In addition to providing

year or less.

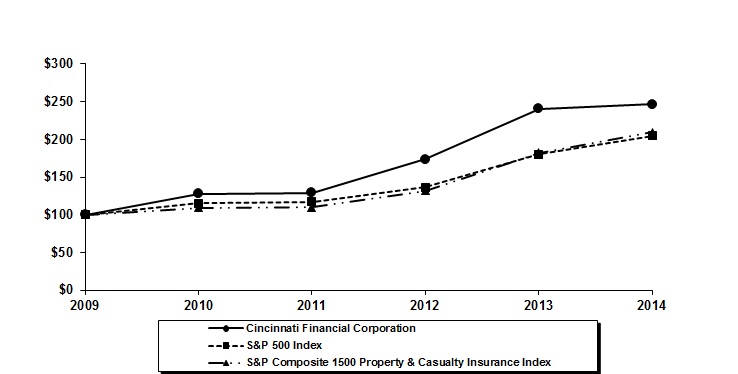

2014.

Liquidity.

| (Dollars in millions) Statutory Information | At December 31, | |||||||

| 2011 | 2010 | |||||||

| Standard market property casualty insurance subsidiary | ||||||||

| Statutory surplus | $ | 3,747 | $ | 3,777 | ||||

| Risk-based capital (RBC) | 3,754 | 3,793 | ||||||

| Authorized control level risk-based capital | 474 | 450 | ||||||

| Ratio of risk-based capital to authorized control level risk-based capital | 7.9 | 8.4 | ||||||

| Written premium to surplus ratio | 0.8 | 0.8 | ||||||

| Life insurance subsidiary | ||||||||

| Statutory surplus | $ | 281 | $ | 303 | ||||

| Risk-based capital (RBC) | 288 | 318 | ||||||

| Authorized control level risk-based capital | 36 | 35 | ||||||

| Ratio of risk-based capital to authorized control level risk-based capital | 7.9 | 9.1 | ||||||

| Total liabilities excluding separate account business | 2,454 | 2,266 | ||||||

| Life statutory risk-based adjusted surplus to liabilities ratio | 11.8 | 14.1 | ||||||

| Excess and surplus insurance subsidiary | ||||||||

| Statutory surplus | $ | 186 | $ | 172 | ||||

| Risk-based capital (RBC) | 186 | 172 | ||||||

| Authorized control level risk-based capital | 13 | 10 | ||||||

| Ratio of risk-based capital to authorized control level risk-based capital | 13.9 | 16.6 | ||||||

| Written premium to surplus ratio | 0.4 | 0.3 | ||||||

(Dollars in millions) Statutory Information | At December 31, | |||||||

| 2014 | 2013 | |||||||

| Standard market property casualty insurance subsidiary | ||||||||

| Statutory capital and surplus | $ | 4,472 | $ | 4,326 | ||||

| Risk-based capital (RBC) | 4,490 | 4,343 | ||||||

| Authorized control level risk-based capital | 563 | 534 | ||||||

| Risk-based capital to authorized control level risk-based capital ratio | 8.0 | 8.1 | ||||||

| Written premium to surplus ratio | 0.9 | 0.9 | ||||||

| Life insurance subsidiary | ||||||||

| Statutory capital and surplus | $ | 223 | $ | 247 | ||||

| Risk-based capital (RBC) | 241 | 264 | ||||||

| Authorized control level risk-based capital | 33 | 31 | ||||||

| Total liabilities excluding separate account business | 2,978 | 2,807 | ||||||

| Risk-based capital to authorized control level risk-based capital ratio | 7.3 | 8.1 | ||||||

| Life statutory risk-based adjusted surplus to liabilities ratio | 8.1 | 9.5 | ||||||

| Excess and surplus lines insurance subsidiary | ||||||||

| Statutory capital and surplus | $ | 266 | $ | 228 | ||||

| Risk-based capital (RBC) | 266 | 228 | ||||||

| Authorized control level risk-based capital | 32 | 25 | ||||||

| Risk-based capital to authorized control level risk-based capital ratio | 8.4 | 9.2 | ||||||

| Written premium to surplus ratio | 0.6 | 0.6 | ||||||

2013.

ratings and one revised its outlook to positive from stable.

| Insurer Financial Strength Ratings | ||||||||||||||||||

Rating agency | Standard market property casualty insurance subsidiary |

Life insurance subsidiary | Excess and insurance subsidiary | Date of

affirmation or | ||||||||||||||

Rating Tier | �� | Rating Tier | Rating Tier | |||||||||||||||

A. M. Best Co. | ambest.com | A+ | Superior | 2 of 16 | A | Excellent | 3 of 16 | A | Excellent | 3 of 16 | Stable outlook (12/ | |||||||

Fitch Ratings | fitchratings.com | A+ | Strong | 5 of 21 | A+ | Strong | 5 of 21 | - | - | - | Stable outlook (11/ | |||||||

Moody's Investors Service | moodys.com | A1 | Good | 5 of 21 | - | - | - | - | - | - | ||||||||

Standard & Poor's Ratings Services | spratings.com | A | Strong | 6 of 21 | A | Strong | 6 of 21 | - | - | - | ||||||||

On October 21, 2011, Moody’s Investors Service affirmed our insurance financial strength ratings that it had assigned in September 2008, changingrevising its outlook to negative. Moody's noted that its rating is supported by our strong regional franchise, solid risk-adjusted capital position, consistent reserve strength, strong financial flexibility and significant holding company liquidity. However, Moody’s expects that operating results may continue to reflect weak underwriting profitability with high weather-related losses.

On August 4, 2011, Standard & Poor’s Ratings Services affirmed our insurer financial strength ratings that it had assigned in July 2010, continuing its stable outlook.positive from stable. S&P said its rating was based onreflected our strong competitive position, which is reinforced by a loyalfavorable geographical footprint and productive agency forceextremely strong capital. With the positive outlook, it acknowledged our general underwriting improvement in recent years and a low-cost infrastructure. S&P also cited our very strong capitalizationtrack record of mitigating potential capital and high degree of financial flexibility.earnings volatility. S&P noted thatits rating could come under pressure if our strengths are partially offset by deteriorating property casualty underwriting results dueoverall operating performance or capital adequacy deteriorated significantly or upon perceived adverse changes to above-average weather-related losses and weak results in our workers’ compensation line of business.

competitive position.

Liquidity.

Consolidated Property Casualty Insurance Earned Premiums by State

| (Dollars in millions) | Earned premiums | % of total earned | Agency locations | Average premium per location | ||||||||||||

| Year ended December 31, 2011 | ||||||||||||||||

| Ohio | $ | 591 | 19.5 | % | 233 | $ | 2.5 | |||||||||

| Illinois | 250 | 8.3 | 124 | 2.0 | ||||||||||||

| Indiana | 208 | 6.9 | 107 | 1.9 | ||||||||||||

| Pennsylvania | 184 | 6.1 | 85 | 2.2 | ||||||||||||

| Georgia | 154 | 5.1 | 80 | 1.9 | ||||||||||||

| North Carolina | 149 | 4.9 | 85 | 1.8 | ||||||||||||

| Michigan | 134 | 4.4 | 118 | 1.1 | ||||||||||||

| Virginia | 123 | 4.1 | 66 | 1.9 | ||||||||||||

| Kentucky | 114 | 3.8 | 43 | 2.7 | ||||||||||||

| Wisconsin | 103 | 3.4 | 51 | 2.0 | ||||||||||||

| Year ended December 31, 2010 | ||||||||||||||||

| Ohio | $ | 599 | 20.5 | % | 224 | $ | 2.7 | |||||||||

| Illinois | 243 | 8.3 | 122 | 2.0 | ||||||||||||

| Indiana | 197 | 6.8 | 105 | 1.9 | ||||||||||||

| Pennsylvania | 176 | 6.0 | 83 | 2.1 | ||||||||||||

| Georgia | 149 | 5.1 | 77 | 1.9 | ||||||||||||

| North Carolina | 143 | 4.9 | 80 | 1.8 | ||||||||||||

| Michigan | 126 | 4.3 | 116 | 1.1 | ||||||||||||

| Virginia | 121 | 4.1 | 60 | 2.0 | ||||||||||||

| Kentucky | 106 | 3.6 | 41 | 2.6 | ||||||||||||

| Tennessee | 102 | 3.5 | 48 | 2.1 | ||||||||||||

2013. We continue efforts to geographically diversify our property casualty risks.

| (Dollars in millions) | Earned premiums | % of total earned | Agency locations | Average premium per location | ||||||

| Year ended December 31, 2014 | ||||||||||

| Ohio | $ | 715 | 17.7 | % | 246 | $ | 2.9 | |||

| Illinois | 288 | 7.1 | 136 | 2.1 | ||||||

| Indiana | 261 | 6.4 | 111 | 2.4 | ||||||

| Pennsylvania | 222 | 5.5 | 99 | 2.2 | ||||||

| Georgia | 216 | 5.3 | 95 | 2.3 | ||||||

| Michigan | 204 | 5.0 | 138 | 1.5 | ||||||

| North Carolina | 201 | 5.0 | 95 | 2.1 | ||||||

| Tennessee | 155 | 3.8 | 60 | 2.6 | ||||||

| Virginia | 146 | 3.6 | 65 | 2.2 | ||||||

| Alabama | 139 | 3.4 | 46 | 3.0 | ||||||

| (Dollars in millions) | 2014 | 2013 | 2012 | Percent of total 2014 | |||||||||||

| Segment: | |||||||||||||||

| Commercial lines insurance | $ | 2,922 | $ | 2,760 | $ | 2,459 | 66.5 | % | |||||||

| Personal lines insurance | 1,068 | 1,005 | 918 | 24.3 | |||||||||||

| Excess and surplus lines insurance | 153 | 128 | 105 | 3.5 | |||||||||||

| Life insurance | 250 | 241 | 249 | 5.7 | |||||||||||

| Total | $ | 4,393 | $ | 4,134 | $ | 3,731 | 100.0 | % | |||||||

| Business line: | |||||||||||||||

| Commercial lines insurance | |||||||||||||||

| Commercial casualty | $ | 969 | $ | 897 | $ | 793 | 22.0 | % | |||||||

| Commercial property | 776 | 673 | 573 | 17.7 | |||||||||||

| Commercial auto | 548 | 507 | 444 | 12.5 | |||||||||||

| Workers' compensation | 365 | 374 | 341 | 8.3 | |||||||||||

| Other commercial | 264 | 309 | 308 | 6.0 | |||||||||||

| Total commercial lines insurance | 2,922 | 2,760 | 2,459 | 66.5 | |||||||||||

| Personal lines insurance | |||||||||||||||

| Personal auto | 489 | 460 | 425 | 11.1 | |||||||||||

| Homeowner | 456 | 428 | 378 | 10.4 | |||||||||||

| Other personal | 123 | 117 | 115 | 2.8 | |||||||||||

| Total personal lines insurance | 1,068 | 1,005 | 918 | 24.3 | |||||||||||

| Excess and surplus lines insurance | 153 | 128 | 105 | 3.5 | |||||||||||

| Life insurance | |||||||||||||||

| Term life insurance | 138 | 129 | 124 | 3.2 | |||||||||||

| Universal life insurance | 41 | 41 | 45 | 0.9 | |||||||||||

| Other life insurance, annuity and disability income products | 71 | 71 | 80 | 1.6 | |||||||||||

| Subtotal | 250 | 241 | 249 | 5.7 | |||||||||||

| Total | $ | 4,393 | $ | 4,134 | $ | 3,731 | 100.0 | % | |||||||

The Segment.

locations.

13

In our personal lines business, we began2015. Our services include various policy administration functions routinely provided by agencies, allowing agency personnel to use predictive modeling tools for our homeowner line of business priorfocus more on marketing efforts and on providing additional service to 2010, and in late 2010 we began using similar analytics for personal auto. We believe we are successfully attracting more of our agents’ preferred business, based on the average quality of our book of business. Quality has improvedtheir clients as measured by the mix of business by insurance score. During 2012, we willneeded. We'll continue to enhance our personal lines model attributesseek other ways to improve policyholder satisfaction through identification and expand our pricing points to add more precision. This will allow us to ensure we are competitive on the most desirable business and to adapt more rapidly to changes in market conditions.

Enhanced performance management processes developed during 2011 should improve our overall effectiveness. Every associate has 2012 goals, with emphasis on alignment to corporate objectives and use of measurements to track progress and accountability. We also are developing additional talent management capabilities to further develop and improve the effectiveness of all associates.

We measure the overall success of our strategy to improve insurance profitability primarily through our GAAP combined ratio for property casualty results, which we believe can be consistently average within the range of 95 percent to 100 100 percent for any five-yearperiod. We also compare our statutory combined ratio to the industry average to gauge our progress.

In addition, we

Operations.

The

2013.

| ◦ |

| Specialty packages – Includes coverages for property, liability and business interruption tailored to meet the needs of specific industry classes such as artisan contractors, dentists, garage operators, financial institutions, metalworkers, printers, religious institutions or smaller main street businesses. Businessowners policies, which combine property, liability and business interruption coverages for small businesses, are included in specialty packages. |

| Machinery and equipment – Specialized coverage provides protection for loss or damage to boilers and machinery, including production and computer equipment and business interruption, due to sudden and accidental mechanical breakdown, steam explosion or artificially generated electrical current. |

Commercial Lines Earned Premiums by State

| (Dollars in millions) | Earned premiums | % of total earned | Agency locations | Average premium per location | ||||||||||||

| Year ended December 31, 2011 | ||||||||||||||||

| Ohio | $ | 341 | 15.5 | % | 232 | $ | 1.5 | |||||||||

| Illinois | 189 | 8.6 | 123 | 1.5 | ||||||||||||

| Pennsylvania | 163 | 7.4 | 85 | 1.9 | ||||||||||||

| Indiana | 138 | 6.3 | 106 | 1.3 | ||||||||||||

| North Carolina | 118 | 5.4 | 82 | 1.4 | ||||||||||||

| Virginia | 101 | 4.6 | 66 | 1.5 | ||||||||||||

| Michigan | 99 | 4.5 | 115 | 0.9 | ||||||||||||

| Georgia | 83 | 3.8 | 75 | 1.1 | ||||||||||||

| Wisconsin | 82 | 3.7 | 51 | 1.6 | ||||||||||||

| Tennessee | 77 | 3.5 | 50 | 1.5 | ||||||||||||

| Year ended December 31, 2010 | ||||||||||||||||

| Ohio | $ | 347 | 16.1 | % | 223 | $ | 1.6 | |||||||||

| Illinois | 187 | 8.7 | 120 | 1.6 | ||||||||||||

| Pennsylvania | 157 | 7.3 | 83 | 1.9 | ||||||||||||

| Indiana | 133 | 6.2 | 104 | 1.3 | ||||||||||||

| North Carolina | 120 | 5.6 | 78 | 1.5 | ||||||||||||

| Virginia | 100 | 4.6 | 60 | 1.7 | ||||||||||||

| Michigan | 96 | 4.5 | 115 | 0.8 | ||||||||||||

| Georgia | 82 | 3.8 | 75 | 1.1 | ||||||||||||

| Wisconsin | 81 | 3.8 | 48 | 1.7 | ||||||||||||

| Tennessee | 79 | 3.7 | 48 | 1.6 | ||||||||||||

2013.

| (Dollars in millions) | Earned premiums | % of total earned | Agency locations | Average premium per location | ||||||

| Year ended December 31, 2014 | ||||||||||

| Ohio | $ | 413 | 14.5 | % | 243 | $ | 1.7 | |||

| Illinois | 209 | 7.3 | 136 | 1.5 | ||||||

| Pennsylvania | 191 | 6.7 | 99 | 1.9 | ||||||

| Indiana | 172 | 6.0 | 109 | 1.6 | ||||||

| North Carolina | 141 | 4.9 | 93 | 1.5 | ||||||

| Michigan | 133 | 4.7 | 134 | 1.0 | ||||||

| Georgia | 122 | 4.3 | 89 | 1.4 | ||||||

| Virginia | 118 | 4.1 | 64 | 1.8 | ||||||

| Tennessee | 111 | 3.9 | 59 | 1.9 | ||||||

| Wisconsin | 105 | 3.7 | 60 | 1.8 | ||||||

Staying abreast of

2013.

Personal Lines Earned Premiums by State

| (Dollars in millions) | Earned premiums | % of total earned | Agency locations | Average premium per location | ||||||||||||

| Year ended December 31, 2011 | ||||||||||||||||

| Ohio | $ | 242 | 31.7 | % | 207 | $ | 1.2 | |||||||||

| Georgia | 66 | 8.6 | 71 | 0.9 | ||||||||||||

| Indiana | 64 | 8.4 | 85 | 0.8 | ||||||||||||

| Illinois | 56 | 7.4 | 90 | 0.6 | ||||||||||||

| Kentucky | 44 | 5.7 | 38 | 1.2 | ||||||||||||

| Alabama | 42 | 5.5 | 41 | 1.0 | ||||||||||||

| Michigan | 32 | 4.2 | 97 | 0.3 | ||||||||||||

| North Carolina | 28 | 3.7 | 77 | 0.4 | ||||||||||||

| Tennessee | 22 | 2.8 | 45 | 0.5 | ||||||||||||

| Virginia | 20 | 2.7 | 47 | 0.4 | ||||||||||||

| Year ended December 31, 2010 | ||||||||||||||||

| Ohio | $ | 246 | 34.1 | % | 199 | $ | 1.2 | |||||||||

| Georgia | 63 | 8.8 | 69 | 0.9 | ||||||||||||

| Indiana | 59 | 8.2 | 82 | 0.7 | ||||||||||||

| Illinois | 52 | 7.2 | 86 | 0.6 | ||||||||||||

| Alabama | 42 | 5.9 | 38 | 1.1 | ||||||||||||

| Kentucky | 40 | 5.5 | 37 | 1.1 | ||||||||||||

| Michigan | 28 | 3.8 | 90 | 0.3 | ||||||||||||

| Tennessee | 22 | 3.1 | 43 | 0.5 | ||||||||||||

| North Carolina | 20 | 2.8 | 67 | 0.3 | ||||||||||||

| Virginia | 20 | 2.8 | 38 | 0.5 | ||||||||||||

| (Dollars in millions) | Earned premiums | % of total earned | Agency locations | Average premium per location | ||||||

| Year ended December 31, 2014 | ||||||||||

| Ohio | $ | 288 | 27.6 | % | 219 | $ | 1.3 | |||

| Georgia | 84 | 8.1 | 84 | 1.0 | ||||||

| Indiana | 77 | 7.4 | 90 | 0.9 | ||||||

| Illinois | 69 | 6.6 | 97 | 0.7 | ||||||

| Michigan | 65 | 6.2 | 114 | 0.6 | ||||||

| Alabama | 56 | 5.4 | 44 | 1.3 | ||||||

| North Carolina | 55 | 5.3 | 82 | 0.7 | ||||||

| Kentucky | 52 | 5.0 | 38 | 1.4 | ||||||

| Tennessee | 41 | 3.9 | 53 | 0.8 | ||||||

| Minnesota | 37 | 3.6 | 54 | 0.7 | ||||||

2013.

Excess and Surplus Lines Earned Premiums by State

| (Dollars in millions) | Earned premiums | % of total earned | ||||||

| Year ended December 31, 2011 | ||||||||

| Ohio | $ | 9 | 12.4 | % | ||||

| Indiana | 7 | 9.7 | ||||||

| Illinois | 5 | 6.8 | ||||||

| Georgia | 5 | 6.6 | ||||||

| Texas | 4 | 6.3 | ||||||

| Missouri | 4 | 5.4 | ||||||

| Pennsylvania | 3 | 4.2 | ||||||

| Michigan | 3 | 4.0 | ||||||

| Kentucky | 3 | 3.7 | ||||||

| North Carolina | 3 | 3.7 | ||||||

| Year ended December 31, 2010 | ||||||||

| Ohio | $ | 7 | 13.2 | % | ||||

| Indiana | 5 | 11.0 | ||||||

| Illinois | 4 | 8.3 | ||||||

| Georgia | 4 | 7.3 | ||||||

| Missouri | 2 | 4.7 | ||||||

| Michigan | 2 | 4.7 | ||||||

| Pennsylvania | 2 | 4.2 | ||||||

| North Carolina | 2 | 4.1 | ||||||

| Texas | 2 | 3.9 | ||||||

| Kentucky | 2 | 3.7 | ||||||

| (Dollars in millions) | Earned premiums | % of total earned | |||

| Year ended December 31, 2014 | |||||

| Ohio | $ | 14 | 9.5 | % | |

| Texas | 13 | 8.7 | |||

| Indiana | 11 | 7.5 | |||

| Illinois | 10 | 6.8 | |||

| Georgia | 10 | 6.6 | |||

| Alabama | 8 | 5.2 | |||

| Missouri | 7 | 4.6 | |||

| Michigan | 6 | 4.1 | |||

| North Carolina | 6 | 4.0 | |||

| Pennsylvania | 5 | 3.5 | |||

2013.

Cincinnati Life seeks to become the

| (Dollars in millions) | Premiums | % of total earned | |||

| Year ended December 31, 2014 | |||||

| Ohio | $ | 48 | 18.6 | % | |

| Pennsylvania | 19 | 7.2 | |||

| Indiana | 17 | 6.5 | |||

| Illinois | 16 | 6.4 | |||

| Georgia | 13 | 5.1 | |||

a general decline in interest rates.

| (Dollars in millions) | At December 31, 2014 | At December 31, 2013 | |||||||||||||||||||||

| Cost or amortized cost | Percent of total | Percent of total | Cost or amortized cost | Percent of total | Percent of total | ||||||||||||||||||

| Fair value | Fair value | ||||||||||||||||||||||

| Taxable fixed maturities | $ | 5,882 | 50.7 | % | $ | 6,330 | 44.2 | % | $ | 5,814 | 52.1 | % | $ | 6,211 | 46.0 | % | |||||||

| Tax-exempt fixed maturities | 2,989 | 25.8 | 3,130 | 21.9 | % | 2,824 | 25.3 | 2,910 | 21.6 | ||||||||||||||

| Common equity securities | 2,583 | 22.3 | 4,679 | 32.7 | % | 2,396 | 21.5 | 4,213 | 31.2 | ||||||||||||||

Nonredeemable preferred equity securities | 145 | 1.2 | 179 | 1.2 | % | 127 | 1.1 | 162 | 1.2 | ||||||||||||||

| Total | $ | 11,599 | 100.0 | % | $ | 14,318 | 100.0 | % | $ | 11,161 | 100.0 | % | $ | 13,496 | 100.0 | % | |||||||

| At December 31, 2011 | At December 31, 2010 | |||||||||||||||||||||||||||||||

| Cost or | Percent | Percent | Cost or | Percent | Percent | |||||||||||||||||||||||||||

| (In millions) | amortized cost | of total | Fair value | of total | amortized cost | of total | Fair value | of total | ||||||||||||||||||||||||

| Taxable fixed maturities | $ | 5,369 | 52.4 | % | $ | 5,847 | 49.8 | % | $ | 5,139 | 50.5 | % | $ | 5,533 | 48.4 | % | ||||||||||||||||

| Tax-exempt fixed maturities | 2,715 | 26.5 | 2,932 | 25.0 | 2,749 | 27.0 | 2,850 | 25.0 | ||||||||||||||||||||||||

| Common equities | 2,088 | 20.4 | 2,854 | 24.3 | 2,211 | 21.7 | 2,940 | 25.7 | ||||||||||||||||||||||||

| Preferred equities | 74 | 0.7 | 102 | 0.9 | 75 | 0.8 | 101 | 0.9 | ||||||||||||||||||||||||

| Total | $ | 10,246 | 100.0 | % | $ | 11,735 | 100.0 | % | $ | 10,174 | 100.0 | % | $ | 11,424 | 100.0 | % | ||||||||||||||||

assets to total assets.

rates.

| At December 31, 2011 | At December 31, 2010 | |||||||||||||||

| Fair | Percent | Fair | Percent | |||||||||||||

| (In millions) | value | of total | value | of total | ||||||||||||

| Moody's Ratings and Standard & Poor's Ratings combined: | ||||||||||||||||

| Aaa, Aa, A, AAA, AA, A | $ | 5,507 | 62.7 | % | $ | 5,216 | 62.2 | % | ||||||||

| Baa, BBB | 2,842 | 32.4 | 2,656 | 31.7 | ||||||||||||

| Ba, BB | 195 | 2.2 | 241 | 2.9 | ||||||||||||

| B, B | 33 | 0.4 | 42 | 0.5 | ||||||||||||

| Caa, CCC | 5 | 0.1 | 19 | 0.2 | ||||||||||||

| Ca, CC | 0 | 0.0 | 0 | 0.0 | ||||||||||||

| Daa, Da, D | 2 | 0.0 | 1 | 0.0 | ||||||||||||

| Non-rated | 195 | 2.2 | 208 | 2.5 | ||||||||||||

| Total | $ | 8,779 | 100.0 | % | $ | 8,383 | 100.0 | % | ||||||||

Our

| (Dollars in millions) | At December 31, 2014 | At December 31, 2013 | |||||||||||

| Fair value | Percent of total | Fair value | Percent of total | ||||||||||

| Combined ratings from Moody's and Standard & Poor's: | |||||||||||||

| Aaa, Aa, A, AAA, AA, A | $ | 5,686 | 60.1 | % | $ | 5,468 | 59.9 | % | |||||

| Baa, BBB | 3,198 | 33.8 | 3,197 | 35.1 | |||||||||

| Ba, BB | 305 | 3.2 | 231 | 2.5 | |||||||||

| B, B | 15 | 0.2 | 16 | 0.2 | |||||||||

| Caa, CCC | 3 | 0.0 | 4 | 0.0 | |||||||||

| Nonrated | 253 | 2.7 | 205 | 2.3 | |||||||||

| Total | $ | 9,460 | 100.0 | % | $ | 9,121 | 100.0 | % | |||||

| At December 31, | ||||||

| 2014 | 2013 | |||||

| Weighted average yield-to-amortized cost | 4.76 | % | 4.86 | % | ||

| Weighted average maturity | 6.4 | yrs | 6.2 | yrs | ||

| Effective duration | 4.4 | yrs | 4.5 | yrs | ||

| At December 31, | ||||||||

| 2011 | 2010 | |||||||

| Weighted average yield-to-amortized cost | 5.3 | % | 5.5 | % | ||||

| Weighted average maturity | 6.7 | yrs | 6.8 | yrs | ||||

| Effective duration | 4.4 | yrs | 5.0 | yrs | ||||

26

| At December 31, | ||||||||

| (In millions) | 2011 | 2010 | ||||||

| Investment-grade corporate | $ | 5,100 | $ | 4,695 | ||||

| States, municipalities and political subdivisions | 320 | 293 | ||||||

| Below investment-grade corporate | 198 | 268 | ||||||

| Government sponsored enterprises | 160 | 200 | ||||||

| Convertibles and bonds with warrants attached | 59 | 69 | ||||||

| United States government | 7 | 5 | ||||||

| Foreign government | 3 | 3 | ||||||

| Total | $ | 5,847 | $ | 5,533 | ||||

| (Dollars in millions) | At December 31, | ||||||

| 2014 | 2013 | ||||||

| Investment-grade corporate | $ | 5,208 | $ | 5,293 | |||

| States, municipalities and political subdivisions | 313 | 301 | |||||

| Below investment-grade corporate | 318 | 240 | |||||

| Commercial mortgage backed | 259 | 143 | |||||

| Government sponsored enterprises | 208 | 200 | |||||

| Foreign government | 10 | 10 | |||||

| Convertibles and bonds with warrants attached | 7 | 17 | |||||

| United States government | 7 | 7 | |||||

| Total | $ | 6,330 | $ | 6,211 | |||

2013.

2014.

| (In millions) | State issued general obligation bonds | Local issued general obligation bonds | Special revenue bonds | Total | Percent of total | |||||||||||||||

| At December 31, 2011 | ||||||||||||||||||||

| Texas | $ | - | $ | 425 | $ | 99 | $ | 524 | 17.9 | % | ||||||||||

| Indiana | - | 16 | 316 | 332 | 11.3 | |||||||||||||||

| Michigan | - | 257 | 12 | 269 | 9.2 | |||||||||||||||

| Illinois | - | 226 | 23 | 249 | 8.5 | |||||||||||||||

| Ohio | - | 132 | 107 | 239 | 8.2 | |||||||||||||||

| Washington | 3 | 174 | 39 | 216 | 7.4 | |||||||||||||||

| Wisconsin | 2 | 115 | 25 | 142 | 4.8 | |||||||||||||||

| Pennsylvania | - | 76 | 8 | 84 | 2.9 | |||||||||||||||

| Florida | - | 21 | 61 | 82 | 2.8 | |||||||||||||||

| Arizona | - | 51 | 27 | 78 | 2.7 | |||||||||||||||

| Colorado | - | 40 | 15 | 55 | 1.9 | |||||||||||||||

| Kansas | - | 27 | 20 | 47 | 1.6 | |||||||||||||||

| New Jersey | - | 30 | 17 | 47 | 1.6 | |||||||||||||||

| New York | - | 18 | 24 | 42 | 1.4 | |||||||||||||||

| Utah | - | 21 | 19 | 40 | 1.4 | |||||||||||||||

| All other states | 1 | 264 | 221 | 486 | 16.4 | |||||||||||||||

| Total | $ | 6 | $ | 1,893 | $ | 1,033 | $ | 2,932 | 100.0 | % | ||||||||||

| At December 31, 2010 | ||||||||||||||||||||

| Texas | $ | - | $ | 425 | $ | 107 | $ | 532 | 18.7 | % | ||||||||||

| Indiana | - | 21 | 328 | 349 | 12.2 | |||||||||||||||

| Michigan | - | 245 | 12 | 257 | 9.0 | |||||||||||||||

| Illinois | - | 219 | 23 | 242 | 8.5 | |||||||||||||||

| Ohio | - | 131 | 107 | 238 | 8.4 | |||||||||||||||

| Washington | - | 166 | 32 | 198 | 6.9 | |||||||||||||||

| Wisconsin | - | 116 | 19 | 135 | 4.7 | |||||||||||||||

| Florida | - | 19 | 67 | 86 | 3.0 | |||||||||||||||

| Pennsylvania | - | 67 | 9 | 76 | 2.7 | |||||||||||||||

| Arizona | - | 46 | 30 | 76 | 2.7 | |||||||||||||||

| Colorado | - | 37 | 15 | 52 | 1.8 | |||||||||||||||

| New Jersey | - | 28 | 17 | 45 | 1.6 | |||||||||||||||

| Kansas | - | 24 | 20 | 44 | 1.5 | |||||||||||||||

| New York | 3 | 15 | 21 | 39 | 1.4 | |||||||||||||||

| Utah | - | 20 | 17 | 37 | 1.3 | |||||||||||||||

| All other states | - | 233 | 211 | 444 | 15.6 | |||||||||||||||

| Total | $ | 3 | $ | 1,812 | $ | 1,035 | $ | 2,850 | 100.0 | % | ||||||||||

| (Dollars in millions) | Local issued general | Special revenue | State issued general | Fair value | Percent of | |||||||||||||

| At December 31, 2014 | obligation bonds | bonds | obligation bonds | total | total | |||||||||||||

| Texas | $ | 368 | $ | 71 | $ | — | $ | 439 | 14.0 | % | ||||||||

| Indiana | 2 | 244 | — | 246 | 7.9 | |||||||||||||

| Ohio | 120 | 78 | 9 | 207 | 6.6 | |||||||||||||

| Michigan | 194 | 8 | — | 202 | 6.5 | |||||||||||||

| Washington | 127 | 30 | 7 | 164 | 5.2 | |||||||||||||

| Illinois | 146 | 18 | — | 164 | 5.2 | |||||||||||||

| Arizona | 78 | 47 | — | 125 | 4.0 | |||||||||||||

| Wisconsin | 87 | 30 | 2 | 119 | 3.8 | |||||||||||||

| Pennsylvania | 83 | 15 | 10 | 108 | 3.5 | |||||||||||||

| Florida | 26 | 74 | — | 100 | 3.2 | |||||||||||||

| New York | 59 | 36 | 4 | 99 | 3.2 | |||||||||||||

| New Jersey | 55 | 15 | 2 | 72 | 2.3 | |||||||||||||

| Kansas | 51 | 21 | — | 72 | 2.3 | |||||||||||||

| Colorado | 44 | 25 | — | 69 | 2.2 | |||||||||||||

| California | 40 | 19 | 3 | 62 | 2.0 | |||||||||||||

| All other states | 493 | 337 | 52 | 882 | 28.1 | |||||||||||||

| Total | $ | 1,973 | $ | 1,068 | $ | 89 | $ | 3,130 | 100.0 | % | ||||||||

| At December 31, 2013 | ||||||||||||||||||

| Texas | $ | 385 | $ | 66 | $ | — | $ | 451 | 15.5 | % | ||||||||

| Michigan | 238 | 9 | — | 247 | 8.5 | |||||||||||||

| Indiana | 8 | 232 | — | 240 | 8.2 | |||||||||||||

| Ohio | 119 | 87 | 6 | 212 | 7.3 | |||||||||||||

| Illinois | 184 | 19 | — | 203 | 7.0 | |||||||||||||

| Washington | 150 | 32 | 5 | 187 | 6.4 | |||||||||||||

| Wisconsin | 108 | 32 | 2 | 142 | 4.9 | |||||||||||||

| Pennsylvania | 93 | 9 | 9 | 111 | 3.8 | |||||||||||||

| Arizona | 55 | 31 | — | 86 | 3.0 | |||||||||||||

| Florida | 24 | 62 | — | 86 | 3.0 | |||||||||||||

| New York | 48 | 31 | 4 | 83 | 2.9 | |||||||||||||

| Colorado | 45 | 17 | — | 62 | 2.1 | |||||||||||||

| New Jersey | 44 | 17 | — | 61 | 2.1 | |||||||||||||

| Minnesota | 42 | 7 | 2 | 51 | 1.8 | |||||||||||||

| Utah | 31 | 19 | — | 50 | 1.7 | |||||||||||||

| All other states | 338 | 270 | 30 | 638 | 21.8 | |||||||||||||

| Total | $ | 1,912 | $ | 940 | $ | 58 | $ | 2,910 | 100.0 | % | ||||||||

| Percent of Publicly Traded Common Stock Portfolio | ||||||||||||||||

| At December 31, 2011 | At December 31, 2010 | |||||||||||||||

| Cincinnati Financial | S&P 500 Industry Weightings | Cincinnati Financial | S&P 500 Industry Weightings | |||||||||||||

| Sector: | ||||||||||||||||

| Information technology | 16.9 | % | 19.0 | % | 13.0 | % | 18.7 | % | ||||||||

| Energy | 14.0 | 12.3 | 12.9 | 12.0 | ||||||||||||

| Consumer staples | 12.3 | 11.5 | 15.4 | 10.6 | ||||||||||||

| Healthcare | 12.0 | 11.8 | 14.1 | 10.9 | ||||||||||||

| Industrials | 11.8 | 10.7 | 11.7 | 11.0 | ||||||||||||

| Consumer discretionary | 9.4 | 10.7 | 8.3 | 10.6 | ||||||||||||

| Financial | 8.5 | 13.4 | 11.7 | 16.1 | ||||||||||||

| Materials | 5.7 | 3.5 | 5.2 | 3.7 | ||||||||||||

| Utilities | 5.5 | 3.9 | 4.2 | 3.3 | ||||||||||||

| Telecomm services | 3.9 | 3.2 | 3.5 | 3.1 | ||||||||||||

| Total | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | ||||||||

| Percent of publicly traded common stock portfolio | |||||||||||

| At December 31, 2014 | At December 31, 2013 | ||||||||||

| Cincinnati Financial | S&P 500 Industry Weightings | Cincinnati Financial | S&P 500 Industry Weightings | ||||||||

| Sector: | |||||||||||

| Information technology | 17.3 | % | 19.8 | % | 18.7 | % | 18.6 | % | |||

| Industrials | 14.3 | 10.3 | 14.0 | 10.9 | |||||||

| Financial | 13.8 | 16.3 | 12.0 | 16.2 | |||||||

| Healthcare | 11.9 | 14.7 | 11.5 | 13.0 | |||||||

| Energy | 10.5 | 8.0 | 10.5 | 10.3 | |||||||

| Consumer staples | 10.5 | 10.0 | 10.5 | 9.8 | |||||||

| Consumer discretionary | 10.2 | 12.1 | 9.8 | 12.5 | |||||||

| Materials | 5.5 | 3.2 | 5.7 | 3.5 | |||||||

| Utilities | 3.7 | 3.3 | 4.2 | 2.9 | |||||||

| Telecomm services | 2.3 | 2.3 | 3.1 | 2.3 | |||||||

| Total | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | |||

Additional information about the composition of investments is included in Item 8, Note 2 of the Consolidated Financial Statements, Page 120. A detailed listing of our portfolio is updated on our website,www.cinfin.com/investors, each quarter when2014. During 2013, we report our quarterly financial results.

purchased $48 million and sold $23 million.

2013.

| Insurance Operations – All of our insurance subsidiaries are subject to licensing and supervision by departments of insurance in the states in which they do business. The nature and extent of such regulations vary, but generally are rooted in statutes that delegate regulatory, supervisory and administrative powers to state insurance departments. Such regulations, supervision and administration of the insurance subsidiaries include, among others, the standards of solvency that must be met and maintained; the licensing of insurers and their agents and brokers; the nature and limitations on investments; deposits of securities |

The legislative and regulatory climate in Florida continues to create uncertainty for the benefit of policyholders; regulation of standard market policy forms and premium rates; policy cancellations and nonrenewals; periodic examination of the affairs of insurance industry. In February 2007, wecompanies; annual and other reports required to be filed on the financial condition of insurers or for other purposes; requirements regarding reserves for unearned premiums, losses and other matters; the nature of and limitations on dividends to policyholders and shareholders; the nature and extent of required participation in insurance guaranty funds; the involuntary assumption of hard-to-place or high-risk insurance business, primarily workers’ compensation insurance; and the collection, remittance and reporting of certain taxes and fees. Our primary insurance regulators have adopted a marketing stancethe Model Audit Rule for annual statutory financial reporting. This regulation closely mirrors the Sarbanes-Oxley Act on matters such as auditor independence, corporate governance and internal controls over financial reporting. The regulation permits the audit committee of continuingCincinnati Financial Corporation’s board of directors to service existing accounts while writing no newalso serve as the audit committee of each of our insurance subsidiaries for purposes of this regulation.

On August 24, 2007, the company received administrative subpoenas from the Florida Office of Insurance Regulation seeking documentsNAIC and testimony concerningstate regulators to identify companies that may be undercapitalized and may merit further regulatory action. The NAIC has a standard formula for annually assessing RBC. The formula for calculating RBC for property casualty companies takes into account asset and credit risks but places more emphasis on underwriting factors for reserving and pricing. The formula for calculating RBC for life insurance for residential risks located in Floridacompanies takes into account factors relating to insurance, business, asset and communications with reinsurers, risk modeling companies, rating agencies and insurance trade associations. We produced documents to respond to the subpoenas. Although inactive, these subpoenas remain outstanding as of December 31, 2011. We continue to assess the changing insurance environment in Florida.

The failure of our risk management strategies could have a material adverse impact on our financial condition and/or results of operations.

Increased advertising by insurers, especially direct marketers, could cause consumers to shift their buying habits, bypassing independent agents altogether.

Additionally, man-made events, such as hydraulic fracturing, could cause damage from earth movement or create environmental and/or health hazards.

Analysis.

equity.

Risk.

Large competitors could intentionally disrupt the market by targeting certain lines or underpricing the market.

Reserves.

The process used to determine our loss reserves is discussed in Item 7, Critical Accounting Estimates, Property Casualty Insurance Loss and Loss Expense Reserves and Life Insurance Policy Reserves, Page 42 and Page 46.

We participated in USAIG, a joint underwriting association of individual insurance companies that collectively functions as a worldwide insurance market for all types of aviation and aerospace accounts. Our participation was terminated after policy year 2002. At year-end 2011, a substantial portion of our total reinsurance receivables were related to USAIG, primarily for events of September 11, 2001. If the pool participants and reinsurers were unable to fulfill their financial obligations and all security collateral that supports the participants’ obligations were to become worthless, we could be liable for an additional pool liability and our financial position and results of operations could be materially affected. At year-end 2011, all pool participants and reinsurers were financially solvent.

The loss or significant restriction on the use of a particular variable, such as credit, in pricing and underwriting our products could lead to future unprofitability and increased costs.

Implementation of the Affordable Care Act (ACA) may affect the ability of the company to grow profitably.

Part II

Cincinnati Financial Corporation had approximately 13,00070,000 shareholders of record as of December 31, 2011. This number does not represent2014. While approximately 13,000 shareholders are registered, the total numbermajority of shareholders because someare beneficial owners whose shares are beneficially held in “street name” by brokers and others on behalf of individual owners of our shares. Manyinstitutional accounts. We believe many of our independent agent representatives and most of the 4,0674,305 associates of our subsidiaries own the company’s common stock.

| (Source: Nasdaq Global Select Market) | 2011 | 2010 | ||||||||||||||||||||||||||||||

| Quarter: | 1st | 2nd | 3rd | 4th | 1st | 2nd | 3rd | 4th | ||||||||||||||||||||||||

| High | $ | 34.33 | $ | 33.55 | $ | 29.54 | $ | 30.79 | $ | 29.65 | $ | 30.38 | $ | 29.39 | $ | 32.27 | ||||||||||||||||

| Low | 31.43 | 27.80 | 23.65 | 24.66 | 25.50 | 25.65 | 25.25 | 28.68 | ||||||||||||||||||||||||

| Period-end close | 32.79 | 29.18 | 26.33 | 30.46 | 28.91 | 25.87 | 28.82 | 31.69 | ||||||||||||||||||||||||

| Cash dividends declared | 0.40 | 0.40 | 0.4025 | 0.4025 | 0.395 | 0.395 | 0.40 | 0.40 | ||||||||||||||||||||||||

| (Source: Nasdaq Global Select Market) | 2014 | 2013 | ||||||||||||||||||||||||||||||

| Quarter: | 1st | 2nd | 3rd | 4th | 1st | 2nd | 3rd | 4th | ||||||||||||||||||||||||

| High | $ | 52.19 | $ | 49.73 | $ | 48.86 | $ | 55.35 | $ | 47.35 | $ | 50.60 | $ | 50.01 | $ | 53.74 | ||||||||||||||||

| Low | 44.90 | 47.00 | 45.69 | 45.09 | 39.60 | 44.53 | 43.62 | 46.61 | ||||||||||||||||||||||||

| Period-end close | 48.66 | 48.04 | 47.05 | 51.83 | 47.22 | 45.92 | 47.16 | 52.37 | ||||||||||||||||||||||||

| Cash dividends declared | 0.44 | 0.44 | 0.44 | 0.44 | 0.4075 | 0.4075 | 0.42 | 0.42 | ||||||||||||||||||||||||

Statements.

| Plan category | Number of securities to be issued upon exercise of outstanding options, warrants and rights at December 31, 2011 | Weighted-average exercise price of outstanding options, warrants and rights | Number of securities remaining available for future issuance under equity compensation plan (excluding securities reflected in column (a)) at December 31, 2011 | |||||||||

| (a) | (b) | (c) | ||||||||||

| Equity compensation plans approved by security holders | 9,357,108 | $ | 36.71 | 4,427,698 | ||||||||

| Equity compensation plans not approved by security holders | - | - | - | |||||||||

| Total | 9,357,108 | $ | 36.71 | 4,427,698 | ||||||||

2014:

| Plan category | Number of securities to be issued upon exercise of outstanding options, warrants and rights at December 31, 2014 | Weighted-average exercise price of outstanding options, warrants and rights | Number of securities remaining available for future issuance under equity compensation plan (excluding securities reflected in column (a)) at December 31, 2014 | |||||||

| (a) | (b) | (c) | ||||||||

Equity compensation plans approved by security holders | 4,958,191 | $ | 39.10 | 6,199,048 | ||||||

Equity compensation plans not approved by security holders | — | — | — | |||||||

| Total | 4,958,191 | $ | 39.10 | 6,199,048 | ||||||

| Period | Total number of shares purchased | Average price paid per share | Total number of shares purchased as part of publicly announced plans or programs | Maximum number of shares that may yet be purchased under the plans or programs | ||||||||||||

| January 1-31, 2011 | 0 | $ | 0.00 | 0 | 8,666,349 | |||||||||||

| February 1-28, 2011 | 0 | 0.00 | 0 | 8,666,349 | ||||||||||||

| March 1-31, 2011 | 0 | 0.00 | 0 | 8,666,349 | ||||||||||||

| April 1-30, 2011 | 0 | 0.00 | 0 | 8,666,349 | ||||||||||||

| May 1-31, 2011 | 0 | 0.00 | 0 | 8,666,349 | ||||||||||||

| June 1-30, 2011 | 0 | 0.00 | 0 | 8,666,349 | ||||||||||||

| July 1-31, 2011 | 0 | 0.00 | 0 | 8,666,349 | ||||||||||||

| August 1-31, 2011 | 1,152,587 | 26.03 | 1,152,587 | 7,513,762 | ||||||||||||

| September 1-30, 2011 | 0 | 0.00 | 0 | 7,513,762 | ||||||||||||

| October 1-31, 2011 | 0 | 0.00 | 0 | 7,513,762 | ||||||||||||

| November 1-30, 2011 | 0 | 0.00 | 0 | 7,513,762 | ||||||||||||

| December 1-31, 2011 | 75,000 | 28.88 | 75,000 | 7,438,762 | ||||||||||||

| Totals | 1,227,587 | 26.20 | 1,227,587 | |||||||||||||

| Period | Total number of shares purchased | Average price paid per share | Total number of shares purchased as part of publicly announced plans or programs | Maximum number of shares that may yet be purchased under the plans or programs | |||||||||

| January 1-31, 2014 | — | — | — | 5,549,493 | |||||||||

| February 1-28, 2014 | — | — | — | 5,549,493 | |||||||||

| March 1-31, 2014 | 150,000 | $ | 47.69 | 150,000 | 5,399,493 | ||||||||

| April 1-30, 2014 | — | — | — | 5,399,493 | |||||||||

| May 1-31, 2014 | — | — | — | 5,399,493 | |||||||||

| June 1-30, 2014 | — | — | — | 5,399,493 | |||||||||

| July 1-31, 2014 | 100,000 | 46.07 | 100,000 | 5,299,493 | |||||||||

| August 1-31, 2014 | 200,000 | 46.11 | 200,000 | 5,099,493 | |||||||||

| September 1-30, 2014 | — | — | — | 5,099,493 | |||||||||

| October 1-31, 2014 | — | — | — | 5,099,493 | |||||||||

| November 1-30, 2014 | — | — | — | 5,099,493 | |||||||||

| December 1-31, 2014 | — | — | — | 5,099,493 | |||||||||

| Totals | 450,000 | 46.63 | 450,000 | ||||||||||

December 31, 2014.

| Years ended December 31, | ||||||||||||||||||||

| (In millions except per share data) | 2011 | 2010 | 2009 | 2008 | 2007 | |||||||||||||||

| Consolidated Income Statement Data | ||||||||||||||||||||

| Earned premiums | $ | 3,194 | $ | 3,082 | $ | 3,054 | $ | 3,136 | $ | 3,250 | ||||||||||

| Investment income, net of expenses | 525 | 518 | 501 | 537 | 608 | |||||||||||||||

| Realized investment gains and losses* | 70 | 159 | 336 | 138 | 382 | |||||||||||||||

| Total revenues | 3,803 | 3,772 | 3,903 | 3,824 | 4,259 | |||||||||||||||

| Net income | 166 | 377 | 432 | 429 | 855 | |||||||||||||||

| Net income per common share: | ||||||||||||||||||||

| Basic | $ | 1.02 | $ | 2.32 | $ | 2.66 | $ | 2.63 | $ | 5.01 | ||||||||||

| Diluted | 1.02 | 2.31 | 2.65 | 2.62 | 4.97 | |||||||||||||||

| Cash dividends per common share: | ||||||||||||||||||||

| Declared | 1.605 | 1.59 | 1.57 | 1.56 | 1.42 | |||||||||||||||

| Paid | 1.6025 | 1.585 | 1.565 | 1.525 | 1.40 | |||||||||||||||

| Shares Outstanding | ||||||||||||||||||||

| Weighted average, diluted | 163 | 163 | 163 | 163 | 172 | |||||||||||||||

| Consolidated Balance Sheet Data | ||||||||||||||||||||

| Invested assets | $ | 11,801 | $ | 11,508 | $ | 10,643 | $ | 8,890 | $ | 12,261 | ||||||||||

| Deferred policy acquisition costs | 510 | 488 | 481 | 509 | 461 | |||||||||||||||

| Total assets | 15,668 | 15,095 | 14,440 | 13,369 | 16,637 | |||||||||||||||

| Gross loss and loss expense reserves | 4,339 | 4,200 | 4,142 | 4,086 | 3,967 | |||||||||||||||

| Life policy reserves | 2,214 | 2,034 | 1,783 | 1,551 | 1,478 | |||||||||||||||

| Long-term debt | 790 | 790 | 790 | 791 | 791 | |||||||||||||||

| Shareholders' equity | 5,055 | 5,032 | 4,760 | 4,182 | 5,929 | |||||||||||||||

| Book value per share | 31.16 | 30.91 | 29.25 | 25.75 | 35.70 | |||||||||||||||

| Value creation ratio | 6.0 | % | 11.1 | % | 19.7 | % | (23.5 | )% | (5.7 | )% | ||||||||||

| Consolidated Property Casualty Operations | ||||||||||||||||||||

| Earned premiums | $ | 3,029 | $ | 2,924 | $ | 2,911 | $ | 3,010 | $ | 3,125 | ||||||||||

| Unearned premiums | 1,631 | 1,551 | 1,507 | 1,542 | 1,562 | |||||||||||||||

| Gross loss and loss expense reserves | 4,280 | 4,137 | 4,096 | 4,040 | 3,925 | |||||||||||||||

| Investment income, net of expenses | 350 | 348 | 336 | 350 | 393 | |||||||||||||||

| Loss ratio | 64.4 | % | 56.5 | % | 58.6 | % | 57.7 | % | 46.6 | % | ||||||||||

| Loss expense ratio | 12.6 | 12.4 | 13.1 | 10.6 | 12.0 | |||||||||||||||

| Underwriting expense ratio | 32.2 | 32.8 | 32.8 | 32.3 | 31.7 | |||||||||||||||

| Combined ratio | 109.2 | % | 101.7 | % | 104.5 | % | 100.6 | % | 90.3 | % | ||||||||||

Per share data adjusted

| (In millions except per share data) | Years ended December 31, | |||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | 2010 | ||||||||||||||||

| Consolidated Income Statement Data | ||||||||||||||||||||

| Earned premiums | $ | 4,243 | $ | 3,902 | $ | 3,522 | $ | 3,194 | $ | 3,082 | ||||||||||

| Investment income, net of expenses | 549 | 529 | 531 | 525 | 518 | |||||||||||||||

| Realized investment gains, net* | 133 | 83 | 42 | 70 | 159 | |||||||||||||||

| Total revenues | 4,945 | 4,531 | 4,111 | 3,803 | 3,772 | |||||||||||||||

| Net income | 525 | 517 | 421 | 164 | 375 | |||||||||||||||

| Net income per common share: | ||||||||||||||||||||

| Basic | $ | 3.21 | $ | 3.16 | $ | 2.59 | $ | 1.01 | $ | 2.30 | ||||||||||

| Diluted | 3.18 | 3.12 | 2.57 | 1.01 | 2.30 | |||||||||||||||

| Cash dividends per common share: | ||||||||||||||||||||

| Declared | 1.76 | 1.655 | 1.62 | 1.605 | 1.59 | |||||||||||||||

| Paid | 1.74 | 1.6425 | 1.615 | 1.6025 | 1.585 | |||||||||||||||

| Diluted weighted average shares outstanding | 165.1 | 165.4 | 163.7 | 163.3 | 163.3 | |||||||||||||||

| Consolidated Balance Sheet Data | ||||||||||||||||||||

| Total investments | $ | 14,386 | $ | 13,564 | $ | 12,534 | $ | 11,801 | $ | 11,508 | ||||||||||

| Net unrealized investment gains | 2,719 | 2,335 | 1,875 | 1,489 | 1,250 | |||||||||||||||

| Deferred policy acquisition costs | 578 | 565 | 470 | 477 | 458 | |||||||||||||||

| Total assets | 18,753 | 17,662 | 16,548 | 15,635 | 15,065 | |||||||||||||||

| Gross loss and loss expense reserves | 4,485 | 4,311 | 4,230 | 4,339 | 4,200 | |||||||||||||||

| Life policy reserves | 2,497 | 2,390 | 2,295 | 2,214 | 2,034 | |||||||||||||||

| Long-term debt | 791 | 790 | 790 | 790 | 790 | |||||||||||||||

| Shareholders' equity | 6,573 | 6,070 | 5,453 | 5,033 | 5,012 | |||||||||||||||

| Book value per share | 40.14 | 37.21 | 33.48 | 31.03 | 30.79 | |||||||||||||||

| Shares outstanding | 163.7 | 163.1 | 162.9 | 162.2 | 162.8 | |||||||||||||||

| Value creation ratio | 12.6 | % | 16.1 | % | 12.6 | % | 6.0 | % | 11.1 | % | ||||||||||

| Consolidated Property Casualty Operations Data | ||||||||||||||||||||

| Earned premiums | $ | 4,045 | $ | 3,713 | $ | 3,344 | $ | 3,029 | $ | 2,924 | ||||||||||

| Unearned premiums | 2,081 | 1,970 | 1,790 | 1,631 | 1,551 | |||||||||||||||

| Gross loss and loss expense reserves | 4,438 | 4,241 | 4,169 | 4,280 | 4,137 | |||||||||||||||

| Investment income, net of expenses | 358 | 348 | 351 | 350 | 348 | |||||||||||||||

| Loss and loss expense ratio | 65.0 | % | 61.9 | % | 63.9 | % | 77.0 | % | 68.9 | % | ||||||||||

| Underwriting expense ratio | 30.6 | 31.9 | 32.2 | 32.3 | 32.9 | |||||||||||||||

| Combined ratio | 95.6 | % | 93.8 | % | 96.1 | % | 109.3 | % | 101.8 | % | ||||||||||

Executive Summary

Although recent years have been difficult for ourStrategy.

One year | Three-year % average | Five-year % average | |||||||

| Value creation ratio: | |||||||||

| As of December 31, 2014 | 12.6 | % | 13.8 | % | 11.7 | % | |||

| As of December 31, 2013 | 16.1 | 11.6 | 13.1 | ||||||

| As of December 31, 2012 | 12.6 | 9.9 | 5.2 | ||||||

| Years ended December 31, | |||||||||

| 2014 | 2013 | 2012 | |||||||

| Value creation ratio major components: | |||||||||

| Net income before net realized gains | 7.2 | % | 8.5 | % | 7.7 | % | |||

| Change in realized and unrealized gains, fixed-maturity securities | 1.2 | (4.5 | ) | 2.7 | |||||

| Change in realized and unrealized gains, equity securities | 4.3 | 10.9 | 2.8 | ||||||

| Other | (0.1 | ) | 1.2 | (0.6 | ) | ||||

| Value creation ratio | 12.6 | % | 16.1 | % | 12.6 | % | |||

| (Dollars are per share) | Years ended December 31, | |||||||||||

| 2014 | 2013 | 2012 | ||||||||||

| Book value change per share: | ||||||||||||

| End of period book value | $ | 40.14 | $ | 37.21 | $ | 33.48 | ||||||

| Less beginning of period book value | 37.21 | 33.48 | 31.03 | |||||||||

| Change in book value | $ | 2.93 | $ | 3.73 | $ | 2.45 | ||||||

| Change in book value: | ||||||||||||

| Net income before realized gains | $ | 2.69 | $ | 2.84 | $ | 2.41 | ||||||

| Change in realized and unrealized gains, fixed-maturity securities | 0.43 | (1.50 | ) | 0.84 | ||||||||

| Change in realized and unrealized gains, equity securities | 1.61 | 3.64 | 0.86 | |||||||||

| Dividend declared to shareholders | (1.76 | ) | (1.66 | ) | (1.62 | ) | ||||||

| Other | (0.04 | ) | 0.41 | (0.04 | ) | |||||||

| Change in book value | $ | 2.93 | $ | 3.73 | $ | 2.45 | ||||||

| One | Three-year | Five-year | ||||||||||

| year | % average | % average | ||||||||||

| Value creation ratio | ||||||||||||

| as of December 31, 2011 | 6.0 | % | 12.3 | % | 1.5 | % | ||||||

| as of December 31, 2010 | 11.1 | 2.4 | 3.7 | |||||||||

| as of December 31, 2009 | 19.7 | (3.2 | ) | 1.7 | ||||||||

| Years ended December 31, | ||||||||||||

| 2011 | 2010 | 2009 | ||||||||||

| Value creation ratio | ||||||||||||

| End of year book value | $ | 31.16 | $ | 30.91 | $ | 29.25 | ||||||

| Less beginning of year book value | 30.91 | 29.25 | 25.75 | |||||||||

| Change in book value | 0.25 | 1.66 | 3.50 | |||||||||

| Dividend declared to shareholders | 1.605 | 1.59 | 1.57 | |||||||||

| Total contribution to value creation ratio | $ | 1.86 | $ | 3.25 | $ | 5.07 | ||||||

| Contribution to value creation ratio from change in book value* | 0.8 | % | 5.7 | % | 13.6 | % | ||||||

| Contribution to value creation ratio from dividends declared to shareholders** | 5.2 | 5.4 | 6.1 | |||||||||

| Value creation ratio | 6.0 | % | 11.1 | % | 19.7 | % | ||||||

In 2011, our

| (Dollars are per share) | Years ended December 31, | |||||||||||

| 2014 | 2013 | 2012 | ||||||||||

| Value creation ratio: | ||||||||||||

| End of year book value | $ | 40.14 | $ | 37.21 | $ | 33.48 | ||||||

| Less beginning of year book value | 37.21 | 33.48 | 31.16 | |||||||||

| Change in book value | 2.93 | 3.73 | 2.32 | |||||||||

| Dividend declared to shareholders | 1.76 | 1.655 | 1.62 | |||||||||

| Total value creation ratio | $ | 4.69 | $ | 5.385 | $ | 3.94 | ||||||

| Value creation ratio from change in book value* | 7.9 | % | 11.1 | % | 7.4 | % | ||||||

| Value creation ratio from dividends declared to shareholders** | 4.7 | 5.0 | 5.2 | |||||||||

| Value creation ratio | 12.6 | % | 16.1 | % | 12.6 | % | ||||||

| Investment income growth, on a |

| ◦ | Over the five years ended December 31, |

Strategic Initiatives Highlights

Management has worked to identify a strategy that can lead to long-term success, with concurrence by the board of directors. Our strategy is intended to position us to compete successfully in the markets we have targeted while appropriately managing risk. We discuss our long-term, proven strategy in Item 1, Our Business and Our Strategy, Page 3. We believe successful implementation of initiatives that support our strategy will help us better serve our agent customers and reduce volatility in our financial results while we also grow earnings and book value over the long-term, successfully navigating challenging economic, market or industry pricing cycles.

We discuss these strategic initiatives, along with related metrics to assess progress, in Item 1, Strategic Initiatives, Page 10. Below is a review of highlights of our financial results for the past three years. Detailed discussion of these topics appears in Results of Operations, Page 50, and Liquidity and Capital Resources, Page 85.

Corporate Financial Highlights

The

| (Dollars in millions except share data) | At December 31, | At December 31, | ||||||

| 2014 | 2013 | |||||||

| Balance sheet data: | ||||||||

| Total investments | $ | 14,386 | $ | 13,564 | ||||

| Total assets | 18,753 | 17,662 | ||||||

| Short-term debt | 49 | 104 | ||||||

| Long-term debt | 791 | 790 | ||||||

| Shareholders' equity | 6,573 | 6,070 | ||||||

| Book value per share | 40.14 | 37.21 | ||||||

| Debt-to-total-capital ratio | 11.3 | % | 12.8 | % | ||||

Balance Sheet Data

| At December 31, | At December 31, | |||||||

| (Dollars in millions except share data) | 2011 | 2010 | ||||||

| Balance sheet data | ||||||||

| Invested assets | $ | 11,801 | $ | 11,508 | ||||

| Total assets | 15,668 | 15,095 | ||||||

| Short-term debt | 104 | 49 | ||||||

| Long-term debt | 790 | 790 | ||||||

| Shareholders' equity | 5,055 | 5,032 | ||||||

| Book value per share | 31.16 | 30.91 | ||||||

| Debt-to-total-capital ratio | 15.0 | % | 14.3 | % | ||||

Invested assets grew 3 percent during 20112014 on a fair value basis, with market gains slightly outpacing anthat added to the 4 percent increase in the cost basis of invested assets of approximately 1 percent.basis. Entering 2012,2015, we believe the portfolio continues to be well-diversified,well diversified and we believe it is well-positionedwell positioned to withstand short-term fluctuations. We discuss our investment strategy in Item 1, Investments Segment, Page 20, and results for the segment in Investment ResultsInvestments Results. Total assets rose 6 percent, primarily due to the increase in total investments. Shareholders’ equity and book value per share each rose 8 percent, for reasons discussed in the preceding Executive Summary.

Short-termour debt rose$55obligations decreased by $54 million primarily to fund share repurchases using our relatively low-cost source of borrowing.in 2014, compared with 2013. Our ratio of debt to total capital (debt plus shareholders’ equity) increased somewhatdecreased by 1.5 percentage points in 2011 but2014 and remains comfortably within our target range.

| Twelve months ended December 31, | 2011-2010 | 2010-2009 | ||||||||||||||||||

| (Dollars in millions except share data) | 2011 | 2010 | 2009 | Change % | Change % | |||||||||||||||

| Income statement data | ||||||||||||||||||||

| Earned premiums | $ | 3,194 | $ | 3,082 | $ | 3,054 | 4 | 1 | ||||||||||||

| Investment income, net of expenses (pretax) | 525 | 518 | 501 | 1 | 3 | |||||||||||||||

| Realized investment gains and losses (pretax) | 70 | 159 | 336 | (56 | ) | (53 | ) | |||||||||||||

| Total revenues | 3,803 | 3,772 | 3,903 | 1 | (3 | ) | ||||||||||||||

| Net income | 166 | 377 | 432 | (56 | ) | (13 | ) | |||||||||||||

| Per share data | ||||||||||||||||||||

| Net income - diluted | $ | 1.02 | $ | 2.31 | $ | 2.65 | (56 | ) | (13 | ) | ||||||||||

| Cash dividends declared | 1.605 | 1.59 | 1.57 | 1 | 1 | |||||||||||||||

| Weighted average shares outstanding | 163,259,222 | 163,274,491 | 162,866,863 | 0 | 0 | |||||||||||||||

| (Dollars in millions except per share data) | Years ended December 31, | 2014-2013 | 2013-2012 | |||||||||||||||

| 2014 | 2013 | 2012 | Change % | Change % | ||||||||||||||

| Net income and comprehensive income data: | ||||||||||||||||||

| Earned premiums | $ | 4,243 | $ | 3,902 | $ | 3,522 | 9 | 11 | ||||||||||

| Investment income, net of expenses (pretax) | 549 | 529 | 531 | 4 | 0 | |||||||||||||

| Realized investment gains, net (pretax) | 133 | 83 | 42 | 60 | 98 | |||||||||||||

| Total revenues | 4,945 | 4,531 | 4,111 | 9 | 10 | |||||||||||||

| Net income | 525 | 517 | 421 | 2 | 23 | |||||||||||||

| Comprehensive income | 765 | 892 | 649 | (14 | ) | 37 | ||||||||||||

| Net income - diluted | $ | 3.18 | $ | 3.12 | $ | 2.57 | 2 | 21 | ||||||||||

| Cash dividends declared | 1.76 | 1.655 | 1.62 | 6 | 2 | |||||||||||||

| Diluted weighted average shares outstanding | 165.1 | 165.4 | 163.7 | 0 | 1 | |||||||||||||

gains.

Higher dividend2014 while interest income was largely responsible forrose 1 percent, growthdriving a net increase in 2011 pretax investment income while higher interest income drove 3 percent growth in 2010. The primary reason for the 2011 increase inof $20 million, or 4 percent. In addition to a larger common stock portfolio generating more dividend income was ain both 2014 and 2013, both years also benefited from higher average dividend payment rates for common stocksrates. Our investment operation’s performance is discussed further in our equity portfolio.

Investments Results.

| (Dollars in millions) | Years ended December 31, | 2011-2010 | 2010-2009 | |||||||||||||||||

| Consolidated property casualty highlights | 2011 | 2010 | 2009 | Change % | Change % | |||||||||||||||

| Net written premiums | $ | 3,098 | $ | 2,963 | $ | 2,911 | 5 | 2 | ||||||||||||

| Earned premiums | 3,029 | 2,924 | 2,911 | 4 | 0 | |||||||||||||||

| Underwriting loss | (276 | ) | (47 | ) | (128 | ) | nm | nm | ||||||||||||

| Pt. Change | Pt. Change | |||||||||||||||||||

| GAAP combined ratio | 109.2 | % | 101.7 | % | 104.5 | % | 7.5 | (2.8 | ) | |||||||||||

| Statutory combined ratio | 108.9 | 101.8 | 104.4 | 7.1 | (2.6 | ) | ||||||||||||||

| Written premium to statutory surplus | 0.8 | 0.8 | 0.8 | 0.0 | 0.0 | |||||||||||||||

| (Dollars in millions) | Years ended December 31, | 2014-2013 | 2013-2012 | |||||||||||||||

| 2014 | 2013 | 2012 | Change % | Change % | ||||||||||||||

| Consolidated property casualty data: | ||||||||||||||||||

| Net written premiums | $ | 4,143 | $ | 3,893 | $ | 3,482 | 6 | 12 | ||||||||||

| Earned premiums | 4,045 | 3,713 | 3,344 | 9 | 11 | |||||||||||||

| Underwriting profit | 186 | 233 | 137 | (20 | ) | 70 | ||||||||||||

| Pt. Change | Pt. Change | |||||||||||||||||

| GAAP combined ratio | 95.6 | % | 93.8 | % | 96.1 | % | 1.8 | (2.3 | ) | |||||||||

| Statutory combined ratio | 95.1 | 92.8 | 95.4 | 2.3 | (2.6 | ) | ||||||||||||

| Written premium to statutory surplus | 0.9 | 0.9 | 0.9 | 0.0 | 0.0 | |||||||||||||

related segments.

We have formal risk management programs overseen by an executive officer and supported by a team of representatives from business areas. The team provides reports to our chairman, our president and chief executive officer and our board of directors, as appropriate, on risk assessments, risk metrics and risk plans. Our use of operational audits, strategic plans and departmental business plans, as well as our culture of open communications and our fundamental respect for our Code of Conduct, continue to help us manage risks on an ongoing basis.

2013.

of $175,000 or more, a threshold amount that was $100,000 for several years prior to 2015.

These trendsmentioned, such as:

industry pricing

inflation

| Net loss and loss expense range of reserves | ||||||||||||||||||||

| Carried | Low | High | Standard | Net income | ||||||||||||||||

| (In millions) | reserves | point | point | error | effect | |||||||||||||||

| At December 31, 2011 | ||||||||||||||||||||

| Total | $ | 3,905 | $ | 3,677 | $ | 4,056 | ||||||||||||||

| Commercial casualty | $ | 1,613 | $ | 1,432 | $ | 1,750 | $ | 159 | $ | 103 | ||||||||||

| Commercial property | 209 | 175 | 229 | 27 | 18 | |||||||||||||||

| Commercial auto | 349 | 333 | 365 | 16 | 10 | |||||||||||||||

| Workers' compensation | 966 | 875 | 1,056 | 90 | 59 | |||||||||||||||

| Personal auto | 176 | 168 | 184 | 8 | 5 | |||||||||||||||

| Homeowners | 121 | 107 | 129 | 11 | 7 | |||||||||||||||

| At December 31, 2010 | ||||||||||||||||||||

| Total | $ | 3,811 | $ | 3,571 | $ | 3,952 | ||||||||||||||

| Commercial casualty | $ | 1,644 | $ | 1,455 | $ | 1,781 | $ | 163 | $ | 106 | ||||||||||

| Commercial property | 155 | 136 | 176 | 20 | 13 | |||||||||||||||

| Commercial auto | 356 | 336 | 376 | 20 | 13 | |||||||||||||||

| Workers' compensation | 1,010 | 906 | 1,079 | 87 | 57 | |||||||||||||||

| Personal auto | 153 | 145 | 161 | 8 | 5 | |||||||||||||||

| Homeowners | 105 | 95 | 114 | 9 | 6 | |||||||||||||||

If actual unpaid loss and loss expenses fall within these ranges, our cash flow and fixed-maturity investments should provide sufficient liquidity to make the subsequent payments. To date, our cash flow has covered our loss and loss expense payments, and we have never had to sell investments to make these payments. If this were to become necessary, however, our fixed-maturity investments should provide us with ample liquidity. At year-end 2011, consolidated fixed-maturity investments exceeded total insurance reserves (including life policy reserves) by $2.226 billion.

| (Dollars in millions) | Net loss and loss expense range of reserves | |||||||||||||||||||

| Carried reserves | Low point | High point | Standard error | Net income effect | ||||||||||||||||

| At December 31, 2014 | ||||||||||||||||||||

| Total | $ | 4,156 | $ | 3,922 | $ | 4,296 | ||||||||||||||

| Commercial casualty | $ | 1,647 | $ | 1,477 | $ | 1,779 | $ | 151 | $ | 98 | ||||||||||

| Commercial property | 230 | 202 | 244 | 21 | 14 | |||||||||||||||

| Commercial auto | 431 | 411 | 450 | 19 | 12 | |||||||||||||||

| Workers' compensation | 983 | 873 | 1,067 | 97 | 63 | |||||||||||||||

| Personal auto | 214 | 204 | 223 | 9 | 6 | |||||||||||||||

| Homeowners | 104 | 95 | 112 | 8 | 5 | |||||||||||||||

| At December 31, 2013 | ||||||||||||||||||||

| Total | $ | 3,942 | $ | 3,727 | $ | 4,078 | ||||||||||||||

| Commercial casualty | $ | 1,532 | $ | 1,368 | $ | 1,643 | $ | 138 | $ | 90 | ||||||||||

| Commercial property | 241 | 223 | 260 | 19 | 12 | |||||||||||||||

| Commercial auto | 371 | 352 | 391 | 19 | 12 | |||||||||||||||

| Workers' compensation | 966 | 873 | 1,059 | 93 | 60 | |||||||||||||||

| Personal auto | 198 | 189 | 207 | 9 | 6 | |||||||||||||||

| Homeowners | 106 | 98 | 113 | 7 | 5 | |||||||||||||||

Policy.

Our long-term equity investment philosophy, emphasizing companies with strong indications of paying and growing dividends, combined with our strong statutory capital and surplus, liquidity and cash flow,

In accordance with ASC 820-10, we

of the Consolidated Financial Statements.

plan's benefit payments that equates to the market value of the selected bonds. The discount rate is reflective of current market interest rate conditions and our plan's liability characteristics.

lines insurance.

Profit-Sharing Commission Accrual

We establish an accrual for property casualty profit-sharing commissions. We base the profit-sharing commission accrual estimate on property casualty underwriting results. Profit-sharing commissions are paid to agencies using a formula that takes into account agency profitability over one-year and three-year periods, premium volume and other factors, including allocations of various expenses. Due to the complexity of the calculation and the variety of allocation factors that can affect profit-sharing commissions for an individual agency, the amount accrued can differ from the actual profit-sharing commissions paid. The profit-sharing commission accrual of $68 million in 2011 contributed 2.3 percentage points to the property casualty combined ratio. If profit-sharing commissions paid were to vary from that amount by 5 percent, it would affect 2012 net income by $2 million (after tax), or 1 cent per share, and the combined ratio by approximately 0.1 percentage points.

Investments Results.

Consolidated Property Casualty Insurance Results of Operations

business, as discussed in Commercial Lines Insurance Results.

| Years ended December 31, | 2011-2010 | 2010-2009 | ||||||||||||||||||

| (Dollars in millions) | 2011 | 2010 | 2009 | Change % | Change % | |||||||||||||||

| Earned premiums | $ | 3,029 | $ | 2,924 | $ | 2,911 | 4 | 0 | ||||||||||||

| Fee revenues | 4 | 4 | 3 | 0 | 33 | |||||||||||||||

| Total revenues | 3,033 | 2,928 | 2,914 | 4 | 0 | |||||||||||||||

| Loss and loss expenses from: | ||||||||||||||||||||

| Current accident year before catastrophe losses | 2,213 | 2,154 | 2,102 | 3 | 2 | |||||||||||||||

| Current accident year catastrophe losses | 407 | 165 | 172 | 147 | (4 | ) | ||||||||||||||

| Prior accident years before catastrophe losses | (280 | ) | (287 | ) | (181 | ) | 2 | (59 | ) | |||||||||||

| Prior accident years catastrophe losses | (5 | ) | (17 | ) | (7 | ) | 71 | (143 | ) | |||||||||||

| Total loss and loss expenses | 2,335 | 2,015 | 2,086 | 16 | (3 | ) | ||||||||||||||

| Underwriting expenses | 974 | 960 | 956 | 1 | 0 | |||||||||||||||

| Underwriting loss | $ | (276 | ) | $ | (47 | ) | $ | (128 | ) | nm | 63 | |||||||||

| Pt. Change | Pt. Change | |||||||||||||||||||

| Ratios as a percent of earned premiums: | ||||||||||||||||||||

| Current accident year before catastrophe losses | 73.0 | % | 73.6 | % | 72.2 | % | (0.6 | ) | 1.4 | |||||||||||

| Current accident year catastrophe losses | 13.4 | 5.6 | 5.9 | 7.8 | (0.3 | ) | ||||||||||||||

| Prior accident years before catastrophe losses | (9.3 | ) | (9.8 | ) | (6.2 | ) | 0.5 | (3.6 | ) | |||||||||||

| Prior accident years catastrophe losses | (0.1 | ) | (0.5 | ) | (0.2 | ) | 0.4 | (0.3 | ) | |||||||||||

| Total loss and loss expenses | 77.0 | 68.9 | 71.7 | 8.1 | (2.8 | ) | ||||||||||||||

| Underwriting expenses | 32.2 | 32.8 | 32.8 | (0.6 | ) | 0.0 | ||||||||||||||

| Combined ratio | 109.2 | % | 101.7 | % | 104.5 | % | 7.5 | (2.8 | ) | |||||||||||

| Combined ratio: | 109.2 | % | 101.7 | % | 104.5 | % | 7.5 | (2.8 | ) | |||||||||||

| Contribution from catastrophe losses and prior years reserve development | 4.0 | (4.7 | ) | (0.5 | ) | 8.7 | (4.2 | ) | ||||||||||||

| Combined ratio before catastrophe losses and prior years reserve development | 105.2 | % | 106.4 | % | 105.0 | % | (1.2 | ) | 1.4 | |||||||||||

| (Dollars in millions) | Years ended December 31, | 2014-2013 | 2013-2012 | |||||||||||||||

| 2014 | 2013 | 2012 | Change % | Change % | ||||||||||||||

| Earned premiums | $ | 4,045 | $ | 3,713 | $ | 3,344 | 9 | 11 | ||||||||||

| Fee revenues | 6 | 4 | 6 | 50 | (33 | ) | ||||||||||||

| Total revenues | 4,051 | 3,717 | 3,350 | 9 | 11 | |||||||||||||

| Loss and loss expenses from: | ||||||||||||||||||

| Current accident year before catastrophe losses | 2,495 | 2,249 | 2,160 | 11 | 4 | |||||||||||||

| Current accident year catastrophe losses | 230 | 199 | 373 | 16 | (47 | ) | ||||||||||||

| Prior accident years before catastrophe losses | (72 | ) | (120 | ) | (357 | ) | 40 | 66 | ||||||||||

| Prior accident years catastrophe losses | (26 | ) | (27 | ) | (39 | ) | 4 | 31 | ||||||||||

| Total loss and loss expenses | 2,627 | 2,301 | 2,137 | 14 | 8 | |||||||||||||

| Underwriting expenses | 1,238 | 1,183 | 1,076 | 5 | 10 | |||||||||||||

| Underwriting profit | $ | 186 | $ | 233 | $ | 137 | (20 | ) | 70 | |||||||||

| Ratios as a percent of earned premiums: | Pt. Change | Pt. Change | ||||||||||||||||

| Current accident year before catastrophe losses | 61.7 | % | 60.6 | % | 64.6 | % | 1.1 | (4.0 | ) | |||||||||

| Current accident year catastrophe losses | 5.7 | 5.4 | 11.1 | 0.3 | (5.7 | ) | ||||||||||||

| Prior accident years before catastrophe losses | (1.8 | ) | (3.3 | ) | (10.7 | ) | 1.5 | 7.4 | ||||||||||

| Prior accident years catastrophe losses | (0.6 | ) | (0.8 | ) | (1.1 | ) | 0.2 | 0.3 | ||||||||||

| Total loss and loss expense | 65.0 | 61.9 | 63.9 | 3.1 | (2.0 | ) | ||||||||||||

| Underwriting expense | 30.6 | 31.9 | 32.2 | (1.3 | ) | (0.3 | ) | |||||||||||

| Combined ratio | 95.6 | % | 93.8 | % | 96.1 | % | 1.8 | (2.3 | ) | |||||||||

| Combined ratio: | 95.6 | % | 93.8 | % | 96.1 | % | 1.8 | (2.3 | ) | |||||||||

Contribution from catastrophe losses and prior years reserve development | 3.3 | 1.3 | (0.7 | ) | 2.0 | 2.0 | ||||||||||||

Combined ratio before catastrophe losses and prior years reserve development | 92.3 | % | 92.5 | % | 96.8 | % | (0.2 | ) | (4.3 | ) | ||||||||

| Years ended December 31, | 2011-2010 | 2010-2009 | ||||||||||||||||||

| (Dollars in millions) | 2011 | 2010 | 2009 | Change % | Change % | |||||||||||||||

| Agency renewal written premiums | $ | 2,867 | $ | 2,692 | $ | 2,665 | 7 | 1 | ||||||||||||

| Agency new business written premiums | 437 | 414 | 405 | 6 | 2 | |||||||||||||||

| Other written premiums | (206 | ) | (143 | ) | (159 | ) | (44 | ) | 10 | |||||||||||

| Net written premiums | 3,098 | 2,963 | 2,911 | 5 | 2 | |||||||||||||||

| Unearned premium change | (69 | ) | (39 | ) | 0 | (77 | ) | nm | ||||||||||||

| Earned premiums | $ | 3,029 | $ | 2,924 | $ | 2,911 | 4 | 0 | ||||||||||||

| (Dollars in millions) | Years ended December 31, | 2014-2013 | 2013-2012 | |||||||||||||||

| 2014 | 2013 | 2012 | Change % | Change % | ||||||||||||||

| Agency renewal written premiums | $ | 3,794 | $ | 3,493 | $ | 3,138 | 9 | 11 | ||||||||||

| Agency new business written premiums | 503 | 543 | 501 | (7 | ) | 8 | ||||||||||||

| Other written premiums | (154 | ) | (143 | ) | (157 | ) | (8 | ) | 9 | |||||||||

| Net written premiums | 4,143 | 3,893 | 3,482 | 6 | 12 | |||||||||||||

| Unearned premium change | (98 | ) | (180 | ) | (138 | ) | 46 | (30 | ) | |||||||||

| Earned premiums | $ | 4,045 | $ | 3,713 | $ | 3,344 | 9 | 11 | ||||||||||

We individually list declared catastrophe events for which our incurred losses reached or exceeded $10 million.

| (In millions, net of reinsurance) | Excess | |||||||||||||||||||||||

| Commercial | Personal | and surplus | ||||||||||||||||||||||

| Dates | Event | Region | lines | lines | lines | Total | ||||||||||||||||||

| 2011 | ||||||||||||||||||||||||

| Jan. 31-Feb. 3 | Freezing, wind | South, Midwest | $ | 4 | $ | 3 | $ | - | $ | 7 | ||||||||||||||

| Feb. 21 | Earthquake | New Zealand | 4 | - | - | 4 | ||||||||||||||||||

| Feb. 27-28 | Hail, wind, tornado | Midwest | 3 | 6 | - | 9 | ||||||||||||||||||

| Mar. 11 | Earthquake | Japan | 7 | - | - | 7 | ||||||||||||||||||

| Mar. 26-28 | Hail, wind | South | 1 | 6 | - | 7 | ||||||||||||||||||

| Apr. 3-5 | Hail, wind, tornado | South, Midwest | 15 | 23 | - | 38 | ||||||||||||||||||

| Apr. 8-11 | Hail, wind, tornado | South, Midwest | 11 | 8 | - | 19 | ||||||||||||||||||

| Apr. 14-16 | Hail, wind, tornado | South, Midwest | 10 | 4 | - | 14 | ||||||||||||||||||

| Apr. 19-20 | Hail, wind | South, Midwest | 13 | 11 | - | 24 | ||||||||||||||||||

| Apr. 22-28 | Hail, wind, tornado | South, Midwest | 45 | 31 | - | 76 | ||||||||||||||||||

| May 20-27 | Hail, wind, tornado | South, Midwest | 42 | 51 | - | 93 | ||||||||||||||||||

| May 29-Jun. 1 | Hail, wind, tornado | East, Midwest | 2 | 1 | - | 3 | ||||||||||||||||||

| Jun. 16-22 | Hail, wind, tornado | South, Midwest | 7 | 6 | - | 13 | ||||||||||||||||||

| Jul. 1-4 | Hail, wind, tornado | Midwest | 3 | 2 | - | 5 | ||||||||||||||||||

| Jul. 10-14 | Hail, wind, tornado | Midwest, West | 4 | 6 | - | 10 | ||||||||||||||||||

| Aug. 18-19 | Hail, wind, tornado | Midwest | 9 | 1 | - | 10 | ||||||||||||||||||

| Aug. 26-28 | Hurricane, wind, tornado | East | 22 | 6 | - | 28 | ||||||||||||||||||

| Sep. 3-6 | Tornado, wind | South | 9 | 5 | - | 14 | ||||||||||||||||||

| All other 2011 catastrophes | 14 | 11 | 1 | 26 | ||||||||||||||||||||

| Development on 2010 and prior catastrophes | 2 | (7 | ) | - | (5 | ) | ||||||||||||||||||

| Calendar year incurred total | $ | 227 | $ | 174 | $ | 1 | $ | 402 | ||||||||||||||||

| 2010 | ||||||||||||||||||||||||

| Jan. 7-12 | Freezing, wind | South, Midwest | $ | 4 | $ | 1 | $ | - | $ | 5 | ||||||||||||||

| Feb. 9-11 | Freezing, wind | East, Midwest | 4 | 1 | - | 5 | ||||||||||||||||||

| Apr. 4-6 | Hail, wind, tornado | South, Midwest | 4 | 6 | - | 10 | ||||||||||||||||||

| Apr. 30 - May 3 | Hail, wind, tornado | South | 21 | 6 | - | 27 | ||||||||||||||||||

| May 7-8 | Hail, wind, tornado | East, Midwest | 2 | 12 | - | 14 | ||||||||||||||||||

| May 12-16 | Hail, wind, tornado | South, Midwest | 7 | 2 | - | 9 | ||||||||||||||||||

| Jun. 4-6 | Hail, wind, tornado | Midwest | 2 | 2 | 1 | 5 | ||||||||||||||||||

| Jun. 17-20 | Hail, wind, tornado | Midwest, West | 5 | 3 | - | 8 | ||||||||||||||||||

| Jun. 21-24 | Hail, wind, tornado | Midwest | 2 | 3 | - | 5 | ||||||||||||||||||

| Jun. 25-28 | Hail, wind, tornado | Midwest | 3 | 5 | - | 8 | ||||||||||||||||||

| Jun. 30 - Jul. 1 | Hail, wind | West | 4 | 4 | - | 8 | ||||||||||||||||||

| Jul. 20-23 | Hail, wind, tornado | Midwest | 12 | 4 | - | 16 | ||||||||||||||||||

| Oct. 4-6 | Hail, wind | South | 6 | 1 | - | 7 | ||||||||||||||||||

| Oct. 26-28 | Hail, wind, tornado | Midwest | 6 | 4 | - | 10 | ||||||||||||||||||

| All other 2010 catastrophes | 19 | 9 | - | 28 | ||||||||||||||||||||

| Development on 2009 and prior catastrophes | (12 | ) | (5 | ) | - | (17 | ) | |||||||||||||||||

| Calendar year incurred total | $ | 89 | $ | 58 | $ | 1 | $ | 148 | ||||||||||||||||

| 2009 | ||||||||||||||||||||||||

| Jan. 26-28 | Freezing | South, Midwest | $ | 5 | $ | 14 | $ | - | $ | 19 | ||||||||||||||

| Feb. 10-13 | Hail, wind | South, Midwest | 13 | 25 | - | 38 | ||||||||||||||||||

| Feb. 18-19 | Hail, wind | South | 1 | 8 | - | 9 | ||||||||||||||||||

| Apr. 9-11 | Hail, wind | South, Midwest | 13 | 21 | - | 34 | ||||||||||||||||||

| May 7-9 | Hail, wind | South, Midwest | 9 | 13 | - | 22 | ||||||||||||||||||

| Jun. 2-6 | Hail, wind | South, Midwest | 3 | 4 | - | 7 | ||||||||||||||||||

| Jun. 10-18 | Hail, wind | South, Midwest | 7 | 4 | - | 11 | ||||||||||||||||||

| Sep. 18-22 | Hail, wind | South | 3 | 4 | - | 7 | ||||||||||||||||||

| All other 2009 catastrophes | 12 | 13 | - | 25 | ||||||||||||||||||||

| Development on 2008 and prior catastrophes | (12 | ) | 5 | - | (7 | ) | ||||||||||||||||||

| Calendar year incurred total | $ | 54 | $ | 111 | $ | - | $ | 165 | ||||||||||||||||

| (Dollars in millions, net of reinsurance) | Excess | |||||||||||||||||

| Commercial | Personal | and surplus | ||||||||||||||||

| Dates | Events | Regions | lines | lines | lines | Total | ||||||||||||

| 2014 | ||||||||||||||||||

| Jan. 5-8 | Freezing, ice, snow, wind | Midwest, Northeast, South | $ | 45 | $ | 24 | $ | 1 | $ | 70 | ||||||||

| Apr. 27-May 1 | Flood, hail, wind | Midwest, Northeast, South | 4 | 9 | — | 13 | ||||||||||||

| May 10-13 | Flood, hail, wind | Midwest | 6 | 7 | — | 13 | ||||||||||||

| May 18-19 | Flood, hail, wind | Midwest, South, West | 23 | 19 | 1 | 43 | ||||||||||||

| Jun. 3-4 | Flood, hail, wind | Midwest | 9 | 1 | — | 10 | ||||||||||||

| All other 2014 catastrophes | 48 | 32 | 1 | 81 | ||||||||||||||

| Development on 2013 and prior catastrophes | (15 | ) | (11 | ) | — | (26 | ) | |||||||||||

| Calendar year incurred total | $ | 120 | $ | 81 | $ | 3 | $ | 204 | ||||||||||

| 2013 | ||||||||||||||||||

| Mar. 18-19 | Hail, wind | South | $ | 4 | $ | 7 | $ | — | $ | 11 | ||||||||

| Apr. 7-11 | Hail, lightning, wind | Midwest, West | 12 | 10 | — | 22 | ||||||||||||

| Apr. 16-19 | Hail, lightning, wind | Midwest | 5 | 6 | — | 11 | ||||||||||||

| May. 18-20 | Hail, lightning, wind | Midwest, Northeast, South | 9 | 1 | — | 10 | ||||||||||||

| May. 28-29 | Hail, lightning, wind | South | 8 | 2 | 1 | 11 | ||||||||||||

| Jun. 24-26 | Hail, lightning, wind | Midwest, Northeast | 5 | 6 | — | 11 | ||||||||||||

| Jul. 9-11 | Hail, lightning, wind | Midwest, Northeast | 5 | 6 | — | 11 | ||||||||||||

| Jul. 23-24 | Hail, lightning, wind | Midwest, South | 14 | 4 | — | 18 | ||||||||||||

| Aug. 6-7 | Hail, lightning, wind | Midwest | 6 | 9 | — | 15 | ||||||||||||

| Nov. 17-18 | Hail, lightning, wind | Midwest, South | 18 | 17 | — | 35 | ||||||||||||

| All other 2013 catastrophes | 28 | 16 | — | 44 | ||||||||||||||

| Development on 2012 and prior catastrophes | (17 | ) | (10 | ) | — | (27 | ) | |||||||||||

| Calendar year incurred total | $ | 97 | $ | 74 | $ | 1 | $ | 172 | ||||||||||

| 2012 | ||||||||||||||||||

| Feb. 28-29 | Hail, tornado, wind | Midwest | $ | 19 | $ | 6 | $ | — | $ | 25 | ||||||||

| Mar. 2-3 | Hail, tornado, wind | Midwest, South | 30 | 48 | — | 78 | ||||||||||||

| Apr. 28-29 | Hail, lightning, wind | Midwest, South | 53 | 26 | 1 | 80 | ||||||||||||

| Jun. 28-Jul. 2 | Hail, lightning, wind | Midwest, Northeast, South | 39 | 42 | — | 81 | ||||||||||||

| Jul. 2-4 | Hail, lightning, wind | Midwest, Northeast | 7 | 5 | — | 12 | ||||||||||||

| Oct. 28-31 | Sandy | Midwest, Northeast, South | 20 | 10 | — | 30 | ||||||||||||

| All other 2012 catastrophes | 43 | 23 | 1 | 67 | ||||||||||||||

| Development on 2011 and prior catastrophes | (17 | ) | (22 | ) | — | (39 | ) | |||||||||||

| Calendar year incurred total | $ | 194 | $ | 138 | $ | 2 | $ | 334 | ||||||||||

| (Dollars in millions) | ||||||||||||||||||||||||

| Accident year loss and loss expenses incurred and ratios to earned premiums: | ||||||||||||||||||||||||

| Accident Year: | 2011 | 2010 | 2009 | 2011 | 2010 | 2009 | ||||||||||||||||||

| as of December 31, 2011 | $ | 2,620 | $ | 2,140 | $ | 2,050 | 86.4 | % | 73.2 | % | 70.4 | % | ||||||||||||

| as of December 31, 2010 | 2,319 | 2,084 | 79.2 | 71.6 | ||||||||||||||||||||

| as of December 31, 2009 | 2,274 | 78.1 | ||||||||||||||||||||||

| (Dollars in millions) | |||||||||||||||||||||

| Accident year loss and loss expenses incurred and ratios to earned premiums: | |||||||||||||||||||||

| Accident year: | 2014 | 2013 | 2012 | 2014 | 2013 | 2012 | |||||||||||||||

| as of December 31, 2014 | $ | 2,725 | $ | 2,391 | $ | 2,416 | 67.4 | % | 64.4 | % | 72.3 | % | |||||||||

| as of December 31, 2013 | 2,448 | 2,431 | 66.0 | 72.7 | |||||||||||||||||

| as of December 31, 2012 | 2,533 | 75.7 | |||||||||||||||||||