UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C.DC 20549

_______________

FORM 10-K

|

| |

| (Mark One) | |

| R | Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

| | |

| | For the fiscal year ended December 31, 20092011 |

| | |

| or |

| | |

£o | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

| | |

| | For the transition period from __________ to __________ |

| | |

| | Commission file number 1-3950 |

Ford Motor Company

(Exact name of Registrant as specified in its charter)

|

| |

| Delaware | 38-0549190 |

| (State of incorporation) | (I.R.S. employer identification no.Employer Identification No.) |

| | |

| One American Road, Dearborn, Michigan | 48126 |

| (Address of principal executive offices) | (Zip code)Code) |

313-322-3000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of each class | | Name of each exchange on which registered *registered* |

| Common Stock, par value $.01 per share | | New York Stock Exchange |

| | |

| 7.50% Notes Due June 10, 2043 | | New York Stock Exchange |

| | |

Ford Motor Company Capital Trust II | | New York Stock Exchange |

6.50% Cumulative Convertible Trust Preferred | | |

Securities, liquidation preference $50 per share | | |

__________

* | * In addition, shares of Common Stock of Ford are listed on certain stock exchanges in Europe. |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes R No £o

Indicate by check mark if the registrant is not required to file reports pursuant to sectionSection 13 or Section 15(d) of the Act.

Yes £o No R

Indicate by check mark if the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes R No £o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes R No £o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. R

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a non-accelerated filer.smaller reporting company. See definitiondefinitions of "large accelerated filer," "accelerated filer," and large accelerated filer""smaller reporting company" in Rule 12b-2 of the Exchange Act. Large accelerated filer R Accelerated filer £o Non-accelerated filer £o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes £o No R

As of June 30, 2009,2011, Ford had outstanding 3,149,667,0033,728,794,458 shares of Common Stock and 70,852,076 shares of Class B Stock. Based on the New York Stock Exchange Composite Transaction closing price of the Common Stock on that date ($6.0713.79 per share), the aggregate market value of such Common Stock was $19,118,478,708.$51,420,075,576. Although there is no quoted market for our Class B Stock, shares of Class B Stock may be converted at any time into an equal number of shares of Common Stock for the purpose of effecting the sale or other disposition of such shares of Common Stock. The shares of Common Stock and Class B Stock outstanding at June 30, 20092011 included shares owned by persons who may be deemed to be "affiliates" of Ford. We do not believe, however, that any such person should be considered to be an affiliate. For information concerning ownership of outstanding Common Stock and Class B Stock, see the Proxy Statement for Ford’sFord's Annual Meeting of Stockholders currently scheduled to be held on May 13, 201010, 2012 (our "Proxy Statement"), which is incorporated by reference under various Items of this Report as indicated below.

As of February 12, 2010,13, 2012, Ford had outstanding 3,297,413,6053,729,894,765 shares of Common Stock and 70,852,076 shares of Class B Stock. Based on the New York Stock Exchange Composite Transaction closing price of the Common Stock on that date ($11.1212.54 per share), the aggregate market value of such Common Stock was $36,667,239,288.$46,772,880,353.

DOCUMENTS INCORPORATED BY REFERENCE

|

| | |

| Document | | Where Incorporated |

| Proxy Statement* | | Part III (Items 10, 11, 12, 13 and 14) |

__________

| |

| * | As stated under various Items of this Report, only certain specified portions of such document are incorporated by reference in this Report. |

Exhibit Index begins on page 90.

FORD MOTOR COMPANY

ANNUAL REPORT ON FORM 10-K

For the Year Ended December 31, 2011

|

| | | |

| Table of Contents | | Page |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Item 1A | | | |

| Item 1B | | | |

| Item 2 | | | |

| Item 3 | | | |

| Item 4 | Mine Safety Disclosures | | |

| Item 4A | | | |

| | | |

| Item 5 | | | |

| Item 6 | | | |

| Item 7 | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Item 7A | | | |

| | | |

| | | |

| | | |

| Item 8 | | | |

| Item 9 | | | |

| Item 9A | | | |

| Item 9B | | | |

| | | |

| Item 10 | | | |

| Item 11 | | | |

| Item 12 | | | |

| Item 13 | | | |

| Item 14 | | | |

| | | |

|

| | | |

| | | |

| Table of Contents | | |

| (continued) | | |

| | | |

| Item 15 | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

PART II.

ITEM 1.Business

Ford Motor Company (referred to herein as "Ford", the "Company", "we", "our" or "us") was incorporated in Delaware in 1919. We acquired the business of a Michigan company, also known as Ford Motor Company, thatwhich had been incorporated in 1903 to produce and sell automobiles designed and engineered by Henry Ford. We are one of the world’s largest producers of cars and trucks. We and our subsidiaries also engage in other businesses, including financing vehicles.

In addition to the information about Ford and itsour subsidiaries contained in this Annual Report on Form 10-K for the year ended December 31, 20092011 ("20092011 Form 10-K Report" or "Report"), extensive information about our Company can be found at www.ford.comwww.corporate.ford.com, including information about our management team, our brands and products, and our corporate governance principles.

The corporate governance information on our website includes our Corporate Governance Principles, Code of Ethics for Senior Financial Personnel, Code of Ethics for the Board of Directors, Standards of Corporate Conduct for all employees, and the Charters for each of the Committees of our Board of Directors. In addition, any amendments to our Code of Ethics or waivers granted to our directors and executive officers will be posted in this area of our website. All of these documents may be accessed by logging ontogoing to our corporate website and clicking on "Investors,"Our Company," then "Company Information,"Corporate Governance," and then "Corporate Governance Policies," or may be obtained free of charge by writing to our Shareholder Relations Department, Ford Motor Company, One American Road, P.O. Box 1899, Dearborn, Michigan 48126-1899.

In addition, all of our recent periodic report filings with the Securities and Exchange Commission ("SEC") pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, are available free of charge through our website. This includes recent Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, and Current Reports on Form 8-K, as well as any amendments to those Reports. Recent Section 16 filings made with the SEC by the Company or any of itsour executive officers or directors with respect to our Common Stock also are made available free of charge through our website. We post each of these documents on our website as soon as reasonably practicable after it is electronically filed with the SEC.

To access our SEC reports or amendments or the Section 16 filings, log ontogo to our corporate website and click "Investors,"Our Company," then "Company Reports,"Investor Relations," and then "View"Reports and SEC Filings," which links to a list of reports filed with the SEC. Our reports filed with the SEC may also be found on the SEC's website at www.sec.gov.

The foregoing information regarding our website and its content is for convenience only. The content of our website isonly and not deemed to be incorporated by reference into this Report nor should it be deemed to have been filed with the SEC.

ITEM 1. Business (continued)

OVERVIEW

Segments. We review and present our business results in two sectors: Automotive and Financial Services. Within these sectors, our business is divided into reportable segments based uponon the organizational structure that we use to evaluate performance and make decisions on resource allocation, as well as availability and materiality of separate financial results consistent with that structure.

OurThe reportable segments within our Automotive and Financial Services segments as ofsectors at December 31, 2009 are2011 were as described in the table below:

|

| | |

| Business Sector | Reportable Segments* (a) | Description |

| | | |

| Automotive: | Ford North America | Primarily includes the sale of Ford, LincolnFord- and Mercury brandLincoln-brand vehicles and related service parts in North America (the United States, Canada and Mexico), together with the associated costs to design, develop, manufacture, distribute and service these vehicles and parts, as well as, for periods prior to January 1, 2010, the sale of Mazda6 vehicles produced by our consolidated subsidiary AutoAlliance International, Inc. ("AAI"). |

| | parts. (b) |

| | Ford South America | Primarily includes the sale of Ford-brand vehicles and related service parts in South America, together with the associated costs to design, develop, manufacture, distribute and service these vehicles and parts. |

| | | |

| Ford Europe | Primarily includes the sale of Ford-brand vehicles and related service parts in Europe, Turkey and Russia, together with the associated costs to design, develop, manufacture, distribute and service these vehicles and parts. |

| | | |

| Ford Asia Pacific Africa | Primarily includes the sale of Ford-brand vehicles and related service parts in the Asia Pacific region and South Africa, together with the associated costs to design, develop, manufacture, distribute and service these vehicles and parts. |

| | |

| Volvo | Primarily includes the sale of Volvo-brand vehicles and related service parts throughout the world (including Europe, North and South America, and Asia Pacific Africa), together with the associated costs to design, develop, manufacture and service these vehicles and parts.

|

| | |

| Financial Services: | Ford Motor Credit Company | Primarily includes vehicle-related financing, leasing, and insurance. |

| | | |

| Other Financial Services | Includes a variety of businesses including holding companies and real estate, and the financing and leasing of some Volvo vehicles in Europe.estate. |

__________

* | |

| (a) | We have experienced a number of changes to our reportable segments in recent years, including:including the following: |

§ | As first reported in our Quarterly Report on Form 10-Q for

|

| ▪ | We discontinued the period ended March 31, 2009, Volvo currently is held for sale.Mercury brand as of the end of 2010. |

§ | |

| ▪ | We sold our Volvo operations on August 2, 2010. |

| |

| ▪ | During the fourth quarter of 2008, we sold a portion of our equity in Mazda Motor Corporation ("Mazda"), reducing our ownership percentage from approximately 33.4% at the time of sale to about 11% ownership currently. Asshortly thereafter. Through a result, beginningsubsequent sale in the fourth quarter of 2010, we further reduced our ownership to about 3.5%. Beginning with the fourth quarter of 2008, we accounthave accounted for our interest in Mazda as a marketable security and no longer report Mazda(instead of as an operating segment.segment). |

§ | As reported in our Quarterly Report on Form 10-Q for the period ended June 30, 2008, we

|

| ▪ | We sold our Jaguar Land Rover operations on June 2, 2008. |

§ | As reported in our Quarterly Report on Form 10-Q for the period ended June 30, 2007, we

|

| ▪ | We sold Aston Martin on May 31, 2007. |

| |

| (b) | For periods prior to January 1, 2009, this segment also included the sale of Mazda6 vehicles produced by our then-consolidated affiliate AutoAlliance International, Inc. ("AAI"). |

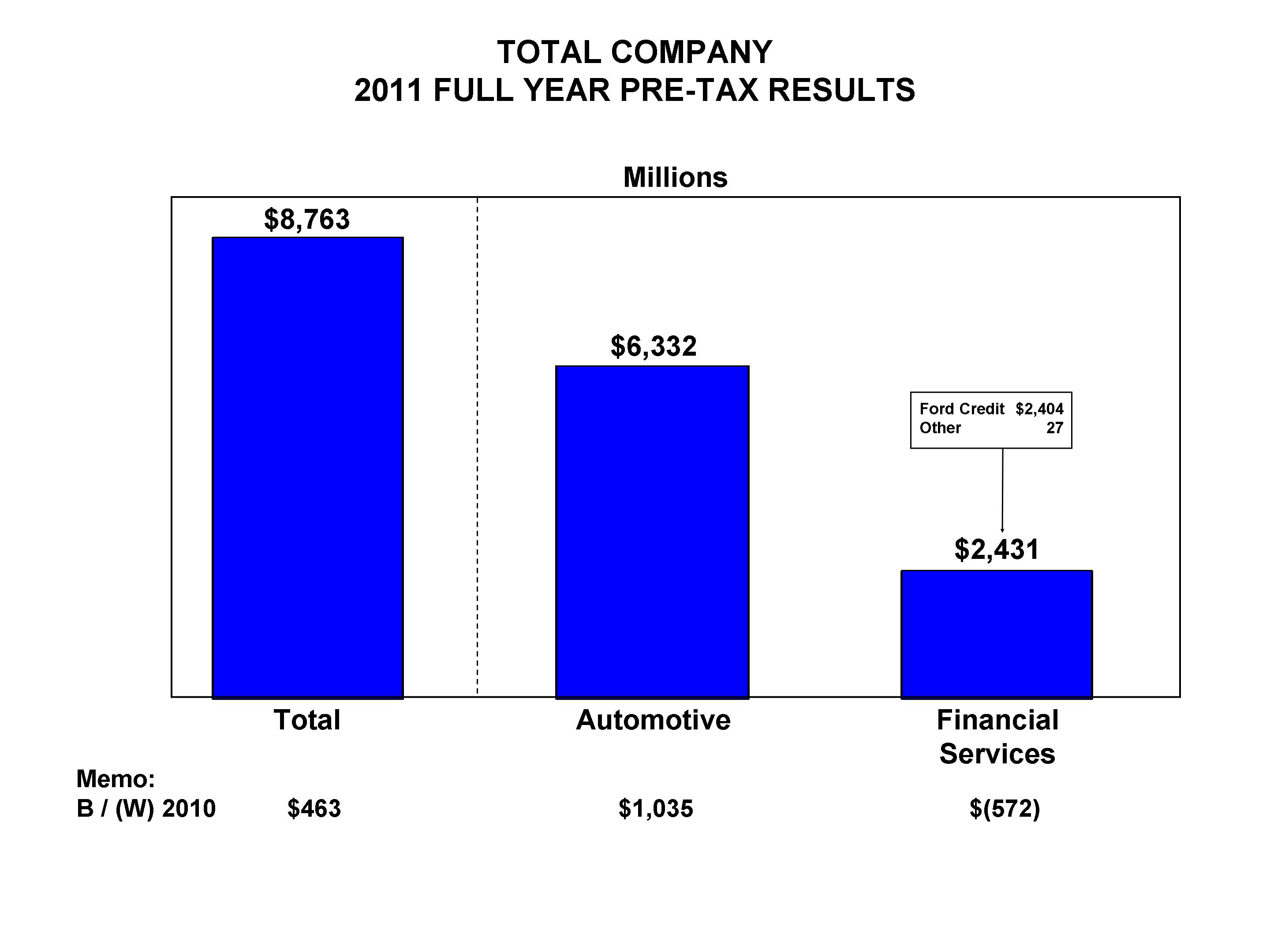

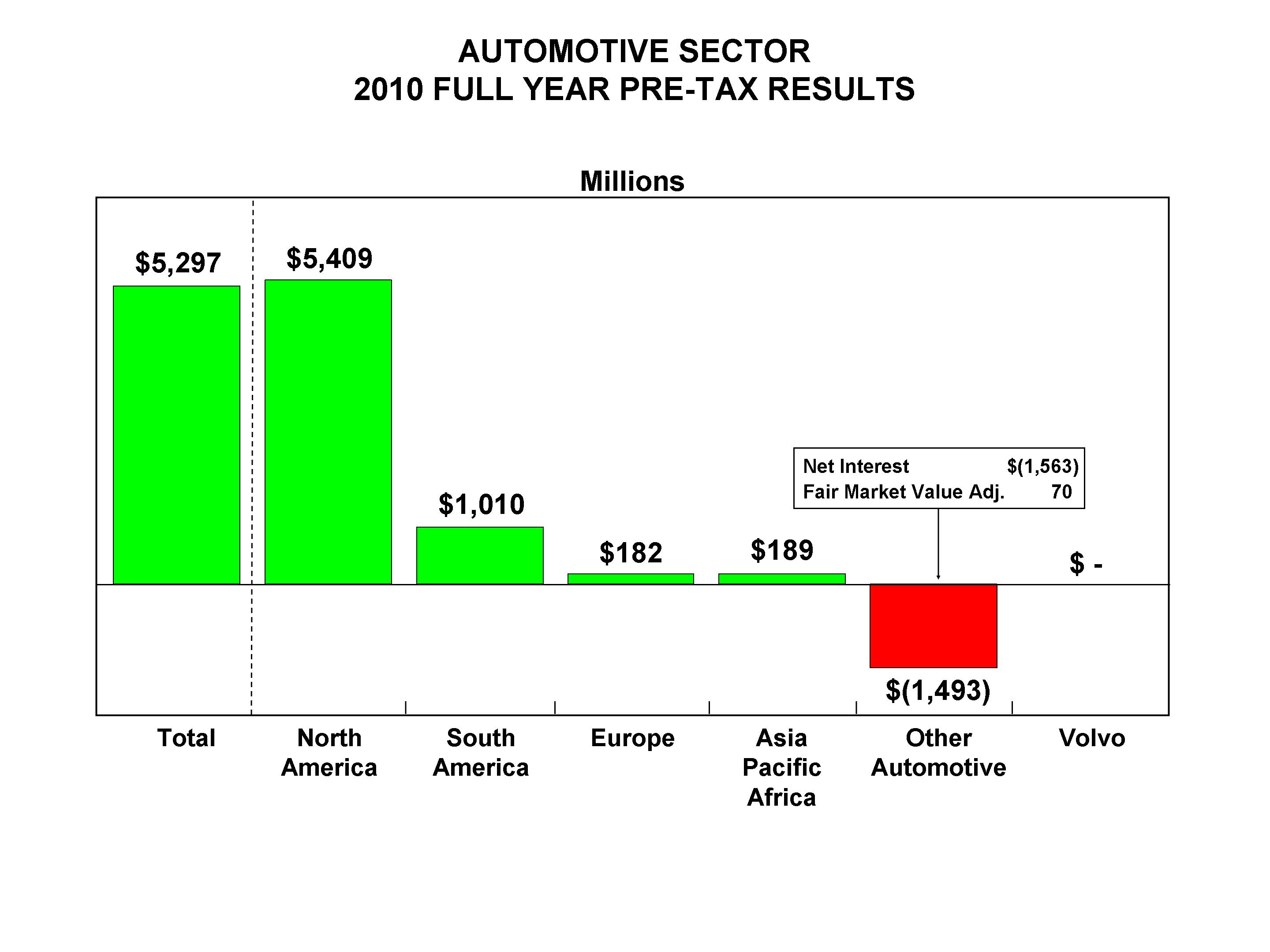

We provide financial information (such as revenue, income, and assets) for each business sector and reportable segment in three areas of this Report: (1) "Item 6. Selected Financial Data;" (2) "Item 7. Management’sManagement's Discussion and Analysis of Financial Condition and Results of Operations" ("Item 7"); and (3) Note 2827 of the Notes to the Financial Statements located at the end of this Report. Financial information relating to certain geographic areas is included in Note 2928 of the Notes to the Financial Statements.

ITEM 1. Business (continued)

AUTOMOTIVE SECTOR

General

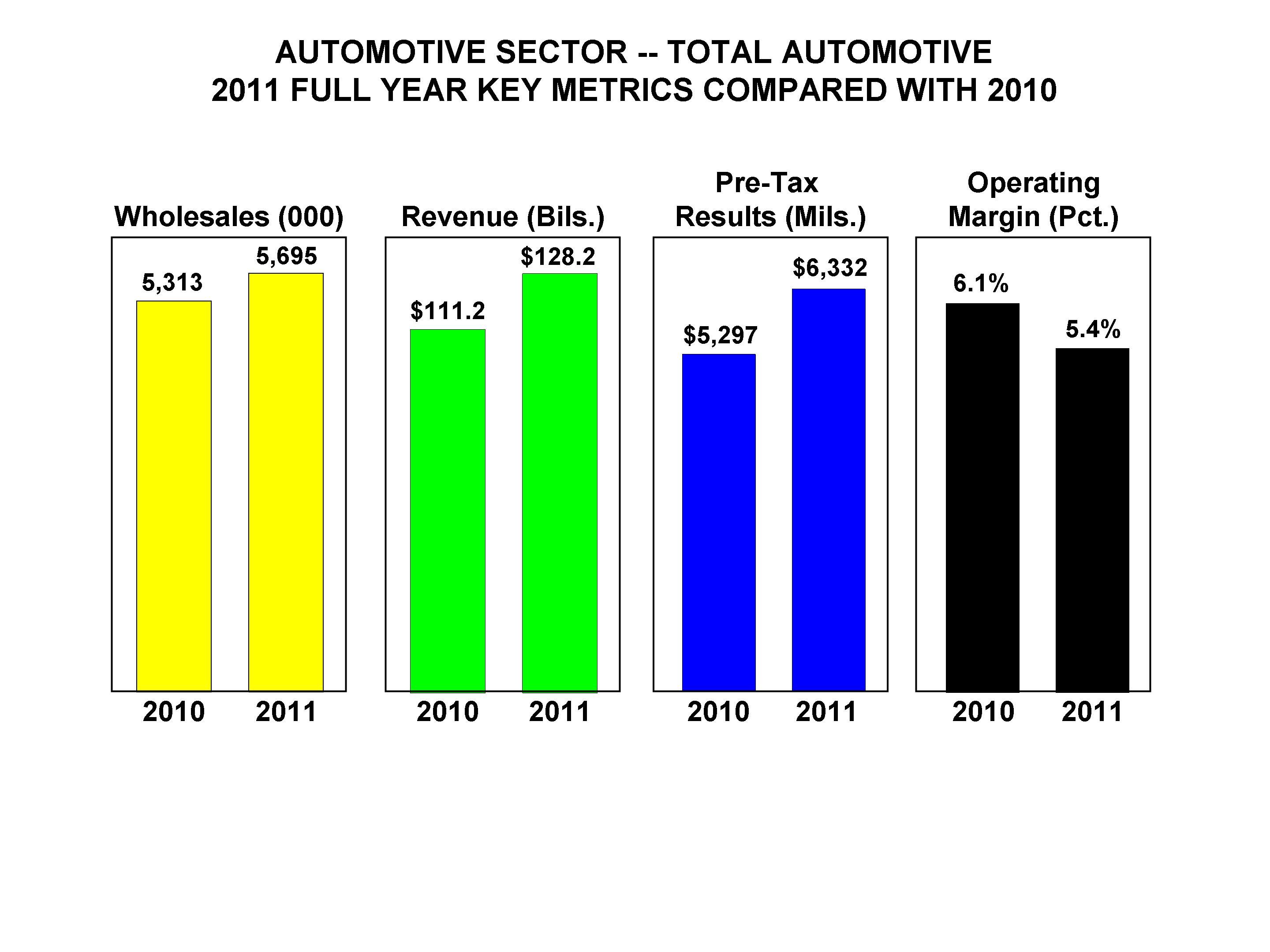

We sell carsOur vehicle brands are Ford and trucks throughout the world.Lincoln. In 2009, our total ongoing Automotive operations (including unconsolidated affiliates in China)2011, we sold approximately 4,817,0005,695,000 vehicles at wholesale throughout the world. See Item 7 for additional discussion of our calculation of wholesale unit volumes.

As of December 31, 2009, our vehicle brands included Ford, Mercury, Lincoln, and Volvo, although Volvo is held for sale. Substantially all of our cars, trucks and parts are marketed through retail dealers in North America, and through distributors and dealers (collectively, "dealerships") outside of North America, the substantial majority of which are independently owned. At December 31, 2009,2011, the approximate number of dealerships worldwide distributing our vehicle brands was as follows:

|

| |

| Brand | Number of Dealerships at December 31, 2009*2011 | | |

Ford | | | 11,682 | 10,653 |

Mercury

Ford-Lincoln (combined) | | | 1,780 | 907 |

Lincoln | | | 1,376 | 230 |

Volvo

Total | | | 2,269 | |

__________

* | Because many of these dealerships distribute more than one of our brands from the same sales location, a single dealership may be counted under more than one brand.11,790 |

In addition to the products we sell to our dealerships for retail sale, we also sell cars and trucks to our dealerships for sale to fleet customers, including daily rental car companies, commercial fleet customers, leasingdaily rental car companies, and governments. We do not depend on any single customer or small group of customers to the extent that the loss of such customer or group of customers would have a material adverse effect on our business.

Through our dealer network and other channels, we provide retail customers with a wide range of after-sale vehicle services and products, including maintenance and light repair, heavy repair, collision repair, vehicle accessories and extended service warranty.contracts. In North America, we market these products and services under several brands, including GenuineFord Service, Lincoln Service, Ford Custom Accessories™, Ford and Lincoln-Mercury Parts and ServiceSM, Ford Custom AccessoriesTM, FordLincoln Extended Service PlanSM,Plans, and MotorcraftSM.

The worldwide automotive industry, Ford included, is affected significantly by general economic conditions, (amongamong other factors)factors, over which we have little control. This is especially so because vehicles are durable goods, which provide consumers latitude in determining whether and when to replace an existing vehicle. The decision whether to purchase a vehicle may be affected significantly by slowing economic growth, geo-politicalgeopolitical events, and other factors (including the cost of purchasing and operating cars and trucks and the availability and cost of credit and fuel). As we recently have seen in the United States and Europe, in particular, the number of cars and trucks sold may vary substantially from year to year. Further, the automotive industry is a highly competitive cyclical business that has a wide and growing variety of product offerings from a growing number of manufacturers.

Our wholesale unit volumes vary with the level of total industry demand and our share of that industry demand. In the short term, our wholesale unit volumes also are influenced by the level of dealer inventory. Our share is influenced by how our products are perceived in comparison to those offered by other manufacturers based on many factors, including price, quality, styling, reliability, safety, fuel efficiency, functionality, and reputation. Our share also is affected by the timing and frequency of new model introductions. Our ability to satisfy changing consumer preferences with respect to type or size of vehicle, as well as design and performance characteristics, impacts our sales and earnings significantly.

ITEM 1. Business (continued)

TheAs with other manufacturers, the profitability of our business is affected by many factors, including:

§ | |

| ▪ | Wholesale unit volumes;volumes |

§ | |

| ▪ | Margin of profit on each vehicle sold;sold - which in turn is affected by many factors, including:such as: |

Market factors - volume and mix of vehicles and options sold, and net pricing (reflecting, among other factors, incentive programs)

Costs of components and raw materials necessary for production of vehicles

Costs for customer warranty claims and additional service actions

Costs for safety, emissions and fuel economy technology and equipment

· | Mix of vehicles and options sold; |

· ▪ | Costs of components and raw materials necessary for production of vehicles; |

· | Level of "incentives" (e.g., price discounts) and other marketing costs; |

· | Costs for customer warranty claims and additional service actions; and |

· | Costs for safety, emissions and fuel economy technology and equipment; and |

§ | As with other manufacturers, aA high proportion of relatively fixed structural costs, including labor costs, which meanso that small changes in wholesale unit volumes can significantly affect overall profitability.profitability |

ITEM 1. Business (continued)

Our industry continues to face a very competitive pricing environment, driven in part by industry excess capacity.capacity, particularly in mature markets such as North America and Europe. For the past several decades, manufacturers typically have given price discounts and other marketing incentives to maintain market share and production levels. A discussion of our strategies to compete in this pricing environment is set forth in the "Overview" section in Item 7.

Competitive Position. The worldwide automotive industry consists of many producers, with no single dominant producer. Certain manufacturers, however, account for the major percentage of total sales within particular countries, especially their countries of origin. Detailed information regarding our competitive position in the principal markets where we compete may be found below as part of the overall discussion of the automotive industry in those markets.Key competitors with global presence include Fiat-Chrysler, General Motors Company, Honda Motor Company, Hyundai-Kia Automotive Group, PSA Peugeot Citroen, Renault-Nissan B.V., Suzuki Motor Corporation, Toyota Motor Corporation, and Volkswagen AG Group.

Seasonality. We generally record the sale of a vehicle (and recognize sales proceeds in revenue) when it is produced and shipped or delivered to our customer (i.e., the dealership). See the "Overview" section in Item 7 for additional discussion of revenue recognition practices.

We manage our vehicle production schedule based on a number of factors, including retail sales (i.e., units sold by our dealerships to their customers at retail) and dealer stock levels (i.e., the number of units held in inventory by our dealerships for sale to retail and fleettheir customers). In the past, we have experienced some seasonal fluctuation in the business, with production in many markets tending to be higher in the first half of the year to meet demand in the spring and summer (typically the strongest sales months of the year). Third quarter production has tended to be the lowest. As a result, operating results for the third quarter typically have been less favorable than other quarters.

Raw Materials. We purchase a wide variety of raw materials from numerous suppliers around the world for use in production of our vehicles. These materials include ferrous metals (e.g., steel and iron castings), non-ferrous metals (e.g., aluminum), precious metals (e.g., palladium), ferrous metals (e.g., steel and iron castings), energy (e.g., natural gas), and plastics/resins (e.g., polypropylene). We believe that we have adequate supplies or sources of availability of the raw materials necessary to meet our needs. There always are always risks and uncertainties however, with respect to the supply of raw materials, thathowever, which could impact availability in sufficient quantities to meet our needs. See the "Overview" section of Item 7 for a discussion of commodity and energy price trends, and "Item 7A. Quantitative and Qualitative Disclosures About Market Risk" ("Item 7A") for a discussion of commodity price risks.

Backlog Orders. We generally produce and ship our products on average within approximately 20 days after an order is deemed to become firm. Therefore, no significant amount of backlog orders accumulates during any period.

Intellectual Property. We own or hold licenses to use numerous patents, copyrights, and trademarks on a global basis. Our policy is to protect our competitive position by, among other methods, filing U.S. and international patent applications to protect technology and improvements that we consider important to the development of our business. We have generated a large number of patents, and expect this portfolio to continue to grow as we actively pursue additional technological innovation. We currently have approximately 15,90017,660 active patents and pending patent applications globally, with an average age for patents in our active patent portfolio of just over 5under five and a half years. In addition to this intellectual property, we also rely on our proprietary knowledge and ongoing technological innovation to develop and maintain our competitive position. Although we believe that these patents, patent applications, and know-how, in the aggregate, are important to the conduct of our business, and we obtain licenses to use certain intellectual property owned by others, none is individually considered material to our business. We also own numerous trademarks and service marks that contribute to the identity and recognition of our Company and its products and services globally. Certain of these marks are integral to the conduct of our business, a loss of any of which could have a material adverse effect on our business.

ITEM 1. Business (continued)

Warranty Coverage and Additional Service Actions. We currently provide warranties on vehicles we sell. Warranties are offered for specific periods of time and/or mileage, and vary depending upon the type of product, usage of the product and the geographic location of its sale. Types of warranty coverage offered include base coverage (e.g., "bumper-to-bumper" coverage in the United States on Ford-brand vehicles for 36 months or 36,000 miles, whichever occurs first), safety restraint coverage, and corrosion coverage. Beginning with 2007 model-year passenger cars and light trucks, Ford extended the powertrain warranty coverage offered on Ford, Lincoln and Mercury vehicles sold in the United States, Canada, and select U.S. export markets (e.g., powertrain coverage for certain vehicles sold in the United States from three years or 36,000 miles to five years or 60,000 miles on Ford and Mercury brands, and from four years or 50,000 miles to six years or 70,000 miles on the Lincoln brand). In compliance with regulatory requirements, we also provide emissions-defects and emissions-performance warranty coverage. Pursuant to these warranties, Fordwe will repair, replace, or adjust all parts on a vehicle that are defective in factory-supplied materials or workmanship during the specified warranty period.

In addition to the costs associated with the warranty coverage provided on our vehicles, we also incur costs as a result of additional service actions not covered by our warranties, including product recalls and customer satisfaction actions.

Estimated warranty and service action costs for each vehicle sold by us are accrued for at the time of sale. Accruals for estimated warranty and service action costs are based on historical experience and subject to adjustment from time to time depending on actual experience. Warranty accrual adjustments required when actual warranty claim experience differs from our estimates may have a material impact on our results.

For additional information with respect to costs forregarding warranty and additional service actions,related costs, see "Critical Accounting Estimates" in Item 7 as well asand Note 3130 of the Notes to the Financial Statements.

ITEM 1. Business (continued)

Industry Sales Volume

Industry sales volume is an internal estimate based on publicly-available data collected from various government, private, and public sources around the globe. The following chart shows industry sales volume for the United States,last five years for certain key markets in each region, and for the marketstotal we track in Europe,within each of our Ford North America, Ford South America, Ford Europe, and Ford Asia Pacific Africa for the last five yearsregions (in millions of units):

| | | | |

| | | | | | | | | | | | | | | | |

| | | | |

United States | | | 10.6 | | | | 13.5 | | | | 16.5 | | | | 17.1 | | | | 17.5 | |

Europe | | | 15.8 | | | | 16.6 | | | | 18.0 | | | | 17.8 | | | | 17.6 | |

South America | | | 4.2 | | | | 4.3 | | | | 4.1 | | | | 3.2 | | | | 2.7 | |

Asia Pacific Africa | | | 24.5 | | | | 20.9 | | | | 20.4 | | | | 18.6 | | | | 17.3 | |

|

| | | | | | | | | | | | | | |

| | Industry Sales Volume (a) |

| | 2011 | | 2010 | | 2009 | | 2008 | | 2007 |

| United States | 13.0 |

| | 11.8 |

| | 10.6 |

| | 13.5 |

| | 16.5 |

|

| Canada | 1.6 |

| | 1.6 |

| | 1.5 |

| | 1.7 |

| | 1.7 |

|

| Mexico | 0.9 |

| | 0.8 |

| | 0.8 |

| | 1.1 |

| | 1.1 |

|

| Ford North America | 15.5 |

| | 14.2 |

| | 12.9 |

| | 16.3 |

| | 19.3 |

|

| | | | | | | | | | |

| Brazil | 3.6 |

| | 3.5 |

| | 3.1 |

| | 2.8 |

| | 2.5 |

|

| Argentina | 0.8 |

| | 0.7 |

| | 0.5 |

| | 0.6 |

| | 0.6 |

|

| Ford South America (b) | 5.4 |

| | 5.0 |

| | 4.2 |

| | 4.3 |

| | 4.1 |

|

| | | | | | | | | | |

| Britain | 2.2 |

| | 2.3 |

| | 2.2 |

| | 2.5 |

| | 2.8 |

|

| Germany | 3.5 |

| | 3.2 |

| | 4.0 |

| | 3.4 |

| | 3.5 |

|

| Ford Europe (c) | 15.3 |

| | 15.3 |

| | 15.9 |

| | 16.6 |

| | 18.0 |

|

| | | | | | | | | | |

| Turkey | 0.9 |

| | 0.8 |

| | 0.6 |

| | 0.5 |

| | 0.6 |

|

| Russia | 2.7 |

| | 2.0 |

| | 1.5 |

| | 3.1 |

| | 2.7 |

|

| | | | | | | | | | |

| China | 18.4 |

| | 18.3 |

| | 14.1 |

| | 9.9 |

| | 9.1 |

|

| India | 3.3 |

| | 3.1 |

| | 2.3 |

| | 2.0 |

| | 2.0 |

|

| Australia | 1.0 |

| | 1.0 |

| | 0.9 |

| | 1.0 |

| | 1.1 |

|

| South Africa | 0.5 |

| | 0.4 |

| | 0.4 |

| | 0.5 |

| | 0.6 |

|

| ASEAN (d) | 2.6 |

| | 2.4 |

| | 1.9 |

| | 2.0 |

| | 1.8 |

|

| Ford Asia Pacific Africa (e) | 30.4 |

| | 30.7 |

| | 24.5 |

| | 20.9 |

| | 20.4 |

|

________________________

* | |

| (a) | Throughout this section,Report, industry sales volume includesand wholesale unit volumes include sales of medium and heavy trucks. See discussion of each |

| |

| (b) | Ford South America industry sales volume and market belowshare are based, in part, on estimated vehicle registrations for definition of the six markets we track.track in the region (i.e., Argentina, Brazil, Chile, Colombia, Ecuador, and Venezuela). |

| |

| (c) | Ford Europe industry sales volume and market share are based, in part, on estimated vehicle registrations for the 19 markets we track (i.e., Austria, Belgium, Britain, Czech Republic, Denmark, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Netherlands, Norway, Poland, Portugal, Spain, Sweden, and Switzerland); sales of Ford-brand vehicles in Turkey and Russia by our unconsolidated affiliates Ford Otomotiv Sanayi Anonim Sirketi ("Ford Otosan") and Ford Sollers Netherlands B.V. ("FordSollers"), respectively, contribute to Ford Europe's wholesale unit volumes, but are not reflected in industry sales volume or market share for the region. |

| |

| (d) | ASEAN includes Indonesia, Malaysia, Philippines, Thailand, and Vietnam. |

| |

| (e) | Ford Asia Pacific Africa industry sales volume and market share are based, in part, on estimated vehicle sales for the 12 markets we track (i.e., Australia, China, Japan, India, Indonesia, Malaysia, New Zealand, Philippines, South Africa, Taiwan, Thailand, and Vietnam); market share data for 2008 to the present include local-brand vehicles produced by our Chinese joint venture Jiangling Motors Corporation, Ltd. ("JMC"). |

U.S. and European industry sales volume declined in 2009 compared with 2008, reflecting weak economic conditions in both markets. The decline in Europe was more modest because the impact of the economic slowdown was offset somewhat by substantial government-sponsored vehicle scrappage program incentives. Asia Pacific Africa industry sales increased in 2009 as compared to 2008, largely driven by growth in China.

United States

Industry Sales Data. The following table shows U.S. industry sales of cars and trucks (in millions of units):

| | | U.S. Industry Sales |

| | | Years Ended December 31, |

| | | | | | | | | | | | | | | |

| | | |

Cars | | | 5.6 | | | | 7.1 | | | | 7.9 | | | | 8.1 | | | | 7.9 | |

Trucks | | | 5.0 | | | | 6.4 | | | | 8.6 | | | | 9.0 | | | | 9.6 | |

ITEM 1. Business (continued)

We classify cars by small, medium, large, and premium segments, and trucks by compact pickup, bus/van (including minivans), full-size pickup, crossover utility vehicles ("CUVs") and traditional sport utility vehicles ("SUVs"), and medium/heavy segments. We refer to CUVs, which are based on car platforms, and SUVs, which are based on truck platforms, collectively as "utilities" or "utility vehicles." In the tables, we have classified all of our luxury cars as "premium," regardless of size. Annually, we review various factors to determine the appropriate classification of vehicle segments and the vehicles within those segments, and this review occasionally results in a change of classification for certain vehicles.Ford North America

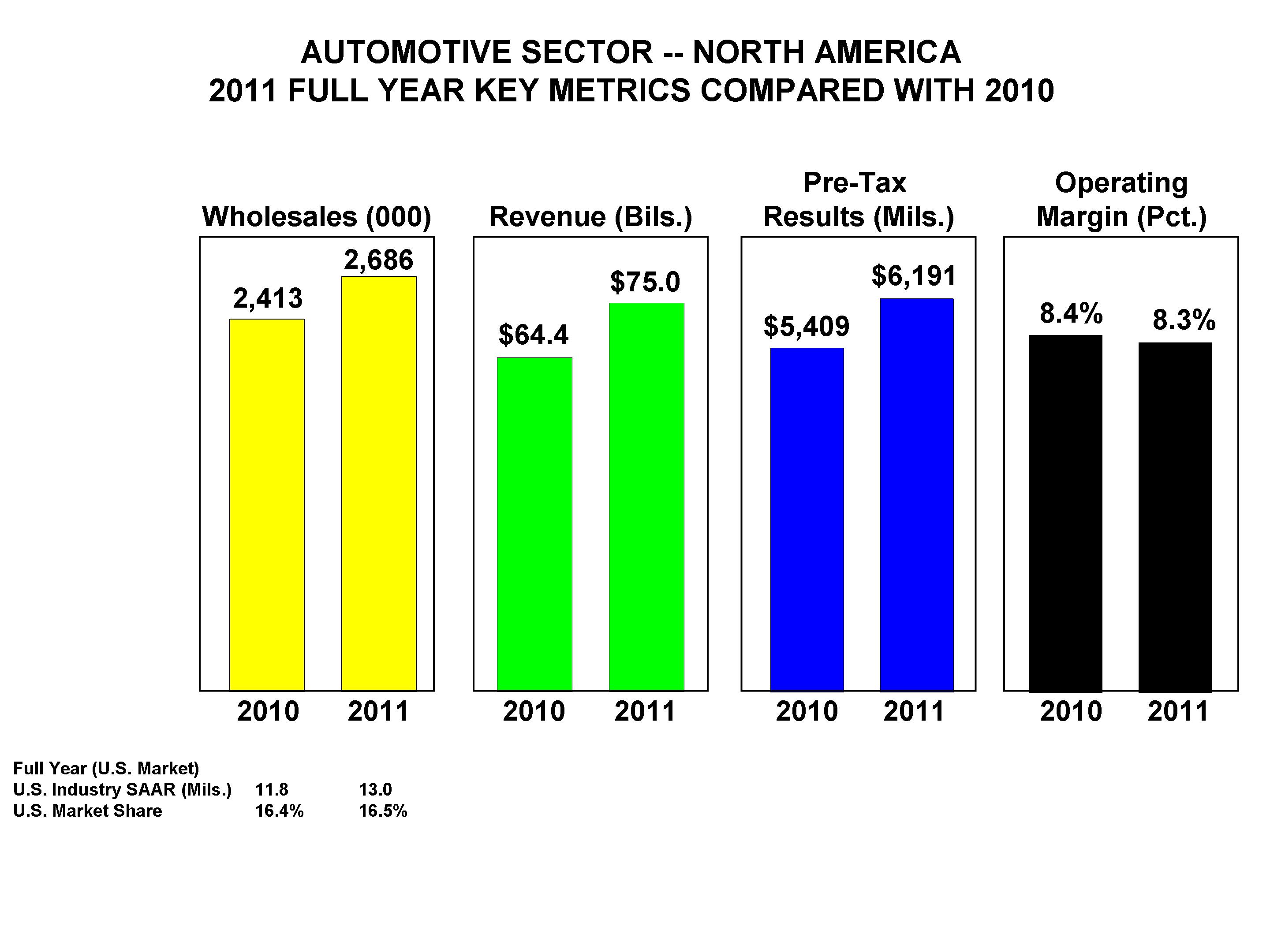

The following tables show our wholesales and market share by market in North America:

|

| | | | | | | | | | | | | | |

| | Wholesales (a) |

| | (in thousands) |

| | 2011 | | 2010 | | 2009 | | 2008 | | 2007 |

| United States | 2,224 |

| | 1,947 |

| | 1,563 |

| | 1,825 |

| | 2,363 |

|

| Canada | 273 |

| | 278 |

| | 223 |

| | 198 |

| | 243 |

|

| Mexico | 88 |

| | 88 |

| | 80 |

| | 134 |

| | 140 |

|

| Ford North America (b) | 2,686 |

| | 2,413 |

| | 1,927 |

| | 2,329 |

| | 2,890 |

|

______________

(a) Throughout this Report, wholesale unit volumes include all Ford-badged units (whether produced by Ford or by an unconsolidated affiliate), units manufactured by Ford that are sold to other manufacturers and units distributed for other manufacturers, and JMC-brand vehicles. Revenue from certain vehicles in wholesale unit volumes (specifically, Ford-badged vehicles produced and distributed by our unconsolidated affiliates, and JMC-brand vehicles) are not included in our revenue. Vehicles sold to daily rental car companies that are subject to a guaranteed repurchase option, as well as other sales of finished vehicles for which the proportionrecognition of U.S. car and truckrevenue is deferred (e.g., consignments), are included in wholesale unit sales by segment for the industry (including domestic and foreign-based manufacturers) and for Ford:volumes.

| | | U.S. Industry Vehicle Mix of Sales by Segment | |

| | | Years Ended December 31, | |

| | | | | | | | | | | | | | | | |

| CARS | | | | | | | | | | | | | | | |

Small | | | 23.7 | % | | | 22.9 | % | | | 19.8 | % | | | 19.0 | % | | | 17.1 | % |

Medium | | | 16.1 | | | | 15.5 | | | | 13.6 | | | | 13.1 | | | | 13.1 | |

Large | | | 5.4 | | | | 6.1 | | | | 7.0 | | | | 7.5 | | | | 7.4 | |

Premium | | | 7.3 | | | | 7.8 | | | | 7.8 | | | | 7.6 | | | | 7.8 | |

Total U.S. Industry Car Sales | | | 52.5 | | | | 52.3 | | | | 48.2 | | | | 47.2 | | | | 45.4 | |

| TRUCKS | | | | | | | | | | | | | | | | | | | | |

Compact Pickup | | | 2.6 | | | | 2.8 | | | | 3.2 | | | | 3.5 | | | | 3.9 | |

Bus/Van | | | 5.5 | | | | 6.1 | | | | 6.6 | | | | 7.8 | | | | 8.1 | |

Full-Size Pickup | | | 10.8 | | | | 11.9 | | | | 13.5 | | | | 13.3 | | | | 14.6 | |

Utilities | | | 27.1 | | | | 24.9 | | | | 26.5 | | | | 25.2 | | | | 25.5 | |

Medium/Heavy | | | 1.5 | | | | 2.0 | | | | 2.0 | | | | 3.0 | | | | 2.5 | |

Total U.S. Industry Truck Sales | | | 47.5 | | | | 47.7 | | | | 51.8 | | | | 52.8 | | | | 54.6 | |

Total U.S. Industry Vehicle Sales | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % |

| | | Ford U.S. Vehicle Mix of Sales by Segment* | |

| | | Years Ended December 31, | |

| | | | | | | | | | | | | | | | |

| CARS | | | | | | | | | | | | | | | |

Small | | | 14.0 | % | | | 15.0 | % | | | 12.8 | % | | | 12.5 | % | | | 11.6 | % |

Medium | | | 12.8 | | | | 9.3 | | | | 7.8 | | | | 12.9 | | | | 8.2 | |

Large | | | 6.8 | | | | 7.7 | | | | 8.4 | | | | 8.2 | | | | 8.9 | |

Premium | | | 3.1 | | | | 3.1 | | | | 2.5 | | | | 3.1 | | | | 2.8 | |

Total Ford U.S. Car Sales | | | 36.7 | | | | 35.1 | | | | 31.5 | | | | 36.7 | | | | 31.5 | |

| TRUCKS | | | | | | | | | | | | | | | | | | | | |

Compact Pickup | | | 3.4 | | | | 3.4 | | | | 3.0 | | | | 3.4 | | | | 4.1 | |

Bus/Van | | | 5.8 | | | | 6.5 | | | | 7.2 | | | | 8.6 | | | | 8.9 | |

Full-Size Pickup | | | 25.6 | | | | 27.2 | | | | 29.1 | | | | 29.6 | | | | 30.7 | |

Utilities | | | 28.2 | | | | 27.4 | | | | 28.6 | | | | 21.1 | | | | 24.3 | |

Medium/Heavy | | | 0.3 | | | | 0.4 | | | | 0.6 | | | | 0.6 | | | | 0.5 | |

Total Ford U.S. Truck Sales | | | 63.3 | | | | 64.9 | | | | 68.5 | | | | 63.3 | | | | 68.5 | |

Total Ford U.S. Vehicle Sales | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % |

__________

* | These data |

| (b) | Throughout this Report, regional wholesale unit volumes include sales of Ford, Lincoln, and Mercury vehicles.wholesales to various export markets. |

|

| | | | | | | | | | | | | | |

| | Market Share (a) |

| | 2011 | | 2010 | | 2009 | | 2008 | | 2007 |

| United States | 16.5 | % | | 16.4 | % | | 15.3 | % | | 14.2 | % | | 14.6 | % |

| Canada | 17.1 | % | | 16.9 | % | | 15.2 | % | | 12.6 | % | | 13.3 | % |

| Mexico | 9.4 | % | | 10.5 | % | | 11.8 | % | | 12.1 | % | | 13.3 | % |

As the tables above indicate, the shift from cars to trucks that began______________

(a) Throughout this Report, market share represents reported retail sales of our brands as a percent of total industry sales volume in the 1980s startedrelevant market (as opposed to reverse in 2005. Priorwholesale unit volumes reflecting sales directly by us to 2005, the proportion of trucks sold in the industry and by Ford had been increasing, reflecting higher sales of SUVs and full-size pickups. In recent years, the percentage of cars sold in the overallour customers, generally our dealers); market and by Ford has trended higher, primarily due to a shift in consumer preferences to smaller, more fuel-efficient vehicles. In 2009, overall changes in our U.S. vehicle mix generally followed the overall direction of U.S. industry trends. Our year-over-year growth in car mix, however, outpaced the industry, primarily fueled by the strength of our medium-car mix and sales led by our redesigned Ford Fusion, Fusion Hybrid, Mercury Milan and Milan Hybrid.share data also exclude Volvo.

United States. Market Share Data.The competitive environment in the United States has intensified and is expected to continuecontinues to intensify as Japanese and Koreanforeign manufacturers increase imports to the United States and increase production capacity in North America. Our principal competitorsOverall, we see a long-term industry trend toward smaller and more fuel-efficient vehicles, and we believe the long-term trend of growth in the United States include General Motors Company ("General Motors"), Chrysler Group LLC ("Chrysler"), Toyota Motor Corporation ("Toyota"), Honda Motor Company ("Honda"), and Nissan Motor Company ("Nissan").U.S. small car segment remains intact. The following tables show U.S.small car and truck marketsegment has increased its share for Ford (Ford, Lincoln, and Mercury brand vehicles only) and for the other five leading vehicle manufacturers. The percentagesfrom 14% in each2004 to 20.6% in 2009 - one of the following tables represent percentagesmost significant segment shifts in the industry. Although small cars dipped to 18.8% of industry in 2010, the segment grew again in 2011, increasing to 19.1% of total industry. At the same time, our sales of small cars at Ford were up 25% in 2011, giving us 10% share of the combinedsmall car segment and truck industry:more than a full percentage point increase compared to 2010 - our best share in the U.S. small car segment since 2003.

ITEM 1. Business (continued)

| | | U.S. Car Market Shares (a) | |

| | | Years Ended December 31, | |

| | | | | | | | | | | | | | | | |

Ford | | | 5.5 | % | | | 5.0 | % | | | 4.6 | % | | | 5.8 | % | | | 5.4 | % |

General Motors | | | 9.1 | | | | 10.0 | | | | 9.8 | | | | 10.0 | | | | 10.2 | |

Chrysler | | | 2.5 | | | | 3.6 | | | | 4.2 | | | | 4.1 | | | | 4.0 | |

Toyota | | | 10.0 | | | | 10.0 | | | | 9.2 | | | | 8.6 | | | | 7.4 | |

Honda | | | 6.5 | | | | 6.6 | | | | 5.3 | | | | 4.9 | | | | 4.8 | |

Nissan | | | 4.8 | | | | 4.4 | | | | 3.8 | | | | 3.2 | | | | 3.3 | |

All Other (b) | | | 14.1 | | | | 12.7 | | | | 11.3 | | | | 10.6 | | | | 10.3 | |

Total U.S. Car Deliveries | | | 52.5 | % | | | 52.3 | % | | | 48.2 | % | | | 47.2 | % | | | 45.4 | % |

| | | U.S. Truck Market Shares (a) | |

| | | Years Ended December 31, | |

| | | | | | | | | | | | | | | | |

Ford | | | 9.8 | % | | | 9.2 | % | | | 10.0 | % | | | 10.2 | % | | | 11.6 | % |

General Motors | | | 10.6 | | | | 12.1 | | | | 13.6 | | | | 14.1 | | | | 15.6 | |

Chrysler | | | 6.3 | | | | 7.2 | | | | 8.4 | | | | 8.4 | | | | 9.2 | |

Toyota | | | 6.7 | | | | 6.4 | | | | 6.7 | | | | 6.3 | | | | 5.6 | |

Honda | | | 4.3 | | | | 4.0 | | | | 4.1 | | | | 3.9 | | | | 3.6 | |

Nissan | | | 2.5 | | | | 2.7 | | | | 2.7 | | | | 2.8 | | | | 2.9 | |

All Other (b) | | | 7.3 | | | | 6.1 | | | | 6.3 | | | | 7.1 | | | | 6.1 | |

Total U.S. Truck Deliveries | | | 47.5 | % | | | 47.7 | % | | | 51.8 | % | | | 52.8 | % | | | 54.6 | % |

| | U.S. Combined Car and Truck Market Shares (a) | |

| | | Years Ended December 31, | |

| | | | | | | | | | | | | | | | |

Ford | | | 15.3 | % | | | 14.2 | % | | | 14.6 | % | | | 16.0 | % | | | 17.0 | % |

General Motors | | | 19.7 | | | | 22.1 | | | | 23.4 | | | | 24.1 | | | | 25.8 | |

Chrysler | | | 8.8 | | | | 10.8 | | | | 12.6 | | | | 12.5 | | | | 13.2 | |

Toyota | | | 16.7 | | | | 16.4 | | | | 15.9 | | | | 14.9 | | | | 13.0 | |

Honda | | | 10.8 | | | | 10.6 | | | | 9.4 | | | | 8.8 | | | | 8.4 | |

Nissan | | | 7.3 | | | | 7.1 | | | | 6.5 | | | | 6.0 | | | | 6.2 | |

All Other (b) | | | 21.4 | | | | 18.8 | | | | 17.6 | | | | 17.7 | | | | 16.4 | |

Total U.S. Car and Truck Deliveries | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % |

__________

(a) | All U.S. sales data are based on publicly available information from the media and trade publications. |

(b) | "All Other" primarily includes companies based in Korea, other Japanese manufacturers and various European manufacturers, and, with respect to the U.S. Truck Market Shares table and U.S. Combined Car and Truck Market Shares table, includes heavy truck manufacturers. |

Although the full-size pickup segment also has begun to grow in share of total industry again, we believe we will need to see a continued and sustainable recovery in the construction industry (including new housing starts) in order to see the full-size pickup segment increase significantly as a percentage of total industry sales. With the full-size pickup segment at 10.7% of industry in 2009, 11.6% in 2010, and unchanged in 2011, we believe the segment is still in its initial phase of a cyclical recovery. The peak year for full-size pickup trucks was 2004, with 14.7% of total industry. Within the full-size pickup truck segment, our F-Series retains strong market leadership.

Our improvementstrong U.S. vehicle sales in 2011 reflect our balanced portfolio of fuel-efficient vehicles. Our results marked the third consecutive year-over-year that our overall U.S. market share primarily ishas increased, with the result of several factors, including favorable acceptance ofimprovement driven in large measure by our redesigned products, product focus on industry growth segments,new Fiesta small car and customers' increasing awarenessEscape and acceptance of our commitment to leadership in quality, fuel efficiency, safety, smart technologies and value.Explorer utilities.

In addition to the Ford, Lincoln, and Mercury vehicles we sell in the U.S. market, we also sell a significant number of Volvo vehicles. Our market share for Volvo vehicles in the United States (which is reflected in "All Other" in the tables above) was approximately 0.6% in 2009, up 0.1 percentage points from 2008. This increase in market share primarily reflected the introduction of the new XC60 and improved sales of the V50.

Fleet Sales.The sales data and market share information provided above include both retail and fleet sales. Fleet sales includeincludes sales to commercial fleet customers, daily rental car companies, and governments; in general, fleet sales tend to be less profitable than retail sales. In 2011, fleet sales were 32% of our total sales; the majority was with commercial fleetand government customers, leasing companies,which are more profitable than daily rentals. In 2011, our daily rental business was 12% of total sales, lower than the industry average of 13%. As the leading manufacturer of commercial vehicles in the United States, commercial buyers are increasingly choosing Ford cars and governments.crossovers because of our improved resale values, and continue to favor Ford trucks and vans.

ITEM 1. Business (continued)

The table below shows our fleetCanada. Industry sales volume in Canada grew 3% in 2011 compared with the prior year. Within that total, truck sales increased by 1.6 percentage points to 56% of overall industry vehicle sales, while car sales decreased to 44% of industry sales volume. Our sales growth in the market earned Ford Canada the sales leadership title for the second year in a row. Strong sales in 2011 primarily reflected increased sales of cars, which gained 14% over the United States,prior year, in addition to our already strong truck sales performance. In 2011, Ford Canada earned segment leadership with Fusion, Mustang, Escape, Explorer, Ranger, F-150, and Super Duty.

Mexico. Industry sales volume in Mexico grew 10% during 2011. Segmentation shifts in the amount of those combinedindustry away from trucks and utilities and toward cars contributed to our share decline. Fleet sales also decreased in the last year as a percentageresult of our total U.S. car and truck sales for the last five years (in thousands):

| | | Ford Fleet Sales* | |

| | | Years Ended December 31, | |

| | | | | | | | | | | | | | | | |

Daily Rental Units | | | 205 | | | | 237 | | | | 304 | | | | 447 | | | | 440 | |

Commercial and Other Units | | | 156 | | | | 217 | | | | 268 | | | | 277 | | | | 256 | |

Government Units | | | 127 | | | | 153 | | | | 158 | | | | 162 | | | | 141 | |

Total Fleet Units | | | 488 | | | | 607 | | | | 730 | | | | 886 | | | | 837 | |

| | | | | | | | | | | | | | | | | | | | | |

Percent of Total U.S. Car and Truck Sales | | | 30 | % | | | 32 | % | | | 30 | % | | | 32 | % | | | 28 | % |

__________

* | These data include sales of Ford, Lincoln, and Mercury vehicles. |

Lower fleet sales in 2009 primarily reflected an overall industry decline in rental, commercial and government sectors. Although total fleet industry volume decreased for the year, we improved year-over-year fleet segment market share. We continue to maintain profitable government and commercial segment cutbacks. Our plans for near-term market share leadership over all brands.growth include new model launches - including in the fastest-growing segment, small cars.

Ford South America

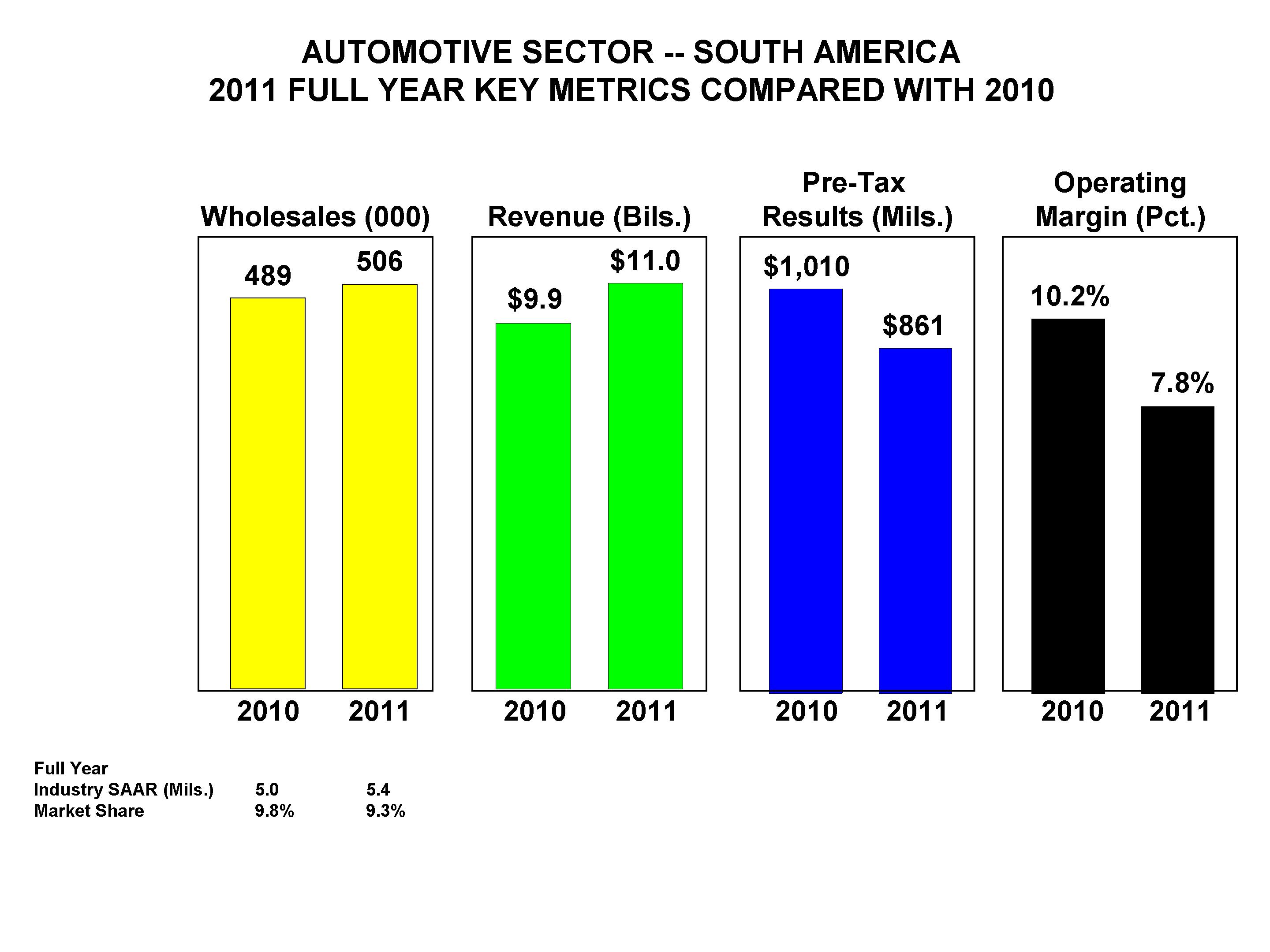

As indicated, we track industry sales and market share for six markets in South America - Argentina, Brazil, Chile, Colombia, Ecuador, and Venezuela. Ford South America's wholesales are more inclusive, tracking Ford-brand vehicles in every market in the region. Brazil and Argentina are our highest-volume South American markets. In particular, Brazil's economy and demographics, with growing per capita income, low vehicle ownership rates, and a young population, have allowed its automotive market to more than double since 2002. These favorable factors are expected to continue to contribute to growth in vehicle sales in Brazil. The following tables show our wholesales and market share in the largest markets and in total:

|

| | | | | | | | | | | | | | |

| | Wholesales |

| | (in thousands) |

| | 2011 | | 2010 | | 2009 | | 2008 | | 2007 |

| Brazil | 346 |

| | 358 |

| | 336 |

| | 297 |

| | 258 |

|

| Argentina | 105 |

| | 85 |

| | 66 |

| | 77 |

| | 77 |

|

| Ford South America | 506 |

| | 489 |

| | 443 |

| | 435 |

| | 438 |

|

|

| | | | | | | | | | | | | | |

| | Market Share |

| | 2011 | | 2010 | | 2009 | | 2008 | | 2007 |

| Brazil | 9.8 | % | | 10.4 | % | | 10.3 | % | | 10.0 | % | | 10.8 | % |

| Argentina | 12.9 |

| | 12.4 |

| | 13.3 |

| | 12.4 |

| | 13.7 |

|

| Ford South America | 9.3 |

| | 9.8 |

| | 10.2 |

| | 9.7 |

| | 10.7 |

|

The competition in Brazil is intensifying, as a number of automotive manufacturers are bringing online substantial capacity increases in the market. The intensifying competitive environment is putting pressure on industry net pricing; our plans to leverage fully our One Ford plan, including the introduction of an all-new lineup of global products over the next two years, beginning in the second half of 2012, should benefit us in this market.

Ford Europe

Industry Sales Data

Market Share Information. Outside of the United States, Europe is our largest market for the sale of cars and trucks. The automotive industry in Europe is intensely competitive. Our principal competitors in Europe include General Motors, Volkswagen A.G. Group, PSA Group, Renault Group,competitive, and Fiat SpA. For the past 10 years, the top six manufacturers have collectively held between 70% and 77% of the total market. This competitive environment is expected to intensify further as Japanese and Korean manufacturers increase their production capacity in Europe,the region and as other manufacturers of premium brands (e.g., BMW, Mercedes-Benz and Audi) continue to broaden their product offerings.

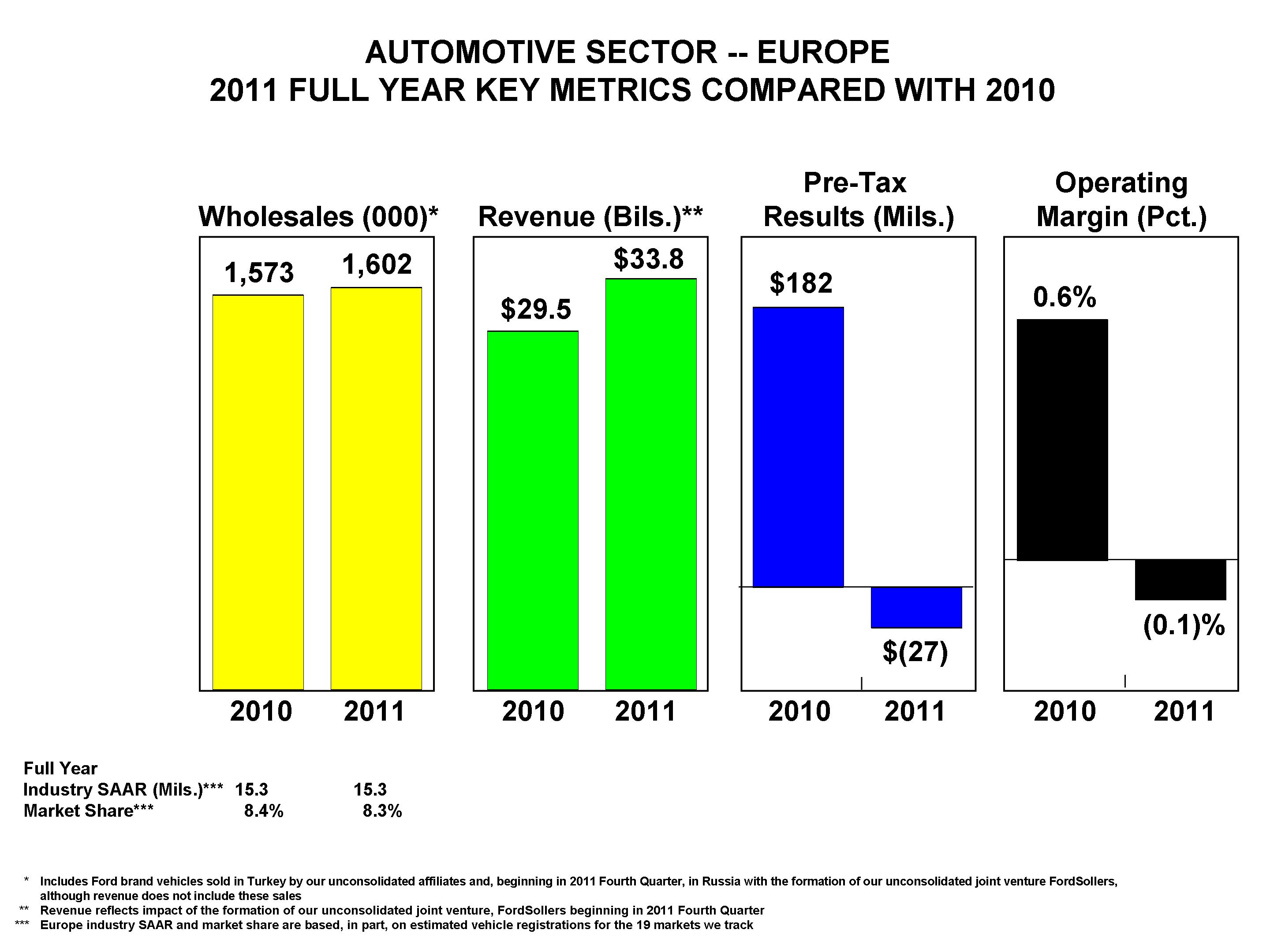

For purposes of this discussion, 2009 market data are based on estimated registrations currently available; percentage change is measured from actual 2008 registrations. WeAs indicated, we track industry salesand market share in Europe for the following 19 markets: Britain, Germany, France, Italy, Spain, Austria, Belgium, Ireland, Netherlands, Portugal, Switzerland, Finland, Sweden, Denmark, Norway,Britain, Czech Republic, Denmark, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Netherlands, Norway, Poland, Portugal, Spain, Sweden, and Poland. In 2009, vehicle manufacturers sold approximately 15.8 million carsSwitzerland. Ford Europe's wholesales are more inclusive, tracking Ford-brand vehicles in every market in the region, including those wholesales in Turkey and trucks in theseRussia from our unconsolidated affiliates, Ford Otosan and FordSollers.

|

| | | | | | | | | | | | | | |

| | Wholesales |

| | (in thousands) |

| | 2011 | | 2010 | | 2009 | | 2008 | | 2007 |

| Ford Europe | 1,602 |

| | 1,573 |

| | 1,568 |

| | 1,820 |

| | 1,918 |

|

|

| | | | | | | | | | | | | |

| | Market Share |

| | 2011 | | 2010 | | 2009 | | 2008 | | 2007 |

| Ford Europe | 8.3 | % | | 8.4 | % | | 9.1 | % | | 8.6%

| | 8.5 | % |

ITEM 1. Business (continued)

Within the 19 markets down 4.8% from 2008. Ford-brand combined car and truck market share in Europe in 2009 was approximately 9.1% (up 0.5 percentage points from the previous year); Volvo market share in Europe was 1.3% (about the same as in 2008).

we track, Britain and Germany are our highest-volume markets within Europe.markets. Any change in the British or German market has a significant effect on the results of Ford Europe. The following tables show our Ford Europe segment. The global economic crisis caused 2009 industrywholesales and market share for Britain and Germany (which are included within the 19 markets data above):

|

| | | | | | | | | | | | | | |

| | Wholesales |

| | (in thousands) |

| | 2011 | | 2010 | | 2009 | | 2008 | | 2007 |

| Britain | 342 |

| | 341 |

| | 354 |

| | 415 |

| | 414 |

|

| Germany | 250 |

| | 216 |

| | 286 |

| | 250 |

| | 230 |

|

|

| | | | | | | | | | | | | |

| | Market Share |

| | 2011 | | 2010 | | 2009 | | 2008 | | 2007 |

| Britain | 15.0 | % | | 15.0 | % | | 16.8%

| | 16.4 | % | | 15.9 | % |

| Germany | 7.4 |

| | 6.9 |

| | 7.6 | | 7.0 |

| | 6.7 |

|

Britain. Industry sales volume in Britain began to decline by 10.5% fromin 2008 levels (which were down considerably from 2007 levels,with the global financial crisis, and since 2003 has remained in the 2.2 million - 2.3 million unit range (compared with 2.8 million units in 2007).

Our market share remained steady in 2011 compared with the prior year, with Ford continuing as the economic crisis hit Britain earlier than many other European countries). Asmarket share leader in the Britain. Unusually high market share in 2009 was driven by the launch of the popular Ford Ka and Ford Fiesta small cars, coincident with the implementation of a result of government stimulusvehicle scrappage program designed to stimulate vehicle sales.

Germany. With 3.5 million new vehicle registrations in Germany, 20092011, Germany's industry sales volume there actually increasedgrew by 18.2%9.6% compared with 2008. Our Ford-brand combinedthe prior year. Germany was the only major market in Europe to experience an increase in industry sales volume in 2011, and remains the largest vehicle market in the European Union. In 2011, both passenger car and truck share in these markets in 2009commercial vehicle industry sales recovered along with the growing economy.

In 2011, Ford was 16.8% in Britain (up 0.4 percentage points from the previousfastest growing manufacturer (with vehicle unit sales up 17.6% compared with the prior year), and 7.6% in Germany (up 0.6increased market share by more than half of a percentage points frompoint primarily driven by the previous year).success of new Ford Focus, C-MAX, and S-MAX, as well as record sales of Ford Transit vehicles.

Turkey and Russia. Although not included in the results for the 19 European markets discussed above, several additional markets in the regionTurkey and Russia also contribute to our Ford Europe segment results. In 2009, Ford'sThe following tables show our wholesales and market share offor Turkey and Russia for the Turkish market increased by 0.4 percentage points to 15.1%, the eighth yearlast five years:

|

| | | | | | | | | | | | | | |

| | Wholesales |

| | (in thousands) |

| | 2011 | | 2010 | | 2009 | | 2008 | | 2007 |

| Turkey | 140 |

| | 130 |

| | 79 |

| | 78 |

| | 100 |

|

| Russia | 124 |

| | 93 |

| | 74 |

| | 183 |

| | 180 |

|

|

| | | | | | | | | | | | | | |

| | Market Share |

| | 2011 | | 2010 | | 2009 | | 2008 | | 2007 |

| Turkey | 15.8 | % | | 15.8 | % | | 15.1 | % | | 14.7 | % | | 16.8 | % |

| Russia | 4.3 |

| | 4.6 |

| | 5.5 |

| | 6.1 |

| | 6.5 |

|

Turkey. Industry growth slowed in a row that the Ford brand led the market in sales in Turkey. Industry sales volume in Russia decreased dramatically during 2009, shrinking by 1.6 million units or about half of its total volume2008 as a result of the economicglobal financial crisis. Beginning in 2009, industry vehicle sales accelerated due to government incentives put in place, with significant continuous increase in the last two years (from nearly 800,000 vehicle unit sales in 2010 to just over 900,000 vehicle unit sales in 2011). As shown above, our 2011 wholesales surpassed pre-crisis levels, and our market share has increased in recent years.

Russia. Following a 50% contraction in 2009 as a result of the impact of the global financial crisis reaching Russia, industry sales volume has returned almost to pre-crisis levels, with industry sales volume of 2.7 million units in 2011. Russia is the second-largest market for vehicle sales in Europe, and is expected to become the largest over the next several years. Our sales grew by 30% in 2011, led by strong sales of Ford-brand vehicles decreased by nearly 56% from 2008the new Focus and Transit. As previously reported, our Russian operations became part of the new FordSollers joint venture which began operations in October 2011. We expect this joint venture to about 82,000 unitscontribute to our ability to continue to grow profitably in 2009.this rapidly expanding market.

ITEM 1. Business (continued)

Motor Vehicle Distribution in Europe. In 2009, the European Commission abolished the 2002 the Commissionblock exemption law that had been specific to vehicle distribution agreements, and adopted instead a new generic regulation applying to all manufacturer-distributor relationships. The new law represents a marked improvement for manufacturers, and we have concluded new agreements with our dealers reflecting most of the European Union ("Commission") adopted a new regulatory schemeimprovements that changed the way motor vehicles are sold and repaired ("Block Exemption Regulation"). Pursuant to this regulation, manufacturers must operate either an "exclusive" distribution system – with exclusive dealer sales territories, but with the possibility of sales to any reseller (e.g., supermarket chains, internet agencies and other resellers not authorized by the manufacturer), who in turn could sell to end customers both within and outside of the dealer’s exclusive sales territory – or a "selective" distribution system.

ITEM 1. Business (continued)

We, like most other automotive manufacturers, elected to establish a "selective" distribution system, allowing us to restrict the dealer’s ability to sell our vehicles to unauthorized resellers. Under this "selective" system, we are entitled to determine the number of dealers we establish but, since October 2005, not their locations. Under either system permitted by the Block Exemption Regulation, the rules make it easier for a dealer to display and sell multiple brands in one store without the need to maintain separate facilities.

Under the Block Exemption Regulation, the Commission also adopted sweeping changes to the repair industry. Dealers no longer could be required by the manufacturer to perform repair work. Instead, dealers could subcontract repair work to independent repair shops that met reasonable criteria set by the manufacturer. These authorized repair facilities could perform warranty and recall work, in addition to other repair and maintenance work. While a manufacturer may continue to require the use of its parts in warranty and recall work, for all other repair work the repair facilities may use parts made by others that are of comparable quality. We have negotiated and implemented Dealer, Authorized Repairer and Spare Part Supply contractswill enter into effect on a country-by-country level and, therefore, the Block Exemption Regulation applies with respect to all of our dealers.

With these rules, the Commission intended to increase competition and narrow price differences from country to country. The Commission's Block Exemption Regulation continues to contribute to an increasingly competitive market for vehicles and parts, and to ongoing price convergence. This has contributed to an increase in marketing expenses, negatively affecting the profitability of Ford Europe and Volvo.

The current Block Exemption Regulation expires on May 31, 2010. In December 2009, the Commission launched a public review process for a revised Block Exemption Regulation and guidelines on motor vehicles sales and repair agreements. The Commission proposes to adopt a new block exemption for repair and maintenance services, in which area the Commission believes competition to be more limited. The Commission also proposes to adopt guidelines dealing with specific issues for both motor vehicle sales and repair. It is expected that the Commission will adopt final regulation in the spring of 2010.

Other Markets

Canada and Mexico. Canada and Mexico also are important markets for us. In Canada, industry sales volume for new cars and trucks in 2009 was approximately 1.48 million units, down 11% from 2008 levels; industry sales volume in Mexico for new cars and trucks in 2009 was approximately 770,000 units, down 28% from 2008. The decrease in industry sales volume in these markets reflected the impact of the global economic slowdown beginning in the fourth quarter of 2008. Our combined car and truck market share (including all of our brands sold in these markets) in 2009 was 15.2% for Canada (up 2.6 percentage points from a year ago), which represents our highest full-year share since 2001 and made Ford the number-one selling brand in Canada, and 11.8% in Mexico (down 0.3 percentage points from the previous year).June 1, 2013.

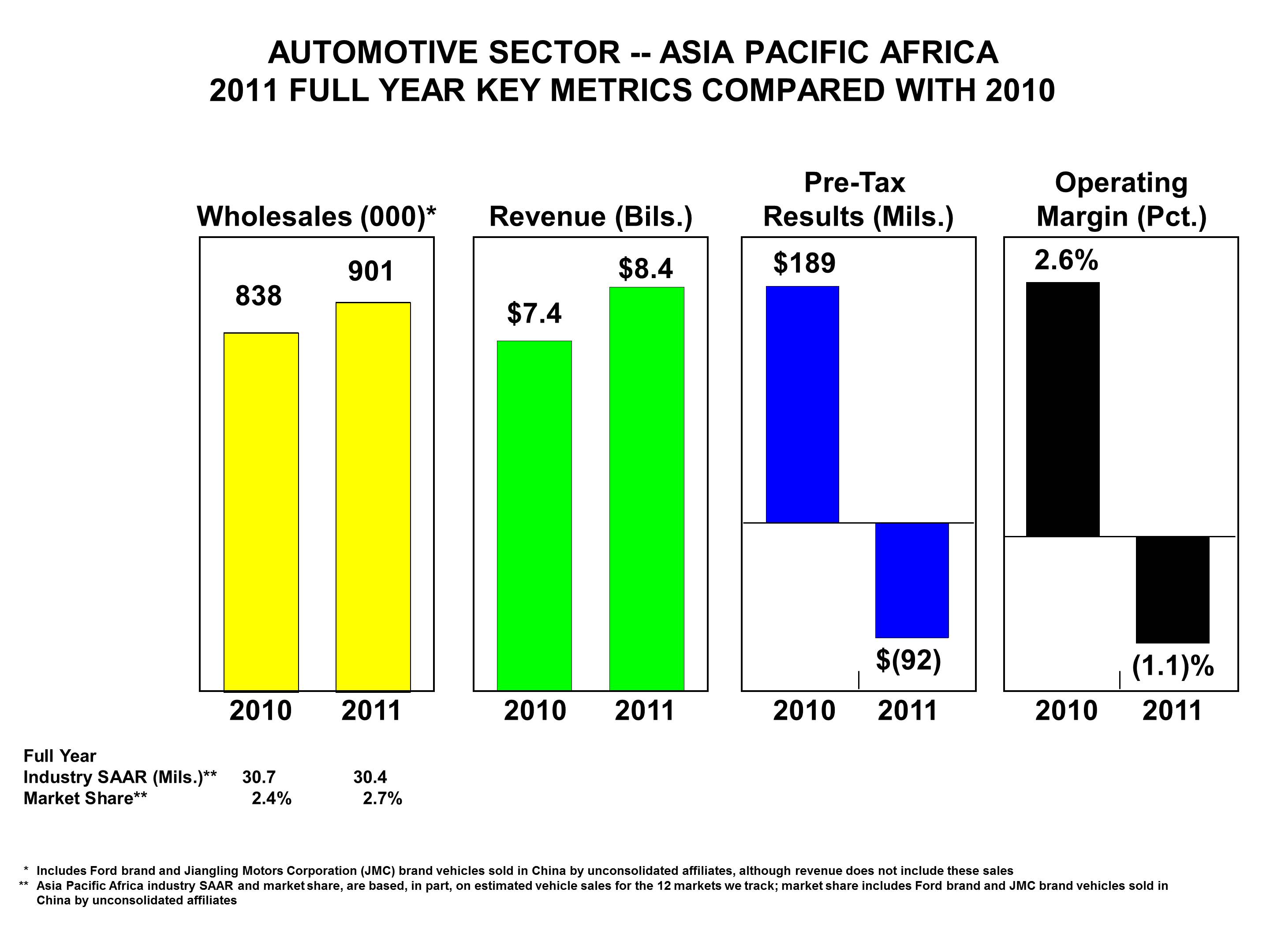

Ford Asia Pacific Africa

Ford Asia Pacific Africa industry sales and market share data focus on our 12 major markets in the region; wholesales are more inclusive, tracking every market in the region. Of the markets we track in this region, ASEAN, Australia, China, India, and South America. Brazil, Argentina, and VenezuelaAfrica are our principal markets in South America. Industry sales in 2009 were approximately 3.1 million units in Brazil (up 11.4% from 2008), 509,000 units in Argentina (down 15.3% from 2008), and 136,000 units in Venezuela (down 49.9% from 2008). Our combined car and truck share for Ford-brand vehicles in these markets was 10.3% in Brazil (up 0.3 percentage points from 2008), 13.3% in Argentina (up 0.9 percentage points from 2008), and 20.9% in Venezuela (up 5.2 percentage points from 2008). In Brazil, 2009 industry sales were strong in comparison to other markets in South America due to government stimulus actions taken in response to the global economic slowdown. We have announced plans for our largest-ever investment in Brazil operations in a five-year period, investing R$4 billion in 2011-2015 to accelerate delivery of more fuel-efficient, high-quality vehicles in Brazil.markets.

Asia Pacific Africa. Australia, China, India, South Africa, and Taiwan are our principal markets in this region. Industry sales in 2009 were approximately 940,000 units in Australia (down 7.4% from 2008), 14.1 million units in China (up 42.1% from 2008), 2.3 million units in India (up 12.2% from 2008), 350,000 units in South Africa (down 27.6% from 2008), and 290,000 units in Taiwan (up 28.4% from 2008). Our combined car and truck share in these markets (including sales of Ford-brand vehicles, and market share for certain unconsolidated affiliates particularly in China) was 10.3% in Australia (about the same as 2008), 1.9% in China (about the same as 2008), 1.3% in India (down 0.1 percentage points from 2008), 7.6% in South Africa (up 0.7 percentage points from 2008) and 6.1% in Taiwan (up 0.6 percentage points from 2008). We anticipate that the ongoing relaxation of import restrictions (including duty reductions) will continue to intensify competition in the region.

ITEM 1. Business (continued)

China and India are the key emerging markets that will continue to drive economic growth in the region. Small cars account for 60% of Asia Pacific Africa industry sales volume, and are anticipated to continue to benefit from government fiscal policy. In lineWe anticipate that the ongoing relaxation of import restrictions (including duty reductions) will continue to intensify competition in the region, particularly around small, ultra-affordable passenger cars. The highly successful launches of our all-new Figo and Fiesta demonstrate our ability to successfully compete in key growth segments. We anticipate further success with these trends,the introduction of the all-new EcoSport later in 2012.

The following tables show our manufacturing capacity investmentswholesales and market share for key markets and in both Thailandtotal for the last five years:

|

| | | | | | | | | | | | | | |

| | Wholesales |

| | (in thousands) |

| | 2011 | | 2010 | | 2009 | | 2008 | | 2007 |

| China | 519 |

| | 483 |

| | 345 |

| | 251 |

| | 203 |

|

| India | 96 |

| | 84 |

| | 30 |

| | 29 |

| | 39 |

|

| Australia | 83 |

| | 104 |

| | 92 |

| | 102 |

| | 108 |

|

| South Africa | 49 |

| | 45 |

| | 38 |

| | 51 |

| | 61 |

|

| ASEAN | 74 |

| | 51 |

| | 38 |

| | 36 |

| | 39 |

|

| Ford Asia Pacific Africa | 901 |

| | 838 |

| | 604 |

| | 532 |

| | 535 |

|

|

| | | | | | | | | | | | | | |

| | Market Share |

| | 2011 | | 2010 | | 2009 | | 2008 | | 2007 |

| China | 2.7 | % | | 2.5 | % | | 2.5 | % | | 2.6 | % | | 2.1 | % |

| India | 2.9 |

| | 2.6 |

| | 1.3 |

| | 1.4 |

| | 1.9 |

|

| Australia | 9.0 |

| | 9.2 |

| | 10.3 |

| | 10.3 |

| | 10.3 |

|

| South Africa | 8.4 |

| | 7.7 |

| | 7.6 |

| | 6.9 |

| | 7.6 |

|

| ASEAN | 2.7 |

| | 1.5 |

| | 1.6 |

| | 1.5 |

| | 2.0 |

|

| Ford Asia Pacific Africa | 2.7 |

| | 2.4 |

| | 2.3 |

| | 2.3 |

| | 2.3 |

|

China and India are nearing completion. At our joint venture assembly facilityburgeoning markets that are expected to continue to experience rapid and substantial growth in Rayong, Thailandthe next ten years, driving new economic growth in the Asia Pacific Africa region. Accordingly, we have invested $500 millionincreased and are planning to increase further our dealer networks and manufacturing capacity in an expansion for the production of small passenger cars. Inregion. We are building seven new plants - four in China, two in India, we have invested $500 million to significantly increase our presence through expansionand one in Thailand - as part of our currentplan to have production capacity of 2.3 million vehicles in the region by mid-decade. These new state-of-the-art highly-flexible manufacturing facilityfacilities will help us reach the goal of increasing worldwide sales to about 8 million vehicles per year by mid-decade.

In China, we also are significantly expanding our research and engineering center in Chennai to begin productionNanjing as part of our new Ford Figo,plan to accelerate our growth in China and construction of a fully-integrated and flexible engine manufacturing plant. As previously announced in September 2009, we also have broken ground on a new plant in Chongqing, China to meet anticipated demand and grow Ford-brand market share.the Asia Pacific Region.

ITEM 1. Business (continued)

FINANCIAL SERVICES SECTOR

Ford Motor Credit Company LLC

Our wholly-owned subsidiary Ford Motor Credit Company LLC ("Ford Credit") offers a wide variety of automotive financing products to and through automotive dealers throughout the world. The predominant share of Ford Credit’s business consists of financing our vehicles and supporting our dealers. Ford Credit’s primary financing products fall into the following three categories:Credit earns its revenue primarily from:

Retail financing. PurchasingPayments made under retail installment sale contracts and retail lease contracts from dealers, and offering financing to commercial customers – primarily vehicle leasing companies and fleet purchasers – to purchase or lease vehicle fleets;

Wholesale financing. Making loans to dealers to finance the purchase of vehicle inventory, also known as floorplan financing; and

Other financing. Making loans to dealers for working capital, improvements to dealership facilities, and to purchase or finance dealership real estate.

Ford Credit also services the finance receivables and leases that it originates and purchases, makes loans to our affiliates, purchases certain receivablespurchases;

Interest supplements and other support payments from us and our subsidiaries and provides insurance services related to its financing programs. Ford Credit’s revenues are earned primarily from payments made under retail installment sale contracts and retail leases (including interest supplements and other support payments it receives from us on special-rate financing programs),programs; and from payments

Payments made under wholesale and other dealer loan financing programs.

As a result of these financing activities, Ford Credit has a large portfolio of finance receivables and leases which it classifies into two segments – "consumer" and "non-consumer." Finance receivables and leases in the consumer segment relate to products offered to individuals and to businesses that finance the acquisition of vehicles from dealers for personal and commercial use. The financing products include retail installment sale contracts for new and used vehicles, and leases for new vehicles to retail customers, government entities, daily rental car companies, and fleet customers. Finance receivables in the non-consumer segment relate primarily to products offered to automotive dealers, including loans to finance the purchase of vehicle inventory (i.e., wholesale financing), for improvements to dealership facilities, for working capital, and for purchase of dealership real estate. Ford Credit also purchases receivables generated by us and our subsidiaries, primarily in connection with the sale of parts and accessories.

Ford Credit does business in all states in the United States and in all provinces in Canada through regional business centers. Outside of the United States, FCE Bank plc ("FCE") is Ford Credit’sCredit's largest operation.operation; Europe is FCE's primary business is to supportlargest market. Within Europe, FCE's largest and most profitable markets are Germany and the saleUnited Kingdom. About 70% of our vehiclesFCE's finance and lease receivables are from FCE's customers and Ford dealers in Europe through our dealer network. FCE offers a variety of retail, leasing and wholesale finance plans in most countries in which it operates; FCE does business inGermany, the United Kingdom, Germany, and most other European countries.France; about 17% are from FCE's customers and Ford Credit, through its subsidiaries, also operatesdealers in the Asia PacificItaly and Latin American regions. In addition,Spain; and about 2% are from FCE's customers and Ford dealers in Greece, Ireland, and Portugal. FCE, through its Worldwide Trade Financing division, also provides financing to dealers in countries where typically we have no established local presence.

Ford Credit's share of retail financing for new Ford Lincoln, and Mercury brandLincoln vehicles sold by dealers in the United States and new Ford-brandFord vehicles sold by dealers in Europe, as well as Ford Credit'sits share of wholesale financing for new Ford Lincoln and Mercury brandLincoln vehicles acquired by dealers in the United States (excluding fleet) and of new Ford-brandFord vehicles acquired by dealers in Europe were as follows during the last three years:were:

| | | United States | | Years Ended December 31, | | Years Ended December 31, |

Financing share – Ford, Lincoln, and Mercury | | | | | | | | | | |

| Financing share – Ford and Lincoln | | 2011 | | 2010 | | 2009 |

Retail installment and lease | | | 29 | % | | | 39 | % | | | 38 | % | 36 | % | | 32 | % | | 29 | % |

Wholesale | | | 79 | | | | 77 | | | | 78 | | 80 |

| | 81 |

| | 79 |

|

| Europe | | | | | | | | | | | | | |

| | |

| | |

|

| Financing share – Ford | | | | | | | | | | | | | |

| | |

| | |

|

Retail installment and lease | | | 28 | % | | | 28 | % | | | 26 | % | 29 | % | | 26 | % | | 28 | % |

Wholesale | | | 99 | | | | 98 | | | | 96 | | 99 |

| | 99 |

| | 99 |

|

See Item 7 and Notes 7, 8, and 9 of the Notes to the Financial Statements for a detailed discussion of Ford Credit's receivables, credit losses, allowance for credit losses, loss-to-receivables ratios, funding sources, and funding strategies. See Item 7A for a discussion of how Ford Credit manages its financial market risks.

ITEM 1. Business (continued)

We routinely sponsor special-rate financing programs available only throughspecial retail and lease incentives to dealers' customers who choose to finance or lease our vehicles from Ford Credit. PursuantIn order to these programs,compensate Ford Credit for the lower interest or lease rates offered to the retail customer, we make interest supplement or other support paymentspay the discounted value of the incentive directly to Ford Credit.Credit when it originates the retail finance or lease contract. These programs increase Ford Credit's financing volume and share of financing sales of our vehicles. See Note 12 of the Notes to the Financial Statements and Item 7 for more information about our accounting for these support payments.programs.

OnIn November 6, 2008, we and Ford Credit entered into an Amended and Restated Support Agreement (“Support Agreement”) (formerly known as the Amended and Restated Profit Maintenance Agreement). Pursuantwith Ford Credit, pursuant to the Support Agreement,which, if Ford Credit’sits managed leverage for a calendar quarter were to be higher than 11.5 to 1 (as reported in Ford Credit’s then-mostits most recent Form 10-Q Report or Form 10-K Report)periodic report), Ford Credit could require us to make or cause to be made a capital contribution to Ford Creditit in an amount sufficient to have caused such managed leverage to have been 11.5 to 1. A copy of the Support Agreement was filed as Exhibit 10 to our Quarterly Report on Form 10-Q for the period ended September 30, 2008. No capital contributions have been made to Ford Credit pursuant to the Support Agreement.this agreement. In addition, Ford Credit has an agreement to maintain FCE’sFCE's net worth in excess of $500 million. Nomillion; no payments have been made by Ford Credit to FCE pursuant to thethat agreement during the 2007 through 2009 periods.in 2001 - 2011.

ITEM 1. Business (continued)

GOVERNMENTAL STANDARDS

Many governmental standards and regulations relating to safety, fuel economy, emissions control, noise control, vehicle recycling, substances of concern, vehicle damage, and theft prevention are applicable to new motor vehicles, engines, and equipment manufactured for sale in the United States, Europe, and elsewhere. In addition, manufacturing and other automotive assembly facilities in the United States, Europe, and elsewhere are subject to stringent standards regulating air emissions, water discharges, and the handling and disposal of hazardous substances. The most significant of the standards and regulations affecting us are discussed below:

Mobile Source Emissions Control

U.S. Requirements –- Federal Emissions Standards. The federal Clean Air Act imposes stringent limits on the amount of regulated pollutants that lawfully may be emitted by new motor vehicles and engines produced for sale in the United States. The current ("Tier 2") emissions regulations promulgated by the U.S. Environmental Protection Agency ("EPA") set standards for cars and light trucks. The Tier 2 emissions standards also establish durability requirements for emissions components to 120,000 miles or 150,000 miles (depending on the specific standards to which the vehicle is certified). These standards present compliance challenges and make it difficult to utilize light-duty diesel technology, which in turn restricts one pathway for improving fuel economy for purposes of satisfying Corporate Average Fuel Economy ("CAFE") standards and upcoming federal greenhouse gas ("GHG") standards.