| “VOD” refers to video on demand, which includes near video on demand (“ |

| “WFOE” refers to Beijing China Broadband Network Technology Co., Ltd., a PRC company and a “wholly foreign-owned enterprise,” which we previously wholly owned and which was sold during the quarter ended March 31, 2014; |

| “YOD Hong Kong” refers to YOU On Demand (Asia) Limited, formerly Sinotop Group Limited, a Hong Kong company, which is wholly- owned by CB Cayman; |

| “YOD WFOE” refers to YOU On Demand (Beijing) Technology Co., Ltd., a PRC company and a “wholly foreign-owned enterprise,” which is wholly-owned by YOD Hong Kong; and |

| “ |

iii

PART I

ITEM 1.

| BUSINESS |

Overview

Ideanomics, Inc. (“Ideanomics” or the “Company”) (Nasdaq: IDEX) was incorporated in the State of Nevada on October 19, 2004. From 2010 through 2017, our primary business activities have beenwere providing premium content video on demand (“VOD”) services, with primary operations in the PRC, through our subsidiaries and variable interest entities (“VIEs”) under the brand name You-on-Demand (“YOD”YOD.”). In our We closed the YOD business we provide premium content and integrated value-added service solutions for the delivery of VOD and paid video programming to digital cable providers, Internet protocol television (“IPTV”) providers, Over-the-Top (“OTT”) streaming providers, mobile manufacturers and operators, as well as direct customers.

during 2019.

Starting in early 2017, while continuing to support our YOD business, we began transitioning ourthe Company transitioned its business model to become a next-generation financial technology (“fintech”) company, with the intention of offering customized products and services based on best-in-class blockchain, artificial intelligence (“AI”) and other technologies to mature and emerging businesses across various industries. To do so, we are building a technology ecosystem through license agreements, joint ventures and strategic acquisitions, which we refer to as our “Fintech Ecosystem.” In parallel, through strategic acquisitions, equity investments and joint ventures, we are buildingcompany. The Company built a network of businesses, operating across industry verticals,principally in the trading of petroleum products and electronic components that we believe havethe Company believed had significant potential to recognize benefits from blockchain and AIartificial intelligence (“AI”) technologies including for example, enhancing operations, addressing cost inefficiencies, improving documentation and standardization, unlocking asset value and improving customer engagement. During 2018, the Company ceased operations in the petroleum products and electronic components trading businesses and disposed of the businesses during 2019. As we looked to deploy fintech solutions in late 2018 and into 2019, we identified a unique opportunity in the Chinese Electric Vehicle (“EV”) industry to facilitate large scale conversion of fleet vehicles from internal combustion engines to EV. This led us to establish our Mobile Energy Global (“MEG”) business unit. Fintech continues to be a sector of interest to us as we look to invest in and develop businesses that can improve the financial services industry, particularly as it relates to deploying blockchain and AI technologies.

Principal Products or Services and Their Markets

Our coreOverview

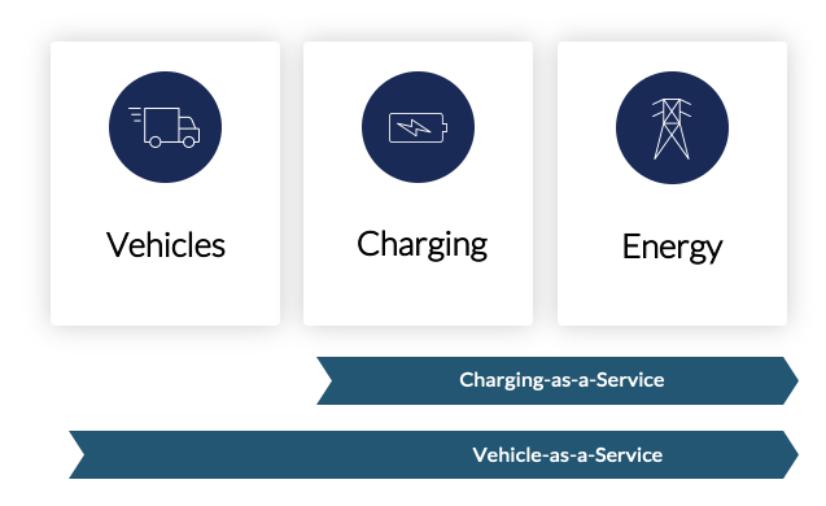

Ideanomics Mobility

Ideanomics Mobility is driving EV adoption by assembling a synergistic ecosystem of subsidiaries and investments across the 3 key pillars of EV: Vehicles, Charging, and Energy. These three pillars provide the foundation for Ideanomics Mobility’s planned offering of unique business strategysolutions such as Charging as a Service (“CaaS”) and Vehicle as a Service (“VaaS.”)

2

Each operating company within Ideanomics Mobility offers its own unique products and participates in a shared services ecosystem fulfilling Ideanomics’ Sales-to-Financing-to-Charging (“S2F2C”) model, with centralized supply chain operations and marketing expertise designed to accelerate growth and business opportunities across the group.

The combination of products from within its subsidiaries and investments, coupled with Ideanomics Mobility’s shared services, will provide the Company with the opportunity to bring to market unique business solutions intended to drive commercial fleet electrification such as Charging-as-a-Service and Vehicle-as-a-Service. These solutions offer fleet operators an opportunity to benefit from an OpEx-driven model which lowers the barrier to entry for the adoption of zero emissions fleets.

The Company believes that the EV market is poised for rapid growth. Bloomberg NEF estimates that global commercial EV sales will reach 1.2 million units in 2023. The global EV charging infrastructure market is expected to grow at a compound annual growth rate of 33.4% from 2021 to 2028 to $144.97 billion. President Biden’s administration is supportive of EV with a goal to achieve a 100% clean-energy economy and states such as California have accelerated timelines to phase out internal combustion engine (“ICE”) vehicles.

Ideanomics Mobility’s mission is to promoteleverage its ecosystem of synergistic operating companies to generate efficiencies and increase business opportunities across the group. With a diverse commercial EV product offering, the company plans to use developmentEV and advancementEV battery sales and financing solutions to attract commercial fleet operators that will generate large scale demand for energy. The Company operates as an end-to-end solutions provider for the procurement, financing, charging and energy management needs for fleet operators of blockchain-commercial EV. Ideanomics Mobility focuses on commercial EV rather than passenger personal EV, as commercial EV is on an accelerated adoption path when compared to consumer EV adoption – which is expected to take between ten to fifteen years. We focus on four distinct commercial vehicle types with supporting income streams: 1) Closed-area heavy commercial, in sectors such as Mining, Airports, and AI-based technologies,Sea Ports 2) Last-mile delivery light commercial 3) Buses and Coaches 4) Taxis. The vehicle financing solutions (such as purchase or leasing) would generate fee-based revenues whereas the charging and energy management would yield recurring revenue streams.

Ideanomics Mobility’s revenues are generated from its S2F2C operating model. The Company’s planned EV revenues will come from the sale of EVs under our positioningMedici Motor Works and Treeletrik brands outside of the China and within China through our MEG operating units sale of other manufacturers vehicles and batteries.

The Company’s presence in the fintech industry overall,China market creates a deep knowledge of the logistics and supply chain for the manufacture of EVs, batteries and related components; this in turn enables the sourcing of high quality components at competitive prices for the Company’s operations outside of China.

Within the Ideanomics Mobility business unit there are four operating companies:

Mobile Energy Global (“MEG”)

The Company’s MEG business operates in China where government clean air regulations and subsidy programs provide a strong impetus for the adoption of commercial EV. The Company competes in China using its S2F2C. Using this model the Company helps the customer find the best vehicle for its needs and earns fees for every completed sale; revenue is derived from the spread between group buying of vehicles and price sold, fees for the arrangement of financing, and payments from subsequent charging and energy management.

Tree Technologies Sdn. Bhd. (“Tree Technologies”)

Tree Technologies is headquartered in Kuala Lumpur, Malaysia and through its Treeletrik brand sells EV bikes, scooters, and batteries throughout the ASEAN region. Two-wheel bikes and scooters form a large part of the transport infrastructure in the ASEAN region; according to Deloitte Consulting, there were 13.7 million motor bikes sold in the six major ASEAN countries in 2019. Environmental regulations in the ASEAN region help accelerate the adoption of EV bikes. The Company has also started to import Treeletrik brand EV bikes into the United States.

3

Medici Motor Works

Medici Motor Works plans to sell its own brand vehicles in the United States, Latin America and Europe. Presently, the Company is working with manufacturers based in China to design and build trucks, buses and closed-area vehicles for mining, airports and seaports.

Solectrac, Inc. (“Solectrac”)

On October 21, 2020 the Company acquired 15%, and on November 23, 2020 the Company subsequently increased its ownership to 24% in California-based Solectrac, Inc. Solectrac develops, assembles and distributes 100% battery-powered electric tractors—an alternative to diesel tractors—for agriculture and utility operations.

According to Research And Markets, the global agricultural tractor market is currently valued at $75 billion, with the North American agricultural tractor market expected to reach $20 billion by bringing technology leaders together with industry leaders2023. The largest segment for agricultural tractors is the below-40HP segment, where Solectrac's initial three models address the broad needs of the market. Its tractors are specifically designed to serve the needs of community-based farms, vineyards, orchards, equestrian arenas, greenhouses, and creating synergies betweenhobby farms.

Founded in 2012 to take electric tractors into commercial production, Solectrac was incorporated as a California Benefit Corp in 2019. It has received grants from the businesses in our expanding Fintech EcosystemIndian U.S. Science and Technology Fund and the businessesNational Science Foundation. In 2020, Solectrac received the World Alliance Solar Impulse Efficient Solutions label from the Solar Impulse Foundation. The label was awarded for being one of the one thousand most efficient and profitable solutions that can transition society to being economically viable while being environmentally sustainable.

Recent Developments Since December 31, 2020

Since December 31, 2020 the Company has completed a number of transactions that have expanded the scope of the Company’s EV activities.

WAVE

On January 15, 2021 acquired 100% of privately held Wireless Advanced Vehicle Electrification, Inc. ("WAVE.")

Founded in our network2011, and headquartered in Salt Lake City, Utah, WAVE is a leading provider of industry verticals, which we referinductive (wireless) charging solutions for medium and heavy-duty EVs. Embedded in roadways and depot facilities, the WAVE system automatically charges vehicles during scheduled stops. The hands-free WAVE system eliminates battery range limitations and enables fleets to as our “Industry Ventures.” Specifically, we believeachieve driving ranges that match that of internal combustion engines.

Deployed since 2012, WAVE has demonstrated the technologies being developedcapability to develop and integrate high-power charging systems into heavy-duty EVs from leading commercial EV manufacturers. With commercially available wireless charging systems up to 250kW and higher power systems in our Fintech Ecosystem can be customizeddevelopment, WAVE provides custom fleet solutions for mass transit, logistics, airport and leveragedcampus shuttles, drayage fleets, and off-road vehicles at ports and industrial sites.

Wireless charging systems offer several compelling benefits over plug-in-based charging systems, including reduced maintenance, improved health and safety, and expedited energy connection and are important to address various use cases presented by our Industry Ventures, which we believe will not only enhance the performancedeployment of our Industry Ventures, butautonomous driving vehicles. Furthermore, wireless in-route charging enables greater route lengths or smaller batteries while also enhancemaintaining battery life, thereby reducing costs for fleet operators. WAVE customers include what is currently the capabilitieslargest EV bus system in the U.S., the Antelope Valley Transit Authority, and its partnerships include Kenworth, Gillig, BYD, Complete Coach Works and the Department of our Fintech Ecosystem. For example, in 2017, we acquired a crude oil trading businessEnergy.

Energica Motor Company, S.P.A. (“Energica”)

On March 3, 2021 the Company purchased 20% of Energica, the world's leading manufacturer of high-performance electric motorcycles and a consumer electronics trading businessthe sole manufacturer of the FIM Enel MotoE™ World Cup. Energica has combined zero emission EV technology with the goalpedigree of gaining experiencehigh-performance mobility synonymous with Italy’s Motor Valley to create a range of exceptional products for the high-performance motorcycle market. To support its products, it has developed proprietary EV battery and DC fast-charging in-house that has applications and synergies with Ideanomics’ broader interests in the traditional logistics managementglobal EV sector.

4

Silk EV Cayman LP (“Silk”)

On January 28, 2021, the Company invested $15.0 million in Silk EV via a promissory note. Silk is an Italian engineering and financing business,design services company that has recently partnered with FAW to form a new company (Silk-FAW) to produce fully electric, luxury vehicles for the Chinese and Global auto markets. Silk-FAW has exclusive rights to develop Hongqi-S brand high-end electric sports cars. The Hongqi brand is the most well-known luxury auto brand in China. Silk-FAW vehicles are being designed in Italy’s Motor Valley and is attracting talent from the luxury and high-performance auto market. Partnering with Silk provides access to Silk-FAW’s Innovation Centers providing an initial use case for technologies in our Fintech Ecosystem,us insight into technological advancements and enabling the application of our learning from operating these businessesall best-in-breed technology evaluated at those centers to support the development of an AI-high-performance sportscars (battery tech, power management systems, high performance motors.)

Ideanomics Capital

Ideanomics Capital is the Company's fintech business unit, which focuses on leveraging technology and blockchain-enabledinnovation to improve efficiency, transparency, and profitability for the financial services industry.

Technology Metals Market Limited (“TM2”)

TM2 is a London based digital commodities issuance and trading platform for more efficient logistics managementtechnology metals. It connects institutional investors, proprietary traders and finance generally.

We referretail investors with metals suppliers – miners, refiners, recyclers and mints. The platform focuses specifically on new metals that currently don’t have an active trading marketplace, such as rhodium, lithium, cobalt, rhenium, etc. The Company’s ownership interest in TM2 provides valuable data and insight into the global technology metals market, which is critical to our YOD business as our legacy YOD segment and all our other operations, including the development of our Fintech Ecosystem and our Industry Ventures, as our Wecast Services segment, to suggest the wide net we are casting in identifying promising technologies and use cases for operations as a next-generation fintech company. The commodities trading componentfuture of the logistics managementCleantech and financing businesses we acquiredEV industries. TM2 connects both pillars of Cleantech and Fintech. The types of metals and materials traded on the TM2 platform are critical to Cleantech (for EV battery production, energy storage systems, solar cells, etc.,) while the Fintech platform is innovative in 2017 provided 99.7%representing these commodities which do not exist on traditional exchanges.

On January 28, 2021, the Company entered into a simple agreement for future equity with TM2 pursuant to which Ideanomics invested $2.1 million. This investment is a follow-on investment further the Company’s prior investment of our revenue$1.2 million in stock-based consideration in December 2019.

Delaware Board of Trade (“DBOT”)

The Delaware Board of Trade (“DBOT”) is a broker dealer that also operates an Alternative Trading System (“ATS,”) presently DBOT is not trading; the business remains in full regulatory compliance. Recent developments have pointed to increased recognition of digital securities’ relevance in regulated global capital markets. As well, regulatory easing of certain restrictions such as the threshold for private securities (Reg A+), along with good demand for products such as pre-IPO issuance, provide good tailwind for the year ended December 31, 2018. As we further develop our FinTech services business and this business continues to mature, we have been gradually phasing out of our logistics management and financing businessbroker dealers business. The Company has filed a continuing membership application for strategic reasons, as further describedprivate placement activities in the Management Discussion and Analysis. During the fourth quarter of 2018 we began experiencing marketprimary markets. The Company believes that growing demand for non-logistics management revenue generating opportunitiesprivate placements, along with increased attention in digital securities, provide a favorable environment for DBOT’s future growth.

Timios

On January 8, 2021 the Company acquired 100% of privately-held Timios Holdings Corp. ("Timios.") Timios, a nationwide title and have begun focusing our efforts on these new market FinTechescrow services opportunities, while phasing out of the oil tradingprovider, which has been expanding in recent years through offering innovative and electronics trading businesses. These new FinTech services market opportunities are in line with our FinTech Ecosystem and Industry Ventures strategy. While we intend to continue to capitalize on our efforts and learnings from the overall logistics management business it is not intended to be our core business. Various other aspects of the development of our Fintech Ecosystem and our Industry Ventures, as described below, are still in the planning and testing phase and are generally not operational or revenue generating.

Fintech Ecosystem

We primarily rely upon third-party intellectual property (“IP”) for the AI and blockchain technology being developed for our Wecast Services segment. In evaluating prospective technologies we seek to acquire, in-license or promote through joint ventures, we are focused on identifying industry leaders with strong and established engineering teams and technologies that are substantially developed. In doing so, we believe we can reduce the risks of reliance on a single technology with speculative functionality and adoption potential, while enhancing our flexibility and adaptability in a rapidly evolving technological environment.

Our strategy is to leverage the technology and teams that comprise our Fintech Ecosystem to create customizedfreedom-of-choice-friendly solutions for the use cases presented to us by our Industry Ventures.real estate transactions. The customization of these business applications would be undertaken by our acquired subsidiaries or the joint ventures, as applicable, with the business development efforts of our parent company focused on expanding the network of technologies in our Fintech Ecosystemproducts include residential and facilitating other synergies between our Fintech Ecosystemcommercial title insurance, closing and our Industry Ventures. While the development and expansion of our Fintech Ecosystem is primarily driven by a desire to match specific technologies with specific use applications in our Industry Ventures, we believe that many of the technologies in our Fintech Ecosystem will have applications outside of our own Industry Ventures, and that the work in customizing technology to our Industry Ventures can be leveraged to develop products and services for third parties.

BDCG Joint Venture

Between December 2017 and April 2018, we formed BBD Digital Capital Group Ltd., a New York corporation (“BDCG”), as a joint venture with management partner Seasail, an affiliate of Big Business Data (“BBD”). We hold approximately 60% of the equity interest of BDCG and have the power to appoint three of the five directors of the board of BDCG. BDCG intends to capitalize on commodity and energy providers’ needs for more precise risk management services, more informed operational planning and more strategic decision-making, specifically in the trading of index funds, futures and commodities. BDCG focuses on developing AI-driven financial datasettlement services, as well as building transactional platformsspecialized offerings for index, futuresthe mortgage process industry.

Ideanomics expects that Timios will become one of the cornerstones of Ideanomics Capital. Timios combines difficult to obtain local and derivativestate licenses, a knowledgeable and experienced team, and a scalable platform to deliver best-in-class services through both centralized processing and localized branch networks. Ideanomics will assist Timios in scaling its business in various ways, including referring client acquisitions and product innovation.

Founded in 2008 by real estate industry veteran Trevor Stoffer, Timios' vision is to bring transparency to real estate transactions. The company offers title and settlement, appraisal management, and real-estate-owned (“REO”) title and closing services in 44 states and currently serves more than 280 national and regional clients.

5

Non-Core Assets

The Company has identified a number of business units that it considers non-core and is evaluating strategies for divesting these assets. The non-core assets are Grapevine, a marketing and ecommerce platform focused on influencer marketing, and FinTech Village a 58-acre development site in West Hartford, Connecticut.

On January 28, 2021, the Company’s Board of Directors accepted an offer of $2.75 million for Fintech Village, and subsequently signed a non-binding sale contract on March 15, 2021. The Company believes that Fintech Village met the criteria for held for sale classification on January 28, 2021.

Sources and Availability of Raw Materials

The Company’s Tree Technologies business located in Malaysia and its WAVE business located in Utah, United States, (acquired in the first quarter of 2021 – see Recent Developments section) assemble and manufacture motor bikes and inductive charging systems respectively. These businesses depend on a ready supply of components that are sourced domestically and internationally and any interruption to the supply of components could have an adverse impact on the Company’s results. The Company’s suppliers that manufacture EVs and batteries depend on a ready supply of raw materials and components, consequently a shortage of raw materials or components could adversely impact their manufacturing process and, potentially, impact the Company’s revenues as it may not be able to complete orders that it had received. The Company may also be adversely impacted if global logistic and supply chains are interrupted.

Seasonality

The Company expects that orders and sales will be influenced by the amount and timing of budgeted expenditure by its customers. Typically, the Company would expect to see higher sales at the start of the year when companies start executing on their capital programs and at the end of the year when companies are spending any surplus or uncommitted budget before the new budget cycle commences. The Company’s operating businesses are in the early stage of their development and consequently do not have sufficient trading histories to project seasonal buying patterns with any degree of confidence.

Working Capital Requirements

As the Company expands its business the need for both global commodity and energy clients. Planned financial data services also include risk management solutions, platforms for trading derivatives and indices, and debt and credit product offerings,working capital will continue to grow. From time to time the Company’s MEG operating division in China has the opportunity to purchase a large number of vehicles at a favorable price, the terms of the purchase contract frequently require the Company to pay some or all of the cost in advance of the delivery of the vehicles with the primary objective being enhancing trading and risk management strategies.

BDCG leverages Pluto, Seasail’s AI technology, which Seasail licensesresultant need to BDCG.Pluto takes in dynamic, multi-variable inputs, such as, in the casecommit material amounts of crude oil, information regarding trading, production origination, economic data and weather,and processes them according to flexible programmed models. For debt and credit products, BDCG has focused on data collection and integration capabilities based on “massive public data” and “acquired third-party data,” including credit and multi-party loans. BBD has accumulated the information of over 100 million companies. Such information contains more than 150 data tables and over 3,700 data fields, and the amount of data continues to grow rapidly. BDCG can use the data accumulated by BBD to create risk and index models. Once these models are layered into a rating and risk management system and loan approval system for trade finance, the AI system can make informed recommendations as to trading and risk management. Pluto is then sold and licensed to third party financial product stakeholders for these services.

We believe we can leverage BDCG’s AI services for the creation of financial products, risk ratings and indexing, and selection and recommendation systems on behalf of key stakeholders. By using AI technology to analyze the digital securitized assets we intend to develop, we aim to elevate not only the quality of the financial product, but also interactions amongstakeholders. We also intend to design thedigital securitized assets we develop to have data attributes that can be integrated into BDCG’s approach for processing financial data.

Fundamental Interactions

In June 2018, we entered into a non-exclusive, royalty-bearing licensing agreement with Fundamental Interactions, Inc. (“FI”), which currently expires on June 25, 2021, with respect to certain blockchain technologies, including FI’s Velocity Ledger, a blockchain-based, software-as-a-service (SaaS) platform that operates as a private blockchain solution for financial services. Through this agreement, we intend to leverage core FI technology and the Velocity Ledger platformworking capital. The Company’s Tree Technologies subsidiary requires working capital to support the tokenization, secondary tradingassembly of EV motor bikes and settlement of new blockchain-based securities.

FinTalk

In September 2018, we entered into an agreementscooters for the acquisition of FinTalk, a secure mobile messaging, collaborationASEAN market. The Company acquired WAVE and information services platform that delivers encrypted text and media messaging, with high performance large file transfer capabilities.

Industry Ventures

We believe there are a number of industries that can benefit from the application of next-generation technologies, such as blockchain, AI, machine learning and big data. Our strategy is not only to promote the development of promising technologies through our Fintech Ecosystem, but also to acquire, invest in and form joint ventures with businessesSolectrac in the various industries that we believe canfirst quarter of 2021 (see the Recent Developments section), both of these businesses will require working capital to fund the purchase of components for the assembly of wireless charging systems and electric tractors, respectively. The Company will continue to raise both debt and equity capital to support the working capital needs of these businesses and its U.S. Head Office functions.

Trade marks, Patents and Licenses

The Company’s Intelligenta business operates under a license granted by Seasail Ventures Limited (“Seasail.”) The license does not have a stated term.

Customer Concentration

The Company is in the process of building out its Ideanomics Mobility unit and has not yet reached a stage of development where the loss of any single customer would have a material adverse effect on the Company.

Reliance on Government Contracts

The Company does not contract directly with the government of the PRC, however it does have investments, partnerships and agreements with the State Own Entities (“SOE”) described above. Additionally, the rate at which commercial fleets convert to EV is heavily

6

influenced by federal and provincial policies in the PRC as they relate to clean air and adoption of EV technology. Consequently, the Company’s results may be well servedadversely impacted by our Fintech Ecosystem. In so doing, we believe that we can benefit both from growthchanges in regulations in the PRC.

Competitive Business Conditions, Competitive Position in the Industry Ventures themselves, as well as fromand Methods of Competition

Ideanomics Mobility

Purchasers of commercial vehicles have the enhanced potential for monetizing the technologies in our Fintech Ecosystem that would come with refining these technologies for our Industry Ventures.

Logistics Managementchoice between traditional ICE vehicles and Financing

Our first group of Industry Ventures has focused on the logistics managementEVs and financing industry. Logistics managementthis is the component of supply chain management that helps organizations plan, manage and implement processes to store and move goods from origin to destination. Logistics financing supports businesses where the order-to-delivery cycle may not correlate with cash flow needs. We believe that by ensuring that information is transparent, accurate and verifiable at various stages during the shipping process, blockchain-enabled logistics management platforms can streamline and standardize the product flow from sellers to buyers and eliminate standard transactional intermediaries in the freight and shipping industry. Further, we believe that by decreasing middle-man costs, we can greatly improve the efficiency of capital utilization, expand margins and accelerate inventory turnover for companies shipping and ordering goods. In addition, we believe that the transparency and security provided by blockchain technologies, combined with the computing power of AI technologies, can reduce existing logistics financing costs, including by improving risk management and decision making, and enable alternative logistics financing solutions.

To support the development of blockchain- and AI-based technologies for the logistics management and financing industries, we entered the commodities trading business, with the primary goal of learning about the needs of buyers and sellers in industries that rely heavily on the shipment of goods to inform our understanding of the features a blockchain platform would need in order to serve this industry vertical. Specifically, we elected to focus on the crude oil and consumer electronics businesses, which are industries that we estimate are sufficiently commoditized and high volume, in order to (i) serve as meaningful controls, (ii) identify inefficiencies in the logistics management and finance industries and (iii) generate data to support the potential future application of AI solutions.

Our crude oil trading business commenced in October 2017, when we formed our Singapore joint venture, Seven Stars Energy Pte. Ltd. (“SSE”), which is 51% owned by us. The other partner in the joint venture is a businessman based in Singapore with extensive experience in the oil trading industry and ownership or control of several large oil tankers. Our consumer electronics trading business commenced on January 2017, and is operated by our subsidiary Amer Global Technology Limited (“Amer”), in which we have a 55% interest. The end customers in our crude oil and consumer electronics trading businesses include about 15 to 20 corporations across the world. Our crude oil trading business does not currently integrate blockchain- or AI-based logistics solutions.

While we have begun phasing out of the crude oil trading business and the electronics trading business, we intendlikely to continue to capitalize on our efforts and learning from these businesses so that we can leveragefor at least the applications of our technologies and FinTech Ecosystem across this business and as part of our Industry Ventures strategy.

Consumer Digital Products

Our second group of Industry Ventures focuses on consumer digital products. We believe that existing communities of consumers, merchants and service providers can significantly benefit from platforms that leverage blockchain technologies to aggregate content and services and products, such as blockchain-based digital membership cards, digital wallets, and loyalty programs that offer cash or other token-based rewards to users within these communities.

In September 2018, we purchased a 65.65% equity interest in Grapevine Logic Inc. (“Grapevine”), and an affiliate of Dr. Bruno Wu, our Chairman of the Board has an option to require us to acquire the remaining stake in Grapevine. Grapevine is an end-to-end influencer marketing platform that facilitates collaboration between advertisers and brands with video based social influencers and content creators. Through the Grapevine platform, more than 4,700 companies have been able to hire the services of over 177,000 social influencers, ultimately helping these companies to promote their products and strengthen their brand. We believe that Grapevine will help us develop strength in the consumer digital products industry vertical by providing the platform for connecting brands with content-producing influencers and their large-scale audience of consumer-driven followers to whom digital tokens, loyalty and discount cards, multi-purpose digital wallets, and other services may be marketed via Grapevine on behalf of Ideanomics, brand advertisers and influencers, all according to a follower’s areas of interest.

Also in September 2018, we announced the proposed joint venture with Asia Times Holdings (“AT”), a Hong Kong company which owns the Asia Times newspaper, to be named Asia Times Financial Limited (“ATF”). Effective February 20, 2019, the Company and AT agreed to terminate their subscription agreement so that the Company will retain approximately 4.0% interest in AT, and not be obligated to make any further investment into AT. In addition, the parties have agreed to terminate the Shareholder’s Agreement for the joint venture, Asia Times Financial.

Financial Services

As evidenced by the proliferation of offerings of blockchain-based tokens in recentnext five years and the rapid growth of an industry to support these offerings, we believe that a core use case for blockchain and AI technology lies in financial services, digital asset securitization, and blockchain-enabled trading platforms. We plan to provide consulting services to companies seeking financing both through the sales of blockchain based instruments, such as securitized assets represented by digital tokens, which we refer to as “digital securitized assets,” as well as through conventional means, such as sales of traditional equity and debt securities. We believe that this dual approach to financial transactions, coupled with a related AI and blockchain enabled financial services platform, will provide us with flexibility to address the needs of issuers and investors. We also aim to use AI-powered analytics from our technology investments for different use cases, such as the trading, pricing, indexing and ratings of digital tokens (including digital securitized assets). Although we do not yet offer products or services in this industry vertical, we believe that ultimately, the Industry Ventures we form, acquire, or invest in this area will become the core of our business.

DigitalAsset Securitization

We believe that we can use AI- and blockchain-enabled technology to provide a seamless method and platform for the creation and trading of digital securitized assets. Specifically, we plan to facilitate the securitization of tangible and intangible assets, such as data and IP, into new financial products, to “tokenize” these financial products by digitally recording them on a blockchain, to enable advanced platforms and capabilities using AI and blockchain technology, and to support the distribution and monetization of digital securitized assets. In so doing, we can be a leader in the transition of traditional financial products, such as commodities, currencies, credit, leasing, real estate and other asset classes, into the asset digitalization era.

Creating digital securitized assets requires the conversion of illiquid, tangible and intangible assets into blockchain enabled securities that we anticipate will, subject to future regulatory approval, be easily traded via exchanges, and as such, are more liquid than the underlying asset. We refer to this process as “digital asset securitization.”

As a first step in this process, we are identifying and engaging in discussions, negotiations and, in some cases, joint ventures, with third parties that own the specific tangible and intangible assets to be securitized, who we refer to as “asset originators,” or that have relationships with asset originators. We may also elect to securitize assets owned by our Company. Next, we will work with domestic and international securities market professionals, including licensed broker-dealers, merchant banks, ratings agencies and financial institutions, to structure and document the securitization of the assets, creating an asset backed financial product that can be more easily distributed and traded. This securitization process may include the pooling of assets, whether within the same asset class or across asset classes or asset originator types, or fractionalization of ownership of individual assets.

Once assets have been securitized, the new asset backed financial product will be represented in the form of digital, blockchain based tokens. We refer to this process as “digital tokenization.” Digital tokens are representative units of value, analogous to a stock certificate or a book-entry position, each of which reflects a holder’s ownership of a security, the terms of which are established in the investment documentation. Each of these tokens will be created by a “smart contract,” a self-executing agreement whose lines of code will reflect the economic and governance terms determined in the asset securitization process.

We intend for our digital tokenization process largely to rely upon technologies already in use and accessible in today’s blockchain market, such as Ethereum’s ERC-20 tokens, thus reducing the need, costs and execution risks of new technology development. We also intend to enter into leverage our Fintech Ecosystem to use blockchains that may be optimized for tokenization of assets in specific industry verticals, including, potentially basing these technologies on FI’s Velocity Ledger. We believe there are myriad benefits that can potentially be afforded by tokenizing securities via Velocity Ledger, including new product creation and market exposure, competitive fees, fast deal execution, and access to institutional investors and broker dealers.

Trading and Financial Services Platforms

We believe that regulated alternative trading systems (“ATSs”) and sophisticated risk management software arepossibly longer. The most important drivers for the development of trading marketsthe commercial fleet EV market are federal and provincial regulations relating to clean air and electronic vehicles including subsidies and incentives to help owners of fleets of commercial vehicles to convert from combustion engines to EV. The speed at which fleet operators convert to EV is highly correlated with government regulations, targets and related subsidies and incentives. If the governments, or municipalities, change the regulations, targets, incentives or subsidies then the rate at which fleet operators convert their vehicles to EV could slow down which in turn may lead to lower revenues for blockchain based digital tokens, including the digital securitized assets we planCompany. Additionally, the rate, and form in which, the commercial fleet EV market develops is dependent upon technological developments in battery and charging systems; deployment of the charging infrastructure to originate as part of our financial services business. Accordingly, we are making strategic investments that are intended to promotesupport widespread commercial EV use and the development of regulated ATSsnew financing and lending structures that will enhanceaddress the blockchain token trading ecosystemdifferent collateral and AI-based ratings systems to enhance the market viability of our digital securitized assets.

Between August 2017 and December 2018, we acquired approximately 36.92%resale values of the capital stockbattery and vehicle versus internal combustion engine vehicles.

In addition to its directly owned operations the Company operates through a network of Delaware Boardinvestment arrangements, partnerships and formal and informal alliances; consequently, its competitive position could be adversely impacted if one of Trade Holdings, Inc. (“DBOT”), which is a FINRA member firm and has filed an initial operations report on Form ATSthe members of the alliance was not able to give notice of operations of DBOT ATS, LLC (“DBOT ATS”), and which we believe is well positioned to develop blockchain-enabled transactional platforms. DBOT operates three business lines, (i) DBOT ATS, which is intended to be an ATS for equity securities not listed onmeet the New York Stock Exchange or the Nasdaq, (ii) DBOT Issuer Services LLC, which is focused on setting and maintaining issuer standards, as well as the provision of issuer services to DBOT designated issuers, and (iii) DBOT Technology Services LLC, which is focused on the provision of market data and marketplace connectivity.

DBOT has entered into agreements with FI (which is also a licensor to Ideanomics), pursuant to which FI is developing a blockchain enabled primary issuance and secondary trading platform for DBOT ATS using the Velocity Ledger. Under the agreements, DBOT will maintain licensing rights for the technology.

Our Fintech Revenue Model:

As part of our transitioning to a next-generation fintech company, we began developing our revenue and business model to be closely aligned with the technologies and industries that we support in our FinTech Ecosystem and Industry Ventures in a way that we can capitalize on the market demand for theseits products, and services.

Our FinTech business and revenue model is directly connected with the agreements and partnerships that we engage in. The underlying economics vary on a case by case basis (due to the particular industry that they are a part of, and specific facts and circumstances for each agreement), but generally they have the following characteristics:

Digital Assets, Blockchain and AI:

Asia Operations:

Lease Financing:

U.S. Operations:

Licensing of Technologies / FinTech Village:

Equity Investments:

Additionally, we benefit from the various equity interests that we have in our various subsidiaries, joint ventures, and partnerships across our Fintech Ecosystem and Industry Ventures. In cases where valuable intellectual property is generated by through these strategic investments, the Company will consider strategic licensing agreements and additional business models in exchange for our services to further enhance revenue.

Legacy YOD Segment

Since 2010, we have provided premium content and integrated value-added service solutions for the delivery of VOD and paid video programming to digital cable providers, IPTV providers, OTT streaming providers, mobile manufacturers and operators, as well as direct customers. The core revenues were generated from both minimum guarantee payments and revenue sharing arrangements with distribution partners as well as subscription or transactional fees from subscribers.

In October 2016, we signed an agreement to form a five year partnership with Zhejiang Yanhua Culture Media Co., Ltd., a company organized under the laws of the PRC (“Yanhua”), where Yanhua will act as the exclusive distribution operator (within the territory of PRC) of our licensed library of major studio films (the “Yanhua Partnership”). We entered into the Yanhua Partnership and exclusive distribution agreement in order to offset losses from high upfront minimum guarantee licensing fees to studios. The Yanhua Partnership modified and improved our legacy major studio paid content business model by moving from a framework that included high and fixed costs and upfront minimum guaranteed payments, rising content costs from major Hollywood studios and low margins to a structure that will now include relatively nominal costs to our Company and the opportunity to reach an even wider audience. With the Yanhua Partnership, Yanhua assumed all sales and marketing costs and will pay us a minimum guarantee in exchange for a percentage of the total revenue share.

Pursuant to the Yanhua Partnership, the existing legacy Hollywood studio paid content as well as other IP content specified in the agreement, along with the corresponding authorized rights letter that we are entitled to, were transferred to Yanhua for RMB13,000,000 (approximately $2 million), to be paid in two equal installments in the amount of RMB6,500,000 (approximately $1 million). The first installment was received on December 30, 2016 and was recognized as revenue in 2017 based on the relative fair value of licensed content delivered to Yanhua. The second installment will be paid if the license content fees due to studios for the existing legacy Hollywood paid contents are settled. To date, the legacy Hollywood studio paid content and other IP hasdecides not been transferred, as the second installment was not yet made.

We still run our legacy YOD segment with limited resources and plan to continue to run it throughcooperate with the Yanhua Partnership, where Yanhua will act asCompany, or goes out of business.

7

Ideanomics Capital

The Company’s Ideanomics Capital business unit operates in sectors that are undergoing rapid change.

DBOT is a broker dealer that also operates an ATS. In April 2020 the exclusive distribution operator (withinCompany ceased trading OTC equities, terminated the PRC) of our licensed library of major studio films. We launched our legacy VOD service through the acquisition of YOD Hong Kong (formerly Sinotop Group Limited) on July 30, 2010, by China CB Cayman. Through a series of contractual arrangements, YOD WFOE, the subsidiary of YOD Hong Kong, controls Sinotop Beijing, a corporation established in the PRC. Sinotop Beijing was the 80% owner of Zhong Hai Media until June 30, 2017, through which we provided: (1) integrated value–added business–to–business (“B2B”) service solutions for the delivery of VOD and enhanced premium content for digital cable; (2) integrated value–added business–to–business–to–customer (“B2B2C”) service solutions for the delivery of VOD and enhanced premium content for IPTV and OTT providers; and (3) a directemployees assigned to user, or business-to-customer (“B2C”), mobile video service app. We sold Zhong Hai Media on June 30, 2017 to Hanghzou for a nominal amount.

Management Team with Significant FinTech, Blockchain and AI Experience

To support our transition to a next-generation AI and blockchain enabled fintech company, we have strategically secured a management team with diversified expertise in operations, technology, fintech, blockchain, AI, capital marketsDBOT and the financial services industry,needed to operate the business. The Company has continued to maintain DBOT’s regulatory licenses and largely transitioned our operations toward the United States, having 18 U.S. employees as of December 31, 2018 comparedrequired regulatory capital. The Company has applied for regulatory approval to three as of December 31, 2017. As of the date ofbroker digital securities and tokens, this filing, key members of our management team include:

Dr. Bruno Wu. Our Chairman of the Board is an experienced investor, technology and media entrepreneur, and philanthropist. Dr. Wu has been actively involved with blockchain enabled and big data technologies since October 2011. After four years of investment and research, in 2015, Dr. Wu and Beijing Sun Seven Stars Culture Development Limited (“SSS”), an affiliate of Dr. Wu and a significant shareholder in our Company, proceeded to execute the strategy of becoming a leader in fintech and asset digitization services by aggregating AI, blockchain and other big data and cloud-based technologies, carefully sourced and selected on a global basis through joint ventures and partnerships. These partnerships focus on customizing and enabling actual business use case applications. Dr. Wu actively participated in the build out of a leading big data hub in Guiyang, China, particularly by endorsing the integration of AI and blockchain. Dr. Wu has committed to transforming our Company into a fintech and asset digitization services flagship, with multiple use case technology engines to be rolled out.

Mr. Alf Poor. Our Chief Executive Officer, and President of the Connecticut Fintech Village, is a former Chief Operating Officer at Global Data Sentinel, a cybersecurity company that specializes in identity management, file access control, protected sharing, reporting and tracking, AI and thread response, and backup and recovery. He isnascent market which the former President and Chief Operating Officer of Agendize Services Inc., a company with an integrated suite of applications that help businesses generate higher quality leads, improve business efficiency and customer engagement. Mr. Poor is a client-focused and profitability-driven management executive with a track record of success at both rapidly-growing technology companies and large, multi-national, organizations.

Mr. Federico Tovar. Our Chief Financial Officer is a seasoned business professional and subject matter expert in AI, fintech, blockchain, IoT and cybersecurity. He was previously the Chief Financial and Strategy Officer of Global Data Sentinel Inc, a privately held and high growth cybersecurity and AI technology company that supports data security across domains, including network, cloud, mobile and IoT, with AI capabilities and next-generation applications in fintech, blockchain, energy, insurance, healthcare, and media industries, amongst others. Mr. TovarCompany believes has developed strategic plans and business models, structured various IP and technology licensing deals, closed on various M&A transactions and debt and equity financing rounds, and formulated corporate growth and financial strategies for technology companies which have resulted in measurable execution strategies.

Ms. Kate Lam is Managing Director, Digital Capital Markets. Ms. Lam has more than twenty years of financial markets experience in marketing multiple asset classes to Propellr, a fintech platform for multi-asset financing. She successfully obtained the SEC broker dealer license for Propellr Securities and integrated regulatory best practices into the platform. As CEO of the broker dealer, she worked closely with engineers and product managers to design specifications for investor vetting, as well as perform due diligences on financing deals. She was also the Head of Institutional Sales and Investor Relations for the company. Prior to Propellr, Ms. Lam held senior management positions at Deutsche Bank, Bear Stearns and Standard Chartered Bank with a client base spanning central banks, global and regional banks, asset managers, global insurance companies and hedge funds.

Dr. George Yuan. Dr. George Yuan is the Chief Technology Officer of BBDCG. Dr. Yuan is a world leading expert on dynamic ontology for credit risk assessment and risk management. He served as the leader for risk management consulting at KPMG (US) and the Director of China / Hong Kong Deloitte Financial Consulting. Dr. Yuan was selected as a National Distinguished Expert in Shanghai’s and Sichuan’s “The Thousand Talents Plan” in 2013 and 2018, and he is the Chief Editor for The Journal of Financial Engineering. Dr. Yuan’s is leading BDCG’s focus on AI driven financial data services as well as transactional platforms for index, futures and derivative trading, for both global commodity and energy clients. Dr. Yuan is the Chief Risk Officer and Chief Engineer of BDCG. Dr. Yuan has held a professorship at the Institute of Risk Management at Tongji University. Dr. Yuan’s study and work has centered around the valuation of financial derivatives and value-at-risk (“VaR”) modeling for market risk, credit risk and operational risk under the framework of the Basel II (Basel III) Accord, financial and credit derivatives pricing, portfolio optimization, risk limit design, commodity forward price curve design, complex position, commodity price risk assessment and asset valuation.

good long term potential.

Corporate Structure

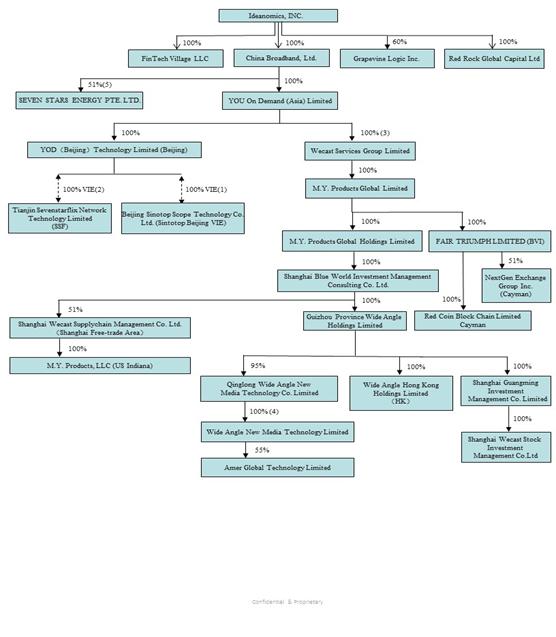

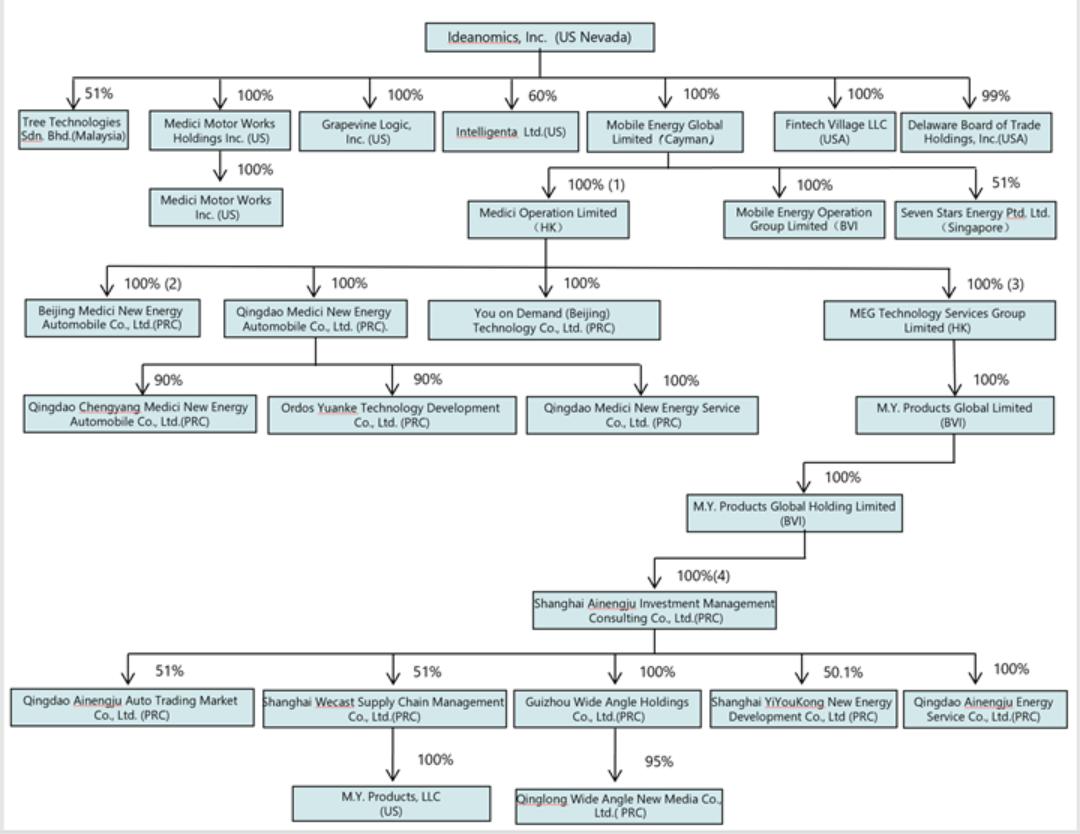

The following chart depicts our corporate structure as of December 31, 2018: 2020:

(1) | In 2020, the |

(2) | In 2020, the Company renamed You On Demand (Beijing) Information Consulting Co., Limited. to Beijing | |

Medici New Energy Automobile Co,, Ltd.

8

(3)

In |

(4) | In 2020, the Company renamed Shanghai |

VIE Structure and Arrangements

The Company consolidated certain VIEs located in the PRC in which it held variable interests and was the primary beneficiary through contractual agreements. The Company was the primary beneficiary because it had the power to direct activities that most significantly affected their economic performance and had the obligation to absorb or right to receive the majority of their losses or benefits. The results of operations and financial position of these VIEs are included in the consolidated financial statements for the year ended December 31, 2019. A shareholder in one of the VIEs is the spouse of Bruno Wu (“Dr. Wu,”) the former Chairman of the Company.

ToRefer to Note 10 of the Notes to Consolidated Financial Statements included in Part IV, Item 8 of this Annual Report on Form 10-K for further information.

The contractual agreements listed below, which collectively granted the Company the power to direct the VIEs activities that most significantly affected their economic performance, as well to cause the Company to have the obligation to absorb or right to receive the majority of their losses or benefits, were terminated by all parties on December 31, 2019. As a result, the Company deconsolidated the VIEs as of December 31, 2019. The deconsolidation resulted in a net loss of $2.0 million recorded in “Gain (loss) on disposal of subsidiaries, net” in the consolidated statements of operations, and a statutory income tax of $0.2 million in the year ended December 31, 2019.

For these consolidated VIEs, their assets were not available to the Company and their creditors did not have recourse to the Company. Prior to December 31, 2019, in order to operate certain legacy business in the PRC and to comply with PRC laws and regulations that prohibit or restrict foreign ownership of companies that provideprovides value-added telecommunication services, we provide services through Sinotop Beijing and SSF, which hold the licenses and approvals to provide digital distribution and Internet content services in the PRC. We have the ability to control Sinotop Beijing and SSF throughCompany entered into a series of contractual agreements as described below, entered into among YOD WFOE, YOD Hong Kong, Sinotop Beijing, SSF and the respective legal shareholders of Sinotop Beijing and SSF.

Through these contractual arrangements, we have acquired both control over and rights to, 100% of the economic benefit of Sinotop Beijing and SSF. Accordingly, Sinotop Beijing and SSF are each considered a VIE, and are therefore consolidated in our financial statements. Pursuant to the belowwith two VIEs. These contractual agreements YOD WFOE can have the assets transferred freely out of each VIE without any restrictions. Therefore, YOD WFOE considers that there is no asset of the respective VIE that can be used onlywere initially set to settle obligation of such VIE, except for the registered capital of each respective VIE, amounting to RMB10.6 million (approximately $1.6 million) for Sinotop Beijing,expire in March 2030 and RMB27.6 million (approximately $4.2 million) has been injected as of December 31, 2018. As Sinotop BeijingApril 2036, respectively, and SSF are incorporated as limited liability companies under PRC Company Law, creditors of these two entities do not have recourse to the general credit of our other entities.

The following is a summary of the common contractual arrangements that provide us with effective control our VIEs and that enable us to receive substantially all of the economic benefits from their operations:

Equity Pledge Agreement

Pursuant to the Equity Pledge Agreement among YOD WFOE and the respective nominee shareholders, the nominee shareholders pledge all of their capital contribution rights in the VIEs to YOD WFOE as security for the performance of the obligations of the VIEs to make all the required technical service fee payments pursuant to the Technical Services Agreement and for performance of the nominee shareholders’ obligation under the Call Option Agreement. The terms of the Equity Pledge Agreement expire upon satisfaction of all obligations under the Technical Services Agreement and Call Option Agreement.

Call Option Agreement

Pursuant to the Call Option Agreement among YOD WFOE, the VIEs and the respective nominee shareholders, the nominee shareholders grant an exclusive option to YOD WFOE, or its designee, to purchase, at any time and from time to time, to the extent permitted under PRC law, all or any portion of the nominee shareholders’ equity in the VIEs. The exercise price of the option shall be determined by YOD WFOE at its sole discretion, subject to any restrictions imposed by PRC law. The term of the agreement is until all of the equity interest in the VIEs held by the nominee shareholders is transferred to YOD WFOE, or its designee and may not be terminated by any party to the agreement without consent of the other parties.

Power of Attorney

Pursuant to the Power of Attorney agreements among YOD WFOE, each VIE and each of the respective nominee shareholders, each nominee shareholder grants YOD WFOE the irrevocable right, for the maximum period permitted by law, to all of its voting rights as shareholder of the VIE. The nominee shareholders may not transfer any of their equity interest in the VIE to any party other than YOD WFOE. The Power of Attorney agreements may not be terminated except until all of the equity in the VIE has been transferred to YOD WFOE or its designee.

Technical Service Agreement

Pursuant to the Technical Service Agreement, between YOD WFOE and each VIE, YOD WFOE has the exclusive right to provide technical service, marketing and management consulting service, financial support service and human resource support services to VIE, and VIE is required to take all commercially reasonable efforts to permit and facilitate the provision of the services by YOD WFOE. As compensation for providing the services, YOD WFOE is entitled to receive service fees from VIE equivalent to YOD WFOE’s cost plus 20-30% of such costs as calculated on accounting policies generally accepted in the PRC. YOD WFOE and VIE agree to periodically review the service fee and make adjustments as deemed appropriate. The term of the Technical Services Agreement is perpetual, and may only be terminated upon written consent of both parties.

Spousal Consent

Pursuant to the Spousal Consent, undersigned by the respective spouse of the nominee shareholders, the spouses unconditionally and irrevocably agree to the execution of the Equity Pledge Agreement, Call Option Agreement and Power of Attorney agreement. The spouses agree to not make any assertions in connection with the equity interest of VIE and to waive consent on further amendment or termination of the Equity Pledge Agreement, Call Option Agreement and Power of Attorney agreement. The spouses further pledge to execute all necessary documents and take all necessary actions to ensure appropriate performance under these agreements upon YOD WFOE’s request. In the event the spouses obtain any equity interests of VIE which are held by the nominee shareholders, the spouses agreed to be bound by the VIE agreements, including the Technical Services Agreement, and comply with the obligations thereunder, including sign a series of written documents in substantially the same format and content as the VIE agreements.

Letter of Indemnification

Pursuant to the Letter of Indemnification among YOD WFOE and each nominee shareholder, YOD WFOE agrees to indemnify such nominee shareholder against any personal, tax or other liabilities incurred in connection with their role in equity transfer to the greatest extent permitted under PRC law. YOD WFOE further waives and releases the nominee shareholders from any claims arising from, or related to, their role as the legal shareholder of the VIE, provided that their actions as a nominee shareholder are taken in good faith and are not opposed to YOD WFOE’s best interests. The nominee shareholders will not be entitled to dividends or other benefits generated therefrom, or receive any compensation in connection with this arrangement. The Letter of Indemnification will remain valid until either the nominee shareholder or YOD WFOE terminates the agreement by giving the other party hereto sixty (60) days’ prior written notice.

Management Services Agreement

In addition to VIE agreements described above, our subsidiary and the parent company of YOD WFOE, YOU On Demand (Asia) Limited, a company incorporated under the laws of Hong Kong (“YOD Hong Kong”) has entered into a Management Services Agreement with each VIE.

Pursuant to such Management Services Agreement, YOD Hong Kong has the exclusive right to provide to the VIE management, financial and other services related to the operation of the VIE’s business, and the VIE is required to take all commercially reasonable efforts to permit and facilitate the provision of the services by YOD Hong Kong. As compensation for providing the services, YOD Hong Kong is entitled to receive a fee from the VIE, upon demand, equal to 100% of the annual net profits as calculated on accounting policies generally accepted in the PRC of the VIE during the term of the Management Services Agreement. YOD Hong Kong may also request ad hoc quarterly payments of the aggregate fee, which payments will be credited against the VIE’s future payment obligations.

In addition, at the sole discretion of YOD Hong Kong, the VIE is obligated to transfer to YOD Hong Kong, or its designee, any part or all of the business, personnel, assets and operations of the VIE which may be lawfully conducted, employed, owned or operated by YOD Hong Kong, including:

(a) business opportunities presented to, or available to the VIE may be pursued and contracted for in the name of YOD Hong Kong rather than the VIE, and at its discretion, YOD Hong Kong may employ the resources of the VIE to secure such opportunities;

(b) any tangible or intangible property of the VIE, any contractual rights, any personnel, and any other items or things of value held by the VIE may be transferred to YOD Hong Kong at book value;

(c) real property, personal or intangible property, personnel, services, equipment, supplies and any other items useful for the conduct of the business may be obtained by YOD Hong Kong by acquisition, lease, license or otherwise, and made available to the VIE on terms to be determined by agreement between YOD Hong Kong and the VIE;

(d) contracts entered into in the name of the VIE may be transferred to YOD Hong Kong, or the work under such contracts may be subcontracted, in whole or in part, to YOD Hong Kong, on terms to be determined by agreement between YOD Hong Kong and the VIE; and

(e) any changes to, or any expansion or contraction of, the business may be carried out in the exercise of the sole discretion of YOD Hong Kong, and in the name of and at the expense of, YOD Hong Kong;

(f) provided, however, that none of the foregoing may cause or have the effect of terminating (without being substantially replaced under the name of YOD Hong Kong) or adversely affecting any license, permit or regulatory status of the VIE.

The term of each Management Services Agreement is 20 years, and maycould not be terminated by the VIE,VIEs, except with the consent of, or a material breach, by YOD Hong Kong.

Loan Agreement

Pursuant to the Loan Agreement among YOD WFOE and the nominee shareholders, YOD WFOE agrees to lend RMB19.8 million and RMB0.2 million, respectively, to the nominee shareholders of SSF for the purpose of establishing SSF and for development of its business. As of December 31, 2018, RMB27.6 million ($4.2 million) and RMB nil have been lent to Lan Yang and Yun Zhu, respectively. Lan Yang has contributed allCompany. A shareholder in one of the RMB27.6 million ($4.2 million) inVIEs is the formspouse of capital contribution and accordinglyDr. Wu, the loan is eliminated with the capital of SSF upon consolidation. The loan can only be repaid by a transfer by the nominee shareholders of their equity interests in SSF to YOD WFOE or YOD WFOE’s designated persons, through (i) YOD WFOE having the right, but not the obligation to at any time purchase, or authorize a designated person to purchase, all or partformer Chairman of the Nominee Shareholders’ equity interests in SSF at such price as YOD WFOE shall determine (the “Transfer Price”), (ii) all monies received by the nominee shareholders through the payment of the Transfer Price being used solely to repay YOD WFOE for the loans, and (iii) if the Transfer Price exceeds the principal amount of the loans, the amount in excess of the principal amount of the loans being deemed as interest payable on the loans, and to be payable to YOD WFOE in cash. Otherwise, the loans shall be deemed to be interest-free. Company.

The term of the Loan Agreement is perpetual, and may only be terminated upon the nominee shareholders receiving repayment notice, or upon the occurrence of an event of default under thekey terms of the agreement.VIE Agreements are summarized as follows:

| ● | Equity Pledge Agreement - The VIEs’ shareholders pledged all of their equity interests in the VIEs to a wholly-owned subsidiary of the Company in the PRC; |

| ● | Call Option Agreement - The VIEs’ shareholders granted an exclusive option to a wholly-owned subsidiary of the Company in the PRC, or its designee, to purchase all or any portion of the VIEs’ Shareholders’ equity in the VIEs; |

| ● | Power of Attorney - The VIEs’ shareholders granted to a wholly-owned subsidiary of the Company in the PRC the irrevocable right, for the maximum period permitted by law, all of its voting rights as shareholders of VIEs; |

| ● | Technical Service Agreement – A wholly-owned subsidiary of the Company in the PRC had the exclusive right to provide technical service, marketing and management consulting service, financial support service and human resource support services to the VIEs, and the VIEs were required to take all commercially reasonable efforts to permit and facilitate the provision of the services; |

| ● | Spousal Consent - The spouses of the VIEs’ shareholders unconditionally and irrevocably agreed to the execution of the Equity Pledge Agreement, Call Option Agreement and Power of Attorney agreement; |

| ● | Letter of Indemnification – A wholly-owned subsidiary of the Company in the PRC agreed to indemnify such nominee shareholder against any personal, tax or other liabilities incurred in connection with their role in equity transfer to the greatest extent permitted under PRC law; |

9

| ● | Management Services Agreement - In addition to agreements described above, another of the Company’s wholly-owned subsidiaries entered into a Management Services Agreement with each VIE. Pursuant to such Management Services Agreement, the wholly-owned subsidiary had the exclusive right to provide to the VIE management, financial and other services related to the operation of the VIE’s business, and the VIE was required to take all commercially reasonable efforts to permit and facilitate the provision of the services by the subsidiary. In addition, at the sole discretion of the subsidiary, the VIE was obligated to transfer to the subsidiary, or its designee, any part or all of the business, personnel, assets and operations of the VIE which could be lawfully conducted, employed, owned or operated by the subsidiary; and |

| ● | Loan Agreement - Pursuant to the Loan Agreement dated April 5, 2016, a wholly-owned subsidiary of the Company in the PRC agreed to lend RMB 19.8 million and RMB 0.2 million, respectively, to the VIEs’ Shareholders, one of whom is the spouse of Dr. Wu, the Company’s former Chairman. The termination of the Loan Agreement resulted in a loss of $5.1 million in the year ended December 31, 2019. |

Our Unconsolidated Equity Investments

We hold a 30%34.0% ownership interest in Shandong Media,Glory, which is our print based media business,through its subsidiary Tree Manufacturing, holds a domestic EV manufacturing license in Malaysia. Tree Manufacturing had entered into a product supply and accounta product distribution arrangement for our investment in Shandong Media underEVs with Tree Technologies, a consolidated subsidiary of the equity method. The business of Shandong Media includes a television programming guide publication, the distribution of periodicals, the publication of advertising, the organization of public relations events, the provision of information related services, copyright transactions, the production of audio and video products, and the provision of audio value added communication services.

We hold a 39% ownership interest in Hua Cheng, and account for our investment in Hua Cheng under the equity method. The business of Hua Cheng mainly includes distribution of content and VOD business on television terminal.

We hold a 50% ownership interest in Wecast Internet Limited, a Hong Kong company (“Wecast Internet”), and account for our investment in Wecast Internet under the equity method. The business of Wecast Internet mainly includes computer network technology development, integrated circuit of software and hardware technology development, technical consultation.

From August 2017 through December 31, 2018, we acquired 36.92% ownership interest in DBOT, and are accounting for our investment in DBOT under the equity method starting from October 2018. DBOT is a FINRA member firm, and filed an initial operations report on Form ATS to give notice of DBOT ATS’s operations. DBOT is powered through blockchain technology licensed from one of our strategic licensing partners.

Company.

In 2018, we signed a joint venturean investment agreement to establish BDCG located in the United StatesIntelligenta for providing blockchain services for financial or energy industries by utilizing AI and big data technology in the United States. We hold a 60%60.0% ownership interest and Seasail ventures limited (“Seasail”) holds 40% of BDCG. The new entity is currently inIntelligenta.

On October 22, 2020, the processCompany acquired 1.4 million common shares, representing 15.0% of ramping up itsthe total common shares outstanding, of Solectrac for a purchase price of $0.91 per share, for total consideration of $1.3 million. On November 19, 2020, Ideanomics acquired an additional 1.3 million shares of common stock for $1.00 per share, for a subsequent investment of $1.3 million. With this subsequent investment, Ideanomics owned 2.7 million common shares out of a total number of issued and outstanding common shares of 10.2 million after the transaction, or 27.0%.

Solectrac develops, assembles and distributes 100% battery-powered electric tractors-an alternative to diesel tractors-for agriculture and utility operations.

Solectrac tractors provide an opportunity for farmers around the world to power their tractors by using the sun, wind, and other clean renewable sources of energy.

Our investments in Shandong Media, Hua Cheng, Wecast Internet, DBOTGlory, BDCG and BDCGSolectrac, where we may exercise significant influence, but not control, isare classified as a long-term equity investmentinvestments and accounted for using the equity method. Under the equity method, the investment is initially recorded at cost and adjusted for our share of undistributed earnings or losses of the investee. Investment losses are recognized until the investment is written down to nil, provided that we do not guarantee the investee’s obligations or we are committed to provide additional funding.

In the years ended December 31, 2020 and 2019, the Company recorded impairment losses with respect to its equity method investments of $16.6 million and $13.1 million, respectively.

Refer to Note 10 of the Notes to Consolidated Financial Statements included in Part IV, Item 8 of this Annual Report on Form 10-K for further information.

Our Competition

Ideanomics Mobility Business Unit

Wecast Services SegmentThe Company’s EV business operates in the market for fleet commercial vehicles, this market is still in its development stage. The Company could face competition from other companies that develop and operate a similar integrated platform for the procurement, purchase, financing, charging and energy management needs of fleet EV operators. The Company could also face competition from companies that only operate in one part of the vehicle purchase and operation cycle, for example, an EV vehicle or battery manufacturer may sell directly to EV fleet operators while also participating in the platform operated by the Company’s MEG business.

10

Other

Grapevine competes in the consumer marketing sector and specializes in designing and managing “influencer” led social media campaigns for brands and advertising agencies that do not have a capability to manage influencer marketing campaigns directly. This is a very competitive sector with multiple competitors.

We will face significant competitionRevenue Recognition

The Company records and reports revenues in accordance with respectgenerally accepted accounting principles in the U.S., particularly ASC 606, Revenue from Contracts with Customers which provides guidance on how revenues should be reported and the timing of when revenues should be reported. ASC 606 includes guidance on when revenue should be recognized on a Gross (Principal) or Net (Agent) basis, the Company’s contracts are typically with large enterprises and consequently are heavily negotiated as to the products and services we plan to offer inbe provided; consequently the blockchain and AI enabled fintech business we are building, and we currently face significant competition with respect to the businesses we operate that currently generate revenue for our Company. Our long-term strategic goal is to leverage blockchain and AI based fintech solutions to offer products and services that will bring transparency, efficiency and cost savings to various markets, including finance, commodities, energy, consumer products and transportation logistics. We therefore face significant competitive pressure not only with other developers of blockchain and AI technologies in the fintech space, but also in the marketsaccounting treatment for the products and services we offerreporting of revenues may vary materially between contracts including whether the revenue is reported on a Principal (Gross) or plan to offer, which are very competitive and subject to rapid technological advances, new market entrants, non-traditional competitors, changes in industry standards and changes in customer needs and consumption models.

We believe that our parallel development strategy of building out our Fintech Ecosystem while developing a network of Industry Ventures will enable us to compete in our planned businesses on the basis of our ability to offer a wider range of value-added services than our competitors. We also believe that our unique position as a cross-border company will give us the ability to create partnerships with companies developing new technologies in both the U.S. and Asia.

While we generate revenues from our crude oil and consumer electronics business, we engage in this business largely for research purposes to support our development of fintech solutions for this space, and not primarily with a view to competitive returns.

YOD Segment

The market for video entertainment is subject to continuous change and aggressive competition. Our primary competitors in this space include Internet based content providers and the DVD market, such as iQiyi.com, Youku, Tencent and Sohu. We also face competitors who may attempt to undercut the market by providing pirated (illegal) content. Although we can provide no assurances that other companies will not enter the market of providing such services, we believe that we will have a competitive advantage over any new market entrant because of our exclusive joint venture partnership with CCTV-6’s pay channel, CHC, and first to market advantage.

Seasonality Variations in Business

We expect a disproportionate amount of our revenues generated from Wecast Services quarter over quarter to be subject to seasoned fluctuations at holiday periods and due to introduction of new consumer electronics products. There may also be fluctuations related to weather changes for the crude oil trading business. This pattern may change, however, as a result of new market opportunities or new product introductions.

Agent (Net) basis.

Regulation

General Regulation of Businesses in the PRC