| (Mark One) | ||

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

| New Jersey | 52-1273725 | |

(State or Other Jurisdiction of Incorporation or Organization) | (IRS Employer Identification Number) |

Large Accelerated Filer o | Accelerated Filer x | Non-Accelerated o | ||||

| Small Reporting Companyo |

Definitive proxy statement in connection with the 2010 Annual Stockholders Meeting to be filed with the Commission pursuant to Regulation 14A will be

| Page | |||||

| |||||

| 1 | |||||

| 6 | |||||

| 7 | |||||

| |||||

| |||||

| |||||

| |||||

| |||||

| |||||

Item 7. | 9 | ||||

| 42 | |||||

Item 8. | F-1 | ||||

| Report of Independent Registered Public Accounting Firm | F-2 | ||||

| Center Bancorp, Inc. and Subsidiaries: | |||||

| F-3 | |||||

| F-4 | |||||

| F-5 | |||||

| F-6 | |||||

| F-8 | |||||

| 44 | |||||

| |||||

| |||||

| |||||

| |||||

| |||||

| |||||

| |||||

Item 15. | 47 | ||||

| 50 | |||||

Information included in or incorporated by reference in this Annual Report on Form 10-K, other filings with the Securities and Exchange Commission and the Corporation’s press releases or other public statements, contain or may contain forward looking statements. Please refer to a discussion of the Corporation’s forward looking statements and associated risks in “Item 1 — Business — Historical Development of Business” and “Item 1A — Risk Factors” in this Annual Report on Form 10-K.

i

This report, in Item 1, Item 7 and elsewhere, includes forward-looking statements within the meaning of Sections 27A of the Securities Act of 1933, as amended, and 21E of the Securities Exchange Act of 1934, as amended, that involve inherent risks and uncertainties. This report contains certain forward-looking statements with respect to the financial condition, results of operations, plans, objectives, future performance and business of Center Bancorp, Inc. and its subsidiaries, including statements preceded by, followed by or that include words or phrases such as “believes,” “expects,” “anticipates,” “plans,” “trend,” “objective,” “continue,” “remain,” “pattern” or similar expressions or future or conditional verbs such as “will,” “would,” “should,” “could,” “might,” “can,” “may” or similar expressions. There are a number of important factors that could cause future results to differ materially from historical performance and these forward-looking statements. Factors that might cause such a difference include, but are not limited to: (1) competitive pressures among depository institutions may increase significantly; (2) changes in the interest rate environment may reduce interest margins; (3) prepayment speeds, loan origination and sale volumes, charge-offs and loan loss provisions may vary substantially from period to period; (4) general economic conditions may be less favorable than expected; (5) political developments, wars or other hostilities may disrupt or increase volatility in securities markets or other economic conditions; (6) legislative or regulatory changes or actions may adversely affect the businesses in which Center Bancorp, Inc. is engaged; (7) changes and trends in the securities markets may adversely impact Center Bancorp, Inc; (8) a delayed or incomplete resolution of regulatory issues could adversely impact our planning; (9) the impact of reputation risk created by the developments discussed above on such matters as business generation and retention, funding and liquidity could be significant; and (10) the outcome of regulatory and legal investigations and proceedings may not be anticipated. Further information on other factors that could affect the financial results of Center Bancorp, Inc. are included in Item 1A of this Annual Report on Form 10-K and in Center Bancorp’s other filings with the Securities and Exchange Commission. These documents are available free of charge at the Commission’s website at http://www.sec.gov and/or from Center Bancorp, Inc. Center Bancorp, Inc. assumes no obligation to update forward-looking statements at any time.

Center Bancorp, Inc., a one-bank holding company, was incorporated in the state of New Jersey on November 12, 1982. Center Bancorp, Inc., commenced operations on May 1, 1983, upon the acquisition of all outstanding shares of capital stock of Union Center National Bank (the “Bank”), its principal subsidiary. The holding company’s sole activity, at this time, is to act as a holding company for the Bank and other subsidiaries. As used herein, the term “Corporation” shall refer to Center Bancorp, Inc. and its direct and indirect subsidiaries and the term “Parent Corporation” shall refer to Center Bancorp, Inc. on an unconsolidated basis. In addition to its principal subsidiary, Center Bancorp, Inc. owns 100 percent of the voting shares of Center Bancorp, Inc. Statutory Trust II, through which it issued trust preferred securities. Center Bancorp, Inc. Statutory Trust II is not a consolidated subsidiary. See Note 10 of the Consolidated Financial Statements.

The Corporation’s wholly-owned subsidiaries are all included in the consolidated financial statements of Center Bancorp, Inc. These subsidiaries include an advertising subsidiary; an insurance subsidiary offering annuity products, property and casualty, life and health insurance, and various investment subsidiaries which hold, maintain and manage investment assets for the Corporation. In the past, the Corporation’s subsidiaries have also included real estate investment trust subsidiaries (the “REIT” subsidiaries) and two title insurance partnerships. The title insurance partnerships were liquidated and ceased operations in December 2009. During the fourth quarter of 2006, the Corporation effected an internal entity reorganization and adopted a plan of liquidation for its one remaining REIT subsidiary, which was completed on November 16, 2007.

During 2001 and 2003, the Corporation formed statutory business trusts, which exist for the exclusive purpose of (i) issuing trust securities representing undivided beneficial interests in the assets of a trust; (ii) investing the gross proceeds of the trust securities in junior subordinated deferrable interest debentures (subordinated debentures) of the Corporation; and (iii) engaging in only those activities necessary or incidental thereto. These subordinated debentures and the related income effects are not eliminated in the consolidated financial statements as the statutory business trusts are not consolidated in accordance with Financial Accounting Standards Board (“FASB”) FASB ASC 810-10 (previously FASB interpretation No. 46(R), “Consolidation of Variable Interest Entities.” Distributions on the subordinated debentures owned by the subsidiary trusts have been classified as interest expense in the Consolidated Statements of Income.

The Corporation issued $10.3 million of subordinated debentures in 2001 and $5.2 million of subordinated debentures in 2003. On December 18, 2006, the Corporation redeemed $10.3 million of subordinated debentures and dissolved Center Bancorp, Inc. Statutory Trust I. At December 31, 2009, the $5.2 million of these securities still outstanding are included as a component of Tier 1 Capital for regulatory purposes. The Tier 1 leverage capital ratio was 7.80 percent at December 31, 2009.

During 2002, the Bank established two investment subsidiaries to hold portions of its securities portfolio. At December 2007, under a plan of liquidation adopted by the Bank, one of the investment companies had been liquidated. During 2008, the Corporation formed a new investment company. In January of 2003, the Corporation established an insurance subsidiary for the sale of insurance and annuity products. The Corporation also formed a title insurance partnership during the later part of 2007 that was fully operational in 2008. During the early part of 2008, the Corporation formed a second title partnership that was fully operational during the second half of 2008. Both title insurance partnerships were liquidated during December, 2009 and the Bank no longer provides title insurance.

The Parent Corporation makes its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K and amendments thereto available on its website atwww.centerbancorp.com without charge as soon as reasonably practicable after filing or furnishing them to the SEC. Also available on the website are the Corporation’s corporate code of ethics that applies to all of the Corporation’s employees, including principal officers and directors, and charters for the Audit Committee, Compensation Committee and Nominating Committee.

The Parent Corporation has filed the certifications of the Chief Executive Officer and Chief Financial Officer required pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 with respect to the Parent Corporation’s Annual Report on Form 10-K as exhibits to this Report. Center Bancorp’s CEO submitted the required annual CEO’s Certification regarding the NASDAQ’s corporate governance listing standards, Section 12(a) CEO Certification, to the NASDAQ within the required time frame after the 2009 annual shareholders’ meeting.

Additionally, the Parent Corporation will provide without charge, a copy of its Annual Report on Form 10-K to any shareholder by mail. Requests should be sent to Center Bancorp, Inc, Attention: Shareholder Relations, 2455 Morris Avenue, Union, New Jersey, 07083.

The Bank offers a broad range of lending, depository and related financial services to commercial, industrial and governmental customers. In 1999, the Bank obtained full trust powers, enabling it to offer a variety of trust services to its customers. In the lending area, the Bank’s services include short and medium term loans, lines of credit, letters of credit, working capital loans, real estate construction loans and mortgage loans. In the depository area, the Bank offers demand deposits, savings accounts and time deposits. In addition, the Bank offers collection services, wire transfers, night depository and lock box services.

The Bank offers a broad range of consumer banking services, including interest bearing and non-interest bearing checking accounts, savings accounts, money market accounts, certificates of deposit, IRA accounts, Automated Teller Machine (“ATM”) accessibility using Star Systems, Inc. service, secured and unsecured loans, mortgage loans, home equity lines of credit, safe deposit boxes, Christmas club accounts, vacation club accounts, money orders and travelers’ checks.

The Bank, through its subsidiary, Center Financial Group LLC, provides financial services, including brokerage services, insurance and annuities, mutual funds and financial planning. In the fourth quarter of 2007, the Corporation formed a title insurance partnership, Center Title LLC, with Progressive Title Company in Parsippany, New Jersey to provide title services in connection with the closing of real estate transactions. In January 2008, the Corporation formed a title insurance partnership, Union Title LLC, with Elite Title Abstract of West Caldwell, New Jersey to provide title services in connection with the closing of real estate loan transactions. Our partnerships with both title companies were liquidated during December, 2009.

The Bank offers various money market services. It deals in U.S. Treasury and U.S. Governmental agency securities, certificates of deposit, commercial paper and repurchase agreements.

The Bank entered into a limited liability company operating agreement with Morris Property Company, LLC, a New Jersey limited liability company, during the fourth quarter of 2008. The purpose of Morris Property Company, LLC is to hold foreclosed assets.

Competitive pressures affect the Corporation’s manner of conducting business. Competition stems not only from other commercial banks but also from other financial institutions such as savings banks, savings and loan associations, mortgage companies, leasing companies and various other financial service and advisory companies. Many of the financial institutions operating in the Corporation’s primary market are substantially larger and offer a wider variety of products and services than the Corporation.

The banking industry is highly regulated. Statutory and regulatory controls increase a bank holding company’s cost of doing business and limit the options of its management to deploy assets and maximize income. The following discussion is not intended to be a complete list of all the activities regulated by the banking laws or of the impact of such laws and regulations on the Corporation or its Bank subsidiary. It is intended only to briefly summarize some material provisions.

Center Bancorp, Inc. is a bank holding company within the meaning of the Bank Holding Company Act of 1956 (the “Holding Company Act”). As a bank holding company, the Parent Corporation is supervised by the Board of Governors of the Federal Reserve System (“FRB”) and is required to file reports with the FRB and provide such additional information as the FRB may require. The Parent Corporation and it subsidiaries are subject to examination by the FRB.

On November 9, 2007, the FRB approved the Parent Corporation’s application to become a Financial Holding Company. A Financial Holding Company may perform the following activities: insurance underwriting, securities dealing and underwriting, financial and investment advisory services, merchant banking and issuing or selling security interests in bank-eligible assets. Financial Holding Companies may also engage in any other activity that the FRB determines to be financial in nature or incidental to financial activities after consultation with the Secretary of the Treasury. A Financial Holding Company may also engage in any non-financial activity that the FRB determines is complementary to a financial activity and does not pose a substantial risk to the safety or soundness of depository institutions or the financial system. As of December 31, 2009, the Corporation officially rescinded its status as a financial services holding company as a result of the discontinuation of the title insurance activities.

The Holding Company Act prohibits the Corporation, with certain exceptions, from acquiring direct or indirect ownership or control of more than five percent of the voting shares of any company which is not a bank and from engaging in any business other than that of banking, managing and controlling banks or furnishing services to subsidiary banks, except that it may, upon application, engage in, and may own shares of companies engaged in, certain businesses found by the FRB to be so closely related to banking “as to be a proper incident thereto.” The Holding Company Act requires prior approval by the FRB of the acquisition by Center Bancorp, Inc. of more than five percent of the voting stock of any other bank. Satisfactory capital ratios and Community Reinvestment Act ratings and anti-money laundering policies are generally prerequisites to obtaining federal regulatory approval to make acquisitions. The policy of the FRB provides that a bank holding company is expected to act as a source of financial strength to its subsidiary bank and to commit resources to support the subsidiary bank in circumstances in which it might not do so absent that policy.

Acquisitions through Union Center National Bank require approval of the Office of the Comptroller of the Currency of the United States (“OCC”). The Holding Company Act does not place territorial restrictions on the activities of non-bank subsidiaries of bank holding companies. The Gramm-Leach-Bliley Act, discussed below, allows the Corporation to expand into insurance, securities, merchant banking activities, and other activities that are financial in nature.

The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994 (“Interstate Banking and Branching Act”) enables bank holding companies to acquire banks in states other than their home state, regardless of applicable state law. The Interstate Banking and Branching Act also authorizes banks to merge across state lines, thereby creating interstate banks with branches in more than one state. Under the legislation, each state had the opportunity to “opt-out” of this provision. Furthermore, a state may “opt-in” with respect tode novo branching, thereby permitting a bank to open new branches in a state in which the bank does not already have a branch. Withoutde novo branching, an out-of-state commercial bank can enter the state only by acquiring an existing bank or branch. The vast majority of states have allowed interstate banking by merger but have not authorizedde novo branching.

New Jersey enacted legislation to authorize interstate banking and branching and the entry into New Jersey of foreign country banks. New Jersey did not authorizede novo branching into the state. However, under federal law, federal savings banks which meet certain conditions may branchde novo into a state, regardless of state law.

The operations of the Bank are subject to requirements and restrictions under federal law, including requirements to maintain reserves against deposits, restrictions on the types and amounts of loans that may be granted, and limitations on the types of investments that may be made and the types of services which may be offered. Various consumer laws and regulations also affect the operations of the Bank. Approval of the Comptroller of the Currency is required for branching, bank mergers in which the continuing bank is a national bank and in connection with certain fundamental corporate changes affecting the Bank. There are various legal limitations, including Sections 23A and 23B of the Federal Reserve Act, which govern the extent to which a bank subsidiary may finance or otherwise supply funds to its holding company or its holding company’s non-bank subsidiaries. Under federal law, no bank subsidiary may, subject to certain limited exceptions, make loans or extensions of credit to, or investments in the securities of, its parent or the non-bank subsidiaries of its parent (other than direct subsidiaries of such bank which are not financial subsidiaries) or take their securities as collateral for loans to any borrower. Each bank subsidiary is also subject to collateral security requirements for any loans or extensions of credit permitted by such exceptions.

The Bank and the OCC have entered into an informal Memorandum of Understanding, or MOU. A memorandum of understanding is characterized by the regulatory authorities as an informal action that is not published or publicly available and that is used when circumstances warrant a milder form of action than a formal supervisory action. Among other things, under the MOU, the Bank has agreed to develop a three year capital program, which will include specific plans for the maintenance of adequate capital and the strengthening of the Bank’s capital structure to meet the Bank’s current and future needs, a profit plan that includes the identification of the major areas and means by which the Board will seek to improve the Bank’s operating performance, and a dividend policy that permits the declaration of a dividend by the Bank only with the prior approval of the OCC. Management is committed to addressing and resolving the issues raised by the OCC and has substantially completed corrective actions to comply with the MOU. In addition, the OCC has established higher minimum capital ratios for the Bank than the regulatory minimums. See “FDICIA.”

The Federal Reserve Board has issued Regulation W, which codifies prior regulations under Sections 23A and 23B of the Federal Reserve Act and interpretative guidance with respect to affiliate transactions. Regulation W incorporates the exemption from the affiliate transaction rules but expands the exemption to cover the purchase of any type of loan or extension of credit from an affiliate. Affiliates of a bank include, among other entities, the bank’s holding company and companies that are under common control with the bank. The Parent Corporation is considered to be an affiliate of the Bank. In general, subject to certain specified exemptions, a bank or its subsidiaries are limited in their ability to engage in “covered transactions” with affiliates:

In addition, a bank and its subsidiaries may engage in covered transactions and other specified transactions only on terms and under circumstances that are substantially the same, or at least as favorable to the bank or its subsidiary, as those prevailing at the time for comparable transactions with nonaffiliated companies. A “covered transaction” includes:

In addition, under Regulation W:

Regulation W generally excludes all non-bank and non-savings association subsidiaries of banks from treatment as affiliates, except to the extent that the Federal Reserve Board decides to treat these subsidiaries as affiliates.

Under the Financial Institutions Reform, Recovery, and Enforcement Act of 1989 (“FIRREA”), a depository institution insured by the Federal Deposit Insurance Corp (“FDIC”) can be held liable for any loss incurred by, or reasonably expected to be incurred by, the FDIC in connection with (i) the default of a commonly controlled FDIC-insured depository institution or (ii) any assistance provided by the FDIC to a commonly controlled FDIC-insured depository institution in danger of default. These provisions have commonly been referred to as FIRREA’s “cross guarantee” provisions. Further, under FIRREA, the failure to meet capital guidelines could subject a bank to a variety of enforcement remedies available to federal regulatory authorities.

FIRREA also imposes certain independent appraisal requirements upon a bank’s real estate lending activities and further imposes certain loan-to-value restrictions on a bank’s real estate lending activities. The bank regulators have promulgated regulations in these areas.

Pursuant to the Federal Deposit Insurance Corporation Improvement Act of 1991 (“FDICIA”), each federal banking agency has promulgated regulations, specifying the levels at which a financial institution would be considered “well capitalized,” “adequately capitalized,” “undercapitalized,” “significantly undercapitalized,” or “critically undercapitalized,” and to take certain mandatory and discretionary supervisory actions based on the capital level of the institution. To qualify to engage in financial activities under the Gramm-Leach-Bliley Act, all depository institutions must be “well capitalized.” The financial holding company of a national bank will be put under directives to raise its capital levels or divest its activities if the depository institution falls from that level.

The OCC’s regulations implementing these provisions of FDICIA provide that an institution will be classified as “well capitalized” if it (i) has a total risk-based capital ratio of at least 10.0 percent, (ii) has a Tier 1 risk-based capital ratio of at least 6.0 percent, (iii) has a Tier 1 leverage ratio of at least 5.0 percent, and (iv) meets certain other requirements. An institution will be classified as “adequately capitalized” if it (i) has a total risk-based capital ratio of at least 8.0 percent, (ii) has a Tier 1 risk-based capital ratio of at least 4.0 percent, (iii) has a Tier 1 leverage ratio of (a) at least 4.0 percent or (b) at least 3.0 percent if the institution was rated 1 in its most recent examination, and (iv) does not meet the definition of “well capitalized.” An institution will be classified as “undercapitalized” if it (i) has a total risk-based capital ratio of less than 8.0 percent, (ii) has a Tier 1 risk-based capital ratio of less than 4.0 percent, or (iii) has a Tier 1 leverage ratio of (a) less than 4.0 percent or (b) less than 3.0 percent if the institution was rated 1 in its most recent examination. An institution will be classified as “significantly undercapitalized” if it (i) has a total risk-based capital ratio of less than 6.0 percent, (ii) has a Tier 1 risk-based capital ratio of less than 3.0 percent, or (iii) has a Tier 1 leverage ratio of less than 3.0 percent. An institution will be classified as “critically undercapitalized” if it has a tangible equity to total assets ratio that is equal to or less than 2.0 percent. An insured depository institution may be deemed to be in a lower capitalization category if it receives an unsatisfactory examination rating. The OCC has established higher minimum capital ratios for the Bank effective as of December 31, 2009: Tier 1 Risk-Based Capital of 10.0 percent, Total Risk-Based Capital of 12.0 percent and Tier 1 Leverage Capital of 8.0 percent. Similar categories apply to bank holding companies. At December 31, 2009, the Bank’s capital ratios were all above the minimum levels required, other than the Tier 1 Leverage Capital ratio, which was slightly below the 8.0 percent established by the OCC for the Bank.

In addition, significant provisions of FDICIA required federal banking regulators to impose standards in a number of other important areas to assure bank safety and soundness, including internal controls, information systems and internal audit systems, credit underwriting, asset growth, compensation, loan documentation and interest rate exposure. Under the MOU between the Bank and the OCC, the bank has agreed to develop a three year capital program, which will include specific plans for the maintenance of adequate capital and the strengthening of the Bank’s capital structure to meet current and future needs.

On November 21, 2008, the Board of Directors of the FDIC adopted a final rule relating to the Temporary Liquidity Guarantee Program (the “TLG Program”). The TLG Program was announced by the FDIC on October 14, 2008, to strengthen confidence and encourage liquidity in the banking system. Under the original TLG Program the FDIC would guarantee, through the earlier of maturity or June 30, 2012, certain newly issued senior unsecured debt issued by participating institutions on or after October 14, 2008, and before June 30, 2009 (the “Debt Guarantee Program”). The Debt Guarantee Program was extended for senior unsecured debt issued after April 1, 2009 and before October 31, 2009, and maturing on or after December 31, 2012. On October 20, 2009, the FDIC established a limited, six-month emergency guarantee facility upon expiration of the Debt Guarantee Program. Under this emergency guarantee facility, certain participating entities can apply to the FDIC for permission to issue FDIC-guaranteed debt during the period starting October 31, 2009 through April 30, 2010. As of December 31, 2009, the Bank had no senior unsecured debt scheduled to mature on or before April 30, 2010.

The other provision of the TLG Program provided full FDIC deposit insurance coverage for non-interest bearing transaction deposit accounts, NOW accounts paying less than 0.5 percent interest per annum and certain types of interest paying attorney trust accounts held at participating FDIC-insured institutions originally

through December 31, 2009 (the “Transaction Account Guarantee Program”). The Transaction Account Guarantee Program has been extended to June 30, 2010. Entities that wish to continue their participation in the Transaction Account Guarantee Program during the extension need not take any additional action. After December 31, 2009, those institutions that have not opted out of the extension will be charged an annualized rate according to the institutions risk category. The assessments will be paid each quarter and will be based on amounts over $250,000 for the portion of the quarter that the institution is assigned to the risk category. The Bank has elected to continue participation in the Transaction Account Guarantee Program.

Substantially all of the deposits of the Bank are insured up to applicable limits by the Deposit Insurance Fund (“DIF”) of the FDIC and are subject to deposit insurance assessments to maintain the DIF. The FDIC utilizes a risk-based assessment system that imposes insurance premiums based upon a risk matrix that takes into account a bank’s capital level and supervisory rating, known as a “CAMEL rating”. On December 16, 2008, the FDIC adopted a final rule increasing risk-based assessment rates uniformly by 7 basis points (7 cents for every $100 of deposits), on an annual basis, for the first quarter of 2009. Subsequently on April 1, 2009, the FDIC issued rules which attempted to improve the methodology of the assessment system by differentiating risk among insured institutions.

On May 22, 2009, the Board of Directors of the FDIC adopted a final rule imposing a special assessment on the entire banking industry. The special assessment was calculated as 5 basis points times each insured depository institution’s assets minus Tier I capital as reported in the report of condition of June 30, 2009 and would not exceed ten times the institutions assessment base for the second quarter 2009 risk-based assessment. This special assessment, which totaled $1.2 million, was collected on September 30, 2009. Including this special assessment, the Bank paid a total of $2.1 million in FDIC assessments in 2009.

On November 12, 2009, the FDIC adopted the final rule which required insured depository institutions to prepay their quarterly risk-based assessments for the fourth quarter of 2009 through the fourth quarter of 2012. An institution’s prepaid assessment for the fourth quarter of 2009 and all of 2010 will be determined by multiplying the total base assessment rate that the institution would have paid for the third quarter of 2009 times the corresponding prepaid assessment base for each quarter. For each quarter of the prepayment period, an institution’s prepaid assessment base will be calculated by increasing its third quarter 2009 assessment base at an annual rate of 5 percent. An institution’s prepaid assessment for each quarter of 2011 and 2012 will be determined by multiplying its prepaid assessment rate plus .75 basis points times the corresponding prepaid assessment base for each quarter. On December 30, 2009, the Corporation remitted an FDIC prepayment in the amount of $5.7 million.

The enactment of the Emergency Economic Stabilization Act of 2008 (“EESA”) temporarily raised the basic limit on federal deposit insurance coverage from $100,000 to $250,000 per depositor. The temporary increase in deposit insurance coverage became effective on October 3, 2008. On May 20, 2009, the temporary increase to $250,000 per depositor was extended through December 31, 2013. On January 1, 2014, deposit insurance coverage will return to $100,000.

In addition to deposit insurance assessments, the FDIC is required to continue to collect from institutions payments for the servicing of obligations of the Financing Corporation (“FICO”) that were issued in connection with the resolution of savings and loan associations, so long as such obligations remain outstanding. The Corporation paid a FICO premium of $82,000 in 2009.

The Gramm-Leach-Bliley Financial Modernization Act of 1999 became effective in early 2000. The Modernization Act:

The Modernization Act also modified other financial laws, including laws related to financial privacy and community reinvestment.

Under the Community Reinvestment Act (“CRA”), as implemented by OCC regulations, a national bank has a continuing and affirmative obligation consistent with its safe and sound operation to help meet the credit needs of its entire community, including low and moderate income neighborhoods. The CRA does not establish specific lending requirements or programs for financial institutions nor does it limit an institution’s discretion to develop the types of products and services that it believes are best suited to its particular community, consistent with the CRA. The CRA requires the OCC, in connection with its examination of a national bank, to assess the bank’s record of meeting the credit needs of its community and to take such record into account in its evaluation of certain applications by such bank.

In response to the events of September 11, 2001, the Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act of 2001 (the “USA PATRIOT Act”), was signed into law on October 26, 2001. The USA PATRIOT Act gives the federal government powers to address terrorist threats through domestic security measures, surveillance powers, information sharing, and anti-money laundering requirements. By way of amendments to the Bank Secrecy Act, the USA PATRIOT Act encourages information sharing among bank regulatory agencies and law enforcement bodies. Further, certain provisions of the USA PATRIOT Act impose affirmative obligations on a broad range of financial institutions, including banks, thrifts, brokers, dealers, credit unions, money transfer agents and parties registered under the Commodity Exchange Act.

Among other requirements, the USA PATRIOT Act imposes the following requirements with respect to financial institutions:

The stated goals of the Sarbanes-Oxley Act of 2002 (the “SOA”) are to increase corporate responsibility, to provide for enhanced penalties for accounting and auditing improprieties by publicly traded companies and to protect investors by improving the accuracy and reliability of corporate disclosures pursuant to the securities laws.

The SOA generally applies to all companies, both U.S. and non-U.S., that file or are required to file periodic reports with the Securities and Exchange Commission (the “SEC”) under the Securities Exchange Act of 1934 (the “Exchange Act”).

The SOA includes specific disclosure requirements and corporate governance rules, requires the SEC and securities exchanges to adopt extensive additional disclosure, corporate governance and other related rules and mandates further studies of certain issues by the SEC. The SOA addresses, among other matters:

In response to recent unprecedented market turmoil, EESA was enacted on October 3, 2008. EESA authorizes the U.S. Treasury Department (the “treasury”) to provide up to $700 billion in funding for the financial services industry. Pursuant to the EESA, the Treasury was initially authorized to use $350 billion for the Troubled Asset Relief Program (“TARP”). Of this amount, the Treasury allocated $250 billion to the TARP Capital Purchase Program. On January 15, 2009, the second $350 billion of TARP monies was released to the Treasury. As described elsewhere in this Annual Report on Form 10-K, the Treasury purchased $10,000,000 of the Parent Corporation’s non-convertible preferred stock (the “Preferred Shares”) under the TARP Capital Purchase Program.

Participants in the TARP Capital Purchase Program were required to accept several compensation-related limitations associated with this Program. In January 2009, five executive officers of the Corporation (Messrs. Weagley, Abrahamian, Shapiro and Boylan and Ms. Wunder) agreed in writing to accept the compensation standards in existence at that time under the Capital Purchase Program and thereby cap or eliminate some of their contractual or legal rights. The provisions agreed to were as follows:

During the CPP Covered Period, the Corporation is not permitted to take federal income tax deductions for compensation paid to the senior executive officers in excess of $500,000 per year, subject to certain exceptions.

On February 17, 2009, the American Recovery and Reinvestment Act of 2009 (the “Stimulus Act”) was enacted. The Stimulus Act contains several provisions designed to establish executive compensation and governance standards for financial institutions (such as the Corporation) that received or will receive financial assistance under TARP. In certain instances, the Stimulus Act modified the compensation-related limitations contained in the TARP Capital Purchase Program; in addition, the Stimulus Act created additional compensation-related limitations and directed the Treasury to establish standards for executive compensation applicable to participants in TARP. In their January 2009 agreements, the Corporation’s executives did not waive their rights with respect to the provisions implemented by the Stimulus Act; other employees now covered by these provisions were not asked and did not agree to waive their rights. The compensation-related limitations applicable to the Corporation which have been added or modified by the Stimulus Act are as follows, which provisions are expected to be included in standards established by the Treasury:

From time to time proposals are made in the U.S. Congress and before various bank regulatory authorities, which would alter the policies of and place restrictions on different types of banking operations. It is impossible to predict the impact, if any, of potential legislative trends on the business of the Corporation and the Bank.

The Corporation’s authority to extend credit to its directors and executive officers, as well as to entities controlled by such persons, is currently governed by the requirements of the National Bank Act, the Sarbanes-Oxley Act of 2002 and Regulation O of the Federal Reserve Bank. Among other things, these provisions require that extensions of credit to insiders (i) be made on terms that are substantially the same as, and follow credit underwriting procedures that are not less stringent than, those prevailing for comparable transactions with unaffiliated persons and that do not involve more than the normal risk of repayment or present other

unfavorable features and (ii) not exceed certain limitations on the amount of credit extended to such persons, individually and in the aggregate, which limits are based, in part, on the amount of the Corporation’s capital. In addition, the Corporation’s Board of Directors must approve extensions of credit in excess of certain limits. Under the SOA, the Corporation and its subsidiaries, other than Union Center National Bank, may not extend or arrange for any personal loans to its directors and executive officers.

The Parent Corporation is a legal entity separate and distinct from the Bank. Virtually all of the revenue of the Parent Corporation available for payment of dividends on its capital stock will result from amounts paid to the Parent Corporation by the Bank. All such dividends are subject to various limitations imposed by federal laws and by regulations and policies adopted by federal regulatory agencies. As a national bank, the Bank may not pay a dividend if it would impair the capital of the Bank. Furthermore, prior approval by the Comptroller of the Currency is required if the total of dividends declared in a calendar year exceeds the total of the Bank’s net profits for that year combined with the retained profits for the two preceding years. The Company’s current MOU provides that the Bank cannot declare a dividend without the prior approval of the OCC.

On January 9, 2009, as part of the TARP Capital Purchase Program, the Parent Corporation entered into a Letter Agreement (the “Letter Agreement”) and a Securities Purchase Agreement — Standard Terms attached thereto (the “Securities Purchase Agreement”) with the Treasury, pursuant to which (i) the Parent Corporation issued and sold, and the Treasury purchased, 10,000 shares of the Parent Corporation’s Fixed Rate Cumulative Perpetual Preferred Stock, Series A, having a liquidation preference of $1,000 per share, for an aggregate purchase price of $10,000,000 in cash, and (ii) the Parent Corporation issued to the Treasury a ten-year warrant (the “Warrant”) to purchase up to 173,410 shares of the Corporation’s common stock at an exercise price of $8.65 per share. The Securities Purchase Agreement contains limitations on the payment of dividends on the common stock. Specifically, the Parent Corporation is unable to declare dividend payments on the common stock (and certain preferred stock if the Corporation issues additional series of preferred stock) if the Parent Corporation is in arrears in the payment of dividends on the Preferred Shares. Further, until the third anniversary of the investment or when all of the Preferred Shares have been redeemed or transferred, the Parent Corporation is not permitted to increase the amount of the quarterly cash dividend above $0.09 per share, which was the amount of the last regular dividend declared by the Parent Corporation prior to October 14, 2008.

If, in the opinion of the OCC, a bank under its jurisdiction is engaged in or is about to engage in an unsafe or unsound practice (which could include the payment of dividends), the OCC may require, after notice and hearing, that such bank cease and desist from such practice or, as a result of an unrelated practice, require the bank to limit dividends in the future. The FRB has similar authority with respect to bank holding companies. In addition, the FRB and the OCC have issued policy statements which provide that insured banks and bank holding companies should generally only pay dividends out of current operating earnings. Regulatory pressures to reclassify and charge off loans and to establish additional loan loss reserves can have the effect of reducing current operating earnings and thus impacting an institution’s ability to pay dividends. Further, as described herein, the regulatory authorities have established guidelines with respect to the maintenance of appropriate levels of capital by a bank or bank holding company under their jurisdiction. Compliance with the standards set forth in these policy statements and guidelines could limit the amount of dividends which the Parent Corporation and the Bank may pay. Under FDICIA, banking institutions which are deemed to be “undercapitalized” will, in most instances, be prohibited from paying dividends.

Credit risks are an inherent part of the lending function. The Corporation has set in place specific policies and guidelines to limit credit risks. The following describes the Corporation’s credit management policy and identifies certain risk elements in its earning assets portfolio.

The maintenance of comprehensive and effective credit policies is a paramount objective of the Corporation. Credit procedures are enforced by the department heads of the different lending units and are maintained at the senior administrative level as well as through internal control procedures.

Prior to extending credit, the Corporation’s credit policy generally requires a review of the borrower’s credit history, repayment capacity, collateral and purpose of each loan. Requests for most commercial and consumer loans are to be accompanied by financial statements and other relevant financial data for evaluation. After the granting of a loan or lending commitment, this financial data is typically updated and evaluated by the credit staff on a periodic basis for the purpose of identifying potential problems. Construction financing requires a periodic submission by the borrowers of sales/leasing status reports regarding their projects, as well as, in most cases, inspections of the project sites by independent engineering firms and/or independent consultants. Advances are normally made only upon the satisfactory completion of periodic phases of construction.

Certain lending authorities are granted to loan officers based upon each officer’s position and experience. However, large dollar loans and lending lines are reported to and are subject to the approval of the Bank’s loan committees and/or board of directors. Either the Chairman of the Board or President chairs the loan committees.

The Corporation has established its own internal loan-to-value (“LTV”) limits for real estate loans. In general, except as described below, these internal limits are not permitted to exceed the following supervisory limits:

It may be appropriate in individual cases to originate loans with loan-to-value ratios in excess of the supervisory LTV limits, based on support provided by other credit factors. The President of the Bank must approve such non-conforming loans. The Bank must identify all non-conforming loans and their aggregate amount must be reported at least quarterly to the Directors’ Loan Committee. Non-conforming loans should not exceed 100% of capital, or 30% with respect to non one to four family residential loans. At present, management is unaware of any exceptions to supervisory LTV limits.

Collateral margin guidelines are based on cost, market or other appraised value to maintain a reasonable amount of collateral protection in relation to the inherent risk in the loan. This does not mitigate the fundamental analysis of cash flow from the conversion of assets in the normal course of business or from operations to repay the loan. It is merely designed to provide a cushion to minimize the risk of loss if the ultimate collection of the loan becomes dependent on the liquidation of security pledged.

The Corporation also seeks to minimize lending risk through loan diversification. The composition of the Corporation’s commercial loan portfolio reflects and is highly dependent upon the economy and industrial make-up of the region it serves. Effective loan diversification spreads risk to many different industries, thereby reducing the impact of downturns in any specific industry on overall loan profitability.

Credit quality is monitored through an internal review process, which includes a credit Risk Grading System that facilitates the early detection of problem loans. Under this grading system, all commercial loans and commercial mortgage loans are graded in accordance with the risk characteristics inherent in each loan. Problem loans include non-accrual loans, and loans which conform to the regulatory definitions of criticized and classified loans.

A Problem Asset Report is prepared monthly and is examined by the senior management of the Bank, the Corporation’s Loan and Discount Committee and Board of Directors. This review is designed to enable management to take such actions as are considered necessary to identify and remedy problems on a timely basis.

The Bank’s internal loan review process is complemented by an independent loan review conducted throughout the year, under the mandate and approval of the Corporation’s Board of Directors. In addition, regularly scheduled audits performed by the Bank’s internal audit function are designed to ensure the integrity of the credit and risk monitoring systems currently in place.

The risk elements identified by the Corporation include non-performing loans, loans past due ninety days or more as to interest or principal payments but not placed on a non-accrual status, potential problem loans, other real estate owned, net, and other non-performing interest-earning assets.

| • | we potentially face increased regulation of our industry and compliance with such regulation may increase our costs and limit our ability to pursue business opportunities; | |

| • | customer demand for loans secured by real estate could be reduced due to weaker economic conditions, an increase in unemployment, a decrease in real estate values or an increase in interest rates; |

asset values and by a lack of liquidity. The liquidity issues have been particularly acute for regional and community banks, as many of the larger financial institutions have significantly curtailed their lending to regional and community banks to reduce their exposure to the risks of other banks. In addition, many of the larger correspondent lenders have reduced or even eliminated federal funds lines for their correspondent customers. Furthermore, regional and community banks generally have less access to the capital markets than do the national and super-regional banks because of their smaller size and limited analyst coverage. Any decline in available funding could adversely impact our ability to originate loans, invest in securities, meet our expenses, or fulfill obligations such as repaying our borrowings or meeting deposit withdrawal demands, any of which could have a material adverse impact on our liquidity, business, results of operations and financial condition.

business, could subject us to additional cost and expense or could change the terms of the Preferred Shares to the detriment of our common shareholders. While it may be possible for us to redeem the Preferred Shares in the event that the U.S. Treasury imposes any changes or additional requirements that we believe are detrimental, there can be no assurances that our federal regulator will approve such redemption or that we will have the ability to implement such redemption, especially in light of regulatory requirements imposed upon financial institutions seeking to redeem TARP securities.

None.

The Bank’s operations are located at nine sites in Union County, New Jersey, consisting of five sites in Union Township, one in Springfield Township, one in Berkeley Heights, one in Vauxhall and one in Summit, New Jersey. The Bank also has three sites in Morris County, New Jersey, consisting of one site in Madison, one site in Boonton/Mountain Lakes, and one site in Morristown, New Jersey. The principal office is located at 2455 Morris Avenue, Union, New Jersey. The principal office is a two story building constructed in 1993. On October 9, 2004, the Bank opened a 19,555 square foot office facility on Springfield Road in Union, New Jersey, which serves as the Bank’s Operations and Data Center. On February 27, 2008, the Corporation

signed an agreement to lease premises at 105 North Avenue, Cranford, New Jersey to be used to construct a full service branch facility. Subsequently, the Corporation has notified the landlord that it wanted to terminate the commitment and completed the termination in the first quarter of 2009.

The following table sets forth certain information regarding the Bank’s leased locations.

The Bank operates a Drive In/Walk Up located at 2022 Stowe Street, Union, New Jersey, adjacent to a part of the Center Office facility. The Bank has three off-site ATM locations. Two are located at New Jersey Transit stations and one is located at the Boys and Girls Club of Union, 1050 Jeanette Avenue, Union, New Jersey.

On January 12, 2010, the Bank entered into a sale/purchase agreement for its 1180 Springfield Road facility. Under the terms of the agreement the premises will be leased with an option to buy. The agreement is expected to be fully consummated in the second quarter of 2010.

Union Center has instituted a suit against Highlands State Bank (“Highlands”) in the Superior Court of New Jersey (Docket No. MRS-C-189-09). counterclaim.

Securities Litigation Reform Act of 1995. Actual results could differ materially from this statement as a result of various factors, including the uncertainties arising in proving facts within the judicial process.

The following table sets forth the name and age of each executive officer of the Parent Corporation, the period during which each such person has served as an officer of the Parent Corporation or the Bank and each such person’s business experience (including all positions with the Parent Corporation and the Bank) for the past five years:

The common stock of the Parent Corporation is traded on the NASDAQ Global Select Market. The Corporation’s symbol is CNBC. As of December 31, 2009, the Corporation had 605 stockholders of record. This does not include beneficial owners for whom CEDE & Company or others act as nominees. On December 31, 2009, the closing low market bid and asked price were $8.92 and $9.07, respectively.

The following table sets forth the high and low bid price, and the dividends declared, on a share of the Corporation’s common stock for the years ended December 31, 2009 and 2008. All amounts are adjusted for prior stock splits and stock dividends.

| Common Stock Price | Common Dividends Declared | |||||||||||||||||||||||

| 2009 | 2008 | |||||||||||||||||||||||

| High Bid | Low Bid | High Bid | Low Bid | 2009 | 2008 | |||||||||||||||||||

| Fourth Quarter | $ | 9.20 | $ | 7.36 | $ | 10.15 | $ | 7.45 | $ | 0.0300 | $ | 0.0900 | ||||||||||||

| Third Quarter | 10.16 | 7.53 | 10.96 | 8.44 | 0.0300 | 0.0900 | ||||||||||||||||||

| Second Quarter | 9.15 | 6.88 | 10.38 | 8.45 | 0.0300 | 0.0900 | ||||||||||||||||||

| First Quarter | 8.50 | 6.43 | 11.32 | 9.95 | 0.0900 | 0.0900 | ||||||||||||||||||

| Total | $ | 0.1800 | $ | 0.3600 | ||||||||||||||||||||

Historically, repurchases have been made from time to time as, in the opinion of management, market conditions warranted, in the open market or in privately negotiated transactions. Shares repurchased were used for stock dividends and other issuances. As of December 31, 2009, Center Bancorp had 14.6 million shares of common stock outstanding. As of December 31, 2009, the Parent Corporation had purchased 1,386,863 common shares at an average cost per share of $11.44 under stock buyback programs announced in 2006, 2007 and 2008. No repurchases were made during 2009. The repurchased shares were recorded as Treasury Stock, which resulted in a decrease in stockholders’ equity.

Information concerning the stock repurchases for the three months ended December 31, 2009 is set forth below.

| Period | Total Number of Shares (or Units) Purchased | Average Price Paid per Share (or Unit) | Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs | ||||||||||||

| October 1, through October 31, 2009 | — | $ | — | 1,386,863 | 652,868 | |||||||||||

| November 1, through November 30, 2009 | — | — | 1,386,863 | 652,868 | ||||||||||||

| December 1, through December 31, 2009 | — | — | 1,386,863 | 652,868 | ||||||||||||

| Total | — | $ | — | 1,386,863 | 652,868 | |||||||||||

As noted elsewhere herein, on January 9, 2009, as part of the U.S. Department of the Treasury’s Troubled Asset Relief Program (“TARP”), the Parent Corporation entered into an agreement with the U.S. Treasury (the “Stock Purchase Agreement”) pursuant to which (i) the Parent Corporation issued and sold, and the U.S. Treasury purchased, 10,000 shares (the “Preferred Shares”) of the Company’s Fixed Rate Cumulative Perpetual Preferred Stock, Series A, having a liquidation preference of $1,000 per share for an aggregate purchase price of $10 million in cash, and (ii) the Parent Corporation issued to the U.S. Treasury a ten-year warrant (the “Warrant”) to purchase up to 173,410 shares of the Parent Corporation’s common stock at an exercise price of $8.65 per share. As a result of the successful completion of the Rights Offering in October 2009, the number of shares underlying the warrant held by the U.S. Treasury was reduced to 86,705 shares or 50 percent of the original 173,410 shares. Until the third anniversary of the issuance of the Preferred Shares, the consent of the U.S. Treasury will be required for any increase in the dividends on the Parent Corporation’s common stock or for any stock repurchases unless the Preferred Shares have been redeemed in their entirety or the U.S. Treasury has transferred the Preferred Shares to third parties. See “Dividends” below for additional restrictions on the payment of dividends.

Federal laws and regulations contain restrictions on the ability of the Parent Corporation and Union Center National Bank to pay dividends. For information regarding restrictions on dividends, see Part I, Item 1, “Business — Dividend Limitations” and Part II, Item 8, “Financial Statements and Supplementary Data — Dividend Restrictions, Note 17 of the Notes to Consolidated Financial Statements.” Pursuant to the MOU between Union Center National Bank and the OCC, the Bank may not declare dividends without the prior approval of the OCC. In addition, under the terms of the trust preferred securities issued by Center Bancorp, Inc. Statutory Trust II, the Parent Corporation can not pay dividends on its common stock if the Corporation defers payments on the junior subordinated debentures which provide the cash flow for the payments on the trust preferred securities. Further, pursuant to the Stock Purchase Agreement, the Parent Corporation is unable to declare dividend payments on the Parent Corporation’s common stock (and certain preferred stock if the Parent Corporation issues additional series of preferred stock) if the Parent Corporation is in arrears in the payment of dividends on the Preferred Shares issued to the U.S. Treasury. Further, until the third anniversary of the U.S. Treasury’s investment or when all of the Preferred Shares have been redeemed or transferred, the Parent Corporation is not permitted to increase the amount of the quarterly cash dividend above $0.09 per share, which was the amount of the last regular dividend declared by the Parent Corporation prior to October 14, 2008.

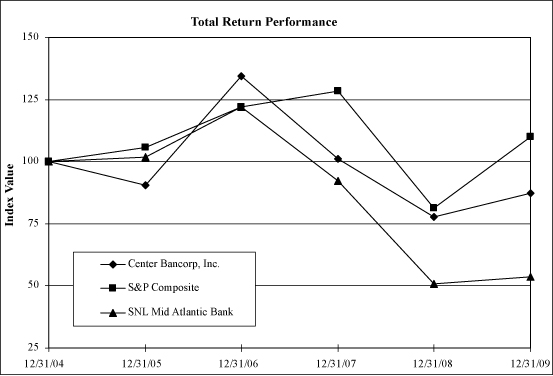

Set forth below is a line graph presentation comparing the cumulative stockholder return on the Parent Corporation’s common stock, on a dividend reinvested basis, against the cumulative total returns of the Standard & Poor’s Composite and the SNL Mid-Atlantic Bank Index for the period from January 1, 2005 through December 31, 2009.

| Fiscal Year Ending | ||||||||||||||||||||||||

| Company/Index/Market | 12/31/2004 | 12/31/2005 | 12/31/2006 | 12/31/2007 | 12/31/2008 | 12/31/2009 | ||||||||||||||||||

| Center Bancorp, Inc. | 100.0 | 90.5 | 134.3 | 101.1 | 77.6 | 87.3 | ||||||||||||||||||

| S&P Composite | 100.0 | 105.7 | 121.9 | 128.5 | 81.3 | 109.8 | ||||||||||||||||||

| SNL Mid-Atlantic Bank Index | 100.0 | 101.8 | 122.1 | 92.4 | 50.9 | 53.6 | ||||||||||||||||||

| Years Ended December 31, | ||||||||||||||||||||

| 2009 | 2008 | 2007 | 2006 | 2005(3) | ||||||||||||||||

| (Dollars in Thousands, Except per Share Data) | ||||||||||||||||||||

| Summary of Income | ||||||||||||||||||||

| Interest income | $ | 51,110 | $ | 49,894 | $ | 52,129 | $ | 53,325 | $ | 50,503 | ||||||||||

| Interest expense | 22,645 | 24,095 | 30,630 | 28,974 | 23,296 | |||||||||||||||

| Net interest income | 28,465 | 25,799 | 21,499 | 24,351 | 27,207 | |||||||||||||||

| Provision for loan losses | 3,261 | 1,561 | 350 | 57 | — | |||||||||||||||

| Net interest income after provision for loan losses | 25,204 | 24,238 | 21,149 | 24,294 | 27,207 | |||||||||||||||

| Other income | 3,906 | 2,644 | 4,372 | 633 | 3,836 | |||||||||||||||

| Other expense | 23,057 | 19,473 | 24,598 | 24,358 | 22,213 | |||||||||||||||

| Income before income tax expense | 6,053 | 7,409 | 923 | 569 | 8,830 | |||||||||||||||

| Income tax expense (benefit) | 1,480 | 1,567 | (2,933 | ) | (3,329 | ) | 1,184 | |||||||||||||

| Net income | $ | 4,573 | $ | 5,842 | $ | 3,856 | $ | 3,898 | $ | 7,646 | ||||||||||

| Net income available to common stockholders | $ | 4,006 | $ | 5,842 | $ | 3,856 | $ | 3,898 | $ | 7,646 | ||||||||||

| Statement of Financial Condition Data | ||||||||||||||||||||

| Investments | $ | 298,124 | $ | 242,714 | $ | 314,194 | $ | 381,733 | $ | 517,730 | ||||||||||

| Total loans | 715,453 | 676,203 | 551,669 | 550,414 | 505,826 | |||||||||||||||

| Goodwill and other intangibles | 17,028 | 17,110 | 17,204 | 17,312 | 17,437 | |||||||||||||||

| Total assets | 1,196,824 | 1,023,293 | 1,017,645 | 1,051,384 | 1,114,829 | |||||||||||||||

| Deposits | 813,705 | 659,537 | 699,070 | 726,771 | 700,601 | |||||||||||||||

| Borrowings | 269,253 | 268,440 | 218,109 | 206,434 | 293,963 | |||||||||||||||

| Stockholders’ equity | 102,551 | 81,713 | 85,278 | 97,613 | 99,489 | |||||||||||||||

| Dividends | ||||||||||||||||||||

| Cash dividends | $ | 2,434 | $ | 4,675 | $ | 4,885 | $ | 4,808 | $ | 4,518 | ||||||||||

| Dividend payout ratio | 60.76 | % | 80.02 | % | 126.69 | % | 123.35 | % | 59.09 | % | ||||||||||

| Cash Dividends Per Share(1) | ||||||||||||||||||||

| Cash dividends | $ | 0.18 | $ | 0.36 | $ | 0.36 | $ | 0.34 | $ | 0.34 | ||||||||||

| Earnings Per Share(1) | ||||||||||||||||||||

| Basic | $ | 0.30 | $ | 0.45 | $ | 0.28 | $ | 0.28 | $ | 0.60 | ||||||||||

| Diluted | $ | 0.30 | $ | 0.45 | $ | 0.28 | $ | 0.28 | $ | 0.60 | ||||||||||

| Weighted Average Common Shares Outstanding(1) | ||||||||||||||||||||

| Basic | 13,382,614 | 13,048,518 | 13,780,504 | 13,959,684 | 12,678,614 | |||||||||||||||

| Diluted | 13,385,416 | 13,061,410 | 13,840,756 | 14,040,338 | 12,725,256 | |||||||||||||||

| Operating Ratios | ||||||||||||||||||||

| Return on average assets | 0.37 | % | 0.58 | % | 0.38 | % | 0.37 | % | 0.69 | % | ||||||||||

| Average stockholders’ equity to average assets | 7.67 | % | 8.28 | % | 9.33 | % | 9.21 | % | 7.79 | % | ||||||||||

| Return on average stockholders’ equity | 4.87 | % | 7.03 | % | 4.09 | % | 4.04 | % | 8.91 | % | ||||||||||

| Return on average tangible stockholders’ equity(2) | 5.96 | % | 8.86 | % | 5.00 | % | 4.93 | % | 10.34 | % | ||||||||||

| Book Value | ||||||||||||||||||||

| Book value per common share(1) | $ | 6.38 | $ | 6.29 | $ | 6.48 | $ | 7.02 | $ | 7.05 | ||||||||||

| Tangible book value per common share(1)(2) | $ | 5.21 | $ | 4.97 | $ | 5.17 | $ | 5.77 | $ | 5.82 | ||||||||||

| Non-Financial Information | ||||||||||||||||||||

| Common stockholders of record | 605 | 640 | 679 | 717 | 767 | |||||||||||||||

| Full-time equivalent staff | 160 | 160 | 172 | 214 | 202 | |||||||||||||||

| Years Ended December 31, | ||||||||||||||||||||

2009 (Restated) | 2008 | 2007 | 2006 | 2005 (3) | ||||||||||||||||

| (Dollars in Thousands, Except per Share Data) | ||||||||||||||||||||

| Summary of Income | ||||||||||||||||||||

| Interest income | $ | 51,110 | $ | 49,894 | $ | 52,129 | $ | 53,325 | $ | 50,503 | ||||||||||

| Interest expense | 22,645 | 24,095 | 30,630 | 28,974 | 23,296 | |||||||||||||||

| Net interest income | 28,465 | 25,799 | 21,499 | 24,351 | 27,207 | |||||||||||||||

| Provision for loan losses | 4,597 | 1,561 | 350 | 57 | — | |||||||||||||||

| Net interest income after provision for loan losses | 23,868 | 24,238 | 21,149 | 24,294 | 27,207 | |||||||||||||||

| Other income | 3,906 | 2,644 | 4,372 | 633 | 3,836 | |||||||||||||||

| Other expense | 23,057 | 19,473 | 24,598 | 24,358 | 22,213 | |||||||||||||||

| Income before income tax expense | 4,717 | 7,409 | 923 | 569 | 8,830 | |||||||||||||||

| Income tax expense (benefit) | 946 | 1,567 | (2,933 | ) | (3,329 | ) | 1,184 | |||||||||||||

| Net income | $ | 3,771 | $ | 5,842 | $ | 3,856 | $ | 3,898 | $ | 7,646 | ||||||||||

| Net income available to common stockholders | $ | 3,204 | $ | 5,842 | $ | 3,856 | $ | 3,898 | $ | 7,646 | ||||||||||

| Statement of Financial Condition Data | ||||||||||||||||||||

| Investments | $ | 298,124 | $ | 242,714 | $ | 314,194 | $ | 381,733 | $ | 517,730 | ||||||||||

| Total loans | 719,606 | 676,203 | 551,669 | 550,414 | 505,826 | |||||||||||||||

| Goodwill and other intangibles | 17,028 | 17,110 | 17,204 | 17,312 | 17,437 | |||||||||||||||

| Total assets | 1,195,488 | 1,023,293 | 1,017,645 | 1,051,384 | 1,114,829 | |||||||||||||||

| Deposits | 813,705 | 659,537 | 699,070 | 726,771 | 700,601 | |||||||||||||||

| Borrowings | 269,253 | 268,440 | 218,109 | 206,434 | 293,963 | |||||||||||||||

| Stockholders’ equity | 101,749 | 81,713 | 85,278 | 97,613 | 99,489 | |||||||||||||||

| Dividends | ||||||||||||||||||||

| Cash dividends | $ | 2,434 | $ | 4,675 | $ | 4,885 | $ | 4,808 | $ | 4,518 | ||||||||||

| Dividend payout ratio | 75.97 | % | 80.02 | % | 126.69 | % | 123.35 | % | 59.09 | % | ||||||||||

Cash Dividends Per Share (1) | ||||||||||||||||||||

| Cash dividends | $ | 0.18 | $ | 0.36 | $ | 0.36 | $ | 0.34 | $ | 0.34 | ||||||||||

Earnings Per Share (1) | ||||||||||||||||||||

| Basic | $ | 0.24 | $ | 0.45 | $ | 0.28 | $ | 0.28 | $ | 0.60 | ||||||||||

| Diluted | $ | 0.24 | $ | 0.45 | $ | 0.28 | $ | 0.28 | $ | 0.60 | ||||||||||

Weighted Average Common Shares Outstanding (1) | ||||||||||||||||||||

| Basic | 13,382,614 | 13,048,518 | 13,780,504 | 13,959,684 | 12,678,614 | |||||||||||||||

| Diluted | 13,385,416 | 13,061,410 | 13,840,756 | 14,040,338 | 12,725,256 | |||||||||||||||

| Operating Ratios | ||||||||||||||||||||

| Return on average assets | 0.31 | % | 0.58 | % | 0.38 | % | 0.37 | % | 0.69 | % | ||||||||||

| Average stockholders’ equity to average assets | 7.66 | % | 8.28 | % | 9.33 | % | 9.21 | % | 7.79 | % | ||||||||||

| Return on average stockholders’ equity | 4.02 | % | 7.03 | % | 4.09 | % | 4.04 | % | 8.91 | % | ||||||||||

Return on average tangible stockholders’ equity (2) | 4.91 | % | 8.86 | % | 5.00 | % | 4.93 | % | 10.34 | % | ||||||||||

| Book Value | ||||||||||||||||||||

Book value per common share (1) | $ | 6.32 | $ | 6.29 | $ | 6.48 | $ | 7.02 | $ | 7.05 | ||||||||||

Tangible book value per common share (1) (2) | $ | 5.15 | $ | 4.97 | $ | 5.17 | $ | 5.77 | $ | 5.82 | ||||||||||

| Non-Financial Information | ||||||||||||||||||||

| Common stockholders of record | 605 | 640 | 679 | 717 | 767 | |||||||||||||||

| Full-time equivalent staff | 160 | 160 | 172 | 214 | 202 | |||||||||||||||

| (1) | All common share and per common share amounts have been adjusted for prior stock splits and stock dividends. |

| (2) | Tangible book value per common share, which is a non-GAAP financial measure, is computed by dividing stockholders’ equity less preferred stock, goodwill and other intangible assets by common shares outstanding. The following table provides certain related reconciliations between Generally Accepted Accounting Principles (“GAAP”)measures (stockholders’ equity and book value per common share) and the related non-GAAP financial measures (tangible stockholders’ equity and tangible book value per common share): |

| 2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||

| (Dollars in Thousands, Except per Share Data) | ||||||||||||||||||||

| Common shares outstanding | 14,572,029 | 12,991,312 | 13,155,784 | 13,910,450 | 14,103,209 | |||||||||||||||

| Stockholders’ equity | $ | 102,551 | $ | 81,713 | $ | 85,278 | $ | 97,613 | $ | 99,489 | ||||||||||

| Less: Preferred Stock | 9,619 | — | — | — | — | |||||||||||||||

| Less: Goodwill and other intangible assets | 17,028 | 17,110 | 17,204 | 17,312 | 17,437 | |||||||||||||||

| Tangible Stockholders’ Equity | $ | 75,904 | $ | 64,603 | $ | 68,074 | $ | 80,301 | $ | 82,052 | ||||||||||

| Book value per common share | $ | 6.38 | $ | 6.29 | $ | 6.48 | $ | 7.02 | $ | 7.05 | ||||||||||

| Less: Goodwill and other intangible assets | 1.17 | 1.32 | 1.31 | 1.25 | 1.23 | |||||||||||||||

| Tangible Book Value per Common Share | $ | 5.21 | $ | 4.97 | $ | 5.17 | $ | 5.77 | $ | 5.82 | ||||||||||

| Years Ended December 31, | ||||||||||||||||||||

2009 (Restated) | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||

| (Dollars in Thousands, Except per Share Data) | ||||||||||||||||||||

| Common shares outstanding | 14,572,029 | 12,991,312 | 13,155,784 | 13,910,450 | 14,103,209 | |||||||||||||||

| Stockholders’ equity | $ | 101,749 | $ | 81,713 | $ | 85,278 | $ | 97,613 | $ | 99,489 | ||||||||||

| Less: Preferred Stock | 9,619 | — | — | — | — | |||||||||||||||

| Less: Goodwill and other intangible assets | 17,028 | 17,110 | 17,204 | 17,312 | 17,437 | |||||||||||||||

| Tangible Stockholders’ Equity | $ | 75,102 | $ | 64,603 | $ | 68,074 | $ | 80,301 | $ | 82,052 | ||||||||||

| Book value per common share | $ | 6.32 | $ | 6.29 | $ | 6.48 | $ | 7.02 | $ | 7.05 | ||||||||||

| Less: Goodwill and other intangible assets | 1.17 | 1.32 | 1.31 | 1.25 | 1.23 | |||||||||||||||

| Tangible Book Value per Common Share | $ | 5.15 | $ | 4.97 | $ | 5.17 | $ | 5.77 | $ | 5.82 | ||||||||||

| 2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||

| (Dollars in Thousands) | ||||||||||||||||||||

| Net income | $ | 4,573 | $ | 5,842 | $ | 3,856 | $ | 3,898 | $ | 7,646 | ||||||||||

| Average stockholders’ equity | $ | 93,853 | $ | 83,123 | $ | 94,345 | $ | 96,505 | $ | 85,772 | ||||||||||

| Less: Average goodwill and other intangible assets | 17,069 | 17,158 | 17,259 | 17,378 | 11,814 | |||||||||||||||

| Average Tangible Stockholders’ Equity | $ | 76,784 | $ | 65,965 | $ | 77,086 | $ | 79,127 | $ | 73,958 | ||||||||||

| Return on average stockholders’ equity | 4.87 | % | 7.03 | % | 4.09 | % | 4.04 | % | 8.91 | % | ||||||||||

| Add: Average goodwill and other intangible assets | 1.09 | 1.83 | 0.91 | 0.89 | 1.43 | |||||||||||||||

| Return on Average Tangible Stockholders’ Equity | 5.96 | % | 8.86 | % | 5.00 | % | 4.93 | % | 10.34 | % | ||||||||||

| Years Ended December, 31 | ||||||||||||||||||||

2009 (Restated) | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||

| (Dollars in Thousands) | ||||||||||||||||||||

| Net income | $ | 3,771 | $ | 5,842 | $ | 3,856 | $ | 3,898 | $ | 7,646 | ||||||||||

| Average stockholders’ equity | $ | 93,850 | $ | 83,123 | $ | 94,345 | $ | 96,505 | $ | 85,772 | ||||||||||

| Less: Average goodwill and other intangible assets | 17,069 | 17,158 | 17,259 | 17,378 | 11,814 | |||||||||||||||

| Average Tangible Stockholders’ Equity | $ | 76,781 | $ | 65,965 | $ | 77,086 | $ | 79,127 | $ | 73,958 | ||||||||||

| Return on average stockholders’ equity | 4.02 | % | 7.03 | % | 4.09 | % | 4.04 | % | 8.91 | % | ||||||||||

| Add: Average goodwill and other intangible assets | 0.89 | 1.83 | 0.91 | 0.89 | 1.43 | |||||||||||||||

| Return on Average Tangible Stockholders’ Equity | 4.91 | % | 8.86 | % | 5.00 | % | 4.93 | % | 10.34 | % | ||||||||||

| (3) | The Corporation completed the acquisition of Red Oak Bank as of the close of business on May 20, 2005. The acquisition was accounted for as a purchase and the excess cost over the fair value of net assets acquired (“goodwill”) in the transaction was $14.7 million. The Corporation also recorded a core deposit intangible of $702,617 in connection with the acquisition. |

| 2009 | 2008 | 2007 | ||||||||||||||||||||||||||||||||||

| Amount | Increase (Decrease) from Prior Year | Percent Change | Amount | Increase (Decrease) from Prior Year | Percent Change | Amount | Increase (Decrease) from Prior Year | Percent Change | ||||||||||||||||||||||||||||

| (Dollars in Thousands) | ||||||||||||||||||||||||||||||||||||

| Interest income: | ||||||||||||||||||||||||||||||||||||

| Investments | $ | 14,226 | $ | (179 | ) | (1.24 | ) | $ | 14,405 | $ | (4,850 | ) | (25.19 | ) | $ | 19,255 | $ | (3,215 | ) | (14.31 | ) | |||||||||||||||

| Loans, including fees | 36,751 | 641 | 1.78 | 36,110 | 2,583 | 7.70 | 33,527 | 1,528 | 4.78 | |||||||||||||||||||||||||||

| Federal funds sold and securities purchased under agreements to resell | 0 | (113 | ) | (100.00 | ) | 113 | (491 | ) | (81.29 | ) | 604 | 57 | 10.42 | |||||||||||||||||||||||

| Restricted investment in bank stocks | 643 | 49 | 8.25 | 594 | 45 | 8.20 | 549 | 42 | 8.28 | |||||||||||||||||||||||||||

| Total interest income | 51,620 | 398 | 0.78 | 51,222 | (2,713 | ) | (5.03 | ) | 53,935 | (1,588 | ) | (2.86 | ) | |||||||||||||||||||||||

| Interest expense: | ||||||||||||||||||||||||||||||||||||

| Deposits | 12,308 | (979 | ) | (7.37 | ) | 13,287 | (7,548 | ) | (36.23 | ) | 20,835 | 2,830 | 15.72 | |||||||||||||||||||||||

| Borrowings | 10,337 | (471 | ) | (4.36 | ) | 10,808 | 1,013 | 10.34 | 9,795 | (1,174 | ) | (10.70 | ) | |||||||||||||||||||||||

| Total interest expense | 22,645 | (1,450 | ) | (6.02 | ) | 24,095 | (6,535 | ) | (21.34 | ) | 30,630 | 1,656 | 5.72 | |||||||||||||||||||||||

| Net interest income on a fully tax-equivalent basis | 28,975 | 1,848 | 6.81 | 27,127 | 3,822 | 16.40 | 23,305 | (3,244 | ) | (12.22 | ) | |||||||||||||||||||||||||

| Tax-equivalent adjustment | (510 | ) | 818 | (61.60 | ) | (1,328 | ) | 478 | (26.47 | ) | (1,806 | ) | 392 | (17.83 | ) | |||||||||||||||||||||

| Net interest income | $ | 28,465 | $ | 2,666 | 10.33 | $ | 25,799 | $ | 4,300 | 20.00 | $ | 21,499 | $ | (2,852 | ) | (11.71 | ) | |||||||||||||||||||

| 2009 | 2008 | 2007 | |||||||||||||||||||||||||||||||||

| Amount | Increase (Decrease) from Prior Year | Percentage Change | Amount | Increase (Decrease) from Prior Year | Percentage Change | Amount | Increase (Decrease) from Prior Year | Percentage Change | |||||||||||||||||||||||||||

| (Dollars in Thousands) | |||||||||||||||||||||||||||||||||||

| Interest income: | |||||||||||||||||||||||||||||||||||

| Investments | $ | 14,226 | $ | (179 | ) | (1.24 | ) | $ | 14,405 | $ | (4,850 | ) | (25.19 | ) | $ | 19,255 | $ | (3,215 | ) | (14.31 | ) | ||||||||||||||

| Loans, including fees | 36,751 | 641 | 1.78 | 36,110 | 2,583 | 7.70 | 33,527 | 1,528 | 4.78 | ||||||||||||||||||||||||||

| Federal funds sold and securities purchased under agreements to resell | 0 | (113 | ) | (100.00 | ) | 113 | (491 | ) | (81.29 | ) | 604 | 57 | 10.42 | ||||||||||||||||||||||

| Restricted investment in bank stocks | 643 | 49 | 8.25 | 594 | 45 | 8.20 | 549 | 42 | 8.28 | ||||||||||||||||||||||||||

| Total interest income | 51,620 | 398 | 0.78 | 51,222 | (2,713 | ) | (5.03 | ) | 53,935 | (1,588 | ) | (2.86 | ) | ||||||||||||||||||||||

| Interest expense: | |||||||||||||||||||||||||||||||||||

| Deposits | 12,308 | (979 | ) | (7.37 | ) | 13,287 | (7,548 | ) | (36.23 | ) | 20,835 | 2,830 | 15.72 | ||||||||||||||||||||||

| Borrowings | 10,337 | (471 | ) | (4.36 | ) | 10,808 | 1,013 | 10.34 | 9,795 | (1,174 | ) | (10.70 | ) | ||||||||||||||||||||||

| Total interest expense | 22,645 | (1,450 | ) | (6.02 | ) | 24,095 | (6,535 | ) | (21.34 | ) | 30,630 | 1,656 | 5.72 | ||||||||||||||||||||||

| Net interest income on a fully tax-equivalent basis | 28,975 | 1,848 | 6.81 | 27,127 | 3,822 | 16.40 | 23,305 | (3,244 | ) | (12.22 | ) | ||||||||||||||||||||||||

| Tax-equivalent adjustment | (510 | ) | 818 | (61.60 | ) | (1,328 | ) | 478 | (26.47 | ) | (1,806 | ) | 392 | (17.83 | ) | ||||||||||||||||||||

| Net interest income | $ | 28,465 | $ | 2,666 | 10.33 | $ | 25,799 | $ | 4,300 | 20.00 | $ | 21,499 | $ | (2,852 | ) | (11.71 | ) | ||||||||||||||||||

2009/2008 Increase (Decrease) Due to Change in: | 2008/2007 Increase (Decrease) Due to Change in: | |||||||||||||||||||||||

Average Volume | Average Rate | Net Change | Average Volume | Average Rate | Net Change | |||||||||||||||||||

| (Dollars in Thousands) | ||||||||||||||||||||||||

| Interest-earning assets: | ||||||||||||||||||||||||

| Investment securities: | ||||||||||||||||||||||||

| Taxable | $ | 3,553 | $ | (1,355 | ) | $ | 2,198 | $ | (2,835 | ) | $ | (364 | ) | $ | (3,199 | ) | ||||||||

| Non-Taxable | (2,463 | ) | 86 | (2,377 | ) | (1,577 | ) | (74 | ) | (1,651 | ) | |||||||||||||

| Loans, net of unearned discount | 3,864 | (3,223 | ) | 641 | 4,807 | (2,224 | ) | 2,583 | ||||||||||||||||

| Federal funds sold and securities purchased under agreements to resell | (56 | ) | (57 | ) | (113 | ) | (294 | ) | (197 | ) | (491 | ) | ||||||||||||

| Restricted investment in bank stocks | 25 | 24 | 49 | 145 | (100 | ) | 45 | |||||||||||||||||

| Total interest-earning assets | 4,923 | (4,525 | ) | 398 | 246 | (2,959 | ) | (2,713 | ) | |||||||||||||||

| Interest-bearing liabilities: | ||||||||||||||||||||||||

| Money market deposits | (545 | ) | (1,298 | ) | (1,843 | ) | 332 | (3,431 | ) | (3,099 | ) | |||||||||||||

| Savings deposits | 1,017 | 483 | 1,500 | (53 | ) | (14 | ) | (67 | ) | |||||||||||||||

| Time deposits | 3,648 | (3,050 | ) | 598 | (410 | ) | (2,170 | ) | (2,580 | ) | ||||||||||||||

| Other interest-bearing deposits | 204 | (1,438 | ) | (1,234 | ) | (1,039 | ) | (763 | ) | (1,802 | ) | |||||||||||||

| Borrowings and subordinated debentures | (463 | ) | (8 | ) | (471 | ) | 2,654 | (1,641 | ) | 1,013 | ||||||||||||||

| Total interest-bearing liabilities | 3,861 | (5,311 | ) | (1,450 | ) | 1,484 | (8,019 | ) | (6,535 | ) | ||||||||||||||

| Change in net interest income | $ | 1,062 | $ | 786 | $ | 1,848 | $ | (1,238 | ) | $ | 5,060 | $ | 3,822 | |||||||||||

| Years Ended December 31, | ||||||||||||||||||||||||||||||||||||

| 2009 | 2008 | 2007 | ||||||||||||||||||||||||||||||||||

| (Tax-Equivalent Basis) | Average Balance | Income/ Expense | Yield/ Rate | Average Balance | Income/ Expense | Yield/ Rate | Average Balance | Income/ Expense | Yield/ Rate | |||||||||||||||||||||||||||

| (Dollars in Thousands) | ||||||||||||||||||||||||||||||||||||

| ASSETS | ||||||||||||||||||||||||||||||||||||

| Interest-earning assets: | ||||||||||||||||||||||||||||||||||||

| Investment securities:(1) | ||||||||||||||||||||||||||||||||||||

| Taxable | $ | 289,414 | $ | 12,727 | 4.40 | % | $ | 211,185 | $ | 10,529 | 4.99 | % | $ | 267,884 | $ | 13,728 | 5.12 | % | ||||||||||||||||||

| Non-taxable | 25,677 | 1,499 | 5.84 | % | 67,890 | 3,876 | 5.71 | % | 95,501 | 5,527 | 5.79 | % | ||||||||||||||||||||||||

| Loans, net of unearned income:(2) | 692,562 | 36,751 | 5.31 | % | 622,533 | 36,110 | 5.80 | % | 541,297 | 33,527 | 6.19 | % | ||||||||||||||||||||||||

| Federal funds sold and securities purchased under agreements to resell | — | — | — | 4,047 | 113 | 2.79 | % | 12,050 | 604 | 5.01 | % | |||||||||||||||||||||||||

| Restricted investment in bank stocks | 10,526 | 643 | 6.11 | % | 10,104 | 594 | 5.88 | % | 7,806 | 549 | 7.03 | % | ||||||||||||||||||||||||

| Total interest-earning assets | 1,018,179 | 51,620 | 5.07 | % | 915,759 | 51,222 | 5.59 | % | 924,538 | 53,935 | 5.83 | % | ||||||||||||||||||||||||

| Non-interest-earning assets: | ||||||||||||||||||||||||||||||||||||

| Cash and due from banks | 128,156 | 16,063 | 18,586 | |||||||||||||||||||||||||||||||||

| Bank owned life insurance | 24,941 | 22,627 | 21,801 | |||||||||||||||||||||||||||||||||

| Intangible assets | 17,069 | 17,158 | 17,259 | |||||||||||||||||||||||||||||||||

| Other assets | 42,980 | 37,602 | 34,547 | |||||||||||||||||||||||||||||||||

| Allowance for loan losses | (6,916 | ) | (5,681 | ) | (5,002 | ) | ||||||||||||||||||||||||||||||

| Total non-interest earning assets | 206,230 | 87,769 | 87,191 | |||||||||||||||||||||||||||||||||