| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) | ||

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) | |

| Wisconsin | 39-0168610 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| (Title of eachclass) | (Name of each exchange on which registered) | ||||

| Class A Common Stock, par value $0.20 per share | New York Stock Exchange | |||||

| Large accelerated filer | x | Accelerated filer | o | |

| Non-accelerated filer | o | Smaller-reporting company | o | |

| (do not check if a smaller reporting company) | ||||

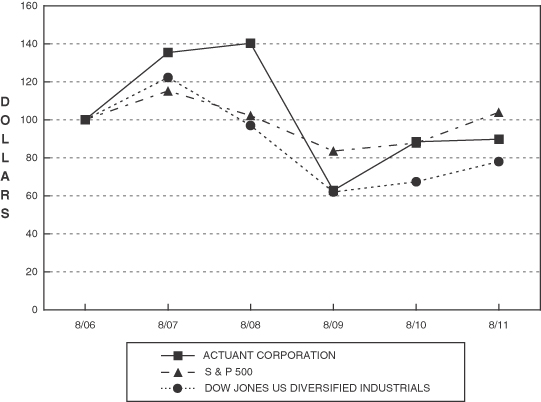

The Industrial segment is primarily involved in the design, manufacture and distribution of branded hydraulic and mechanical tools to the maintenance, industrial, infrastructure and production automation markets. The Energy segment provides joint integrity products and services, customized offshore vessel mooring solutions, as well as Financial information related to the Company's reportable segments is included in Note 13, "Business Segment, Geographic and Customer Information" in the notes to the consolidated financial statements. excellence process utilizes various continuous improvement techniques to reduce costs and improve efficiencies across all locations and functions worldwide, thereby expanding profit margins. Strong cash flow generation is achieved by maximizing returns on assets and minimizing primary working capital needs. Our LEAD efforts also support our Growth + Innovation (“G + I”) initiative, a Al Masaood Trading. Tig Tesco Intl. energy asset owners. Fleetwood. Financial information related to the Company's geographic areas is included in Note 10, "Income Taxes" and Note 13, "Business Segment, Geographic and Customer Information" in the notes to the consolidated financial statements. Quarter 1 Quarter 2 Quarter 3 Quarter 4 At August 31, Name Position Robert C. Arzbaecher William Gustav H.P. Boel Mark E. Goldstein Sheri R. Grissom Brian K. Kobylinski Andrew G. Lampereur Sheri L. Roberts Theodore C. Wozniak mutual funds. Mr. Goldstein is also a director at Pall Corporation. experience to Actuant. Mr. Lampereur was also a director of Robbins & Myers, Inc. from 2005 through 2013. flows. difficulties in integrating and managing personnel, financial reporting and other systems used by the acquired businesses; the failure of acquired businesses to perform in accordance with our expectations; failure to achieve anticipated synergies between our business units and the business units of acquired businesses; the loss of customers of acquired businesses; or the loss of key managers of acquired businesses. agreements would adversely affect us. attract and retain qualified employees. If we are unable to attract and retain qualified individuals or our costs to do so increase significantly, our operations would be materially adversely affected. Industrial Energy Electrical Engineered Solutions Corporate and other Mine Safety Disclosures The Company’s Class A common stock is traded on the New York Stock Exchange under the symbol ATU. At September 30, Fiscal Period 2011 2010 In fiscal 28, 2012. 2013 Actuant Corporation S&P 500 Dow Jones US Diversified Industrials Statement of Earnings Data(1)(2): Net sales Gross profit Selling, administrative and engineering expenses Restructuring charges Impairment charges Amortization of intangible assets Operating profit Earnings from continuing operations Diluted earnings per share from continuing operations Cash dividends per share Diluted weighted average common shares outstanding Balance Sheet Data(at end of period)(2): Total assets Total debt Weasler Engineering, Inc. Mastervolt Intl. Holding B.V. Selantic Biach Industries Hydrospex Team Hydrotec The Cortland Companies Cortland Cable Company Sanlo, Inc. Superior Plant Services, LLC Templeton, Kenly & Co, Inc. BH Electronics, Inc. T.T. Fijnmechanica B.V. Injectaseal Deutschland GmbH Veha Haaksbergen B.V. Maxima Technologies Statements of Earnings Data: Net sales Cost of products sold Gross profit Selling, administration and engineering expenses Restructuring charges Impairment charges Amortization of intangible assets Operating profit Financing costs, net Other expense (income), net Earnings from continuing operations before income tax expense Income tax expense Earnings from continuing operations Loss from discontinued operations, net of income taxes Net earnings Other Financial Data: Depreciation Capital expenditures resulting subdued demand for our products and services. Consolidated operating profit for fiscal profits and assets. Net Sales Operating Profit Operating Profit % Net Sales Operating Profit Operating Profit % 2012 Energy segment operating profit increased earn-out provision. Net Sales Operating Profit Operating Profit % Net Sales Operating Profit (Loss) Operating Profit % 2012 Engineered Solutions segment operating profit following the refinancing of our Senior Notes in the third quarter of fiscal 2012. Net sales Net gain (loss) on disposal Loss from operations of discontinued businesses(1) Income tax benefit (expense) Loss from discontinued operations, net of income tax for the last three fiscal years: Net cash provided by operating activities Net cash used in investing activities Net cash provided by (used in) financing activities Effect of exchange rate changes on cash Net increase (decrease) in cash and cash equivalents Accounts receivable, net Inventory, net Accounts payable Net primary working capital Our Senior Credit Facility, which See Note Facility. in the range of $35 to 40 million, but could vary from that depending on business and growth opportunities. 2013 Long-term debt Interest on long-term debt Operating leases Acquisition deferred purchase price $7 million at August 31, 2012. We perform an analysis of the historical sales usage of the individual inventory items on hand and a reserve is recorded to adjust inventory cost to market value. The inventory valuation assumptions used are based on historical experience. We believe that such estimates are made based on consistent and appropriate methods; however, actual results may differ from these estimates under different assumptions or conditions. the values of assets in use, and often requires the application of judgment regarding estimates and assumptions. While the ultimate responsibility resides with management, for material acquisitions we retain the services of certified valuation specialists to assist with assigning estimated values to certain acquired assets and assumed liabilities, including intangible assets and tangible long-lived assets. Acquired intangible assets, excluding goodwill, are valued using a discounted cash flow methodology based authority rulings and changes in tax laws, changes in projected levels of taxable income and future tax planning strategies could affect the actual effective tax rate and tax balances recorded liabilities being translated into U.S. dollars, our reporting currency. INDEX TO FINANCIAL STATEMENT SCHEDULEPART IItem 1.Business 1 Item 1. Item 1A. Item 1B. Item 2. Item 3. Item 4. 8 Item 1B.Unresolved Staff Comments12Item 2.Properties12Item 3.Legal Proceedings13Item 4.(Removed and Reserved)13PART IIItem 5.14Item 6. 16Item 7. 17Item 7A. 28Item 8. 29Item 9. Item 9A. Item 9B. 69 Item 9A.Controls and Procedures69Item 9B.Other Information69PART IIIItem 10.70Item 11. 70Item 12. 70Item 13. 70Item 14. 70 PART IVItem 15. 71truck, automotive, agricultural, industrial, production automation, oil & gas, energy, power generation, maintenance, energy, marine, solar, infrastructure, residential and commercial construction, truck, automotive, specialty vehicle and retail electrical Do-It-Yourself (“DIY”)agriculture industries, market acceptance of existing and new products, successful integration of acquisitions and related restructuring, operating margin risk due to competitive pricing and operating efficiencies, supply chain risk, material, labor, or overhead cost increases, foreign currency risk, interest rate risk, commodity risk, the impact of geopolitical activity on the economy, the timing or strength of an economic uncertainty and the impact onrecovery in the Company’s served markets, litigation matters, the Company’s ability to access capital markets and other factors that may be referred to or noted in the Company’s reports filed with the Securities and Exchange Commission from time to time. We disclaim any obligation to publicly update or revise any forward-looking statements as a result of new information, future events or any other reason.fourthree operating and reportable segments as follows: Industrial, Energy Electrical and Engineered Solutions. umbilical, rope and cable solutions to the global oil & gas, power generation and energy markets. The Electrical segment is primarily involved in the design, manufacture and distribution of a broad range of electrical products to the retail DIY, wholesale, original equipment manufacturer (“OEM”), solar, utility, marine and other harsh environmentenergy markets. The Engineered Solutions segment provides highly engineered position and motion control systems to OEMsoriginal equipment manufacturers (“OEM”) in various on and off-highway vehicle markets, as well as, a variety of other products to the industrial and agricultural markets.internalcore sales growth (overall sales growth excluding the impact of acquisitions, divestitures and foreign currency rate changes) that exceeds the annual growth rates of the gross domestic product in the geographic regions in which we operate. In addition to internalcore sales growth, we are focused on acquiring complementary businesses. Following an acquisition, we seek to drive cost reductions, develop additional cross-selling opportunities and deepen customer relationships. We also focus on profit margin expansion and cash flow generation to achieve our financial objectives. Our LEAD (“Lean Enterprise Across Disciplines”) operational new process focused on improvingincreasing core sales growth. The cash flow that results from efficient asset management and improved profitability is used to reduce debt and fund both strategic acquisitions, treasury share repurchases and internal growth opportunities.TheseOur hydraulic and mechanical tools are marketed primarily through ourthe Enerpac, Simplex, Precision Sure-Lock and Milwaukee Cylinder brand names.TheOurThese hydraulic tools operate at very high pressures of approximately 5,000 to 12,000 pounds per square inch and are generally sold by a diverse group of industrial and specialty fluid power distributors to customers in the infrastructure, mining, steel mill, cement, rail, oil & gas, power generation and general maintenance industries. Key industrial distributors include W.W. Grainger, Applied Industrial Technologies, MSC, Maskin K. Lund, Industrial Air Tool and MSC, which collectively generate less than 10% of this segment’s sales. heavy lifting solutions, which combine hydraulics, steel fabrication and electronic controls with engineering and application knowledge, are typically utilized in major infrastructure projects (bridges, stadiums, tunnels and offshore platforms) for heavy lifting, launching & skidding or synchronous lifting applications.railroad, bridge, infrastructure and mining markets.security, reliability, up-time and productivity are key value drivers. Products include joint integrity tools and connectors for oil & gas and power generation installations, mooring solutions, as well as umbilical, rope and cable solutions. In addition to these products, the Energy segment also provides manpower services, including machining, engineering and maintenance activities. The products and services of the Energy segment are distributed and marketed under various brand names (principally Hydratight, D.L. Ricci, Morgrip, Cortland, FibronBX, Puget Sound Rope, Biach, Selantic, Viking SeaTech and Selantic)Jeyco) to OEMs, maintenance and service organizations and energy producers in emerging and developed countries.The Hydratight businesses also provideprovides manpower services where our highly trained technicians perform bolting, machining and joint integrity work for customers. Our joint integrity business operates to world class safety standards while delivering products and services through a localized infrastructure of rental and maintenance depots. Service, product sales and rental revenue each generate approximately one-third of our joint integrity sales. This business maintains strong relationships with a variety of leading firms such as Statoil, BJ Services, Petrobras, Baker Hughes, Bechtel and British Petroleum. umbilical, rope and cable solutions that maximize performance, safety and efficiency for customers in thevarious markets including oil & gas, heavy marine, subsea, ROV and seismic markets.seismic. With its global design and manufacturing capabilities, the Cortland business is able to provide customized synthetic ropes, heavy lift slings, electro-mechanicalspecialized mooring, rigging and towing systems, electro-optical-mechanical cables and umbilicals to customers, including leading firms such as CGG Veritas,Sercel, Expro, General Electric and Sercel.Halliburton. These products are utilized in critical applications, often deployed in harsh environments (sub seaoperating conditions (sub-sea oil & gas production, maintenance and exploration) and are required to meet robust safety standards. Additional custom designed products are also sold tointo a variety of other niche markets including mining, medical, security, aerospace and defense.ElectricalElectrical segment is involved in the design, manufacture and distribution of a broad range of electrical products to the retail DIY, OEM, electrical distribution, power transformation and harsh environment electrical markets. Our Electrical businesses share core competencies in product branding, distribution and channel management, global sourcing and managing the logistics of SKU intensive product lines. The Electrical segment sells its products through a combination of distributors, direct sales personnel and manufacturers’ representatives.The Electrical segment provides the retail DIY market with a variety of electrical tools and consumables such as wire strippers, electrical meters, connectors, terminals, cable ties, staples and other wire management products and conduit bending equipment under the Gardner Bender, Del City and A.W. Sperry brands. These products are sold to leading retailers such as Lowe’s, The Home Depot, Menards, True Value and Ace Hardware, as well as numerous electrical distributors and OEM’s. This segment also sells power transformation products in North America including low voltage, single-phase dry type transformers and custom toroidal transformers under the Acme Electric brand name and high voltage switches under the Turner Electric brand name. These transformers are sold through electrical wholesale distributors, as well as directly to OEMs such as Rockwell Automation, Eaton, Yaskawa and General Electric. Product offerings also include electrical components and systems for the harsh environment and marine markets under the Ancor, Marinco, Guest, Mastervolt and B.E.P Marine brand names. These products are primarily sold to various customers in the industrial, marine, power generation, industrial and retail markets, including West Marine, Applied Materials and Kohler. TheAugust 2013 acquisition of Mastervolt in fiscal 2011 increasedViking SeaTech (“Viking”) further expands the Electrical segment’s product offerings, including batteries, generators, battery chargers, inverters, display panels, wiringEnergy segment's geographic presence, technologies and fully integrated systems,services provided to the global energy market. Headquartered in Aberdeen, Scotland, Viking is an offshore support specialist providing a comprehensive range of equipment and services to the oil & gas industry. Viking servesEuropean solar markets. Solar products (primarily high efficiency solar inverters for residential and small commercial applications) are sold through local distributors and installers.instrumentation and flexible power transmission systems.instrumentation. Products in the Engineered Solutions segment are primarily marketed directly to OEMs through a technical sales organization. Within this segment, engineering capabilities, technical service, quality and established customer relationships are key competitive advantages.70%one-half of this segment’s revenue comes from the vehicle systemsVehicle Systems product line (Power-Packer, Gits and Power Gear brands), which is soldwith sales to the truck, automotive, off-highway and specialty vehicle markets. Products include hydraulic cab-tilt and latching systems which are sold to global heavy duty truck OEMs such as Volvo, Iveco, Scania, Paccar-DAF, FAW and CNHTC and automotive electro-hydraulic convertible top latching and actuation systems. The automotive convertible top actuation systems are utilized on both retractable soft and hard top vehicles manufactured by OEMs such as Daimler, Audi, Volkswagen, Renault, Peugeot, Saab, BMW, Volvo and Nissan. Our diesel engine air flow solutions, such as exhaust gas recirculation (EGR)(“EGR”) systems and air flow actuators, are used by diesel engine and turbocharger manufacturers to reduce emissions, improve fuel efficiency and increase horsepower. Primary end markets include heavy duty truck and off-highway equipment serving customers such as Caterpillar, DAF, Detroit Diesel, Garrett Turbochargers,Cummins, Honeywell and Borg Warner. We also sell actuation systems to various automotive and specialty vehicle OEMscustomers (principally in the defense, recreational vehicle and off-highway markets) such as Honeywell, BorgWarner, Oshkosh BAE Systems and Winnebago.fiscal 2011 acquisitionbroad range of Weasler Engineering further diversified the Engineered Solutions segment. Weasler is a global designer and manufacturer of highly engineered drive train components and systems for agricultural, lawn & turf and industrial markets. The diverse products, technologies and engineered solutions of Weasler Maxima Technologies,Engineering, maximatecc, Elliott Manufacturing Sanlo and Nielsen SessionsSanlo comprise the Other product linesline within the Engineered Solutions segment. Products include severe-duty electronic instrumentation (including displays and clusters, machine controls and sensors), HMI solutions and power transmission products (highly engineered drive trainpower transmission components including drive shafts, torque limiters, gearboxes, torsional dampers and torsional dampers), custom designed flexible shafts and push pull cable assemblies, custom steel cable assemblies and a comprehensive line of case, container and industrial hardware.shafts). These products are sold to a variety of niche markets including agricultural implement, lawn & turf, construction, forestry, industrial, aerospace, material handling and security.worldwide,globally, with our principal markets outside the United States being Europe and Asia. In fiscal 20112013 we derived approximately 48%43% of our net sales from the United States, 35%38% from Europe 12%and the Middle East, 14% from Asia and 5% from other areas. We have operations around the world and this geographic diversity allows us to draw on the skills of a global workforce, provides flexibility to our operations, allows us to drive economies of scale, provides revenue streams that may help offset economic trends that are specific to individual countries and offers us an opportunity to access new markets. In addition, we believe that our future growth depends, in part, on our ability to develop products and sales opportunities that successfully target developing countries. Although international operations are subject to certain risks, we continue to believe that a global presence is key to maintaining strong relationships with many of our global customers.approximated $18were $21 million $15, $17 million and $16$12 million in fiscal 2011, 20102013, 2012 and 2009,2011, respectively. We also incur significant costs in connection with fulfilling custom orders and developing unique solutions for unique customer applications,needs, which are not included in these research and development expense totals.640586 patents (excluding pending applications), we create products that satisfy specific customer needs and make tasks easier and more efficient for our customers. We own numerous United States and foreign patents and trademarks. No individual patent or trademark is believed to be of such importance that its termination would have a material adverse effect on our business.operations.of components we source from a network of global suppliers. We have implemented single piece flow methodology in most of our manufacturing plants, which reduces inventory levels, lowers “re-work” costs and shortens lead times to customers. We manufacture the majority of the products we sell, but strategically source components and finished goods from an established global network of qualified suppliers. Components are purchased frombuilt to our highly engineered specifications by a variety of suppliers, including those in low cost countries such as China, Turkey and Mexico. We have built strong relationships with our key suppliers and, while we single source certain of our components, we believe that in most cases there are several qualified alternative sources.Energy and ElectricalEnergy segments have relatively short order-to-ship cycles, while our OEM oriented Engineered Solutions segment has a longer cycle, and therefore typically has a larger backlog. We had order backlogs of approximately $260$209 million and $204 million at both August 31, 20112013 and 2010,2012, respectively. Substantially all orders are expected to be completed in the nextfilled within twelve months. While we typically enjoy a stronger second half of our fiscal year, our consolidated sales in total are not subject to significant seasonal fluctuations. 2011 2010 22 % 23 % 23 % 23 % 27 % 27 % 28 % 27 % 100 % 100 % 2013 2012 Quarter 1 (September-November) 24 % 24 % Quarter 2 (December - February) 23 % 24 % Quarter 3 (March - May) 27 % 27 % Quarter 4 (June- August) 26 % 25 % 100 % 100 % Employees2011,2013, we employed approximately 6,2006,700 individuals. Our employees are not subject to collective bargaining agreements, with the exception of approximately 375365 U.S. production employees, as well as certain international employees covered by government mandated collective labor agreements. We believe we have a good working relationship with our employees.17,14, “Contingencies and Litigation” in the notes to consolidated financial statements.20112013 are listed below. Age 53 51 President and Chief Executive Officer; Chairman of the BoardL. Axline 57 63Executive Vice President—Global Customer RelationshipsWilliam S. Blackmore55 Executive Vice President—Engineered Solutions Segment 68 66 Executive Vice President; Director 57 55 Executive Vice President and Chief Operating OfficerPresident; Director 49 47 Executive Vice President—Global Human Resources 47 45 Executive Vice President—Industrial Segment and Energy SegmentsChina 50 48 Executive Vice President and Chief Financial Officer 47 Executive Vice President—Energy Segment David L. Scheer 54 52 Executive Vice President—Electrical Segment 55 53 Executive Vice President—Business Development President and Chief Executive Officer and Chairman of the Board of Directors. Mr. Arzbaecher was namedwill continue in his role as Chairman of Board, but will step down as Chief Executive Officer of the Company at the January 2014 Annual Meeting, after having served as President and Chief Executive Officer of the Company in Augustsince 2000. HePrior to that, he served as Vice President and Chief Financial Officer of Actuantthe Company starting in 1994 and Senior Vice President in 1998. He served as Vice President, Finance of Tools & Supplies from 1993 to 1994. He joined Actuantthe Company in 1992 as Corporate Controller. From 1988 through 1991, Mr. Arzbaecher was employed by Grabill Aerospace Industries LTD, where he last held the position of Chief Financial Officer.William L. Axline, Executive Vice President—Global Customer Relationships. In fiscal 2011, Mr. Axline was appointed to the newly created position of Executive Vice President—Global Customer Relationships. Mr. Axline joined Actuant in January 2008 as Executive Vice President of the Electrical Segment. Prior to Actuant, Mr. Axline held the role of Executive Vice President, Chief Operating Officer of Fluidmaster,Arzbaecher is also a director at CF Industries Holding, Inc. from 2003 to 2007. Prior to joining Fluidmaster, he served as President, Chief Executive Officer, of Distribution America,and Fiduciary Management, Inc. from 2001 to 2003 and held the role of Vice President, General Manager at Alltrade, Inc. from 1999 to 2000. Mr. Axline also had over 27 years of leadership experience with The Stanley Works.(“Rexnord”) from 1997 to 2000. Prior to 1997, Mr. Blackmore held various general management positions at Rexnord and Pillar Industries.2530 years currently(in various executive roles) and has served as a member of the Board of Directors and an Executive Vice President in charge ofsince 2000. In addition to his Board responsibilities, Mr. Boel currently oversees our LEAD initiatives. Following the spin-off of the Company’s Electronics segment in fiscal 2000,Mr. Boel has announced that he leftwill retire from the Company as an employee but served as aand not stand for re-election to his Board of Directors role at the January 2014 Annual Meeting.During this time heMr Goldstein was employed by APW Ltd., where he last held the position of Senior Vice President. In September 2002, he rejoined the Company as an employee and was named business leader of the European Electrical business in addition to his Board responsibilities. Prior to the spin-off, he held various positions with Actuant, including President of the Industrial business segment, PresidentCompany and added to the Board of Engineered Solutions EuropeDirectors in August 2013, and President of Enerpac.Mark E. Goldstein,will assume Chief Executive Vice President and Chief Operating Officer.Officer responsibilities after the January 2014 Annual Meeting. Mr. Goldstein has beenwas Actuant’s Chief Operating Officer since fiscal 2007. He joined the Company in fiscal 2001 as the leader of the Gardner Bender business and was appointed Executive Vice President—Tools and Supplies in 2003.increasingly responsible human resourcesresource leadership positions with several leading global organizations including Johns Manville, McKechnie Group and General Electric. Ms. Grissom brings to Actuant over 20 years of global human resources experience.Energy Segments.China. Mr. Kobylinski joined Actuantthe Company in 1993 and progressed through a number of management roles within the Electrical Segment. He became Vice President of Business Development for Actuant in 2002 and was named Global Business Leader, Hydratight in 2005. InFrom 2007 to 2013, he was promoted to the position of Industrial and Energy Segment Leader.Leader and currently serves as the Industrial Segment Leader with responsibility for the Company's China operations. Prior to Actuant,joining the Company, Mr. Kobylinski was employed by Fort Howard Corporation and Federated Insurance.Actuantthe Company in 1993 as Corporate Controller, a position he held until 1996 when he was appointed Vice President of Finance for Gardner Bender. In 1998, Mr. Lampereur was appointed Vice President, General Manager for Gardner Bender. He was appointed to his present position in August 2000. Prior to joining Actuant,the Company, Mr. Lampereur held a number of financial management positions at Terex Corporation.(2005-2010) and Sigma Electric Manufacturing (2002-2005).from 2005 through 2010. Mr. Scheer also previously held various management positions at Rexel USA, Thomas & Betts and Electroline Manufacturing.risk factors discussed in this section should be considered together with other information in the Form 10-Krisks and shoulduncertainties described below are those that we have identified as material, but are not be considered the only risks and uncertainties facing us. If any of the Company.The Company’sevents contemplated by the following risks actually occurs, then our business, financial condition, or results of operations could be materially adversely affected. Additional risks and uncertainties not currently known to us or that we currently believe are immaterial also may adversely impact our business.flows or liquidity may be adversely affected by a prolonged economic downturn or economic uncertainty.gas, marine and electrical)gas) that typically are adversely affected by downward economic cycles. As global economic conditions deteriorate or economic uncertainty continues, our customers may experience deterioration of their businesses, which may delay or lengthen sales cycles. Unforeseen events may also require additional restructuring costs. Although we expect that the related cost savings and realization of efficiencies will offset the restructuring related costs over time, we may not achieve the net benefits. Like most industrial companies, our sensitivity to economic cycles may have a material effect on our financial condition, results of operations, cash flows and liquidity. for acquisitions on terms acceptable to us, our ability to identify acquisition candidates and increased competition for acquisitions. The process of integrating acquired businesses into our existing operations may result in unforeseen operating difficulties and may require additional financial resources and attention from management that would otherwise be available for the ongoing development or expansion of our existing operations. Failure to effectively execute our acquisition strategy or successfully integrate the acquired businesses could have an adverse effect on our financial condition, results of operations, cash flows and liquidity.2011,2013, goodwill and other intangible assets totaled $1,368$1,112 million, or about 67%52% of our total assets. The goodwill results from our acquisitions, representing the excess of cost over the fair value of the net tangible and other identifiable intangible assets we have acquired. We assess annually whether there has been impairment in the value of our goodwill or indefinite-lived intangible assets. If future operating performance at one or more of our reporting units were to fall significantly below current levels, we could be required to recognize a non-cash charge to operating earnings for goodwill or other intangible asset impairment. Any significant goodwill or intangible asset impairment wouldcould negatively affect our financial condition and results of operations. See Note 6, “Impairment Charges”3, “Discontinued Operations” in the notes to consolidated financial statements for more information regarding goodwill and intangible asset impairment charges recognized in fiscal 20102013 and 2009.If2012.failsreviews its operations for businesses which may no longer be aligned with its strategic initiatives and long-term objectives. During fiscal 2013, we announced our intention to divest the Electrical Segment (a discontinued operation at August 31, 2013). Divestitures pose risks and challenges that could negatively impact our business, including required separation/carve-out activities and costs, disputes with buyers or potential impairmentitsour customers do not accept the new products it develops, the Company’swe develop, our business could be adversely affected.productioncommercialization of new products or failure to gain market acceptance of new products and technologies may reduce future sales and adversely affect our competitive position. We continue to invest in the development and marketing of new products through our GrowthG + InnovationI process. There can be no assurance that we will have sufficient resources to make such investments, that we will be able to make the technological advances necessary to maintain competitive advantages or that we can recover major research and development expenses. If we fail to make innovations, launch products with quality problems or the market does not accept our new products, then our financial condition, results of operations, cash flows and liquidity could be adversely affected. A lack of successful new product developments may also cause customers to buy from a competitor or may cause us to have to lower our prices to compete. Our substantial debt level may adversely affect our future performance.ability to service our debt obligations would be harmed if we failfailure to comply with the financial and other covenants in our debt agreements.decreasereduction in our liquidity and impair our ability to pay amounts due on our indebtedness. Moreover, if we are required to repay any of our debt before it becomes due, we may be unable to borrow additional amounts or otherwise obtain the cash necessary to repay that debt, when due, which could seriously harm our business.the Company’sour manufacturing operations and suppliers are located outside the United States. Our international operations present special risks, primarily from currency exchange rate fluctuations, exposure to local economic and political conditions, export and import restrictions, controls on repatriation of cash and exposure to local political conditions. In particular, our results of operations have been significantly affected by fluctuations in foreign currency exchange rates, especially the euroEuro and British pound. For example, since approximately one-third of our revenue is generated in Europe, the weakening of the U.S. dollar against the euro and British pound in fiscal 2011 favorably impacted our results of operations due to the translation of non-U.S. dollar denominated revenues. In addition, there have been several proposals to reform international taxation rules in the United States. We earn a substantial portion of our income from international operations and therefore changes to United States international tax rules may have a material adverse effect on future results of operations or liquidity. To the extent that we expand our international presence, these risks may increase.we useare used in our products include steel, plastic resin, copper, brass, steel wire and rubber. Most of our suppliers are not currently parties to long-term contracts with us. Consequently, we are vulnerable to fluctuations in prices of such raw materials. If market prices for certain materials such as steel, plastic resin and copper rise, it could have a negative effect on our operating results and ability to manufacture our respective products on a timely basis. Factors such as supply and demand, freight costs and transportation availability, inventory levels, the level of imports and general economic conditions may affect the prices of raw materials that we need. If we experience a significant increase in raw material prices, or if we are unable to pass along increases in raw material prices to our customers, our results of operations could be adversely affected. In addition, an increasing portion of our products are sourced from low cost regions. Changes in export laws, taxes and disruptions in transportation routes could adversely impact our results of operations.Chief Operating Officer,President, Chief Financial Officer and executives in charge of our segments. We currently do not have employment agreements with most of these or other officers. The departure of key personnel without adequate replacement could severely disrupt our business operations. Additionally, we need qualified managers and skilled employees with technical and manufacturing industry experience to operate our businesses successfully. From time to time there may be shortages of skilled labor which may make it more difficult and expensive for us topatents,patent, trademark, copyright and trade secret laws, employee and third-party non-disclosure agreements and other contracts to establish and protect our technology and other intellectual property rights. The agreements may be breached or terminated, and we may not have adequate remedies for any breach, and existing trade secrets, patent and copyright law afford us limited protection. Policing unauthorized use of our intellectual property is difficult. A third party could copy or otherwise obtain and use our products or technology without authorization. Litigation may be necessary for us to defend against claims of infringement or to protect our intellectual property rights and could result in substantial cost to us and diversion of our efforts. Further, we might not prevail in such litigation which could harm our business.2011,2013, the Company operated the following facilities in its continuing operations (square footage in thousands): Number of Locations Distribution /

Sales /

Admin Square Footage Manufacturing Total Owned Leased Total 8 12 20 157 496 653 11 16 27 26 485 511 6 7 13 127 624 751 15 3 18 677 716 1,393 1 3 4 353 90 443 41 41 82 1,340 2,411 3,751 Number of Locations Square Footage Manufacturing Total Owned Leased Total Industrial 8 12 20 157 546 703 Energy 11 29 40 40 974 1,014 Engineered Solutions 18 5 23 634 817 1,451 Corporate and other 1 4 5 353 111 464 38 50 88 1,184 2,448 3,632 locationsfacilities are located in the United States, the United Kingdom, the Netherlands, Mexico, Turkey and China. We also maintain a presence in Australia, Austria,Azerbaijan, Brazil, Canada, Finland, France, Germany, Hong Kong, Hungary, India, Indonesia, Italy, Japan, Kazakhstan, Malaysia, Mexico, New Zealand, Norway, Poland, Russia, Singapore, South Africa, South Korea, Spain, TurkeySweden and the United Arab Emirates. See Note 108 “Leases” in the notes to the consolidated financial statements for information with respect to our lease commitments. In addition to the facilities above, we retain responsibility for approximately 14 owned or leasedfour facilities that are now idle and available for sale or sublease.covered byrecoverable through insurance. In our opinion, the resolution of these contingencies is not likely to have a material adverse effect on our financial condition, results of operation or cash flows. For further information refer to Note 17,14, “Contingencies and Litigation” in the notes to consolidated financial statements.(Removed and Reserved)Item 5. Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities Market Information2011,2013, there were 1,8091,655 shareholders of record of Actuant Corporation Class A common stock. The high and low sales prices of the common stock were as follows for the previous two fiscal years:

Year High Low June 1, 2011 to August 31, 2011 $ 27.65 $ 17.47 March 1, 2011 to May 31, 2011 29.29 23.94 December 1, 2010 to February 28, 2011 30.41 23.91 September 1, 2010 to November 30, 2010 23.97 20.06 June 1, 2010 to August 31, 2010 $ 21.74 $ 17.47 March 1, 2010 to May 31, 2010 23.87 18.10 December 1, 2009 to February 28, 2010 19.80 15.93 September 1, 2009 to November 30, 2009 17.31 13.37 Fiscal Year Period High Low 2013 June 1, 2013 to August 31, 2013 $ 37.22 $ 31.18 March 1, 2013 to May 31, 2013 34.61 29.16 December 1, 2012 to February 28, 2013 31.77 26.20 September 1, 2012 to November 30, 2012 31.33 25.38 2012 June 1, 2012 to August 31, 2012 $ 29.12 $ 24.23 March 1, 2012 to May 31, 2012 29.97 24.33 December 1, 2011 to February 29, 2012 28.94 20.05 September 1, 2011 to November 30, 2011 24.09 17.63 Dividends2011,2013, the Company declared a dividend of $0.04$0.04 per common share payable on October 14, 201115, 2013 to shareholders of record on September 30, 2011.2013. In fiscal 2010,2012, the Company declared a dividend of $0.040.04 per common share payable on October 15, 201016, 2012 to shareholders of record on September 30, 2010. Period June 1 to June 30, 2013 200,000 $ 31.67 3,658,606 July 1 to July 31, 2013 592,119 33.89 3,066,487 August 1 to August 31, 2013 50,000 34.76 3,016,487 842,119 $ 33.41 20062008 to August 31, 2011.COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN.Among Actuant Corporation, the S&P 500 Indexand the Dow Jones US Diversified Industrials Index

Copyright© 2011