UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 20032006

Commission File Number 1-7850

SOUTHWEST GAS CORPORATION

(Exact name of registrant as specified in its charter)

| California | 88-0085720 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

5241 Spring Mountain Road Post Office Box 98510 Las Vegas, Nevada | 89193-8510 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (702) 876-7237

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Common Stock, $1 par value | New York Stock Exchange, Inc. | |

7.70% Preferred Trust Securities | New York Stock Exchange, Inc. |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.Yes þ No¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.Yes ¨ Noþ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.Yesþ No No¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark whether the registrant is an accelerated filer.a shell company (as defined in Rule 12b-2 of the Exchange Act).Yesþ No¨

Noþ

Aggregate market value of the voting and non-voting common stock held by nonaffiliates of the registrant:

$715,068,7821,275,488,075 as of June 30, 2003

2006

The number of shares outstanding of common stock:

Common Stock, $1 Par Value, 34,517,48141,997,015 shares as of March 1, 2004

February 15, 2007

DOCUMENTS INCORPORATED BY REFERENCE

Description | Part Into Which Incorporated | |

Annual Report to Shareholders for the Year Ended December 31, | Parts I, II, and IV | |

| Part III |

PART I

| PAGE | ||||||||

Item 1. | 1 | |||||||

| 1 | ||||||||

| 1 | ||||||||

| 2 | ||||||||

| 3 | ||||||||

| 3 | ||||||||

| 4 | ||||||||

| 5 | ||||||||

| 5 | ||||||||

| 5 | ||||||||

Item 1A. | 6 | |||||||

Item 1B. | 8 | |||||||

Item 2. | 8 | |||||||

Item 3. | ||||||||

Item 4. | ||||||||

Item 4A. | 9 | |||||||

| PART II | ||||||||

Item 5. | 10 | |||||||

Item 6. | 10 | |||||||

Item 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION | 10 | ||||||

Item 7A. | 10 | |||||||

Item 8. | ||||||||

Item 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING | 11 | ||||||

Item 9A. | ||||||||

Item 9B. | 12 | |||||||

| PART III | ||||||||

Item 10. | DIRECTORS, | |||||||

Item 11. | ||||||||

Item 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND | |||||||

Item 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | |||||||

Item 14. | ||||||||

| PART IV | ||||||||

Item 15. | EXHIBITS, FINANCIAL STATEMENT SCHEDULES | |||||||

BUSINESS Southwest Gas Corporation (the “Company”) was incorporated Southwest is engaged in the business of purchasing, transporting, and distributing natural gas in portions of Arizona, Nevada, and California. Southwest is the largest distributor of natural gas in Arizona, selling and transporting natural gas in most of central and southern Arizona, including the Phoenix and Tucson metropolitan areas. Southwest is also the largest distributor Northern Pipeline Construction Co. (“NPL” or the “construction services” segment), a wholly owned subsidiary, is a full-service underground piping contractor that provides utility companies with trenching and installation, replacement, and maintenance services for energy distribution systems. Financial information concerning the Company’s business segments is included in Note The Company maintains a website (www.swgas.com) for the benefit of shareholders, investors, customers, and other interested parties. The Company makes its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports available, free of charge, through its website as soon as reasonably practicable after such material is electronically filed with, or furnished to, the Securities and Exchange Commission (“SEC”). The Company’s Corporate Governance Guidelines, Code of Business Conduct and Ethics, and charters of the nominating and corporate governance, audit, and compensation committees of the board of directors are also available on the website and are available in print by request. Southwest is subject to regulation by the Arizona Corporation Commission (“ACC”), the Public Utilities Commission of Nevada (“PUCN”), and the California Public Utilities Commission (“CPUC”). These commissions regulate public utility rates, practices, facilities, and service territories in their respective states. The CPUC also regulates the issuance of all securities by the Company, with the exception of short-term borrowings. Certain accounting practices, transmission facilities, and rates are subject to regulation by the Federal Energy Regulatory Commission (“FERC”). NPL is not regulated by the state utilities commissions in any of its operating areas. As of December 31, 2006. The table below lists the percentage of operating margin (operating revenues less net cost of gas) by major customer class for the years indicated: For the Year Ended Residential and Small Commercial Other Sales Customers December 31, 2003 December 31, 2002 December 31, 2001 For the Year Ended December 31, 2006 December 31, 2005 December 31, 2004 Southwest is not dependent on any one or a few customers Item 1. BUSINESSeffectivein March 1931 under the laws of the state of California. The Company is comprisedcomposed of two business segments: natural gas operations (“Southwest” or the “natural gas operations” segment) and construction services. and transporter of natural gas in Nevada, serving the Las Vegas metropolitan area and northern Nevada. In addition, Southwest distributes and transports natural gas in portions of California, including the Lake Tahoe area and the high desert and mountain areas in San Bernardino County.1112 of the Notes to Consolidated Financial Statements, which is included in the 20032006 Annual Report to Shareholders and is incorporated herein by reference.2003,2006, Southwest purchased transported, and distributed or transported natural gas to 1,531,0001,784,000 residential, commercial, and industrial customers in geographically diverse portions of Arizona, Nevada, and California. There were 67,00071,000 customers added to the system during 2003 (and an additional 9,000 in central Arizona associated with the acquisition of Black Mountain Gas Company (“BMG”) in October 2003). Distribution Transportation 84% 6% 10% 83% 7% 10% 82% 8% 10% Distribution Residential and

Small Commercial Other Sales

Customers Transportation 85 % 6 % 9 % 86 % 5 % 9 % 86 % 5 % 9 % to the extentsuch that the loss of any one or several would have a significant adverse impact on earnings.earnings or cash flows.

Transportation of customer-secured gas to end-users accounted for 5448 percent of total system throughput in 2003.2006. Customers who utilized this service transported 118 million dekatherms in 2006, 127 million dekatherms in 2005, and 126 million dekatherms in 2004. Although thethese volumes were significant, these customers provide a much smaller proportionate share of operating margin. Customers who utilized this service transported 134 million dekatherms in 2003, 133 million dekatherms in 2002, and 127 million dekatherms in 2001.

The demand for natural gas is seasonal. Variability in weather from normal temperatures can materially impact results of operations. It is the opinion of management that comparisons of earnings for interim periods do not reliably reflect overall trends and changes in operations. Also, earnings for interim periods can be significantly affected by the timing of general rate relief.

Rates that Southwest is authorized to charge its distribution system customers are determined by the ACC, PUCN, and CPUC in general rate cases and are derived using rate base, cost of service, and cost of capital experienced in aan historical test year, as adjusted in Arizona and Nevada, and projected for a future test year in California. The FERC regulates the northern Nevada transmission and liquefied natural gas (“LNG”) storage facilities of Paiute Pipeline Company (“Paiute”), a wholly owned subsidiary, and the rates it charges for transportation of gas directly to certain end-users and to various local distribution companies (“LDCs”). The LDCs transporting on the Paiute system are: Sierra Pacific Power Company (serving Reno and Sparks, Nevada), Avista Utilities (serving South Lake Tahoe, California), and Southwest Gas Corporation (serving Truckee, South Lake Tahoe and North Lake Tahoe, California and various locations throughout northern Nevada).

Rates charged to customers vary according to customer class and rate jurisdiction and are set at levels that are intended to allow for the recovery of all prudently incurred costs, including a return on rate base sufficient to pay interest on debt preferred securities distributions,and subordinated debentures, and a reasonable return on common equity. Rate base consists generally of the original cost of utility plant in service, plus certain other assets such as working capital and inventories, less accumulated depreciation on utility plant in service, net deferred income tax liabilities, and certain other deductions. Rate schedules in allSouthwest’s service areasterritories, with the exception of Nevada, contain purchased gas adjustment (“PGA”) clauses, which allow Southwest to file for rate adjustments as the cost of purchased gas changes. In Nevada, tariffs provide for annual adjustment dates for changeseffective November 2005, Southwest began operating under the deferred energy regulations as established by the Nevada Administrative Code, which governs the recovery of energy costs in the state. These provisions result in little difference from purchased gas costs. Southwest may make additional requestsadjustment clauses in the method used to adjust rates, if market conditions warrant. In Arizona, Southwest adjusts rates monthlyaccount for changes inor report purchased gas costs, within pre-established limits. In California, a monthlyincluding the ability of the Company to defer over or under-collections of gas costs to balancing accounts. Effective October 2005, the Company began filing for quarterly gas cost adjustments in Nevada, calculated on a twelve-month rolling average. These adjustments are made effective immediately upon filing each quarter, but are subject to an annual prudence review and audit of the natural gas costs incurred. The Company filed its first quarterly adjustment based on forecasted monthly prices is used to adjust rates. PGAin April 2006. Deferred energy and purchased gas adjustment (collectively “PGA”) rate changes affect cash flows but have no direct impact on profit margin. Filings to change rates in accordance with PGA clauses are subject to audit by the appropriate state regulatory commission staff. Information with respect to recent general rate cases and PGA filings is included in the Rates and Regulatory Proceedings section of Management’s Discussion and Analysis (“MD&A”) in the 20032006 Annual Report to Shareholders.

The table below lists the docketed general rate filings last initiated and the status of such filing within each ratemaking area:

Ratemaking Area | Type of Filing | Month Filed | Month Final Rates

| |||

Arizona | General rate case | December 2004 | March 2006 | |||

California: | ||||||

Northern and Southern | General rate case | February 2002 | May 2003 | |||

Northern and Southern | Annual attrition | October 2006 | January 2007 | |||

Nevada: | ||||||

Northern and Southern | General rate case | March 2004 | September 2004 | |||

FERC: | ||||||

Paiute | General rate case | January 2005 | August 2005 |

Deliveries of natural gas by Southwest are made under a priority system established by state regulatory commissions. The priority system is intended to ensure that the gas requirements of higher-priority customers, primarily residential customers and other customers who use 500 therms or less of gas per day, or less, are fully satisfied on a daily basis before lower-priority customers, primarily electric utility and large industrial customers able to use alternative fuels, are provided any quantity of gas or capacity.

Demand for natural gas is greatly affected by temperature. On cold days, use of gas by residential and commercial customers may be as much as six times greater than on warm days because of increased use of gas for space heating. To fully satisfy this increased high-priority demand, gas is withdrawn from storage in certain service areas, or peaking supplies are purchased from suppliers. If necessary, service to interruptible lower-priority customers may be curtailed to provide the needed delivery system capacity. No curtailmentweather-related curtailments occurred during the latest peak heating season. Southwest maintains no significant backlog on its orders for gas service.

Southwest is responsible for acquiring (purchasing) and arranging delivery of (transporting)(transporting via interstate pipelines) natural gas to its system for all sales customers.

The primary objective of Southwest with respect toin acquiring gas supply is to ensure that adequate as well as economical, supplies of natural gas are available from reliable sources.sources at the best cost. Gas is acquired from a wide variety of sources and a mix of purchase provisions, including spot market purchases and firm supplies with a variety of terms. During 2003,2006, Southwest acquired gas supplies from 4856 suppliers. ThisSouthwest regularly monitors the number of suppliers, their quality and their relative contribution to the overall customer supply portfolio. New suppliers are contracted whenever possible, and solicitations for supplies are extended to the largest possible list of suppliers. Competitive pricing, flexibility in meeting Southwest requirements, and aggressive participation by suppliers who have demonstrated reliability of service are key to their inclusion in the annual portfolio mix. The goal of this practice mitigatesis to mitigate the risk of nonperformance by any one supplier.

supplier and ensure competitive prices for customer supplies.

Balancing reliable supply assurances with the associated costs results in a continually changing mix of purchase provisions within the supply portfolios. To address the unique requirements of its various market areas, Southwest assembles and administers a separate natural gas supply portfolio for each of its jurisdictional areas. Firm and spot market natural gas purchases are made in a competitive bid environment. Southwest has experienced price volatility over the past five years, as the weighted average delivered cost of natural gas has ranged from a low of 2838 cents per therm in 19992002 to a high of 5579 cents per therm in 2001. During 2003, Southwest paid an average of 46 cents per therm. 2006. Price volatility is expected to continue throughout 2007.

To mitigate customer exposure to market price volatility, Southwest continues to purchase a significant percentage of its forecasted annual normal weather requirements under firm, fixed-price arrangements that are secured periodically throughout the year.

About half of Southwest’s annual normal weather supply needs are secured using short duration contracts (one year or less). For the 2006/2007 heating season, fixed-price contracts ranged in price from $6 to $11 per dekatherm. Natural gas purchases not covered by fixed-price contracts are made under variable-price contracts with firm quantities and on the spot market. Prices for these contracts are not known until the month of purchase.

The firm, fixed-price arrangements are structured such that a stated volume of gas is required to be scheduled by Southwest and delivered by the supplier. If the gas is not needed by Southwest or cannot be procured by the supplier, the contract provides for fixed or market-based penalties to be paid by the non-performing party. In the event that demand on Southwest’s system is lower than expected, Southwest may have the opportunity to forego the purchase at a negotiated price in excess of the contracted price during periods of extreme price volatility. Any savings would reduce the overall cost of gas for the purchase period.

In managing its gas supply portfolios, Southwest uses the fixed-price and variable-price arrangements noted above, but does not currently utilize other stand-alone derivative financial instruments for speculative purposes or for hedging. During 2007, Southwest intends to supplement its current volatility mitigation program with stand-alone financial derivative instruments. InThe combination of fixed-price contracts and derivative instruments should increase flexibility for Southwest and increase supplier diversification. The costs of such derivative financial instruments are expected to be recovered from customers. None of the future stand-aloneCompany’s current long-term financial instruments or other contracts are derivatives may be usedthat are marked to hedge against possible price increases. However, any such change would be undertakenmarket or contain embedded derivatives with the knowledge of Southwest’s various regulatory commissions.

significant mark-to-market value.

Storage capabilityavailability can influence the average annual price of gas, as storage allows a company to purchase natural gas in larger quantities during the off-peak season and store it for use in high demand periods when prices may be greater.greater or supplies/capacity tighter. Southwest currently has no storage availability in its Arizona or southern Nevada rate jurisdictions. Limited storage capabilities existavailability exists in southern and northern California and northern Nevada. A contract with

Southern California Gas Company is intended for delivery only within Southwest’s southern California rate jurisdiction. In addition, a contract with Paiute for its LNG facility allows for peaking capability only in northern Nevada and northern California allows for peaking capability only.California. Gas is purchased for injection during the off-peak period for use in the high demand months, but is again limited in its impact on the overall price. The LNG plant is currently leased from a third party, and the contract expires in July 2005. While

negotiations continue between the owner of the plant and Paiute to allow for the purchase of the facility, preparations are being made to provide alternatives to the leased facility to be in service by July 2005.

Gas supplies for the southern system of Southwest (Arizona, southern Nevada, and southern California properties) are primarily obtained from producing regions in Colorado and New Mexico (San Juan basin), Texas (Permian basin), and Rocky Mountain areas. For its northern system (northern Nevada and northern California properties), Southwest primarily obtains gas from Rocky Mountain producing areas and from Canada.

Southwest arranges for transportation of gas to its Arizona, Nevada, and California service territories through the pipeline systems of El Paso Natural Gas Company (“El Paso”), Kern River Gas Transmission Company (“Kern River”), Transwestern Pipeline Company (“Transwestern”), Northwest Pipeline Corporation, Tuscarora Gas Pipeline Company (“Tuscarora”), Southern California Gas Company, and Paiute. Supply and pipeline capacity availability on both short- and long-term bases is continuallyregularly monitored by Southwest to ensure the reliability of service to its customers. Southwest currently receives firm transportation service, both on a short- and long-term basis, for all of its service territories on the pipeline systems noted above and also has interruptible contracts in place that allow additional capacity to be acquired should an unforeseen need arise.

Southwest is dependent upon the El Paso pipeline system for the transportation of gas to virtually all of its Arizona service territories and, for part of 2006, to a portion of its southern Nevada service territory. During 2005, Southwest entered into negotiations with alternative transportation service providers to evaluate capacity options for its southern Nevada service territory. After evaluating several proposals, Transwestern was chosen to replace the capacity previously provided by El Paso for southern Nevada, effective September 2006. The new five-year contract with Transwestern extends capacity during winter months and provides greater flexibility in meeting monthly requirements. Rates under the new contract do not differ significantly from those previously paid. El Paso service is available in Southern Nevada on an interruptible basis.

The Company believes that the current level of contracted firm interstate capacity is sufficient to serve each of its service territories. As the need arises to acquire additional capacity on one of the interstate pipeline transmission systems, primarily due to customer growth, Southwest will continue to consider available options to obtain that capacity, either through the use of firm contracts with a pipeline company or by purchasing capacity on the open market.

Southwest is dependent upon the El Paso pipeline system for the transportation of gas to virtually all of its Arizona service territories. Historically, Southwest received transportation service from El Paso to its Arizona service territories under a full requirements contract. Under full requirements service, El Paso was obligated to transport all of a customer’s gas requirements each day, and the customer was obligated to have El Paso, and only El Paso, transport its requirements. Virtually all of El Paso’s customers in Arizona, New Mexico, and Texas have been full requirements customers, while El Paso has transported gas for its customers in California and Nevada subject to a specific maximum daily quantity, or contract demand limitation.

Since November 1999, the Federal Energy Regulatory Commission has been examining capacity allocation issues on the El Paso system in several proceedings. This examination resulted in a series of orders by the FERC in which all of the major full requirements transportation service agreements on the El Paso system, including the agreement by which Southwest obtained the transportation of gas supplies to its Arizona service areas, were converted to contract demand-type service agreements, with fixed maximum service limits, effective September 2003. At that time, all of the transportation capacity on the system was allocated among the shippers. In order to help ensure that the converting full requirements shippers would have adequate capacity to meet their needs, El Paso was authorized to expand the capacity on its system by adding compression.

The FERC is continuing to examine issues related to the implementation of the full requirements conversion. Petitions for judicial review of the FERC’s orders mandating the conversion have been filed.

Management believes that it is difficult to predict the ultimate outcome of the proceedings or the impact of the FERC action on Southwest. Southwest has had adequate capacity for its customers’ needs during the 2003/2004 heating season to date and management believes adequate capacity exists for the remainder of the heating season. Additional costs may be incurred to acquire capacity in the future as a result of the FERC order. However, it is anticipated that any additional costs would be collected from customers principally through the PGA mechanism.

Electric utilities are the principal competitors of Southwest for the residential and small commercial markets throughout its service areas. Competition for space heating, general household, and small commercial energy needs generally occurs at the initial installation phase when the customer/builder typically makes the decision as to which type of equipment to install and operate. The customer will generally continue to use the chosen energy source for the life of the equipment. As a result of its success in these markets, Southwest has experienced consistent growth among the residential and small commercial customer classes.

Unlike residential and small commercial customers, certain large commercial, industrial, and electric generation customers have the capability to switch to alternative energy sources. To date, Southwest has been successful in retaining most of these customers by setting rates at levels competitive with alternative energy sources such as electricity, fuel oils, and coal. However, increases inhigh natural gas prices if sustained for an extended period of time, may impact Southwest’s ability to retain some of these customers. Overall, management does not anticipate any material adverse impact on operating margin from fuel switching.

Southwest continues to competecompetes with interstate transmission pipeline companies, such as El Paso, Kern River, Transwestern and Tuscarora, Gas Transmission Company, to provide service to certain large end-users. End-use customers located in close proximity to these interstate pipelines pose a potential bypass threat. Southwest attempts to closely monitor each customer situation and provide competitive service in order to retain the customer. Southwest has remained competitive through the use of negotiated transportation contract rates, special long-term contracts with electric generation and cogeneration customers, and other tariff programs. These competitive response initiatives have mitigated the loss of margin earned from large customers.

Federal, state, and local laws and regulations governing the discharge of materials into the environment have had little direct impact upon Southwest. Environmental efforts, with respect to matters such as protection of endangered species and archeological finds, have increased the complexity and time required to obtain pipeline rights-of-way and construction permits. However, increased environmental legislation and regulation are also beneficial to the natural gas industry. Because natural gas is one of the most environmentally safe fossil fuels currently available, its use can help energy users to comply with stricter environmental standards.

At December 31, 2003,2006, the natural gas operations segment had 2,5502,525 regular full-time equivalent employees, of which 507 full-time equivalent non-exempt employees in central Arizona were represented by the International Brotherhood of Electrical Workers. No other natural gas operations segment employees are represented by a union.employees. Southwest believes it has a good relationship with its employees and that compensation, benefits, and working conditions afforded its employees are comparable to those generally found in the utility industry.

No employees are represented by a union.

Northern Pipeline Construction Co.NPL is a full-service underground piping contractor that provides utility companies with trenching and installation, replacement, and maintenance services for energy distribution systems. NPL contracts primarily with LDCs to install, repair, and maintain energy distribution systems from the town border station to the end-user. The primary focus of business operations is main and service replacement as well as new business installations. Construction work varies from relatively small projects to the piping of entire communities. Construction activity is seasonal in most areas. Peak construction periods are the summer and fall months in colder climate areas, such as the midwest.Midwest. In the warmer climate areas, such as the southwestern United States, construction continues year round.

Construction activity is also cyclical and can be significantly impacted by changes in general and local economic conditions, including interest rates, employment levels, job growth, equipment resale market, and local and federal tax rates.

NPL business activities are often concentrated in utility service territories where existing energy lines are scheduled for replacement. An LDC will typically contract with NPL to provide pipe replacement services and new line installations. Contract terms generally specify unit-price or fixed-price arrangements. Unit-price contracts establish prices for all of the various services to be performed during the contract period. These contracts often have annual pricing reviews. During 2003,2006, approximately 9491 percent of revenue was earned under unit-price contracts. As of December 31, 20032006, no significant backlog existed with respect to outstanding construction contracts.

Materials used by NPL in its pipeline construction activities are typically specified, purchased, and supplied by NPL’s customers. Construction contracts also contain provisions which make customers generally liable for remediating environmental hazards encountered during the construction process. Such hazards might include digging in an area that was contaminated prior to construction, finding endangered animals, digging in historically significant sites, etc.

Otherwise, NPL’s operations have minimal environmental impact (dust control, normal waste disposal, handling harmful materials, etc.).

Competition within the industry has traditionally been limited to several regional competitors in what has been a largely fragmented industry. Several national competitors also exist within the industry. NPL currently operates in approximately 1716 major markets nationwide. Its customers are the primary LDCs in those markets. During 2003,2006, NPL served 4159 major customers, with Southwest accounting for approximately 3027 percent of theirNPL revenues. With the exception of onethree other customercustomers that in total accounted for approximately 1231 percent of revenue, no other customer had a relatively significant contribution to NPL revenues.

Employment fluctuates between seasonal construction periods, which are normally heaviest in the summer and fall months. At December 31, 2003,2006, NPL had 1,8222,377 regular full-time equivalent employees. Employment peaked in May 2003September 2006 when there were 2,0402,526 employees. The majority of theMost employees are represented by unions and are covered by collective bargaining agreements, which is typical of the utility construction industry.

Operations are conducted from 17 field locations with corporate headquarters located in Phoenix, Arizona. All buildingsBuildings are normally leased from third parties. The lease terms are typically five years or less. Field location facilities consist of a small building for repairs and land to store equipment.

NPL is not directly affected by regulations promulgated by the ACC, PUCN, CPUC, or FERC in its construction services. NPL is an unregulated construction subsidiary of Southwest Gas Corporation. However, because NPL performs work for the regulated natural gas segment of the Company, its construction costs are subject indirectly to “prudency reviews” just as any other capital work that is performed by third parties or directly by Southwest. However, such “prudency reviews” would not bring NPL under the regulatory jurisdiction of any of the commissions noted above.

RISK FACTORS |

Although the Company is not able to predict all factors that may affect future results, described below (and inItem 7A. Quantitative and Qualitative Disclosures about Market Riskof this report) are some of the risk factors identified by the Company that may have a negative impact on our future financial performance or affect whether we achieve the goals or expectations expressed or implied in any forward-looking statements contained herein. Unless indicated otherwise, references below to “we,” “us” and “our” should be read to refer to Southwest Gas Corporation and its subsidiaries.

Our liquidity, and in certain circumstances our earnings, may be reduced during periods in which natural gas prices are rising significantly or are more volatile.

Increases in the cost of natural gas may arise from a variety of factors, including weather, changes in demand, the level of production and availability of natural gas, transportation constraints, transportation capacity cost increases, federal and state energy and environmental regulation and legislation, the degree of market liquidity, natural disasters, wars and other catastrophic events, national and worldwide economic and political conditions, the price and availability of alternative fuels, and the success of our strategies in managing price risk.

Rate schedules in each of our service territories contain purchased gas adjustmentPGA clauses which permit us to file for rate adjustments to recover increases in the cost of purchased gas. Increases in the cost of purchased gas have no direct impact on our profit margins, but do affect cash flows and can therefore impact the amount of our capital resources. We have used short-term borrowings in the past to temporarily finance increases in purchased gas costs, and we expect to do so during 2004,2007, if the need again arises.

We may file requests for rate increases to cover the rise in the costs of purchased gas. Due to the nature of the regulatory process, there is a risk of a disallowance of full recovery of these costs during any period in which there has been a substantial run-up of these costs or our costs are more volatile. Any disallowance of purchased gas costs maywould reduce cash flow and earnings.

Increases in the cost of natural gas may arise from a variety of factors, including weather, changes in demand, the level of production and availability of natural gas, transportation constraints, transportation capacity cost increases, federal and state energy and environmental regulation and legislation, the degree of market liquidity, natural disasters, wars and other catastrophic events, and the success of our strategies in managing price risk.

Governmental policies and regulatory actions can reduce our earnings.

Regulatory commissions set our rates and determine what we can charge for our rate-regulated services. Our ability to obtain timely future rate increases depends on regulatory discretion. Governmental policies and regulatory actions, including those of the ACC, the CPUC, the FERC, and the PUCN relating to allowed rates of return, rate structure, purchased gas and investment recovery, operation and construction of

facilities, present or prospective wholesale and retail competition, changes in tax laws and policies, and changes in and compliance with environmental and safety laws and policies, can reduce our earnings. Risks and uncertainties relating to delays in obtaining regulatory approvals, conditions imposed in regulatory approvals, or determinations in regulatory investigations can also impact financial performance.

In particular, the timing and amount of rate relief can materially impact results of operation.

We are unable to predict what types of conditions might be imposed on Southwest or what types of determinations might be made in pending or future regulatory proceedings or investigations. We nevertheless believe that it is not uncommon for conditions to be imposed in regulatory proceedings, for Southwest to agree to conditions as part of a settlement of a regulatory proceeding, or for determinations to be made in regulatory investigations that will reduce our earnings and liquidity. For example, we may request recovery of a particular operating expense in a general rate case filing that a regulator disallows.disallows, negatively impacting our earnings.

Significant customer growth in Arizona and Nevada could strain our capital resources.

We continue to experience significant population and customer growth throughout our service territories. During 2003,2006, we added 67,00071,000 customers, a fivefour percent growth rate. Another 9,000 customers were added in October 2003 with the BMG acquisition. Over the past ten years, customer growth has averaged five percent per year. This growth has required large amounts of capital to finance the investment in new transmission and distribution plant. In 2003,2006, our natural gas construction expenditures totaled $228$306 million. Approximately 7276 percent of these current-period expenditures represented new construction, and the balance represented costs associated with routine replacement of existing transmission, distribution, and general plant.

Cash flows from operating activities (net of dividends) have been inadequate,insufficient, and are expected to continue to be inadequate,insufficient, to fund all necessary capital expenditures. We have funded this shortfall through the issuance of additional debt and equity securities, and expect to continue to do so. However, our ability to issue additional securities is dependent upon, among other things, conditions in the capital markets, regulatory authorizations, our credit rating, and our level of earnings.

Significant customer growth in Arizona and Nevada could also impact earnings.

Our ability to earn the rates of return authorized by the ACC and the PUCN is also more difficult because of significant customer growth. The rates we charge our distribution customers in Arizona and Nevada are derived using rate base, cost of service, and cost of capital experienced in a historical test year, as adjusted. This results in “regulatory lag” which delays our recovery of some of the costs of capital improvements and operating costs from customers in Arizona and Nevada.

Our earnings are greatly affected by variations in temperature during the winter heating season.

The demand for natural gas is seasonal and is greatly affected by temperature. Variability in weather from normal temperatures can materially impact results of operations.operations, particularly in our Arizona service territories where rates are highly leveraged. On cold days, use of gas by residential and commercial customers may be as much as six times greater than on warm days because of the increased use of gas for space heating. Weather has been and will continue to be one of the dominant factors in our financial performance.

Uncertain economic conditions may affect our ability to finance capital expenditures.

Our ability to finance capital expenditures and other matters will depend upon general economic conditions in the capital markets. The direction of interest rates is uncertain. Declining interest rates are generally believed to be favorable to utilities while rising interest rates are believed to be unfavorable because of the high capital costs of utilities. In addition, our authorized rate of return is based upon certain assumptions regarding interest rates. If interest rates are lower than assumed rates, our authorized rate of return in the future could be reduced. If interest rates are higher than assumed rates, it will be more difficult for us to earn our currently authorized rate of return.

The nature of our operations presents inherent risks of loss that could adversely affect our results of operations.

Our operations are subject to inherent hazards and risks such as gas leaks, fires, natural disasters, explosions, pipeline ruptures, and other hazards and risks that may cause unforeseen interruptions, personal injury, or property damage. Additionally, our facilities, machinery, and equipment, including our pipelines, are subject to third party damage from construction activities and vandalism. Any of these events could cause environmental pollution, personal injury or death claims, damage to our properties or the properties of others, or loss of revenue by us or others.

We maintain liability insurance for some, but not all, risks associated with the operation of our natural gas pipelines and facilities. In connection with these liability insurance policies, we have been responsible for an initial deductible or self-insured retention amount per incident, after which the insurance carriers would be responsible for amounts up to the policy limits. The Company’s current insurance contracts limit the self-insured retention to $1 million per incident plus payment of the first $5 million in aggregate claims above $1 million. We cannot predict the likelihood that any future event will occur which will result in a claim exceeding $1 million; however, a large claim for which we were deemed liable would reduce our earnings.

We rely on having access to interstate pipelines’ transportation capacity. If these pipelines were not available, it could impact our ability to meet our customers’ full requirements.

We must acquire both sufficient natural gas supplies and interstate pipeline capacity to meet customer requirements. We must contract for reliable and adequate delivery capacity for our distribution system, while considering the dynamics of the interstate pipeline capacity market, our own in-system resources, as well as the characteristics of our customer base. Interruptions to or reductions of interstate pipeline service caused by physical constraints, excessive customer usage or other force majeure could reduce our normal supply of gas, particularly in our Arizona service territories where we are wholly dependent upon the El Paso pipeline system. A prolonged interruption or reduction of service, particularly during the winter heating season, would reduce cash flow and earnings.

A significant reduction in our credit ratings could materially and adversely affect our business, financial condition, and results of operations.

We cannot be certain that any of our current ratings will remain in effect for any given period of time or that a rating will not be lowered or withdrawn entirely by a rating agency if, in its judgment, circumstances in the future so

warrant. For example, in May 2006, Moody’s Investors Service, Inc. (“Moody’s”) lowered its rating on the Company’s unsecured long-term debt to Baa3 from Baa2 and changed the outlook for the rating to stable from negative. The change in credit rating will result in an estimated annualized increase of $375,000 in interest expense on existing long-term debt. No debt covenants were affected by the downgrade.warrant. Any future downgrade could further increase our borrowing costs, which would diminish our financial results. We would likely be required to pay a higher interest rate in future financings, and our potential pool of investors and funding sources could decrease. A downgrade could require additional support in the form of letters of credit or cash or other collateral and otherwise adversely affect our business, financial condition and results of operations.

UNRESOLVED STAFF COMMENTS |

None.

PROPERTIES |

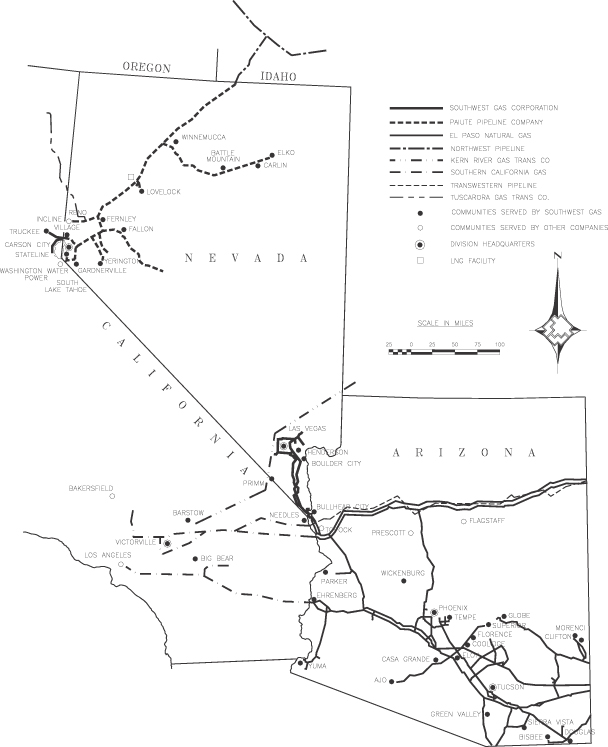

The plant investment of Southwest consists primarily of transmission and distribution mains, compressor stations, peak shaving/storage plants, service lines, meters, and regulators, which comprise the pipeline systems and facilities located in and around the communities served. Southwest also includes other properties such as land, buildings, furnishings, work equipment, vehicles, and software systems in plant investment. The northern Nevada and northern California properties of Southwest are referred to as the northern system; the Arizona, southern Nevada, and southern California properties are referred to as the southern system. Several properties are leased by Southwest, including an LNG storage plant in northern Nevada, a portion of the corporate headquarters office complex located in Las Vegas, Nevada and the administrative offices in Phoenix, Arizona. Total gas plant, exclusive of leased property, at December 31, 20032006 was $3.1$3.8 billion, including construction work in progress. It is the opinion of management that the properties of Southwest are suitable and adequate for its purposes.

Substantially all gas main and service lines are constructed across property owned by others under right-of-way grants obtained from the record owners thereof, on the streets and grounds of municipalities under authority conferred by franchises or otherwise, or on public highways or public lands under authority of various federal and state statutes. None of the numerous county and municipal franchises are exclusive, and some are of limited duration. These franchises are renewed regularly as they expire, and Southwest anticipates no serious difficulties in obtaining future renewals.

With respect to the right-of-way grants, Southwest has had continuous and uninterrupted possession and use of all such rights-of-way, and the associated gas mains and service lines, commencing with the initial stages of the construction of such facilities. Permits have been obtained from public authorities and other governmental entities in certain instances to cross or to lay facilities along roads and highways. These permits typically are revocable at the election of the grantor and Southwest occasionally must relocate its facilities when requested to do so by the grantor. Permits have also been obtained from railroad companies to cross over or under railroad lands or rights-of-way, which in some instances require annual or other periodic payments and are revocable at the election of the grantors.

Southwest operates two primary pipeline transmission systems: (i)

a system (including an LNG storage facility) owned by Paiute a wholly owned subsidiary, extending from the Idaho-Nevada border to the Reno, Sparks, and Carson City areas and communities in the Lake Tahoe area in both California and Nevada and other communities in northern and western Nevada; and (ii)

a system extending from the Colorado River at the southern tip of Nevada to the Las Vegas distribution area.

The following map showsSouthwest provides natural gas service in parts of Arizona, Nevada, and California. Service areas in Arizona include most of the locationscentral and southern areas of major Southwest facilitiesthe state including Phoenix, Tucson, Yuma, and transmission lines,surrounding communities. Service areas in northern Nevada include Carson City, Yerington, Fallon, Lovelock, Winnemucca, and principal communities to which Southwest supplies gas either as a wholesaler or distributor. The map also shows major supplier transmission lines that are interconnected withElko. Service areas in southern Nevada include the Southwest systems.

Las Vegas valley (including Henderson and Boulder City) and Laughlin. Service areas in southern California include Barstow, Big Bear, Needles, and Victorville. Service areas in northern California include the Lake Tahoe area and Truckee.

Information on properties of NPL can be found on page 65 of this Form 10-K under Construction Services.

LEGAL PROCEEDINGS |

The Company maintains liability insurance for various risks associated with the operation of its natural gas pipelines and facilities. In May 2005, a leaking natural gas line was involved in a fire that severely injured an individual. By December 2005, the Company had recorded a total liability related to this incident equal to the Company’s maximum self-insured retention level for the policy year August 2004 to July 2005 of $11 million. In the fourth quarter of 2006, the case was settled. The amount of the settlement that exceeded $11 million was covered by insurance. The Company’s current insurance contracts limit the self-insured retention to $1 million per incident plus payment of the first $5 million in aggregate claims above $1 million.

The Company is named as a defendant in various legal proceedings. The ultimate dispositions of these proceedings are not presently determinable; however, it is the opinion of management that none of this litigation individually or in the aggregate will have a material adverse impact on the Company’s financial position or results of operations.

SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

None.

DIRECTORS AND EXECUTIVE OFFICERS OF THE REGISTRANT |

The listing of the executive officers of the Company is set forth underPart III Item 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE, which by this reference is incorporated herein.

PART II

Item 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

The principal markets on which the common stock of the Company is traded are the New York Stock Exchange and the Pacific Exchange. At March 1, 2004, there were 23,259 holders of record of common stock, and the market price of the common stock was $23.45. The quarterly market price of, and dividends on, Company common stock required by this item are included in the 2003 Annual Report to Shareholders filed as an exhibit hereto and incorporated herein by reference.

The Company has a common stock dividend policy which states that common stock dividends will be paid at a prudent level that is within the normal dividend payout range for its respective businesses, and that the dividend will be established at a level considered sustainable in order to minimize business risk and maintain a strong capital structure throughout all economic cycles. The quarterly common stock dividend was 20.5 cents per share throughout 2003. The dividend of 20.5 cents per share has been paid quarterly since September 1994.

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

The principal market on which the common stock of the Company is traded is the New York Stock Exchange. At February 15, 2007, there were 23,306 holders of record of common stock, and the market price of the common stock was $38.80. The quarterly market price of, and dividends on, Company common stock required by this item are included in the 2006 Annual Report to Shareholders filed as an exhibit hereto and incorporated herein by reference.

Item 6. SELECTED FINANCIAL DATAThe Company’s common stock dividend policy states that common stock dividends will be paid at a prudent level within the normal dividend payout range for its respective businesses, and that dividends will be established at a level considered sustainable in order to minimize business risk and maintain a strong capital structure throughout all economic cycles. The quarterly common stock dividend was 20.5 cents per share throughout 2005 and 2006. The dividend of 20.5 cents per share has been paid quarterly since September 1994. In February 2007, the Board of Directors increased the quarterly dividend payout to 21.5 cents per share, effective with the June 2007 payment.

SELECTED FINANCIAL DATA |

Information required by this item is included in the 20032006 Annual Report to Shareholders and is incorporated herein by reference.

Item 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Information required by this item is included in the 2003 Annual Report to Shareholders and is incorporated herein by reference.

Item 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Information required by this item is included in the 20032006 Annual Report to Shareholders under the heading “Management’s Discussion and Analysis” and under Notes 6 and 7 of the Notes to Consolidated Financial Statements and is incorporated herein by reference.

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

The Company is exposed to various forms of market risk, including commodity price risk, weather risk, and interest rate risk. The following describes the Company’s exposure to these risks.

Commodity Price Risk

About half of Southwest’s annual normal weather gas supply needs are secured using short duration contracts (one year or less). For the 2006/2007 heating season, fixed-price contracts ranged in price from $6 to $11 per dekatherm. Natural gas purchases not covered by fixed-price contracts are made under variable-price contracts with firm quantities and on the spot market. Prices for these contracts are not known until the month of purchase. The PGA mechanism allows Southwest to file to change the gas cost component of the rates charged to its customers to reflect increases or decreases in the price expected to be paid to its suppliers and companies providing interstate pipeline transportation service. Filings to change rates in accordance with PGA clauses are subject to audit by state regulatory commission staffs.

The Company does not currently utilize stand-alone derivative financial instruments, other than fixed-price term and variable-rate contracts, for speculative purposes or for hedging. During 2007, Southwest intends to supplement its current volatility mitigation program with stand-alone derivative instruments. The combination of fixed-price contracts and derivative instruments should increase flexibility for Southwest and increase supplier diversification. The Company intends to pursue the recovery of such costs as part of the PGA mechanisms upon approval by Southwest’s regulatory commissions in each jurisdiction.

Weather Risk

A significant portion of the Company’s operating margin is volume driven with current rates based on an assumption of normal weather. Demand for natural gas is greatly affected by temperature. On cold days, use of gas by residential and commercial customers may be as much as six times greater than on warm days because of increased use of gas for

space heating. Space heating-related volumes are the primary component of billings for these customer classes and are concentrated in the months of November to April. Variances in temperatures from normal levels, especially during these months, have a significant impact on the margin and associated net income of the Company. This impact is most pronounced in Arizona, where 54 percent of Southwest’s customers are located and where rates are highly leveraged.

The Company continues to pursue mechanisms in each of its service territories intended to stabilize the recovery of the Company’s fixed costs and reduce fluctuations in customers’ bills due to colder or warmer-than-normal weather. In California, the CPUC authorized a margin tracker balancing account in April 2004 that mitigates margin volatility due to weather and other usage variations. In Nevada, the PUCN approved certain rate design improvements in September 2004 to mitigate weather variations, including an increase in the monthly basic service charge and the use of declining block rates. In Arizona, most of Southwest’s requests for weather mitigation measures in its recent general rate case were rejected in the ACC’s final order approved in February 2006. The ACC did however encourage Southwest to work with the ACC Staff and other interested parties prospectively to seek rate design alternatives that will provide benefits to all affected stakeholders.

Interest Rate Risk

Interest rate risk is the risk that changes in interest rates could adversely affect earnings or cash flows. Specific interest rate risks for the Company include the risk of increasing interest rates on variable-rate obligations. Interest rate risk sensitivity analysis is used to measure interest rate risk by computing estimated changes in cash flows as a result of assumed changes in market interest rates. In Nevada, fluctuations in interest rates on variable-rate Industrial Development Revenue Bonds (“IDRBs”) are tracked and recovered from ratepayers through an interest balancing account. As of December 31, 2006 and 2005, the Company had $197 million and $224 million, respectively, in variable-rate debt outstanding, excluding Nevada variable-rate IDRBs. Assuming a constant outstanding balance in variable-rate debt for the next twelve months, a hypothetical one percent change in interest rates would increase or decrease interest expense for the next twelve months by approximately $2 million.

Other risk information is included under the heading “Company Risk Factors” inItem 1. Business1A. Risk Factors of this report.

Item 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

The Consolidated Financial Statements of Southwest Gas Corporation and Notes thereto, together with the reports of PricewaterhouseCoopers LLP, Independent Auditors, and Arthur Andersen LLP, Independent Public Accountants, are included in the 2003 Annual Report to Shareholders and are incorporated herein by reference.

FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA The CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE None.Item 9. CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSUREOn May 28, 2002, the Company dismissed Arthur Andersen LLP as its independent auditor. The decision to dismiss Arthur Andersen was recommended by the Company’s Audit Committee and approved by its Board of Directors.Arthur Andersen’s report on the financial statements of the Company for the year ended December 31, 2001 did not contain an adverse opinion or a disclaimer of opinion and was not qualified or modified as to uncertainty, audit scope, or accounting principles.During the years ended December 31, 2000 and 2001, and the interim period between December 31, 2001 and May 28, 2002, there were no disagreements between the Company and Arthur Andersen on any matter of accounting principles or practices, financial statement disclosure or auditing scope or procedure, which disagreements, if not resolved to the satisfaction of Arthur Andersen, would have caused it to make reference to the subject matter of the disagreements in connection with its report. During the years ended December 31, 2000 and 2001, and the interim period between December 31, 2001 and May 28, 2002, there were no reportable events (as defined in Item 304(a)(1)(v) of Regulation S-K promulgated by the SEC). In May 2002, Arthur Andersen furnished the Company with a letter addressed to the SEC stating that it agrees with the statements above. A copy of the letter was included as an exhibit to the Form 8-K filed by the Company in May 2002.Company engaged PricewaterhouseCoopers LLP as its independent auditor, effective May 28, 2002. During the years ended December 31, 2000Consolidated Financial Statements of Southwest Gas Corporation and 2001, and the interim period between December 31, 2001 and May 28, 2002, neither the Company nor anyone on its behalf consultedNotes thereto, together with PricewaterhouseCoopers LLP regarding (i) the application of accounting principles to a specified transaction, either completed or proposed, (ii) the type of audit opinion that might be rendered on the Company’s financial statements, or (iii) any matter that was either the subject of a disagreement (as described above) or a reportable event.The Company has not been able to obtain, after reasonable efforts, the written consent of Arthur Andersen to the incorporation by reference in the Company’s previously filed Form S-3 Registration Statements (Nos. 333-98995 and 333-106419) and Form S-8 Registration Statements (Nos. 333-31223, 333-106762 and 333-111034) of the report of Arthur Andersen on the 2001 financial statementsPricewaterhouseCoopers LLP, are included in thisthe 2006 Annual Report as requiredto Shareholders and are incorporated herein by the Securities Act of 1933. Therefore, in reliance on Rule 437a promulgated under the Securities Act of 1933, the Company has dispensed with the requirement to file a written consent from Arthur Andersen with this Annual Report. As a result, the ability of persons who purchase the Company’s securities pursuant to these Registration Statements to assert claims against Arthur Andersen may be limited.reference.Because the Company has not been able to obtain the written consent of Arthur Andersen, such persons may not have an effective remedy against Arthur Andersen for any untrue statements of a material fact contained in Arthur Andersen’s report or the financial statements covered thereby or any omissions to state a material fact required to be stated therein.Item 9A. CONTROLS AND PROCEDURESThe Company has established disclosure controls and procedures that are designed to provide reasonable assurance that information required to be disclosed in reports filed or submitted under the Securities Exchange Act of 1934 is recorded, processed, summarized, and reported within the time periods specified in the SEC’s rules and forms. A control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Further, the design of a control system must reflect the fact that there are resource constraints, and benefits of controls must be considered relative to their costs. Additionally, controls can be circumvented by the individual acts of some persons, by collusion of two or more people, or management override of the control. Because of the inherent limitations in a cost-effective control system, misstatements due to error or fraud may occur and not be detected.

Based on the most recent evaluation, as of December 31, 2003, management of the Company, including the Chief Executive Officer and Chief Financial Officer, believe the Company’s disclosure controls and procedures are effective at attaining the level of reasonable assurance noted above.

There have been no changes in the Company’s internal controls over financial reporting during the fourth quarter that have materially affected, or are likely to materially affect, the Company’s internal controls over financial reporting.

PART III

CONTROLS AND PROCEDURES |

Disclosure Controls and Procedures

The Company has established disclosure controls and procedures that are designed to provide reasonable assurance that information required to be disclosed in reports filed or submitted under the Securities Exchange Act of 1934 is recorded, processed, summarized, communicated to management, and reported within the time periods specified in the SEC’s rules and forms. A control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Further, the design of a control system must reflect the fact that there are resource constraints, and benefits of controls must be considered relative to their costs. Additionally, controls can be circumvented by the individual acts of some persons, by collusion of two or more people, or management override of the control. Because of the inherent limitations in a cost-effective control system, misstatements due to error or fraud may occur and may not be detected.

Based on the most recent evaluation, as of December 31, 2006, management of the Company, including the Chief Executive Officer and Chief Financial Officer, believe the Company’s disclosure controls and procedures are effective at attaining the level of reasonable assurance noted above.

Internal Control Over Financial Reporting

The report of management of the Company required to be reported herein is incorporated by reference to the information reported in the 2006 Annual Report to Shareholders under the caption “Management’s Report on Internal Control Over Financial Reporting” on page 61.

The Attestation Report of the Registered Public Accounting Firm required to be reported herein is incorporated by reference to the information reported in the 2006 Annual Report to Shareholders under the caption “Report of Independent Registered Public Accounting Firm” on page 62.

There has been no change in our internal control over financial reporting that occurred during our most recent fiscal quarter that has materially affected or is reasonably likely to materially affect our internal control over financial reporting.

OTHER INFORMATION |

None.

Item 10. DIRECTORS AND EXECUTIVE OFFICERS OF THE REGISTRANTPART III

DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE |

(a)Identification of Directors. Information with respect to Directors is set forth under the heading “Election of Directors” in the definitive 20042007 Proxy Statement, which by this reference is incorporated herein.

(b)Identification of Executive Officers. The name, age, position, and period position held during the last five years for each of the Executive Officers of the Company as of December 31, 2006 are as follows:

Name | Age | Position | Period | |||

| ||||||

Jeffrey W. Shaw | Chief Executive Officer | 2004-Present | ||||

President | 2003-2004 | |||||

Senior Vice President/Gas Resources and Pricing | 2002-2003 | |||||

Senior Vice President/Finance and Treasurer | 2002 | |||||

James P. Kane | 60 | President | 2004-Present | |||

Executive Vice President/Operations | 2002-2004 | |||||

George C. Biehl | Executive Vice President/Chief Financial Officer and | |||||

| Corporate Secretary | ||||||

| 2002-Present | |||||

John P. Hester | ||||||

Senior Vice President/Regulatory Affairs & Energy Resources | 2006-Present | |||||

Vice President/Regulatory Affairs and Systems Planning | 2003-2006 | |||||

Director/State Regulatory Affairs and Systems Planning | 2002-2003 | |||||

Edward | ||||||

Senior Vice President/ | ||||||

| 2004-Present | |||||

Vice President/Finance | 2003-2004 | |||||

Vice President/Finance and Treasurer | 2002-2003 | |||||

Vice President/Chief Accounting Officer | 2002 | |||||

Christina A. Palacios | 61 | Senior Vice President/Central Arizona Division | 2005-Present | |||

Senior Vice President/Southern Arizona Division | 2004-2005 | |||||

Vice President/Southern Arizona Division | 2002-2004 | |||||

Thomas R. Sheets | Senior Vice President/Legal Affairs and General Counsel | |||||

2002-Present | ||||||

Dudley J. Sondeno | Senior Vice President/Chief Knowledge and | |||||

Technology Officer | 2002-Present | |||||

Roy R. Centrella | Vice President/Controller and Chief Accounting Officer | 2002-Present | ||||

Controller | ||||||

2002 | ||||||

Kenneth J. Kenny | Vice President/Treasurer | 2005-Present | ||||

Treasurer | 2003-2005 | |||||

Assistant Treasurer/Director Financial Services | ||||||

2002-2003 |

(c)Identification of Certain Significant EmployeesEmployees.. None.

(d)Family Relationships. No Directors or Executive Officers are related to any other either by blood, marriage, or adoption.

(e)Business Experience. Information with respect to Directors is set forth under the heading “Election of Directors” in the definitive 20042007 Proxy Statement, which by this reference is incorporated herein. All Executive Officers have held responsible positions with the Company for at least five years as described in (b) above.

(f)Involvement in Certain Legal Proceedings. None.

(g)Promoters and Control Persons. None.

(h)Audit Committee Financial Expert. Information with respect to the financial expert of the Board of Directors’ audit committee is set forth under the heading “Committees of the Board” in the definitive 20042007 Proxy Statement, which by this reference is incorporated herein.

(i)Identification of the Audit Committee. Information with respect to the composition of the Board of Directors’ audit committee is set forth under the heading “Committees of the Board” in the definitive 20042007 Proxy Statement, which by this reference is incorporated herein.

(j)Material Changes in Director Nomination Procedures for Security Holders.None.

Section 16(a) Beneficial Ownership Reporting Compliance. Section 16(a) of the Securities Exchange Act of 1934 requires officers and directors, and persons who own more than ten percent of a registered class of equity securities, to file reports of ownership and changes in ownership with the SEC and the New York Stock Exchange. Officers, directors, and beneficial owners of more than ten percent of any class of equity securities are required by SEC regulation to furnish the Company with copies of all Section 16(a) forms they file.

The Company has adopted procedures to assist its directors and executive officers in complying with Section 16(a) of the Securities Exchange Act, of 1934, as amended, which includes assisting in the preparation of forms for filing. For 2003,2006, all reports were timely filed.

Code of Business Conduct and Ethics.The Company has adopted a code of business conduct and ethics for its employees, including its chief executive officer, chief financial officer, chief accounting officer, and non-employee directors. A code of ethics is defined as written standards that are reasonably designed to deter wrongdoing and to promote: 1) honest and ethical conduct; 2) full, fair, accurate, timely, and understandable disclosure in reports and documents that a registrant files; 3) compliance with applicable governmental laws, rules, and regulations; 4) the prompt internal reporting of violations of the code to an appropriate person or persons identified in the code; and 5) accountability for adherence to the code. The Company’s Code of Business Conduct & Ethics can be viewed on the Company’s website (www.swgas.com). If any substantive amendments to the Code of Business Conduct & Ethics are made or any waivers are granted, including any implicit waiver, from a provision of the Code of Business Conduct & Ethics, to the Company’s chief executive officer, chief financial officer and chief accounting officer, the Company will disclose the nature of such amendment or waiver on the Company’s website, www.swgas.com.

EXECUTIVE COMPENSATION |

Information with respect to executive compensation is set forth under the heading “Executive Compensation and Benefits”Compensation” in the definitive 20042007 Proxy Statement, which by this reference is incorporated herein.

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS |

(a)Security Ownership of Certain Beneficial Owners. Information with respect to security ownership of certain beneficial owners is set forth under the heading “Securities Ownership by Directors, Director Nominees, Executive Officers, and Certain Beneficial Owners” in the definitive 20042007 Proxy Statement, which by this reference is incorporated herein.

(b)Security Ownership of Management. Information with respect to security ownership of management is set forth under the heading “Securities Ownership by Directors, Director Nominees, Executive Officers, and Certain Beneficial Owners” in the definitive 20042007 Proxy Statement, which by this reference is incorporated herein.

(c)Changes in ControlControl.. None.

(d)Securities Authorized for Issuance Under Equity Compensation Plans.

At December 31, 2003,2006, the Company had two stock-based compensation plans. With respect to the first plan, the Company may grant options to purchase shares of common stock to key employees and outside directors.

Equity Compensation Plan Information

| Equity Compensation Plan Information | |||||||

Plan category | Number of securities to be issued upon exercise of outstanding options, warrants and rights | Weighted average exercise price of outstanding options, warrants and rights | Number of securities remaining available for future issuance | ||||

(Thousands of shares) | |||||||

Equity compensation plans approved by security holders | 1,502 | $ | 21.83 | 1,016 | |||

Equity compensation plans not approved by security holders | — | — | — | ||||

Total | 1,502 | $ | 21.83 | 1,016 | |||

Plan category | Number of securities to be issued upon exercise of outstanding options, warrants and rights | Weighted average exercise price of outstanding options, warrants and rights | Number of securities remaining available for future issuance | ||||

(Thousands of shares) | |||||||

Equity compensation plans approved by security holders | 957 | $ | 26.26 | — | |||

Equity compensation plans not approved by security holders | — | — | — | ||||

Total | 957 | $ | 26.26 | — | |||

Pursuant to the terms of the management incentive plan, the Company may issue restricted stock in the form of performance shares to encourage key employees to remain in its employment to achieve short-term and long-term performance goals.

Plan category | Number of securities to be issued upon vesting of performance shares | Weighted-average grant date fair value of award | Number of securities remaining available for future issuance | Number of securities to be issued upon vesting of performance shares | Weighted-average grant date fair value of award | Number of securities remaining available for future issuance | |||||||||

(Thousands of shares) | |||||||||||||||

Equity compensation plans approved by security holders | 381 | $ | 21.41 | — | 319 | $ | 24.61 | — | (a) | ||||||

Equity compensation plans not approved by security holders | — | — | — | — | — | — | |||||||||

Total | 381 | $ | 21.41 | — | 319 | $ | 24.61 | — | |||||||

(a) | No common shares are registered for this plan, but performance shares are authorized for future grant under the terms of the plan. |

Additional information regarding the two equity compensation plans is included in Note 910 of the Notes to Consolidated Financial Statements in the 20032006 Annual Report to Shareholders.

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE |

Information with respect to certain relationships and related transactions, and director independence is set forth under the heading “Governance of the Company” in the definitive 2007 Proxy Statement, which by this reference is incorporated herein.

None.

PRINCIPAL ACCOUNTING FEES AND SERVICES |

Information with respect to accounting fees and services associated with PricewaterhouseCoopers LLP is set forth under the heading “Selection of Independent Accountants” in the definitive 20042007 Proxy Statement, which by this reference is incorporated herein.

PART IV

Item 15.

| EXHIBITS, FINANCIAL STATEMENT SCHEDULES |

(a) | The following documents are filed as part of this report on Form 10-K: |

(1) | The Consolidated Financial Statements of the Company (including the Reports of Independent |

Consolidated Balance Sheets | ||

Consolidated Statements of Income | 39 | |

Consolidated Statements of Cash Flows | 40 | |

Consolidated Statements of Stockholders’ Equity and Comprehensive Income | 41 | |

Notes to Consolidated Financial Statements | 42 | |

Management’s Report | ||

Report of Independent Registered Public |

(2) | All schedules have been omitted because the required information is either inapplicable or included in the Notes to Consolidated Financial Statements. |

(3) | SeeLIST OF |

(b) Reports on Form 8-K.

On February 17, 2004, the Company furnished summary financial information for the quarter and year ended December 31, 2003 pursuant to Item 12 of Form 8-K.

(b) SeeLIST OF EXHIBITS.(c) SeeLIST OF EXHIBITS.

Exhibit | Description of Document | |

| 1.01 | Sales Agency Financing Agreement, dated as of March 16, 2006, between Southwest Gas Corporation and BNY Capital Markets, Inc. Incorporated herein by reference to the report on Form 8-K dated March 16, 2006. | |

| 3(i) | Restated Articles of Incorporation, as amended. Incorporated herein by reference to the report on Form 10-Q for the quarter ended March 31, 1997. | |

| 3(ii) | Amended Bylaws of Southwest Gas Corporation. Incorporated herein by reference to the report on Form | |

| 4.01 | ||

Indenture between City of Big Bear Lake, California, and Harris Trust and Savings Bank as Trustee, dated December 1, 1993, with respect to the issuance of $50,000,000 Industrial Development Revenue Bonds (Southwest Gas Corporation Project), 1993 Series A, due 2028. Incorporated herein by reference to the report on Form 10-K for the year ended December 31, 1993. | ||

Form of Deposit Agreement. Incorporated herein by reference to the Registration Statement on Form S-3, No. 33-55621. | ||

Form of Depositary Receipt (attached as Exhibit A to Form of Deposit Agreement included as Exhibit | ||

Indenture between the Company and Harris Trust and Savings Bank dated July 15, 1996, with respect to Debt Securities. Incorporated herein by reference to the report on Form 8-K dated July 26, 1996. | ||

First Supplemental Indenture of the Company to Harris Trust and Savings Bank dated August 1, 1996, supplementing and amending the Indenture dated as of July 15, 1996, with respect to 7 1/2% and 8% Debentures, due 2006 and 2026, respectively. Incorporated herein by reference to the report on Form 8-K dated July 31, 1996. | ||

Second Supplemental Indenture of the Company to Harris Trust and Savings Bank dated December 30, 1996, supplementing and amending the Indenture dated as of July 15, 1996, with respect to Medium-Term Notes. Incorporated herein by reference to the report on Form 8-K dated December 30, 1996. | ||

Indenture between Clark County, Nevada, and Harris Trust and Savings Bank as Trustee, dated as of October 1, 1999, with respect to the issuance of $35,000,000 Industrial Development Revenue Bonds (Southwest Gas Corporation), Series 1999A and Taxable Series 1999B or convertibles of Series B (Series C and D), due 2038. Incorporated herein by reference to the report on Form 10-K for the year ended December 31, 1999. | ||