3

ITEM 1. |

Quality Systems, Inc., The Company also provides revenue cycle management (“RCM”) services through the Practice Solutions Division.

operating divisions: QSI Dental Division and NextGen Division. Through our acquisitions of HSI and PMP in 2008, we continued to strengthen our RCM service offerings. During fiscal year 2010, as a result of certain organizational changes, the composition of the Company’s NextGen Division was revised to exclude the former NextGen Practice Solutions unit and the Company’s RCM entities (HSI and PMP), both of which are now administered and aggregated in the Company’s Practice Solutions Division. Following the reorganization, the Company now operates three reportable operating segments (not including Corporate), comprised of the NextGen Division, the QSI Dental Division and the Practice Solutions Division. As a result, our fiscal year 2010 and 2009 results have beenre-casted to reflect this change.

2008:

| Segment Revenue Breakdown | Segment Revenue Growth | |||||||||||||||||||||||

| for the Year Ended March 31, | for the Year Ended March 31, | |||||||||||||||||||||||

| 2010 | 2009 | 2008 | 2010 | 2009 | 2008 | |||||||||||||||||||

| QSI Dental Division | 5.9 | % | 6.5 | % | 8.6 | % | 8.1 | % | (1.2 | )% | (3.3 | )% | ||||||||||||

| NextGen Division | 79.4 | % | 83.1 | % | 91.4 | % | 13.6 | % | 19.6 | % | 21.3 | % | ||||||||||||

| Practice Solutions Division | 14.7 | % | 10.4 | % | 0.0 | % | 67.5 | % | N/A | N/A | ||||||||||||||

| Consolidated | 100.0 | % | 100.0 | % | 100.0 | % | 18.9 | % | 31.6 | % | 18.7 | % | ||||||||||||

The NextGen Division, with headquarters in Horsham, Pennsylvania,product and Software as a second significant location in Atlanta, Georgia, focuses principally on developingService, or SaaS model, based NextDDS financial and marketing products and services for medical practices.

Both divisions develop and market practice management software that is designed to automate and streamline a number of the administrative functions required for operating a medical or dental practice. Examples of practice management software functions include scheduling and billing capabilities. It is important to note that in both the medical and dental environments, practice

clinical software.

management software systems have already been implemented by the vast majority of practices. Therefore, we actively compete for the replacement market. In addition, both divisions develop and market software that automates the patient record. Adoption rates for this software, commonly referred to as clinical software, are relatively low. Therefore, we are typically competing to replace paper-based patient record alternatives as opposed to replacing previously purchased systems.

Electronic Data Interchange (EDI)/connectivity products are intended to automate a number of manual, often paper-based or telephony intensive communications between patients and/or providers and/or payors. Two of the more common EDI services are forwarding insurance claims electronically from providers to payors and assisting practices with issuing statements to patients. Most client practices utilize at least some of these services from us or one of our competitors. Other EDI/connectivity services are used more sporadically by client practices. We typically compete to displace incumbent vendors for claims and statements accounts, and attempt to increase usage of other elements in our EDI/connectivity product line. In general, EDI services are only sold to those accounts utilizing software from one of our divisions.

The NextGen Division also offers Revenue Cycle Management (RCM) services under the Practice Solutions name. Services provided through the Practice Solutions/RCM unit consist primarily of billing and collections services for medical practices. The Practice Solutions unit utilizes NextGen EPM software to a significant extent.

The QSI Dental Division’s practice management software suite utilizes a UNIX operating system. Its Clinical Product Suite (CPS)(“CPS”) utilizes a Windows NT2 operating system and can be fully integrated with the practice management software from each division.Division. CPS incorporates a wide range of clinical tools including, but not limited to, periodontal charting and digital imaging of X-ray and inter-oral camera images as part of the electronic patient record. The divisionDivision develops, markets, and manages our EDI/Electronic Data Interchange (“EDI”)/connectivity applications. The QSInet Application Service Provider (ASP/Internet)(“ASP/Internet”) offering is also developed and marketed by the Division.

4

Our

| • | NextGen ambulatory product suite that integrates as one system to streamline patient care with standardized, real-time clinical and administrative workflow through the practice, which consists of: |

| ○ | NextGen Electronic Health Records (“NextGenehr”) to ensure complete, accurate documentation to manage patient care electronically and to improve clinical processes and patient outcomes with electronic charting at the point of care; and | |

| ○ | NextGen Enterprise Practice Management (“NextGenepm”) to automate business processes, from front-end scheduling to back-end collections and financial and administrative processes for increased performance and efficiencies. |

| • | NextGen inpatient products that deliver secure, highly adaptable, and easy to use applications to patient centered hospitals and health systems, which consists of: |

| ○ | NextGen Clinicals, which resides on an advanced truly active web 2.0 platform — and is designed to initiate widespread work efficiency and communication, reduce errors andtime-to-chart, and improve care; and | |

| ○ | NextGen Financials, which is a financial and administrative system that helps hospitals significantly improve the smart operations and financial and regulatory management of their facilities. |

| • | NextGen Community Connectivity, which consists of: |

| ○ | NextGen Health Information Exchange (“HIE”), formerly Community Health Solution, to exchange patient data securely with community healthcare organizations; | |

| ○ | NextGen Patient Portal (“NextMD.com”) to communicate with patients online and import information directly into NextGenehr; and | |

| ○ | NextGen Health Quality Measures (“HQM”) to allow seamless quality measurement and reporting for practice and physician performance initiatives. |

5

| • | EDI services that are intended to automate a number of manual, often paper-based or telephony intensive communications between patientsand/or providersand/or payors; | |

| • | Hosting services that allow practices seeking the benefits of IT automation but not the maintenance of in-house hardware and networking; | |

| • | NextGuard — Data Protection services that provide an off-site, data archiving, restoration, and disaster recovery preparedness solution for practices to protect clinical and financial data; | |

| • | Consulting services, such as data conversions or interface development, that allow practices to build custom add-on features; and | |

| • | Physician Resources services that allow practices to consult with the NextGen Division’s physician team. |

Inclusive of divisional EDI revenue,

In addition to the aforementioned software solutions whicheconomic cycles, we offer through our two divisions, each division offers comprehensive hardware and software installation services, maintenance and support services, and system training services.

On May 20, 2008, the Company acquired Lackland Acquisition II, LLC dba Healthcare Strategic Initiatives (HSI). The acquisition resulted in HSI becoming a wholly owned subsidiary of QSI. We plan to operate HSI as a stand alone Company within the NextGen Division.

3 NextGen is a registered trademark

6

4 NextMD is a registered trademarkhealth care information technology. While we are unsure of NextGen Healthcare Information Systems, Inc.

HSI is a full-service healthcare revenue management company servicing the revenue cycle management needs of physician groups and a variety of other healthcare clients. HSI has historically and primarily focused on assisting its clients in increasingimmediate impact from the accuracy and speed of client billing and collections activities.

Industry Background

ToARRA, the long-term potential could be significant.

| • | Continued development and enhancement of select software solutions in target markets; |

| • | Continued investments in our infrastructure including, but not limited to, product development, sales, marketing, implementation, and support; |

| • | Continued efforts to make infrastructure investments within an overall context of maintaining reasonable expense discipline; |

| • | Addition of new customers through maintaining and expanding sales, marketing and product development activities; |

| • | Expanding our relationship with existing customers through delivery of |

| • | Continuing our gold standard commitment of service in support of our customers. |

7

comprehensive systems implementation, maintenance and support services. Any single transaction may or may not include software, hardware or services.

The QSI Division’s character-based practice management system is available We offer both standard licenses and SaaS arrangements in both dental and medical versions and primarily uses the IBM RS6000[5] central processing unit and IBM’S AIX[6] version of the UNIX operating system as a platform for our application software enabling a wide range of flexible and functional systems. The hardware components, as well as the requisite operating system licenses, are purchased from manufacturers or distributors of those components.

We configure and test the hardware components and incorporate our software and other third party packages into completed systems. We continually evaluate third party hardware components with a view toward utilizing hardware that is functional, reliable and cost-effective.

offerings; although to date, SaaS arrangements have represented less than 5% of our arrangements.

We also offer practice management solutions for both dental and medical practices through the Internet. These products are marketed under the QSINet and NextGen WEB trade names, respectively.

Clinical Systems. Our dental charting software system, the Clinical Product Suite (CPS),epm product is a comprehensivehighly configurable, cost-effective proven solution designed specifically forthat enables the dental group practice environment. CPS integrates the dental practiceeffective management product with a computer-based clinical information system that incorporates a wide range of clinical tools, including:

|

|

|

|

|

|

|

|

|

|

|

|

both single and multi-practice settings.

CPS incorporates Windows-based client-server technology consisting of one or more file servers together with any combination of one or more desktop, laptop, or pen-based PC workstations. The file server(s) used in connection with CPS utilize(s) a Windows NT or Windows 2000 or Windows XP operating system and the hardware is typically a Pentium[7]-based single or multi-processor platform. Based on the server configuration chosen, CPS is scalable from one to hundreds of workstations. A typical configuration may also include redundant disk storage, magnetic tape units, intra- and extra-oral cameras, digital X-ray components, digital scanners, conventional and flat screen displays, and printers. The hardware components, including the requisite operating system licenses, are purchased from third party manufacturers or distributors either directly by the customer or by us for resale to the customer.

6 AIX is a registered trademark of International Business Machines Corporation.

7 Pentium is a registered trademark of Intel Corporation.

8 Microsoft and SQL Server is a registered trademark of Microsoft Corporation.

9 Oracle is a registered trademark of Oracle Corporation.

NextGen Division provides clinical software applications that are complementary to, and are integrated with, our medical practice management offerings and interface with many of the other leading practice management software systems on the market. The applications incorporated into our practice management solutions and others such as scheduling, eligibility, billing and claims processing are augmented by clinical information captured by NextGen EMR,ehr, including services rendered and diagnoses used for billing purposes. We believe that we currently provide a comprehensive information management solution for the medical marketplace.

NextGen EMRehr stores and maintains clinical data including:

| • | Data captured using user-customizable input “templates”; |

| • | Scanned or electronically acquired images, including X-rays and photographs; |

| • | Data electronically acquired through interfaces with clinical instruments or external systems; |

| • | Other records, documents or notes, including electronically captured handwriting and annotations; and |

| • | Digital voice recordings. |

8

| • | Electronic claims submission service that submits Health Insurance Portability and Accountability Act of 1996 (“HIPAA”) compliant insurance claims electronically to insurance payers; | |

| • | Electronic remittance and payment posting service that uses NextGen Document Management system to link an image of each explanation of benefit (“EOB”) to the corresponding encounter at the time of payment posting to minimizes the need for storage of paper EOBs; and | |

| • | Accounts receivablefollow-up methodology that allows practices to establish parameters, adjustment rules and standards for account elevation. |

9

| • | Electronic claims submission through our relationships with a number of payors and national claims clearinghouses; | |

| • | Electronic patient statement processing, appointment reminder cards and calls, recall cards, patient letters, and other correspondence; | |

| • | Electronic insurance eligibility verification; and | |

| • | Electronic posting of remittances from insurance carriers into the accounts receivable application. |

NextGen also markets revenue cycle management services through our Practice Solutions unit. This service provides billing services to solo and group practices.

Connectivity Services. We make available EDI capabilities and connectivity services to our customers. The EDI/connectivity capabilities encompass direct interfaces between our products and external third party systems, as well as transaction-based services. Services include:

|

|

|

|

|

|

|

|

Revenue Cycle Management Services Our Nextgen Practice Solutions unit offers revenue cycle management services to physicians. On May 20, 2008, we acquired HSI, a full-service healthcare revenue management company servicing the revenue cycle management needs of physician groups and a variety of other healthcare clients. HSI has historically and primarily focused on assisting its clients in increasing the accuracy and speed of client billing and collections activities.

Internet Applications. Our NextGen Division maintains an Internet-based patient health portal, NextMD®. NextMDNextMD.com. NextMD.com is a vertical portal for the healthcare industry, linking patients with their physicians, while providing a centralized source of health-oriented information for both consumers and medical professionals. Patients whose physicians are linked to the portal are able to request appointments, send appointment changes or cancellations, receive test results on-line, request prescription refills, viewand/or pay their statements, and communicate with their physicians, all in a secure, on-line environment. Our NextGen suite of information systems are or can be linked to NextMD,NextMD.com, integrating a number of these features with physicians’ existing systems.

2008.

10

MSO’s, PHO’s

11

12

ITEM 1A. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Our software products are generally shipped as orders are received and accordingly, we have historically operated with a minimal backlog of license fees. As a result, revenue in any quarter is dependent on orders booked and shipped in that quarter and is not predictable with any degree of certainty. Furthermore, our systems can be relatively large and expensive and

individual systems sales can represent a significant portion of our revenue and profits for a quarter such that the loss or deferral of even one such sale can adversely affect our quarterly revenue and profitability.

Clients often defer systems purchases until our quarter end, so quarterly results generally cannot be predicted and frequently are not known until after the quarter has concluded.

Our sales are dependent upon clients’ initial decisions to replace or substantially modify their existing information systems, and subsequently a decision as to which products and services to purchase. These are major decisions for healthcare providers, and accordingly, the sales cycle for our systems can vary significantly and typically ranges from six to twenty four months from initial contact to contract execution/shipment.

Because a significant percentage of our expenses are relatively fixed, a variation in the timing of systems sales, implementations, and installations can cause significant variations in operating results from quarter to quarter. As a result, we believe that interim period-to-period comparisons of ourbusiness, results of operations are not necessarily meaningful and should notfinancial condition may be relied upon as indicationsadversely affected. The software market generally is characterized by rapid technological change, changing customer needs, frequent new product introductions, and evolving industry standards. The introduction of future performance. Further,products incorporating new technologies and the emergence of new industry standards could render our historical operating results are not necessarily indicative of future performance for any particular period.

We currently recognize revenue pursuant to Statement of Position (SOP) 97-2, as modified by SOP 98-9existing products obsolete and Staff Accounting Bulletin (SAB) 104. SAB 104 summarizes the staff’s views in applying generally accepted accounting principles to revenue recognition in financial statements.

unmarketable. There can be no assurance that applicationwe will be successful in developing and subsequent interpretationsmarketing new products that respond to technological changes or evolving industry standards. New product development depends upon significant research and development expenditures which depend ultimately upon sales growth. Any material shortfall in revenue or research

13

| • | potentially dilutive issuances of our securities, the incurrence of debt and contingent liabilities and amortization expenses related to intangible assets, which could adversely affect our results of operations and financial condition; | |

| • | use of cash as acquisition currency may adversely affect interest or investment income, thereby potentially adversely affecting our earnings and /or earnings per share; | |

| • | difficulty in effectively integrating any acquired technologies or software products into our current products and technologies; | |

| • | difficulty in predicting and responding to issues related to product transition such as development, distribution and customer support; | |

| • | the possible adverse effect of such acquisitions on existing relationships with third party partners and suppliers of technologies and services; | |

| • | the possibility that staff or customers of the acquired company might not accept new ownership and may transition to different technologies or attempt to renegotiate contract terms or relationships, including maintenance or support agreements; | |

| • | the possibility that the due diligence process in any such acquisition may not completely identify material issues associated with product quality, product architecture, product development, intellectual property issues, key personnel issues or legal and financial contingencies, including any deficiencies in internal controls and procedures and the costs associated with remedying such deficiencies; |

14

| • | difficulty in integrating acquired operations due to geographical distance, and language and cultural differences; and | |

| • | the possibility that acquired assets become impaired, requiring us to take a charge to earnings which could be significant. |

customers, our vendors and us to accurately forecast and plan future business activities, and they could cause constrained spending on our products and services,and/or delay and lengthen sales cycles.

15

Our common stock price has been volatile, which could result in substantial losses for investors purchasing shares of our common stock and in litigation against us. Volatility may be caused by a number of factors including but not limited to:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Furthermore, the stock market in general, and the market for software, healthcare and high technology companies in particular, has experienced extreme volatility that often has been unrelated to the operating performance of particular companies. These broad market and industry fluctuations may adversely affect the trading price of our common stock, regardless of actual operating performance.

Moreover, in the past, securities class action litigation has often been brought against a company following periods of volatility in the market price of its securities. We may in the future be the target of similar litigation. Securities litigation could result in substantial costs and divert management’s attention and resources.

Two of our directors are significant shareholders, which makes it possible for them to have significant influence over the outcome of all matters submitted to our shareholders for approval and which influence may be alleged to conflict with our interests and the interests of our other shareholders. Two of our directors and principal shareholders beneficially owned an aggregate of approximately 36% of the outstanding shares of our common stock at March 31, 2008. Our Bylaws permit our shareholders to cumulate their votes, the effect of which is to provide shareholders with sufficiently large concentrations of our shares the opportunity to assure themselves one or more seats on our Board. The amounts required to assure a Board position can vary based upon the number of shares outstanding, the number of shares voting, the number of directors to be elected, the number of “broker non-votes”, and the number of shares held by the shareholder exercising cumulative voting rights. In the event that cumulative voting is invoked, it is likely that the two of our directors holding an aggregate of approximately 36% of the outstanding shares of our common stock at March 31, 2008 will each have sufficient votes to assure themselves of one or more seats on our Board. With or without cumulative voting, these shareholders will have significant influence over the outcome of all matters submitted to our shareholders for approval, including the election of our directors and other corporate actions. In addition, such influence by one or both of these affiliates could have the effect of discouraging others from attempting to purchase us, take us over, and/or reducing the market price offered for our common stock in such an event.

from traditional software license, implementation and training fees, as well as the resale of computer hardware. Today, the majority of our customers pay an initial license fee for the use of our products, in addition to a periodic maintenance fee. While the intent of the new subscription based delivery model is to further penetrate the smaller practice market, there can be no assurance that this delivery model will not become increasingly popular with both small and large customers. If the marketplace increasingly demands subscription pricing, we may be forced to further adjust our sales, marketing and pricing strategies accordingly, by offering a higher percentage of our products and services through these means. Shifting to a significantly greater degree of subscription pricing could adversely affect our financial condition, cash flows and quarterly and annual revenue and results of operations, as our revenue would initially decrease substantially. There can be no assurance that the marketplace will not increasingly embrace subscription pricing.Many of our competitors have greater resources than we do. In order to compete successfully, we must keep pace with our competitors in anticipating and responding to the rapid changes involving the industry in which we operate, or our business, results of operations and financial condition may be adversely affected. The software market generally is characterized by rapid technological change, changing customer needs, frequent new product introductions, and evolving industry standards. The introduction of products incorporating new technologies and the emergence of new industry standards could render our existing products obsolete and unmarketable. There can be no assurance that we will be successful in developing and marketing new products that respond to technological changes or evolving industry standards. New product development depends upon significant research and development expenditures which depend ultimately upon sales growth. Any material shortfall in revenue or research funding could impair our ability to respond to technological advances or opportunities in the marketplace and to remain competitive. If we are unable, for technological or other reasons, to develop and introduce new products in a timely manner in response to changing market conditions or customer requirements, our business, results of operations and financial condition may be adversely affected.In response to increasing market demand, we are currently developing new generations of certain of our software products. There can be no assurance that we will successfully develop these new software products or that these products will operate successfully, or that any such development, even if successful, will be completed concurrently with or prior to introduction of competing products. Any such failure or delay could adversely affect our competitive position or could make our current products obsolete.We face risk and/or the possibility of claims from activities related to strategic partners, which could be expensive and time-consuming, divert personnel and other resources from our business and result in adverse publicity that could harm our business. We rely on third parties to provide services that affect our business. For example, we use national clearinghouses in the processing of some insurance claims and we outsource some of our hardware maintenance services and the printing and delivery of patient statements for our customers. These third parties could raise their prices and/or be acquired by competitors of our which could potentially create short and long-term disruptions to our business negatively impacting our revenue, profit and/or stock price. We also have relationships with certain third parties where these third parties serve as sales channels through which we generate a portion of our revenue. Due to these third-party relationships, we could be subject to claims as a result of the activities, products, or services of these third-party service providers even though we were not directly involved in the circumstances leading to those claims. Even if these claims do not result in liability to us, defending and investigating these claims could be expensive and time-consuming, divert personnel and other resources from our business and result in adverse publicity that could harm our business.website,Web site content, which may cause us expense and management distraction.distraction. We could be subject to third party claims based on the nature and content of information supplied on our websiteWeb site by us or third parties, including content providers or users. We could also be subject to

16

17

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A failuredevelopment and maintenance of the Internet infrastructure, which is not within our control, and which may diminish Internet usage and availability as well as access to successfully integrate acquired businessesour Web site

| • | state and federal privacy and confidentiality laws; | |

| • | our contracts with customers and partners; | |

| • | state laws regulating healthcare professionals; | |

| • | Medicaid laws; | |

| • | the HIPAA and related rules proposed by the Health Care Financing Administration; and | |

| • | Health Care Financing Administration standards for Internet transmission of health data. |

18

19

There is significant uncertainty in the healthcare industry in which we operate, and we are subject to the possibility of changing government regulation, which may adversely impact our business, financial condition and results of operations.The healthcare industry is subject to changing political, economic and regulatory influences that may affect the procurement processes and operation of healthcare facilities. During the past several years, the healthcare industry has been subject to an increase in governmental regulation of, among other things, reimbursement rates and certain capital expenditures.–— even if we are ultimately successful in the defense of such matters. Furthermore, a party making a claim against us could secure a judgment awarding substantial damages, as well as injunctive or other equitable relief that could effectively block our ability to provide products or services. In addition, we cannot assure you that licenses for any intellectual property of third parties that might be required for our products or services will be available on commercially reasonable terms, or at all.shipments.shipments. We depend upon licenses for some of the technology used in our products as well as other services from third-party vendors. Most of these arrangements can be continued/renewed only by mutual consent and may be terminated for any number of reasons. We may not be able to continue using the products or services made available to us under these arrangements on commercially reasonable terms or at all. As a result, we may have to discontinue, delay or reduce product shipments or services provided until we can obtain equivalent technology or services. Most of our third-party licenses are non-exclusive. Our competitors may obtain the right to use any of the business elements covered by these arrangements and use these elements to compete directly with us. In addition, if our vendors choose to discontinue providing their technology or services in the future or are unsuccessful in their continued research and development efforts, we may not be able to modify or adapt our own products.We face the possibility of damages resulting from internal and external security breaches, and viruses. In the course of our business operations, we compile and transmit confidential information, including patient health information, in our processing centers and other facilities. A breach of security in any of these facilities could damage our reputation and result in damages being assessed against us. In addition, the other systems with which we may interface, such as the Internet and related systems may be vulnerable to security breaches, viruses, programming errors, or similar disruptive problems. The effect of these security breaches and related issues could disrupt our ability to perform certain key business functions and could potentially reduce demand for our services. Accordingly, we have expended significant resources toward establishing and enhancing the security of our related infrastructures, although no assurance can be given that they will be entirely free from potential breach. Maintaining and enhancing our infrastructure security may require us to expend significant capital in the future.The success of our strategy to offer our EDI services and Internet solutions depends on the confidence of our customers in our ability to securely transmit confidential information. Our EDI services and Internet solutions rely on encryption, authentication and other security technology licensed from third parties to achieve secure transmission of confidential information. We may not be able to stop unauthorized attempts to gain access to or disrupt the transmission of communications by our customers. Anyone who is able to circumvent our security measures could misappropriate confidential user information or interrupt our, or our customers’ operations. In addition, our EDI and Internet solutions may be vulnerable to viruses, physical or electronic break-ins, and similar disruptions.Any failure to provide secure infrastructure and/or electronic communication services could result in a lack of trust by our customers causing them to seek out other vendors, and/or, damage our reputation in the market making it difficult to obtain new customers.We are subject to the development and maintenance of the Internet infrastructure, which is not within our control, and which may diminish Internet usage and availability as well as access to our website. We deliver Internet-based services and, accordingly, we are dependent on the maintenance of the Internet by third parties. The Internet infrastructure may be unable to support the demands placed on it and our performance may decrease if the Internet continues to experience it’s historic trend of expanding usage. As a result of damage to portions of its infrastructure, the Internet has experienced a variety of performance problems which may continue into the foreseeable future. Such Internet related problems may diminish Internet usage and availability of the Internet to us for transmittal of our Internet-based services. In addition, difficulties, outages, and delays by Internet service providers, online service providers andother website operators may obstruct or diminish access to our website by our customers resulting in a loss of potential or existing users of our services.Our failure to manage growth could harm our business, results of operations and financial condition. We have in the past experienced periods of growth which have placed, and may continue to place, a significant strain on our non-cash resources. We also anticipate expanding our overall software development, marketing, sales, client management and training capacity. In the event we are unable to identify, hire, train and retain qualified individuals in such capacities within a reasonable timeframe, such failure could have an adverse effect on us. In addition, our ability to manage future increases, if any, in the scope of our operations or personnel will depend on significant expansion of our research and development, marketing and sales, management, and administrative and financial capabilities. The failure of our management to effectively manage expansion in our business could have an adverse effect on our business, results of operations and financial condition.Our operations are dependent upon our key personnel. If such personnel were to leave unexpectedly, we may not be able to execute our business plan. Our future performance depends in significant part upon the continued service of our key technical and senior management personnel, many of whom have been with us for a significant period of time. These personnel have acquired specialized knowledge and skills with respect to our business. We maintain key man life insurance on only one of our employees. Because we have a relatively small number of employees when compared to other leading companies in our industry, our dependence on maintaining our relationships with key employees is particularly significant. We are also dependent on our ability to attract high quality personnel, particularly in the areas of sales and applications development.The industry in which we operate is characterized by a high level of employee mobility and aggressive recruiting of skilled personnel. There can be no assurance that our current employees will continue to work for us. Loss of services of key employees could have an adverse effect on our business, results of operations and financial condition. Furthermore, we may need to grant additional equity incentives to key employees and provide other forms of incentive compensation to attract and retain such key personnel. Failure to provide such types of incentive compensation could jeopardize our recruitment and retention capabilities.Our products may be subject to product liability legal claims, which could have an adverse effect on our business, results of operations and financial condition. Certain of our products provide applications that relate to patient clinical information. Any failure by our products to provide accurate and timely information could result in claims against us. In addition, a court or government agency may take the position that our delivery of health information directly, including through licensed practitioners, or delivery of information by a third party site that a consumer accesses through our Web sites, exposes us to assertions of malpractice, other personal injury liability, or other liability for wrongful delivery/handling of healthcare services or erroneous health information. We maintain insurance to protect against claims associated with the use of our products as well as liability limitation language in our end-user license agreements, but there can be no assurance that our insurance coverage or contractual language would adequately cover any claim asserted against us. A successful claim brought against us in excess of or outside of our insurance coverage could have an adverse effect on our business, results of operations and financial condition. Even unsuccessful claims could result in our expenditure of funds for litigation and management time and resources.•Certain healthcare professionals who use our Internet-based products will directly enter health information about their patients including information that constitutes a record under applicable law that we may store on our computer systems. Numerous federal and state laws and regulations, the common law, and contractual obligations, govern collection, dissemination, use and confidentiality of patient-identifiable health information, including:•state and federal privacy and confidentiality laws;•our contracts with customers and partners;•state laws regulating healthcare professionals;•Medicaid laws;•the Health Insurance Portability and Accountability Act of 1996 (HIPAA) and related rules proposed by the Health Care Financing Administration; and•Health Care Financing Administration standards for Internet transmission of health data.The Health Insurance Portability and Accountability Act of 1996 establishes elements including, but not limited to, federal privacy and security standards for the use and protection of Protected Health Information. Any failure by us or by our personnel or partners to comply with applicable requirements may result in a material liability to us.Although we have systems and policies in place for safeguarding Protected Health Information from unauthorized disclosure, these systems and policies may not preclude claims against us for alleged violations of applicable requirements. Also, third party sites and/or links that consumers may access through our web sites may not maintain adequate systems to safeguard this information, or may circumvent systems and policies we have put in place. In addition, future laws or changes in current laws may necessitate costly adaptations to our policies, procedures, or systems.There can be no assurance that we will not be subject to product liability claims, that such claims will not result in liability in excess of our insurance coverage, that our insurance will cover such claims or that appropriate insurance will continue to be available to us in the future at commercially reasonable rates. Such product liability claims could adversely affect our business, results of operations and financial condition.We are subject to the effect of payor and provider conduct which we cannot control and accordingly, there is no assurance that revenues for our services will continue at historic levels. We offer certain electronic claims submission products and services as part of our product line. While we have implemented certain product features designed to maximize the accuracy and completeness of claims submissions, these features may not be sufficient to prevent inaccurate claims data from being submitted to payors. Should inaccurate claims data be submitted to payors, we may be subject to liability claims.Electronic data transmission services are offered by certain payors to healthcare providers that establish a direct link between the provider and payor. This process reduces revenue to third party EDI service providers such as us. As a result of this, or other market factors, we are unable to ensure that we will continue to generate revenue at or in excess of prior levels for such services.A significant increase in the utilization of direct links between healthcare providers and payors could adversely affect our transaction volume and financial results. In addition, we cannot provide assurance that we will be able to maintain our existing links to payors or develop new connections on terms that are economically satisfactory to us, if at all.

20

In addition, developments

In addition, our

operations.operations. Based on our reading and interpretations of relevant guidance, principles or

21

price.

| • | the size and timing of orders from clients; | |

| • | the specific mix of software, hardware, and services in client orders; | |

| • | the length of sales cycles and installation processes; | |

| • | the ability of our clients to obtain financing for the purchase of our products; | |

| • | changes in pricing policies or price reductions by us or our competitors; | |

| • | the timing of new product announcements and product introductions by us or our competitors; | |

| • | changes in revenue recognition or other accounting guidelines employed by usand/or established by the Financial Accounting Standards Board or other rule-making bodies; | |

| • | accounting policies concerning the timing of the recognition of revenue; | |

| • | the availability and cost of system components; |

22

Continuing worldwide political

| • | the financial stability of clients; | |

| • | market acceptance of new products, applications and product enhancements; | |

| • | our ability to develop, introduce and market new products, applications and product enhancements; | |

| • | our success in expanding our sales and marketing programs; | |

| • | deferrals of client orders in anticipation of new products, applications, product enhancements, or public/private sector initiatives; | |

| • | execution of or changes to our strategy; | |

| • | personnel changes; and | |

| • | general market/economic factors. |

Our future policy concerning stock splits is uncertain. While we effectedcycle for our systems can vary significantly and typically ranges from six to twenty four months from initial contact to contract execution/shipment.

| • | actual or anticipated quarterly variations in operating results; | |

| • | rumors about our performance, software solutions, or merger and acquisition activity; | |

| • | changes in expectations of future financial performance or changes in estimates of securities analysts; | |

| • | governmental regulatory action; | |

| • | health care reform measures; |

23

| • | client relationship developments; | |

| • | purchases or sales of company stock; | |

| • | activities by one or more of our major shareholders concerning our policies and operations; | |

| • | changes occurring in the markets in general; | |

| • | macroeconomic conditions, both nationally and internationally; and | |

| • | other factors, many of which are beyond our control. |

ITEM 1B. |

24

| |

ITEM 2. |

lease for approximately 24,000 square feet where our principal administrative, accounting and QSI Division operations will reside after May 2008. This lease expires in May 2013.

In September 2005, we executed a lease for approximately 3,300 square feet of space in a building adjacent to our corporate office in Irvine to house additional corporate staff and NextGen training operations. This lease originally expires in January 2011, however, this lease will terminate early in December 2008 and the NextGen training center along with the additional corporate staff will move to the new corporate headquarters described above.

We lease approximately 78,000 square feet of space for the principal office of our NextGen Division in Horsham, Pennsylvania. This lease expires in March 2011. In January 2007, we executed a new lease for approximately 35,000 square feet of space for the NextGen Division in Atlanta, Georgia. This lease expires in October 2011. In May 2006, we executed a lease for approximately 3,000 square feet of space in Dallas, Texas for NextGen staff and a new NextGen training facility. In addition, we lease approximately 6,000 square feet of space in Santa Ana, California, to house our assembly and warehouse operations of the QSI Division. We also have an aggregate of approximately 3,000 square feet of space in Minnesota, Utah, Wisconsin, and Washington to house additional sales, training, development and service operations. These leases, excluding options, have expiration dates ranging from month-to-month to October 2011.California. Should we continue to grow, we may be required to lease additional space. We believe that suitable additional or substitute space is available, if needed, at market rates.

| Square Feet | ||||

| QSI Dental Division | ||||

| Irvine, California — Corporate Headquarters | 24,000 | |||

| Other U.S. locations | 5,000 | |||

| NextGen Division | ||||

| Horsham, Pennsylvania | 98,000 | |||

| Austin, Texas | 39,000 | |||

| Atlanta, Georgia | 35,000 | |||

| Laguna Hills, California | 4,500 | |||

| Practice Solutions Division | ||||

| St. Louis, Missouri | 66,500 | |||

| Hunt Valley, Maryland | 33,500 | |||

| Total leased properties | 305,500 | |||

| ITEM 3. |

ITEM 4. |

No matter was submitted to a vote of security holders during the fourth quarter of fiscal year 2008.

ITEM 5. | MARKET FOR REGISTRANT’S COMMON |

| High | Low | |||||||

| Quarter Ended | ||||||||

| June 30, 2008 | $ | 35.97 | $ | 29.00 | ||||

| September 30, 2008 | $ | 47.94 | $ | 27.34 | ||||

| December 31, 2008 | $ | 44.98 | $ | 25.70 | ||||

| March 31, 2009 | $ | 48.46 | $ | 34.26 | ||||

| June 30, 2009 | $ | 62.00 | $ | 43.44 | ||||

| September 30, 2009 | $ | 64.16 | $ | 50.87 | ||||

| December 31, 2009 | $ | 65.98 | $ | 57.63 | ||||

| March 31, 2010 | $ | 68.59 | $ | 51.30 | ||||

25

|

|

|

|

|

|

|

|

Quarter Ended |

| High |

| Low |

| ||

|

|

| |||||

|

|

|

|

|

| ||

June 30, 2006 |

| $ | 38.27 |

| $ | 28.30 |

|

September 30, 2006 |

| $ | 42.00 |

| $ | 30.43 |

|

December 31, 2006 |

| $ | 43.68 |

| $ | 34.75 |

|

March 31, 2007 |

| $ | 45.44 |

| $ | 36.85 |

|

June 30, 2007 |

| $ | 42.44 |

| $ | 36.96 |

|

September 30, 2007 |

| $ | 45.35 |

| $ | 32.37 |

|

December 31, 2007 |

| $ | 38.99 |

| $ | 26.08 |

|

March 31, 2008 |

| $ | 36.30 |

| $ | 26.90 |

|

On January 30, 2008, the Board approved a quarterly cash dividend of $0.25 per share on our outstanding shares of common stock, payable to shareholders of record as of March 14, 2008 and was distributed to shareholders on or about April 7, 2008.

On October 25, 2007, the Board approved a quarterly cash dividend of $0.25 per share on our outstanding shares of common stock, payable to shareholders of record as of December 14, 2007 and was distributed to shareholders on or about January 7, 2008.

On July 31, 2007, our Board of Directors approved a regular quarterly dividend of $0.25 per share payable on its outstanding shares of common stock. The cash dividend record date was September 14, 2007 and was distributed to shareholders on or about October 5, 2007.

On May 31, 2007, the Board declared a quarterly cash dividend of $0.25 per share on our outstanding shares of common stock, payable to shareholders of record as of June 15, 2007 and was distributed to shareholders on July 5, 2007.

In February 2007, we paid a $1.00 per share dividend on shares of our common stock. The record date for the dividend was February 13, 2007.

In March 2006, we paid a $0.875 per share dividend on shares of our common stock. The record date for

In January 2006, we announced that our Board of Directors had declaredapproved a 2-for-1 stock split with respect toquarterly cash dividend of $0.30 per share on our outstanding shares of common stock, forpayable to shareholders of record as of June 17, 2010 with an expected distribution date on March 3, 2006. or about July 6, 2010.

In March 2005, we paid a one-time dividend on shares of our common stock equal to $0.75 per share. The record date for the dividend was February 24, 2005. The dividend per share amount has been adjusted to reflect the stock split noted above.

In February 2005, we announced that our Board of Directors declared a 2-for-1 stock split with respect to our outstanding shares of common stock. The stock split record date was March 4, 2005 and the stock began trading post split on March 28, 2005.

dates indicated:

| Record | Payment | Dividend | ||||||

Board Approval Date | Date | Date | Amount | |||||

Fiscal year 2010 | ||||||||

| January 27, 2010 | March 23, 2010 | April 5, 2010 | $ | 0.30 | ||||

| October 28, 2009 | December 23, 2009 | January 5, 2010 | 0.30 | |||||

| July 23, 2009 | September 25, 2009 | October 5, 2009 | 0.30 | |||||

| May 27, 2009 | June 12, 2009 | July 6, 2009 | 0.30 | |||||

Fiscal year 2009 | ||||||||

| January 28, 2009 | March 11, 2009 | April 3, 2009 | $ | 0.30 | ||||

| October 30, 2008 | December 15, 2008 | January 5, 2009 | 0.30 | |||||

| August 4, 2008 | September 15, 2008 | October 1, 2008 | 0.30 | |||||

| May 29, 2008 | June 15, 2008 | July 2, 2008 | 0.25 | |||||

Fiscal year 2008 | ||||||||

| January 30, 2008 | March 14, 2008 | April 7, 2008 | $ | 0.25 | ||||

| October 25, 2007 | December 14, 2007 | January 7, 2008 | 0.25 | |||||

| July 31, 2007 | September 14, 2007 | October 5, 2007 | 0.25 | |||||

| May 31, 2007 | June 15, 2007 | July 5, 2007 | 0.25 | |||||

26

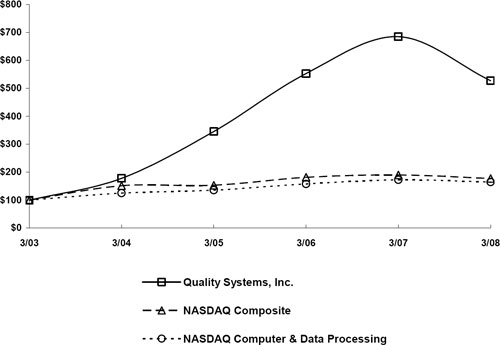

Among Quality Systems, Inc., The NASDAQ Composite Index

And The NASDAQ Computer & Data Processing Index

| |

|

27

Recent Sales of Unregistered Securities

We did not make any unregistered sales of our common stock during the fourth quarter of 2008.

ITEM 6. |

| Year Ended March 31, | ||||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

| (In thousands, except per share data) | ||||||||||||||||||||

| Statements of Income Data: | ||||||||||||||||||||

| Revenue | $ | 291,811 | $ | 245,515 | $ | 186,500 | $ | 157,165 | $ | 119,287 | ||||||||||

| Cost of revenue | 110,807 | 88,890 | 62,501 | 50,784 | 39,828 | |||||||||||||||

| Gross profit | 181,004 | 156,625 | 123,999 | 106,381 | 79,459 | |||||||||||||||

| Selling, general and administrative expenses | 86,951 | 69,410 | 53,260 | 45,337 | 35,554 | |||||||||||||||

| Research and development costs | 16,546 | 13,777 | 11,350 | 10,166 | 8,087 | |||||||||||||||

| Amortization of acquired intangible assets | 1,783 | 1,035 | — | — | — | |||||||||||||||

| Income from operations | 75,724 | 72,403 | 59,389 | 50,878 | 35,818 | |||||||||||||||

| Interest income | 226 | 1,203 | 2,661 | 3,306 | 2,108 | |||||||||||||||

| Other income (expense) | 268 | (279 | ) | 953 | — | — | ||||||||||||||

| Income before provision for income taxes | 76,218 | 73,327 | 63,003 | 54,184 | 37,926 | |||||||||||||||

| Provision for income taxes | 27,839 | 27,208 | 22,925 | 20,952 | 14,604 | |||||||||||||||

| Net income | $ | 48,379 | $ | 46,119 | $ | 40,078 | $ | 33,232 | $ | 23,322 | ||||||||||

| Basic net income per share | $ | 1.69 | $ | 1.65 | $ | 1.47 | $ | 1.24 | $ | 0.88 | ||||||||||

| Diluted net income per share | $ | 1.68 | $ | 1.62 | $ | 1.44 | $ | 1.21 | $ | 0.85 | ||||||||||

| Basic weighted average shares outstanding | 28,635 | 28,031 | 27,298 | 26,882 | 26,413 | |||||||||||||||

| Diluted weighted average shares outstanding | 28,796 | 28,396 | 27,770 | 27,550 | 27,356 | |||||||||||||||

| Dividends declared per common share | $ | 1.20 | $ | 1.15 | $ | 1.00 | $ | 1.00 | $ | 0.875 | ||||||||||

| March 31, | March 31, | March 31, | March 31, | March 31, | ||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

| Balance Sheet Data: | ||||||||||||||||||||

| Cash and cash equivalents | $ | 84,611 | $ | 70,180 | $ | 59,046 | $ | 60,028 | $ | 57,255 | ||||||||||

| Working capital | $ | 118,935 | $ | 98,980 | $ | 79,932 | $ | 76,616 | $ | 61,724 | ||||||||||

| Total assets | $ | 310,180 | $ | 242,101 | $ | 187,908 | $ | 150,681 | $ | 122,247 | ||||||||||

| Total liabilities | $ | 121,891 | $ | 86,534 | $ | 74,203 | $ | 59,435 | $ | 49,838 | ||||||||||

| Total shareholders’ equity | $ | 188,289 | $ | 155,567 | $ | 113,705 | $ | 91,246 | $ | 72,409 | ||||||||||

28

(In Thousands, Except Per Share Data)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Year ended March 31, |

| |||||||||||||

| ||||||||||||||||

|

| 2008 |

| 2007 |

| 2006 |

| 2005 |

| 2004 |

| |||||

|

|

| ||||||||||||||

| ||||||||||||||||

Statements of Income Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenue |

| $ | 186,500 |

| $ | 157,165 |

| $ | 119,287 |

| $ | 88,961 |

| $ | 70,934 |

|

Cost of revenue |

|

| 62,501 |

|

| 50,784 |

|

| 39,828 |

|

| 32,669 |

|

| 28,673 |

|

|

|

| ||||||||||||||

Gross profit |

|

| 123,999 |

|

| 106,381 |

|

| 79,459 |

|

| 56,292 |

|

| 42,261 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Selling, general and administrative expenses |

|

| 53,260 |

|

| 45,337 |

|

| 35,554 |

|

| 24,776 |

|

| 19,482 |

|

Research and development costs |

|

| 11,350 |

|

| 10,166 |

|

| 8,087 |

|

| 6,903 |

|

| 6,139 |

|

|

|

| ||||||||||||||

Income from operations |

|

| 59,389 |

|

| 50,878 |

|

| 35,818 |

|

| 24,613 |

|

| 16,640 |

|

Interest income |

|

| 2,661 |

|

| 3,306 |

|

| 2,108 |

|

| 876 |

|

| 386 |

|

Other income |

|

| 953 |

|

| — |

|

| — |

|

| — |

|

| — |

|

|

|

| ||||||||||||||

| ||||||||||||||||

Income before provision for income taxes |

|

| 63,003 |

|

| 54,184 |

|

| 37,926 |

|

| 25,489 |

|

| 17,026 |

|

Provision for income taxes |

|

| 22,925 |

|

| 20,952 |

|

| 14,604 |

|

| 9,380 |

|

| 6,626 |

|

|

|

| ||||||||||||||

Net income |

| $ | 40,078 |

| $ | 33,232 |

| $ | 23,322 |

| $ | 16,109 |

| $ | 10,400 |

|

|

|

| ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic net income per share |

| $ | 1.47 |

| $ | 1.24 |

| $ | 0.88 |

| $ | 0.63 |

| $ | 0.42 |

|

Diluted net income per share |

| $ | 1.44 |

| $ | 1.21 |

| $ | 0.85 |

| $ | 0.61 |

| $ | 0.40 |

|

Basic weighted average shares outstanding |

|

| 27,298 |

|

| 26,882 |

|

| 26,413 |

|

| 25,744 |

|

| 24,872 |

|

Diluted weighted average shares outstanding |

|

| 27,770 |

|

| 27,550 |

|

| 27,356 |

|

| 26,406 |

|

| 25,932 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance Sheet Data (at end of period): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

| $ | 59,046 |

| $ | 60,028 |

| $ | 57,255 |

| $ | 51,157 |

| $ | 51,395 |

|

Working capital |

| $ | 79,932 |

| $ | 76,616 |

| $ | 61,724 |

| $ | 55,111 |

| $ | 53,415 |

|

Total assets |

| $ | 187,908 |

| $ | 150,681 |

| $ | 122,247 |

| $ | 99,442 |

| $ | 86,678 |

|

Total liabilities |

| $ | 74,203 |

| $ | 59,435 |

| $ | 49,838 |

| $ | 36,711 |

| $ | 25,673 |

|

Total shareholders’ equity |

| $ | 113,705 |

| $ | 91,246 |

| $ | 72,409 |

| $ | 62,731 |

| $ | 61,005 |

|

ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

The

| • | Management Overview. This section provides a general description of our Company and operating segments, a discussion as to how we derive our revenue, background information on certain trends and developments affecting our Company, a summary of our acquisition transactions and a discussion on management’s strategy for driving revenue growth. | |

| • | Critical Accounting Policies and Estimates. This section discusses those accounting policies that are considered important to the evaluation and reporting of our financial condition and results of operations, and whose application requires us to exercise subjective or complex judgments in making estimates and assumptions. In addition, all of our significant accounting policies, including our critical accounting policies, are summarized in Note 2 to the Consolidated Financial Statements included in this Report. | |

| • | Overview of Results of Operations and Results of Operations by Operating Divisions. These sections provide our analysis and outlook for the significant line items on our Consolidated Statements of Income, as well as other information that we deem meaningful to understand our results of operations on both a consolidated basis and an operating division basis. | |

| • | Liquidity and Capital Resources. This section provides an analysis of our liquidity and cash flows and discussions of our contractual obligations and commitments as of March 31, 2010. | |

| • | New Accounting Pronouncements. This section provides a summary of the most recent authoritative accounting standards and guidance that have either been recently adopted by our Company or may be adopted in the future. |

29

30

We believe revenue recognition, valuation of marketable securities, the allowance for doubtful accounts, capitalized software costs, share-based compensation and income taxes are among the most critical accounting policies that affect our consolidated financial statements.

Revenue Recognition. We currently recognize revenue pursuant to SOP 97-2, as amended by SOP 98-9. We generate revenue from the sale of licensing rights to use our software products sold directly to end-users and value-added resellers (VARs). We also generate revenue from sales of hardware and third party software, and implementation, training, software customization, EDI, post-contract support (“maintenance”) and other services performed for customers who license our products.

A typical system contract contains multiple elements of the above items. SOP 97-2, as amended, requires revenue earned on software arrangements involving multiple elements to be allocated to each element based on the relative fair values of those elements. The fair value of an element must be based on vendor specific objective evidence (VSOE). We limit our assessment of VSOE for each element to either the price charged when the same element is sold separately (using a rolling average of stand alone transactions) or the price established by management having the relevant authority to do so, for an element not yet sold separately. VSOE calculations are updated and reviewed at the end of each quarter or annually depending on the nature of the product or service.

When evidence of fair value exists for the delivered and undelivered elements of a transaction, then discounts for individual elements are aggregated and the total discount is allocated to the individual elements in proportion to the elements’ fair value relative to the total contract fair value.

When evidence of fair value exists for the undelivered elements only, the residual method, provided for under SOP 98-9, is used. Under the residual method, we defer revenue related to the undelivered elements in a system sale based on VSOE of fair value of each of the undelivered elements, and allocate the remainder of the contract price net of all discounts to revenue

recognized from the delivered elements. Undelivered elements of a system sale may include implementation and training services, hardware and third party software, maintenance, future purchase discounts, or other services. If VSOE of fair value of any undelivered element does not exist, all revenue is deferred until VSOE of fair value of the undelivered element is established or the element has been delivered.

We bill for the entire contract amount upon contract execution except for maintenance which is billed separately. Amounts billed in excess of the amounts contractually due are recorded in accounts receivable as advance billings. Amounts are contractually due when services are performed or in accordance with contractually specified payment dates. Provided the fees are fixed and determinable and collection is considered probable, revenue from licensing rights and sales of hardware and third party software is generally recognized upon shipment and transfer of title. In certain transactions whose collections risk is high, the cash basis method is used to recognize revenue. If the fee is not fixed or determinable, then the revenue recognized in each period (subject to application of other revenue recognition criteria) will be the lesser of the aggregate of amounts due and payable or the amount of the arrangement fee that would have been recognized if the fees were being recognized using the residual method. Fees which are considered fixed or determinable at the inception of our arrangements must includebelieve the following characteristics:

| ||

| Revenue Recognition | Judgments and Uncertainties | |

| We generate revenue from the sale of licensing rights to use our software products sold directly to end-users and value-added resellers, or VARs. We also generate revenue from sales of hardware and third party software, implementation, training, software customization, EDI, post-contract support (maintenance) and other services, including RCM services, performed for customers who license our products. Revenue from implementation and training services is recognized as the corresponding services are performed. Maintenance revenue is recognized ratably over the contractual maintenance period. RCM revenue is derived from services fees, which include amounts charged for ongoing billing and other related services and are generally billed to the customer as a percentage of total collections. We do not recognize revenue for services fees until these collections are made as the services fees are not fixed or determinable until such time. | A typical system contract contains multiple elements of the above items. FASB ASC Topic 985-605-25,Software, Revenue Recognition, Multiple Elements,or ASC 985-605-25, requires revenue earned on software arrangements involving multiple elements to be allocated to each element based on the relative fair values of those elements. The fair value of an element must be based on vendor specific objective evidence (“VSOE”). We limit our assessment of VSOE for each element to either the price charged when the same element is sold separately or the price established by management having the relevant authority to do so, for an element not yet sold separately. VSOE calculations are updated and reviewed at the end of each quarter or annually depending on the nature of the product or service. We have established VSOE for the related undelivered elements based on the bell-shaped curve method. Maintenance VSOE for our largest customers is based on stated renewal rates only if the rate is determine d to be substantive and falls within our customary pricing practices. When evidence of fair value exists for the undelivered elements only, the residual method, provided for under ASC 985-605, is used. Under the residual method, we defer revenue related to the undelivered elements in a system sale based on VSOE of fair value of each of the undelivered elements, and allocate the remainder of the contract price net of all discounts to revenue recognized from the delivered elements. Undelivered elements of a system sale may include implementation and training services, hardware and third party software, maintenance, future purchase discounts, or other services. If VSOE of fair value of any undelivered element does not exist, all revenue is deferred until VSOE of fair value of the undelivered element is established or the element has been delivered. We bill for the entire system sales contract amount upon contract execution, except for maintenance which is billed separately. Amounts billed in excess of the amounts contractually due are recorded in accounts receivable as advance billings. Amounts are contractually due when services are performed or in accordance with contractually specified payment dates. Provided the fees are fixed or determinable and collection is considered probable, revenue from licensing rights and sales of hardware and third party software is generally recognized upon shipment and transfer of title. In certain transactions whose collections risk is high, the cash basis method is used to recognize revenue. If the fee is not fixed or determinable, then the revenue recognized in each period (subject to application of other revenue recognition criteria) will be the lesser of the aggregate of amounts due and payable or the amount of the arrangement fee that would have been recognized if the fees were being recognized using the residual method. Fees which are considered fixed or determinable at the inception of our arrangements must include the following characteristics: | |

| • The fee must be negotiated at the outset of an arrangement, and generally be based on the specific volume of products to be delivered without being subject to change based on variable pricing mechanisms such as the number of units copied or distributed or the expected number of | ||

| • Payment terms must not be considered extended. If a significant portion of the fee is due more than 12 months after delivery or after the expiration of the license, the fee is presumed not fixed |

Revenue from implementation and training services is recognized as the corresponding services are performed. Maintenance revenue is recognized ratably over the contractual maintenance period.

31

Contract accounting is applied where services include significant software modification, development or customization. In such instances, the arrangement fee is accounted for in accordance with Statement of Position No. 81-1 “Accounting for Performance of Construction-Type and Certain Production-Type Contracts” (SOP 81-1).

Pursuant to SOP 81-1, we use the percentage of completion method provided all of the following conditions exist:

| ||

| Revenue Recognition (continued) | Effect if Actual Results Differ from Assumptions | |

| Although we believe that our approach to estimates and judgments as described herein is reasonable, actual results could differ and we may be exposed to increases or decreases in revenue that could be material. | ||

Valuation of Marketable Securities and ARS Put Option Rights Our investments at March 31, 2010 and 2009 are in tax exempt municipal ARS which are classified as either current or non-current marketable securities on our Consolidated Balance Sheets, depending on the liquidity and timing of expected realization of such securities. Our ARS are held by UBS Financial Services Inc.. On November 13, 2008, we entered into an Auction Rate Security Rights Agreement with UBS, whereby the we accepted UBS’s offer to purchase the Company’s ARS investments at any time during the period of June 30, 2010 through July 2, 2012. As a result, we had obtained an asset, ARS put option rights, whereby the we have a right to “put” the ARS back to UBS. We expect to exercise its ARS put option rights and put its ARS back to UBS on June 30, 2010, the earliest date allowable under the Rights Agreement. | Judgments and Uncertainties Marketable securities are recorded at fair value, based on quoted market rates or on valuation analysis when appropriate. The The fair value of our marketable securities has been estimated by management based on certain assumptions of what market participants would use in pricing the asset in a current transaction, or level 3 — unobservable inputs in accordance with FASB ASC Topic 820-10,Fair Value Measurements and Disclosures-Overall, or ASC 820-10. Management used a model to estimate the fair value of these securities that Effect if Actual Results Differ from Assumptions Although we believe that our approach to estimates and judgments as described herein is reasonable, actual results could differ and we may be exposed to increases or | |

| Allowance for Doubtful Accounts | Judgments and Uncertainties | |

| We maintain allowances for doubtful accounts for estimated losses resulting from the inability of our customers to make required payments. We perform credit evaluations of our customers and maintain reserves for estimated credit losses. Reserves for potential credit losses are determined by establishing both specific and general reserves. | Specific reserves are based on management’s estimate of the probability of collection for certain troubled accounts. General reserves are established based on our historical experience of bad debt expense and the aging of our accounts receivable balances net of deferred revenue and specifically reserved accounts. If the financial condition of our customers were to deteriorate resulting in an impairment of their ability to make payments, additional allowances would be required. Effect if Actual Results Differ from Assumptions Although we believe that our approach to estimates and judgments as described herein is reasonable, actual results could differ and we may be exposed to increases or decreases in required reserves that could be material. |

32

| Software Development Costs | Judgments and Uncertainties | |

| Development costs incurred in the research and development of new software products and enhancements to existing software products are expensed as incurred until technological feasibility has been established. After technological feasibility is established with the completion of a working model of the enhancement or product, any additional development costs are capitalized in accordance with FASB ASC Topic985-20,Software, Costs of Computer Software to be | We perform an annual review of the recoverability of such capitalized software costs. At the time a determination is made that capitalized amounts are not recoverable based on the estimated cash flows to be Effect if Actual Results Differ from Assumptions Although we believe that our approach to estimates and judgments as described herein is reasonable, actual results could differ and we may be exposed to increases or decreases in revenue that could be material. | |

| Goodwill | Judgments and Uncertainties | |

| Goodwill is related to the NextGen Division and the | In accordance with FASB ASC Topic 350-20,Intangibles — Goodwill and Other, Goodwill, or ASC 350-20, we test goodwill for impairment annually at the end of | |

|

| Effect if Actual Results Differ from Assumptions |

| We | |

|

| The carrying values of |

We measure completion using labor input hours. Costs of providing services, including services accounted for in accordance with SOP 81-1, are expensed as incurred.

If a situation occurs in which a contract is so short term that the consolidated financial statements would not vary materially from using the percentage-of-completion method or in which we are unable to make reliable estimates of progress of completion of the contract, the completed contract method is utilized.

Product returns are estimated in accordance with Statement of Financial Accounting Standards No. 48, “Revenue Recognition When Right of Return Exists” (SFAS 48). The Company also ensures that the other criteria in SFAS 48 have been met prior to recognition of revenue:

| goodwill at March 31, 2010 were $46.2 million. We have determined that there was no risk of impairment to our goodwill as of March 31, 2010. | ||

|

| |

|

| |

|

|

33

Business Combinations — Purchase Price Allocations During the last three fiscal years, we completed three significant acquisitions: In February 2010, we acquired Opus for $20.6 million. In October 2008, we acquired PMP for $19.7 million, including transaction costs. In May 2008, we acquired HSI for $15.6 million, including transaction costs. | Judgments and Uncertainties In accordance with business combination accounting under FASB ASC Topic 805,Business Combinations, or ASC 805, we allocate the purchase price of | |

|

| Effect if Actual Results Differ from Assumptions |

|

| |

| We do not | |

| Intangible Assets | Judgments and Uncertainties | |

| Intangible assets consist of capitalized software costs, customer relationships, trade names and certain intellectual property. Intangible assets related to customer relationships and trade names arose in connection with the acquisition of HSI, PMP, Opus, and Sphere. | These intangible assets were recorded at fair value and are stated net of accumulated amortization and impairments. Intangible assets are amortized over their remaining estimated useful lives, ranging from 3 to 9 years. Our amortization policy for | |

| Effect if Actual Results Differ from Assumptions | ||

| Although we believe that our approach to estimates and judgments as described herein is reasonable, actual results could differ and we may be exposed to decreases in the fair value of our intangible assets, resulting in impairment charges that could be material. | ||

| Share-Based Compensation | Judgments and Uncertainties | |

| We have a stock-based compensation plan, which includes stock options and restricted stock units. See Note 2, “Summary of Significant Accounting Policies,” and Note 13, Consolidated Financial Statements of this Report for a complete discussion of our stock-based compensation programs. | We apply the provisions of FASB ASC Topic 718,Compensation — Stock Compensation,or ASC 718, which requires the measurement and recognition of compensation expense for all share-based payment awards made to employees and directors based on estimated fair values. ASC 718 requires us to estimate the fair value of “Share-Based Awards,” to the share-based payment awards on the date of grant using an option-pricing model. We estimate the expected term of the option using historical exercise experience. We estimate volatility by using the |

34

| Share-Based Compensation (continued) | Effect if Actual Results Differ from Assumptions | |

| We do not believe there is a reasonable likelihood there will be a material change in the future estimates or assumptions we use to determine stock-based compensation expense. However, if actual results are not consistent with our estimates or assumptions, we may be exposed to changes in stock-based compensation expense that could be material. | ||

| Self-Insured Liabilities | Judgments and Uncertainties | |