UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 20042006

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period Fromto

Commission File Number 001-13533

NOVASTAR FINANCIAL, INC.

(Exact Name of Registrant as Specified in its Charter)

| Maryland | 74-2830661 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

| 8140 Ward Parkway, Suite 300, Kansas City, MO | 64114 | |

| (Address of Principal Executive Office) | (Zip Code) |

Registrant’s Telephone Number, Including Area Code:(816) 237-7000

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange on Which Registered | |

| Common Stock, $0.01 par value | New York Stock Exchange | |

| Redeemable Preferred Stock | New York Stock Exchange |

Securities Registered Pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined by Rule 405 of the Securities

Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the

Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark whether the registrant is an accelerated filera shell company (as defined in Exchange Act Rule 12b-2). Yes ¨ No x No ¨

The aggregate market value of voting and non-voting stock held by non-affiliates of the registrant as of June 30, 20042006 was approximately $948,751,931$972,533,092, based upon the closing sales price of the registrant’s common stock as reported byon the New York Stock Exchange Composite Transactions on such date.

The number of shares of the Registrant’s Common Stock outstanding on March 11, 2005February 28, 2007 was 27,860,629.37,410,228.

Documents Incorporated by Reference

Items 10, 11, 12, 13 and 14 of Part III are incorporated by reference to the NovaStar Financial, Inc. definitive proxy statement to shareholders, which will be filed with the Commission no later than 120 days after December 31, 2004.2006.

FORM 10-K

For the Fiscal Year Ended December 31, 20042006

TABLE OF CONTENTS

Item 1. | 2 | |||||

Item | ||||||

| Item 1B. | ||||||

| 31 | |||||

| Item 2. | 31 | |||||

| Item 3. | ||||||

| 31 | |||||

| Item 4. | ||||||

Item 5. | ||||||

| 33 | |||||

| Item 6. | ||||||

| 34 | |||||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |||||

| 36 | |||||

| Item 7A. | ||||||

| 79 | |||||

| Item 8. | ||||||

| 80 | |||||

| Item 9. | Changes in and Disagreements | |||||

| 128 | |||||

| Item 9A. | ||||||

| 128 | |||||

| Item 9B. | ||||||

Item 10. | ||||||

| Item 11. | ||||||

| Executive Compensation | |||||

| 130 | |||||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |||||

| 131 | |||||

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | |||||

| 131 | |||||

| Item 14. | ||||||

Item 15. | ||||||

Item 1.BusinessSafe Harbor Statement

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, regarding management’s beliefs, estimates, projections, and assumptions with respect to, among other things, our future operations, business plans and strategies, as well as industry and market conditions, all of which are subject to change at any time without notice. Actual results and operations for any future period may vary materially from those projected herein and from past results discussed herein. Some important factors that could cause actual results to differ materially from those anticipated include: our ability to successfully integrate acquired businesses or assets with our existing business; our ability to generate sufficient liquidity on favorable terms; the size, frequency and structure of our securitizations; impairments on our mortgage assets; interest rate fluctuations on our assets that differ from our liabilities; increases in prepayment or default rates on our mortgage assets; changes in assumptions regarding estimated loan losses and fair value amounts; our continued status as a REIT; changes in origination and resale pricing of mortgage loans; our compliance with applicable local, state and federal laws and regulations or opinions of counsel relating thereto and the impact of new local, state or federal legislation or regulations, or opinions of counsel relating thereto, or court decisions on our operations; the initiation of margin calls under our credit facilities; the ability of our servicing operations to maintain high performance standards and maintain appropriate ratings from rating agencies; our ability to expand origination volume while maintaining an acceptable level of overhead; our ability to adapt to and implement technological changes; the stability of residential property values; the outcome of litigation or regulatory actions pending against us or other legal contingencies; compliance with new accounting pronouncements; the impact of general economic conditions; and the risks that are from time to time included in our filings with the Securities and Exchange Commission (the “SEC”), including this Annual Report on Form 10-K. Other factors not presently identified may also cause actual results to differ. Words such as “believe,” “expect,” “anticipate,” “promise,” “plan,” and other expressions or words of similar meanings, as well as future or conditional verbs such as “will,” “would,” “should,” “could,” or “may” are generally intended to identify forward-looking statements. This document speaks only as of its date and we expressly disclaim any duty to update the information herein.

We are a Maryland corporation formed on September 13, 1996 which operates as a specialty finance company that originates, purchases, securitizes, sells, invests in and services residential nonconforming loans. We operate through three separate but inter-related units—mortgage lendingloans and loan servicing, mortgage portfolio management and branch operations.mortgage-backed securities. We offer a wide range of mortgage loan products to nonconforming borrowers, commonly referred to as “nonconforming borrowers,” who generally do not satisfy the credit, collateral, documentation or other underwriting standards prescribed by conventional mortgage lenders and loan buyers, including United States of America government-sponsored entities such as Fannie Mae or Freddie Mac. We retain significant interests in the nonconforming loans we originate and purchase through our mortgage securities investment portfolio. Through our servicing platform, we then service all of the loans we retain interests in, in order to better manage the credit performance of those loans.

We have elected to be taxed as a real estate investment trust or REIT,(“REIT”) under the Internal Revenue Code of 1986, as amended (Code)(the “Code”). Management believes the tax-advantaged structure ofFor so long as we maintain our status as a REIT, maximizes the after-tax returns from mortgage assets. Wewe must meet numerous rules established by the Internal Revenue Service (IRS) to retain our status as a REIT.(“IRS”). In summary, theythese rules require us to:

Restrict investments to certain real estate related assets,assets;

Avoid certain investment trading and hedging activities,activities; and

Distribute virtually all REIT taxable income to stockholders.our shareholders.

As long as we maintain our REIT status, distributions to stockholdersour shareholders will generally be deductible by us for income tax purposes. This deduction effectively eliminates REIT level income taxes. Management believes it has and will continue to meetthat we have met the requirements to maintain our REIT status for 2006 and prior years. We are, however, currently evaluating whether it is in shareholders’ best interests to retain our REIT status.

We operate three core businesses:

Mortgage portfolio management;

Mortgage lending; and

Loan servicing.

Segment information regarding these businesses for the three years ended December 31, 2006 is included in Note 16 to our consolidated financial statements.

Mortgage Portfolio Management

portfolios.

EarningsIn 2005 we began retaining various subordinate securities from our securitization transactions. In 2006, we began purchasing subordinated ABS of other ABS issuers. We will continue to acquire, retain, and aggregate ABS with the intention of securing non-recourse long-term financing through collateralized debt obligation (“CDO”) securitizations. In the future, we may enter into derivative transactions referencing third party ABS, commonly referred to as “synthetic” assets. We also intend to retain the risk of the underlying securities by investing in the equity and subordinated debt of CDO securitizations. CDO equity securities bear the first-loss and second-loss credit risk with respect to the securities owned by the securitization entity. Our goal is to leverage our extensive portfolio management experience by purchasing securities that are higher in the capital structure than our residual securities and executing CDOs for long-term non-recourse financing, thereby generating good risk-adjusted returns. We closed our first CDO securitization which was structured as a financing transaction on February 8, 2007, and we expect to continue to purchase securities that are higher in the capital structure and finance them with CDOs.

The long-term mortgage loan portfolio on our balance sheet consists of mortgage loans and securities generate a substantial portion of our earnings. Gross interest income was $224.0 million, $170.4 million and $107.1 millionclassified as held-in-portfolio resulting from securitization transactions treated as financings completed in the three years ended December 31, 2004, 2003second and 2002, respectively. Net interest income before credit losses/recoveries from the portfolio was $171.4 million, $130.1 millionthird quarters of 2006 (NHES Series 2006-1 and $79.4 millionNHES Series 2006-MTA1). We have financed our investment in the three years ended December 31, 2004, 2003 and 2002, respectively. See our discussion of interest income under the heading “Results of Operations” and “Net Interest Income”. See Note 15 to our consolidated financial statements for a summary of operating results and total assets for mortgage portfolio management.these loans by issuing ABB.

A significant risk toThe credit performance and prepayment rates of the nonconforming loans underlying our operations, relating to our portfolio management, issecurities, as well as the risk thatloans classified as held-in-portfolio, directly affects the profitability of this segment. In addition short-term interest rates have a significant impact on our assets will not adjust at the same times or amounts that rates on our liabilities adjust. Many of the loans in our portfolio have fixed rates of interest for a period of time ranging from 2 to 30 years. Our funding costs are generally not constant or fixed. We use derivative instruments to mitigate the risk of our cost of funding increasing or decreasing at a faster rate than the interest on the loans (both those on the balance sheet and those that serve as collateral for mortgage securities – available-for-sale).this segment’s profitability.

In certain circumstances, because we enter into interest rate agreements that do not meet the hedging criteria set forth in accounting principles generally accepted in the United States of America, we are required to record the change in the value of derivatives as a component of earnings even though they may reduce our interest rate risk. In times where short-term rates rise or drop significantly, the value of our agreements will increase or decrease, respectively. As a result, we recognized losses on these derivatives of $8.9 million, $30.8 million and $36.8 million in 2004, 2003 and 2002, respectively.

Mortgage Lending and Loan Servicing

The mortgage lending operation is significant to our financial results as it produces the loans that ultimately collateralize the mortgage securities – available-for-sale that we hold in our portfolio. During 2004, we originated and purchased $8.4 billion in nonconforming mortgage loans, the majority of which were retained in our servicing portfolio and serve as collateral for our securities. The loans we originate and purchase are sold, either in securitization transactions structured as sales or infinancing transactions, or are sold outright sales to third parties. We recognized gainsfinance the loans we originate and purchase by using warehouse repurchase agreements on sales ofa short-term basis. For long-term financing, we securitize our mortgage assets totaling $145.0 million, $144.0 millionloans and $53.3 million during the three years ended December 31, 2004, 2003 and 2002, respectively. In securitization transactions accounted for as sales, we retain interest-only, prepayment penalty, overcollateralization and other subordinated securities, along with the right to service the loans. See Note 15 to our consolidated financial statements for a summary of operating results and total assets for mortgage lending and loan servicing.issue ABB.

Our wholly-owned subsidiary, NovaStar Mortgage, Inc.,mortgage lending operations generate earnings primarily from securitizing and selling loans for a premium. We also earn revenue from fees from loan originations and interest income on mortgage loans held-for-sale. The timing, size and structure of our securitization transactions have a significant impact on the gain on sale recognized and ultimately the profitability of this segment. In addition the market prices for whole loans and short-term interest rates have a significant impact on this segment’s profitability.

Our mortgage lending segment originates and purchases primarily nonconforming, single-family residential mortgage loans. Our mortgage lending operation continues to innovate in loan origination. Our lending decisions are driven by three primary objectives:

Originating loans that perform in line with expectations,

Maintaining economically sound pricing (profitable coupons), and

Controlling costs of origination.

In our nonconforming lending operations, we lend to individuals who generally do not qualify for agency/conventional lending programs because of a lack of available documentation, or previous credit difficulties.difficulties or higher loan-to-value (“LTV”) ratios. These types of borrowers are generally willing to pay higher mortgage loan origination fees and interest rates than those charged by conventional lending sources.lenders. Because these borrowers typically use the proceeds of the mortgage loans to consolidate debt and to finance home improvements, education and other consumer needs, loan volume is generally less dependent on general levels of interest rates or home sales and therefore less cyclical than conventional mortgage lending.

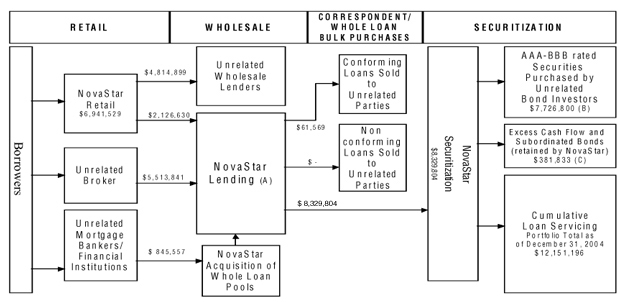

Our nationwide loan origination network includes wholesale loan brokers, mortgage lenders, and correspondent institutions, andall of which are independent of any of the NovaStar Financial entities, as well as our own direct to consumer operations. We have developed a nationwide network of wholesale loan brokers and mortgage lenders who submit mortgage loans to us. Except for NovaStar Home Mortgage brokers described below, these brokers and mortgage lenders are independent from any of the NovaStar entities. Our sales force, which includes account executives in 3938 states, develops and maintains relationships with this network of independent retail brokers. Our correspondent origination channel consists of a network of institutions from which we purchase nonconforming mortgage loans on a bulk or flow basis. Our direct to consumer originationoperations channel consists of call centers where we contact potential borrowers as well as a network of branch operations which use telemarketing and internet loan lead sourceswe acquired in the fourth quarter of 2006 in order to originate mortgage loans.expand this origination channel.

We underwrite, process, fund and service the nonconforming mortgage loans sourced through our broker network of wholesale loan brokers and mortgage lenders and our direct to consumer operations in centralized facilities. Further details regarding the loan originations are discussed under the “Mortgage Loans” section of “Management’s Discussion and Analysis of Financial Condition and Results of Operations”.

A significant risk to our mortgage lending operations is liquidity risk – the risk that we will not have financing facilities and cash available to fund and hold loans prior to their sale or securitization. We maintain committed lending facilities with large banking and investment institutions to reduce this risk. On a short-term basis, we finance mortgage loans using warehouse repurchase agreements. In addition, we have access to facilities secured by our mortgage securities – available-for-sale. Details regarding available financing arrangements and amounts outstanding under those arrangements are included in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note 7 to the consolidated financial statements.Loan Servicing

For long-term funding, we pool our mortgage loans and issue asset-backed bonds (ABB). Primary bonds – AAA through BBB rated – are issued to the public. We retain the interest-only, prepayment penalty, overcollateralization and other subordinated bonds. We also retain the right to service the loans. Prior to 1999, our ABB transactions were executed and designed to meet accounting rules that resulted in securitizations being treated as financing transactions. The mortgage loans and related debt continue to be presented on our consolidated balance sheets, and no gain was recorded. Beginning in 1999, our securitization transactions have been structured to qualify as sales for accounting and income tax purposes. The loans and related bond liability are not recorded in our consolidated financial statements. We do, however, record the value of the securities and servicing rights we retain. Details regarding ABBs we issued can be found in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and in Note 7 to our consolidated financial statements.

LoanManagement believes loan servicing remains a critical part of our business operation. In the opinion of management,operation because maintaining contact with our borrowers is critical in managing credit risk and infor borrower retention. Nonconforming borrowers are more prone to late payments and are more likely to default on their obligations than conventional borrowers. By servicing our loans, we strive to identify problems with borrowers early and take quick action to address problems. BorrowersIn addition, borrowers may be motivated to refinance their mortgage loans either by improving their personal credit or due to a decrease in interest rates. By keeping in close touch with borrowers, we can provide them with information about companyNovaStar Financial products to encourage them to refinance with us.

We retain the servicing rights with respect to the loans we securitize. Mortgage servicing yields fee income for us in the form of contractual fees approximating 0.50% of the outstanding balance of loans we service that have been securitized. In addition we receive fees paid by the borrowers for normal customer service and processing fees. In additionWe also earn interest income on funds we receive contractual fees approximating 0.50% of the outstanding balance and rights to future cash flows arising after the investors in the securitization trusts have received the return for which they contracted. We recognized $41.5 million, $21.1 million and $10.0 million in loan servicing fee income from the securitization trusts during the three years ended December 31, 2004, 2003 and 2002, respectively. See also “Mortgage Loan Servicing” under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for further discussion and analysishold as custodian as part of the servicing operations.

Branch Operationsprocess.

In 1999, we opened our retail mortgage broker business operating under the name NovaStar Home Mortgage, Inc. (“NHMI”). Prior to 2004, many of these NHMI branches were supported by LLC’s operating under LLC agreements where we owned a minority interest in the LLC and the branch manager was the majority interest holder. In December 2003, we decided to terminate the LLC’s effective January 1, 2004. As of January 1, 2004, continuing branches that formerly operated under LLC agreements became operating units of NHMI and their financial results are included in the consolidated financial statements. See Note 14 to our consolidated financial statements for further discussion. Branch offices offer conforming and nonconforming loans to potential borrowers. Loans are brokered for approved investors, including NovaStar Mortgage. The NHMI branches are considered departmental functions of NHMI under which the branch manager (department head) is an employee of NHMI and receives compensation based on the profitability of the branch (department) as bonus compensation. See Note 15 to our consolidated financial statements for a summary of operating results and total assets for our branches.

We routinely close branches and branch managers voluntarily terminate their employment with us, which generally results in the branch’s closure. As the demand for conforming loans declined significantly during 2004, many branches were not able to produce sufficient fees to meet operating expense demands. As a result of these conditions, a significant number of branch managers voluntarily terminated employment with us. We have also terminated many branches when loan production results were substandard. In these terminations, the branch and all operations are eliminated. Note 14 to our consolidated financial statements provides detail regarding the impact of the discontinued operations and modifications to our branch program.

The branch business provides an additional source for mortgage loan originations that, in most cases, we will eventually sell, either in securitizations or in outright sales to third parties. During 2004 and 2003, our branches brokered $3.7 billion and $6.4 billion, respectively, in nonconforming loans, of which we funded $1.7 billion and $1.2 billion, respectively.

Following is a diagram of the industry in which we operate and our loan production including nonconforming and conforming during 2004 (in thousands).

Market in Which NovaStar Operates and Competes

Over the last ten years, the nonconforming lending market has grown from less than $50 billion annually to approximately $640 billion in 2006 as estimated by Inside Mortgage Finance Publications. A significant portion of nonconforming loans are made to borrowers who are using equity in their primary residence to consolidate installment or consumer debt, or take cash out for personal reasons. The nonconforming market has grown through a variety of interest rate environments. Management estimates that in 2006 we had a 1-2% share of the nonconforming loan market.

We face intense competition in the business of originating, purchasing, selling and securitizing mortgage loans. The number of market participants is believed to be well in excess of 100 companies who originate and purchase nonconforming loans. No single participant holds a dominant share of the lending market. We compete for borrowers with consumer finance companies, conventional mortgage bankers, commercial banks, credit unions, thrift institutions and other independent wholesale mortgage lenders. Our principal competition in the business of holding mortgage loans and mortgage securities – available-for-sale are life insurance companies, institutional investors such as mutual funds and pension funds, other well-capitalized publicly-owned mortgage lenders and certain other mortgage acquisition companies structured as REITs. Many of these competitors are substantially larger than we are and have considerably greater financial resources than we do.

Competition among industry participants can take many forms, including convenience in obtaining a loan, amount and term of the loan, customer service, marketing/distribution channels, loan origination fees and interest rates. To the extent any competitor significantly expands their activities in the nonconforming and subprime market, we could be materially adversely affected.

Our principal competition in the business of holding mortgage loans and mortgage securities are life insurance companies, institutional investors such as mutual funds and pension funds, other well-capitalized, publicly-owned mortgage lenders and certain other mortgage acquisition companies structured as REITs. Many of these competitors are substantially larger than we are and have considerably greater financial resources than we do.

One of our key competitive strengths is our employees and the level of service they are able to provide our borrowers. We service our nonconforming loans and, in doing so, we are able to stay in close contact with our borrowers and identify potential problems early.

We also believe we compete successfully due to our:

experienced management team;

use of technology to enhance customer service and reduce operating costs;

vertical integration – we broker and/or originate, purchase, fund, service and manage mortgage loans;

access to capital markets to securitize our assets.

Risk Management

Management recognizes the following primary risks associated with the business and industry in which it operates.

Interest Rate/Market

Liquidity/Funding

Credit

Prepayment

Regulatory

Interest Rate/Market Risk

Risk.Our investment policy sets the following general goals:

(1) Maintaingoals are to maintain the net interest margin between our assets and liabilities and

(2) Diminish to diminish the effect of changes in interest rate levels on ourthe market value of our assets.

Interest Rate Risk. When interest rates on our assets do not adjust at the same time or in the same amounts as the interest rates ason our liabilities or when the assets have fixed rates and the liabilities are adjusting,have adjustable rates, future earnings potential is affected. We express this interest rate risk as the risk that the market value of our assets will increase or decrease at different rates than that of theour liabilities. Expressed another way, this is the risk that our net asset value will experience an adverse change when interest rates change. We assess the risk based on the change in market values given increases and decreases in interest rates. We also assess the risk based on the impact to net income in changing interest rate environments.

Management primarily usesThe interest rates under our primary financing sources where the interest rate resetsreset frequently. As of December 31, 2004,2006, rates on a majority of our borrowings under all financing arrangements adjust daily or monthly.monthly off London Inter-Bank Offered Rate (“LIBOR”). On the other hand, very few of the mortgage assets we own adjust on a monthly or daily basis. Most of the mortgage loans contain features where theirhave rates that are fixed for some period of time and then adjust frequently thereafter.ranging from 2 to 30 years. For example, one of our loan products is the “2/28” loan. This loan is fixed for its first two years and then adjusts every six months thereafter.

While short-term borrowing rates are low and long-term asset rates are high, this portfolio structure produces good results. However, if short-term interest rates rise rapidly, earning potential iswould be significantly affected and impairments may be incurred, as the asset rate resets would lag the borrowing rate resets.

We transfer interest rate agreements at the time of securitization into the securitization trusts to protect the third-party bondholders from interest rate risk and to decrease the volatility of future cash flows related to the securitized mortgage loans. We enter into these interest rate agreements as we originate and purchase mortgage loans in our mortgage lending segment. At the time of a securitization structured as a sale, we transfer interest rate agreements into the securitization trusts and they are removed from our balance sheet. The trust assumes the obligation to make payments and obtains the right to receive payments under these agreements. Generally, net settlement obligations paid by the trust for these interest rate agreements reduce the excess interest cash flows to our residual securities. Net settlement receipts from these interest rate agreements are either used to cover interest shortfalls on the third-party primary bonds or to provide credit enhancement with any remaining funds then flowing to our residual securities. For securitizations structured as financings the derivatives will remain on our balance sheet. Generally, these interest rate agreements do not meet the hedging criteria set forth in accounting principles generally accepted in the United States of America (“GAAP”) while they are on our balance sheet; therefore, we are required to record their change in value as a component of earnings even though they may reduce our interest rate risk. In times when short-term rates rise or drop significantly, the value of our agreements will increase or decrease, respectively. Occasionally, we enter into interest rate agreements that do meet the hedging criteria set forth in GAAP. In these instances, we record their change in value, if effective, directly to other comprehensive income on our statement of shareholder’s equity.

Interest Rate Sensitivity Analysis. ToWe model financial information in a variety of interest rate scenarios to assess interest rate sensitivity as an indication of exposure to interest rate risk, management relies on models of financial information in a variety of interest rate scenarios.risk. Using these models, the fair value and interest rate sensitivity of each financial instrument, or groups of similar instruments, is estimated, and then aggregated to form a comprehensive picture of the risk characteristics of the balance sheet. The risks are analyzed on a market value basis.

The following table summarizes management’s estimates of the changes in market value of our same mortgage assets and interest rate agreements assuming interest rates were 100 and 200 basis points, or 1one and 2two percent higher andor lower. The cumulative change in market value represents the change in market value of mortgage assets, net of the change in market value of interest rate agreements. The change in market value of the liabilities on our balance sheet due to a change in interest rates is insignificant since a majority of our short-term borrowings and ABB are adjustable rate; however, as noted above, rapid increases in short-term interest rates would negatively impact the interest-rate spread between our liabilities onand assets and, consequently, our balance sheet which finance our mortgage assets is insignificant.earnings.

Interest Rate Sensitivity - Market Value

(dollars in thousands)

| Basis Point Increase (Decrease) in Interest Rate (A) | Basis Point Increase (Decrease) in Interest Rates (A) | ||||||||||||||||||||||||||||||

| (200) (C) | (100) | 100 | 200 | (200) | (100) | 100 | 200 | ||||||||||||||||||||||||

As of December 31, 2004: | |||||||||||||||||||||||||||||||

As of December 31, 2006: | |||||||||||||||||||||||||||||||

Change in market values of: | |||||||||||||||||||||||||||||||

Assets | 70,438 | $ | 33,198 | $ | (34,045 | ) | $ | (72,840 | ) | ||||||||||||||||||||||

Assets – non trading (B) | $ | 226,262 | $ | 105,038 | $ | (78,698 | ) | $ | (150,481 | ) | |||||||||||||||||||||

Assets – trading (C) | 9,999 | 7,080 | (14,120 | ) | (30,707 | ) | |||||||||||||||||||||||||

Interest rate agreements | (54,085 | ) | (28,046 | ) | 27,832 | 55,113 | (40,018 | ) | (20,946 | ) | 23,998 | 49,264 | |||||||||||||||||||

Cumulative change in market value | 16,353 | $ | 5,152 | $ | (6,213 | ) | $ | (17,727 | ) | $ | 196,243 | $ | 91,172 | $ | (68,820 | ) | $ | (131,924 | ) | ||||||||||||

Percent change of market value portfolio equity (B) | 3.3 | % | 1.0 | % | (1.3 | )% | (3.6 | )% | |||||||||||||||||||||||

Percent change of market value portfolio equity (D) | 34.0 | % | 15.8 | % | (11.9 | %) | (22.9 | %) | |||||||||||||||||||||||

As of December 31, 2003: | |||||||||||||||||||||||||||||||

As of December 31, 2005: | |||||||||||||||||||||||||||||||

Change in market values of: | |||||||||||||||||||||||||||||||

Assets | N/A | $ | 34,499 | $ | (65,216 | ) | $ | (144,343 | ) | ||||||||||||||||||||||

Assets – non trading (B) | $ | 95,322 | $ | 41,344 | $ | (41,417 | ) | $ | (84,971 | ) | |||||||||||||||||||||

Assets – trading (C) | 1,134 | 983 | (2,837 | ) | (7,512 | ) | |||||||||||||||||||||||||

Interest rate agreements | N/A | (31,250 | ) | 34,073 | 69,497 | (33,502 | ) | (17,365 | ) | 20,072 | 41,616 | ||||||||||||||||||||

Cumulative change in market value | N/A | $ | 3,249 | $ | (31,143 | ) | $ | (74,846 | ) | $ | 62,954 | $ | 24,962 | $ | (24,182 | ) | $ | (50,867 | ) | ||||||||||||

Percent change of market value portfolio equity (B) | N/A | 1.0 | % | (9.1 | )% | (21.9 | )% | ||||||||||||||||||||||||

Percent change of market value portfolio equity (D) | 11.0 | % | 4.4 | % | (4.2 | %) | (8.9 | %) | |||||||||||||||||||||||

| (A) | Change in market value of assets or interest rate agreements in a parallel shift in the yield curve, up and down 1% and 2%. |

| (B) | Includes mortgage loans held-for-sale, mortgage loans held-in-portfolio, mortgage securities—available-for-sale and mortgage servicing rights. |

| (C) | Consists of mortgage securities – trading. |

| (D) | Total change in estimated market value as a percent of market value portfolio equity as of December 31. |

Hedging.In orderWe use derivative instruments to addressmitigate the risk of our cost of funding increasing at a mismatch offaster rate than the interest rate indices and adjustment periods on our assets and liabilities, the hedging section of the investment policy is followed, as approved by the Board. Specifically, theloans. We adhere to an interest rate risk management program that is approved by our Board. This program is formulated with the intent to offset the potential adverse effects resulting from rate adjustment limitations on mortgage assets and the differences between interest rate adjustment indices and interest rate adjustment periods of adjustable-rate mortgage loans and related borrowings.

We use interest rate cap and swap contracts to mitigate the risk of the costfinancing expense of variable rate liabilities increasing at a faster rate than the earningsincome produced on assets during a period of rising rates. In this way, managementManagement intends generally to hedge as much of the interest rate risk as determined to be in our best interest, given the cost and risk of hedging transactions and the needlimitations on our ability to maintainhedge imposed on us by REIT status.tax requirements.

We seek to build a balance sheet and undertake an interest rate risk management program that is likely, in management’s view, to enable us to maintain an equity liquidation value sufficient to maintain operations given a variety of potentially adverse circumstances. Accordingly, the hedging program addresses both income preservation, as discussed in the first part of this section, and capital preservation concerns.

Interest rate cap and swap agreements are legal contracts between us and a third-party firm or “counterparty”. TheUnder an interest rate cap agreement the counterparty agrees to make payments to us in the future should the one-month LIBOR interest rate rise above the strike rate specified in the contract. We make either quarterly or monthly premium payments or have chosen to pay the premiums at the beginning to the counterparties under contract. Each contract has either a fixed or amortizing notional face amount on which the interest is computed, and a set term to maturity. When the referenced LIBOR interest rate rises above the contractual strike rate, we earn cap income. Payments on an annualized basis equal the contractual notional face amount times the difference between actual LIBOR and the strike rate. Interest rate swaps have similar characteristics. However,Under interest rate swap agreements allow us towe pay a fixed rate of interest while receiving a rate that adjusts with one-month LIBOR.

The following table summarizes the key contractual terms associated with our interest rate risk management contracts. Substantially allcontracts on our balance sheet as of theDecember 31, 2006. All of our pay-fixed swapsswap contracts and interest rate capscap contracts are indexed to one-month LIBOR.

We have determined the following estimated net fair value amounts by using available market information and valuation methodologies we deem appropriate as of December 31, 2004.2006.

Interest Rate Risk Management Contracts

(dollars in thousands)

| Maturity Range | |||||||||||||||||||

Net Fair Value | Total Notional Amount | 2005 | 2006 | 2007 | |||||||||||||||

Pay-fixed swaps: | |||||||||||||||||||

Contractual maturity | $ | 6,143 | $ | 1,350,000 | $ | 285,000 | $ | 840,000 | $ | 225,000 | |||||||||

Weighted average pay rate | 3.0 | % | 2.4 | % | 3.1 | % | 3.5 | % | |||||||||||

Weighted average receive rate | 2.4 | % | (A | ) | (A | ) | (A | ) | |||||||||||

Interest rate caps: | |||||||||||||||||||

Contractual maturity | $ | 5,819 | $ | 650,000 | $ | 450,000 | $ | 200,000 | $ | — | |||||||||

Weighted average strike rate | 1.7 | % | 1.6 | % | 2.0 | % | — | ||||||||||||

| Net Fair Value | Total Notional Amount | Maturity Range | |||||||||||||||||||||||||

| 2007 | 2008 | 2009 | 2010 | 2011 | |||||||||||||||||||||||

Pay-fixed swaps: | |||||||||||||||||||||||||||

Contractual maturity | $ | 6,527 | $ | 1,575,000 | $ | 490,000 | $ | 720,000 | $ | 365,000 | $ | — | $ | — | |||||||||||||

Weighted average pay rate | 4.9 | % | 4.7 | % | 5.0 | % | 4.9 | % | — | — | |||||||||||||||||

Weighted average receive rate | 5.4 | % | (A | ) | (A | ) | (A | ) | — | — | |||||||||||||||||

Interest rate caps: | |||||||||||||||||||||||||||

Contractual maturity | $ | 4,634 | $ | 610,000 | $ | 80,000 | $ | 285,000 | $ | 195,000 | $ | 40,000 | $ | 10,000 | |||||||||||||

Weighted average strike rate | 5.0 | % | 4.9 | % | 4.9 | % | 5.0 | % | 5.2 | % | 5.4 | % | |||||||||||||||

| (A) | The pay-fixed swaps receive rate is indexed to one-month |

Liquidity/Funding RiskWe had no interest rate agreements with contractual maturities beyond 2011 as of December 31, 2006.

MortgageLiquidity/Funding Risk.A significant risk to our mortgage lending requires significantoperations is the risk that we will not have financing facilities and cash available to fund loan originations and purchases. Our warehouse lending arrangements, includinghold loans prior to their sale or securitization, to fund required repurchase agreements, support the mortgage lending operation. Our warehouse mortgage lenders allow us to borrow between 98%requests and 100% of the outstanding principal. Funding for the difference – generally 2% of the principal - must come from cash on hand. If we are unable to obtain sufficient cash resources,margin calls or that we may not be able to operatesecuritize our loans or securities upon favorable terms. On a short-term basis, we finance mortgage loans using warehouse repurchase agreements that we maintain with large banking and investment institutions. In addition, we have access to facilities secured by our mortgage lending (banking) segment.

We are currently dependent upon a limited number of primary credit facilities forsecurities and servicing advance receivables. For long-term financing, we depend on securitizations and CDOs. Other matters also impact our liquidity and funding of our mortgage loan originations and acquisitions. Any failure to renew or obtain adequate funding under these financing arrangements could harm our lending operations and our overall performance. An increase in the cost of financing in excess of any change in the income derived from our mortgage assets could also harm our earnings and reduce the cash available for distributions to our stockholders. In October 1998, the subprime mortgage loan market faced a liquidity crisis with respect to the availability of short-term borrowings from major lenders and long-term borrowings through securitization. At that time, we faced significant liquidity constraints that harmed our business and our profitability. We can provide no assurance that those adverse circumstances will not recur.

We use repurchase agreements to finance the acquisition of mortgage assets in the short-term. In a repurchase agreement, we sell an asset and agree to repurchase the same asset at some period in the future. Generally, the repurchase agreements we entered into stipulate that we must repurchase the asset in 30 days. For financial accounting purposes, these arrangements are treated as secured financings. We retain the assets on our balance sheet and record an obligation to repurchase the asset. For our repurchase agreements secured by mortgage loans, the amount we may borrow is generally 98% of the mortgage loan market value. For our repurchase agreements secured by mortgage securities, the amount we may borrow is generally 75% of the mortgage securities market value. When asset market values decrease, we are required to repay the margin, or difference in market value. To the extent the market values of assets financed with repurchase agreements decline rapidly, we will be required to meet cash margin calls. If cash is unavailable, we may default on our obligations under the applicable repurchase agreement. In that event, the lender retains the right to liquidate the collateral we provided to it to settle the amount due from us.

We are dependent on the securitization market for the sale of our loans because we securitize loans directly and many of our whole loan buyers purchase our loans with the intention to securitize. The securitization market is dependent upon a number of factors, including general economic conditions, conditions in the securities market generally and conditions in the asset-backed securities market specifically. In addition, poor performance of our previously securitized loans could harm our access to the securitization market. Accordingly, a decline in the securitization market, the ability to obtain attractive terms or a change in the market’s demand for our loans could have a material adverse effect on our results of operations, financial condition and business prospects.

risk. See the “Liquidity and Capital Resources” section of “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for further discussion of liquidity risks and resources available to us.

Credit Risk

. Credit risk is the risk that we will not fully collect the principal we have invested in mortgage loans or the amount we have invested in securities. Nonconforming mortgage loans comprise substantially our entire mortgage loan portfolio and serve as collateral for our mortgage securities – available-for-sale. Our nonconformingsecurities. Nonconforming borrowers include individuals who do not qualify for agency/conventional lending programs because of a lack of conventional documentation or previous credit difficulties but have considerable equity in their homes. Often, they are individuals or families who have built up high-rate consumer debt and are attempting to use the equity in their home to consolidate debt and reduce the amount of money it takes to service their monthly debt obligations. Our underwriting guidelines are intended to evaluate the credit history of the potential borrower, the capacity and willingness of the borrower to repay the loan, and the adequacy of the collateral securing the loan.

UnderwritingOur underwriting staff workworks under the credit policies established by our Chief Credit Officer.Committee. Underwriters are given approval authority only after their work has been reviewed for a period of time. Thereafter, the Chief Credit Officer re-evaluates the authority levels of all underwriting personnel on an ongoing basis. All loans in excess of $350,000 currently require the approval of an underwriting supervisor. Our Chief Credit Officer or our President must approve loans in excess of $1,000,000.

TheOur underwriting guidelines take into consideration the number of times the potential borrower has recently been late on a mortgage payment and whether that payment was 30, 60 or 90 days past due. Factors such as FICO score, bankruptcy and foreclosure filings, debt-to-income ratio, and loan-to-value ratio are also considered. The credit grade that is assigned to the borrower is a reflection of the borrower’s historical credit and the loan-to-value determined by the amount of documentation the borrower could produce to support income.credit. Maximum loan-to-value ratios for each credit grade depend on the level of income documentation provided by the potential borrower. In some instances, when the borrower exhibits strong compensating factors, exceptions to the underwriting guidelines may be approved.

In 2006, we saw the performance of our 2006 vintage production drop to unacceptable levels. We believe this performance is related to a few key fundamentals such as:

Downturn in the housing market

Underwriting guidelines that worked in a stronger housing market were no longer effective in the weaker 2006 market

Tolerance levels previously allowed for appraisals were no longer effective in the weaker 2006 market

KeyGoing forward, the key area of focus for our credit management function is to ensure that the 2007 vintage performs better than 2006 and in line with our successful underwriting process is the use of NovaStarIS®. NovaStarIS® is the second generation of our proprietary automated underwriting system. IS provides more consistency in underwriting loans and allows underwriting personnel to focus more of their time on loans that are not initially accepted by the IS system.expectations. In this regard, we have taken several steps which include:

Our mortgage loan portfolio by credit grade, allTightening of which are nonconforming can be accessed viaunderwriting guidelines

Enhancing our website at www.novastarmortgage.com.appraisal review process

Identifying loans with unacceptable levels of risk.

A toolOther strategies we use for managing credit risk isare to diversify the markets in which we originate, purchase and own mortgage loans. Presented via our website at www.novastarmortgage.com is a breakdownloans and the purchase of the geographic diversification of our loans. Details regarding loans charged off are disclosed in Note 2 to our consolidated financial statements.

mortgage insurance. We have purchased mortgage insurance on manya majority of the loans that are held in our portfolio – on the balance sheet and those that serve as collateral for our mortgage securities – available-for-sale.securities. The use of mortgage insurance is discussed under “Premiums for Mortgage Loan Insurance” in “Management’s Discussion and Analysis of Financial Condition and Results of Operations”. Details regarding loans charged off are disclosed in Note 2 to our consolidated financial statements.

Prepayment Risk

.Generally speaking, when market interest rates decline, borrowers are more likely to refinance their mortgages. The higher the interest rate a borrower currently has on his or her mortgage the more incentive he or she has to refinance the mortgage when rates decline. In addition, the higher the credit grade, the more incentive there is to refinance increases when credit ratings improve. When home values rise, loan-to-value ratios drop, making it more likely that a borrower has a low loan-to-value ratio, he or she is more likely towill do a “cash-out” refinance. Each of these factors increases the chance for higher prepayment speeds during the term of the loan.speeds.

The majority of our mortgage securities available-for-sale portfolio consists of securities which are “interest-only” in nature. These securities represent the net cash flow – interest income – on the underlying loans in excess of the cost to finance the loans. When borrowers repay the principal on their mortgage loans early, the effect is to shorten the period over which interest is earned, and therefore, reduce the cash flow and yield on our securities.

We mitigate prepayment risk by originating and purchasing loans that include a penalty if the borrower repays the loan in the early months of the loan’s life. For theA majority of our loans have a prepayment penalty is charged equalup to but no greater than 80% of six months interest on the principal balance that is to be paid in full.being repaid. As of December 31, 2004, 73%2006, 60% of our securitizedthe loans had a prepayment penalty. These loanswhich serve as collateral for our mortgage securities – available-for-sale.had a prepayment penalty. As of December 31, 2004, 65%2006, 60% of our mortgage loans - held-for-saleon our balance sheet had a prepayment penalty, which serve as collateral for our short-term borrowings.penalty. During 2004, 72%2006, 62% of the loans we originated and purchased had prepayment penalties.

Regulatory Risk

Risk.As a mortgage lender, we are subject to many laws and regulations. Any failure to comply with these rules and their interpretations or with any future interpretations or judicial decisions could harm our profitability or cause a change in the way we do business. For example, several lawsuits have been filed challenging types of payments made by mortgage lenders to mortgage brokers. Similarly,

State and local governing bodies are focused on the nonconforming lending business and are concerned about borrowers paying “excessive fees” in obtaining a mortgage loan – generally termed “predatory lending”. In several instances, states or local governing bodies have imposed strict laws on lenders to curb predatory lending. To date, these laws have not had a significant impact on our branch operations, we allowbusiness. We have capped fee structures consistent with those adopted by federal mortgage agencies and have implemented rigid processes to ensure that our branch managers considerable autonomy, which could result in our facing greater exposure to third-party claims if our compliance programslending practices are not strictly adhered to.predatory in nature.

Several states and cities are considering or have passed laws, regulations or ordinances aimed at curbing predatory lending practices. The federal government is also considering legislative and regulatory proposals in this regard. In general, these proposals involve loweringWe regularly monitor the existing federal Homeownership and Equity Protection Act thresholds for defining a “high-cost” loan, and establishing enhanced protections and remedies for borrowers who receive such loans. Passage of these laws and rules could reduce our loan origination volume. In addition, many whole loan buyers may elect not to purchase any loan labeled as a “high cost” loan under any local, state or federal law or regulation. Rating agencies likewise may refuse to rate securities backed by such loans. Accordingly, these laws and rules could severely restrict the secondary market for a significant portion of our loan production. This would effectively preclude us from continuing to originate loans either in jurisdictions unacceptable to the rating agencies or otherwise within newly defined thresholds and could have a material adverse effect on our business.

Recently enacted and effective laws, regulations and standards relating to corporate governance and disclosure requirements applicable to public companies, including the Sarbanes-Oxley Act of 2002, new Securities and Exchange Commission regulations and New York Stock Exchange rules have increased the costs of corporate governance, reporting and disclosure practices. These costs may increase in the future due to our continuing implementation of compliance programs mandated by these requirements. In addition, these new laws, rules and regulations create newthat apply to our business and analyze any changes to them. We integrate many legal bases for administrative enforcement and civilregulatory requirements into our automated loan origination system to reduce inadvertent non-compliance due to human error. We also maintain policies and criminal proceedings against us in case of non-compliance, thereby increasingprocedures, summaries and checklists to help our risks of liabilityorigination personnel comply with these laws. Our training programs are designed to teach our personnel about the significant laws, rules and potential sanctions.regulations that affect their job responsibilities.

Other Risk Factors

Although management considers the risk components set forth above to be its primary business risks, the following are other risks that should be considered by our investors. Further information regarding these risks is included in our registration statements filed with the Commission.

U.S. Federal Income Tax Consequences

The following general discussion summarizes the material U.S. federal income tax considerations regarding our qualification and taxation as a REIT. This discussion is based on interpretations of the Code, regulations issued thereunder, and rulings and decisions currently in effect (or in some cases proposed), all of which are subject to change. Any such change may be applied retroactively and may adversely affect the federal income tax consequences described herein. This summary does not discuss all of the tax consequences that may be relevant to particular shareholders or shareholders subject to special treatment under the federal income tax laws. Accordingly, you should consult your own tax advisor regarding the federal, state, local, foreign, and other tax consequences of your ownership of our common stock and our REIT status and any termination of our REIT status, and regarding potential changes in applicable tax laws.

General.Since inception, we have elected to be taxed as a REIT under Sections 856 through 859 of the Code. We believe we have complied, and intend to comply in the future for so long as we remain a REIT, with the requirements for qualification as a REIT under the Code. To the extent that we qualify as a REIT for federal income tax purposes, we generally will not be subject to federal income tax on the amount of income or gain that is distributed to shareholders. However, origination and broker operations are conducted through NovaStar Mortgage, and NovaStar Home Mortgage, which areis owned by NFI Holding Corporation, Inc. – a taxable REIT subsidiary (TRS)(“TRS”). Consequently, all of the taxable income of NFI Holding Corporation, Inc. is subject to federal and state corporate income taxes. In general, a TRS may hold assets that a REIT cannot hold directly and generally may engage in any real estate or non-real estate related business. However, special rules do apply to certain activities between a REIT and its TRS. For example, a TRS will be subject to earnings stripping limitations on the deductibility of interest paid to its REIT. In addition, a REIT will be subject to a 100% excise tax on certain excess amounts to ensure that (i) tenants who payamounts paid to a TRS for services are based on amounts that would be charged in an arm’s-length amount by the TRS,transaction, (ii) fees paid to a REIT by its TRS are reflected at fair market value and (iii) interest paid by a TRS to its REIT is commercially reasonable.

The REIT rules generally require that a REIT invest primarily in real estate related assets, that its activities be passive rather than active and that it distribute annually to its shareholders substantially all of its taxable income. We could be subject to a number of taxes if we failed to satisfy those rules or if we acquired certain types of income-producing real property through foreclosure. Although no complete assurance can be given, we do not expect that we will be subject to material amounts of such taxes.

Failure to satisfy certain Code requirements could cause loss of REIT status. If we fail to qualify, or elect to terminate our status, as a REIT for any taxable year, we would be subject to federal income tax (including any applicable minimum tax) at regular corporate rates and would not receive deductions for dividends paid to shareholders. As a result, the amount of after-tax earnings available for distribution to shareholders would decrease substantially. While we intend to operate in a manner that will enable us to qualify as a REIT in future taxable years, there can be no certainty that such intention will be realized.

Qualification as a REIT. Qualification as a REIT requires that we satisfy a variety of tests relating to income, assets, distributions and ownership.ownership so long as we remain a REIT. The significant tests are summarized below.

Sources of IncomeIncome.. WeTo qualify as a REIT, we must satisfy two tests with respect to the sourcesgross income requirements, each of income: the 75% income test, and the 95% income test. The 75% income test requires that we derivewhich is applied on an annual basis. First, at least 75% of our gross income, excluding gross income from prohibited transactions, for each taxable year generally must be derived directly or indirectly from:

rents from certain passive real estate-related activities. In orderproperty;

interest on debt secured by mortgages on real property or on interests in real property;

dividends or other distributions on, and gain from the sale of, stock in other REITs;

gain from the sale of real property or mortgage loans;

amounts, such as commitment fees, received in consideration for entering into an agreement to satisfymake a loan secured by real property, unless such amounts are determined by income and profits;

income derived from a Real Estate Mortgage Investment Conduit (“REMIC”) in proportion to the 95% income test,real estate assets held by the REMIC, unless at least 95% of the REMIC’s assets are real estate assets, in which case all of the income derived from the REMIC; and

interest or dividend income from investments in stock or debt instruments attributable to the temporary investment of new capital during the one-year period following our receipt of new capital that we raise through equity offerings or public offerings of debt obligations with at least a five-year term.

Second, at least 95% of our gross income, excluding gross income from prohibited transactions, for each taxable year must be derived from the same sources asthat qualify for purposes of the 75% gross income test, and from (i) dividends, (ii) interest, (iii) certain qualifying hedges entered into prior to January 1, 2005 and (iv) gain from the sale or from dividendsother disposition of stock, securities, or, interest from any source. certain qualifying hedges entered into prior to January 1, 2005.

Management believes that we were in compliance with both of the income tests for the 20042006 and 20032005 calendar years.

Nature and Diversification of AssetsAssets.. As of the last day of each calendar quarter, we must meet six requirements under the two asset tests. Under the 75% of assets test, at least 75% of the value of our total assets must represent cash or cash items (including receivables), government securities or real estate assets. Under the 25% of assets test, no more than 25% of the value of our total assets can be represented by securities, other than (A) government securities, (B) stock of a qualified REIT subsidiary and (C) securities that qualify as real estate assets under the 75% assets test (collectively((A), (B) and (C) are collectively the “75% Securities”). Additionally, under the 25% assets test, no more than 20% of the value of our total assets can be represented by securities of one or more taxable REIT subsidiaries and no more than 5% of the value of our total assets can be represented by the securities of a single issuer, excluding 75% Securities. Furthermore, we may not own more than 10% of the total voting power or the total value of the outstanding securities of any one issuer, excluding 75% Securities.

If we inadvertently fail to satisfy one or more of the asset tests at the end of a calendar quarter, such failure would not cause us to lose our REIT status. We could still avoid disqualification by eliminating any discrepancy within 30 days after the close of the calendar quarter in which the discrepancy arose. Management believes that we arewere in compliance with all of the requirements of both asset tests for all quarters during 20042006 and 2003.2005.

Ownership of Common StockStock.. Our capital stock must be held by a minimum of 100 persons for at least 335 days of each year. In addition, at all times during the second half of each taxable year, no more than 50% in value of our capital stock may be owned directly or indirectly by 5 or fewer individuals. We use the calendar year as our taxable year for income tax purposes. The Code requires us to send annual information questionnaires to specified shareholders in order to assure compliance with the ownership tests. Management believes that we have complied with these stock ownership tests for 20042006 and 2003.2005.

DistributionsDistributions.. WeTo maintain REIT status, we must distribute at least 90% of our taxable income and any after-tax net income from certain types of foreclosure property less any non-cash income. No distributions are required in periods in which there is no taxable income. Management believes that we have complied with these distribution requirements for 2005 and intends to comply with these requirements with respect to 2006 taxable income.

Taxable IncomeIncome.. We use the calendar year for both tax and financial reporting purposes. However, there may be differences between taxable income may, and in our case does, differ from income computed in accordance with accounting principles generally accepted in the United States of America (GAAP).GAAP. These differences primarily arise from timing and character differences in the recognition of revenue and expense and gains and losses for tax and GAAP purposes. Additionally, taxable income that is subject to the distribution requirement does not include the taxable income of our taxable subsidiary,TRS, although the subsidiary’s operating results are included in our GAAP results.

Personnel

As of December 31, 2004,2006, we employed 3,5022,048 people. Of these, 1,738 were employed inManagement believes that relations with its employees are good. None of our mortgage portfolio management and mortgage lending and loan servicing operations. Our branches employed 1,721 people as of December 31, 2004. The remaining employees were employed in our branch administrative functions.are represented by a union or covered by a collective bargaining agreement.

Available Information

A copyCopies of the filings we have madeour annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to these reports filed or furnished with the Securities and Exchange Commission (SEC) may be obtained onSEC are available free of charge through our Internet site (www.novastarmortgage.com) as soon as reasonably practicable after filing with the SEC. References to our website (www.novastarmortgage.com), throughdo not incorporate by reference the information on such website into this Annual Report on Form 10-K and we disclaim any such incorporation by reference. Copies of our board committee charters, our board’s Corporate Governance Guidelines, Code of Conduct, and other corporate governance information are available at the SEC (www.sec.gov)Corporate Governance section of our Internet site (www.novastarmortgage.com), or by contacting us directly. Our investor relations contact information follows.

Investor Relations

8140 Ward Parkway, Suite 300

Kansas City, MO 64114

816.237.7000816.237.7424

Email: ir@novastar1.com

Risk Factors

You should carefully consider the risks described below before investing in our publicly traded securities. The risks described below are not the only ones facing us. Our business is also subject to the risks that affect many other companies, such as competition, inflation, technological obsolescence, labor relations, general economic conditions and geopolitical events. Additional risks not currently known to us or that we currently believe are immaterial also may impair our business, operations and our liquidity.

Risks Related to Securitization, Loan Sale, and Borrowing Activities

Our growth is dependent on leverage, which may create other risks.

Our success is dependent, in part, upon our ability to grow our assets through the use of leverage. Leverage creates an opportunity for increased net income, but at the same time creates risks. For example, while we will incur leverage only when there is an expectation that it will enhance returns, leveraging magnifies both positive and negative changes in our net worth. In addition, there can be no assurance that we will be able to meet our debt service obligations and, to the extent that we cannot, our financial condition and our ability to meet minimum REIT dividend requirements will be materially and adversely affected. Furthermore, if we were to liquidate, our debt holders and lenders will receive a distribution of our available assets before any distributions are made to our common shareholders.

An interruption or reduction in the securitization market or our ability to access this market would harm our financial position.

We are dependent on the securitization market for long-term financing of our origination and purchase of mortgage loans and mortgage securities, which we initially finance with our short-term financing. In addition, many of the buyers of our whole loans purchase the loans with the intention of securitizing them. A disruption in the securitization market could prevent us from being able to sell loans or mortgage securities at a favorable price or at all. Factors that could disrupt the securitization market include an international liquidity crisis such as occurred in the fall of 1998, sudden changes in interest rates, changes in the non-conforming loan market, a terrorist attack, an outbreak of war or other significant event risk, and market specific events such as a default under a comparable type of securitization. Further, poor performance of our previously securitized loans could harm our access to the securitization market.

In addition, a court recently found a lender and securitization underwriter liable for consumer fraud committed by a company to whom they provided financing and underwriting services. In the event other courts or regulators adopted the same liability theory, lenders and underwriters could be named as defendants in more litigation and as a result they may exit the business or charge more for their services, all of which could have a negative impact on our ability to securitize our mortgage loans and mortgage securities and the securitization market in general.

A decline in our ability to obtain long-term funding for our mortgage loans or mortgage securities in the securitization market in general or on attractive terms or a decline in the market’s demand for our mortgage loans or mortgage securities could harm our results of operations, financial condition and business prospects and could result in defaults under our short term financing arrangements for these assets.

We may not be able to continue to sell our mortgage loans on terms and conditions that are profitable to us.

A portion of our revenues comes from the gains on sale generated by sales of pools of our mortgage loans as whole loans. We make whole loan sales to a limited number of institutional purchasers, some of which may be frequent, repeat purchasers, and others of which may make only one or a few purchases from us. We cannot assure you that we will continue to have purchasers for our loans on terms and conditions that will be profitable to us. Also, even though our mortgage loans are generally marketable to multiple purchasers, certain loans may be marketable to only one or a few purchasers, thereby increasing the risk that we may be unable to sell such loans at a profit.

Failure to renew or obtain adequate funding under warehouse repurchase agreements may harm our business.

We are dependent upon several warehouse repurchase agreements to provide short term financing for our origination and purchase of mortgage loans pending their sale or securitization. In addition, we utilize warehouse repurchase agreements for short and medium term financing for our purchase and retention of mortgage securities. Under a warehouse repurchase agreement, we sell an asset and agree to repurchase the same asset at some point in time in the future. Generally, the repurchase agreements we enter into require monthly roll-over repurchase transactions, with a six- to nine-month maximum financing period for mortgage loans and a three-year maximum financing period for securities retained from our mortgage loan securitizations. For financial accounting purposes, these arrangements are treated as secured financings. We retain the assets on our balance sheet and record an obligation to repurchase the assets. The amount we may borrow under these arrangements is generally 95% to 100% of the asset market value with respect to performing mortgage loans and 70% to 80% of the asset market value with respect to nonperforming mortgage loans. Additionally, the amount we may borrow under these arrangements is generally 40% to 95% of the asset market value with respect to mortgage securities depending on the investment rating.

These warehouse repurchase agreements contain numerous representations, warranties and covenants, including requirements to maintain a certain minimum net worth, to maintain minimum equity ratios, to maintain our REIT status, and other customary debt covenants. Events of default under these facilities include material breaches of representations and warranties, failure to comply with covenants, material adverse effects upon or changes in our business, assets, or financial condition, and other customary matters. Events of default under certain of our facilities also include termination of our status as servicer with respect to certain securitized loan pools and failure to maintain profitability over consecutive quarters. If we were unable to make the necessary representations and warranties at the time we need financing, we would not be able to obtain needed funds. In addition, if we default under any warehouse repurchase agreement under which borrowings are then outstanding, the lenders under substantially all of our existing warehouse repurchase agreements could demand immediate payment of all outstanding amounts pursuant to cross-default provisions. Any failure to renew or obtain adequate funding under these financing arrangements for any reason, or any demand by warehouse lenders for immediate payment of outstanding balances, could harm our lending and loan purchase operations and have a material adverse effect on our results of operations, financial condition and business prospects. In addition, an increase in the cost of warehouse financing in excess of any change in the income derived from our mortgage assets could also harm our earnings and reduce the cash available for distribution to our shareholders. In October 1998, the subprime mortgage loan market faced a liquidity crisis with respect to the availability of short-term borrowings from major lenders and long-term borrowings through securitization. At that time, we faced significant liquidity constraints which harmed our business and our profitability. There is no assurance that a comparable situation will not occur in the future.

A decline in the market value of mortgage assets financed under our warehouse finance arrangements may result in margin calls or similar obligations, which may require that we liquidate assets at a disadvantageous time.

When, in a lender’s opinion, the market value of assets subject to a warehouse repurchase agreement decreases for any reason, including a rise in interest rates or general concern about the value or liquidity of the assets, we are required to repay the margin or difference in market value, or post additional collateral. If cash or additional collateral is unavailable to meet margin calls, we may default on our obligations under the applicable repurchase agreement, which would cross-default substantially all of our warehouse repurchase agreements. In that event, our lenders would have the right to liquidate the collateral we provided them to settle the amount due from us and, in general, the right to recover any deficiency from us.

In addition, we utilize warehouse financing arrangements for the accumulation of third-party mortgage-backed securities and related credit default derivatives for purposes of CDO offerings. Under these arrangements, the financing party has the right to liquidate any assets that decline in credit quality or fail to continue to meet eligibility requirements, and the right to liquidate the entire pool of financed assets if the related CDO offering does not occur by a specified date. If a liquidation results in a net loss, we are required to pay to the financing party the amount of the net loss.

In order to obtain cash to satisfy a margin call or a net loss payment obligation, we may be required to liquidate assets at a disadvantageous time, which could cause us to incur further losses and adversely affect our results of operations and financial condition. In addition, an unplanned liquidation of assets could change our mix of investments, which in turn could jeopardize our REIT status or our ability to rely on certain exemptions under the Investment Company Act of 1940, as amended (the “Investment Company Act”).

We may be required to repurchase mortgage loans or indemnify mortgage loan purchasers as a result of breaches of representations and warranties, borrower fraud, or certain borrower defaults, which could harm our liquidity, results of operations and financial condition.

When we sell mortgage loans, whether as whole loans or pursuant to a securitization, we are required to make customary representations and warranties to the purchaser about the mortgage loans and the manner in which they were originated. Our whole loan sale agreements require us to repurchase or substitute mortgage loans in the event we breach any of these representations or warranties. In addition, we may be required to repurchase mortgage loans as a result of borrower fraud or in the event of early payment default on a mortgage loan. Likewise, we are required to repurchase or substitute mortgage loans if we breach a representation or warranty in connection with our securitizations. The remedies available to us against the originating broker or correspondent may not be as broad as the remedies available to a purchaser of mortgage loans against us, and we face the further risk that the originating broker or correspondent may not have the financial capacity to perform remedies that otherwise may be available to us. Therefore, if a purchaser enforces its remedies against us, we may not be able to recover losses from the originating broker or correspondent. Repurchased loans are typically sold at a significant discount to the unpaid principal balance and, prior to sale, can be financed by us, if at all, only at a steep discount to our cost. As a result, significant repurchase activity could harm our liquidity, cash flow, results of operations, financial condition and business prospects.

Recently, we have received an increased number of repurchase and indemnity demands from purchasers of whole loans as a result of borrower fraud and early borrower payment defaults, which has had a negative impact on our results of operations. While we have taken steps to enhance our underwriting policies and procedures, there can be no assurance that these steps will be effective. To the extent that repurchase and indemnity demands continue at this rate or increase, our results of operations and financial condition will be adversely affected.

Our investments in mortgage securities and loans are subject to changes in credit spreads which could adversely affect our ability to realize gains on the sale of such investments and may subject us to margin calls or similar liquidity requirements.