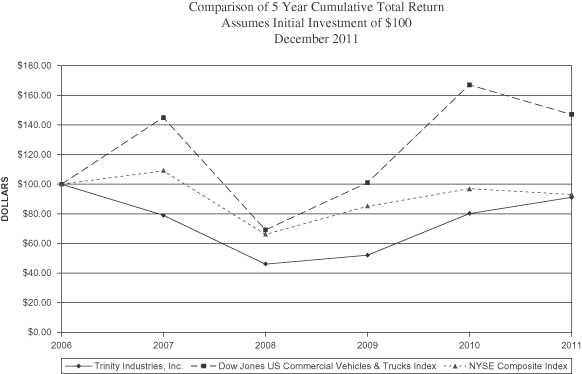

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | |||||||||||||||||||

Trinity Industries, Inc. | 100 | 79 | 46 | 52 | 80 | 91 | ||||||||||||||||||

Dow Jones US Commercial Vehicles & Trucks Index | 100 | 145 | 69 | 101 | 167 | 147 | ||||||||||||||||||

New York Stock Exchange Composite Index | 100 | 109 | 66 | 85 | 97 | 93 | ||||||||||||||||||

2007.

(Mark One)

| (Mark One) | |

| þ | ANNUAL REPORT PURSUANT TO SECTION 13OR 15(d) OF THE SECURITIES EXCHANGE ACTOF 1934 |

OR

| OR | |

| ¨ | TRANSITION REPORT PURSUANT TOSECTION 13 OR 15(d) OF THESECURITIES EXCHANGE ACT OF 1934 |

| Delaware | 75-0225040 | |

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

2525 Stemmons Freeway, Dallas, Texas | 75207-2401 | |

| (Address of principal executive offices) | (Zip Code) | |

Title of each class |

| |

Common Stock ($1.00 par value) | New York Stock Exchange, Inc. | |

Large accelerated filer þAccelerated filer ¨Non-accelerated filer ¨Smaller reporting company ¨ (Do not check if a smaller reporting company) | ||||||

Indicate by check mark whether the Registrant is a shellcompany (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

$1,938.9 million.

79,118,471.

| Caption | Page | |||||

| ||||||

| Item 5. | ||||||

| ||||||

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | ||||||

| Item 10. | ||||||

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | ||||||

Certain Relationships and Related Transactions, and Director Independence | ||||||

www.trin.net.

Railcars

Inland barges

Structuralstructural wind towers

Highway products

Concreteaggregates;

Tank containers

Steel parts and steel components.

|

|

|

|

|

|

|

2012

.Our crash cushionstank heads we manufacture in the production of our tank cars and containers. We also sell our tank heads to a broad range of other protective barriers include multiple proprietary productsmanufacturers. There is strong competition in the tank heads business.

We sell highway products in Canada, Mexico, and all 50 of the United States. We compete against several national and regional guardrail manufacturers. We also export our proprietary highway products to more than 60 countries worldwide.

In addition, we provide hot-dip galvanizing services toforeign manufacturers of fabricated steel materials from our production facilities in north Texas and manufacture a line of construction equipmentstructural wind towers for the mining industry.

North American market.

564.1 million.

We are a leading manufacturer in North America of structural wind towers used in the wind energy market. These towers are manufactured in the United States and Mexico to customer specifications and installed by our customers. Our customers are generally turbine producers. Our structural wind towers backlog as of December 31, 2011 was approximately $934.3 million. Approximately $412.5 million of this backlog is involved in litigation filed by the Company against one of our structural wind tower customers for breach of contract by failing to comply with the customer’s multi-year, contractual purchase obligations.

We are a leading manufacturer in North America of tank containers and tank heads for pressure and non-pressure vessels. We manufacture tanks in the United States and Mexico. We market a portion of our products in Mexico under the brand name of TATSA®. In 2011, we began manufacturing frac tanks to support industries requiring temporary liquid storage, primarily the oil and gas industry.

We manufacture tank heads, which are pressed metal components used in the manufacturing of many of our finished products, as well as pressure rated or non-pressure rated, depending on their intended use. We use a significant portion of the tank heads we manufacture in the production of our tank cars and containers. We also sell our tank heads to a broad range of other manufacturers. There is strong competition in the tank heads business.

We manufacture tanks that are used by industrial plants, utilities, residences, and small businesses in suburban and rural areas. We also manufacture fertilizer containers for bulk storage, farm storage, and the application and distribution of anhydrous ammonia. Our tank products range from nine-gallon tanks for motor fuel use to 1.8 million-gallon bulk storage spheres. We sell our tanks to dealers and large industrial users. In the United States we generally deliver the containers to our customers who install and fill the containers. Our competitors include large and small manufacturers of tanks.

We manufacture utility, traffic, and lighting structures, which are used principally by municipalities, and various other local and state governmental entities. We also manufacture transmission structures to be used in the erection of private and public electric transmission lines. These structures are manufactured in the United States and Mexico to customer specifications and installed by our customers.

There are a number of well-established entities that actively compete with us in the business of manufacturing energy equipment including several domestic and foreign manufacturers of structural wind towers for the North American market.

All Other. All Other includes our captive insurance and transportation companies; legal, environmental, and maintenance costs associated with non-operating facilities; other peripheral businesses; and the change in market valuation related to ineffective commodity hedges.

| As of December 31, | ||||||||

| 2011 | 2010 | |||||||

| (in millions) | ||||||||

Rail Group | ||||||||

External Customers | $ | 1,973.2 | $ | 346.6 | ||||

Leasing Group | 621.9 | 111.0 | ||||||

|

|

|

| |||||

| $ | 2,595.1 | $ | 457.6 | |||||

Inland Barge | $ | 494.6 | $ | 508.0 | ||||

Structural wind towers | $ | 934.3 | $ | 1,000.0 | ||||

| December 31, 2012 | December 31, 2011 | |||||||

| (in millions) | ||||||||

| Rail Group | ||||||||

| External Customers | $ | 2,867.5 | $ | 1,973.2 | ||||

| Leasing Group | 834.7 | 621.9 | ||||||

| $ | 3,702.2 | $ | 2,595.1 | |||||

| Inland Barge | $ | 564.1 | $ | 494.6 | ||||

| Structural wind towers | $ | 680.3 | $ | 934.3 | ||||

remainder contracted for delivery in future years.

Cement. Cement required for theour ready-mix concrete and aggregates businessoperations is received primarily from Texas. In 2011,2012, the supply of cement was sufficient in our markets to meet demand. We have not experienced difficulties supplying concrete to our customers.

Business Group | December 31, | 2012 | |||

Rail Group | 6,210 | ||||

Construction Products Group | 1,950 | ||||

Inland Barge Group | 2,010 | ||||

Energy Equipment Group | 4,580 | ||||

Railcar Leasing and Management Services Group | 130 | ||||

All Other | 340 | ||||

| Corporate | 270 | ||||

| 15,490 | |||||

| |||||

activities, or properties, may give rise to additional compliance and other costs that could have a material adverse effect on our financial condition and operations.

particularly natural gas for plant operations and diesel fuel for vehicles, could have a material adverse effect upon our ability to conduct our business. The likelihood of such an occurrence or its duration, and its ultimate effect on our operations, cannot be reasonably predicted at this time.

| Name | Age | Office | Officer Since | |||

Timothy R. Wallace* | 59 | Chairman, Chief Executive Officer, and President | 1985 | |||

James E. Perry* | 41 | Senior Vice President and Chief Financial Officer | 2005 | |||

William A. McWhirter II* | 48 | Senior Vice President and Group President | 2005 | |||

D. Stephen Menzies* | 57 | Senior Vice President and Group President | 2001 | |||

S. Theis Rice* | 62 | Senior Vice President, Human Resources and Chief Legal Officer | 2002 | |||

| Donald G. Collum | 64 | Vice President and Chief Audit Executive | 2005 | |||

| Tammy D. Gilbert | 52 | Vice President, Information Technology | 2012 | |||

| Virginia C. Gray, Ph.D. | 53 | Vice President, Organizational Development | 2007 | |||

Mary E. Henderson* | 54 | Vice President, Chief Accounting Officer, and Controller | 2009 | |||

| John M. Lee | 52 | Vice President, Business Development | 1994 | |||

| Gail M. Peck | 45 | Vice President and Treasurer | 2010 | |||

| Heather Perttula Randall | 39 | Vice President, Legal Affairs and Government Relations | 2011 | |||

| Jared S. Richardson | 40 | Vice President, Associate General Counsel and Secretary | 2010 | |||

| Stephen W. Smith | 63 | Vice President | 2012 | |||

| C. Michael Williams | 57 | Vice President, Human Resources | 2012 | |||

Name | Age | Office | Officer Since | Term Expires | ||||

| Timothy R. Wallace* | 58 | Chairman, Chief Executive Officer, and President | 1985 | May 2012 | ||||

| James E. Perry* | 40 | Senior Vice President and Chief Financial Officer | 2005 | May 2012 | ||||

| Antonio Carrillo* | 45 | Senior Vice President and Group President | 2010 | May 2012 | ||||

| William A. McWhirter II* | 47 | Senior Vice President and Group President | 2005 | May 2012 | ||||

| D. Stephen Menzies* | 56 | Senior Vice President and Group President | 2001 | May 2012 | ||||

| S. Theis Rice* | 61 | Senior Vice President, Human Resources and Chief Legal Officer | 2002 | May 2012 | ||||

| Madhuri A. Andrews | 45 | Vice President, Information Technology | 2008 | May 2012 | ||||

| Donald G. Collum | 63 | Vice President and Chief Audit Executive | 2005 | May 2012 | ||||

| Virginia C. Gray, Ph.D. | 52 | Vice President, Organizational Development | 2007 | May 2012 | ||||

| Mary E. Henderson* | 53 | Vice President, Chief Accounting Officer, and Controller | 2009 | May 2012 | ||||

| John M. Lee | 51 | Vice President, Business Development | 1994 | May 2012 | ||||

| Gail M. Peck | 44 | Vice President and Treasurer | 2010 | May 2012 | ||||

| Heather Perttula Randall | 38 | Vice President, Legal Affairs and Government Relations | 2011 | May 2012 | ||||

| Jared S. Richardson | 39 | Associate General Counsel and Secretary | 2010 | May 2012 |

|

1934.

Mr. Carrillo joined Trinity in 1996 asAmerica's Vice President, of Operations of Trinity Industries de MexicoTransition, Transformation, and in 1999 became the President of Trinity Industries de Mexico. In 2005, he was named President of Trinity’s Energy Equipment Group. In 2009, Mr. Carrillo was named Group President of the Energy Equipment GroupProject/Program Management. She has also held executive positions with Electronic Data Systems, Sabre Holdings, American Airlines, and in 2010 was named Vice President. He was elected Senior Vice President in 2011. Mr. Carrillo retains responsibility for Trinity’s operations in Mexico.

Dr. Gray joined Trinity in 2007 and was appointed Vice President, Organizational Development. Prior to that, she was President of Vehicles of Change, a consulting firm focused on improving organizational effectiveness.

Harris Methodist Hospital.

In 2012, Mr. Menzies joined Trinity in 2001 as President of Trinity Industries Leasing Company. In 2006, he becameMcWhirter was named Senior Vice President and Group President forTrinityRail®.

of the Construction Products, Energy Equipment, and Inland Barge Groups.

Following a period of weak railcar demand that began in 2009, new orders for railcars improved significantly in 2011 due to increased demand for the shipment of commodities, replacement of older railcars, and federal tax benefits received from taking delivery of railcars in 2011 and 2012. Orders for structural wind towers have been slow since mid-2008 when energy development companies encountered tightened credit markets, lower demand for electricity and heightened competition arising from declining natural gas prices. The continued slowdown in the residential and commercial construction markets negatively impacted the results of our Construction Products Group as well. We continually assess our manufacturing capacity and take steps to align our production capacity with demand for our products. As a result of our assessment, we adapted to the rapid decline in market conditions that began in 2009 by reducing our production footprint and staffing levels and causing certain facilities to be on non-operating status. Due to improvements in demand, we increased production staff at certain facilities in late 2010 and during 2011. We expect that facilities on non-operating status will be available for future operations to the extent that demand further increases.

To the extent that we do not have such arrangements in place, an increase in steel prices could materially lower our margins and profitability. In general, we believe there is enough capacity in the supply industryaddition, our ability to meet current production level demands. We believedemands is dependent on the existing contracts and commercial relationships we have in place will meet our current production forecasts. However, anyability to obtain a sufficient amount of steel. An unanticipated interruption in our supply chain could have an adverse impact on both our margins and production schedules.

permits.

apply and if we are found liable in any such incident, it could have a material adverse effect on our financial condition, business, and operations.

As of December 31, 2011, there was $308.5 million of indebtedness outstanding and $166.5 million was available under the TILC warehouse loan facility. Borrowings under the warehouse facility are secured by the specific railcars financed by such borrowings and the underlying leases. A decline in the value of the railcars securing borrowings under the warehouse facility or in the creditworthiness of the lessees under the associated leases could reduce TRLWT’s ability to obtain long-term financing for such railcars. Additionally, fluctuations in interest rates from the time TRLWT purchases railcars with short-term borrowings under the warehouse facility and the time TRLWT obtains permanent financing for such railcars could decrease our profitability on the leasing of the railcars and could have an adverse impact on our financial results. If TRLWT is unable to obtain long-term financing to replace borrowings under the warehouse facility, the lenders under the warehouse facility may foreclose on the portion of TRLWT’s lease fleet pledged to secure its loan facility, which foreclosure, if a significant number of railcars is affected, could result in the loss of a significant amount of TRLWT’s assets.

goods produced in America; more stringent or restrictive laws, rules, and regulations relating to labor or the environment; adverse tax consequences; and price exchange controls could limit operations affecting production throughput and makemaking the manufacture and distribution of our products less timely or more difficult. Furthermore, any material change in the quotas, regulations, or duties on imports imposed by the United StatesU.S. government and agencies, or on exports by the government of Mexico or its agencies, could affect our ability to export products that we manufacture in Mexico. Because we have operations outside the United States,U.S., we could be adversely affected by final judgments of non-compliance with the U.S. Foreign Corrupt Practices Act and similar anti-corruption laws of other countries.

mine safety and health regulations in the United StatesU.S. or in foreign jurisdictions in which we operate could increase our operating costs. We are unable to predict the ultimate cost of compliance with these health and safety laws and regulations. Accordingly, there can be no assurance that we will not become involved in future litigation, investigations, or other proceedings or if we were found to be responsible or liable in any litigation, investigations, or proceedings, that such costs would not be material to us.

period financial statements. For a further discussion of some of our critical accounting policies and standards and recent accounting changes, see Critical Accounting Policies and Estimates in Management’sManagement's Discussion and Analysis of Financial Condition and Results of Operations and Note 1 Summary of Significant Accounting Policies of the Notes to Consolidated Financial Statements.

| Approximate Square Feet | Approximate Square Feet Located In | |||||||||||||||

| Owned | Leased | US | Mexico | |||||||||||||

Rail Group | 5,278,900 | 32,000 | 3,573,100 | 1,737,800 | ||||||||||||

Construction Products Group | 1,494,400 | 63,400 | 1,557,800 | — | ||||||||||||

Inland Barge Group | 919,000 | 97,100 | 1,016,100 | — | ||||||||||||

Energy Equipment Group | 1,505,500 | 261,100 | 923,600 | 843,000 | ||||||||||||

Executive Offices | 173,000 | — | 173,000 | — | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| 9,370,800 | 453,600 | 7,243,600 | 2,580,800 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||

| Approximate Square Feet | Approximate Square Feet Located In | |||||||||||

| Owned | Leased | US | Mexico | |||||||||

| Rail Group | 6,185,400 | 92,700 | 4,280,600 | 1,997,500 | ||||||||

| Construction Products Group | 1,833,900 | 98,100 | 1,932,000 | — | ||||||||

| Inland Barge Group | 948,500 | 97,100 | 1,045,600 | — | ||||||||

| Energy Equipment Group | 1,799,500 | 250,300 | 1,206,800 | 843,000 | ||||||||

| Executive Offices | 186,000 | — | 186,000 | — | ||||||||

| 10,953,300 | 538,200 | 8,651,000 | 2,840,500 | |||||||||

| Production Capacity Utilized | |||||

Rail Group | |||||

| 70 | % | |||

Construction Products Group | 75 | % | |||

| Inland Barge Group | % | ||||

Energy Equipment Group | % | ||||

| Market for Registrant's Common Equity, Related Stockholder Mattersand Issuer Purchases of Equity Securities. |

Our common stock is traded on the New York Stock Exchange under the ticker symbol “TRN”. The following table shows the closing price range of our common stock by quarter for the years ended December 31, 20112012 and 2010.

| Prices | ||||||||

Year Ended December 31, 2011 | High | Low | ||||||

Quarter ended March 31, 2011 | $ | 36.67 | $ | 26.31 | ||||

Quarter ended June 30, 2011 | 37.76 | 30.54 | ||||||

Quarter ended September 30, 2011 | 37.25 | 21.05 | ||||||

Quarter ended December 31, 2011 | 30.62 | 19.94 | ||||||

Year Ended December 31, 2010 | High | Low | ||||||

Quarter ended March 31, 2010 | $ | 20.58 | $ | 15.22 | ||||

Quarter ended June 30, 2010 | 26.46 | 17.72 | ||||||

Quarter ended September 30, 2010 | 22.27 | 16.45 | ||||||

Quarter ended December 31, 2010 | 26.68 | 22.01 | ||||||

2011.

| Prices | |||||||

| Year Ended December 31, 2012 | High | Low | |||||

| Quarter ended March 31, 2012 | $ | 35.93 | $ | 29.69 | |||

| Quarter ended June 30, 2012 | 33.48 | 22.80 | |||||

| Quarter ended September 30, 2012 | 33.55 | 21.85 | |||||

| Quarter ended December 31, 2012 | 36.05 | 29.01 | |||||

| Year Ended December 31, 2011 | High | Low | |||||

| Quarter ended March 31, 2011 | $ | 36.67 | $ | 26.31 | |||

| Quarter ended June 30, 2011 | 37.76 | 30.54 | |||||

| Quarter ended September 30, 2011 | 37.25 | 21.05 | |||||

| Quarter ended December 31, 2011 | 30.62 | 19.94 | |||||

At December 31, 2011,2012, we had approximately 1,8581,867 record holders of common stock. The par value of the common stock is $1.00 per share.

Trinity has paid 191195 consecutive quarterly dividends. Quarterly dividends declared by Trinity for the years ended December 31, 20112012 and 20102011 are as follows:

Year Ended December 31, | ||||||||

| 2011 | 2010 | |||||||

Quarter ended March 31, | $ | 0.08 | $ | 0.08 | ||||

Quarter ended June 30, | 0.09 | 0.08 | ||||||

Quarter ended September 30, | 0.09 | 0.08 | ||||||

Quarter ended December 31, | 0.09 | 0.08 | ||||||

|

|

|

| |||||

Total | $ | 0.35 | $ | 0.32 | ||||

|

|

|

| |||||

| Year Ended December 31, | |||||||

| 2012 | 2011 | ||||||

| Quarter ended March 31, | $ | 0.09 | $ | 0.08 | |||

| Quarter ended June 30, | 0.11 | 0.09 | |||||

| Quarter ended September 30, | 0.11 | 0.09 | |||||

| Quarter ended December 31, | 0.11 | 0.09 | |||||

| Total | $ | 0.42 | $ | 0.35 | |||

-

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | |||||||||||||||||||

Trinity Industries, Inc. | 100 | 79 | 46 | 52 | 80 | 91 | ||||||||||||||||||

Dow Jones US Commercial Vehicles & Trucks Index | 100 | 145 | 69 | 101 | 167 | 147 | ||||||||||||||||||

New York Stock Exchange Composite Index | 100 | 109 | 66 | 85 | 97 | 93 | ||||||||||||||||||

2007.

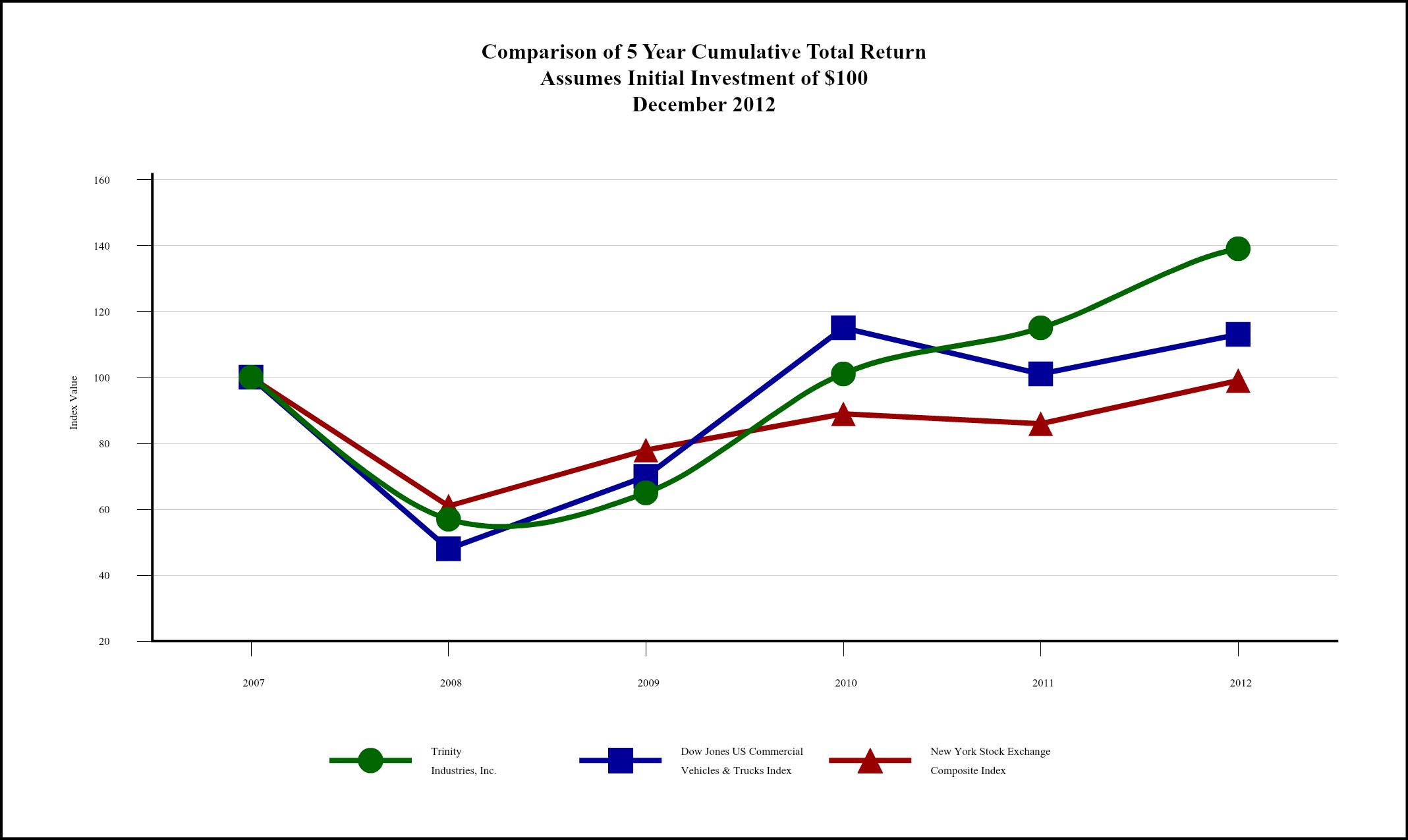

| 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | ||||||||||||

| Trinity Industries, Inc. | 100 | 57 | 65 | 101 | 115 | 139 | |||||||||||

| Dow Jones US Commercial Vehicles & Trucks Index | 100 | 48 | 70 | 115 | 101 | 113 | |||||||||||

| New York Stock Exchange Composite Index | 100 | 61 | 78 | 89 | 86 | 99 | |||||||||||

Period | Number of Shares Purchased (1) | Average Price Paid per Share (1) | Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs (2) | Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May Yet Be Purchased Under the Plans or Programs (2) | ||||||||||||

October 1, 2011 through October 31, 2011 | 12,327 | $ | 21.53 | — | $ | 200,000,000 | ||||||||||

November 1, 2011 through November 30, 2011 | 161 | $ | 28.09 | — | $ | 200,000,000 | ||||||||||

December 1, 2011 through December 31, 2011 | 122 | $ | 29.77 | — | $ | 200,000,000 | ||||||||||

|

|

|

| |||||||||||||

Total | 12,610 | $ | 21.70 | — | $ | 200,000,000 | ||||||||||

|

|

|

| |||||||||||||

2012

:| Period | Number of Shares Purchased (1) | Average Price Paid per Share (1) | Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs (2) | Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May Yet Be Purchased Under the Plans or Programs (2) | ||||||||||

| October 1, 2012 through October 31, 2012 | 3,659 | $ | 31.23 | — | $ | 200,000,000 | ||||||||

| November 1, 2012 through November 30, 2012 | 61,383 | $ | 31.84 | — | $ | 200,000,000 | ||||||||

| December 1, 2012 through December 31, 2012 | 361 | $ | 35.22 | — | $ | 200,000,000 | ||||||||

| Total | 65,403 | $ | 31.82 | — | $ | 200,000,000 | ||||||||

| (in millions, except percent and per share data) | Year Ended December 31, | |||||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

Statement of Operations Data: | ||||||||||||||||||||

Revenues | $ | 3,075.1 | $ | 2,155.5 | $ | 2,420.9 | $ | 3,803.4 | $ | 3,723.3 | ||||||||||

Operating profit (loss) | 425.3 | 303.8 | (30.9 | ) | 559.5 | 529.8 | ||||||||||||||

Income (loss) from continuing operations | 145.7 | 75.4 | (137.7 | ) | 282.4 | 289.8 | ||||||||||||||

Discontinued operations: | ||||||||||||||||||||

Loss from discontinued operations, net of benefit for income taxes of $—, $—, $—, $(0.0), and $(0.2) | — | — | — | (1.5 | ) | (0.7 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net income (loss) | $ | 145.7 | $ | 75.4 | $ | (137.7 | ) | $ | 280.9 | $ | 289.1 | |||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net income (loss) attributable to Trinity | $ | 142.2 | $ | 67.4 | $ | (137.7 | ) | $ | 280.9 | $ | 289.1 | |||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net income (loss) attributable to Trinity Industries, Inc. per common share: | ||||||||||||||||||||

Basic: | ||||||||||||||||||||

Continuing operations | $ | 1.77 | $ | 0.85 | $ | (1.81 | ) | $ | 3.49 | $ | 3.58 | |||||||||

Discontinued operations | — | — | — | (0.02 | ) | (0.01 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| $ | 1.77 | $ | 0.85 | $ | (1.81 | ) | $ | 3.47 | $ | 3.57 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Diluted: | ||||||||||||||||||||

Continuing operations | $ | 1.77 | $ | 0.85 | $ | (1.81 | ) | $ | 3.47 | $ | 3.55 | |||||||||

Discontinued operations | — | — | — | (0.02 | ) | (0.01 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| $ | 1.77 | $ | 0.85 | $ | (1.81 | ) | $ | 3.45 | $ | 3.54 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Weighted average number of shares outstanding: | ||||||||||||||||||||

Basic | 77.5 | 76.8 | 76.4 | 78.4 | 78.7 | |||||||||||||||

Diluted | 77.8 | 77.0 | 76.4 | 78.8 | 79.4 | |||||||||||||||

Dividends declared per common share | $ | 0.35 | $ | 0.32 | $ | 0.32 | $ | 0.31 | $ | 0.26 | ||||||||||

Balance Sheet Data: | ||||||||||||||||||||

Total assets | $ | 6,121.0 | $ | 5,760.0 | $ | 4,656.4 | $ | 4,911.6 | $ | 4,039.7 | ||||||||||

Debt — recourse | 457.7 | 450.3 | 646.0 | 584.4 | 590.3 | |||||||||||||||

Debt — non-recourse | 2,517.2 | 2,457.4 | 1,199.1 | 1,190.3 | 643.9 | |||||||||||||||

Stockholders’ equity | $ | 1,948.3 |

| $ | 1,845.7 | $ | 1,806.3 | $ | 1,912.3 | $ | 1,812.7 | |||||||||

Ratio of total debt to total capital | 60.4 | % | 61.2 | % | 50.5 | % | 48.1 | % | 40.5 | % | ||||||||||

Book value per share | $ | 24.29 | $ | 23.13 | $ | 22.81 | $ | 24.08 | $ | 22.27 | ||||||||||

Effective

| Year Ended December 31, | |||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2008 | |||||||||||||||

| (in millions, except percent and per share data) | |||||||||||||||||||

| Statement of Operations Data: | |||||||||||||||||||

| Revenues | $ | 3,811.9 | $ | 2,938.3 | $ | 1,930.7 | $ | 2,162.9 | $ | 3,423.6 | |||||||||

| Operating profit (loss) | 574.8 | 426.8 | 294.2 | (36.1 | ) | 536.7 | |||||||||||||

| Income (loss) from continuing operations | 251.9 | 146.8 | 69.4 | (140.8 | ) | 266.8 | |||||||||||||

| Income (loss) from discontinued operations, net of provision (benefit) for income taxes of $1.1, $(0.4), $3.6, $2.0, and $7.8 | 1.8 | (1.1 | ) | 6.0 | 3.1 | 14.1 | |||||||||||||

| Net income (loss) | $ | 253.7 | $ | 145.7 | $ | 75.4 | $ | (137.7 | ) | $ | 280.9 | ||||||||

| Net income (loss) attributable to Trinity Industries, Inc. | $ | 255.2 | $ | 142.2 | $ | 67.4 | $ | (137.7 | ) | $ | 280.9 | ||||||||

| Net income (loss) attributable to Trinity Industries, Inc. per common share: | |||||||||||||||||||

| Basic: | |||||||||||||||||||

| Continuing operations | $ | 3.18 | $ | 1.78 | $ | 0.77 | $ | (1.85 | ) | $ | 3.30 | ||||||||

| Discontinued operations | 0.02 | (0.01 | ) | 0.08 | 0.04 | 0.17 | |||||||||||||

| $ | 3.20 | $ | 1.77 | $ | 0.85 | $ | (1.81 | ) | $ | 3.47 | |||||||||

| Diluted: | |||||||||||||||||||

| Continuing operations | $ | 3.17 | $ | 1.78 | $ | 0.77 | $ | (1.85 | ) | $ | 3.28 | ||||||||

| Discontinued operations | 0.02 | (0.01 | ) | 0.08 | 0.04 | 0.17 | |||||||||||||

| $ | 3.19 | $ | 1.77 | $ | 0.85 | $ | (1.81 | ) | $ | 3.45 | |||||||||

| Weighted average number of shares outstanding: | |||||||||||||||||||

| Basic | 77.3 | 77.5 | 76.8 | 76.4 | 78.4 | ||||||||||||||

| Diluted | 77.5 | 77.8 | 77.0 | 76.4 | 78.8 | ||||||||||||||

| Dividends declared per common share | $ | 0.42 | $ | 0.35 | $ | 0.32 | $ | 0.32 | $ | 0.31 | |||||||||

| Balance Sheet Data: | |||||||||||||||||||

| Total assets | $ | 6,669.9 | $ | 6,121.0 | $ | 5,760.0 | $ | 4,656.4 | $ | 4,911.6 | |||||||||

| Debt - recourse | $ | 458.1 | $ | 455.0 | $ | 449.4 | $ | 645.5 | $ | 583.9 | |||||||||

| Debt - non-recourse | $ | 2,596.9 | $ | 2,517.2 | $ | 2,457.4 | $ | 1,199.1 | $ | 1,190.3 | |||||||||

| Stockholders' equity | $ | 2,137.6 | $ | 1,948.3 | $ | 1,845.7 | $ | 1,806.3 | $ | 1,912.3 | |||||||||

| Ratio of total debt to total capital | 58.8 | % | 60.4 | % | 61.2 | % | 50.5 | % | 48.1 | % | |||||||||

| Book value per share | $ | 27.02 | $ | 24.29 | $ | 23.13 | $ | 22.81 | $ | 24.08 | |||||||||

accompanying consolidated balance sheets.

•Company Overview

•Executive Summary

•Results of Operations

•Liquidity and Capital Resources

•Contractual Obligations and Commercial Commitments

•Critical Accounting Policies and Estimates

•Recent Accounting Pronouncements

Forward Looking•Forward-Looking Statements

As

| As of December 31, | ||||||||

| 2011 | 2010 | |||||||

| (in millions) | ||||||||

Rail Group | ||||||||

External Customers | $ | 1,973.2 | $ | 346.6 | ||||

Leasing Group | 621.9 | 111.0 | ||||||

|

|

|

| |||||

| $ | 2,595.1 | $ | 457.6 | |||||

Inland Barge | $ | 494.6 | $ | 508.0 | ||||

Structural wind towers | $ | 934.3 | $ | 1,000.0 | ||||

| December 31, 2012 | December 31, 2011 | ||||||

| (in millions) | |||||||

| Rail Group | |||||||

| External Customers | $ | 2,867.5 | $ | 1,973.2 | |||

| Leasing Group | 834.7 | 621.9 | |||||

| $ | 3,702.2 | $ | 2,595.1 | ||||

| Inland Barge | $ | 564.1 | $ | 494.6 | |||

| Structural wind towers | $ | 680.3 | $ | 934.3 | |||

remainder contracted for delivery in future years.

In May 2011, the Company’s inland barge manufacturing facility in Missouri experienced a flood resulting in significant damages to Trinity’s property and a temporary disruption of its production activities. The Company is insured against losses due to property damage and business interruption subject to certain deductibles. Trinity received $35.0 million in payments from its insurance carriers of which $22.7 million pertained to the replacement of or repairs to damaged property, plant, and equipment with a net book value of $5.7 million, with the remainder pertaining primarily to the reimbursement of flood-related expenses and lost production. Accordingly, the Company recognized a gain of $17.0 million in the fourth quarter of 2011 from the disposition of flood-damaged property, plant, and equipment. Additionally, our barge manufacturing operations incurred approximately $8.6 million in costs, net of insurance reimbursements, related to damages and lost productivity resulting from the flood. During the fourth quarter of 2011, the Company’s inland barge production capacity at its Missouri operations was restored to its pre-flood levels. With respect to the flood at our Tennessee manufacturing facility in May 2010, operating profit in 2011 includes insurance proceeds of $6.5 million and a $0.6 million gain from the disposition of damaged property, plant, and equipment related to the flood.

In July 2011, TRIP Rail Holdings LLC (“TRIP Holdings”) issued $175.0 million in Senior Secured Notes (the “TRIP Holdings Senior Secured Notes”) and TRIP Rail Master Funding LLC (“TRIP Master Funding”), a Delaware limited liability company and limited purpose, wholly-owned subsidiary of TRIP Holdings, issued $857.0 million in Secured Railcar Equipment Notes (the “TRIP Master Funding Secured Railcar Equipment Notes”). The proceeds from the TRIP Holdings Senior Secured Notes and the TRIP Master Funding Secured Railcar Equipment Notes were primarily used by TRIP Master Funding to purchase all of the railcar equipment owned by TRIP Rail Leasing LLC (“TRIP Leasing”) which, in turn, repaid the borrowings under its Warehouse Loan Agreement in full.

The TRIP Holdings Senior Secured Notes have a stated final maturity date of July 6, 2014 and bear interest at 8.00% payable quarterly with a yield to call interest rate of 12.00% for redemptions or other prepayments on or prior to January 15, 2013 and 15.00% for redemptions or other prepayments after such date. The TRIP Holdings Senior Secured Notes are secured, among other things, by a pledge of each equity investor’s ownership interest in TRIP Holdings and certain distributions made to TRIP Holdings from TRIP Master Funding and are non-recourse to Trinity, TILC, TRIP Master Funding, and the other equity investors in TRIP Holdings. Trinity purchased $112.0 million of the TRIP Holdings Senior Secured Notes in July 2011.

The TRIP Master Funding Secured Railcar Equipment Notes were issued pursuant to an Indenture, dated as of July 6, 2011 between TRIP Master Funding and Wilmington Trust Company, as indenture trustee, with a final maturity date in July 2041. The TRIP Master Funding Secured Railcar Equipment Notes consist of three classes of notes with the Class A-1a notes bearing interest at 4.37%, the Class A-1b notes bearing interest at Libor plus 2.50%

2010

| Year Ended December 31, 2012 | |||||||||||||||

| Revenues | Percent Change 2012 versus 2011 | ||||||||||||||

| External | Intersegment | Total | |||||||||||||

| ($ in millions) | |||||||||||||||

| Rail Group | $ | 1,512.1 | $ | 500.9 | $ | 2,013.0 | 57.9 | % | |||||||

| Construction Products Group | 461.2 | 22.5 | 483.7 | 6.7 | |||||||||||

| Inland Barge Group | 675.2 | — | 675.2 | 23.1 | |||||||||||

| Energy Equipment Group | 506.0 | 52.6 | 558.6 | 18.1 | |||||||||||

| Railcar Leasing and Management Services Group | 644.4 | 2.7 | 647.1 | 17.2 | |||||||||||

| All Other | 13.0 | 68.4 | 81.4 | 31.7 | |||||||||||

| Eliminations – Lease subsidiary | — | (485.9 | ) | (485.9 | ) | ||||||||||

| Eliminations – Other | — | (161.2 | ) | (161.2 | ) | ||||||||||

| Consolidated Total | $ | 3,811.9 | $ | — | $ | 3,811.9 | 29.7 | ||||||||

| Year Ended December 31, 2011 | |||||||||||||||

| Revenues | Percent Change 2011 versus 2010 | ||||||||||||||

| External | Intersegment | Total | |||||||||||||

| ($ in millions) | |||||||||||||||

| Rail Group | $ | 931.7 | $ | 343.0 | $ | 1,274.7 | 144.1 | % | |||||||

| Construction Products Group | 440.4 | 12.9 | 453.3 | 28.1 | |||||||||||

| Inland Barge Group | 548.5 | — | 548.5 | 29.9 | |||||||||||

| Energy Equipment Group | 454.8 | 18.0 | 472.8 | 12.7 | |||||||||||

| Railcar Leasing and Management Services Group | 551.4 | 0.6 | 552.0 | 18.8 | |||||||||||

| All Other | 11.5 | 50.3 | 61.8 | 27.4 | |||||||||||

| Eliminations – Lease subsidiary | — | (325.5 | ) | (325.5 | ) | ||||||||||

| Eliminations – Other | — | (99.3 | ) | (99.3 | ) | ||||||||||

| Consolidated Total | $ | 2,938.3 | $ | — | $ | 2,938.3 | 52.2 | ||||||||

| Year Ended December 31, 2010 | |||||||||||||||

| Revenues | |||||||||||||||

| External | Intersegment | Total | |||||||||||||

| ($ in millions) | |||||||||||||||

| Rail Group | $ | 289.7 | $ | 232.4 | $ | 522.1 | |||||||||

| Construction Products Group | 333.5 | 20.5 | 354.0 | ||||||||||||

| Inland Barge Group | 422.3 | — | 422.3 | ||||||||||||

| Energy Equipment Group | 408.5 | 11.1 | 419.6 | ||||||||||||

| Railcar Leasing and Management Services Group | 464.5 | — | 464.5 | ||||||||||||

| All Other | 12.2 | 36.3 | 48.5 | ||||||||||||

| Eliminations – Lease subsidiary | — | (216.8 | ) | (216.8 | ) | ||||||||||

| Eliminations – Other | — | (83.5 | ) | (83.5 | ) | ||||||||||

| Consolidated Total | $ | 1,930.7 | $ | — | $ | 1,930.7 | |||||||||

| Year Ended December 31, 2011 | ||||||||||||||||

| Revenues | Percent Change | |||||||||||||||

| External | Intersegment | Total | 2011 versus 2010 | |||||||||||||

| (in millions, except percents) | ||||||||||||||||

Rail Group | $ | 931.7 | $ | 343.0 | $ | 1,274.7 | 144.1 | % | ||||||||

Construction Products Group | 577.2 | 12.9 | 590.1 | 2.0 | % | |||||||||||

Inland Barge Group | 548.5 | — | 548.5 | 29.9 | % | |||||||||||

Energy Equipment Group | 454.8 | 18.0 | 472.8 | 12.7 | % | |||||||||||

Railcar Leasing and Management Services Group | 551.4. | 0.6 | 552.0 | 18.8 | % | |||||||||||

All Other | 11.5 | 50.3 | 61.8 | 27.4 | % | |||||||||||

Eliminations – lease subsidiary | — | (325.5 | ) | (325.5 | ) | |||||||||||

Eliminations – other | — | (99.3 | ) | (99.3 | ) | |||||||||||

|

|

|

|

|

| |||||||||||

Consolidated Total | $ | 3,075.1 | $ | — | $ | 3,075.1 | 42.7 | % | ||||||||

|

|

|

|

|

| |||||||||||

| Year Ended December 31, 2010 | ||||||||||||||||

| Revenues | Percent Change | |||||||||||||||

| External | Intersegment | Total | 2010 versus 2009 | |||||||||||||

| (in millions, except percents) | ||||||||||||||||

Rail Group | $ | 289.7 | $ | 232.4 | $ | 522.1 | (41.7 | )% | ||||||||

Construction Products Group | 558.3 | 20.5 | 578.8 | 7.5 | % | |||||||||||

Inland Barge Group | 422.3 | — | 422.3 | (19.9 | )% | |||||||||||

Energy Equipment Group | 408.5 | 11.1 | 419.6 | (17.7 | )% | |||||||||||

Railcar Leasing and Management Services Group | 464.5 | — | 464.5 | 25.5 | % | |||||||||||

All Other | 12.2 | 36.3 | 48.5 | 0.2 | % | |||||||||||

Eliminations – lease subsidiary | — | (216.8 | ) | (216.8 | ) | |||||||||||

Eliminations – other | — | (83.5 | ) | (83.5 | ) | |||||||||||

|

|

|

|

|

| |||||||||||

Consolidated Total | $ | 2,155.5 | $ | — | $ | 2,155.5 | (11.0 | )% | ||||||||

|

|

|

|

|

| |||||||||||

| Year Ended December 31, 2009 | ||||||||||||||||

| Revenues | ||||||||||||||||

| External | Intersegment | Total | ||||||||||||||

| (in millions) | ||||||||||||||||

Rail Group | $ | 485.2 | $ | 410.1 | $ | 895.3 | ||||||||||

Construction Products Group | 524.0 | 14.5 | 538.5 | |||||||||||||

Inland Barge Group | 527.3 | — | 527.3 | |||||||||||||

Energy Equipment Group | 502.2 | 7.8 | 510.0 | |||||||||||||

Railcar Leasing and Management Services Group | 370.2 | — | 370.2 | |||||||||||||

All Other | 12.0 | 36.4 | 48.4 | |||||||||||||

Eliminations – lease subsidiary | — | (391.6 | ) | (391.6 | ) | |||||||||||

Eliminations – other | — | (77.2 | ) | (77.2 | ) | |||||||||||

|

|

|

|

|

| |||||||||||

Consolidated Total | $ | 2,420.9 | $ | — | $ | 2,420.9 | ||||||||||

|

|

|

|

|

| |||||||||||

Our revenues for the yearyears ended December 31, 2012 and 2011 increased from the previous year primarily due to higher shipment volumes in our Rail and Inland Barge Groups while our Leasing Group experienced increased revenue primarily due to higher railcar sales from the lease fleet, higher rentalincreased revenues from lease fleet additions, and higher rental rates. Our revenues for the year ended December 31, 2010 decreased from 2009 primarily due to the impact

| Year Ended December 31, | ||||||||||||

| 2011 | 2010 | 2009 | ||||||||||

| (in millions) | ||||||||||||

Rail Group | $ | 77.3 | $ | 1.5 | $ | (355.9 | ) | |||||

Construction Products Group | 53.4 | 47.4 | 32.6 | |||||||||

Inland Barge Group | 106.4 | 69.0 | 125.2 | |||||||||

Energy Equipment Group | 8.9 | 35.1 | 73.8 | |||||||||

Railcar Leasing and Management Services Group | 254.5 | 207.0 | 149.0 | |||||||||

All Other | (3.8 | ) | (11.4 | ) | 0.8 | |||||||

Corporate | (43.6 | ) | (33.8 | ) | (30.8 | ) | ||||||

Eliminations – lease subsidiary | (28.3 | ) | (8.4 | ) | (22.6 | ) | ||||||

Eliminations – other | 0.5 | (2.6 | ) | (3.0 | ) | |||||||

|

|

|

|

|

| |||||||

Consolidated Total | $ | 425.3 | $ | 303.8 | $ | (30.9 | ) | |||||

|

|

|

|

|

| |||||||

| Year Ended December 31, | |||||||||||

| 2012 | 2011 | 2010 | |||||||||

| (in millions) | |||||||||||

| Rail Group | $ | 199.0 | $ | 77.3 | $ | 1.5 | |||||

| Construction Products Group | 44.8 | 54.9 | 37.8 | ||||||||

| Inland Barge Group | 124.7 | 106.4 | 69.0 | ||||||||

| Energy Equipment Group | 18.2 | 8.9 | 35.1 | ||||||||

| Railcar Leasing and Management Services Group | 300.9 | 254.5 | 207.0 | ||||||||

| All Other | (10.2 | ) | (3.8 | ) | (11.4 | ) | |||||

| Corporate | (51.5 | ) | (43.6 | ) | (33.8 | ) | |||||

| Eliminations – lease subsidiary | (50.8 | ) | (28.3 | ) | (8.4 | ) | |||||

| Eliminations – other | (0.3 | ) | 0.5 | (2.6 | ) | ||||||

| Consolidated Total | $ | 574.8 | $ | 426.8 | $ | 294.2 | |||||

Our operating profit for the year ended December 31,

| Year Ended December 31, | ||||||||||||

| 2011 | 2010 | 2009 | ||||||||||

| (in millions) | ||||||||||||

Interest income | $ | (1.5 | ) | $ | (1.4 | ) | $ | (1.7 | ) | |||

Interest expense | 185.3 | 182.1 | 123.2 | |||||||||

Other, net | 4.0 | 6.8 | (5.3 | ) | ||||||||

|

|

|

|

|

| |||||||

Total | $ | 187.8 | $ | 187.5 | $ | 116.2 | ||||||

|

|

|

|

|

| |||||||

| Year Ended December 31, | |||||||||||

| 2012 | 2011 | 2010 | |||||||||

| (in millions) | |||||||||||

| Interest income | $ | (1.5 | ) | $ | (1.5 | ) | $ | (1.4 | ) | ||

| Interest expense | 194.7 | 185.3 | 182.1 | ||||||||

| Other, net | (4.3 | ) | 4.0 | 6.8 | |||||||

| Consolidated Total | $ | 188.9 | $ | 187.8 | $ | 187.5 | |||||

| Year Ended December 31, | ||||||||||||

2011 | 2010 | 2009 | ||||||||||

Statutory rate | 35.0 | % | 35.0 | % | 35.0 | % | ||||||

State taxes | 2.1 | 3.3 | 1.9 | |||||||||

Impairment of goodwill | — | — | (23.7 | ) | ||||||||

Changes in valuation allowances | — | — | (6.5 | ) | ||||||||

Tax settlements | — | 4.4 | — | |||||||||

Changes in tax reserves | — | (9.6 | ) | — | ||||||||

Other, net | 1.6 | 2.0 | (0.3 | ) | ||||||||

|

|

|

|

|

| |||||||

Effective rate | 38.7 | % | 35.1 | % | 6.4 | % | ||||||

|

|

|

|

|

| |||||||

| Year Ended December 31, | ||||||||

| 2012 | 2011 | 2010 | ||||||

| Statutory rate | 35.0 | % | 35.0 | % | 35.0 | % | ||

| State taxes | 2.0 | 2.1 | 3.4 | |||||

| Tax settlements | (0.6 | ) | — | 4.8 | ||||

| Changes in tax reserves | (1.4 | ) | 0.4 | (10.7 | ) | |||

| Other, net | (0.3 | ) | 1.1 | 2.5 | ||||

| Effective rate | 34.7 | % | 38.6 | % | 35.0 | % | ||

The current provision for income taxes of $30.9$31.7 million exceedsexceeded expected cash taxes of $12.1 million related to 2011 income due to additional accruals for uncertain tax positions, refunds of excess payments from prior years, and prior year true ups.

| Year Ended December 31, | Percent Change | |||||||||||||||||||

| 2011 | 2010 | 2009 | 2011 versus 2010 | 2010 versus 2009 | ||||||||||||||||

| ($ in millions) | ||||||||||||||||||||

Revenues: | ||||||||||||||||||||

Rail | $ | 1,105.5 | $ | 391.9 | $ | 776.8 | 182.1 | % | (49.5 | )% | ||||||||||

Components | 169.2 | 130.2 | 118.5 | 30.0 | % | 9.9 | % | |||||||||||||

|

|

|

|

|

| |||||||||||||||

Total revenues | $ | 1,274.7 | $ | 522.1 | $ | 895.3 | 144.1 | % | (41.7 | )% | ||||||||||

Operating profit (loss) | $ | 77.3 | $ | 1.5 | $ | (355.9 | ) | |||||||||||||

Operating profit (loss) margin | 6.1 | % | 0.3 | % | (39.8 | )% | ||||||||||||||

Railcar shipments in 2011 increased by 9,315 railcars to approximately 14,065 railcars when compared with 2010. Railcars shipped in 2010 and 2009 were approximately 4,750 and 9,100 railcars, respectively.

| Year Ended December 31, | Percent Change | ||||||||||||||||

| 2012 | 2011 | 2010 | 2012 versus 2011 | 2011 versus 2010 | |||||||||||||

| ($ in millions) | |||||||||||||||||

| Revenues: | |||||||||||||||||

| Rail | $ | 1,850.5 | $ | 1,105.5 | $ | 391.9 | 67.4 | % | 182.1 | % | |||||||

| Components | 162.5 | 169.2 | 130.2 | (4.0 | ) | 30.0 | |||||||||||

| Total revenues | 2,013.0 | 1,274.7 | 522.1 | 57.9 | 144.1 | ||||||||||||

| Operating costs: | |||||||||||||||||

| Cost of revenues | 1,773.9 | 1,167.3 | 489.3 | 52.0 | 138.6 | ||||||||||||

| Selling, engineering, and administrative costs | 40.1 | 34.0 | 31.3 | 17.9 | 8.6 | ||||||||||||

| Property disposition (gains)/losses | — | (3.9 | ) | — | |||||||||||||

| Operating profit | $ | 199.0 | $ | 77.3 | $ | 1.5 | |||||||||||

| Operating profit margin | 9.9 | % | 6.1 | % | 0.3 | % | |||||||||||

| Year Ended December 31, | ||||||||||||

| 2011 | 2010 | 2009 | ||||||||||

| (in millions, except railcars) | ||||||||||||

External Customers | $ | 1,973.2 | $ | 346.6 | $ | 75.6 | ||||||

Leasing Group | 621.9 | 111.0 | 119.8 | |||||||||

|

|

|

|

|

| |||||||

Total | $ | 2,595.1 | $ | 457.6 | $ | 195.4 | ||||||

|

|

|

|

|

| |||||||

Number of railcars | 29,000 | 5,960 | 2,320 | |||||||||

For

| Year Ended December 31, | |||||||||||

| 2012 | 2011 | 2010 | |||||||||

| (in millions) | |||||||||||

| External Customers | $ | 2,867.5 | $ | 1,973.2 | $ | 346.6 | |||||

| Leasing Group | 834.7 | 621.9 | 111.0 | ||||||||

| Total | $ | 3,702.2 | $ | 2,595.1 | $ | 457.6 | |||||

| Year Ended December 31, | ||||||||

| 2012 | 2011 | 2010 | ||||||

| Beginning balance | 29,000 | 5,960 | 2,320 | |||||

| Orders received | 22,350 | 37,105 | 8,390 | |||||

| Shipments | (19,360 | ) | (14,065 | ) | (4,750 | ) | ||

| Ending balance | 31,990 | 29,000 | 5,960 | |||||

Operating profit for the Rail Group increased $75.8 million for the year ended December 31, 2011 compared to the same period last year. This increase was primarily due to significantly higher volume of railcars delivered during the year. Operating loss for the Rail Group decreased $357.4 million for the year ended December 31, 2010 compared to the prior year. This decrease was primarily due to a $325.0 million goodwill impairment charge during the quarter ended June 30, 2009. The effect of significantly reduced railcar shipments on operating profit during 2010 was partially offset by a reduction in operating expenses.

2017.

2012 | 55,200 | |||

2013 | 59,600 | |||

2014 | 62,100 | |||

2015 | 61,600 | |||

2016 | 60,000 |

TILC

| 2013 | 53,000 | |

| 2014 | 62,200 | |

| 2015 | 63,100 | |

| 2016 | 57,700 | |

| 2017 | 55,300 | |

| Year Ended December 31, | Percent Change | ||||||||||||||||

| 2012 | 2011 | 2010 | 2012 versus 2011 | 2011 versus 2010 | |||||||||||||

| ($ in millions) | |||||||||||||||||

| Revenues: | |||||||||||||||||

| Highway Products | $ | 376.1 | $ | 377.0 | $ | 312.9 | (0.2 | )% | 20.5 | % | |||||||

| Aggregates | 65.1 | 45.5 | 32.1 | 43.1 | 41.7 | ||||||||||||

| Other | 42.5 | 30.8 | 9.0 | * | * | ||||||||||||

| Total revenues | 483.7 | 453.3 | 354.0 | 6.7 | 28.1 | ||||||||||||

| Operating costs: | |||||||||||||||||

| Cost of revenues | 387.0 | 357.9 | 280.8 | 8.1 | 27.5 | ||||||||||||

| Selling, engineering, and administrative costs | 52.0 | 40.8 | 36.1 | 27.5 | 13.0 | ||||||||||||

| Property disposition (gains)/losses | (0.1 | ) | (0.3 | ) | (0.7 | ) | |||||||||||

| Operating profit | $ | 44.8 | $ | 54.9 | $ | 37.8 | |||||||||||

| Operating profit margin | 9.3 | % | 12.1 | % | 10.7 | % | |||||||||||

| Year Ended December 31, | Percent Change | |||||||||||||||||||

| 2011 | 2010 | 2009 | 2011 versus 2010 | 2010 versus 2009 | ||||||||||||||||

| ($ in millions) | ||||||||||||||||||||

Revenues: | ||||||||||||||||||||

Concrete and Aggregates | $ | 182.3 | $ | 256.9 | $ | 291.4 | (29.0 | )% | (11.8 | )% | ||||||||||

Highway Products | 377.0 | 312.9 | 238.0 | 20.5 | % | 31.5 | % | |||||||||||||

Other | 30.8 | 9.0 | 9.1 | * | (1.1 | )% | ||||||||||||||

|

|

|

|

|

| |||||||||||||||

Total revenues | $ | 590.1 | $ | 578.8 | $ | 538.5 | 2.0 | % | 7.5 | % | ||||||||||

Operating profit | $ | 53.4 | $ | 47.4 | $ | 32.6 | ||||||||||||||

Operating profit margin | 9.0 | % | 8.2 | % | 6.1 | % | ||||||||||||||

*not meaningful

| Year Ended December 31, | Percent Change | ||||||||||||||||

| 2012 | 2011 | 2010 | 2012 versus 2011 | 2011 versus 2010 | |||||||||||||

| ($ in millions) | |||||||||||||||||

| Revenues | $ | 675.2 | $ | 548.5 | $ | 422.3 | 23.1 | % | 29.9 | % | |||||||

| Operating costs: | |||||||||||||||||

| Cost of revenues | 538.9 | 445.0 | 350.3 | 21.1 | 27.0 | ||||||||||||

| Selling, engineering, and administrative costs | 15.4 | 14.7 | 12.7 | 4.8 | 15.7 | ||||||||||||

| Property disposition (gains)/losses | (3.8 | ) | (17.6 | ) | (9.7 | ) | |||||||||||

| Operating profit | $ | 124.7 | $ | 106.4 | $ | 69.0 | |||||||||||

| Operating profit margin | 18.5 | % | 19.4 | % | 16.3 | % | |||||||||||

Operating profitequipment that were under lease to third-party customers.

Inland Barge Group

| Year Ended December 31, | Percent Change | |||||||||||||||||||

| 2011 | 2010 | 2009 | 2011 versus 2010 | 2010 versus 2009 | ||||||||||||||||

| ($ in millions) | ||||||||||||||||||||

Revenues | $ | 548.5 | $ | 422.3 | $ | 527.3 | 29.9 | % | (19.9 | )% | ||||||||||

Operating profit | $ | 106.4 | $ | 69.0 | $ | 125.2 | ||||||||||||||

Operating profit margin | 19.4 | % | 16.3 | % | 23.7 | % | ||||||||||||||

Revenues and operating profit increased for the year ended December 31, 2011 compared to the prior year2010 due to higher volumes of tank barges and a change in the mix of tank barge types. In addition,As with 2012, we experienced improved efficiencies related to higher tank barge production in 2011 as compared with 2010.

| Impact to operating profit as a result of the floods Benefit (Cost) | ||||||||

| Year Ended December 31, | ||||||||

| 2011 | 2010 | |||||||

(in millions) | ||||||||

Tennessee flood – May 2010 | ||||||||

Costs, net of insurance advances related to damages and lost productivity | $ | — | $ | (4.6 | ) | |||

Insurance proceeds related to business interruption | 6.5 | — | ||||||

Gain on disposition of damaged property, plant, and equipment | 0.6 | 9.7 | ||||||

|

|

|

| |||||

| $ | 7.1 | $ | 5.1 | |||||

Missouri flood – May 2011 | ||||||||

Costs, net of insurance advances related to damages and lost productivity | $ | (8.6 | ) | $ | — | |||

Gain on disposition of damaged property, plant, and equipment | 17.0 | — | ||||||

|

|

|

| |||||

| 8.4 | — | |||||||

|

|

|

| |||||

Combined net effect of both floods | $ | 15.5 | $ | 5.1 | ||||

Excluding the net $5.1 million increase in operating profit in 2010 resulting from the effectsfollows:

Impact to Operating Profit as a Result of Floods Benefit (Cost) | |||||||||||

| Year Ended December 31, | |||||||||||

| 2012 | 2011 | 2010 | |||||||||

| (in millions) | |||||||||||

| Tennessee flood - May 2010 | |||||||||||

| Costs, net of insurance advances related to damages and lost productivity | $ | — | $ | — | $ | (4.6 | ) | ||||

| Insurance proceeds related to business interruption | — | 6.5 | — | ||||||||

| Gain on disposition of damaged property, plant, and equipment | — | 0.6 | 9.7 | ||||||||

| — | 7.1 | 5.1 | |||||||||

| Missouri flood - May 2011 | |||||||||||

| Costs, net of insurance advances related to damages and lost productivity | — | (8.6 | ) | — | |||||||

| Gain on disposition of damaged property, plant, and equipment | 0.4 | 17.0 | — | ||||||||

| 0.4 | 8.4 | — | |||||||||

| Combined net effect of both floods | $ | 0.4 | $ | 15.5 | $ | 5.1 | |||||

| Year Ended December 31, | Percent Change | |||||||||||||||||||

| 2011 | 2010 | 2009 | 2011 versus 2010 | 2010 versus 2009 | ||||||||||||||||

| ($ in millions) | ||||||||||||||||||||

Revenues: | ||||||||||||||||||||

Structural wind towers | $ | 245.2 | $ | 252.1 | $ | 358.3 | (2.7 | )% | (29.6 | )% | ||||||||||

Other | 227.6 | 167.5 | 151.7 | 35.9 | % | 10.4 | % | |||||||||||||

|

|

|

|

|

| |||||||||||||||

Total revenues | $ | 472.8 | $ | 419.6 | $ | 510.0 | 12.7 | % | (17.7 | )% | ||||||||||

Operating profit | $ | 8.9 | $ | 35.1 | $ | 73.8 | ||||||||||||||

Operating profit margin | 1.9 | % | 8.4 | % | 14.5 | % | ||||||||||||||

| Year Ended December 31, | Percent Change | ||||||||||||||||

| 2012 | 2011 | 2010 | 2012 versus 2011 | 2011 versus 2010 | |||||||||||||

| ($ in millions) | |||||||||||||||||

| Revenues: | |||||||||||||||||

| Structural wind towers | $ | 262.4 | $ | 245.2 | $ | 252.1 | 7.0 | % | (2.7 | )% | |||||||

| Other | 296.2 | 227.6 | 167.5 | 30.1 | 35.9 | ||||||||||||

| Total revenues | 558.6 | 472.8 | 419.6 | 18.1 | 12.7 | ||||||||||||

| Operating costs: | |||||||||||||||||

| Cost of revenues | 510.3 | 432.1 | 360.7 | 18.1 | 19.8 | ||||||||||||

| Selling, engineering, and administrative costs | 30.8 | 31.8 | 25.9 | (3.1 | ) | 22.8 | |||||||||||

| Property disposition (gains)/losses | (0.7 | ) | — | (2.1 | ) | ||||||||||||

| Operating profit | $ | 18.2 | $ | 8.9 | $ | 35.1 | |||||||||||

| Operating profit margin | 3.3 | % | 1.9 | % | 8.4 | % | |||||||||||

Revenues and operating profit decreased for the year ended towers.

wind towers shipped. As of December 31, 2011,2012

manufacture of towers.

| Year Ended December 31, | Percentage Change | ||||||||||||||||

| 2012 | 2011 | 2010 | 2012 versus 2011 | 2011 versus 2010 | |||||||||||||

| ($ in millions) | |||||||||||||||||

| Revenues: | |||||||||||||||||

| Wholly owned subsidiaries: | |||||||||||||||||

| Leasing and management | $ | 409.8 | $ | 375.1 | $ | 345.4 | 9.3 | % | 8.6 | % | |||||||

| Railcar sales | 118.6 | 59.4 | 3.1 | * | * | ||||||||||||

| 528.4 | 434.5 | 348.5 | 21.6 | 24.7 | |||||||||||||

| TRIP Holdings: | |||||||||||||||||

| Leasing and management | 118.7 | 117.5 | 116.0 | 1.0 | 1.3 | ||||||||||||

| Railcar sales | — | — | — | — | — | ||||||||||||

| 118.7 | 117.5 | 116.0 | 1.0 | 1.3 | |||||||||||||

| Total revenues | $ | 647.1 | $ | 552.0 | $ | 464.5 | 17.2 | 18.8 | |||||||||

| Operating Profit: | |||||||||||||||||

| Wholly-owned subsidiaries: | |||||||||||||||||

| Leasing and management | $ | 175.2 | $ | 156.3 | $ | 131.7 | |||||||||||

| Railcar sales: | |||||||||||||||||

| Railcars owned one year or less at the time of sale | 24.8 | 13.2 | 0.2 | ||||||||||||||

| Railcars owned more than one year at the time of sale | 32.8 | 11.8 | 6.6 | ||||||||||||||

| 232.8 | 181.3 | 138.5 | |||||||||||||||

| TRIP Holdings: | |||||||||||||||||

| Leasing and management | 67.4 | 68.8 | 68.5 | ||||||||||||||

| Railcar sales: | |||||||||||||||||

| Railcars owned one year or less at the time of sale | — | — | — | ||||||||||||||

| Railcars owned more than one year at the time of sale | 0.7 | 4.4 | — | ||||||||||||||

| 68.1 | 73.2 | 68.5 | |||||||||||||||

| Total operating profit | $ | 300.9 | $ | 254.5 | $ | 207.0 | |||||||||||

| Operating profit margin: | |||||||||||||||||

| Leasing and management | 45.9 | % | 45.7 | % | 43.4 | % | |||||||||||

| Railcar sales | * | * | * | ||||||||||||||

| Total operating profit margin | 46.5 | 46.1 | 44.6 | ||||||||||||||

Depreciation, interest, and rent expense(1): | |||||||||||||||||

| Depreciation expense | $ | 120.5 | $ | 115.7 | $ | 112.6 | |||||||||||

| Rent expense | $ | 50.9 | $ | 48.6 | $ | 48.6 | |||||||||||

| Interest expense: | |||||||||||||||||

| Wholly-owned subsidiaries | $ | 101.2 | $ | 101.3 | $ | 91.7 | |||||||||||

| TRIP Holdings: | |||||||||||||||||

| External | 60.0 | 53.1 | 46.9 | ||||||||||||||

| Intercompany | 13.1 | 6.4 | — | ||||||||||||||

| 73.1 | 59.5 | 46.9 | |||||||||||||||

| Total interest expense | $ | 174.3 | $ | 160.8 | $ | 138.6 | |||||||||||

| Fleet utilization: | |||||||||||||||||

| Wholly-owned subsidiaries | 98.4 | % | 99.3 | % | 99.3 | % | |||||||||||

| TRIP Holdings | 99.2 | % | 99.9 | % | 99.9 | % | |||||||||||

| Total fleet | 98.6 | % | 99.5 | % | 99.4 | % | |||||||||||

| Year Ended December 31, | Percent Change | |||||||||||||||||||

| 2011 | 2010 | 2009 | 2011 versus 2010 | 2010 versus 2009 | ||||||||||||||||

| ($ in millions) | ||||||||||||||||||||

Revenues: | ||||||||||||||||||||

Wholly-owned subsidiaries: | ||||||||||||||||||||

Leasing and management | $ | 375.1 | $ | 345.4 | $ | 329.3 | 8.6 | % | 4.9 | % | ||||||||||

Railcar sales(1) | 59.4 | 3.1 | 40.9 | * | * | |||||||||||||||

|

|

|

|

|

| |||||||||||||||

| 434.5 | 348.5 | 370.2 | 24.7 | % | (5.9 | )% | ||||||||||||||

TRIP Holdings: | ||||||||||||||||||||

Leasing and management | 117.5 | 116.0 | — | 1.3 | % | — | ||||||||||||||

Railcar sales(1) | — | — | — | — | — | |||||||||||||||

|

|

|

|

|

| |||||||||||||||

| 117.5 | 116.0 | — | 1.3 | % | — | |||||||||||||||

|

|

|

|

|

| |||||||||||||||

Total revenues | $ | 552.0 | $ | 464.5 | $ | 370.2 | 18.8 | % | 25.5 | % | ||||||||||

Operating profit: | ||||||||||||||||||||

Wholly-owned subsidiaries: | ||||||||||||||||||||

Leasing and management | $ | 156.3 | $ | 131.7 | $ | 128.5 | ||||||||||||||

Railcar sales(1): | ||||||||||||||||||||

Railcars owned one year or less at the time of sale | 13.2 | 0.2 | 2.1 | |||||||||||||||||

Railcars owned more than one year at the time of sale | 11.8 | 6.6 | 18.4 | |||||||||||||||||

|

|

|

|

|

| |||||||||||||||

| 181.3 | 138.5 | 149.0 | ||||||||||||||||||

TRIP Holdings: | ||||||||||||||||||||

Leasing and management | 68.8 | 68.5 | — | |||||||||||||||||

Railcar sales(1): | ||||||||||||||||||||

Railcars owned one year or less at the time of sale | — | — | — | |||||||||||||||||

Railcars owned more than one year at the time of sale | 4.4 | — | — | |||||||||||||||||

|

|

|

|

|

| |||||||||||||||

| 73.2 | 68.5 | — | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||

Total operating profit | $ | 254.5 | $ | 207.0 | $ | 149.0 | ||||||||||||||

Operating profit margin: | ||||||||||||||||||||

Leasing and management | 45.7 | % | 43.4 | % | 39.0 | % | ||||||||||||||

Railcar sales | * | * | * | |||||||||||||||||

Total operating profit margin | 46.1 | % | 44.6 | % | 40.2 | % | ||||||||||||||

Fleet utilization: | ||||||||||||||||||||

Wholly-owned subsidiaries | 99.3 | % | 99.3 | % | 97.8 | % | ||||||||||||||

TRIP Holdings | 99.9 | % | 99.9 | % | — | |||||||||||||||

Total fleet | 99.5 | % | 99.4 | % | 97.8 | % | ||||||||||||||

Total revenues increased for the year ended December 31, 20112012 compared to the prior year primarily due to increased railcar sales from the lease fleet, increased revenues related to additions to the lease fleet and higher rental rates. Total revenues increased for the year ended December 31, 2011 compared to 2010 primarily due to increased railcar sales from the lease fleet, as well as rental revenues related to additions to the lease fleet and higher rental rates. Total revenues decreased

revenues related to additions2012 when compared to the lease fleet of our wholly-owned subsidiaries. Additionally,prior year. Interest expense increased during 2012 compared with 2011 due to the adoption of an accounting pronouncement, the Leasing Group's results of operations for the years ended December 31, 2011 and December 31, 2010 include TRIP Holdings and its subsidiaries. See Notes 1 and 6refinancing of the Notes to Consolidated Financial Statements.

TRIP warehouse loan in 2011. Operating profit increased for the year ended

December 31, 2011 compared to2011.

| No. of cars | Average age | Average remaining lease term | ||||||||||

Wholly-owned subsidiaries | 54,595 | 6.6 | 3.5 | |||||||||

TRIP Holdings | 14,350 | 4.3 | 3.1 | |||||||||

|

| |||||||||||

Total fleet | 68,945 | 6.1 | 3.4 | |||||||||

| No. of cars | Average age | Average remaining lease term | ||||||

| Wholly-owned subsidiaries | 57,000 | 7.1 | 3.3 | |||||

| TRIP Holdings | 14,455 | 5.3 | 3.1 | |||||

| Total fleet | 71,455 | 6.7 | 3.3 | |||||

| Year Ended December 31, | Percent Change | |||||||||||||||||||

| 2011 | 2010 | 2009 | 2011 versus 2010 | 2010 versus 2009 | ||||||||||||||||

| ($ in millions) | ||||||||||||||||||||

Revenues | $ | 61.8 | $ | 48.5 | $ | 48.4 | 27.4 | % | 0.2 | % | ||||||||||

Operating profit (loss) | $ | (3.8 | ) | $ | (11.4 | ) | $ | 0.8 | ||||||||||||

| Year Ended December 31, | Percent Change | ||||||||||||||||

| 2012 | 2011 | 2010 | 2012 versus 2011 | 2011 versus 2010 | |||||||||||||

| ($ in millions) | |||||||||||||||||

| Revenues | $ | 81.4 | $ | 61.8 | $ | 48.5 | 31.7 | % | 27.4 | % | |||||||

| Operating costs: | |||||||||||||||||

| Cost of revenues | 86.8 | 61.8 | 55.6 | 40.5 | 11.2 | ||||||||||||

| Selling, engineering, and administrative costs | 5.2 | 5.8 | 5.3 | (10.3 | ) | 9.4 | |||||||||||

| Property disposition (gains)/losses | (0.4 | ) | (2.0 | ) | (1.0 | ) | |||||||||||

| Operating loss | $ | (10.2 | ) | $ | (3.8 | ) | $ | (11.4 | ) | ||||||||

sales volume.

| Year Ended December 31, | Percent Change | ||||||||||||||||

| 2012 | 2011 | 2010 | 2012 versus 2011 | 2011 versus 2010 | |||||||||||||

| ($ in millions) | |||||||||||||||||

| Operating costs | $ | (51.5 | ) | $ | (43.6 | ) | $ | (33.8 | ) | 18.1 | % | 29.0 | % | ||||

| Year Ended December 31, | Percent Change | |||||||||||||||||||

| 2011 | 2010 | 2009 | 2011 versus 2010 | 2010 versus 2009 | ||||||||||||||||

| ($ in millions) | ||||||||||||||||||||

Operating costs | $ | 43.6 | $ | 33.8 | $ | 30.8 | 29.0 | % | 9.7 | % | ||||||||||

The increase in operating costs for the yearyears ended December 31, 2012 and 2011 compared to 2010with the prior year is due to higher incentive and deferred compensation costs. Thecosts and an increase in operating costs for the year ended December 31, 2010 compared to 2009 is due to additional costs from the acquisitioncertain legal reserves.

| Year Ended December 31, | ||||||||||||

| 2011 | 2010 | 2009 | ||||||||||

| (in millions) | ||||||||||||

Total cash provided by (required by) | ||||||||||||

Operating activities | $ | 104.3 | $ | 170.5 | $ | 707.3 | ||||||

Investing activities | (85.0 | ) | (308.2 | ) | (187.4 | ) | ||||||

Financing activities | (22.2 | ) | (120.1 | ) | (69.9 | ) | ||||||

|

|

|

|

|

| |||||||

Net increase (decrease) in cash and cash equivalents | $ | (2.9 | ) | $ | (257.8 | ) | $ | 450.0 | ||||

|

|

|

|

|

| |||||||

2011

| Year Ended December 31, | |||||||||||

| 2012 | 2011 | 2010 | |||||||||

| (in millions) | |||||||||||

| Total cash provided by (required by): | |||||||||||

| Operating activities | $ | 527.4 | $ | 110.9 | $ | 170.5 | |||||

| Investing activities | (311.4 | ) | (85.0 | ) | (308.2 | ) | |||||

| Financing activities | 5.9 | (28.8 | ) | (120.1 | ) | ||||||

| Net increase (decrease) in cash and cash equivalents | $ | 221.9 | $ | (2.9 | ) | $ | (257.8 | ) | |||

2011

2011.

TILC warehouse loan facility. Debt retirements during 2010 totaled $363.9 million including $40.0 million in debt assumed as a result of the Quixote acquisition. We also purchased an additional equity interest in TRIP Holdings from one of its other investors for $28.6 million in the comparable prior year period. Restricted cash increased by $33.2 million during 2011. We intend to use our cash and committed credit facilities to fund the operations, expansions, and growth initiatives of the Company.

2010 compared with 2009

Operating Activities. Net cash provided by the operating activities of continuing operations for the year ended December 31, 2010 was $170.5 million compared to $707.3 million of net cash provided by the operating activities of continuing operations for the same period in 2009.

Accounts receivables at December 31, 2010 increased by $62.2 million or 39% since December 31, 2009 due to higher shipping volumes at year end primarily in our Rail and Energy Equipment Groups. Raw materials inventory at December 31, 2010 increased by $72.3 million or 75% since December 31, 2009 primarily attributable to higher levels in our Rail and Energy Equipment Groups required to meet production demands. Finished goods inventory decreased slightly by $9.3 million since December 31, 2009 primarily due to lower finished goods inventory in our Rail Group. Accounts payable increased by $53.4 million or 70% since December 31, 2009 primarily due to higher production activity while accrued liabilities decreased by $59.5 million due to the normal settlement of certain items during the year.

Investing Activities. Net cash required by investing activities of continuing operations for the year ended December 31, 2010 was $308.2 million compared to $187.4 million for the same period in 2009. Capital expenditures for the year ended December 31, 2010 were $254.8 million, of which $213.8 million were for net additions to the lease fleet and $12.0 million were for replacement of flood-damaged property. This compares to $390.4 million of capital expenditures for the same period in 2009, of which $343.0 million were for net additions to the lease fleet. Proceeds from the sale of property, plant, and equipment and other assets were $84.5 million for the year ended December 31, 2010, comprised primarily of the sale of assets in our Construction Products Group for $30.8 million, railcar sales from the lease fleet totaling $33.6 million, and proceeds from the disposition of flood-damaged property, plant and equipment of $12.0 million. This compares to $273.0 million for the same period in 2009 comprised primarily of railcar sales from the lease fleet, which included $144.4 million to TRIP Leasing, and the sale of non-operating assets. Cash required related to acquisitions amounted to $49.9 million, excluding $17.1 million in cash balances acquired from Quixote.

Financing Activities. Net cash required by financing activities during the years ended December 31, 2010 and 2009 was $120.1 million and $69.9 million, respectively. As stated previously, in 2010, TRL 2010 issued $369.2 million in aggregate principal amount of Secured Railcar Equipment Notes which are non-recourse to Trinity. A portion of the proceeds from the TRL 2010 financing was used to retire, in full, our 6.5% Senior Notes due March 2014 and repay a portion of our borrowings under our TILC warehouse loan facility. In addition,Debt retirements during the year ended December 31, 2010 we retired $40.0 totaled $363.5 million including $40.0 million in debt assumed as a result of the Quixote acquisition. We also purchased an additional equity interest in TRIP Holdings from one of its other investors for $28.6 million.$

28.6 million in the comparable prior year period. Restricted cash increased by $33.2 million during 2011.

As of December 31, 2011, peak borrowings for the year of $308.52012

On July 6, 2011, TRIP Holdings

The TRIP Master Funding Secured Railcar Equipment Notes were issued pursuant to an Indenture, dated July 6, 2011 between TRIP Master Funding and Wilmington Trust Company, as indenture trustee, with astated final maturity date in July 2041.of

On December 9, 2010,TRL

further increases.

Statements for information about the investment in TRIP Holdings.

Statements for information about off balance sheet arrangements.

2012

. See Note 11 of the Notes to Consolidated Financial Statements for a description of the Company's debt instruments.| Included in accompanying balance sheet at December 31, 2011 | ||||||||||||||||||||

| Notional Amount | Interest Rate(1) | Liability | AOCL —loss/ (income) | Noncontrolling Interest | ||||||||||||||||

| (in millions, except %) | ||||||||||||||||||||

Interest rate locks: | ||||||||||||||||||||

2005-2006 | $ | 200.0 | 4.87 | % | — | $ | (2.3 | ) | — | |||||||||||

2006-2007 | $ | 370.0 | 5.34 | % | — | $ | 10.6 | — | ||||||||||||

TRIP Holdings(2) | $ | 788.5 | 3.60 | % | — | $ | 23.4 | $ | 17.5 | |||||||||||

Interest rate swaps: | ||||||||||||||||||||

TRIP Rail Master Funding secured railcar equipment notes | $ | 89.5 | 2.62 | % | $ | 4.8 | $ | 2.7 | $ | 2.0 | ||||||||||

2008 debt issuance | $ | 474.7 | 4.13 | % | $ | 48.9 | $ | 46.7 | — | |||||||||||

| Included in accompanying balance sheet at December 31, 2012 | ||||||||||||||||||

Notional Amount | Interest Rate(1) | Liability | AOCL – loss/ (income) | Noncontrolling Interest | ||||||||||||||

| (in millions, except %) | ||||||||||||||||||

| Expired hedges: | ||||||||||||||||||

| 2006 secured railcar equipment notes | $ | 200.0 | 4.87 | % | $ | — | $ | (1.9 | ) | $ | — | |||||||

| Promissory notes | $ | 370.0 | 5.34 | % | $ | — | $ | 7.2 | $ | — | ||||||||

| TRIP Holdings | $ | 788.5 | 3.60 | % | $ | — | $ | 19.9 | $ | 14.9 | ||||||||

| Open hedges: | ||||||||||||||||||

| TRIP Master Funding secured railcar equipment notes | $ | 78.4 | 2.62 | % | $ | 5.2 | $ | 2.9 | $ | 2.2 | ||||||||

| Promissory notes | $ | 443.8 | 4.13 | % | $ | 37.6 | $ | 34.9 | $ | — | ||||||||

(1) | Weighted average fixed interest rate |

| Effect on interest expense-increase/(decrease) | |||||||||||||||

| Year Ended December 31, | Expected effect during next twelve months(1) | ||||||||||||||

| 2012 | 2011 | 2010 | |||||||||||||

| (in millions) | |||||||||||||||

| Expired hedges: | |||||||||||||||

| 2006 secured railcar equipment notes | $ | (0.3 | ) | $ | (0.4 | ) | $ | (0.4 | ) | $ | (0.3 | ) | |||

| Promissory notes | $ | 3.3 | $ | 3.5 | $ | 3.8 | $ | 3.1 | |||||||

| TRIP Holdings | $ | 6.0 | $ | 17.4 | $ | 29.3 | $ | 5.6 | |||||||

Open hedges(2): | |||||||||||||||

| TILC Warehouse | $ | — | $ | — | $ | 0.5 | $ | — | |||||||

| TRIP Master Funding secured railcar equipment notes | $ | 2.0 | $ | 1.1 | $ | — | $ | 1.8 | |||||||

| Promissory notes | $ | 18.4 | $ | 19.6 | $ | 19.7 | $ | 16.7 | |||||||

|

| Effect on interest expense — increase/(decrease) | ||||||||||||||||

| Expected effect during next twelve months(1) | ||||||||||||||||

| Year Ended December 31, | ||||||||||||||||

| 2011 | 2010 | 2009 | ||||||||||||||

| (in millions) | ||||||||||||||||

Interest rate locks: | ||||||||||||||||

2005-2006 | $ | (0.4 | ) | $ | (0.4 | ) | $ | (0.4 | ) | $ | (0.3 | ) | ||||

2006-2007 | $ | 3.5 | $ | 3.8 | $ | 4.0 | $ | 3.4 | ||||||||

TRIP Holdings(2) | $ | 17.4 | $ | 29.3 | — | $ | 6.0 | |||||||||

Interest rate swaps: | ||||||||||||||||

TILC warehouse | — | $ | 0.5 | $ | 2.9 | — | ||||||||||

TRIP Rail Master Funding secured railcar equipment notes | $ | 1.1 | — | — | $ | 1.7 | ||||||||||

2008 debt issuance | $ | 19.6 | $ | 19.7 | $ | 21.6 | $ | 17.0 | ||||||||

(1) | Based on fair value as of December 31, |

(2) |

|

hedges with changes in the fair value of the instruments of $4.5

In anticipation of a future debt issuance,

The effect on interest expense results primarily from monthly interest settlements.

| Effect on operating income — increase/(decrease) | ||||||||||||

| Year Ended December 31, | ||||||||||||

| 2011 | 2010 | 2009 | ||||||||||

| (in millions) | ||||||||||||

Fuel hedges(1) | ||||||||||||

Effect of mark to market valuation | $ | 0.0 | $ | 0.0 | $ | (0.3 | ) | |||||

Settlements | 0.4 | (0.1 | ) | (1.2 | ) | |||||||

|

|

|

|

|

| |||||||

| $ | 0.4 | $ | (0.1 | ) | $ | (1.5 | ) | |||||

Foreign exchange hedges(2) | $ | 0.1 | $ | (0.9 | ) | $ | (1.9 | ) | ||||

| Effect on operating income - increase/(decrease) | |||||||||||

| Year Ended December 31, | |||||||||||

| 2012 | 2011 | 2010 | |||||||||

| (in millions) | |||||||||||

Fuel hedges(1) | |||||||||||

| Effect of mark-to-market valuation | $ | 0.4 | $ | 0.0 | $ | 0.0 | |||||

| Settlements | 0.0 | 0.4 | (0.1 | ) | |||||||

| $ | 0.4 | $ | 0.4 | $ | (0.1 | ) | |||||

Foreign exchange hedges(2) | $ | (0.4 | ) | $ | 0.1 | $ | (0.9 | ) | |||

(1) | Included in cost of revenues in the accompanying consolidated statement of operations |

(2) | Included in other, net in the accompanying consolidated statement of operations |