UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20112012

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period fromto

Commission File Number: 0-51937001-34927

Compass Diversified Holdings

(Exact name of registrant as specified in its charter)

| Delaware | 57-6218917 | |

(Jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

Commission File Number: 0-51938001-34926

Compass Group Diversified Holdings LLC

(Exact name of registrant as specified in its charter)

| Delaware | 20-3812051 | |

(Jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

Sixty One Wilton Road Second Floor Westport, CT | 06880 | |

| (Address of principal executive offices) | (Zip Code) |

(203) 221-1703

(Registrants’ telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

| Shares representing beneficial interests in Compass Diversified Holdings (“trust shares”) | New York Stock Exchange |

Securities registered pursuant to Section 12 (g) of the Act: None

Indicate by check mark if the registrants are collectively a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrants are collectively not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrants (1) have filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrants were required to file such reports), and (2) have been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrants have submitted electronically and posted on their corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrants’ knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrants are collectively a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrants are collectively a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the outstanding shares of trust stock held by non-affiliates of Compass Diversified Holdings at June 30, 20112012 was $650,945,059$550,707,370 based on the closing price on the New York Stock Exchange on that date. For purposes of the foregoing calculation only, all directors and officers of the registrant have been deemed affiliates.

There were 48,300,000 shares of trust stock without par value outstanding at February 25, 2012.2013.

Documents Incorporated by Reference

Certain information in the registrant’s definitive proxy statement to be filed with the Commission relating to the registrant’s 20112012 Annual Meeting of Stockholders is incorporated by reference into Part III.

| ||||||

| Page | ||||||

Item 1. | ||||||

Item 1A. | ||||||

Item 1B. | ||||||

Item 2. | ||||||

Item 3. | ||||||

Item 4. | ||||||

Item 5. | ||||||

Item 6 | ||||||

Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |||||

Item 7A. | ||||||

Item 8. | ||||||

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |||||

Item 9A | ||||||

Item 9B. | ||||||

Item 10. | ||||||

Item 11. | ||||||

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |||||

Item 13. | Certain Relationships and Related Transactions and Director Independence | |||||

Item 14. | ||||||

Item 15. | ||||||

NOTE TO READER

In reading this Annual Report on Form 10-K, references to:

the “Trust” and “Holdings” refer to Compass Diversified Holdings;

“businesses”, “operating segments”, “subsidiaries” and “reporting units” all refer to, collectively, the businesses controlled by the Company;

the “Company” refer to Compass Group Diversified Holdings LLC;

the “Manager” refer to Compass Group Management LLC (“CGM”);

the “initial businesses” refer to, collectively, Staffmark Holdings, Inc., Crosman Acquisition Corporation, Compass AC Holdings, Inc. and Silvue Technologies Group, Inc.;

the “2007 acquisitions” refer to, collectively, the acquisitions of Aeroglide Corporation, HALO Branded Solutions and American Furniture Manufacturing;

the “2008 acquisitions” refer to, collectively, the acquisitions of Fox Factory Inc. and Staffmark Investment LLC;

the “2010 acquisitions” refer to, collectively, the acquisitions of Liberty Safe and Security Products, LLC and ERGObabyErgobaby Carrier, Inc.;

the “2011 acquisition” refer to the acquisition of CamelBak Products, LLC;

the “2012 acquisition” refer to the acquisition of Arnold Magnetic Technologies;

the “2007 disposition” refer to the sale of Crosman Acquisition Corporation;

the “2008 dispositions” refer to, collectively, the sales of Aeroglide Corporation and Silvue Technologies Group, Inc.;

the “2011 disposition” refersrefer to the sale of Staffmark Holdings, Inc.;

the “2012 disposition” refer to the sale of HALO Branded Solutions.;

the “Trust Agreement” refer to the amended and restated Trust Agreement of the Trust dated as of April 25, 2007;

the “Prior Credit Agreement” refer to the Credit Agreement with a group of lenders led by Madison Capital, LLC which provided for a “Prior Revolving Credit Facility” and a “Prior Term Loan Facility”;

the “Credit Facility” refer to the Credit Facility with a group of lenders led by TD Securities (USA) LLC (“TD Securities”) which provides for a Revolving Credit Facility and a Term Loan Facility;

the “Revolving Credit Facility” refer to the $290 million Revolving Credit Facility provided by the Credit Facility that matures in December 2016;

the “Term Loan Facility” refer to the $225$252.5 million Term Loan Facility, as of December 31, 2011,2012, provided by the Credit Facility that matures in December 2017;

the “LLC Agreement” refer to the second amended and restated operating agreement of the Company dated as of January 9, 2007; and

“we”, “us” and “our” refer to the Trust, the Company and the businesses together.

Statement Regarding Forward-Looking Disclosure

This Annual Report on Form 10-K, including the sections entitled “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business,” contains forward-looking statements. We may, in some cases, use words such as “project,” “predict,” “believe,” “anticipate,” “plan,” “expect,” “estimate,” “intend,” “should,” “would,” “could,” “potentially,” or “may” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Forward-looking statements in this Annual Report on Form 10-K are subject to a number of risks and uncertainties, some of which are beyond our control, including, among other things:

our ability to successfully operate our businesses on a combined basis, and to effectively integrate and improve any future acquisitions;

our ability to remove our Manager and our Manager’s right to resign;

our trust and organizational structure, which may limit our ability to meet our dividend and distribution policy;

our ability to service and comply with the terms of our indebtedness;

our cash flow available for distribution and our ability to make distributions in the future to our shareholders;

our ability to pay the management fee, profit allocation when due and pay the put price if and when due;

our ability to make and finance future acquisitions;

our ability to implement our acquisition and management strategies;

the regulatory environment in which our businesses operate;

trends in the industries in which our businesses operate;

changes in general economic or business conditions or economic or demographic trends in the United States and other countries in which we have a presence, including changes in interest rates and inflation;

environmental risks affecting the business or operations of our businesses;

our and our Manager’s ability to retain or replace qualified employees of our businesses and our Manager;

costs and effects of legal and administrative proceedings, settlements, investigations and claims; and

extraordinary or force majeure events affecting the business or operations of our businesses.

including, among other things:

Our actual results, performance, prospects or opportunities could differ materially from those expressed in or implied by the forward-looking statements. A description of some of the risks that could cause our actual results to differ appears under the section “Risk Factors”. Additional risks of which we are not currently aware or which we currently deem immaterial could also cause our actual results to differ.

In light of these risks, uncertainties and assumptions, you should not place undue reliance on any forward-looking statements. The forward-looking events discussed in this Annual Report on Form 10-K may not occur. These forward-looking statements are made as of the date of this Annual Report. We undertake no obligation to publicly update or revise any forward-looking statements to reflect subsequent events or circumstances, whether as a result of new information, future events or otherwise, except as required by law.

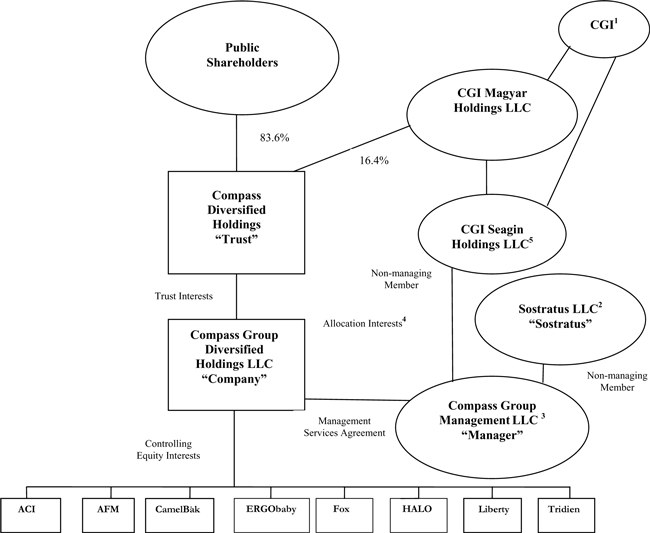

Compass Diversified Holdings, a Delaware statutory trust (“Holdings”, or the “Trust”), was incorporated in Delaware on November 18, 2005. Compass Group Diversified Holdings, LLC, a Delaware limited liability Company (the “Company”), was also formed on November 18, 2005. The Trust and the Company (collectively “CODI”) were formed to acquire and manage a group of small and middle-market businesses headquartered in North America. The Trust is the sole owner of 100% of the Trust Interests, as defined in our LLC Agreement, of the Company. Pursuant to thatthe LLC Agreement, the Trust owns an identical number of Trust Interests in the Company as exist for the number of outstanding shares of the Trust. Accordingly, our shareholders are treated as beneficial owners of Trust Interests in the Company and, as such, are subject to tax under partnership income tax provisions.

The Company is the operating entity with a board of directors whose corporate governance responsibilities are similar to that of a Delaware corporation. The Company’s board of directors oversees the management of the Company and our businesses and the performance of Compass Group Management LLC (“CGM” or our “Manager”). Our Manager is the sole owner of our Allocation Interests, as defined in our LLC Agreement.

Overview

We acquire controlling interests in and actively manage businesses that we believe operate in industries with long-term macroeconomic growth opportunities, and that have positive and stable cash flows, face minimal threats of technological or competitive obsolescence and have strong management teams largely in place.

Our unique public structure provides investors with an opportunity to participate in the ownership and growth of companies which have historically been owned by private equity firms, wealthy individuals or families. Through the acquisition of a diversified group of businesses with these characteristics, we also offer investors an opportunity to diversify their own portfolio risk while participating in the ongoing cash flows of those businesses through the receipt of distributions.

Our disciplined approach to our target market provides opportunities to methodically purchase attractive businesses at values that are accretive to our shareholders. For sellers of businesses, our unique structure allows us to acquire businesses efficiently with little or no financing contingencies and, following acquisition, to provide our businesses with substantial access to growth capital.

We believe that private company operators and corporate parents looking to sell their businesses may consider us an attractive purchaser because of our ability to:

provide ongoing strategic and financial support for their businesses;

maintain a long-term outlook as to the ownership of those businesses where such an outlook is required for maximization of our shareholders’ return on investment; and

consummate transactions efficiently without being dependent on third-party financing on a transaction-by-transaction basis.

In particular, we believe that our outlook on length of ownership and active management on our part may alleviate the concern that many private company operators and parent companies may have with regard to their businesses going through multiple sale processes in a short period of time. We believe this outlook both reduces the risk that businesses may be sold at unfavorable points in the overall market cycle and enhances our ability to develop a comprehensive strategy to grow the earnings and cash flows of our businesses, which we expect will better enable us to meet our long-term objective of paying distributions to our shareholders and increasing shareholder value.

Finally, we have found that our ability to acquire businesses without the cumbersome delays and conditions typical of third party transactional financing can be very appealing to sellers of businesses who are interested in confidentiality and certainty to close.

We believe our management team’s strong relationships with industry executives, accountants, attorneys, business brokers, commercial and investment bankers, and other potential sources of acquisition opportunities offer us substantial opportunities to assess small to middle market businesses that may be available for acquisition. In addition, the flexibility, creativity, experience and expertise of our management team in structuring transactions allows us to consider non-traditional and complex transactions tailored to fit a specific acquisition target.

In terms of the businesses in which we have a controlling interest as of December 31, 2011,2012, we believe that these businesses have strong management teams, operate in strong markets with defensible market niches and maintain long standing customer relationships. We believe that the strength of this model, which provides for significant industry, customer and geographic diversity, has become even more apparent in the current challenging economic environment.

20112012 Highlights

AcquisitionsAcquisition of Arnold Magnetics

On August 24, 2011,March 5, 2012, we purchased a 96.6% controlling interest (on a primary and fully diluted basis) in CamelBak Products, LLC (“CamelBak”)Arnold Magnetics, with headquarters in Petaluma, California. CamelBak invented the hands-free hydration categoryRochester, NY. Arnold Magnetics has an operating history of more than 100 years and is thea leading global leadermanufacturer of engineered magnetic solutions for a wide range of specialty applications and end-markets, including energy, medical, aerospace and defense, consumer electronics, general industrial and automotive. From its nine manufacturing facilities located in the designUnited States, the United Kingdom, Switzerland and manufacture of personal hydrationChina, the company produces high performance permanent magnets, flexible magnets and precision foil products for outdoor, recreationthat are mission critical in motors, generators, sensors and military use. other systems and components. Based on its long-term relationships, Arnold Magnetics has built a diverse and blue-chip customer base totaling more than 2,000 clients worldwide.

The purchase price, including minorityproceeds from non-controlling interests, of $258.6was approximately $130.5 million (excluding acquisition-related costs) and was based on a total enterprise value of $245$124.2 million and included $13.6approximately $6.3 million in cash and working capital. Acquisition related costs were approximately $4.8 million. We funded the acquisition through drawingsavailable cash on hand and a draw of $25 million on our Prior Revolving Credit Facility as well as through funds provided by a private placement of 1,575,000 of our common shares to CGI Magyer Holdings LLC (“CMH”), our largest shareholder. An affiliate of CMH also purchased $45.0 million of convertible preferred stockFacility. Arnold’s management and certain other investors invested in CamelBak Acquisition Corp. a majority owned subsidiary of us. Otherthe transaction alongside us, collectively representing approximately 3.4% in initial non-controlling interest holders, including management of CamelBak, purchased $2.0 million of CamelBak common stock. on a primary and fully diluted basis. CGM acted as an advisor to us in the transaction and received fees and expense payments totaling approximately $1.2 million.

Preferred Stock Redemption

On March 6, 2012, CamelBakwe redeemed itsCamelBak’s 11% convertible preferred stock for $45.3 million plus accrued dividends of $2.7 million, from an affiliate of CMH ($47.7 million), ourCGI Magyar Holdings LLC, CODI’s largest shareholder, and noncontrolling shareholders ($0.3 million).shareholder. The redemption was funded by intercompany debtwith available cash on hand.

Debt Re-pricing

On April 2, 2012, we exercised our option for an incremental term loan in the amount of $30 million. The incremental term loan was issued at 99% of par value and increased the term loans outstanding under the Credit Facility from approximately $224.4 million to approximately $254.4 million. In addition, in connection with the option we reduced the margin on Term Loan Facility LIBOR Loans from 6.00% to 5.00%, Base Rate Loans from 5.00% to 4.00% and reduced the LIBOR floor from 1.50% to 1.25%. We paid an equity contribution from usamendment fee of $19.2approximately $2.2 million, and $25.9 million, respectively. In addition, noncontrolling shareholdersincurred additional fees and expenses of CamelBak invested $2.9 millionapproximately $0.6 million. Net proceeds from this incremental term loan were used to reduce outstanding loans on the Revolving Credit Facility.

Sale of equity in order for us and noncontrolling shareholders to maintain existing ownership percentages of CamelBak common stock of 89.9% and 10.1%, respectively.HALO

On November 21, 2011 our majority owned subsidiary, The ERGObaby Carrier, Inc. (“ERGObaby”) acquiredMay 1, 2012, we sold all of the issued and outstanding capital stock of Orbit Baby, Inc. (“Orbit Baby”) for $17.5 million. Founded in 2004 and based in Newark, California, Orbit Baby produces and markets a premium line of stroller travel systems, including car seats, strollers and bassinets that are interchangeable using a patented hub ring.

Disposition

On October 17, 2011, we sold our majority-owned subsidiary, StaffmarkHALO to Candlelight Investment Holdings, Inc. (“Staffmark”) for aThe total enterprise value received for HALO was $76.5 million.

At the closing, we received approximately $66.0 million in cash in respect of $295 millionour debt and equity interests in HALO and for the payment of accrued interest and fees after payments to a subsidiarynon-controlling shareholders and payment of Japan-based Recruit Co., Ltd.all transaction expenses. We received an additional approximately $217.2$0.8 million at the time of sale in 2012 that were held in escrow. The net proceeds after deducting fees, costs and non-controlling shareholder’s interests.were used to repay outstanding debt under our Revolving Credit Facility. We recorded a gainloss on the sale of $88.6 million and used the net proceeds to pay down our Prior Revolving Credit Facility.HALO of $0.5 million.

Refinancing

On October 27, 2011, we entered into a new Credit Facility which includes a Revolving Credit Facility totaling $290 million and a Term Loan Facility totaling $225 million. This Credit Facility, with a group of lenders led by TD Securities aggregating $515 million replaces our Prior Credit Agreement which was with a group of lenders led by Madison Capital, LLC. The Revolving Credit Facility is for a term of five years and the Term Loan Facility is for a term of six years.

20112012 Distributions

For the 20112012 fiscal year we declared and paid distributions to our shareholders totaling $1.44 per share.

The following is a brief summary of the businesses in which we own a controlling interest at December 31, 2011:2012:

Advanced Circuits

Compass AC Holdings, Inc. (“Advanced Circuits” or “ACI”), headquartered in Aurora, Colorado, is a provider of prototype, quick-turn and production rigid printed circuit boards, or “PCBs”, throughout the United States. PCBs are a vital component of virtually all electronic products. The prototype and quick-turn portions of the PCB industry are characterized by customers requiring high levels of responsiveness, technical support and timely delivery. We made loans to and purchased a controlling interest in Advanced Circuits, on May 16, 2006, for approximately $81.0 million. We currently own 69.6%69.4% of the outstanding stock of Advanced Circuits on a primary basis and 69.4% on a fully diluted basis.

American Furniture

AFM Holding Corporation (“American Furniture” or “AFM”) headquartered in Ecru, Mississippi, is a leader in the manufacturing of low-cost upholstered stationary and motion furniture, including sofas, loveseats, sectionals, recliners and complementary products to the promotional furniture market. We made loans to and purchased a controlling interest in AFM on August 31, 2007 for approximately $97.0 million. As a result of the recapitalization of American Furniture’s outstanding debt with additional equity during 2011, weWe currently own approximately 99.9% of AFM’s outstanding stock on a primary basis and fully diluted basis.

Arnold

AMT Acquisition Corporation (“Arnold” or “Arnold Magnetics”), headquartered in Rochester, NY, with nine additional facilities worldwide, is a manufacturer of engineered, application specific permanent magnets. Arnold Magnetics products are used in applications such as general industrial, reprographic systems, aerospace and defense, advertising and promotional, consumer and appliance, energy, automotive and medical technology. Arnold Magnetics is the largest U.S. manufacturer of engineered magnets as well as only one of two domestic producers to design, engineer and manufacture rare earth magnetic solutions. We made loans to, and purchased a controlling interest in Arnold on March 5, 2012 for approximately $122.4 million. We currently own 96.7% of the outstanding stock of Arnold on a primary basis and 87.6% on a fully diluted basis.

CamelBak

CamelBak Products LLC (“CamelBak”), headquartered in Petaluma, California, is a diversified hydration and personal protection platform offering products for outdoor, recreation and military applications. CamelBak offers a broad range of recreational / military hydration packs, reusable water bottles, specialized military gloves and performance accessories. We made loans to, and purchased a controlling interest in, CamelBak on August 24, 2011 for approximately $211.6 million. We currently own 89.9% of the outstanding stock of CamelBak on a primary basis and 76.7%79.7% on a fully diluted basis.

ERGObabyErgobaby

Ergobaby Carrier, Inc. (“Ergobaby”), headquartered in Los Angeles, California, is a premier designer, marketermanufacturer and distributor of baby wearing products, stroller travel systems and accessories. ERGObaby’sErgobaby’s reputation for product innovation, reliability and safety has led to numerous awards and accolades from consumer surveys and publications. ERGObabyErgobaby offers a broad range of wearable baby carriers, stroller travel systems and related products that are sold through more than 900600 retailers and web shops in the United States and internationally. On November 18, 2011 ERGObaby acquired the premium stroller manufacturer and distributer, Orbit Baby for approximately $17.5 million. We made loans to, and purchased a controlling interest in, ERGObabyErgobaby on September 16, 2010 for approximately $85.2 million. We currently own 81.1% of the outstanding stock of ERGObabyErgobaby on a primary basis and 74.6%77.1% on a fully diluted basis.

Fox

Fox Factory Holding Corp. (“Fox”) headquartered in Scotts Valley, California, is a designer, manufacturer and marketer of high end suspension products for mountain bikes and power sports, which includes; all-terrain vehicles, snowmobiles and other off-road vehicles. Fox acts both as a tier one supplier to leading action sports original equipment manufacturers (“OEM”) and provides after-market products to retailers and distributors (“Aftermarket”). Fox’s products are recognized as the industry’s performance leaders by retailers and end-users alike. We made loans to and purchased a controlling interest in Fox on January 4, 2008, for approximately $80.4 million. We currently own 78.0%75.8% of the outstanding common stock on a primary basis and 67.9% on a fully diluted basis.

HALO

HALO Lee Wayne LLC, operating under the brand names of HALO and Lee Wayne (“HALO”), headquartered in Sterling, Illinois, serves as a one-stop shop for over 40,000 customers providing design, sourcing, management and fulfillment services across all categories of its customer promotional product needs in effectively communicating a logo or marketing message to a target audience. HALO has established itself as a leader in the promotional products and marketing industry through its focus on servicing its group of over 600 account executives. We made loans to and purchased a controlling interest in HALO on February 28, 2007 for approximately $62.0 million. We currently own 88.7% of the outstanding common stock on a primary basis and 72.3%70.6% on a fully diluted basis.

Liberty Safe

Liberty Safe and Security Products, Inc. (“Liberty Safe” or “Liberty”), headquartered in Payson, Utah, is a designer, manufacturer and marketer of premium home and gun safes in North America. From it’s over 200,000 square foot manufacturing facility, Liberty produces a wide range of home and gun safe models in a broad assortment of sizes, features and styles. We made loans to and purchased a controlling interest in Liberty Safe on March 31, 2010 for approximately $70.2 million. We currently own 96.2% of the outstanding stock of Liberty Safe on a primary basis and 87.6%86.7% on a fully diluted basis.

Tridien

Anodyne Medical Device, Inc. (“Anodyne”, which was rebranded as “Tridien” in September 2010) headquartered in Coral Springs, Florida, is a leading designer and manufacturer of powered and non-powered medical therapeutic support services and patient positioning devices serving the acute care, long-term care and home health care markets. Tridien is one of the nation’s leading designers and manufacturers of specialty therapeutic support surfaces and is able to manufacture products in multiple locations to better serve a national customer base. We made loans to and purchased a controlling interest in Tridien from CGI on August 1, 2006 for approximately $31.0 million. We currently own 73.9%81.3% of the outstanding capital stock on a primary basis and 60.0%67.4% on a fully diluted basis.

Our businesses also represent our operating segments. See “ – Our Businesses” and “Note E – Operating Segment Data” to our Consolidated Financial Statements for further discussion of our businesses as our operating segments.

Tax Reporting

Information returns will be filed by the Trust and the Company with the IRS, as required, with respect to income, gain, loss, deduction and other items derived from the company’s activities. The Company has and will file a partnership return with the IRS and intends to issue a Schedule K-1 to the trustee. The trustee intends to provide information to each holder of shares using a monthly convention as the calculation period. For 2011,2012, and future years, the Trust has, and will continue to file a Form 1065 and issue Schedule K-1 to shareholders. For 2011,2012, we delivered the Schedule K-1 to shareholders within the same time frame as we delivered the schedule to shareholders for the 20102011 and 20092010 taxable year. The relevant and necessary information for tax purposes is readily available electronically through our website. Each holder will be deemed to have consented to provide relevant information, and if the shares are held through a broker or other nominee, to allow such broker or other nominee to provide such information as is reasonably requested by us for purposes of complying with our tax reporting obligations.

WHERE YOU CAN FIND ADDITIONAL INFORMATION

We have filed with the SEC Forms S-1 and S-3 under the Securities Act, and Forms 10-Q, 10-K, and 8-K under the Exchange Act, which include exhibits, schedules and amendments. In addition, copies of such reports are available free of charge that can be accessed indirectly through our websitehttp://www.compassdiversifiedholdings.com and are available as soon as reasonably practicable after such documents are electronically filed or furnished with the SEC.

| (1) | CGI and its affiliates beneficially own approximately 16.4% of the Trust shares and is our single largest holder. Mr. |

| (2) | Owned by members of our |

| (3) | Mr. |

| (4) | The Allocation Interests, which carry the right to receive a profit allocation, represent less than 0.1% equity interest in the Company. |

| (5) | Mr. Day is a non-managing member. |

Our Manager

Our Manager, CGM, has been engaged to manage the day-to-day operations and affairs of the Company and to execute our strategy, as discussed below. Our management team has worked together since 1998. Collectively, our management team has approximately 90 years ofextensive experience in acquiring and managing small and middle market businesses. We believe our Manager is unique in the marketplace in terms of the success and experience of its employees in acquiring and managing diverse businesses of the size and general nature of our businesses. We believe this experience will provide us with an advantage in executing our overall strategy. Our management team devotes a majority of its time to the affairs of the Company.

We have entered into a management services agreement (the “Management Services Agreement”) pursuant to which our Manager manages the day-to-day operations and affairs of the Company and oversees the management and operations of our businesses. We pay our Manager a quarterly management fee for the services it performs on our behalf. In addition, our Manager receives a profit allocation with respect to its Allocation Interests in us. See Part III, Item 13 “Certain Relationships and Related Transactions” for further descriptions of the management fees and profit allocation to be paid to our Manager. In consideration of our Manager’s acquisition of the Allocation Interests, we entered into a Supplemental Put agreement with our Manager pursuant to which our Manager has the right to cause us to purchase its Allocation Interests upon termination of the Management Services Agreement. Our Manager owns 100% of the Allocation Interests of the Company, for which it paid $0.1 million.

The Company’s Chief Executive Officer and Chief Financial Officer are employees of our Manager and have been seconded to us. Neither the Trust nor the Company has any other employees. Although our Chief Executive Officer and Chief Financial Officer are employees of our Manager, they report directly to the Company’s board of directors. The management fee paid to our Manager covers all expenses related to the services performed by our Manager, including the compensation of our Chief Executive Officer and other personnel providing services to us. The Company reimburses our Manager for the salary and related costs and expenses of our Chief Financial Officer and his staff, who dedicate substantially all of their time to the affairs of the Company.

See Part III, Item 13, “Certain Relationships and Related Party Transactions and Director Independence”.

Market Opportunity

We acquire and actively manage small and middle market businesses. We characterize small to middle market businesses as those that generate annual cash flows of up to $60 million. We believe that the merger and acquisition market for small to middle market businesses is highly fragmented and provides opportunities to purchase businesses at attractive prices. We believe that the following factors contribute to lower acquisition multiples for small and middle market businesses:

there are fewer potential acquirers for these businesses;

third-party financing generally is less available for these acquisitions;

sellers of these businesses frequently consider non-economic factors, such as continuing board membership or the effect of the sale on their employees; and

these businesses are less frequently sold pursuant to an auction process.

We believe that opportunities exist to augment existing management at such businesses and improve the performance of these businesses upon their acquisition. In the past, our management team has acquired businesses that were owned by entrepreneurs or large corporate parents. In these cases, our management team has frequently found that there have been opportunities to further build upon the management teams of acquired businesses beyond those in existence at the time of acquisition. In addition, our management team has frequently found that financial reporting and management information systems of acquired businesses may be improved, both of which can lead to improvements in earnings and cash flow. Finally, because these businesses tend to be too small to have their own corporate development efforts, we believe opportunities exist to assist these businesses as they pursue organic or external growth strategies that were often not pursued by their previous owners. We believe the current financing environment is conducive to our ability to consummate acquisitions.

Our Strategy

We have two primary strategies that we use in order to provide distributions to our shareholders and increase shareholder value. First, we focus on growing the earnings and cash flow from our businesses. We believe that the scale and scope of our businesses give us a diverse base of cash flow upon which to further build. Second, we identify, perform due diligence on, negotiate and consummate additional platform acquisitions of small to middle market businesses in attractive industry sectors in accordance with acquisition criteria established by the board of directors

Management Strategy

Our management strategy involves the proactive financial and operational management of the businesses we own in order to pay distributions to our shareholders and increase shareholder value. Our Manager oversees and supports the management teams of each of our businesses by, among other things:

recruiting and retaining talented managers to operate our businesses using structured incentive compensation programs, including minority equity ownership, tailored to each business;

regularly monitoring financial and operational performance, instilling consistent financial discipline, and supporting management in the development and implementation of information systems to effectively achieve these goals;

assisting management in their analysis and pursuit of prudent organic growth strategies;

identifying and working with management to execute attractive external growth and acquisition opportunities;

assist management in controlling and right-sizing overhead costs, particularly in the current challenging economic environment; and

forming strong subsidiary level boards of directors to supplement management in their development and implementation of strategic goals and objectives.

Specifically, while our businesses have different growth opportunities and potential rates of growth, we expect our Manager to work with the management teams of each of our businesses to increase the value of, and cash generated by, each business through various initiatives, including:

making selective capital investments to expand geographic reach, increase capacity, or reduce manufacturing costs of our businesses;

investing in product research and development for new products, processes or services for customers;

improving and expanding existing sales and marketing programs;

pursuing reductions in operating costs through improved operational efficiency or outsourcing of certain processes and products; and

consolidating or improving management of certain overhead functions.

In terms of the difficult economic environment we are currently facing, we and each of our subsidiary management teams have been, and will continue to be, intensely focused on performance and cost control measures through this economic cycle.

Our businesses typically acquire and integrate complementary businesses. We believe that complementary acquisitions will improve our overall financial and operational performance by allowing us to:

leverage manufacturing and distribution operations;

leverage branding and marketing programs, as well as customer relationships;

add experienced management or management expertise;

increase market share and penetrate new markets; and

realize cost synergies by allocating the corporate overhead expenses of our businesses across a larger number of businesses and by implementing and coordinating improved management practices.

We incur third party debt financing almost entirely at the Company level, which we use, in combination with our equity capital, to provide debt financing to each of our businesses and to acquire additional businesses We believe this financing structure is beneficial to the financial and operational activities of each of our businesses by aligning our interests as both equity holders of, and lenders to, our businesses, in a manner that we believe is more efficient than our businesses borrowing from third-party lenders.

Acquisition Strategy

Our acquisition strategy involves the acquisition of businesses that we expect to produce stable and growing earnings and cash flow. In this respect, we expect to make acquisitions in industries other than those in which our businesses currently operate if we believe an acquisition presents an attractive opportunity. We believe that attractive opportunities will continue to present themselves, as private sector owners seek to monetize their interests in longstanding and privately-held businesses and large corporate parents seek to dispose of their “non-core” operations.

Our ideal acquisition candidate has the following characteristics:

is an established North American based company;

maintains a significant market share in defensible industry niche (i.e., has a “reason to exist”);

has a solid and proven management team with meaningful incentives;

has low technological and/or product obsolescence risk; and

maintains a diversified customer and supplier base.

We benefit from our Manager’s ability to identify potential diverse acquisition opportunities in a variety of industries. In addition, we rely upon our management team’s experience and expertise in researching and valuing prospective target businesses, as well as negotiating the ultimate acquisition of such target businesses. In particular, because there may be a lack of information available about these target businesses, which may make it more difficult to understand or appropriately value such target businesses, on our behalf, our Manager:

engages in a substantial level of internal and third-party due diligence;

critically evaluates the management team;

identifies and assesses any financial and operational strengths and weaknesses of the target business;

analyzes comparable businesses to assess financial and operational performances relative to industry competitors;

actively researches and evaluates information on the relevant industry; and

thoroughly negotiates appropriate terms and conditions of any acquisition.

The process of acquiring new businesses is both time-consuming and complex. Our management team historically has taken from two to twenty-four months to perform due diligence, negotiate and close acquisitions. Although our management team is always at various stages of evaluating several transactions at any given time, there may be periods of time during which our management team does not recommend any new acquisitions to us. Even if an acquisition is recommended by our management team, our board of director’s may not approve it.

Upon acquisition of a new business, we rely on our manager’s team’s experience and expertise to work efficiently and effectively with the management of the new business to jointly develop and execute a successful business plan.

We believe, due to our financing structure, in which both equity and debt capital are raised at the Company level, allowing us to acquire businesses without transaction specific financing that the current difficult financing environment is conducive to our ability to consummate transactions that may be attractive in both the short- and long-term.

In addition to acquiring businesses, we sell businesses that we own from time to time when attractive opportunities arise that outweigh the value that we believe we will be able to bring such businesses consistent with our long-term investment strategy. As such, our decision to sell a business is based on our belief that doing so will increase shareholder value to a greater extent than through our continued ownership of that business. Upon the sale of a business, we may use the proceeds to retire debt or retain proceeds for acquisitions or general corporate purposes. We do not expect to make special distributions at the time of a sale of one of our businesses; instead, we expect to pay shareholder distributions over time through the earnings and cash flows of our businesses.

Since our inception in May 2006, we have recorded gains on sales of our businesses of over $197 million, or $4.08 per share.approximately $198 million. We sold Crosman in January 2007, and Aeroglide and Silvue in June 2008, and Staffmark in 2011.2011 and HALO in 2012. We sold Crosman, our

majority owned recreational products company for approximately $143 million and our net proceeds and gain on sale were approximately $110 million and $36 million, respectively. We sold Aeroglide, our majority owned designer and manufacturer of industrial drying and cooling equipment for approximately $95 million and our net proceeds and gain on sale were approximately $78 million and $34 million, respectively. We sold Silvue, our majority owned developer and producer of proprietary, high performance liquid coating systems for approximately $95 million and our net proceeds and gain on sale were approximately $64 million and $39 million, respectively and werespectively. We sold Staffmark, our majority-owned provider of temporary staffing solutions subsidiary for approximately $295 million and our net proceeds and gain on sale were approximately $217 million and $89 million, respectively.respectively We sold HALO, our majority owned fulfillment provider of promotional items for $76.5 million and our net proceeds upon sale were approximately $66.0 million and our loss on sale was approximately $0.5 million.

Strategic Advantages

Based on the experience of our management team and its ability to identify and negotiate acquisitions, we believe we are well-positioned to acquire additional businesses. Our management team has strong relationships with business brokers, investment and commercial bankers, accountants, attorneys and other potential sources of acquisition opportunities. In addition, our management team also has a successful track record of acquiring and managing small to middle market businesses in various industries. In negotiating these acquisitions, we believe our management team has been able to successfully navigate complex situations surrounding acquisitions, including corporate spin-offs, transitions of family-owned businesses, management buy-outs and reorganizations.

Our management team has a large network of approximately 2,000 deal intermediaries who we expect to expose us to potential acquisitions. Through this network, as well as our management team’s proprietary transaction sourcing efforts, we have a substantial pipeline of potential acquisition targets. Our management team also has a well-established network of contacts, including professional managers, attorneys, accountants and other third-party consultants and advisors, who may be available to assist us in the performance of due diligence and the negotiation of acquisitions, as well as the management and operation of our acquired businesses.

Finally, because we intend to fund acquisitions through the utilization of our Revolving Credit Facility, we expect to minimize the delays and closing conditions typically associated with transaction specific financing, as is typically the case in such acquisitions. We believe this advantage iscan be a powerful one, especially in the currenta tight credit environment, and is highly unusual in the marketplace for acquisitions in which we operate.

Valuation and Due Diligence

When evaluating businesses or assets for acquisition, our management team performs a rigorous due diligence and financial evaluation process. In doing so, we evaluate the operations of the target business as well as the outlook for the industry in which the target business operates. While valuation of a business is, by definition, a subjective process, we define valuations under a variety of analyses, including:

discounted cash flow analyses;

evaluation of trading values of comparable companies;

expected value matrices; and

examination of recent transactions.

One outcome of this process is a projection of the expected cash flows from the target business. A further outcome is an understanding of the types and levels of risk associated with those projections. While future performance and projections are always uncertain, we believe that with detailed due diligence, future cash flows will be better estimated and the prospects for operating the business in the future better evaluated. To assist us in identifying material risks and validating key assumptions in our financial and operational analysis, in addition to our own analysis, we engage third-party experts to review key risk areas, including legal, tax, regulatory, accounting, insurance and environmental. We also engage technical, operational or industry consultants, as necessary.

A further critical component of the evaluation of potential target businesses is the assessment of the capability of the existing management team, including recent performance, expertise, experience, culture and incentives to perform. Where necessary, and consistent with our management strategy, we actively seek to augment, supplement or replace existing members of management who we believe are not likely to execute our business plan for the target business. Similarly, we analyze and evaluate the financial and operational information systems of target businesses and, where necessary, we enhance and improve those existing systems that are deemed to be inadequate or insufficient to support our business plan for the target business.

Financing

We have a Credit Facility with a group of lenders led by TD Securities that we entered into on October 27, 2011. This Credit Facility replaced the Prior Credit Agreement.2011 and amended on April 2, 2012. The Credit Facility provides for a Revolving Credit Facility totaling $290.0 million, subject to borrowing base restrictions, and a Term Loan Facility totaling $225$255 million. The Term Loan Facility requires quarterly payments of $0.6 million, that will commence March 31, 2012, andwith a final payment of the outstanding principal balance on October 27, 2017. The Revolving Credit Facility matures on October 27, 2016.

The Credit Facility provides for letters of credit under the Revolving Credit Facility in an aggregate face amount not to exceed $100 million outstanding at any time. At no time may the (i) aggregate principal amount of all amounts outstanding under the Revolving Credit Facility, plus (ii) the aggregate amount of all outstanding letters of credit, exceed the borrowing availability under the Credit Facility. At December 31, 2012, we had outstanding letters of credit totaling approximately $2.9$1.8 million. The borrowing availability under the Revolving Credit Facility at December 31, 20112012 was approximately $287.1$264.2 million.

The Credit Facility is secured by all of the assets of the Company, including all of its equity interests in, and loans to, its subsidiaries. (See Note I to the consolidated financial statements for more detail regarding our Credit Facility). This Credit Facility replaced the Prior Credit Agreement which included a $340 million revolving credit facility that expired in December 2012 and a $72.5 million term loan facility that expired in December 2013.

We intend to finance future acquisitions through our Revolving Credit Facility, cash on hand and, if necessary, additional equity and debt financings. We believe, and it has been our experience, that having the ability to finance our acquisitions with the capital resources raised by us, rather than negotiating separate third party financing specifically related to the acquisition of individual businesses, provides us with an advantage in acquiring attractive

businesses by minimizing delay and closing conditions that are often related to acquisition-specific financings. This is especially true given the recent disruptions in the overall economy and current volatility in the financial markets. In this respect, we believe that in the future, we may need to pursue additional debt or equity financings, or offer equity in Holdings or target businesses to the sellers of such target businesses, in order to fund multiple future acquisitions.

Our Businesses

Advanced Circuits

Overview

Advanced Circuits, headquartered in Aurora, Colorado, is a provider of prototype, quick-turn and production rigid PCBs, throughout the United States. Advanced Circuits also provides its customers with assembly services in order to meet its customers’ complete PCB needs. The prototype and quick-turn portions of the PCB industry are characterized by customers requiring high levels of responsiveness, technical support and timely delivery. Due to the critical roles that PCBs play in the research and development process of electronics, customers often place more emphasis on the turnaround time and quality of a customized PCB than on the price. Advanced Circuits meets this market need by manufacturing and delivering custom PCBs in as little as 24 hours, providing customers with over 98% error-free production and real-time customer service and product tracking 24 hours per day. During 2011 approximately 63% of Advanced Circuits sales were derived from highly profitable prototype and quick turn production PCBs. In each of the years 2012, 2011 and 2010, approximately 60%, 63% and 2009, approximately 64% and 66% of Advanced Circuits’ sales were derived from highly profitable prototype and quick-turn production PCBs. Advanced Circuits’ success is demonstrated by its broad base of over 11,000 customers with which it does business throughout the year. These customers represent numerous end markets, and for each of the years ended December 31, 2012, 2011 2010 and 2009,2010, no single customer accounted for more than 2% of net sales. Advanced Circuits’ senior management, collectively, has approximately 90 years of experience in the electronic components manufacturing industry and closely related industries.

For the full fiscal years ended December 31, 2012, 2011 2010 and 2009,2010, Advanced Circuits had net sales of approximately $84.1 million, $78.5 million $74.5 million and $46.5$74.5 million, respectively and operating income of $24.0 million, $26.6 million $20.4 million and $16.3$20.4 million, respectively. Advanced Circuits had total assets of $91.4 million, $88.7 million $92.0 million and $72.6$92.0 million at December 31, 2012, 2011 2010 and 2009,2010, respectively. Net sales from Advanced Circuits represented 10.1%9.5%, 11.2%12.9%, and 9.2%14.8% of our consolidated net sales for the years 2012, 2011 2010 and 2009,2010, respectively.

History of Advanced Circuits

Advanced Circuits commenced operations in 1989 through the acquisition of the assets of a small Denver based PCB manufacturer, Seiko Circuits. During its first years of operations, Advanced Circuits focused exclusively on manufacturing high volume, production run PCBs with a small group of proportionately large customers. In 1992, after the loss of a

significant customer, Advanced Circuits made a strategic shift to limit its dependence on any one customer. As a result, Advanced Circuits began focusing on developing a diverse customer base, and in particular, on providing research and development professionals at equipment manufacturers and academic institutions with low volume, customized prototype and quick-turn PCBs.

In 1997, Advanced Circuits increased its capacity and consolidated its facilities into its current headquarters in Aurora, Colorado. In 2003, to support its growth, Advanced Circuits expanded its PCB manufacturing facility by approximately 37,000 square feet or approximately 150%.

In March 2010, Advanced Circuits acquired Circuit Express, Inc. (“CEI”) for approximately $16.1 million. Based in Tempe, Arizona and founded in 1987, CEI focuses on quick-turn and prototype manufacturing of rigid PCBs primarily for the aerospace and defense related industry customers. CEI also specializes in expedited delivery in as fast as 24 hours. CEI reported net sales of approximately $16.4 million in 2010 and $18.7 million for the full fiscal 2011 year.

On May 23, 2012, Advanced Circuits acquired Universal Circuits for approximately $2.3 million. Universal Circuits supplies PCBs to major military, aerospace, and medical original equipment manufacturers and contract manufacturers. UCI’s Minnesota facility meets certain Department of Defense clearance requirements and is noted for custom and advanced technologies. Universal Circuits’ sales are primarily in the long-lead sector.

We purchased a controlling interest in Advanced Circuits on May 16, 2006.

Industry

The PCB industry, which consists of both large global PCB manufacturers and small regional PCB manufacturers, is a vital component to all electronic equipment supply chains, as PCBs serve as the foundation for virtually all electronic products, including cellular telephones, appliances, personal computers, routers, switches and network servers. PCBs are used by manufacturers of these types of electronic products, as well as by persons and teams engaged in research and development of new types of equipment and technologies. According to an IPC 2011 Statistical Report, (March 2011) domestic net sales in 2010, of rigid PCBs grew at the rate of almost 18% to approximately $1.6 billion in 2010 compared to $1.4 billion in 2009.

In contrast to global trends, however, production of PCBs in North America has declined since 2000 and is expected to grow slightly over the next several years according to the IPC 2010 Analysis. The rapid decline in United States production was caused by (i) reduced demand for and spending on PCBs following the technology and telecom industry decline in early 2000; and (ii) increased competition for volume production of PCBs from Asian competitors benefiting from both lower labor costs and less restrictive waste and environmental regulations. While Asian manufacturers have made large market share gains in the PCB industry overall, prototype and quick-turn production, some of the more complex volume production and military production have remained strong in the United States.

Both globally and domestically, the PCB market can be separated into three categories based on required lead time and order volume:

Prototype PCBs -– These PCBs are typically manufactured for customers in research and development departments of original equipment manufacturers, or OEMs, and academic institutions. Prototype PCBs are manufactured to the specifications of the customer, within certain manufacturing guidelines designed to increase speed and reduce production costs. Prototyping is a critical stage in the research and development of new products. These prototypes are used in the design and launch of new electronic equipment and are typically ordered in volumes of 1 to 50 PCBs. Because the prototype is used primarily in the research and development phase of a new electronic product, the life cycle is relatively short and requires accelerated delivery time frames of usually less than five days and very high, error-free quality. Order, production and delivery time, as well as responsiveness with respect to each, are key factors for customers as PCBs are indispensable to their research and development activities.

Quick-Turn Production PCBs - –These PCBs are used for intermediate stages of testing for new products prior to full scale production. After a new product has successfully completed the prototype phase, customers undergo test marketing and other technical testing. This stage requires production of larger quantities of PCBs in a short period of time, generally 10 days or less, while it does not yet require high production volumes. This transition stage between low-volume prototype production and volume production is known as quick-turn production. Manufacturing specifications conform strictly to end product requirements and order quantities are typically in volumes of 10 to 500. Similar to prototype PCBs, response time remains crucial as the delivery of quick-turn PCBs can be a gating item in the development of electronic products. Orders for quick-turn production PCBs conform specifically to the customer’s exact end product requirements.

Volume Production PCBs -– These PCBs, which we sometimes refer to as “long lead” and “sub-contract” are used in the full scale production of electronic equipment and specifications conform strictly to end product requirements. Volume Production PCBs are ordered in large quantities, usually over 100 units, and response time is less important, ranging between 15 days to 10 weeks or more.

These categories can be further distinguished based on board complexity, with each portion facing different competitive threats. Advanced Circuits competes largely in the prototype and quick-turn production portions of the North American market, which have not been significantly impacted by the Asian based manufacturers due to the quick response time required for these products. TheManagement believes the North American prototype and quick-turn production sectors combined representPCB market is estimated to be approximately $1.9$3.5 billion in the PCB production industry in 2010.2012.

Several significant trends are present within the PCB manufacturing industry, including:

Increasing Customer Demand for Quick-Turn Production Services -– Rapid advances in technology are significantly shortening product life-cycles and placing increased pressure on OEMs to develop new products in shorter periods of time. In response to these pressures, OEMs invest heavily in research and development, which results in a demand for PCB companies that can offer engineering support and quick-turn production services to minimize the product development process.

Increasing Complexity of Electronic Equipment -– OEMs are continually designing more complex and higher performance electronic equipment, requiring sophisticated PCBs. To satisfy the demand for more advanced electronic products, PCBs are produced using exotic materials and increasingly have higher layer counts and greater component densities. Maintaining the production infrastructure necessary to manufacture PCBs of increasing complexity often requires significant capital expenditures and has acted to reduce the competitiveness of local and regional PCB manufacturers lacking the scale to make such investments.

Shifting of High Volume Production to Asia -– Asian based manufacturers of PCBs are capitalizing on their lower labor costs and are increasing their market share of volume production of PCBs used, for example, in high-volume consumer electronics applications, such as personal computers and cell phones. Asian based manufacturers have been generally unable to meet the lead time requirements for prototype or quick-turn PCB production or the volume production of the most complex PCBs. This “off shoring” of high-volume production orders has placed increased pricing pressure and margin compression on many small domestic manufacturers that are no longer operating at full capacity. Many of these small producers are choosing to cease operations, rather than operate at a loss, as their scale, plant design and customer relationships do not allow them to focus profitably on the prototype and quick-turn sectors of the market.

Products and Services

A PCB is comprised of layers of laminate and contains patterns of electrical circuitry to connect electronic components. Advanced Circuits typically manufactures 2 to 20 layer PCBs, and has the capability to manufacture up even higher layer PCBs. The level of PCB complexity is determined by several characteristics, including size, layer count, density (line width and spacing), materials and functionality. Beyond complexity, a PCB’s unit cost is determined by the quantity of identical units ordered, as engineering and production setup costs per unit decrease with order volume, and required production time, as longer times often allow increased efficiencies and better production management. Advanced Circuits primarily manufactures lower complexity PCBs.

To manufacture PCBs, Advanced Circuits generally receives circuit designs from its customers in the form of computer data files emailed to one of its sales representatives or uploaded on its interactive website. These files are then reviewed to ensure data accuracy and product manufacturability. While processing these computer files, Advanced Circuits generates images of the circuit patterns that are then physically developed on individual layers, using advanced photographic processes. Through a variety of plating and etching processes, conductive materials are selectively added and removed to form horizontal layers of thin circuits, called traces, which are separated by insulating material. A finished multilayer PCB laminates together a number of layers of circuitry. Vertical connections between layers are achieved by metallic plating through small holes, called vias. Vias are made by highly specialized drilling equipment capable of achieving extremely fine tolerances with high accuracy.

Advanced Circuits assists its customers throughout the life-cycle of their products, from product conception through volume production. Advanced Circuits works closely with customers throughout each phase of the PCB development process, beginning with the PCB design verification stage using its unique online FreeDFM.com tool, FreeDFM.comTM, which was launched in 2002, enables customers to receive a free manufacturability assessment

report within minutes, resolving design problems that would prohibit manufacturability before the order process is completed and manufacturing begins. The combination of Advanced Circuits’ user-friendly website and its design verification tool reduces the amount of human labor involved in the manufacture of each order as PCBs move from Advanced Circuits’ website directly to its computer numerical control, or CNC, machines for production, saving Advanced Circuits and customers cost and time. As a result of its ability to rapidly and reliably respond to the critical customer requirements, Advanced Circuits generally receives a premium for their prototype and quick-turn PCBs as compared to volume production PCBs.

Advanced Circuits manufactures all high margin prototypes and quick-turn orders internally but often utilizes external partners to manufacture production orders that do not fit within its capabilities or capacity constraints at a given time. As a result, Advanced Circuits constantly adjusts the portion of volume production PCBs produced internally to both maximize profitability and ensure that internal capacity is fully utilized.

The following table shows Advanced Circuits’ gross revenue by products and services for the periods indicated:

Gross Sales by Products and Services(1)(1)

| Year Ended December 31, | Year Ended December 31, | |||||||||||||||||||||||

| 2011 | 2010 | 2009 | 2012 | 2011 | 2010 | |||||||||||||||||||

Prototype Production | 29.3 | % | 28.9 | % | 30.6 | % | 28.4 | % | 29.3 | % | 28.9 | % | ||||||||||||

Quick-Turn Production | 33.6 | % | 32.6 | % | 36.4 | % | 31.9 | % | 33.6 | % | 32.6 | % | ||||||||||||

Volume Production (including assembly) | 35.5 | % | 36.1 | % | 30.1 | % | 38.1 | % | 35.5 | % | 36.1 | % | ||||||||||||

Third Party | 1.6 | % | 2.4 | % | 2.9 | % | 1.6 | % | 1.6 | % | 2.4 | % | ||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | ||||||||||||

|

|

|

|

|

| |||||||||||||||||||

| (1) | As a percentage of gross sales, exclusive of sale discounts. |

Competitive Strengths

Advanced Circuits has established itself as a leading provider of prototype and quick-turn PCBs in North America and focuses on satisfying customer demand for on-time delivery of high-quality PCBs. Advanced Circuits’ management believes the following factors differentiate it from many industry competitors:

Numerous Unique Orders Per Day -– For the year ended December 31, 2011,2012, Advanced Circuits received on average over 250approximately 300 customer orders per day. Due to the large quantity of orders received, Advanced Circuits is able to combine multiple orders in a single panel design prior to production. Through this process, Advanced Circuits is able to reduce the number of costly, labor intensive equipment set-ups required to complete several manufacturing orders. As labor represents the single largest cost of production, management believes this capability gives Advanced Circuits a unique advantage over other industry participants. Advanced Circuits maintains proprietary software that maximizes the number of units placed on any one panel design. A single panel set-up typically accommodates 1 to 12 orders. Further, as a “critical mass” of like orders is required to maximize the efficiency of this process, management believes Advanced Circuits is uniquely positioned as a low cost manufacturer of prototype and quick-turn PCBs.

Diverse Customer Base -– Advanced Circuits possesses a customer base with little industry or customer concentration exposure. During fiscal year ended December 31, 2011,2012, Advanced Circuits did business with over 11,000 customers and added approximately 185over 170 new customers per month. For each of the years ended December 31, 2012, 2011 2010 and 2009,2010, no customer represented over 2% of net sales.

Highly Responsive Culture and Organization -– A key strength of Advanced Circuits is its ability to quickly respond to customer orders and complete the production process. In contrast to many competitors that require a day or more to offer price quotes on prototype or quick-turn production, Advanced Circuits offers its customers quotes within seconds and the ability to place or track orders any time of day. In addition, Advanced Circuits’ production facility operates three shifts per day and is able to ship a customer’s product within 24 hours of receiving its order.

Proprietary FreeDFM.com Software -– Advanced Circuits offers its customers unique design verification services through its online FreeDFM.com tool. This tool, which was launched in 2002, enables customers to receive a free manufacturability assessment report, within minutes, resolving design problems before customers place their orders. The service is relied upon by many of Advanced Circuits’ customers to reduce design errors and minimize production costs. Beyond improved customer service, FreeDFM.com has the added benefit of improving the efficiency of Advanced Circuits’ engineers, as many routine design problems, which typically require an engineer’s time and attention to identify, are identified and sent back to customers automatically.

Established Partner Network -– Advanced Circuits has established third party production relationships with PCB manufacturers in North America and Asia. Through these relationships, Advanced Circuits is able to offer its customers a complete suite of products including those outside of its core production capabilities. Additionally, these relationships allow Advanced Circuits to outsource orders for volume production and focus internal capacity on higher margin, short lead time, production and quick-turn manufacturing.

Business Strategies

Advanced Circuits’ management is focused on strategies to increase market share and further improve operating efficiencies. The following is a discussion of these strategies:

Increase Portion of Revenue from Prototype and Quick-Turn Production -– Advanced Circuits’ management believes it can grow revenues and cash flow by continuing to leverage its core prototype and quick-turn capabilities. Over its history, Advanced Circuits has developed a suite of capabilities that management believes allow it to offer a combination of price and customer service unequaled in the market. Advanced Circuits intends to leverage this factor, as well as its core skill set, to increase net sales derived from higher margin prototype and quick-turn production PCBs. In this respect, marketing and advertising efforts focus on attracting and acquiring customers that are likely to require these premium services. And while production composition may shift, growth in these products and services is not expected to come at the expense of declining sales in volume production PCBs, as Advanced Circuits intends to leverage its extensive network of third-party manufacturing partners to continue to meet customers’ demand for these services.

Acquire Customers from Local and Regional Competitors -– Advanced Circuits’ management believes the majority of its competition for prototype and quick-turn PCB orders comes from smaller scale local and regional PCB manufacturers. As an early mover in the prototype and quick-turn sector of the PCB market, Advanced Circuits has been able to grow faster and achieve greater production efficiencies than many industry participants. Management believes Advanced Circuits can continue to use these advantages to gain market share. Further, Advanced Circuits continues to enter into prototype and quick-turn manufacturing relationships with several subscale local and regional PCB manufacturers. According to a November 2010 IPC study, approximately 309 PCB manufacturers operate in the United States with only 26 generating annual sales in excess of $20 million. Management believes that while many of these manufacturers maintain strong, longstanding customer relationships, they are unable to produce PCBs with short turn-around times at competitive prices. As a result, Advanced Circuits sees an opportunity for growth by providing production support to these manufacturers or direct support to the customers of these manufacturers, whereby the manufacturers act more as a broker for the relationship.

Remain Committed to Customers and Employees -– Advanced Circuits has remained focused on providing the highest quality productproducts and serviceservices to its customers. We believe this focus has allowed Advanced Circuits to achieve its outstanding delivery and quality record. Advanced Circuits’ management believes this reputation is a key competitive differentiator and is focused on maintaining and building upon it. Similarly, management believes its committed base of employees is a key differentiating factor. Advanced Circuits currently has a profit sharing program and tri-annual bonuses for all of its employees. Management also occasionally sets additional performance targets for individuals and departments and establishes rewards, such as lunch celebrations or paid vacations, if these goals are met. Management believes that Advanced Circuits’ emphasis on sharing rewards and creating a positive work environment has led to increased loyalty. As a result, Advanced Circuits plans on continuing to focus on similar programs to maintain this competitive advantage.

Research and Development

Advanced Circuits engages in continual research and development activities in the ordinary course of business to update or strengthen its order processing, production and delivery systems. By engaging in these activities, Advanced Circuits expects to maintain and build upon the competitive strengths from which it benefits currently. Research and development expenses were not material in each of the years 2012, 2011 2010 and 2009.2010.

Customers

Advanced Circuits’ focus on customer service and product quality has resulted in a broad base of customers in a variety of end markets, including industrial, consumer, telecommunications, aerospace/defense, biotechnology and electronics manufacturing. These customers range in size from large, blue-chip manufacturers to small, not-for-profit university engineering departments. The following table sets forth management’s estimate of Advanced Circuits’ approximate customer breakdown by industry sector for the fiscal years ended December 31, 2012, 2011 2010 and 2009:2010:

Industry Sector | 2011 Customer Distribution | 2010 Customer Distribution | 2009 Customer Distribution | |||||||||

Electrical Equipment and Components | 30 | % | 29 | % | 33 | % | ||||||

Measuring Instruments | 8 | % | 10 | % | 13 | % | ||||||

Electronics Manufacturing Services | 19 | % | 18 | % | 15 | % | ||||||

Engineer Services | 8 | % | 10 | % | 5 | % | ||||||

Industrial and Commercial Machinery | 10 | % | 6 | % | 8 | % | ||||||

Business Services | 1 | % | 1 | % | 2 | % | ||||||

Wholesale Trade-Durable Goods | 1 | % | 1 | % | 1 | % | ||||||

Educational Institutions | 8 | % | 7 | % | 8 | % | ||||||

Transportation Equipment | 9 | % | 8 | % | 10 | % | ||||||

All Other Sectors Combined | 6 | % | 10 | % | 5 | % | ||||||

|

|

|

|

|

| |||||||

Total | 100 | % | 100 | % | 100 | % | ||||||

|

|

|

|

|

| |||||||

Industry Sector Electrical Equipment and Components Measuring Instruments Electronics Manufacturing Services Engineer Services Industrial and Commercial Machinery Business Services Wholesale Trade-Durable Goods Educational Institutions Transportation Equipment All Other Sectors Combined Total 2012 Customer

Distribution 2011 Customer

Distribution 2010 Customer

Distribution 28 % 30 % 29 % 8 % 8 % 10 % 20 % 19 % 18 % 5 % 8 % 10 % 12 % 10 % 6 % 1 % 1 % 1 % 1 % 1 % 1 % 10 % 8 % 7 % 9 % 9 % 8 % 6 % 6 % 10 % 100 % 100 % 100 %

Management estimates that over 90% of its orders are generated from existing customers. Moreover, approximately two-thirds of Advanced Circuits’ orders in each of the years 2012, 2011 2010 and 20092010 were delivered within five days (not including CEI orders.)

Sales and Marketing

Advanced Circuits has established a “consumer products” marketing strategy to both acquire new customers and retain existing customers. Advanced Circuits uses initiatives such as direct mail postcards, web banners, aggressive pricing specials and proactive outbound customer call programs as part of this strategy. Advanced Circuits spends approximately 1% of net sales each year on its marketing initiatives and advertising and has 4457 employees dedicated to its marketing and sales efforts. These individuals are organized geographically and each is responsible for a region of North America. The sales team takes a systematic approach to placing sales calls and receiving inquiries and, on average, will place over 250 outbound sales calls and receive between 160 and 200approximately 140 inbound phone inquiries per day. Beyond proactive customer acquisition initiatives, management believes a substantial portion of new customers are acquired through referrals from existing customers. In addition, other customers are acquired over the internet where Advanced Circuits generates over 90% of its orders from its website.