Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Indicate by check mark whether the registrantRegistrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrantRegistrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes xþ No ¨ Indicate by check mark whether the registrantRegistrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrantRegistrant was required to submit and post such files). Yes ¨þ No ¨ Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’sRegistrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨þ Indicate by check mark whether the registrantRegistrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. Large accelerated filer xþ Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨ �� (Do not check if a smaller reporting company) Indicate by check mark whether the registrantRegistrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No xþ The aggregate market value of the Common Shares (the only common equity)equity of the Registrant) held by non-affiliates computed by reference to the closing price on the New York Stock Exchange on November 28, 2008,30, 2010, the last business day of the registrant’sRegistrant’s most recently completed second fiscal quarter, was approximately $1,423,212,576.$717,342,269. For this purpose, executive officers and directors of the Registrant are considered affiliates. Indicate the number of shares outstanding of each of the registrant’sRegistrant’s classes of common stock, as of the latest practicable date. On July 24, 2009,26, 2011, the number of Common Shares issued and outstanding was 79,092,675.74,328,346. DOCUMENT INCORPORATED BY REFERENCE: Selected portions of the Registrant’s definitive Proxy Statement to be furnished to shareholders of the Registrant in connection with the Annual Meeting of Shareholders to be held on September 30, 2009,29, 2011, are incorporated by reference into Part III of this Annual Report on Form 10-K to the extent provided herein.

TABLE OF CONTENTS i

SAFE HARBOR STATEMENT Selected statements contained in this Annual Report on Form 10-K, including, without limitation, in “PART I – Item 1. – Business” and “PART II – Item 7. – Management’s Discussion and Analysis of Financial Condition and Results of Operations,” constitute “forward-looking statements” as that term is used in the Private Securities Litigation Reform Act of 1995 (the “Act”). Forward-looking statements reflect our current expectations, estimates or projections concerning future results or events. These statements are often identified by the use of forward-looking words or phrases such as “believe,” “expect,” “anticipate,” “may,” “could,” “intend,” “estimate,” “plan,” “foresee,” “likely,” “will,” “should” or other similar words or phrases. These forward-looking statements include, without limitation, statements relating to: | | • | | business plans or future or expected growth, performance, sales, volumes, cash flows, earnings, balance sheet strengths, debt, financial condition or other financial measures; |

| | • | | projected profitability potential, capacity and working capital needs; |

| | • | | demand trends for the Companyus or itsour markets; |

| | • | | pricing trends for raw materials and finished goods;goods and the impact of pricing changes; |

| | • | | anticipated capital expenditures and asset sales; |

| | • | | anticipated improvements and efficiencies in costs, operations, sales, inventory management, sourcing and sourcingthe supply chain and the results thereof; |

| | • | | anticipated impacts of transformation efforts;

|

| • | | the ability to make acquisitions and the projected timing, results, benefits, costs, charges and expenditures related to head countacquisitions, newly-created joint ventures, headcount reductions and facility dispositions, shutdowns and consolidations; |

| | • | | the alignment of operations with demand; |

| | • | | the ability to operate profitably and generate cash in down markets; |

| • | | the ability to capture and maintain margins and market share and to develop or take advantage of future opportunities, new products and markets; |

| | • | | expectations for Company and customer inventories, jobs and orders; |

| | • | | expectations for the economy and markets or improvements therein; |

| | • | | expected benefits from transformation plans, cost reduction efforts and other new initiatives; |

| | • | | expectations for increasing volatility or improving and sustaining earnings, earnings potential, margins or shareholder value; |

| | • | | effects of judicial rulings; and |

| | • | | other non-historical matters. |

Because they are based on beliefs, estimates and assumptions, forward-looking statements are inherently subject to risks and uncertainties that could cause actual results to differ materially from those projected. Any number of factors could affect actual results, including, without limitation, those that follow: | | • | | the effect of national, regional and worldwide economic conditions generally and within major product markets, including a prolonged or substantial economic downturn; |

| | • | | the effect of conditions in national and worldwide financial markets; |

| | • | | product demand and pricing; |

| | • | | changes in product mix, product substitution and market acceptance of the Company’sour products; |

| | • | | fluctuations in pricing, quality or availability of raw materials (particularly steel), supplies, transportation, utilities and other items required by operations; |

| | • | | effects of facility closures and the consolidation of operations; |

| | • | | the effect of financial difficulties, consolidation and other changes within the steel, automotive, construction and other industries in which the Company participates;we participate; |

| | • | | failure to maintain appropriate levels of inventories; |

| | • | | financial difficulties (including bankruptcy filings) of original equipment manufacturers, end-users and customers, suppliers, joint venture partners and others with whom the Company doeswe do business; |

| • | | failure to maintain, or any adverse changes in, our existing committed credit facilities, or our credit ratings;

|

| | • | | the ability to realize targeted expense reductions from head countheadcount reductions, facility closures and other cost reduction efforts; |

ii

| | • | | the ability to realize other cost savings and operational, sales and sourcing improvementimprovements and efficiencies, and other expected benefits from transformation initiatives, on a timely basis; |

| | • | | the overall success of, and the ability to integrate, newly-acquired businesses and achieve synergies and other expected benefits and cost savings therefrom; |

ii

| • | | the overall success of newly-created joint ventures, including the demand for their products, and the ability to achieve the anticipated benefits and cost savings therefrom; |

| | • | | capacity levels and efficiencies, and other expected benefits from transformation initiatives within facilities, within major product markets and within the industry as a whole; |

| | • | | the effect of disruption in the business of suppliers, customers, facilities and shipping operations due to adverse weather, casualty events, equipment breakdowns, acts of war or terrorist activities or other causes; |

| | • | | changes in customer demand, inventories, spending patterns, product choices and supplier choices; |

| | • | | risks associated with doing business internationally, including economic, political and social instability, and foreign currency exposure;exposure and the acceptance of our products in new markets; |

| | • | | the ability to improve and maintain processes and business practices to keep pace with the economic, competitive and technological environment; |

| | • | | adverse claims experience with respect to workers’worker’s compensation, product recalls or product liability, casualty events or other matters; |

| | • | | deviation of actual results from estimates and/or assumptions used by the Companyus in the application of itsour significant accounting policies; |

| | • | | level of imports and import prices in the Company’sour markets; |

| | • | | the impact of judicial rulings and governmental regulations, including those adopted by the United States Securities and Exchange Commission and other governmental agencies as contemplated by the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, both in the United States and abroad; and |

| | • | | other risks described from time to time in the filings of Worthington Industries, Inc. with the United States Securities and Exchange Commission, including those described in “PART I – Item 1A. –— Risk Factors” of this Annual Report on Form 10-K. |

We note these factors for investors as contemplated by the Act. It is impossible to predict or identify all potential risk factors. Consequently, you should not consider the foregoing list to be a complete set of all potential risks and uncertainties. Any forward-looking statements in this Annual Report on Form 10-K are based on current information as of the date of this Annual Report on Form 10-K, and we assume no obligation to correct or update any such statements in the future, except as required by applicable law. iii

PART I Item 1. — Business General Overview Worthington Industries, Inc. is a corporation formed under the laws of the State of Ohio (individually, the “Registrant” or “Worthington Industries” or, collectively with the subsidiaries of Worthington Industries, Inc., “we,” “our,” “Worthington,”“Worthington” or the “Company”). Founded in 1955, Worthington is primarily a diversified metalmetals processing company, focused on value-added steel processing and manufactured metal products. Our manufactured metal products include: pressure cylinder products such as metalpropane, oxygen and helium tanks, hand torches, refrigerant and industrial cylinders, camping cylinders, scuba tanks and helium balloon kits; framing pressure cylinders, automotive past-systems and current-model year service stampingsstairs for mid-rise buildings; steel pallets and racks; and, through joint ventures, metal ceilingsuspension grid systems for concealed and laser-welded blanks.lay-in panel ceilings, laser welded blanks; light gauge steel framing for commercial and residential construction and current and past model automotive service stampings. Worthington is headquartered at 200 Old Wilson Bridge Road, Columbus, Ohio 43085, telephone (614) 438-3210. The common shares of Worthington Industries are traded on the New York Stock Exchange under the symbol WOR. Worthington Industries maintains an Internet web site at www.worthingtonindustries.com. This uniform resource locator, or URL, is an inactive textual reference only and is not intended to incorporate Worthington Industries’ web site into this Annual Report on Form 10-K. Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports, filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), as well as Worthington Industries’ definitive annual meeting proxy materials filed pursuant to Section 14 of the Exchange Act, are available free of charge, on or through the Worthington Industries web site, as soon as reasonably practicable after such material is electronically filed with, or furnished to, the Securities and Exchange Commission (the “SEC”). Business Segments

At the end of the fiscal year ended May 31, 20092011 (“fiscal 2009”2011”), the Companywe had 4135 manufacturing facilities worldwide and held equity positions in six12 joint ventures, which operated an additional 1943 manufacturing facilities worldwide. The Company hasOur operations are managed principally on a products and services basis and include three principal reportable business segments: Steel Processing, Pressure Cylinders and Metal Framing and Pressure Cylinders.Framing. The Steel Processing reportable business segment consists of the Worthington Steel business unit (“Worthington Steel”)., and includes Precision Specialty Metals, Inc. (“PSM”), a specialty stainless processor located in Los Angeles, California, and Spartan Steel Coating, LLC (“Spartan”), a consolidated joint venture that operates a cold-rolled hot dipped galvanizing line. The Pressure Cylinders reportable business segment consists of the Worthington Cylinders business unit (“Worthington Cylinders”) and India-based Worthington Nitin Cylinders Limited (“WNCL), a consolidated joint venture that manufactures high pressure, seamless steel cylinders for compressed natural gas storage in motor vehicles and for industrial gases. The Metal Framing reportable business segment consists of the Dietrich Metal Framing business unit (“Dietrich”). The Pressure Cylinders business segment consists

As more fully described in theRecent Developments section herein, on March 1, 2011, we contributed certain assets of Dietrich to a newly-formed joint venture, Clarkwestern Dietrich Building Systems LLC (“ClarkDietrich”), in which we received a 25% noncontrolling interest. We retained seven of the Worthington Cylinder13 metal framing facilities, which continue to operate, on a short-term basis, to support the transition of the business unit (“Worthington Cylinders”). into the new joint venture. Following this brief transition period, these assets will be disposed of. The financial results and operating performance of the retained facilities will continue to be reported within our Metal Framing operating segment until their expected disposition in fiscal 2012. The contributed net assets, which were deconsolidated effective March 1, 2011, will continue to be reported within Metal Framing on a historical basis. All other business units not included in these three reportable businessoperating segments are combined and disclosed in the ‘Other’Other category, which also includes income and expense items not allocated to theour reportable business segments. The Other category includes the Worthington Steelpac Systems, LLC (“Steel Packaging”) and Worthington Global Group, LLC (the “Global Group”) operating segments. As more fully described in the Recent Developments section herein, on May 9, 2011, we contributed substantially all of the net assets of our then automotive body panels subsidiary, The Gerstenslager Company (“Gerstenslager”), to ArtiFlex Manufacturing, LLC (“ArtiFlex”), a newly-formed joint venture in which we received a 50% noncontrolling interest. As a result of this transaction, we no longer maintain an Automotive Body Panels operating segment. We will continue to report the financial results and operating performance of this former operating segment on a historical basis through May 9, 2011 as part of the Other category for segment reporting purposes. During the third quarter of fiscal 2011, we made certain organizational changes impacting the internal reporting and management structure of our previously reported Mid-Rise Construction, ServicesMilitary Construction and Steel PackagingCommercial Stairs operating segments. As a result of these organizational changes, management responsibilities and internal reporting for these businesses were re-aligned and combined into a single operating segment, the Global Group. The purpose of the Global Group is to identify and develop potential growth platforms by applying our core competencies in metals manufacturing and construction methods. The first set of initiatives includes expansion of high density mid-rise residential construction in emerging international markets and development of new business units.in sectors such as renewable energy. The composition of our reportable business segments was unchanged from this development. Worthington holdsWe hold equity positions in six12 joint ventures, which are further discussed below underin the subheading “Joint Ventures.” Only one of the sixJoint Ventures section herein. The Spartan and WNCL joint ventures isare consolidated and itswith their operating results are reported inwithin the Steel Processing and Pressure Cylinders reportable business segment.segments, respectively.

During fiscal 2009,2011, the Steel Processing, Pressure Cylinders and Metal Framing and Pressure Cylinders businessoperating segments served approximately 1,100, 3,9002,700 and 2,0002,200 customers, respectively, located primarily in the United States. Foreign salesoperations accounted for approximately 9%8% of consolidated net sales during fiscal 2011 and were comprised primarily of sales to customers in Canada and Europe. No single customer accounted for over 5%10% of consolidated net sales. Further reportable business segment data is provided insales during fiscal 2011. Refer to “Item 8. – Financial Statements and Supplementary Data – Notes to Consolidated Financial Statements – Note HM – Segment Data” of this Annual Report on Form 10-K. That data10-K for a full description of our reportable business segments. Recent Developments On July 1, 2011, our Pressure Cylinders operating segment purchased substantially all of the net assets of the BernzOmatic business (“Bernz”) from Irwin Industrial Tool Company, a subsidiary of Newell Rubbermaid, Inc. (the “Seller”), for cash consideration of approximately $51.0 million. The assets purchased include substantially all of the operating assets of Bernz, including machinery and equipment, intellectual property, inventories and the Bernz-owned facility in Winston-Salem, North Carolina. We will lease the Medina, New York facility from the Seller. Accounts receivable as of the closing date are being retained by the Seller. Foreign inventories and operations will transition to us over a period of approximately 90 days. We also generally assumed the trade accounts payable of Bernz arising in the ordinary course of business as of the closing date. On May 9, 2011, our automotive body panel subsidiary, The Gerstenslager Company, closed an agreement with International Tooling Solutions, LLC, a tooling design and build company, to combine their businesses in a newly-formed joint venture. This new joint venture, ArtiFlex, provides an integrated solution for engineering, tooling, stamping, assembly and other services to customers primarily in the automotive industry. Our investment in ArtiFlex is incorporated herein by reference. accounted for under the equity method, as our ownership interest does not constitute a controlling financial interest. As we do not have a controlling financial interest in ArtiFlex, the contributed net assets were deconsolidated effective May 9, 2011.On March 18, 2011, we joined with Gestamp Renewables group to create Gestamp Worthington Wind Steel, LLC, a 50%-owned joint venture focused on producing towers for wind turbines being constructed in North America. This unconsolidated joint venture has identified Cheyenne, Wyoming as the site of the initial production facility. We anticipate contributing $9.5 million of cash to the Gestamp JV, mostly in fiscal 2012. Our investment in this joint venture is accounted for under the equity method, as our ownership interest does not constitute a controlling financial interest. On March 1, 2011, we closed an agreement with Marubeni-Itochu Steel America Inc. (“MISA”) to combine certain assets of Dietrich and ClarkWestern Building Systems in a newly-created joint venture. In exchange for the contributed net assets, we received a 25% interest in the new joint venture, ClarkDietrich, as well as the assets of certain MISA Metals, Inc. (“MMI”) steel processing locations, some of which were subsequently classified as assets held for sale in our consolidated balance sheet. Our contribution to ClarkDietrich consisted of our metal framing business, including all of the related working capital and six of the 13 facilities. We retained and continue to operate the remaining facilities, on a short-term basis, to support the transition of the business into the new joint venture. Our investment in ClarkDietrich is accounted for under the equity method, as our ownership interest does not constitute a controlling financial interest. As we do not have a controlling financial interest in ClarkDietrich, the contributed net assets were deconsolidated effective March 1, 2011. On December 28, 2010, we acquired a 60% ownership interest in Nitin Cylinders Limited, which is now Worthington Nitin Cylinders Limited, for cash consideration of approximately $21.2 million. WNCL is a manufacturer of high pressure, seamless steel cylinders for compressed industrial gases and compressed natural gas storage in motor vehicles. The results of this joint venture are consolidated in our Pressure Cylinders operating segment due to our controlling financial interest. On November 19, 2010, we joined with Hubei Modern Urban Construction and Development Group Co., Ltd. (“HMUCG”) of China to create Worthington Modern Steel Framing Manufacturing Co. Ltd (“WMSFMCo.”). We contributed approximately $6.2 million of cash in exchange for our 40% ownership interest in the joint venture. The purpose of WMSFMCo. is to design, manufacture, assemble and distribute steel framing materials and accessories for construction projects in five Central Chinese provinces and to provide project management and building design and construction supply services for those projects. Our investment in this joint venture is accounted for under the equity method, as our ownership interest does not constitute a controlling financial interest. On June 21, 2010, our Pressure Cylinders operating segment acquired, for cash consideration of $12.2 million, the net assets of Hy-Mark Cylinders, Inc. (“Hy-Mark”), which manufactured extruded aluminum cylinders for medical oxygen, scuba, beverage service, industrial specialty and professional racing applications. The assets of Hy-Mark have been moved to our pressure cylinders facility located in Mississippi. Transformation Plan In our fiscal year ended May 31, 2008 (“fiscal 2008”), we initiated a Transformation Plantransformation plan (the "Plan"“Transformation Plan”) with the overall goal to improve the Company'sof improving our sustainable earnings potential, asset utilization and operational performance. TheTo accomplish this, the Transformation Plan is being implemented over a three-year period and focuses on cost reduction, margin expansion and organizational capability improvements and, in the process, seeks to drive excellence in three core competencies: sales, operationssales; operations; and supply chain management. The Transformation Plan is comprehensive in scope and includes aggressive diagnostic and implementation phases. To date, we have completed the transformation phases in each of the core facilities within our Steel Processing and Metal Framing business segments.operating segment, including the facilities of our Mexican joint venture, Serviacero Planos, S. de R. L. de C.V. We also substantially completed the transformation phases at our metal framing facilities prior to their contribution to ClarkDietrich. We retained a consulting firm to assist in the development and implementation of the Plan. The services provided by this firm included diagnostic tools, performance improvement technologies, project management techniques, benchmarking information, and insights that directly relate to the Plan. Internal transformation teams have also been formed and are dedicated to the Plan efforts. As of May 31, 2009, responsibility for executing the Plan has been successfully transitioned to our internal transformation teams.

Plan initiatives executed to date include facility closings, head count reductions, other cost reductions, an enhanced and more focused commercial sales effort, improved operating efficiencies, a consolidated sourcing and supply chain strategy, and a continued emphasis on safety. The positive results2011, we have recognized approximately $67.9 million of these efforts, however, have been over-shadowed by the negative impact of the recessionary business conditions.

Pre-taxtotal restructuring charges associated with the Transformation Plan, totaled $43,041,000 forincluding charges of $18.1 million, $43.0 million, $4.2 million and $2.6 million during fiscal 2009.2008, fiscal 2009, fiscal 2010 and fiscal 2011, respectively. See “Item 8. – Financial Statements and Supplementary Data – Notes to Consolidated Financial Statements – Note ND – Restructuring” and Other Expense” of this Annual Report on Form 10-K for further information onregarding our restructuring charges. That information is incorporated herein by reference.

We anticipate that we will incur an additional $6,000,000 in restructuring chargeshave seen positive results from these efforts, even with the negative impact of the recent economic recession. Accordingly, during theour upcoming fiscal year, ending May 31, 2010.we plan to initiate the diagnostics phase in our Pressure Cylinders operating segment. Recent Developments

On June 2, 2008, Worthington purchased substantially allAs this process began, we retained a consulting firm to assist in the development and implementation of the assets of The Sharon Companies Ltd. (“Worthington Stairs”)Transformation Plan. As it progressed, we formed internal teams dedicated to this effort, and they ultimately assumed full responsibility for $37,150,000. Worthington Stairs designs and manufactures steel egress stair systems forexecuting the commercial construction market, and operates one manufacturing facility in Akron, Ohio. It operates asTransformation Plan. These internal teams are now an integral part of our business and constitute what we refer to as the Construction Services segment, Worthington Integrated Building Systems, LLCCenters of Excellence (“WIBS”COE”). The purchase price was allocated to the acquired assets and assumed liabilities based on their estimated fair values at the date of acquisition, with goodwill representing the excess of the purchase price over the fair value allocated to the net assets. The purchase price allocated to intangible assets will be amortized over a weighted average life of 13 years.

On July 31, 2008, our Worthington Steelpac Systems, LLC (“Steelpac”) subsidiary purchased the assets of Laser Products (“Laser”) for $3,425,000. Laser is a steel rack fabricator primarily serving the auto industry. The purchase price was allocated to working capital, fixed assets, and customer list. The purchase price allocated to customer list will be amortized over ten years.

On October 1, 2008, Worthington expanded and modified Worthington Specialty Processing (“WSP”), our joint venture with United States Steel Corporation (“U.S. Steel”). U.S. Steel contributed ProCoil Company L.L.C., its steel processing facility in Canton, Michigan that slits, cuts-to-length and presses blanks from steel coils to desired specifications, and also provides laser welding services and warehouses material for automotive customers. Worthington contributed its steel processing subsidiary in Taylor, Michigan that slits, cuts-to-length and tension levels steel coils, plus $2,500,000 in cash. After the contributions, Worthington owns 51% and U.S. Steel owns 49% of WSP. The joint ventureCOE will continue to be accounted for usingmonitor the equity method as both parties have equal control. WSP is expected to better serve the changing needsperformance metrics and new processes instituted across our transformed operations and drive continuous improvements in all areas of our operations. The majority of the automotive and flat-rolled customers by allowing each of the three entities to maximize their individual processing specialties with this expansion of the joint venture.

During October 2008, we sold our 49% equity interest in Canessa Worthington Slovakia s.r.o. for approximately $3,700,000 to the Magnetto Group, the other member of the joint venture. The gain on the transaction was immaterial.

During January 2009, we sold our 60% equity interest in Aegis Metal Framing, LLC for approximately $24,000,000 to MiTek Industries, Inc., the other member of the joint venture. This resulted in a pre-tax gain of $8,331,000.

During May 2009, we sold our 50% equity interest in Accelerated Building Technologies, LLC to NOVA Chemicals Corporation, the other member of the joint venture. The sales price and loss on the transaction were immaterial.

On June 1, 2009, we purchased the assetsexpenses related to the business of Piper Metal Forming Corporation (“Piper”), U.S. Respiratory, Inc. and Pacific Cylinders, Inc., for approximately $10,000,000, subject to closing adjustments. Piper is a manufacturer of aluminum high pressure cylinders, and impact extruded steel and aluminum parts, serving the medical, automotive, defense, oil services and other commercial markets, with one manufacturing location in New Albany, Mississippi. U.S. Respiratory provides value-added assembly and distribution of Piper’s medical cylinder products. Pacific Cylinders provides West Coast distribution from Diamond Springs, California. The revenues of this group were approximately $30,000,000 for the 2008 calendar year. These assetsCOE will be included in our Pressure Cylinders business segment.selling, general and administrative (“SG&A”) expense going forward.

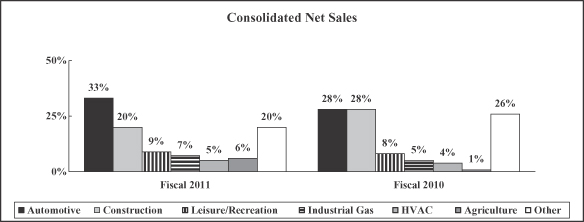

Steel Processing TheOur Steel Processing businessoperating segment consists of the Worthington Steel business unit, andwhich includes Precision Specialty Metals, Inc.,PSM, a specialty stainless processor located in Los Angeles, California, (“PSM”), and Spartan, Steel Coating, LLC (“Spartan”), a consolidated joint venture whichthat operates a cold-rolled hot dipped galvanizing line. For fiscal 2009, the2011, fiscal year ended May 31, 2008 (“2010 and fiscal 2008”), and the fiscal year ended May 31, 2007 (“fiscal 2007”),2009, the percentage of consolidated net sales generated by theour Steel Processing operating segment was 45%approximately 58%, 48%51%, and 49%45%, respectively.

Worthington Steel is one of America’sthe largest independent intermediate processors of flat-rolled steel.steel in the United States. It occupies a niche in the steel industry by focusing on products requiring exact specifications. These products cannot typically be supplied as efficiently by steel mills or end-users of these products. TheOur Steel Processing businessoperating segment including Spartan, owns and operates nine manufacturing facilities – one each in California, Indiana, Maryland, Michigan, and South Carolina and three in Ohio – and leases one manufacturing facility in Alabama.

Worthington Steel serves approximately 1,100 customers, from these facilities, principally in the agricultural, appliance, automotive, construction, hardware, furniture, HVAC, lawn and garden, hardware, furniture, office equipment, electrical control, tubing, leisure and recreation, appliance, agricultural, HVAC, container,office equipment and aerospacetubing markets. Automotive-related customers have historically represented approximately half of this businessoperating segment’s net sales. No single customer represented greater than 6%10% of net sales for the Steel Processing businessoperating segment during fiscal 2009.2011.

Worthington Steel buys coils of steel from integrated steel mills and mini-mills and processes them to the precise type, thickness, length, width, shape temper and surface quality required by customer specifications. Computer-aided processing capabilities include, among others: pickling, a chemical process using an acidic solution to remove surface oxide which develops on hot-rolled steel; slitting, which cuts steel to specific widths; cold reducing, which achieves close tolerances of thickness and temper by rolling;thickness; hot-dipped galvanizing, which coats steel with zinc and zinc alloys through a hot-dipped process; hydrogen annealing, a thermal process that changes the hardness and certain metallurgical characteristics of steel; cutting-to-length, which cuts flattened steel to exact lengths; tension leveling, a method of applying pressure to achieve precise flatness tolerances for steel; edging, which conditions the edges of the steel by imparting round, smooth or knurled edges; non-metallic coating, including dry lubrication, acrylic and paint; and configured blanking, which stamps steel into specific shapes. Worthington Steel also toll processes steel for steel mills, large end-users, service centers and other processors. Toll processing is different from typical steel processing in that the mill, end-user or other party retains title to the steel and has the responsibility for selling the end product. Toll processing enhances Worthington Steel’s participation in the market for wide sheet steel and large standard orders, which is a market generally served by steel mills rather than by intermediate steel processors. The steel processing industry is fragmented and highly competitive. There are many competitors, including other independent intermediate processors. Competition is primarily on the basis of price, product quality and the ability to meet delivery requirements. Technical service and support for material testing and customer-specific applications enhance the quality of products (See “Item 1. – Business – Technical Services”). However, the extent to which technical service capability has improved Worthington Steel’s competitive position has not been quantified. Worthington Steel’s ability to meet tight delivery schedules is, in part, based on the proximity of our facilities to customers, suppliers and one another. The extent to which plant location has impacted Worthington Steel’s competitive position has not been quantified. Processed steel products are priced competitively, primarily based on market factors, including, among other things, competitive market pricing, the cost and availability of raw materials, transportation and shipping costs, and overall economic conditions in the United States and abroad. As noted in theMetal FramingRecent Developmentssection herein, on March 1, 2011 we acquired certain steel processing assets of MISA Metals, Inc. Pressure Cylinders The Metal Framing businessOur Pressure Cylinders operating segment consistingconsists of the DietrichWorthington Cylinders business unit designs and produces metal framing components and systems and related accessories for the commercial and residential construction markets within the United States and Canada.WNCL, a consolidated joint venture based in India. For fiscal 2009,2011, fiscal 2008,2010 and fiscal 2007,2009, the percentage of consolidated net sales generated by the Metal Framingour Pressure Cylinders operating segment was 25%approximately 24%, 26%,24% and 26%20%, respectively.

Metal Framing products include steel studs and track, floor and wall system components, roof trusses and other building product accessories, such as metal corner bead, lath, lath accessories, clips, fasteners and vinyl bead and trim.

The Metal Framing business segment has 15 operating facilities located throughout the United States: one each in Colorado, Florida, Georgia, Hawaii, Illinois, Indiana, Kansas, Maryland, and New Jersey, and two each in California, Ohio, and Texas. This business segment also has two operating facilities in Canada: one each in British Columbia and Ontario.

Dietrich is the largest metal framing manufacturer in the United States, supplying approximately one-third of the metal framing products sold in the United States. Dietrich is the second largest metal framing manufacturer in Canada with a market share between 25% and 30%. Dietrich serves approximately 3,900 customers, primarily consisting of wholesale distributors, commercial and residential building contractors, and mass merchandisers. During fiscal 2009, Dietrich’s three largest customers represented approximately 17%, 10% and 10%, respectively, of the net sales for the business segment, while no other customer represented more than 3% of net sales for the business segment.

The light-gauge metal framing industry is very competitive. Dietrich competes with seven large regional or national competitors and numerous small, more localized competitors, primarily on the basis of price, service, breadth of product line and quality. As is the case in the Steel Processing business segment, the proximity of facilities to customers and their project sites provides a service advantage and impacts freight and shipping costs. Dietrich’s products are transported by both common and dedicated carriers. The extent to which facility location has impacted Dietrich’s competitive position has not been quantified.

Dietrich uses numerous trademarks and patents in its business. Dietrich licenses from Hadley Industries the “UltraSTEEL®” registered trademark and the United States and Canadian patents to manufacture “UltraSTEEL®” metal framing and accessory products. The “Spazzer®” trademark is used in connection with wall component products that are the subject of four United States patents, two foreign patents, one pending United States patent application, and several pending foreign patent applications. The trademark “TradeReady®” is used in connection with floor-system products that are the subject of four United States patents, numerous foreign patents, one pending United States patent application, and several pending foreign patent applications. The “Clinch-On®” trademark is used east of the Rocky Mountains in connection with corner bead and metal trim products for gypsum wallboard. Dietrich licenses the “PRO X®” and the “SLP-TRK®" trademarks as well as the patent to manufacture "SLP-TRK®" slotted track in the United States and “Pro XR” header system from Brady Construction Innovations, Inc. Dietrich also has a number of other patents, trademarks and trade names relating to specialized products. The Metal Framing business segment intends to continue to use these trademarks and renew its registered trademarks.

Pressure Cylinders

TheOur Pressure Cylinders segment consists of the Worthington Cylinders business unit. For fiscal 2009, fiscal 2008, and fiscal 2007, the percentage of consolidated net sales generated by Worthington Cylinders was 20%, 19%, and 18%, respectively.

Worthington Cylinders operates eight manufacturing facilities with three in Ohio and one each in Wisconsin, Austria, Canada, the Czech Republic and Portugal.

The Pressure Cylinders businessoperating segment produces a diversified line of pressure cylinders, includingincluding: low-pressure liquefied petroleum gas (“LPG”) and refrigerant gas cylinders; high-pressure and industrial/specialty gas cylinders; seamless steel high pressure cylinders for compressed natural gas storage in motor vehicles; aluminum-lined, composite-wrapped high-pressure cylinders; airbrake tanks; and certain consumer products. The following is a more detailed discussion of these products:

LPG cylinders are sold to manufacturers, distributors and mass merchandisers and are used to hold fuel for gas barbecue grills, recreational vehicle equipment, residential and light commercial heating systems, industrial forklifts propane-fueled camping equipment, hand held torches, and commercial/residential cooking (the latter, generally outside North America). Refrigerant gas cylinders are sold primarily to major refrigerant gas producers and distributors and are used to hold refrigerant gases for commercial, residential and automotive air conditioning and refrigeration systems. High-pressure Industrial gas products include high-pressure, acetylene and industrial/specialty gas (steel and aluminum) cylinders. These cylinders are sold primarily to gas producers and distributors for gas containment for uses such as containers for gases used in: cutting, and welding, metals; breathing (medical, diving and firefighting);, semiconductor production;production, and beverage delivery;delivery. Retail products include camping fuel cylinders, barbecue grill cylinders, propane accessories, including propane-fueled camping equipment, hand held torches and accessories and Balloon Time helium balloon kits for all party occasions. These products are sold primarily to manufacturers, distributors and mass merchandisers. Alternative fuel cylinders include Type I, II, III and ASME tanks for containment of compressed natural gas, systems. Worthington Cylinders also produces recovery tanks for refrigerant gases,hydrogen and propane. Specialty products include air reservoirs for truck and trailertruck trailers, which are sold to original equipment manufacturers, and “Balloon Time®” helium kits which include non-refillable cylinders. a variety of fire suppression and chemical tanks. While a large percentage of cylinder sales within Pressure Cylinders are made to major accounts, Worthington Cylinders hasthis operating segment serves approximately 2,0002,700 customers. During fiscal 2009,2011, no single customer represented more than 10% of net sales for the businessgenerated by our Pressure Cylinders operating segment. WorthingtonThe Pressure Cylinders operating segment produces low-pressure steel cylinders within a wide range of refrigerant capacities of 15 to 1,000 pounds and steel and aluminum cylinders within a wide range of LPG capacities of 14.1 ounces to 420 pounds.capacities. Low-pressure cylinders are produced by precision stamping, drawing, welding and/or brazing component parts to customer specifications. They are then tested, painted and packaged, as required. High-pressure steel cylinders are manufactured by several processes, including deep drawing, tube spinning and billet piercing.

In the United States and Canada, high-pressure and low-pressure cylinders are primarily manufactured in accordance with U.S.United States Department of Transportation and Transport Canada specifications. Outside the United States and Canada, cylinders are manufactured according to European norm specifications, as well as various other international standards. In the United States and Canada, Worthington Cylinders has one principal domestic competitor in the low-pressure non-refillable refrigerant market, one principal domestic competitor in the low-pressure LPG cylinder market and twothree principal domestic competitors in the high-pressure cylinder market. There are also several foreign competitors in these markets. We believe that Worthington Cylinders believes that it has the largest domestic market share in both low-pressure cylinder markets. In the European high-pressure cylinder market, there are also several competitors. We believe that Worthington Cylinders believes that it is a leading producer in both the high-pressure cylinder and low-pressure non-refillable cylinder markets in Europe. Worthington Cylinders generally has a strong competitive position for its retail and specialty products, but competition varies on a product-by-product basis. As with Worthington’sour other businessoperating segments, competition is based upon price, service and quality. The Pressure Cylinders businessoperating segment uses the trade name “Worthington Cylinders” to conduct business and the registered trademark “Balloon Time®” to market low-pressure helium balloon kits; the registered trademark “FLAMESAVER“Bernzomatic™®” to market certain LP gas cylinders;fuel cylinders and hand held torches; the registered trademark “WORTHINGTON PRO GRADE™®” to market certain LPG cylinders, hand torch cylinderstorches and camping fuel cylinders; and the registered trademark “MAP-PRO™®” Pro-Max® to market certain hand torch cylinders.cylinders; and the registered trademark SCI® to market certain cylinders for transportation of compressed gases for inflation of flotation bags and escape slides, Self Contained Breathing Cylinders (SCBA) for firefighting and cylinders to contain compressed natural gas. The Pressure Cylinders businessoperating segment intends to continue to use these trademarks and renew itsthese registered trademarks. As noted under “Recent Developments”,Recent Developmentssection herein, Hy-Mark and the recently acquired Piper business will be included inconsolidated joint venture with Nitin Cylinders Limited, WNCL, became part of the Pressure Cylinders operating segment during fiscal 2011. Metal Framing The Metal Framing operating segment consists of our Dietrich Metal Framing business segment.unit. As more fully described in “Item 8. – Financial Statements and Supplementary Data – Notes to Consolidated Financial Statements – Note A – Summary of Significant Accounting Policies,” on March 1, 2011, we contributed certain assets of Dietrich to a newly-formed joint venture, ClarkDietrich. We retained seven of the 13 metal framing facilities, which continue to operate, on a short-term basis, to support the transition of the business into the new joint venture. Following this brief transition period, these assets will be disposed of. The financial results and operating performance of the retained facilities will continue to be reported within our Metal Framing operating segment until their expected disposition in fiscal 2012. The contributed net assets, which were deconsolidated effective March 1, 2011, will continue to be reported within Metal Framing on a historical basis. Refer to theJoint Venturessection herein for additional information about the operations of ClarkDietrich. Other The “Other”Other category consists of operating segments that do not meet the applicable aggregation criteria and materiality tests for purposes of separate disclosure, and other corporate related entities. These businessThrough May 9, 2011, these operating segments areincluded Automotive Body Panels, Construction ServicesSteel Packaging, and Steel Packaging. Thethe Global Group. On May 9, 2011, in connection with the contribution of our automotive body panels subsidiary, Gerstenslager, to ArtiFlex and the resulting deconsolidation of the contributed net assets, we no longer maintain a separate Automotive Body Panels business segmentoperating segment. Accordingly, subsequent to May 9, 2011, the operating segments comprising the Other category consists of The Gerstenslager Company (“Gerstenslager”), whichSteel Packaging and the Global Group. Each of these operating segments is ISO/TS 16949:2002explained in more detail below. We will continue to report the historical financial results and ISO14001 certified. Gerstenslager provides stamping, blanking, assembly, painting, packaging, die management, warehousing, distribution management and other services to customers, primarilyoperating performance of our former Automotive Body Panels operating segment on a historical basis through May 9, 2011. This former operating segment has historically been reported in the automotive industry. Gerstenslager operates two facilities in Ohio. Gerstenslager is a major supplier to“Other” category for segment reporting purposes, as it has not meet the automotive past-model year market and manages more than 3,600 finished good part numbers and more than 12,500 stamping dies/fixture setsapplicable aggregation criteria or materiality thresholds for separate disclosure. Accordingly, this organizational change did not impact the past- and current-model year automotive and truck manufacturers, both domestic and transplant.composition of our reportable segments.

The Construction Services business segment operates out of three facilities, one each in Tennessee, Washington, and Ohio. This business segment consists of the WIBS business unit which includes Worthington Mid-Rise Construction, Inc., which designs and builds mid-rise light-gauge steel framed commercial structures and multi-family housing units; Worthington Military Construction, Inc., which is involved in the supply and construction of metal framing products for, and in the framing of, single family housing, with a focus on military; and Worthington Stairs, a manufacturer of pre-engineered steel egress stair solutions.

Steel Packaging.The Steel Packaging businessoperating segment consists of Steelpac, which is an ISO-9001: 2000 certified manufacturer of engineered, recyclable steel shipping solutions. Steelpacpackaging solutions for external and internal movement of product. Steel Packaging operates three facilities, with one facility in each inof Indiana, Ohio and Pennsylvania. SteelpacSteel Packaging designs and manufactures reusable custom platforms, racks and pallets made of steel for supporting, protecting and handling products throughout the shipping process for industries such as automotive, lawn and garden and recreational vehicles. Global Group. The purpose of the Global Group operating segment, which comprises our Mid-Rise Construction, Military Construction and Commercial Stairs business units, is to identify and develop potential growth platforms by applying our core competencies in metals manufacturing and construction methods. The Global Group operates a business platform that includes high density mid-rise residential construction in emerging markets. Other operating activities of the Global Group include the design, supply and build of mid-rise light gauge steel framed commercial structures and multi-family housing units; the supply and construction of metal framing products for, and in the framing of, single family housing, with a focus on military housing; and the manufacturing of pre-engineered steel egress stair solutions. Segment Financial Data Financial information for the reportable business segments is provided in “Item 8. – Financial Statements and Supplementary Data – Notes to Consolidated Financial Statements – Note HM – Segment Data” of this Annual Report on Form 10-K. That financial information is incorporated herein by reference. Financial Information About Geographic Areas ForeignIn fiscal 2011, our foreign operations represented 9%, 9%, and 8% of consolidated net sales, for5% of pre-tax earnings attributable to controlling interest and 32% of consolidated net assets. During fiscal 2011, fiscal 2010 and fiscal 2009, fiscal 2008,we had operations in North America, China, Europe and fiscal 2007, respectively.India. Summary information about Worthington’sour foreign operations, including net sales and fixed assets by geographic region, is set forthprovided in “Item 8. – Financial Statements and Supplementary Data – Notes to Consolidated Financial Statements – Note A – Summary of Significant Accounting Policies – Risks and Uncertainties” of this Annual Report on Form 10-K. That summary information is incorporated herein by reference. For fiscal 2009, fiscal 2008, and fiscal 2007, Worthington had operations in North America and Europe. Net sales by geographic region are provided in “Item 8. – Financial Statements and Supplementary Data – Notes to Consolidated Financial Statements – Note H –Segment Data” of this Annual Report on Form 10-K. That information is incorporated herein by reference.

Suppliers The primary raw material purchased by Worthington is steel. We purchase steel from major primary producers of steel, both domestic and foreign. The amount purchased from any particular supplier varies from year-to-yearyear to year depending on a number of factors including market conditions, then current relationships and prices and terms offered. In nearly all market conditions, particularly now, steel is available from a number of suppliers and generally any supplier relationship or contract can and has been replaced with little or no significant interruption to our business. In fiscal 2009, Worthington2011, we purchased approximately 1.71.8 million tons of steel (58%(68% hot-rolled, 30%18% galvanized and 12%14% cold-rolled) on a consolidated basis. Steel is purchased in large quantities at regular intervals from major primary producers, both domestic and foreign. In the Steel Processing businessoperating segment, steel is primarily purchased and processed based on specific customer orders. The Metal Framing and Pressure Cylinders business segments purchaseoperating segment purchases steel to meet production schedules. For certain raw materials, there are more limited suppliers – for example, hydrogen and zinc, which are generally purchased at market prices. Since there are a limited number of suppliers in the hydrogen and zinc markets, if delivery from a major supplier is disrupted due to a force majeure type occurrence, it may be difficult to obtain an alternative supply. Raw materials are generally purchased in the open market on a negotiated spot-market basis at prevailing market prices. Supply contracts are also entered into, some of which have fixed pricing.pricing and some of which are indexed (monthly or quarterly). During fiscal 2009, the Company2011, we purchased steel from the following major suppliers, in alphabetical order: AK Steel Corporation; ArcelorMittal; California Steel Industries, Inc; Duferco Farrell Corp; Gallatin Steel Company; North Star BlueScope Steel LLC; Nucor Corporation; Severstal North America, Inc.; Steel Dynamics, Inc.; Stemcor Holdings Limited; United States Steel Corporation;Corporation (“U.S. Steel”); USS-POSCO Industries, and USS-POSCO Industries.RG Steel LLC. Alcoa, Inc. was the primary aluminum supplier for the Pressure Cylinders businessoperating segment in fiscal 2009.2011. Major suppliers of zinc to the Steel Processing businessoperating segment were, in alphabetical order: Considar Metal Marketing Inc. (a/k/a HudBay); Industrias Peñoles; Teck Cominco Limited; U. S.U.S. Zinc; and Xstrata Zinc Canada. Approximately 20.531 million pounds of zinc were purchased in fiscal 2009. Worthington believes its2011. We believe our supplier relationships are good. Technical Services Worthington employsWe employ a staff of engineers and other technical personnel and maintainsmaintain fully equipped laboratories to support operations. These facilities enable verification, analysis and documentation of the physical, chemical, metallurgical and mechanical properties of raw materials and products. Technical service personnel also work in conjunction with the sales force to determine the types of flat-rolled steel required for customer needs. Additionally, technical service personnel design and engineer metal framing structures and provide sealed shop drawings to the building construction markets. To provide these services, Worthington

maintainswe maintain a continuing program of developmental engineering with respect to product characteristics and performance under varying conditions. Laboratory facilities also perform metallurgical and chemical testing as dictated by the regulations of the U.S.United States Department of Transportation, Transport Canada, and other associated agencies, along with International Organization for Standardization (ISO) and customer requirements. All design work complies with applicable current local and national building code requirements. An IASIASI (International Accreditations Service, Incorporated) accredited product-testing laboratory supports these design efforts.

Seasonality and Backlog Sales areHistorically, sales have generally been weaker in the third quarter of theour fiscal year, primarily due to reduced activity in the building and construction industry as a result of theinclement weather, as well as customer plant shutdowns in the automotive industry due to holidays. Sales are generally strongest in the fourth quarter of theour fiscal year when all of theas our operating segments are normallygenerally operating at seasonal peaks.

We do not believe backlog is a significant indicator of our business. Employees As of May 31, 2009, Worthington employed2011, we had approximately 6,4008,400 employees, in its operations, including our unconsolidated joint ventures. Approximately 13%7% of these employees wereare represented by collective bargaining units. Worthington believes it has good relationships with its employees in general, including those covered by collective bargaining units. Joint Ventures As part of aour strategy to selectively develop new products, markets and technological capabilities and to expand an international presence, while mitigating the risks and costs associated with those activities, Worthington participateswe participate in onetwo consolidated and fiveten unconsolidated joint ventures. Consolidated Spartan is a 52%-owned consolidated joint venture with a subsidiary of Severstal North America, Inc. (“Severstal”), located in Monroe, Michigan. It operates a cold-rolled, hot-dipped galvanizing line for toll processing steel coils into galvanized and galvannealed products intended primarily for the automotive industry. Spartan'sSpartan’s financial results are fully consolidated into thewithin our Steel Processing reportable business segment. The equity ownership ofowned by Severstal is shown as minoritynoncontrolling interest on the Company’sour consolidated balance sheets and itsSeverstal’s portion of operating incomenet earnings is eliminatedincluded as net earnings attributable to noncontrolling interest in miscellaneous expenseour consolidated statements of earnings. WNCL is a 60%-owned consolidated joint venture with India-based Nitin Cylinders Limited (“Nitin”). WNCL manufactures high pressure, seamless steel cylinders for compressed natural gas storage in motor vehicles, and produces cylinders for compressed industrial gases. WNCL’s financial results are fully consolidated within our Pressure Cylinders reportable business segment. The equity owned by Nitin is shown as noncontrolling interest on the Company’sour consolidated balance sheets and Nitin’s portion of net earnings is included as net earnings attributable to noncontrolling interest in our consolidated statements of earnings. Unconsolidated ArtiFlex, a 50%-owned joint venture with ITS-H Holdings, LLC, provides an integrated solution for engineering, tooling, stamping, assembly and other services to customers primarily in the automotive industry. ArtiFlex owns and operates four manufacturing facilities – one each in Kentucky and Ohio; and two facilities in Michigan – and leases another manufacturing facility in Ohio. ClarkDietrich, a 25%-owned joint venture with ClarkWestern Building Systems, LLC, is the industry leader in the manufacture and supply of light gauge steel framing products in the United States. ClarkDietrich manufactures a full line of drywall studs and accessories, structural studs and joists, metal lath and accessories, and shaft wall studs and track used primarily in residential and commercial construction. This joint venture operates 13 manufacturing facilities, one each in Connecticut, Florida, Georgia, Hawaii, Illinois, Kansas, and Maryland and two each in California, Ohio and Texas. Gestamp Worthington Wind Steel, LLC (the “Gestamp JV”), a 50%-owned joint venture with Gestamp Wind Steel U.S., Inc., focuses on producing towers for wind turbines being constructed in the North American market. The Gestamp JV plans to construct a manufacturing facility in Cheyenne, Wyoming, that is expected to begin operating prior to the end of the fourth quarter of fiscal 2012. LEFCO Worthington, LLC ("(“LEFCO Worthington"Worthington”), a 49%-owned joint venture with LEFCO Industries, LLC, is a minority business enterprise which offers engineered wooden crates, specialty pallets and steel rack systems for a variety of industries. LEFCO Worthington operates one manufacturing facility in Cleveland, Ohio. Samuel Steel Pickling Company (“Samuel”), a 31.25%-owned joint venture with Samuel Manu-Tech Pickling, operates a steel pickling facility in Twinsburg, Ohio, and one in Cleveland, Ohio. Samuel also performs in-line slitting, side trimming, pickle dry, under winding and the application of dry lube coatings during the pickling process. Serviacero Planos, S.A.S. de R.L. de C.V. ("(“Serviacero Worthington"Worthington”), a 50%-owned joint venture with Inverzer, S.A. de C.V., operates three facilities in Mexico, one each in Leon, Queretaro and Monterrey. The Monterrey facility, opened in mid-July 2009, has not been included as part of our location count. Serviacero Worthington provides steel processing services such as slitting, multi-blanking and cutting-to-length to customers in a variety of industries including automotive, appliance, electronics and heavy equipment. TWB Company, L.L.C. (“TWB”), a 45%-owned joint venture with ThyssenKrupp Steel North America, Inc., is a leading North American supplier of tailor welded blanks. TWB produces laser-welded blanks for use in the automotive industry for products such as inner-door panels, bodysides,body sides, rails and pillars. TWB operates facilities inin: Prattville, Alabama; Monroe, Michigan; and in Puebla, Ramos Arizpe (Saltillo) and Hermosillo, Mexico. TWB closed its Columbus, Indiana facility during fiscal 2009. Worthington Armstrong Venture (“WAVE”), a 50%-owned joint venture with Armstrong Ventures, Inc., a subsidiary of Armstrong World Industries, Inc., is one of the three largest global manufacturers and multiple smaller international manufacturers of suspension grid systems for concealed and lay-in panel ceilings used in commercial and residential ceiling markets. It competes with the two other global manufacturers and numerous smaller manufacturers. WAVE operates seveneight facilities in fivesix countries: Aberdeen, Maryland; Benton Harbor, Michigan; and North Las Vegas, Nevada, within the United States; Shanghai, the Peoples Republic of China; Team Valley, United Kingdom; Valenciennes,Prouvy, France; Marval, Pune, India; and Madrid, Spain. WSP,WMSFMCo, a 40%-owned joint venture with China-based HMUCG, designs, manufactures, assembles and distributes steel framing materials and accessories for construction projects in five Central Chinese provinces and also provides project management and building design and construction supply services thereto. This joint venture operates one facility located in Xiantao City, Hubei Province, China.

Worthington Specialty Processing (“WSP”), a 51%-owned joint venture with U.S. Steel, operates three steel processing facilities located in Canton, Jackson and Taylor, Michigan, which are managed by Worthington Steel. WSP serves primarily as a toll processor for U.S. Steel and others. Its services include slitting, blanking, cutting-to-length, laser welding, tension leveling and warehousing. WSP is considered to be jointly controlled and not consolidated due to substantive participating rights of the minority partner. See “Item 8. – Financial Statements and Supplementary Data – Notes to Consolidated Financial Statements – Note JB – Investments in Unconsolidated Affiliates” for furtheradditional information about Worthington’s participation inour unconsolidated joint ventures. Environmental Regulation Worthington’sOur manufacturing facilities, generally in common with those of similar industries making similar products, are subject to many federal, state and local requirements relating to the protection of the environment. WorthingtonWe continually examinesexamine ways to reduce emissions and waste and to decrease costs related to

environmental compliance. The cost of compliance or capital expenditures for environmental control facilities required to meet environmental requirements are not anticipated to be material when compared with overall costs and capital expenditures and, accordingly, are not anticipated to have a material effect on theour financial position, results of operations, cash flows, or the competitive position of the Company.Worthington or any particular segment. Item 1A. — Risk Factors Future results and the market price for Worthington Industries’ common shares are subject to numerous risks, many of which are driven by factors that cannot be controlled or predicted. The following discussion, as well as other sections of this Annual Report on Form 10-K, including “Item“PART II – Item 7. – Management'sManagement’s Discussion and Analysis of Financial Condition and Results of Operations,” describe certain business risks. Consideration should be given to the risk factors described below as well as those in the Safe Harbor Statement at the beginning of this Annual Report on Form 10-K, in conjunction with reviewing the forward-looking statements and other information contained in this Annual Report on Form 10-K. These risks are not the only risks we face. Our business operations could also be affected by additional factors that are not presently known to us or that we currently consider to be immaterial in our operations. Economic or Industry Downturns The current global recession hasthat began in 2008 adversely affected and is likely tomay continue to adversely affect our business and our industries, as well as the industries and businesses of many of our customers and suppliers. The volatile domestic and global recessionary climate is havinghad significant negative impacts on our business. The global recession, hasand the sluggish pace of the recovery from the global recession, resulted in a significant decrease in customer demand throughout nearly all of our markets, including our two largest markets – construction and automotive. The impacts of government approvedexisting and proposedany new government measures to aid economic recovery, including economicvarious measures intended to provide stimulus legislationto the economy in general or to certain industries, and assistancethe growing debt levels of the United States and other countries, continue to automotive manufacturers and others, are currentlybe unknown. Overall, operating levels across many of our businessesbusiness segments have fallen and may remain at depressed levels until economic conditions improve and demand increases. Continued volatility While certain sectors of the economy have stabilized and recovered from the economic downturn, we are unable to predict the strength, pace or sustainability of the economic recovery or the effects of government intervention or debt levels. Overall general economic conditions, both domestically and globally, have improved from the lows reached during the recession. The automotive market has shown signs of strengthening, and the construction market has shown signs of stabilizing. However, global economic conditions remain fragile, and the possibility remains that the domestic or global economies, or certain industry sectors of those economies that are key to our sales, may not recover as quickly as anticipated, or could further deteriorate, which could result in the United Statesa corresponding decrease in demand for our products and worldwide capital and credit markets has impacted and is likely to continue to significantlynegatively impact our end marketsresults of operations and result in continued negative impacts on demand, increased credit and collection risks and other adverse effects on our business. The domestic and worldwide capital and credit markets have experienced and are experiencing significant volatility, disruptions and dislocations with respect to price and credit availability. These have caused diminished availability of credit and other capital in our end markets, including automotive and construction, and for participants in, and the customers of, those markets. There is continued uncertainty as to when and if the capital and credit markets will improve and the impact this period of volatility will have on our end markets and business in general.financial condition.

The construction and automotive industries account for a significant portion of our net sales, and reductions in demand from these industries have adversely impacted and are likely tomay continue to adversely affect our business. The overall downturn in the economy, the disruption in capital and credit markets, declining real estate values, high unemployment rates and reduced consumer confidence and spending have caused significant reductions in demand from our end markets in general and, in particular, the construction and automotive end markets. Demand in the commercial and residential construction markets has weakenedbeen weak as it has become morebeen difficult for companies and consumers to obtain credit for construction projects and the economic slowdown has caused delays in or cancellations of construction projects. Non-residential construction, including publicly financed state and municipal projects, has slowed significantly due to overcapacity of commercial properties and the reluctance of state and local governments to borrow money to spend on capital projects when faced with stagnant or declining tax revenues and increased operating costs. The domestic auto industry is currently experiencingcontinues to experience a very difficult operating environment, which has resulted in and will likelymay continue to result in lower levels of vehicle production and an associated decrease in demand for products sold to the automotive industry. Many automotive manufacturers and their suppliers have reduced production levels and eliminated manufacturing capacity, through the closure of facilities, extension of temporary shutdowns, reduction in operations and other cost reduction actions. The construction industry has shown signs of stabilizing from further erosion, and the automotive industry has strengthened and shown signs of recovery from the lows reached in recent years. However, both the construction and automotive markets remain depressed compared to historical norms, and we cannot predict the strength, pace or sustainability of recovery in these markets. The difficulties faced by thesethe automotive and construction industries are likely tohave adversely affected and may continue to adversely affect our business. If demand for the products we sell to the automotive or construction markets were to be further reduced, this could negatively affect our sales, financial results and cash flows. Financial difficulties and bankruptcy filings by the Company’sour customers could have an adverse impact on our business. Many of our customers are experiencing extremelyhave experienced and continue to experience challenging financial conditions. General Motors and Chrysler have gone through bankruptcy proceedings and both companies have implemented plans towhich significantly reducereduced their production capacity and their dealership networks. Certain other customers have filed or are contemplating filingmay in the future file bankruptcy petitions. These and other customers may be in need of additional capital or credit to continue operations. The bankruptcies and financial difficulties of certain customers and/or failure in their effortsfailure to obtain credit or otherwise improve their overall financial condition could result in numerous changes within the markets we serve, including additional plant closings, decreased production, reduced demand, changes in product mix, unfavorable changes in the prices, terms or conditions we are able to obtain and other changes that may result in decreased purchases from us and otherwise negatively impact our business. These conditions also increase the risk that our customers may delay or default on their payment obligations to us, particularly customers in hard hit industries such as automotive and construction. The overallrelative weakness amongin the automotive manufacturers and their suppliers has increasedindustry continues the risk that at least some of the Company'sour customers whichwho are suppliers to the automotive industry could have further financial difficulties. The same is true of the Company'sour customers in other industries, including construction, which are also experiencing significant financial weakness. The automotive industry has shown signs of strengthening from the low levels of recent years, and the construction industry has shown signs of stabilizing. However, economic conditions remain fragile, and the possibility remains that these markets may not recover as quickly as anticipated, or could further deteriorate. Should the economy or any applicable marketof our markets not improve, the risk of bankruptcy filings by the Company'sour customers willmay continue to increase. Such bankruptcy filings may result in not only in a reduction in our sales, but also in a loss associated with theour potential inability to collectioncollect outstanding accounts receivables.receivable from the affected customers. While the Company takeswe have taken and will continue to take steps intended to mitigate the impact of financial difficulties and potential bankruptcy filings by itsour customers, these matters could have a negative impact on the Company'sour business. The loss of significant volume from key customersevents in Japan could adversely affect us. In fiscal 2009, our largest customer accounted for approximately 4%business and financial results. A number of our consolidated gross sales,customers, particularly in the automotive market, rely upon suppliers in Japan for certain components of their products. The earthquakes, tsunami and nuclear power plant problems in Japan prevented some companies from receiving sufficient supplies of components, and demand in some industries, such as automotive, has been adversely affected. Other risks resulting from this tragedy include potential disruptions to other industries which include our ten largest customers accounted for approximately 22% or suppliers, negative macroeconomic effects on international trade and/or our customers, and unforeseen challenges which could develop as the situation in Japan evolves and the full scope of our consolidated gross sales. A significant lossthe damage and its effects is comprehended. While there exists a risk that the effects of or decrease in, business from any of these customersthe disaster could continue to have an adverse effect on our sales and financial results ifus, we cannot obtain replacement business. Also, dueare unable at this time to consolidationreliably evaluate the scope or probability of those risks.