[X] | ||

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

[ ] | ||

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

.

(Exact Name of Registrant as Specified in Its Charter)

Delaware | |||||||

43-2052503 | |||||||

| (Jurisdiction of Incorporation or Organization) | (IRS Employer Identification No.) | ||||||

125 West 55th Street New York, New York 10019 (Address of Principal Executive Offices) (Zip Code) Registrant’s Telephone Number, Including Area Code:(212) 231-1000 Securities registered pursuant to Section 12(b) of the Act: | |||||||

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, Including Area Code:(212) 231-1000

Securities Registered Pursuant to Section 12(b) of the Act:

Title of Each Class: | Name of Exchange on Which Registered: | |||||

| Limited Liability Company Interests of Macquarie Infrastructure Company LLC (“LLC Interests”) | New York Stock Exchange | |||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yeso [ ] Nox [X]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrants’ knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yeso [ ] Nox [X]

| Page | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| PART I | |||||||||||||||

| Item 1. | |||||||||||||||

Business | 3 | ||||||||||||||

Item 1A.

| |||||||||||||||

| |||||||||||||||

| |||||||||||||||

| |||||||||||||||

| |||||||||||||||

| Risk Factors | 23 | ||||||||||||||

Item 1B. | Unresolved Staff Comments | 39 | |||||||||||||

| Item 2. | Properties | 39 | |||||||||||||

| Item 3. | Legal Proceedings | 41 | |||||||||||||

| Item 4. | [Removed and Reserved] | 41 | |||||||||||||

PART II | |||||||||||||||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | ||||||||||||||

Item 6.

| Selected Financial Data | 43 | |||||||||||||

Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | ||||||||||||||

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | ||||||||||||||

Item 8. | Financial Statements and Supplementary Data | ||||||||||||||

Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | ||||||||||||||

Item 9A.

| |||||||||||||||

| |||||||||||||||

| Controls and Procedures | 151 | ||||||||||||||

Item 9B. | Other Information | 153 | |||||||||||||

PART III | |||||||||||||||

| Item 10. | Directors and Executive Officers of the Registrant | ||||||||||||||

Item 11.

| Executive Compensation | 153 | |||||||||||||

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | ||||||||||||||

Item 13.

| |||||||||||||||

| |||||||||||||||

| |||||||||||||||

| Item 14. | Principal Accountant Fees and Services | 154 | |||||||||||||

PART IV | |||||||||||||||

| Item 15. | Exhibits, Financial Statement Schedules | 154 | |||||||||||||

i

In 2007, we made an election

officer and chief financial officer and seconds or makes other personnel available as required. The services performed for the Company are provided at our Manager’s expense, and includes the compensation of our seconded personnel.

The challenges posed byAviation, the economic conditionsrevenues of which are based on patronage.

Over the medium term, subject to having access to external sources of capital at a reasonable cost, we may resume growth through acquisition of additional infrastructure businesses. Such acquisitions may be bolt-ons to existing business platforms.

We have reduced long-term debt balances through the application of accumulated cash generated by our businesses (which was historically distributed to shareholders) and proceeds from the sale of the non-controlling stake in District Energy. We have eliminated all debt at the MIC holding company level and reduced the balance outstanding on the primary facility at Atlantic Aviation. We expect to continue to reduce the debt of Atlantic Aviation through the application of cash generated by that business. This componenteach of our strategy has strengthenedbusinesses;

We intendbusiness to continue to seek opportunities to reduce expenses through rationalization of staffing and business process improvements. In addition, we are actively seeking opportunities to improve the marketing and organic growth of our businesses. We are prudently managing reinvestment in our businesses in the form of maintenance capital expenditures without compromising service levels or operational capabilities of these businesses. Executing this component of our strategy is expected to improve the generation of free cash flow by our businesses.

We have reinvested substantially all of the cash flows generated at IMTT in economically attractive growth opportunities, primarily additional storage capacity. We will continue to reinvest cash flow generated by this business in additional growth projects that we expect will also generate appropriate returns.

We have also reinvested a portion of the cash generated by each of District Energy and The Gas Company into projects that support customer acquisition. We will continue to reinvest in such opportunities in the future.

We intend to meet our contractual obligations with respect to the deployment of growth capital, such as our leasehold improvement obligations at Atlantic Aviation. We have sufficient committed financing to meet these expenditures. We expect that these projects will increase the amount of free cash flow generated by this business.

| Proportion of Terminal Revenue from Major Commodities Stored | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Petroleum/Asphalt | Chemical | Renewable/Vegetable & Animal Oil | Other | |||||||||||||

| 60% | 27% | 9% | 4% | |||||||||||||

| Proportion of Terminal Revenue from Major Commodities Stored | ||||||

| Petroleum/Asphalt | Chemical | Renewables/Vegetable & Animal Oil | Other | |||

| 58% | 29% | 9% | 4% | |||

Financial information for 100% of this business is as follows ($ in millions):

| As of, and for the Year Ended, December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2009 | 2008 | |||||||||||||

| Revenue | $ | 557.2 | $ | 346.2 | $ | 352.6 | |||||||||

| EBITDA excluding non-cash items | 236.8 | 147.7 | 136.6 | ||||||||||||

| Total assets | 1,221.9 | 1,064.8 | 1,006.3 | ||||||||||||

| As of, and for the Year Ended, December 31, | ||||||||||||

| 2009 | 2008 | 2007 | ||||||||||

| Revenue | $ | 346.2 | $ | 352.6 | $ | 275.2 | ||||||

| EBITDA excluding non-cash items | 147.7 | 136.6 | 89.0 | |||||||||

| Total assets | 1,064.8 | 1,006.3 | 862.5 | |||||||||

The following table summarizes the location of each IMTT facility and the corresponding numbermillions of tanks in service,barrels of storage capacity in service and number of ship and barge docks available for product transfer. This information reflects the site assetsis as of December 31, 20092010 and does not include tanks used in packaging, recovery tanks, and/or other storage capacity not typically available for rent.

| Facility | Land | Aggregate Capacity of Storage Tanks in Service | Number of Ship & Barge Berths in Service | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (Millions of Barrels) | ||||||||||||||

Facilities in the United States: | ||||||||||||||

| Bayonne, NJ | Owned | 16.0 | 20 | |||||||||||

| St. Rose, LA* | Owned | 14.7 | 16 | |||||||||||

| Gretna, LA* | Owned | 2.0 | 5 | |||||||||||

| Avondale, LA* | Owned | 1.1 | 4 | |||||||||||

| Geismar, LA* | Owned | 0.9 | 3 | |||||||||||

| Lemont, IL | Owned/Leased | 1.0 | 1 | |||||||||||

| Joliet, IL | Owned | 0.9 | 3 | |||||||||||

| Richmond, CA | Owned | 0.7 | 2 | |||||||||||

| Chesapeake, VA | Owned | 1.0 | 1 | |||||||||||

| Richmond, VA | Owned | 0.4 | 1 | |||||||||||

Facilities in Canada: | ||||||||||||||

Quebec City, Quebec(1) | Leased | 2.0 | 2 | |||||||||||

Placentia Bay, Newfoundland(2) | Leased | 3.0 | 2 | |||||||||||

| Total | 43.7 | 60 | ||||||||||||

| Facility | Land | Number of Storage Tanks in Service | Aggregate Capacity of Storage Tanks in Service | Number of Ship & Barge Berths in Service | ||||||||||||

| (Millions of Barrels) | ||||||||||||||||

| Facilities in the United States: | ||||||||||||||||

| Bayonne, NJ | Owned | 600 | 16.0 | 18 | ||||||||||||

| St. Rose, LA* | Owned | 205 | 13.4 | 16 | ||||||||||||

| Gretna, LA* | Owned | 56 | 2.0 | 5 | ||||||||||||

| Avondale, LA* | Owned | 82 | 1.1 | 4 | ||||||||||||

| Geismar, LA* | Owned | 34 | 0.9 | 3 | ||||||||||||

| Lemont, IL | Owned/Leased | 155 | 1.1 | 3 | ||||||||||||

| Joliet, IL | Owned | 71 | 0.7 | 2 | ||||||||||||

| Richmond, CA | Owned | 46 | 0.6 | 1 | ||||||||||||

| Chesapeake, VA | Owned | 23 | 1.0 | 1 | ||||||||||||

| Richmond, VA | Owned | 12 | 0.4 | 1 | ||||||||||||

| Facilities in Canada: | ||||||||||||||||

| Quebec City, Quebec(1) | Leased | 53 | 1.9 | 2 | ||||||||||||

| Placentia Bay, Newfoundland(2) | Leased | 6 | 3.0 | 2 | ||||||||||||

| Total | 1,343 | 42.1 | 58 | |||||||||||||

| * | Collectively the “Louisiana” facilities. |

| (1) | Indirectly 66.7% owned and managed by IMTT. |

| (2) | Indirectly 20.1% owned and managed by IMTT. |

IMTT-Bayonne has the capability to quickly load and unload the largest bulk liquid transport ships entering NYH. The U.S. Army Corp of Engineers (USACE) has dredged the Kill Van Kull channel passing the IMTT-Bayonne docks to 45 feet (IMTT has dredged some but not all of its docks to that depth). Most competitors in NYH have facilities located on the southern portion of the Arthur Kill (water depth of approximately 35 feet) and force large ships to transfer product through lightering (transferring cargo to barges at anchorage) before docking. This technique substantially increases the cost of loading and unloading vessels. This competitive advantage for Bayonne may improve as the USACE has announced plans to dredgeis in the process of dredging the Kill Van Kull to 50 feet (with no planned increase in the depth of the southern portion of the Arthur Kill).

Demand for third-party bulk liquid storage in NYH has remained strong during the past several years, as illustrated by the capacity utilization at the Bayonne facility. For the three years ended December 31, 2009, IMTT-Bayonne on average rented over 94% of its available storage capacity.years.

Demand for third-party bulk liquid storage on the lower Mississippi River has remained strong during the past several years, as illustrated by the capacity utilization at the IMTT Louisiana facilities. For the three years ended December 31, 2009, IMTT rented approximately 96% of the aggregate available storage capacity at St. Rose, Gretna, Avondale and Geismar.years.

The IMTT head office in New Orleans provides the business with central management, performs support functions such as accounting, tax, finance, human resources, insurance, information technology and legal services and provides support for functions that have been partially de-centralized to the terminal level such as engineering and environmental and occupational health and safety regulatory compliance. IMTT’s senior management team, other than the terminal managers, have on average 36 years experience in the bulk liquid storage industry and 2829 years service with IMTT.

The shareholders’ agreementShareholders’ Agreement is filedincluded as an exhibit to this Annual Report on Form 10-K.

Financial information for this business is as follows ($ in millions):

| As of, and for the Year Ended, December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2009 | 2008 | |||||||||||||

| Revenue | $ | 210.6 | $ | 175.4 | $ | 213.0 | |||||||||

| EBITDA excluding non-cash items | 44.4 | 37.6 | 27.9 | ||||||||||||

| Total assets | 350.4 | 344.9 | 330.2 | ||||||||||||

| % of our consolidated revenue | 25.0 | % | 24.7 | % | 21.8 | % | |||||||||

| As of, and for the Year Ended, December 31, | ||||||||||||

| 2009 | 2008 | 2007 | ||||||||||

| Revenue | $ | 175.4 | $ | 213.0 | $ | 170.4 | ||||||

| EBITDA excluding non-cash items | 37.6 | 27.9 | 25.6 | |||||||||

| Total assets | 344.9 | 330.2 | 313.1 | |||||||||

| % of our consolidated revenue | 24.7 | % | 21.8 | % | 22.6 | % | ||||||

The Gas Company’s long-term strategy is to increase and diversify its customer base. The business intends to increase penetration of the residential, the expanding government (primarily military) and the tourism-related markets. The business also intends to invest in and promote the value of The Gas Company’s products and services and its attractiveness as a cleaner alternative to other energy sources in Hawaii.

The business’ utility rates are established by the HPUC in periodic rate cases typically initiated by The Gas Company. The business initiates a rate case by submitting a request to the HPUC for an increase in the rates based, for example, upon materially higher costs related to providing the service. Following initiation of the rate increase request by The Gas Company and submission by the Division of Consumer Advocacy and other intervening parties of their positions on the rate request, and potentially an evidentiary hearing, the HPUC issues a decision establishing the revenue requirements and the resulting rates that The Gas Company will be allowed to charge.

Any decision by Chevron regarding its operations in Hawaii could affect the business’ cost of LPG and may adversely impact its non-utility contribution margin and profitability. In an effort to mitigate the risk of supply disruption and/or a potential increase in costs, the business ishas been evaluating a number of alternatives, including additional shipments of foreign sourced product.product and additional storage.

District Energy operates the largest district cooling system in the United States. The system currently serves overapproximately 100 customers in downtown Chicago under long-term contracts and one customer outside the downtown area. District Energy produces chilled water at five plants located in downtown Chicago and distributes it through a closed loop of underground piping for use in the air conditioning systems of large commercial, retail and residential buildings in the central business district. The first of the plants became operational in 1995, and the most recent came on line in June 2002. With modifications made in 2009, the downtown system has the capacity to produce approximately 92,000 tons of chilled water, although it has approximately 102,000103,000 tons of cooling under contract. The business is able to sell continuous service capacity in excess of the total system capacity because not all customers use their full capacity at the same time.

| As of, and for the Year Ended, December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2009 | 2008 | |||||||||||||

| Revenue | $ | 56.8 | $ | 48.6 | $ | 48.0 | |||||||||

| EBITDA excluding non-cash items | 22.8 | 20.8 | 21.1 | ||||||||||||

| Total assets | 228.5 | 234.8 | 227.1 | ||||||||||||

| % of our consolidated revenue | 6.8 | % | 6.8 | % | 4.9 | % | |||||||||

| As of, and for the Year Ended, December 31, | ||||||||||||

| 2009 | 2008 | 2007 | ||||||||||

| Revenue | $ | 48.6 | $ | 48.0 | $ | 49.5 | ||||||

| EBITDA excluding non-cash items | 20.8 | 21.1 | 5.5 | |||||||||

| Total assets | 234.8 | 227.1 | 232.6 | |||||||||

| % of our consolidated revenue | 6.8 | % | 4.9 | % | 6.6 | % | ||||||

Growth: This business intends to grow revenue and profits by marketing its services to developers in the downtown Chicago market. Its value proposition is centered on high reliability, efficiency and ease of operation and maintenance. The management team develops and maintains relationships with property developers, engineers, architects and city planners as a means of keeping District Energy and these attributes “top of mind” when they select among building cooling systems and services.

Corrective maintenance

District Energy is not subject to substantial competitive pressures. Customers are generally not allowed to cool their premises by means other than the chilled water service the business provides. In addition, the primary alternative available to building owners is the installation of a stand-alone water chilling system (self-cooling). While competition from self-cooling exists, the business expects that the vast majority of its current contracts will be renewed at maturity. Installation of a water chilling system can require significant building reconfiguration as well as space for reconfiguration, and capital expenditure, whereas District Energy has the advantage of economies of scale in terms of efficiency, staff and electricity procurement.

Financial information for this business is as follows ($ in millions):

| As of, and for the Year Ended, December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2009 | 2008 | |||||||||||||

| Revenue | $ | 573.4 | $ | 486.1 | $ | 716.3 | |||||||||

| EBITDA excluding non-cash items | 117.5 | 106.5 | 137.1 | ||||||||||||

| Total assets | 1,410.1 | 1,473.2 | 1,660.8 | ||||||||||||

| % of our consolidated revenue | 68.2 | % | 68.5 | % | 73.3 | % | |||||||||

| As of and for the Year Ended, December 31, | ||||||||||||

| 2009 | 2008 | 2007 | ||||||||||

| Revenue | $ | 486.1 | $ | 716.3 | $ | 534.3 | ||||||

| EBITDA excluding non-cash items | 106.5 | 137.1 | 119.9 | |||||||||

| Total assets | 1,473.2 | 1,660.8 | 1,763.7 | |||||||||

| % of our consolidated revenue | 68.5 | % | 73.3 | % | 70.8 | % | ||||||

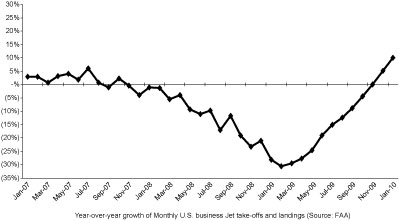

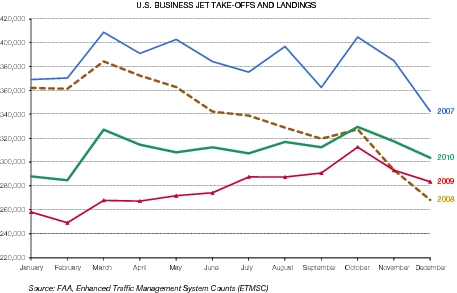

Despite improved access to general aviation resulting from an expansion of fractional and charter offerings and the challenges facing commercial aviation including potential mainline carrier consolidation and security-related delays, all of which strengthened the general aviation industry, FBO gross profit has been negatively affected by thesector. The business believes business jet traffic will continue to expand if economic downturn which resulted in a reduction in the volume of fuel sold. See “Risk Factors” in Part I, Item 1A.activity continues to recover.

In 2009, in response to customer demand,

Competition in the FBO business exists on a local basis at most of the airports at which Atlantic Aviation operates. The FBO at the East 34th Street Heliport in New York and 32 of the other FBOs in the network are the only FBOs at their respective airports. The remaining 39 FBOs have one or more competitors at the airport.locations. The FBOs compete on the basis of location of the facility relative to runways and street access, service, value-added features, reliability and price. To a lesser extent, each FBO also faces competitive pressure from the fact that aircraft may take on sufficient fuel at one location and not need to refuel at a specific destination. FBO operators also face indirect competition from facilities located at other nearby airports.

The day-to-day operations of Atlantic Aviation are managed by individual site managers who are responsible for all aspects of the operations at their site. Responsibilities include ensuring that customer requirements are met by the staff employed at the site and that revenue is collected, and expenses incurred, in accordance with internal guidelines. Local managers are, within the specified guidelines, empowered to make decisions as to fuel pricing and other services, thereby improving responsiveness and customer service. Local managers within a geographic region are supervised by one of fivefour regional managers covering the United States.

As of December 31, 2009, on a consolidated basis, continuing operations had total long-term debt outstanding of $1.2 billion, plus additional availability under existing credit facilities. In addition, IMTT had total long-term debt outstanding of $632.2 million at December 31, 2009. The terms of these debt arrangements generally require compliance with significant operating and financial covenants. The ability of each of our businesses or investments to meet their respective debt service obligations and to refinance or repay their outstanding indebtedness will depend primarily upon cash produced by that business.

This indebtedness could have important consequences, including:

If our businesses are unable to comply with the terms of any of their various debt agreements, they may be required to refinance a portion or all of the related debt or obtain additional financing. As discussed further

herein, our businesses may not be able to refinance or obtain additional financing because of their high levels of debt and debt incurrence restrictions under their debt agreements or because of adverse conditions in credit markets generally. Our businesses also may be forced to default on various debt obligations if cash flow from the relevant operating business is insufficient and refinancing or additional financing is unavailable, and, as a result, the relevant debt providers may accelerate the maturity of their obligations. If any of our businesses or investments are unable to repay their debts when due, they would become insolvent.

Our total assets reflect a substantial amount of goodwill and other intangible assets. At December 31, 2009, goodwill and other intangible assets, net, represented approximately 56.3% of total assets from continuing operations. Goodwill and other intangible assets were primarily recognized as a result of the acquisitions of our businesses and investments. Other intangible assets consist primarily of airport operating rights, trade names and customer relationships. On at least an annual basis, we assess whether there has been an impairment in the value of goodwill and assess for impairment of other intangible assets with indefinite lives when there are triggering events or circumstances. If the carrying value of the tested asset exceeds its estimated fair value, impairment is deemed to have occurred. In this event, the amount is written down to fair value. Under current accounting rules, this would result in a charge to reported earnings. We have recognized significant impairments in the past, and any future determination requiring the write-off of a significant portion of goodwill or other intangible assets would negatively affect our reported earnings and total capitalization, and could be material.

The Company is a holding company with no operations. Therefore, it is dependent upon the ability of our businesses and investments to pay dividends and make distributions to the Company to enable it to meet its expenses, reduce any outstanding debt at the holding company level and to make distributions to shareholders in the future. The ability of our operating subsidiaries and the businesses in which we will hold investments to make distributions to the Company is subject to limitations based on their operating performance, the terms of their debt agreements and the applicable laws of their respective jurisdictions. In addition, the ability of each business to reduce its outstanding debt will be similarly limited by its operating performance, as discussed below and in Part 1, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” If, as a consequence of these various limitations and restrictions, we are unable to receive sufficient dividends and/or distributions from our businesses, we may be limited in our ability to reduce the level of any outstanding debt and declare distributions on our LLC interests. In addition, we may be unable to pay our management fees to our Manager. If our Manager resigned, it would trigger a change-in-control default provision under the credit facilities of some of our businesses, which would permit the relevant lenders to accelerate the indebtedness.

We own 50% of IMTT and 50.01% of District Energy and may acquire less than majority ownership in other businesses in the future. Our ability to influence the management of jointly owned businesses, and the ability of these businesses to continue operating without disruption, depends on our reaching agreement with our co-investors and reconciling investment and performance objectives for these businesses. To the extent that we are unable to agree with co-investors regarding the business and operations of the relevant investment, the performance of the investment and the operations may suffer, and could have a material adverse effect on our results. Furthermore, we may, from time to time, own non-controlling interests in investments. Management and controlling shareholders of these investments may develop different objectives than we have and may not make distributions to us at levels that we had anticipated. Our inability to exercise significant influence over the operations, strategies and policies of non-controlled investments means that decisions could be made that could adversely affect our results and our ability to generate cash and pay distributions on our LLC interests.

Our businesses generally are, and will continue to be, subject to substantial regulation by governmental agencies. In addition, our businesses rely on obtaining and maintaining government permits, licenses, concessions, leases or contracts. Government entities, due to the wide-ranging scope of their authority, have significant leverage over us in their contractual and regulatory relationships with us that they may exercise in a manner that causes us delays in the operation of our businesses or pursuit of our strategy, or increased administrative expense. Furthermore, government permits, licenses, concessions, leases and contracts are generally very complex, which may result in periods of non-compliance, or disputes over interpretation or enforceability. If we fail to comply with these regulations or contractual obligations, we could be subject to monetary penalties or we may lose our rights to operate the affected business, or both. Where our ability to operate an infrastructure business is subject to a concession or lease from the government, the concession or lease may restrict our ability to operate the business in a way that maximizes cash flows and profitability. Further, our ability to grow our current and future businesses will often require consent of numerous government regulators. Increased regulation restricting the ownership or management of U.S. assets, particularly infrastructure assets, by non-U.S. persons, given the non-U.S. ultimate ownership of our Manager, may limit our ability to pursue acquisitions. Any such regulation may also limit our Manager’s ability to continue to manage our operations, which could cause disruption to our businesses and a decline in our performance. In addition, any required government consents may be costly to seek and we may not be able to obtain them. Failure to obtain any required consents could limit our ability to achieve our growth strategy.

Our contracts with government entities may also contain clauses more favorable to the government counterparty than a typical commercial contract. For instance, a lease, concession or general service contract may enable the government to terminate the agreement without requiring them to pay adequate compensation. In addition, government counterparties also may have the discretion to change or increase regulation of our operations, or implement laws or regulations affecting our operations, separate from any contractual rights they may have. Governments have considerable discretion in implementing regulations that could impact these businesses. Because our businesses provide basic services, and face limited competition, governments may be influenced by political considerations to take actions that may hinder the efficient and profitable operation of our businesses and investments.

Where our businesses or investments are sole or predominant service providers in their respective service areas and provide services that are essential to the community, they are likely to be subject to rate regulation by governmental agencies that will determine the prices they may charge. We may also face fees or other charges imposed by government agencies that increase our costs and over which we have no control. We may

be subject to increases in fees or unfavorable price determinations that may be final with no right of appeal or that, despite a right of appeal, could result in our profits being negatively affected. In addition, we may have very little negotiating leverage in establishing contracts with government entities, which may decrease the prices that we otherwise might be able to charge or the terms upon which we provide products or services. Businesses and investments we acquire in the future may also be subject to rate regulation or similar negotiating limitations.

Our businessesdistributions from IMTT is limited, and investments are subject to federal, state and local safety, health and environmental laws and regulations. These laws and regulations affect all aspects of their operations and are frequently modified. There is a risk that any one of our businesses or investments may not be able to comply with some aspect of these laws and regulations, resulting in fines or penalties. Additionally, if new laws and regulations are adopted or if interpretations of existing laws and regulations change, we could be required to increase capital spending and incur increased operating expenses in order to comply. Because the regulatory environment frequently changes, we cannot predict when or how we may be affectednegatively impacted by disagreements with our co-investor regarding IMTT’s business and operations.

A significant and sustained increase in the price of oil could have a negative impact on the profitability of a number of our businesses. Higher prices for jet fuel could result in less use of aircraft by general aviation customers, which would have a negative impact on the profitability of Atlantic Aviation. Higher fuel prices could increase the cost of power to our businesses generally which they may not be able to fully pass on to customers.

the level of air travel, adversely affecting Atlantic Aviation. General aviation travel is primarily a function of economic activity. Consequently, during periods of economic downturn, FBO customers are more likely to curtail air travel.

Some of Atlantic Aviation’s competitors are pursuing more aggressive pricing strategies. These competitors operate FBOs at a number of airports where Atlantic Aviation operates or at airports near where it operates. This competition, combined with the continuation or worsening of current economic conditions, has in recent periods and may continue to result in increased focus on cost among customers and, consequently, a decline in corporate jet usage and increased price sensitivity. These factors may cause volumes of fuel sales and market share to decline and may result in increased margin pressure, adversely affecting the profitability of this business.

the relevant authority to terminate the lease at their convenience. In each case, Atlantic Aviation would then lose the income from that location and potentially the expected returns from prior capital expenditures. Atlantic Aviation would also likely be in default under the loan agreements and be obliged to repay its lenders a portion or the entire outstanding loan amount. Any such events would have a material adverse effect on Atlantic Aviation’s results of operations.

PCAA is in the process of completing a sale of its assets through a Chapter 11 bankruptcy. Creditors of the businessFAA traffic data may also attempt to seek recovery from the Company and, through the Company, seek recourse to the assets of our other businesses, regardless of the merits of such a claim or lack thereof, which could result in substantial legal costsconclusions in strategic planning, mergers and significant disruption of management time and resources, thereby adversely affecting our profitability.acquisitions or macro pricing decisions that are ultimately unfavorable.

unable to do so quickly, our operations are likely to experience a disruption, our financial results could be adversely affected, perhaps materially, and the market price of our LLC interests may decline substantially. In addition, the coordination of our internal management, acquisition activities and supervision of our businesses and investments are likely to suffer if we were unable to identify and reach an agreement with a single institution or group of executives having the expertise possessed by our Manager and its affiliates.

The operating agreement of the Company, which we refer to as the LLC agreement, contains a number of provisions that could have the effect of making it more difficult for a third-party to acquire, or discouraging a third-party from acquiring, control of the company.Company. These provisions include:

None.

A summary of property, by island, follows. For more information regarding The Gas Company’s operations, see “Our Businesses and Investments — The Gas Company — Fuel Supply, SNG Plant and Distribution System” in Part I, Item 1.

| Island | Description | Use | Own/Lease | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SNG Plant | Production of SNG | Lease | ||||||||||||

| Kamakee Street Buildings and Maintenance yard | Engineering, Maintenance Facility, Warehouse | Own | ||||||||||||

| LPG Baseyard | Storage facility for tanks and cylinders | Lease | ||||||||||||

| Topa Fort Street Tower | Executive Offices | Lease | ||||||||||||

| Various Holding Tanks | Store and supply LPG to utility customers | Lease | ||||||||||||

| Maui | Office, tank storage facilities and baseyard | Island-wide operations | Lease | |||||||||||

| Kauai | Office | Island-wide operations | Own | |||||||||||

| Kauai | Tank storage facility and baseyard | Island-wide operations | Lease | |||||||||||

| Hawaii | Office, tank storage facilities and baseyard | Island-wide operations | Own | |||||||||||

| Plant Number | Ownership or Lease Information | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| P-1 | The building and equipment are owned by District Energy and the business has a long-term property lease until 2043 with an option to renew for 49 years. | ||||||||

| P-2 | Property, building and equipment are owned by District Energy. | ||||||||

| P-3 | District Energy has a property lease that expires in 2033 with a right to renew for ten years. The equipment is owned by District Energy but the landlord has a purchase option over approximately one-fourth of the equipment. | ||||||||

| P-4 | District Energy has a property lease that expires in 2016 and the business may renew the lease for another 10 years for the P-4B property unilaterally, and for P-4A, with the consent of the landlord. The equipment at P-4A and P-4B is owned by District Energy. The landlord can terminate the service agreement and the P-4A property lease upon transfer of the property, on which P-4A and P-4B are located, to a third-party. | ||||||||

| P-5 | District Energy has an exclusive perpetual easement for the use of the basement where the equipment is located. The equipment is owned by District Energy. | ||||||||

| Stand-Alone | District Energy has a contractual right to use the property pursuant to a service agreement and will own the equipment until the earliest of 2025 when the equipment reverts to the customer or if the customer exercises an early purchase option. | ||||||||

There

None.

| High | Low | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

Fiscal 2009 | ||||||||||

| First Quarter | $ | 5.74 | $ | 0.79 | ||||||

| Second Quarter | 4.36 | 1.50 | ||||||||

| Third Quarter | 9.38 | 3.10 | ||||||||

| Fourth Quarter | 12.60 | 7.38 | ||||||||

Fiscal 2010 | ||||||||||

| First Quarter | $ | 14.13 | $ | 12.20 | ||||||

| Second Quarter | 16.95 | 12.79 | ||||||||

| Third Quarter | 15.50 | 12.49 | ||||||||

| Fourth Quarter | 21.17 | 15.40 | ||||||||

Fiscal 2011 | ||||||||||

| First Quarter (through February 15, 2011) | $ | 24.39 | $ | 20.56 | ||||||

| High | Low | |||||||

| Fiscal 2008 | ||||||||

| First Quarter | $ | 39.01 | $ | 29.13 | ||||

| Second Quarter | 33.24 | 25.29 | ||||||

| Third Quarter | 25.00 | 12.63 | ||||||

| Fourth Quarter | 12.90 | 2.32 | ||||||

| Fiscal 2009 | ||||||||

| First Quarter | $ | 5.74 | $ | 0.79 | ||||

| Second Quarter | 4.36 | 1.50 | ||||||

| Third Quarter | 9.38 | 3.10 | ||||||

| Fourth Quarter | 12.60 | 7.38 | ||||||

| Fiscal 2010 | ||||||||

| First Quarter (through February 18, 2010) | $ | 13.96 | $ | 12.20 | ||||

As of February 25, 2010,23, 2011, we had 45,292,91345,715,448 LLC interests issued and outstanding that we believe were held by 90105 holders of record, representing over 16,000approximately 20,000 beneficial holders.

Because our LLC interests are listed on the NYSE, our Chief Executive Officer is required to make, and on July 6, 2009 did make, an annual certification to the NYSE stating that he was not aware of any violation by the Company of the corporate governance listing standards of the NYSE. In addition, we have filed, as exhibits to this annual report on Form 10-K, the certifications of the Chief Executive Officer and Chief Financial Officer required under Section 302 of the Sarbanes-Oxley Act of 2002 to be filed with the SEC regarding the quality of our public disclosure.

Since January 1, 2008,businesses. In particular we have made or declaredstrengthened the following distributions:balance sheet of our Atlantic Aviation business by reducing its long-term debt and we have improved the financial flexibility of our bulk liquid storage by increasing the size and extending the maturity of its primary debt facility. As a result of these improvements, and taking into consideration the prospect of continued generation of excess cash by our businesses, we expect to resume payment of quarterly cash distributions to shareholders commencing with a distribution for the first quarter of 2011 to be paid during the second quarter of 2011.

| Declared | Period Covered | $ per LLC Interest | Record Date | Payable Date | ||||||||||||

| February 25, 2008 | Fourth quarter 2007 | $ | 0.635 | March 5, 2008 | March 10, 2008 | |||||||||||

| May 5, 2008 | First quarter 2008 | $ | 0.645 | June 4, 2008 | June 10, 2008 | |||||||||||

| August 4, 2008 | Second quarter 2008 | $ | 0.645 | September 4, 2008 | September 11, 2008 | |||||||||||

| November 4, 2008 | Third quarter 2008 | $ | 0.20 | December 3, 2008 | December 10, 2008 | |||||||||||

The declaration and payment of any future distribution will be subject to a decision of the Company’s Board of Directors, which includes a majority of independent directors. The Company’s Board of Directors will take into account such matters as the state of the capital markets and general business conditions, our financial condition, results of operations, capital requirements and any contractual, legal and regulatory restrictions on the payment of distributions by us to our shareholders or by our subsidiaries to us, and any other factors that the Board of Directors deems relevant. In particular, each of our businesses and investments have substantial debt commitments and restrictive covenants, which must be satisfied before any of them can pay dividends or make distributions to us. Any or all of these factors could affect both the timing and amount, if any, of future distributions. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources” in Part II, Item 7.

The table below sets forth information with respect to LLC interests authorized for issuance as of December 31, 2009:

| Macquarie Infrastructure Company LLC | |||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Year Ended Dec 31, 2010 | Year Ended Dec 31, 2009(1) | Year Ended Dec 31, 2008(1) | Year Ended Dec 31, 2007(1) | Year Ended Dec 31, 2006(1) | |||||||||||||||||||

| ($ In Thousands, Except Per LLC Interest Data) | |||||||||||||||||||||||

Statement of operations data: | |||||||||||||||||||||||

Revenue | |||||||||||||||||||||||

| Revenue from product sales | $ | 514,344 | $ | 394,200 | $ | 586,054 | $ | 445,852 | $ | 262,432 | |||||||||||||

| Revenue from product sales – utility | 113,752 | 95,769 | 121,770 | 95,770 | 50,866 | ||||||||||||||||||

| Service revenue | 204,852 | 215,349 | 264,851 | 207,680 | 125,773 | ||||||||||||||||||

| Financing and equipment lease income | 7,843 | 4,758 | 4,686 | 4,912 | 5,118 | ||||||||||||||||||

| Total revenue | 840,791 | 710,076 | 977,361 | 754,214 | 444,189 | ||||||||||||||||||

Cost of revenue | |||||||||||||||||||||||

| Cost of product sales | 326,734 | 233,376 | 408,690 | 303,796 | 193,821 | ||||||||||||||||||

| Cost of product sales – utility | 90,542 | 73,907 | 105,329 | 66,226 | 16,127 | ||||||||||||||||||

Cost of services(2) | 53,088 | 46,317 | 63,850 | 53,387 | 37,905 | ||||||||||||||||||

Gross profit | 370,427 | 356,476 | 399,492 | 330,805 | 196,336 | ||||||||||||||||||

| Selling, general and administrative expenses | 201,787 | 209,783 | 227,288 | 181,830 | 111,006 | ||||||||||||||||||

| Fees to manager – related party | 10,051 | 4,846 | 12,568 | 65,639 | 18,631 | ||||||||||||||||||

Goodwill impairment(3) | — | 71,200 | 52,000 | — | — | ||||||||||||||||||

Depreciation(4) | 29,721 | 36,813 | 40,140 | 20,502 | 12,102 | ||||||||||||||||||

Amortization of intangibles(5) | 34,898 | 60,892 | 61,874 | 32,356 | 18,283 | ||||||||||||||||||

Loss on disposal of assets(6) | 17,869 | — | — | — | — | ||||||||||||||||||

| Total operating expenses | 294,326 | 383,534 | 393,870 | 300,327 | 160,022 | ||||||||||||||||||

Operating income (loss) | 76,101 | (27,058 | ) | 5,622 | 30,478 | 36,314 | |||||||||||||||||

| Dividend income | — | — | — | — | 8,395 | ||||||||||||||||||

| Interest income | 29 | 119 | 1,090 | 5,705 | 4,670 | ||||||||||||||||||

Interest expense(7) | (106,834 | ) | (95,456 | ) | (88,652 | ) | (65,356 | ) | (60,484 | ) | |||||||||||||

| Loss on extinguishment of debt | — | — | — | (27,512 | ) | — | |||||||||||||||||

| Equity in earnings (losses) and amortization charges of investees | 31,301 | 22,561 | 1,324 | (32 | ) | 12,558 | |||||||||||||||||

| Loss on derivative instruments | — | (25,238 | ) | (2,843 | ) | (1,362 | ) | (822 | ) | ||||||||||||||

| Gain on sale of equity investment | — | — | — | — | 3,412 | ||||||||||||||||||

| Gain on sale of investment | — | — | — | — | 49,933 | ||||||||||||||||||

| Gain on sale of marketable securities | — | — | — | — | 6,737 | ||||||||||||||||||

| Other income (expense), net | 712 | 570 | (198 | ) | (1,260 | ) | (89 | ) | |||||||||||||||

| Net income (loss) from continuing operations before income taxes | 1,309 | (124,502 | ) | (83,657 | ) | (59,339 | ) | 60,624 | |||||||||||||||

| Benefit for income taxes | 8,697 | 15,818 | 14,061 | 16,764 | 4,287 | ||||||||||||||||||

| Net income (loss) from continuing operations | $ | 10,006 | $ | (108,684 | ) | $ | (69,596 | ) | $ | (42,575 | ) | $ | 64,911 | ||||||||||

| Net income (loss) from discontinued operations, net of taxes | 81,323 | (21,860 | ) | (110,045 | ) | (9,960 | ) | (15,016 | ) | ||||||||||||||

| Net income (loss) | $ | 91,329 | $ | (130,544 | ) | $ | (179,641 | ) | $ | (52,535 | ) | $ | 49,895 | ||||||||||

| Less: net income (loss) attributable to noncontrolling interests | 659 | (1,377 | ) | (1,168 | ) | (481 | ) | (23 | ) | ||||||||||||||

| Net income (loss) attributable to MIC LLC | $ | 90,670 | $ | (129,167 | ) | $ | (178,473 | ) | $ | (52,054 | ) | $ | 49,918 | ||||||||||

| Basic income (loss) per share from continuing operations attributable to MIC LLC interest holders | $ | 0.21 | $ | (2.43 | ) | $ | (1.56 | ) | $ | (1.05 | ) | $ | 2.23 | ||||||||||

| Basic income (loss) per share from discontinued operations attributable to MIC LLC interest holders | 1.78 | (0.44 | ) | (2.41 | ) | (0.22 | ) | (0.50 | ) | ||||||||||||||

| Basic income (loss) per share attributable to MIC LLC interest holders | $ | 1.99 | $ | (2.87 | ) | $ | (3.97 | ) | $ | (1.27 | ) | $ | 1.73 | ||||||||||

| Weighted average number of shares outstanding: basic | 45,549,803 | 45,020,085 | 44,944,326 | 40,882,067 | 28,895,522 | ||||||||||||||||||

| Macquarie Infrastructure Company | ||||||||||||||||||||||

| Year Ended Dec 31, 2009 | Year Ended Dec 31, 2008(1) | Year Ended Dec 31, 2007(1) | Year Ended Dec 31, 2006(1) | Year Ended Dec 31, 2005(1) | ||||||||||||||||||

| ($ In Thousands, Except Per LLC Interest/Trust Stock Data) | ||||||||||||||||||||||

| Statement of operations data: | ||||||||||||||||||||||

| Revenue | ||||||||||||||||||||||

| Revenue from product sales | $ | 394,200 | $ | 586,054 | $ | 445,852 | $ | 262,432 | $ | 142,785 | ||||||||||||

| Revenue from product sales – utility | 95,769 | 121,770 | 95,770 | 50,866 | — | |||||||||||||||||

| Service revenue | 215,349 | 264,851 | 207,680 | 125,773 | 96,800 | |||||||||||||||||

| Financing and equipment lease income | 4,758 | 4,686 | 4,912 | 5,118 | 5,303 | |||||||||||||||||

| Total revenue | 710,076 | 977,361 | 754,214 | 444,189 | 244,888 | |||||||||||||||||

| Cost of revenue: | ||||||||||||||||||||||

| Cost of product sales | 231,139 | 406,997 | 302,283 | 192,399 | 84,480 | |||||||||||||||||

| Cost of product sales – utility | 71,252 | 103,216 | 64,371 | 14,403 | — | |||||||||||||||||

| Cost of services(2) | 46,317 | 63,850 | 53,387 | 37,905 | 37,085 | |||||||||||||||||

| Gross profit | 361,368 | 403,298 | 334,173 | 199,482 | 123,323 | |||||||||||||||||

| Selling, general and administrative expenses | 214,865 | 231,273 | 185,370 | 114,333 | 78,127 | |||||||||||||||||

| Fees to manager - related party | 4,846 | 12,568 | 65,639 | 18,631 | 9,294 | |||||||||||||||||

| Goodwill impairment(3) | 71,200 | 52,000 | — | — | — | |||||||||||||||||

| Depreciation(4) | 36,813 | 40,140 | 20,502 | 12,102 | 6,007 | |||||||||||||||||

| Amortization of intangibles(5) | 60,892 | 61,874 | 32,356 | 18,283 | 11,013 | |||||||||||||||||

| Operating (loss) income | (27,248 | ) | 5,443 | 30,306 | 36,133 | 18,882 | ||||||||||||||||

| Dividend income | — | — | — | 8,395 | 12,361 | |||||||||||||||||

| Interest income | 119 | 1,090 | 5,705 | 4,670 | 4,034 | |||||||||||||||||

| Interest expense | (91,154 | ) | (88,652 | ) | (65,356 | ) | (60,484 | ) | (23,449 | ) | ||||||||||||

| Loss on extinguishment of debt | — | — | (27,512 | ) | — | — | ||||||||||||||||

| Equity in earnings (losses) and amortization of charges of investees | 22,561 | 1,324 | (32 | ) | 12,558 | 3,685 | ||||||||||||||||

| Loss on derivative instruments | (29,540 | ) | (2,843 | ) | (1,362 | ) | (822 | ) | — | |||||||||||||

| Gain on sale of equity investment | — | — | — | 3,412 | — | |||||||||||||||||

| Gain on sale of investment | — | — | — | 49,933 | — | |||||||||||||||||

| Gain on sale of marketable securities | — | — | — | 6,737 | — | |||||||||||||||||

| Other income (expense), net | 760 | (19 | ) | (1,088 | ) | 92 | 136 | |||||||||||||||

| Net (loss) income from continuing operations before income taxes and noncontrolling interests | (124,502 | ) | (83,657 | ) | (59,339 | ) | 60,624 | 15,649 | ||||||||||||||

| Benefit for income taxes | 15,818 | 14,061 | 16,764 | 4,287 | 3,615 | |||||||||||||||||

| Net (loss) income from continuing operations before noncontrolling interests | (108,684 | ) | (69,596 | ) | (42,575 | ) | 64,911 | 19,264 | ||||||||||||||

| Noncontrolling interests | 486 | 585 | 554 | 528 | 719 | |||||||||||||||||

| Net (loss) income from continuing operations | $ | (109,170 | ) | $ | (70,181 | ) | $ | (43,129 | ) | $ | 64,383 | $ | 18,545 | |||||||||

| Discontinued operations | ||||||||||||||||||||||

| Net loss from discontinued operations before income taxes and noncontrolling interests | $ | (23,647 | ) | (180,104 | ) | $ | (9,679 | ) | $ | (27,150 | ) | $ | (3,865 | ) | ||||||||

| Benefit (provision) for income taxes | 1,787 | 70,059 | (281 | ) | 12,134 | — | ||||||||||||||||

| Macquarie Infrastructure Company LLC | |||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Year Ended Dec 31, 2010 | Year Ended Dec 31, 2009(1) | Year Ended Dec 31, 2008(1) | Year Ended Dec 31, 2007(1) | Year Ended Dec 31, 2006(1) | |||||||||||||||||||

| ($ In Thousands, Except Per LLC Interest Data) | |||||||||||||||||||||||

| Diluted income (loss) per share from continuing operations attributable to MIC LLC interest holders | $ | 0.21 | $ | (2.43 | ) | $ | (1.56 | ) | $ | (1.05 | ) | $ | 2.23 | ||||||||||

| Diluted income (loss) per share from discontinued operations attributable to MIC LLC interest holders | 1.78 | (0.44 | ) | (2.41 | ) | (0.22 | ) | (0.50 | ) | ||||||||||||||

| Diluted income (loss) per share attributable to MIC LLC interest holders | $ | 1.99 | $ | (2.87 | ) | $ | (3.97 | ) | $ | (1.27 | ) | $ | 1.73 | ||||||||||

| Weighted average number of shares outstanding: diluted | 45,631,610 | 45,020,085 | 44,944,326 | 40,882,067 | 28,912,346 | ||||||||||||||||||

| Cash distributions declared per share | $ | — | $ | — | $ | 2.125 | $ | 2.385 | $ | 2.075 | |||||||||||||

Statement of cash flows data: | |||||||||||||||||||||||

Cash flow from continuing operations | |||||||||||||||||||||||

| Cash provided by operating activities | $ | 98,555 | $ | 82,976 | $ | 95,579 | $ | 93,499 | $ | 38,979 | |||||||||||||

| Cash used in investing activities | (24,774 | ) | (516 | ) | (56,716 | ) | (638,853 | ) | (681,994 | ) | |||||||||||||

| Cash (used in) provided by financing activities | (76,528 | ) | (117,818 | ) | 1,698 | 570,618 | 556,259 | ||||||||||||||||

| Effect of exchange rate | — | — | — | (1 | ) | (272 | ) | ||||||||||||||||

| Net (decrease) increase in cash | $ | (2,747 | ) | $ | (35,358 | ) | $ | 40,561 | $ | 25,263 | $ | (87,028 | ) | ||||||||||

Cash flow from discontinued operations | |||||||||||||||||||||||

| Cash (used in) provided by operating activities | $ | (12,703 | ) | $ | (4,732 | ) | $ | (1,904 | ) | $ | 3,051 | $ | 7,386 | ||||||||||

| Cash provided by (used in) investing activities | 134,356 | (445 | ) | (26,684 | ) | (5,157 | ) | (4,202 | ) | ||||||||||||||

| Cash (used in) provided by financing activities | (124,183 | ) | 2,144 | (1,215 | ) | (3,072 | ) | 6,069 | |||||||||||||||

Cash (used in) provided by discontinued operations(8) | $ | (2,530 | ) | $ | (3,033 | ) | $ | (29,803 | ) | $ | (5,178 | ) | $ | 9,253 | |||||||||

Change in cash of discontinued operations held for sale(8) | $ | 2,385 | $ | (208 | ) | $ | 2,459 | $ | 5,902 | $ | (2,740 | ) | |||||||||||

| Macquarie Infrastructure Company | ||||||||||||||||||||||

| Year Ended Dec 31, 2009 | Year Ended Dec 31, 2008(1) | Year Ended Dec 31, 2007(1) | Year Ended Dec 31, 2006(1) | Year Ended Dec 31, 2005(1) | ||||||||||||||||||

| ($ In Thousands, Except Per LLC Interest/Trust Stock Data) | ||||||||||||||||||||||

| Net loss from discontinued operations before noncontrolling interests | (21,860 | ) | (110,045 | ) | (9,960 | ) | (15,016 | ) | (3,865 | ) | ||||||||||||

| Noncontrolling interests | (1,863 | ) | (1,753 | ) | (1,035 | ) | (551 | ) | (516 | ) | ||||||||||||

| Net loss from discontinued operations | $ | (19,997 | ) | $ | (108,292 | ) | $ | (8,925 | ) | $ | (14,465 | ) | $ | (3,349 | ) | |||||||

| Net loss | $ | (129,167 | ) | $ | (178,473 | ) | $ | (52,054 | ) | $ | 49,918 | $ | 15,196 | |||||||||

| Basic and diluted (loss) earnings per LLC interest/trust stock from continuing operations | $ | (2.43 | ) | $ | (1.56 | ) | $ | (1.05 | ) | $ | 2.23 | $ | 0.69 | |||||||||

| Basic and diluted loss per LLC interest/trust stock from discontinued operations | (0.44 | ) | (2.41 | ) | (0.22 | ) | (0.50 | ) | (0.13 | ) | ||||||||||||

| Weighted average number of shares outstanding: basic | 45,020,085 | 44,944,326 | 40,882,067 | 28,895,522 | 26,919,608 | |||||||||||||||||

| Weighted average number of shares outstanding: diluted | 45,020,085 | 44,944,326 | 40,882,067 | 28,912,346 | 26,929,219 | |||||||||||||||||

| Cash dividends declared per LLC interest/trust stock | $ | — | $ | 2.125 | $ | 2.385 | $ | 2.0750 | $ | 1.5877 | ||||||||||||

| Statement of cash flows data: | ||||||||||||||||||||||

| Cash flow from continuing operations | ||||||||||||||||||||||

| Cash provided by operating activities | $ | 82,976 | $ | 95,579 | $ | 93,499 | $ | 38,979 | $ | 39,033 | ||||||||||||

| Cash used in investing activities | (516 | ) | (56,716 | ) | (638,853 | ) | (681,994 | ) | (126,262 | ) | ||||||||||||

| Cash (used in) provided by financing activities | (117,818 | ) | 1,698 | 570,618 | 556,259 | 77,945 | ||||||||||||||||

| Effect of exchange rate | — | — | (1 | ) | (272 | ) | (331 | ) | ||||||||||||||

| Net (decrease) increase in cash | $ | (35,358 | ) | $ | 40,561 | $ | 25,263 | $ | (87,028 | ) | $ | (9,615 | ) | |||||||||

| Cash flow from discontinuing operations | ||||||||||||||||||||||

| Cash (used in) provided by operating activities | $ | (4,732 | ) | $ | (1,904 | ) | $ | 3,051 | $ | 7,386 | $ | 4,514 | ||||||||||

| Cash used in investing activities | (445 | ) | (26,684 | ) | (5,157 | ) | (4,202 | ) | (75,688 | ) | ||||||||||||

| Cash provided by (used in) financing activities | 2,144 | (1,215 | ) | (3,072 | ) | 6,069 | 55,902 | |||||||||||||||

| Net (decrease) increase in cash(6) | (3,033 | ) | (29,803 | ) | (5,178 | ) | 9,253 | (15,272 | ) | |||||||||||||

| Change in cash of discontinued operations held for sale(6) | $ | (208 | ) | $ | 2,459 | $ | 5,902 | $ | (2,740 | ) | $ | (5,931 | ) | |||||||||

| (1) | Reclassified to conform to current period presentation. |

| (2) | Includes depreciation expense of $6.6 million, $6.1 million, $5.8 million, $5.8 |

| (3) | Reflects non-cash impairment charge of $71.2 million and $52.0 million recorded during the first six months of 2009 and the fourth quarter of 2008, respectively, at Atlantic Aviation. |

| (4) | Includes a non-cash impairment charge of $7.5 million and $13.8 million recorded during the first six months of 2009 and the fourth quarter of 2008, respectively, at Atlantic Aviation. |

| (5) | Includes a non-cash impairment charge of $23.3 million and $21.7 million for contractual arrangements recorded |

| (6) | Loss on disposal includes write-offs of intangible assets of $10.4 million, property, equipment, land and leasehold improvements of $5.6 million and goodwill of $1.9 million at Atlantic Aviation. |

| (7) | Interest expense includes non-cash losses on derivative instruments of $23.4 million and $4.3 million for the years ended December 31, 2010 and 2009, respectively. |

| (8) | Cash of discontinued operations held for sale is reported in assets of discontinued operations held for sale in our consolidated balance sheets. The net |

| Macquarie Infrastructure Company LLC | |||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Year Ended Dec 31, 2010 | Year Ended Dec 31, 2009 | Year Ended Dec 31, 2008 | Year Ended Dec 31, 2007 | Year Ended Dec 31, 2006 | |||||||||||||||||||

| ($ In Thousands) | |||||||||||||||||||||||

Balance sheet data: | |||||||||||||||||||||||

| Assets of discontinued operations held for sale | $ | — | $ | 86,695 | $ | 105,725 | $ | 258,899 | $ | 268,327 | |||||||||||||

| Total current assets from continuing operations | 125,427 | 129,866 | 193,890 | 201,604 | 216,620 | ||||||||||||||||||

Property, equipment, land and leasehold improvements, net(1) | 563,451 | 580,087 | 592,435 | 577,498 | 425,045 | ||||||||||||||||||

Intangible assets, net(2) | 705,862 | 751,081 | 811,973 | 846,941 | 513,466 | ||||||||||||||||||

Goodwill(3) | 514,253 | 516,182 | 586,249 | 636,336 | 352,213 | ||||||||||||||||||

| Total assets | $ | 2,196,742 | $ | 2,339,221 | $ | 2,552,436 | $ | 2,813,029 | $ | 2,097,531 | |||||||||||||

| Liabilities of discontinued operations held for sale | $ | — | $ | 220,549 | $ | 224,888 | $ | 225,042 | $ | 220,452 | |||||||||||||

| Total current liabilities from continuing operations | 171,286 | 174,647 | 135,311 | 121,892 | 62,981 | ||||||||||||||||||

| Deferred income taxes | 156,328 | 107,840 | 83,228 | 202,683 | 163,923 | ||||||||||||||||||

| Long-term debt, net of current portion | 1,089,559 | 1,166,379 | 1,327,800 | 1,225,150 | 758,400 | ||||||||||||||||||

| Total liabilities | 1,510,047 | 1,764,453 | 1,918,175 | 1,841,159 | 1,227,946 | ||||||||||||||||||

| Members’ equity | $ | 691,149 | $ | 578,526 | $ | 628,838 | $ | 966,552 | $ | 864,425 | |||||||||||||

| Macquarie Infrastructure Company | ||||||||||||||||||||||

| Year Ended Dec 31, 2009 | Year Ended Dec 31, 2008(1) | Year Ended Dec 31, 2007(1) | Year Ended Dec 31, 2006(1) | Year Ended Dec 31, 2005(1) | ||||||||||||||||||

| ($ In Thousands) | ||||||||||||||||||||||

| Balance sheet data: | ||||||||||||||||||||||

| Assets of discontinued operations held for sale | $ | 86,695 | $ | 105,725 | $ | 258,899 | $ | 268,327 | $ | 288,846 | ||||||||||||

| Total current assets from continuing operations | 129,866 | 193,890 | 201,604 | 216,620 | 144,856 | |||||||||||||||||

| Property, equipment, land and leasehold improvements, net(2) | 580,087 | 592,435 | 577,498 | 425,045 | 240,260 | |||||||||||||||||

| Intangible assets, net(3) | 751,081 | 811,973 | 846,941 | 513,466 | 260,849 | |||||||||||||||||

| Goodwill(4) | 516,182 | 586,249 | 636,336 | 352,213 | 148,122 | |||||||||||||||||

| Total assets | 2,339,221 | 2,552,436 | 2,813,029 | 2,097,531 | 1,363,300 | |||||||||||||||||

| Liabilities of discontinued operations held for sale | $ | 220,549 | $ | 224,888 | $ | 225,042 | $ | 220,452 | $ | 207,321 | ||||||||||||

| Total current liabilities from continuing operations | 174,647 | 135,311 | 121,892 | 62,981 | 26,322 | |||||||||||||||||

| Deferred income taxes | 107,840 | 83,228 | 202,683 | 163,923 | 113,794 | |||||||||||||||||

| Long-term debt, including related party, net of current portion | 1,166,379 | 1,327,800 | 1,225,150 | 758,400 | 438,247 | |||||||||||||||||

| Total liabilities | 1,764,453 | 1,918,175 | 1,841,159 | 1,227,946 | 790,632 | |||||||||||||||||

| Members' equity | $ | 578,526 | $ | 628,838 | $ | 966,552 | $ | 864,425 | $ | 567,665 | ||||||||||||

| (1) |

| Includes a non-cash impairment charge of $7.5 million and $13.8 million recorded during the first six months of 2009 and the fourth quarter of 2008, respectively, at Atlantic Aviation. |

| (2) | Includes a non-cash impairment charge of $23.3 million and $21.7 million for contractual arrangements recorded |

| (3) | Reflects non-cash impairment charge of $71.2 million and $52.0 million recorded during the first six months of 2009 and the fourth quarter of 2008, respectively, at Atlantic Aviation. |

On January 28, 2010, we agreed to sell the assets of PCAA through a bankruptcy process, which we expect to complete in the first half of 2010. This business is now a discontinued operation and is therefore separately reported in our consolidated financial statements and is no longer a reportable segment.

The uncertainty and instability in the credit markets appears to be subsiding. This is evident in the increase in the volume of lending activity and the price at which such lending is occurring compared with levels during the height of the global financial crisis.

Despite the improvement in the credit markets, we expect towill continue to strengthen our consolidated balance sheet and thoseapply excess cash flow generated by Atlantic Aviation to the reduction of our operating entities through prudent reduction inthat business’ term loan principal, consistent with the amount of long-termamendments to the debt outstanding, further increasing the likelihoodfacility that we will be ableagreed to in

As part2010, the business recorded a non-cash loss on disposal of the bankruptcy filing, we have no obligation to and have no intention of committing additional capital to this business and our ongoing liabilities are expected to be no more than $5.3 million in guarantees of a single parking facility lease. Creditorsits assets totaling $4.4 million. This sale is pending as of this business do not have recourse to any assets of our holding company or any assets of our other businesses, other than approximately $5.3 millionreport date.

On December 23, 2009 we sold 49.99% ofand no amounts were outstanding under the non-controlling interest of District Energy to John Hancock Life Insurance Company and John Hancock Life Insurance Company (U.S.A.) (collectively “John Hancock”) for $29.5 million. The proceeds of the sale, along with other cash resources, were used to fully repay the $66.4 million balance on our holding company revolving credit facility as described below.

At Marchof December 31, 2009 we reclassifiedor at the outstanding balance drawn on the revolving credit facility at our non-operating holding company from long-term debt to current portion of long-term debt on our consolidated balance sheet due to its scheduledfacility’s maturity on March 31, 2010. During the year, we were in discussions with our lenders to convert theThis facility to a term loan and extend the maturity date of the $66.4 million outstanding balance.was not renewed or replaced. We have no holding company debt.

By December 2009, we had received unanimous approval from the lenders to extend the term of the facility. However, using the net cash proceeds we received from the sale of the 49.99% non-controlling interest in District Energy, and cash on hand, we paid off the outstanding principal balance on December 28, 2009 and avoided the substantial costs that would have been incurred had the terms of the facility been amended. Shortly thereafter we elected to reduce the amount available on the revolving credit facility from $97.0 million to $20.0 million through to the maturity of the facility at March 31, 2010.

in the markets serviced by IMTT’s major facilities. This condition, when combined with the attributes of IMTT’s facilities such as deep water drafts and access to land based infrastructure, have allowed IMTT to increase prices while maintaining very high storage capacity utilization rates.

Two key factors will likely have

The shareholders’ agreement between us, IMTT Holdings and its other shareholders specifies a default distribution policy for IMTT. Although the default under the shareholders’ agreement is to distribute excess cash, shareholders have indicated that they are prepared to reinvest excess cash generated during 2010 in new growth opportunities rather than pay distributions.

Thermal Chicago’s principal direct expense is electricity. Other direct expenses are water, labor, operations and maintenance and depreciation and accretion. Electricity usage, and to a lesser extent water usage, fluctuates in line with the volume of chilled water produced. Thermal Chicago focuses on minimizing the cost of electricity consumed per unit of chilled water produced by operating its plants to maximize efficient use of electricity. Other direct expenses are largely fixed regardless of the volumes of chilled water produced.

| Year Ended December 31, | Change (From 2009 to 2010) Favorable/(Unfavorable) | Change (From 2008 to 2009) Favorable/(Unfavorable) | |||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2009(1) | 2008(1) | $ | % | $ | % | |||||||||||||||||||||||||

| ($ In Thousands) (Unaudited) | |||||||||||||||||||||||||||||||

Revenue | |||||||||||||||||||||||||||||||

| Revenue from product sales | $ | 514,344 | $ | 394,200 | $ | 586,054 | 120,144 | 30.5 | (191,854 | ) | (32.7 | ) | |||||||||||||||||||

| Revenue from product sales – utility | 113,752 | 95,769 | 121,770 | 17,983 | 18.8 | (26,001 | ) | (21.4 | ) | ||||||||||||||||||||||

| Service revenue | 204,852 | 215,349 | 264,851 | (10,497 | ) | (4.9 | ) | (49,502 | ) | (18.7 | ) | ||||||||||||||||||||

| Financing and equipment lease income | 7,843 | 4,758 | 4,686 | 3,085 | 64.8 | 72 | 1.5 | ||||||||||||||||||||||||

| Total revenue | 840,791 | 710,076 | 977,361 | 130,715 | 18.4 | (267,285 | ) | (27.3 | ) | ||||||||||||||||||||||

Costs and expenses | |||||||||||||||||||||||||||||||

| Cost of product sales | 326,734 | 233,376 | 408,690 | (93,358 | ) | (40.0 | ) | 175,314 | 42.9 | ||||||||||||||||||||||

| Cost of product sales — utility | 90,542 | 73,907 | 105,329 | (16,635 | ) | (22.5 | ) | 31,422 | 29.8 | ||||||||||||||||||||||

| Cost of services | 53,088 | 46,317 | 63,850 | (6,771 | ) | (14.6 | ) | 17,533 | 27.5 | ||||||||||||||||||||||

Gross profit | 370,427 | 356,476 | 399,492 | 13,951 | 3.9 | (43,016 | ) | (10.8 | ) | ||||||||||||||||||||||

| Selling, general and administrative | 201,787 | 209,783 | 227,288 | 7,996 | 3.8 | 17,505 | 7.7 | ||||||||||||||||||||||||

| Fees to manager — related party | 10,051 | 4,846 | 12,568 | (5,205 | ) | (107.4 | ) | 7,722 | 61.4 | ||||||||||||||||||||||

| Goodwill impairment | — | 71,200 | 52,000 | 71,200 | NM | (19,200 | ) | (36.9 | ) | ||||||||||||||||||||||

| Depreciation | 29,721 | 36,813 | 40,140 | 7,092 | 19.3 | 3,327 | 8.3 | ||||||||||||||||||||||||

| Amortization of intangibles | 34,898 | 60,892 | 61,874 | 25,994 | 42.7 | 982 | 1.6 | ||||||||||||||||||||||||

| Loss on disposal of assets | 17,869 | — | — | (17,869 | ) | NM | — | — | |||||||||||||||||||||||

| Total operating expenses | 294,326 | 383,534 | 393,870 | 89,208 | 23.3 | 10,336 | 2.6 | ||||||||||||||||||||||||

Operating income (loss) | 76,101 | (27,058 | ) | 5,622 | 103,159 | NM | (32,680 | ) | NM | ||||||||||||||||||||||

Other income (expense) | |||||||||||||||||||||||||||||||

| Interest income | 29 | 119 | 1,090 | (90 | ) | (75.6 | ) | (971 | ) | (89.1 | ) | ||||||||||||||||||||

Interest expense(2) | (106,834 | ) | (95,456 | ) | (88,652 | ) | (11,378 | ) | (11.9 | ) | (6,804 | ) | (7.7 | ) | |||||||||||||||||

| Equity in earnings and amortization charges of investees | 31,301 | 22,561 | 1,324 | 8,740 | 38.7 | 21,237 | NM | ||||||||||||||||||||||||

| Loss on derivative instruments | — | (25,238 | ) | (2,843 | ) | 25,238 | NM | (22,395 | ) | NM | |||||||||||||||||||||

| Other income (expense), net | 712 | 570 | (198 | ) | 142 | 24.9 | 768 | NM | |||||||||||||||||||||||

| Net income (loss) from continuing operations before income taxes | 1,309 | (124,502 | ) | (83,657 | ) | 125,811 | 101.1 | (40,845 | ) | (48.8 | ) | ||||||||||||||||||||

| Benefit for income taxes | 8,697 | 15,818 | 14,061 | (7,121 | ) | (45.0 | ) | 1,757 | 12.5 | ||||||||||||||||||||||

| Net income (loss) from continuing operations | $ | 10,006 | $ | (108,684 | ) | $ | (69,596 | ) | 118,690 | 109.2 | (39,088 | ) | (56.2 | ) | |||||||||||||||||

| Net income (loss) from discontinued operations, net of taxes | 81,323 | (21,860 | ) | (110,045 | ) | 103,183 | NM | 88,185 | 80.1 | ||||||||||||||||||||||

| Net income (loss) | $ | 91,329 | $ | (130,544 | ) | $ | (179,641 | ) | 221,873 | 170.0 | 49,097 | 27.3 | |||||||||||||||||||

| Less: net income (loss) attributable to noncontrolling interests | 659 | (1,377 | ) | (1,168 | ) | (2,036 | ) | (147.9 | ) | 209 | 17.9 | ||||||||||||||||||||

| Net income (loss) attributable to MIC LLC | $ | 90,670 | $ | (129,167 | ) | $ | (178,473 | ) | 219,837 | 170.2 | 49,306 | 27.6 | |||||||||||||||||||

| Year Ended December 31 | Change (From 2008 to 2009) Favorable/(Unfavorable) | Change (From 2007 to 2008) Favorable/(Unfavorable) | ||||||||||||||||||||||||||

| 2009 | 2008(1) | 2007(1) | $ | % | $ | % | ||||||||||||||||||||||

| ($ In Thousands) | ||||||||||||||||||||||||||||

| Revenue | ||||||||||||||||||||||||||||

| Revenue from product sales | $ | 394,200 | $ | 586,054 | $ | 445,852 | (191,854 | ) | (32.7 | ) | 140,202 | 31.4 | ||||||||||||||||

| Revenue from product sales — utility | 95,769 | 121,770 | 95,770 | (26,001 | ) | (21.4 | ) | 26,000 | 27.1 | |||||||||||||||||||

| Service revenue | 215,349 | 264,851 | 207,680 | (49,502 | ) | (18.7 | ) | 57,171 | 27.5 | |||||||||||||||||||

| Financing and equipment lease income | 4,758 | 4,686 | 4,912 | 72 | 1.5 | (226 | ) | (4.6 | ) | |||||||||||||||||||

| Total revenue | 710,076 | 977,361 | 754,214 | (267,285 | ) | (27.3 | ) | 223,147 | 29.6 | |||||||||||||||||||

| Costs and expenses | ||||||||||||||||||||||||||||

| Cost of product sales | 231,139 | 406,997 | 302,283 | 175,858 | 43.2 | (104,714 | ) | (34.6 | ) | |||||||||||||||||||

| Cost of product sales – utility | 71,252 | 103,216 | 64,371 | 31,964 | 31.0 | (38,845 | ) | (60.3 | ) | |||||||||||||||||||

| Cost of services | 46,317 | 63,850 | 53,387 | 17,533 | 27.5 | (10,463 | ) | (19.6 | ) | |||||||||||||||||||

| Gross profit | 361,368 | 403,298 | 334,173 | (41,930 | ) | (10.4 | ) | 69,125 | 20.7 | |||||||||||||||||||

| Selling, general and administrative | 214,865 | 231,273 | 185,370 | 16,408 | 7.1 | (45,903 | ) | (24.8 | ) | |||||||||||||||||||

| Fees to manager – related party | 4,846 | 12,568 | 65,639 | 7,722 | 61.4 | 53,071 | 80.9 | |||||||||||||||||||||

| Goodwill impairment | 71,200 | 52,000 | — | (19,200 | ) | (36.9 | ) | (52,000 | ) | NM | ||||||||||||||||||

| Depreciation | 36,813 | 40,140 | 20,502 | 3,327 | 8.3 | (19,638 | ) | (95.8 | ) | |||||||||||||||||||

| Amortization of intangibles | 60,892 | 61,874 | 32,356 | 982 | 1.6 | (29,518 | ) | (91.2 | ) | |||||||||||||||||||

| Total operating expenses | 388,616 | 397,855 | 303,867 | 9,239 | 2.3 | (93,988 | ) | (30.9 | ) | |||||||||||||||||||

| Operating (loss) income | (27,248 | ) | 5,443 | 30,306 | (32,691 | ) | NM | (24,863 | ) | (82.0 | ) | |||||||||||||||||

| Other income (expense) | ||||||||||||||||||||||||||||

| Interest income | 119 | 1,090 | 5,705 | (971 | ) | (89.1 | ) | (4,615 | ) | (80.9 | ) | |||||||||||||||||

| Interest expense | (91,154 | ) | (88,652 | ) | (65,356 | ) | (2,502 | ) | (2.8 | ) | (23,296 | ) | (35.6 | ) | ||||||||||||||

| Loss on extinguishment of debt | — | — | (27,512 | ) | — | NM | 27,512 | NM | ||||||||||||||||||||

| Equity in earnings (losses) and amortization charges of investees | 22,561 | 1,324 | (32 | ) | 21,237 | NM | 1,356 | NM | ||||||||||||||||||||

| Loss on derivative instruments | (29,540 | ) | (2,843 | ) | (1,362 | ) | (26,697 | ) | NM | (1,481 | ) | (108.7 | ) | |||||||||||||||

| Other income (expense), net | 760 | (19 | ) | (1,088 | ) | 779 | NM | 1,069 | 98.3 | |||||||||||||||||||

| Net loss from continuing operations before noncontrolling interests | (124,502 | ) | (83,657 | ) | (59,339 | ) | (40,845 | ) | (48.8 | ) | (24,318 | ) | (41.0 | ) | ||||||||||||||

| Benefit for income taxes | 15,818 | 14,061 | 16,764 | 1,757 | 12.5 | (2,703 | ) | (16.1 | ) | |||||||||||||||||||

| Net loss from continuing operations before noncontrolling interests | (108,684 | ) | (69,596 | ) | (42,575 | ) | (39,088 | ) | (56.2 | ) | (27,021 | ) | (63.5 | ) | ||||||||||||||

| Net income attributable to noncontrolling interests | 486 | 585 | 554 | 99 | 16.9 | (31 | ) | (5.6 | ) | |||||||||||||||||||

| Net loss from continuing operations | $ | (109,170 | ) | $ | (70,181 | ) | $ | (43,129 | ) | (38,989 | ) | (55.6 | ) | (27,052 | ) | (62.7 | ) | |||||||||||

| Discontinued operations | ||||||||||||||||||||||||||||

| Net loss from discontinued operations before income taxes and noncontrolling interests | (23,647 | ) | (180,104 | ) | (9,679 | ) | 156,457 | 86.9 | (170,425 | ) | NM | |||||||||||||||||

| Benefit (provision) for income taxes | 1,787 | 70,059 | (281 | ) | (68,272 | ) | (97.4 | ) | 70,340 | NM | ||||||||||||||||||

| Net loss from discontinued operations before noncontrolling interests | (21,860 | ) | (110,045 | ) | (9,960 | ) | 88,185 | 80.1 | (100,085 | ) | NM | |||||||||||||||||

| Net loss attributable to noncontrolling interests | (1,863 | ) | (1,753 | ) | (1,035 | ) | 110 | 6.3 | 718 | 69.3 | ||||||||||||||||||

| Net loss from discontinued operations | $ | (19,997 | ) | $ | (108,292 | ) | $ | (8,925 | ) | 88,295 | 81.5 | (99,367 | ) | NM | ||||||||||||||

| Net loss | $ | (129,167 | ) | $ | (178,473 | ) | $ | (52,054 | ) | 49,306 | 27.6 | (126,419 | ) | NM | ||||||||||||||

| (1) | Reclassified to conform to current period presentation. |

| (2) | Interest expense includes non-cash losses on derivative instruments of $23.4 million and $4.3 million for the years ended December 31, 2010 and 2009, respectively. |

The fees payable to our Manager in 2008 were lower primarily due to performance fees of $44.0 million in 2007 that did not recur in 2008. Our Manager elected to reinvest these performance fees in additional LLC interests. Base fees paid to our Manager in 2008 also decreased due to our lower market capitalization.

Goodwill is considered impaired when the carrying amount of a reporting unit’s goodwill exceeds its implied fair value. Based on the testing performed, we recognized goodwill impairment charges at Atlantic Aviation in

Interest expenseterm loan debt at Atlantic Aviation and the repayment in the full amount of the outstanding balance of $66.4 million of MIC holding company debt during December 2009.

We recognized a loss on extinguishment of debt of $27.5 million in 2007, related to refinancings at Atlantic Aviation and District Energy. This loss included a $14.7 million make-whole payment for District Energy. The remainder was a non-cash write-off of previously deferred financing costs.

We discontinued hedge accounting at Atlantic Aviation as of February 25, 2009 and April 1, 2009 for our other businesses. In addition, in the first quarter of 2009, The Gas Company, District Energy and Atlantic Aviation each entered into LIBOR-based basis swaps. These basis swaps have lowered the effective cash interest rate on these businesses’ debt through March 2010.

For the year ended December 31, 2009, loss on derivative instruments represents the change in fair value of interest rate swaps from the dates that hedge accounting was discontinued. In addition, loss on derivative instruments includes the reclassification of amounts from accumulated other comprehensive loss into earnings, as Atlantic Aviation pays down its debt more quickly than anticipated.

We

Due to our NOL carryforwards, we do not expect to have regular taxable income or pay regular federal income tax payments through at least 2012. The cash state and local taxes paid by our businesses is discussed below in the sections entitledIncome Taxes for each of our individual businesses.

Further, approximately $53.4

On January 28, 2010, we agreed to sell the assets of PCAA through a bankruptcy process, which we expect to complete in the first half of 2010. Thisdebt. The results of operations from this business have beenand the gain from the bankruptcy sale are separately reported as a discontinued operationoperations in our consolidated financial statements and prior comparable periods have been re-statedrestated to conform to the current period presentation. See Note 4, “Discontinued Operations”, in our consolidated financial statements in “Financial Statements and Supplementary Data” in Part II, Item 8, of this Form 10-K for financial information and further discussions.

Corporate allocation and other intercompany fees charged to PCAA have been reported in earnings from discontinued operations in our consolidated continuing results of operations.

Effective this reporting period, we are

We define Free Cash Flow as cash from operating activities, less maintenance capital expenditures and changes in working capital. Working capital movements are excluded on the basis that these are largely timing differences in payables and receivables, and are therefore not reflective of our ability to generate cash.

A reconciliation of net lossincome (loss) attributable to MIC LLC from continuing operations to free cash flow from continuing operations, on a consolidated basis, is provided below:

| Year Ended December 31, | Change (From 2009 to 2010) Favorable/(Unfavorable) | Change (From 2008 to 2009) Favorable/(Unfavorable) | |||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 2009(1) | 2008(1) | $ | % | $ | % | |||||||||||||||||||||||||