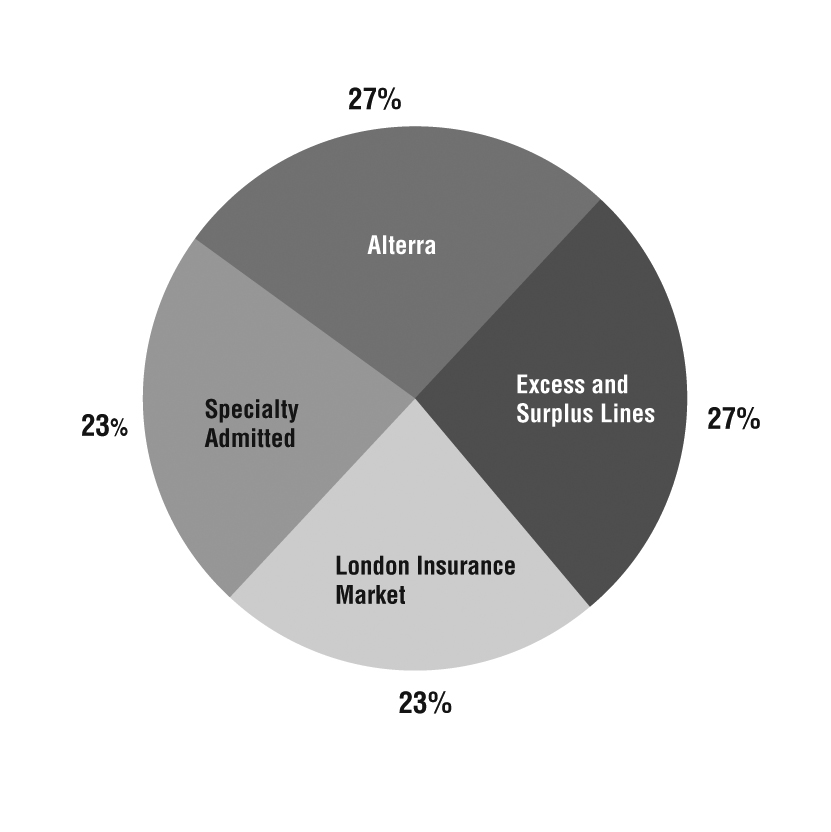

10, 2014 Item No. Part I 1. 1A. 1B. 2. 3. 4. 4A. Part II 5. 6. 7. 7A. 8. Financial Statements and Supplementary Data The response to this item is submitted in Item 15 and on page 83. 9. 9A. 9B. Part III 10. 11. 12. 13. 14. *Portions of Item 10 and Items 11, 12, 13 and 14 will be incorporated by reference from the Registrant’s 2011 Proxy Statement pursuant to instructions G(1) and G(3) of the General Instructions to Form 10-K. Part IV 15. Exhibits, Financial Statement Schedules a. Documents filed as part of this Form 10-K (1) Financial Statements Consolidated Statements of Changes in Equity for the Years Ended December 31, 2010, 2009 and 2008 Consolidated Statements of Cash Flows for the Years Ended December 31, 2010, 2009 and 2008 Notes to Consolidated Financial Statements for the Years Ended December 31, 2010, 2009 and 2008 (2) Schedules have been omitted since they either are not required or are not applicable, or the information called for is shown in the Consolidated Financial Statements and Notes thereto. (3) See Index to Exhibits for a list of Exhibits filed as part of this report b. See Index to Exhibits and Item 15a(3) c. See Index to Financial Statements and Item 15a(2) and Reinsurance form of treaty reinsurance contracts, which are contractual arrangements that provide for automatic reinsuring of a type or category of risk underwritten by cedents. Generally, we participate on reinsurance treaties with a number of other reinsurers, each with an allocated portion of the treaty, with the terms and conditions of the treaty being substantially the same for each participating reinsurer. With treaty reinsurance contracts, we do not separately evaluate each of the individual risks assumed under the contracts and are largely dependent on the individual underwriting decisions made by the cedent. Accordingly, we review and analyze the cedent's risk management and underwriting practices in deciding whether to provide treaty reinsurance and in pricing of treaty reinsurance contracts. Rio de Janeiro, Brazil, using Lloyd's admitted status, through Markel Europe using a representative office in Bogota, Colombia and a service company in Buenos Aires, Argentina, and through Markel Resseguradora do Brasil S.A. (Markel Brazil), a reinsurance company in Rio de Janeiro. Additionally, MIICL, Markel Syndicate 3000 and Lloyd's Syndicate 1400 are able to offer reinsurance in a number of other Latin American countries from their offices outside of Latin America. recent three years, we still consider the overall property and casualty insurance market to be soft. We routinely review the pricing of our major product lines and underwriting profitability.UNITED STATESSECURITIES AND EXCHANGE COMMISSIONWashington, D.C. 20549FORM 10-KAnnual report pursuant to Section 13 or 15(d) of theSecurities Exchange Act of 1934 for the fiscal year ended December 31, 20102013Commission File Number 001-15811MARKEL CORPORATION(Exact name of registrant as specified in its charter)A Virginia CorporationIRS Employer Identification No. 54-19592844521 Highwoods Parkway, Glen Allen, Virginia 23060-6148(Address of principal executive offices) (Zip code)Registrant’sRegistrant's telephone number, including area code: (804) 747-0136Securities registered pursuant to Section 12(b) of the Act:Common Stock, no par value7.50% Senior Debentures due 2046New York Stock Exchange, Inc.(title of each class and name of the exchange on which registered)Securities registered pursuant to Section 12(g) of the Act: NoneIndicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No xIndicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’sregistrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large"large accelerated filer,” “accelerated filer”" "accelerated filer" and “smaller"smaller reporting company”company" in Rule 12b-2 of the Exchange Act.Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No xThe aggregate market value of the shares of the registrant’sregistrant's Common Stock held by non-affiliates as of June 30, 20102013 was approximately $3,020,713,353.$7,085,000,000.The number of shares of the registrant’sregistrant's Common Stock outstanding at February 16, 2011: 9,718,932.Documents Incorporated By ReferenceThe portions of the registrant’sregistrant's Proxy Statement for the Annual Meeting of Shareholders scheduled to be held on May 9, 2011,12, 2014, referred to in Part III.Index and Cross References-Form 10-K Annual Report Page Business 12-33, 129-131 Risk Factors 30-33 Unresolved Staff Comments NONE Properties (note 5) 53 Legal Proceedings (note 14) 69 [Reserved] Executive Officers of the Registrant 132 Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities 83, 129-130 Selected Financial Data 34-35 Management’s Discussion and Analysis of Financial Condition and Results of Operations 88-128 Quantitative and Qualitative Disclosures About Market Risk 120-125 Changes in and Disagreements With Accountants on Accounting and Financial Disclosure NONE Controls and Procedures 85-87, 126 Other Information NONE Directors, Executive Officers and Corporate Governance* 132 Code of Conduct 131 Executive Compensation* Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters* Certain Relationships and Related Transactions, and Director Independence* Principal Accounting Fees and Services* 36 37 38 39 40-83 84-86 Item No. Page Part I 1. Business 2-25, 127-128 1A. Risk Factors 21-25 1B. Unresolved Staff Comments NONE 2. Properties (note 6) 49 3. Legal Proceedings (note 17) 68-69 4. Mine Safety Disclosures NONE Part II 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities 84, 127 6. Selected Financial Data 26-27 7. Management's Discussion and Analysis of Financial Condition and Results of Operations 88-126 7A. Quantitative and Qualitative Disclosures About Market Risk 120-124 8. Financial Statements and Supplementary DataThe response to this item is submitted in Item 15 and on page 84. 9. Changes in and Disagreements With Accountants on Accounting and Financial Disclosure NONE 9A. Controls and Procedures 86-87, 124 9B. Other Information NONE Part III 10. Directors, Executive Officers and Corporate Governance* 129 Code of Conduct 128 11. Executive Compensation* 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters* 13. Certain Relationships and Related Transactions, and Director Independence* 14. Principal Accounting Fees and Services* *Portions of Item 10 and Items 11, 12, 13 and 14 will be incorporated by reference from the Registrant's 2014 Proxy Statement pursuant to instructions G(1) and G(3) of the General Instructions to Form 10-K. Part IV 15. Exhibits, Financial Statement Schedules a. Documents filed as part of this Form 10-K (1) Financial Statements Consolidated Balance Sheets 28 Consolidated Statements of Income and Comprehensive Income 29 Consolidated Statements of Changes in Equity 30 Consolidated Statements of Cash Flows 31 Notes to Consolidated Financial Statements 32-84 Reports of Independent Registered Public Accounting Firm 85-86 (2) Schedules have been omitted since they either are not required or are not applicable, or the information called for is shown in the Consolidated Financial Statements and Notes thereto. (3) See Index to Exhibits for a list of Exhibits filed as part of this report b. See Index to Exhibits and Item 15a(3) c. See Index to Financial Statements and Item 15a(2) Markel Corporation & SubsidiariesBUSINESS OVERVIEWWe are a diverse financial holding company serving a variety of niche markets. Our principal business markets and underwrites specialty insurance products and programs.products. We believe that our specialty product focus and niche market strategy enable us to develop expertise and specialized market knowledge. We seek to differentiate ourselves from competitors by our expertise, service, continuity and other value-based considerations. We compete in three segments of the specialty insurance marketplace: the Excess and Surplus Lines, the Specialty Admitted and the London markets. We also own interests in various industrial and service businesses that operate outside of the specialty insurance marketplace. Our financial goals are to earn consistent underwriting and operating profits and superior investment returns to build shareholder value.On May 1, 2013, we completed the acquisition of Alterra Capital Holdings Limited (Alterra), a Bermuda-headquartered global enterprise providing diversified specialty property and casualty insurance and reinsurance products to corporations, public entities and other property and casualty insurers. Total purchase consideration was $3.3 billion. The acquisition of Alterra creates additional size and scale, providing us with additional insurance and investment opportunities.Specialty InsuranceThe specialty insurance market differs significantly from the standard market. In the standard market, insurance rates and forms are highly regulated, products and coverages are largely uniform with relatively predictable exposures and companies tend to compete for customers on the basis of price. In contrast, the specialty market provides coverage for hard-to-place risks that generally do not fit the underwriting criteria of standard carriers. For example, United States insurance regulations generally require an Excess and Surplus Lines (E&S) account to be declined by admitted carriers before an E&S company may write the business. Hard-to-place risks written in the Specialty Admitted market cover insureds engaged in similar, but highly specialized activities who require a total insurance program not otherwise available from standard insurers or insurance products that are overlooked by large admitted carriers. Hard-to-place risks in the London market are generally distinguishable from standard risks due to the complexity or significant size of the risk.Competition in the specialty insurance market tends to focus less on price than in the standard insurance market and more on other value-based considerations, such as availability, service and expertise. While specialty market exposures may have higher perceived insurance risks than their standard market counterparts, we seek to manage these risks to achieve higher financial returns. To reach our financial and operational goals, we must have extensive knowledge and expertise in our chosen markets. Many of our accounts are considered on an individual basis where customized forms and tailored solutions are employed.By focusing on the distinctive risk characteristics of our insureds, we have been able to identify a variety of niche markets where we can add value with our specialty product offerings. Examples of niche insurance markets that we have targeted include wind and earthquake exposedearthquake-exposed commercial properties, liability coverage for highly specialized professionals, equine-related risks, workers’workers' compensation insurance for small businesses, yachts and other watercraft, motorcyclesclassic cars and marine, energy and environmental-related activities. Our market strategy in each of these areas of specialization is tailored to the unique nature of the loss exposure, coverage and services required by insureds. In each of our niche markets, we assign teams of experienced underwriters and claims specialists who provide a full range of insurance services.MarketsThe E&S market focuses on hard-to-place risks and loss exposures that generally cannot be writtenWe also participate in the standard market. E&S eligibility allowsreinsurance market in certain classes of reinsurance product offerings, which were expanded in 2013 through the acquisition of Alterra. In the reinsurance market, our clients are other insurance subsidiaries to underwrite unique loss exposures with more flexible policy forms and unregulated premium rates. Thiscompanies, or cedents. We typically results in coverages that are more restrictive and more expensive than coverageswrite our reinsurance products in the standard market.12 |Our reinsurance products are written on both a quota share and excess of loss basis. Quota share contracts require us to share the losses and expenses in an agreed proportion with the cedent. Excess of loss contracts require us to indemnify the cedent against all or a specified portion of losses and expenses in excess of a specified dollar or percentage amount. In both types of contracts, we may provide a ceding commission to the cedent.We distinguish ourselves in the reinsurance market by the expertise of our underwriting teams, our access to global reinsurance markets, our ability to offer large lines and our ability to customize reinsurance solutions to fit our client's needs. Our specialty reinsurance product offerings include coverage for property, professional liability, automobile, general casualty and credit and surety risks.2MarketsIn 2009,the United States, we write business in the excess and surplus lines (E&S) and specialty admitted insurance and reinsurance markets. In 2012, the E&S market represented approximately $33$35 billion, or 7%, of the approximately $475$523 billion United States property and casualty (P&C) industry.(1) We areIn 2012, our legacy Markel operations were the sixtheighth largest E&S writer in the United States as measured by direct premium writings.writings and Alterra's legacy operations were the twenty-ninth.(1) In 2010, we wrote $898 millionOur E&S insurance operations are conducted through Essex Insurance Company (Essex), domiciled in Delaware, and Evanston Insurance Company (Evanston), domiciled in Illinois. The majority of business in our Excess and Surplus Lines segment.We also write business in the Specialty Admitted market. Most of these risks, although unique and hard-to-place in the standard market, must remain with anspecialty admitted insurance company for marketingoperations are conducted through Markel Insurance Company (MIC), domiciled in Illinois; Markel American Insurance Company (MAIC), domiciled in Virginia; FirstComp Insurance Company (FCIC), domiciled in Nebraska; and regulatory reasons. The Specialty Admitted market is subject to more state regulation than the E&S market, particularly with regard to rate and form filing requirements, restrictions on the ability to exit lines of business, premium tax payments and membershipEssentia Insurance Company (Essentia), domiciled in various state associations, such as state guaranty funds and assigned risk plans. In late 2010, we acquired Aspen Holdings, Inc. and began writing workers’ compensation insurance within the Specialty Admitted market. In 2010, we wrote $375 million of business in our Specialty Admitted segment.The London market, which produced approximately $50 billion of gross written premium in 2009, is the largest insurance market in Europe and third largest in the world.(2) The London market is known for its ability to provide innovative, tailored coverage and capacity for unique and hard-to-place risks. It is primarilyMissouri.As a broker market, which means that insurance brokers bring mostresult of the business to the market. The London market is also largelyacquisition of Alterra, we have expanded our United States insurance and reinsurance operations, effective May 1, 2013. Our E&S insurance operations include Alterra Excess & Surplus Insurance Company (AESIC) and our specialty admitted operations include Alterra America Insurance Company (AAIC), both domiciled in Delaware. Our United States reinsurance operations are conducted through Alterra Reinsurance USA Inc. (Alterra Re USA), a subscription market, which means that loss exposures brought into the market are typically insured by more than one insurance company or Lloyd’s syndicate, often due to the high limits of insurance coverage required. We write business on both a direct and subscription basisConnecticut-domiciled reinsurance company.In Europe, we participate in the London market. When we write business in the subscription market, we prefer to participate as lead underwriter in order to control underwriting terms, policy conditions and claims handling.In 2009, gross premium written through Lloyd’s syndicates generated approximately two-thirds of the London market’s international insurance business(2), making Lloyd’s the world’s second largest commercial surplus lines insurer(1) and fifth largest reinsurer.(3) Corporate capital providers often provide a majority of a syndicate’s capacity and also often own or control the syndicate’s managing agent. This structure permits the capital provider to exert greater influence on, and demand greater accountability for, underwriting results. In 2009, corporate capital providers accounted for approximately 95% of total underwriting capacity in Lloyd’s.(4)We participate in the London market through Markel International, which includes Markel Capital Limited (Markel Capital) and Markel International Insurance Company Limited (MIICL). Markel Capital is the corporate capital provider for our syndicate at Lloyd’s, Markel Syndicate 3000, through which our Lloyd's of London (Lloyd's) operations are conducted. Markel Syndicate 3000 is managed by Markel Syndicate Management Limited.Limited (MSM). As a result of the acquisition of Alterra, our Lloyd's operations also include Alterra Corporate Capital 2 Limited and Alterra Corporate Capital 3 Limited, corporate capital providers to Lloyd's Syndicate 1400. Since October 1, 2013, MSM has also managed Lloyd's Syndicate 1400. Markel International is headquartered in London, England. In 2010,addition to regional offices in the United Kingdom, Markel International has offices in Canada, Spain, Germany, Sweden, Switzerland, the Netherlands, Hong Kong, China, Malaysia and Singapore. The London insurance market, which produced approximately $69 billion of gross written premium in 2012,(2) is the largest insurance market in Europe and third largest in the world.(3) In 2012, gross premium written through Lloyd's syndicates generated approximately half of the London market's international insurance business,(2) making Lloyd's the world's largest commercial surplus lines insurer(1) and fourth largest reinsurer.(4) Corporate capital providers often provide a majority of a syndicate's capacity and also generally own or control the syndicate's managing agent. This structure permits the capital provider to exert greater influence on, and demand greater accountability for, underwriting results. In 2012, corporate capital providers accounted for approximately 89% of total underwriting capacity in Lloyd's.(5) Our other European operations acquired through Alterra are conducted through Markel Europe plc (Markel Europe), which is headquartered in Dublin, Ireland. Markel Europe also operates branches in London, England and Zurich, Switzerland.We also added insurance and reinsurance operations in Bermuda and Latin America through the acquisition of Alterra. In Bermuda, we wrote $709 millionconduct our insurance and reinsurance operations through Markel Bermuda Limited (Markel Bermuda), which is registered as a Class 4 insurer and a Class C long term insurer under the insurance laws of businessBermuda. In Latin America, we provide reinsurance through MSM in our London Insurance Market segment.(1) U.S. Surplus Lines Segment Review Special Report, A.M. Best (September 23, 2013).(2) London Company Market Statistics Report, International Underwriting Association (October 2013).(3) UK Insurance Key Facts, Association of British Insurers (September 2013).(4) Global Reinsurance Segment Review Special Report, A.M. Best (August 26, 2013).(5) Lloyd's Annual Report 2012.3In 2010, 28%2013, 25% of consolidated gross premium writings related to foreign risks (i.e., coverage for risks located outside of the United States), of which 25% were from the United Kingdom and 17%13% were from Canada. In 2009, 26%2012, 30% of our premium writings related to foreign risks, of which 28%20% were from the United Kingdom.Kingdom and 16% were from Canada. In 2008, 23%2011, 31% of our premium writings related to foreign risks, of which 32%20% were from the United Kingdom.Kingdom and 18% were from Canada. In each of these years, there were no other individual foreign countries from which premium writings were material. Premium writings are attributed to individual countries based upon location of risk.(1)U.S. Surplus Lines – 2010 Market Review Special Report,A.M. Best Research(September 2010).(2)Insurance 2010, TheCityUK(December 2010).(3)Top Ten Global Reinsurers by Net Reinsurance Premiums Written 2009, Business Insurance(September 2010).(4)Lloyd’s Highlights, Lloyd’s(April 2010).| 13Most of our business is placed through insurance and reinsurance brokers. Some of our insurance business is also placed through managing general agents. We seek to develop and capitalize on relationships with insurance and reinsurance brokers, insurance and reinsurance companies, large global corporations and financial intermediaries to develop and underwrite business. As a result of the acquisition of Alterra, a significant volume of premium for the property and casualty insurance and reinsurance industry is produced through a small number of large insurance and reinsurance brokers. During the year ended December 31, 2013, the top three independent brokers accounted for approximately 19% of our gross premiums written.CompetitionMarkel Corporation & SubsidiariesBUSINESS OVERVIEW (continued)CompetitionWe compete with numerous domestic and international insurance companies and reinsurers, Lloyd’sLloyd's syndicates, risk retention groups, insurance buying groups, risk securitization programs and alternative self-insurance mechanisms. Competition may take the form of lower prices, broader coverages, greater product flexibility, higher quality services or higher ratings by independent rating agencies. In all of our markets, we compete by developing specialty products to satisfy well-defined market needs and by maintaining relationships with agents, brokers and insureds who rely on our expertise. This expertise is our principal means of competing. We offer over 100 product lines. Eacha diverse portfolio of these products, haseach with its own distinct competitive environment.environment, which enables us to be responsive to changes in market conditions for individual product lines. With each of our products, we seek to compete with innovative ideas, appropriate pricing, expense control and quality service to policyholders, agents and brokers.Few barriers exist to prevent insurers and reinsurers from entering our segmentsmarkets of the P&Cproperty and casualty industry. Market conditions and capital capacity influence the degree of competition at any point in time. Periods of intense competition, which typically include broader coverage terms, lower prices and excess underwriting capacity, are referred to as a “soft"soft market.”" A favorable insurance market is commonly referred to as a “hard market”"hard market" and is characterized by stricter coverage terms, higher prices and lower underwriting capacity. During soft markets, unfavorable conditions exist due in part to what many perceive to beas excessive amounts of capital in the industry. In an attempt to use their capital, many insurance companies seek to write additional premiums without appropriate regard for ultimate profitability, and standard insurance companies are more willing to write specialty coverages. The opposite is typically true during hard markets.The Insurance Market CycleAfter a decade Historically, the performance of softthe property and casualty reinsurance and insurance industries has tended to fluctuate in cyclical periods of price competition and excess underwriting capacity, followed by periods of high premium rates and shortages of underwriting capacity. This cyclical market conditions,pattern can be more pronounced in the specialty insurance industryand reinsurance markets in which we compete than the standard insurance market.We have experienced favorable conditions beginning in late 2000, which continued through 2003 for most product lines. During 2004, the market began to soften and the industry began to show signs of increased competition. Since 2005, we have been in a soft insurance market and have experienced intense competition. During the current soft market cycle, we have experiencedconditions including price deterioration in virtually all of our product areas duelines since the mid-2000s. During 2011, unfavorable pricing trends continued for some of our product lines; however, price declines stabilized for most of our product lines, and we achieved moderate price increases in partseveral lines. During 2012 and 2013, we have generally seen low to an increased presence of standard insurance companiesmid-single digit favorable rate changes in our markets. During 2008, given the rapid deterioration in underwriting capacity as a result of the disruptions in the financial markets and losses from catastrophes, the rate of decline in prices began to slow. However, the effects of the economic environment contributed to further declines in gross premium volume in 2009 and 2010. Premiums for many of our product lines are based upon our insureds’as market conditions improved and revenues, gross receipts or payroll, which have been negativelyand payrolls of our insureds were favorably impacted by improving economic conditions; however, during the depressed levelsfourth quarter of business activity in recent years. In 2010,2013, we continuedbegan to experience pricing pressure due in part to intense competition, which resulted in further price deterioration across many ofsoftening prices on our catastrophe exposed property product lines most notablyand in our professional and products liability programs within the Excess and Surplus Lines segment. However, we experienced moderate price increases in severalreinsurance book. Despite stabilization of prices on certain product lines during 2010,the most notably those offered by Markel International.have pursuedwill continue to pursue price increases for most product lines in many product areas; however, as a result of continued soft insurance market conditions, our targeted price increases have been met with resistance in the marketplace, particularly within the Excess and Surplus Lines segment. In general, we believe prevailing rates within the property and casualty insurance marketplace are lower than our targeted pricing levels. When2014, when possible. However, when we believe the prevailing market price will not support our underwriting profit targets, the business is not written. As a result of our underwriting discipline, gross premium volume for many ofmay vary when we alter our product lines, most notably within the Excess and Surplus Lines segment, has declined and, if the competitive environment does notofferings to maintain or improve could decline further in the future.14 |4

To facilitate this strategy, we have a product line leadership group that has primary responsibility for both developing and maintaining underwriting and pricing guidelines on our existing products and new product development. The product line leadership group is under the direction of our Chief Underwriting Officer.

is comprised of all of the active property and casualty underwriting operations of the former Alterra companies.

| 15

Alterra previously offered life and annuity reinsurance products. In 2010, Alterra ceased writing life and annuity reinsurance contracts and placed this business into run-off. Results attributable to the run-off of life and annuity reinsurance business are included in our Other Insurance (Discontinued Lines) segment.

BUSINESS OVERVIEW (continued)

2010 CONSOLIDATED GROSS PREMIUM VOLUME ($2.0 billion) Consolidated Gross Premium Volume (

$3.9 billion)

Our Excess

the standard market.

TheEvanston.

Markel Northeast (Red Bank, NJ)

Markel Southeast (Glen Allen, VA)

Markel Midwest (Deerfield, IL)

Markel Mid South (Plano, TX)

Markel West (Woodland Hills, CA and Scottsdale, AZ)

We also have a product line leadership group that has primary responsibility both for developing and maintaining underwriting and pricing guidelines on our existing products and for new product development. The product line leadership group also delegates underwriting authority to the regional underwriters to ensure that the products needed by our customers are available through the regional offices and provides underwriting training and development so that our regional underwriting teams have the expertise to underwrite the risk or to refer risks to our product line experts as needed. The product line leadership group is under the direction of our Chief Underwriting Officer, who also is ultimately responsible for the underwriting activities of our Specialty Admitted and London Insurance Market segments.

16 |

Product offerings within the Excess and Surplus Lines segment include:

Property and Casualty

Professional Liability

Excess and Umbrella

Environmental

Transportation

Inland Marine

Ocean Marine

Miscellaneous Coverages

These product offerings are generally available in all of the regional offices included in the Excess and Surplus Lines segment.

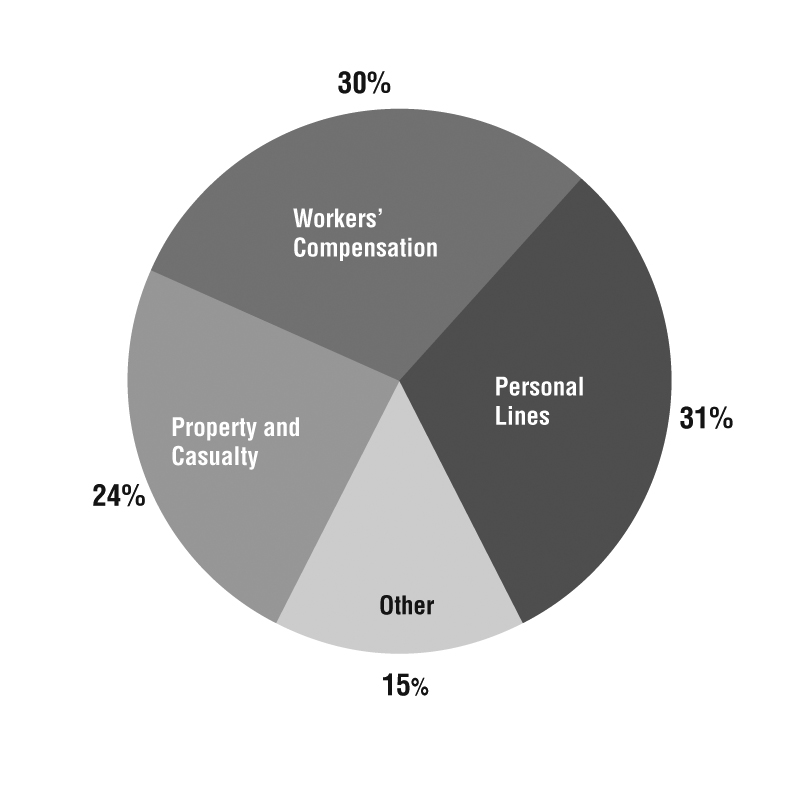

EXCESSAND SURPLUS LINES SEGMENT

2010 GROSS PREMIUM VOLUME ($898MILLION)

Our property and casualty product offerings include a variety of liability coverages focusing on light-to-medium casualty exposures such as restaurants and bars, child and adult care facilities, vacant properties, builder’s risk, general or artisan contractors and office buildings. In addition, we offer third party protection on either an occurrence or claims-made basis to manufacturers, distributors, importers and re-packagers of manufactured products. We also provide property coverages for similar classes of business ranging from small, single-location accounts to large, multi-state, multi-location accounts. Property coverages consist principally of fire, allied lines (including windstorm, hail and water damage) and other specialized property coverages, including catastrophe-exposed property risks such as earthquake and wind on both a primary and excess basis. Catastrophe-exposed property risks are typically larger and are lower frequency and higher severity in nature than more standard property risks.

| 17

Markel Corporation & Subsidiaries

BUSINESS OVERVIEW (continued)

Our professional liabilityproperty risks range from small, single-location accounts to large, multi-state, multi-location accounts. Casualty product offerings include a variety of primary liability coverages targeting apartments and office buildings, retail stores, contractors and recreational and hospitality businesses. We also offer products liability coverages on either an occurrence or claims-made basis to manufacturers, distributors, importers and re-packagers of manufactured products.

We offer

Our environmental product offerings target small to mid-sized environmental contractors and provide a complete array of environmental coverages, including environmental consultants’consultants' professional liability, contractors’contractors' pollution liability and site specific environmental impairment liability. The professional liability cover is offered on a claims-made basis and targets risks inherent in the businesses of environmental consultants and engineers. The contractors’ pollution liability cover is offered on either a claims-made or occurrence basis and protects environmental contractors, trade contractors and general contractors. Thesite-specific environmental impairment liability cover is offered on a claims-made basis and protects commercial, industrial, environmental, habitational and institutional facilities against pollution to their premises.

Our transportation product offerings includecoverages;

Our industry;

18 |

Our builder's risk coverage;

Miscellaneous coverages offered include cargo;

In the Specialty Admitted market, we wrote business through the following underwriting units during 2010:

Markel Specialty (Glen Allen, VA)

Markel American Specialty Personal and Commercial Lines (Pewaukee, WI)

FirstComp (Omaha, NE)

SPECIALTY ADMITTED SEGMENT

2010 GROSS PREMIUM VOLUME ($375MILLION)

| 19

Markel Corporation & Subsidiaries

BUSINESS OVERVIEW (continued)

Markel Specialty.The Markel Specialty unit focuses on providing total insurance programs for businesses engaged in highly specialized activities. These activities typically do not fit the risk profiles of standard insurers and make complete coverage difficult to obtain from a single insurer.

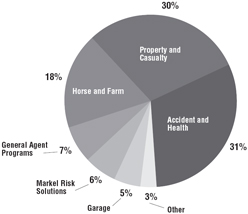

The Markel Specialty unitsegment is organized into product areas that concentrate on particular markets and customer groups. The property and casualty division writes commercial coverages for youth and recreation oriented organizations, such as children’s camps, conference centers, YMCAs, YWCAs, Boys and Girls Clubs, child care centers, nursery schools, private and Montessori schools and gymnastics, martial arts and dance schools. This division also writes commercial coverages for social service organizations, museums and historic homes, performing arts organizations, bed and breakfast inns, outfitters and guides, hunting and fishing lodges, dude ranches and rod and gun clubs. The horse and farm operations specialize in insurance coverages for equine-related risks, such as horse mortality, theft, infertility, transit and specified perils. We also provide property and liability coverages for farms and boarding, breeding and training facilities. The accident and health division writes liability and accident insurance for amateur sports organizations, accident and medical insurance for colleges, universities, public schools and private schools, monoline accident and medical coverage for various niche markets, short-term medical insurance, pet health insurance, stop-loss insurance for self-insured medical plans and medical excess reinsurance coverage. The garage division provides commercial coverages for auto repair garages, gas stations and convenience stores and used car dealers. The general agent programs division develops partnerships with managing general agents to offer single source admitted and non-admitted programs for a specific class or line of business. We seek general agents who utilize retailers as their primary source of distribution. Underwriting, policy issuance and business development authority are delegated to the managing general agent. The Markel Risk Solutions facility works with select retail producers on a national basis to provide admitted market solutions to accounts having difficulty finding coverage in the standard marketplace. Accounts of various classes and sizes are written with emphasis placed on individual risk underwriting and pricing.

The majority of Markel Specialty business is produced by retail insurance agents. Management grantsagents who have very limited underwriting authority to a fewauthority. Agents are carefully selected agents and controls agency business is controlled through regular audits and pre-approvals.pre- approvals. Certain products and programs are also marketed directly to consumers or distributed through wholesale producers. Markel Specialty business is primarily written on Markel Insurance Company (MIC). MIC is domiciledPersonal lines coverages included in Illinois and is licensed to write P&C insurance in all 50 states and the District of Columbia.

MARKEL SPECIALTY

2010 GROSS PREMIUM VOLUME ($230MILLION)

20 |

Markel American Specialty Personal and Commercial Lines.The Markel American Specialty Personal and Commercial Lines unit offers its insurance products in niche markets and focuses its underwriting on marine, recreational vehicle, property and other personal and commercial line coverages. The marine division markets personal lines insurance coverage for watercraft, older boats, high performance boats and yachts. The marine division also provides coverage for small fishing ventures, charters, utility boats and boat rentals. The recreational vehicle division provides coverage for motorcycles, snowmobiles and ATVs. The property division provides coverage for mobile homes, dwellings and homeowners that do not qualify for standard homeowners coverage, as well as contents coverage for renters. Mobile home coverages include primary, seasonal and rental mobile homes. Coverage is offered for motor homes, as well as motor home rental operations. Commercial coverages include specialty insurance products, most notably professional liability coverages that we design and administer on behalf of other insurance carriers and ultimately assume on a reinsurance basis. Other products offered by this unit include special event protection, which provides for cancellation and/or liability coverage for weddings, anniversary celebrations and other personal events; supplemental natural disaster coverage, which offers additional living expense protection for loss due to specific named perils including flood; renters’ protection coverage, which provides tenant homeowner’s coverage on a broader form than the standard renter’s policy; excess flood coverage, which provides coverage above the National Flood Insurance Program limits; and collector vehicle coverage, which provides comprehensive coverage for a variety of collector vehicles including antique autos and motorcycles.

Markel American Specialty Personal and Commercial Lines products are characterized by high numbers of transactions, low average premiums and creative solutions for under-served and emerging markets. The unit distributes its marine, property and other products through wholesale or specialty retail producers. The recreational vehicle program and some marine productssegment are marketed directly to the consumer using direct mail, internet and telephone promotions, as well as relationships with various motorcycle and boat manufacturers, dealers and associations.

MARKEL AMERICAN SPECIALTY PERSONALAND COMMERCIAL LINES

2010 GROSS PREMIUM VOLUME ($104MILLION)

| 21

Markel Corporation & Subsidiaries

BUSINESS OVERVIEW (continued)

FirstComp.On October 15, 2010, we completed our acquisition of Aspen Holdings, Inc., a Nebraska-based privately held corporation whose FirstComp MAIC is also licensed to write property and casualty insurance group provides workers’in Puerto Rico. Essentia is also licensed in the U.S. Virgin Islands and specializes in coverage for classic cars and boats. FCIC is currently licensed in 28 states and specializes in workers' compensation insurance and related services, principally to small businesses, in 31 states. The majority of FirstComp business is produced by retail insurance agents. FirstComp business produced for our benefit is written on FirstComp Insurance Company, which is domiciled in Nebraska, or MIC. FirstComp also produces business for unaffiliated insurance companies through FirstComp Underwriters Group, Inc. and FirstComp Insurance Agency, Inc., which act as managing general agents. FirstComp has distribution relationships with more than 8,000 independent insurance agencies. These agencies are generally located in small towns and have been underserved by other market participants because of their size. For expense efficiency reasons, carriers often will not do business with agencies that do not have large books of business. Utilizing its proprietary technology platform, FirstComp is able to service these small agencies in a cost-efficient manner.

The FirstComp operations collectively produced approximately $290 million of gross written premiums in 2010. During 2010, thecoverage.

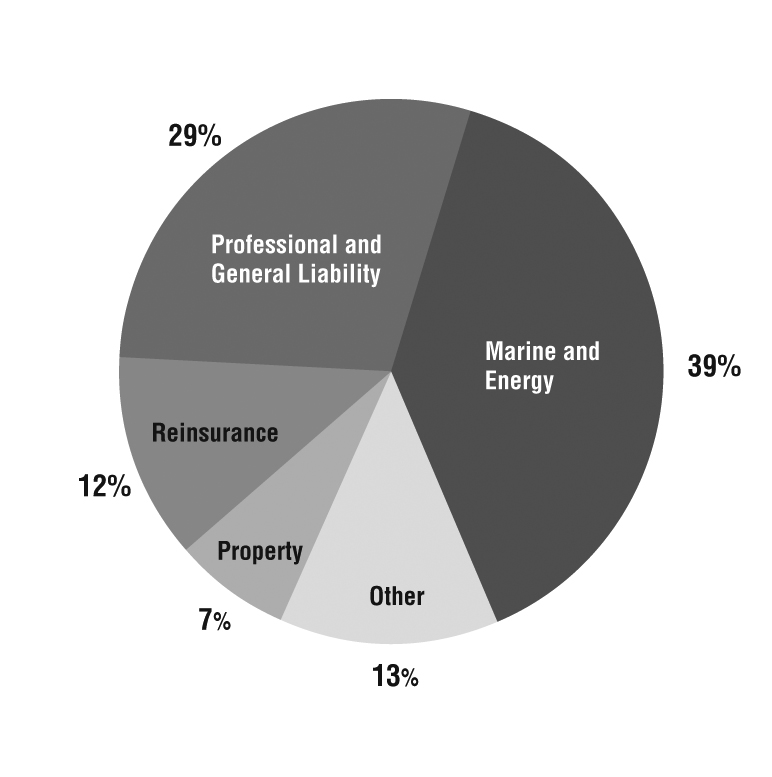

London Insurance Market Segment

Our London Insurance Market segment reported gross premium volume of $709.0

2010 GROSS PREMIUM VOLUME ($709MILLION.

This

22 |

Markel International.Markel International is comprised of the following underwriting divisions which, to better serve the needs of our customers, have the ability to write business through either MIICL or Markel Syndicate 3000:3000.

Non-Marine Property

Professional and Financial Risks

Retail

Specialty

Equine

Trade Credit

Elliott Special Risks (ESR)

The

The Non-Marine Property division writes

The Professional and Financial Risks division underwrites professional indemnity, directors’ and officers’ liability, intellectualWe also provide property some miscellaneous defense costs, incidental commercial crime and general liability coverages. The professional indemnity account offers unique solutions in four main professional classes including miscellaneous professionals and consultants, construction professionals, financial service professionals and professional practices. The miscellaneous professionals and consultants class includes coverages for a wide range of professionals including management consultants, publishers, broadcasters, pension trustees and public officials. The construction class includes coverages for surveyors, engineers, architects and estate agents. The financial services class includes coverages for insurance brokers, insurance agents, financial consultants, stockbrokers, fund managers, venture capitalists and bankers. The professional practices class includes coverages for accountants and solicitors. The directors’ and officers’ liability account offers coverage to public, private and non-profit companies of all sizes on either an individual or blanket basis. The Professional and Financial Risks division writes business on a worldwide basis, limiting exposure in the United States.

The Retail division offers a full range of professional liability products, including professional indemnity, directors’ and officers’ liability and employment practices liability, through six branch offices in England and one branch office in Scotland. In addition, coverage is provided for small to

| 23

Markel Corporation & Subsidiaries

BUSINESS OVERVIEW (continued)

medium-sized commercial property risks on both a stand-alone and package basis. Thebasis through our branch offices provide insureds and brokers with direct access to decision-making underwriters who possess specialized knowledge of their local markets. The division also underwrites certain niche liability products such as coverages for social welfare organizations.

The Specialty division provides property treaty reinsurance on an excess of loss and proportional basis for per risk and catastrophe exposures. A significant portion ofoffices.

The Equine division writes bloodstock, livestockindemnity;

The Trade Credit division writes parks;

ESR underwrites a diverse portfolio of property and casualty coverages for Canadian domiciled insureds. ESR provides primary general liability,

excess product recall insurance. These products are underwritten on an individual risk basis.

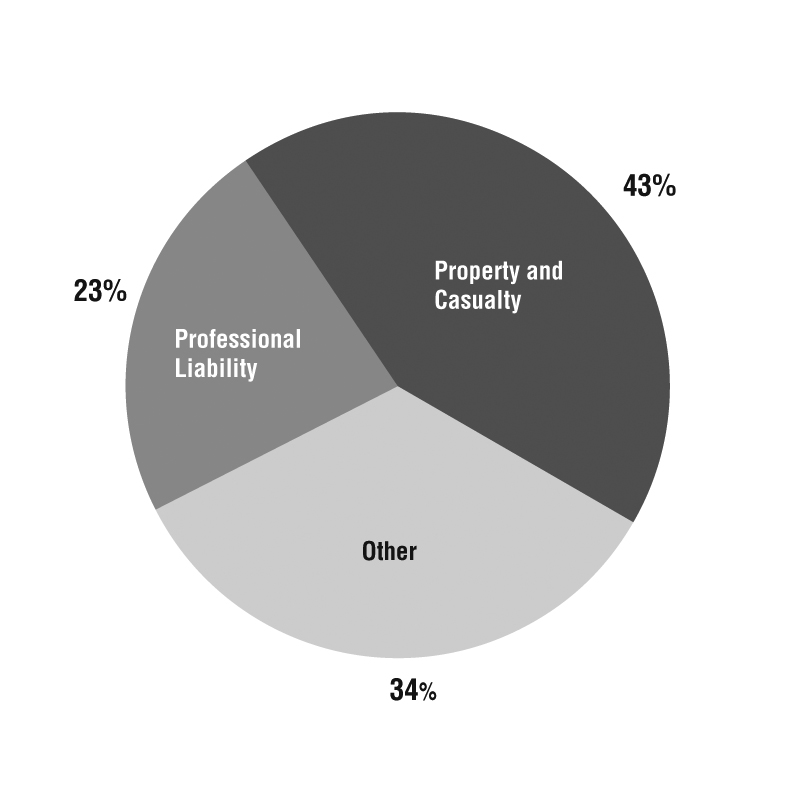

unit offers property and casualty quota share and excess of loss reinsurance through Alterra Re USA, Alterra at Lloyd's, Markel Europe, Markel Bermuda and Markel Brazil to insurance and reinsurance companies worldwide. Alterra Re USA is licensed or accredited to provide reinsurance in all 50 states and the District of Columbia. We typically write our reinsurance products in the Alterra segment in the form of treaty reinsurance contracts, on both a quota share and excess of loss basis. Our reinsurance products may include features such as contractual provisions that require our cedent to share in a portion of losses resulting from ceded risks, may require payment of additional premium amounts if we incur greater losses than those projected at the time of the execution of the contract, may require reinstatement premium to restore the coverage after there has been a loss occurrence or may provide for experience refunds if the losses we incur are less than those projected at the time the contract is executed. Reinsurance products offered include agriculture, auto, credit and surety, general casualty, marine and energy, professional liability, property and workers' compensation.

The ceding of insurance does

24 |

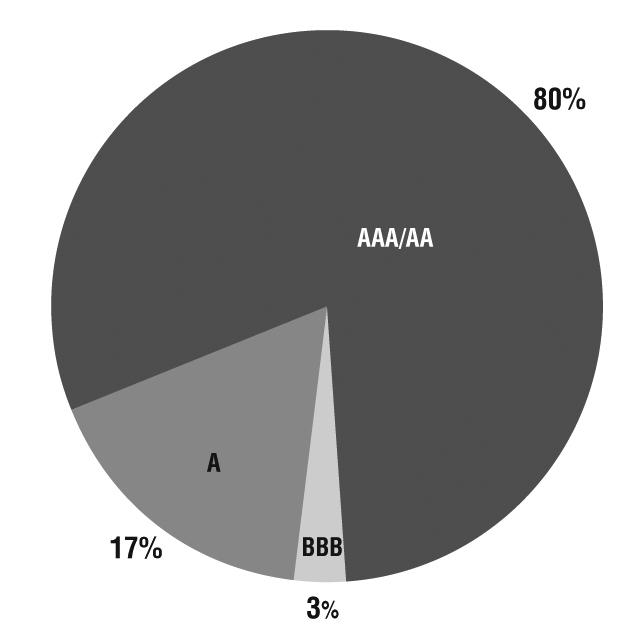

Standard & Poor’sPoor's (S&P) rating of “A”"A" (excellent) or better; (ii) maintain minimum capital and surplus of $500 million and (iii) provide collateral for recoverables in excess of an individually established amount. In addition, certain foreign reinsurers for our United States insurance operations must provide collateral equal to 100% of recoverables, with the exception of reinsurers who have been granted authorized status by an insurance company’scompany's state of domicile. Lloyd’sLloyd's syndicates generally must have a minimum of a “B”"B" rating from Moody’sMoody's Investors Service (Moody’s)(Moody's) to be our reinsurers.

Over time, we will attempt to bring the reinsurance programs used within the Alterra segment into compliance with our internal ceded reinsurance guidelines.

Reinsurers | A.M. Best Rating | Reinsurance Recoverable | ||||

| (dollars in thousands) | ||||||

Munich Re Group | A+ | $ | 167,148 | |||

Lloyd’s of London | A | 131,960 | ||||

Fairfax Financial Group | A | 89,166 | ||||

XL Capital Group | A | 60,484 | ||||

Swiss Re Group | A | 55,292 | ||||

Ace Group | A+ | 51,577 | ||||

W.R. Berkley Group | A+ | 36,669 | ||||

HDI Group | A | 35,299 | ||||

Aspen (Bermuda) Group | A | 33,301 | ||||

White Mountains Insurance Group | A- | 31,607 | ||||

Reinsurance recoverable on paid and unpaid losses for ten largest reinsurers | 692,503 | |||||

Total reinsurance recoverable on paid and unpaid losses | $ | 1,023,848 | ||||

| Reinsurers | A.M. Best Rating | Reinsurance Recoverable | |||

(dollars in thousands) | |||||

| Fairfax Financial Group | A | $ | 212,591 | ||

| Munich Re Group | A+ | 186,457 | |||

| Lloyd's of London | A | 159,342 | |||

| AXIS Capital Holdings Limited | A | 143,949 | |||

| Alleghany Corporation | A | 117,729 | |||

| Platinum Underwriters Holdings Ltd | A | 106,397 | |||

| Partner Re Group | A+ | 105,627 | |||

| Swiss Re Group | A+ | 83,562 | |||

| XL Capital Group | A | 81,844 | |||

| Arch Insurance Group | A+ | 72,320 | |||

| Reinsurance recoverable on paid and unpaid losses for ten largest reinsurers | 1,269,818 | ||||

| Total reinsurance recoverable on paid and unpaid losses | $ | 2,032,626 | |||

| 25

Markel Corporation & Subsidiaries

BUSINESS OVERVIEW (continued)

Investments

Total

ANNUAL TAXABLE EQUIVALENT TOTAL INVESTMENT RETURNS

| Years Ended December 31, | Weighted Average Five-Year Annual Return | Weighted Average Ten-Year Annual Return | ||||||||||||||||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2010 | ||||||||||||||||||||||||

Equities | 25.9 | % | (0.4 | %) | (34.0 | %) | 25.7 | % | 20.8 | % | 6.2 | % | 7.6 | % | ||||||||||||||

Fixed maturities(1) | 5.2 | % | 5.6 | % | 0.2 | % | 9.8 | % | 5.4 | % | 5.3 | % | 5.5 | % | ||||||||||||||

Total portfolio, before foreign currency effect | 9.6 | % | 4.1 | % | (6.9 | %) | 11.7 | % | 8.1 | % | 5.3 | % | 5.7 | % | ||||||||||||||

Total portfolio | 11.2 | % | 4.8 | % | (9.6 | %) | 13.2 | % | 7.9 | % | 5.4 | % | 6.0 | % | ||||||||||||||

Invested assets, end of year (in millions) | $ | 7,524 | $ | 7,775 | $ | 6,893 | $ | 7,849 | $ | 8,224 | ||||||||||||||||||

|

Equivalent Total Investment Returns

Weighted Average Five-Year Annual Return | Weighted Average Ten-Year Annual Return | ||||||||||||||||||||||||

| Years Ended December 31, | |||||||||||||||||||||||||

| 2013 | 2012 | 2011 | 2010 | 2009 | |||||||||||||||||||||

| Equities | 33.3 | % | 19.6 | % | 3.8 | % | 20.8 | % | 25.7 | % | 21.6 | % | 12.4 | % | |||||||||||

| Fixed maturities | 0.0 | % | 5.1 | % | 7.6 | % | 5.4 | % | 9.8 | % | 4.9 | % | 4.4 | % | |||||||||||

| Total portfolio, before foreign currency effect | 6.9 | % | 8.6 | % | 6.7 | % | 8.1 | % | 11.7 | % | 8.2 | % | 6.0 | % | |||||||||||

| Total portfolio | 6.8 | % | 9.0 | % | 6.5 | % | 7.9 | % | 13.2 | % | 8.4 | % | 6.0 | % | |||||||||||

| Invested assets, end of year (in millions) | $ | 17,612 | $ | 9,333 | $ | 8,728 | $ | 8,224 | $ | 7,849 | |||||||||||||||

26 |

is regarded by S&P as having predominantly speculative characteristics with respect to capacity to pay interest and repay principal. Moody’sMoody's ratings range from “Aaa”"Aaa" to “C”"C" with ratings of “Baa”"Baa" or higher considered investment grade.

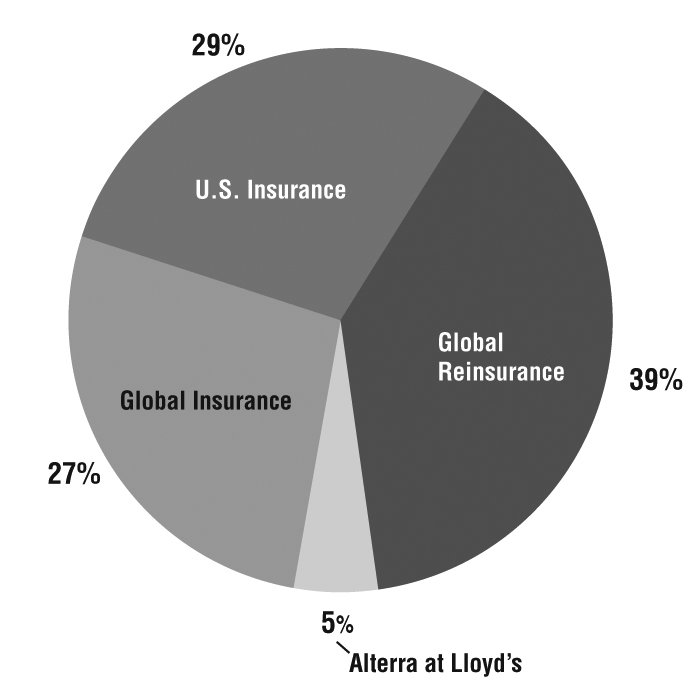

2013

Non-Insurance Operations (Markel Ventures)

| 27

Markel Corporation & Subsidiaries

BUSINESS OVERVIEW (continued)

In December 2010, we acquired controlling interests in RD Holdings, LLC (RetailData), a company that provides retail intelligence services,

Markel Ventures operations.

28 |

years as of December 31.

The jurisdictions of our principal insurance subsidiaries are the United States, the United Kingdom and Bermuda.

As an

Additional requirements include group-level reporting, submission of an annual enterprise risk report by a regulated insurance company's ultimate controlling person and information regarding an insurer's non-insurer's affiliates.

| 29

MIICL must also provide 14 days advance written notice to the PRA of any transaction or proposed transaction with a connected or related person.

BUSINESS OVERVIEW (continued)

Bermuda is regulated by the BMA under the Insurance Act 1978 of Bermuda and its related regulations (Bermuda Insurance Act). The Bermuda Insurance Act imposes solvency and liquidity standards and auditing and reporting requirements on Markel Bermuda and grants to the BMA powers to supervise, investigate and intervene in the affairs of Bermuda insurance and reinsurance companies.

Six

In addition to Best, seven

Our Lloyd's syndicates are part of a group rating for the Lloyd's overall market, which has been assigned an FSR of "A+" (strong) by Fitch.

30 |

changes in operations,

emerging economic and social trends,

uncertainties relating to asbestos and environmental exposures,

inflation or deflation, and

changes in the regulatory and litigation environments.

earnings, which may be material.

| 31

Markel Corporation & Subsidiaries

BUSINESS OVERVIEW (continued)

32 |

| 33

Markel Corporation & Subsidiaries

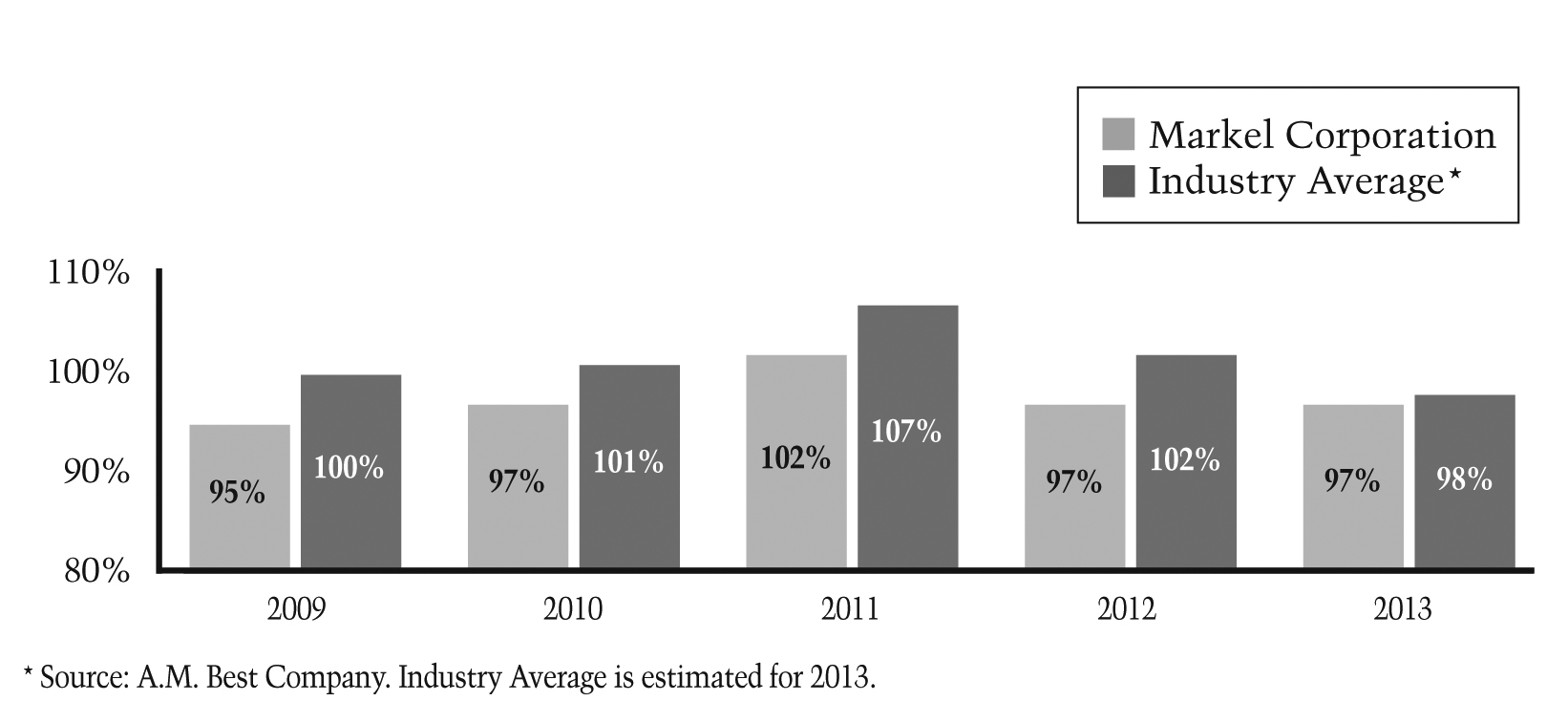

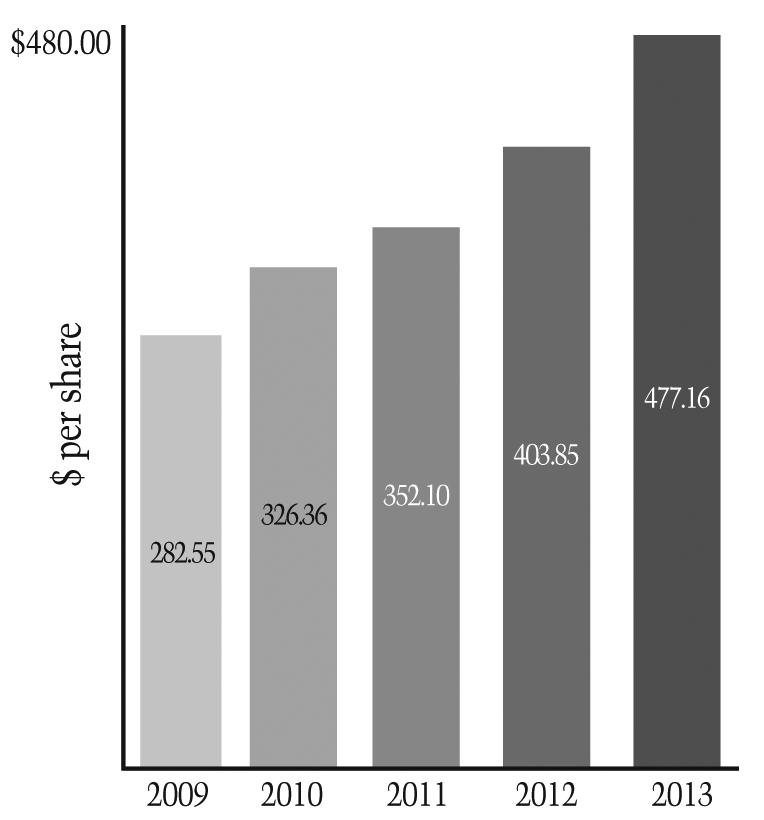

RESULTSOF OPERATIONS Earned premiums Net investment income Total operating revenues Net income (loss) to shareholders Comprehensive income (loss) to shareholders Diluted net income (loss) per share FINANCIAL POSITION Total investments and cash and cash equivalents Total assets Unpaid losses and loss adjustment expenses Convertible notes payable Senior long-term debt and other debt 8.71% Junior Subordinated Debentures Shareholders’ equity Common shares outstanding (at year end, in thousands) OPERATING DATA Book value per common share outstanding Growth (decline) in book value per share 5-Year CAGR in book value per share(2) Closing stock price RATIO ANALYSIS U.S. GAAP combined ratio(3) Investment yield(4) Taxable equivalent total investment return(5) Investment leverage(6) Debt to total capital Reflects the acquisition of Alterra Capital Holdings Limited effective May 1, 2013, which included the issuance of equity totaling $2.3 billion. CAGR—compound annual growth rate. The U.S. GAAP combined ratio measures the relationship of incurred losses, loss adjustment expenses and underwriting, acquisition and insurance expenses to earned premiums. Investment yield reflects net investment income as a percentage of monthly average invested Investment leverage represents total invested assets divided by SELECTED FINANCIAL DATA(dollars in millions, except per share data) 2010 2009 2008 $ 1,731 $ 1,816 $ 2,022 273 260 282 2,225 2,069 1,977 267 202 (59 ) 431 591 (403 ) $ 27.27 $ 20.52 $ (5.95 ) $ 8,224 $ 7,849 $ 6,893 10,826 10,242 9,512 5,398 5,427 5,492 — — — 1,016 964 694 — — — 3,172 2,774 2,181 9,718 9,819 9,814 OPERATING PERFORMANCE MEASURES(1) $ 326.36 $ 282.55 $ 222.20 16 % 27 % (16 %) 13 % 11 % 10 % $ 378.13 $ 340.00 $ 299.00 97 % 95 % 99 % 4 % 4 % 4 % 8 % 13 % (10 %) 2.6 2.8 3.2 24 % 26 % 24 % 2013 2012 2011 Results of Operations Earned premiums $ 3,232 $ 2,147 $ 1,979 Net investment income 317 282 264 Total operating revenues 4,323 3,000 2,630 Net income (loss) to shareholders 281 253 142 Comprehensive income (loss) to shareholders 459 504 252 Diluted net income (loss) per share $ 22.48 $ 25.89 $ 14.60 Financial Position Total investments, cash and cash equivalents and restricted cash and cash equivalents (invested assets) $ 17,612 $ 9,333 $ 8,728 Total assets 23,956 12,557 11,532 Unpaid losses and loss adjustment expenses 10,262 5,371 5,399 Senior long-term debt and other debt 2,256 1,493 1,294 Shareholders' equity 6,674 3,889 3,388 Common shares outstanding (at year end, in thousands) 13,986 9,629 9,621 OPERATING PERFORMANCE MEASURES (1, 2, 3) Operating Data Book value per common share outstanding $ 477.16 $ 403.85 $ 352.10 Growth (decline) in book value per share 18 % 15 % 8 % 5-Year CAGR in book value per share (4)17 % 9 % 9 % Closing stock price $ 580.35 $ 433.42 $ 414.67 Ratio Analysis U.S. GAAP combined ratio (5)97 % 97 % 102 % Investment yield (6)3 % 4 % 4 % Taxable equivalent total investment return (7)7 % 9 % 7 % Investment leverage (8)2.6 2.4 2.6 Debt to capital 25 % 28 % 28 % (1)(2)Effective January 1, 2012, we prospectively adopted Financial Accounting Standards Board Accounting Standards Update No. 2010-26, Accounting for Costs Associated with Acquiring or Renewing Insurance Contracts.(3)Operating Performance Measures provide a basis for management to evaluate our performance. The method we use to compute these measures may differ from the methods used by other companies. See further discussion of management’smanagement's evaluation of these measures in Management’sManagement's Discussion & Analysis of Financial Condition and Results of Operations.(2)(4)(3)(5)34 |2007 2006 2005 2004 2003 2002 2001 10-Year

CAGR (2) $ 2,117 $ 2,184 $ 1,938 $ 2,054 $ 1,864 $ 1,549 $ 1,207 6 % 305 269 242 204 183 170 171 6 % 2,551 2,576 2,200 2,262 2,092 1,770 1,397 7 % 406 393 148 165 123 75 (126 ) — 337 551 64 273 222 73 (77 ) — $ 40.64 $ 39.40 $ 14.80 $ 16.41 $ 12.31 $ 7.53 $ (14.73 ) — $ 7,775 $ 7,524 $ 6,588 $ 6,317 $ 5,350 $ 4,314 $ 3,591 10 % 10,164 10,117 9,814 9,398 8,532 7,409 6,441 7 % 5,526 5,584 5,864 5,482 4,930 4,367 3,700 6 % — — 99 95 91 86 116 — 691 760 609 610 522 404 265 — — 106 141 150 150 150 150 — 2,641 2,296 1,705 1,657 1,382 1,159 1,085 15 % 9,957 9,994 9,799 9,847 9,847 9,832 9,820 — $ 265.26 $ 229.78 $ 174.04 $ 168.22 $ 140.38 $ 117.89 $ 110.50 12 % 15 % 32 % 3 % 20 % 19 % 7 % 8 % — 18 % 16 % 11 % 20 % 13 % 13 % 18 % — $ 491.10 $ 480.10 $ 317.05 $ 364.00 $ 253.51 $ 205.50 $ 179.65 — 88 % 87 % 101 % 96 % 99 % 103 % 124 % — 4 % 4 % 4 % 4 % 4 % 4 % 5 % — 5 % 11 % 2 % 8 % 11 % 8 % 8 % — 2.9 3.3 3.9 3.8 3.9 3.7 3.3 — 21 % 27 % 33 % 34 % 36 % 36 % 33 % — (4)(6)assets.(5)(7)TaxableSee "Investing Results" in Management's Discussion & Analysis of Financial Condition and Results of Operations for detail regarding the calculation of taxable equivalent total investment return includes net investment income, realized investment gains or losses, the change in fair value of the investment portfolio and the effect of foreign currency exchange rate movements during the period as a percentage of average invested assets. Tax-exempt interest and dividend payments are grossed up using the U.S. corporate tax rate to reflect an equivalent taxable yield.(6)(8)shareholders’shareholders' equity.

| 35

Markel Corporation & Subsidiaries

ASSETS Investments, available-for-sale, at estimated fair value: Fixed maturities (amortized cost of $5,256,980 in 2010 and $4,961,745 in 2009) Equity securities (cost of $996,088 in 2010 and $843,841 in 2009) Short-term investments (estimated fair value approximates cost) Investments in affiliates TOTAL INVESTMENTS Cash and cash equivalents Receivables Reinsurance recoverable on unpaid losses Reinsurance recoverable on paid losses Deferred policy acquisition costs Prepaid reinsurance premiums Goodwill and intangible assets Other assets TOTAL ASSETS LIABILITIESAND EQUITY Unpaid losses and loss adjustment expenses Unearned premiums Payables to insurance companies Senior long-term debt and other debt (estimated fair value of $1,086,000 in 2010 and $1,011,000 in 2009) Other liabilities TOTAL LIABILITIES Commitments and contingencies Shareholders’ equity: Common stock Retained earnings Accumulated other comprehensive income TOTAL SHAREHOLDERS’ EQUITY Noncontrolling interests TOTAL EQUITY TOTAL LIABILITIES AND EQUITY2010 2009 2008 2007 2006 2005 2004 5-Year CAGR (3) 10-Year CAGR (3) $ 1,731 $ 1,816 $ 2,022 $ 2,117 $ 2,184 $ 1,938 $ 2,054 10 % 6 % 273 260 282 305 269 242 204 2 % 6 % 2,225 2,069 1,977 2,551 2,576 2,200 2,262 17 % 8 % 267 202 (59 ) 406 393 148 165 — — 431 591 (403 ) 337 551 64 273 — — $ 27.27 $ 20.52 $ (5.95 ) $ 40.64 $ 39.40 $ 14.80 $ 16.41 — — $ 8,224 $ 7,849 $ 6,893 $ 7,775 $ 7,524 $ 6,588 $ 6,317 21 % 13 % 10,826 10,242 9,512 10,164 10,117 9,814 9,398 20 % 11 % 5,398 5,427 5,492 5,526 5,584 5,864 5,482 13 % 8 % 1,016 964 694 691 866 849 855 — — 3,172 2,774 2,181 2,641 2,296 1,705 1,657 25 % 17 % 9,718 9,819 9,814 9,957 9,994 9,799 9,847 — — $ 326.36 $ 282.55 $ 222.20 $ 265.26 $ 229.78 $ 174.04 $ 168.22 17 % 13 % 16 % 27 % (16 )% 15 % 32 % 3 % 20 % — — 13 % 11 % 10 % 18 % 16 % 11 % 20 % — — $ 378.13 $ 340.00 $ 299.00 $ 491.10 $ 480.10 $ 317.05 $ 364.00 — — 97 % 95 % 99 % 88 % 87 % 101 % 96 % — — 4 % 4 % 4 % 4 % 4 % 4 % 4 % — — 8 % 13 % (10 )% 5 % 11 % 2 % 8 % — — 2.6 2.8 3.2 2.9 3.3 3.9 3.8 — — 24 % 26 % 24 % 21 % 27 % 33 % 34 % — — 27MARKEL CORPORATION AND SUBSIDIARIESCONSOLIDATED BALANCE SHEETS December 31, 2010 2009 (dollars in thousands) $ 5,431,226 $ 5,112,136 1,721,971 1,349,829 325,340 492,581 — 43,633 7,478,537 6,998,179 745,259 850,494 312,096 279,879 798,090 886,442 70,568 65,703 188,783 156,797 80,293 68,307 645,900 502,833 506,063 433,262 $ 10,825,589 $ 10,241,896 $ 5,398,406 $ 5,427,096 839,537 717,728 50,715 46,853 1,015,947 963,648 333,292 294,857 7,637,897 7,450,182 884,457 872,876 1,735,973 1,514,398 551,093 387,086 3,171,523 2,774,360 16,169 17,354 3,187,692 2,791,714 $ 10,825,589 $ 10,241,896 December 31, 2013 2012 (dollars in thousands) ASSETS Investments, available-for-sale, at estimated fair value: Fixed maturities (amortized cost of $10,129,141 in 2013 and $4,562,278 in 2012) $ 10,142,536 $ 4,979,283 Equity securities (cost of $1,566,553 in 2013 and $1,387,305 in 2012) 3,251,798 2,406,951 Short-term investments (estimated fair value approximates cost) 1,452,288 973,330 Total Investments 14,846,622 8,359,564 Cash and cash equivalents 1,978,526 863,766 Restricted cash and cash equivalents 786,926 109,415 Receivables 1,141,773 413,883 Reinsurance recoverable on unpaid losses 1,854,414 778,774 Reinsurance recoverable on paid losses 102,002 51,145 Deferred policy acquisition costs 260,967 157,465 Prepaid reinsurance premiums 383,559 110,332 Goodwill 967,717 674,930 Intangible assets 565,083 374,295 Other assets 1,067,922 663,019 Total Assets $ 23,955,511 $ 12,556,588 LIABILITIES AND EQUITY Unpaid losses and loss adjustment expenses $ 10,262,056 $ 5,371,426 Life and annuity benefits 1,486,574 — Unearned premiums 2,127,115 1,000,261 Payables to insurance and reinsurance companies 295,496 103,212 Senior long-term debt and other debt (estimated fair value of $2,372,000 in 2013 and $1,688,000 in 2012) 2,256,227 1,492,550 Other liabilities 777,850 613,897 Total Liabilities 17,205,318 8,581,346 Redeemable noncontrolling interests 72,183 86,225 Commitments and contingencies Shareholders' equity: Common stock 3,288,863 908,980 Retained earnings 2,294,909 2,068,340 Accumulated other comprehensive income 1,089,805 911,337 Total Shareholders' Equity 6,673,577 3,888,657 Noncontrolling interests 4,433 360 Total Equity 6,678,010 3,889,017 Total Liabilities and Equity $ 23,955,511 $ 12,556,588 See accompanying notes to consolidated financial statements.36 |28

Earned premiums Net investment income Net realized investment gains (losses): Other-than-temporary impairment losses Other-than-temporary impairment losses recognized in other comprehensive income (loss) Other-than-temporary impairment losses recognized in net income (loss) Net realized investment gains (losses), excluding other-than-temporary impairment losses Net realized investment gains (losses) Other revenues TOTAL OPERATING REVENUES OPERATING EXPENSES Losses and loss adjustment expenses Underwriting, acquisition and insurance expenses Amortization of intangible assets Other expenses TOTAL OPERATING EXPENSES OPERATING INCOME (LOSS) Interest expense INCOME (LOSS) BEFORE INCOME TAXES Income tax expense (benefit) NET INCOME (LOSS) Net income attributable to noncontrolling interests NET INCOME (LOSS)TO SHAREHOLDERS OTHER COMPREHENSIVE INCOME (LOSS) Change in net unrealized gains on investments, net of taxes: Net holding gains (losses) arising during the period Unrealized other-than-temporary impairment losses on fixed maturities arising during the period Reclassification adjustments for net gains (losses) included in net income (loss) Change in net unrealized gains on investments, net of taxes Change in foreign currency translation adjustments, net of taxes Change in net actuarial pension loss, net of taxes TOTAL OTHER COMPREHENSIVE INCOME (LOSS) COMPREHENSIVE INCOME (LOSS) Comprehensive income attributable to noncontrolling interests COMPREHENSIVE INCOME (LOSS)TO SHAREHOLDERS NET INCOME (LOSS) PER SHARE Basic DilutedMARKEL CORPORATION AND SUBSIDIARIESCONSOLIDATED STATEMENTS OF OPERATIONSINCOME AND COMPREHENSIVE INCOME (LOSS) Years Ended December 31, 2010 2009 2008 (dollars in thousands, except per share data) OPERATING REVENUES $ 1,730,921 $ 1,815,835 $ 2,022,184 272,530 259,809 282,148 (11,644 ) (95,570 ) (339,164 ) (563 ) 5,620 — (12,207 ) (89,950 ) (339,164 ) 48,569 (6,150 ) (68,430 ) 36,362 (96,100 ) (407,594 ) 185,580 89,782 79,845 2,225,393 2,069,326 1,976,583 946,229 992,863 1,269,025 724,876 736,660 738,546 16,824 6,698 5,742 168,290 80,499 74,889 1,856,219 1,816,720 2,088,202 369,174 252,606 (111,619 ) 73,663 53,969 48,210 295,511 198,637 (159,829 ) 27,782 (3,782 ) (101,395 ) $ 267,729 $ 202,419 $ (58,434 ) 936 781 333 $ 266,793 $ 201,638 $ (58,767 ) $ 195,648 $ 326,959 $ (594,767 ) 672 (5,405 ) — (32,831 ) 52,883 264,898 163,489 374,437 (329,869 ) (2,282 ) 19,239 (7,893 ) 2,749 (4,268 ) (6,740 ) 163,956 389,408 (344,502 ) $ 431,685 $ 591,827 $ (402,936 ) 1,122 832 333 $ 430,563 $ 590,995 $ (403,269 ) $ 27.31 $ 20.54 $ (5.95 ) $ 27.27 $ 20.52 $ (5.95 ) Years Ended December 31, 2013 2012 2011 (dollars in thousands, except per share data) OPERATING REVENUES Earned premiums $ 3,231,616 $ 2,147,128 $ 1,979,340 Net investment income 317,373 282,107 263,676 Net realized investment gains: Other-than-temporary impairment losses (4,706 ) (12,078 ) (14,250 ) Other-than-temporary impairment losses recognized in other comprehensive income — — (5,946 ) Other-than-temporary impairment losses recognized in net income (4,706 ) (12,078 ) (20,196 ) Net realized investment gains, excluding other-than-temporary impairment losses 67,858 43,671 56,053 Net realized investment gains 63,152 31,593 35,857 Other revenues 710,942 539,284 351,077 Total Operating Revenues 4,323,083 3,000,112 2,629,950 OPERATING EXPENSES Losses and loss adjustment expenses 1,816,273 1,154,068 1,209,986 Underwriting, acquisition and insurance expenses 1,312,312 929,472 810,179 Amortization of intangible assets 55,223 33,512 24,291 Other expenses 663,528 478,248 309,046 Total Operating Expenses 3,847,336 2,595,300 2,353,502 Operating Income 475,747 404,812 276,448 Interest expense 114,004 92,762 86,252 Income Before Income Taxes 361,743 312,050 190,196 Income tax expense 77,898 53,802 41,710 Net Income 283,845 258,248 148,486 Net income attributable to noncontrolling interests 2,824 4,863 6,460 Net Income to Shareholders $ 281,021 $ 253,385 $ 142,026 OTHER COMPREHENSIVE INCOME Change in net unrealized gains on investments, net of taxes: Net holding gains arising during the period $ 225,545 $ 266,425 $ 141,839 Change in unrealized other-than-temporary impairment losses on fixed maturities arising during the period (141 ) (160 ) 3,943 Reclassification adjustments for net gains included in net income (40,830 ) (24,051 ) (22,341 ) Change in net unrealized gains on investments, net of taxes 184,574 242,214 123,441 Change in foreign currency translation adjustments, net of taxes (10,143 ) 1,534 (4,191 ) Change in net actuarial pension loss, net of taxes 4,065 6,664 (9,459 ) Total Other Comprehensive Income 178,496 250,412 109,791 Comprehensive Income 462,341 508,660 258,277 Comprehensive income attributable to noncontrolling interests 2,852 4,858 6,424 Comprehensive Income to Shareholders $ 459,489 $ 503,802 $ 251,853 NET INCOME PER SHARE Basic $ 22.57 $ 25.96 $ 14.66 Diluted $ 22.48 $ 25.89 $ 14.60 See accompanying notes to consolidated financial statements.| 3729Markel Corporation & Subsidiaries

January 1, 2008 Net loss Change in net unrealized gains on investments, net of taxes Change in foreign currency translation adjustments, net of taxes Change in net actuarial pension loss, net of taxes Comprehensive loss Issuance of common stock Repurchase of common stock Restricted stock units expensed Other December 31, 2008 Net income Change in net unrealized gains on investments, net of taxes Cumulative effect of adoption of FASB ASC 320-10, net of taxes Change in foreign currency translation adjustments, net of taxes Change in net actuarial pension loss, net of taxes Comprehensive income Issuance of common stock Restricted stock units expensed Acquisitions Other December 31, 2009 Net income Change in net unrealized gains on investments, net of taxes Change in foreign currency translation adjustments, net of taxes Change in net actuarial pension loss, net of taxes Comprehensive income Issuance of common stock Repurchase of common stock Restricted stock units expensed Stock options issued Purchase of noncontrolling interest Other DECEMBER 31, 2010MARKEL CORPORATION AND SUBSIDIARIESCONSOLIDATED STATEMENTS OF CHANGES IN EQUITY Common

Shares Common

Stock Retained

Earnings Accumulated

Other

Comprehensive

Income Total

Shareholders’

Equity Noncontrolling

Interests Total Equity (in thousands) 9,957 $ 866,362 $ 1,417,269 $ 357,531 $ 2,641,162 $ (136 ) $ 2,641,026 — — (58,767 ) — (58,767 ) 333 (58,434 ) — — — (329,869 ) (329,869 ) — (329,869 ) — — — (7,893 ) (7,893 ) — (7,893 ) — — — (6,740 ) (6,740 ) — (6,740 ) (403,269 ) 333 (402,936 ) 10 — — — — — — (153 ) — (60,601 ) — (60,601 ) — (60,601 ) — 2,187 — — 2,187 — 2,187 — 1,195 — — 1,195 64 1,259 9,814 869,744 1,297,901 13,029 2,180,674 261 2,180,935 — — 201,638 — 201,638 781 202,419 — — — 374,437 374,437 — 374,437 — — 15,300 (15,300 ) — — — — — — 19,188 19,188 51 19,239 — — — (4,268 ) (4,268 ) — (4,268 ) 590,995 832 591,827 6 — — — — — — — 2,638 — — 2,638 — 2,638 — — — — — 16,204 16,204 (1 ) 494 (441 ) — 53 57 110 9,819 872,876 1,514,398 387,086 2,774,360 17,354 2,791,714 — — 266,793 — 266,793 936 267,729 — — — 163,489 163,489 — 163,489 — — — (2,468 ) (2,468 ) 186 (2,282 ) — — — 2,749 2,749 — 2,749 430,563 1,122 431,685 32 8,185 — — 8,185 — 8,185 (133 ) — (45,218 ) — (45,218 ) — (45,218 ) — 2,543 — — 2,543 — 2,543 — 9,133 — — 9,133 — 9,133 — (8,345 ) — 237 (8,108 ) (1,557 ) (9,665 ) — 65 — — 65 (750 ) (685 ) 9,718 $ 884,457 $ 1,735,973 $ 551,093 $ 3,171,523 $ 16,169 $ 3,187,692 (in thousands) CommonShares CommonStock RetainedEarnings AccumulatedOtherComprehensiveIncome TotalShareholders'Equity NoncontrollingInterests Total Equity Redeemable Noncontrolling Interests December 31, 2010 9,718 $ 884,457 $ 1,735,973 $ 551,093 $ 3,171,523 $ 871 $ 3,172,394 $ 15,298 Net income (loss) 142,026 — 142,026 (190 ) 141,836 6,650 Other comprehensive income (loss) — 109,827 109,827 — 109,827 (36 ) Comprehensive Income (Loss) 251,853 (190 ) 251,663 6,614 Issuance of common stock 16 1,182 — — 1,182 — 1,182 — Repurchase of common stock (113 ) — (42,913 ) — (42,913 ) — (42,913 ) — Restricted stock awards expensed — 5,818 — — 5,818 — 5,818 — Acquisitions — — — — — — — 62,189 Other — 50 — — 50 (79 ) (29 ) (9,870 ) December 31, 2011 9,621 891,507 1,835,086 660,920 3,387,513 602 3,388,115 74,231 Net income (loss) 253,385 — 253,385 (262 ) 253,123 5,125 Other comprehensive income (loss) — 250,417 250,417 — 250,417 (5 ) Comprehensive Income (Loss) 503,802 (262 ) 503,540 5,120 Issuance of common stock 47 9,145 — — 9,145 — 9,145 — Repurchase of common stock (39 ) — (16,873 ) — (16,873 ) — (16,873 ) — Restricted stock awards expensed — 6,462 — — 6,462 — 6,462 — Acquisitions — — — — — — — 15,055 Adjustment of redeemable noncontrolling interests — — (3,101 ) — (3,101 ) — (3,101 ) 3,101 Purchase of noncontrolling interest — 1,430 — — 1,430 — 1,430 (3,573 ) Other — 436 (157 ) — 279 20 299 (7,709 ) December 31, 2012 9,629 908,980 2,068,340 911,337 3,888,657 360 3,889,017 86,225 Net income (loss) 281,021 — 281,021 (958 ) 280,063 3,782 Other comprehensive income — 178,468 178,468 — 178,468 28 Comprehensive Income (Loss) 459,489 (958 ) 458,531 3,810 Issuance of common stock 71 24,518 — — 24,518 — 24,518 — Repurchase of common stock (109 ) — (57,388 ) — (57,388 ) — (57,388 ) — Restricted stock awards expensed (3 ) 25,239 — — 25,239 — 25,239 — Acquisition of Alterra 4,398 2,330,199 — — 2,330,199 — 2,330,199 — Adjustment of redeemable noncontrolling interests — — 1,963 — 1,963 — 1,963 (1,963 ) Purchase of noncontrolling interest — (136 ) — — (136 ) — (136 ) (11,716 ) Other — 63 973 — 1,036 5,031 6,067 (4,173 ) December 31, 2013 13,986 $ 3,288,863 $ 2,294,909 $ 1,089,805 $ 6,673,577 $ 4,433 $ 6,678,010 $ 72,183 See accompanying notes to consolidated financial statements.38 |30

OPERATING ACTIVITIES Net income (loss) Adjustments to reconcile net income (loss) to net cash provided by operating activities: Deferred income tax expense (benefit) Depreciation and amortization Net realized investment losses (gains) Decrease in receivables Decrease (increase) in deferred policy acquisition costs Increase (decrease) in unpaid losses and loss adjustment expenses, net Increase (decrease) in unearned premiums, net Increase (decrease) in payables to insurance companies Other NET CASH PROVIDEDBY OPERATING ACTIVITIES INVESTING ACTIVITIES Proceeds from sales of fixed maturities and equity securities Proceeds from maturities, calls and prepayments of fixed maturities Cost of fixed maturities and equity securities purchased Net change in short-term investments Cost of investments in affiliates Acquisitions, net of cash acquired Additions to property and equipment Other NET CASH USEDBY INVESTING ACTIVITIES FINANCING ACTIVITIES Additions to senior long-term debt and other debt Repayment and retirement of senior long-term debt and other debt Repurchases of common stock Purchase of noncontrolling interest Other NET CASH PROVIDED (USED)BY FINANCING ACTIVITIES Effect of foreign currency rate changes on cash and cash equivalents Increase (decrease) in cash and cash equivalents Cash and cash equivalents at beginning of year CASHAND CASH EQUIVALENTSAT ENDOF YEARMARKEL CORPORATION AND SUBSIDIARIESCONSOLIDATED STATEMENTS OF CASH FLOWS Years Ended December 31, 2010 2009 2008 (dollars in thousands) $ 267,729 $ 202,419 $ (58,434 ) 7,185 (9,144 ) (100,417 ) 53,587 31,172 31,191 (36,362 ) 96,100 407,594 7,647 21,035 24,829 (13,910 ) 26,958 18,536 (109,371 ) 6,213 235,045 37,799 (91,933 ) (84,244 ) 1,115 (8,260 ) 2,609 7,872 7,903 (79,709 ) 223,291 282,463 397,000 340,546 205,561 683,316 383,618 312,951 404,444 (957,193 ) (726,954 ) (702,292 ) 202,882 23,616 (467,026 ) — — (8,481 ) (214,156 ) (154,920 ) (10,070 ) (42,103 ) (21,906 ) (17,673 ) 3,063 27,943 (34,190 ) (283,343 ) (333,709 ) (151,972 ) 42,897 507,346 102,425 (30,021 ) (255,293 ) (100,190 ) (45,218 ) — (60,601 ) (3,001 ) — — (10,267 ) (441 ) 64 (45,610 ) 251,612 (58,302 ) 427 9,749 (24,387 ) (105,235 ) 210,115 162,339 850,494 640,379 478,040 $ 745,259 $ 850,494 $ 640,379 Years Ended December 31, 2013 2012 2011 (dollars in thousands) OPERATING ACTIVITIES Net income $ 283,845 $ 258,248 $ 148,486 Adjustments to reconcile net income to net cash provided by operating activities: Deferred income tax expense 4,050 37,648 5,649 Depreciation and amortization 190,066 87,326 70,572 Net realized investment gains (63,152 ) (31,593 ) (35,857 ) Decrease (increase) in receivables 142,065 (36,590 ) (10,745 ) Decrease (increase) in deferred policy acquisition costs (103,704 ) 37,209 (5,891 ) Increase (decrease) in unpaid losses and loss adjustment expenses, net 290,130 (28,052 ) 57,000 Decrease in life and annuity benefits (40,235 ) — — Increase in unearned premiums, net 97,249 71,073 59,612 Increase (decrease) in payables to insurance and reinsurance companies (150,764 ) 19,190 (3,665 ) Increase (decrease) in income taxes payable 81,995 (9,909 ) 28,036 Other 13,976 (12,017 ) (1,879 ) Net Cash Provided By Operating Activities 745,521 392,533 311,318 INVESTING ACTIVITIES Proceeds from sales of fixed maturities and equity securities 879,564 336,548 288,046 Proceeds from maturities, calls and prepayments of fixed maturities 1,475,938 510,697 343,502 Cost of fixed maturities and equity securities purchased (1,651,397 ) (426,439 ) (713,102 ) Net change in short-term investments (470,423 ) (428,292 ) (216,972 ) Proceeds from sales of equity method investments 313,557 — — Cost of equity method investments (38,018 ) (40,650 ) (9,880 ) Change in restricted cash and cash equivalents (263,014 ) (37,642 ) (16,795 ) Additions to property and equipment (47,725 ) (45,519 ) (60,132 ) Acquisitions, net of cash acquired (12,198 ) (243,675 ) (120,102 ) Other 1,103 (2,158 ) 14,329 Net Cash Provided (Used) By Investing Activities 187,387 (377,130 ) (491,106 ) FINANCING ACTIVITIES Additions to senior long-term debt and other debt 547,214 492,792 336,181 Repayment and retirement of senior long-term debt and other debt (321,978 ) (313,790 ) (90,557 ) Repurchases of common stock (57,388 ) (16,873 ) (42,913 ) Issuance of common stock 24,518 9,145 1,182 Purchase of redeemable noncontrolling interests (11,852 ) (2,143 ) — Distributions to noncontrolling interests (5,124 ) (7,684 ) (9,259 ) Other (23 ) (19,485 ) (45 ) Net Cash Provided By Financing Activities 175,367 141,962 194,589 Effect of foreign currency rate changes on cash and cash equivalents 6,485 3,142 (1,823 ) Increase in cash and cash equivalents 1,114,760 160,507 12,978 Cash and cash equivalents at beginning of year 863,766 703,259 690,281 CASH AND CASH EQUIVALENTS AT END OF YEAR $ 1,978,526 $ 863,766 $ 703,259 See accompanying notes to consolidated financial statements.| 3931Markel Corporation & Subsidiaries