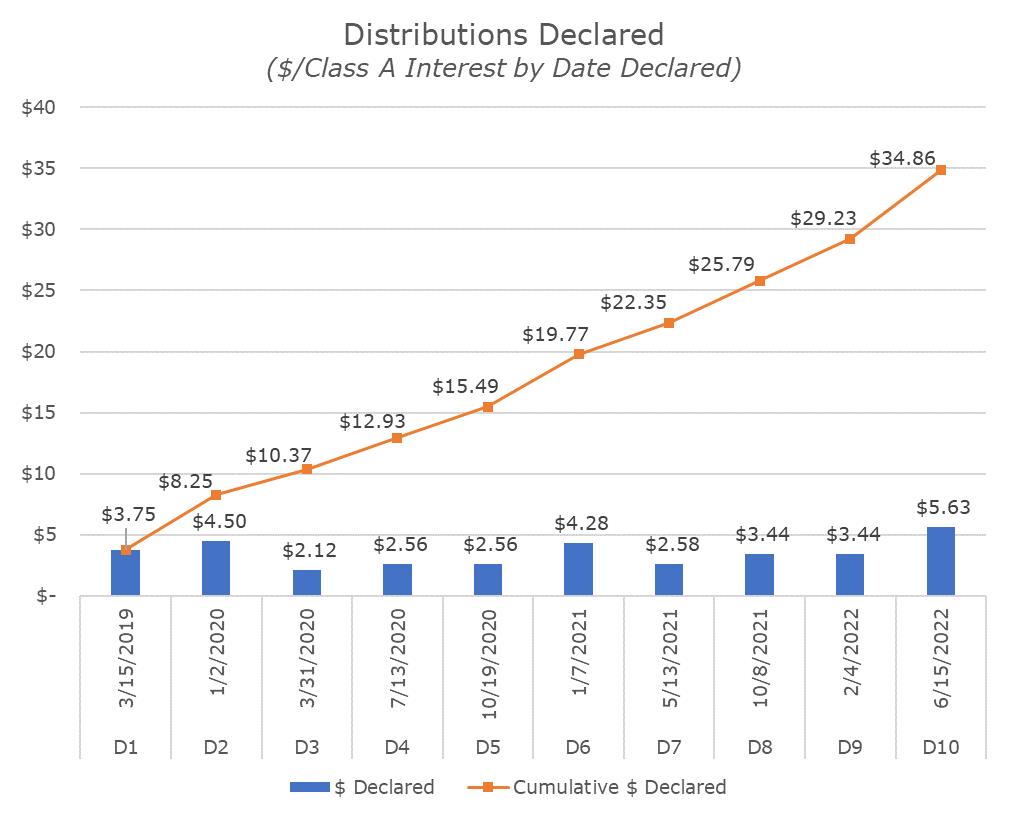

The following table shows the Trust’s teneleven cash distributions to Class A Interestholders since its February 15, 2019 Plan Effective Date:

The Trust’s distributions have primarily come from the net proceeds of real estate sales, except for the ninth distribution, which included the Trust’s net proceeds from the settlement of litigation against Comerica Bank.

23

Part I

Item 1.

| Business (Continued) |

Item 1. Business (Continued)

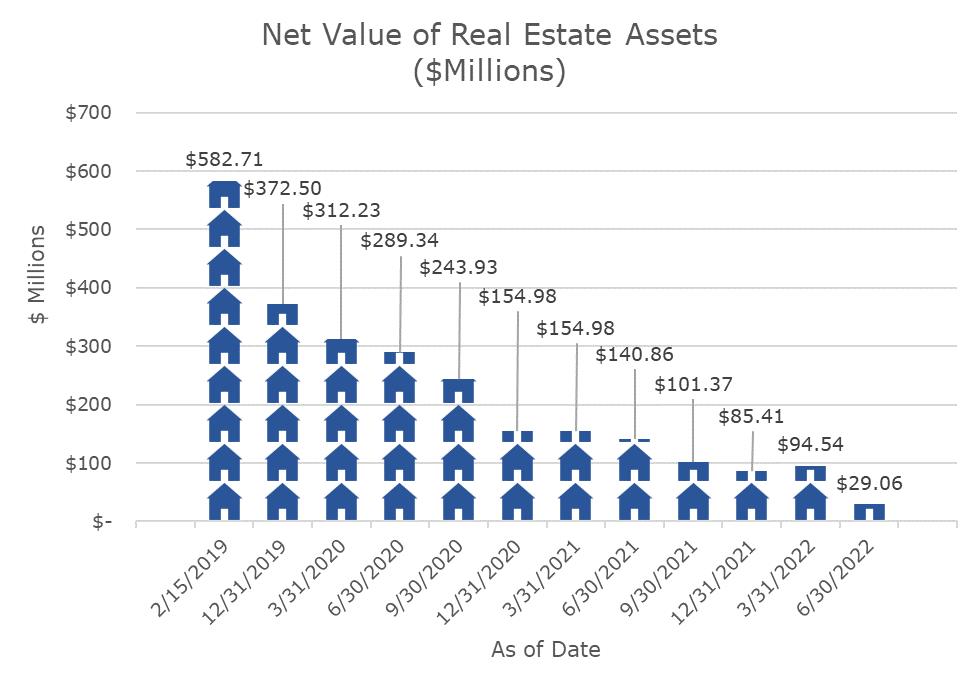

Reflective of the progress toward the completion of its liquidation activities, the following two tables show the Trust’sWind-Down Group’s decreasing number of real estate assets and amount of net carrying values of the real estate assets since the Plan Effective Date and through June 30, 2022:2023:

Part I

Item 1. Business (Continued)

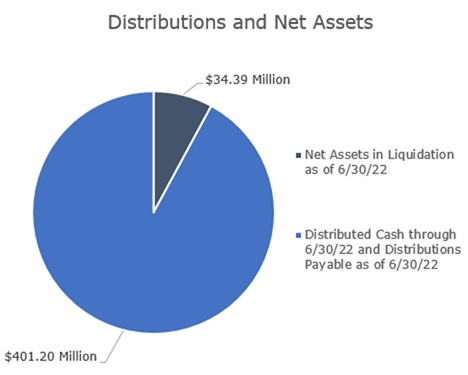

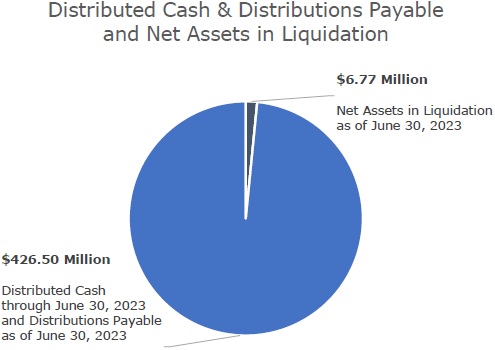

The Trust’s distributed cash through June 30, 2022 and2023, together with its distributions payable as of June 30, 20222023, totaled approximately $401.2$426.55 million. The Trust’s consolidated net assets in liquidation as of June 30, 2022 was2023 were approximately $34.39$6.77 million.

| B. | Organization of the Company |

On the Plan Effective Date, the Plan was implemented, and the Trust and the Wind-Down Entity were formed.

1. The Trust

The Trust was established for the benefit of its Interestholders and for the purpose of collecting, administering, distributing and liquidating the Trust assets in accordance with the Plan and the Trust Agreement, to resolve disputed claims asserted against the Debtors, to litigate and/or settle the Causes of Action, and to pay certain allowed claims and statutory fees, in each case to the extent required by the Plan. The Trust has no objective to continue or engage in the conduct of a trade or business, except to the extent reasonably necessary to, and consistent with, the purpose of the Trust as set forth in the Plan.

By operation of the Plan, (i) the real estate assets of the Debtors were automatically vested in the Wind-Down Group; (ii) all existing equity interests in Woodbridge Group of Companies, LLC and Woodbridge Mortgage Investment Fund 1, LLC (together, the “Remaining Debtors”) were cancelled and extinguished and new equity interests in the Remaining Debtors, representing all of the issued and outstanding equity interests of the Remaining Debtors, were issued to the Trust; and (iii) all of the Debtors other than the Remaining Debtors were automatically dissolved.

As of the Plan Effective Date, each of the Debtors’ directors, officers and managers was terminated and the Trust succeeded to all of their powers in respect of the assets vested in the Trust. Each of the Debtors other than the Remaining Debtors was automatically dissolved on the Plan Effective Date pursuant to the Plan.

By operation of the Plan, the following assets were transferred to the Trust on the Plan Effective Date:

an aggregate of $5.0 million in cash from the Debtors for the purpose of funding the Trust’s initial expenses of operation;

the following Causes of Action: (i) all claims and causes of action formerly held or acquired by the Debtors and (ii) all causes of action contributed by Noteholders or Unitholders (as defined in Section C of this Item 1) to the Trust as “Contributed Claims” pursuant to the Plan;

all of the outstanding membership interests of the Wind-Down Entity; and

certain other non-real estate related assets and entities.

On the Plan Effective Date and by operation of the Plan, the Wind-Down Entity became a wholly-owned subsidiary of the Trust. The Wind-Down Entity was organized for the purpose of accepting, holding, and administering the Debtors’ real estate assets and distributing the net proceeds of liquidating such real estate assets to the Trust in accordance with the Plan and the Limited Liability Company Agreement of the Wind-Down Entity (the(as amended, the “Wind-Down Entity LLC Agreement”), consistent with the purposes of the Trust. As of the Plan Effective Date, the Wind-Down Group received, in the aggregate, assets consisting of approximately $31.34 million in cash and approximately $585.01 million of real estate and other assets.

| C. | 4

Part I

Item 1. Business (Continued)

C.Material Developments Leading to Confirmation of the Plan

|

Prior to the commencement of the Bankruptcy Cases, the Debtors were part of a group of more than 275 affiliated entities formed by, and formerly controlled by, Robert Shapiro (“Shapiro”) which were used by Shapiro to perpetrate a large-scale “Ponzi” scheme. As part of the scheme, Shapiro is believed to have used the group of affiliated entities to raise more than $1.22 billion from over 10,000 investors nationwide. Money was raised in the form of one of two primary products: (1) five-year private placement products that were styled, marketed or sold as “units” in Woodbridge Mortgage Investment Fund 1, LLC, Woodbridge Mortgage Investment Fund 2, LLC, Woodbridge Mortgage Investment Fund 3, LLC, Woodbridge Mortgage Investment Fund 3a, LLC, Woodbridge Mortgage Investment Fund 4, LLC, Woodbridge Commercial Bridge Loan Fund 1, LLC, and Woodbridge Commercial Bridge Loan Fund 2, LLC (each, a “Fund Debtor”) and (2) purportedly secured promissory products of 12 to 18 months that were styled, marketed or sold as “notes,” “mortgages” or “loans” by one or more Fund Debtors. In this Annual Report, any and all investments, interests or other rights with respect to any of the Fund Debtors that were styled, marketed or sold as “units” are referred to as “Units” and the holders of Units are referred to as “Unitholders.” Similarly, in this Annual Report, any and all investments, interests or other rights with respect to any of the Fund Debtors that were styled, marketed or sold as “notes,” “mortgages” or “loans” are referred to as “Notes” and the holders of Notes are referred to as “Noteholders.”

The proceeds of the sale of Units and Notes were not used for the purposes that were represented to investors, but were instead used to pay (i) over $400 million of “interest” and “principal” to existing investors, (ii) approximately $64.5 million in commissions to sales agents engaged in the sale of the investments, and (iii) at least $21.2 million for the personal benefit of Shapiro or his related entities or family members (including, for example, the purchase of luxury items, travel, wine, and the like). Additionally, the Debtors and Shapiro used investor funds to purchase at least 193 residential and commercial properties located primarily in Los Angeles, California, and Carbondale, Colorado. The Debtors had one segment, known as “Riverdale,” which did, in fact, originate loans to unrelated third parties, but the dollar amount of these third-party loans was a fraction of the amount of the loans made to disguised affiliates.

In the years leading up to the commencement of their Bankruptcy Cases, the Debtors faced a variety of inquiries from state and federal regulators. In particular, in or around September 2016, the SEC began investigating certain of the Debtors (and certain non-debtor affiliates) in connection with possible securities law violations, including the alleged offer and sale of unregistered securities, the sale of securities by unregistered brokers, and the commission of fraud in connection with the offer, purchase, and sale of securities.

In late 2017, the Debtors found it increasingly difficult to raise new capital from investors. The Debtors were unable to make the December 1, 2017 interest and principal payments due on the Notes. Shapiro hired an outside financial restructuring firm and a chief restructuring officer to manage the Debtors on or about December 1, 2017, and on December 4, 2017 chapter 11 bankruptcy cases for 279 of the Debtors were commenced (cases for the 27 other Debtors were filed on later dates). An immediate effect of commencement of the Bankruptcy Cases was the imposition of the automatic stay under Bankruptcy Code section 362(a), which, with limited exceptions, enjoined the commencement or continuation of all collection efforts by creditors, the enforcement of liens against property of the Debtors, and the continuation of litigation against the Debtors during the pendency of the Bankruptcy Cases. Under Chapter 11 of the Bankruptcy Code, a company may continue to operate its business under the supervision of the Bankruptcy Court while it attempts to reorganize.

As of the commencement of the Bankruptcy Cases, certain discovery-related disputes regarding administrative subpoenas issued by the SEC were proceeding before the United States District Court for the Southern District of Florida, but the SEC had not yet asserted any claims against any of the Debtors or their affiliates. Subsequent to the commencement of the Bankruptcy Cases, the SEC commenced legal proceedings in the Florida district court against, among other defendants, Shapiro, a trust related to Shapiro or his family, and the Debtors.

Part I

Item 1. Business (Continued)

In addition to the SEC investigation, certain of the Debtors received information requests from state securities regulators in approximately 25 states. As of the commencement of the Bankruptcy Cases, regulators in eight states had filed civil or administrative actions against one or more of the Debtors and certain of their sales agents, alleging they engaged in the unregistered offering of securities in their respective jurisdictions and unlawfully acted as unregistered investment advisors or broker-dealers. Six states—Massachusetts, Texas, Arizona, Pennsylvania, South Dakota and Michigan—entered permanent cease and desist orders against one or more of the Debtors related to their alleged unregistered sale of securities. Several of these inquiries were resolved prior to the commencement of the Bankruptcy Cases through settlements, which included the entry of consent orders. Certain of the Debtors entered into consent orders with California, Arizona, Michigan, Oregon, Idaho, and Colorado during the Bankruptcy Cases.

On December 14, 2017, the Office of the United States Trustee for the District of Delaware (the “U.S. Trustee’s Office”) formed the Official Committee of Unsecured Creditors (the “Unsecured Creditors’ Committee”). On December 20, 2017, the SEC filed its action in the Florida district court, as discussed above, detailing much of the massive fraud perpetrated by Shapiro before the commencement of the Bankruptcy Cases. The SEC asked the Florida district court to appoint a receiver who would displace the Debtors’ management in the Bankruptcy Cases, but the Florida district court declined to immediately act on this request in light of the pending Bankruptcy Cases.

On December 28, 2017, the Unsecured Creditors’ Committee filed a motion seeking appointment of a chapter 11 trustee to replace the Debtors’ management team, arguing that the team was “hand-picked by Shapiro, and ha[d] done his bidding both before and after the filing of these cases.” The SEC later made a similar request, arguing that the new “independent” management team was “completely aligned [with Shapiro] in controlling this bankruptcy.”

On or about January 23, 2018, the Debtors, the Unsecured Creditors’ Committee, the SEC, and groups of Noteholders and Unitholders entered into a term sheet (the “Joint Resolution”) that resolved the trustee motions and several other matters. The Joint Resolution included, among other provisions, the following key provisions:

| • | A new board of managers (with no ties whatsoever to Shapiro) was formed to govern the Debtors (the “New Board”). The New Board consisted of Richard Nevins, M. Freddie Reiss, and Michael Goldberg. |

The New Board was empowered to select a CEO or CRO, subject to the consent of the Unsecured Creditors’ Committee and the SEC.

The New Board was empowered, subject to the SEC’s consent, to select new counsel for the Debtors or to re-confirm Gibson Dunn & Crutcher LLP as counsel for the Debtors.

| • | The holders of Units were permitted to form a single one- or two-member fiduciary Unitholder committee (the “Unitholder Committee”) to advocate for the interests of Unitholders. |

| • | The holders of Notes were permitted to form a single six- to nine-member fiduciary Noteholder committee (the “Noteholder Committee”) to advocate for the interests of Noteholders. |

As authorized by the Joint Resolution, the New Board selected Frederick Chin to serve as the Chief Executive Officer and Bradley D. Sharp to serve as the Chief Restructuring Officer during the pendency of the Bankruptcy Cases. Under the direction of the New Board, the Debtors also retained and employed Development Specialists, Inc. as the Debtors’ restructuring advisor and Klee, Tuchin, Bogdanoff & Stern LLP (n/k/a KTBS Law LLP) as new bankruptcy co-counsel to represent them in the Bankruptcy Cases with Young Conaway Stargatt & Taylor LLP.

On April 16, 2018, the Debtor defendants in the Florida proceedings entered into a consent agreement with the SEC and consented to the entry of a judgment. Under the consent agreement and the judgment, the Debtors agreed, among other things, that (i) the Debtor defendants would be permanently enjoined from violations of certain sections of the Securities Act and the Exchange Act; (ii) upon motion of the SEC, the Florida district court would determine whether it was appropriate to order disgorgement and/or a civil penalty against the Debtor defendants, and if so, the amount of any such disgorgement and/or civil penalty; and (iii) in connection with any hearing regarding disgorgement and/or a civil penalty, inter alia, the Debtor defendants would be precluded from arguing that they did not violate the federal securities laws as alleged in the SEC action and the Debtor defendants would not challenge the validity of the consent agreement or judgment. On May 1, 2018, the Bankruptcy Court approved the consent agreement and the judgment. On May 21, 2018, the Florida district court entered the judgment against the Debtor defendants in the SEC action and entered an order administratively closing such action. The Debtors reached a settlement with the SEC to resolve the disgorgement and civil penalty claims asserted by the SEC against the Debtor defendants.

Part I

Item 1. Business (Continued)

During the Bankruptcy Cases, the Debtors sold numerous parcels of owned real property, in each case with Bankruptcy Court approval. Additionally, the major constituencies in the Bankruptcy Cases reached agreements on several matters, including new management for the Debtors, the manner and timing of the liquidation of the Debtors’ assets, and the relative priorities to such distributions among creditors, certain of which agreements were embodied in the Plan.

Under the Plan, on the Plan Effective Date, former Noteholders, Unitholders, and general unsecured creditors holding allowed claims were granted Class A Interests in exchange for their claims. Pursuant to a compromise in the Plan, former Unitholders also received Class B Interests (Unitholders received Class A Interests on account of only 72.5% of their allowed Unit Claims and received Class B Interests on account of the remaining 27.5% of their allowed Unit Claims).

The Plan incorporated a “netting” mechanism for Note and Unit investors whereby such investors received Liquidation Trust Interests based on their “Net” Note Claim (defined as claims arising from or in connection with any Notes) or their “Net” Unit Claim (defined as claims arising from or in connection with any Units). The netting was achieved by reducing the Note or Unit claim by the aggregate amount of all pre-bankruptcy distributions received by the Noteholder or Unitholder (other than return of principal). For example, a Noteholder holding a Note with a face amount of $100,000 who received $10,000 of “interest” before the Debtors filed bankruptcy would be deemed to hold a Net Note Claim of $90,000. Such Noteholder would receive Class A Interests on account of a $90,000 Net Note Claim.

On December 24, 2019, the Trust’s Registration Statement on Form 10 became effective under the Exchange Act. The trading symbol for the Trust’s Class A Interests is WBQNL. Bid and ask prices for the Trust’s Class A Interests are quoted on the OTC Link® ATS, the SEC-registered alternative trading system. The Class A Interests are eligible for the Depository Trust Company’s Direct Registration (DRS) services. The Class B Interests are not registered with the SEC.

D.Plan Provisions Regarding the Company

| D. | Plan Provisions Regarding the Company |

| 1. | Corporate governance provisions |

Under the Plan and the Wind-Down Entity LLC Agreement, the Trust is required at all times to be the sole and exclusive owner of all membership interests of the Wind-Down Entity. The Trust is prohibited from selling, transferring, or otherwise disposing of its membership interests in the Wind-Down Entity without approval of the Bankruptcy Court, and the Wind-Down Entity is prohibited from issuing any equity interest to any other person. Under

Formerly under the Plan and the Wind-Down Entity LLC Agreement, the Wind-Down Entity iswas required to be managed by a three-member boardBoard of managers,Managers, one of whom iswas required to be the chief executive officer. SinceChief Executive Officer. Accordingly, the Plan Effective Date, the board of managers of the Wind-Down Entity (the “Board of Managers”) has initially consisted of Richard Nevins, M. Freddie Reiss, and Frederick Chin, with Mr. Chin as the Chief Executive Officer of the Wind-Down Entity. On November 30, 2022, the Wind-Down Entity LLC Agreement was amended to reduce the Wind-Down Entities’ Board of Managers to two members and to eliminate the chief executive officerrequirement that the Chief Executive Officer serve as a member of the Board of Managers, effective upon Mr. Chin’s resignation on December 31, 2022. Marion W. Fong was appointed to serve as Chief Executive Officer of the Wind-Down Entity has been Frederick Chin. Theeffective as of January 1, 2023. Ms. Fong is not a member of the Board of Managers. On March 27, 2023, the Wind-Down Entity is also conducting business underLLC Agreement was further amended and the name “Viewpoint Collection.”Board of Managers was reduced to one person, M. Freddie Reiss, following the sale of the last single-family home and the resignation of Richard Nevins on April 29, 2023.

The Wind-Down Entity is required to advise the Trust regarding its affairs on at least a monthly basis, reasonably make available such information as is necessary for any reporting by the Trust and advise the Trust of material actions. Excess cash of the Wind-Down Entity (cash that is in excess of budgeted reserve for ongoing operations and other anticipated obligations including potential construction defect claimsand expenses as determined by the Board of Managers) is required to be remitted to the Trust on a quarterly basis, and the Wind-Down Entity is restricted in its ability to invest or gift any of its assets or make asset acquisitions.

The Bankruptcy Court has retained certain jurisdiction regarding the Trust, the Liquidation Trustee, the Supervisory Board, the Wind-Down Entity, the Board of Managers, and assets of the Trust and the Wind-Down Entity, including the determination of all disputes arising out of or related to administration of the Trust and the Wind-Down Entity.

Part I

Item 1. Business (Continued)

The Wind-Down Entity is also conducting business under the name “Viewpoint Collection.”

| 2. | Treatment under the Plan of holders of claims against and equity interests in the Debtors |

The Plan identified 12 types of Claims against and equity interests in the Debtors, eight of which were “classified” (i.e., placed into formalized classes under the Plan) and four of which are not. Claims required to be paid in full under the Plan are referred to as “Unimpaired Claims.” Four types of claims are not classified—(i) claims arising under Bankruptcy Code sections 503(b), 507(a)(2), 507(b), or 1114(e)(2) (“Administrative Claims”Claims”), (ii) claims by professionals employed in the Bankruptcy Cases pursuant to Bankruptcy Code sections 327, 328, 1103, or 1104 for compensation or reimbursement of costs and expenses relating to services provided during the period from the Petition Date through and including the Plan Effective Date (“Professional Fee Claims”Claims”), (iii) tax claims entitled to priority under Bankruptcy Code section 507(a)(8) (“Priority Tax Claims”Claims”), and (iv) debtor-in-possession financing claims (“DIP Claims”Claims”). The foregoing claims are all Unimpaired Claims and have been or will be paid in full. Although the amounts may be subject to negotiation based on the Debtors’ and creditors’ records, and to ultimate determination, if necessary, in the Bankruptcy Court, liabilities resulting from any such Administrative Claims, Professional Fee Claims, Priority Tax Claims, and DIP Claims that are allowed are analogous, in substance, to accounts payable. As of September 23, 2022,27, 2023, there were no allowed and unpaid DIP claims.Claims. As of September 23, 2022,27, 2023, there were no unpaid Administrative Claims, approximately $.18 million of unpaid Priority Tax Claims and no remaining unpaid Professional Fee Claims.

The remaining eight types are claims and equity interests that have been classified. Classified claims and equity interests are treated in accordance with the priorities established under the Bankruptcy Code.

The classified claims and equity interests under the Plan are the following (each, a “Class” of claims or interests):

“Class 1 Claims” or “Other Secured Claims,” which are claims, other than DIP Claims, that are secured by a valid, perfected, and enforceable lien on property in which the Debtors have an interest, which lien is valid, perfected, and enforceable under applicable law and not subject to avoidance under the Bankruptcy Code or applicable non-bankruptcy law.

“Class 2 Claims” or “Priority Claims,” which are claims that are entitled to priority under Bankruptcy Code section 507(a), other than Administrative Claims and Priority Tax Claims.

“Class 3 Claims” or “Standard Note Claims,” which are any Note Claims other than Non-Debtor Loan Note Claims (as defined below).

“Class 4 Claims” or “General Unsecured Claims,” which are unsecured, non-priority claims that are not Note Claims, Subordinated Claims (as defined below), or Unit Claims.

“Class 5 Claims” or “Unit Claims,” which are Unit Claims (as defined in Item 1, Section C of this Annual Report).

“Class 6 Claims” or “Non-Debtor Loan Note Claims,” which are any Note Claims that are or were purportedly secured by an unreleased assignment or other security interest in any loans or related interests as to which the lender was a Debtor and the underlying borrower actually is or actually was a person that is not a Debtor.

“Class 7 Claims” or “Subordinated Claims,” which are collectively, (a) any claim, secured or unsecured, for any fine, penalty, or forfeiture, or for multiple, exemplary, or punitive damages, to the extent such fine, penalty, forfeiture, or damages are not compensation for actual pecuniary loss suffered by the holder of such claim and (b) any other claim that is subordinated to General Unsecured Claims, Note Claims, or Unit Claims pursuant to Bankruptcy Code section 510, a final order of the Bankruptcy Court, or by consent of the creditor holding such claim.

“Class 8” or “Equity Interests,” which are all previously issued and outstanding common stock, preferred stock, membership interests, or other ownership interests in any of the Debtors outstanding immediately prior to the Plan Effective Date.

Holders of Class 1 Claims are creditors of the Wind-Down Entity, and holders of Class 2 Claims are creditors of the Trust. Although the amounts may be subject to negotiation based on the Debtors’ and creditors’ records, and to ultimate determination, if necessary, in the Bankruptcy Court, liabilities resulting from any such claims that are allowed are analogous, in substance, to accounts payable. As of September 23, 2022,27, 2023, there were no allowed and unpaid Class 1 Claims or Class 2 Claims.

Part I

Item 1. Business (Continued)

Under the Plan, three Classes of claims, when the claims are allowed under the Plan, entitle the holders thereof to become holders of Liquidation Trust Interests. The holders of these claims belonged, as of the Petition Date, to one or more of the following categories:

Standard Note Claims (Class 3)

General Unsecured Claims (Class 4)

Unit Claims (Class 5)

Standard Note Claims are Claims arising from any and all investments, interests or other rights with respect to any of the seven Debtors identified as a “Fund Debtor” under the Plan that were styled, marketed or sold as “notes,” “mortgages,” or “loans.” As of September 23, 2022,27, 2023, the aggregate outstanding amount of allowed Class 3 Standard Note Claims (net of prepetition distributions of interest) was approximately $702.64$702.68 million, including those Class 6 Non-Debtor Loan Note Claims that were reclassified as Class 3 Standard Note Claims in accordance with the Plan. See “Holders of Non-Debtor Loan Note Claims” below. The Trust’s estimate of the aggregate outstanding amount of disputed Class 3 Standard Note Claims as of September 23, 202227, 2023 is approximately $0.05$0.02 million (in each case, net of prepetition distributions of interest).

General Unsecured Claims include any unsecured, non-priority claim asserted against any of the Debtors that is not a Note Claim, Subordinated Claim or Unit Claim, and generally include the claims of trade vendors, landlords, general liability claimants, utilities, contractors, employees and numerous others. As of September 23, 2022,27, 2023, the aggregate outstanding amount of allowed Class 4 General Unsecured Claims was approximately $5.98$5.97 million, and the Trust estimates that the aggregate outstanding amount of disputed Class 4 General Unsecured Claims as of September 23, 202227, 2023 was approximately $0.41$0.23 million.

Unit Claims are Claims arising from any and all investments, interests or other rights with respect to any of the seven Debtors identified as a “Fund Debtor” under the Plan that were styled, marketed or sold as “units.” As of September 23, 2022,27, 2023, the aggregate outstanding amount of allowed Class 5 Unit Claims was approximately $178.77 million, and the Trust estimates that the aggregate outstanding amount of disputed Class 5 Unit Claims as of September 23, 202227, 2023 was approximately $0.09 million (in each case, net of prepetition distributions of interest).

Holders of allowed claims in Classes 3, 4 and 5 are deemed to hold an amount and class of Liquidation Trust Interests that is prescribed by the Plan based on the amount of their respective claims, as follows:

| • | Each holder of an allowed claim in Class 3 (Standard Note Claims) is deemed to hold one (1) Class A Interest for each $75.00 of Net Note Claims held by the applicable Noteholder with respect to its Allowed Note Claims. |

| • | Each holder of an allowed claim in Class 4 (General Unsecured Claims) is deemed to hold one (1) Class A Interest for each $75.00 of allowed General Unsecured Claims held by the applicable creditor. |

| • | Each holder of an allowed claim in Class 5 (Unit Claims) is deemed to hold 0.725 of a Class A Interest and 0.275 of a Class B Interest for each $75.00 of Net Unit Claims held by the applicable Unitholder with respect to its allowed Unit Claims. |

In addition, under the Plan, holders of Standard Note Claims and Unit Claims were permitted, at the time they cast their votes on the Plan, to elect to contribute their causes of action against any non-released persons to the Trust for prosecution (the “Contributed Claims”). The relative share of the Trust recoveries for any so electing Noteholder or Unitholder in respect of its respective Class 3 Claim or Class 5 Claim has been enhanced by having the amount that otherwise would be the applicable Net Note Claim or Net Unit Claim increased by a multiplier of 105%, referred to as the “Contributing Claimant’s Enhancement Multiplier.” The Plan releases the Debtors, the members of the New Board, the Unsecured Creditors’ Committee, the Noteholder Committee, and the Unitholder Committee, and any party related to such persons from liability, but generally excludes from such release any prepetition insider of any of the Debtors, any non-debtor affiliates of the Debtors or insider of any such non-debtor affiliates, any prepetition employee of any of the Debtors involved in the marketing or sale of Notes or Units, and any other person involved in such marketing, including certain persons identified on a schedule attached to the Plan.

Distributions of cash by the Trust on account of Class A Interests and Class B Interests are required to be made in accordance with a prescribed priority, referred to as the “Liquidation Trust Interests Waterfall.” (See “Part I, Item 1. Business, D. Plan Provisions Regarding the Company, 4. Liquidation Trust Interests under the Plan.”) Fractional Liquidation Trust Interests, if any, are rounded in accordance with the rounding convention established by the Plan.

Part I

Item 1. Business (Continued)

Other Classes under the Plan include Subordinated Claims, Non-Debtor Loan Note Claims, and Equity Interests. Although holders of Subordinated Claims are not Interestholders of the Trust, they are deemed to have retained a residual right to receive any cash that remains in the Trust after the final administration of all the Trust assets and payment in full to holders of both Class A Interests and Class B Interests, including interest at the rate and to the extent set forth in the Plan. The Trust does not expect that there will be any such residual cash.

| 3. | Assets and liabilities of the Company |

The following is the Company’s consolidated statements of net assets in liquidation as of the Plan Effective Date and June 30, 20222023 ($ in millions):

| | | Plan Effective Date | | | June 30, 2023 | |

| | | | | | | |

| Net real estate assets held for sale, net | | $ | 582.71 | | | $ | 0.77 | |

| Cash and cash equivalents | | | 36.02 | | | | 25.70 | |

| Restricted cash | | | 0.32 | | | | 4.47 | |

| Other assets | | | 2.29 | | | | 2.65 | |

| | | | | | | | | |

| Total assets | | $ | 621.34 | | | $ | 33.59 | |

| | | | | | | | | |

| Accounts payable and accrued liabilities | | | 5.78 | | | | 0.04 | |

| Distributions payable | | | - | | | | 1.28 | |

| Accrued liquidation costs | | | 232.07 | | | | 25.50 | |

| | | | | | | | | |

| Total liabilities | | $ | 237.85 | | | $ | 26.82 | |

| | | | | | | | | |

| Net assets in liquidation: | | | | | | | | |

| Restricted for Qualifying Victims | | | - | | | | 3.49 | |

| All Interestholders | | | 383.49 | | | | 3.28 | |

| | | | | | | | | |

| Total net assets in liquidation | | $ | 383.49 | | | $ | 6.77 | |

| | | Plan | | | | |

| | | Effective | | | | |

| | | Date | | | June 30, 2022 | |

| | | | | | | |

| Net real estate assets held for sale, net | | $ | 582.71 | | | $ | 29.06 | |

| Cash and cash equivalents | | | 36.02 | | | | 96.81 | |

| Restricted cash | | | 0.32 | | | | 6.12 | |

| Other assets | | | 2.29 | | | | 5.83 | |

| | | | | | | | | |

| Total assets | | $ | 621.34 | | | $ | 137.82 | |

| | | | | | | | | |

| Accounts payable and accrued liabilities | | $ | 5.78 | | | $ | 0.12 | |

| Distributions payable | | | - | | | | 68.77 | |

| Accrued liquidation costs | | | 232.07 | | | | 34.54 | |

| | | | | | | | | |

| Total liabilities | | $ | 237.85 | | | $ | 103.43 | |

| | | | | | | | | |

| Net assets in liquidation: | | | | | | | | |

| Restricted for Qualifying Victims | | $ | - | | | $ | 3.48 | |

| All Interestholders | | | 383.49 | | | | 30.91 | |

| | | | | | | | | |

| Total net assets in liquidation | | $ | 383.49 | | | $ | 34.39 | |

The status of outstanding Unimpaired and Impaired Claims as of September 23, 202227, 2023 is summarized below, with amounts in millions:

| | | Estimated Allowed Claims | |

| | Disputed Claims at Asserted Amount | |

| Unimpaired Claims (Liabilities) | | $ | 0.13 | | | | $ | 0.45 | |

| Impaired Claims (Beneficial Interests) | | $ | 887.76 | | (a) | | $ | 0.46 | |

| | | Estimated Allowed Claims | | | | Disputed Claims at Asserted Amount | |

| Unimpaired Claims (Liabilities) | | $ | 0.13 | | | | $ | 0.49 | |

| Impaired Claims (Beneficial Interests) | | $ | 887.73 | (a) | | | $ | 0.55 | |

| (a) | Includes an estimated $0.34 million of additional claims expected to be allowed from the approximate $0.46 million of disputed claims. |

(a) Includes an estimated $0.34 million of additional claims expected to be allowed from the approximate $0.55 million of disputed claims.

Part I

Item 1. Business (Continued)

| 4. | Liquidation Trust Interests under the Plan |

Each holder of an allowed claim in the Plan’s Class 3 (Standard Note Claims), Class 4 (General Unsecured Claims) and Class 5 (Unit Claims) was granted one or more beneficial interests in the Trust (a Liquidation Trust Interest) of a class (i.e. either Class A and/or Class B) and in an amount prescribed by the Plan and the Trust Agreement, as follows:

In the case of an allowed claim in the Plan’s Class 3 (Standard Note Claims), the holder was granted one (1) Class A Interest in the Trust for each $75.00 of Net Note Claims held by the applicable Noteholder with respect to its Allowed Note Claims. Allowed Net Note Claims are determined as the outstanding principal amount of Note Claims held by a particular Noteholder, minus the aggregate amount of all prepetition distributions (other than return of principal) received by such Noteholder.

In the case of an allowed claim in the Plan’s Class 4 (General Unsecured Claims), the holder was granted one (1) Class A Interest in the Trust for each $75.00 of allowed General Unsecured Claims held by the applicable creditor.

In the case of an allowed claim in the Plan’s Class 5 (Unit Claims), the holder was granted 0.725 of a Class A Interest in the Trust and 0.275 of a Class B Interest in the Trust for each $75.00 of Net Unit Claims held by the applicable Unitholder with respect to its allowed Unit Claims. Allowed Net Unit Claims were determined as the outstanding principal amount of Unit Claims held by a particular Unitholder, minus the aggregate amount of all prepetition distributions (other than return of principal) received by such Unitholder.

The Plan permitted Noteholders and Unitholders to contribute certain causes of action (the Contributed Claims) to the Trust. In the case of any Noteholder or Unitholder that elected, on such holder’s Plan ballot, to contribute such holder’s Contributed Claims to the Trust, the relative share of Liquidation Trust Interests granted to any so electing Noteholder or Unitholder has been enhanced by increasing the amount that otherwise would be the applicable Net Note Claim or Net Unit Claim by the Contributing Claimant’s Enhancement Multiplier of 105% before converting such Net Note Claim or Net Unit Claim to Liquidation Trust Interests.

With respect to disputed claims, upon resolution of any disputed claims and to the extent such claims become allowed claims, holders of such Claims in the Plan’s Class 3, Class 4 and Class 5 will be granted Liquidation Trust Interests.

As of September 23, 2022,27, 2023, approximately $887.39$887.42 million of Class 3, Class 4 and Class 5 Claims are allowed. The Trust estimates, as of September 23, 2022,27, 2023, that approximately $0.34 million of additional Class 3, Class 4 and Class 5 Claims will ultimately be allowed. As more such claims become allowed, additional Liquidation Trust Interests will be granted. The percentage recovery to be received by each Class A Interestholder will be based on (i) the amount of cash ultimately available for distribution to such holders; and (ii) the actual amount of Class 3, Class 4, and Class 5 Claims that ultimately become allowed.

The Plan provides for a Liquidation Trust Interests Waterfall that specifies the priority and manner of distribution of available cash, excluding distributions of the net proceeds from Forfeited Assets. On each distribution date, the Liquidation Trustee is required to distribute available cash as follows:

First, to each Interestholder of Class A Interests pro rata based on such Interestholder’s number of Class A Interests, until the aggregate amount of all such distributions on account of the Class A Interests equals the product of (i) the total number of all Class A Interests and (ii) $75.00;

Thereafter, to each Interestholder of Class B Interests pro rata based on such Interestholder’s number of Class B Interests, until the aggregate amount of all such distributions on account of the Class B Interests equals the product of (i) the total number of all Class B Interests and (ii) $75.00;

Thereafter, to each Interestholder of a Liquidation Trust Interest (whether a Class A Interest or a Class B Interest) pro rata based on such Interestholder’s number of Liquidation Trust Interests until the aggregate amount of all such distributions on account of the Liquidation Trust Interests equals an amount equivalent to interest, at a per annum fixed rate of 10%, compounded annually, accrued on the aggregate principal amount of all Net Note Claims, allowed General Unsecured Claims, and Net Unit Claims outstanding from time to time on or after December 4, 2017, treating each distribution of available cash made after the Plan Effective Date pursuant to the immediately preceding two subparagraphs as reductions of such principal amount; and

Thereafter, pro rata to the holders of allowed Subordinated Claims until such claims are paid in full, including interest, at a per annum fixed rate of 10% or such higher rate as may be specified in any consensual agreement or order relating to a given Holder, compounded annually, accrued on the principal amount of each allowed Subordinated Claim outstanding from time to time on or after December 4, 2017.

1113

Part I

Item 1.

| Business (Continued) |

Item 1. Business (Continued)

Pursuant to the Plan and the Trust Agreement, distributions to Interestholders are net of any costs and expenses incurred by the Trust, including in connection with administering the Trust and litigating or otherwise resolving the various Causes of Action and disputed claims. Amounts withheld from distribution may include cost of collecting, administering, distributing, and liquidating the Trust assets such as fees and expenses of the Liquidation Trustee, reserves for contingent liabilities, including potential construction defect claims of the Wind-Down Entity and/or its subsidiaries, premiums for directors’ and officers’ insurance, and fees and expenses of attorneys and consultants. Distributions will be made only from assets of the Trust and only to the extent that the Trust has sufficient assets (in excess of amounts retained for contingent liabilities, including potential construction defect claims and future costs and expenses, among other things) to make such payments in accordance with the Plan and the Trust Agreement. No distribution is required to be made to any Interestholder unless such Interestholder is to receive in such distribution at least $10.00.

Distributions will be made at the sole discretion of the Liquidation Trustee in accordance with the provisions of the Plan and the Trust Agreement. Since the Plan Effective Date, the Liquidation Trustee has declared teneleven distributions to the Class A Interestholders. The distributions include a cash distribution on account of the then-allowed claims and a deposit is made into a restricted cash account for amounts that are or may become payable (a) in respect of Class A Interests that may be issued in the future upon the allowance of unresolved bankruptcy claims, (b) in respect of Class A Interests issued on account of recently allowed claims, (c) for holders of Class A Interests who failed to cash checks mailed in respect of prior distributions, (d) for distributions that were withheld due to pending avoidance actions and (e) for holders of Class A Interests for which the Trust is awaiting further beneficiary information.

On August 3, 2023, at the recommendation of the Liquidation Trustee, the Trust suspended the making of additional Trust distributions pending the result of the investigation of a construction defect claim.

Sections 7.6 and 7.18 of the Plan provide that distributions that have not been cashed within 180 calendar days of their issuance shall be null and void and the holder of the associated Liquidation Trust Interests “shall be deemed to have forfeited its rights to any reserved and future distributions under the Plan,” with such amounts to become “Available Cash” of the Trust for all purposes. On February 1, 2022, the Trust sent letters to the holders of the Class A Interests who had failed to cash distribution checks in respect of prior distributions, which checks were issued more than 180 days prior to the date of the letter. The letter informed each recipient that, unless the Trust was contacted on or before February 28, 2022, such recipient’s reserved and future distribution would be deemed forfeited in accordance with the Plan. The Trust provided this final notice simply as a one-time courtesy and reserved its rights to strictly enforce the Plan’s forfeiture provisions, and any other provision of the Plan, against any person (including any recipient of the final notice) at any time in the future, without further notice.

1214

Part I

Item 1.

| Business (Continued) |

Item 1. Business (Continued)

The following tables summarize the distributions declared, distributions paid and the activity in the restricted cash account for the periods from February 15, 2019 (inception) through June 30, 20222023 and from February 15, 2019 through September 23, 2022:27, 2023:

| | |

| | | During the Period from February 15, 2019 (inception) through June 30, 2023 ($ in Millions) | | | During the Period from February 15, 2019 (inception) through September 27, 2023 ($ in Millions) | |

| Date Declared | | $ per Class A Interest | | | Total Declared | | | Paid | | | Restricted Cash Account | | | Total Declared | | | Paid | | | Restricted Cash Account | |

| | | | | | | | | | | | | | | | | | | | | | | |

| Distributions Declared | | | | | | | | | | | | | | | | | | | | | | |

| First | 3/15/2019 | | $ | 3.75 | | | $ | 44.70 | | | $ | 42.32 | | | $ | 2.38 | | | $ | 44.70 | | | $ | 42.32 | | | | 2.38 | |

| Second | 1/2/2020 | | | 4.50 | | | | 53.44 | | | | 51.20 | | | | 2.24 | | | | 53.44 | | | | 51.20 | | | | 2.24 | |

| Third | 3/31/2020 | | | 2.12 | | | | 25.00 | | | | 24.19 | | | | 0.81 | | | | 25.00 | | | | 24.19 | | | | 0.81 | |

| Fourth | 7/13/2020 | | | 2.56 | | | | 29.97 | | | | 29.24 | | | | 0.73 | | | | 29.97 | | | | 29.24 | | | | 0.73 | |

| Fifth | 10/19/2020 | | | 2.56 | | | | 29.96 | | | | 29.21 | | | | 0.75 | | | | 29.96 | | | | 29.21 | | | | 0.75 | |

| Sixth | 1/7/2021 | | | 4.28 | | | | 50.01 | | | | 48.67 | | | | 1.34 | | | | 50.01 | | | | 48.67 | | | | 1.34 | |

| Seventh (a) | 5/13/2021 | | | 2.58 | | | | 30.04 | | | | 29.35 | | | | 0.69 | | | | 30.04 | | | | 29.35 | | | | 0.69 | |

| Eighth | 10/8/2021 | | | 3.44 | | | | 40.02 | | | | 39.14 | | | | 0.88 | | | | 40.02 | | | | 39.14 | | | | 0.88 | |

| Ninth | 2/4/2022 | | | 3.44 | | | | 39.98 | | | | 39.15 | | | | 0.83 | | | | 39.98 | | | | 39.15 | | | | 0.83 | |

| Tenth | 6/15/2022 | | | 5.63 | | | | 65.02 | | | | 64.19 | | | | 0.83 | | | | 65.02 | | | | 64.19 | | | | 0.83 | |

| Eleventh | 5/10/2023 | | | 2.18 | | | | 25.02 | | | | 24.90 | | | | 0.12 | | | | 25.02 | | | | 24.90 | | | | 0.12 | |

| Subtotal | | | $ | 37.04 | | | $ | 433.16 | | | $ | 421.56 | | | $ | 11.60 | | | $ | 433.16 | | | $ | 421.56 | | | $ | 11.60 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Distributions Reversed | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Disallowed (b) | | | | | | | | | | | | | | | | (6.27 | ) | | | | | | | | | | | (6.31 | ) |

| Returned (c) | | | | | | | | | | | | | | | | 0.74 | | | | | | | | | | | | 0.74 | |

| Forfeited (d) | | | | | | | | | | | | | | | | (1.13 | ) | | | | | | | | | | | (1.13 | ) |

| Subtotal | | | | | | | | | | | | | | | | (6.66 | ) | | | | | | | | | | | (6.70 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Distributions Paid from Reserve Account (e) | | | | | | | | | | | | | | | | (3.66 | ) | | | | | | | | | | | (3.66 | )

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Distributions Payable, Net: | | | | | | | as of 6/30/2023: | | | $ | 1.28 | | | as of 9/27/2023: | | | $ | 1.24 | |

| | | | | | | During the Period from

February 15, 2019 (inception) through

June 30, 2022 ($ in Millions) | | | During the Period from

February 15, 2019 (inception) through

September 23, 2022 ($ in Millions) | |

| Date Declared | | $ per

Class A Interest | | | Total Declared | | | Paid | | | Restricted Cash Account | | | Total Declared | | | Paid | | | Restricted Cash Account | |

| | | | | | | | | | | | | | | | | | | | | | | |

| Distributions Declared | | | | | | | | | | | | | | | | | | | | | | |

| First | 3/15/2019 | | $ | 3.75 | | | $ | 44.70 | | | $ | 42.32 | | | $ | 2.38 | | | $ | 44.70 | | | $ | 42.32 | | | $ | 2.38 | |

| Second | 1/2/2020 | | | 4.50 | | | | 53.43 | | | | 51.19 | | | | 2.24 | | | | 53.43 | | | | 51.19 | | | | 2.24 | |

| Third | 3/31/2020 | | | 2.12 | | | | 25.00 | | | | 24.19 | | | | 0.81 | | | | 25.00 | | | | 24.19 | | | | 0.81 | |

| Fourth | 7/13/2020 | | | 2.56 | | | | 29.97 | | | | 29.24 | | | | 0.73 | | | | 29.97 | | | | 29.24 | | | | 0.73 | |

| Fifth | 10/19/2020 | | | 2.56 | | | | 29.95 | | | | 29.20 | | | | 0.75 | | | | 29.95 | | | | 29.20 | | | | 0.75 | |

| Sixth | 1/7/2021 | | | 4.28 | | | | 50.01 | | | | 48.67 | | | | 1.34 | | | | 50.01 | | | | 48.67 | | | | 1.34 | |

| Seventh (a) | 5/13/2021 | | | 2.58 | | | | 30.02 | | | | 29.33 | | | | 0.69 | | | | 30.02 | | | | 29.33 | | | | 0.69 | |

| Eighth | 10/8/2021 | | | 3.44 | | | | 40.02 | | | | 39.14 | | | | 0.88 | | | | 40.02 | | | | 39.14 | | | | 0.88 | |

| Ninth | 2/4/2022 | | | 3.44 | | | | 39.98 | | | | 39.15 | | | | 0.83 | | | | 39.98 | | | | 39.15 | | | | 0.83 | |

| Tenth (b) | 6/15/2022 | | | 5.63 | | | | 65.04 | | | | - | | | | - | | | | 65.02 | | | | 64.19 | | | | 0.83 | |

| Total/Subtotal | | | $ | 34.86 | | | $ | 408.12 | | | $ | 332.43 | | |

| 10.65 | | | $ | 408.10 | | | $ | 396.62 | | |

| 11.48 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Distributions Returend / (Reversed) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Disallowed (c) | | | | | | | | | | | | | | | | (3.64 | ) | | | | | | | | | | | (6.27 | ) |

| Returned (d) | | | | | | | | | | | | | | | | 0.74 | | | | | | | | | | | | 0.74 | |

| Forfeited (e) | | | | | | | | | | | | | | | | (1.16 | ) | | | | | | | | | | | (1.15 | ) |

| Subtotal | | | | | | | | | | | | | | | | (4.06 | ) | | | | | | | | | | | (6.68 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Distributions Paid from Reserve Account (f) | | | | | | | | | | | | | | | (2.86 | ) | | | | | | | | | | | (3.57 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Distributions Payable: | | | | | | | | | | | as of 6/30/2022: | | | | | | | | | | | as of 9/23/2022: | | | | | |

| Subtotal | | | | | | | | | | | | | | |

| 3.73 | | | | | | | | | | |

| 1.23 |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Tenth distribution

| | | | | | | | | | | | | | | | 65.04 | (b) | | | | | | | | | | | - |

|

| Total distributions payable | | | | | | | | | | | | | | | $ | 68.77 | | | | | | | | | | | $ | 1.23 | |

(a) The seventh distribution included the cash the Trust received from Fair Funds.

(b) On July 15, 2022, $64.19 million was paid.

(c) As a result of claims being disallowed or Class A Interests cancelled.

(d) Distribution checks returned or not cashed.

(e) Distributions forfeited as Interestholders did not cash checks that were over 180 days old.

(f) Paid as claims are allowed or resolved.

| (a) | The seventh distribution included the cash the Trust received from Fair Funds. |

| (b) | As a result of claims being disallowed or Class A Interests cancelled. |

| (c) | Distribution checks returned or not cashed. |

| (d) | Distributions forfeited as Interestholders did not cash checks that were over 180 days old. |

| (e) | Paid as claims are allowed or resolved. |

As claims are resolved, additional Class A Interests may be issued or cancelled (see “Part 1, Item 1. Business, D. Plan Provisions Regarding the Company, 2. Treatment under the Plan of holders of claims against and equity interests in the Debtors and 3. Assets and liabilities of the Company”). Therefore, the total amount of a distribution declared may change. In addition, distributions may change between the date declaredif Interestholders that were previously deemed to have forfeited their rights to receive Class A Interest distributions subsequently respond and the date paid.if overpaid distributions are returned.

E. Operations and Management of the Company

| E. | Operations and Management of the Company |

Michael I. Goldberg, Esq. is the Liquidation Trustee. The Liquidation Trustee was unanimously selected by the Unsecured Creditors’ Committee, the Noteholder Committee, and the Unitholder Committee and approved by the Bankruptcy Court.

Part I

Item 1. Business (Continued)

The Trust is also required to have a trustee that has its principal place of business in the State of Delaware (the “Delaware Trustee”). The Delaware Trustee is Wilmington Trust Company, National Association, who has been appointed for the purpose of fulfilling the requirements of the Delaware Statutory Trust Act.

The Trust does not have directors, executive officers or employees. Subject to supervision by the Supervisory Board, the Liquidation Trustee has the full power, right, authority and discretion, unless otherwise provided in the Plan, to carry out and implement all applicable provisions of the Plan.

In addition to other actions that the Liquidation Trustee has the authority to take, the Liquidation Trustee may do any and all of the following:

review, reconcile, compromise, settle, or object to claims and resolve such objections as set forth in the Plan, free of any restrictions of the Bankruptcy Code or applicable bankruptcy rules;

calculate and make distributions and calculate and establish reserves under and in accordance with the Plan;

retain, compensate, and employ professionals and other persons to represent the Liquidation Trustee with respect to and in connection with its rights and responsibilities;

establish, maintain, and administer documents and accounts of the Debtors as appropriate, which are to be segregated to the extent appropriate in accordance with the Plan;

maintain, conserve, collect, settle, and protect the Trust’s assets (subject to the limitations described in the Plan);

sell, liquidate, transfer, assign, distribute, abandon, or otherwise dispose of the assets of the Trust or any part of such assets or interest in such assets upon such terms as the Liquidation Trustee determines to be necessary, appropriate, or desirable;

negotiate, incur, and pay the expenses of the Trust;

prepare and file any and all informational returns, reports, statements, tax returns, and other documents or disclosures relating to the Debtors that are required under the Plan, by any governmental unit, or by applicable law;

compile and maintain the official claims register, including for purposes of making initial and subsequent distributions under the Plan;

take such actions as are necessary or appropriate to wind-down and dissolve the Debtors;

comply with the Plan, exercise the Liquidation Trustee’s rights, and perform the Liquidation Trustee’s obligations; and

exercise such other powers as deemed by the Liquidation Trustee to be necessary and proper to implement the Plan.

The powers and authority of the Liquidation Trustee are subject to limitations under the Trust Agreement. On behalf of the Trust or the Interestholders, the Liquidation Trustee is prohibited from doing any of the following:

entering into or engaging in any trade or business (other than the management and disposition of the assets of the Trust), and no part of the Trust’s assets or the proceeds, revenue or income therefrom may be used or disposed of by the Trust in furtherance of any trade or business;

except as expressly permitted in the Trust Agreement, reinvesting any assets of the Trust;

selling, transferring, or otherwise disposing of the Trust’s membership interests in the Wind-Down Entity without further approval of the Bankruptcy Court; or

incurring any indebtedness except as contemplated by the Plan or the Trust Agreement.

1416

Part I

Item 1. Item 1.

| Business (Continued) |

The Liquidation Trustee is permitted to invest cash of the Trust, including any earnings thereon or proceeds therefrom, any cash realized from the liquidation of the assets of the Trust, or any cash that is remitted to the Trust from the Wind-Down Entity or any other person. Investments by the Liquidation Trustee are not required to comply with Bankruptcy Code section 345(b). Accordingly, the Liquidation Trustee will not be required to obtain a secured bond from financial institutions at which Trust funds are deposited or invested. However, investments must be investments that are permitted to be made by a “liquidating trust” within the meaning of Treasury Regulation section 301.7701-4(d), as reflected in such regulation, or under applicable guidelines, rulings, or other controlling authorities. Accordingly, cash not available for distribution and cash pending distribution is expected to be held in demand and time deposits, such as short-term certificates of deposit, in banks or other savings institutions, or other temporary, liquid investments such as Treasury bills.

The Liquidation Trustee is subject to removal and replacement following notice to the SEC and upon a determination by the Bankruptcy Court that “cause” exists for such removal and replacement, using the standard set forth under Bankruptcy Code Section 1104.

Pursuant to the Plan and the Trust Agreement, the activities of the Liquidation Trustee are subject to the supervision of the Supervisory Board, a six-member supervisory board currently consisting of Lynn Myrick, John J. O’Neill, and Terry Goebel (all three of whom were nominated by the Unsecured Creditors’ Committee), Jay Beynon (nominated by the Noteholder Committee), Dr. Raymond C. Blackburn (nominated by the Unitholder Committee), and M. Freddie Reiss (elected to such position by the other members of the Supervisory Board). Mr. Reiss is the sole member of the Audit Committee of the Supervisory Board.

Under the Plan, the Supervisory Board has the rights and powers of a duly elected board of directors of a Delaware corporation. The Supervisory Board is charged with supervision of the Liquidation Trustee in accordance with the Plan and the Trust Agreement, determination of the Liquidation Trustee’s incentive compensation, if any, and approval of the appointment of any successor Liquidation Trustee. In the event that votes or consents by the Supervisory Board for and against any matter (other than any matter regarding the supervision, evaluation or compensation of the Liquidation Trustee) are equally divided, the Liquidation Trustee has the power to cast the deciding vote.

Additionally, approval by the Supervisory Board or, in the absence of such approval, an order of the Bankruptcy Court, is necessary concerning any of the following matters:

any sale or other disposition of an asset of the Trust, or any release, modification or waiver of existing rights as to an asset of the Trust, if the asset at issue exceeds $500,000 in estimated value;

any compromise or settlement of litigation or controverted matter proposed by the Liquidation Trustee involving claims in excess of $500,000; and

any retention by the Liquidation Trustee of professionals.

The approval of sale of real estate assets owned by the Wind-Down Group is the subject of an agreed-upon protocol between the Trust and the Wind-Down Entity.

Members of the Supervisory Board may resign following written notice to the Liquidation Trustee and the other members of the Supervisory Board. Such resignation will become effective on the later to occur of (i) the day specified in such written notice and (ii) the date that is thirty (30) days after the date such notice is delivered. A member of the Supervisory Board may be removed only by entry of a Bankruptcy Court order finding that cause exists to remove such member.