UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

FOR ANNUAL AND TRANSITION REPORTS

PURSUANT TO SECTIONS 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended June 30, 20052007

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to.

Commission file number 0-25259

BOTTOMLINE TECHNOLOGIES (de), INC.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 02-0433294 | |

(State or Other Jurisdiction Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

325 Corporate Drive Portsmouth, New Hampshire | 03801 | |

| (Address of Principal Executive Offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (603) 436-0700

Securities registered pursuant to Section 12(b) of the Act: None

Title of each class: | Name of each exchange on which registered: | |

Common Stock, $.001 par value per share | The NASDAQ Global Market |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $.001 par value per share

(Title of Class) None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, (as definedor a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act Rule 12b-2). Yes(Check one):

Large accelerated filer ¨ Accelerated filer x NoNon-accelerated filer ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.): Yes ¨ No x

The aggregate market value of the voting stock held by non-affiliates of the registrant, based on the last sale price of the registrant’s common stock at the close of business on December 31, 20042006 was $192,646,459$264,628,793 (reference is made to Part II, Item 5 herein for a statement of assumptions upon which this calculation is based). The registrant has no non-voting stock.

There were 22,457,99324,614,538 shares of common stock, $.001 par value per share, of the registrant outstanding as of August 31, 2005.

2007.

DOCUMENTS INCORPORATED BY REFERENCE

Items 10, 11, 12, 13 and 14 of Part III (except for information required with respect to our executive officers, which is set forth under “Part I—Executive Officers and Other Key Employees of the Registrant”) have been omitted from this report, as we expect to file with the Securities and Exchange Commission, not later than 120 days after the close of our fiscal year ended June 30, 2005,2007, a definitive proxy statement for our 2007 annual meeting of stockholders. The information required by Items 10, 11, 12, 13 and 14 of Part III of this report, which will appear in our definitive proxy statement, is incorporated by reference into this report.

This Annual Report on Form 10-K contains forward-looking statements that involve risks and uncertainties. Any statements (including statements to the effect that we “believe,” “expect,” “anticipate,” “plan” and similar expressions) that are not statements relating to historical matters should be considered forward-looking statements. Our actual results may differ materially from the results discussed in the forward-looking statements as a result of numerous important factors, including those discussed in “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Certain Factors That May Affect Future Results.”“Item 1A. Risk Factors”.

| Item 1. | Business. |

Our Company

We provide software products and services for business paymentselectronic payment and invoice management.solutions to corporations, financial institutions and banks around the world. Our solutions enable organizationsare used to streamline, automate and manage standardizeprocesses and control transaction-based processes across the enterprise, particularly those that involve makingtransactions involving global payments, sendinginvoice receipt and receiving invoices, receiving payments, generating business documentsapproval, collections, cash management, risk mitigation, reporting and conducting electronic banking.document archive. We offer software designed to run on-site at the customer’s location as well as hosted solutions. OurHistorically, our software ishas been sold predominantly on a perpetual license basis. Today, however, many of our newer offerings are sold on both a licensesubscription and subscriptiontransaction basis.

Our offerings include software solutions that banks use to provide web-based payment and reporting capability to their corporate customers. We also provide a hosted solution, Legal eXchange, that receives, manages and controls legal invoices and the related spend management for insurance companies and other large consumers of outside legal services. Our corporate customers rely on our solutions to automate their payment and accounts payable processes and to streamline and manage the production and retention of electronic documents.

Our software applications address the global payment and related process requirements of business enterprises, permitting them to achieve greater operating efficiency, increase visibility of the cash cycle and better comply with applicable regulations and standards. We support a broad range of global networks and payment standards, including Automated Clearing House (ACH), Financial Electronic Data Interchange (EDI), Fed Wire transfer, BACS (ACH for the UK), BACSTEL-IP and SWIFT, as well as new and evolving standards.

Our end-to-end productssolutions complement and leverage our customers’ existing information systems, accounting applications and banking relationships. As a result, our solutions can be deployed quickly and efficiently. To help our customers receive the maximum value from our products and meet their own particular needs, we also provide professional services for installation, training, consulting and product enhancement. Additionally, we offer our customers a broad range of equipment and supplies products that complement our software products.

Bottomline was originally organized as a New Hampshire corporation in 1989 and was reincorporated as a Delaware corporation in August 1997. We maintain our corporate headquarters in Portsmouth, New Hampshire and our international headquarters in Reading, England. We maintain a website with the address www.bottomline.com. Our website includes links to our Code of Business Conduct and Ethics, and our Audit Committee, Compensation Committee, and Nominating and Corporate Governance Committee charters. We are not including the information contained in our website as part of, or incorporating it by reference into, this Annual Report on Form 10-K. We make available free of charge, through our website, our annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, and amendments to these reports, as soon as reasonably practical after such material is electronically filed with, or furnished to, the Securities and Exchange Commission (SEC).

Our Strategy

Our objective is to be the leading global provider of business payment and invoice management software solutions and services. Key elements of our strategy include the following:

Providing software and services which enable banks to offer their corporate customers leading global payment capability and functionality;

Continuing to add customers and functionality to our growing Legal eXchange network;

Leveraging our market positionleading payment and document management software solutions for enterprise customers;

Increasing the investment in our AP Automation solutions to capitalize on growth opportunities in electronic paymentsthe new and invoice management;significant market opportunity for that offering;

Increasing the saledeployment of our hosted solutions, as well as subscription and subscription-basedtransaction based pricing, in order to increase our recurring revenue contribution;

Broadening our relationships with our existing customer base by selling existing applications, as well as newly-developed products;new product offerings, into that base; and

Pursuing strategic acquisitions that expand our geographical footprint or complement our product functionality.

Our Products and Services

PaymentsPayment and Payments Lifecycle ManagementDocument Automation

We offer payment systems capable of producingThe payments automation capabilities inherent in our WebSeries® and PayBase® solutions can produce a wide variety of domestic and international payment instructions along with consolidated bank reporting of cash activity including ACH, EDI, Fed WireFedwire transfer, BACSBACSTEL-IP and BACSTEL-IP, as well as SWIFT messaging and paper checks in most currencies. Our products helpThrough our payments automation capabilities, customers can reduce administrative expenses and strengthen controlcompliance and fraud protection. Our web-based systems cananti-fraud controls. Users are able to gather and access data via the Internet on payment and bank account information, including account totals and detailed transaction data, providing improved workflow, financial reporting and bank communications. We

To help augment financial document composition and delivery we offer Formscape, a suite of software solutions for automating purchase-to-pay, document and financial transaction processes and also offer hosted solutions that allow our customers to outsource their payment processing.

Invoice ReceiptCreate!form, a document process automation suite. Our Formscape and Invoice Presentment Management

WeCreate!form products offer web-based invoice processing systems for businesses that reduce administrative costs by allowing organizations to electronically send, receive and manage invoices.

We also offer a payer side solution, In View A/P, which electronically aggregates, formats and transfers invoice data into customers’ accounting systems. For vendors unable to provide electronic files, a browser-accessed manual payment request screen lets them create “electronic invoices” on demand. Our biller-side product, NTX, is a secure, business-to-business electronic invoice presentment and payment system that allows organizations to present invoices and invoicing information, accommodate internal workflows for review and approval, provide online dispute resolution and accept payments over the Internet.

Our legal bill receipt service, Legal eXchange, automates the receipt, reconciliation, review, approval and management of legal invoices. The Legal eXchange system incorporates a rules engine, helping to ensure that charges are in conformity with preset billing parameters.

Document Output and Archive Management

Our electronic document solution, Createform, offers advanced design, output formatting and delivery capabilities that enable customers to allow organizations to streamline their business communications by replacing pre-printedreplace paper-based forms (such as invoices, purchase orders and shipping notices) with more efficient attractive and cost-effective customized electronic documents. Our solutions allow customers toWith the capabilities of these product suites, users can centrally manage, distribute and archive businessimportant documents such as invoices, checks, statements, purchase orders and other transactional documents. These products give customers the flexibility to select the most effective means of delivery, whetherthen distribute them via the web,email, print, fax or archive,the Web.

Spend Management

Our hosted spend management solution, Legal eXchange, integrates with claims management and time and billing systems to automate legal invoice management processes and to integrate these products with existing enterprise software applications.

provide insight into all areas of a company’s outside legal spend. Legal eXchange’s combination of automated invoice routing and a sophisticated rules engine allows corporate legal and insurance claims departments to create more efficient processes for managing invoices generated by outside law firms, while offering access to important legal spend factors including budgeting, expense monitoring and outside counsel performance.

Electronic Banking

Our electronic banking solutions allowWebSeries Electronic Banking Platform allows banks and financial service providersinstitutions to deploy Internet-based services. Our software interfaces directly to a multitude of in-house systems to provide efficient application integration across one or more financial institutions. Our solutions support a variety of cash management functions, including balanceservices for their corporate clients. Based on patented technology and transaction reporting, lockbox reporting, controlled disbursements, positive pay, check imaging, stop

payments,complementary existing systems, our banking platform enables users to leverage a single Web-based interface for the origination and a broad arrayprocessing of electronic funds transfer instructions. Real-time host links enableall types of inbound and outbound domestic and international payments. The software architecture of our banking platform allows banks and financial institutions to provide their corporate customers with up-to-the-minute accessconfigure highly specialized solution sets for Enterprise Cash Management, Wholesale Banking and Retail Branch Payments using modules for ACH, International Payments, Check Management, Information Reporting, Unattended Payment and File Transmission, and Distributed Document Printing.

AP Automation

Our AP Automation solutions allow businesses and enterprises to critical data.

automate the accounts payable invoice receipt and management process and facilitate the ultimate payment. These solutions are offered on a subscription and transaction-based model. We have continued to significantly invest in the on-going development and enhancement of our AP Automation solutions to include a wider range of functionality and to enable high volume usage in a hosted environment.

Professional Services

Our teams of service professionals draw on extensive experience to provide consulting, project implementation and training services to our clients. By easing the implementation of our products, these services help our customers accelerate the time to value. By improving the overall customer experience, these services help us retain customers and drive future revenues.

revenue generating arrangements from existing customers.

Equipment and Supplies

We offer consumable products for laser check printing, including magnetic ink character recognition toner and blank-paper check stock. We also provide printers and printer-related equipment, primarily through arrangements with our hardware vendors, to complement our software product offerings.

Our Customers

We support overmore than 9,000 customers, including 3,000 that access our payment and invoice automation capabilities through convenient subscription-basedsubscription and transaction-based services. Our customers are in industries such as financial services, insurance, health care, technology, communications, education, media, manufacturing and government. We provide our products and services to approximately 6065 of the Fortune 100 companies and 90approximately 80 of the FTSE (Financial Times) 100 companies. Our customers include leading organizations such as British Airways, Cisco Systems, Citibank,Bank of America, HSBC, Australia and New Zealand Banking Group (ANZ), Franklin Templeton, GMAC, and John Deere. Our solutions include a hosted offering that automates the receipt, review and approval of legal invoices used by American International Group, Liberty Mutual, and Safeco Insurance, among others.British Airways, Vodafone and Hertz Corporation.

Our Competition

The markets in which we participate are highly competitive. We believe our ability to compete depends on factors within and beyond our control, including:

the performance, reliability, features, price and ease of use of our offerings as compared to competitor alternatives;

our industry knowledge and expertise;

the execution of our sales organizations;

our ability to secure and maintain strategic relationships;

our ability to support our customers; and

the timing and market acceptance of new products and enhancements to existing products by us and by our current and future competitors.

For corporateOur payment and invoicing solutions, wedocument automation products compete primarily with companies that provide a broad offering of electronic data interchange products, such as CheckFree, Pegasystems, Velosant and Edocs, companies that provide solutions to create, publish, manage and archive electronic documents, such as Adobe, and Optio Software, StreamServe and Xerox and companies that offer electronic payment and laser check printing software and services, such as Payformance, MHC Associates, and ACOM Solutions in the US and Microgen, Albany Software Ltd., Access EuropeDirect

Debit, Ltd., and Eiger Systems Limited in the UK.Europe. Our products also compete with companies that provide a diverse array of accounts payable automation and workflow capabilities, such as Xign (now part of JP Morgan Chase), BasWare, Digital Vision and 170 Systems. To a lesser extent, we compete with providers of enterprise resource planning solutions and providers of traditional payment products, including check stock and check printing software and services. In addition, some financial institutions compete with us as outsourced check printing and electronic payment services for their customers.

For electronic banking,Electronic Banking, we primarily compete with companies such as S1 Corporation and Digital InsightACI Worldwide that offer a wide range of financial services including electronic banking applications. We also encounter

competition to a lesser degree from Metavante, SunGard, Fundtech and Politzer and Haney,Fundtech, as well as companies that provide traditional treasury workstation solutions.

In the legal billing market,For our Legal eXchange solution, we compete with a number of companies, including DataCert, CT Corporation, VisibillityTyMetrix, LexisNexis CounselLink and Allegient Systems.

Although we believe that we compete favorably in each of the markets in which we participate, the markets for our products and services are intensely competitive and characterized by rapid technological change and a number of factors could adversely affect our ability to compete in the future, including those discussed in “Management’s Discussion and Analysis of Financial Conditions and Results of Operations—Certain Factors That May Affect Future Results”“Item 1A. Risk Factors”.

Our Operating Segments

We organize our business by segments in order to maximize market opportunities. Our operating segments are organized principally by the type of productsproduct or services offered. We have aggregated similaroffered and by geography. As of July 1, 2006 we revised the structure of our internal operating segments intoand changed the nature of the financial information that is provided to and used by our chief operating decision maker. The change in segment structure as of July 1, 2006 resulted in three reportable segments, and that change is reflected for all periods presented. Our reportable segments are as follows:

Licensed Technology.Payments and Transactional Documents.Our Licensed TechnologyPayments and Transactional Documents segment includes licensedsupplies software products that provide a range of financial business process management solutions, including making and collecting payments, sending and receiving invoices, accounts payable automation and generating and storing business documents. This segment also includesprovides an array of standard professional services and equipment and supplies that complement and enhance our core software products. Revenue associated with this segment has historically been recorded upon delivery. This segment also incorporates the Company’s check printing and accounts payable automation solutions, revenue for which is typically recorded on a per transaction basis or ratably over the expected life of the customer relationship.

Banking Solutions.The Banking Solutions segment provides solutions that are specifically designed for banking and financial institution customers. These solutions typically involve lengthy implementation periods and a significant level of customization. Due to the tailored nature of these products, revenue is generally recognized on a percentage of completion basis.

Outsourced Solutions.OurThe Outsourced Solutions segment provides customers with outsourced orand hosted solutionssolution offerings that facilitate payment processing and invoice receipt and presentment.presentment and spend management. The majority of the activity in this segment is associated with our Legal eXchange solution, which provides customers the opportunity to create more efficient processes for managing invoices generated by outside law firms while offering access to important legal spend factors such as budgeting, expense monitoring and outside counsel performance. Revenue for this segment is generally recognized on a per transaction basis or proportionatelyratably over a specified subscription period or the estimated life of the contract.customer relationship.

Tailored Solutions.Our Tailored Solutions segment includes solutions specifically designed for banking and financial institutions customers. These solutions typically involve longer implementation periods and generally require a significant level of professional services. Due to the customized nature of these products, revenue is normally recognized on a percentage of completion basis.

Each of our operating segmentssegment has a dedicated sales force and, periodically, a sales person in one operating segment will sell products orand services that are typically sold within a different operating segment. In such cases,

the transaction can beis generally recorded by the operating segment to which the sales person is assigned. Accordingly, segment results can include the results of transactions that have been allocated to a specific segment based on the contributing sales resource, rather than the nature of the product or service. As an example, a long-term, percentage of completion contract with a financial institution could be reported under the Licensed Technology segment if the sales person of record is assigned to the sales force of that segment. Conversely, a transaction can be recorded by the operating segment primarily responsible for delivery to the customer, even if the sales person is assigned to a different operating segment.

OurThe Company’s chief operating decision makers assessmaker assesses segment performance based on a variety of factors that can include segment revenue and a segment measure of profit or loss. Each segment’s measure of profit or loss is on a pre-tax basis and excludes stock compensation expense and acquisition-related expenses such as amortization of intangible assets and charges related to acquired in-process research and development and stock compensation expense associated with stock options assumed in prior business acquisitions.development. There are no inter-segment sales; accordingly the measure of segment revenue and profit or loss reflects only revenues from our external customers. The costs of certain corporate level expenses, primarily general and administrative expenses, are allocated to ourthe Company’s operating segments at predetermined rates that approximate cost.

The Company does not track or assign its assets by operating segment.

Segment information for years prior to 2004 cannot be prepared without significant allocation of resources and expense. Accordingly, we are not disclosing segment information for years prior to 2004 as it is

impracticable to do so. The following represents a summary of our reportable segments for the years ended June 30, 20042005, 2006 and 2005.2007.

| Fiscal Year Ended June 30 | ||||||||||||

| 2004 | 2005 | Change from 2004 | ||||||||||

| (in thousands) | ||||||||||||

Revenues: | ||||||||||||

Licensed Technology | $ | 58,721 | $ | 71,185 | $ | 12,464 | ||||||

Outsourced Solutions | 14,099 | 16,156 | 2,057 | |||||||||

Tailored Solutions | 9,312 | 9,164 | (148 | ) | ||||||||

Total revenues | $ | 82,132 | $ | 96,505 | $ | 14,373 | ||||||

Segment measure of profit (loss) | ||||||||||||

Licensed Technology | $ | 4,302 | $ | 7,692 | $ | 3,390 | ||||||

Outsourced Solutions | (639 | ) | 2,102 | 2,741 | ||||||||

Tailored Solutions | (1,040 | ) | (762 | ) | 278 | |||||||

Total measure of segment profit | $ | 2,623 | $ | 9,032 | $ | 6,409 | ||||||

| Fiscal Year Ended June 30, | |||||||||||

| 2005 | 2006 | 2007 | |||||||||

| (in thousands) | |||||||||||

Revenues: | |||||||||||

Payments and Transactional Documents | $ | 79,946 | $ | 77,600 | $ | 84,506 | |||||

Banking Solutions | 9,164 | 12,706 | 20,017 | ||||||||

Outsourced Solutions | 7,395 | 11,359 | 13,812 | ||||||||

Total revenues | $ | 96,505 | $ | 101,665 | $ | 118,335 | |||||

Segment measure of profit (loss): | |||||||||||

Payments and Transactional Documents | $ | 9,048 | $ | 5,784 | $ | 2,041 | |||||

Banking Solutions | (745 | ) | (1,155 | ) | 576 | ||||||

Outsourced Solutions | 729 | 2,609 | 3,561 | ||||||||

Total measure of segment profit | $ | 9,032 | $ | 7,238 | $ | 6,178 | |||||

A reconciliation of the measure of segment profit to our GAAP income (loss) for 20042005, 2006 and 2005,2007, before the provision for income taxes, is as follows:

| Fiscal Year Ended June 30, | Fiscal Year Ended June 30, | |||||||||||||||||||

| 2004 | 2005 | 2005 | 2006 | 2007 | ||||||||||||||||

| (in thousands) | (in thousands) | |||||||||||||||||||

Segment measure of profit | $ | 2,623 | $ | 9,032 | $ | 9,032 | $ | 7,238 | $ | 6,178 | ||||||||||

Less: | ||||||||||||||||||||

Amortization of intangible assets | (4,277 | ) | (3,217 | ) | (3,217 | ) | (4,491 | ) | (9,324 | ) | ||||||||||

Stock compensation expense | (41 | ) | (14 | ) | (14 | ) | (6,984 | ) | (7,945 | ) | ||||||||||

In-process research and development | (842 | ) | — | |||||||||||||||||

Acquisition related technology write-offs | — | (189 | ) | — | ||||||||||||||||

Other income, net | 288 | 444 | 444 | 3,252 | 3,177 | |||||||||||||||

Income (loss) before provision for income taxes | $ | (2,249 | ) | $ | 6,245 | $ | 6,245 | $ | (1,174 | ) | $ | (7,914 | ) | |||||||

Financial Information About Geographic Areas

Revenues, based on the point of sales, not the location of the customer, are as follows:

| Fiscal Year Ended June 30, | Fiscal Year Ended June 30, | |||||||||||||||||||||||||||||||||||

| 2003 | 2004 | 2005 | 2005 | 2006 | 2007 | |||||||||||||||||||||||||||||||

| ($ in thousands) | (in thousands) | |||||||||||||||||||||||||||||||||||

United States | $ | 40,965 | 57.5 | % | $ | 45,942 | 55.9 | % | $ | 46,527 | 48.2 | % | $ | 46,527 | 48.2 | % | $ | 54,331 | 53.5 | % | $ | 65,064 | 55.0 | % | ||||||||||||

United Kingdom | 30,300 | 42.5 | % | 34,883 | 42.5 | % | 48,300 | 50.1 | % | |||||||||||||||||||||||||||

Europe | 48,300 | 50.1 | % | 45,471 | 44.7 | % | 51,507 | 43.5 | % | |||||||||||||||||||||||||||

Australia | — | — | 1,307 | 1.6 | % | 1,678 | 1.7 | % | 1,678 | 1.7 | % | 1,863 | 1.8 | % | 1,764 | 1.5 | % | |||||||||||||||||||

Total | $ | 71,265 | 100.0 | % | $ | 82,132 | 100.0 | % | $ | 96,505 | 100.0 | % | $ | 96,505 | 100.0 | % | $ | 101,665 | 100.0 | % | $ | 118,335 | 100.0 | % | ||||||||||||

At June 30, 2005, long-livedLong-lived assets, of $21.6 millionwhich are based on geographical designation, were located in the US, $24.9 million were located in the UK and $133,000 were located in Australia. At June 30, 2004, long-lived assets of $24.2 million were located in the US, $17.7 million were located in the UK and $106,000 were located in Australia.as follows:

Fiscal Year Ended June 30, | ||||||

| 2006 | 2007 | |||||

| (in thousands) | ||||||

Long-lived assets: | ||||||

United States | $ | 4,169 | $ | 4,664 | ||

Europe | 3,970 | 5,195 | ||||

Australia | 214 | 195 | ||||

Total long-lived assets | $ | 8,353 | $ | 10,054 | ||

A significant and growing percentage of our revenues have been generated by our international operations. Ouroperations and our future growth rates and success are in part dependent on our continued growth and success in international

markets. As is the case with most international operations, the success and profitability of these operations is subject to numerous risks and uncertainties including currency exchange rate fluctuations that are not hedged currently. A number of other factors could also have a negative effect on our business and results from operations outside the US, including different regulatory and industry standards and certification requirements;requirements, reduced protection for intellectual property rights in some countries;countries, import or export licensing requirements;requirements, the complexities of foreign tax jurisdictions;jurisdictions and difficulties and costs of staffing and managing our foreign operations.

Sales and Marketing

As of June 30, 2005,2007, we employed 65137 sales executivesand marketing employees worldwide, of whom 3166 were focused on the Americas markets, 3167 were focused on European markets and 34 were focused on Asia Pacific markets. We market and sell our products directly through our sales forces and indirectly through a variety of channel partners and reseller relationships. We market and sell our products domestically and internationally, with aan international focus on the UKEurope and to a lesser degree, Australia. We also maintain an inside sales group which provides a lower-cost channel into maintaining existing customers and expanding our customer base.

Product Development and Engineering

Our product development and engineering organization included 7999 employees as of June 30, 2005.2007. We also use off-shore development resources to supplement our internal development teams. We have three primary development groups: software engineering, quality assurance and technical support.writing. We spent $10.1$9.4 million, $9.3$12.3 million, and $9.4$16.1 million on product development and engineering costs in fiscal years 2003, 20042005, 2006 and 2007. The 2006 and 2007 expenditures include the impact of stock compensation expense, based on accounting rules that we adopted on July 1, 2005.

Our software engineers have substantial experience in advanced software development techniques as well as extensive knowledge of the complex processes involved in business payment and invoicing systems. Our engineers participate in the Microsoft Developer Network, IBM Partner World for Developers, and the Oracle Partner Developer Program. They maintain extensive knowledge of software development trends and best practices. Our technology focuses on providing business solutions utilizing industry standards, providing a path for extendibility and scalability of our products. Security, control and fraud prevention, as well as data management and information reporting, are priorities in the technology we develop and deploy.

Our quality assurance engineers have extensive knowledge of our products and expertise in software quality assurance techniques. Members of the quality assurance group make use of automated software testing tools to facilitate comprehensive and timely testing of products. The quality assurance group members participate in beta releases, including tests of new products or enhancements, and provide initial training materials for customer support and service.

Our technical support group provides all product documentation as well as technical support for released products. The technical writers are versed in current document technology and work closely with the software engineers to create and maintain documentation that is clear, current and complete. The technical support engineers are responsible for the analysis of reported software problems and work closely with customers and customer support staff. The group’s broad knowledge of our products, our technology, and our customers’ infrastructure allows themit to rapidly respond to customer support needs.

Backlog

At the end of fiscal year 2005,2007, our backlog was $45.1$59.7 million, including deferred revenues of $22.2$27.7 million. At the end of fiscal year 2004,2006, our backlog was $38.5$43.5 million, including deferred revenues of $17.6$21.1 million. We do not believe that backlog is a meaningful indicator of sales that can be expected for any period, and there can be no assurance that backlog at any point in time will translate into revenue in any specific subsequent period. However, we estimate that approximately 90% of our deferred revenues and 65% to 75% of our backlog will be recognized as revenue in fiscal year 2006.

Proprietary Rights

We rely upon a combination of patents, copyrights, trademarks and trade-secret laws to establish and maintain proprietary rights in our technology and products. We had 3437 active patent applications relating to our products as of June 30, 2005.2007. We have been awarded four9 patents, 3 of which were awarded in fiscal year 2007, and expect to receive others. The earliest year of expiration for our awarded patents is 2015.

We intend to continue to file patent applications as we develop new technologies.

There can be no assurance, however, that our existing patent applications, or any others that may be filed in the future, will issue or will be of sufficient scope and strength to provide meaningful protection of our technology or any commercial advantage to us, or that the issued patents will not be challenged, invalidated or circumvented. In addition, we rely upon a combination of copyright and trademark laws and non-disclosure and other intellectual property contractual arrangements to protect our proprietary rights. Given the rapidly changing nature of the industry’s technology, the creative abilities of our development, marketing and service personnel may be as or more important to our competitive position as the legal protections and rights afforded by patents. We also enter into agreements with our employees and clients that seek to limit and protect our intellectual property and the distribution of proprietary information. However, there can be no assurance that the steps we have taken to protect our intellectual property will be adequate to deter misappropriation of proprietary information, and we may not be able to detect unauthorized use and take appropriate steps to enforce our proprietary rights.

Government Regulation

Although our operations have not been subject to any material industry-specific governmental regulation, some of our existing and potential customers are subject to extensive federal and state governmental regulations.

In addition, governmental regulation in the financial services industry is evolving, particularly with respect to payment technology, and our customers may become subject to increased regulation in the future. Accordingly, our products and services must be designed to work within the regulatory constraints under which our customers operate.

Employees

As of June 30, 2005,2007, we had 475555 full-time employees, 166137 of whom were in sales and marketing, 152228 of whom were in professional services and customer support, 7999 of whom were in development and 7891 of whom were in administration and finance. None of our employees are represented by a labor union. We have not experienced any work stoppages and we believe that employee relationships are good. Our future success will depend in part on our ability to attract, retain and motivate highly qualified technical and managerial personnel in a highly competitive market.

| Item 1A. | Risk Factors |

Item 2.PropertiesInvesting in our common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below before making an investment decision involving our common stock. The risks and uncertainties described below are not the only ones facing our company. Additional risks and uncertainties may also impair our business operations..

If any of the following risks actually occur, our business, financial condition or results of operations would likely suffer. In that case, the trading price of our common stock could fall, and you may lose all or part of the money you paid to buy our common stock.

Our common stock has experienced and may continue to undergo extreme market price and volume fluctuations

Stock markets in general, and The NASDAQ Global Market in particular, have experienced extreme price and volume fluctuations, particularly in recent years. Broad market fluctuations of this type may adversely affect the market price of our common stock. The stock prices for many companies in the technology sector have experienced wide fluctuations that often have been unrelated to their operating performance. The market price of our common stock has experienced and may continue to undergo extreme fluctuations due to a variety of factors, including:

changes in or our failure to meet analysts’ or investors’ estimates or expectations;

general and industry-specific business, economic and market conditions;

actual or anticipated fluctuations in operating results, including those arising as a result of any impairment of goodwill or other intangible assets related to past or future acquisitions;

public announcements concerning us, including announcements of litigation, our competitors or our industry;

introductions of new products or services or announcements of significant contracts by us or our competitors;

acquisitions, strategic partnerships, joint ventures, or capital commitments by us or our competitors;

adverse developments in patent or other proprietary rights; and

announcements of technological innovations by our competitors.

A growing number of our customer arrangements involve selling our products and services on a hosted basis, which may have the effect of delaying revenue recognition and increasing development or start-up expenses

An increasing number of our customer arrangements involve offering certain of our products and services on a hosted basis. These arrangements typically include a contractually defined service period as well as performance criteria that our products or services are required to meet over the duration of the service period. Arrangements entered into on a hosted basis generally delay the timing of revenue recognition and often require the incurrence of up-front costs, which can be significant. We are currently making significant investments in certain of our hosted offerings, such as our accounts payable automation products, and there can be no assurance that these products will ultimately gain broad market acceptance. Additionally, there is a risk that we might be unable to consistently maintain the performance requirements, or service levels, called for under any such hosted arrangements. Such events, to the extent occurring, could have a material and adverse effect on our operating results.

Our future financial results will be impacted by our success in selling new products in a subscription and transaction based revenue model

A substantial portion of our revenues and profitability were historically generated from software license revenues. We are currently offering certain of our newer product sets under a subscription and transaction based revenue model, which we believe has certain advantages over a perpetual license model, including better predictability of revenue.

A subscription and transaction based revenue model typically results in no up-front revenue. Additionally, there can be no assurance that our customers, or the markets in which we compete, will respond favorably to the approach we have taken with our newer offerings. To the extent that our new subscription and transaction based offerings do not receive general marketplace acceptance, our financial results could be materially and adversely affected.

We make significant investments in existing products and new product offerings that can adversely affect our operating results and may not be successful

We operate in a highly competitive and rapidly evolving technology environment and believe that it is important to enhance existing product offerings and develop new product offerings to meet strategic opportunities as they evolve. Investments in existing product enhancements and new product offerings can have a negative impact on our operating results, and any existing product enhancements or new product offerings may not be accepted in the marketplace or generate material revenues. For example, during our fiscal year ended June 30, 2007, our operating results were affected by a significant increase in product development expenses as we continued to make investments in our banking and accounts payable automation products.

Integration of acquisitions could interrupt our business and our financial condition could be harmed

We have made several recent business acquisitions, including Formscape in October 2006. We may in the future continue to acquire, or make investments in, other businesses, products or technologies. Any acquisition or strategic investment we have made in the past or may make in the future may entail numerous risks, including the following:

difficulties integrating acquired operations, personnel, technologies or products;

inadequacy of existing operating, financial and management information systems to support the combined organization or new operations;

write-offs related to impairment of goodwill and other intangible assets;

entrance into markets in which we have no or limited prior experience or knowledge;

diversion of management’s focus from our core business concerns;

dilution to existing stockholders and earnings per share;

incurrence of substantial debt; and

exposure to litigation from third parties, including claims related to intellectual property or other assets acquired or liabilities assumed.

Any such difficulties encountered as a result of any merger, acquisition or strategic investment could have a material adverse effect on our business, operating results and financial condition.

As a result of our acquisitions, we could be subject to significant future write-offs with respect to intangible assets, which may adversely affect our future operating results

We review our intangible assets, including goodwill, periodically for impairment. At June 30, 2007, the carrying value of our goodwill and our other intangible assets was approximately $53 million and $31 million, respectively. While we reviewed our goodwill and intangible assets during the fourth quarter of fiscal year 2007 and concluded that there was no impairment, we could be subject to future impairment charges with respect to these intangible assets, or intangible assets arising as a result of acquisitions in future periods. Such charges, to the extent occurring, would likely have a material adverse effect on our operating results.

Our fixed costs may lead to operating results below analyst or investor expectations if our revenues are below anticipated levels, which could adversely affect the market price of our common stock

A significant percentage of our expenses, particularly personnel and facilities costs, are relatively fixed and based in part on anticipated revenue levels. In recent years, we have experienced slowing growth rates with certain of our licensed software products and in 2006 we experienced a decrease in the growth of our software license revenues as a result of the BACSTEL-IP initiative ending in the UK. A decline in revenues without a corresponding and timely slowdown in expense growth could negatively affect our business. Significant revenue shortfalls in any quarter may cause significant declines in operating results since we may be unable to reduce spending in a timely manner.

Quarterly or annual operating results that are below the expectations of public market analysts could adversely affect the market price of our common stock. Factors that could cause fluctuations in our operating results include the following:

economic conditions, which may affect our customers’ and potential customers’ budgets for information technology expenditures;

the timing of orders and longer sales cycles;

the timing of product implementations, which are highly dependent on customers’ resources and discretion;

the incurrence of costs relating to the integration of software products and operations in connection with acquisitions of technologies or businesses; and

the timing and market acceptance of new products or product enhancements by either us or our competitors.

Because of these factors, we believe that period-to-period comparisons of our results of operations are not necessarily meaningful.

Our mix of products and services could have a significant effect on our financial condition, results of operations and the market price of our common stock

The gross margins for our products and services vary considerably. Our software revenues generally yield significantly higher gross margins than do our subscription and transaction, service and maintenance and equipment and supplies revenue streams. In recent fiscal years, we experienced a decrease in our software license fees. If software license fees were to again decline, or if the mix of our products and services in any given period does not match our expectations, our results of operations and the market price of our common stock could be significantly adversely affected.

We face risks associated with our international operations that could harm our financial condition and results of operations

A significant percentage of our revenues have been generated by our international operations, and our future growth rates and success are in part dependent on our continued growth and success in international markets. We have operations in the US, UK, Australia, France and Germany. As is the case with most international operations, the success and profitability of these operations are subject to numerous risks and uncertainties that include, in addition to the risks our business as a whole faces, the following:

difficulties and costs of staffing and managing foreign operations;

differing regulatory and industry standards and certification requirements;

the complexities of foreign tax jurisdictions;

reduced protection for intellectual property rights in some countries;

currency exchange rate fluctuations; and

import or export licensing requirements.

A significant percentage of our revenues to date have come from our payment management offerings and our future performance will depend on continued market acceptance of these solutions

A significant percentage of our revenues to date have come from the license and maintenance of our payment management offerings and sales of associated products and services. Any significant reduction in demand for our payment management offerings could have a material adverse effect on our business, operating results and financial condition. Our future performance could depend on the following factors:

continued market acceptance of our payment management offerings including our overall accounts payable automation solution;

prospective customers’ dependence upon enterprises seeking to enhance their payment functions to integrate electronic payment capabilities;

our ability to introduce enhancements to meet the market’s evolving needs for secure payments and cash management solutions; and

acceptance of software solutions offered on a hosted basis.

Our future financial results will depend on our ability to manage growth effectively

In the past, rapid growth has strained our managerial and other resources. If rapid growth resumes, our ability to manage that growth will depend in part on our ability to continue to enhance our operating, financial and management information systems. We cannot assure you that our personnel, systems and controls will be adequate to support future growth. If we are unable to manage growth effectively, the quality of our services, our ability to retain key personnel and our business, operating results and financial condition could be materially adversely affected.

We face significant competition in our targeted markets, including competition from companies with significantly greater resources

In recent years, we have encountered increasing competition in our targeted markets. We compete with a wide range of companies, ranging from small start-up enterprises with limited resources, which compete principally on the basis of technology features or specific customer relationships, to large companies, which can leverage significant customer bases and financial resources. Given the size and nature of the markets we target, the implementation of our growth strategy and our success in competing for market share is dependent on our ability to grow our sales and marketing capabilities and maintain an appropriate level of financial resources.

An increasing number of large and more complex customer contracts, or contracts that involve the delivery of services over contractually committed periods, generally delay the timing of our revenue recognition and in the short-term may adversely affect our operating results, financial condition and the market price of our stock

Due to an increasing number of large and more complex customer contracts, we have experienced, and will likely continue to experience, delays in the timing of our revenue recognition. These large and complex customer contracts generally require significant implementation work, product customization and modification, resulting in the recognition of revenue over the period of project completion, which normally spans several quarters. Delays in revenue recognition on these contracts could affect our operating results, financial condition and the market price of our common stock.

We depend on key employees who are skilled in e-commerce, payment, cash and document management and invoice presentment methodology and Internet and other technologies

Our success depends upon the efforts and abilities of our executive officers and key technical employees who are skilled in e-commerce, payment methodology and regulation, and Internet, database and network technologies. The loss of one or more of these individuals could have a material adverse effect on our business. We currently do not maintain “key man” life insurance policies on any of our employees. While some of our executive officers have employment or retention agreements with us, the loss of the services of any of our executive officers or other key employees could have a material adverse effect on our business, operating results and financial condition.

We must attract and retain highly skilled personnel with knowledge in e-commerce, payment, cash and document management and invoice presentment methodology and Internet and other technologies

We believe that our success is in part dependent upon our ability to attract, hire, train and retain highly skilled technical, sales and marketing, and support personnel, particularly with expertise in e-commerce, payment, cash management and invoice methodology and Internet and other technologies. Competition for qualified personnel is intense. As a result, we may experience increased compensation costs that may not be offset through either improved productivity or higher sales prices. There can be no assurance that we will be successful in attracting, recruiting or retaining existing personnel. Based on our experience, it takes an average of nine months for a salesperson to become fully productive. We cannot assure you that we will be successful in increasing the productivity of our sales personnel, and the failure to do so could have a material adverse effect on our business, operating results and financial condition.

Increased competition may result in price reductions and decreased demand for our product solutions

The markets in which we compete are intensely competitive and characterized by rapid technological change. Some competitors in our targeted markets have longer operating histories, significantly greater financial, technical, and marketing resources, greater brand recognition and a larger installed customer base than we do. We expect to face additional competition as other established and emerging companies enter the markets we

address. In addition, current and potential competitors may make strategic acquisitions or establish cooperative relationships to expand their product offerings and to offer more comprehensive solutions. This growing competition may result in price reductions of our products and services, reduced revenues and gross margins and loss of market share, any one of which could have a material adverse effect on our business, operating results and financial condition.

Our success depends on our ability to develop new and enhanced products, services and strategic partner relationships

The markets in which we compete are subject to rapid technological change and our success is dependent on our ability to develop new and enhanced products, services and strategic partner relationships that meet evolving market needs. Trends that could have a critical impact on us include:

evolving industry standards, mandates and laws, such as those mandated by the National Automated Clearing House Association and the Association for Payment Clearing Services;

rapidly changing technology, which could cause our software to become suddenly outdated or could require us to make our products compatible with new database or network systems;

developments and changes relating to the Internet that we must address as we maintain existing products and introduce any new products; and

the loss of any of our key strategic partners who serve as a valuable network from which we can leverage industry expertise and respond to changing marketplace demands.

There can be no assurance that technological advances will not cause our products to become obsolete or uneconomical. If we are unable to develop and introduce new products, or enhancements to existing products, in a timely and successful manner, our business, operating results and financial condition could be materially adversely affected. Similarly, if our new products did not receive general marketplace acceptance, or if the sales cycle of any of our new products significantly delayed the timing of revenue recognition, our results could be negatively affected.

Our products could be subject to future legal or regulatory actions, which could have a material adverse effect on our operating results

Our software products and hosted services offerings facilitate the transmission of business documents and information including, in some cases, confidential financial data related to payments, invoices and cash management. Our web-based software products, and certain of our hosted services offerings, transmit this data electronically. While we believe that all of our product and service offerings comply with current regulatory and security requirements, there can be no assurance that future legal or regulatory actions will not impact our product and service offerings. To the extent that regulatory or legal developments mandate a change in any of our products or services, or alter the demand for or the competitive environment of our products and services, we might not be able to respond to such requirements in a timely or successful manner. If this were to occur, our business, operating results and financial condition could be materially adversely affected.

Any unanticipated performance problems or bugs in our product offerings could have a material adverse effect on our future financial results

If the products that we offer and continue to introduce do not sustain marketplace acceptance, our future financial results will be adversely affected. Since many of our software solutions are still in early stages of adoption and since most of our software products are continually being enhanced or further developed in response to general marketplace demands, any unanticipated performance problems or bugs that we have not been able to detect could result in additional development costs, diversion of technical and other resources from our other development efforts, negative publicity regarding us and our products, harm to our customer

relationships and exposure to potential liability claims. In addition, if our products do not enjoy wide commercial success, our long-term business strategy will be adversely affected, which could have a material adverse effect on our business, operating results and financial condition.

We could incur substantial costs resulting from warranty claims or product liability claims

Our software license agreements typically contain provisions that afford customers a degree of warranty protection in the event that our software fails to conform to its written specifications. These agreements typically contain provisions intended to limit the nature and extent of our risk of warranty and product liability claims. There is a risk, however, that a court might interpret these terms in a limited way or could hold part or all of these terms to be unenforceable. Furthermore, some of our licenses with our customers are governed by non-U.S. law, and there is a risk that foreign law might provide us less or different protection. While we maintain general liability insurance, including coverage for errors and omissions, we cannot be sure that our existing coverage will continue to be available on reasonable terms or will be available in amounts sufficient to cover one or more large claims. Although we have not experienced any material warranty or product liability claims to date, a warranty or product liability claim, whether or not meritorious, could result in substantial costs and a diversion of management’s attention and our resources, which could have an adverse effect on our business, operating results and financial condition.

We could be adversely affected if we are unable to protect our proprietary technology and could be subject to litigation regarding our intellectual property rights, causing serious harm to our business

We rely upon a combination of patent, copyright and trademark laws and non-disclosure and other intellectual property contractual arrangements to protect our proprietary rights. However, we cannot assure you that our patents, pending applications for patents that may issue in the future, or other intellectual property will be of sufficient scope and strength to provide meaningful protection to our technology or any commercial advantage to us, or that the patents will not be challenged, invalidated or circumvented. We enter into agreements with our employees and customers that seek to limit and protect the distribution of proprietary information. Despite our efforts to safeguard and maintain our proprietary rights, there can be no assurance that such rights will remain protected or that we will be able to detect unauthorized use and take appropriate steps to enforce our intellectual property rights.

In recent years, there has been significant litigation in the United States involving patents and other intellectual property rights. We may be a party to litigation in the future to protect our intellectual property rights or as a result of an alleged infringement of the intellectual property rights of others. Any such claims, whether or not meritorious, could require us to spend significant sums in litigation, pay damages, delay product implementations, develop non-infringing intellectual property or acquire licenses to intellectual property that is the subject of the infringement claim. These claims could have a material adverse effect on our business, operating results and financial condition.

We engage off-shore development resources which may not be successful and which may put our intellectual property at risk

In order to optimize our research and development capabilities and to meet development timeframes, we contract with off-shore third party vendors in India and elsewhere for certain development activities. While our experience to date with these resources has been positive, there are a number of risks associated with off-shore development activities that include but are not limited to the following:

less efficient and less accurate communication and information flow as a consequence of time, distance and language barriers between our primary development organization and the off-shore resources, resulting in delays or deficiencies in development efforts;

disruption due to political or military conflicts around the world;

misappropriation of intellectual property from departing personnel, which we may not readily detect; and

currency exchange rate fluctuations that could adversely impact the cost advantages intended from these agreements.

To the extent that these or unforeseen risks occur, our operating results and financial condition could be adversely impacted.

Some anti-takeover provisions contained in our charter and under Delaware law could hinder a takeover attempt

We are subject to the provisions of Section 203 of the General Corporation Law of the State of Delaware prohibiting, under some circumstances, publicly-held Delaware corporations from engaging in business combinations with some stockholders for a specified period of time without the approval of the holders of substantially all of our outstanding voting stock. Such provisions could delay or impede the removal of incumbent directors and could make more difficult a merger, tender offer or proxy contest involving us, even if such events could be beneficial, in the short-term, to the interests of the stockholders. In addition, such provisions could limit the price that some investors might be willing to pay in the future for shares of our common stock. Our certificate of incorporation and bylaws contain provisions relating to the limitations of liability and indemnification of our directors and officers, dividing our board of directors into three classes of directors serving three-year terms and providing that our stockholders can take action only at a duly called annual or special meeting of stockholders.

We may incur significant costs from class action litigation as a result of expected volatility in our common stock

In the past, companies that have experienced market price volatility of their stock have been the targets of securities class action litigation. In August 2001, we were named as a party in one of the so-called “laddering” securities class action suits relating to the underwriting of our initial public offering. We could incur substantial costs and experience a diversion of our management’s attention and resources in connection with any such litigation, which could have a material adverse effect on our business, financial condition and results of operations.

| Item 1B. | Unresolved Staff Comments. |

There are no material unresolved written comments from the staff of the SEC regarding our periodic or current reports received not less than 180 days before the end of our fiscal year to which this Form 10-K relates.

| Item 2. | Properties. |

We currently lease approximately 65,000 square feet of office space at our corporate headquarters in Portsmouth, New Hampshire under a lease that expires in 2012. We also occupy approximately 20,00037,000 square feet of leased domestic offices in Great Neck, New York, Morrisville, North Carolina, and Waltham, Massachusetts.

Chicago, Illinois.

We own approximately 16,000 square feet of office space in Reading, England and occupylease approximately 28,00038,000 square feet of leased internationaloffice space throughout the UK, including locations in Andover, Hertford, Hook, and Fleet. In addition, we lease approximately 6,000 square feet of office space in Hertford, Reading, London, and Manchester, England, Belfast, Ireland and Melbourne and Sydney, Australia.Australia and approximately 2,000 square feet in Linden, Germany.

Our New Hampshire facility serves as our corporate headquarters and is used by employees associated with all of our operating segments in addition to our management, administrative, sales and marketing and customer

support teams. Our New York facility is used to support the product development initiatives of all of our operating segments. Our North Carolina facility and all of our European facilities are used predominantly by personnel associated with our payments and transactional documents operating segment. Our Illinois facility is used principally by personnel who support aspects of our Legal eXchange solution, which is a component of our outsourced solutions segment. Our Australian facilities are used by personnel associated with our payment and transactional documents and banking solutions operating segments.

| Item 3. | Legal Proceedings. |

On October 19, 2004, a complaint was filed against Formscape, Inc. (Formscape), which the Company acquired in October 2006, by Cindy Bernstein, a former employee of Formscape. The complaint, which was subsequently amended, was pending in the United States District Court for the Eastern District of North Carolina, Western Division and alleged disparate treatment in violation of Title VII of the Civil Rights Act, wrongful discharge in violation of public policy, fraud, unfair and deceptive trade practices, discrimination in business, breach of contract and quantum meruit. The plaintiff sought damages for back salary, benefits and commissions as well as punitive damages, treble damages, attorney fees and costs. Formscape filed a petition for summary judgment and in January 2007 the court, in response to that petition, ruled that certain of the plaintiff’s charges were invalid as a point of law.

On January 24, 2007, the parties filed a motion with the court requesting the court appoint a magistrate judge to serve as a mediator and in May 2007, the parties entered into a General Release and Settlement Agreement (the “Settlement Agreement”) as a result of the mediation process. Under the terms of the Settlement Agreement, the Company was required to pay $300,000 to the plaintiff, $150,000 of which had been recorded as a liability in the preliminary purchase price allocation of the Formscape acquisition and $150,000 of which the Company recovered from amounts held in escrow to secure the indemnification obligations of the Formscape selling stockholders under the terms of the Formscape share purchase agreement. Accordingly, no expense was recorded by the Company as a result of the Settlement.

On August 10, 2001, a class action complaint was filed against usthe Company in the United States District Court for the Southern District of New York: Paul Cyrek v. Bottomline Technologies, Inc.; Daniel M. McGurl; Robert A. Eberle; FleetBoston Robertson Stephens, Inc.; Deutsche Banc Alex Brown Inc.; CIBC World Markets; and

J.P. Morgan Chase & Co. A consolidated amended class action complaint,In re Bottomline Technologies Inc. Initial Public Offering Securities Litigation, was filed on April 20, 2002. The amended complaint supersedes the class action complaint filed against usthe Company in the United States District Court for the Southern District of New York on August 10, 2001.

The amended complaint filed in the action asserts claims under Sections 11, 12(2) and 15 of the Securities Act of 1933, as amended, and Sections 10(b) and 20(a) of the Securities Exchange Act of 1934, as amended (Exchange Act). The amended complaint asserts, among other things, that the description in ourthe Company’s prospectus for ourits initial public offering was materially false and misleading in describing the compensation to be earned by the underwriters of ourthe offering, and in not describing certain alleged arrangements among underwriters and initial purchasers of ourthe Company’s common stock from the underwriters. The amended complaint seeks damages (or, in the alternative, tender of the plaintiffs’ and the class’s Bottomline common stock and rescission of their purchases of ourthe Company’s common stock purchased in the initial public offering), costs, attorneys’ fees, experts’ fees and other expenses.

In July 2002, Bottomline, Daniel M. McGurl and Robert A. Eberle joined in an omnibus motion to dismiss, which challenged the legal sufficiency of plaintiffs’ claims. The motion was filed on behalf of hundreds of issuer and individual defendants named in similar lawsuits. Plaintiffs opposed the motion, and the court heard oral argument on the motion in early November 2002. On February 19, 2003, the court issued an order denying the motion to dismiss as to Bottomline. In addition, in early October 2002, Daniel M. McGurl and Robert A. Eberle were dismissed from this case without prejudice. A special litigation committee of the board of directors of

Bottomline authorized Bottomline to negotiate a settlement of the pending claims substantially consistent with a memorandum of understanding negotiated among class plaintiffs, all issuer defendants and their insurers. The parties have negotiated a settlement, which is subject to approval by the court. On February 15, 2005, the court issued an Opinion and Order preliminarily approving the settlement, provided that the defendants and plaintiffs agree to a modification narrowing the scope of the bar order set forth in the original settlement agreement. IfThe parties agreed to the modification narrowing the scope of the bar order, and on August 31, 2005, the court issued an order preliminarily approving the settlement. On December 5, 2006, the United States Court of Appeals for the Second Circuit overturned the District Court’s certification of the class of plaintiffs who are pursuing the claims that would be settled in the settlement against the underwriter defendants. Plaintiffs filed a Petition for Rehearing and Rehearing En Banc with the Second Circuit on January 5, 2007 in response to the Second Circuit’s decision and have informed the District Court that they would like to be heard as to whether the settlement may still be approved even if the decision of the Court of Appeals is not approved, we intendreversed. The District Court indicated that it would defer consideration of final approval of the settlement pending plaintiffs’ request for further appellate review. On April 6, 2007, plaintiffs’ Petition for Rehearing of the Second Circuit’s decision was denied. As a result of the overturned class certification on June 25, 2007, the District Court signed an order terminating the settlement. The Company intends to vigorously defend ourselvesitself against this amended complaint. We doBottomline does not currently believe that the outcome of this proceeding will have a material adverse impact on ourits financial condition, results of operations or cash flows.

| Item 4. |

No matter was submitted to a vote of our stockholders, through the solicitation of proxies or otherwise, during the fourth quarter of fiscal year 2007.

Executive Officers and Other Key Employees of the Registrant

Our executive officers and other key employees and their respective ages as of August 31, 2007, are as follows:

| Age | Positions | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Robert A. Eberle | 46 | President, Chief Executive Officer and Director | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Peter S. Fortune | 48 | Chief Operating Officer and President of | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Kevin M. Donovan | 37 | Chief Financial Officer and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Eric A. Campbell | 50 | Chief Technology Officer | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Paul J. Fannon | 39 | Managing Director, Transactional Services Europe | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Thomas D. Gaillard | 44 | Vice President and General Manager, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Craig A. Jones | 50 | Vice President and General Manager, Global Banking and Finance | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 42 | Managing Director, Group Sales Europe | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Nigel K. Savory | 40 | Managing Director, Europe |

Robert A. Eberle has served as a director since September 2000 and as Chief Executive Officer since November 2006. Mr. Eberle has served as President since August 2004. From April 2001 to November 2006, Mr. Eberle served as Chief Operating Officer. Mr. Eberle served as Chief Financial Officer from September 1998 to August 2004.

Peter S. Fortune has served as Chief Operating Officer since November 2006, and as President of Bottomline Europe since we acquired the predecessor company in August 2000. From November 2005 to November 2006, Mr. Fortune served as Chief marketing Officer.

Kevin M. Donovanhas served as Chief Financial Officer since August 2004 and as Treasurer since May 2001. Mr. Donovan served as Vice President, Finance from January 2000 to August 2004.

Richard A. Bellhas served as Vice President and General Manager, Financial Process Solutions North America since September 2005. From January 2001 to September 2005, Mr. Bell served as Vice President of Create!form, which we acquired in September 2003.

Eric A. Campbell has served as Chief Technology Officer since May 2000.

Paul J. Fannon has served as Managing Director, Transactional Services Europe since December 2003. From December 2001 through December 2003, Mr. Fannon served as Managing Director, Payment Solutions Europe.

Thomas D. Gaillardhas served as Vice President and General Manager, Transactional Services North America since July 2003. From May 2002 to July 2003, Mr. Gaillard served as Vice President, Corporate Development.

Craig A. Joneshas served as Vice President and General Manager, Global Banking and Finance, since July 2006. From July 2003 to July 2006, Mr. Jones served as Vice President and General Manager, Financial Process Solutions North America. From July 2002 to July 2003, Mr. Jones served as Vice President of Product Management. From September 1999 to July 2002, Mr. Jones served as Vice President of Marketing.

Christopher W. Peck has served as Managing Director, Group Sales Europe since July 2003. From August 2000, when we acquired the predecessor company, through July 2003, Mr. Peck served as Group Sales Director of Bottomline Europe. From March 1994 to August 2000, Mr. Peck served as Group Sales Director of Checkpoint Security Services Limited and from March 1999 to August 2000, Mr. Peck served in the same capacity for Checkpoint Holdings.

Nigel K. Savory has served as Managing Director, Payment Solutions Europe since December 2003. From December 2001 through December 2003, Mr. Savory served as the Managing Director Transaction Services Europe. From August 2000, the date we acquired the predecessor company, through December 2001, Mr. Savory served as the European Business Development Director of Bottomline Europe. From January 1998 through August 2000, Mr. Savory served as the European Business Development Director of Checkpoint Security Services Limited.

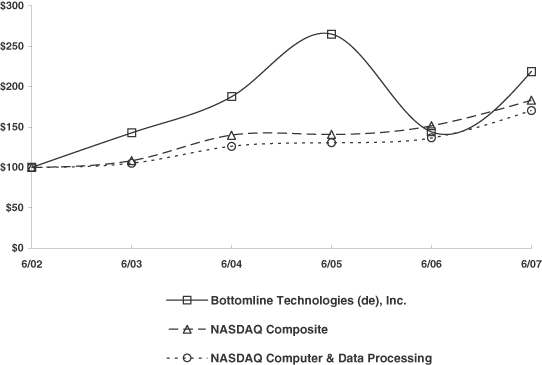

Our common stock is traded on The NASDAQ Global Market under the symbol EPAY. The following table sets forth, for the periods indicated, the high and low sale prices of our common stock, as quoted on The NASDAQ Global Market (previously the NASDAQ National Market).

Period | High | Low | ||||

Fiscal 2006 | ||||||

First quarter | $ | 18.62 | $ | 14.57 | ||

Second quarter | $ | 15.67 | $ | 10.01 | ||

Third quarter | $ | 13.75 | $ | 10.33 | ||

Fourth quarter | $ | 14.00 | $ | 8.05 | ||

Fiscal 2007 | ||||||

First quarter | $ | 10.38 | $ | 6.98 | ||

Second quarter | $ | 11.62 | $ | 9.28 | ||

Third quarter | $ | 13.24 | $ | 10.24 | ||

Fourth quarter | $ | 13.13 | $ | 10.50 | ||

As of August 31, 2007, there were approximately 198 holders of record of our common stock. Because many of the shares are held by brokers and other institutions on behalf of stockholders, we are unable to estimate the total number of individual stockholders represented by these holders of record.

The closing price for our common stock on August 31, 2007 was $13.18. For purposes of calculating the aggregate market value of the shares of our common stock held by non-affiliates, as shown on the cover page of this report, it has been assumed that all the outstanding shares were held by non-affiliates except for the shares beneficially held by our directors and executive officers. However, there may be other persons who may be deemed to be affiliates of ours.