| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

| ||

| 04-2833935 | |||

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||

| 01581-3335 | |||

| (Address of principal executive offices) | (Zip Code) | ||

Registrant’s telephone number, including area code: | (508) | |

Securities registered pursuant to Section 12(b) of the Act: | Common Stock, par value $.01 per share | |

Name of each exchange on which registered | NASDAQ Global Market | |

Securities registered pursuant to Section 12(g) of the Act: | None | |

Large Accelerated Filer | ¨ | Accelerated Filer | x | Non-Accelerated Filer | ¨ | Smaller Reporting Company | ¨ |

$235,280,802.

our target markets is essential to our growth; (Olympus) and Fuji Corporation (Fuji) for digital still Customer Military Customers in Total Raytheon Company DRS Technologies sales to Skyworks Solutions and the customers who use our displays for military applications will represent a significant portion of our revenues for 2012; our expectation that we will continue developing HBT transistor wafers and other gallium arsenide products for advanced integrated circuit applications from other compound materials; our expectation that we will continue to pursue other U.S. government development contracts for applications that relate to our commercial product applications; our expectation that sales of our III-V products for wireless handset applications and our display products for consumer electronic applications will decline; our belief that products using HBT transistor wafers are easier to design, which can translate into reduced component costs and smaller equipment; our expectation that we will prosecute and defend our proprietary technology aggressively; our belief that it is important to retain personnel with experience and expertise relevant to our business;our belief that our products are targeted towards markets that are still developing and our competitive strength is creating new technologies;our belief that it is important to invest in research and development to remain profitableachieve profitability even during periods when we are not profitable; our belief that we are a leading developer and manufacturer of advanced semiconductor materials and miniature displays; our belief that our products enable our customers to develop and market an improved generation of products; our belief that therethat the technical nature of our products and markets demands a commitment to close relationships with our customers; our belief that our Golden-i industrial reference design will provide for increased worker productivity, safety and improved manufacturing quality; our belief that our ability to develop and expand the our wearable technologies and to market and license our wearable technologies will be increased salesimportant for our revenue growth and ability to achieve profitability and positive cash flow; the impact of 3G, 4Gthe timing of development of the market segment for our wearable computing products on our ability to grow revenues; our expectation that we will incur significant development and smart phonesmarketing costs in 2012;2014 to commercialize the our wearable technologies; our statement that we may make equity investments in companies; our expectation that KoBrite will incur additional losses in the near term; our expectation that the operations at our Korean facility, Kowon, will cease and the cash and marketable debt securities held by Kowon will eventually be remitted back to the U.S.; our expectation that revenue will be between $110between $18 million and $120$22 million for 2012; 2014;our ability to forecast our revenues and operating results;our expectation that 2012 revenueswe will primarily be to customers locatedhave a consolidated net loss in the range of $32 million to $40 million in 2014; our expectation that excluding the effects of working capital, stock buybacks, and other investing activities our cash usage will be between $30 million and $35 million to fund operations for fiscal year 2014; our expectation that the U.S.; government will significantly reduce funding for programs through which we sell high margin military products; our belief that a strengthening of the U.S. dollar could increase the price of our products in foreign markets; the impact of new regulations relating to conflict minerals on customer demands and increased costs related to compliance with such regulations; our expectationbelief that our future success will depend primarily upon the technical expertise, creative skills and management abilities of our officers and key employees rather than on patent ownership;our belief that our extensive portfolio of patents, trade secrets and non-patented know-how provides us with a manufacturing/distribution partner will commence selling Golden-icompetitive advantage in the wearable technologies market; our belief that our ability to develop innovative products enhances our opportunity to grow within our targeted markets; our belief that continued introduction of new products in 2012; our expectation that we will not receive additional amounts from the sale of patents;target markets is essential to our growth; our expectation that our CyberDisplaydisplay products will benefit from further general technological advances in the design and production of integrated circuits and active matrix LCDs, resulting in further improvements in resolution and miniaturization; our expectation that a significant reduction or delay in orders from any of our significant military customers could result in us not being able to achieve profitability in 2012; our belief that our HBT transistor wafers offer greater power efficiency, improved signal quality and less complexity over gallium arsenide field effect transistors; our belief that our manufacturing process offers greater miniaturization, reduced cost, higher pixel density, full color capability and lower power consumption compared to conventional active matrix LCD manufacturing approaches; our expectation not to pay cash dividends for the foreseeable future and to retain earnings for the development of our businesses; our expectation based on current negotiations with our customers and certain contractual obligations, that the sales prices of certain products will decline in fiscal year 2012; our expectation that sales prices of our displays for military applications will remain relatively flat in 2012; our plan to base production and inventory levels based on internal forecasts of customer demands; our belief that the overall increase or decrease in the average sales price of our display products will be dependent on the sales mix of commercial and military display sales; our belief that we may have impairment charges on Kowon’s long-lived assets; our expectation that we will expend between $5.0between $2.0 million and $8.0 $3.0 million on capital expenditures over the next twelve months; our intent to reduce our per unit production costs primarily through increasing manufacturing yield, lowering fixed costs per unit through increased sales volume, and increasing productivity and efficiency; our expectation that the market for display products for military applications will not be seasonal; our expectation that prices of our HBT transistor and display products sold for consumer electronic applications will decline by approximately 5 to 7 percent during fiscal year 2012, but may decline more depending on final negotiations with our customers; our expectation that competition will increase; our belief that our CyberDisplay products are well suited for new applications such as reading e-mail and browsing the Internet using digital wireless devices and other consumer electronics devices; our belief that small form factor displays will be a critical component in the development of advanced wireless communications systems; our belief that wireless handset makers are looking to create products that complement or eventually replace wireless handsets; our belief that general technological advances in the design and fabrication of integrated circuits, LCD technology and LCD manufacturing processes will allow us to continue to enhance our CyberDisplaydisplay product manufacturing process; our expectation that a significant market for new wireless communication devices, including personal entertainment systems, will develop; our belief that continued introduction of new products in2 our belief that our future success will depend primarily upon the technical expertise, creative skills and management abilities of our officers and key employees rather than on patent ownership; our belief that our available cash resources will support our operations and capital needs for at least the next twelve months; our expectation that we will have taxes based on federal alternative minimum tax rules and on our foreign operations in 2014; our expectation that we will have a state tax provision in 2014; our expectation that the adoption of certain accounting standards will not have a material impact on our financial position or results of operations;our belief that our business is not disproportionately affected by climate change regulations; our belief that our operations have not been materially affected by inflation; and our belief that the effect, if any, of reasonably possible near-term changes in interest rates on our financial position, results of operations, and cash flows should not be material. These forward-looking statements are based on current expectations, estimates, forecasts and projections about the industries in which we operate, management’smanagement's beliefs, and assumptions made by management. In addition, other written or oral statements, which constitute forward-looking statements, may be made by or on behalf of us. Words such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “could”, “seeks”, “estimates”, and variations of such words and similar expressions are intended to identify such forward-looking statements. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions, which are difficult to predict. Therefore, actual outcomes and results may differ materially from what is expressed or forecasted in such forward-looking statements, whether as a result of new information, future events or otherwise. Factors that could cause or contribute to such differences in outcomes andItem 1. Business manufacturerdisplay products. 2012 2011 Consolidated III-V Product Line Pro Forma Consolidated III-V Product Line Pro Forma Revenues $ 93.4 $ 58.8 $ 34.6 $ 131.1 $ 66.5 $ 64.6 2012 Consolidated III-V Product Line Pro Forma Total Assets $ 176.2 $ 50.7 $ 125.5 We useWearable technologies integrate a variety of commercially available software packages such as Microsoft Windows CE, Nuance Dragon NaturallySpeaking and Hillcrest Labs with our proprietary semiconductor material technologysoftware and display products to create a reference design manufacture and market our products. Our products enable ourwhich we offer to license to customers who wish to develop and market an improved generation of products for applicationsmobile industrial products. We licensed our first reference design known as Golden-i® in wireless and consumer electronic devices. Our fiscal year ends on the last Saturday in December. The fiscal years ended December 31, 2011, December 25, 2010 and December 26, 2009 are referred to herein as fiscal years 2011, 2010 and 2009, respectively. Our principal executive offices are located at 200 John Hancock Road, Taunton, Massachusetts. Our telephone number is (508) 824-6696.We commercially develop and manufacture Gallium Arsenide-based heterojunction bipolar transistor wafers (HBT transistor wafers) and other commercial semiconductor products that use Gallium Nitride and Gallium Arsenide-based substrates. We collectively refer to our customer began shipping products based on compound semiconductor materials,our technology in 2013. Through 2013 our revenues from licensing our Golden-i technologies has been de minimis. We have rebranded the category and refer to the headset reference designs and other technologies we developed as Kopin Wearable technologies of which primarily consists of our HBT transistor wafers, as our “III-V” products because we use elements categorized on the III and V columns ofGolden-i headset reference design is for the periodic table of elements to manufacture such products. industrial market segment.HBT transistor wafers are customer-specific arrays of vertically oriented transistors that our customers use primarily to produce high performance integrated circuits for wireless communications products. Sales of our HBT transistor wafers to Skyworks Solutions, Inc. (Skyworks Solutions) accounted for approximately 28%, 25% and 20% of our total revenues for fiscal years 2011, 2010 and 2009, respectively. Skyworks Solutions also uses the foundry services of Advanced Wireless Semiconductor Company (AWSC) to process our HBT transistor wafers on its behalf. We sell HBT transistor wafers directly to AWSC for eventual resale by AWSC to Skyworks Solutions and its other customers. Although we do not know exactly how much of our sales to AWSC are for Skyworks we believe an investor should view our sales to Skyworks Solutions and AWSC in the aggregate when evaluating the importance of Skyworks Solutions as a customer to Kopin. Sales to AWSC were 9%, 12% and 8%, of our 2011, 2010 and 2009 revenues, respectively. In addition to Skyworks Solutions, original equipment manufacturers such as RF Micro Devices and TriQuint Semiconductor purchase our HBT transistor wafers.Our CyberDisplay™display products consist of miniature, high performance, high resolution displays either sold separately or in various configurations with optical lenses and electronics contained in either plastic or metal housings. Current applications which include CyberDisplayminiature, high performance, high resolution display products are military devices, such as thermal weapon sights, and consumer devices such as camcorders, digital cameras,cameras; and devices that are capable of browsingaccessing the Internet usingor digital wirelessstorage devices for viewing data or video. When our display products are configured as spatial light modulators, the applications include industrial equipment for 3D Automated Optical Inspection and viewing video from other consumer electronics devices such as MP3 or iPod™ storage devices.training simulation equipment. We have sold our CyberDisplay productdisplay products to Raytheon Company, DRS RSTA Inc., BAE Systems (directly and through a third party QiOptiq), and ITT for use in military applications and to Samsung Electronics Co., Ltd. (Samsung) for use in digital camcorders,, Eastman Kodak Company (Kodak), Olympus Corporation3cameras and DRS Technologies, BAE Systems (through a third party QiOptic), Raytheon and ITT for use in military applications.cameras. For fiscal years 2013, 2012 and 2011, 2010 and 2009, significantwere as follows: (Note theare shown below. The caption “Military Customers in Total” in the table below includes Raytheon, DRS Technologies and QiOptic but excludes research and development contractscontracts. We sell our displays to Japanese customers through Ryoden Trading Company. (“*” denotes that the customer’scustomer's revenues were less than 10% of our total company revenues)) Percent of Total

Revenues 2011 2010 2009 30 % 33 % 45 % 12 % 18 % 14 % * * 19 % Customer 2013 2012 2011 Military Customers in Total 38% 57% 60% Raytheon Company 14% 22% 23% DRS RSTA Inc. * 21% 18% QiOptiq Defense Inc. * * 10% Ryoden Trading Company 18% 12% 15% U. S. Government funded research and development contracts 10% 10% 8% Golden-i™ productfiscal year ends on the last Saturday in December. The fiscal years ended December 28, 2013, December 29, 2012, and December 31, 2011 are referred to herein as fiscal years 2013, 2012 and 2011, respectively. Our principal executive offices are located at 125 North Drive, Westborough, Massachusetts. Our telephone number is (508) 870-5959.head worn computer headset which we developed that includes a microprosessorbillion wireless hand-held devices are sold annually for communication, data input, storage and an optical pod which includes a CyberDisplay product. In 2010, we entered into a license agreement with a customer who acquiredretrieval, accessing the exclusive rights to develop Golden-i productsinternet, and other purposes. Derivative wireless devices such as Bluetooth headsets and Smart Watches are available for the industrial market. In 2011 we commenced selling Golden-i Developer Kits which providedpurpose of allowing the basic functionality in orderuser to spur interest from potential end customers of our licenseeaccess their wireless handsets' voice and also software application developers. Sales of the Golden-i Developer Kits were diminimis in 2011 and we do not expect significant revenue from this product in 2012.Industry OverviewIII-V ProductsAdvanced semiconductor materials are used in the manufacture of integrated circuits for high frequency, low power applications. The rapid growth intext communication features without holding the wireless communications industry has fueled demandhandset. Wearable computing devices also include body-worn devices such as scanners and terminals which are sold in industrial markets to improve worker productivity. The user interface for these integrated circuits for use indevices is typically either a key pad or a touch screen however some wireless handsets.In first generationdevices include voice recognition software as an additional feature to allow the user to search the Internet. We believe wireless handset makers are looking to create products that work as a complement to the wireless handsets integrated circuits used in high frequency, low power amplifiers were generally constructed with silicon-based semiconductors. These integrated circuits, while relatively inexpensiveor to manufacture, were unable to delivereventually replace the ever increasing performance demanded by wireless handset manufacturers and their customers. This inability led tohandset. Wireless network companies are encouraging the development of gallium arsenidemore products that utilize their network capacity and other companies are developing products which provide continuous access to social media outlets. In order for usethe markets for these new products to develop further advances in wireless communications. Gallium arsenide is generally regarded as having better performance characteristics than silicon due, in part, to its inherent physical properties that permit gallium arsenide integrated circuits to operate at muchthe devices and application software will be required. Device improvements include smaller higher frequencies than silicon integrated circuits, or operate at the same frequency withresolution displays, lower power consumption. The reduction in system power requirements is particularly important in portable applications, such as wireless handsets, because it extends battery life.The high performance characteristics of gallium arsenide have led to an increased use of gallium arsenide-based transistors to satisfy the industry’s need for even greater performance. Since the mid 1990s these gallium arsenide transistors include our HBT transistor wafer for use in wireless handset products which use digital signal processingprocessors, longer-life batteries, compact optics and generally operate at higher cellular frequencies. Air interface standards in these frequency bands include Global System Mobile, or GSM, Time Division Multiple Access, or TDMA,software including voice recognition and Code Division Multiple Access, or CDMA, and provide improved capacity, sound quality and capabilities at cellular and wireless frequency bands, but are incompatible with each other and have fragmentednoise cancellation. For the market for equipment. Suppliers of wireless handsets now offer multi-modethese devices to grow application software must be developed that exploit their new features and multi-band wireless handsets which are capable of switching from one high frequency band to another to enable consumers to use wireless handsets across various territories and different interface standards. This new generation of products is significantly more complex than the prior generation and requires certain key features, including:Simpler system design;Support for higher frequencies;

4

Lower power consumption;

Improved signal quality; and

Wider range of operating temperatures.

CyberDisplay™ Products

Small form factor displays are used in military, consumer electronic and industrial products such as thermal weapon sights, camcordersdigital cameras, training and digital cameras.simulation products and metrology tools. We expect the market for wireless communications devices, including personal entertainment systems, will continue to grow. In order for this market to develop, advances in wireless communications systems such as greater bandwidth and increased functionality, including real-time wireless data, broadband Internet access and mobile television, will be necessary. We believe small form factor displays will be a critical component in the development of advanced mobile wireless communications systems as these systems must provide high resolution images without compromising the portability of the product.

|

|

We believe that the high growth potential for portable communications products can be realized effectively only if these products are available at a reasonable priceintegrated to create headset reference designs which use voice as the user interface and are able to clearly present to end users the information they wish to access without compromising the size of the product. These products, as well as future models of digital cameras and other consumer electronics, are well suited forthrough the use of wireless technologies can contact other users or information from the cloud. The headset reference designs range from a miniature, low cost display with low power consumption and sharp monochrome or rich, full color high resolution images. To date, display technologies have not fully addressed these needs due to constraints with respect to size, power consumption, resolution, cost or full color capability.

Golden-i™ Products

Laptop computers, PCs and tablets are used in the work place as stand alone devices or as part of systems. These devices requireheadset which resembles typical eyeglasses but include audio capabilities allowing the user to operatecommunicate with other users to our industrial headset reference design, called Golden-i, which includes an optical pod with one of our display products, a key board for data inputmicroprocessor, memory and information retrieval. Ifvarious commercially available software packages that we license such as Microsoft Windows CE or Android, Nuance Dragon NaturallySpeaking, Ask Ziggy natural speech, and Hillcrest Labs motion control. All of our headset reference designs utilize operating system software we developed and include our proprietary noise cancellation technologies. The optical pod allows the user of these devices works outdoorsto view information such as WEB data, technical diagrams, streaming video or in environments withface to face communication. When viewing schematics or similar conditions the device may have to be “ruggedized”, which adds weight, increases its size and adds cost. The display performance of these devices is affected by ambient lighting conditions. In addition ifdocuments the user is requiredcapable of zooming-in to wear gloves insee finer details or zooming out to see an entire system perspective. Some headset reference designs have a camera feature which enables the performanceuser to stream live video to a remote subject matter expert so that both the user and expert can analyze the issue at the same time.

5

Our Solution

III-Vprimary interface as opposed to a touch screen or keyboard.

We manufacture our HBT transistor wafers using our proprietary metal organic chemical vapor deposition (MOCVD) semiconductor growth techniques and our Wafer Engineering™ process. Our Wafer Engineering™ process significantly reduces the number of defects which naturally occur when different semiconductor materials are combined. By depositing films of atomic-level thickness on gallium arsenide or indium phosphide wafers, we are able to create HBT transistor wafers that consist of a series of material layers which form a vertical transistor. This transistor structure enables the design of integrated circuits in which individual transistors are vertically arranged.

We believe that the vertical structure of an HBT transistor offers the following advantages to an integrated circuit manufacturer:

|

|

We believe our HBT transistor wafers also offer the following additional advantages over gallium arsenide field effect transistors:

|

|

|

CyberDisplay™ Products

6

a Binocular Display Module or BDM, and thermal weapon sight eyepieces which contain a CyberDisplay, light emitting diode, optics, and electronics in a hermetically sealed housing. In contrastrefer to current passive matrix and active matrix LCD approaches, our CyberDisplayas CyberDisplay™ products, utilize high quality, single crystal silicon—thesilicon-the same high quality silicon used in conventional integrated circuits. This single crystal silicon is not grown on glass; rather, it is first formed on a silicon wafer and patterned into an integrated circuit (including the active matrix, driver circuitry and other logic circuits) in an integrated circuit foundry. The silicon wafer is then sent to our facilities and the integrated circuit is lifted off as a thin film and transferred to glass using our proprietary Wafer™ Engineering technology, so that the transferred layer is a fully functional active matrix integrated circuit.

circuit which now resides on a transparent substrate.

Greater miniaturization;

Higher pixel density;

Full color capability; and

Lower power consumption.

After the CyberDisplay display, has been packaged and if it is to be used in a weapon sight such as a thermal weapon sight, the packaged display is sentfabricated, tested and routed to our “Higher Level Assembly” or HLA assembly area, where it is incorporated in tointo a module we manufacture.module. We offer a variety of models with varying levels of complexity but common to all is a light emitting diode,our display, illuminations source, optics and electronics in a housingsealed unit.

Golden-i™ Technology

7

commands and head gestures. The systemcamera feature which allows the user to access information or operate remote devices through the internet using WiFi or Bluetooth or potentially other wireless networks. The optical pod allows the user to view information such as technical diagrams, streaming video or face to face communication. When viewing schematics or similar documents the user is capable of zooming-in to see finer details or zooming out to see an entire system perspective. The Golden-i product has a camera feature which enables the user to stream livesend video to a Remote Subject Matter Expert so that both the user and expert can analyze the issue at the same time.remote third party. Our Golden-i products are significantly lighter than competing solutions such as laptops, PCs or tablets. We believe our Golden-i technology will provide for increased worker productivity, safety and improved manufacturing quality through more efficient issue resolution and improved communication.

Strategy

Our strategybusiness model is to develop products which are centered on the mobile world. Our III-V products improve the speedlicense our reference designs and volume of voice and data which can be transmitted wirelessly to mobile devices such as 3G and 4G smartphones, our micro display was created to be the destination pointenter into agreements for the data flowing oversale of the wireless networksoptical pod or to sell our display and components separately. We offer our Golden-i device is designedproducts to provide a hands-free remote access, controldevelopers and collaboration via the internet through the wireless networks. Our objective is to be the leading suppliermanufacturers of advanced semiconductor materials and miniature displays and display systems that enable our customers to develop and manufacture differentiated communications,industrial products, military industrial andproducts, consumer electronic devices in high volumes.products, 3d metrology equipment manufacturers and manufacturers of the next generation of mobile devices. The critical elements of our strategy include:

|

|

|

|

8

III-V Products

We

Using our HBT transistor wafers, our customers have developed gallium arsenide power amplifiers for wireless handsets. Our HBT transistor wafers are used in Code Division Multiple Access, Global System Mobile and Time Division Multiple Access power amplifiers, third generation (3G) and fourth generation (4G) wireless handset standards.

In addition to wireless handset power amplifiers, our HBT transistor wafers are also being used in the fabrication of power amplifiers for devices which communicate using wireless fidelity or “WiFi” integrated circuits. Our HBT transistor wafers are also used in high-speed fiber optic switching.

WeGolden-i headset reference design our HBT transistor wafers in collaboration with our customers’ engineering teams in order to create customized products that meet their specific application needs. Our largest customer for our HBT transistor wafers is Skyworks Solutions. Skyworks Solutions also uses the foundry services of Advanced Wireless Semiconductor Company to process our HBT transistor wafers on its behalf. We sell HBT transistor wafers directly to AWSC for eventual resale by AWSC to Skyworks Solutions and their other customers. Other customers of our gallium arsenide products include RF Micro Devices and TriQuint Semiconductor. For fiscal years 2011, 2010 and 2009, sales of gallium arsenide products to Skyworks Solutions accounted for approximately 28%, 25%, and 20% of our total revenues, respectively. Sales to AWSC in 2011, 2010 and 2009 were 9%, 12% and 8% of our 2011, 2010 and 2009 revenues, respectively. Although we do not know exactly how much of our sales to AWSC are for products sold to Skyworks Solutions, we believe an investor should view our sales to Skyworks Solutions and AWSC in the aggregate for evaluating the importance of Skyworks Solutions as a customer to Kopin. We have a supply agreement with Skyworks Solutions which is scheduled to terminate in July 2012, excluding the agreement’s last buy option.

CyberDisplay™significant.

9

Golden-i™ Products

Our business model is to generate revenues by licensing for a royalty fee the Golden-i technology and knowhow, which includes the operating software and patented product designs, and selling a CyberDisplay product to a partner who develops and manufactures or distributes products based on the Golden-i technology. Our revenues in 2011 from the sale of Golden-i Development Kits were not significant and while we anticipate our licensee customer will introduce a product in 2012, we do not believe the revenues will be material in 2012.

We principally sell

20102013, 2012, and 20092011 we incurred total research and development expenses of $25.9$17.5 million, $19.7$14.3 million and $14.1

10

$16.6 million, respectively. Included in total research and development expenses are our internal development programs for new HBT and CyberDisplay products and development of the processes to manufacture CyberDisplay products using 8 inch wafers, which were $22.1 million, $17.0 million and $10.6 million, respectively, for fiscal years 2011, 2010 and 2009.

We intend to continue developing HBT transistor wafers and other gallium arsenide products for advanced integrated circuit applications from other compound materials. We are working with current and potential customers in the development of the next generation of HBT transistor wafers, including developing GaN (Gallium Nitride) HEMT (high electron mobility transistor) wafers.

CyberDisplay™ Products

Our display product development efforts are focused towards continually enhancing the resolution, performance and manufacturability of our CyberDisplaydisplay products. A principal focus of this effort is the improvement of manufacturing processes for very small active matrix pixels with our eight inch manufacturing line, which we will use in succeeding generations of our CyberDisplaydisplay products. The pixel size of our current CyberDisplaytransmissive display products ranges from 8.46.8 to 15 microns. These pixel sizes are much smaller than a pixel size of approximately 100 microns in a typical laptop computer display. The resolutions of our current commercially available CyberDisplaydisplay products are 320 x 240, 432 x 240, 640 x 480, 854 x 480, 800 x 600, and1,024 x 768, 1,280 x 1,024 pixels.and 2,048 x 1,536 pixels. In addition, we have demonstrated 2,048 x 2,048 resolution displays in a 0.96-inch diagonal size. We are also working on further decreasing the power consumption of our CyberDisplaydisplay products. The pixel size of our current reflective display products ranges from 8.2 to 13.6 microns. The resolutions of our current commercially available reflective display products are 1,024 x 768 and 1,280 x 1,024 pixels. Additional display development efforts include expanding the resolutions offered, increasing the quantity of CyberDisplay’sdisplay active matrix pixel arrays processed on each wafer by further reducing the display size, increasing the light throughput of our pixels, increasing manufacturing yields, and increasing the functionality of our HLA products.

Golden-i™

unit and improving the overall fit and fashion of the reference design.

III-V

With respect to our HBT transistor wafers, we presently compete with several companies, including IQE, Visual Photonics Epitaxy Co. Ltd. (VPEC), and Hitachi Cable, as well as integrated circuit manufacturers with in-house transistor growth capabilities, such as RF Micro Devices and Fujitsu. For our III-V products, pricing

11

competition is intense. The production of gallium arsenide integrated circuits has been and continues to be more costly than the production of silicon integrated circuits. Although we have reduced production costs of our HBT transistor wafers by achieving higher volumes and reducing raw material costs, we cannot be certain we will be able to continue to decrease production costs. In addition, we believe the costs of producing gallium arsenide integrated circuits by our customers will continue to exceed the costs associated with the production of competing silicon integrated circuits. As a result, we must target markets where these higher costs are justified by their superior performance.

CyberDisplay™ Products

Golden-i™

These companies are substantially larger than Kopin from revenue, cash flow and asset perspectives. In addition, Google has developed a device named Google Glass which is a headset product with similar form and function as our headsets. Google is substantially larger than Kopin from revenue, cash flow and asset perspectives.

12

months after their earliest claim to priority and since publication of discoveries in the scientific and patent literature lags behind actual discoveries, we cannot be certain that we were the first to conceive of inventions covered by pending patent applications or the first to file patent applications on such inventions. We cannot be certain that our pending patent applications or those of our licensorslicensor's will result in issued patents or that any issued patents will afford protection against a competitor. In addition, we cannot be certain that others will not obtain patents that we would need to license, circumvent or cease manufacturing and sales of products covered by these patents, nor can we be sure that licenses, if needed, would be available to us on favorable terms, if at all.

13

production, or a cessation of operations. Any failure on our part to control the use of, or adequately restrict the discharge of, hazardous substances, or otherwise comply with environmental regulations, could subject us to significant future liabilities. Any failure on our part to obtain any required licenses for the export of technical data and/or sales of our products or to otherwise comply with ITAR, could subject us to significant future liabilities. In addition, we cannot be certain that we have not in the past violated applicable laws or regulations, which violations could result in required remediation or other liabilities.

On January 11, 2011, we purchased

We own 78%FDD within our consolidated financial statements.

From Kopin Taiwan Corp’s (KTC) inception in 2002 through July 2009April 2013, the Company owned approximately 35% of KTC. In July 2009, the Company purchased 19,572,468 and 128,226 shares of KTC common stock for approximately $5,975,000 and $300,000, respectively, which increased the Company’s ownership to approximately 87%. Accordingly since July 2009 the Company has included KTC in its consolidated financial statements. In 2010, the Company purchased 14,349,809 shares of KTC common stock for approximately $6,150,000 to increase the Company’s ownership to approximately 90%.

One of our Directors is chairman of KTC and owns approximately 1%acquired 51% of the outstanding common stock of KTC.

eMDT America, Inc. (eMDT), a private company, for $400,000 and began consolidating eMDT, Inc into our financial statements in April of that year.

we wrote it down to $0.

14

display module, and other modules include lenses, backlights, printed circuit boards and other components, which we purchase from third party suppliers. Some of these third party contractors and suppliers are small companies with limited financial resources. In addition, relative to the commercial market, the military buys a small number of units which prevents us from qualifying and buying components

01581.

Officers

John C.C. Fan, age 68

President, Chief Executive Officer and Chairman

Founded Kopin in 1985

Richard A. Sneider, age 51

Treasurer and Chief Financial Officer

Joined Kopin 1998

Hong Choi, age 60

Vice President and Chief Technology Officer

Joined Kopin in 2000

Bor-Yeu Tsaur, age 56

| John C.C. Fan, age 70 | Bor-Yeu Tsaur, age 58 | |||||

| Ÿ | President, Chief Executive Officer and Chairman | Ÿ | Executive Vice President—Display Operations | |||

| Ÿ | Founded Kopin in 1984 | Ÿ | Joined Kopin in 1997 | |||

| Richard A. Sneider, age 53 | Michael Presz, age 60 | |||||

| Ÿ | Treasurer and Chief Financial Officer | Ÿ | Vice President—Government Programs and Special Projects | |||

| Ÿ | Joined Kopin in 1998 | Ÿ | Joined Kopin in 1994 | |||

| Hong Choi, age 62 | ||||||

| Ÿ | Vice President and Chief Technology Officer | |||||

| Ÿ | Joined Kopin in 2000 | |||||

Executive Vice President—Display Operations

Joined Kopin in 1997

Michael Presz, age 58

Vice President—Government Programs and Special Projects

Joined Kopin in 1994

Daily Hill, age 54

Senior Vice President—III-V Operations

Joined Kopin in 1987

| Item 1A. | Risk Factors |

15

Our revenues, profitability and cash flows could be negatively affected if sales of our CyberDisplay products for military applications significantly decline. A significant part of our fiscal year 2011 income from operations and our strategy to maintain profitability in fiscal year 2012 and beyond is to sell our CyberDisplay products for use in U.S. military applications because these products are sold with higher margins than our commercial display or III-V products. Our ability to continue to generate revenues and profits from sales to the U.S. military will be affected by the following events:

The U.S. federal government has incurred and is expected to continue to incur large federal budget deficits. As part of its plan to deal with the federal deficits the U.S. federal government has stated its intention to reduce spending on military programs. The current federal budget forecasts lower unit purchases of thermal weapon sights (TWS) that incorporate our display products.

We are currently selling our display products to three defense contractors who in turn incorporate our product in to their TWS product which they sell to the U.S. military. The U.S. military has stated its intention to reduce the number of suppliers for this TWS program. We sell different display products to each of the three suppliers. One supplier buys only a display while the other two buy a display module. Our sales price and profits are different by product type ; accordingly our revenues and profits will be affected by who the military decides to source the TWS product. In addition the winner of the program has the option to procure displays from our competition in which case we may significantly less revenue than we have historically from this program.

There are new U.S. military production and development programs that we are bidding on such as the Enhanced Night Vision Goggle. We are competing against other display solutions and we may not be awarded contracts. In addition the government may delay awarding or implementing these programs.

If the U.S. government significantly reduces funding for the TWS programs, and we are not able to win additional programs, we will not be profitable.

Our revenues, profitability and cash flows could be negatively affected if certain wireless handset trends do not meet expectations. Our Heterojunction Bipolar Transistor (HBT) wafers are sold to manufacturers who in turn produce Power Amplifier (PA) chip sets which are sold to wireless handset manufactures. The PA chip set amplifies signal strength in a wireless handset such as the voice signal. With the advent of smartphone the number of signals emitting from a wireless handset has increased. For instance the handset may have a voice signal, a GPS signal, and a WiFi signal. The number of our products which ultimately end up in a wireless handset is dependent on the number of signals emitting from a wireless handset. For instance smartphones, “3G” and “4G” wireless handsets typically contains more of our III-V products than a basic wireless handset. An important factor in our strategy to grow our III-V product sales is based on the expectation that the sales of smart phones, 3G and 4G wireless handsets and similar devices will become an increasing percentage of the overall sales of wireless handsets. Some industry estimates have smartphones growing at a constant annual rate of 25% or more over the next four to five years. We anticipate at least double digit growth rates for smartphones, 3G and 4G handsets and similar devices over the next few years.

In addition to the fact that a smartphone would generally contain more content of our product a smartphone typically requires our latest HBT products, called Bifets and BiHEMTs, which are more complex than the traditional HBT used in a basic wireless handset. Our Bifet and BiHEMT products have higher average selling prices than our traditional HBT. Our revenues, profits and cash flows may be negatively impacted if the following occur:

The rate of growth of smartphones, 3G and 4G wireless handset and similar devices is lower than expected;

Our customers are able to design and sell products which can meet the increasing needs of smartphones, 3G, 4G and similar devices without the need to increase the amount content of our products in their products so that our expectation of demand increase because of smartphone, 3G and 4G wireless handsets and similar devices does not happen; and

16

We and our competitors overestimate the growth rate of smartphones, 3G and 4G wireless handsets and similar devices and we expand capacity at a rate in excess of demand. Historically this over capacity situation results in average sales prices declining at faster than normal rate.

and profitability. If we are unable to reduce the cost ofcommercialize our wearable computing products our financial results couldwe may not be negatively impacted. The sales prices of our commercial products and, to a lesser extent, our military products, have historically declined each year. Our strategy to maintain our gross margin is to improve manufacturing efficiencies and yields, consolidate production facilities, shift production of legacy III-V products to Kopin Taiwan Corporation (KTC) which has is a lower cost production facility, increase production of larger diameter wafers (8-inch for display products) and use our purchasing power to obtain reduced raw material and component pricing from our vendors. In 2009, we obtained an 87% interest in KTCable to increase our capacity to produce 6-inch HBT transistor wafers. In order to use KTC’s production capacity KTC’s production processes must be qualified by our customers.revenues, achieve profitability or positive cash flow.

| Sales as a Percent of Total Revenue | ||||||||||||

Customer | 2011 | 2010 | 2009 | |||||||||

Skyworks Solutions, Inc (A) | 28 | % | 25 | % | 20 | % | ||||||

Advanced Wireless Semiconductor Company | 9 | 12 | 8 | |||||||||

Military Customers (B) | 30 | 33 | 45 | |||||||||

United States Government Funded Research and Development Contracts | 4 | 3 | 6 | |||||||||

Raytheon Company (B) | 12 | 18 | 14 | |||||||||

DRS Technologies (B) | * | * | 19 | |||||||||

17

A significant reduction or delay in orders from any of our significant commercial customers would materially reduce our revenue and cash flow are expected to come from sales of military products. The U.S. federal government has incurred and adversely affectis expected to continue to incur large federal budget deficits and the U.S. federal government has stated its intention to reduce spending on military programs. Accordingly our ability to achieve or maintain profitabilitygenerate revenues and cash flow from sales to the U.S. military is dependent on our displays being qualified in new U.S. military programs and the future.U.S. military funding these new programs. If we experience a significant reductionare unable to be qualified into new U.S. military programs or delay in orders from any ofthese programs are not funded our significant military customers ourability to generate revenues, achieve profitability and positive cash flow will be negatively impacted and we will not achieve profitability in 2011, unless the other military customers increased orders to sufficiently offset the decline. The sales to Skyworks Solutions and, to some extent, AWSC have been under a purchase and supply agreement with Skyworks Solutions which expires in July 2012.impacted.

Ifunable to supply our display products to our customers. In the past, we failexperienced several power outages at our facilities which ranged in duration from one to keep pace with changing technologies,four days. Additionally, as we may lose customers. Rapidly changing customer requirements, evolving technologies and industry standards characterize the wireless communications, semiconductor materials andintroduce new equipment into our manufacturing processes, our display industries. To achieve our goals, we need to enhance our existing products and develop and market new products that keep pace with continuing changes in industry standards, requirements and customer preferences. If we cannot keep pace with these changes, our business could suffer.

If our security systems are penetrated and confidential and or proprietary information were taken we could be subject to fines, law suitsespecially wide variations in manufacturing yields and loss of customers.efficiency. We rely on our electronic information systems to perform the routine transactions to run our business.may experience manufacturing problems that would result in delays in product introduction and delivery or yield fluctuations. We transact business over the internet with customers, vendors electronically and our subsidiaries. We have implemented security measures to protect unauthorized access to this information. We haveare also implemented security policies which limit access via the internet from the companysubject to the outside world based onrisks associated with the individual’s positionshortage of raw materials used in the company. We routinely receive security patches for the software we use from the software providers. Our primary concerns are inappropriate access to personnel information, information covered under the International Traffic in Arms Regulation, product designs and manufacturing information, financial information andmanufacture of our intellectual property, trade secrets and know-how. If our security systems are penetrated and confidential and or proprietary information where taken we could be subject to fines, law suites and loss of customersproducts.

Lack of control over production capacity and delivery schedules;

Limited control over quality assurance, manufacturing yields and production costs;

The risks associated with international commerce, including unexpected changes in legal and regulatory requirements, changes in tariffs and trade policies and political and economic instability; and

Natural disasters such as earthquakes, tsunami, mudslides, drought, hurricanes and tornadoes.

18

19

subcontractor to perform under the contract. If the federal government terminates a contract with our customer our contract with our customers generally would entitle us to recover only our incurred or committed costs, settlement expenses and profit on the work completed prior to termination. However, under certain circumstances, our recovery costs upon termination for convenience of such a contract may be limited. As is common with government contractors, we have experienced occasional performance issues under some of our contracts. We may in the future receive show-cause or cure notices under contracts that, if not addressed to the federal government’sgovernment's satisfaction, could give the government the right to terminate those contracts for default or to cease procuring our services under those contracts.

Our CyberDisplay™products may not be widely accepted by the market. Our success will in large part depend on the widespread adoption of the viewing format of our CyberDisplay products in multiple applications. Our success also depends upon the widespread consumer acceptance of our customers’ products. CyberDisplay products work best when used close to the eye, which may not be acceptable to consumers. In addition, CyberDisplay products are not designed for a shared experience amongst multiple viewers at the same time. Potential customers may be reluctant to adopt our CyberDisplay products because of concerns surrounding perceived risks relating to:

The introduction of our display technology generally;

20

Consumer acceptance of our CyberDisplay products; and

The relative complexity, reliability, usefulness and cost-effectiveness of our display products compared to other display products available in the market or that may be developed by our competitors. In addition, our customers may be reluctant to rely upon a relatively small company like us for a critical component. We cannot assure investors that prospective customers will adopt our CyberDisplay products or that consumers will accept our CyberDisplay products in future applications. If we fail to achieve market acceptance of our CyberDisplay products, our business may not be successful and we may not be able to maintain profitability.

We generally do not have long-term contracts with our CyberDisplay customers, which makes forecasting our revenues and operating results difficult. We generally do not enter into long-term agreements with our commercial CyberDisplaydisplay customers obligating them to purchase our products. Our business is characterized by short-term purchase orders and shipment schedules and we generally permit orders to be canceled or rescheduled before shipment without significant penalty. As a result, our customers may cease purchasing our products at any time, which makes forecasting our revenues difficult. In addition, due to the absence of substantial non-cancelable backlog, we typically plan our production and inventory levels based on internal forecasts of customer demand, which are highly unpredictable and can fluctuate substantially. Our operating results are difficult to forecast because we are continuing to invest in capital equipment and increasing our operating expenses for new product development. If we fail to accurately forecast our revenues and operating results, our business may not be successful and the value of investors’investors' investment in us may decline.

fines, law suites and loss of customers.

The timing and successful introduction of additional manufacturing capacity;

The timing of the initial selection of our III-VWearable technology and CyberDisplaydisplay products as a component in our customers’customers' new products;

Availability of interface electronics for our CyberDisplay;

Competitive pressures on selling prices of our products;

The timing and cancellation of customer orders;

Our ability to introduce new products and technologies on a timely basis;

21

Our ability to successfully reduce costs;

The cancellation of U.S. government contracts; and

Our ability to secure agreements from our major customers for the purchase of our products.

The Federal Acquisition Regulation, which comprehensively regulates the formation, administration and performance of federal government contracts;

The Truth in Negotiations Act, which requires certification and disclosure of all cost and pricing data in connection with contract negotiations;

The Cost Accounting Standards and Cost Principles, which impose accounting requirements that govern our right to reimbursement under certain cost-based federal government contracts; and

Laws, regulations and executive orders restricting the use and dissemination of information classified for national security purposes and the export of certain products, services and technical data. We engage in international work falling under the jurisdiction of U.S. export control laws. Failure to comply with these control regimes can lead to severe penalties, both civil and criminal, and can include debarment from contracting with the U.S. government.

Termination of contracts;

Forfeiture of profits;

Cost associated with triggering of price reduction clauses;

Suspension of payments;

•Fines; and

•Suspension or debarment from doing business with federal government agencies.

22

Increased competition may resultprofit on contracts that did not have government funding in decreased demand or lower prices for our products. Competition in the markets for our products is intense and we may not be able to compete successfully. We compete with several companies, mostplace, any of whom are much larger than us, who are primarily engaged in the business of designing, manufacturing and selling integrated circuits or alternative display technologies, as well as the supply of other discrete products. Our competitorswhich could develop new process technologies that may be superior to ours, including technologies that target markets in which our products are sold. Many of our existing and potential competitors have strong market position, considerable internal manufacturing capacity, established intellectual property rights and substantial technological capabilities. Furthermore, they also have greater financial, technical, manufacturing, and marketing resources than we do, and we may not be able to compete successfully with them.

In addition, many of our existing and potential customers manufacture or assemble displays and wireless communications devices and have substantial in-house technological capabilities and substantially greater resources than we do. We may not be able to sell our products to these customers and they may commercialize their internal capabilities to become our competitors. If one of our large customers establishes internal design and manufacturing capabilities, it could have an adverse effect on our operating results.

We expect competition to increase. This could mean lower prices or reduced demand for our products. Any of these developments would have an adverse effect on our operating results.

Disruptions of our production of our III-V and CyberDisplay products would adversely affect our operatingoperations, cash flow and financial results. If we were

Our supply chain is complex and we may be unable to verify the origins for all metals used in our products. We purchase materials from foreign sources and they may not cooperate and provide us with the necessary information to allow us to comply with the Act. This may require us to find alternative sources which could delay product shipments. We may not be successful in protectingalso encounter challenges with our intellectual propertycustomers and proprietary rights. Our success depends in part on our ability to protect our intellectual property and proprietary rights. We have obtained certain domestic and foreign patents and we intend to continue to seek patents on our inventions when appropriate. We also attempt to protect our proprietary information with contractual arrangements and under trade secret laws. Our employees and consultants generally enter into agreements containing provisions with respect to confidentiality and the assignment of rights to inventions made by them while in our employ. These measures may not adequately protect our intellectual and proprietary rights. Existing trade secret, trademark and copyright laws afford only limited protection and our patents could be invalidated or circumvented. Moreover, the laws of certain foreign countries in which our products are or may be manufactured or sold may not fully protect our

23

intellectual property rights. Misappropriation of our technology and the costs of defending our intellectual property rights from misappropriation could substantially impair our business. Ifstockholders if we are unable to protect our intellectual property and proprietary rights, our business may not be successful and the value of investors’ investment in us may decline.

Our products could infringe on the intellectual property rights of others. Companies in the wireless communications, semiconductor and display industries steadfastly pursue and protect intellectual property rights. This has resulted in considerable and costly litigation to determine the validity of patents and claims by third parties of infringement of patents or other intellectual property. Our products could be found to infringe on the intellectual property rights of others. Other companies may hold or obtain patents or inventions or other proprietary rights in technology necessary for our business. Periodically companies inquire aboutcertify that our products and technology in their attempts to assess whether we violate their intellectual property rights. If we are forced to defend against infringement claims, we may face costly litigation, diversion of technical and management personnel, and product shipment delays, even if the allegations of infringement are unwarranted. If there is a successful claim of infringement against us and we are unable to develop non-infringing technology or license the infringed or similar technology on a timely basis, or if we are required to cease using one or more of our business or product names due to a successful trademark infringement claim against us, it could adversely affect our business.conflict free.

We may pursue acquisitions and investments that could adversely affect our business. In the past we have made, and in the future we may make, acquisitions of, and investments in, businesses, products and technologies that could complement or expand our business. If we identify an acquisition candidate, we may not be able to successfully negotiate or finance the acquisition or integrate the acquired businesses, products or technologies into our existing business and products. Future acquisitions could result in potentially dilutive issuances of equity securities, the incurrence of debt and contingent liabilities, amortization expenses and write-downs of acquired assets. In January 2011 we acquired Forth Dimension Displays Ltd. (FDD). If we are unable to operate FDD profitably our results of operations will be negatively affected.

We may incur significant liabilities if we fail to comply with stringent environmental laws and regulations and the International Traffic in Arms Regulations or if we did not comply with these regulations in the past. We are subject to a variety of federal, state and local governmental regulations related to the use, storage, discharge and disposal of toxic or otherwise hazardous chemicals used in our manufacturing process. We are also subject to federal International Traffic in Arms Regulations (ITAR) laws which regulate the export of technical data and sale of products to other nations which may use these products for military purposes. The failure to comply with present or future regulations could result in fines being imposed on us, suspension of production, or a cessation of operations. Any failure on our part to control the use of, or adequately restrict the discharge of, hazardous substances, or otherwise comply with environmental regulations, could subject us to significant future liabilities. Any failure on our part to obtain any required licenses for the export of technical data and/or sales of our products or to otherwise comply with ITAR, could subject us to significant future liabilities. In addition, we cannot be certain

24

| Item 1B. | Unresolved Staff Comments |

| Item 2. | Properties |

We lease our domestic III-V product manufacturing facilities and corporate headquarters located in Taunton, Massachusetts. The Taunton facilities occupy 25,100 and 60,000 square feet, including 6,000 and 6,400 square feet of contiguous environmentally controlled production clean rooms under leases that expire in 2012 and 2020, respectively. We do not anticipate renewing the Taunton lease which expires in 2012.

Santa Clara, California which houses our wearable computing Tech center. These facility leases expire in 2014 and 2016, respectively.

2016. Ikanos Consulting, Ltd., our subsidiary in the United Kingdom, leases two properties which occupy an aggregate of 7,000 square feet. These leases expire in 2016 and 2017.

| Item 3. | Legal Proceedings |

| Item 4. | Mine Safety Disclosures |

25

applicable.

Fiscal Year Ended December 31, 2011 First Quarter Second Quarter Third Quarter Fourth Quarter Fiscal Year Ended December 25, 2010 First Quarter Second Quarter Third Quarter Fourth Quarter Plan Category Total equity compensation plans approved by security holders (1)Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities High Low $ 4.40 $ 3.97 5.22 4.29 4.85 3.31 4.24 3.07 $ 4.74 $ 3.60 4.50 3.21 3.85 2.75 4.48 3.37 High Low Fiscal Year Ended December 28, 2013 First Quarter $ 3.71 $ 3.17 Second Quarter 3.78 3.13 Third Quarter 4.33 3.30 Fourth Quarter 4.28 3.43 Fiscal Year Ended December 29, 2012 First Quarter $ 4.08 $ 3.30 Second Quarter 4.05 3.06 Third Quarter 3.86 3.23 Fourth Quarter 3.87 2.94 9, 2012,7, 2014, there were approximately 481458 stockholders of record of our common stock, which does not reflect those shares held beneficially or those shares held in “street” name.31, 201128, 2013 about shares of the Company’s common stock issuable upon exercise of outstanding options, warrants and rights and available for issuance under our existing equity compensation plans. Number of securities to

be issued upon exercise

of outstanding options,

warrants and rights Weighted-average

exercise price of

outstanding options,

warrants and rights Number of securities

remaining available

for future issuance

under equity

compensation plans

(excluding securities

reflected in column (a)) (a) 1,903,325 $ 5.07 580,178 (2) Plan Category Weighted-average exercise price of outstanding options, warrants and rights Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column a) Total equity compensation plans approved by security holders (1) 558,850 $ 5.09 1,237,080 (2) (1) Consists of the 2001 Equity Incentive Plan and the 2010 Equity Incentive Plan. (2) Shares available under the 2010 Equity Incentive Plan.

26

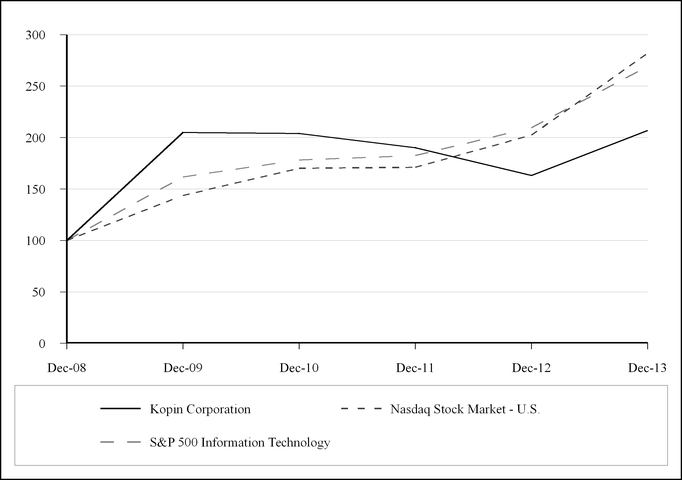

Period September 25, 2011 through October 22, 2011 October 23, 2011 through November 19, 2011 November 20, 2011 through December 31, 2011 (1)(2) Total Statement of Operations Data: Revenues: Net product revenues Research and development revenues Total revenues Expenses: Cost of product revenues Research and development—funded programs Research and development—internal Selling, general and administrative Impairment of intangible assets and goodwill (Loss) income from operations Other income and expense: Interest income Other income and expense, net Foreign currency transaction (losses) gains Gain (loss) on loans to KTC Gain on remeasurement of investment in KTC Impairment of investment in Kenet Other-than-temporary impairment of marketable debt securities Other-than-temporary impairment of Micrel common stock Gain on sales of investments Gain on sales of patents Income (loss) before benefit (provision) for income taxes, equity (losses) earnings in unconsolidated affiliates and net (income) loss of noncontrolling interest Tax benefit (provision) Income (loss) before equity (losses) earnings in unconsolidated affiliates and net (income) loss of noncontrolling interest Equity (losses) earnings in unconsolidated affiliates Net income (loss) Net (income) loss attributable to the noncontrolling interest Net income (loss) attributable to the controlling interest Net income (loss) per share: Basic Diluted Weighted average number of common shares outstanding: Basic Diluted Balance Sheet Data: Cash and cash equivalents and marketable debt securities Working capital Total assets Long-term obligations Total stockholders’ equity GAAP operating (loss) income Share-based compensation expense Impairment of intangible assets and goodwill Insurance proceeds Non-GAAP operating income GAAP net income Share-based compensation expense Impairment of intangible assets and goodwill Insurance proceeds Release of valuation allowance Non-GAAP net income GAAP net income per share, diluted Share-based compensation expense Impairment of intangible assets and goodwill Insurance proceeds Release of valuation allowance Non-GAAP net income per share, diluted 31, 2006.xx, 2008. Data points on the graph are annual. Note that historical price performance is not necessarily indicative of future performance.

The following table provides information regarding repurchases of common stock made by us during the fiscal quarter ended December 31, 2011: Total number

of Shares

Purchased Average

Price Paid

per Share Total Number

of Shares

Purchased as

Part of

Publicly

Announced

Plans or

Programs Maximum

Approximate

Dollar of

Shares that

May Yet Be

Purchased

Under the

Plans or

Programs (a) 117,920 $ 3.62 117,920 $ 11,512,702 99,694 $ 3.98 99,694 $ 11,116,085 383,785 $ 3.88 144,486 $ 10,585,373 601,399 $ 3.84 362,100 (1)Amount in column (a) includes shares of our common stock withheld from employees in connection with the satisfaction of tax withholding obligations under restricted stock agreements between Kopin and certain of its key employees.(2)On December 8, 2010 the Board of Directors of the Company approved a stock repurchase plan for up to $15 million of our common stock through December 8, 2012.27Item 6. Selected Financial Data Fiscal Year Ended 2011 2010 2009 2008 2007 (in thousands, except per share data) $ 125,465 $ 116,623 $ 108,118 $ 107,582 $ 94,191 5,680 3,763 6,537 7,223 3,958 131,145 120,386 114,655 114,805 98,149 82,110 81,224 75,983 77,980 78,625 3,742 2,693 3,586 5,076 3,157 22,133 17,041 10,561 10,898 8,300 18,929 14,838 14,136 15,980 18,009 5,000 — — — — 131,914 115,796 104,266 109,934 108,091 (769 ) 4,590 10,389 4,871 (9,942 ) 1,305 2,192 2,181 3,281 4,451 93 77 728 49 17 12 (419 ) (1,005 ) 2,296 93 — — 1,188 (1,188 ) — — — 599 — — — — — (2,691 ) — (151 ) — (927 ) (1,252 ) — — — — (224 ) (123 ) 369 2,598 — — — 156 770 6,324 — — 1,784 5,218 9,088 271 4,438 1,015 9,808 19,477 5,142 (5,504 ) 3,541 (252 ) (690 ) (792 ) (465 ) 4,556 9,556 18,787 4,350 (5,969 ) (296 ) (600 ) 483 (1,081 ) (275 ) $ 4,260 $ 8,956 $ 19,270 $ 3,269 $ (6,244 ) (662 ) (22 ) 173 (683 ) (312 ) $ 3,598 $ 8,934 $ 19,443 $ 2,586 $ (6,556 ) $ 0.06 $ 0.14 $ 0.29 $ 0.04 $ (0.10 ) $ 0.06 $ 0.13 $ 0.29 $ 0.04 $ (0.10 ) 64,406 66,020 66,850 67,876 67,544 65,234 66,712 67,458 68,164 67,544 Fiscal Year Ended 2011 2010 2009 2008 2007 105,419 110,947 114,547 100,016 93,304 123,948 132,098 134,198 116,841 107,931 194,564 192,096 183,224 159,677 161,054 1,296 945 903 867 806 170,788 170,625 164,302 141,394 141,034 28DISCUSSION REGARDING THE USE OF NON-GAAP FINANCIAL MEASURESOur earnings release contains some or all We have revised the prior period amounts for the sale of the following financial measuresIII-V product line, which have not been calculated in accordance with United States Generally Accepted Accounting Principles (GAAP): (i) non-GAAP operating income and operating margin, (ii) non-GAAP net income, and (iii) non-GAAP net income per share (diluted). As set forth in the “Unaudited Reconciliation of Non-GAAP Financial Measures” table found below, we derive such non-GAAP financial measures by excluding certain expenses and other items from the respective GAAP financial measure that is most directly comparable to each non-GAAP financial measure. Management uses these non-GAAP financial measures to evaluate our operating performance and compare it against past periods, make operating decisions, forecast for future periods, compare operating performance against peer companies and determine payments under certain compensation programs. These non-GAAP financial measures provide management with additional means to understand and evaluate the operating results and trends in our ongoing business by eliminating certain non-recurring expenses (which may not occur in each period presented) and other items that management believes might otherwise make comparisons of our ongoing business with prior periods and competitors more difficult, obscure trends in ongoing operations or reduce management's ability to make useful forecasts.We provide investors with non-GAAP operating income and operating margin and non-GAAP net income because we believe it is important for investors to be able to closely monitor and understand changes in our ability to generate income from ongoing businessreflected as discontinued operations. We believe these non-GAAP financial measures give investors an additional method to evaluate historical operating performance and identify trends, additional means of evaluating period-over-period operating performance and a method to facilitate certain comparisons of operating results to peer companies. We also believe that providing non-GAAP operating income and operating margin allows investors to assess the extent to which ongoing operations impact our overall financial performance. We further believe that providing non-GAAP net income and non-GAAP net income per share (diluted) allows investors to assess the overall financial performance of ongoing operations by eliminating the impact of certain tax items which may not occur in each period for which financial information is presented and which represent gains unrelated to our ongoing operations. We believe that disclosing these non-GAAP financial measures contributes to enhanced financial reporting transparency and provides investors with added clarity about complex financial performance measures.We calculate non-GAAP operating income by excluding from GAAP operating income, stock compensation expense and intangible assets and goodwill impairment charges. We calculate non-GAAP net income and net income per share (diluted) by excluding from GAAP net income and net income per share (diluted), stock compensation expense, goodwill impairment charges, insurance proceeds, and certain tax items, which may not occur in all periods for which financial information is presented. We exclude the items identified above from the respective non-GAAP financial measure referenced above for the reasons set forth with respect to each such excluded item below:Stock Compensation—we believe (1) the total amount of expense is partially outside of our control because it is based on factors such as stock price volatility and interest rates, which may be unrelated to our performance during the period in which the expense is incurred, (2) it is an expense based upon a valuation methodology premised on assumptions that vary over time, and (3) the amount of the expense can vary significantly between companies due to factors that can be outside of the control of such companies.Impairment of Intangible Assets and Goodwill—we believe such losses reflect forecasted results and do not necessarily reflect the performance of our ongoing operations for the period in which such charges are recognized.Gains from Insurance Proceeds—we believe such gains are outside the control of management and we do not believe that they reflect the underlying performance of ongoing business operations for such period.Certain Income Tax Items—includes the release of the valuation allowance which was recorded against the deferred tax assets of our Taiwanese subsidiary which do not result in a current tax refund.29 Fiscal Year Ended 2013 2012 2011 2010 2009 (in thousands, except per share data) Statement of Operations Data: Revenues: Net product revenues $ 20,575 $ 31,299 $ 59,509 $ 54,969 $ 62,512 Research and development revenues 2,323 3,343 5,150 3,172 5,691 Total revenues 22,898 34,642 64,659 58,141 68,203 Expenses: Cost of product revenues 20,655 22,042 34,659 35,597 39,003 Research and development—funded programs 1,551 2,178 3,341 2,175 3,060 Research and development—internal 15,983 12,121 13,218 10,972 8,295 Selling, general and administrative 19,125 17,166 15,991 12,322 13,047 Impairment of intangible assets and goodwill 1,511 1,705 5,000 — — 58,825 55,212 72,209 61,066 63,405 (Loss) income from operations (35,927 ) (20,570 ) (7,550 ) (2,925 ) 4,798 Other income and expense: Interest income 1,119 1,126 1,291 1,978 2,053 Other income and (expense), net 235 174 143 (31 ) 464 Foreign currency transaction (losses) gains (387 ) (1,032 ) 10 (304 ) (942 ) Impairment of investments (5,000 ) — — — — Loss on remeasurement of investment in Ikanos — (558 ) — — — Other-than-temporary impairment of marketable debt securities — — (151 ) — (927 ) Gain on sales of investments 1,899 856 369 2,598 — Gain on sales of patents — — 156 770 6,324 (2,134 ) 566 1,818 5,011 6,972 (Loss) income before benefit (provision) for income taxes, equity losses in unconsolidated affiliates and net loss (income) of noncontrolling interest (38,061 ) (20,004 ) (5,732 ) 2,086 11,770 Tax benefit (provision) 12,933 (1,099 ) — 54 (690 ) (Loss) income before equity losses in unconsolidated affiliates and net loss (income) of noncontrolling interest (25,128 ) (21,103 ) (5,732 ) 2,140 11,080 Equity losses in unconsolidated affiliates (625 ) (680 ) (297 ) (600 ) (341 ) (Loss) income from continuing operations $ (25,753 ) $ (21,783 ) $ (6,029 ) $ 1,540 $ 10,739 Income from discontinued operations, net of tax 20,147 2,789 9,713 7,300 8,436 The non-GAAP financial measures presented in the table below should not be considered in isolation and are not an alternative for the respective GAAP financial measure that is most directly comparable to each such non-GAAP financial measure. Investors are cautioned against placing undue reliance on these non-GAAP financial measures and are urged to review and consider carefully the adjustments made by management to the most directly comparable GAAP financial measures to arrive at these non-GAAP financial measures. Non-GAAP financial measures may have limited value as analytical tools because they may exclude certain expenses that some investors consider important in evaluating operating performance or ongoing business. Further, non-GAAP financial measures are likely to have limited value for purposes of drawing comparisons between companies because different companies may calculate similarly titled non-GAAP financial measures in different ways because non-GAAP measures are not based on any comprehensive set of accounting rules or principles.Fiscal year ended: 2011 2010 (769,339 ) $ 4,589,969 3,924,000 2,584,000 4,999,512 — — (1,500,000 ) $ 8,154,173 $ 5,673,969 $ 3,597,927 $ 8,934,151 3,924,000 2,584,000 4,999,512 — — (1,787,000 ) (4,266,000 ) — $ 8,255,439 $ 9,731,151 $ 0.06 $ 0.13 0.06 0.04 0.08 — — (0.03 ) (0.07 ) — $ 0.13 $ 0.15

30

| Net (loss) income | (5,606 | ) | (18,994 | ) | 3,684 | 8,840 | 19,175 | ||||||||||||

| Net loss (income) attributable to the noncontrolling interest | 896 | 632 | (605 | ) | (11 | ) | 268 | ||||||||||||

| Net (loss) income attributable to the controlling interest | $ | (4,710 | ) | $ | (18,362 | ) | $ | 3,079 | $ | 8,829 | $ | 19,443 | |||||||

| Net (loss) income per share: | |||||||||||||||||||

| Basic: | |||||||||||||||||||

| Continuing operations | $ | (0.40 | ) | $ | (0.33 | ) | $ | (0.10 | ) | $ | 0.02 | $ | 0.16 | ||||||

| Discontinued operations | 0.32 | 0.04 | 0.15 | 0.12 | 0.13 | ||||||||||||||

| Net (loss) income per share: | $ | (0.08 | ) | $ | (0.29 | ) | $ | 0.05 | $ | 0.14 | $ | 0.29 | |||||||

| Diluted: | |||||||||||||||||||

| Continuing operations | $ | (0.40 | ) | $ | (0.33 | ) | $ | (0.10 | ) | $ | 0.02 | $ | 0.16 | ||||||

| Discontinued operations | 0.32 | 0.04 | 0.15 | 0.11 | 0.13 | ||||||||||||||

| Net (loss) income per share: | $ | (0.08 | ) | $ | (0.29 | ) | $ | 0.05 | $ | 0.13 | $ | 0.29 | |||||||