UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT

pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

FOR THE FISCAL YEAR ENDED JUNE 30, 20052007

000-15701

(Commission file number)

NATURAL ALTERNATIVES INTERNATIONAL, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 84-1007839 | |

| (State of incorporation) | (IRS Employer Identification No.) | |

1185 Linda Vista Drive San Marcos, California 92078 | (760) 744-7340 | |

| (Address of principal executive offices) | (Registrant’s telephone number) | |

Securities registered pursuant to Section 12(b) of the Act:

None

Title of each class | Name of exchange on which registered | |

Common Stock, $0.01 par value per share | Nasdaq Global Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Common Stock, $0.01 par value per shareIndicate by check mark if Natural Alternatives International, Inc. (NAI) is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act of 1933. ¨ Yes x No

Indicate by check mark if NAI is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act of 1934. ¨ Yes x No

Indicate by check mark whether Natural Alternatives International, Inc. (NAI)NAI (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that NAI was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of NAI’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x¨

Indicate by check mark whether NAI is a large accelerated filer, an accelerated filer, (as defined in Rule 12b-2 of the Act).or a non-accelerated filer. (Check one):

Large accelerated filer ¨ YesAccelerated filer ¨ Non-accelerated filer x No

Indicate by check mark whether NAI is a shell company (as defined in Rule 12b-2 of the Exchange Act.): Yes ¨ NoYes x No

The aggregate market value of NAI’s common stock held by non-affiliates of NAI as of the last business day of NAI’s most recently completed second fiscal quarter (December 31, 2004)29, 2006) was approximately $41,243,757$45,238,820 (based on the closing sale price of $9.23$8.67 reported by Nasdaq on December 31, 2004)29, 2006). For this purpose, all of NAI’s officers and directors and their affiliates were assumed to be affiliates of NAI.

As of September 8, 2005, 6,032,367October 15, 2007, 6,977,199 shares of NAI’s common stock were outstanding, net of 61,000180,941 treasury shares.

DOCUMENTS INCORPORATED BY REFERENCE

Part III (Items 10, 11, 12, 13 and 14) of this Form 10-K incorporates by reference portions of NAI’s definitive proxy statement for its Annual Meeting of Stockholders to be held December 2, 2005,11, 2007, to be filed on or before October 28, 2005.2007.

(i)

SPECIAL NOTE ABOUT FORWARD-LOOKING STATEMENTS

Certain statements in this report, including information incorporated by reference, are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, Section 21E of the Securities Exchange Act of 1934, and the Private Securities Litigation Reform Act of 1995. Forward-looking statements reflect current views about future events and financial performance based on certain assumptions. They include opinions, forecasts, intentions, plans, goals, projections, guidance, expectations, beliefs or other statements that are not statements of historical fact. Words such as “may,” “will,” “should,” “could,” “would,” “expects,” “plans,” “believes,” “anticipates,” “intends,” “estimates,” “approximates,” “predicts,” or “projects,” or the negative or other variation of such words, and similar expressions may identify a statement as a forward-looking statement. Any statements that refer to projections of our future financial performance, our anticipated growth and trends in our business, our goals, strategies, focus and plans, and other characterizations of future events or circumstances, including statements expressing general optimism about future operating results, are forward-looking statements. Forward-looking statements in this report may include statements about:

future financial and operating results, including projections of net sales, revenue, income, net income per share, profit margins, expenditures, liquidity, goodwill valuation and other financial items;

development of new products, brands and marketing strategies;

• | the effect of the discontinuance of Dr. Cherry’s television program and our ability to develop a new marketing plan for, and to sustain, our Pathway to Healing® product line; |

distribution channels, product sales and performance and timing of product shipments;

• | our ability to expand the customer base of the As We Change® catalog and achieve higher sales, profitability and cash flows as a result; |

inventories and the impactadequacy and intended use of accounting pronouncements;our facilities;

current or future customer orders;

the impact on our business and results of operations and variations in quarterly net sales from seasonal and other factors;

management’s goals and plans for future operations; and

our ability to improve operational efficiencies, manage costs and business risks and improve or maintain profitability;

growth, expansion, diversification and acquisition strategies, the success of such strategies, and the benefits we believe can be derived from such strategies;

personnel;

the outcome of regulatory, tax and litigation matters;

sources and availability of raw materials;

operations outside the United States;

the adequacy of reserves and allowances;

overall industry and market performance;

competition;

current and future economic and political conditions;

the impact of accounting pronouncements; and

other assumptions described in this report underlying or relating to any forward-looking statements.

The forward-looking statements in this report speak only as of the date of this report and caution should be taken not to place undue reliance on any such forward-looking statements. Forward-looking statements are subject to certain events, risks, and uncertainties that may be outside of our control. When considering forward-looking statements, you should carefully review the risks, uncertainties and other cautionary statements in this report as they identify certain important factors that could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. These factors include, among others, the risks described under Item 71A of Part I and elsewhere in this report, as well as in other reports and documents we file with the SEC.United States Securities and Exchange Commission (SEC).

| ITEM 1. | BUSINESS |

Overview

Our vision is to enrich the world through the best of nutrition.

As our primary business activity, we provide private label contract manufacturing services to companies that market and distribute vitamins, minerals, herbs, and other nutritional supplements, as well as other health care products, to consumers both within and outside the United States. Additionally, under our direct-to-consumer marketing program, we develop, manufacture and market our own products, as well as market third party branded products, including a variety of high quality nutritional, beauty, skin care, exercise, lifestyle and work with nationally recognized physicians to develop brand nameother personal care products, that reflect their individual approaches to restoring, maintaining or improving health.

through our wholly owned subsidiary, Real Health Laboratories, Inc. (RHL), an integrated direct marketer of branded nutritional supplements and other lifestyle products. RHL’s operations include in-house creative, catalog design, supply chain management and call center and fulfillment activities.

Our U.S.-based manufacturing facilities are located in Vista, California. These facilities were recertified in June 2005 by the Therapeutic Goods Administration (“TGA”)(TGA) of Australia after theirits audit of our Good Manufacturing Practices (“GMP”)(GMP). TGA evaluates new therapeutic products, prepares standards, develops testing methods and conducts testing programs to ensure that products are high in quality, safe and effective. The TGA also conducts a range of assessment and monitoring activities including audits of the manufacturing practices of companies who export and sell products to Australia. TGA certification enables us to manufacture products for export into countries that have signed the Pharmaceutical Inspection Convention, which include most European countries as well as several Pacific Rim countries. TGA certifications are generally reviewed every eighteen months.

months and our existing TGA certification is currently under review.

Our California facilities also have been awarded GMP registration annually by NSF International (NSF) through the NSF Dietary Supplements Certification Program since October 2002.

GMP requirements are regulatory standards and guidelines establishing necessary processes, procedures and documentation for manufacturers in an effort to assure the products produced by that manufacturer have the identity, strength, composition, quality and purity they are represented to possess.

Natural Alternatives International Europe S.A. (NAIE), our wholly owned subsidiary existing under the laws of Switzerland, also operates a manufacturing, warehousing, packaging and distribution facility in Manno, Switzerland. In January 2004, NAIE obtained a pharmaceutical license to process pharmaceuticals for packaging, importation, export and sale within Switzerland and other countries from the Swissmedic Authority of Bern, Switzerland. In March 2007, following the expansion of NAIE’s manufacturing facilities to include powder filling capabilities, NAIE obtained an additional pharmaceutical license from the Swissmedic Authority certifying NAIE’s expanded facilities conform to GMP. We believe the licensethese licenses and NAIE’s new capabilities help strengthen our relationships with existing customers and can help improve our ability to develop relationships with new customers. The license islicenses are valid until January 2009.

In addition to our operations in the United States and Switzerland, we have a full-time representative in Japan who provides a range of services to our customers currently present in or seeking to expand into the Japanese market and other markets in the Pacific Rim. These services include regulatory and marketing assistance along with guidance and support in adapting products to these markets.

Originally founded in 1980, Natural Alternatives International, Inc. reorganized as a Delaware corporation in 1989. Unless the context requires otherwise, all references in this report to the “Company,” “NAI,” “we,” “our,” and “us” refer to Natural Alternatives International, Inc. and, as applicable, NAIE, RHL and our other wholly owned subsidiaries. Our principal executive offices are located at 1185 Linda Vista Drive, San Marcos, California, 92078.

Business Strategy

Our goals are to increaseachieve long-term growth and diversify our net sales while improving our overall financial results.sales. To achieveaccomplish these goals, we have sought and intend to continue to seek to:

leverage our state of the strengthart facilities to increase the value of the goods and services we provide to our existing customer relationships through new product introductions;

invest in expanding and marketing our own branded products, including those acquired through our acquisition opportunities;of RHL; and

improve operational efficiencies and manage costs.costs and business risks to improve profitability.

Overall, we believe there is an opportunity to enhance consumer confidence in the quality of our nutritional supplements and their adherence to label claims through the education provided by direct sales and direct-to-consumer marketing programs. We believe our GMP and TGA certified manufacturing operations, science based product formulation,formulations, peer-reviewed clinical studies and regulatory expertise provide us with a sustainable competitive advantage by providing our customers with a high degree of confidence in our products.the products we manufacture.

WeWhile today’s consumer may have access to a variety of information, we believe the lack of relevant and reliable consumer educationmany consumers remain uneducated about nutrition and nutritional supplementation, combined withuncertain about the duplicationrelevance or reliability of brands and products in the retail sales channel createinformation they have or are confused about conflicting claims or information, which we believe creates a significant opportunity for the direct sales marketing channel. The direct sales marketing channel has proved, and we believe will continue to prove, to be a highly effective method for marketing high quality nutritional supplements as associates or other personalities educate consumers on the benefits of science based nutritional supplements. We believe this education process can lead to premium product pricing and avoid competing with brands of inferior quality and lower pricing in other distribution channels. Our two largest customers operate in the direct sales marketing channel. Thus, our growth has been fueled primarily by the effectiveness of our customers in this marketing channel.

Further, we believe our acquisition of RHL in December 2005 has strengthened our ability to achieve certain of our goals. Through RHL, we are able to market our own branded products and have expanded our distribution channels. Our acquisition of RHL also has provided the following benefits:

Additional expertise in direct marketing and retail channels;

Existing, leading branded products in the Food, Drug and Mass Market (FDM) retail channel; and

Access to additional direct marketing and mass-market channels for our products and concepts.

We believe our comprehensive approach to customer service is unique within our industry. We believe this approach, together with our commitment to high quality, innovative products and the leadership ofinvestment in our experienced management team,branded products, will provide the means to implement our strategies and achieve our goals. There can be no assurance, however, that we will successfully implement any of our business strategies or that we will increase or diversify our net sales or improve our overall financial results.

Products, Principal Markets and Methods of Distribution

Our primary business activity is to provide private label contract manufacturing services to companies that market and distribute vitamins, minerals, herbs, and other nutritional supplements, as well as other health care products, to consumers both within and outside the United States. Our private label contract manufacturing customers include companies that market nutritional supplements through direct sales marketing channels, direct response television and retail stores. We manufacture products in a variety of forms, including capsules, tablets, chewable wafers and powders to accommodate a variety of consumer preferences.

We provide strategic partnering services to our private label contract manufacturing customers, including the following:

customized product formulation;

clinical studies;

manufacturing;

marketing support;

international regulatory and label law compliance;

international product registration; and

packaging in multiple formats and labeling design.

Additionally, under our direct-to-consumer marketing program,branded products segment, we develop, manufacture and market our own products. Under the direct-to-consumer marketing program, weproducts and work with nationally recognized physicians and others to develop brand name products that reflect their individual approaches to restoring, maintaining or improving health. Direct-to-consumer marketing programThese products are sold through a variety of distribution channels including television, programs, print media and the internet.

We believealso market the direct-to-consumer marketing program can be an effective method for marketing ourReal Health® Laboratories branded nutritional supplement product line, as well as third party products, through the As We Change® (AWC) catalog and certain other distribution channels. The Real Health® Laboratories nutritional supplement product line consists of ten condition-specific, custom formulated products and is marketed through mass retail, with distribution to FDM retailers. The AWC catalog is a lifestyle catalog geared towards women between the ages of 45 and 65. The quarterly print catalog offers a variety of high quality nutritional, supplements. In March 2000, we launched Dr. Cherry’s Pathway to Healingbeauty, skin care, exercise, lifestyle and other personal care products.TM product line. As of June 30, 2005, the product line included nineteen condition specific, custom formulated products. The products are primarily marketed through a weekly television program.

For the last three fiscal years ended June 30, our net sales were derived from our private label contract manufacturing and direct-to-consumer marketing program were as followsthe following (dollars in thousands):

| Fiscal 2005 | Fiscal 2004 | Fiscal 2003 | |||||||

Private Label Contract Manufacturing | $ | 83,382 | $ | 68,493 | $ | 45,768 | |||

Direct-to-Consumer Marketing Program | 8,110 | 10,041 | 10,194 | ||||||

Total Net Sales | $ | 91,492 | $ | 78,534 | $ | 55,962 | |||

| 2007 | 2006 | 2005 | |||||||||||||

| $ | % | $ | % | $ | % | ||||||||||

Private Label Contract Manufacturing | $ | 80,732 | 83 | $ | 85,758 | 86 | $ | 83,862 | 91 | ||||||

Branded Products | 16,396 | 17 | 13,854 | 14 | 8,110 | 9 | |||||||||

Total Net Sales | $ | 97,128 | 100 | $ | 99,612 | 100 | $ | 91,972 | 100 | ||||||

Research and Development

We are committed to quality research and development. We focus on the development of new science based products and the improvement of existing products. We periodically test and validate our products to help ensure their stability, potency, efficacy and safety. We maintain quality control procedures to verify that our products comply with applicable specifications and standards established by the Food and Drug Administration and other regulatory agencies. We also direct and participate in clinical research studies, often in collaboration with scientists and research institutions, to validate the benefits of a product and provide scientific support for product claims and marketing initiatives. We believe our commitment to research and development, team of experienced personnel, as well as our facilities and strategic alliances with our suppliers and customers, allow us to effectively identify, develop and market high-quality and innovative products.

As part of the services we provide to our private label contract manufacturing customers, we may perform, but are not required to perform, certain research and development activities related to the development or improvement of their products. While our customers typically do not pay directly for this service, the cost of this service is included as a component of the price we charge to manufacture and deliver their products. Research and development costs, which include costs associated with international regulatory compliance services we provide to our customers, are expensed as incurred.

Our research and development expenses for the last three fiscal years ended June 30 were $1.9 million for 2007, $1.7 million for 2006 and $3.5 million for 2005, $2.8 million for 2004 and $1.7 million for 2003.2005.

Sources and Availability of Raw Materials

We use raw materials in our operations including powders, excipients, empty capsules, and components for packaging and distributing our finished products. We typically buy raw materials in bulk from a limited number of qualified vendors located both within and outside the United States. During fiscal 2005, Carrington Laboratories Incorporated was our largest supplier, accounting for 35% of our total raw material purchases.

We test the raw materials we buy to ensure their quality, purity and potency before we use them in our products. We typically buy raw materials in bulk from qualified vendors located both within and outside the United States. During the fiscal year ended June 30, 2005, we2007, our three largest suppliers accounted for 39% of our total raw material purchases. We did not experience any significant shortages or difficulties obtaining adequate supplies of raw materials during fiscal 2007 and we do not anticipate any significant shortages or difficulties in the near term.

Major Customers

NSA International, Inc. has been our largest customer over the past several years. During the fiscal year ended June 30, 2005,2007, NSA International, Inc. accounted for approximately 40% of our net sales. Our second largest customer was Mannatech, Incorporated, which accounted for approximately 39%31% of our net sales during fiscal 2005.2007. Both NSA International, Inc. and Mannatech, Incorporatedof these customers are private label contract manufacturing customers. No other customer accounted for 10% or more of our net sales during fiscal 2005. Our sales and marketing team is focused2007. We continue to focus on obtaining new private label contract manufacturing customers and developing new direct-to-consumer marketing programsgrowing our branded products, including those acquired through the acquisition of RHL, to reduce the risks associated with deriving a significant portion of our net sales from a limited number of customers.

Competition

We compete with other manufacturers, distributors and distributorsmarketers of vitamins, minerals, herbs, and other nutritional supplements, beauty, skin care, exercise, lifestyle and other personal care products, both within and outside the United States. The nutritional supplement industry isand lifestyle product industries are highly fragmented and competition for the sale of nutritional supplements and lifestyle products comes from many sources. These products are sold primarily through retailers (drug store chains, supermarkets, and mass market discount retailers), health and natural food stores, and direct sales channels (mail order, network marketing and e-marketing companies). The products we produce for our private label contract manufacturing customers may compete with our direct-to-consumerown branded products, although we believe such competition is limited.

We believe private label contract manufacturing competition in our industry is based on, among other things, customized services offered, product quality and safety, innovation, price and customer service. We believe we compete favorably with other companies because of our ability to provide comprehensive turn key solutions for customers, our certified manufacturing operations and our commitment to quality and safety through our research and development activities.

Our future competitive position in the industryfor both private label contract manufacturing and branded products will likely depend on, but not be limited to, the following:

the continued acceptance of our products by our customers and consumers;

our ability to continue to develop high quality, innovative products;

our ability to attract and retain qualified personnel;

the effect of any future governmental regulations on our products and business;

the results of, and publicity from, product safety and performance studies performed by governments and other research institutions;

the continued growth of the global nutrition industry; and

our ability to respond to changes within the industry and consumer demand, financially and otherwise.

The nutritional supplement industry isand lifestyle product industries are highly competitive and we expect the level of competition to remain high over the near term. We do not believe it is possible to accurately estimate the number or size of our competitors. The nutritional supplement industry has undergone consolidation in the recent past and we expect that trend to continue in the near term.

Government Regulation

Our business is subject to varying degrees of regulation by a number of government authorities in the United States, including the United States Food and Drug Administration (FDA), the Federal Trade Commission (FTC), the Consumer Product Safety Commission, the United States Department of Agriculture, and the Environmental

Protection Agency. Various agencies of the states and localities in which we operate and in which our products are sold also regulate our business, such as the California Department of Health Services, Food and Drug Branch. The areas of our business that these and other authorities regulate include, among others:

product claims and advertising;

product labels;

product labels;ingredients; and

The FDA, in particular, regulates the formulation, manufacturing, packaging, storage, labeling, promotion, distribution and sale of vitamin and other nutritional supplements in the United States, while the FTC regulates marketing and advertising claims. TheIn August 2007, a new rule issued by the FDA issued a final rule called “Statements Made for Dietary Supplements Concerning the Effectwent into effect requiring companies that manufacture, package, label, distribute or hold nutritional supplements to meet certain GMPs to ensure such products are of the Productquality specified and are properly packaged and labeled. Companies have up to three years to comply with the new requirements depending on the Structure or Functionsize of the Body,” which includes regulations requiring companies, their suppliers and manufacturerscompany. In our case, given the current number of our employees, we would be required to meet GMP incomply with the preparation, packaging, storage and shipment of their products. The FDA also published a Notice of Advance Rule Making for Good Manufacturing Practices that would require manufacturing of dietary supplements to follow GMP. While the final regulations are subject to revision, wenew requirements by June 25, 2009. We are committed to meeting or exceeding the standards set by the FDA on a timely basis and believe we are well positioned to operate within the new GMPs mandated by the FDA.

The FDA has also issued regulations governingregulates the labeling and marketing of dietary supplements and nutritional products. They include:products, including:

the identification of dietary supplements or nutritional products and their nutrition and ingredient labeling;

requirements related to the wording used for claims about nutrients, health claims, and statements of nutritional support;

labeling requirements for dietary supplements or nutritional products for which “high potency” and “antioxidant” claims are made;

notification procedures for statements on dietary supplements or nutritional products; and

premarket notification procedures for new dietary ingredients in nutritional supplements.

The Dietary Supplement Health and Education Act of 1994 (DSHEA) revised the provisions of the Federal Food, Drug and Cosmetic Act concerning the composition and labeling of dietary supplements and defined dietary supplements to include vitamins, minerals, herbs, amino acids and other dietary substances used to supplement diets. DSHEA generally provides a regulatory framework to help ensure safe, quality dietary supplements and the dissemination of accurate information about such products. The FDA is generally prohibited from regulating active ingredients in dietary supplements as drugs unless product claims, such as claims that a product may heal, mitigate, cure or prevent an illness, disease or malady, trigger drug status.

In December 2006, the Dietary Supplement and Nonprescription Drug Consumer Protection Act was passed, which further revised the provisions of the Federal Food, Drug and Cosmetic Act. Under the new act, manufacturers, packers or distributors whose name appears on the product label of a dietary supplement or nonprescription drug are required to include contact information on the product label for consumers to use in reporting adverse events associated with the product’s use and to notify the FDA of any serious adverse event report within 15 business days of receiving such report. Events reported to the FDA would not be considered an admission from a company that its product caused or contributed to the reported event. The new act becomes effective in December 2007. The FDA is in the process of developing industry guidance on how to comply with this new law. We are committed to meeting or exceeding the provisions of this act on a timely basis.

We are also subject to a variety of other regulations in the United States, including those relating to bioterrorism, taxes, labor and employment, import and export, the environment and intellectual property.

Our operations outside the United States are similarly regulated by various agencies and entities in the countries in which we operate and in which our products are sold. The regulations of these countries may conflict with those in the United States and may vary from country to country. The sale of our products in certain European countries is subject to the rules and regulations of the European Union, which may be interpreted differently among the countries within the European Union. In markets outside the United States, we may be required to obtain approvals, licenses or certifications from a country’s ministry of health or comparable agency before we begin operations or the marketing of products in that country. Approvals or licenses may be conditioned on reformulation of our products for a particular market or may be unavailable for certain products or product ingredients. These regulations may limit our ability to enter certain markets outside the United States.

Intellectual Property

Trademarks. We have developed and use registered trademarks in our business, particularly relating to corporate, brand and product names. We own 2128 trademark registrations in the United States and have sixfive trademark applications pending with the United States Patent and Trademark Office. Federal registration of a trademark enables the registered owner of the mark to bar the unauthorized use of the registered mark in connection with a similar productproducts in the same channels of trade by any third party anywhere in the United States, regardless of whether the registered owner has ever used the trademark in the area where the unauthorized use occurs.

We have filed applications and own trademark registrations and intend to register additional trademarks in foreign countries where our products are or may be sold in the future. We have one trademark application filedregistered with the Japan TrademarkPatent Office.

We also claim ownership and protection of certain product names, unregistered trademarks and service marks under common law. Common law trademark rights do not provide the same level of protection afforded by registration of a trademark. In addition, common law trademark rights are limited to the geographic area in which the trademark is actually used. We believe these trademarks, whether registered or claimed under common law, constitute valuable assets, adding to our recognition and the marketing of our products and that these proprietary rights have been and will continue to be important in enabling us to compete.

Trade Secrets. We own certain intellectual property, including trade secrets that we seek to protect, in part, through confidentiality agreements with employees and other parties. Although we regard our proprietary technology, trade secrets, trademarks and similar intellectual property as critical to our success, we rely on a combination of trade secrets, contract, patent, copyright and trademark law to establish and protect ourthe rights in our products and technology. In addition, the laws of certain foreign countries may not protect our intellectual property rights to the same extent as the laws of the United States.

Patents and Patent Licenses. We own certain United States patents. In addition, we have licensedan exclusive worldwide rightslicense to four certain United States patents, and each patent’s corresponding foreign patent application, and are currently involved in research and development of products employing the licensed inventions. These patents relate to the ingredient formerly known as “Oxford Factor”.Factor.” We are currently selling this ingredient to a customer for use in a limited market under the name of Beta-AlanineTM. We also have a nonexclusive worldwide license to five certain United States patents and are currently involved in research and development of products employing the licensed inventions.

Backlogs

Our backlog, comprised primarily of private label contract manufacturing orders, was approximately $16.0$15.1 million at September 3, 2007, and $24.3 million at September 2, 2005 and $15.8 million at September 2, 2004.2006. Our private label contract manufacturing sales are made primarily pursuant to standard purchase orders for the delivery of products. Quantities of our private label contract manufacturing products to be delivered and delivery schedules are frequently revised to reflect changes in our customers’ needs. Customer orders generally can be cancelled or rescheduled without significant penalty to the customer. For these reasons, our backlog as of any particular date is not representative of actual sales for any succeeding period, and therefore, we believe that backlog is not necessarily a good indicator of future revenue.

Working Capital Practices

We manufacture products based on anticipated demand or following receipt of customer specific purchase orders and as a result our inventory primarily consists of raw materials and work in process. Our raw material purchases are made primarily pursuant to standard purchase orders for the delivery of raw materials based upon anticipated demand. Customer specific delivery requirements, combined withcustomer cancellation or rescheduling of orders and raw material lead times impact the amount of inventory on hand at any given time. We typically purchase raw materials on 30-day payment terms. Discounts are taken periodically for early payment.

Third party branded products inventory offered in our As We Change® catalog is purchased in advance of catalog mailings to ensure products are available when the catalogs are mailed.

Sales

Private label contract manufacturing sales are typically made based upon 30-day terms. A 2% discount is provided to customers that pay within 10 days of invoice date.

RHL warrants its products for full satisfaction, generally from 30 to 120 days. Our policy requires us to replace the product or refund the purchase price to the customer.

Employees

As of June 30, 2005,2007, we employed 208240 full-time employees in the United States, sixfive of whom held executive management positions. Of the remaining full-time employees, 3244 were employed in research, laboratory and quality control, 1134 in sales and marketing, and 159157 in manufacturing and administration. From time to time we use temporary personnel to help us meet short-term operating requirements. These positions typically are in manufacturing and manufacturing support. As of June 30, 2005,2007, we had 5071 temporary personnel.

As of June 30, 2005,2007, NAIE employed an additional 25 full-time employees. Most of these positions are in the areas of manufacturing and manufacturing support.

Our employees are not represented by a collective bargaining agreement and we have not experienced any work stoppages as a result of labor disputes. We believe our relationship with our employees is good.

Seasonality

WeAlthough we believe there is no material impact on our business or results of operations from seasonal factors.

factors, we have experienced and expect to continue to experience variations in quarterly net sales due to the timing of private label contract manufacturing orders and variations in product offerings included in our As We Change® catalog.

Financial Information about Our Business SegmentSegments and Geographic Areas

Following our acquisition of RHL on December 5, 2005 through June 30, 2006, our business consisted of two segments identified as NAI, which primarily provides private label contract manufacturing services to companies that market and distribute nutritional supplements and other health care products, and RHL, which markets and distributes branded nutritional supplements and other lifestyle products.

Effective July 1, 2006, we changed our reporting segments to reflect the structure of our organization after the integration of previously outsourced fulfillment and call center activities for our Dr. Cherry Pathway to Healing®product line into RHL’s existing operations. The new reportable segments are as follows:

Private label contract manufacturing, in which we primarily provide manufacturing services to companies that market and distribute nutritional supplements and other health care products; and

Branded products, in which we market and distribute branded nutritional supplements and other lifestyle products in the following distribution channels:

• | Direct-to-consumer marketing programs, under which we develop, manufacture and market our own products and work with nationally recognized physicians and others to develop brand name products that reflect their individual approaches to restoring, maintaining or improving health. These products are sold through a variety of distribution channels, including television programs, print media and the internet. The Dr. Cherry Pathway to Healing®product line is sold under a direct-to-consumer marketing program; |

• | Food, Drug and Mass Market (FDM) retail channel in which we sell the Real Health® Laboratories nutritional supplement product line; and |

• | As We Change® (AWC) catalog, a lifestyle catalog geared towards women between the ages of 45 and 65, in which we sell our own branded products as well as third party products. The quarterly print catalog offers a variety of high quality nutritional, beauty, skin care, exercise, lifestyle and other personal care products. |

Our business consists of one industry segment, the development,private label contract manufacturing marketing and distribution of nutritional supplements. Our products are sold both withinin the United States and in markets outside the United States, including Europe, Australia and Japan. OurThe primary market outside the United States is Europe.

For the last three fiscal years, net sales by geographic region were as follows (dollars in thousands):

| Fiscal 2005 | Fiscal 2004 | Fiscal 2003 | |||||||

Net Sales | |||||||||

United States | $ | 67,784 | $ | 56,350 | $ | 41,838 | |||

Markets Outside the United States | 23,708 | 22,184 | 14,124 | ||||||

Total Net Sales | $ | 91,492 | $ | 78,534 | $ | 55,962 | |||

The allocation of net sales between the United States and markets outside the United States is based on the location of the customers. Products manufactured by NAIE accounted for 46% of net sales in markets outside the United States in fiscal 2005, 42% in fiscal 2004 and 51% in fiscal 2003. No Our branded products manufactured by NAIE wereare only sold in the United States during the last three fiscal years.States.

For additional financial information, including financial information about our business segment and geographic areas, please see the consolidated financial statements and accompanying notes to the consolidated financial statements included under Item 8 of this report.

As we continue to expand intoOur activities in markets outside the United States we will become increasinglyare subject to political, economic and other risks in the countries in which theour products are sold and in which we operate. For more information about these and other risks, please see Items 1A, 7 and 7A in this report.

| ITEM 1A. | RISK FACTORS |

You should carefully consider the risks described below, as well as the other information in this report, when evaluating our business and future prospects. If any of the following risks actually occur, our business, financial condition and results of operations could be seriously harmed. In that event, the market price of our common stock could decline and you could lose all or a portion of the value of your investment in our common stock.

Because we derive a significant portion of our revenues from a limited number of customers, our revenues would be adversely affected by the loss of a major customer or a significant change in its business, personnel or the timing or amount of its orders.

We have in the past and expect to continue to derive a significant portion of our revenues from a relatively limited number of customers. During the fiscal year ended June 30, 2007, sales to one customer, NSA International, Inc., were approximately 40% of our total net sales. Our second largest customer was Mannatech, Incorporated, which accounted for approximately 31% of our net sales during fiscal 2007. The loss of one of these customers or other major customers, a significant decrease in sales or the growth rate of sales to these customers, or a significant change in their business or personnel, would materially affect our financial condition and results of operations. Furthermore, the timing of our customers’ orders is impacted by their marketing programs, supply chain management, entry into new markets and new product introductions, all of which are outside of our control. All of these attributes have had and will have a significant impact on our business. Based on press releases issued by Mannatech, Incorporated, Mannatech achieved record sales in each of its fiscal years ended December 31, 2006, 2005 and 2004. While Mannatech similarly reported record sales for its second quarter ended June 30, 2007, based on disclosures in its quarterly report on Form 10-Q for such quarter filed with the SEC, it’s outlook for the remainder of 2007 is uncertain due to certain negative publicity and heightened litigation and regulatory activities that have affected or may affect recruiting efforts and sales in the near term. Thus, there can be no assurance that its prior sales levels will continue.

Our future growth and stability depends, in part, on our ability to diversify our sales. Our efforts to establish new products, brands, markets and customers could require significant initial investments, which may or may not result in higher sales and improved financial results.

Our business strategy depends in large part on our ability to develop new products, marketing strategies, brands and customer relationships. These activities often require a significant up-front investment including, among others, customized formulations, regulatory compliance, product registrations, package design, product testing, pilot production runs, marketing, brand development and the build up of initial inventory. We may experience significant delays from the time we increase our operating expenses and make investments in inventory until the time we generate net sales from new products or customers, and it is possible that we may never generate any revenue from new products or customers after incurring such expenditures. If we incur significant expenses and investments in inventory that we are not able to recover, and we are not able to compensate for those expenses, our operating results could be adversely affected.

On December 5, 2005, we acquired RHL and may, in the future, pursue acquisitions of other companies that, if not successful, could adversely affect our business, financial condition and results of operations.

On December 5, 2005, we completed our acquisition of RHL, an integrated direct marketer of nutritional supplements and other lifestyle products. RHL’s business is subject to all of the operational risks that normally arise for a direct marketing company, including those related to competition, profitability, economic conditions, suppliers, customers, adverse publicity, product liability claims and other litigation, regulation, personnel, and intellectual property rights.

In the future, we may pursue additional acquisitions of other companies as part of our strategy focused on long-term growth and diversification of sales and our customer base. Acquisitions, including the RHL acquisition, involve numerous risks, including:

potential difficulties related to integrating the products, personnel and operations of the acquired company;

failure to operate as a combined organization utilizing common information and communication systems, operating procedures, financial controls and human resources practices;

diverting management’s attention from the normal daily operations of the business;

entering markets in which we have no or limited prior direct experience and where competitors in such markets have stronger market positions;

potential loss of key employees of the acquired company;

potential inability to achieve cost savings and other potential benefits expected from the acquisition;

an uncertain sales and earnings stream from the acquired company; and

| ��� | potential impairment charges, which may be significant, against goodwill and purchased intangible assets acquired in the acquisition due to changes in conditions and circumstances that occur after the acquisition, many of which may be outside of our control. |

There can be no assurance that our acquisition of RHL or other acquisitions that we may pursue will be successful. If we pursue an acquisition but are not successful in completing it, or if we complete an acquisition but are not successful in integrating the acquired company’s employees, products or operations successfully, our business, financial position or results of operations could be adversely affected.

We are required to assess the value of goodwill annually for potential impairment, which requires, among others, significant management judgment to forecast future operating results used in the determination. In the fourth quarter of fiscal 2007, we recorded a $7.0 million non-cash, goodwill impairment charge and may, in the future, be required to recognize additional impairment charges, which could be significant, against goodwill and purchased intangible assets due to changes in conditions and circumstances, many of which may be outside of our control.

Following the acquisition of RHL on December 5, 2005, we recorded approximately $7.5 million of goodwill. In the fourth quarter of fiscal 2007, we recorded a $7.0 million non-cash, goodwill impairment charge as a result of our annual testing of goodwill. There can be no assurance that an additional non-cash impairment charge will not be required. Any such additional charge could have a negative effect on our results of operations but would not impact our cash flows or cash position.

Our operating results will vary and there is no guarantee that we will earn a profit. Fluctuations in our operating results may adversely affect the share price of our common stock.

While our net sales and income from operations have been relatively positive during the past three fiscal years, when compared to prior periods, there can be no assurance that our net sales will improve in the near term, or that we will earn a profit in any given year. We have experienced losses in the past and may incur losses in the future. Our operating results will fluctuate from year to year and/or from quarter to quarter due to various factors including differences related to the timing of revenues and expenses for financial reporting purposes and other factors described in this report. At times, these fluctuations may be significant. Fluctuations in our operating results may adversely affect the share price of our common stock.

A significant or prolonged economic downturn could have a material adverse effect on our results of operations.

Our results of operations are affected by the level of business activity of our customers, which in turn is affected by the level of consumer demand for their products. A significant or prolonged economic downturn may adversely affect the disposable income of many consumers and may lower demand for the products we produce for our private label contract manufacturing customers, as well as our branded products. A decline in consumer demand and the level of business activity of our customers due to economic conditions could have a material adverse effect on our revenues and profit margins.

Because our direct-to-consumer sales rely on the marketability of key personalities, the inability of a key personality to perform his or her role or the existence of negative publicity surrounding a key personality may adversely affect our revenues.

For the fiscal year ended June 30, 2007, our direct-to-consumer products accounted for approximately 7% of our net sales. These products may be marketed with a key personality through a variety of distribution channels. The inability or failure of a key personality to fulfill his or her role, or the ineffectiveness of a key personality as a spokesperson for a product, a reduction in the exposure of a key personality due to the discontinuance of a marketing program or otherwise or negative publicity about a key personality may adversely affect the sales of our product associated with that personality and could affect the sale of other products. A decline in sales would negatively affect our results of operations and financial condition.

Our industry is highly competitive and we may be unable to compete effectively. Increased competition could adversely affect our financial condition.

The market for our products is highly competitive. Many of our competitors are substantially larger and have greater financial resources and broader name recognition than we do. Our larger competitors may be able to devote greater resources to research and development, marketing and other activities that could provide them with a competitive advantage. Our market has relatively low entry barriers and is highly sensitive to the introduction of new products that may rapidly capture a significant market share. Increased competition could result in price reductions, reduced gross profit margins or loss of market share, any of which could have a material adverse effect on our financial condition and results of operations. There can be no assurance that we will be able to compete in this intensely competitive environment.

We may not be able to raise additional capital or obtain additional financing if needed.

Our cash from operations may not be sufficient to meet our working capital needs and/or to implement our business strategies. Although we amended our credit facility to increase our working capital line of credit to $12.0 million, there can be no assurance that this line of credit will be sufficient to meet our needs. Furthermore, if we fail to maintain certain loan covenants we may no longer have access to the credit line. The credit line terminates in November 2008. As a result, we may need to raise additional capital or obtain additional financing.

At any given time it may be difficult for companies to raise capital due to a variety of factors, some of which may be outside a company’s control, including a tightening of credit markets, overall poor performance of stock markets, and/or an economic slowdown in the United States or other countries. Thus, there is no assurance we would be able to raise additional capital if needed. To the extent we do raise additional capital, the ownership position of existing stockholders could be diluted. Similarly, there can be no assurance that additional financing will be available if needed or that it will be available on favorable terms. Under the terms of our credit facility, there are limits on our ability to create, incur or assume additional indebtedness without the approval of our lender.

Our inability to raise additional capital or to obtain additional financing if needed would negatively affect our ability to implement our business strategies and meet our goals. This, in turn, would adversely affect our financial condition and results of operations.

The failure of our suppliers to supply quality materials in sufficient quantities, at a favorable price, and in a timely fashion could adversely affect the results of our operations.

We buy our raw materials from a limited number of suppliers. During fiscal 2007, approximately 39% of our total raw material purchases were from three suppliers. The loss of any of our major suppliers or of a supplier that provides any hard to obtain materials could adversely affect our business operations. Although we believe that we could establish alternate sources for most of our raw materials, any delay in locating and establishing relationships with other sources could result in product shortages, with a resulting loss of sales and customers. In certain situations we may be required to alter our products or to substitute different materials from alternative sources.

We rely solely on one supplier to process certain raw materials that we use in the product line of our largest customer. The loss of or unexpected interruption in this service would materially adversely affect our results of operations and financial condition.

A shortage of raw materials or an unexpected interruption of supply could also result in higher prices for those materials. Although we may be able to raise our prices in response to significant increases in the cost of raw materials, we may not be able to raise prices sufficiently or quickly enough to offset the negative effects of the cost increases on our results of operations.

There can be no assurance that suppliers will provide the quality raw materials needed by us in the quantities requested or at a price we are willing to pay. Because we do not control the actual production of these raw materials, we are also subject to delays caused by interruption in production of materials based on conditions outside of our control, including weather, transportation interruptions, strikes and natural disasters or other catastrophic events.

Our business is subject to the effects of adverse publicity, which could negatively affect our sales and revenues.

Our business can be affected by adverse publicity or negative public perception about our industry, our competitors, or our business generally. This adverse publicity may include publicity about the nutritional supplements industry generally, the efficacy, safety and quality of nutritional supplements and other health care products or ingredients in general or our products or ingredients specifically, and regulatory investigations, regardless of whether these investigations involve us or the business practices or products of our competitors. There can be no assurance that we will be able to avoid any adverse publicity or negative public perception in the future. Any adverse publicity or negative public perception will likely have a material adverse effect on our business, financial condition and results of operations. Our business, financial condition and results of operations also could be adversely affected if any of our products or any similar products distributed by other companies are alleged to be or are proved to be harmful to consumers or to have unanticipated health consequences.

We could be exposed to product liability claims or other litigation, which may be costly and could materially adversely affect our operations.

We could face financial liability due to product liability claims if the use of our products results in significant loss or injury. Additionally, the manufacture and sale of our products involves the risk of injury to consumers from tampering by unauthorized third parties or product contamination. We could be exposed to future product liability claims that, among others: our products contain contaminants; we provide consumers with inadequate instructions about product use; or we provide inadequate warning about side effects or interactions of our products with other substances.

We maintain product liability insurance coverage, including primary product liability and excess liability coverage. The cost of this coverage has increased dramatically in recent years, while the availability of adequate insurance coverage has decreased. While we currently expect to be able to continue our product liability insurance, there can be no assurance that we will in fact be able to continue such insurance coverage, that our insurance will be adequate to cover any liability we may incur, or that our insurance will continue to be available at an economically reasonable cost.

Additionally, it is possible that one or more of our insurers could exclude from our coverage certain ingredients used in our products. In such event, we may have to stop using those ingredients or rely on indemnification or similar arrangements with our customers who wish to continue to include those ingredients in their products. A substantial increase in our product liability risk or the loss of customers or product lines could have a material adverse effect on our results of operations and financial condition.

If we or our private label contract manufacturing customers expand into additional markets outside the United States or our or their sales in markets outside the United States increase, our business would become increasingly subject to political, economic, regulatory and other risks in those markets, which could adversely affect our business.

Our future growth may depend, in part, on our ability and the ability of our private label contract manufacturing customers to expand into additional markets outside the United States or to improve sales in markets outside the United States. There can be no assurance that we or our customers will be able to expand in existing markets outside

the United States, enter new markets on a timely basis, or that new markets outside the United States will be profitable. There are significant regulatory and legal barriers in markets outside the United States that must be overcome. We will be subject to the burden of complying with a wide variety of national and local laws, including multiple and possibly overlapping and conflicting laws. We also may experience difficulties adapting to new cultures, business customs and legal systems. Our sales and operations outside the United States are subject to political, economic and social uncertainties including, among others:

changes and limits in import and export controls;

increases in custom duties and tariffs;

changes in government regulations and laws;

coordination of geographically separated locations;

absence in some jurisdictions of effective laws to protect our intellectual property rights;

changes in currency exchange rates;

economic and political instability; and

currency transfer and other restrictions and regulations that may limit our ability to sell certain products or repatriate profits to the United States.

Any changes related to these and other factors could adversely affect our business, profitability and growth prospects. If we or our customers expand into additional markets outside the United States or improve sales in markets outside the United States, these and other risks associated with operations outside the United States are likely to increase.

Our products and manufacturing activities are subject to extensive government regulation, which could limit or prevent the sale of our products in some markets and could increase our costs.

The manufacturing, packaging, labeling, advertising, promotion, distribution, and sale of our products are subject to regulation by numerous national and local governmental agencies in the United States and in other countries. Failure to comply with governmental regulations may result in, among other things, injunctions, product withdrawals, recalls, product seizures, fines, and criminal prosecutions. Any action of this type by a governmental agency could materially adversely affect our ability to successfully market our products. In addition, if the governmental agency has reason to believe the law is being violated (for example, if it believes we do not possess adequate substantiation for product claims), it can initiate an enforcement action. Governmental agency enforcement could result in orders requiring, among other things, limits on advertising, consumer redress, divestiture of assets, rescission of contracts, and such other relief as may be deemed necessary. Violation of these orders could result in substantial financial or other penalties. Any action by the governmental agency could materially adversely affect our ability and our customers’ ability to successfully market those products.

In markets outside the United States, before commencing operations or marketing our products, we may be required to obtain approvals, licenses, or certifications from a country’s ministry of health or comparable agency. Approvals or licensing may be conditioned on reformulation of products or may be unavailable with respect to certain products or product ingredients. We must also comply with product labeling and packaging regulations that vary from country to country. Furthermore, the regulations of these countries may conflict with those in the United States and with each other. The sale of our products in certain European countries is subject to the rules and regulations of the European Union, which may be interpreted differently among the countries within the European Union. The cost of complying with these various and potentially conflicting regulations can be substantial and can adversely affect our results of operations.

We cannot predict the nature of any future laws, regulations, interpretations, or applications, nor can we determine what effect additional governmental regulations, when and if adopted, would have on our business. They could include requirements for the reformulation of certain products to meet new standards, the recall or discontinuance of certain products, additional record keeping, expanded or different labeling, and additional scientific substantiation. Any or all of these requirements could have a material adverse effect on our operations.

If we are unable to attract and retain qualified management personnel, our business will suffer.

Our executive officers and other management personnel are primarily responsible for our day-to-day operations. We believe our success depends largely on our ability to attract, maintain and motivate highly qualified management personnel. Competition for qualified individuals can be intense, and we may not be able to hire additional qualified personnel in a timely manner and on reasonable terms. Our inability to retain a skilled professional management team could adversely affect our ability to successfully execute our business strategies and achieve our goals.

Our manufacturing, fulfillment and call center activities are subject to certain risks.

We manufacture the vast majority of our products at our manufacturing facility in California and our fulfillment and call center activities are centralized at RHL’s facility. As a result, we are dependent on the uninterrupted and efficient operation of these facilities, which are located within approximately 45 miles of each other in the San Diego area of Southern California. Our manufacturing, fulfillment and call center operations are subject to power failures, blackouts, the breakdown, failure or substandard performance of equipment, the improper installation or operation of equipment, natural or other disasters, and the need to comply with the requirements or directives of governmental agencies, including the FDA. In addition, we may in the future determine to expand or relocate our facilities, which may result in slow downs or delays in our operations. While we have implemented and are evaluating various emergency, contingency and disaster recovery plans and maintain business interruption insurance, there can be no assurance that the occurrence of these or any other operational problems at our facilities in California or at NAIE’s facility in Switzerland would not have a material adverse effect on our business, financial condition and results of operations. Furthermore, there can be no assurance that our contingency plans will prove to be adequate or successful if needed or that our insurance will continue to be available at a reasonable cost or, if available, will be adequate to cover any losses that we may incur from an interruption in our manufacturing and distribution operations.

We may be unable to protect our intellectual property rights or may inadvertently infringe on the intellectual property rights of others.

We possess and may possess in the future certain proprietary technology, trade secrets, trademarks, tradenames, licenses and similar intellectual property. There can be no assurance that we will be able to protect our intellectual property adequately. In addition, the laws of certain foreign countries may not protect our intellectual property rights to the same extent as the laws of the United States. Litigation in the United States or abroad may be necessary to enforce our intellectual property rights, to determine the validity and scope of the proprietary rights of others or to defend against claims of infringement. This litigation, even if successful, could result in substantial costs and diversion of resources and could have a material adverse effect on our business, results of operation and financial condition. If any such claims are asserted against us, we may seek to obtain a license under the third party’s intellectual property rights. There can be no assurance, however, that a license would be available on terms acceptable or favorable to us, if at all.

Collectively, our officers and directors own a significant amount of our common stock, giving them influence over corporate transactions and other matters and potentially limiting the influence of other stockholders on important policy and management issues.

Our officers and directors, together with their families and affiliates, beneficially owned approximately 24% of our outstanding shares of common stock as of June 30, 2007, including approximately 19% of our outstanding shares of common stock beneficially owned by Mark LeDoux, our Chief Executive Officer and the Chairman of the Board, and his family and affiliates. As a result, our officers and directors, and in particular Mr. LeDoux, could influence such business matters as the election of directors and approval of significant corporate transactions.

Various transactions could be delayed, deferred or prevented without the approval of stockholders, including:

transactions resulting in a change in control;

mergers and acquisitions;

tender offers;

election of directors; and

proxy contests.

There can be no assurance that conflicts of interest will not arise with respect to the officers and directors who own shares of our common stock or that conflicts will be resolved in a manner favorable to us or our other stockholders.

If our information technology system fails, our operations could suffer.

Our business depends to a large extent on our information technology infrastructure to effectively manage and operate many of our key business functions, including order processing, customer service, product manufacturing and distribution, cash receipts and payments and financial reporting. A long term failure or impairment of any of our information technology systems could adversely affect our ability to conduct day-to-day business.

If certain provisions of our Certificate of Incorporation, Bylaws and Delaware law are triggered, the future price investors might be willing to pay for our common stock could be limited.

Certain provisions in our Certificate of Incorporation, Bylaws and Delaware corporate law help discourage unsolicited proposals to acquire our business, even if the proposal would benefit our stockholders. Our Board of Directors is authorized, without stockholder approval, to issue up to 500,000 shares of preferred stock having such rights, preferences, and privileges, including voting rights, as the Board of Directors designates. The rights of our common stockholders will be subject to, and may be adversely affected by, the rights of holders of any preferred stock that may be issued in the future. Any or all of these provisions could delay, deter or prevent a takeover of our company and could limit the price investors are willing to pay for our common stock.

Our stock price could fluctuate significantly.

Stock prices in general have been historically volatile and ours is no different. The trading price of our stock may fluctuate in response to:

broad market fluctuations and general economic and/or political conditions;

fluctuations in our financial results;

relatively low trading volumes;

future offerings of our common stock or other securities;

the general condition of the nutritional supplement or lifestyle product industries;

increased competition;

regulatory action;

adverse publicity;

manipulative or illegal trading practices by third parties; and

product and other public announcements.

The stock market has historically experienced significant price and volume fluctuations. There can be no assurance that an active market in our stock will continue to exist or that the price of our common stock will not decline. Our future operating results may be below the expectations of securities analysts and investors. If this were to occur, the price of our common stock would likely decline, perhaps substantially.

From time to time our shares may be listed for trading on one or more foreign exchanges, with or without our prior knowledge or consent. Certain foreign exchanges may have less stringent listing requirements, rules and enforcement procedures than the Nasdaq Global Market or other markets in the United States, which may increase the potential for manipulative trading practices to occur. These practices, or the perception by investors that such practices could occur, may increase the volatility of our stock price or result in a decline in our stock price, which in some cases could be significant.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

Not applicable.

| ITEM 2. | PROPERTIES |

This table summarizes our facilities as of June 30, 2005.2007. We believe our facilities are adequate to meet our operating requirements for the foreseeable future.

Location | Nature of Use | Square Feet | How Held | Lease Expiration

| ||||

San Marcos, CA USA | Owned/leased | Various | ||||||

Vista, CA USA(1) | Manufacturing, warehousing, packaging and distribution | 162,000 | Leased | March 2014 | ||||

Manno, Switzerland | Manufacturing, warehousing, packaging and distribution | Leased | December 2015 | |||||

San Diego, CA USA(3) | RHL headquarters, warehousing, call center and fulfillment | 16,000 | Leased | May 2009 | ||||

| (1) | This facility is used by NAI primarily for its private label contract manufacturing segment. |

| (2) | This facility is used by NAIE, our wholly owned Swiss |

| This facility is used primarily by RHL, our wholly owned subsidiary, for our branded products segment. |

| (4) | We expect to renew our leases in the normal course of |

| We use approximately 93,000 square feet for |

| We own approximately 29,500 square feet and lease the remaining 10,800 square feet. The lease for approximately 8,000 square feet terminates in February 2008 and the lease for the remaining space |

| ITEM 3. | LEGAL PROCEEDINGS |

From time to time, we become involved in various investigations, claims and legal proceedings that arise in the ordinary course of our business. These matters may relate to product liability, employment, intellectual property, tax, regulation, contract or other matters. The resolution of these matters as they arise will be subject to various uncertainties and, even if such claims are without merit, could result in the expenditure of significant financial and managerial resources. While unfavorable outcomes are possible, based on available information, we generally do not believe the resolution of these matters including that discussed below, will result in a material adverse effect on our business, consolidated financial condition, or results of operation. However, a settlement payment or unfavorable outcome could adversely impact our results of operation. Our evaluation of the likely impact of these actions including that discussed below, could change in the future and we could have unfavorable outcomes that we do not expect.

On February 10, 2005, a complaint was filed against NAI on behalf of Novogen Research Pty. Ltd. in the United States District Court, Southern District of New York alleging a cause of action for patent infringement of a Novogen patent by products manufactured by NAI. The parties are attempting to resolve the matter in an out-of-court settlement but if we are unable to do so we intend to vigorously defend the action.

As of September 8, 2005, other than as set forth above,October 15, 2007, neither NAI nor its subsidiaries were a party to any material pending legal proceeding nor was any of their property the subject of any material pending legal proceeding.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

We did not submit any matters to our stockholders for a vote during the fourth quarter ended June 30, 2005.

2007.

ITEM 5. MARKET FOR OUR COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

| ITEM 5. | MARKET FOR OUR COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Information

Our common stock trades on the Nasdaq NationalGlobal Market under the symbol “NAII.” Below are the high and low closing prices of our common stock as reported on the Nasdaq NationalGlobal Market for each quarter of the fiscal years ended June 30, 20052007 and 2004:2006:

| Fiscal 2005 | Fiscal 2004 | |||||||||||

| High | Low | High | Low | |||||||||

First Quarter | $ | 9.65 | $ | 6.32 | $ | 5.47 | $ | 4.68 | ||||

Second Quarter | $ | 11.46 | $ | 7.88 | $ | 6.41 | $ | 4.70 | ||||

Third Quarter | $ | 9.85 | $ | 6.37 | $ | 9.60 | $ | 6.20 | ||||

Fourth Quarter | $ | 8.21 | $ | 6.75 | $ | 13.80 | $ | 7.27 | ||||

| Fiscal 2007 | Fiscal 2006 | |||||||||||

| High | Low | High | Low | |||||||||

First Quarter | $ | 10.84 | $ | 7.77 | $ | 8.25 | $ | 6.64 | ||||

Second Quarter | $ | 9.25 | $ | 8.37 | $ | 6.80 | $ | 5.27 | ||||

Third Quarter | $ | 9.26 | $ | 7.90 | $ | 8.54 | $ | 6.34 | ||||

Fourth Quarter | $ | 8.22 | $ | 7.05 | $ | 10.86 | $ | 8.00 | ||||

In addition to the Nasdaq NationalGlobal Market, our shares are also listed for trading on the Berlin-Bremen Stock Exchange, the Frankfurt Stock Exchange, and the XETRA Stock Exchange, each of which is a foreign exchange located in Germany. We are not aware of any other exchanges on which our shares are traded.

Holders

As of September 8, 2005,October 15, 2007, there were approximately 360317 stockholders of record of our common stock.

Dividends

We have never paid a dividend on our common stock and we do not intend to pay a dividend in the foreseeable future. Our current policy is to retain all earnings to help provide funds for future growth. Additionally, under the terms of our credit facility, we are precluded from paying a dividend.

Recent Sales of Unregistered Securities

During the fiscal year ended June 30, 2005,2007, we did not sell any unregistered securities.

Repurchases

During the fourth quarter of the fiscal 2005,year ended June 30, 2007, we did not repurchase any shares of our common stock, nor were any repurchases made on our behalf.

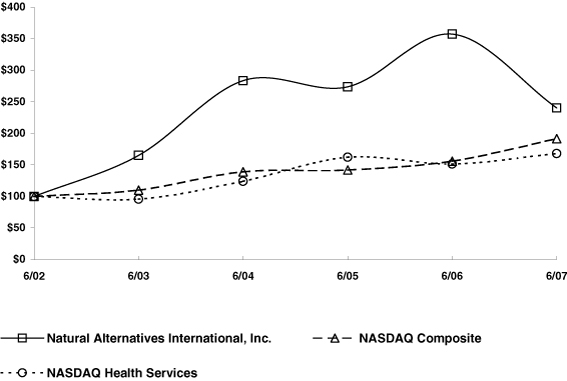

Performance Graph

The graph below provides a comparison of cumulative total returns for our common stock, the Nasdaq Composite Index, and the Nasdaq Health Services Index for the five year period ended June 30, 2007. The graph assumes an investment of $100 on June 30, 2002 in each of our common stock, and the stock comprising the Nasdaq Composite Index and the Nasdaq Health Services Index. Each of the indices assumes that all dividends were reinvested. The graph lines merely connect the prices on the dates indicated and do not reflect fluctuations between those dates.

The stock performance shown above is not indicative of future performance.

The performance information above is not deemed to be filed with the SEC or subject to the liabilities of Section 18 of the Securities Exchange Act of 1934, as amended, and shall not be deemed incorporated by reference by any general statement incorporating by reference this report into any filing with the SEC, except to the extent we specifically incorporate this information by reference.

ITEM 6. SELECTED FINANCIAL DATA

| ITEM 6. | SELECTED FINANCIAL DATA |