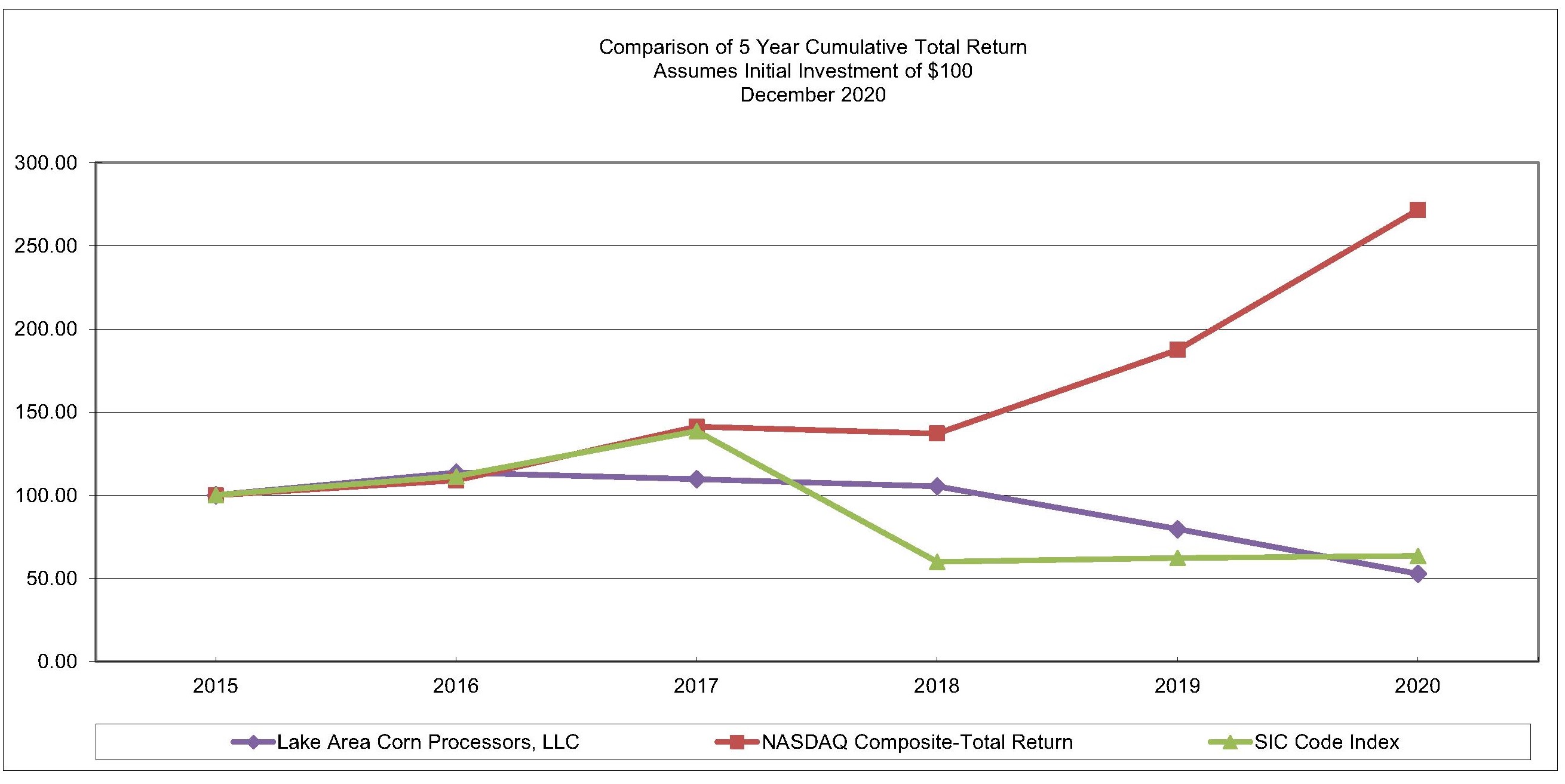

INDEX

| Page No. | |||||

2

CAUTIONARY STATEMENTS REGARDING FORWARD-LOOKING STATEMENTS

This annual report contains historical information, as well as forward-looking statements that involve known and unknown risks and relate to future events, our future financial performance, or our expected future operations and actions. In some cases, you can identify forward-looking statements by terms such as "may," "will," "should," "expect," "plan," "anticipate," "believe," "estimate," "future," "intend," "could," "hope," "predict," "target," "potential," or "continue" or the negative of these terms or other similar expressions. These forward-looking statements are only our predictions based upon current information and involve numerous assumptions, risks and uncertainties. Our actual results or actions may differ materially from these forward-looking statements for many reasons, including the reasons described in this report. While it is impossible to identify all such factors, factors that could cause actual results to differ materially from those estimated by us include:

•A slowdown in global and regional economic activity, demand for our products and the potential for labor shortages and shipping disruptions resulting from pandemics including COVID-19;

•Reductions in the corn-based ethanol use requirement in the Federal Renewable Fuels Standard;

•The impact of small refinery exemptions from the RFS which have reduced ethanol demand;

•Oversupply in the ethanol industry resulting in lower market ethanol prices;

•Negative operating margins which result from lower ethanol prices;

•Lower ethanol prices due to the Chinese and Brazilian ethanol tariffs;

•Lower distillers grains prices due to the Chinese antidumpinganti-dumping and countervailing duty tariffs;

•Lower gasoline prices may negatively impact ethanol prices which could hurt our profitability;

•Availability and costs of raw materials, particularly corn and natural gas;

•Changes in the price and market for ethanol, distillers grains and corn oil;

•Our ability to maintain liquidity and maintain our risk management positions;

•Changes in the availability and cost of credit;

•Changes and advances in ethanol production technology;

•The effectiveness of our risk management strategy to offset increases in the price of our raw materials and decreases in the prices of our products;

•Overcapacity within the ethanol industry causing supply to exceed demand;

•Our ability to market and our reliance on third parties to market our products;

•The decrease or elimination of governmental incentives which support the ethanol industry;

•Changes in the weather or general economic conditions impacting the availability and price of corn;

•Our ability to generate free cash flow to invest in our business and service our debt;

•Changes in plant production capacity or technical difficulties in operating the plant;

•Changes in our business strategy, capital improvements or development plans;

•Our ability to retain key employees and maintain labor relations;

•Our liability resulting from potential litigation;

•Competition from alternative fuels and alternative fuel additives; and

•Other factors described elsewhere in this report.

The cautionary statements referred to in this section also should be considered in connection with any subsequent written or oral forward-looking statements that may be issued by us or persons acting on our behalf. We undertake no duty to update these forward-looking statements, even though our situation may change in the future. Furthermore, we cannot guarantee future results, events, levels of activity, performance, or achievements. We caution you not to put undue reliance on any forward-looking statements, which speak only as of the date of this report. You should read this report and the documents that we reference in this report and have filed as exhibits completely and with the understanding that our actual future results may be materially different from what we currently expect. We qualify all of our forward-looking statements by these cautionary statements.

3

PART I

ITEM 1.BUSINESS.

Overview

Lake Area Corn Processors, LLC is a South Dakota limited liability company that owns and manages an ethanol plant that has a nameplate production capacity of 4090 million gallons of ethanol per year through its wholly-owned subsidiary Dakota Ethanol, L.L.C. The ethanol plant producerscurrently produces at rates in excess of 5090 million gallons of ethanol per year. The ethanol plant is located near Wentworth, South Dakota. Lake Area Corn Processors, LLC is referred to in this report as "LACP," the "Company," "we," or "us." Dakota Ethanol, L.L.C. is referred to in this report as "Dakota Ethanol" or the "ethanol plant."

Since September 4, 2001, we have been engaged in the production of ethanol and distillers grains. Fuel grade ethanol is our primary product accounting for the majority of our revenue. We also sell distillers grains and corn oil, the principal co-products of the ethanol production process.

The ethanol industry experienced industry-wide record low ethanol prices throughout most of 2018 and 2019 due to reduced demand and high industry inventory levels. This continued into 2020 and the situation was compounded by the crisis associated with the 2019 novel coronavirus disease (“COVID-19”). In response to these unfavorable operating conditions and a slowdown in global and regional economic activity and a disruption in transportation fuel demand resulting from the COVID-19 pandemic, we reduced our ethanol production rate early in 2020 which impacted our total ethanol production for our 2020 fiscal year.

General Development of Business

LACP was formed as a South Dakota cooperative on May 25, 1999. On August 20, 2002, our members approved a plan to reorganize into a South Dakota limited liability company. The reorganization became effective on August 31, 2002, and the assets and liabilities of the cooperative were transferred to the newly formed limited liability company. Following the reorganization, our legal name was changed to Lake Area Corn Processors, LLC.

Our ownership of Dakota Ethanol represents our primary asset and source of revenue. Since we operate Dakota Ethanol as a wholly-owned subsidiary, all net income generated by Dakota Ethanol is passed to LACP. We make distributions of the income received from Dakota Ethanol to our unit holders in proportion to the number of units held by each member comparedmember.

We entered into a loan agreement with the Small Business Association through First State Bank, Gothenburg, NE on April 4, 2020 for $760,400 as part of the Paycheck Protection Program under Division A, Title I of the Coronavirus Aid, Relief and Economic Security Act (CARES Act). The loan matures in January 2023 and has an interest rate of 1%. Proceeds of the loan are restricted for use towards payroll costs and other allowable uses such as covered utilities for incurred before December 31, 2020 under the Paycheck Protection Program Rules. Provisions of the agreement allow for a portion of the loan to be forgiven if certain qualifications are met. We applied for forgiveness of this loan. The Paycheck Protection Program Flexibility Act, which was put into effect on June 5, 2020, may effect the units held byterms of our members generally.loan.

On July 11, 2017,June 5, 2020, we madeentered into a $10 million investment in Ring-neck Energy & Feed, LLC. Ring-neck Energy & Feed, LLC plans to construct an ethanol plant in Onida, South Dakota. We have the right to appoint a member of Ring-neck Energy & Feed, LLC's board of managers.

During our 2019 fiscal year, we completed a new $8 million term loan which we used to finance a portion of our investment in Ring-neck Energy & Feed, LLC. We agreed to make annual principal payments of $1 million plus accrued interest starting on August 1, 2018 and annually thereafter until the maturity date on August 1, 2025.

Financial Information

Please refer to "Item 7 - Management's Discussion and Analysis of Financial Condition and Results of Operations" for information regarding our results of operations and "Item 8 - Financial Statements and Supplementary Data" for our audited consolidated financial statements.

4

Principal Products

The principal products produced at the ethanol plant are fuel grade ethanol, distillers grains and corn oil. The table below shows the approximate percentage of our total revenue which is attributed to each of our primary products for each of our last three fiscal years.

| Product | Fiscal Year 2020 | Fiscal Year 2019 | Fiscal Year 2018 | |||||||||||||||||

| Ethanol | 76% | 78% | 77% | |||||||||||||||||

| Distillers Grains | 20% | 18% | 20% | |||||||||||||||||

| Corn Oil | 4% | 4% | 3% | |||||||||||||||||

| Product | Fiscal Year 2017 | Fiscal Year 2016 | Fiscal Year 2015 | |||

| Ethanol | 79% | 78% | 76% | |||

| Distillers Grains | 17% | 18% | 20% | |||

| Corn Oil | 4% | 3% | 3% | |||

Ethanol

Ethanol is ethyl alcohol, a fuel component made primarily from corn and various other grains. Ethanol is primarily used as: (i) an octane enhancer in fuels; (ii) an oxygenated fuel additive for the purpose of reducing ozone and carbon monoxide vehicle emissions; and (iii) a non-petroleum-based gasoline substitute. Ethanol produced in the United States is primarily used for blending

with unleaded gasoline and other fuel products. Ethanol blended fuel is typically designated in the marketplace according to the percentage of the fuel that is ethanol, with the most common fuel blend being E10, which includes 10% ethanol. The United States Environmental Protection Agency ("EPA") has approved the use of gasoline blends that contain 15% ethanol, or E15, for use in all vehicles manufactured in model year 2001 and later. In addition, flexible fuel vehicles can use gasoline blends that contain up to 85% ethanol called E85.

An ethanol plant is essentially a fermentation plant. Ground corn and water are mixed with enzymes and yeast to produce a substance called "beer," which contains approximately 15% alcohol, 11% solids and 74% water. The "beer" is boiled to separate the water, resulting in ethyl alcohol, which is then dehydrated to increase the alcohol content. This product is then mixed with a certified denaturant, such as gasoline, to make the product unfit for human consumption which allows it to be sold commercially.

Distillers Grains

A principal co-product of the ethanol production process is distillers grains, a high protein, high-energy animal feed supplement primarily marketed to the dairy and beef industry. We primarily produce distillers grains in two forms, modified/wet distillers grains and dried distillers grains. Modified/wet distillers grains have a higher moisture content than dried distillers grains. Our modified/wet distillers grains are sold primarily in our local market because they have a shorter shelf life and are more expensive to transport than dried distillers grains.

Corn Oil

We separate a portion of the corn oil contained in our distillers grains which we market separately from our distillers grains. The corn oil that we produce is not food grade corn oil and therefore cannot be used for human consumption. The primary uses for the corn oil that we produce are animal feed, industrial uses and biodiesel production.

Principal Product Markets

Ethanol

The primary market for our ethanol is the domestic fuel blending market. However the ethanol industry has focused on increasing ethanol exports. According to the U.S. Energy Information Administration, Brazil, Canada, India and Mexico were top destinations for ethanol exports in recent years2020. However, overall exports of ethanol for this period decreased compared to the same period last year due to escalating trade barriers and the impacts of COVID-19. Tariffs implemented by Brazil and China on ethanol imported from the United States has experienced increasedreduced export demand from these markets. Trade barriers with key markets may continue to take a toll on ethanol exports. This increase inexport demand negatively effecting domestic ethanol exports follows a conscious effort by the United States ethanol industry to expand ethanol exports along with lower ethanol prices which encouraged exports. During 2017, the primary export markets served by the United States ethanol industry were Canada, Brazil, India, China, South Korea, the Philippines and Peru. However, ethanolprices. Ethanol export demand is more unpredictable than domestic demand and tends to fluctuate throughout the year as it is subject to monetary and political forces in other nations. BothAn example of this, the imposition of a tax on imported ethanol by Brazil and China, each a major sourcehas created uncertainty as to the viability of export demand in the past, have instituted tariffs onthat market for ethanol produced in the United States during 2017. The imposition of these tariffs have resulted in a decline in demand from these top importers requiringand has required the United States producers to seek out alternative markets.

5

Export demand has negatively impacted ethanol exports to the European Union, other countries have increased their ethanol imports. Further, some ethanol exports to the European Union have continued despite the tariffalso decreased due to the relatively lower price of ethanol produceddisruption in global fuel demand resulting from travel restrictions in response to the United States.COVID-19 pandemic. Restricted travel, new lockdown measures and slow economic growth continue to have a negative effect on global fuel consumption and it is unknown when such demand will recover as reopening efforts continue to evolve.

Ethanol is generally blended with gasoline before it is sold to the end consumer. Therefore, the primary purchasers of ethanol are fuel blending companies which mix the ethanol we produce with gasoline. As discussed below in the section entitled "Distribution of Principal Products," we have a third party marketer that sells all of our ethanol. Our ethanol marketer makes substantially all decisions regarding where our ethanol is sold.

Distillers Grains

Distillers grains are primarily used as animal feed. Distillers grains are typically fed to animals instead of other traditional animal feeds such as corn and soybean meal. Distillers grains exports have increased in recent years as distillers grains have become a more accepted animal feed. Currently, the United States ethanol industry exports a significant amount of distiller grains. During 2017,According to the U.S. Grains Council, during the 2019/2020 marketing year, the largest importers of United States distiller grains were Mexico, Turkey,China, Canada, Japan, Colombia and South Korea, Thailand, China and Canada. Korea.

During 2016, China began an anti-dumping and countervailing duty investigation related to distillers grains imported from the United States which contributed to a decline in distillers grains shipped to China. In September 2016, China issued a preliminary ruling on the anti-dumping investigation imposing an immediate duty on distillers grains that are produced in the United States.

We anticipate that the vast majority of our distillers grains will continue to be sold in the domestic market due to our plant's location. Further, management anticipates that we will continue to sell a large proportion of our distillers grains in the modified/wet form which is marketed locally.

Corn Oil

The primary markets for corn oil are the industrial chemicals market, animal feeding market and the biodiesel production market. Corn oil demand was higher during 2017 due to increased biodiesel production. ThisThe biodiesel blenders' tax credit expired at the end of 2016.2017. However, in early 2018on December 20, 2019, the biodiesel blenders' tax credit was reinstated retroactively for 20172018 and 2019 after it expired at the end of 2016, but no2017, and a forward looking extension was included so this may not provide support for corn oil prices during our 2018 fiscal year.the years 2020, 2021, and 2022. Since corn oil can be used as a feedstock to produce biodiesel, when biodiesel production increases it has a positive impact on corn oil prices. Further,However, additional corn oil supply has continued to enter the market which has negatively impacted corn oil prices. The market for corn oil is expected to continue to shift as changes in supply and demand of corn oil interact. Our corn oil is primarily marketed in the United States and we do not expect that significant exports of corn oil will occur in the near future.

Distribution of Principal Products

Ethanol Distribution

We have an ethanol marketing agreement with RPMG, Inc. ("RPMG"), a professional third party marketer, which is the sole marketer of our ethanol. We are an equity owner of Renewable Products Marketing Group, LLC ("RPMG, LLC"), the parent company of RPMG, which allows us to realize favorable marketing fees in the sale of our ethanol, distillers grains and corn oil. Our ethanol marketing agreement provides that we can sell our ethanol either through an index arrangement or at a fixed price agreed to between us and RPMG. The term of our ethanol marketing agreement is perpetual, until it is terminated according to the terms of the agreement. The primary reasons our ethanol marketing agreement would terminate are if we cease to be an owner of RPMG, LLC, if there is a breach of our ethanol marketing agreement which is not cured, or if we give advance notice to RPMG that we wish to terminate our ethanol marketing agreement. Notwithstanding our right to terminate our ethanol marketing agreement, we may be obligated to continue to market our ethanol through RPMG for a period of time after termination. Further, following termination we agreed to accept an assignment of certain railcar leases which RPMG has secured to service our ethanol sales. If our ethanol marketing agreement is terminated, it would trigger a redemption by RPMG, LLC of our ownership interest in RPMG, LLC.

6

Distillers Grains Distribution

Other than the distillers grains that we market locally without a third party marketer, our distillers grains are marketed by RPMG. Our distillers grains marketing agreement with RPMG automatically renews for additional one-year terms unless notice of termination is given as provided by the distillers grains marketing agreement. We pay RPMG a commission based on each ton of distillers grains sold by RPMG.

We market a portion of our distillers grains to our local market without the use of an external marketer. Currently, we market approximately 65%62%, based on volume, of our distillers grains internally. Shipments of these products are made to local markets by truck. This has allowed us to sell less distillers grains in the form of dried distillers grains which has decreased our natural gas usage and improved our margins from the sale of distillers grains.

Corn Oil Distribution

We market all of our corn oil through RPMG. Our corn oil marketing agreement automatically renews for additional one year terms unless either party gives 180 days notice that the agreement will not be renewed. We pay RPMG a commission based on each pound of our corn oil that is sold by RPMG.

New Products and Services

We did not introduce any new products or services during our20172020 fiscal year.

Patents, Trademarks, Licenses, Franchises and Concessions

We do not currently hold any patents, trademarks, franchises or concessions. We were granted a license by Broin and Associates, Inc. ("Broin"), the company that designed and built the ethanol plant, to use certain ethanol production technology necessary to operate our ethanol plant. The cost of the license granted by Broin was included in the amount we paid Broin to design and build our ethanol plant.

Sources and Availability of Raw Materials

Corn Feedstock Supply

The major raw material required for our ethanol plant to produce ethanol, distillers grains and corn oil is corn. The plant operates at a rate in excess of its nameplate capacity of 4090 million gallons of ethanol per year, producingyear. We anticipate using approximately 51 million gallons of ethanol annually from approximately 1831 million bushels of corn. The area surrounding the ethanol plant currentlyusually provides an ample supply of corn to meet and exceed our raw material requirements for the production capacity of the plant.

Corn prices have been volatile in recent years due to changes in corn demand as well as yield and production fluctuations that have had a significant impact on corn prices. CornHigh corn prices were lower during our 2017 fiscal year as a result of five consecutive years of favorable corn crops which has increased the amount of corn available to us. As a result of these favorable corn crops, we have not had difficulty securing the corn we need to operate the ethanol plant at prices that have allowed us to operate profitably. However, as we experienced during 2012, an unfavorable corn crop can have a significant negative impacteffect on our profitability.operating margins unless the price of ethanol and distillers grains out paces rising corn prices. We could experience a drought or other unfavorable weather conditionconditions during our 20182021 fiscal year which could impact the price we pay for corn and could negatively impact the availability of corn near our plant. If we experience a localized shortage of corn, we may be forced to purchase corn from producers who arelocated farther away from our ethanol plant which can increase our transportation costs. In addition, if new corn customers enter the market, it can increase demand for corn which could result in higher corn prices. Since corn is the primary raw material we use to produce our products, the availability and cost of corn can have a significant impact on the profitability of our operations.

Corn is supplied to us primarily from our members who are local agricultural producers and from purchases of corn on the open market. We anticipate purchasing corn from third parties should our members fail to supply us with enough corn to operate the ethanol plant at capacity. We do not anticipate experiencing difficulty purchasing the corn we require to operate the ethanol plant.

We have an agreement with John Stewart & Associates ("JSA") to provide us with consulting services related to our risk management strategy. We pay JSA a fee of $2,500 per month to assist us in making risk management decisions regarding our commodity purchases. The agreement renews on a month-to-month basis.

7

Natural Gas

Natural gas is an important input to our manufacturing process. We purchase our natural gas on the open market and the price for our natural gas is based on market rates. We have a contract with Northern Natural Gas for the interstate transportation of our natural gas. We contract with NorthWestern Energy for the local transportation of our natural gas. Both contracts expire in 2018.2028. We have had no interruptions or shortages in the supply of natural gas to the plant since operations commenced in 2001. We anticipate that we will be able to purchase sufficient natural gas to continue to operate the ethanol plant during our 20182021 fiscal year.

Electricity

Electricity is necessary for lighting and powering much of the machinery and equipment used in the production process. We contract with Sioux Valley Energy, Inc. to provide all of the electric power and energy requirements for the ethanol plant. We have had no interruptions or shortages in the supply of electricity to the plant since operations commenced in 2001.

Water

Water is a necessary part of the ethanol production process. It is used in the fermentation process and to produce steam for the cooking, evaporation, and distillation processes. We contract with Big Sioux Community Water System, Inc. to meet our water requirements. Our current agreement with Big Sioux is for a five-year term commencingwas modified in December 2014February 2020 and is renewable for additional five year terms.expires in 2025. Since our operations commenced in September 2001, we have had no interruption in the supply of water and all of our requirements have been met.

Seasonal Factors in Business

We experience some seasonality of demand for our ethanol, distillers grains and corn oil. Since ethanol is predominantly blended with gasoline for use in automobiles, ethanol demand tends to shift in relation to gasoline demand. As a result, we experience some seasonality of demand for ethanol in the summer months related to increased driving and, as a result, increased gasoline demand. In addition, we experience some increased ethanol demand during holiday seasons related to increased gasoline demand. We also experience decreased distillers grains demand during the summer months due to natural depletion in the size of herds at cattle feed lots. Further, we expect some seasonality of demand for our corn oil since the biodiesel industry is a major corn oil user and biodiesel plants typically reduce production during the winter months. We experience some seasonality in the price we pay for natural gas with premium pricing during the winter months. This increase in natural gas prices coincides with increased natural gas demand for heating needs in the winter months.

Working Capital

We primarily use our working capital for purchases of raw materials necessary to operate the ethanol plant, for payments on our credit facilities, for distributions to our members and for capital expenditures to maintain and upgrade the ethanol plant. Our primary sources of working capital are income from our operations and investments as well as our revolving lines of credit with our primary lender, FCSA.Farm Credit. For our 20182021 fiscal year, we anticipate using cash from our operations and our credit facilities for our plant expansion project and to maintain our current plant infrastructure. Management believes that our current sources of working capital are sufficient to sustain our operations for our 20182021 fiscal year and beyond.

Dependence on One or a Few Major Customers

As discussed above, we have entered into marketing agreements with RPMG to market our ethanol, distillers grains and corn oil. Therefore, we rely on RPMG to market almost all of our products, except for the modified/wet distillers grains that we market locally. Our financial success will be highly dependent on RPMG's ability to market our products at competitive prices. Any loss of RPMG as our marketing agent or any lack of performance under these agreements or inability to secure competitive prices could have a significant negative impact on our revenues. While we believe we can secure new marketers if RPMG were to fail, we may not be able to secure such new marketers at rates which are competitive with RPMG's.

8

Our Competition

Ethanol Competition

We are in direct competition with numerous ethanol producers in the sale of our products and with respect to raw material purchases related to those products. Many of the ethanol producers with which we compete have greater resources than we do. While management believes we are a lower cost producer of ethanol, larger ethanol producers may be able to take advantage of economies of scale due to their larger size and increased bargaining power with both ethanol, distillers grains and corn oil customers and raw material suppliers. As of January 23, 2018,December 31, 2020, the Renewable Fuels Association estimates that there are213 210 ethanol production facilities in the United States with capacity to produce approximately 16.217.6 billiongallons of ethanol per year. According to RFA estimates, approximately 3%of the ethanol production capacity in the United States was not operating as ofJanuary 23, 2018. The largest ethanol producers include Archer Daniels Midland, Flint Hills Resources, Green Plains Renewable Energy, POET Biorefining, and Valero Renewable Fuels, each of which is capable of producing significantly more ethanol than we produce.

The following table identifies the largest ethanol producers in the United States along with their production capacities.

U.S. FUEL ETHANOL PRODUCTION CAPACITY

BY TOP PRODUCERS

Producers of Approximately 700800

million gallons per year (MMgy) or more

| Company | Current Capacity (MMgy) | Percent of Total | ||||||||||||

| Archer Daniels Midland | 1,716 | 9.8% | ||||||||||||

| POET Biorefining | 1,805 | 10.3% | ||||||||||||

| Green Plains Renewable Energy | 1,128 | 6.4% | ||||||||||||

| Valero Renewable Fuels | 1,730 | 9.8% | ||||||||||||

| Flint Hills Resources | 840 | 4.8% | ||||||||||||

| Company | Current Capacity (MMgy) | Percent of Total | ||

| Archer Daniels Midland | 1,716 | 11% | ||

| POET Biorefining | 1,629 | 10% | ||

| Green Plains Renewable Energy | 1,475 | 9% | ||

| Valero Renewable Fuels | 1,400 | 9% | ||

| Flint Hills Resources | 840 | 5% | ||

The products that we produce are commodities. Since our products are commodities, there are typically no significant differences between the products we produce and the products of our competitors that would allow us to distinguish our products in the market. As a result, competition in the ethanol industry is primarily based on price and consistent fuel quality.

We have experienced increased competition from oil companies that have purchased ethanol production facilities. These oil companies are required to blend a certain amount of ethanol each year. Therefore, the oil companies may be able to operate their ethanol production facilities at times when it is unprofitable for us to operate our ethanol plant. Further, some ethanol producers own multiple ethanol plants which may allow them to compete more effectively by providing them flexibility to run certain production facilities while they have other facilities shut down. Finally some ethanol producers who own ethanol plants in geographically diverse areas of the United States may spread the risk they encounter related to feedstock prices due to localized corn shortages or poor growing conditions.

A number of automotive, industrial and power generation manufacturers are developing alternative clean power systems using fuel cells, plug-in hybrids, electric cars or clean burning gaseous fuels. Electric car technology has recently grown in popularity, especially in urban areas, and continues to represent a source of competition for the ethanol industry. While there are currently a limited number of vehicle recharging stations, making electric cars not feasible for all consumers, there has been increased focus on developingdevelopment of these recharging stations to make electric carwhich is making this technology more widely available in the future.available. Additional competition from these other sources of alternative energy, particularly in the automobile market, could reduce the demand for ethanol, which would negatively impact our profitability.

In addition to domestic producers of ethanol, we face competition from ethanol produced in foreign countries, particularly Brazil. Ethanol imports have been lower in recent years and ethanol exports have been higher. As of May 1, 2013, Brazil increased its domestic ethanol use requirement from 20% to 25% which decreased the amount of ethanol available in Brazil for export. Further, in August 2017, Brazil instituted a quota and tariff on ethanol produced in the United States and exported to Brazil which reduced exports to Brazil. Brazil increased the quota during our 2019 fiscal year which resulted in additional demand from Brazil, however, without this quota and tariff, Brazilian exports likely would have been higher. In December 2020, the Brazilian quota expired so all ethanol produced in the United States and exported to Brazil is now subject

9

to Brazil's import tariff. In the future, we may experience increased ethanol imports from Brazil which could put negative pressure on domestic ethanol prices and result in excess ethanol supply in the United States.

Competition among ethanol producers may continue to increase as gasoline demand decreases due to more fuel efficient vehicles being produced. If the concentration of ethanol used in most gasoline does not increase and gasoline demand is lower due to increased fuel efficiency by the vehicles operated in the United States, competition may increase among ethanol producers to supply the ethanol market.

Distillers Grains Competition

Our ethanol plant competes with other ethanol producers in the production and sales of distillers grains. Distillers grains are primarily used as an animal feed supplement which replaces corn and soybean meal. As a result, we believe that distillers grains prices are positively impacted by increases in corn and soybean prices. In addition, in recent years the United States ethanol industry has increased exports of distillers grains which management believes has positively impacted demand and prices for distillers grains in the United States. In the event these distillers grains exports decrease, including as a result of the Chinese tariffs which have significantly reduced export demand for distillers grains, it could lead to an oversupply of distillers grains in the United States. An oversupply of distillers grains could result in increased competition among ethanol producers for sales of distillers grains which could negatively impact market distillers grains prices in the United States.

Corn Oil Competition

We compete with many ethanol producers for the sale of corn oil. Many ethanol producers have installed the equipment necessary to separate corn oil from the distillers grains they produce which has increased competition for corn oil sales and has resulted in lower market corn oil prices.sales.

Governmental Regulation

Federal Ethanol Supports

The ethanol industry is dependent on several economic incentives to produce ethanol, the most significant of which is the Federal Renewable Fuels Standard (the "RFS"). The RFS requires that in each year, a certain amount of renewable fuels must be used in the United States. The RFS is a national program that does not require that any renewable fuels be used in any particular area or state, allowing refiners to use renewable fuel blends in those areas where it is most cost-effective. The RFS statutory volume requirement increases incrementally each year until the United States is required to use 36 billion gallons of renewable fuels by 2022. Starting in 2009, the RFS required that a portion of the RFS must be met by certain "advanced" renewable fuels. These advanced renewable fuels include ethanol that is not made from corn, such as cellulosic ethanol and biomass based biodiesel. The use of these advanced renewable fuels increases each year as a percentage of the total renewable fuels required to be used in the United States.

The United States Environmental Protection Agency (the "EPA") has the authority to waive the RFS statutory volume requirement, in whole or in part, provided one of the following two conditions have been met: (1) there is inadequate domestic renewable fuel supply; or (2) implementation of the requirement would severely harm the economy or environment of a state, region or the United States. Annually,Recently, the EPA is supposedhas been granting small refinery exemptions from the RFS while not using its authority to passwaive the RFS statutory volume requirements. These small refinery exemptions created unallocated gallons reducing the corn-based conventional biofuel RFS requirements by 2.25 billion gallons in 2018 and 2 billion gallons in 2019. These small refinery exemptions have had a rule that establishes the number of gallons of different types of renewable fuels that must be usedsignificant negative impact on domestic demand for ethanol and have resulted in negative operating margins in the United States which is called the renewable volume obligations.ethanol industry.

10

Most ethanol that is used in the United States is sold in a blend called E10. E10 is a blend of 10% ethanol and 90% gasoline. E10 is approved for use in all standard vehicles. Estimates indicate that gasoline demand in the United States is approximately 140143 billion gallons per year. Assuming that all gasoline in the United States is blended at a rate of 10% ethanol and 90% gasoline, the maximum demand for ethanol is 14.014.3 billion gallons per year. This is commonly referred to as the "blend wall," which represents a theoretical limit where more ethanol cannot be blended into the national gasoline pool. This is a theoretical

limit because it is believed that it would not be possible to blend ethanol into every gallon of gasoline that is being used in the United States and it discounts the use of higher percentage blends such as E15 or E85. These higher percentage blends may lead to additional ethanol demand if they become more widely available and accepted by the market.

Many in the ethanol industry believe that it will be impossible to meet the RFS requirement in future years without an increase in the percentage of ethanol that can be blended with gasoline for use in standard (non-flex fuel) vehicles. The EPA has approved the use of E15, gasoline which is blended at a rate of 15% ethanol and 85% gasoline, in vehicles manufactured in the model year 2001 and later. However, there are still state hurdles that need to be addressed in some states before E15 will become more widely available. Many states still have regulatory issues that prevent the sale of E15. Sales of E15 may be limited because it is not approved for use in all vehicles, the EPA requires a label that management believes may discourage consumers from using E15, and retailers may choose not to sell E15 due to concerns regarding liability. In addition, different gasoline blendstocks may be required at certain times of the year in order to use E15 due to federal regulations related to fuel evaporative emissions which may limit E15 sales in these markets. As a result, the approval of E15 by the EPA has not had an immediate impact on ethanol demand in the United States. In June 2019, the Trump Administration approved the use of E15 year-round which has somewhat expanded the use of E15.

In May 2020, the United States Department of Agriculture ("USDA") announced the Higher Blends Infrastructure Incentive Program which consists of up to $100 million in funding for grants to be used to increase the availability of higher blends of ethanol and biodiesel fuels. Funds may be awarded to retailers such as fueling stations and convenience stores to assist in the cost of installation or upgrading of fuel pumps and other infrastructure. In October 2020, the USDA announced the first round of awards to recipients of $22 million worth of grants. Recently the USDA closed on an additional $30 million worth of grants in a second round of funding.

Effect of Governmental Regulation

The government's regulation of the environment changes constantly. We are subject to extensive air, water and other environmental regulations and we have been required to obtain a number of environmental permits to construct and operate the ethanol plant. It is possible that more stringent federal or state environmental rules or regulations could be adopted, which could increase our operating costs and expenses. It also is possible that federal or state environmental rules or regulations could be adopted that could have an adverse effect on the use of ethanol. Plant operations are governed by the Occupational Safety and Health Administration ("OSHA"). OSHA regulations may change such that the costs of operating the ethanol plant may increase. Any of these regulatory factors may result in higher costs or other adverse conditions effecting our operations, cash flows and financial performance.

We have obtained all of the necessary permits to operate the ethanol plant. During our20172020 fiscal year, our costs of environmental compliance were approximately $166,000.$219,000. We anticipate that our environmental compliance costs will be approximately $292,000$230,000 during our2018 2021 fiscal year. Although we have been successful in obtaining all of the permits currently required, any retroactive change in environmental regulations, either at the federal or state level, could require us to obtain additional or new permits or spend considerable resources in complying with such regulations.

In late 2009, California passed a Low Carbon Fuels Standard ("LCFS"). The California LCFS requires that renewable fuels used in California must accomplish certain reductions in greenhouse gases which is measured using a lifecycle analysis, similar to the RFS. The LCFS could have a negative impact on demand for corn-based ethanol and result in decreased ethanol prices affecting our ability to operate profitably.

In August 2017, Brazil instituted an import quota for ethanol produced in the United States and exported to Brazil, along with a 20% tariff on ethanol imports in excess of the quota. The quota expired in December 2020 so all U.S. ethanol exports to Brazil are now subject to the tariff. This tariff and quota have reduced exports of ethanol to Brazil and may continue to negatively impact ethanol exports from the United States. Any reduction in ethanol exports could negatively impact market ethanol prices in the United States. RecentlyIn addition, the Chinese government increased the tariff on United States ethanol imports into China from 30% to 45% and ultimately to 70%. Due to other recent tariff activity between the United States and China, management does not expect these Chinese tariffs to be removed in the near term. Both China and Brazil announced ithave been major

11

sources of import demand for United States ethanol and distillers grains. These trade actions may remove this tariff.result in negative operating margins for United States ethanol producers.

We are subject to environmental oversight by the EPA. There is always a risk that the EPA may enforce certain rules and regulations differently than South Dakota's environmental administrators. South Dakota or EPA rules are subject to change, and any such changes could result in greater regulatory burdens on plant operations. We could also be subject to environmental or nuisance claims from adjacent property owners or residents in the area arising from possible foul smells or other air or water discharges from the ethanol plant. Such claims may result in an adverse result in court if we are deemed to engage in a nuisance that substantially impairs the fair use and enjoyment of property.

Employees

As ofDecember 31, 2017,2020, we had a total of 3943 full-time employees. We do not expect to hire a significantthe number of employees to materially change in the next 12 months.

ITEM 1A. RISK FACTORS.

You should carefully read and consider the risks and uncertainties below and the other information contained in this report. The risks and uncertainties described below are not the only ones we may face. The following risks, together with additional risks and uncertainties not currently known to us or that we currently deem immaterial could impair our financial condition and results of operation.

Risks Relating to Our Business

We are subject to global and regional economic downturns and related risks and the effects of COVID-19 or another pandemic may materially and adversely affect demand and the market price for our products. The level of demand for our products is affected by global and regional demographic and macroeconomic conditions. A significant downturn in global economic growth, or recessionary conditions in major geographic regions for prolonged periods, may lead to reduced demand for our products, which could have a negative effect on the market price of our products. In December 2019, a novel coronavirus surfaced in Wuhan, China (“COVID-19”). The spread of COVID-19 worldwide has resulted in businesses suspending or substantially curtailing global operations and travel, quarantines, and an overall substantial slowdown of economic activity. Transportation fuels in particular, including ethanol, have experienced significant price declines and reduced demand. The effects of COVID-19 have and may continue to materially and adversely affect the market price for our products, our business, results of operations and liquidity.

COVID-19 or another pandemic may negatively impact our ability to operate our business which could decrease or eliminate the value of our units. COVID-19 has resulted in significant uncertainty in many areas of our business. We do not know how long these conditions will last. This uncertainty is expected to negatively impact our operations. We may experience labor shortages if our employees are unable or unwilling to come to work. If our suppliers cannot deliver the supplies we need to operate our business or if we are unable to ship our products due to trucking or rail shipping disruptions, we may be forced to suspend operations or reduce production. If we are unable to operate the ethanol plant at capacity, it may result in unfavorable operating results. Any shut down of operations or reduction in production, especially for an extended period of time, could reduce or eliminate the value of our units.

The EPA issued small refinery exemption waivers to the RFS requirement which has resulted in demand destruction and negatively impacted profitability in the ethanol industry. During 2019, the ethanol industry learned that the EPA has been issuing small refinery waivers to the ethanol use requirements in the RFS. In previous years, when the EPA issued small refinery exemption waivers, the EPA reallocated the waived gallons to other refiners. The EPA under the Trump Administration was granting significantly more waivers than in the past and was not reallocating the waived gallons to other refiners. These actions have resulted in demand destruction in 2019 and 2020 which led to reduced market ethanol prices and negative operating margins in the ethanol industry. This reduction in ethanol demand has negatively impacted the profitability of our operations. In January 2020, the Tenth Circuit Court of Appeals ruled that small refinery exemptions may only be granted to refineries that had secured them continuously each year since 2010. Consistent with this ruling, in September 2020, the EPA denied certain small refinery exemption petitions filed by oil refineries in 2020 seeking retroactive relief from their ethanol use requirements for prior years. These small refinery exemption waivers have impacted the ethanol industry which could reduce or eliminate the value of our units.

12

The spread between ethanol and corn prices can vary significantly which can negatively impact our financial condition. Our only source of revenue comes from sales of our ethanol, distillers grains and corn oil. The primary raw materials we use to produce our ethanol, distillers grains and corn oil are corn and natural gas. In order to operate the ethanol plant profitably, we must maintain a positive spread between the revenue we receive from sales of our products and our corn and natural gas costs. This spread between the market price of our products and our raw material costs has been volatile in the past. If we were to experience a period of time where this spread is negative, and the negative margins continue for an extended period of time, it may prevent us from profitably operating the ethanol plant which could decrease the value of our units.

Decreasing gasoline prices may lower ethanol prices which could negatively impact our ability to operate profitably. In recent years,Recently, the price of ethanol has been less than the price of gasoline which increased ethanol demand. However, in recent years, at times gasoline prices have decreased significantly which have reduced the spread between the price of gasoline and the price of ethanol. ThisWhen it occurs, this trend has negatively impacted ethanol prices. If this trend continues for a significant period of time, it could hurt our ability to profitably operate the ethanol plant which could decrease the value of our units.

We may be forced to reduce production or cease production altogether if we are unable to secure the corn we require to operate the ethanol plant. We require a significant amount of corn to operate the ethanol plant at capacity. In recent years, other than in our 2019 fiscal year, the supply of corn in the market has been higher and we have not had difficulty securing the corn we require at prices that allow us to operate profitably. However, poor weather conditions can have a significant impact on corn production. If the corn crop harvested in future years is smaller than we have recently experienced, it is possible that we could experience corn shortages in the future which could negatively impact our ability to operate the ethanol plant. We may also experience a shortage of corn in our local market which may not increase national corn prices but may require us to increase our corn basis in order to attract corn which can impact our overall corn costs. If we are unable to secure the corn we require to continue to operate the ethanol plant, or we

are unable to secure corn at prices that allow us to operate profitably, we may have to reduce production or cease operating altogether which may negatively impact the value of our units.

Our revenue will be greatly affected by the price at which we can sell our ethanol, distillers grains and corn oil. Our ability to generate revenue is dependent on our ability to sell the ethanol, distillers grains and corn oil that we produce. Ethanol, distillers grains and corn oil prices can be volatile as a result of a number of factors. These factors include overall supply and demand, the market price of corn, the market price of gasoline, levels of government support, general economic conditions and the availability and price of competing products. Ethanol, distillers grains and corn oil prices tend to fluctuate based on changes in energy prices and other commodity prices, such as corn and soybean meal. Exports of our products and the various trade actions taken by China and Brazil have impacted the market prices for our products. If we experience lower prices for our products for a significant period of time, the value of our units may be negatively affected.

Our business is not diversified. Our success depends primarily on our ability to profitably operate our ethanol plant. We do not have any other lines of business or any other significant source of revenue if we are unable to operate our ethanol plant and manufacture ethanol, distillers grains and corn oil. If economic or political factors adversely affect the market for ethanol, distillers grains and corn oil, we may not be able to continue our operations. Our business would also be significantly harmed if our ethanol plant could not operate at full capacity for any extended period of time, which could reduce or eliminate the value of our units.

Our inability to secure credit facilities we may require in the future may negatively impact our liquidity. While we do not currently require more financing than we have, in the future we may need additional financing. If we require financing in the future and we are unable to secure such financing, or we are unable to secure the financing we require on reasonable terms, it may have a negative impact on our liquidity which could negatively impact the value of our units.

Our product marketer may fail to market our products at competitive prices which may cause us to operate unprofitably.RPMG is the sole marketer of all of our ethanol, corn oil and some of our distillers grains, and we rely heavily on its marketing efforts to successfully sell our products. Because RPMG sells ethanol, corn oil and distillers grains for a number of other producers, we have limited control over its sales efforts. Our financial performance is dependent upon the financial health of RPMG as most of our revenue is attributable to RPMG's sales. If RPMG breaches our marketing agreements or it cannot market all of the ethanol, corn oil and distillers grains we produce, we may not have any readily available means to sell our ethanol, corn oil and distillers grains and our financial performance could be negatively affected. While we market a portion of our distillers grains internally to local consumers, we do not anticipate that we would have the ability to sell all of the distillers grains, corn oil and ethanol we produce ourselves. If our agreements with RPMG terminate, we may seek other arrangements to sell our ethanol, corn oil and distillers grains, including selling our own products, but we may not be able to achieve results comparable to those achieved by RPMG which could harm our financial performance. Switching marketers may negatively impact our cash flow and our ability to continue to operate the ethanol plant. If we are unable to sell all of our ethanol, distillers grain and corn oil at prices that allow us to operate profitably, it may decrease the value of our units.

13

We engage in hedging transactions which involve risks that could harm our business. We are exposed to market risk from changes in commodity prices. Exposure to commodity price risk results from our dependence on corn and natural gas in the ethanol production process. We seek to minimize the risks from fluctuations in the prices of corn, natural gas and ethanol through the use of hedging instruments. These hedging instruments can be risky and can negatively impact our liquidity. In times when commodity prices are volatile, we may be required to use significant amounts of cash to make margin calls as a result of our hedging positions. The effectiveness of our hedging strategies is dependent on the price of corn, natural gas and ethanol and our ability to sell sufficient products to use all of the corn and natural gas for which we have futures contracts. Our hedging activities may not successfully reduce the risk caused by price fluctuation which may leave us vulnerable to corn and natural gas prices. We may choose not to engage in hedging transactions in the future and our operations and financial conditions may be adversely affected during periods in which corn and/or natural gas prices increase. These hedging transactions could impact our ability to profitably operate the ethanol plant and negatively impact our liquidity.

We may incur casualty losses that are not covered by insurance which could negatively impact the value of our units. We have purchased insurance which we believe adequately covers our potential losses from foreseeable risks. However, there are risks that we may encounter for which there is no insurance or for which insurance is not available on terms that are acceptable to us. If we experience a loss which materially impairs our ability to operate the ethanol plant which is not covered by insurance, the value of our units could be reduced or eliminated.

Our operations may be negatively impacted by natural disasters, severe weather conditions, and other unforeseen plant shutdowns which can negatively impact our operations. Our operations may be negatively impacted by events outside of our control such as natural disasters, severe weather, strikes, train derailments and other unforeseen events which may negatively

impact our operations. If we experience any of these unforeseen circumstances which negatively impact our operations, it may affect our cash flow and negatively impact the value of our business.

We depend on our management and key employees, and the loss of these relationships could negatively impact our ability to operate profitably. We are highly dependent on our management team to operate our ethanol plant. We may not be able to replace these individuals should thethey decide to cease their employment with us, or if they become unavailable for any other reason. While we seek to compensate our management and key employees in a manner that will encourage them to continue their employment with us, they may choose to seek other employment. Any loss of these managers or key employees may prevent us from operating the ethanol plant profitably and could decrease the value of our units.

We may violate the terms of our loan agreements and financial covenants which could result in our lender demanding immediate repayment of our loans. We have a credit facility with Farm Credit Services of America ("FCSA").Credit. Our credit agreements with FCSAFarm Credit include various financial loan covenants. We are currently in compliance with all of our financial loan covenants. Current management projections indicate that we will be in compliance with our loan covenants for at least the next 12 months. However, unforeseen circumstances may develop which could result in us violating our loan covenants. If we violate the terms of our loan agreements, FCSA,Farm Credit, our primary lender, could deem us in default of our loans and require us to immediately repay any outstanding balance of our loans. If we do not have the funds available to repay the loans and we cannot find another source of financing, we may fail which could decrease the value of our units.

Risks Related to Ethanol Industry

Excess ethanol supply in the market could put negative pressure on the price of ethanol which could lead to tight operating margins and may impact our ability to operate profitably. In the past the ethanol industry has confronted market conditions where ethanol supply exceeded demand which led to unfavorable operating conditions. Most recently, in 2012, profitability in the ethanol industry was reduced due to increased ethanol imports from Brazil at a time when gasoline demand in the United States was lower and domestic ethanol supplies were higher. This disconnect between ethanol supply and demand resulted in lower ethanol prices at a time when corn prices were higher which led to unfavorable operating conditions. We may experience periods of time when ethanol supply exceeds demand which could negatively impact our profitability. During 2020 we experienced excess ethanol supply compared to demand which negatively impacted profitability in the industry. The United States benefited from additional exports of ethanol in recent years which may not continue to occur during our 20182021 fiscal year. We may experience periods of ethanol supply and demand imbalance during our 20182021 fiscal year. If we experience excess ethanol supply, either due to increased ethanol production or lower gasolinedomestic or foreign demand, it could negatively impact the price of ethanol which could hurt our ability to profitably operate the ethanol plant.

Demand for ethanol may not increase past current levels unless higher percentage blends of ethanol are more widely used. Currently, ethanol is primarily blended with gasoline for use in standard (non-flex fuel) vehicles to create a blend which is 10% ethanol and 90% gasoline. Estimates indicate that approximately 140143 billion gallons of gasoline are sold in the

14

United States each year. Assuming that all gasoline in the United States is blended at a rate of 10% ethanol and 90% gasoline, the maximum domestic demand for ethanol is 14.014.3 billion gallons. This is commonly referred to as the "blend wall," which represents a theoretical limit where more ethanol cannot be blended into the national gasoline pool. Many in the ethanol industry believe that the ethanol industry has reached this blend wall. In order to expand demand for ethanol, higher percentage blends of ethanol must be utilized in standard vehicles. Such higher percentage blends of ethanol are a contentious issue. Automobile manufacturers and environmental groups have fought against higher percentage ethanol blends. The EPA approved the use of E15 for standard (non-flex fuel) vehicles produced in the model year 2001 and later. The fact that E15 has not been approved for use in all vehicles and the labeling requirements associated with E15 may lead to gasoline retailers refusing to carry E15. In addition, restrictions on the evaporative emissions of E15 during the summer months can limit the availability of E15 in some markets. Without an increase in the allowable percentage blends of ethanol that can be used in all vehicles, demand for ethanol may not continue to increase which could decrease the selling price of ethanol and could result in our inability to operate the ethanol plant profitably, which could reduce or eliminate the value of our units.

Changes and advances in ethanol production technology could require us to incur costs to update our plant or could otherwise hinder our ability to compete in the ethanol industry or operate profitably. Advances and changes in the technology of ethanol production are expected to occur. Such advances and changes may make the ethanol production technology installed in our plant less desirable or obsolete. These advances could also allow our competitors to produce ethanol at a lower cost than we are able. If we are unable to adopt or incorporate technological advances, our ethanol production methods and processes could be less efficient than our competitors, which could cause our plant to become uncompetitive or completely obsolete. If our competitors develop, obtain or license technology that is superior to ours or that makes our technology obsolete, we may be required to incur significant costs to enhance or acquire new technology so that our ethanol production remains competitive. Alternatively, we may be required to seek third-party licenses, which could also result in significant expenditures. These third-party licenses may not be available or, once obtained, they may not continue to be available on commercially reasonable terms. These costs could negatively impact our financial performance by increasing our operating costs and reducing our net income.

Decreases in ethanol demand may result in excess production capacity in our industry. The supply of domestically produced ethanol is at an all-time high. According to the Renewable Fuels Association, as of January 23, 2018,December 31, 2020, there are 213210 ethanol plants in the United States with capacity to produceproduct approximately 16.217.6 billion gallons of ethanol per year. Excess ethanol production capacity may have an adverse impact on our results of operations, cash flows and general financial condition. According to the Renewable Fuels Association, approximately 3% of the ethanol production capacity in the United States was idled as of January 23, 2018. Further, ethanol demand may be negatively impacted by reductions in the RFS. While the United States is currently exporting ethanol which has generally resulted in increased ethanol demand, these ethanol exports may not continue. If ethanol demand does not grow at the same pace as increases in supply, we expect the selling price of ethanol to decline. If excess capacity in the ethanol industry continues to occur, the market price of ethanol may decline to a level that is inadequate to generate sufficient cash flow to cover our costs, which could negatively affect our profitability.

We operate in an intensely competitive industry and compete with larger, better financed companies which could impact our ability to operate profitably. There is significant competition among ethanol producers. There are numerous producer-owned and privately-owned ethanol plants operating throughout the Midwest and elsewhere in the United States. We also face competition from ethanol producers located outside of the United States. The largest ethanol producers include Archer Daniels Midland, Flint Hills Resources, Green Plains Renewable Energy, POET Biorefining, and Valero Renewable Fuels, each of which is capable of producing significantly more ethanol than we produce. Further, many believe that there will be consolidation occurring in the ethanol industry which will likely lead to a few companies that control a significant portion of the United States ethanol production market. We may not be able to compete with these larger producers. These larger ethanol producers may be able to affect the ethanol market in ways that are not beneficial to us which could negatively impact our financial performance and the value of our units.

Competition from the advancement of alternative fuels and other technologies may lessen demand for ethanol. Alternative fuels, gasoline oxygenates and ethanol production methods are continually under development. A number of automotive, industrial and power generation manufacturers are developing alternative clean power systems using fuel cells, plug-in hybrids, and electric cars or clean burning gaseous fuels. Like ethanol, these emerging technologies offer an option to address worldwide energy costs, the long-term availability of petroleum reserves and environmental concerns. If these alternative technologies continue to expand and gain broad acceptance and become readily available to consumers for motor vehicle use, we may not be able to compete effectively. This additional competition could reduce the demand for ethanol, resulting in lower ethanol prices that might adversely affect our results of operations and financial condition.

Consumer resistance to the use of ethanol based on the belief that ethanol is expensive, adds to air pollution, harms engines and/or takes more energy to produce than it contributes or based on perceived issues related to the use of corn as the feedstock to produce ethanol may affect demand for ethanol. Certain individuals believe that the use of ethanol will have a negative impact on gasoline prices at the pump. Some also believe that ethanol adds to air pollution and harms car and truck

15

engines. Still other consumers believe that the process of producing ethanol actually uses more fossil energy, such as oil and natural gas, than the amount of energy that is produced. Further, some consumers object to the fact that ethanol is produced using corn as the feedstock which these consumers perceive as negatively impacting food prices. These consumer beliefs could potentially be wide-spread and may be increasing as a result of recent efforts to increase the allowable percentage of ethanol that may be blended for use in vehicles. If consumers choose not to buy ethanol based on these beliefs, it would affect demand for the ethanol we produce which could negatively affect our profitability and financial condition.

If exports of ethanol are reduced, including as a result of the imposition byof tariffs on U.S. ethanol, ethanol prices may be negatively impacted. The United States ethanol industry was supported during our 20172020 fiscal year with exports of ethanol, which has generally over the recent years increased demand for our ethanol. Management believes these additional exports of ethanol were due to lower market ethanol prices in the United States and increased global demand for ethanol. However, these ethanol exports may not continue. In 2012, the European Union concluded an anti-dumping investigation related to ethanol produced in the United States and exported to Europe. As a result of this investigation, the European Union has imposed a tariff on ethanol which is produced in the United States and exported to Europe. Further, in 2017 both Brazil and China implemented tariffs on ethanol produced in the United States. These tariffs have resulted in decreased demand for ethanol from these countries which has negatively impacted ethanol prices in the United States. Any decrease in ethanol prices or demand may negatively impact our ability to profitably operate the ethanol plant.

Distillers grains demand and prices may continue to be negatively impacted by the Chinese antidumping and countervailing duty investigation. China was historically the world's largest importer of distillers grains produced in the United States. On January 12, 2016, the Chinese government announced that it would commence an anti-dumping and countervailing duty investigation related to distillers grains imported from the United States. In January 2017, the Chinese set the final anti-dumping duties from 42.2% to 53.7%, and set the final anti-subsidy tariffs from 11.2% to 12%. Both during the investigation and after the announcement of the duty, distillers grains demand and prices have been negatively impacted. While we expect China to continue to import some distillers grains, due to continued trade disputes and tensions between the United States and China, management does not expect these tariffs to be removed in the near term which could continue to negatively impact market distillers grains demand and prices. This reduction in demand along with lower domestic corn prices could negatively impact our ability to profitably operate the ethanol plant.

A reduction in ethanol exports to Brazil due to the imposition by the Brazilian government of a tariff on U.S. ethanol could have a negative impact on ethanol prices. Brazil has historically been a top destination for ethanol produced in the United States. However, in 2017, Brazil imposed a 20% tariff on ethanol which is produced in the United States and exported to Brazil. This tariff has resulted in a decline in demand for ethanol from Brazil. The effect of the tariff had been mitigated somewhat by the adoption of a rate tariff quota that allowed 750 million liters of ethanol annually to be allowed into Brazil before the tariff applies. However, this rate tariff quota expired on December 14, 2020, so all of the ethanol exports to Brazil is now subject to the 20% tariff. This tariff has negatively impacted ethanol demand and prices in the United States, and could negatively impact our ability to profitably operate the ethanol plant.

Overcapacity within the ethanol industry could cause an oversupply of ethanol and a decline in ethanol prices. Excess ethanol production capacity could have an adverse impact on our results of operations, cash flows and general financial condition. If demand for ethanol does not grow at the same pace as increases in supply, we would expect the price of ethanol to decline. If excess capacity in the ethanol industry occurs, the market price of ethanol may decline to a level that is inadequate to generate sufficient cash flow to cover our costs which could reduce the value of our units.

Many ethanol producers are expanding their production capacity which could lead to an oversupply of ethanol in the United States. Recently, many ethanol producers have commenced projects to expand their ethanol production capacities. These expansions could result in a significant increase in the supply of ethanol in the United States. Currently, ethanol prices are supported by ethanol exports which may not continue at their current levels. While many in the ethanol industry are working to increase the amount of ethanol that is used domestically, specifically in the form of E15, which contains 15% ethanol as compared to the 10% ethanol which is used in most current blends, adoption of E15 has not been as rapid as most ethanol producers would like. Also, the additional ethanol capacity which is being constructed may exceed current domestic and export demand. An oversupply of ethanol negatively impacts domestic ethanol prices which could negatively impact our ability to profitably operate the ethanol plant.

We made significant investments in Guardian Hankinson, LLC and Ring-neck Energy & Feed, LLC which may fail. In December 2013, we made a $12 million investment in Guardian Hankinson, LLC, an entity that owns an ethanol plant in North Dakota. In addition, in July 2017, we made a $10 million investment in Ring-neck Energy & Feed, LLC. Both of these companies will face many of the same risks that we face in operating our ethanol plant. Further, we have limited control over the management decisions made by Guardian Hankinson, LLC and Ring-neck Energy & Feed, LLC. If Guardian Hankinson, LLC or Ring-neck Energy & Feed, LLC is ultimately unsuccessful, it could negatively impact the return we receive on our investment which could negatively impact our financial performance and the value of our units.

16

Failures of our information technology infrastructure could have a material adverse effect on operations. We utilize various software applications and other information technology that are critically important to our business operations. We rely on information technology networks and systems, including the Internet, to process, transmit and store electronic and financial information, to manage a variety of business processes and activities, including production, manufacturing, financial, logistics, sales, marketing and administrative functions. We depend on our information technology infrastructure to communicate internally and externally with employees, customers, suppliers and others. We also use information technology networks and systems to comply with regulatory, legal and tax requirements. These information technology systems, some of which are managed by third parties, may be susceptible to damage, disruptions or shutdowns due to failures during the process of upgrading or replacing software, databases or components thereof, power outages, hardware failures, computer viruses and ransomware attacks by computer hackers or other cybersecurity risks, telecommunication failures, user errors, natural disasters, terrorist attacks or other catastrophic events. If any of our significant information technology systems suffer severe damage, disruption or shutdown, and our disaster recovery and business continuity plans do not effectively resolve the issues in a timely manner, our product sales, financial condition and results of operations may be materially and adversely affected.

A cyber attack or other information security breach could have a material adverse effect on our operations and result in financial losses. We are regularly the target of attempted cyber and other security threats and must continuously monitor and develop our information technology networks and infrastructure to prevent, detect, address and mitigate the risk of unauthorized access, misuse, computer viruses and ransomware as well as other events that could have a security impact. If we are unable to prevent cyber attacks and other information security breaches, we may encounter significant disruptions in our operations which could adversely impact our business, financial condition and results of operations or result in the unauthorized disclosure of confidential information. Such breaches may also harm our reputation, result in financial losses or subject us to litigation or other costs or penalties.

Risks Related to Regulation and Governmental Action

Government incentives for ethanol production may be reduced or eliminated in the future, which could hinder our ability to operate at a profit.The ethanol industry is assisted by various federal and state ethanol incentives, includingthe most important of which is the RFS set forth in the Energy Policy Act of 2005. The RFS helps support a market for ethanol that might disappear without this incentive. The United States Environmental Protection Agency ("EPA")EPA has the authority to waive the RFS statutory volume requirement, in whole or in part, provided certain conditions have been met. Annually, the EPA is supposed to pass a rule that establishes the number of gallons of different types of renewable fuels that must be used in the United States which is called the renewable volume obligations. In the past, the EPA has set the renewable volume obligations below the statutory volume requirements. On November 30, 2017,December 19, 2019, the EPA released its final rule and set the 20182020 total volume obligation at 19.2920.09 billion gallons of which 15.0 billion gallons could be met by corn-based ethanol. The EPA has not yet set the RVO for 2021. If the EPA were to significantly reduce the volume requirements under the RFS or if the RFS were to be otherwise reduced or eliminated by the exercise of the EPA waiver authority or by Congress in the future, the market price and demand for ethanol could decrease which will negatively impact our financial performance.

The California Low Carbon Fuel Standard may decrease demand for corn-based ethanol which could negatively impact our profitability. California passed a Low Carbon Fuels Standard ("LCFS") which requires that renewable fuels used in California must accomplish certain reductions in greenhouse gases which reductions are measured using a lifecycle analysis. Management believes that these regulations could preclude corn-based ethanol produced in the Midwest from being used in California. California represents a significant ethanol demand market. If the ethanol industry is unable to supply corn-based ethanol to California, it could significantly reduce demand for the ethanol we produce. This could result in a reduction of our revenues and negatively impact our ability to profitably operate the ethanol plant.

Changes in environmental regulations or violations of these regulations could be expensive and reduce our profitability. We are subject to extensive air, water and other environmental laws and regulations. In addition, some of these laws require our plant to operate under a number of environmental permits. These laws, regulations and permits can often require expensive pollution control equipment or operational changes to limit actual or potential impacts to the environment. A

17

violation of these laws and regulations or permit conditions can result in substantial fines, damages, criminal sanctions, permit revocations and/or plant shutdowns. In the future, we may be subject to legal actions brought by environmental advocacy groups and other parties for actual or alleged violations of environmental laws or our permits. Additionally, any changes in environmental laws and regulations, both at the federal and state level, could require us to spend considerable resources in order to comply with future environmental regulations. The expense of compliance could be significant enough to reduce our profitability and negatively affect our financial condition.