UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(MARK ONE)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 20052006

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROMTO.

COMMISSION FILE NUMBER 1-14037

MOODY’S CORPORATION

(EXACT NAME OF REGISTRANT AS SPECIFIED IN ITS CHARTER)

| DELAWARE | 13-3998945 | |

| (STATE OF INCORPORATION) | (I.R.S. EMPLOYER IDENTIFICATION NO.) |

99 CHURCH STREET, NEW YORK, NEW YORK 10007

(ADDRESS OF PRINCIPAL EXECUTIVE OFFICES)

(ZIP CODE)

REGISTRANT’S TELEPHONE NUMBER, INCLUDING AREA CODE: (212) 553-0300.

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

TITLE OF EACH CLASS | NAME OF EACH EXCHANGE | |

COMMON STOCK, PAR VALUE $.01 PER SHARE | NEW YORK STOCK EXCHANGE | |

| PREFERRED SHARE PURCHASE RIGHTS | NEW YORK STOCK EXCHANGE

|

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þx No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þx

Indicate by check mark whether the Registrant: (1) has filed all reports required by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months and (2) has been subject to such filing requirements for the past 90 days. Yes þx No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer (see definition of “accelerated filer and large accelerated filer” in Exchange Act Rule 12b-2).

Large Accelerated Filer þx Accelerated Filer ¨ Non-accelerated Filer ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No þx

The aggregate market value of Moody’s Corporation Common Stock held by nonaffiliates* on June 30, 20052006 (based upon its closing transaction price on the Composite Tape on such date) was approximately $13.5$15.3 billion.

As of January 31, 2006, 289.62007, 278.5 million shares of Common Stock of Moody’s Corporation were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive proxy statement for use in connection with its annual meeting of stockholders scheduled to be held on April 25, 2006,24, 2007, are incorporated by reference into Part III of this Form 10-K.

The Index to Exhibits is included as Part IV, Item 15(3) of this Form 10-K.

| * | Calculated by excluding all shares held by executive officers and directors of the Registrant without conceding that all such persons are “affiliates” of the Registrant for purposes of federal securities laws. |

PART I

ITEM 1. BUSINESS

| ITEM 1. | BUSINESS |

Background

As used in this report, except where the context indicates otherwise, the terms “Moody’s” or “the Company”the “Company” refer to Moody’s Corporation and its subsidiaries. The Company’s executive offices are located at 99 Church Street, New York, NY 10007 and its telephone number is (212) 553-0300.

Prior to September 30, 2000, the Company operated as part of The Dun & Bradstreet Corporation (“Old D&B”). On September 8, 2000, the Board of Directors of Old D&B approved a plan to separate into two publicly traded companies – the Company and The New D&B Corporation (“New D&B”). On September 30, 2000 (“the Distribution Date”), Old D&B distributed to its shareholders all of the outstanding shares of New D&B common stock (the “2000 Distribution”). New D&B comprised the business of Old D&B’s Dun & Bradstreet operating company (the “D&B Business”). The remaining business of Old D&B consisted solely of the business of providing ratings and related research and credit risk management services (the “Moody’s Business”) and was renamed “Moody’s Corporation”.

New D&B is the accounting successor to Old D&B, which was incorporated under the laws of the State of Delaware on April 8, 1998. Old D&B began operating as an independent publicly-owned corporation on July 1, 1998 as a result of its June 30, 1998 spin-off (the “1998 Distribution”) from the corporation now known as “R.H. Donnelley Corporation” and previously known as “The Dun & Bradstreet Corporation” (“Donnelley”). Old D&B became the accounting successor to Donnelley at the time of the 1998 Distribution.

Prior to the 1998 Distribution, Donnelley was the parent holding company for subsidiaries then engaged in the businesses currently conducted by New D&B, Moody’s and Donnelley. Prior to November 1, 1996, it also was the parent holding company of subsidiaries conducting business under the names Cognizant Corporation (“Cognizant”) and ACNielsen Corporation (“ACNielsen”). On that date Donnelley effected a spin-off of the capital stock of Cognizant and ACNielsen to its stockholders (the “1996 Distribution”). Cognizant subsequently changed its name to Nielsen Media Research, Inc. in connection with its 1998 spin-off of the capital stock of IMS Health Incorporated (“IMS Health”).

For purposes of governing certain ongoing relationships between the Company and New D&B after the 2000 Distribution and to provide for an orderly transition, the Company and New D&B entered into various agreements including a Distribution Agreement, Tax Allocation Agreement, Employee Benefits Agreement, Shared Transaction Services Agreement, Insurance and Risk Management Services Agreement, Data Services Agreement and Transition Services Agreement.

Detailed descriptions of the 1996, 1998 and 2000 Distributions are contained in the Company’s 2000 annual report on Form 10-K, filed on March 15, 2001.

The Company

Moody’s is a provider of (i) credit ratings, research and analysis covering fixed incomefixed-income securities, other debt instruments and the entities that issue such instruments in the global capital markets, and credit training services and (ii) quantitative credit risk assessment products and services and credit processing software for banks, corporations and investors in credit-sensitive assets. Founded in 1900, Moody’s employs approximately 2,9003,400 people worldwide. Moody’s maintains offices in 22 countries and has expanded into developing markets through joint ventures or affiliation agreements with local rating agencies. Moody’s customers include a wide range of corporate and governmental issuers of securities as well as institutional investors, depositors, creditors, investment banks, commercial banks and other financial intermediaries. Moody’s is not dependent on a single customer or a few customers, such that a loss of any one would have a material adverse effect on its business.

2

Moody’s operates in two reportable segments: Moody’s Investors Service and Moody’s KMV. For additional financial information on these segments, see Part II, Item 8,8. “Financial Statements – Note 17 – Segment Information”.

Moody’s Investors Service publishes rating opinions on a broad range of credit obligors and credit obligations issued in domestic and international markets, including various corporate and governmental obligations, structured finance securities and commercial paper programs. It also publishes investor-oriented credit information, research and economic commentary, including in-depth research on major debt issuers, industry studies, special comments and credit opinion handbooks. Moody’s credit ratings and research help investors analyze the credit risks associated with fixed-income securities. Such independent credit ratings and research also contribute to efficiencies in markets for other obligations, such as insurance policies and derivative transactions, by providing credible and independent assessments of credit risk. Moody’s provides ratings and

2

credit research on governmental and commercial entities in approximatelymore than 100 countries. Moody’s global and increasingly diverse services are designed to increase market efficiency and may reduce transaction costs. As of December 31, 2005,2006, Moody’s had ratings relationships with more than 11,000 companies12,000 corporate issuers and more than 25,000approximately 29,000 public finance issuers. Additionally, the Company has rated more than 70,00096,000 structured finance obligations. Ratings are disseminated via press releases to the public through a variety of print and electronic media, including the Internet and real-time information systems widely used by securities traders and investors.

Beyond credit rating services for issuers, Moody’s Investors Service provides research services, data and analytic tools that are utilized by institutional investors and other credit and capital markets professionals. These services cover various segments of the loan and debt capital markets, and are sold to more than 7,3009,300 customer accounts worldwide. Within these accounts, more than 25,00029,000 users accessed Moody’s research website (www.moodys.com) during calendar year 2005.2006. In addition to these clients, more than 123,000148,000 other individuals visited Moody’s website to retrieve current ratings and other information made freely available to the public.

The Moody’s KMV business develops and distributes quantitative credit risk assessment products and services and credit processing software for banks, corporations and investors in credit-sensitive assets. Moody’s KMV serves more than 1,8001,700 clients operating in more than 80approximately 85 countries, including most of the world’s largest financial institutions. Moody’s KMV’s quantitative credit analysis tools include models that estimate the probability of default for approximately 28,00029,000 publicly traded firms globally, updated daily. In addition, Moody’s KMV’s RiskCalc™™ models extend the availability of these probabilities to privately held firms in many of the world’s economies. Moody’s KMV also offers services to value and improve the performance of credit-sensitive portfolios.

Prospects for Growth

Over recent decades, global public and private fixed-income markets have grown significantly in terms of outstanding principal amount and types of securities. While there is potential for periodic cyclical disruption in these developments, Moody’s believes that the overall trend and outlook remain favorable for continued secular growth in capital market activity worldwide. In addition, the securities being issued in the global fixed-income markets are becoming more complex. Moody’s expects that these trends will provide continued long-term demand for high-quality, independent credit opinions. These phenomena are especially apparent internationally, where economic expansion and integration isare driving increased use of public fixed-income markets for corporate financing activities, and factors such as increased adoption and enabling regulation and increased acceptance of new financial technologies by debt issuers and investors have driven growth in structured finance issuance.

Technology,Communication technology, such as the Internet, makes information about investment alternatives widely available throughout the world. This technology facilitates issuers’ ability to place securities outside their national markets and investors’ capacity to obtain information about securities issued outside their national markets. Issuers and investors are also more readily able to obtain information about new financing techniques and new types of securities that they may wish to purchase or sell, many of which may be unfamiliar to them. This availability of

3

information promotes worldwide financial markets and a greater need for credible and globally comparable opinions about credit ratings.risk. As a result, a number of new capital markets have emerged. In addition, more issuers and investors are accessing developed capital markets.

Another trend that is increasing the size of the worldworld’s capital markets is the ongoing disintermediation of financial systems. Issuers are increasingly financing in the global public capital markets, in addition to, or in substitution for, traditional financial intermediaries. Moreover, financial intermediaries are selling assets in the global public capital markets, in addition to or instead of retaining those assets. Structured finance securities markets for many types of assets have developed in many countries and are contributing to these trends.

The complexity of capital market instruments is also growing. Consequently, assessing the credit risk of such instruments becomes more of a challenge for financial intermediaries and asset managers. In the credit markets, reliable third-party ratings and research increasingly supplement or substitute for traditional in-house research as the scale, geographic scope and complexity of financial markets grow.

Growth in issuance of structured finance securities has generally been stronger than growth in straight corporate and financial institutions debt issuance, and Moody’s expects that trend to continue. Growth in structured finance has reflected increased adoptionacceptance of structured finance as an acceptablea financing and refinancing mechanism, regulatory changes that facilitate the use of structured finance, and increases in the scope of asset types, including for example consumer debt, that forms collateralform the underlying asset pools for structured finance securities.

Rating fees paid by debt issuers account for most of the revenue of Moody’s Investors Service. Therefore, a substantial portion of Moody’s revenue is dependent upon the volume and number of debt securities issued in the global capital markets that Moody’s rates. Moody’s is therefore affected by the performance of, and the prospects for, the major world economies

3

and by the fiscal and monetary policies pursued by their governments. However, annual fee arrangements with frequent debt issuers, annual debt monitoring fees and annual fees from commercial paper and medium-term note programs, bank and insurance company financial strength ratings, mutual fund ratings, subscription-based research and other areas are less dependent on, or independent of, the volume or number of debt securities issued in the global capital markets.

Moody’s operations are also subject to various risks inherent in carrying on business internationally. Such risks include currency fluctuations and possible nationalization, expropriation, exchange and price controls, changes in the availability of data from public sector sources, limits on providing information across borders and other restrictive governmental actions. Management believes that the risks of nationalization or expropriation are reduced because the Company’s basic service is the creation and dissemination of information, rather than the production of products that require manufacturing facilities or the use of natural resources. However, the formation of, for example, a new government-sponsored regional or global rating agency would pose a risk to Moody’s growth prospects. Management believes that this risk, compared to other regulatory changes under consideration for the credit rating industry, is relatively low because of the likelihood that substantial investments over a sustained period would be required.required, with uncertainty about the likelihood of financial success.

Legislative bodies and regulators in both the United States and Europe continue to conduct regulatory reviews of credit rating agencies, which may result in an increased number of competitors, restrictions on certain business expansion activities by Moody’s Investors Service or increased costs of doing business for Moody’s. At present, Moody’s is unable to assess the nature and effect any regulatory changes may have on future growth opportunities. See “Regulation” below.

Growth in Moody’s KMV is expected from increased adoption of quantitative credit management techniquesawareness and of integrated risk-management solutionsadoption by financial institutions globallyof active credit portfolio management and the estimation of economic capital, for which MKMV provides products and services. In addition, Moody’s KMV will continue to see revenue growth from the implementation of internal rating tools for Basel II compliance and credit analysis best practices. This growth will be realized by, for example, the development of new private firm default probability models for specific countries and by corporations managing, for example, trade receivables. Increased useexpanding analysis capabilities of credit models is expected under the forthcoming revised international bank regulatory regime, known as “Basel II”, that is anticipated to be implemented by national regulatory authorities by January 2007. Moody’s KMV also expects to introduce new products.asset classes.

4

Competition

The Moody’s Investors Service business competes with other credit rating agencies and with investment banks and brokerage firms that offer credit opinions and research. Institutional investors also have in-house credit research capabilities. Moody’s largest competitor in the global credit rating business is Standard & Poor’s Ratings Services (“S&P”), a division of The McGraw-Hill Companies, Inc. There are some rating markets, based on industry, geography and/or instrument type, in which Moody’s has made investments and obtained market positions superior to S&P’s. In other markets, the reverse is true.

Another rating agency competitor ofIn addition to S&P, Moody’s iscompetitors include Fitch, a subsidiary of Fimalac S.A. Although Moody’s, Dominion Bond Rating Service, Ltd. of Canada (“DBRS”) and S&P are each larger than Fitch, competition is expected to increase.A.M. Best Company, Inc. One or more additional significant rating agencies also may emerge in the United States as the Securities and Exchange Commission (“SEC”) has expanded, and may continue to expand the number of Nationally Recognized Statistical Rating Organizations (“NRSRO”). In February 2003, the SEC designated Dominion Bond Rating Service, Ltd. of Canada (“DBRS”) a NRSRO and in March 2005, the SEC designated A.M. Best Company, Inc. a NRSRO. Competition may also emerge in developed or developing markets outside the United States over the next few years for example, in response toas the growth in the European capital markets and in developing markets. Any suchnumber of rating agencies that may emerge may receive support from local governments or other institutions.

Additional rating agencies have been established, primarily in emerging markets and as a result of local capital market regulation. Regulators worldwide have perceived that credit ratings can further regulatory objectives for the development of public fixed-income securities markets. The result has been the creation of a number of primarily national rating agencies in various countries. Certain of these regulatory efforts may have the unintended effect of producing less credible ratings over time. Attempts to standardize ratings systems or criteria may make all rating systems and agencies appear undifferentiated, obscuring variations in the quality of the ratings providers. In addition, since Moody’s believes that some of its most significant challenges and opportunities will arise outside the United States, it will have to compete with rating agencies that may have a stronger local presence or a longer operating history in those markets.increase.

Financial regulators are reviewing their approach to supervision and have sought or are seeking comments on changes to the global regulatory framework.framework that could affect Moody’s. Bank regulators, under the oversight of the Basel Committee on Banking Supervision, have proposed using refined risk assessments as the basis for minimum capital requirements. The proposed Standardized Approach relies on rating agency opinions, while the proposed Internal Ratings Based Approach relies on systems and processes maintained by the regulated bank. The increased regulatory focus on credit risk presents both opportunities and challenges for Moody’s. Global demand for credit ratings and risk management services may rise, but regulatory actions may result in a greater number of rating agencies and/or additional regulation of Moody’s and its competitors. Alternatively, banking or securities market regulators could seek to reduce the use of ratings in regulations, thereby reducing certain elements of demand for ratings, or otherwise seek to control the analysis or business of rating agencies.

Credit rating agencies such as Moody’s also compete with other means of managing credit risk, such as credit insurance. Competitors that develop quantitative methodologies for assessing credit risk also may pose a competitive threat to Moody’s.

Moody’s KMV’s main competitors for quantitative measures of default risk include the RiskMetrics Group, S&P, CreditSights, R&I’s Financial Technology Institute (in Japan), Fitch Algorithmics, Dun and Bradstreet, models developed internally by customers and other smaller vendors. Other firms may compete in the future. Baker Hill, acquired by Experian, eCredit and Bureau van Dijk Electronic Publishing are Moody’s KMV’s main competitors in the software market to assist banks in their commercial lending activities. Mercer Oliver Wyman competes with the professional services group at Moody’s KMV for certain credit risk consulting services business.

54

Moody’s Strategy

Moody’s intends to focus on the following opportunities:

Expansion in Financial Centers

Moody’s serves its customers through its global network of offices and business affiliations. Moody’s currently maintains full-servicecomprehensive rating and marketing operations in financial centers including Frankfurt, Hong Kong, London, Madrid, Milan, New York, Paris, Singapore, Sydney and Tokyo. Moody’s expects that its global network will position it to benefit from the expansion of worldwide capital markets and thereby increase revenue. Moody’s also expects that the growth of its Moody’s Investors Service business as a consequence of financial market integration in Europe will continue. Additionally, Moody’s expects to continue its expansion into developing markets either directly or through joint ventures. This will allow Moody’s to extend its credit opinion franchise to local and regional obligors, through domestic currency ratings and national scale ratings. These developing market efforts have been supported in 2006 by the acquisition of 100% of CRA Rating Agency in the Czech Republic to form Moody’s Central Europe and the acquisition of a 49% stake in China Cheng Xin International Credit Rating Co. Ltd. in China, and in January 2007 by the acquisition of 99% of PT Kasnic Credit Rating in Indonesia to form Moody’s Indonesia. Moody’s expects to continue its expansion into developing markets either directly or through joint ventures.

New Rating Products

Moody’s is pursuing numerous initiatives to expand credit ratings, including from public fixed-income securities markets to other sectors with credit risk exposures. Within established capital markets, Moody’s continues to expand its rating coverage of bank loans and project finance loans and securities. In developing markets, Moody’s seeks to extend its credit opinion franchise to local and regional obligors, through domestic currency ratings and national scale ratings. In global and local counterparty markets, Moody’s offers a distinct setsets of rating products to address the creditworthiness of financial firms, throughincluding bank financial strength and deposit ratings, and through insurance financial strength ratings. Moody’s has also introduced issuer ratings for corporations not active in the debt markets. For company ratings, Moody’s seeks toAs the structured finance markets continue to add value throughgrow worldwide and secondary markets continue to develop, demand for research, data and analysis supporting these markets has heightened. In order to capitalize on market developments and to enhance ratings surveillance efficiency, Moody’s has created a new products group within structured finance to focus on new ratings products, such as hedge fund operations quality ratings, and to identify, design, develop and maintain value-added research, analytics and data products serving the Enhanced Analysis Initiative by providing greater scope and depthstructured finance market. The acquisition of analysis of issues related to company creditworthiness, including enhanced liquidity and cash flowWall Street Analytics in December 2006 broadens Moody’s capabilities in the analysis and evaluationmonitoring of accounting, corporate governancecomplex debt securities and risk transference issues. Moody’s has also introduced mutual fund indicesprovides a deeper pool of dedicated analytic and style-based analyticalproduct development staff to create new software analytic tools to assist in evaluating fund portfolio characteristics and their performance. Finally, infor the structured finance market.

In response to growing investor demand for expanded credit opinion in the high yield market, Moody’s has announced its intention to introduceintroduced a number of new products, including joint default analysis, corporate financial metrics, and both loss-given-default and probability-of-default ratings.

Additional Opportunities in SecuritizationStructured Finance

The repackaging of financial assets has had a profound effect on the fixed-income markets. New patterns of securitization are expected to emerge in the next decade. Although the bulk of assets securitized in the past five years have been consumer assets owned by banks, commercial assets — principally commercial mortgages, term receivables and corporate obligations — are now increasingly being securitized. Securitization has evolved into a strategic corporate finance tool in North America, Europe and Japan, and is evolving elsewhere internationally. Ongoing global development of non-traditional financial instruments, such asespecially credit derivatives, future flow securities, hybrids, credit-linked bonds and catastrophe bondshas accelerated in recent years. Increasingly complex collateralized debt obligations (“CDO”s) have been introduced, which should continue to support growth. Moody’s has introduced new services enabling investors to monitor the performance of their investments in structured finance, covering asset-backed finance, commercial mortgage finance, residential mortgage finance and credit derivatives.

Internet-Enhanced Products and Services

Moody’s is expanding its use of the Internet and other electronic media to enhance client service. Moody’s website provides the public with instant access to ratings and provides the public and subscribers with credit research. Internet delivery also enables Moody’s to provide services to more individuals within a client organization than were available with paper-based products and to offer higher-value services because of more timely delivery. Moody’s expects that access to these applications will increase client use of Moody’s services. Moody’s expects to continue to invest in electronic media to capitalize on these and other opportunities.

65

Expansion of Credit Research Products and Investment Analytic Tools

Moody’s plans to expand its research and analytic services through internal development and by acquisition. To respond to client demand, new product initiatives are generally more analyticanalytical and data-intensive than traditional narrative research offerings. Such services address investor interest in replicating the monitoring activities conducted by, for example, Moody’s securitization analysts and provide the means for customers to gain access to raw data and proprietary ratios used by Moody’s analysts in the rating process for municipalities, companies and financial institutions. These products represent important sources of growth for the research business unit. Moreover, Moody’s continues to explore opportunities to extend its research relevance in new domestic or regional markets (e.g., China) as well as new functional markets (e.g., hedge funds).

New Quantitative Credit Risk Assessment Services

Moody’s will continue to provide banks and other financial institutions with quantitative credit risk assessment services. Moody’s believes that there will be increased demand for such services because they enableassist customers trading or holding credit-sensitive assets to produce better performance. Also, recent proposals by international bank regulatory authorities to recognize banks’ internal credit risk management systems for the purpose of determining regulatory capital are expected to encourage adoption of such services.services by banks from third-party providers. Moody’s also expects to provide extensions to existing services and new services, such as valuations of credit-sensitive assets.

Regulation

In the United States, Moody’s Investors Service has been designated as a NRSRO by the SEC. The SEC first applied the NRSRO designation in 1975 to companies whose credit ratings could be used by broker-dealers for purposes of determining their net capital requirements. Since that time, Congress (including in certain mortgage-related legislation), the SEC (including in certain of its regulations under the Securities Act of 1933, as amended, the Securities Exchange Act of 1934, as amended and the Investment Company Act of 1940, as amended) and other governmental and private bodies have used the ratings of NRSROs to distinguish between, among other things, “investment grade” and “non-investment grade” securities. Moody’s Investors Service has also voluntarily registersregistered with the SEC as a NRSRO under the Investment Advisers Act of 1940, as amended. Once SEC rules under the Credit Rating Agency Reform Act of 2006, discussed below, are promulgated and become effective, approved NRSROs will be required to register pursuant to the Securities Exchange Act of 1934.

Over the past several years, U.S. regulatory and congressional authorities have questionedreviewed the suitability of continuing to use ratings in federal securities laws and, if such use is continued, the potential need for altering the regulatory framework under which rating agencies operate. Following is a summary of some recent developmentsThis review ultimately resulted in the U.S.

In February 2005, Moody’s participated in a hearing held bypassage of the United States Senate Committee on Banking, Housing and Urban Affairs (the “Banking Committee”) on Examining the Role of Credit Rating AgenciesAgency Reform Act of 2006 (“Reform Act”) in September 2006. The stated objectives of the Capital Markets. Primary areas of inquiry by senators on the Banking Committee included: (i) potential conflicts of interest affecting credit rating agenciesReform Act are to foster competition, transparency and how those conflicts can be avoided or properly managed; and (ii) the degree of competitionaccountability in the credit ratings industry and how competition might be increased. Moody’s written statement submittedrating industry. It makes changes to the Committee can be found onSEC’s processes for designating rating agencies as NRSROs, and formalizes theRegulatory Affairspage of the Company’s website at www.moodys.com. The Banking Committee has scheduled another hearing for March 7, 2006.

In March 2005, framework through which the SEC disclosedoversees them. However, the legislation provides that in considering the oversight of NRSROs, it may pursue a voluntary compliance and oversight framework for rating agencies that are designated as NRSROs, or it could seek legislative authority for formal oversight of NRSROs. Moody’s continues to cooperate with the SEC in its efforts to developshall not regulate the voluntary framework withsubstance of credit ratings or the NRSROs.

In April 2005,procedures and methodologies by which any NRSRO determines credit ratings. The Reform Act requires the SEC releasedto issue final implementing rules by June 26, 2007. On February 5, 2007, the SEC published for public comment a Proposed Rule on the “Definitionits proposed rules, addressing registration, recordkeeping, financial reporting, policies for handling of Nationally Recognized Statistical Rating Organization”. The proposed definition of the term NRSRO is an entity that: (i) issues publicly available credit ratings that are current assessments of the creditworthiness of obligors with

7

respect to specific securities or money market instruments; (ii) is generally accepted in the financial markets as an issuer of crediblematerial non-public information and reliable ratings, including ratings for a particular industry or geographic segment, by the predominant users of securities ratings; and (iii) uses systematic procedures designed to ensure credible and reliable ratings, manage potentialmanaging conflicts of interest, and prevent the misuse of nonpublic information, and has sufficient financial resourcescertain prohibitions against unfair, coercive or abusive practices. Interested parties have until March 12, 2007 to ensure compliance with those procedures. Numerous market participants, including Moody’s, respondedsubmit comments to the request for comment. Moody’s response can be found on theRegulatory Affairspage of the Company’s website.

In addition, in June 2005 the SEC produced technical assistance pursuant to a congressional request relating to statutory authority that the SEC may need if Congress determines that it is appropriate to create a comprehensive oversight regime for credit rating agencies. Congress had also requested that market participants provide their views on the SEC’s technical assistance. Moody’s comments can be found on theRegulatory Affairspage of the Company’s website.

In June 2005, U.S. House Representative Michael Fitzpatrick (R-PA) introduced H.R. 2990, the “Credit Rating Agency Duopoly Relief Act of 2005”. The House of Representatives’ Financial Services Subcommittee on Capital Markets held hearings on H.R. 2990 in June and November 2005, at which several interested parties testified. Representative Michael Oxley (R-OH), Chair of the House of Representatives’ Financial Services Committee, has indicated his intention to advance H.R. 2990 during 2006; the next steps in the process have not yet been announced.

At present,SEC. Moody’s is unablereviewing the proposed rules and intends to assesssubmit comments to the likelihood of any regulatory or legislative changes that may result from ongoing reviews in the United States, nor the nature and effect of any such regulatory changes.SEC.

Internationally, several regulatory developments have occurred:

IOSCO—In December 2004, the Technical Committee of the International Organization of Securities Commissions (“IOSCO”) published the Code of Conduct Fundamentals for Credit Rating Agencies (the “IOSCO Code”). The IOSCO Code is the product of approximately two years of collaboration among IOSCO, rating agencies and market participants, and incorporates provisions that address three broad areas:

Ÿ

the quality and integrity of the rating process;

•

credit rating agency independence and the avoidance of conflicts of interest; and

•

credit rating agency responsibilities to the investing public and issuers.

The IOSCO Code is not binding on credit rating agencies. It relies on voluntary compliance and public disclosure of areas of non-compliance by credit rating agencies so that users of credit ratings can better assess rating agency behavior and performance.

6

Moody’s Investors Service endorsed the IOSCO Code and in June 2005 published its Code of Professional Conduct (the “Moody’s Code”) pursuant to the IOSCO Code. In April 2006, Moody’s Investors Service published its first annual report on the implementation of Moody’s Code. The report discusses policies, procedures and processes that implement the Moody’s Code. The report also describes differences between the Moody’s Code and the IOSCO Code and how Moody’s believes that the objectives of the IOSCO Code are otherwise addressed. Both Moody’s Code and the report can be found on theRegulatory Affairspage of the Company’s website.

European CommissionUnion— In January 2006, theThe European Commission (“Commission”) produced for the European Parliamentissued a “CommunicationCommunication on Credit Rating Agencies” (the “Communication”). The Communication wasrating agencies in response to a February 2004 Parliament resolution asking the Commission to assess the need for legislative initiatives related to rating agencies. In the Communication, the Commission concluded that at present no additional legislation is required.January 2006. The Commission noted that recent European Union (“EU”) financial services legislative measures that are relevant to credit rating agencies, combined with a self-regulatory framework for rating agencies based on the IOSCO Code, can effectively addressprovided a suitable framework for the major concerns raised byoversight of rating agencies and that no legislative actions were required at the European Parliament. In addition, thetime. The Commission indicated that it will askwould monitor developments related to rating agencies and asked the Committee of European Securities Regulators (“CESR”) to monitor rating agencies’ compliance with the IOSCO Code and report back regularly.

8

regularly.CESR completed a process to assess such compliance and published a report in January 2007. The Commission also stated that it will monitor developments related toCESR process focused on four internationally active rating agencies and that it could in the future re-evaluate its approach or take legislative action.

Moody’s cannot predict whether the European Parliament will agree with the Commission’s conclusion, or whether regulation or legislation relating to rating agencies will be enacted in the EU.

European Union Market Abuse Directive — In 2003, the EU adopted the Market Abuse Directive (the “Directive”), which provides a common European framework for the prohibition of insider dealing and market manipulation, and promotes market integrity by ensuring prompt and fair disclosure of information about financial instruments to the public. The EU countries are currently adopting legislation that implements the Directive. While the Directive is applicable to all participantsoperate in the European capital markets,Union, including Moody’s, and involved discussions with the EU has excluded creditindividual rating agencies from certainas well as a survey of market participants. CESR concluded that the four rating agencies are largely compliant with the IOSCO Code and identified a few areas where it believed rating agencies could improve their processes and disclosures and where the IOSCO Code could be improved. CESR indicated that for its rules that specifically address2007 report, it will look into these areas in particular as well as the type and amount of information that should be disclosed to the market. Depending on how each EU country adopts the Directive, it could, among other things, alter rating agencies’ communications with issuers as partimpact of the rating assignment processReform Act and increase Moody’s cost of doingthe SEC’s implementing rules on the rating business in Europe and the legal risk associated with such business.European Union. As a result of the CESR report, in January 2007 the Commission reiterated its stance that the self-regulatory approach was, at present, the appropriate regulatory framework for rating agencies in Europe.

The Basel Committee—In June 2004, the Basel Committee on Banking Supervision published itsa new capital adequacy framework (“Basel II”) to replace its initial 1988 framework. Under Basel II, ratings assigned by recognized credit rating agencies (called External Credit Assessment Institutions, or “ECAIs”) wouldcould be an alternative available toused by banks to determinein determining credit risk weights for many of their institutional credit exposures. National authorities will begin implementing these aspects of Basel II during 2007. Recognized ECAIs could be subject to a broader range of oversight. It is anticipated that Basel II will be implemented by national regulatory authorities by January 2007.

In the EU, Basel II has been adopted through the Capital Requirements Directive (“CRD”), which, among other things, setsets out criteria for recognizing ECAIs within the EU. The Commission created the Committee of European Banking Supervisors (“CEBS”), comprised of European banking regulators, to advise it on banking policy issues that include implementing the CRD. In January 2006, CEBS published “Guidelines for a common approach to the recognition of External Credit Assessment Institutions”. The guidelines that provide the basis for a consistent approach by EU Member States to the implementation of the CRD’s ECAI recognition and supervision criteria,criteria. Moody’s completed an application process pursuant to the CEBS guidelines and in August 2006, CEBS expectsannounced a shared view among EU banking authorities that nationalMoody’s should be recognized as an ECAI. However, as each Member State must formally recognize ECAIs for use in its jurisdiction, the recognition process is ongoing.

Bank regulators in EU Member States will applyother jurisdictions globally have begun the guidelines.

ECAI recognition process, and Moody’s has been recognized in several jurisdictions. At this time Moody’s cannot predict the long-term impact of Basel II on the manner in which the Company conducts its business. However, Moody’s does not currently believe that Basel II will materially affect its financial position or results of operations.

Finally, Moody’s is subject to regulation in certain non-U.S. jurisdictions in which it operates. Some recent regulatory actions outside the United States are noted below:

Italy — In implementing the Market Abuse Directive, Italy passed two laws during 2005 that were relevant to rating agencies — the EU Law 2004 and the Reform of Savings Law. The EU Law 2004 stated that certain provisions of the Market Abuse Directive related to fair disclosure of information about financial instruments to the public were applicable to credit opinions published in the Italian Market, although the European Commission had explicitly excluded rating agencies from those provisions. The Reform of Savings Law amended the EU Law 2004 and excluded rating agencies from the fair disclosure provisions. The EU Law 2004 had also directed theCommissione Nazionale per la Società e la Borsa(“CONSOB”) to implement an appropriate regulatory framework to supervise rating agency conduct in Italy. CONSOB adopted regulations in November 2005 that require rating agencies to adopt measures related to disclosure of information about financial instruments and to disclose whether such measures differ from those articulated in the IOSCO Code.

Other legislation and regulation relating to credit rating and research services has been considered from time to time by local, national and multinational bodies and is likely to be considered in the future. In certain countries, governments may provide financial or other support to locally-based rating agencies. In addition, governments

9

may from time to time establish official rating agencies or credit ratings criteria or procedures for evaluating local issuers. If enacted, any such legislation and regulation could significantly change the competitive landscape in which Moody’s operates. In addition, the legal status of rating agencies has been addressed by courts in various decisions and is likely to be considered and addressed in legal proceedings from time to time in the future. Management of Moody’s cannot predict whether these or any other proposals will be enacted, the outcome of any pending or possible future legal proceedings, regulatory or legislative actions, or the ultimate impact of any such matters on the competitive position, financial position or results of operations of Moody’s.

Intellectual Property

Moody’s and its affiliates own and control a variety of trade secrets, confidential information, trademarks, trade names, copyrights, patents, databases and other intellectual property rights that, in the aggregate, are of material importance to Moody’s business. Management of Moody’s believes that each of the “Moody’s”, “Moody’s KMV” and the “M Circle Logo” trademarks and related names, marks and logos are of material importance to Moody’s. Moody’s is licensed to use certain technology and other intellectual property rights owned and controlled by others, and, similarly, other companies are licensed to use certain technology and other intellectual property rights owned and controlled by Moody’s. Moody’s considers its trademarks, service marks, databases, software and other intellectual property to be proprietary, and Moody’s relies on a combination of copyright, trademark, trade secret, patent, non-disclosure and contractual safeguards for protection.

7

In 2002, Moody’s formed two subsidiaries that hold some of its intellectual property. The first, MIS Quality Management Corp., was formed to own, manage, protect, enforce and license the trademarks of Moody’s and its affiliates. The second, Moody’s Assurance Company, Inc., is a New York State “captive” insurance company that self-insures Moody’s against certain risks and owns Moody’s ratings databases, methodologies and related software and processes in addition to other assets in support of its insurance program.

The names of Moody’s products and services referred to herein are trademarks, service marks or registered trademarks or service marks owned by or licensed to Moody’s or one or more of its subsidiaries.

Employees

As of December 31, 2005,2006, the number of full-time equivalent employees of Moody’s was approximately 2,900.3,400.

Available Information

Moody’s investor relations Internet website is http://ir.moodys.com/. Under the “SEC Filings” tab at this website, the Company makes available free of charge its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports as soon as reasonably practicable after they are filed with, or furnished to, the SEC.

10

EXECUTIVE OFFICERS OF THE REGISTRANT

Name, Age and Position | Biographical Data | |

Jeanne M. Dering, Executive Vice President, Global Regulatory Affairs and Compliance | Ms. Dering has served as the Company’s Executive Vice President, Global Regulatory Affairs and Compliance since May 2005. Previously, she had served as the Company’s Senior Vice President and Chief Financial Officer since October 1, 2000 and in February 2005 was named Executive Vice President and Chief Financial Officer. In addition, she | |

Jennifer Elliott, Vice President and Chief Human Resources Officer | Ms. Elliott has served as the Company’s Vice President and Chief Human Resources Officer since February 2005. Previously, she had served as Managing Director for Moody’s Australia since 1999 and was also a director of Moody’s Investors Service Pty Limited. She was Vice President and Senior Analyst in Moody’s Structured Finance Group from 1996 until 1999 and an Analyst in that group from 1993 until 1996. Prior thereto, she was a banking and finance lawyer in Sydney, Australia. | |

John J. Goggins, Senior Vice President and General Counsel | Mr. Goggins has served as the Company’s Senior Vice President and General Counsel since October 1, 2000. Mr. Goggins joined Moody’s Investors Service, Inc. in February 1999 as Vice President and Associate General Counsel and became General Counsel in 2000. | |

8

Linda S. Huber, Executive Vice President and Chief Financial Officer | Ms. Huber has served as the Company’s Executive Vice President and Chief Financial Officer since May 2005. Prior thereto, she served as Executive Vice President and Chief Financial Officer at U.S. Trust Company, a subsidiary of Charles Schwab & Company, Inc., from 2003 to 2005. Prior to U.S. Trust, she was Managing Director at Freeman & Co. from 1998 through 2002. She served PepsiCo as Vice President of Corporate Strategy and Development | |

11

| from 1997 until 1998 and as Vice President and Assistant Treasurer from 1994 until 1997. She served as Vice President in the Energy Investment Banking Group at Bankers Trust Company from 1991 until 1994 and as an Associate in the Energy Group at First Boston Corporation from 1986 through 1990. She also held the rank of Captain in the U.S. Army where she served from 1980 to 1984. | ||

Joseph (Jay) McCabe, Senior Vice | Mr. McCabe has served as the Company’s Senior Vice President | |

Raymond W. McDaniel, Jr., Chairman and Chief Executive Officer, Moody’s Corporation and President, Moody’s Investors Service, Inc. | Mr. McDaniel has served as the Company’s Chairman and Chief Executive Officer since April 2005. Mr. McDaniel served as the Company’s President from October 2004 to April 2005 and as Chief Operating Officer from January 2004 to April 2005. He has served as a member of the Board of Directors since April 2003 and President of Moody’s Investors Service, Inc. since November 2001. Mr. McDaniel also served as Executive Vice President of the Company from April 2003 to January 2004 and Senior Vice President from October 1, 2000 until April 2003. He served as Senior Managing Director, Global Ratings and Research, of Moody’s Investors Service, Inc., from November 2000 until November 2001. Prior thereto, he had served as Managing Director, International, since 1996 and served as Managing Director, Europe, from 1993 until 1996. He also served as Associate Director in Moody’s Structured Finance Group from 1989 until 1993, and as Senior Analyst in the Mortgage Securitization Group from 1988 to 1989. Mr. McDaniel is also a director of John Wiley & Sons, Inc. | |

| Mr. | |

129

ITEM 1A. RISK FACTORS

| ITEM 1A. | RISK FACTORS |

The following risk factors and other information included in this annual report on Form 10-K should be carefully considered. The risks and uncertainties described below are not the only ones the Company faces. Additional risks and uncertainties not presently known to the Company or that the Company’s management currently deems minor or insignificant also may impair its business operations. If any of the following risks occur, Moody’s business, financial condition, operating results and cash flows could be materially adversely affected.

Changes in the Volume of Debt Securities Issued in Domestic and/or Global Capital Markets and Changes in Interest Rates and Other Volatility in the Financial Markets

Approximately 80% of Moody’s revenue in 20052006 was derived from ratings, a significant portion of which was related to the issuance of credit-sensitive securities in the global capital markets. Moody’s revenue growth from these sources in 2005 was in line with its compound annual growth rate from 2001 through 2004 as continued strength in global structured finance, strong financial institutions issuance and ratings of bank credit facilities was partially offset by the impacts of declines in U.S. high yield issues and in investment grade corporate finance issuance volumes in the U.S. and Europe. The Company anticipates that a substantial part of its business will continue to be dependent on the number and dollar volume of debt securities issued in the capital markets. Therefore, the Company’s results could be adversely affected by a reduction in the level of debt issuance.

Unfavorable financial or economic conditions that either reduce investor demand for debt securities or reduce issuers’ willingness or ability to issue such securities could reduce the number and dollar volume of debt issuance for which Moody’s provides ratings services. In addition, increases in interest rates or credit spreads, volatility in financial markets or the interest rate environment, significant regulatory, political or economic events, defaults of significant issuers and other market and economic factors may negatively impact the general level of debt issuance, the debt issuance plans of certain categories of borrowers, and/or the types of credit-sensitive products being offered. A sustained period of market decline or weakness could also have a material adverse effect on Moody’s business and financial results.

Possible Loss of Market Share or Revenue Through Competition or Regulation

The markets for credit ratings, research and credit risk management services are increasingly competitive. Moody’s competes on the basis of a number of factors, including quality of ratings, clientcustomer service, research, reputation, regulatory qualification, price, geographic scope, range of products and technological innovation. For example, a large investment grade default could impact the Company’s reputation and potentially lead to greater regulatory oversight. Moody’s faces increasing competition from, among others, S&P, Fitch, DBRS, local rating agencies in a number of international jurisdictions and niche companies that provide ratings for particular types of financial products or issuers (such as A.M. Best Company, Inc., with respect to the insurance industry). Since Moody’s believes that some of its most significant challenges and opportunities will arise outside the U.S., it will have to compete with rating agencies that may have a stronger local presence or a longer operating history in those markets. These local providers or comparable competitors that may emerge in the future may receive support from local governments or other institutions that Moody’s does not receive.

Currently, Moody’s, S&P, Fitch, DBRS and A.M. Best Company, Inc. are designated as NRSROs by the SEC. In March 2005,September 2006, the United States Congress passed into law the Credit Rating Agency Reform Act of 2006. As a direct result, the SEC disclosed that in consideringis mandated to complete a rule-making process which implements the oversight of NRSROs, it may pursue a voluntary compliance and oversight frameworklegislation (see “Regulation”, above, for rating agencies that are designated as NRSROs, or it could seek legislative authority for formal compliance and oversight for NRSROs.

In April 2005, the SEC released for public comment a Proposed Rule on the “Definition of Nationally Recognized Statistical Rating Organization”. The proposed definition of the term NRSRO is an entity that: (i) issues publicly available credit ratings that are current assessments of the creditworthiness of obligors with respect to specific securities or money market instruments; (ii) is generally accepted in the financial markets as an issuer of credible and reliable ratings, including ratings for a particular industry or geographic segment,further information) by the predominant users of securities ratings; and (iii) uses systematic procedures designed to ensure credible and

13

reliable ratings, manage potential conflicts of interest, and prevent the misuse of nonpublic information, and has sufficient financial resources to ensure compliance with those procedures. Numerous market participants, including Moody’s, responded to the request for comment. Moody’s response can be found on theRegulatory Affairs page of the Company’s website.

In addition, in June 2005 the SEC produced technical assistance pursuant to a congressional request, relating to statutory authority that the SEC may need if Congress determines that it is appropriate to create a comprehensive oversight regime for credit rating agencies. Congress had also requested that market participants provide their views on the SEC’s technical assistance. Moody’s comments can be found on theRegulatory Affairs page of the Company’s website.

2007. At present, Moody’s is unable to assess the likelihoodimpact of any regulatory changes that may result from the SEC’s ongoing review. However, the elimination of the NRSRO concept, retention of the NRSRO concept with different regulatory oversight, or SEC recognition of additional NRSROs could result in loss of market share or revenue for Moody’s, or higher costs of operations.rule-making process.

Introduction of Competing Products or Technologies by Other Companies

The markets for credit ratings, research and credit risk management services are increasingly competitive. The ability to provide innovative products and technologies that anticipate customers’ changing requirements and to utilize emerging technological trends is a key factor in maintaining market share. Competitors may develop quantitative methodologies or related services for assessing credit risk that customers and market participants may deem preferable, more cost-effective or more valuable than the credit risk assessment methods currently employed by Moody’s. Moody’s growth prospects could also be adversely affected by limitations of its information technologies that fail to provide adequate capacity and capabilities to meet increased demands of producing quality ratings and research products.

Increased Pricing Pressure from Competitors and/or Customers

In the credit rating, research and credit risk management markets, competition for customers and market share has spurred more aggressive tactics by some competitors in areas such as pricing and service. While Moody’s seeks to compete primarily on the basis of the quality of its products and service, if its pricing and services are not sufficiently competitive with its current and future competitors, Moody’s may lose market share.

10

Possible Loss of Key Employees to Investment or Commercial Banks or Elsewhere and Related Compensation Cost Pressures

Moody’s success depends in part upon recruiting and retaining highly skilled, experienced financial analysts and other professionals. Competition for qualified staff in the financial services industry is intense, and Moody’s ability to attract staff could be impaired if it is unable to offer competitive compensation and other incentives. Investment banks and other competitors for analyst talent may be able to offer higher compensation than Moody’s. Moody’s also may not be able to identify and hire employees in some markets outside the U.S. with the required experience or skills to perform sophisticated credit analysis. Moody’s may lose key employees due to other factors, such as catastrophes, that could lead to disruption of business operations. Moody’s ability to compete effectively will continue to depend, among other things, on its ability to attract new employees and to retain and motivate existing employees.

Exposure to Litigation Related to Moody’s Rating Opinions

Moody’s faces litigation from time to time from parties claiming damages relating to ratings actions. In addition, as Moody’s international business expands, these types of claims may increase because foreign jurisdictions may not have legal protections or liability standards comparable to those in the U.S. (such as protections for the expression of credit opinions as is provided by the First Amendment). These risks often may be difficult to assess or quantify and their existence and magnitude often remains unknown for substantial periods of time.

14

Potential Emergence of Government-Sponsored Credit Rating Agencies

When governments adopt regulations that require debt securities to be rated, establish criteria for credit ratings or authorize only certain entities to provide credit ratings, the competitive balance among rating agencies and the level of demand for ratings may be positively or negatively affected. Government-mandated ratings criteria may also have the effect of displacing objective assessments of creditworthiness. In these circumstances, debt issuers may be less likely to base their choice of rating agencies on criteria such as independence and credibility, and more likely to base their choice on their assumption as to which credit rating agency might provide a higher rating, which may negatively affect the Company.

Potential for New U.S., Foreign, State and Local Legislation and Regulations, Including Those Relating to Nationally Recognized Statistical Rating Organizations

In the United States and other countries, the laws and regulations applicable to credit ratings and rating agencies continue to evolve and are presently subject to review by a number of legislative or regulatory bodies, including the SEC in the United States and the CESR on behalf of the European Union. It is possible that such reviews could lead to greater oversight or regulation concerning the issuance of credit ratings or the activities of credit rating agencies. Such additional regulations could, potentially, increase the costs associated with the operation of a credit rating agency, alter the rating agencies’ communications with the issuers as part of the rating assignment process, increase the legal risk associated with the issuance of credit ratings, change the regulatory framework to which credit rating agencies are subject and/or affect the competitive environment in which credit rating agencies operate. A description of certain of the more recent regulatory initiatives in the United States and other countries is described above under the section entitled “Regulation” in Item 1,1. “Business”, of this Form 10-K. At present, Moody’s is unable to predict the regulatory changes that may result from ongoing reviews by the SEC or other regulatory bodies or the effect that any such changes may have on its business.

Exposure to Increased Risk from Multinational Operations

Moody’s maintains offices outside the U.S. and derives a significant portion of its revenue from sources outside the U.S. operationsOperations in different countries expose Moody’s to a number of legal, economic and regulatory risks such as:

changes in legal and regulatory requirements affecting either Moody’s operations or its customers’ use of ratings

possible nationalization, expropriation, price controls and other restrictive governmental actions

restrictions on the ability to convert local currency into U.S. dollars

currency fluctuations

export and import restrictions, tariffs and other trade barriers

difficulty in staffing and managing offices as a result of, among other things, distance, travel, cultural differences and intense competition for trained personnel

longer payment cycles and problems in collecting receivables

11

political and economic instability

potentially adverse tax consequences

Any of these factors could have a material adverse effect on the business, financial condition and results of operations of the Company in the future.

15

ITEM 1B. UNRESOLVED STAFF COMMENTS

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

| ITEM 2. | PROPERTIES |

ITEM 2. PROPERTIES

The executive offices of Moody’s arecorporate headquarters is located at 99 Church Street, New York, New York, with approximately 441,000 square-feet. During the fourth quarter of 2006, the Company completed the sale of its corporate headquarters and is leasing back the building until the headquarters relocation is completed. On October 20, 2006, the Company entered into an operating lease agreement with 7 World Trade Center, LLC for 589,945 square-feet of an office building located at 7 World Trade Center at 250 Greenwich Street, New York, New York, which will serve as Moody’s new headquarters beginning in a 297,000-square-foot property owned by Moody’s.mid- to late 2007. As of December 31, 2006, Moody’s operations are alsowere conducted from 11 other15 U.S. offices and 3032 non-U.S. office locations, all of which are leased. These other properties are geographically distributed to meet operating and sales requirements worldwide. These properties are generally considered to be both suitable and adequate to meet current operating requirements and virtually all space is being utilized.

ITEM 3. LEGAL PROCEEDINGS

| ITEM 3. | LEGAL PROCEEDINGS |

From time to time, Moody’s is involved in legal and tax proceedings, claims and litigation that are incidental to the Company’s business, including claims based on ratings assigned by Moody’s. Moody’s is also subject to ongoing tax audits in the normal course of business. Management periodically assesses the Company’s liabilities and contingencies in connection with these matters based upon the latest information available. Moody’s discloses material pending legal proceedings, other than routine litigation incidental to Moody’s business, material proceedings known to be contemplated by governmental authorities, and other pending matters that it may determine to be appropriate. For those matters where it is both probable that a liability has been incurred and the amount of loss can be reasonably estimated, the Company has recorded reserves in the consolidated financial statements and periodically adjusts these reserves as appropriate. In other instances, because of the uncertainties related to both the probable outcome and/or the amount or range of loss, management does not record a liability but discloses the contingency if significant. As additional information becomes available, the Company adjusts its assessments and estimates of such liabilities accordingly.

The discussion of the litigationlegal matters under the heading “Legacy Contingencies” underPart II, Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations”Operations—Contingencies”, commencing aton page 3528 of this annual report on Form 10-K, is incorporated into this Item 3 by reference.

Based on its review of the latest information available, in the opinion of management, the ultimate liability of the Company in connection with pending legal and tax proceedings, claims and litigation will not have a material adverse effect on Moody’s financial position, results of operations or cash flows, subject to the contingencies described in Part II, Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Operations—Contingencies”.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

During the fourth quarter of the fiscal year covered by this annual report on Form 10-K, no matter was submitted to a vote of security holders.

1612

PART II

ITEM 5. MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED SHAREHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

| ITEM 5. | MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED SHAREHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES. |

Information in response to this Item is set forth under the captions “Common Stock Information” and “Dividends” in Item 7 of this annual report on Form 10-K.10-K, and under the caption “Equity Compensation Plan Information” in the Company’s definitive proxy statement for use in connection with its annual meeting of stockholders scheduled to be held on April 24, 2007, and is incorporated herein by reference.

MOODY’S PURCHASES OF EQUITY SECURITIES

For the Three Months Ended December 31, 20052006

Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Program | Approximate Dollar Value of Shares That May yet be Purchased Under the Program (1) | |||||||

October 1 - 31 | 3,870,122 | (2) | $ | 51.00 | 3,869,900 | $ | 1,022.0 million | ||||

November 1 - 30 | 1,610,352 | $ | 55.34 | 1,610,352 | $ | 932.9 million | |||||

December 1 - 31 | 1,262,619 | $ | 60.95 | 1,262,619 | $ | 856.0 million | |||||

Total | 6,743,093 | 6,742,871 | |||||||||

Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Program | Approximate Dollar Value of Shares That May yet be Purchased Under the Program (2) | |||||||

October 1 – 31 | 971,702 | (1) | $ | 63.44 | 971,479 | $ | 1,850.3 million | ||||

November 1 – 30 | 722,982 | (1) | 67.23 | 722,016 | 1,801.8 million | ||||||

December 1 – 31 | 562,500 | 69.99 | 562,500 | 1,762.4 million | |||||||

Total | 2,257,184 | 2,255,995 | |||||||||

| (1) |

| Includes the surrender to the Company of |

| (2) | As of the last day of each of the months. On June 5, 2006, the Board of Directors authorized a $2 billion share repurchase program. There is no established expiration date for this authorization. During August 2006, the Company had completed its previous $1 billion share repurchase program, which had been authorized by the Board of Directors in October 2005. |

During the fourth quarter of 2005,2006, Moody’s repurchased 6.72.3 million shares at an aggregate cost of $363.4$149.6 million and issued 1.61.1 million shares of stock under employee stockstock-based compensation plans. Since becoming a public company in October 2000 and through December 31, 2005,2006, Moody’s has repurchased 66.484.4 million shares at a total cost of $1.8$2.9 billion, including 32.138.6 million shares to offset issuances under employee stockstock-based compensation plans.

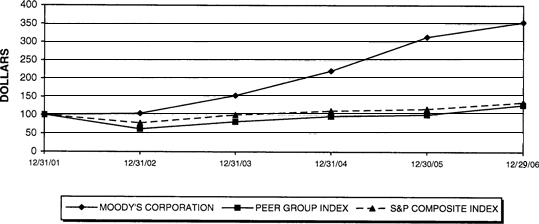

PERFORMANCE GRAPH

17The following graph compares the total cumulative shareholder return of the Company to the performance of Standard & Poor’s Stock 500 Index (the “S&P 500”) and an index of performance peer group companies (the “Performance Peer Group”).

The Company does not believe there are any publicly traded companies that represent strict peers. However, each of the companies in the Performance Peer Group offers business information products in one or more segments of its business. The Performance Peer Group consists of Dow Jones & Company, Inc., The McGraw-Hill Companies, Pearson PLC, Reuters Group PLC, Thomson Corporation and Wolters Kluwer nv.

The comparison assumes that $100.00 was invested in the Company’s common stock (the “Common Stock”) and in each of the foregoing indices on December 31, 2001. The comparison also assumes the reinvestment of dividends, if any. The total return for the Common Stock was 254% during the performance period as compared with a total return during the same period of 35% for the S&P 500 and 27% for the Performance Peer Group.

COMPARISON OF CUMULATIVE TOTAL RETURN

SINCE DECEMBER 31, 2001

MOODY’S CORPORATION, S&P COMPOSITE INDEX AND PEER GROUP INDEX

| PERIOD ENDING | ||||||||||||

| 12/31/2001 | 12/31/2002 | 12/31/2003 | 12/31/2004 | 12/30/2005 | 12/29/2006 | |||||||

Moody's Corporation | 100.00 | 104.01 | 153.07 | 220.51 | 313.63 | 354.23 | ||||||

Peer Group Index | 100.00 | 61.80 | 81.57 | 96.18 | 100.97 | 127.43 | ||||||

S&P Composite Index | 100.00 | 77.90 | 100.25 | 111.15 | 116.61 | 135.03 | ||||||

The comparisons in the graph above are provided in response to disclosure requirements of the SEC and are not intended to forecast or be indicative of future performance of the Common Stock.

13

ITEM 6. SELECTED FINANCIAL DATA

| ITEM 6. | SELECTED FINANCIAL DATA |

The Company’s selected consolidated financial data should be read in conjunction with Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the Moody’s Corporation consolidated financial statements and notes thereto.

| Year Ended December 31, | Year Ended December 31, | |||||||||||||||||||||||||||||||||||||||

amounts in millions, except per share data | 2005 | 2004 | 2003 | 2002 | 2001 | 2006 | 2005 | 2004 | 2003 | 2002 (1) | ||||||||||||||||||||||||||||||

Results of operations | ||||||||||||||||||||||||||||||||||||||||

Revenue | $ | 1,731.6 | $ | 1,438.3 | $ | 1,246.6 | $ | 1,023.3 | $ | 796.7 | $ | 2,037.1 | $ | 1,731.6 | $ | 1,438.3 | $ | 1,246.6 | $ | 1,023.3 | ||||||||||||||||||||

Expenses | 792.0 | 651.9 | 583.5 | 485.2 | 398.2 | |||||||||||||||||||||||||||||||||||

Expenses, excluding gain on sale of building | 938.2 | 792.0 | 651.9 | 583.5 | 485.2 | |||||||||||||||||||||||||||||||||||

Gain on sale of building (2) | (160.6 | ) | — | — | — | — | ||||||||||||||||||||||||||||||||||

Operating income | 939.6 | 786.4 | 663.1 | 538.1 | 398.5 | 1,259.5 | 939.6 | 786.4 | 663.1 | 538.1 | ||||||||||||||||||||||||||||||

Non-operating expense, net (2) | (4.9 | ) | (15.1 | ) | (6.7 | ) | (20.7 | ) | (16.6 | ) | ||||||||||||||||||||||||||||||

Non-operating income (expense), net (3) | 1.0 | (4.9 | ) | (15.1 | ) | (6.7 | ) | (20.7 | ) | |||||||||||||||||||||||||||||||

Income before provision for income taxes | 934.7 | 771.3 | 656.4 | 517.4 | 381.9 | 1,260.5 | 934.7 | 771.3 | 656.4 | 517.4 | ||||||||||||||||||||||||||||||

Provision for income taxes | 373.9 | 346.2 | 292.5 | 228.5 | 169.7 | 506.6 | 373.9 | 346.2 | 292.5 | 228.5 | ||||||||||||||||||||||||||||||

Net income | $ | 560.8 | $ | 425.1 | $ | 363.9 | $ | 288.9 | $ | 212.2 | $ | 753.9 | $ | 560.8 | $ | 425.1 | $ | 363.9 | $ | 288.9 | ||||||||||||||||||||

Earnings per share (3) | ||||||||||||||||||||||||||||||||||||||||

Earnings per share (4) | ||||||||||||||||||||||||||||||||||||||||

Basic | $ | 1.88 | $ | 1.43 | $ | 1.22 | $ | 0.94 | $ | 0.67 | $ | 2.65 | $ | 1.88 | $ | 1.43 | $ | 1.22 | $ | 0.94 | ||||||||||||||||||||

Diluted | $ | 1.84 | $ | 1.40 | $ | 1.19 | $ | 0.92 | $ | 0.66 | $ | 2.58 | $ | 1.84 | $ | 1.40 | $ | 1.19 | $ | 0.92 | ||||||||||||||||||||

Weighted average shares outstanding (3) | ||||||||||||||||||||||||||||||||||||||||

Weighted average shares outstanding (4) | ||||||||||||||||||||||||||||||||||||||||

Basic | 297.7 | 297.0 | 297.8 | 307.8 | 315.2 | 284.2 | 297.7 | 297.0 | 297.8 | 307.8 | ||||||||||||||||||||||||||||||

Diluted | 305.6 | 304.7 | 304.6 | 315.0 | 320.4 | 291.9 | 305.6 | 304.7 | 304.6 | 315.0 | ||||||||||||||||||||||||||||||

Dividends declared per share | $ | 0.24 | $ | 0.15 | $ | 0.11 | $ | 0.09 | $ | 0.09 | $ | 0.29 | $ | 0.24 | $ | 0.15 | $ | 0.11 | $ | 0.09 | ||||||||||||||||||||

| Year Ended December 31, | Year Ended December 31, | |||||||||||||||||||||||||||||||||||||||

| 2005 | 2004 | 2003 | 2002 | 2001 | 2006 | 2005 | 2004 | 2003 | 2002 | |||||||||||||||||||||||||||||||

Balance sheet data | ||||||||||||||||||||||||||||||||||||||||

Total assets (4) | $ | 1,457.2 | $ | 1,389.3 | $ | 959.9 | $ | 633.7 | $ | 505.4 | ||||||||||||||||||||||||||||||

Total assets | $ | 1,497.7 | $ | 1,457.2 | $ | 1,389.3 | $ | 959.9 | $ | 633.7 | ||||||||||||||||||||||||||||||

Long-term debt (5) | $ | 300.0 | $ | — | $ | 300.0 | $ | 300.0 | $ | 300.0 | $ | 300.0 | $ | 300.0 | $ | — | $ | 300.0 | $ | 300.0 | ||||||||||||||||||||

Shareholders’ equity (deficit) | $ | 309.4 | $ | 317.5 | $ | (32.1 | ) | $ | (327.0 | ) | $ | (304.1 | ) | $ | 167.4 | $ | 309.4 | $ | 317.5 | $ | (32.1 | ) | $ | (327.0 | ) | |||||||||||||||

| (1) | The 2002 results of operations include revenue of $42.1 million, expenses of $42.8 million and an operating loss of $0.7 million related to KMV, which was acquired in April 2002. |

| (2) |

| (3) | The 2003 amount |

| Prior period earnings per share and weighted average shares outstanding have been adjusted to reflect the May 2005 2-for-1 stock split. |

| (5) | At December 31, 2004, the notes payable scheduled to mature in September 2005 were classified as a current liability. |

1814

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

This discussion and analysis of financial condition and results of operations should be read in conjunction with the Moody’s Corporation consolidated financial statements and notes thereto included elsewhere in this annual report on Form 10-K.

This Management’s Discussion and Analysis of Financial Condition and Results of Operations contains Forward-Looking Statements. See “Forward-Looking Statements” commencing on page 3931 and Item 1A,1A. “Risk Factors” commencing on page 1310 for a discussion of uncertainties, risks and other factors associated with these statements.

The Company

Except where otherwise indicated, the terms “Moody’s” and the “Company” refer to Moody’s Corporation and its subsidiaries. Moody’s is a provider of (i) credit ratings, research and analysis covering fixed incomefixed-income securities, other debt instruments and the entities that issue such instruments in the global capital markets, and credit training services, and (ii) quantitative credit risk assessment products and services and credit processing software for banks, corporations and investors in credit-sensitive assets. Moody’s operates in two reportable segments: Moody’s Investors Service and Moody’s KMV.

Moody’s Investors Service publishes rating opinions on a broad range of credit obligors and credit obligations issued in domestic and international markets, including various corporate and governmental obligations, structured finance securities and commercial paper programs. It also publishes investor-oriented credit information, research and economic commentary, including in-depth research on major debt issuers, industry studies, special comments and credit opinion handbooks.

The Moody’s KMV business develops and distributes quantitative credit risk assessment products and services and credit processing software for banks, corporations and investors in credit-sensitive assets.