ASBURY AUTOMOTIVE GROUP, INC.

(Exact name of Registrant as specified in its charter)

| Delaware | 01-0609375 | ||||||||||||||||||

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||

| 2905 Premiere Parkway, NW, | Suite 300 | ||||||||||||||||

| Duluth, | Georgia | 30097 | |||||||||||||||

| ( | (Zip Code) | ||||||||||||||||

(770) 418-8200

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Trading | ||||||||||||||

| Title of each class | Symbol(s) | Name of each exchange on which registered | ||||||||||||

| Common | ABG | New York Stock Exchange | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act:

None.

a

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes xNo o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, (as definedor an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Act).

Exchange Act.

| Large Accelerated Filer | ☒ | Accelerated Filer | |||||||||||||||||

| Non-Accelerated Filer | ☐ | Smaller Reporting Company | ☐ | ||||||||||||||||

| Emerging Growth Company | |||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of

the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.

7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o ☐No x

Based on the closing price of the registrant's common stock as of June 30, 2017,2023, the aggregate market value of the common stock held by non-affiliates of the registrant was $1.16$4.92 billion (based upon the assumption, solely for purposes of this computation, that all of the officers and directors of the registrant were affiliates of the registrant).

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of the latest practicable date: The number of shares of common stock outstanding as of February 26, 201827, 2024 was 20,913,251.20,404,121.

DOCUMENTS INCORPORATED BY REFERENCE

List hereunder the following documents if incorporated by reference and the Part of the Form 10-K into which the document is incorporated:

Portions of the registrant's definitive Proxy Statement for the 20182024 Annual Meeting of Stockholders, to be filed within 120 days after the end of the registrant's fiscal year, are incorporated by reference into Part III, Items 10 through 14 of this Annual Report on Form 10-K.

ASBURY AUTOMOTIVE GROUP, INC.

ANNUAL REPORT ON FORM 10-K

FOR THE YEAR ENDED

DECEMBER 31, 20172023

| Page | ||||||||||

| PART I | ||||||||||

| PART II | ||||||||||

| PART III | ||||||||||

| PART IV | ||||||||||

PART I.

Forward-Looking Information

Certain of the discussions and information included or incorporated by reference in this report may constitute "forward-looking statements" within the meaning of the federal securities laws. Forward-looking statements are statements that are not historical in nature and may include statements relating to our goals, plans and projections regarding industry and general economic trends, our expected financial position, results of operations or market position and our business strategy. Such statements can generally be identified by words such as "may," "target," "could," "would," "will," "should," "believe," "expect," "anticipate," "plan," "intend," "foresee," and other similar words or phrases. Forward-looking statements may also relate to our expectations and assumptions with respect to, among other things:

•the seasonally adjusted annual rate ("SAAR") of new vehicle sales in the U.S.;United States;

•general economic conditions and its expected impact on our revenuesrevenue and expenses;

•our expected parts and service revenue due to, among other things, improvements in manufacturing quality;vehicle technology;

•our ability to limit our exposure to regional economic downturns due to our geographic diversity and brand mix;

•manufacturers' willingness to continue tocontinued use of incentive programs to drive demand for their product offerings;

•our capital allocation strategy, including as it relates to acquisitions and divestitures, stock repurchases, dividends and capital expenditures;

•the growth of import and luxurythe brands that comprise our portfolio over the long-term;

•disruptions in the production and supply of vehicles and parts from our ability to mitigate any future negative trends in new vehicle sales; and

•our estimated future capital expenditures, which can be impacted by increasing prices and labor shortages and acquisitions and divestitures.

Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause our actual future results, performance or achievements to be materially different from any future results, performance, or achievements expressed or implied by the forward-looking statements. Such factors include, but are not limited to:

•the ability to acquire and successfully integrate acquired businesses into our existing operations and realize expected benefits and synergies from such acquisitions;

•the effects of increased expenses or unanticipated liabilities incurred as a result of, or due to activities related to our acquisitions or divestitures;

•changes in general economic and business conditions, including the current inflationary environment, the current interest rate environment, changes in employment levels, consumer demand, preferences and confidence levels, consumer demand and preferences, the availability and cost of credit, fuel prices and levels of discretionary personal income and interest rates;income;

•our ability to executegenerate sufficient cash flows, maintain our balanced automotive retailingliquidity and service business strategy;obtain any necessary additional funds for working capital, capital expenditures, acquisitions, stock repurchases, debt maturity payments and other corporate purposes, if necessary or desirable;

•significant disruptions in the production and delivery of vehicles and parts for any reason, including supply shortages, the ongoing conflict in Russia and Ukraine, including any government sanctions imposed in connection therewith, natural disasters, severe weather, civil unrest, product recalls, work stoppages or other occurrences that are outside of our control;

•our ability to successfully attract and retain skilled employees;

•our ability to successfully operate, including our ability to maintain, and obtain future necessary regulatory approvals, for Total Care Auto, Powered by Landcar ("TCA"), our finance and insurance ("F&I ") product provider;

•adverse conditions affecting the vehicle manufacturesmanufacturers whose brands we sell, and their ability to design, manufacture, deliver and market their vehicles successfully;

•changes in the mix and total number of vehicles we are able to sell;

•our outstanding indebtedness and our continued ability to comply with applicable covenants in our various financing and lease agreements, or to obtain waivers of these covenants as necessary;

4

•high levels of competition in our industry, which may create pricing and margin pressures on our products and services;

•our relationships with manufacturers of the vehicles we sell and our ability to renew, and enter into new framework and dealer agreements with vehicle manufacturers whose brands we sell, on terms acceptable to us;

•the availability of manufacturer incentive programs and our ability to earn these incentives;

•failure of our, or those of our third-party service providers, management information systems or systems;

•any data security breaches;breaches occurring, including with regard to personally identifiable information ("PII");

•changes in laws and regulations governing the operation of automobile franchises, including trade restrictions, consumer protections, accounting standards, taxation requirements and environmental laws;

•changes in, or the imposition of, new tariffs or trade restrictions on imported vehicles or parts;

•adverse results from litigation, regulatory investigations or other similar proceedings involving us;us, including costs, expenses, settlements and judgments related thereto;

•our ability to generate sufficient cash flows, maintain our liquidityconsummate planned or pending mergers, acquisitions and obtain any necessary additional funds for working capital, capital expenditures, acquisitions, stock repurchases and/or dividends, debt maturity payments, and other corporate purposes;dispositions;

•any disruptions in the financial markets, which may impact our ability to access capital;

•our relationships with, and the financial stability of, our lenders and lessors;

•our ability to execute our initiatives and other strategies; and

•our ability to leverage gains fromscale and cost structure to improve operating efficiencies across our dealership portfolio.

Many of these factors are beyond our ability to control or predict, and their ultimate impact could be material. Moreover, the factors set forth under "Item 1A. Risk Factors" and "Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations" below and other cautionary statements made in this report should be read and considered as forward-looking statements subject to such uncertainties. We urge you to carefully consider those factors.

Forward-looking statements speak only as of the date of this report. We expressly disclaim any obligation to update any forward-looking statement contained herein.

Additional Information

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to such reports filed pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, are made available free of charge on our website at http://www.asburyauto.com as soon as practical after such reports are filed with the U.S. Securities and Exchange Commission (the "Commission"). In addition, the proxy statement that will be delivered to our stockholders in connection with our 20172024 Annual Meeting of Stockholders, when filed, will also be available on our website, and at the URL stated in such proxy statement. We also make available on our website copies of our certificate of incorporation, bylaws, and other materials that outline our corporate governance policies and practices, including:

•the respective charters of our audit committee, governance and nominating committee, compensation and human resources committee, and capital allocation and risk management committee;

•our criteria for independence of the members of our boardBoard of directors,Directors, audit committee, and compensation and human resources committee;

•our Corporate Governance Guidelines; and

•our Code of Business Conduct and Ethics for Directors, Officers, and Employees.

We intend to provide any information required by Item 5.05 of Form 8-K (relating to amendments or waivers of our Code of Business Conduct and Ethics for Directors, Officers, and Employees) by disclosure on our website.

You may also obtain a printed copy of the foregoing materials by sending a written request to: Investor Relations Department, Asbury Automotive Group, Inc., 2905 Premiere Parkway, NW, Suite 300, Duluth, Georgia 30097. In addition, the Commission makes available on its website, free of charge, reports, proxy and information statements, and other information regarding issuers, such as us, that file electronically with the Commission. The Commission's website is http://www.sec.gov. Unless otherwise specified, information contained on our website, available by hyperlink from our website or on the Commission's website, is not incorporated into this report or other documents we file with, or furnish to, the Commission.

5

Except as the context otherwise requires, "we," "our," "us," "Asbury," and "the Company" refer to Asbury Automotive Group, Inc. and its subsidiaries.

Item 1. BUSINESS

Asbury Automotive Group, Inc., a Delaware corporation organized in 2002, is a Fortune 500 company and one of the largest franchised automotive retailers in the United States. Our mission and vision is to put the guest experience first and follow our "North Star" to be the most guest-centric automotive retailer in the industry. We follow three key principles to guide us: (1) have a fun, supportive and inclusive culture where team members thrive personally while building meaningful bonds with one another; (2) be great brand ambassadors and exceptional stewards of capital for our partners who fuel our mission; and (3) be caring professionals who strive to delight our guests and foster love for the brand. Our strong organizational culture and purposeful mission allow us to continuously deliver best-in-class experiences to our guests. As of December 31, 2023, we owned and operated 208 new vehicle franchises, representing 31 brands of automobiles at 158 dealership locations, 37 collision centers, and Total Care Auto, Powered by Landcar ("TCA" or "TCA Business"), our finance and insurance ("F&I") product provider, within 16 states. Our store operations are conducted by our subsidiaries.

Our omni-channel platform is designed to engage with customers where and when they want to interact and to increase our market share through digital innovation. We are focused on providing a high level of customer service and have designed our dealerships’ services to meet the increasingly sophisticated needs of customers throughout the vehicle ownership lifecycle. Our digital capabilities further enhance our physical dealership network and drive additional revenue. Our ability to provide a low friction experience across our omni-channel platform drives customer satisfaction and repeat business across our dealership portfolio.

Acquisitions

On December 11, 2023, the Company completed the acquisition of the business of the Jim Koons ("Koons") Automotive Companies, (collectively, the "Koons acquisition"), thereby acquiring 20 new vehicle dealerships, six collision centers and the real property related thereto for an aggregate purchase price of approximately $1.50 billion, which includes $256.1 million of new vehicle floor plan financing and $103.8 million of assets held for sale related to Koons Lexus of Wilmington. The acquisition was funded with borrowings under Asbury’s existing credit facility and cash on hand. The Koons acquisition diversifies Asbury's geographic mix, with expansion in the greater Washington-Baltimore region of the United States.

There were no acquisitions during the year ended December 31, 2022.

On December 17, 2021, the Company completed the acquisition of the businesses of the Larry H. Miller ("LHM") Dealerships and TCA (collectively, the "LHM acquisition"), thereby acquiring 54 new vehicle dealerships, seven used cars stores, 11 collision centers, a used vehicle wholesale business, the real property related thereto, and the entities comprising the TCA business for a total purchase price of $3.48 billion. The purchase price was financed through a combination of cash, debt, including senior notes, real estate facilities, new and used vehicle floor plan facilities and the proceeds from the issuance of common stock. As a result of the transaction, the Company operates in two reportable segments, the Dealerships and TCA segments.

In addition our geographic footprint decreases our exposure to regional economic conditionsthe LHM acquisition, during the year ended December 31, 2021, we acquired the assets of 11 franchises (10 dealership locations) in the Denver, Colorado market and our brand diversification decreases our exposurethree franchises (one dealership location) in the Indianapolis, Indiana market for a combined purchase price of $485.7 million. We funded these acquisitions with an aggregate of $455.1 million of cash and $9.6 million of floor plan borrowings for the purchase of the related new vehicle inventory. In the aggregate, these acquisitions included purchase price holdbacks of $21.0 million for potential indemnity claims made by us with respect to manufacturer-specific risks, such as brand perception or production disruptions. Approximately 84%the acquired franchises.

Divestitures

During the year ended December 31, 2023, we sold one franchise (one dealership location) in Austin, Texas. The Company recorded a pre-tax gain totaling $13.5 million.

6

During the year ended December 31, 2022, we sold one franchise (one dealership location) in St. Louis, Missouri, three franchises (three dealership locations) and service,one collision center in Denver, Colorado, two franchises (two dealership locations) in Spokane, Washington, one franchise (one dealership location) in Albuquerque, New Mexico and finance11 franchises (nine dealership locations) and insurance which historically have been more stable throughout economic cycles.two collision centers in North Carolina. The Company recorded a pre-tax gain totaling $207.1 million.

During the year ended December 31, 2021, we sold one franchise (one dealership location) in the Charlottesville, Virginia market. The Company recorded a pre-tax gain totaling $8.0 million.

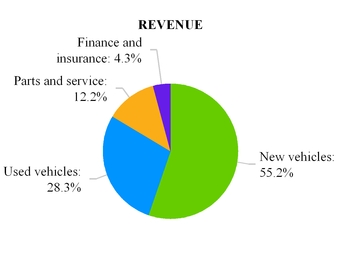

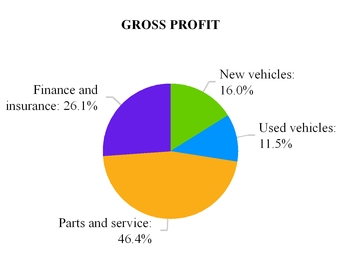

Four Key Components of Our Business

The following charts presentchart presents the contribution to total revenue and gross profit by each line of business for the year ended December 31, 2017:2023:

7

Our new vehicle franchise retail network within our Dealerships segment is made up of dealerships located in 17 metropolitan markets in 916 states operating primarily under eight locally-branded16 locally branded dealership groups. The following chart provides a detailed breakdown of our markets,states, brand names, and franchises as of December 31, 2017:

2023:

____________________________

| Dealership Group Brand Name | State | Franchise | ||||||||||||||

| Coggin Automotive Group | Florida | Acura, BMW, | ||||||||||||||

| Courtesy Autogroup | Florida | Chrysler, Dodge, Genesis, Honda, Hyundai, Infiniti, Jeep, Kia, Mercedes-Benz, Nissan, | ||||||||||||||

| Crown Automotive Company | South Carolina | |||||||||||||||

| Virginia | ||||||||||||||||

| David McDavid Auto Group | Texas | |||||||||||||||

| Greenville Automotive Group | South Carolina | Land Rover, Porsche, Toyota, Volvo | ||||||||||||||

| Hare, Bill Estes & Kahlo Automotive Groups | Indiana | Buick, Chevrolet(b), Chrysler(a), Dodge(a), Ford, GMC, Honda, Isuzu, Jeep(a), Toyota | ||||||||||||||

| Jim Koons Automotive Companies | Maryland | Buick, Chevrolet(a), Ford, GMC, Kia, Mercedes-Benz, Sprinter, Toyota(b), Volvo | ||||||||||||||

| Virginia | Buick(a), Chevrolet, Chrysler, Dodge, Ford(b), GMC(a), Hyundai, Jeep, Kia, Toyota(a) | |||||||||||||||

| Delaware | Lexus | |||||||||||||||

| Larry H. Miller Dealerships | Arizona | Chrysler(b), Dodge(c), Fiat, Ford, Genesis, Hyundai, Jeep(b), Nissan, Toyota, Volkswagen(a) | ||||||||||||||

| California | Toyota(a) | |||||||||||||||

| Colorado | Chrysler(a), Dodge(b), Fiat, Ford, Jeep(a), Nissan(b), Volkswagen | |||||||||||||||

| Idaho | Chrysler, Dodge, Honda, Jeep, | |||||||||||||||

| New Mexico | ||||||||||||||||

| Utah | ||||||||||||||||

| Washington | Honda | |||||||||||||||

| Mike Shaw, Stevinson & Arapahoe Automotive Groups | Colorado | |||||||||||||||

| Nalley Automotive Group | Georgia | Acura, Audi, Bentley, BMW, | ||||||||||||||

| Park Place Automotive | Texas | Acura, Lexus(a), Land Rover, Mercedes-Benz(b), Porsche, Volvo, Sprinter(b) | ||||||||||||||

| Plaza Motor Company | Missouri | Audi, BMW, Infiniti, | ||||||||||||||

(a)This state has two of these franchises.

(b)This state has three of these franchises.

(c)This state has four of these franchises.

(d)This state has five of these franchises.

8

Operations

New Vehicle Sales

The following table reflects the number of franchises we owned as of December 31, 20172023 and the percentage of new vehicle revenues represented by class and franchise for the year ended December 31, 2017:2023:

| Class/Franchise | Number of Franchises Owned | % of New Vehicle Revenues | ||||||||||||

| Luxury | ||||||||||||||

| Lexus | 9 | 11 | % | |||||||||||

| Mercedes-Benz | 9 | 8 | ||||||||||||

| BMW | 5 | 3 | ||||||||||||

| Acura | 4 | 2 | ||||||||||||

| Infiniti | 4 | 1 | ||||||||||||

| Land Rover | 3 | 2 | ||||||||||||

| Porsche | 3 | 2 | ||||||||||||

| Volvo | 3 | 1 | ||||||||||||

| Audi | 2 | 1 | ||||||||||||

| Genesis | 2 | 1 | ||||||||||||

| Lincoln | 2 | 1 | ||||||||||||

| Bentley | 1 | * | ||||||||||||

| Jaguar | 1 | * | ||||||||||||

| Total Luxury | 48 | 33 | % | |||||||||||

| Import | ||||||||||||||

| Toyota | 19 | 16 | % | |||||||||||

| Honda | 13 | 10 | ||||||||||||

| Hyundai | 9 | 4 | ||||||||||||

| Nissan | 9 | 3 | ||||||||||||

| Sprinter | 8 | 1 | ||||||||||||

| Kia | 4 | 2 | ||||||||||||

| Volkswagen | 4 | 1 | ||||||||||||

| Subaru | 3 | 2 | ||||||||||||

| Fiat | 2 | * | ||||||||||||

| MINI | 1 | * | ||||||||||||

| Isuzu | 1 | * | ||||||||||||

| Total Import | 73 | 39 | % | |||||||||||

| Domestic | ||||||||||||||

| Chrysler, Dodge, Jeep, Ram | 52 | 12 | % | |||||||||||

| Chevrolet, Buick, GMC | 22 | 6 | ||||||||||||

| Ford | 13 | 10 | ||||||||||||

| Total Domestic | 87 | 28 | % | |||||||||||

| Total Franchises | 208 | 100 | % | |||||||||||

| Class/Franchise | Number of Franchises Owned | % of New Vehicle Revenues | ||||

| Luxury | ||||||

| Mercedes-Benz | 4 | 7 | % | |||

| Lexus | 4 | 7 | ||||

| BMW | 7 | 6 | ||||

| Acura | 6 | 4 | ||||

| Infiniti | 4 | 3 | ||||

| Audi | 2 | 3 | ||||

| Lincoln | 3 | 1 | ||||

| Volvo | 2 | 1 | ||||

| Land Rover | 2 | 1 | ||||

| Jaguar | 2 | 1 | ||||

| Porsche | 1 | * | ||||

| Bentley | 1 | * | ||||

| Total Luxury | 38 | 34 | % | |||

| Import | ||||||

| Honda | 11 | 18 | % | |||

| Toyota | 6 | 11 | ||||

| Nissan | 10 | 12 | ||||

| Kia | 2 | 2 | ||||

| Hyundai | 3 | 2 | ||||

| Volkswagen | 1 | 1 | ||||

| MINI | 1 | * | ||||

| smart (a) | — | * | ||||

| Isuzu | 1 | * | ||||

| Sprinter | 3 | * | ||||

| Total Import | 38 | 46 | % | |||

| Domestic | ||||||

| Ford | 6 | 11 | % | |||

| Chevrolet | 3 | 4 | ||||

| Dodge | 3 | 3 | ||||

| Jeep | 2 | 1 | ||||

| GMC | 1 | 1 | ||||

| Chrysler | 2 | * | ||||

| Buick | 1 | * | ||||

| Total Domestic | 18 | 20 | % | |||

| Total Franchises | 94 | 100 | % | |||

* Franchise accounted for less than 1% of new vehicle revenues for the year ended December 31, 2017.2023.

Our new vehicle revenues include new vehicle sales and lease transactions arranged by our dealerships with third-party financial institutions. We believe that leasing provides a number of benefits to our other business lines, including the historical customer loyalty to the leasing dealership for repairs and maintenance services and the fact that lessors typically give the leasing dealership the first option to purchase the off-lease vehicle.

9

Used Vehicle Sales

We sell used vehicles at all of our franchised dealership locations. Used vehicle sales include the sale of used vehicles to individual retail customers ("used retail") and the sale of used vehicles to other dealers at auction ("wholesale") (the terms "used retail" and "wholesale" collectively referred to as "used").

Gross profit from the sale of used vehicles depends primarily on our dealerships' ability to obtain a high quality supply of used vehicles and our use of technology to manage our inventory. Our new vehicle operations typically provide our used vehicle operations with a large supply of trade-ins and off-lease vehicles, which we believe are good sources of high quality used vehicles. We also purchase a portion of our used vehicle inventory at "open" auctions and auctions restricted to new vehicle dealers. Additionally, our used vehicle sales benefit from our ability to sell certified pre-owned vehicles from our franchised dealerships.

Parts and Service

We provide vehicle repair and maintenance services, sell replacement parts, and recondition used vehicles at all of our dealerships. In addition, we provide collision repair services at our 2437 free-standing collision repair centers that we operate either on the premises of, or in close proximity to, our dealerships. Historically, parts and service revenues have been more stable than those from vehicle sales. Industry-wide, parts and service revenues have consistently increased over time primarily due to the increased cost of maintaining vehicles, the added technical complexity of vehicles, and the increasing number of vehicles on the road.

The automotive parts and service industry tends to be highly fragmented, with franchised dealerships and independent repair shops competing for this business. We believe, however, that the increased use of advanced technology in vehicles is making it difficult for independent repair shops to compete effectively with franchised dealerships as they may not be able to make the investment necessary to perform major or technical repairs. In an effort to maintain the necessary knowledge to service vehicles and further develop our technician staff, we focus on our internal and manufacturer specific training and development programs for new and existing technicians. We believe our parts and service business is also well-positioned to benefit from the service work potentially generated through the sale of extended service contracts to customers who purchase new and used vehicles from us, as historically these customers tend to have their vehicles serviced at the location where they purchased the extended service contract. In addition, our franchised dealerships benefit from manufacturer policies requiring that warranty and recall related repairs be performed at a franchised dealership. We believe that our collision repair centers provide us with an attractive opportunity to grow our business due to the high margins provided by collision repair services and the fact that we are able to source original equipment manufacturer parts from our franchised dealerships.

Finance and Insurance

We offer a wide variety of automotive finance and insurance ("F&I")&I products to our customers. Through the acquisition of TCA in December 2021, we offer extended vehicle service contracts, prepaid maintenance contracts, key replacement contracts, guaranteed asset protection contracts, paintless dent repair contracts, appearance protection contracts, tire and wheel, and lease wear and tear contracts. These F&I products are sold to our customers via our network of dealerships.

In addition to the TCA F&I products, we offer our customers a variety of vehicle protection products through independent third parties in connection with the purchase of vehicles. These products are underwritten and administered by these third parties. Under our arrangements with the providers of these products, we primarily sell the products on a straight commission basis. We are subject to chargebacks for service and other contracts as a result of early termination, default, or prepayment of the contract. In addition, we participate in future profits associated with the performance of the third-party held underlying portfolio for certain products pursuant to retrospective commission arrangements.

We also arrange third-party financing for the sale or lease of vehicles to our customers in exchange for a feecompensation paid to us by the third-party financial institution. We do not directly finance our customers' vehicle purchases or leases, therefore our exposure to losses in connection with those third-party financing arrangements is limited generally to the fees thatcompensation we receive. The feescompensation we receive areis subject to chargeback, or repayment, to the third-party finance company if a customer defaults or prepays the retail installment contract typically during some limited time period at the beginning of the contract term. We have negotiated agreements with certain lenders pursuant to which we receive additional feescompensation upon reaching a certain volume of business.

F&I revenue in our TCA segment represents the premium revenue earned from customers a variety of vehicle protectionfor F&I products primarily sold in connection with the purchase of vehicles. These productsvehicles at our dealerships. The premium revenue is recognized over the life of the F&I

10

product contract as services are underwrittenprovided. We capitalize costs, such as employee sales commissions, to obtain customer contracts, and administered by independent third-parties. Under our arrangements withamortize those costs over the providers of these products, we primarily sell the products on a straight commission basis. We are subject to chargebacks for insurance contracts as a result of early termination, default, or prepaymentlife of the contract. Amortization of costs to obtain customer contracts is included in selling, general and administrative expenses in the consolidated statements of income. The portion of commissions that are paid to affiliated dealerships are eliminated in the TCA segment upon consolidation. The Dealerships segment also provides vehicle repair and maintenance services to TCA customers in connection with claims related to TCA's products. Upon consolidation, the associated service revenue and costs recorded by the Dealerships segment are eliminated against claims expense recorded by the TCA segment. Third-party claims paid related to the contracts are recognized in F&I cost of sales.

In addition, we participate in future profits associated withF&I revenue includes investment income and other gains and losses related to the performance of the third-party held underlying portfolio for certain products pursuant to retrospective commission arrangements. The following is a brief description of some of the vehicle protection products we offer to our customers:

Business Strategy

We seek to be the most guest-centric automotive retailer and to create long-term value for our stockholders by striving to drive operational excellence and deploy capital to its highest risk adjusted returns. To achieve these objectives, we employ the strategies described below.

We are guided by our mission and vision to be the most guest-centric automotive retailer in the industry and use that framework as our North Star. We have designed our dealerships’ services to meet the needs of an increasingly sophisticated and demanding automotive consumer. We endeavor to establish relationships that we believe will result in both repeat business and additional business through customer referrals. Furthermore, we provide our dealership managers with appropriate incentives to employ efficient selling approaches, engage in extensive follow-up to develop long-term relationships with customers, and extensively train our sales staff to meet customer needs.

Accelerate same store growth and guest experience through technology investment.

As part of our long-term growth strategy, we invest in technologies or partner with leading software platform vendors to develop applications that (i) serve our guests with omni-channel buying options offering enhanced speed, and transparency, (ii) drive a more efficient guest experience at a lower cost to serve and (iii) offer tailored recommendations to value add products and services.

Grow F&I product penetration and expand TCA's service offerings across the full dealership portfolio.

We are positioned to leverage the acquisition of LHM to improve profitability via the ownership of TCA, a highly scalable provider of a full-suite of F&I products. TCA’s key offerings include vehicle service contracts, prepaid maintenance, protection plans, key and remote replacement, leased vehicle protection and tire and wheel protection. We are continuing to integrate TCA’s service offerings across our full dealership portfolio to increase our F&I product penetration and profitability. We expect to complete the rollout of TCA's service offerings to all of our dealerships in 2024.

Attract, retain and retaininvest in top talent to drive growth and optimize operations.

We believe the core of our business success lies in our talent pool, so we are focused on attracting, hiring and retaining the best talent

people. We also invest in resources to train and develop our employees. Our executive management team has extensive experience in the auto retail sector and is able to leverage experience from all positions throughout the Company. In addition, we believe that local management of dealership operations enables our retail network to provide market specific responses to sales, customer service and inventory requirements. The general manager of each of our dealerships is responsible for the operations, personnel and financial performance of that dealership as well as other day-to-day operations. We believe our general managers' familiarity with their respective markets enables them to effectively run day-to-day operations, market to customers, and recruit new employees. The general manager of each dealership is supported, in most cases, by a new vehicle sales manager, a used vehicle sales manager, an F&I manager, a parts manager, and a service manager. Our dealership management teams typically have many years of experience in the automotive retail industry. This management structure is complemented by support from our market-based management teams and the corporate office, which we refer to as the Dealership Support Center ("DSC"), through our advanced technology solutions, centralized processes, marketing support, and financial oversight.

Leverage our scale and cost structure to improve our operating efficienciesefficiencies.

We are positioned to leverage our significant scale so that we are able to achieve competitive operating margins by centralizing and streamlining various back-office functions. We are able to improve financial controls and lower servicing costs by maintaining key store-level accounting and administrative activities in our shared service centers, and we leverage our scale to reduce costs related to purchasing certain equipment, supplies, and services through national vendor relationships. Similarly, we are able to leverage our scale to implement these best practices when integrating newly acquired dealerships allowing us to continue to improve our operating efficiencies.

Deploy Capitalcapital to Highest Returnshighest returns and continue to invest in the business.

Our capital allocation decisions are made within the context of maintaining sufficient liquidity and a prudent capital structure. We continually evaluatetarget a 2.5x to 3.5x adjusted net leverage ratio, which is calculated as set forth in our investment opportunities based upon: (i)credit facility, in a normal

11

business environment. The Company’s adjusted net leverage ratio was 2.5x at December 31, 2023, compared to 1.7x at December 31, 2022. We believe our cash position and cash equivalents on hand, (ii) the funds that we expect to generate through future operations, (iii)borrowing capacity, combined with our current and expected borrowing availability under our credit facilities and mortgage financings, (iv) amountsfuture cash generation capability, provides us with financial flexibility to, among other things, reinvest in our new vehicle floor plan notes payable offset accounts,business, acquire dealerships and (v) the potential impact of any contemplated or pending future transactions, including, but not limited to, financings, acquisitions, dispositions or other capital expenditures.

We continually evaluate our existing dealership network and seek to make strategic investments whichthat will increase the capacity of our dealerships and improve the customer experience. In addition, we continue to execute on our strategy of selectively acquiring our leased properties where financing rates make it attractive to be an owner.owner and provide us a further means to finance our business.

Evaluate opportunities to refine ourthe dealership portfolio, including acquiring value added operating assets and dealershipsportfolio.

We evaluate dealership acquisition opportunities based on market position and geography, brand representation and availability, key personnel, and other factors. We believe our financial position, IT systems, management structure, and experience, position us to efficiently and opportunistically complete, integrate, and benefit from dealership acquisitions. We alsocontinually evaluate the financial and operating results of our owned dealerships, as well as each dealership'sdealership’s geographical location and, based on various financial and strategic rationales, may make decisions to dispose of dealerships to refine our dealership and real estate portfolio. We also evaluate dealership acquisition opportunities based on market position and geography, brand representation and availability, key personnel and other factors. Our approach to dispositions and acquisitions is highly disciplined with a focus on long-term strategic value to stockholders.

We continually evaluate additional opportunities to drive revenue growth while maintaining our disciplined approach to capital allocation. In February 2024, the Company announced an update to stockholders through share repurchase programs and/our strategic outlook targeting revenue of $30 billion or dividends

Competition

The automotive retail and service industry is highly competitive with respect to price, service, location, and selection. For new vehicle sales, our dealerships compete with other franchised dealerships, primarily in their regions. Our new vehicle store competitors also have franchise agreements with the various vehicle manufacturers, and as such, generally obtain new vehicle inventory from vehicle manufacturers on the same terms as us. The franchise agreements grant the franchised dealership a non-exclusive right to sell the manufacturer's (or distributor's) brand of vehicles and offer related parts and service within a specified market area. State automotive franchise laws restrict competitors from relocating their stores or establishing new stores of a

particular vehicle brand within a specified area that is served by our dealership of the same vehicle brand. Recently, certain electric vehicle manufacturers have been permitted to circumvent the state automotive franchise laws of several states in the United States thereby permitting them to sell their new vehicles directly to consumers. We rely on our advertising and merchandising, sales expertise, service reputation, strong local branding, and location of our dealerships to assist in the sale of new vehicles.

Our used vehicle operations compete with other franchised dealerships, non-franchised automotive dealerships, regional and national vehicle rental companies, and Internet-basedinternet-based vehicle brokers for the supply and resale of used vehicles.

We compete with other franchised dealerships to perform warranty and recall-related repairs and with other franchised dealerships and independent service centers for non-warranty repair and maintenance services. We compete with other automobile dealers, service stores, and auto parts retailers in our parts operations. We believe that we have a competitive advantage in parts and service sales due to our ability to use factory-approved replacement parts, our skilled manufacturer trained and certified technicians, our competitive prices, our familiarity with manufacturer brands and models, and the quality of our customer service.

We compete with a broad range of financial institutions in arranging financing for our customerscustomers' vehicle purchases. In addition, many financial institutions are now offering F&I products through the Internet,internet, which has increased competition and may reduce our profits on certain of these items. We believe that the principal competitive factors in providing financing are convenience, interest rates, and flexibility in contract length.

Seasonality

The automobile industry has historically been subject to seasonal variations. Demand for new vehicles is generally highest during the second, third, and fourth quarters of each year and, accordingly, we expect our revenues and operating results to generally be higher during these periods. In addition, we typically experience higher sales of luxury vehicles, in the fourth quarter, which have higher average selling prices and gross profit per vehicle retailed.retailed, in the fourth quarter. Revenues and operating results may be impacted significantly from quarter to quarter by changing economic conditions, vehicle manufacturer incentive programs, or adverse weather events.

12

Dealer and Framework Agreements

Each of our dealerships operate pursuant to a dealer agreement between the dealership and the manufacturer (or in some cases the distributor) of each brand of new vehicles sold and/or serviced at the dealership. The dealer agreements grant the franchised dealership a non-exclusive right to sell the manufacturer's (or distributor's) brand of vehicles and offer related parts and service within a specified market area. Each dealer agreement also grants our dealerships the right to use the manufacturer's trademarks and service marks in connection with the dealershipsdealerships' operations and they also impose numerous operational requirements related to, among other things, the following:

•inventories of new vehicles and manufacturer replacement parts;

•maintenance of minimum net working capital requirements, and in some cases, minimum net worth requirements;

•achievement of certain sales and customer satisfaction targets;

•advertising and marketing practices;

•facilities and signs;

•products offered to customers;

•dealership management;

•personnel training;

•information systems;

•geographic market, including but not limited to requirements to meet sales and service targets within an assigned market area, geographic limitations on where the dealership may locate or advertise, and restrictions on the export of vehicles; and

•dealership monthly and annual financial reporting.

Our dealer agreements are for various terms, ranging from one year to indefinite. We expect that we will be able to renew expiring agreements in the ordinary course of business. However, typical dealer agreements give the manufacturer the right to terminate or the option of non-renewal of the dealer agreement under certain circumstances, subject to applicable state automotive dealership franchise laws, including:

•insolvency or bankruptcy of the dealership;

•failure to adequately operate the dealership or to maintain required capitalization levels;

•impairment of the reputation or financial condition of the dealership;

•change of ownership or management of the dealership without manufacturer consent;

•certain extraordinary corporate transactions such as a merger or sale of all or substantially all of our assets without manufacturer consent;

•failure to complete facility upgrades required by the manufacturer or agreed to by the dealer;

•failure to maintain any license, permits or authorization required to conduct the dealership's business;

•conviction of a dealer/manager or owner for certain crimes; or

•material breach of other provisions of a dealer agreement.

Notwithstanding the terms of any dealer agreement, the states in which we operate have automotive dealership franchise laws thatwhich provide that it is unlawful for a manufacturer to terminate or not renew a franchise unless "good cause" exists.

In addition to requirements under dealer agreements, we are subject to provisions contained in supplemental agreements, framework agreements, dealer addenda and manufacturers' policies, collectively referred to as "framework agreements." Framework agreements impose requirements on us in addition to those described above. Such agreements also define other standards and limitations, including:

•company-wide performance criteria;

•capitalization requirements;

•limitations on changes in our ownership or management;

13

•limitations on the number of a particular manufacturer's franchises owned by us;

•restrictions or prohibitions on our ability to pledge the stock of certain of our subsidiaries; and

•conditions for consent to proposed acquisitions, including sales and customer satisfaction criteria, as well as limitations on the total local, regional, and national market share percentage that would be represented by a particular manufacturer's franchises owned by us after giving effect to a proposed acquisition.

Some dealer agreements and framework agreements grant the manufacturer the right to terminate or not renew our dealer and framework agreements, or to compel us to divest our dealerships, for a number of reasons, including default under the agreement, any unapproved change of control (which specific(specific changes vary from manufacturer to manufacturer, but which include material changes in the composition of our Board of Directors during a specified time period, the acquisition of 5% or more of our voting stock by another vehicle manufacturer or distributor, the acquisition of 20% or more of our voting stock by third parties, and the acquisition of an ownership interest sufficient to direct or influence management and policies), or certain other unapproved events (including certain extraordinary corporate transactions such as a merger or sale of all or substantially all of our assets). Triggers of the clauses are often based upon actions by our stockholders and are generally outside of our control. Some of our dealer agreements and framework agreements also give the manufacturer a right of first refusal if we propose to sell any dealership representing the manufacturer's brands to a third-party. These agreements may also attempt to limit the protections available under applicable state laws and require us to resolve disputes through binding arbitration. For additional information, please refer to the risk factor captioned "We are dependent upon our relationships with the manufacturers of vehicles that we sell and are subject to restrictions imposed by, and significant influence from, these vehicle manufacturers. Any of these restrictions or any changes or deterioration of these relationships could have a material adverse effect on our business, financial condition, results of operations, and cash flows."

Our framework agreements with certain manufacturers contain provisions that, among other things, attempt to limit the protections available to dealers under these laws. If these laws are repealed in the states in which we operate, manufacturers may be able to terminate our franchises without providing us with advance notice, an opportunity to cure or a showing of good cause. Without the protection of these laws, it may also be more difficult for us to renew our dealer agreements upon expiration.

Changes in laws that provide manufacturers the ability to terminate our dealer agreements could materially adversely affect our business, financial condition and results of operations. Furthermore, if a manufacturer seeks protection from creditors in

bankruptcy, courts have held that the federal bankruptcy laws may supersede these laws, resulting in either the termination, non-renewal or rejection of franchises by such manufacturers, which, in turn, could materially adversely affect our business, financial condition, and results of operations. For additional information, please refer to the risk factor captioned "If state laws that protect automotive retailers are repealed, weakened, or superseded by our framework agreements with manufacturers, our dealerships will be more susceptible to termination, non-renewal or renegotiation of their dealer agreements which could have a materially adverse effect on our business, financial condition, and results of operations."

Regulations

We operate in a highly regulated industry. In every state in which we operate, we must obtain one or more licenses issued by state regulatory authorities in order to operate our business. In addition, we are subject to numerous complex federal, state, and local laws regulating the conduct of our business, including those relating to our sales, operations, finance and insurance, advertising,marketing, and employment practices. These laws and regulations include state franchise laws and regulations, product standards and recalls, consumer protection laws, privacy and data security laws, anti-money laundering laws, and other extensive laws and regulations applicable to new and used motor vehicle dealers. These laws also include federal and state wage and hour, anti-discrimination, and other laws governing employment practices.

Industry Regulations

The Federal Trade Commission ("FTC") has regulatory authority over automotive dealers and has implemented enforcement initiatives relating to the marketing practices of automotive dealers. Our operations are also subject to the National Traffic and Motor Vehicle Safety Act, Federal Motor Vehicle Safety Standards and other product standards promulgated by the United States Department of Transportation, and the rules and regulations of various state motor vehicle regulatory agencies.

Our financing activities with customers are subject to federal truth-in-lending, consumer leasing, and equal credit opportunity laws and regulations, as well as state and local motor vehicle finance laws, leasing laws, installment finance laws, usury laws, and other installment state and leasing laws and regulations. Some U.S. states regulate fees and charges that may be paidcollected as a result of vehicle sales.sales and service. Claims arising out of actual or alleged violations of law may be asserted against us or our stores by individuals or governmental entities and may expose us to significant damages, fines or other penalties, including revocation or suspension of our license to conduct store operations. Our financing activities, as well as our sale of finance and insurance products, may also be impacted indirectly by laws and regulations that govern automotive finance

14

companies and Consumer Protection Act was signed into law and establishedother financial institutions, including regulations adopted by the Consumer Financial Protection Bureau ("CFPB"(the "CFPB") with broad regulatory powers. Although automotive dealers are generally excluded from.

Our TCA business involves the CFPB's regulatory authority, the CFPB has announced its intention to regulate automotive financing activities through its regulationoffer and sale of automotive finance companiesextended vehicle service contracts, debt protection products, vehicle protection plans and other financial institutions that service the automotive industry.miscellaneous vehicle protection products, which are subject to a wide range of federal, state and local laws and regulations. The CFPB has issued regulatory guidance instructing financial institutions to monitor dealer lending practices for potential discrimination, resulting from the system used to compensate dealers for assisting in the customer financing transaction. The CFPB has instructed lenders that, if discrimination is found, the lender would be required to change dealer compensation practices. In addition, the CFPB has announced its intention to regulate the saleDepartments of other finance and insurance products. The Federal Trade Commission has certainInsurance of U.S. states have regulatory authority over automotive dealersour TCA business. Our TCA business is subject to state licensing and has implemented an enforcement initiative relating to the advertising practices of automotive dealers.registration requirements, and financial responsibility and security requirements. For additional information, please refer to the risk factor captionedfactors captioned: "Our operations are subject to extensive governmental laws and regulations. If we are found to be in purported violation of or subject to liabilities under any of these laws or regulations, or if new laws or regulations are enacted that adversely affect our operations, our business, our reputation, financial condition, results of operations, and prospects could suffer" and "Our TCA business is subject to a wide range of federal, state and local laws and regulations, some of which we may not have previously been subject. If we are found to be in purported violation of or subject to liabilities under any of these laws or regulations, or if new laws or regulations are enacted that adversely affect our TCA business, our business, results of operations, financial condition, cash flows, reputation and prospects could suffer."

Environmental, Health and Safety Laws and Regulations

We are subject to a wide range of environmental laws and regulations, including those governing discharges into water, air emissions, storage of petroleum substances and chemicals, handling and disposal of solid and hazardous wastes, remediation of various types of contamination, and otherwise relating to health, safety and protection of the environment. For example, and without creating an exhaustive list: as with automobile dealerships generally, and service and parts and collision repair center operations in particular, our business involves the generation, use, handling, and disposal of hazardous or toxic substances and wastes and the use of above ground and underground storage tanks (ASTs and USTs). Operations involving the management of wastes and the use of ASTs and USTs are subject to requirements of the Resource Conservation and Recovery Act, analogous state statutes, and their implementing regulations. Pursuant to these laws, federal and state environmental agencies have established approved methods for handling, storing, treating, transporting, and disposing of regulated substances and wastes with which we must comply. We also are subject to laws and regulations governing responses to any releases of contamination at or from our facilities or at facilities that receive our hazardous wastes for treatment or disposal. The Comprehensive Environmental Response, Compensation and Liability Act ("CERCLA") and similar state statutes, can impose strict and joint and several liability for cleanup costs on those that are considered to have contributed to the release of a "hazardous substance." We also are subject to the Clean Water Act, analogous state statutes, and their implementing regulations which, among other things, prohibit discharges of pollutants into regulated waters without permits, require containment of potential discharges of oil or hazardous substances, and require preparation of spill contingency plans. Currently, we are not aware of any non-compliance with these or any other environmental requirements applicable to our operations, nor are we aware of any material remedial liabilities to which we are subject.

We have incurred, and will continue to incur, costs and capital expenditures to comply with these laws and regulations and to obtain and maintain all necessary environmental permits.regulations. We believe that our operations currently are being conducted in substantial compliance with all applicable environmental laws.regulations. From time to time, we may experience incidents and encounter conditions that are not in compliance with environmental laws and regulations. We may occasionally receive notices from environmentalgovernmental agencies regarding potential violations of environmentalthese laws or regulations. In such cases, we will work with the agencies to address any issues and to implement appropriate corrective action when necessary. However, none of our dealerships havehas been subject to any material environmental liabilities in the past, nor do we know of any fact or condition that would result in any material environmental liabilities being incurred in the future.

Mission and Vision

At Asbury, our North Star and our mission is to be the most guest-centric automotive retailer. Our success depends on our employees and their commitment to delivering a consistent and exceptional guest experience. Our employees work at locations in Colorado, Florida, Georgia, Indiana, Missouri, South Carolina, Texas, California, Arizona, New Mexico, Idaho, Utah, Washington, Virginia, Maryland and Delaware. We believe that our employees help to set us apart from our competitors, and, therefore, we understand they are our greatest asset. As a result, a critical part of our business strategy is investing in, supporting and developing our employees so that they are trained and incentivized to provide best-in-class service to our guests.

As of December 31, 2017,2023, we employed approximately 8,00015,000 full-time and part-time employees, none of whom were covered by collective bargaining agreements. We believe we have good relations with our employees.

We strive to recruit new employees based on their diversity of thought, background and experience as well as diversity of personal characteristics to best reflect our guests and communities we serve.

15

The goal of our diversity, equity and inclusion ("DE&I") efforts is to create more welcoming and inclusive workplaces throughout our dealerships and offices to enable us to attract, retain and develop the careers of diverse, highly talented team members. We intend to continue to learn and develop - working towards building a workplace where every Asbury team member feels included and welcomed.Our Chief Diversity Equity and Inclusion Officer and her team lead the strategic focus and execution of our DE&I strategy in partnership with our operations leadership and support teams throughout the company.

Community Outreach

Through our Asbury Cares program, we support selected community partner organizations to focus on reducing social inequality. Since 2021, we have awarded all of our employees with an additional 40 hours of paid time off per year that can only be used to volunteer with our local community partners. We have seen significant year-over-year growth in employee participation in our community engagement events.

A significant portion of our Asbury Cares Community Initiative revolves around education and making sure that young people in underserved communities have access to a quality education. We formed a partnership with HBCU Change, an app-based organization that lets users round up their spending and donate to historically black colleges and universities ("HBCU"). We learned that many HBCUs historically lag in funding and resources compared to other public or private universities and many have closed their doors in recent years. Many of our Asbury team members are proud HBCU alumni and these institutions provide a unique community of support and understanding for not only African American students, but students of all races and backgrounds.

In partnership with HBCU Change, we launched a campaign to help raise funds for HBCUs across the country and in the local communities where we operate. All the point-of-sale credit card machines in all our locations show a prompt asking our guests if they would like to round up their change or donate $1, $3, $5, or a custom amount to HBCUs in their communities. At the end of each quarter, the funds raised are donated to the HBCUs across the country. Through donations from our guests and company match, we have contributed more than $1 million to HBCUs since the start of our partnership with HBCU Change in May 2021.

Recruitment and Talent Development

When recruiting for open positions, we search for people of varying backgrounds, perspectives, and experiences in order to support a diverse and inclusive culture. We also partner with local colleges and trade schools to develop apprenticeship and internship programs. This allows us to help provide valuable training to entry-level candidates while also growing our pipeline.

Our goal is to promote employees from within to career growth opportunities whenever possible. We invest resources to train and develop our employees to reach their career goals. In 2022, we launched a training curriculum for all store positions. In addition, we offer our employees access to an online career path tool, which helps them plan their desired career path and see the required performance goals and milestones to be considered for a promotion. Our fixed operations organization encourages technicians to obtain and maintain certification status with our vehicle manufacturers, and in most cases, our dealership pays for the training. Our employees also attend vehicle manufacturer-sponsored and industry training events.

We pride ourselves on rewarding and developing talented and tenured employees.

Compensation and Benefits

We offer competitive compensation and benefits to attract and retain the best people, including the following benefits for our full-time employees:

•Health, dental, and vision benefits with multiple plan choices;

•Discounted healthcare premiums for biometric screening and completion of health survey; and

•Employee assistance program.

Saving and retirement

•Holiday match; and

•401(k) match.

16

Paid time off

•Up to 4 weeks paid time off;

•Paid pregnancy leave; and

•Paid parental leave.

Disability and accident insurance

•Short-term disability and long-term disability insurance;

•Accident insurance, hospital indemnity, employee critical illness insurance;

•Employer paid life insurance; and

•Supplemental life insurance.

Scholarships for education

•Annual scholarship program.

Broad employee equity ownership

•We also lead the industry by offering equity awards to frontline employees because we want them to be owners of our Company and committed to our long-term success.

Self-Insurance Programs

Due to the inherent risk in the automotive retail industry, our operations expose us to a variety of liabilities. These risks generally require significant levels of insurance covering liabilities such as claims from employees, customers, or other third parties, for personal injury and property relatedproperty-related losses occurring in the course of our operations. We may be subject to fines and civil and criminal penalties in connection with alleged violations of federal and state laws or regulatory environments. Further, the automobile retail industry is subject to substantial risk of real and personal property loss, due to the significant concentration of property values located at the various dealership locations.

Provisions for retained losses and deductibles are made by charges to expense based upon periodic evaluations of the estimated ultimate liabilities on reported and unreported claims. The insurance companies that underwrite our insurance require that we secure certain of our obligations for deductible reimbursements with collateral. Our collateral requirements are set by the insurance companies and, to date, have been satisfied by posting surety bonds, letters of credit, and/or cash deposits. Our collateral requirements may change from time to timetime-to-time based on, among other things, our claims experience.

17

Item 1A. Risk Factors

In addition to the other information contained, referred to or incorporated by reference into this report, you should consider carefully the following factors when evaluating our business and before making an investment decision. Our business, operations, ability to implement our strategy, reputation, results of operations, financial condition, cash flows, and prospects may be materially adversely affected by the risks described below. In addition, other risks or uncertainties not presently known to us or that we currently do not deem material could arise, any of which could also materially adversely affect us.

Risks Related to Our Business

Operating Risks

Disruptions in the production and delivery of new vehicles and parts from manufacturers due to the lack of availability of parts and key components from suppliers could have a material adverse effect on our business, results of operations, financial condition and cash flows.

Historically, we have generated a significant portion of our revenue through new vehicle sales, and new vehicle sales also tend to lead to sales of higher-margin products and services, such as F&I products and vehicle-related parts and service.In addition, new vehicle buyers often trade in an owned vehicle, or turn in a leased vehicle, to us at the time of purchase, and these traded vehicles have historically been an important source for our used vehicle inventory. We rely exclusively on the various vehicle manufacturers for our new vehicle inventory and maintenance and replacement parts inventory. In turn, our vehicle manufacturers rely on certain third-party suppliers to manufacture and deliver certain parts and key components for their vehicles. As a result, our profitability is dependent to a great extent on various aspects of vehicle manufacturers’ operations and timely delivery of new vehicles and parts.

Property loss or other uninsured liabilities could have a material adverse impact on our results of operations.

We are subject to substantial risk of property loss due to the significant concentration of property at dealership locations, including vehicles and parts. We have historically experienced business interruptions from time to time at several of our dealerships, due to actual or threatened adverse weather conditions or natural disasters, such as hurricanes, earthquakes, tornadoes, floods, hail storms, fires or other extraordinary events. Concentration of property at dealership locations also makes the automotive retail business particularly vulnerable to theft, fraud and misappropriation of assets. Illegal or unethical conduct by employees, customers, vendors, and unaffiliated third parties can result in loss of assets, disrupt operations, impact brand reputation, jeopardize manufacturer and other relationships, result in the imposition of fines or penalties, and subject us to governmental investigations or lawsuits. While we maintain insurance to protect against a number of losses, this insurance coverage often contains significant deductibles. In addition, we "self-insure" a portion of our potential liabilities, meaning we do not carry insurance from a third-party for such liabilities, and are wholly responsible for any related losses including for certain potential liabilities that some states prohibit the maintenance of insurance to protect against. In certain instances, our insurance may not fully cover a loss depending on the applicable deductible or the magnitude and nature of the claim. Additionally, changes in the cost or availability of insurance in the future could substantially increase our costs to maintain our current level of coverage or could cause us to reduce our insurance coverage and increase our self-insured risks. To the extent we incur significant additional costs for insurance, suffer losses that are not covered by in-force insurance or suffer losses for which we are self-insured, our financial condition, results of operations and cash flows could be materially adversely impacted.

If we are unable to acquire and successfully integrate additional businesses into our existing operations, and realize expected benefits and synergies from such acquisitions, our revenue and earnings growth may be adversely affected.

We believe that the automotive retailing industry is a mature industry whose sales are significantly impacted by the prevailing economic climate, both nationally and in local markets. Accordingly, we believe that our future growth depends in part on our ability to manage expansion, control costs in our operations and acquire and effectively integrate acquired dealerships into our organization. For example, with the recent consummation of the Koons acquisition, we will experience significantly more sales, and have more assets and employees than we did prior to the transaction. The integration processes require us to expend significant capital and significantly expand the scope of our operations and financial systems. Integration also requires support or other actions by third-parties such as vendors, suppliers, and licensing agencies and the untimely or inadequate responses from such third-parties can delay or otherwise negatively impact the integration process.

When seeking to acquire other dealerships, we often compete with several other national, regional and local dealership groups, and other strategic and financial buyers, some of which may have greater financial resources than us. Competition for attractive acquisition targets may result in fewer acquisition opportunities for us and we may have to forgo acquisition opportunities to the extent we cannot negotiate such acquisitions on acceptable terms.

18

We also face additional risks commonly encountered with growth through acquisitions. These risks include, but are not limited to: (i) failing to obtain manufacturers’ consents to acquisitions of additional franchises; (ii) incurring significant transaction-related costs for both completed and failed acquisitions; (iii) incurring significantly higher capital expenditures and operating expenses; (iv) failing to integrate the operations and personnel of the acquired dealerships and impairing relationships with employees; (v) incorrectly valuing entities to be acquired or incurring undisclosed liabilities at acquired dealerships; (vi) disrupting our ongoing business and diverting our management resources to newly acquired dealerships; (vii) failing to achieve expected performance levels; (viii) impairing relationships with manufacturers and customers as a result of changes in management; (ix) failing to realize expected benefits and synergies from the transaction; and (ix) failing to implement or improve controls, policies and information systems and related security measures in the acquired businesses.

We may not adequately anticipate all the demands that our growth will impose on our personnel, procedures and structures, including our financial and reporting control systems, information technology systems, data processing systems, and management structure. Moreover, our failure to retain qualified management personnel at any acquired dealership may increase the risks associated with integrating the acquired dealership. If we cannot adequately anticipate and respond to these demands, we may fail to realize acquisition synergies and our resources will be focused on incorporating new operations into our structure rather than on areas that may be more profitable.

We are a holding company and as a result are dependent on our operating subsidiaries to generate sufficient cash and distribute cash to us to service our indebtedness and fund our ongoing operations.

Our ability to make payments on our indebtedness and fund our ongoing operations depends on our operating subsidiaries' ability to generate cash in the future and distribute that cash to us. It is possible that our subsidiaries may not generate cash from operations in an amount sufficient to enable us to service our indebtedness. In addition, many of our subsidiaries are required to comply with the provisions of franchise agreements, dealer agreements, other agreements with manufacturers, mortgages, and credit facility providers. Many of these agreements contain minimum working capital or net worth requirements, and are subject to change at least annually. Although the requirements contained in these agreements did not restrict our subsidiaries from distributing cash to us as of December 31, 2023, unexpected changes to our financial metrics or to the terms of our franchise agreements, dealer agreements, or other agreements with manufacturers could require us to alter the manner in which we distribute or use cash. If our operating subsidiaries are unable to generate and distribute sufficient cash to us to service our indebtedness and fund our ongoing operations, our financial condition may be materially adversely affected.

Our inability to execute a substantial portion of our business strategy, including our mission to grow and transform our business, could have an adverse effect on our business, results of operations, financial condition and cash flows.

Our inability to execute a substantial portion of our business strategy, could adversely affect our business, results of operations, financial condition and cash flows. We seek to execute on our strategic plan using a variety of growth efforts including, driving same-store revenue growth and acquiring additional revenue through strategic acquisitions. Many of the factors that impact our ability to execute our strategic vision, such as the advancement of certain technologies, general economic conditions and legal and regulatory obstacles are beyond our control.

Consumers are increasingly shopping for new and used vehicles, automotive repair and maintenance service and other automotive products and services online and through mobile applications, including through third-party online and mobile sales platforms, with which we compete, that are designed to generate consumer sales that are sold to automotive dealers. We have invested and will continue to invest in our omni-channel and other online applications in furtherance of our strategic vision. We face increased competition for market share from other automotive retailers and other sales platforms that have also invested in digital channels. There can be no assurance that our initiatives and investments in digital channels will be successful or result in improved financial performance.

We may not adequately anticipate all the demands that our growth will impose on our personnel, procedures and structures, including our financial and reporting control systems, information technology systems, data processing systems, and management structure. Furthermore, we may decide to alter or discontinue aspects of our strategic plan and may adopt alternative or additional strategies in response to business or competitive factors or other factors or events beyond our control. We cannot give assurance that we will be able to execute a substantial portion of our strategic plan which could have a material adverse effect on our business, financial condition, results of operations, and cash flows.

19

Goodwill and manufacturer franchise rights comprise a significant portion of our total assets. We must test our goodwill and manufacturer franchise rights for impairment at least annually, which could result in a material, non-cash write-down of goodwill or manufacturer franchise rights and could have a material adverse effect on our results of operations and stockholders’ equity.