the emergence of newer, more competitive technologies and products.

We have no experience manufacturing our products on a large-scale commercial basis and may be unable to do so.

To date, we have focused primarily on research, development and low volumelow-volume manufacturing and have no experience manufacturing our products on a large-scale commercial basis. In 2000, we completed construction of our 50,000 square foot manufacturing facility, and have continued to develop our manufacturing capabilities and processes. We do not know whether or when we will be able to develop efficient, low-cost manufacturing capabilities and processes that will enable us to manufacture our products in commercial quantities while meeting the quality, price, engineering, design and production standards required to successfully market our products. Our failure to develop such manufacturing processes and capabilities could have a material adverse effect on our business, financial condition and results of operations. Even if we are successful in developing our manufacturing capabilities and processes, we do not know whether we will do so in time to meet our product commercialization schedule or to satisfy the requirements of our distributors or customers.

We have not developed andor produced the products that we have agreed to sell to GE Fuel Cell Systems.

Our distribution agreement with GEFCS has been amended on a numbersome of occasions, most recently in April 2005. The amendments to our distribution agreement permit us the ability to sell directly or negotiate nonexclusive distribution rights to third parties for our GenCore® back-up power product line, our GenSite™ hydrogen generation product line and our GenSys® prime power product line (for telecommunication and broadband applications). In exchange, starting in the fourth quarter of 2005 we are required to pay a 5% commission for GenCore®, and starting in the fourth quarter of 2005 we are required to pay a 5% commission for GenSite™, in each case based on sales price, to GEFCS. We are also required to pay a 5% commission for GenSys® sales beginning in the fourth quarter of 2006. The distribution agreement expires on December 31, 2014.distributors.

We have not developed or produced certain products meeting all specificationsthat are required by the GEFCSsome of our distribution agreement.agreements, including those with Smartlink, IST, Tyco, and Logan Energy Systems. There can be no assurance that we will complete development of products meeting specifications required by GEFCSthese distributor agreements and deliver them on schedule. Pursuant to these distribution agreements, the distribution agreement, GEFCS hasdistributors have the right to provide notice to us if, in its good faiththeir judgment, we have materially deviated from the multi-generation product plan in the distribution agreement. Should GEFCSa distributor provide such notice, and we cannot mutually agree to a modification to the multi-generation product plan,distributor agreement, then GEFCSthe distributor has the right to terminate the distribution agreement for cause, subjectcause.

Our orders may not ship or convert to revenue.

We have accepted orders from our rightsdistributors, which include firm orders, stocking orders and orders that require certain conditions or contingencies to cure. In addition, GEFCS has the rightbe satisfied prior to terminate the distribution agreement for cause if we fail to provide GEFCS with products that, in GEFCS’ reasonable judgment,shipment, some of which are materially competitive with alternative PEM fuel cell-powered generator sets, subject to our rights to cure.

GE Energy, the operating business of General Electric Company, which controls GEFCS through GE MicroGen, has agreed not to sell or distribute PEM fuel cell systems and related components manufactured by parties other than us through any entity other than GEFCS. GE Energy is not, however, prohibited from developing non-PEM fuel cell systems and other distributed energy systems and products that would compete directly or indirectly against our PEM fuel cell systems or other products we may manufacture. GE Energy is not required to provide us with any information concerning the developments of such products, or plans or intentions to manufacture such products by GE Energy. The development of different energy product solutions by GE Energy could harm the marketabilityoutside of our technologycontrol. Historically, shipments made against these orders can occur between thirty (30) days and twenty-four (24) months from the date of acceptance of the order. Orders received during the year ended December 31, 2006 were 539. Backlog on December 31, 2006 was 572 units. Of the unit orders in backlog on December 31, 2006, orders for 103 units were older than 12 months. The time periods from receipt of an order to shipment date and installation date vary widely and are determined by providing potential customers with an alternative to our products.

As discussed above in “Distribution, Marketing and Strategic Relationships” we are currently in discussion with GE to restructure our agreements,a number of factors, including the distribution agreement,terms of the customer contract and cannot predict the outcomecustomer’s deployment plan. Orders include firm orders, stocking orders and orders that require certain conditions or contingencies and certain redesign elements to be satisfied prior to shipment, some of those discussions.which are outside of the Company’s control. Some or all of our current and future orders may not result in an actual shipment and therefore not convert to revenue.

Delays in our product development wouldcould have a material impact on our commercialization schedule.

If we experience delays in meeting our development goals, or if our products exhibit technical defects or if we are unable to meet cost or performance goals, including power output, useful life and reliability, our commercialization schedule will be delayed. In this event, potential purchasers of our products may choose alternative technologies, and any delays could allowallowing potential competitors to gain market advantages. We cannot assure you that we will successfully meet our commercialization schedule in the future.

We may need to secure additional funding to complete our product development and commercialization plans and we may be unable to raise additional capital.

Our cash requirements depend on numerous factors, including completion of our product development activities, ability to commercialize our products and market acceptance of our products. We expect to devote substantial capital resources to continue development programs, establish a manufacturing infrastructure and develop manufacturing processes. Additionally, we expect to devote substantial capital resources to expand our marketing organization and establish a sales organization. Weorganizations. Despite the infusion of equity capital from our transaction with Smart Hydrogen Inc. in June 2006, we may need to raise additional funds to achieve commercialization of our products. However, we do not know whether we will be able to secure additional funding or funding on acceptable terms to pursue

our commercialization plans. If additional funds are raised through the issuance of equity securities, the percentage ownership of our then current stockholders will be reduced. If adequate funds are not available to satisfy either short-term or long-term capital requirements, we may be required to limit operations in a manner inconsistent with our development and commercialization plans, which could affect operations in future periods.

We may be unable to establish relationships, or we may lose existing relationships, with third parties for certain aspects of product development, manufacturing, distribution and servicing and the supply of key components for our products.

We will need to enter into additional strategic relationships in order to complete our current product development and commercialization plans. We will also require partners to assist in the distribution, servicing and supply of components for our anticipated back-up power and on-site hydrogen generation products, both of which are in development. If we are unable to identify or enter into satisfactory agreements with potential partners, including those relating to the distribution of and service and support for our anticipated back-up power and on-site hydrogen generation products, we may not be able to complete our product development and commercialization plans on schedule, or at all. We may also need to scale back these plans in the absence of needed partners, which would adversely affect our future prospects for development and commercialization of future products. In addition, any arrangement with a strategic partner may require us to issue a significant amount of equity securities to the partner, provide the partner with representation on our board of directors and/or commit significant financial resources to fund our product development efforts in exchange for their assistance or the contribution to us of intellectual property. Any such issuance of equity securities would reduce the percentage ownership of our then current stockholders. While we have entered into relationships with suppliers of some key components for our products, we do not know when or whether we will secure supply relationships for all required components and subsystems for our products, or whether such relationships will be on terms that will allow us to achieve our objectives. Our business, prospects, results of operations and financial condition could be harmed if we fail to secure relationships with entities which can develop or supply the required components for our products and provide the required distribution and servicing support. Additionally, the agreements governing our current relationships allow for termination by our partners under certain circumstances. If any of our current strategic partners was to terminate any of its agreements with us, there could be a material adverse impact on the development and commercialization of our products and the operation of our business, financial condition, results of operations and prospects.

We will rely on our partners to develop and provide components for our products.

A supplier’s failure to develop and supply components in a timely manner, or at all, or to develop or supply components that meet our quality, quantity or cost requirements, or our inability to obtain substitute sources of these components on a timely basis or on terms acceptable to us, could harm our ability to manufacture our products. In addition, to the extent that our supply partners use technology or manufacturing processes that are proprietary, we may be unable to obtain comparable components from alternative sources.

We face intense competition and may be unable to compete successfully.

The markets for on-site energy products are intensely competitive. There are a number of companies located in the United States, Canada and abroad that are developing PEM and other fuel cell technologies and energy products that compete with our products. Some of our competitors in the fuel cell sector are much larger than we are and may have the manufacturing, marketing and sales capabilities to complete research, development and commercialization of commercially viable fuel cell products more quickly and effectively than we can.

In addition, there are many companies engaged in all areas of traditional and alternative energy generation in the United States, Canada and abroad, including, among others, major electric, oil, chemical, natural gas, batteries, generatorsbattery, generator and specialized electronics firms, as well as universities, research institutions and foreign government-sponsored companies. These firms are engaged in forms of power generation such as solar and wind

power, reciprocating engines and microturbines, as well as traditional grid-supplied electric power. Many of these entities have substantially greater financial, research and development, manufacturing and marketing resources than we do.

We must lower the cost of our products and demonstrate their reliability.

Our initial fuel cell systems currently cost significantly more than many established competing technologies. If we are unable to develop products that are competitive with competing technologies in terms of price, reliability and longevity, consumers will be unlikely to buy our products. The price of our products depends largely on material and manufacturing costs. We cannot guarantee that we will be able to lower these costs to the level where we will be able to produce a competitive product or that any product produced using lower cost materials and manufacturing processes will not suffer from a reduction in performance, reliability and longevity.

Failure of our field tests could negatively impact demand for our products.

We are currently field-testing a number of our products and we plan to conduct additional field tests in the future. We may encounter problems and delays during these field tests for a number of reasons, including the failure of our technology or the technology of third parties, as well as our failure to maintain and service our products properly. Many of these potential problems and delays are beyond our control. Any problem or perceived problem with our field tests could materially harm our reputation and impair market acceptance of, and demand for, our products.

Further regulatory changes and electric utility industry restructuring may affect demand for our products.

The market for electric power generation products is heavily influenced by federal and state governmental regulations and policies concerning the electric utility industry.and telecommunications industries. A change in the current regulatory policies could deter further investment in the research and development of alternative energy sources, including fuel cells, and could result in a significant reduction in the demand for our products. We cannot predict how deregulation or restructuring of the industry will affect the market for our products.

Our business may become subject to future government regulation, which may impact our ability to market our products.

Our products will be subject to federal, local, and non-U.S. laws and regulations, including, for example, state and local ordinances relating to building codes, public safety, electrical and gas pipeline connections, hydrogen transportation and siting and related matters. Further, as products are introduced into the market commercially, governments may impose new regulations. We do not know the extent to which any such regulations may impact our ability to distribute, install and service our products. Any regulation of our products, whether at the federal, state, local or foreign level, including any regulations relating to installation and servicing of our products, may increase our costs and the price of our products.

Utility companies could place barriers on our entry into the marketplace where customers depend on traditional grid supplied energy.

Utility companies often charge fees to industrial companies for disconnecting from the grid, for using less electricity or for having the capacity to use power from the grid for back-up purposes and may charge similar fees to residential customers in the future. The imposition of such fees could increase the cost to grid-connected customers of using our products and could make our products less desirable, thereby harming our revenue and profitability.

Alternatives to our technology or improvements to traditional energy technologies could make our products less attractive or render them obsolete.

Our products are among a number of alternative energy products being developed. A significant amount of public and private funding is currently directed toward development of microturbines, solar power, wind power and other types of fuel cell technologies. Improvements are also being made to the existing electric transmission system. Technological advances in alternative energy products, improvements in the electric power grid or other fuel cell technologies may make our products less attractive or render them obsolete.

The hydrocarbon fuels and other raw materials on which our products rely may not be readily available or available on a cost-effective basis.

Our products depend largely on the availability of natural gas, liquid propane and hydrogen gas. If these fuels are not readily available, or if their prices are such that energy produced by our products costs more than energy provided by other sources, our products could be less attractive to potential users.

In addition, platinum is a key material in our PEM fuel cells. Platinum is a scarce natural resource and we are dependent upon a sufficient supply of this commodity. Any shortages could adversely affect our ability to produce commercially viable fuel cell systems and significantly raise our cost of producing our fuel cell systems.

Our products use flammable fuels that are inherently dangerous substances.

Our fuel cell systems use natural gas, liquid propane and hydrogen gas in catalytic reactions, which produce less heat than a typical gas furnace. While our products do not use this fuel in a combustion process, natural gas, liquid propane and hydrogen gas are flammable fuels that could leak in a home or office and combust if ignited by another source. Further, while we are not aware of any accidents involving our products, any such accidents involving our products or other products using similar flammable fuels could materially suppress demand for, or heighten regulatory scrutiny of, our products.

Product liability or defects could negatively impact our results of operations.

Any liability for damages resulting from malfunctions or design defects could be substantial and could materially adversely affect our business, financial condition, results of operations and prospects. In addition, a

well-publicized actual or perceived problem could adversely affect the market’s perception of our products resulting in a decline in demand for our products and could divert the attention of our management, which may materially and adversely affect our business, financial condition, results of operations and prospects.

Future acquisitions may disrupt our business, distract our management and reduce the percentage ownership of our stockholders.

As part of our business strategy we may engage in acquisitions that we believe will provide us with complementary technologies, products, channels, revenue streams, expertise and/or other valuable assets. However, we may not be able to identify suitable acquisition candidates. If we do identify suitable candidates, we may not be able to acquire them on commercially acceptable terms, or at all. If we acquire another company, we may not be able to successfully integrate the acquired business into our existing business in a timely and non-disruptive manner. We may have to devote a significant amount of time and management and financial resources to do so. Even with this investment of management and financial resources, an acquisition may not produce the desired revenues, earnings or business synergies. In addition, an acquisition may reduce the percentage ownership of our then current stockholders. If we fail to integrate the acquired business effectively, or if key employees of that business leave, the anticipated benefits of the acquisition would be jeopardized. The time, capital and management and other resources spent on an acquisition that fails to meet our expectations could cause our business and financial condition to be materially and adversely affected. In addition, from an accounting perspective, acquisitions can involve non-recurring charges and amortization or impairment of significant amounts of intangible assets that could adversely affect our results of operations.

We may not be able to protect important intellectual property, and we could incur substantial costs defending against claims that our products infringe on the proprietary rights of others.

PEM fuel cell technology was first developed in the 1950s, and fuel processing technology has been practiced on a large scale in the petrochemical industry for decades. Accordingly, we do not believe that we can establish a significant proprietary position in the fundamental component technologies in these areas. However, our ability to compete effectively will depend, in part, on our ability to protect our proprietary system-level technologies, systems designs and manufacturing processes. We rely on patents, trademarks, and other policies and procedures related to confidentiality to protect our intellectual property. However, some of our intellectual property is not covered by any patent or patent application. Moreover, we do not know whether any of our pending patent applications will issuebe issued or, in the case of patents issued or to be issued, that the claims allowed are or will be sufficiently broad to protect our technology or processes. Even if all of our patent applications are issued and are sufficiently broad, our patents may be challenged or invalidated. We could incur substantial costs in prosecuting or defending patent infringement suits or otherwise protecting our intellectual property rights. While we have attempted to safeguard and maintain our proprietary rights, we do not know whether we have been or will be completely successful in doing so. Moreover, patent applications filed in foreign countries may be subject to laws, rules and procedures that are substantially different from those of the United States, and any resulting foreign patents may be difficult and expensive to enforce. In addition, we do not know whether the U.S. Patent & Trademark Office will grant federal registrations based on our pending trademark applications. Even if federal registrations are granted to us, our trademark rights may be challenged. It is also possible that our competitors or others will adopt trademarks similar to ours, thus impeding our ability to build brand identity and possibly leading to customer confusion. We could incur substantial costs in prosecuting or defending trademark infringement suits.

Further, our competitors may independently develop or patent technologies or processes that are substantially equivalent or superior to ours. If we are found to be infringing third party patents, we could be required to pay substantial royalties and/or damages, and we do not know whether we will be able to obtain licenses to use such patents on acceptable terms, if at all. Failure to obtain needed licenses could delay or prevent the development, manufacture or sale of our products and could necessitate the expenditure of significant resources to develop or acquire non-infringing intellectual property.

Asserting, defending and maintaining our intellectual property rights could be difficult and costly, and failure to do so may diminish our ability to compete effectively and may harm our operating results. We may need to pursue lawsuits or legal action in the future to enforce our intellectual property rights, to protect our trade secrets and domain names and to determine the validity and scope of the proprietary rights of others. If third parties prepare and file applications for trademarks used or registered by us, we may oppose those applications and be required to participate in proceedings to determine the priority of rights to the trademark. Similarly, competitors may have filed applications for patents, may have received patents and may obtain additional patents and proprietary rights relating to products or technology that block or compete with ours. We may have to participate in interference proceedings to determine the priority of invention and the right to a patent for the technology. Litigation and interference proceedings, even if they are successful, are expensive to pursue and time consuming, and we could use a substantial amount of our financial resources in either case.

We rely, in part, on contractual provisions to protect our trade secrets and proprietary knowledge.

Confidentiality agreements to which we are party may be breached, and we may not have adequate remedies for any breach. Our trade secrets may also be known without breach of such agreements or may be independently developed by competitors. Our inability to maintain the proprietary nature of our technology and processes could allow our competitors to limit or eliminate any competitive advantages we may have.

We may have difficulty managing change in our operations.

We continue to undergo rapid change in the scope and breadth of our operations as we advance the development of our products. Such rapid change is likely to place a significant strain on our senior management

team and other resources. We will be required to make significant investments in our engineering, logistics, financial and management information systems and to motivate and effectively manage our employees. Our business, prospects, results of operations and financial condition could be harmed if we encounter difficulties in effectively managing the budgeting, forecasting and other process control issues presented by such a rapid change.

We face risks associated with our plans to market, distribute and service our products internationally.

We intend to market, distribute and service our products internationally. We have limited experience developing and no experience manufacturing our products to comply with the commercial and legal requirements of international markets. Our success in international markets will depend, in part, on our ability and that of our partners to secure relationships with foreign sub-distributors, and our ability to manufacture products that meet foreign regulatory and commercial requirements. Additionally, our planned international operations are subject to other inherent risks, including potential difficulties in enforcing contractual obligations and intellectual property rights in foreign countries and fluctuations in currency exchange rates. Also, to the extent our operations and assets are located in foreign countries, they are potentially subject to nationalization actions over which we will have no control.

Our international sales and operations may be adversely affected.

Our international sales and operations are subject to risks associated with changes in local government laws, regulations and policies, including those related to tariffs and trade barriers, investments, taxation, exchange controls, employment regulations and repatriation of earnings. Our international sales and operations are also sensitive to changes in foreign national priorities, including government budgets, as well as to political and economic instability. International transactions may involve increased financial and legal risks due to differing legal systems and customs in foreign countries. For example, as a condition of sale or to the awarding of a contract, some international customers may require us to agree to offset arrangements, which may include in-country purchases, manufacturing and financial support arrangements. The contract may provide for penalties in the event we fail to perform in accordance with the offset requirements. In addition, as part of our globalization strategy, we have invested in certain countries, including Venezuela, Brazil, China, India, Russia and South Africa, which carry high levels of currency, political and economic risk. While these factors or the impact of these factors are difficult to predict, any one or more of them could adversely affect our business, financial condition or operating results.

Our government contracts could restrict our ability to effectively commercialize our technology.

Some of our technology has been developed under government funding by the United States and by other countries. The United States government has a non-exclusive, royalty-free, irrevocable world-wide license to practice or have practiced any of our technology developed under contracts funded by the government. In some cases, government agencies in the United States can require us to obtain or produce components for our systems from sources located in the United States rather than foreign countries. Our contracts with government agencies are also subject to the risk of termination at the convenience of the contracting agency, potential disclosure of our confidential information to third parties and the exercise of “march-in” rights by the government. March-in rights refer to the right of the United States government or government agency to license to others any technology developed under contracts funded by the government if the contractor fails to continue to develop the technology. The implementation of restrictions on our sourcing of components or the exercise of march-in rights could harm our business, prospects, results of operations and financial condition. In addition, under the Freedom of

Information Act, any documents that we have submitted to the government or to a contractor under a government funding arrangement are subject to public disclosure that could compromise our intellectual property rights unless such documents are exempted as trade secrets or as confidential information and treated accordingly by such government agencies.

Our future plans could be harmed if we are unable to attract or retain key personnel.

We have attracted a highly skilled management team and specialized workforce, including scientists, engineers, researchers and manufacturing, marketing and sales professionals. Our future success will depend, in part, on our ability to attract and retain qualified management and technical personnel. We do not know whether we will be successful in hiring or retaining qualified personnel. Our inability to hire qualified personnel on a timely basis, or the departure of key employees, could materially and adversely affect our development and commercialization plans and, therefore, our business, prospects, results of operations and financial condition.

GE MicroGen, Inc.Smart Hydrogen will have substantial control over us and DTE Energy Technologies, Inc. have representatives on our board of directors.

Under our agreement with GE MicroGen, we are requiredcould limit your ability to use our best efforts to cause one individual nominated by GE Energy, an operating business of General Electric Company, to be elected to our board of directors for as long as our distribution agreement with GEFCS remains in effect. Currently, Richard R. Stewart serves on our board of directors as GE Energy’s nominee. In addition, a current employee of DTE, Robert J. Buckler, and a former employee of DTE, Larry G. Garberding, currently serve on our board of directors. Both GEFCS and DTE have entered into distribution agreements with us. As discussed above in “Distribution, Marketing and Strategic Relationships” we are currently in discussion with GE to restructure certain agreements, including the distribution agreement, and cannot predictinfluence the outcome of those discussions.key transactions, including a change of control.

Smart Hydrogen and its affiliates beneficially own approximately 35.1% of the outstanding shares of our common stock. As a result, these stockholders will significantly influence or control certain matters requiring approval by our stockholders, including the approval of mergers or other extraordinary transactions. The interests of these stockholders may differ from yours and these stockholders may vote in a way with which you disagree and which may be adverse to your interests. This concentration of ownership may have the effect of delaying, preventing or deterring a change of control of our company, could deprive our stockholders of an opportunity to receive a premium for their common stock as part of a sale of our company and might ultimately affect the market price of our common stock.

If a substantial number of shares of the Company’s common stock become available for sale and are sold in a short period of time, the market price of our common stock could decline.

After its recently-completed investment in the Company, Smart Hydrogen holds approximately 35.1% of the Company’s outstanding common stock on a fully-diluted basis. If Smart Hydrogen or its affiliates sell substantial amounts of our common stock in the public market following this investment, the market price of our common stock could decrease significantly. The perception in the public market that Smart Hydrogen might sell shares of common stock could also depress the trading price of our common stock. Smart Hydrogen and its affiliates are subject to an Investor Rights Agreement with the Company pursuant to which Smart Hydrogen and its affiliates are prohibited from selling shares of the Company’s common stock until at least December 31, 2007. The market price of shares of our common stock may drop significantly when the restrictions on resale by Smart Hydrogen and its affiliates lapse. A decline in the price of shares of our common stock might impede our ability to raise capital through the issuance of additional shares of our common stock or other equity securities.

Provisions in our charter documents and Delaware law may prevent or delay an acquisition of us, which could decrease the value of our common stock.

Our certificate of incorporation and bylaws and Delaware law contain provisions that could make it hardermore difficult for a third party to acquire us without the consent of our board of directors. These provisions include those that:

authorize the issuance of up to 5,000,000 shares of preferred stock in one or more series without a stockholder vote;

limit stockholders’ ability to call special meetings;

establish advance notice requirements for nominations for election to our board of directors or for proposing matters that can be acted on by stockholders at stockholder meetings; and

provide for staggered terms for our directors.

In addition, in certain circumstances Delaware law also imposes restrictions on mergers and other business combinations between us and any holder of 15% or more of our outstanding common stock.

Our stock price has been and could remain volatile.

The market price of our common stock has historically experienced and may continue to experience significant volatility. Since our initial public offering in October 1999, the market price of our common stock has fluctuated from a high of $156.50 per share in the first quarter of 2000 to a low of $3.39$2.79 per share in the fourth quarter of 2002.March 2007. Our progress in developing and commercializing our products, our quarterly operating results, announcements of new products by us or our competitors, our perceived prospects, changes in securities’securities analysts’ recommendations or earnings’earnings estimates, changes in general conditions in the economy or the financial markets, adverse events related to our strategic relationships, significant sales of our common stock by existing stockholders including one or more of our strategic partners and other developments affecting us or our

competitors could cause the market price of our common stock to fluctuate substantially. In addition, in recent years, the stock market, and in particular the market for technology-related stocks, has experienced significant price and volume fluctuations. This volatility has affected the market prices of securities issued by many companies for reasons unrelated to their operating performance and may adversely affect the price of our common stock. In addition, we may be subject to additional securities class action litigation as a result of volatility in the price of our common stock, which could result in substantial costs and diversion of management’s attention and resources and could harm our stock price, business, prospects, results of operations and financial condition.

Our failure to comply with Nasdaq’sNASDAQ’s listing standards could result in the delisting of our common stock by NasdaqNASDAQ from the Nasdaq NationalNASDAQ Global Market and severely limit the ability to sell our common stock.

Our common stock is currently traded on the Nasdaq NationalNASDAQ Global Market. Under Nasdaq’sNASDAQ’s listing maintenance standards, if the closing bid price of our common stock is under $1.00 per share for 30 consecutive trading days, NasdaqNASDAQ will notify us that we may be delisted from the Nasdaq NationalNASDAQ Global Market. If the closing bid price of our common stock does not thereafter regain compliance for a minimum of 10 consecutive trading days during the 90 days following notification by Nasdaq, NasdaqNASDAQ, NASDAQ may delist our common stock from trading on the Nasdaq NationalNASDAQ Global Market. There can be no assurance that our common stock will remain eligible for trading on the Nasdaq NationalNASDAQ Global Market. In addition, if our common stock is delisted, our stockholders would not be able to sell our common stock on the Nasdaq NationalNASDAQ Global Market, and their ability to sell any of our common stock would be severely, if not completely, limited.

| Item 1B. | Unresolved Staff Comments |

We have not received written comments from the Securities and Exchange Commission regarding our periodic or current reports under the Securities Exchange Act of 1934, as amended, that were received 180 days or more before December 31, 2005 and remain unresolved.None.

| Item 2. | Properties |

Our principal executive offices are located in Latham, New York. At our 36-acre campus, we own a 56,000 square foot research and development center, a 32,000 square foot office building and a 50,000 square foot manufacturing facility and believe that these facilities are sufficient to accommodate our anticipated production volumes for at least the next two years.

| Item 3. | Legal Proceedings |

None.

| Item 4. | Submission of Matters to a Vote of Security Holders |

None.

PART II

| Item 5. | Market for Registrant’s Common Equity, |

Market Information. Our common stock is traded on the Nasdaq NationalNASDAQ Global Market under the symbol “PLUG.” As of March 1, 2006,2007, there were approximately 2,600 record holders of our common stock. However, management believes that a significant number of shares are held by brokers under a “nominee name” and that the number of beneficial shareholders of our common stock exceeds 80,000. The following table sets forth high and low last reported sale prices for our common stock as reported by the Nasdaq NationalNASDAQ Global Market for the periods indicated:

| Sales prices | Sales prices | |||||||||||

| High | Low | High | Low | |||||||||

2004 | ||||||||||||

2006 | ||||||||||||

1st Quarter | $ | 10.65 | $ | 6.75 | $ | 6.09 | $ | 4.59 | ||||

2nd Quarter | $ | 10.24 | $ | 6.85 | $ | 6.43 | $ | 4.64 | ||||

3rd Quarter | $ | 7.55 | $ | 4.62 | $ | 4.85 | $ | 3.64 | ||||

4th Quarter | $ | 7.27 | $ | 5.45 | $ | 4.49 | $ | 3.77 | ||||

2005 | ||||||||||||

1st Quarter | $ | 8.20 | $ | 5.11 | $ | 8.20 | $ | 5.11 | ||||

2nd Quarter | $ | 7.63 | $ | 5.21 | $ | 7.63 | $ | 5.21 | ||||

3rd Quarter | $ | 7.73 | $ | 5.85 | $ | 7.73 | $ | 5.85 | ||||

4th Quarter | $ | 7.12 | $ | 4.84 | $ | 7.12 | $ | 4.84 | ||||

Dividend Policy. We have never declared or paid cash dividends on our common stock and do not anticipate paying cash dividends in the foreseeable future. Any future determination as to the payment of dividends will depend upon capital requirements and limitations imposed by our credit agreements, if any, and such other factors as our board of directors may consider.

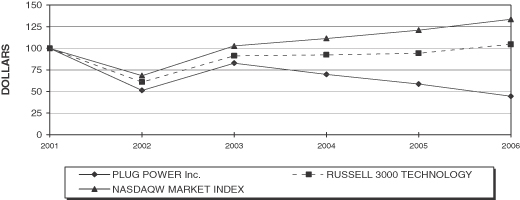

Five-Year Performance Graph. Below is a line graph comparing the percentage change in the cumulative total return on the Company’s Common Stock, based on the market price of the Company’s Common Stock, with the total return of companies included within the NASDAQ Market Index and the companies included within the Russell 3000 Technology Composite for the period commencing December 31, 2001 and ending December 31, 2006. The calculation of the cumulative total return assumes a $100 investment in the Company’s Common Stock, the NASDAQ Market Index and the Russell 3000 Technology Composite on December 31, 2001 and the reinvestment of all dividends.

Index | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | ||||||

PLUG POWER INC. | 100.00 | 51.37 | 82.95 | 69.91 | 58.70 | 44.51 | ||||||

RUSSELL 3000 TECHNOLOGY | 100.00 | 60.94 | 91.42 | 92.51 | 94.35 | 104.62 | ||||||

NASDAQW MARKET INDEX | 100.00 | 68.47 | 102.71 | 111.54 | 121.11 | 133.55 |

| Item 6. | Selected Financial Data |

The following tables set forth selected financial data and other operating information of the Company. The selected statement of operations and balance sheet data for 2006, 2005, 2004, 2003, 2002, and 20012002 as set forth below are derived from the audited financial statements of the Company. The information is only a summary and you should read it in conjunction with the Company’s audited financial statements and related notes and other financial information included herein and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

| Years Ended December 31, | Years Ended December 31, | |||||||||||||||||||||||||||||||||||||||

| 2005 | 2004 | 2003 | 2002 | 2001 | 2006 | 2005 | 2004 | 2003 | 2002 | |||||||||||||||||||||||||||||||

| (in thousands, except per share data) | (in thousands, except per share data) | |||||||||||||||||||||||||||||||||||||||

Statement Of Operations: | ||||||||||||||||||||||||||||||||||||||||

Product and service revenue | $ | 4,881 | $ | 5,306 | $ | 7,517 | $ | 9,427 | $ | 2,574 | $ | 2,657 | $ | 4,881 | $ | 5,306 | $ | 7,517 | $ | 9,427 | ||||||||||||||||||||

Research and development contract revenue | 8,606 | 10,835 | 4,985 | 2,391 | 3,168 | 5,179 | 8,606 | 10,835 | 4,985 | 2,391 | ||||||||||||||||||||||||||||||

Total revenue | 13,487 | 16,141 | 12,502 | 11,818 | 5,742 | 7,836 | 13,487 | 16,141 | 12,502 | 11,818 | ||||||||||||||||||||||||||||||

Cost of product and service revenues | 4,098 | 5,368 | 7,150 | 7,602 | 5,080 | 4,833 | 4,098 | 5,368 | 7,150 | 7,602 | ||||||||||||||||||||||||||||||

Cost of research and development contract revenues | 12,076 | 13,474 | 7,010 | 3,739 | 6,211 | 7,637 | 12,076 | 13,474 | 7,010 | 3,739 | ||||||||||||||||||||||||||||||

In-process research and development | — | — | 3,000 | — | — | — | — | — | 3,000 | — | ||||||||||||||||||||||||||||||

Research and development expense | 36,319 | 35,203 | 40,070 | 40,289 | 60,600 | 41,577 | 36,319 | 35,203 | 40,070 | 40,289 | ||||||||||||||||||||||||||||||

General and administrative expense | 8,973 | 8,423 | 7,183 | 6,956 | 7,492 | 12,268 | 8,973 | 8,423 | 7,183 | 6,956 | ||||||||||||||||||||||||||||||

Other expense (income), net | 3764 | 412 | 1,128 | 450 | (529 | ) | ||||||||||||||||||||||||||||||||||

Other income (expense), net | 8,169 | (3,764 | ) | (412 | ) | (1,128 | ) | (450 | ) | |||||||||||||||||||||||||||||||

Net loss | $ | (51,743 | ) | $ | (46,739 | ) | $ | (53,039 | ) | $ | (47,218 | ) | $ | (73,112 | ) | $ | (50,310 | ) | $ | (51,743 | ) | $ | (46,739 | ) | $ | (53,039 | ) | $ | (47,218 | ) | ||||||||||

Loss per share, basic and diluted | $ | (0.66 | ) | $ | (0.64 | ) | $ | (0.88 | ) | $ | (0.93 | ) | $ | (1.56 | ) | $ | (0.58 | ) | $ | (0.66 | ) | $ | (0.64 | ) | $ | (0.88 | ) | $ | (0.93 | ) | ||||||||||

Weighted average number of common shares outstanding | 78,463 | 73,126 | 60,146 | 50,645 | 46,840 | 86,100 | 78,463 | 73,126 | 60,146 | 50,645 | ||||||||||||||||||||||||||||||

Balance Sheet Data: | ||||||||||||||||||||||||||||||||||||||||

(at end of the period) | ||||||||||||||||||||||||||||||||||||||||

Unrestricted cash, cash equivalents and marketable securities | $ | 97,563 | $ | 66,849 | $ | 102,004 | $ | 55,848 | $ | 92,682 | ||||||||||||||||||||||||||||||

Unrestricted cash, cash equivalents and available-for-sale securities | $ | 269,123 | $ | 97,563 | $ | 66,849 | $ | 102,004 | $ | 55,848 | ||||||||||||||||||||||||||||||

Total assets | 139,784 | 117,997 | 160,589 | 108,683 | 151,374 | 307,920 | 139,784 | 117,997 | 160,589 | 108,683 | ||||||||||||||||||||||||||||||

Current portion of long-term obligations | 527 | 427 | 545 | 530 | 530 | — | 527 | 427 | 545 | 530 | ||||||||||||||||||||||||||||||

Long-term obligations | 4,659 | 4,996 | 5,306 | 5,727 | 6,172 | 1,112 | 4,659 | 4,996 | 5,306 | 5,727 | ||||||||||||||||||||||||||||||

Stockholders’ equity | 124,955 | 102,113 | 144,286 | 92,697 | 135,003 | 294,528 | 124,955 | 102,113 | 144,286 | 92,697 | ||||||||||||||||||||||||||||||

Working capital | 95,511 | 64,073 | 99,286 | 56,876 | 90,366 | 267,002 | 95,511 | 64,073 | 99,286 | 56,876 | ||||||||||||||||||||||||||||||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The following discussion should be read in conjunction with our accompanying Financial Statements and Notes thereto included within this Annual Report on Form 10-K. In addition to historical information, this Annual Report on Form 10-K and the following discussion contain statements that are not historical facts and are considered forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements contain projections of our future results of operations or of our financial position or state other forward-looking information. In some cases you can identify these statements by forward-looking words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “should,” “will” and “would” or similar words. We believe that it is important to communicate our future expectations to our investors. However, there may be events in the future that we are not able to accurately predict or control and that may cause our actual results to differ materially from the expectations we describe in our forward-looking statements. Investors are cautioned not to rely on forward-looking statements because they involve risks and uncertainties, and actual results may differ materially from those discussed as a result of various factors,

including, but not limited to: the risk that orders will not ship or convert to revenue, in whole or in part; our ability to develop commercially viable on-site energy products; the cost and timing of developing our on-site energy products; market acceptance of our on-site energy products; our ability to manufacture on-site energy products on a large-scale commercial basis; competitive factors, such as price competition and competition from other traditional and alternative energy companies; the cost and availability of components and parts for our on-site energy products; the ability to raise and provide the necessary capital to develop, manufacture and market our on-site energy products; our ability to establish relationships with third parties with respect to product development, manufacturing, distribution and servicing and the supply of key product components; our ability to protect our intellectual property; our ability to lower the cost of our on-site energy products and demonstrate their reliability; the cost of complying with current and future governmental regulations; the impact of deregulation and restructuring of the electric utility industry on demand for our on-site energy products; fluctuations in the trading price and volume of our common stock and other risks and uncertainties discussed under Item IA—Risk Factors. Readers should not place undue reliance on our forward-looking statements. These forward-looking statements speak only as of the date on which the statements were made and are not guarantees of future performance. Except as may be required by applicable law, we do not undertake or intend to update any forward-looking statements after the date of this Annual Report on Form 10-K.

Overview

We design and develop on-site energy systems based on proton exchange membrane fuel cell technology, for commercial and residential energy consumers worldwide. We are focused on a platform-based systems, architecture, which includesinclude proton exchange membrane, (PEM)or PEM, fuel cell and fuel processing technologies, from which we are offering or developing multiple products. We are currently offering our GenCore® product for commercial sale. Our GenCore® product is a back-up power product for telecommunications, broadband, utility and industrial uninterruptible power supply, (UPS)or UPS, applications. We are also developing additional products for continuous run power applications, with optional combined heat and power capability for remote small commercial and remote residential applications.

We are a development stage enterprise in the early period of field-testing and marketing our initial commercial products to a limited number of customers, including telecommunications companies, utilities, government entities and our distribution partners. Our initial commercial product, the GenCore® 5T, is designed to provide direct-current (DC) backup power for the targeted application described above. See “Product Development and Commercialization.” The GenCore® 5T is fueled by hydrogen and does not require a fuel processor.

Our sales and marketing strategy is to build a network of leading distributors who have established relationships, and sub-distributor networks, that can distribute and service our products in specifictargeted geographic and/or market segments. We have distribution agreements in place with 4 domestic16 distributors, including Tyco, Electronics Power Systems, Inc., (Tyco) our largest North American distribution partner and 13 international distributors, including IST, Holdings Ltd. (IST) our distribution partner in South Africa with whom we recently jointly received a $3 million customer buy-down grant from the International Finance Corporation to install 400 fuel cell systems over the next three years.in 2005. We also form relationships with customers and enter into development and demonstration programs with telecommunications companies, electric utilities, government agencies and other energy providers. Many of our initial sales of GenSys® and GenCore® 5T are contract specificcontract-specific arrangements containing multiple obligations that may include a combination of fuel cell systems, continued service, maintenance and other support. While contract terms require payment upon delivery and installation of the fuel cell system and are not contingent on the achievement of specific milestones or other substantive performance, theThe multiple obligations within our contractual arrangements are not accounted for separately based on our limited commercial experience and available evidence of fair value. As a result, we defer recognition of product and service revenue and recognize revenue on a straight linestraight-line basis over the stated contractual terms as the continued service, maintenance and other support obligations expire, which are generally for periods of twelve to twenty-seventhirty months. However, if the warranty or service period is expected to exceed the contractual warranty/service period the deferred revenue would be recognized over that expected longer warranty/service period and may not begin until units are installed. See “Critical Accounting Policies and Estimates—Revenue Recognition.”

As we gain commercial experience, including field experience relative to service and warranty of our initial products, the fair values for the multiple elements within our future contracts may become determinable and we

may, in future periods, recognize product revenue upon delivery or installation of the product, or we may continue to defer recognition, based on application of appropriate guidance within EITF 00-21, “Accounting for Revenue Arrangements with Multiple Deliverables,” or changes in the manner in which we structure contractual agreements, including our agreements with distribution partners.

Our cash requirements depend on numerous factors, including completion of our product development activities, ability to commercialize our fuel cell systems, market acceptance of our systems and other factors. We expect to pursue the expansion of our operations through internal growth and strategic acquisitions. As of December 31, 2005,2006, we had unrestricted cash and cash equivalents and marketableavailable-for-sale securities totaling $97.6$269.1 million and working capital of $95.5$267.0 million. Additionally, we have restricted cash in the amount of $4.0 million, which is escrowed to secure the mortgage on our headquarters facility.

During the year ended December 31, 2005,2006, cash used by operating activities was $39.9$46.1 million, consisting primarily of a net loss of $51.7$50.3 million offset, in part, by non-cash expenses in the amount of $12.7$8.1 million, including $3.4$3.2 million for amortization and depreciation $2.9and $4.9 million for stock based compensation, $688,000 for amortization of intangible assets and $5.8 million for equity losses in affiliates.compensation. Cash used in investing activities for the year ended December 31, 20052006 was $28.6$163.6 million, consisting of $27.6$161.3 million of net of purchases of marketable securities, and $1.0$1.3 million used to purchase property, plant and equipment.equipment and a $1.0 million loan made to a potential investee. Cash provided by financing activities was $71.4$214.8 million, consisting primarily of net proceeds, in the amount of $70.6$214.4 million, from the issuancesale of commonour Class B capital stock duringto Smart Hydrogen and payment of $4.0 million to settle our debt obligation related to the Company’s public offeringpurchase of the facilities in the third quarter of 2005.1999.

We have financed our operations through December 31, 20052006, primarily from the sale of equity, which has provided cash in the amount of $420.8$635.7 million since inception. Additionally cumulativeCumulative net cash used in operating activities has been $302.2$348.4 million, and cash used in investing activities has been $90.0$253.6 million, including our purchase of property, plant and equipment of $32.7$34.0 million and our net investments in marketable securities in the amount of $75.9$237.3 million offset, in part, by net proceeds from acquisition of $29.5 million.

Product Development and Commercialization

We are focused on a fuel cell technology platform from which we believe we can offer multiple products. We currently have one commercial product line, GenCore®, which we continue to enhance and broaden:

GenCore®—Back-up Power for Telecommunication, Broadband, Utility and UPS Applications—We currently offer the GenCore® product line which is focused on providing direct-current (DC) backup power in a power range of 1-12 kilowatts for applications in the telecom, broadband, utility and industrial UPS market applications. Our GenCore® products are fueled by hydrogen and do not require a fuel processor. In the fourth quarter of 2003, we began initial shipments of the GenCore® 5T product, and have shipped 233 units through December 31, 2005. See “Distribution, Marketing and Strategic Relationships” for additional information regarding product development and commercialization.

Additionally, we continue to advance the development of our other technology platforms:

GenSys®—Remote Continuous Power for Light Commercial and Residential Applications—We plan to continue to develop GenSys® into a platform that is expected to support a number of products, including systems fueled by liquefied petroleum gas, (LPG)or LPG, for remote applications and, eventually, both grid independent and grid-connected light commercial and residential applications fueled by LPG or natural gas. In connection with the development of our GenSys® platform, we are developing combined heat and power (CHP) fuel cell systems for light commercial and residential applications that provide supplemental heat as electricity is produced. We began field-testing of the next generation GenSys®, our continuous run product, in the third quarter of 2005. See “Distribution, Marketing and Strategic Relationships” for additional information regarding product development and commercialization.

Home Energy Station—We have been developing technology in support of the automotive fuel cell market under a series of agreements with Honda R&D Co Ltd. of Japan (Honda), a subsidiary of Honda Motor Co., Ltd., under which we have exclusivelydeveloped, on a joint and jointly developedexclusive basis, and tested three phases of prototype fuel cell systems that provide electricity and heat to a home or business, while also providing

hydrogen fuel for a fuel cell vehicle (the “Home(named the Home Energy Station”)Station). In OctoberSince 2003, we have successfully demonstrated three successive prototype generations of the first prototype Home Energy Station at Honda R&D Americas’ facility in Torrance, California. In September 2004, underCalifornia and at Plug Power’s facility in Latham, NY. The companies are currently collaborating on the second phase of our work with Honda, we successfully demonstrated a second-generationfourth generation prototype Home Energy Station pursuant to the latest agreement signed in early 2006. Across each generation of the Home Energy Station, at our Latham NY headquarters. In September 2005, Plug Power and Honda installed our third-generation Home Energy Station in Torrance, California. Honda now utilizes the systems in both New York and California for refueling prototype Honda FCX fuel cell vehicles in their test programs. Across each generation of the HES, we have significantly reduced size and weight, as well as improved performance. We are currently negotiating a contract with Honda funding our joint development of the fourth generation system during 2006, as well as a separate agreement funding joint research & development, in 2006, of technology that may be utilized in future systems.

We also have longer-term product development plans that potentially include GenSite™ a product which supplies on-site hydrogen, and GenDrive™ a product offering battery replacement for material handling equipment.

GenSite™—On-Site Hydrogen Generation—We expect to combine our proprietary fuel processor technology with existing components for gas compression, purification and storage as the basis for GenSite™, an on-site hydrogen gas generator. This product is expected to target certain applications now served by packaged hydrogen gas (cylinders or tube trailers) or electrolyzers. We presently have a prototype system in our research and product development facilities in Apeldoorn, Holland, and another system at our Latham, NY headquarters.

GenDrive™—Battery Replacement for Material Handling—The GenCore® platform is expected to provide the basis for our development of the GenDrive™ product, a hydrogen-fueled battery-replacement module for material handling equipment. We continue to explore the potential for partnerships with end users of this product to develop the GenDrive™ product.

Results of Operations

Comparison of the Years Ended December 31, 2006 and December 31, 2005.

Product and service revenue. Product and service revenue decreased to $2.7 million for the year ended December 31, 2006, from $4.9 million for the year ended December 31, 2005, primarily due to a decrease in the amount of revenue recognized for units shipped prior to 2006. We defer recognition of product and service revenue at the time of delivery and recognize revenue as the continued service, maintenance and other support obligations expire. However, if the warranty or service period is expected to exceed the contractual warranty/service period the deferred revenue would be recognized over that expected longer warranty/service period and may not begin until units are installed. The costs associated with the product, service and other obligations are expensed as they are incurred.

Many of our initial sales of GenSys® and GenCore® 5T products contain multiple obligations that may include a combination of fuel cell systems, continued service, maintenance and other support. While contract terms generally require payment shortly after delivery and installation of the fuel cell system and are not contingent on the achievement of specific milestones or other substantive performance, the multiple obligations within our contractual arrangements are not accounted for separately based on our limited commercial experience and available evidence of fair value of the different components. As a result, we defer recognition of product and service revenue and recognize revenue on a straight-line basis as the continued service, maintenance and other support obligations expire, which are generally for periods of twelve to thirty months. However, if the warranty or service period is expected to exceed the contractual warranty/service period the deferred revenue would be recognized over that expected longer warranty/service period and recognition of revenue may not begin until units are installed. See “Critical Accounting Policies and Estimates—Revenue Recognition.”

During the year ended December 31, 2006, we shipped 152 fuel cell systems and recognized product and service revenue against these current year deliveries in the amount of $779,000. We also recognized $1.9 million of revenue originally deferred at December 31, 2005. This compares to 134 fuel cell systems shipped for the year ended December 31, 2005, during which we recognized $940,000 of product and service revenue against 2005 deliveries and $4.0 million of revenue originally deferred at December 31, 2004. Of the 2006 shipments, 43 units were on a consignment basis and no revenues were recorded in 2006. Total installations for the year ended December 31, 2006 were 94 units compared with the 91 units for the comparable 2005 period. Units shipped and not installed at December 31, 2006 were 149 (including units shipped on consignment), compared with 99 at the end of 2005.

During 2006 and 2005, we invoiced $2.3 million and $2.5 million, respectively, for the delivery of fuel cell systems and recognized revenue of $2.7 million and $4.9 million, respectively. Any differences between the amounts invoiced and the recognized revenue is a result of deferred revenue recognized in accordance with our revenue recognition policy as described above.

Research and development contract revenue. Research and development contract revenue decreased to $5.2 million for the year ended December 31, 2006 from $8.6 million for the year ended December 31, 2005. The decrease is the result of spending levels decreasing for material purchases and subcontractor activity as the U.S. Department of Energy, or DOE, and the U.S. Department of Defense, or DOD, programs wind down and decreased activity under our contract with the National Institute of Standards and Technology, or NIST, and with

Honda R&D Co., Ltd. of Japan. We expect to continue certain research and development contract work that is directly related to our current product development efforts. Research and development contract revenue primarily relates to cost reimbursement research and development contracts associated with the development of PEM fuel cell technology. We generally share in the cost of these programs with our cost-sharing percentages being from 20% to 51% of total project costs. Revenue from “time and material” contracts is recognized on the basis of hours expended plus other reimbursable contract costs incurred during the period. We expect to continue certain research and development contract work that is directly related to our current product development efforts.

Cost of product and service revenue. Cost of product and service revenue increased to $4.8 million for the year ended December 31, 2006 from $4.1 million for the year ended December 31, 2005. Cost of product and service revenue includes the direct material cost incurred in the manufacture of the products we sell as well as the labor and material costs incurred for product maintenance, replacement parts and service under our contractual obligations. These costs consist primarily of production materials and fees paid to outside suppliers for subcontracted components and services. The year over year increase to cost of product and service revenue is primarily the result of an increase in warranty costs resulting from a greater number of units placed in the field during 2006. For the year ended December 31, 2006 installations were 94 units compared with 91 units for the year ended December 31, 2005.

Cost of research and development contract revenue. Cost of research and development contract revenue decreased to $7.6 million for the year ended December 31, 2006 from $12.1 million for the year ended December 31, 2005. Cost of research and development contract revenue includes costs associated with research and development contracts including: compensation and benefits for engineering and related support staff, fees paid to outside suppliers for subcontracted components and services, fees paid to consultants for services provided, materials and supplies used and other directly allocable general overhead costs allocated to specific research and development contracts. The decrease in these costs is directly related to the decreased activity under the development agreements described above under research and development contract revenue.

Noncash research and development expense.Noncash research and development expense increased to $2.8 million for the year ended December 31, 2006 from $1.6 million for the year ended December 31, 2005. Noncash research and development expense represents the fair value of vested stock grants and vested stock options to employees, consultants and others in exchange for services provided. The increase is primarily the result of the Company’s adoption of SFAS 123R during the first quarter of fiscal 2006 (see Note 2 in the Notes to Consolidated Financial Statements).

Other research and development expense. Other research and development expense increased to $38.8 million for the year ended December 31, 2006 from $34.7 million for the year ended December 31, 2005. The increase in other research and development expense is primarily the result of our accelerated efforts to advance the development of our next generation continuous run product combined with continued research and development activities related to future product initiatives. We also had fewer resources allocated to research and development programs reflected in cost of revenues for research and development under DOE, NIST and Honda research and development contracts (as discussed above). Other research and development expense includes: materials to build development and prototype units, cash compensation and benefits for the engineering and related staff, expenses for contract engineers, fees paid to outside suppliers for subcontracted components and services, fees paid to consultants for services provided, materials and supplies consumed, facility related costs such as computer and network services and other general overhead costs.

Other research and development expense also includes amortization in the amount of $0 and $700,000 for the years ended December 31, 2006 and 2005, respectively, related to the portion of the H Power purchase price that represented capitalized technology and was recorded on our balance sheet under the caption “Intangible assets”. As of December 31, 2005, the carrying value of these intangible assets had been fully amortized.

Noncash general and administrative expense.Noncash general and administrative expense was $1.4 million for the year ended December 31, 2006 compared to $1.5 million for the year ended December 31, 2005. Noncash

general and administrative expense represents the fair value of vested stock grants and vested stock options to employees, consultants and others in exchange for services provided. The year over year expense remained relatively flat as the increase in expenses resulting from the adoption of SFAS 123R (see Note 2 in the Notes to Consolidated Financial Statements) was offset by a decrease in expenses for consultants.

Other general and administrative expense. Other general and administrative expenses increased to $10.8 million for the year ended December 31, 2006 from $7.4 million for the year ended December 31, 2005. Other general and administrative expense includes cash compensation, benefits and related costs in support of our general corporate functions, including general management, finance and accounting, human resources, marketing, information technology and legal services. The increase in other general and administrative expenses is primarily a result of increased headcount, charges related to severance packages for departing employees and payments made to strategic consultants.

Interest income and net realized gains/losses from the sale of available-for-sale securities.Interest income and net realized gains/losses from the sale of available-for-sale securities, consisting primarily of interest earned on our cash, cash equivalents and available-for-sale securities, increased to $8.3 million for the year ended December 31, 2006 from $2.2 million for the year ended December 31, 2005. The increase was the result of higher cash and marketable securities balances as a result of the sale of our Class B capital stock to Smart Hydrogen Inc. in 2006 and slightly higher yields on our investment portfolio. Total net realized gains/losses from available-for-sale securities was approximately a $68 thousand gain and a $74 thousand loss for the years ended December 31, 2006 and 2005, respectively.

Interest expense. Interest expense consists of interest on a long-term obligation related to the purchase of our facilities and interest paid on capital lease obligations. Interest expense was $171,000 for the year ended December 31, 2006, compared to $146,000 for the year ended December 31, 2005. As of December 31, 2006 the debt associated with the purchase of the facility was paid for in full. The long-term debt accrued interest at a variable rate that was approximately 4.44% for the year ended December 31, 2005.

Equity in losses of affiliates. Equity in losses of affiliates was $0 for the year ended December 31, 2006 and $5.8 million for the year ended December 31, 2005. Equity in losses of affiliates, which we accounted for under the equity method of accounting, was our proportionate share of the amount of the net loss of GE Fuel Cell Systems, or GEFCS, and the amortization of our original investments. During the quarter ended December 31, 2005, the Company recorded an impairment loss equal to 100% of the remaining carrying value of the Company’s investment in GEFCS due to the changes in the relationship that eventually resulted in GEFCS being dissolved in the first quarter of fiscal 2006.

Income taxes. We did not report a benefit for federal and state income taxes in the consolidated financial statements as the deferred tax asset generated from our net operating loss has been offset by a full valuation allowance because it is more likely than not that the tax benefits of the net operating loss carry forward will not be realized.

Comparison of the Years Ended December 31, 2005 and December 31, 2004.

Product and service revenue. Product and service revenue decreased to $4.9 million for the year ended December 31, 2005, from $5.3 million for the year ended December 31, 2004. We defer recognition of product and service revenue at the time of delivery and recognize revenue as the continued service, maintenance and other support obligations expire. The costs associated with the product, service and other obligations are expensed as they are incurred.

Many of our initial sales of GenSys® and GenCore® 5T products are contract specific arrangements containing multiple obligations that may include a combination of fuel cell systems, continued service, maintenance and other support. While contract terms require payment upon delivery and installation of the fuel cell system and are not contingent on the achievement of specific milestones or other substantive performance, the multiple obligations within our contractual arrangements are not accounted for separately based on our limited commercial experience and available evidence of fair value. As a result, we defer recognition of product and service revenue and recognize revenue on a straight-line basis over the stated contractual terms, as the continued service, maintenance and other support obligations expire, which are generally for periods of twelve to twenty-seven months. See “Critical Accounting Policies and Estimates—Revenue Recognition.”

During the year ended December 31, 2005, we delivered 135134 fuel cell systems and recognized product and service revenue against these current year deliveries in the amount of $940,000 combined with the recognition of

$4.0 $4.0 million of revenue originally deferred at December 31, 2004. This compares to 150 fuel cell systems delivered for the year ended December 31, 2004, during which we recognized $1.4 million of product and service revenue against 2004 deliveries combined with the recognition of $3.9 million of revenue originally deferred at December 31, 2005.2003.

During 2005 and 2004, we invoiced $2.5 million and $5.7 million, respectively, for the delivery of fuel cell systems and recognized revenue of $4.9 million and $5.3 million in 2005 and 2004, respectively. The difference between the amounts invoiced and the recognized revenue in 2005 and 2004 represents a component of deferred revenue at December 31, 2005 and 2004. During 2006, we expect to recognize substantially all of the deferred revenue as of December 31, 2005.

Research and development contract revenue. Research and development contract revenue decreased to $8.6 million for the year ended December 31, 2005 from $10.8 million for the year ended December 31, 2004. The decrease is the result of prior spending levels dropping off for material purchases and subcontractor activity as the U.S. Department of Energy (DOE) programs wind down and decreased activity under our contract with National Institute of Standards and Technology (NIST) and with Honda R&D Co., Ltd. of Japan. We expect to continue certain research and development contract work that is directly related to our current product development efforts. Research and development contract revenue primarily relates to cost reimbursement research and development contracts associated with the development of PEM fuel cell technology. We generally share in the cost of these programs with cost-sharing percentages between 20% and 60%. Revenue from “time and material” contracts is recognized on the basis of hours utilized, plus other reimbursable contract costs incurred during the period.

Cost of product and service revenue. Cost of product and service revenue decreased to $4.1 million for the year ended December 31, 2005 from $5.4 million for the year ended December 31, 2004. Cost of product and service revenue includes the direct material cost incurred in the manufacture of the products we sell, as well as the labor and material costs incurred for product maintenance, replacement parts and service under our contractual obligations. These costs consist primarily of production materials and fees paid to outside suppliers for subcontracted components and services. The year over year decrease to cost of product and service revenue is directly related to an increased proportion of our fuel cell system deliveries coming from GenCore® product which has a lower direct materials cost per unit than our GenSys® product. Our GenCore® products are fueled by hydrogen and do not require a fuel processor, thereby eliminating certain costs. For the year ended December 31, 2005 we shipped 121120 GenCore® units and 14 GenSys® units compared to 93 and 56 GenCore® and GenSys® units, respectively, in 2004.

Cost of research and development contract revenue. Cost of research and development contract revenue decreased to $12.1 million for the year ended December 31, 2005 from $13.5 million for the year ended December 31, 2004. Cost of research and development contract revenue includes costs associated with research and development contracts including: compensation and benefits for engineering and related support staff, fees paid to outside suppliers for subcontracted components and services, fees paid to consultants for services, and materials and supplies and other directly allocable general overhead costs allocated to specific research and development contracts. The decrease in these costs is directly related to the decreased activity under the development agreements described above under research and development contract revenue.

Noncash research and development expense.Noncash research and development expense decreased to $1.6 million for the year ended December 31, 2005 from $2.6 million for the year ended December 31, 2004. Noncash research and development expense represents the fair value of vested stock grants to employees, consultants and others in exchange for services provided. The decrease is primarily the result of fully expensing amortization of stock based compensation associated with restricted stock issued in June 2003 under our employee stock option exchange program.2003. In 2004 we had a full year of such amortization.

Other research and development expense. Other research and development expense increased to $34.7 million for the year ended December 31, 2005 from $32.6 million for the year ended December 31, 2004.

The increase in research and development expense is primarily the result of our accelerated efforts to advance the development of our next generation continuous run product combined with continued research and development activities related to future product initiatives. We also had fewer resources allocated to research and development programs reflected in cost of revenues for research and development under DOE, NIST and Honda research and development contracts (as discussed above).

Other research and development expense also includesincluded amortization in the amount of $700,000 and $3.5 million for the years ended December 31, 2005 and 2004, respectively. For the year ended December 31, 2005, amortization expense included $700,000 related to the portion of the H Power purchase price that was capitalized and recorded on our balance sheet under the caption “Intangible assets”. For the year ended