UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, | Commission File Number: 001-14965 |

The Goldman Sachs Group, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 13-4019460 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

200 West Street | 10282 | |

New York, N.Y. |

| |

| (Address of principal executive offices) | (Zip Code) | |

(212) 902-1000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: | Name of each exchange on which registered: | |

Common stock, par value $.01 per share | New York Stock Exchange | |

Depositary Shares, Each Representing 1/1,000th Interest in a Share of Floating Rate Non-Cumulative Preferred Stock, Series A | New York Stock Exchange | |

Depositary Shares, Each Representing 1/1,000th Interest in a Share of 6.20% Non-Cumulative Preferred Stock, Series B | New York Stock Exchange | |

Depositary Shares, Each Representing 1/1,000th Interest in a Share of Floating Rate Non-Cumulative Preferred Stock, Series C | New York Stock Exchange | |

Depositary Shares, Each Representing 1/1,000th Interest in a Share of Floating Rate Non-Cumulative Preferred Stock, Series D | New York Stock Exchange | |

Depositary Shares, Each Representing 1/1,000th Interest in a Share of Floating Rate Non-Cumulative Preferred Stock, Series I | New York Stock Exchange | |

Depositary Shares, Each Representing 1/1,000th Interest in a Share of 5.50% Fixed-to-Floating Rate Non-Cumulative Preferred Stock, Series | New York Stock Exchange | |

Depositary Shares, Each Representing 1/1,000th Interest in a Share of 6.375% Fixed-to-Floating Rate Non-Cumulative Preferred Stock, Series K | New York Stock Exchange | |

| ||

| ||

| ||

| ||

| ||

| ||

| ||

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yesx NoYes¨ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

Yes¨ NoYesx No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yesx NoYes¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yesx NoYes¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of the Annual Report on Form 10-K or any amendment to the Annual Report on Form 10-K.x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ | |||

(Do not check if a smaller reporting company) | ||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes¨ NoYesx No

As of June 30, 2011,2014, the aggregate market value of the common stock of the registrant held by non-affiliates of the registrant was approximately $66.6$72.4 billion.

As of February 17, 2012,6, 2015, there were 494,904,018435,621,157 shares of the registrant’s common stock outstanding.

Documents incorporated by reference: Portions of The Goldman Sachs Group, Inc.’s Proxy Statement for its 20122015 Annual Meeting of Shareholders are incorporated by reference in the Annual Report on Form 10-K in response to Part III, Items 10, 11, 12, 13 and 14.

THE GOLDMAN SACHS GROUP, INC.

ANNUAL REPORT ON FORM 10-K FOR THE FISCAL YEAR ENDED DECEMBER 31, 20112014

| Form 10-K Item Number | Page No. | |||||

| 1 | ||||||

| 1 | ||||||

| 1 | ||||||

| 1 | ||||||

| 2 | ||||||

| 3 | ||||||

| 5 | ||||||

| 5 | ||||||

| 6 | ||||||

| 6 | ||||||

| 6 | ||||||

| 8 | ||||||

| 23 | ||||||

Cautionary Statement Pursuant to the U.S. Private Securities Litigation Reform Act of 1995 | 24 | |||||

| 44 | ||||||

| 45 | ||||||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | ||||||

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | ||||||

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | ||||||

Certain Relationships and Related Transactions, and Director Independence | ||||||

| II-1 | ||||||

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Goldman Sachs is a leading global investment banking, securities and investment management firm that provides a wide range of financial services to a substantial and diversified client base that includes corporations, financial institutions, governments and high-net-worth individuals.

When we use the terms “Goldman Sachs,” “the firm,” “we,” “us” and “our,” we mean The Goldman Sachs Group, Inc. (Group Inc.), a Delaware corporation, and its consolidated subsidiaries.

References to “this“the 2014 Form 10-K” are to our Annual Report on Form 10-K for the fiscal year ended December 31, 2011.2014. All references to 2011, 20102014, 2013 and 20092012 refer to our fiscal years ended, or the dates, as the context requires, December 31, 2011,2014, December 31, 20102013 and December 31, 2009,2012, respectively.

Group Inc. is a bank holding company and a financial holding company regulated by the Board of Governors of the Federal Reserve System (Federal Reserve Board). Our U.S. depository institution subsidiary, Goldman Sachs Bank USA (GS Bank USA), is a New York State-chartered bank.

As of December 2011,2014, we had offices in over 30 countries and 48%49% of our total staff was based outside the Americas (which includes the countries in North and South America).Americas. Our clients are located worldwide, and we are an active participant in financial markets around the world. In 2011,2014, we generated 38%42% of our net revenues outside the Americas. For more information onabout our geographic results, see Note 25 to the consolidated financial statements in Part II, Item 8 of this the 2014Form 10-K.

Our Business Segments and Segment Operating Results

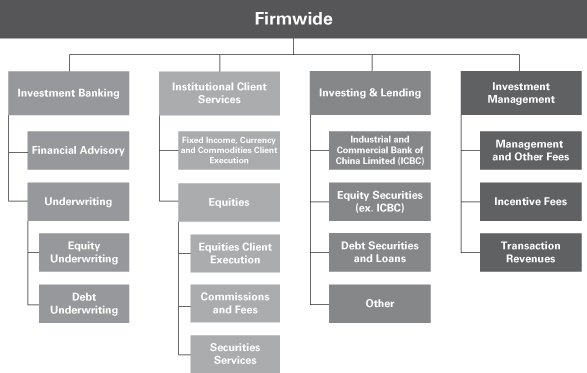

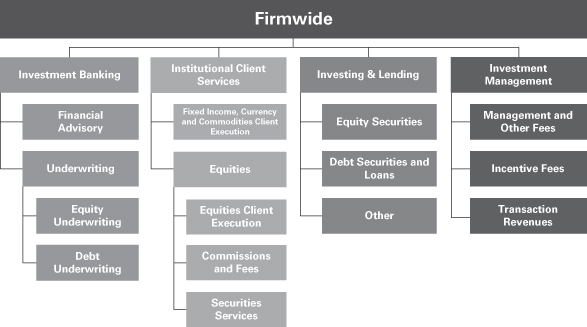

We report our activities in four business segments: Investment Banking, Institutional Client Services, Investing & Lending and Investment Management. The chart below presents our four business segments.

| Goldman Sachs | 1 |

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

The table below presents our segment operating results.

| Year Ended December 1 | % of 2011 | Year Ended December 1 | % of 2014 | |||||||||||||||||||||||||||||||

| $ in millions | 2011 | 2010 | 2009 | Net Revenues | 2014 | 2013 | 2012 | | Net Revenues | | ||||||||||||||||||||||||

Investment Banking | Net revenues | $ | 4,355 | $ | 4,810 | $ | 4,984 | 15 | % | |||||||||||||||||||||||||

Net revenues | $ 6,464 | $ 6,004 | $ 4,926 | 19% | ||||||||||||||||||||||||||||||

| Operating expenses | 2,962 | 3,511 | 3,482 | |||||||||||||||||||||||||||||||

Operating expenses | 3,688 | 3,479 | 3,333 | |||||||||||||||||||||||||||||||

Pre-tax earnings | $ 2,776 | $ 2,525 | $ 1,593 | |||||||||||||||||||||||||||||||

Institutional Client Services |

Institutional Client Services |

| ||||||||||||||||||||||||||||||||

Net revenues | $15,197 | $15,721 | $18,124 | 44% | ||||||||||||||||||||||||||||||

| Pre-tax earnings | $ | 1,393 | $ | 1,299 | $ | 1,502 | ||||||||||||||||||||||||||||

Operating expenses | 10,880 | 11,792 | 12,490 | |||||||||||||||||||||||||||||||

Pre-tax earnings | $ 4,317 | $ 3,929 | $ 5,634 | |||||||||||||||||||||||||||||||

Investing & Lending | ||||||||||||||||||||||||||||||||||

Net revenues | $ 6,825 | $ 7,018 | $ 5,891 | 20% | ||||||||||||||||||||||||||||||

Institutional Client Services | Net revenues | $ | 17,280 | $ | 21,796 | $ | 32,719 | 60 | % | |||||||||||||||||||||||||

Operating expenses | 2,819 | 2,686 | 2,668 | |||||||||||||||||||||||||||||||

Pre-tax earnings | $ 4,006 | $ 4,332 | $ 3,223 | |||||||||||||||||||||||||||||||

Investment Management |

Investment Management |

| ||||||||||||||||||||||||||||||||

Net revenues | $ 6,042 | $ 5,463 | $ 5,222 | 17% | ||||||||||||||||||||||||||||||

| Operating expenses | 12,697 | 14,291 | 13,691 | |||||||||||||||||||||||||||||||

Operating expenses | 4,647 | 4,357 | 4,296 | |||||||||||||||||||||||||||||||

Pre-tax earnings | $ 1,395 | $ 1,106 | $ 926 | |||||||||||||||||||||||||||||||

Total net revenues | $34,528 | $34,206 | $34,163 | |||||||||||||||||||||||||||||||

| Pre-tax earnings | $ | 4,583 | $ | 7,505 | $ | 19,028 | ||||||||||||||||||||||||||||

Investing & Lending | Net revenues | $ | 2,142 | $ | 7,541 | $ | 2,863 | 7 | % | |||||||||||||||||||||||||

| Operating expenses | 2,673 | 3,361 | 3,523 | |||||||||||||||||||||||||||||||

| Pre-tax earnings/(loss) | $ | (531 | ) | $ | 4,180 | $ | (660 | ) | ||||||||||||||||||||||||||

Investment Management | Net revenues | $ | 5,034 | $ | 5,014 | $ | 4,607 | 18 | % | |||||||||||||||||||||||||

| Operating expenses | 4,018 | 4,051 | 3,673 | |||||||||||||||||||||||||||||||

| Pre-tax earnings | $ | 1,016 | $ | 963 | $ | 934 | ||||||||||||||||||||||||||||

Total | Net revenues | $ | 28,811 | $ | 39,161 | $ | 45,173 | |||||||||||||||||||||||||||

| Operating expenses 2 | 22,642 | 26,269 | 25,344 | |||||||||||||||||||||||||||||||

| Pre-tax earnings | $ | 6,169 | $ | 12,892 | $ | 19,829 | ||||||||||||||||||||||||||||

Total operating expenses 2 | 22,171 | 22,469 | 22,956 | |||||||||||||||||||||||||||||||

Total pre-tax earnings | $12,357 | $11,737 | $11,207 | |||||||||||||||||||||||||||||||

| 1. | Financial information concerning our business segments for |

| 2. | Includes |

Investment Banking serves corporatepublic and governmentprivate sector clients around the world. We provide financial advisory services and help companies raise capital to strengthen and grow their businesses. We seek to develop and maintain long-term relationships with a diverse global group of institutional clients, including governments, states and municipalities. Our goal is to deliver to our institutional clients the entire resources of the firm in a seamless fashion, with investment banking serving as the main initial point of contact with Goldman Sachs.

Financial AdvisoryAdvisory.. Financial Advisory includes strategic advisory assignments with respect to mergers and acquisitions, divestitures, corporate defense activities, restructurings, spin-offs and risk management, restructurings and spin-offs.management. In particular, we help clients execute large, complex transactions for which we provide multiple services, including “one-stop” acquisition financing and cross-border structuring expertise. Financial Advisory also includes revenues from derivative transactions directly related to these client advisory assignments.

We also assist our clients in managing their asset and liability exposures and their capital. In addition, we may provide lending commitments and bank loan and bridge loan facilities in connection with our advisory assignments.

UnderwritingUnderwriting.. The other core activity of Investment Banking is helping companies raise capital to fund their businesses. As a financial intermediary, our job is to match the capital of our investing clients — who aim to grow the savings of millions of people — with the needs of our corporatepublic and governmentprivate sector clients — who need financing to generate growth, create jobs and deliver products and services. Our underwriting activities include public offerings and private placements, including domesticlocal and cross-border transactions, of a wide range of securities and other financial instruments. Underwriting also includes revenues from derivative transactions entered into with institutionalpublic and private sector clients in connection with our underwriting activities.

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Equity Underwriting. We underwrite common and preferred stock and convertible and exchangeable securities. We regularly receive mandates for large, complex transactions and have held a leading position in worldwide public common stock offerings and worldwide initial public offerings for many years.

Debt Underwriting.We underwrite and originate various types of debt instruments, including investment-grade and high-yield debt, bank loans and bridge loans, and emerging- and growth-market debt, which may be issued by, among others, corporate, sovereign, municipal and agency issuers. In addition, we underwrite and originate structured securities, which include mortgage-related securities and other asset-backed securities.

| 2 | Goldman Sachs 2014 Form 10-K | |||

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Institutional Client Services serves our clients who come to the firm to buy and sell financial products, raise funding and manage risk. We do this by acting as a market maker and offering market expertise on a global basis. Institutional Client Services makes markets and facilitates client transactions in fixed income, equity, currency and commodity products. In addition, we make markets in and clear client transactions on major stock, options and futures exchanges worldwide. Market makers provide liquidity and play a critical role in price discovery, which contributes to the overall efficiency of the capital markets. Our willingness to make markets, commit capital and take risk in a broad range of products is crucial to our client relationships.

Our clients are primarily institutions that are professional market participants, including investment entities whose ultimate customers include individual investors investing for their retirement, buying insurance or putting aside surplus cash in a deposit account.

Through our global sales force, we maintain relationships with our clients, receiving orders and distributing investment research, trading ideas, market information and analysis. As a market maker, we provide prices to clients globally across thousands of products in all major asset classes and markets. At times we take the other side of transactions ourselves if a buyer or seller is not readily available and at other times we connect our clients to other parties who want to transact. Much of this connectivity between the firm and its clients is maintained on technology platforms and operates globally wherever and whenever markets are open for trading.

Institutional Client Services and our other businesses are supported by our Global Investment Research division, which, as of December 2011,2014, provided fundamental research on more than 3,7003,600 companies worldwide and more than 40 national economies, as well as on industries, currencies and commodities.

Institutional Client Services generates revenues in four ways:

| Ÿ | In large, highly liquid markets (such as markets for U.S. Treasury bills, large capitalization S&P 500 stocks or certain mortgage pass-through securities), we execute a high volume of transactions for our clients for modest spreads and |

| Ÿ | In less liquid markets (such as mid-cap corporate bonds, growth market currencies |

| Ÿ | We also structure and execute transactions involving customized or tailor-made products that address our clients’ risk exposures, investment objectives or other complex needs (such as a jet fuel hedge for an airline) |

| Ÿ | We provide financing to our clients for their securities trading activities, as well as securities lending and other prime brokerage services. |

Institutional Client Services activities are organized by asset class and include both “cash” and “derivative” instruments. “Cash” refers to trading the underlying instrument (such as a stock, bond or barrel of oil). “Derivative” refers to instruments that derive their value from underlying asset prices, indices, reference rates and other inputs, or a combination of these factors (such as an option, which is the right or obligation to buy or sell a certain bond or stock index on a specified date in the future at a certain price, or an interest rate swap, which is the agreement to convert a fixed rate of interest into a floating rate or vice versa).

| Goldman Sachs | 3 |

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Fixed Income, Currency and Commodities Client Execution. Includes interest rate products, credit products, mortgages, currencies and commodities.

| Ÿ | Interest Rate Products. Government bonds, money market instruments such as commercial paper, treasury bills, repurchase agreements and other highly liquid securities and instruments, as well as interest rate swaps, options and other derivatives. |

| Ÿ | Credit Products.Investment-grade corporate securities, high-yield securities, credit derivatives, bank and |

| Ÿ | Mortgages.Commercial mortgage-related securities, loans and derivatives, residential mortgage-related securities, loans and derivatives (including U.S. government agency-issued collateralized mortgage obligations, other prime, subprime and Alt-A securities and loans), and other asset-backed securities, loans and derivatives. |

| Ÿ | Currencies.Most currencies, including growth-market currencies. |

| Ÿ | Commodities. |

Equities.Includes equityequities client execution, commissions and fees, and securities services.

Equities Client Execution.Execution.We make markets in equity securities and equity-related products, including convertible securities, options, futures and over-the-counter (OTC) derivative instruments, on a global basis. As a principal, we facilitate client transactions by providing liquidity to our clients with large blocks of stocks or options,derivatives, requiring the commitment of our capital. In addition, we engage in insurance activities where we reinsure and purchase portfolios of insurance risk and pension liabilities.

We also structure and executemake markets in derivatives on indices, industry groups, financial measures and individual company stocks. We develop strategies and provide information about portfolio hedging and restructuring and asset allocation transactions for our clients. We also work with our clients to create specially tailored instruments to enable sophisticated investors to establish or liquidate

investment positions or undertake hedging strategies. We are one of the leading participants in the trading and development of equity derivative instruments.

Our exchange-based market-making activities include making markets in stocks and exchange-traded funds. In the United States, we are one of the leading Designated Market Makers (DMMs) for stocks traded on the NYSE. For ETFs, we are registered market makers on NYSE Arca. In listed options, we are registered as a primary or lead market maker or otherwise make markets on the International Securities Exchange, the Chicago Board Options Exchange, NYSE Arca, the Boston Options Exchange, the Philadelphia Stock Exchange and NYSE Amex. Infunds, futures and options on futures, we are market makers on the Chicago Mercantile Exchange and the Chicago Board of Trade.major exchanges worldwide.

Commissions and Fees. We generate commissions and fees from executing and clearing institutional client transactions on major stock, options and futures exchanges worldwide.worldwide, as well as OTC transactions. We increasingly provide our clients with access to a broad spectrum of equity execution services, including electronic “low-touch” equity trading platforms,access and electronic trades account formore traditional “high-touch” execution. While the majority of our equity trading activity. However, aactivity is “low-touch,” the majority of our net revenues in these activities continue to be derived from our traditional “high-touch” handling of more complex trades.activity. We expect both types of activity to remain important.

Securities Services.Includes financing, securities lending and other prime brokerage services.

| Ÿ | Financing Services.We provide financing to our clients for their securities trading activities through margin loans that are collateralized by securities, cash or other acceptable collateral. We earn a spread equal to the difference between the amount we pay for funds and the amount we receive from our client. |

| Ÿ | Securities Lending Services.We provide services that principally involve borrowing and lending securities to cover institutional clients’ short sales and borrowing securities to cover our short sales and otherwise to make deliveries into the market. In addition, we are an active participant in broker-to-broker securities lending and third-party agency lending activities. |

| Ÿ | Other Prime Brokerage Services. We earn fees by providing clearing, settlement and custody services globally. In addition, we provide our hedge fund and other clients with a technology platform and reporting which enables them to monitor their security portfolios and manage risk exposures. |

| 4 | Goldman Sachs |

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

|

Our investing and lending activities, which are typically longer-term, include the firm’s investing and relationship lending activities across various asset classes, primarily including debt securities and loans, public and private equity securities, and real estate. These activities include investing directly in publicly and privately traded securities and in loans, and also through certain investment funds that we manage. We also provide financing to our clients. We manage a diversified global portfolio of investments in equity securities and debt securities and other investments in privately negotiated transactions, leveraged buyouts, acquisitions and investments in funds managed by external parties.

ICBC. We have an investment in the ordinary shares of ICBC, the largest bank in China.also provide financing to our clients.

Equity Securities (excluding ICBC)Securities.. We make corporate, real estate and infrastructure equity-related investments.

Debt Securities and LoansLoans.. We make corporate, real estate, infrastructure and infrastructureother debt security-related investments. In addition, we provide credit to corporate clients through loan facilities and to high-net-worth individuals primarily through secured loans.

OtherOther.. Our other investments primarily include our consolidated investment entities,investments, for which are entities we hold for investment purposes strictly for capital appreciation. These entities have a definedan exit strategy and which are engaged in activities that are not closely related to our principal businesses. We also invest directly in distressed assets, currencies, commodities and other assets, including power generation facilities.

Investment Management provides investment and wealth advisory services to help clients preserve and grow their financial assets. Our clients include institutions and high-net-worth individuals, as well as retail investors who access our products through a network of third-party distributors around the world.

We manage client assets across a broad range of asset classes and investment strategies, including equity, fixed income and alternative investments. Alternative investments primarily include hedge funds, credit funds, private equity, real estate, currencies, commodities, and asset allocation strategies. Our investment offerings include those managed on a fiduciary basis by our portfolio managers as well as strategies managed by third-party managers. We offer our investments in a variety of structures, including separately managed accounts, mutual funds, private partnerships, and other commingled vehicles.

We also provide customized investment advisory solutions designed to address our clients’ investment needs. These solutions begin with identifying clients’ objectives and continue through portfolio construction, ongoing asset allocation and risk management and investment realization. We draw from a variety of third-party managers as well as our proprietary offerings to implement solutions for clients.

We supplement our investment advisory solutions for high-net-worth clients with wealth advisory services that include income and liability management, trust and estate planning, philanthropic giving and tax planning. We also use the firm’s global securities and derivatives market-making capabilities to address clients’ specific investment needs.

Management and Other Fees. The majority of revenues in management and other fees is comprised of asset-based management fees on client assets. The fees that we charge vary by asset class and are affected by investment performance as well as asset inflows and redemptions. Other fees we receive include financial counseling fees generated through our wealth advisory services and fees related to the administration of real estate assets.

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Assets under supervision include assets under management and other client assets. Assets under management include only those client assets where we earn a fee for managing assets on a discretionary basis. This includes net assets in our mutual funds, hedge funds, credit funds and private equity funds (including real estate funds), and separately managed accounts for institutional and individual investors. Other client assets include client assets invested with third-party managers, bank deposits and advisory relationships where we earn a fee for advisory and other services, but do not have investment discretion. Assets under managementsupervision do not include the self-directed brokerage assets of our clients, including brokerage accounts, or interest-bearing deposits held through ourclients. Long-term assets under supervision represent assets under supervision excluding liquidity products. Liquidity products represent money markets and bank depository institution subsidiaries.deposit assets.

| Goldman Sachs 2014 Form 10-K | 5 |

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Incentive Fees.In certain circumstances, we are also entitled to receive incentive fees based on a percentage of a fund’s or a separately managed account’s return, or when the return exceeds a specified benchmark or other performance targets. Such fees include overrides, which

consist of the increased share of the income and gains derived primarily from our private equity funds when the return on a fund’s investments over the life of the fund exceeds certain threshold returns. Incentive fees are recognized only when all material contingencies are resolved.

Transaction Revenues.We receive commissions and net spreads for facilitating transactional activity in high-net-worth client accounts. In addition, we earn net interest income primarily associated with client deposits and margin lending activity undertaken by such clients.

The tables below present assets under management by asset class and by distribution channel and client category.

| As of December | ||||||||||||

| in billions | 2011 | 2010 | 2009 | |||||||||

Alternative investments | $ | 142 | $ | 148 | $ | 146 | ||||||

Equity | 126 | 144 | 146 | |||||||||

Fixed income | 340 | 340 | 315 | |||||||||

Total non-money market assets | 608 | 632 | 607 | |||||||||

Money markets | 220 | 208 | 264 | |||||||||

Total assets under management | $ | 828 | $ | 840 | $ | 871 | ||||||

| As of December | ||||||||||||

| in billions | 2011 | 2010 | 2009 | |||||||||

Directly Distributed: | ||||||||||||

Institutional | $ | 283 | $ | 286 | $ | 297 | ||||||

High-net-worth individuals | 227 | 229 | 231 | |||||||||

Third-Party Distributed: | ||||||||||||

Institutional, high-net-worth individuals and retail | 318 | 325 | 343 | |||||||||

Total | $ | 828 | $ | 840 | $ | 871 | ||||||

Business Continuity and Information Security

Business continuity and information security, including cybersecurity,cyber security, are high priorities for Goldman Sachs. Their importance has been highlighted by Hurricane Sandy and several recent highly publicized cyber attacks against financial institutions and large consumer-based companies that resulted in the unauthorized disclosure of personal information of clients and/or customers, as well as other cyber attacks involving the theft and destruction of corporate information.

Our Business Continuity Program has been developed to provide reasonable assurance of business continuity in the event of disruptions at the firm’s critical facilities and to comply with regulatory requirements, including those of FINRA. Because we are a bank holding company, our Business Continuity Program is also subject to review by the Federal Reserve Board. The key elements of the program are crisis planning and management, people recovery, facilities, business recovery, systems and data recovery, and process improvement. In the area of information security, we have developed and implemented a framework of principles,

policies and technology to protect the information assets provided to us by our clients and thosethat of the firm from cyber attacks and other misappropriation, corruption or loss. Safeguards are applied to maintain the confidentiality, integrity and availability of information resources.information.

Management believes that a major strength and principal reason for the success of Goldman Sachs is the quality and dedication of our people and the shared sense of being part of a team. We strive to maintain a work environment that fosters professionalism, excellence, diversity, cooperation among our employees worldwide and high standards of business ethics.

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Instilling the Goldman Sachs culture in all employees is a continuous process, in which training plays an important part. All employees are offered the opportunity to participate in education and periodic seminars that we sponsor at various locations throughout the world. Another important part of instilling the Goldman Sachs culture is our employee review process. Employees are reviewed by supervisors, co-workers and employees they supervise in a 360-degree review process that is integral to our team approach, and includes an evaluation of an employee’s performance with respect to risk management, compliance and diversity.

As of December 2011,2014, we had 33,30034,000 total staff, excluding staff at consolidated entities held for investment purposes. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Results of Operations — Operating Expenses” in Part II, Item 7 of this Form 10-K for additional information on our consolidated entities held for investment purposes.staff.

The financial services industry — and all of our businesses — are intensely competitive, and we expect them to remain so. Our competitors are other entities that provide investment banking, securities and investment management services, as well as those entities that make investments in securities, commodities, derivatives, real estate, loans and other financial assets. These entities include brokers and dealers, investment banking firms, commercial banks, insurance companies, investment advisers, mutual funds, hedge funds, private equity funds and merchant banks. We compete with some entities globally and with others on a regional, product or niche basis. Our competition is based on a number of factors, including transaction execution, products and services, innovation, reputation and price.

We also face intense competition in attracting and retaining qualified employees. Our ability to continue to compete effectively will depend upon our ability to attract new employees, retain and motivate our existing employees and to continue to compensate employees competitively amid intense public and regulatory scrutiny on the compensation practices of large financial institutions. Our pay practices and those of our principal competitors are subject to review by, and the standards of, the Federal Reserve Board and regulators outside the United States, including the Financial Services Authority (FSA) in the United Kingdom. See “Regulation — Banking Regulation” and “Regulation — Compensation Practices” below and “Risk Factors — Our businesses may be adversely affected if we are unable to hire and retain qualified employees” in Part I, Item 1A of this Form 10-K for more information on the regulation of our compensation practices.

| 6 | Goldman Sachs 2014 Form 10-K |

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Over time, there has been substantial consolidation and convergence among companies in the financial services industry. This trend acceleratedindustry and, in recent years asparticular, the credit crisis caused numerous mergers and asset acquisitions among industry participants. Many commercial banks and other broad-based financial services firms have the ability to support investment banking and securities products with commercial banking, insurance and other financial services revenues in an effortEfforts by our competitors to gain market share which hashave resulted in pricing pressure in our investment banking and client execution businesses and could result in pricing pressure in other of our businesses.

Moreover, we have faced, and expect to continue to face, pressure to retain market share by committing capital to businesses or transactions on terms that offer returns that may not be commensurate with their risks. In particular, corporate clients seek such commitments (such as agreements to participate in their commercial paper backstop or other loan facilities) from financial services firms in connection with investment banking and other assignments.

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Consolidation and convergence have significantly increased the capital base and geographic reach of some of our competitors, and have also hastened the globalization of the securities and other financial services markets. As a result, we have had to commit capital to support our international operations and to execute large global transactions. To take advantage of some of our most significant opportunities, we will have to compete successfully with financial institutions that are larger and have more capital and that may have a stronger local presence and longer operating history outside the United States. We also compete with smaller institutions that offer more targeted services, such as independent advisory firms. Some clients may perceive these firms to be less susceptible to potential conflicts of interest than we are, and, as discussed below, our ability to effectively compete with them could be affected by regulations and limitations on activities that apply to us but may not apply to them.

We have experienced intense price competition in some of our businesses in recent years. For example, over the past several years the increasing volume of trades executed electronically, through the internet and through alternative trading systems, has increased the pressure on trading commissions, in that commissions for “low-touch” electronic trading are generally lower than for “high-touch” non-electronic trading. It appears that this trend toward electronic and other “low-touch,” low-commission trading will continue. In addition, we believe that we will continue to experience competitive pressures in these and other areas in the future as some of our competitors seek to obtain market share by further reducing prices.

The provisions of the U.S. Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act), the requirements promulgated by the Basel Committee on Banking Supervision (Basel Committee) and other financial regulation could affect our competitive position to the extent that limitations on activities, increased fees and compliance costs or other regulatory requirements do not apply, or do not apply equally, to all of our competitors or are not implemented uniformly across different jurisdictions. For example, the provisions of the Dodd-Frank Act that prohibit proprietary trading and restrict investments in certain hedge and private equity funds differentiate between U.S.-based and non-U.S.-based banking organizations and give non-U.S.-based banking organizations greater flexibility to trade outside of the United States and to form and invest in funds outside the United States. Likewise, the obligations with respect to derivative transactions under Title VII of the Dodd-Frank Act depend, in part, on the location of the counterparties to the transaction. The impact of the Dodd-Frank Act and other regulatory developments on our competitive position will depend to a large extent on the manner in which the required rulemaking and regulatory guidance evolve, the extent of international convergence, and the development of market practice and structures under the new regulatory regimes as discussed further under “Regulation” below.

We also face intense competition in attracting and retaining qualified employees. Our ability to continue to compete effectively will depend upon our ability to attract new employees, retain and motivate our existing employees and to continue to compensate employees competitively amid intense public and regulatory scrutiny on the compensation practices of large financial institutions. Our pay practices and those of certain of our competitors are subject to review by, and the standards of, the Federal Reserve Board and regulators outside the United States, including the Prudential Regulation Authority (PRA) and the Financial Conduct Authority (FCA) in the United Kingdom. We also compete for employees with institutions whose pay practices are not subject to regulatory oversight. See “Regulation — Bank Holding Company Regulation” and “Regulation — Compensation Practices” below and “Risk Factors — Our businesses may be adversely affected if we are unable to hire and retain qualified employees” in Part I, Item 1A of the 2014 Form 10-K for more information about the regulation of our compensation practices.

| Goldman Sachs 2014 Form 10-K | 7 |

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

As a participant in the banking, securities, investment management, OTCand derivatives futures and options and insurance industries, we are subject to extensive regulation worldwide. Regulatory bodies around the world are generally charged with safeguarding the integrity of the securities and other financial markets and with protecting the interests of the customers of market participants, including depositors in banking entities and the customers of broker-dealers.banks, broker-dealers, investment advisers, swap dealers and security-based swap dealers.

The financial services industry has been the subject of intense regulatory scrutiny in recent years. Our businesses have been subject to increasing regulation and supervision in the United States and other countries, and we expect this trend to continue in the future. In particular, the Dodd-Frank Act, which was enacted in July 2010, significantly altered the financial regulatory regime within which we operate. Not all the rules required or expected to be implemented under the Dodd-Frank Act have been proposed or adopted, and certain of the rules that have been proposed or adopted under the Dodd-Frank Act are subject to phase-in or transitional periods. The implications of the Dodd-Frank Act for our businesses willcontinue to depend to a large extent on the rules that will be adoptedimplementation of the legislation by the Federal Reserve Board, the FDIC, the SEC, the CFTCU.S. Commodity Futures Trading Commission (CFTC) and other agencies, to implement the legislation, as well as the development of market practices and structures under the regime established by the legislation and the implementing rules. SimilarOther reforms have been adopted or are being considered by other regulators and policy makers worldwide, as discussed further throughout this section. We will continue to assessupdate our business, risk management, and compliance practices to conform to developments in the regulatory environment.

BankingBank Holding Company Regulation

Group Inc. is a bank holding company under the Bank Holding Company Act of 1956 (BHC Act) and a financial holding company under amendments to the BHC Act effected by the U.S. Gramm-Leach-Bliley Act of 1999 (GLB Act).

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Supervision and Regulation

As a bank holding company and a financial holding company under the BHC Act, Group Inc. is subject to supervision and examination by the Federal Reserve Board. Under the system of “functional regulation” established under the BHC Act, the Federal Reserve Board serves as the primary regulator of our consolidated organization, but generally defers to the primary regulators of our U.S. non-bank subsidiaries with respect to the activities of those subsidiaries. Such “functionally regulated” U.S. non-bank subsidiaries include broker-dealers registered with the SEC, such as our principal U.S. broker-dealer, Goldman, Sachs & Co. (GS&Co.), insurance companiesentities registered with or regulated by state insurance authorities,the CFTC with respect to futures-related and swaps-related activities and investment advisers registered with the SEC with respect to their investment advisory activitiesactivities.

As discussed further below, our principal U.S. bank subsidiary, GS Bank USA, is supervised and entities regulated by the CFTC with respectFederal Reserve Board, the FDIC, the New York State Department of Financial Services and the Consumer Financial Protection Bureau (CFPB). In addition, Group Inc. has two limited purpose trust company subsidiaries that are not permitted to certain futures-related activities.accept deposits or make loans (other than as incidental to their trust activities) and are not insured by the FDIC. The Goldman Sachs Trust Company, N.A., a national banking association that is limited to fiduciary activities, is regulated by the Office of the Comptroller of the Currency and is a member bank of the Federal Reserve System. The Goldman Sachs Trust Company of Delaware, a Delaware limited purpose trust company, is regulated by the Office of the Delaware State Bank Commissioner.

| 8 | Goldman Sachs 2014 Form 10-K |

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Activities

The BHC Act generally restricts bank holding companies from engaging in business activities other than the business of banking and certain closely related activities. As a financialFinancial holding company, we maycompanies, however, generally can engage in a broader range of financial and related activities than are otherwise permissible for bank holding companies as long as wethey continue to meet the eligibility requirements for financial holding companies. These requirements include Group Inc.that the financial holding company and oureach of its U.S. depository institution subsidiaries (currently GS Bank USA and our national bank trust company subsidiary) each maintainingmaintain their respective status as “well-capitalized” and “well-managed.” The broader range of permissible activities for financial holding companies

includes underwriting, dealing and making markets in securities insurance underwriting and making investments in nonfinancialnon-financial companies. In addition, wefinancial holding companies are permitted under the GLB Act to continue to engage in certain commodities activities in the United States that may otherwise be impermissible for bank holding companies, so long as the assets held pursuant to these activities do not equal 5% or more of ourtheir consolidated assets.

AsThe Federal Reserve Board, however, has the authority to limit our ability to conduct activities that would otherwise be permissible for a bankfinancial holding company, and will do so if we do not satisfactorily meet certain requirements of the Federal Reserve Board. In addition, we are required to obtain prior Federal Reserve Board approval before engaging in certain banking and other financial activities both in the United States and abroad.

We expectVolcker Rule

In December 2013, the final rules to face additional limitations on our activities upon implementation of thoseimplement the provisions of the Dodd-Frank Act referred to as the “Volcker Rule” were adopted.

The Volcker Rule prohibits “proprietary trading,” which will prohibit “proprietary trading” (but will allowbut permits activities such as underwriting, market-making related activitiesmarket making and risk-mitigation hedging activities)hedging. We are also required to calculate daily quantitative metrics on covered trading activities (as defined in the rule) and will limitprovide these metrics to regulators on a monthly basis. In addition, the Volcker Rule limits the sponsorship of, and investment in, hedge funds and private equity funds“covered funds” (as defined in the rule) by banking entities, including bank holding companies.Group Inc. and its subsidiaries. It also limits certain types of transactions between us and our sponsored funds, similar to the limitations on transactions between depository institutions and their affiliates as described below under “Regulation of GS Bank USA — Transactions with Affiliates.” Covered funds include our private equity funds, certain of our credit and real estate funds, our hedge funds and certain other investment structures.

We are required to be in compliance with the prohibition on proprietary trading and to develop an extensive compliance program by July 2015. In October 2011, federal regulators proposed rulesDecember 2014, the Federal Reserve Board extended the compliance period through July 2016 for investments in, and relationships with, covered funds that were in place prior to implementDecember 31, 2013, and indicated that it intends to further extend the compliance period through July 2017.

The limitation on investments in covered funds requires us to reduce our investment in each such fund to 3% or less of the fund’s net asset value, and to reduce our aggregate investment in all such funds to 3% or less of our Tier 1 capital. In anticipation of the final rule, we limited our initial investment in certain new covered funds to 3% of the fund’s net asset value.

We continue to manage our existing funds, taking into account the transition periods under the Volcker RuleRule. We plan to continue to conduct our investing and lending activities in ways that included an extensive request for comments onare permissible under the proposal. The proposed rules are highly complex,Volcker Rule.

See “Management’s Discussion and many aspectsAnalysis of Financial Condition and Results of Operations — Regulatory Developments — Volcker Rule” in Part II, Item 7 of the Volcker Rule remain unclear. The full impact on us will not be known with certainty until the rules are finalized. The Volcker Rule provisions are scheduled to take effect no later than July 2012, and companies will be required to come into compliance within two years after the effective date (subject to possible extensions).2014 Form 10-K for information about our investments in covered funds.

| Goldman Sachs | 9 |

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

While many aspectsLeveraged Lending

During the past several years, the U.S. federal bank regulatory agencies have raised concerns over origination and other practices in leveraged lending markets. The agencies have issued guidance that focuses on transaction structures and risk management frameworks and outlined high-level principles for safe-and-sound leveraged lending, including underwriting standards, valuation and stress testing. Although the full impact of the Volcker Rule remain unclear, we evaluated the prohibition on “proprietary trading”guidance remains uncertain, implementation of this guidance and determined that businesses that engage in “bright line” proprietary trading are most likely to be prohibited. In 2011 and 2010, we liquidated substantially all of our Principal Strategies and global macro proprietary trading positions.

In addition, we evaluated the limitations on sponsorship of, and investments in, hedge funds and private equity funds. The firm earns management fees and incentive fees for investment management services from private equity and hedge funds, which are included in our Investment Management segment. The firm also makes investments in funds, and the gains and losses from such investments are included in our Investing & Lending segment; these gains and losses will be impacted by the Volcker Rule. The Volcker Rule limitation on investments in hedge funds and private equity funds requires the firm to reduce its investment in each private equity and hedge fund to 3% or less of net asset value, and to reduce the firm’s aggregate investment in all such funds to 3% or less of the firm’s Tier 1 capital. Over the period from 1999 through 2011, the firm’s aggregate net revenues from its investments in hedge funds and private equity funds were not material to the firm’s aggregate total net revenues over the same period. We are continuing to manage our existing private equity funds, taking into account the transition periods under the Volcker Rule. With respect to our hedge funds, we currently plan to comply with the Volcker Rule by redeeming certain of our interestsany related changes in the funds. We currently expect to redeem up to approximately 10% of certain hedge funds’ total redeemable units per quarter over ten consecutive quarters, beginning in the quarter ending March 2012 and ending in June 2014. In addition, we have limited the firm’s initial investment to 3% for certain new funds.

The Dodd-Frank Act also establishes a Bureau of Consumer Financial Protection having broad authority to regulate providers of credit, payment and other consumer financial products and services, and this Bureau has oversight over certain ofleveraged lending market could adversely affect our products and services.leveraged lending business.

Capital and Liquidity Requirements

As a bank holding company, we are subject to consolidated regulatory capital requirements administered by the Federal Reserve Board.Board, and GS Bank USA is subject to broadlysubstantially similar capital requirements as(as discussed below. below), also administered by the Federal Reserve Board.

Under the Federal Reserve Board’s capital adequacy requirements, and the regulatory framework for prompt corrective action that is applicable to GS Bank USA, both Group Inc. and GS Bank USA must meet specific regulatory capital requirements that involve quantitative measures of assets, liabilities and certain off-balance-sheet items. The sufficiency of our capital levels and those of GS Bank USA, as well as GS Bank USA’s prompt corrective action classification, areis also subject to qualitative judgments by regulators.

Other regulated subsidiaries, including GS&Co. and Goldman Sachs International (GSI), are also subject to capital requirements. We expect Group Inc., GS Bank USA, GS&Co., GSI and other regulated subsidiaries to become subject to increased capital requirements over time.

Capital Ratios. Since January 1, 2014, we have been subject to the Federal Reserve Board’s revised risk-based capital and leverage ratio regulations, inclusive of certain transitional provisions (Revised Capital Framework). These regulations are largely based on the Basel Committee’s final capital framework for strengthening international capital standards (Basel III), and also implement certain provisions of the Dodd-Frank Act. The Revised Capital Framework also introduces a new Tier 1 Leveragesupplementary leverage ratio (supplementary leverage ratio) for Advanced approach banking organizations.

See “Management’s Discussion and Basel 1Analysis of Financial Condition and Results of Operations — Equity Capital Ratios.SeeManagement and Regulatory Capital” in Part II, Item 7 of the 2014 Form 10-K and Note 20 to the consolidated financial statements in Part II, Item 8 of this the 2014Form 10-K for the aspects of the Revised Capital Framework that are most relevant to us as an Advanced approach banking organization, including information onabout our Common Equity Tier 1 (CET1), CET1 ratio, Tier 1 capital, Tier 1 capital ratio, Total capital, Total capital ratio, risk-weighted assets (RWAs), Tier 1 capital, total capital, risk-weighted assetsleverage ratio and Tier 1supplementary leverage ratio, and for a discussion of minimum required ratios. For information on our Tier 1 common ratio, see “— Equity Capital — Consolidated Regulatory Capital Ratios” in Part II, Item 7 of this Form 10-K.

Pending Changes in Capital Requirements.We are currently working to implement the requirements set out in the Federal Reserve Board’s Risk-Based Capital Standards: Advanced Capital Adequacy Framework — Basel 2, as applicable to us as a bank holding company (Basel 2), which are based on the advanced approaches under the Revised Framework for the International Convergence of Capital Measurement and Capital Standards issued by the Basel Committee. U.S. banking regulators have incorporated the Basel 2 framework into the existing risk-based capital requirements by requiring that internationally active banking organizations, such as us, adopt Basel 2, once approved to do so by regulators. As required by the Dodd-Frank Act, U.S. banking regulators have adopted a rule that requires large banking organizations, upon adoption of Basel 2, to continue to calculate risk-based capital ratios under both Basel 2 and the Federal Reserve Board’s regulatory requirements currently applicable to bank holding companies (Basel 1), which are based on the 1988 Capital Accord of the Basel Committee. For each of the Tier 1 and Total capital ratios, the lower of the Basel 1 and Basel 2 ratios calculated will be used to determine whether the bank meets its minimum risk-based capital requirements.

| 10 | Goldman Sachs |

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

The U.S. federal bank regulatory agencies have issued revised proposals to modify their market risk regulatory capital requirements for banking organizations in the United States that have significant trading activities. These modifications are designed to address the adjustments to the market risk framework that were announced by the Basel Committee in June 2010 (Basel 2.5), as well as the prohibition on the use of credit ratings, as required by the Dodd-Frank Act. Once implemented, it is likely that these changes will result in increased capital requirements for market risk.

Additionally, the guidelines issued by the Basel Committee in December 2010 (Basel 3) revise the definition of Tier 1 capital, introduce Tier 1 common equity as a regulatory metric, set new minimum capital ratios (including a new “capital conservation buffer,” which must be composed exclusively of Tier 1 common equity and will be in addition to the minimum capital ratios), introduce a Tier 1 leverage ratio within international guidelines for the first time, and make substantial revisions to the computation of risk-weighted assets (RWAs) for credit exposures. Implementation of the new requirements is expected to take place over the next several years. The federal banking agencies have not yet proposed rules to implement the Basel 3 guidelines in the United States.

In addition, both the Basel Committee and U.S. banking regulators implementing the Dodd-Frank Act have indicated that they will impose more stringent capital standards on systemically important financial institutions. In November 2011, the Basel Committee published its final provisions for assessing the global systemic importance of banking institutions and the range of additional Tier 1 common equity that should be maintained by banking institutions deemed to be globally systemically important. The additional capital for these institutions would initially range from 1% to 2.5% of Tier 1 common equity and could be as much as 3.5% for a bank that increases its systemic footprint (e.g., by increasing total assets). The firm was one of 29 institutions identified by the Financial Stability Board (established at the direction of the Group of 20) as globally systemically important under the Basel Committee’s methodology. Therefore, depending upon the manner and timing of the U.S. banking regulators’ implementation of the Basel Committee’s methodology, we expect that the minimum Tier 1 common ratio requirement applicable to us will include this additional capital assessment. The final determination of whether an institution is classified as globally systemically important and the calculation of the required additional capital amount is expected to be disclosed by the Basel Committee no later than November 2014 based on data through the end of 2013.

In December 2011, the Federal Reserve Board proposed rules to implement the enhanced prudential standards and early remediation requirements contemplated by the Dodd-Frank Act. The proposed rules would apply to bank holding companies with $50 billion or more in total consolidated assets such as us, as well as systemically important nonbank financial institutions. With respect to the enhanced prudential standards, the proposed rules address risk-based capital and leverage requirements, liquidity requirements, overall risk management requirements and concentration/credit exposure limits. The proposed rules do not include the additional capital requirements for globally systemically important banking institutions but contemplate the Federal Reserve Board’s adopting such requirements. The proposed rules require increased involvement by boards of directors in liquidity and risk management and stress testing, single-counterparty credit limits (including more stringent requirements for credit exposure among major financial institutions) and public disclosure of the Federal Reserve Board’s annual stress tests and a bank holding company’s annual and semi-annual internal stress tests. The proposed early remediation rules are modeled after the prompt corrective action regime, described below, but are designed to require action beginning in earlier stages of a company’s financial distress by mandating action on the basis of a range of triggers, including capital and leverage, stress test results, liquidity and risk management.

The Dodd-Frank Act will subject us at a firmwide level to the same leverage and risk-based capital requirements that apply to depository institutions and directs banking regulators to impose additional capital requirements. The Federal Reserve Board is expected to adopt the new leverage and risk-based capital regulations in 2012. As a consequence of these changes, Tier 1 capital treatment for our junior subordinated debt issued to trusts will be phased out over a three-year period beginning on January 1, 2013. The interaction among the Dodd-Frank Act, the Basel Committee’s proposed changes and other proposed or announced changes from other governmental entities and regulators adds further uncertainty to our future capital requirements and those of our subsidiaries.

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Liquidity Ratios under Basel 3.III.Historically, regulation and monitoring of bank and bank holding company liquidity has been addressed as a supervisory matter, both in the United States and internationally, without required formulaic measures. Basel 3 will requireIII, which is subject to implementation by national regulators, requires banks and bank holding companies to measure their liquidity against two specific liquidity tests that, although similar in some respects to liquidity measures historically applied by banks and regulators for management and supervisory purposes, will be mandated by regulation. One test, referred to as the liquidity coverage ratio (LCR), is designed to ensure that the banking entity maintains an adequate level of unencumbered high-quality liquid assets equal to the entity’s expected net cash outflow for a 30-day time horizon (or, if greater, 25% of its expected total cash outflow) under an acute short-term liquidity stress scenario. The other, referred to as the net stable funding ratio (NSFR), is designed to promote more medium- and long-term stable funding of the assets and off-balance-sheet activities of bankingthese entities over a one-year time horizon. These requirements may incentivize banking entities to increase their holdings of U.S. Treasury securities and certain other sovereign debtthat qualify as a component ofhigh-quality liquid assets and increase the use of long-term debt as a funding source. The liquidity coverage ratio is not expected

During 2014, the U.S. federal bank regulatory agencies approved final rules implementing the LCR for Advanced approach banking organizations that are generally consistent with the Basel Committee’s framework as described above, but which include accelerated transitional provisions and more stringent requirements related to be introducedboth the range of assets that qualify as a requirement untilhigh-quality liquid assets and cash outflow assumptions for certain types of funding. Under the accelerated transition timeline, the LCR became effective in the United States on January 1, 2015, with a phase-in period whereby firms must meet an 80% minimum ratio in 2015, which will increase 10% per year until 2017. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Liquidity Risk Management” in Part II, Item 7 of the net stable funding ratio is not expected to2014Form 10-K for information about the LCR.

During 2014, the Basel Committee issued its final framework for calculation of the NSFR. Under the Basel Committee framework, the NSFR will be introduced as a requirement untileffective on January 1, 2018. WhileThe U.S. federal bank regulatory agencies have not yet proposed rules implementing the principles behindNSFR for U.S. banking organizations. We are currently evaluating the new framework are broadly consistent with our current liquidity management framework, it is possible thatimpact of the refinement andBasel Committee’s NSFR framework.

The implementation of these standards, and any amendments or modifications adopted by the U.S. federal bank regulatory agencies, could impact our liquidity and funding requirements and practices.

We also expect that liquidity requirements applicable to us and several of our subsidiaries will be impactedpractices in the future byfuture.

Stress Tests. The Federal Reserve Board has issued final rules implementing the various developments arising from the Basel Committee,requirements of the Dodd-Frank Act and actions by other governmental entities and regulators.

Payment of Dividends and Stock Repurchases

Dividend payments by Group Inc.concerning the Dodd-Frank Act supervisory stress tests to its shareholders and stock repurchases by Group Inc. are subject to the oversight of the Federal Reserve Board. Under rules adoptedbe conducted by the Federal Reserve Board and semi-annual company-run stress tests for bank holding companies with total consolidated assets of $50 billion or more. The stress test rules require increased involvement by boards of directors in November 2011,stress testing and public disclosure of the dividendresults of both the Federal Reserve Board’s annual stress tests and share repurchase policiesa bank holding company’s annual supervisory stress tests, and semi-annual internal stress tests. Certain stress test requirements are also applicable to GS Bank USA, as discussed below.

Our internally developed severely adverse scenario is designed to stress the firm’s risks and idiosyncratic vulnerabilities and assess the firm’s pro-forma capital position and ratios under the hypothetical stressed environment. We publish summaries of our annual and mid-cycle stress tests results on our web site as described under “Available Information” below. Our annual Dodd-Frank Act stress test submission is incorporated into the annual capital plans that we are required to submit to the Federal Reserve Board as part of the Comprehensive Capital Analysis and Review (CCAR). The purpose of CCAR is to ensure that large bank holding companies

such as Group Inc., are reviewed by the Federal Reserve Board based on capital plans and stress tests submitted by the bank holding company, and will be assessed against, among other things, the bank holding company’s ability to meet and exceed minimum regulatory capital ratios, its expected sources and uses of capital over the planning horizon (generally a period of two years) under baseline and stressed scenarios, and any potential impact of changes to its business plan and activities on its capital adequacy and liquidity. The purpose of the capital plan review is to ensure that these institutions have robust, forward-looking capital planning processes that account for each institution’s unique risks and that permit continued operations during times of economic and financial stress. As part of the capital plan review,CCAR, the Federal Reserve Board will evaluateevaluates an institution’s plan to make capital distributions, such as repurchasing or redeeming stock or increasing dividend payments.payments, across a range of macro-economic and firm-specific assumptions.

| Goldman Sachs 2014 Form 10-K | 11 |

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Federal

Payment of Dividends and state law impose limitations on the payment of dividendsStock Repurchases. Dividend payments by our depository institution subsidiaries to Group Inc. to its shareholders and stock repurchases by Group Inc. are subject to the oversight of the Federal Reserve Board. The dividend and share repurchase policies of large bank holding companies, such as Group Inc., are reviewed by the Federal Reserve Board, through the CCAR process, based on capital plans and stress tests submitted by the bank holding company, and are assessed against, among other things, the bank holding company’s ability to meet and exceed minimum regulatory capital ratios under stressed scenarios, its expected sources and uses of capital over the planning horizon under baseline and stressed scenarios, and any potential impact of changes to its business plan and activities on its capital adequacy and liquidity.

In general,October 2014, the Federal Reserve Board issued a final rule modifying the regulations for capital planning and stress testing. The modifications change the dates for submitting the capital plan and stress test results beginning with the 2016 cycle and include a limitation on capital distributions to the extent that actual capital issuances are less than the amount indicated in the capital plan submission.

The Federal Reserve Board informed us that it did not object to our proposed capital actions through the first quarter of dividends that may be paid by GS Bank USA or2015, including the repurchase of outstanding common stock, an increase in our national bank trust company subsidiary is limitedquarterly common stock dividend, and the possible issuance, redemption and modification of other capital securities. We submitted our 2015 capital plan and proposed capital actions to the lesserFederal Reserve Board in January 2015 and expect to publish a summary of our annual Dodd-Frank Act stress test results in March 2015.

Enhanced Prudential Standards. In February 2014, the Federal Reserve Board adopted rules to implement certain of the amounts calculated under a “recent earnings” test and an “undivided profits” test. Under the recent earnings test, a dividend may not be paid if the total of all dividends declaredenhanced prudential standards contemplated by the entityDodd-Frank Act. Effective on January 1, 2015, the rules require bank holding companies with $50 billion or more in any calendar yeartotal consolidated assets to comply with enhanced liquidity and overall risk management standards, including a buffer of highly liquid assets based on projected funding needs for 30 days, and increased involvement by boards of directors in liquidity and overall risk management. Although the liquidity buffer under these rules has some similarities to the LCR (and is described by the agencies as complementary to the LCR), it is a separate requirement that is in excessaddition to the LCR. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Risk Management and Risk Factors — Overview and Structure of Risk Management” and “— Liquidity Risk Management” in Part II, Item 7 of the current year’s net income combined with the retained net income of the two preceding years, unless the entity obtains prior regulatory approval. Under the undivided profits test, a dividend may not be paid in excess of the entity’s “undivided profits” (generally, accumulated net profits that have not been paid out as dividends or transferred to surplus). The payment of all dividends is subject to approval by the banking regulators, which have authority to prohibit or limit the payment if, in the banking regulator’s opinion, payment of a dividend would constitute an unsafe or unsound practice in light of the financial condition of the banking organization.2014 Form 10-K for information about our risk management practices and liquidity.

Regulatory Proposals

In addition certainto the regulatory rule changes that have already been adopted (as discussed above), both the Federal Reserve Board and the Basel Committee have proposed other changes, which are discussed below. The full impact of Group Inc.’s non-bank subsidiariesthese proposals on the firm will not be known with certainty until after any resulting rules are subjectfinalized and market practices develop under the final rules. Furthermore, these proposals, the Dodd-Frank Act, other reform initiatives proposed and announced by the U.S. federal bank regulatory agencies, the Basel Committee, and other governmental entities and regulators (including the European Union (EU), the PRA and the FCA) are not in all cases consistent with one another, which adds further uncertainty to separate regulatory limitations on dividendsour future capital, leverage and distributions, includingliquidity requirements, and those of our broker-dealer and our insurance subsidiaries as described below.subsidiaries.

| 12 | Goldman Sachs |

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Federal Reserve Board Proposals. In December 2014, the Federal Reserve Board proposed a rule to establish risk-based capital surcharges for U.S. Global Systemically Important Banks (G-SIBs). For these institutions, the proposed rule would implement the framework developed by the Basel Committee for assessing the global systemic importance of banking institutions and determining the range of additional CET1 that should be maintained by those deemed to be G-SIBs. Under the Basel Committee’s framework, the required amount of additional CET1 forG-SIBs will initially range from 1% to 2.5% and could be higher in the future for a banking institution that increases its systemic footprint (e.g., by increasing total assets). The Federal Reserve Board stated that its framework would result in surcharges higher than those calculated under the methodology published by the Basel Committee, with expected surcharges ranging from 1% to 4.5%. The proposed rule treats the Basel Committee’s methodology as a floor and introduces an alternative calculation to determine the applicable surcharge, which includes a significantly higher surcharge for systemic risk and, as part of the calculation of the applicable surcharge, a new factor based on a G-SIB’s use of short-term wholesale funding. Under the Federal Reserve Board’s proposed rule, U.S.G-SIBs would be required to meet the capital surcharges on a phased-in basis beginning in 2016 through 2019. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Equity Capital Management and Regulatory Capital” in Part II, Item 7 of the 2014 Form 10-K for additional information about our minimum capital ratios and capital buffers.

In December 2011, the Federal Reserve Board proposed rules to implement the enhanced prudential standards and early remediation requirements contemplated by the Dodd-Frank Act. Although most components of these proposals have now been addressed in final rules that are described above, the single-counterparty credit limits and early remediation requirements are still under consideration. The proposed single-counterparty credit limits impose more stringent requirements for credit exposure among major financial institutions, which (together with other provisions incorporated into the Basel III capital rules) may affect our ability to transact or hedge with other financial institutions. The proposed early remediation rules are modeled on the prompt corrective action regime, described below, but are designed to require action to begin in earlier stages of a company’s financial distress, based on a range of triggers, including capital and leverage, stress test results, liquidity and risk management.

Basel Committee and Financial Stability Board Proposals. The Basel Committee published its final guidelines for calculating incremental capital requirements for domestic systemically important banking institutions (D-SIBs). These guidelines are complementary to the framework outlined above for G-SIBs, but are more principles-based in order to provide an appropriate degree of national discretion. The impact of these guidelines on the regulatory capital requirements of GS Bank USA, GSI and other of our subsidiaries will depend on how they are implemented by the banking and non-banking regulators in the United States and other jurisdictions.

The Basel Committee has recently issued several updates which propose further changes to capital regulations. In particular, it has finalized a revised standard approach for calculating RWAs for counterparty credit risk on derivatives exposures (“Standardized Approach for measuring Counterparty Credit Risk exposures,” known as “SA-CCR”). In addition, it has published guidelines for measuring and controlling large exposures (“Supervisory Framework for measuring and controlling Large Exposures”), and issued an updated framework for regulatory capital treatment of banking book securitizations.

The Basel Committee has also issued consultation papers on a “Fundamental Review of the Trading Book” and on the design of a capital floor framework based on the standardized approach. The impact of all of these developments on the firm (including RWAs and regulatory capital ratios) will not be known until after any resulting rules are finalized by the U.S. federal bank regulatory agencies.

In November 2014, the Financial Stability Board issued a set of principles and a term sheet on a new minimum standard for “total loss-absorbing capacity” of G-SIBs and indicated that it expects to finalize its proposal by late 2015. The proposal would require G-SIBs to maintain minimum ratios of regulatory capital plus certain types of debt instruments to RWAs and leverage exposure. Under the proposal, the requirements will be effective no earlier than January 1, 2019. The proposal is subject to change, and its impact on us will depend on, among other things, how it is implemented by the U.S. federal bank regulatory agencies.

| Goldman Sachs 2014 Form 10-K | 13 |

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Resolution and Recovery Plans

As required by the Dodd-Frank Act, the Federal Reserve Board and FDIC have jointly issued a rule requiring each bank holding company with over $50 billion in assets and each designated systemically important financial institution to provide to regulators an annual plan for its rapid and orderly resolution in the event of material financial distress or failure (resolution plan). Our resolution plan must, among other things, demonstrate that GS Bank USA is adequately protected from risks arising from our other entities. The regulators’ joint rule sets specific standards for the resolution plans, including requiring a detailed resolution strategy and analyses of the company’s material entities, organizational structure, interconnections and interdependencies, and management information systems, among other elements. Group Inc. submitted resolution plans to its regulators in 2012, 2013 and 2014. In August 2014, the Federal Reserve Board and the FDIC indicated that Group Inc. and other large industry participants had certain shortcomings in the 2013 resolution plans that must be addressed in the 2015 resolution plans, which are required to be submitted on or before July 1, 2015. If we fail to cure the deficiencies in a timely manner and the Federal Reserve Board and the FDIC jointly determine that our resolution plan, after any permitted resubmission, is not credible, the Federal Reserve Board and the FDIC may jointly impose more stringent capital, leverage or liquidity requirements on us or restrictions on our growth, activities or operations until we submit a plan that remedies the deficiencies. If the Federal Reserve Board and the FDIC ultimately determine that we have been unable to remedy the deficiencies, they may jointly order us to divest assets or operations in order to facilitate our orderly resolution in the event of our failure.