| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended March 31, |

or

| or | |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For transition period from to |

| Ohio | 34-0907152 | ||

| State or other jurisdiction of incorporation or organization | (I.R.S. Employer Identification No.) | ||

| 425 Walnut Street, Suite 1800, Cincinnati, Ohio | 45202 | ||

| (Address of principal executive offices) | (Zip Code) | ||

Registrant’s

| Title of each class | Name of each exchange on which registered | |

| Common Shares, without par value | The NASDAQ Stock Market LLC | |

As of June 1, 2012, the Registrant had the following number of Common Shares outstanding: 21,935,487 of which 7,518,422 were held by affiliates.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’sour definitive Proxy Statement to be used in connection with its 2012 Annual Meeting of Shareholders are incorporated by referenceproxy statement into Part III of the Original Filing is hereby deleted.

Amendment No. 1 does not amend or otherwise update any other information in the Original Filing and does not purport to reflect any information or events subsequent to the filing thereof. Accordingly, this Amendment should be read in conjunction with the Original Filing and with our filings with the SEC subsequent to the Original Filing.

AGILYSYS, INC.

ANNUAL REPORT ON FORM 10-K

Year Ended March 31, 2012

TABLE OF CONTENTS

| ||||||

| ||||||

| ||||||

| ||||||

| ||||||

| ||||||

| ||||||

| ||||||

| ||||||

| ||||||

| ||||||

| ||||||

| ||||||

| ||||||

| PART III | ||||||

ITEM 10. | ||||||

ITEM 11. | ||||||

ITEM 12. | ||||||

ITEM 13. | ||||||

ITEM 14. | ||||||

| PART IV | ||||||

ITEM 15. | ||||||

| R. Andrew Cueva | Age 42 | Director since 2008 |

2

| Keith M. Kolerus | Age 67 | Director since 1998 |

| Robert A. Lauer | Age 69 | Director since 2001 |

| Robert G. McCreary III | Age 61 | Director since 2001 |

| James H. Dennedy | Age 47 | Director since 2009 |

| Jerry C. Jones | Age 57 | Director since 2012 |

| John Mutch | Age 56 | Director since 2009 |

| Name | Age | Current Position | Previous Positions |

| Robert R. Ellis | 39 | Senior Vice President and Chief Financial Officer since October 2011, Treasurer since January 2012, and Chief Operating Officer since October 2012. | Vice President of Accounting and Financial Operations and Principal Accounting Officer at Radiant Systems, Inc. from 2007 to October 2011. Corporate Controller and director at Radiant from 2003 to 2007. |

| Kyle C. Badger | 45 | Senior Vice President, General Counsel and Secretary since October 2011. | Executive Vice President, General Counsel and Secretary at Richardson Electronics, Ltd. from 2007 to October 2011. Senior Counsel at Ice Miller LLP from 2006 to 2007. Partner at McDermott, Will & Emery LLP from 2003 to 2006. |

| Larry Steinberg | 45 | Senior Vice President and Chief Technology Officer since June 2012. | Senior Vice President, Technology for us in May 2012. Principal Development Manager, Microsoft Corporation from August 2009 to April 2012, and Principal Architect from June 2007 to July 2009. Founder and Chief Technology Officer of Engyro Corporation from March 1995 to May 2007. |

| Janine K. Seebeck | 37 | Vice President and Controller since November 2011. | Vice President of Finance, Asia Pacific, at Premiere Global Services, Inc. from 2008 to April 2011. Vice President, Corporate Controller at Premiere from 2002 to 2008. |

This Annual ReportThe Code of Business Conduct adopted by our board of directors applies to all directors, officers, and employees of the Company and incorporates additional ethics standards applicable to our Chief Executive Officer, Chief Financial Officer, and other publiclysenior financial officers of the Company, and any person performing a similar function. The Code of Business Conduct is reviewed annually by the Audit Committee, and recommendations for change are submitted to the board of directors for approval. The Code of Business Conduct is available documents,on our website at www.agilysys.com, under Investor Relations. The Company has in place a hotline available for use by all employees, as described in the Code of Business Conduct. Any employee can anonymously report potential violations of the Code of Business Conduct through the hotline, which is managed by an independent third party. Reported violations are promptly reported to and investigated by the Company. Reported violations are addressed by the Company and, if related to accounting, internal accounting controls, or auditing matters, the Audit Committee. In addition, we intend to post on our website all disclosures that are required by law or NASDAQ listing standards concerning any amendments to, or waivers from, any provision of the Code of Business Conduct.

Director | Fees Earned or Paid in Cash ($)(1) | Stock Awards ($)(2) | Total ($) | |||

| R. Andrew Cueva | 50,000 | — | 50,000 | |||

| Jerry Jones | 35,000 | 70,000 | 105,000 | |||

| Keith M. Kolerus | 82,500 | 70,000 | 152,500 | |||

| Robert A. Lauer | 55,000 | 70,000 | 125,000 | |||

| Robert G. McCreary, III | 35,000 | 70,000 | 105,000 | |||

| John Mutch | 47,500 | 70,000 | 117,500 | |||

| (1) | Fees are paid quarterly. |

| (2) | Amounts in this column represent the grant date fair value of the restricted shares computed in accordance with Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 718. As of March 31, 2013, the aggregate number of unexercised stock options held by each non-employee director was as follows: Mr. Kolerus, 22,500; Mr. Lauer, 22,500; and Mr. McCreary, 22,500. |

Component | Threshold | Maximum | ||||

Payout (% of target incentive) | Required Achievement of Performance Measures (%) | Payout (% of target incentive) | Required Achievement of Performance Measures (%) | |||

| Revenue | 90 | 97.7 | 150 | 108.3 | ||

| Gross Profit | 90 | 92.6 | 150 | 101.9 | ||

| Adjusted Operating Income | 90 | 83.3 | 150 | 283.3 | ||

| Adjusted Operating Income-RSG | 90 | 83.3 | 150 | 283.3 | ||

3

Part I

Overview

We are

| Performance Metrics | Annual Incentive | |||||||||

| Target Incentive as a % of salary | Component | Weight | Target | Actual | Target (1) | Payout (1) | ||||

| James H. Dennedy – 88% | Revenue: AGYS | 25% | $216.0M | $234.2M | $87,500 | $131,250 | ||||

| Gross Profit: AGYS | 40% | $86.4M | $89.3M | $140,000 | $210,000 | |||||

| AOI: AGYS | 35% | $3.0M | $6.6M | $122,500 | $168,534 | |||||

| Total | $350,000 | $509,784 | ||||||||

| Robert R. Ellis – 75% | Revenue: AGYS | 25% | $216.0M | $234.2M | $56,250 | $84,375 | ||||

| Gross Profit: AGYS | 40% | $86.4M | $89.3M | $90,000 | $135,000 | |||||

| AOI: AGYS | 35% | $3.0M | $6.6M | $78,750 | $108,343 | |||||

| Total | $225,000 | $327,718 | ||||||||

| Kyle C. Badger– 50% | Revenue: AGYS | 15% | $216.0M | $234.2M | $18,750 | $28,125 | ||||

| Gross Profit: AGYS | 20% | $86.4M | $89.3M | $25,000 | $37,500 | |||||

| AOI: AGYS | 15% | $3.0M | $6.6M | $18,750 | $25,796 | |||||

| MBO | 50% | $62,500 | $62,500 | |||||||

| Total | $125,000 | $153,921 | ||||||||

| Paul A. Civils – 55% | AOI: RSG | 75% | $11.0M | $11.0M | $107,250 | $144,720 | ||||

| MBO | 25% | $35,750 | $35,750 | |||||||

| Total | $143,000 | $180,470 | ||||||||

| Larry Steinberg - 60% | Revenue: AGYS | 15% | $216.0M | $234.2M | $18,147 | $27,221 | ||||

| Gross Profit: AGYS | 20% | $86.4M | $89.3M | $24,196 | $36,294 | |||||

| AOI: AGYS | 15% | $3.0M | $6.6M | $18,147 | $24,967 | |||||

| MBO | 50% | $60,490 | $60,490 | |||||||

| Total | $120,980 | $148,972 | ||||||||

| (1) | Pro-rated from hire date for Mr. Steinberg. See Grants of Plan-Based Awards table for annualized award amounts. |

Name | Percent of Salary (%) | Total LTIP Value ($) | SSARs Granted (#) | Restricted Shares Granted (#) | |||

| James H. Dennedy | 190 | 760,000 | 78,350 | 50,938 | |||

| Robert R. Ellis | 60 | 171,000 | 17,628 | 11,461 | |||

| Kyle C. Badger | 50 | 125,000 | 12,886 | 8,378 | |||

| Paul A. Civils | 65 | 169,000 | 17,422 | 11,327 | |||

| Larry Steinberg | 85 | 191,279 | 17,513 | 11,067 | |||

We operate extensively throughout North America, with additional salesnarrowly defining a voluntary termination that triggers severance benefits. Additionally, the Company benefits greatly from the non-competition, non-disclosure, and support officesnon-solicitation clauses contained in the United Kingdomemployment agreements. Except for Messrs. Dennedy and Asia. Agilysys hasBadger, the employment agreements do not contain a change of control provision. For each of Messrs. Dennedy and Badger, if there is a change of control within two operating segments: Hospitality Solutions Group (HSG)years after April 1, 2012, and Retail Solutions Group (RSG).

Reference herein to any particular year or quarter refers to periodsOctober 31, 2011, respectively,(the dates of their employment agreements), and within the fiscal year ended March 31. For example, fiscal 2012 referssame two-year period his employment with the Company or its successor is terminated without cause, then he will be paid severance equal to two years of each of his base salary and target annual incentive. This change in control benefit enhances our ability to maintain a shareholder focused approach to change of control situations and provides these executives reasonable support following both a change of control and termination (commonly called a “double trigger” requirement). The Compensation Committee

Title | Multiple of Director Annual Retainer and Executive Base Salary | Number of Shares | ||

| 2 Years | 4 Years | 2 Years | 4 Years | |

| Director | 3x | 6x | 15,000 | 45,000 |

| CEO | 2.5x | 5x | 125,000 | 250,000 |

| Senior Vice President | 0.5x | 2x | 15,000 | 75,000 |

| LTIP Participants | — | 0.5x | 2,500 | 15,000 |

History2013 and Significant Events

Organized in 1963the Proxy Statement for its 2013 Annual Meeting of Shareholders.

In 2007, we divested KeyLink Systems and exited the enterprise computer distribution business. We used the proceeds from that sale to return cash to shareholders and fund a number of acquisitions that broadened our solutions and capabilities portfolios. In calendar 2007, we acquired InfoGenesis and Visual One Systems Corp., significantly expanding our specialized offerings to the hospitality industry through enterprise-class, point-of-sale (POS) and software solutions tailored for a variety of applications in cruise, golf and spa, gaming, lodging, resort and catering. These offerings feature highly intuitive, secure and robust solutions, easily scalable across multiple departments or property locations. In fiscal 2008, we began reporting three primary operating segments: Hospitality Solutions Group (HSG), Retail Solutions Group (RSG) and Technology Solutions Group (TSG).

In fiscal 2012, we sold our TSG segment and restructured the business model to focus on higher-margin opportunities in the hospitality and retail sectors, which also hold greater potential for profitable growth. In that same year, we reduced our real-estate footprint and lowered overhead costs by relocating corporate services from Solon, Ohio to Alpharetta, Georgia, which moved senior management closer to our operating units.

Today, we are focused on providing end-to-end solutions that utilize state-of-the-art technology to enhance guest experiences2013 compensation for our customers wishing to promote their respective brands. We helpNamed Executive Officers, including our customers win the guest recruitment battleCEO and in turn, grow revenue, reduce costs and increase efficiency. This is accomplished by developing and deploying intuitive solutions that increase speed and accuracy, enabling more effective management, intelligent upselling, reduced shrinkage, improved brand recognition and better control of the customer relationship. Our strategy is to increase the proportion of revenue we derive from ongoing support and maintenance agreements, software as a subscription service, cloud applications and professional services.

Products, Support and Professional Services

We are a leading developer and marketer of end-to-end technology solutions for the hospitality and retail industries, including hardware and software products; support, maintenance and subscription services; and professional services. Areas of specialization are point-of-sale, property management, inventory and procurement, mobile and wireless solutions designed to streamline operations, improve efficiency and enhance the guest experience.

4

To align with our strategic restructuring in fiscal 2012 and enhance transparency into the business, we commenced presenting revenue and costs of goods sold in three categories:

Products (hardware and software)

Support, maintenance and subscription services

Professional services

Total revenue from continuing operations for these three specific areas of offerings follows:

| For The Year Ended March 31, | ||||||||||||

| (In thousands) | 2012 | 2011 | 2010 | |||||||||

Products | $ | 105,141 | $ | 104,769 | $ | 103,501 | ||||||

Support, maintenance and subscription services | 73,171 | 70,729 | 63,218 | |||||||||

Professional services | 30,577 | 27,183 | 26,787 | |||||||||

Total | $ | 208,889 | $ | 202,681 | $ | 193,506 | ||||||

Products: Products revenue includes resold hardware and proprietary and remarketed software that are deployed as an integral component of the solutions we provide. Our proprietary product suite is comprised of:

Property Management Systems (“PMS”)

|

Agilysys Visual One™ PMS is installed in hotels ranging from 50-1,500 rooms. For complex resorts that require an enterprise-wide system, Visual One provides an integrated solution with interfaces to leading global distribution systems (GDSs) and other Agilysys products.

Agilysys Guest Express Kiosk module is a self-service kiosk system for both the LMS PMSCFO and the Visual One PMS that expedites front desk check-in and check-out. Using the Guest Express Kiosk module, hotel guests can check in, encode a room key, check out and obtain a receipt — all without having to wait in line at the front desk.

Point-of-Sale

Agilysys InfoGenesis™ POS is award-winning, enterprise level software primarilyother three most highly compensated executive officers whose total compensation exceeded $100,000 for food and beverage products. The software is centralized and designedfiscal year 2013.

Agilysys MPOS is a handheld point-of-sale solution that integrates with InfoGenesis POS to enable guest service in any location.

Agilysys eMenu, an online ordering application, enables our customers to capitalize on the popularity of Web and kiosk ordering while maintaining their existing company brand and workflow.

Agilysys eCash takes traditional cashless payment and stored value card capabilities and integrates them directly with InfoGenesis POS, increasing customers’ payment options.

Name and Principal Position | Year | Salary ($)(1) | Bonus ($)(2) | Stock Awards ($)(3) | Option Awards ($)(3) | Non-Equity Incentive Plan Compen-sation Earnings ($)(4) | Change in Pension Value and Non- qualified Deferred Compen- sation Earnings ($) | All Other Compen- sation ($)(5) | Total ($) | ||||||||

| James H. Dennedy | FY13 | 400,000 | — | 379,997 | 380,309 | 509,784 | — | 20,481 | 1,690,571 | ||||||||

| President and | FY12 | 309,928 | — | 311,640 | — | 369,045 | — | 10,780 | 1,001,393 | ||||||||

| Chief Executive Officer | |||||||||||||||||

| Robert R. Ellis | FY13 | 290,934 | — | 85,499 | 85,566 | 327,718 | — | 11,186 | 800,903 | ||||||||

| Senior Vice President, Chief Operating Officer, Chief | FY12 | 131,705 | — | 123,199 | 81,335 | 88,591 | — | 3,520 | 428,350 | ||||||||

| Financial Officer and Treasurer | |||||||||||||||||

| Kyle C. Badger | FY13 | 250,000 | — | 62,500 | 62,548 | 153,921 | — | 37,796 | 566,765 | ||||||||

| Senior Vice President, General | — | ||||||||||||||||

| Counsel and Secretary | |||||||||||||||||

| Paul A. Civils | FY13 | 260,000 | — | 84,499 | 84,566 | 180,470 | — | 21,319 | 630,854 | ||||||||

| Senior Vice President and | FY12 | 255,000 | — | 82,874 | 82,877 | 129,082 | — | 22,656 | 572,489 | ||||||||

| General Manager | |||||||||||||||||

| Larry Steinberg | FY13 | 201,511 | 39,550 | 574,750 | 95,660 | 148,972 | — | 7,646 | 1,068,089 | ||||||||

| Senior Vice President, Chief | |||||||||||||||||

| Technology Officer | |||||||||||||||||

InfoGenesis POS, eMenu and eCash are available through either traditional software licensing or via subscription.

Inventory & Procurement

Agilysys Stratton Warren System (SWS) integrates with all leading financial and POS software products. The software manages the entire procurement process via e-commerce, from the point of business development to managing enterprise-wide backend systems and daily operations.

|

5

|

|

Eatec and Stratton Warren System solutions are available either through traditional software licensing or via subscription.

Document Management

Agilysys DataMagine™ provides a U.S.-patented imaging module and archiving solution that allows users to capture and retrieve documents and system-generated information. DataMagine integrates with all Agilysys products, adding functionality and increasing benefit to customers.

Activities

Agilysys GolfPro is a module that offers golf property managers complete pro shop management. Tee time scheduling, member profile/billing, tournament management and Web and e-mail access are bundled into one solution.

Agilysys Spa Management software covers all aspects of running a spa business, from scheduling guests for services to managing staff schedules. The software also integrates with Agilysys PMS solutions.

|

Agilysys Visual One Activities software streamlines the management of all of the amenities and activities a property has to offer. Staff can easily schedule and personalize reservations for guests; activities then appear on itinerary/confirmations.

Support, Maintenance and Subscription Services:Contracted technical support, maintenance and subscription services are a significant portion of our consolidated revenue. Growth has been driven by a strategic focus on developing and promoting these offerings, which typically generate higher profit margins than products revenue. In addition to our deliberate positioning, market demand for proper maintenance and updates that enhance reliability, as well as the desire for flexibility in purchasing options, are reinforcing this trend. Our commitment to exceptional service has enabled us to become a trusted partner with customers who wish to optimize the level of service they provide to their guests and maximize commerce opportunities both on- and off-premise.

Professional Services:We have industry-leading expertise in designing, implementing, integrating and installing customized solutions into both legacy and newly created platforms. For existing enterprises, we seamlessly integrate new systems; and for start-ups and fast-growing customers, we become a partner that can manage large-scale rollouts and tight construction schedules. Extensive experience ranges from staging equipment to phased rollouts and training staff in a manner that saves time and money for our customers.

Prior to the divestiture of TSG operations, we resold IT products and services from the Hewlett-Packard Company (HP), International Business Machines Corporation (IBM), Oracle Corporation (Oracle) and other original equipment manufacturers (OEMs). Operating results from the former TSG are reported as components of discontinued operations.

We have maintained our strong relationship with IBM Retail Services and intend to continue to be a leading provider of related solutions and services in the supermarket, drug chain, general-retail and other hospitality segments.

Segment Reporting

Subsequent to the sale of our TSG business in fiscal 2012, we were left with two remaining reportable business segments: HSG and RSG. Prior to that, we had been reporting three business segments: HSG, RSG and TSG. See Note 16 to Consolidated Financial Statements titledBusiness Segments for a discussion of our segment reporting.

Hospitality Solutions Group (HSG)

HSG develops, markets and sells property and lodging management, point-of-sale, and inventory and procurement applications to operate hotel, casino, destination resort, cruise line and foodservice management establishments in the hospitality industry. We offer solutions that provide comprehensive control of the customer’s property operations — from reservations, check in, point-of-sale and other guest-engagement activities to inventory and procurement management and document management.

6

Retail Solutions Group (RSG)

RSG is one of the largest North American systems integrators of retail point-of-sale, self-service and wireless solutions with proprietary business consulting, implementation and hardware maintenance and support services. Our extensive experience in all phases of wireless infrastructure and integration with legacy systems enables our customers to capture the promise of today’s mobile technology. Our mobile solutions extend the customer’s operations to portable devices, increasing customer satisfaction and productivity with integrated software that reduces security exposure. We also sell POS and mobile POS (MPOS) solutions to facilitate the check-out process as well as other self-service capabilities.

Our RSG expertise encompasses a suite of support and professional services including consultation, analysis, design, installation and implementation, as well as onsite maintenance and ongoing help-desk support. Our comprehensive portfolio of support services provides total lifecycle management for our customers’ in-store solutions to help increase their return on investment and lower their total cost of ownership.

Representative Agilysys clients include:

| For Mr. Steinberg, salary is from start date through March 31, 2013. |

|

| ||

| For Mr. Steinberg, amount consists of hiring bonus. |

| |||

| Stock Awards include grants of restricted shares and performance shares. Option Awards include SSAR grants. Amounts disclosed do not represent the economic value received by the Named Executive Officers. The value, if any, recognized upon the exercise of a SSAR will depend upon the market price of the shares on the date the SSAR is exercised. The value, if any, recognized for restricted and performance shares will depend upon the market price of the shares upon vesting. In accordance with SEC rules, the values for restricted and performance shares and SSARs are equal to the aggregate grant date fair value for each award computed in accordance with FASB ASC Topic 718. The values for restricted and performance shares are based on the closing price on the grant date. The values for SSARs are based on the Black-Scholes option pricing model. A discussion of the assumptions used in determining these valuations is set forth in Note 14 of the Notes to Consolidated Financial Statements of the Company’s 2013 Annual Report. For Stock Awards, the amounts shown represent grants of restricted shares to each Named Executive Officer as part of the executive's annual long-term equity grant and for Mr. Steinberg includes grants of restricted shares as a long-term inducement award upon his hire. |

| |||

| Amounts represent annual incentive payments received in 2013 and 2012 based on pre-set incentive goals established at the beginning of each fiscal year and tied to the Company’s financial, strategic, and operational goals. |

| ||

| All other compensation includes the following compensation, calculated based on the aggregate incremental cost to the Company of the benefits noted: |

Name | 401(k) Company Match ($) | Executive Life Insurance ($) | Relocation ($)(a) | Severance ($) | Gross-ups ($) | All Other ($)(b) | Total ($) | |||||||

| J. Dennedy | 9,139 | 1,654 | 7,755 | — | — | 1,933 | 20,481 | |||||||

| R. Ellis | 8,931 | 754 | — | — | — | 1,501 | 11,186 | |||||||

| K. Badger | 8,891 | 909 | 27,149 | — | — | 847 | 37,796 | |||||||

| P. Civils | 6,514 | 6,295 | — | — | — | 8,510 | 21,319 | |||||||

| L. Steinberg | 5,771 | 993 | — | — | — | 882 | 7,646 | |||||||

| |||

| Messrs. Dennedy and Badger received travel and relocation assistance during their transition to the Company's corporate offices, including expenses for travel, temporary housing, car rental, moving, and incidentals. Amount disclosed represents actual cost to the Company, or amount reimbursed to the executive officer, for such expenses. |

Name | Grant Date | Estimated Future Payouts Under Non-Equity Incentive Plan Awards ($)(1) | Estimated Future Payouts Under Equity Incentive Plan Awards ($) | All Other Stock Awards Number of Shares of Stock (#)(2) | All Other Option Awards: Number of Securities Underlying Options (#)(3) | Exercise or Base Price of Option Awards ($/share) | Grant Date Fair Value of Stock and Option Awards ($)(4) | ||||||||

Threshold ($) | Target ($) | Maximum ($) | Threshold (#) | Target (#) | Maximum (#) | ||||||||||

James H. Dennedy | 6/12/12 | 50,938 | 78,350 | 7.46 | 760,306 | ||||||||||

| 3/20/12 | 315,000 | 350,000 | 525,000 | ||||||||||||

Robert R. Ellis | 6/12/12 | 11,461 | 17,628 | 7.46 | 171,065 | ||||||||||

| 3/20/12 | 153,900 | 171,000 | 256,500 | ||||||||||||

| 11/8/12 | 202,500 | 225,000 | 337,500 | ||||||||||||

| Kyle C. Badger | 6/12/12 | 8,378 | 12,886 | 7.46 | 125,048 | ||||||||||

| 3/20/12 | 112,500 | 125,000 | 187,500 | ||||||||||||

| Paul A. Civils | 6/12/12 | 11,327 | 17,422 | 7.46 | 169,065 | ||||||||||

| 3/20/12 | 128,700 | 143,000 | 214,500 | ||||||||||||

| Larry Steinberg (5) | 5/9/12 | 48,794 | 17,513 | 8.64 | 670,410 | ||||||||||

| 5/9/12 | 108,882 | 120,980 | 181,470 | — | 17,728 | 17,728 | |||||||||

| |||

| Amounts shown in the columns under Estimated Future Payouts Under Non-Equity Incentive Plan Awards represent fiscal year 2013 annual threshold, target, and maximum cash-based annual incentives granted under the annual incentive plan. Total threshold, target, and maximum payouts were conditioned on achievement of weighted goals based on revenue, gross profit, adjusted operating income, and achievement of individual MBOs as applicable for each Named Executive Officer. For Mr. Ellis, the non-equity incentive award on November 8, 2012 replaced the award o March 20, 2012, upon his being appointed to the additional office of Chief Operating Officer. Fiscal year 2013 payouts for each Named Executive Officer pursuant to these awards are shown in the Summary Compensation Table above in the column titled Non-Equity Incentive Plan Compensation. Threshold, target, and maximum amounts represent annualized award amounts. Actual payouts for fiscal year 2013 for Mr. Steinberg were pro-rated based on his hire date. Further explanation of potential and actual payouts by component is set forth in the Compensation Discussion and Analysis – Annual Incentives. |

| |

| (2) | The |

| The share amounts represent SSARs granted at the fair market value of the shares on the grant date as fiscal year 2013 long-term incentive awards. The SSARs are exercisable in thirds beginning on March 31, 2013. All SSARs have a seven-year term. |

| |||

(4) | The |

| ||||

| For Mr. Steinberg, grants were approved on March 29, 2012, effective as of his date of hire on May 9, 2012. |

| Name (1) | Grant Date | Option Awards | Stock Awards | |||||||||

Number of Securities Underlying Unexercised Options (#) | Option Exercise Price ($) | Option Date Expiration | Number of Shares of Stock That Have Not Vested (#)(3) | Market Value of Shares of Stock That Have Not Vested ($)(4) | ||||||||

Exercisable | Unexercisable (2) | |||||||||||

| James H. Dennedy | 6/12/2012 | 26,116 | 52,234 (a) | 7.46 | 6/12/2019 | 33,959 (e) | 337,552 | |||||

| Robert R. Ellis | 10/10/2011 | 10,700 | 5,350 (b) | 8.14 | 10/10/2018 | 5,379 (f) | 53,467 | |||||

| 6/12/2012 | 5,876 | 11,752 (b) | 7.46 | 06/12/2019 | 7,641 (f) | 75,952 | ||||||

| Kyle C. Badger | 10/31/2011 | 7,462 | 3,732 (c) | 8.49 | 10/31/2018 | 3,556 (g) | 35,347 | |||||

| 6/12/2012 | 4,295 | 8,591 (c) | 7.46 | 6/12/2019 | 5,586 (g) | 55,525 | ||||||

| Paul A. Civils | 7/28/2006 | 8,000 | 15.85 | 7/28/2016 | ||||||||

| 5/21/2007 | 12,000 | 22.21 | 5/21/2017 | |||||||||

| 5/23/2008 | 12,000 | 9.82 | 5/23/2018 | |||||||||

| 11/13/2008 | 40,000 | 2.51 | 11/13/2018 | |||||||||

| 5/22/2009 | 15,700 | 6.83 | 5/22/2016 | |||||||||

| 6/7/2010 | 40,000 | 6.20 | 6/7/2017 | |||||||||

| 8/11/2011 | 11,882 | 5,941 | 7.42 | 8/11/2018 | 3723 | 37,007 | ||||||

| 6/12/2012 | 5,807 | 11,615 | 7.46 | 6/12/2019 | 7,552 | 75,067 | ||||||

| Larry Steinberg | 5/9/2012 | 5,837 | 11,676 (d) | 8.64 | 5/9/2019 | 56,167 (h) | 558,300 | |||||

| |

| (1) | For Mr. Civils, all unvested SSARs were forfeited upon separation, and unexercised SSARs expired 90 days after separation. |

| (2) | As of March 31, 2013, the vesting schedule for the time-vested SSARs was as follows: |

| (a) | 26,117 on March 31, 2014 and 2015 |

| (b) | 11,226 on March 31, 2014 and 5,876 on March 31, 2015 |

| (c) | 8,027 on March 31, 2014 and 4,296 on March 31, 2015 |

| (d) | 5,838 on March 31, 2014 and 2015 |

| (3) | As of March 31, 2013, the vesting schedule for the time-vested stock awards was as follows: |

| (e) | 16,979 on March 31, 2014 and 16,980 March 31, 2015 |

| (f) | 9,199 on March 31, 2014 and 3,821 on March 31, 2015 |

| (g) | 6,349 on March 31, 2014 and 2,793 on March 31, 2015 |

| (h) | 10,356 on March 31, 2014, 16,840 on May 9, 2014, 10,356 on March 31, 2015; 887 on May 9, 2015; and 17,728 upon the successful development and sale of our next generation property management system. |

| (4) | Calculated based on the closing price of the shares on March 28, 2013 of $9.94 per share. |

Name | Option Awards | Stock Awards | ||||||

Number of Shares Acquired on Exercise (#) | Value Realized on Exercise ($) | Number of Shares Acquired on Vesting (#)(1) | Value Realized on Vesting ($)(2) | |||||

| James H. Dennedy | — | — | 23,979 | 224,911 | ||||

| Robert R. Ellis | — | — | 9,198 | 91,428 | ||||

| Kyle C. Badger | — | — | 6,348 | 63,099 | ||||

| Paul A. Civils | — | — | 7,498 | 74,350 | ||||

| Larry Steinberg | — | — | 10,355 | 102,929 | ||||

| (1) | Includes partial vesting of time-vested restricted shares granted in 2012 and 2013. |

| (2) | The | |||

|

| |||

|

| |||

|

|

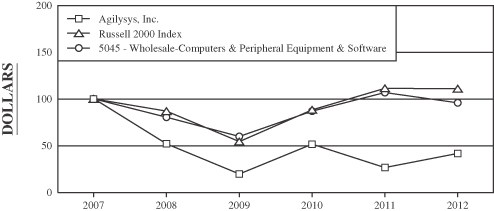

Change of Control Fourth quarter Third quarter Second quarter First quarter Fourth quarter Third quarter Second quarter First quarter January 1-31 February 1-29 March 1-31 Total Agilysys, Inc. Russell 2000 Peer Group Operating results Net revenue Gross profit Operating loss Loss from continuing operations, net of taxes Income (loss) from discontinued operations, net of taxes Net (loss) income Per share data (1) Basic and diluted Loss from continuing operations Income (loss) from discontinued operations Net (loss) income Weighted-average shares outstanding Basic and diluted Balance sheet data at year end Cash and cash equivalents Working capital Total assets (2) Total debt Total shareholders’ equity IndustryTermination and MarketsThe hospitalityfollowing table and retail industries encompass a wide variety of market sectors and customers. We operate extensively throughout North America, with additional sales and support officesdiscussion summarize certain information related to the total potential payments which would have been made to the Named Executive Officers in the United Kingdom, Singapore and Hong Kong. Sales to customers outsideevent of termination of their employment with the United States represent less than 10% of our total revenue.The hospitality industry is made upCompany, including in the event of a numberchange of defined markets including lodging, casinos, cruise ships, resorts and spas, franchise operators, restaurant chains, stadiums, arenas and other customer-service providers. control, effective March 31, 2013, the last business day of fiscal year 2013.Employment Agreements - Fiscal Year 2013 Active Named Executive Officers. The industry is highly fragmented. For example, in the lodging segment, no single hotel brand accounts for more than 4% of all hotel rooms in the United States. According toSmith Travel Research, the U.S. lodging industry generated $108 billion in room revenue in calendar 2011, with an average of approximately 60% of 4.9 million available rooms occupied. This compares with 57.5% in 2010 and a market-cycle peak occupancy rate of 63.1% in 2006.The hospitality industry is economically sensitive. Business and destination-resort travelNamed Executive Officers are correlated with the economic conditions in their respective markets. Competition is intense for consumer spending, and hospitality industry participants are seeking ways to enhance the experience of their guests. We are seizing this opportunity by providing guests connectivity and intuitive engagement tools, enabling our customers to enhance their brands and better manage their operations’ growth and profitability. In addition to product solutions that are designed and customized to meet unique facility or multi-facility needs, we also provide an array of support and subscription options for maintaining systems and professional services for implementation and rollouts.We have a significant customer base in the commercial casino and gaming sector. Roughly one-quarter of the U.S. adult population visits a casino at least once a year. Amenities in contemporary casinos extend well beyond gaming to include a variety of entertainment and leisure options as well as modern convention centers and meeting facilities to attract the business market. International gaming markets are growing rapidly both in size and new jurisdictions. Asian gaming markets are reporting robust growth. In 2006, gross gaming revenue in Macau surpassed that of the Las Vegas Strip — with a significant number of U.S.-based operators seeking to open new properties in the region. As the market-share leader in providing Property Management Systems (PMS) to casinos on the Las Vegas Strip, we are well positioned to benefit from these strong and long-standing relationships as our customer base expands into international markets. Additionally, as modern facilities evolve toward cashless operations and digital track-and-log of unique guest behavior, we are able to provide the requisite technologies and expertise to satisfy their needs.We also have expertise in serving the unique needs of Cruise ship operators. According to theCruise Industry Overview — 2011 State of the Cruise Industry report, the cruise industry is the fastest growing category in the leisure travel market. In 2011, the industry7anticipated a total of 16 million passengers, a 6.6% increase from 2010. In addition, 14 new ships were introduced, featuring such modern amenities as planetariums, golf simulators, water parks, ice-skating rinks and rock-climbing walls. The current order book, which extends through 2014, includes 26 new builds.Similarly, the modern retail industry is rapidly transitioning to a higher level of engagement with customers. Retailers selling directly to consumers include: purveyors of softlines, such as clothing, accessory/shoe and department stores; and hardlines, such as home improvement, home furnishings and electronics; as well as staples such as groceries. Integrating our innovative technology with marketing is allowing Retail Solutions customers to enjoy the benefits of gift cards and loyalty programs. Other solutions such as mobile POS enable them to reduce wait times, increase accuracy and accelerate management reporting. For rapidly expanding retailers and retailers that are engaged in large store-wide POS technology refreshment, we manage large-scale implementation and roll-out — including procurement, staging and installation, post-sale service and maintenance contracts — to ensure a reliable and secure environment.CustomersOur customers include large, medium-sized and boutique companies, and divisions or departments of large corporations in the hospitality and retail industries. We concentrate on serving the needs of customers in a range of customer-focused settings where brand differentiation is important, particularly in the lodging, casino, destination resort, cruise line, foodservice and retail industries where competition for guest recruitment is intense.Currently, our customer base is highly fragmented, with no single customer representing more than 10% of consolidated revenue from continuing operations.SeasonalityPrior to the sale of TSG, we traditionally had experienced a seasonal increase in sales during our fiscal third quarter ending December 31. The HSG and RSG operating units have traditionally experienced a seasonal decrease in revenue during our fiscal first quarter ending June 30. Although we are unable to predict whether uneven sales patterns will continue over the long term, we believe this particular pattern is moderating as a result of exiting the TSG business. For example, third-quarter revenue from continuing operations was 25%, 29% and 31% of annual revenue for fiscal years 2012, 2011 and 2010, respectively. In addition, occasionally the timing of large one-time orders such as those associated with substantial retail product rollouts will create volatility in our quarterly results.CompetitionWe face a competitive market environment for the solutions we provide. Competition exists with respect to developing and maintaining relationships with customers, pricing for products and solutions, levels of support and customer service. We compete with a number of other solution providers and, occasionally, with some of our own suppliers in the RSG business segment.Within HSG, we compete with other full-service providers that sell and service bundled POS and PMS solutions comprised of hardware, software, support and services. These companies, some of which are much larger than we are, include MICROS Systems, Inc., NCR, Par Technology, Multi-System, Inc., and Infor. We also compete with software companies like IDeaS Revenue Solutions, POSitouch, Northwind and Xpient Solutions and, to a lesser extent, hardware vendors such as IBM, HP, Dell, Casio, and Toshiba. In addition, we compete with PMS systems that are designed and maintained in-house by large hotel chains.RSG’s competitive market place is highly fragmented and regionalized. We compete primarily with regional integrators, regional and national Value Added Resellers Solution Providers and niche vendors.Environmental MattersWe believe we are in compliance in all material respects with all applicable environmental laws. Presently, we do not anticipate that such compliance will have a material effect on capital expenditures, earnings or competitive position with respect to any of our operations.EmployeesAs of June 1, 2012, we had 751 employees. We are noteach a party to an employment agreement with the Company. If we terminate any collective bargaining agreements, have had no strikesof the Named Executive Officers employment without cause, he will receive his base salary and applicable health benefits for 12 months and his target annual incentive following termination. If the Company changes his position such that his compensation or work stoppagesresponsibilities are substantially lessened, or, for Mr. Civils, if he is required to relocate more than 50 miles away, he may terminate his employment within 30 days of the change in position and considerwill receive his severance benefits. If he is terminated for cause or voluntarily terminates his employment for any reason other than a change in position, he is prohibited for a one-year period following termination (the “Noncompetition Period”) from being employed by, owning, operating, controlling, or being connected with any business that competes with the Company. If any of these executives is terminated without cause or terminates his employment due to change in position, we may, in our employee relationssole discretion, elect to pay his severance benefits for all or any part of the Noncompetition Period, which payments are in lieu of the severance payments and benefits coverage described above and, so long as we make such payments, he will be good.8Accessbound by the non-competition provisions described above. Each executive's agreement also contains an indefinite non-disclosure provision for the protection of the Company's confidential information and one-year non-solicitation and non-compete provisions. For each of Messrs. Dennedy and Badger, if there is a change of control within two years after April 1, 2012, and October 31, 2011, respectively, (the dates of their employment agreement), and within the same two-year period his employment with the Company or its successor is terminated without cause, then he will be paid severance equal to InformationOurtwo years of each of his base salary and target annual reports on Form 10-K, quarterly reports on Form 10-Q,incentive.22Termination and Change of ControlVoluntary Termination or Termination for Cause ($)(1) JamesDennedyRobertEllisKyleBadgerPaulCivilsLarrySteinbergBase and Incentive — — — — — Accelerated Vesting — — — — — Termination without Cause or by Employee for Change in Position ($)(1) Base & Incentive 750,000 525,000 375,000 403,000 360,000 Health Insurance (2) 12,955 13,149 12,955 8,714 11,015 Accelerated Vesting — — — — — _______ _______ _______ _______ _______ Total 762,955 538,149 387,955 411,714 371,015 Change of Control ($)(3) Base & Incentive 1,500,000 — 750,000 — — Health Insurance — — — — — Accelerated Vesting/SSARs (4) 129,540 38,775 26,717 43,777 15,179 Accelerated Vesting/Stock (4) 337,552 129,419 90,871 112,074 558,300 _______ _______ _______ _______ _______ Total 1,967,092 168,194 867,588 155,851 573,479 Death or Disability ($)(5) Accelerated Vesting/SSARs (4) 129,540 38,775 26,717 43,777 15,179 Accelerated Vesting/Stock (4) 337,552 129,419 90,871 112,074 558,300 _______ _______ _______ _______ _______ Total 467,092 168,194 117,588 155,851 573,479 (1) “Cause” is defined as (i) breach of employment agreement or any other duty to the Company, (ii) dishonesty, fraud, or failure to abide by the published ethical standards, conflicts of interest, or material breach of Company policy, (iii) conviction of a felony crime or crime involving misappropriation of money or other Company property, (iv) misconduct, malfeasance, or insubordination, or (v) gross failure to perform (not including failure to achieve quantitative targets). Mr. Dennedy has 30 days to cure a breach of his employment agreement, any duty to the Company, or a material breach of Company policy. A “change in position” is the substantial lessening of compensation or responsibilities or, for Mr. Civils, the requirement to relocate to a facility more than 50 miles away. After a change in position, the executive has 30 days to notify the Company of his termination of employment. A “voluntary termination” includes death, disability, or legal incompetence. (2) Health Insurance consists of health care and dental care benefits. The amount reflects 12 months of benefits for the Named Executive Officers that participate in the Company's plans. These benefits have been calculated based on actual cost to us for fiscal year 2013. (3) Messrs. Dennedy and Badger are the only Named Executive Officers with change of control provisions. (4) SSARs and restricted shares vest upon a change of control. For SSARs (except as qualified below) the value of accelerated vesting is calculated using the closing price of $9.94 per share on March 28, 2013 less the exercise price per share for the total number of SSARs accelerated. The potential payment from the accelerated SSARs includes only the proceeds from the exercise of SSARs with an exercise price less than $9.94 since there would be no proceeds upon the exercise of “underwater” SSARs. The value of restricted shares upon vesting reflects that same $9.94 closing price. Values represent potential vesting under a hypothetical change of control situation on March 31, 2013. (5) All SSARs and restricted shares vest upon death or disability. 23Item 12. Security Ownership of CertainBeneficial Owners and Management and RelatedShareholder Matters.BENEFICIAL OWNERSHIP OF COMMON SHARESThe following table shows the number of common shares beneficially owned as of July 19, 2013 by (i) each current reports on Form 8-Kdirector; (ii) our Named Executive Officers; (iii) all directors and any amendmentsexecutive officers as a group; and (iv) each person who is known by us to these reports are available freebeneficially own more than 5% of charge through our corporate website,http://www.agilysys.com, as soon as reasonably practicable after such material is electronically filed with, or furnishedcommon shares.NameCommon SharesShares Subjectto Exercisable OptionsRestrictedShares (1)Total SharesBeneficially Owned (1)Percent ofClass (2)Directors R. Andrew Cueva (3) 5,284,648 — — 5,284,648 24.0 Jerry C. Jones 8,055 — 5,654 13,709 * Keith M. Kolerus 112,348 22,500 5,654 140,502 * Robert A. Lauer 69,441 22,500 5,654 97,595 * Robert G. McCreary, III (4) 48,599 22,500 5,654 76,753 * John Mutch 43,433 — 5,654 49,087 * Named Executive Officers Kyle C. Badger 23,063 11,757 16,411 51,231 Paul A. Civils (4) 11,941 145,389 11,275 168,605 * James H. Dennedy 146,142 26,116 59,269 231,527 1.0 Robert R. Ellis 39,671 16,576 25,540 81,787 * Larry Steinberg 10,355 5,837 68,283 84,475 * All directors and Executive Officers 5,797,696 273,175 209,048 6,279,919 Other Beneficial Owners MAK Capital One, LLC et al590 Madison Avenue, 9th FloorNew York, New York 100227,056,934 (4) 32.0 Dimensional Fund Advisors LP6300 Bee Cave RoadPalisades West, Building OneAustin, Texas 787461,846,222 (5) 8.3 The Vanguard Group, Inc.100 Vanguard BoulevardMalvern, Pennsylvania 193551,150,798 (6) 5.2 Black Rock, Inc.40 East 52nd StreetNew York, New York 100221,222,240 (7) 5.5 (1) Beneficial ownership of the shares comprises both sole voting and dispositive power, or voting and dispositive power that is shared with a spouse, except for restricted shares for which individual has sole voting power but no dispositive power until such shares vest. (2) * indicates beneficial ownership of less than 1% on July 19, 2013. (3) Comprised entirely of shares beneficially owned by MAK Capital Fund L.P. and excludes shares beneficially owned by Paloma International L.P. Mr. Cueva may be deemed to share beneficial ownership in shares that MAK Capital Fund L.P. may be deemed to beneficially own; however, Mr. Cueva disclaims beneficial ownership of the shares, except to the extent of his pecuniary interest in MAK Capital Fund L.P.’s interest in such shares. The inclusion in this table of the shares beneficially owned by MAK Capital Fund L.P. shall not be deemed an admission by Mr. Cueva of beneficial ownership of all of the reported shares. (4)For Mr. Civils, amounts are as of July 1, 2013. 24(5)As reported on a Schedule 13D/A dated May 31, 2011. MAK Capital One LLC has shared voting and dispositive power with respect to all of the shares. MAK Capital One LLC serves as the investment manager of MAK Capital Fund LP (“MAK Fund”). MAK GP LLC is the general partner of MAK Fund. Michael A. Kaufman, managing member and controlling person of MAK GP LLC and MAK Capital One LLC, has shared voting and dispositive power with respect to all of the shares. MAK Fund and R. Andrew Cueva have shared voting and dispositive power with respect to 5,284,648 shares. Paloma International L.P. (“Paloma”), through its subsidiary Sunrise Partners Limited Partnership, and S. Donald Sussman, controlling person of Paloma, have shared voting and dispositive power with respect to 1,772,286 shares. The principal business address of MAK Capital One LLC, MAK GP LLC and Messrs. Kaufman and Cueva is 590 Madison Avenue, 9th Floor, New York, New York 10022. The principal address of MAK Fund is c/o Dundee Leeds Management Services Ltd., 129 Front Street, Hamilton, HM 12, Bermuda. The principal address of Paloma and Sunrise Partners Limited Partnership is Two America Lane, Greenwich, Connecticut 06836-2571. The principal business address for Mr. Sussman is 6100 Red Hook Quarters, Suites C1-C6, St. Thomas, US Virgin Islands 00802-1348.On May 31, 2011, MAK Fund, Paloma and Computershare Trust Company, N.A. (the “Trustee”) entered into an Amended and Restated Voting Trust Agreement (the “Revised Voting Trust Agreement”) to clarify the Securities and Exchange Commission (SEC). The information posted on our website is not incorporated into this Annual Report on Form 10-K (Annual Report). Reports, proxy and information statements, and other information regarding issuers that file electronically, are maintainedeffect on the SEC website,http://www.sec.gov.Item 1A. RiskFactors.Risks Relating to Our BusinessContinuing challenging global economic conditions could adversely affect our business and financial results.The continued global economic downturn has significantly adversely affected global economic conditions. Our revenue and profitability depend significantly on general economic conditions and the level of capital available to our customers. Our business trends and revenue growth continue to be affectedvoting trust created by the challenging economic climate. These difficult economic conditions andVoting Trust Agreement dated as of December 31, 2009, were the uncertainty about future economic conditions may adversely affect our customers’ level of spending, abilityreporting persons (named above) to obtain financing for purchases, ability to make timely payments to us and adoption of new technologies, which could require us to increase our allowance for doubtful accounts, negatively impact our days sales outstanding, lead to increased price competition and adversely affect our results of operations.Our future success will depend on our ability to develop new products, product upgrades and services that achieve market acceptance.Our business is characterized by rapid and continual changes in technology and evolving industry standards. We believe that in order to remain competitive in the future we will need to continue to develop new products, product upgrades and services, requiring the investment of significant financial resources. If we fail to accurately anticipate our customer’s needs and technological trends,beneficially own one-third or are otherwise unable to complete the development of a product or product upgrade on a timely basis, we will be unable to introduce new products or product upgrades into the market on a timely basis, if at all, and our business and operating results would be materially and adversely affected.The development process for most new products and product upgrades is complicated, involves a significant commitment of time and resources and is subject to a number of risks and challenges including:Managing the lengthmore of the development cycle for new products and product enhancements, which has frequently been longer than we originally expected;Adapting to emerging and evolving industry standards and to technological developments by our competitors and customers; andExtending the operation of our products and services to new and evolving platforms, operating systems and hardware products, such as mobile devices.If we are not successful in managing these risks and challenges, or if our new products, product upgrades, and services are not technologically competitive or do not achieve market acceptance, our business and operating results could be adversely affected.We face extensive competition in the markets in which we operate, and our failure to compete effectively could result in price reductions and/or decreased demand for our products and services.Several companies offer products and services similar to ours. The rapid rate of technological change in the hospitality market makes it likely we will face competition from new products designed by companies not currently competing with us. We believe our competitive ability depends on our product offerings, our experience in the hospitality industry, our product development and systems integration capability, and our customer service organization. There is no assurance, however, we will be able to compete effectively in the hospitality technology market in the future.If we fail to meet our customers’ performance expectations, our reputation may be harmed, causing us to lose customers or exposing us to legal liability.Our ability to attract and retain customers depends to a large extent on our relationships with our customers and our reputation for high quality professional services and integrity. As a result, if a customer is not satisfied with our services or solutions, our reputation may be damaged. Moreover, if we fail to meet our clients’ performance expectations, we may lose clients and be subject to legal liability, particularly if such failure adversely impacts our clients’ businesses.9In addition, many of our projects are critical to the operations of our customers’ businesses. While our contracts typically include provisions designed to limit our exposure to legal claims relating to our products and services, these provisions may not adequately protect us or may not be enforceable in all cases. The general liability insurance coverage that we maintain, including coverage for errors and omissions, is subject to important exclusions and limitations. We cannot be certain that this coverage will continue to be available on reasonable terms or will be available in sufficient amounts to cover one or more large claims, or that the insurer will not disclaim coverage as to any future claim. A successful assertion of one or more large claims against us that exceeds our available insurance coverage or changes in our insurance policies, including premium increases or the imposition of large deductible or co-insurance requirements, could adversely affect our profitability.We are subject to pricing pressures for our products and services which could cause us to lose market share and decrease revenue and profitability.We compete for customers based on several factors, including price. In some cases, we may have to reduce our pricing to obtain business. If we are not able to maintain favorable pricing for our products and services, our gross profit and our profitability could suffer.Our cloud-based solutions present execution and competitive risks.Our solutions offered in the cloud accessible via the web without hardware installation or software downloads present new and difficult technology challenges. These offerings depend on integration of third-party hardware, software and cloud hosting vendors working together with our products. As a result, we may be subject to claims if customers experience service disruptions, breaches or other quality issues related to our cloud-based solutions.Actual or perceived security vulnerabilities in our software products may result in reduced sales or liabilities.Our software may be used in connection with processing sensitive data (e.g., credit card numbers), and is sometimes used to store such data. It may be possible for the data to be compromised if our customer does not maintain appropriate security procedures. In those instances, the customer may attempt to seek damages from us. While we believe that all of our current software complies with applicable industry security requirements and that we take appropriate security measures to reduce the possibility of breach through our support and other systems, we cannot assure that our customers’ systems will not be breached, or that all unauthorized access can be prevented. If a customer, or other person, seeks redress from usCompany’s outstanding voting securities as a result of a security breach, our business could be adversely affected.Hosting of software applications presents increased security risks.As we expand our software hosting capabilities and offer more of our software applications to our customers on a hosted basis, our responsibility for data and system security with respect to data held in our hosting centers increases significantly. While we believe that our current software applications comply with applicable laws and industry security requirements, and while we believe that we use appropriate security measures to reduce the possibility of unauthorized access or misuse of datadecrease in the hosting center, we cannot provide absolute assurance that our hosted systemstotal number of voting securities outstanding. In such event, regardless of the reporting persons’ economic interest in the Company, its voting power will not be breached,effectively limited to no more than 23% or that all unauthorized access can be prevented. If27% of the voting securities in the event of a security breach were to occur,shareholder vote on (i) a customer, regulatory agency,merger, consolidation, conversion, sale or disposition of stock or assets or other person could seek redress from us,business combination which could adversely affect our business.Additionally, as we expand our software hosting capabilities and offer morerequires approval of our software applications to our customers ontwo-thirds of the Company’s voting power (a “Strategic Transaction”) or (ii) a hosted basis, our potential liability increases significantly. Specifically, an outage in our data centers can affect numerous customers. While we believe that our data centers have been designed and engineered to reducetransaction other than a Strategic Transaction which requires approval of two-thirds of the likelihood of outages, we cannot provide assurance that our hosted systems will not suffer from unanticipated outagesCompany’s voting power (an “Other Transaction”), respectively. In connection with a Strategic Transaction or deficient performance. If an unanticipated outage were to occur, a customer could suffer economic damages and seek redress from us, which could adversely affect our business.We may not be able to enforce or protect our intellectual property rights.We rely on a combination of copyright, patent, trademark and trade secret laws and restrictions on disclosure to protect our intellectual property rights. We cannot be certain thatOther Transaction, the steps we have taken will prevent unauthorized use of our technology. Any failure to protect our intellectual property rightsreporting persons would diminish or eliminate the competitive advantages that we derive from our proprietary technology.10We may be subject to claims of infringement of third-party intellectual property rights.While we do not believe that our products and services infringe any patents or other intellectual property rights, from time to time, we receive claims that we have infringed the intellectual property rights of others. Any such claim, with or without merit, could result in costly litigation and distract management from day-to-day operations. If we are found liable, we could be obligated to pay significant damages or enter into license agreements.We are subject to litigation, which may be costly.As a company that does business with many customers, employees and suppliers, we are subject to litigation. The results of such litigation are difficult to predict, and we may incur significant legal expenses if any such claim were filed. While we generally take steps to reduce the likelihood that disputes will result in litigation, litigation is very commonplace and could have an adverse effect on our business.If we acquire new businesses, we may not be able to successfully integrate them or attain the anticipated benefits.As part of our operating history and growth strategy, we have acquired other businesses. In the future, we may continue to seek acquisitions. We can provide no assurance that we will be able to identify and acquire targeted businesses or obtain financing for such acquisitions on satisfactory terms. The process of integrating acquired businesses into our operations may result in unforeseen difficulties and may requirepossess the total voting power only over a disproportionate amount of resources and management attention. If integration of our acquired businesses is not successful, we may not realize the potential benefits of an acquisition or suffer other adverse effects.Our dependence on certain strategic partners makes us vulnerable to the extent we rely on them.We rely on a concentrated number of vendors forvoting securities that would equal the majority of our hardware and for certain software and related services needs. We do not have long term agreements with many of these vendors. If we can no longer obtain these hardware, software or services needs from our major suppliers duetotal voting power it would possess were it to mergers, acquisitions or consolidation within the marketplace, material changes in their partner programs, their refusal to continue to supply to us on reasonable terms or at all, and we cannot find suitable replacement suppliers, it may have a material adverse impact on our future operating results and gross margins.If we fail to retain key employees, our business may be harmed.Our success depends on the skill, experience and dedication of our employees. If we are unable to retain and attract sufficiently experienced and capable personnel, especially in product development, sales and management, our business and financial results may suffer. For example, if we are unable to retain and attract a sufficient number of skilled technical personnel, our ability to develop high quality products and provide high quality customer service may be impaired. Experienced and capable personnel in the technology industry remain in high demand, and there is continual competition for their talents. When talented employees leave, we may have difficulty replacing them, and our business may suffer. There can be no assurance that we will be able to successfully retain and attract the personnel that we need.Our profitability is partly dependent upon restructuring and executing planned cost savings.To allow us to operate more efficiently and control costs, we have incurred restructuring charges related to the consolidation and streamlining of various functions of our workforce. As part of our restructuring efforts, we incurred severance costs, lease termination costs and exit costs. We may not realize the expected benefits of these initiatives and may incur additional restructuring costs in the future. In addition, we could experience delays, business disruptions, unanticipated employee turnover and increased litigation-related costs in connection with our restructuring efforts. The complex nature of these restructuring initiatives could cause difficulties or delays in the implementation of any such initiative or the impacthold only one-third of the restructuring initiatives may not be immediately apparent. There can be no assurance that our estimates of the savings achievable by these initiatives will be realized, which could have an adverse impact on our financial condition or results of operations.If we fail to maintain an effective system of internal controls, we may not be able to detect fraud, which could have a material adverse effect on our business.While we believe our internal control over financial reporting is effective, a controls system cannot provide absolute assurance that the objectives of the controls system are met, and no evaluation of controls can provide absolute assurance that control issues and instances of fraud, if any, within our company have been detected.11We have encountered risks associated with maintaining large cash balances.While we have attempted to invest our cash balances in investments generally considered to be relatively safe, we nevertheless confront credit and liquidity risks. Bank failures could result in reduced liquidity or the actual loss of money held in deposit accounts in excess of federally insured amounts, if any.We may incur additional goodwill and intangible asset impairment charges that adversely affect our operating results.We review our goodwill and other intangible asset balances for impairment on at least an annual basis. During the fourth quarter of fiscal 2012, we concluded that certain software developed technology within HSG was no longer available for sale. As a result we recorded an impairment charge of $9.7 million, which impacted HSG’s operations. In fiscal 2011, we recognized non-cash impairment charges for goodwill and intangible assets totaling $1.0 million. Our future operating results and the market price of our common stock could be materially adversely affected if we are required to further write down the carrying value of goodwill and/or other intangible assets associated with any of our reporting units in the future.We may have exposure to greater than anticipated tax liabilities.Some of our products and services may be subject to sales taxes in states where we have not collected and remitted such taxes from our customers. We have reserves for certain state sales tax contingencies based on the likelihood of obligation. These contingencies are included in “Accrued liabilities” in our Consolidated Balance Sheets. We believe we have appropriately accrued for these contingencies. In the event that actual results differ from these reserves, we may need to make adjustments, which could materially impact our financial condition and results of operations.Risks Relating to the Industries We ServeOur business depends to a significant degree on the hospitality and retail industries, and a weakening could adversely affect our business and results of operations.Because our customer base is concentrated in the hospitality and retail industries, our business is largely dependent on the health of those industries. Our sales are dependent in large part on the health of the hospitality and retail industries, which in turn is dependent on the domestic and international economy. Instabilities or downturns in the hospitality and retail industries could disproportionately impact our revenue, as clients may exit the industry or delay, cancel or reduce planned expenditures for our products. A general downturn in the hospitality and retail industries could disproportionately impact our revenue, as clients may exit the industry or delay, cancel or reduce planned expenditures for our products.Higher oil and gas prices worldwide could have a material adverse impact on the hospitality industry, and indirectly, on our business.Material increases in oil and gas prices tend to reduce discretionary spending by consumers, such as on travel and dining, as well as on retail spending generally. Reductions in discretionary spending by consumers adversely affect our customers and, indirectly, our business. Moreover, increases in oil and gas prices also directly adversely affect our customer base in other ways. For example, oil and gas price increases can result in higher ingredient and food costs for our restaurant customers.Consolidation in the industries that we serve could adversely affect our business.Customers that we serve may seek to achieve economies of scale and other synergies by combining with or acquiring other companies. Many of the industries that we serve have experienced recent consolidations, including the hotel, casino, quick serve restaurant and grocery industries. Although recent consolidations in these industries have not materially adversely affected our business, there is no assurance that future consolidation will not have such affect. For example, if one of our current customers merges or consolidates with a company that relies on another provider’s products or services, it could decide to reduce or cease its purchases of products or services from us, which could have an adverse effect our business.Risks Relating to Our StockOur stock has been volatile and we expect that it will continue to be volatile.Our stock price has been volatile, and we expect it will continue to be volatile. For example, during the year ended March 31, 2012, the trading price of our common stock ranged from a high of $10.00 to a low of $4.43.voting securities. The volatility of our stock price may be due12to factors other than those specific to our business, such as economic news or other events generally affecting the trading markets. Additionally, our ownership base has been and may continue to be concentrated in a few shareholders, which could increase the volatility of our common share price over time.Our largest shareholder, MAK Capital, currently holds approximately 31% of our common shares, which could impact corporate policy and strategy, and MAK Capital’s interests may differ from those of other shareholders.Pursuant to the approval by shareholders of a control share acquisition proposal, MAK Capital holds approximately 31% of our outstanding common shares. As a significant shareholder whose responses could potentially affect the interests of Agilysys and the other shareholders, our Board may consider MAK Capital’s potential response to a particular decision of the Board in considering the range of possible corporate policies and strategies in the future, potentially influencing corporate policy and strategic planning.MAK entered into aRevised Voting Trust Agreement with Computershare,will become effective if and when the number of shares owned by the reporting persons equals or exceeds one-third of the voting securities then outstanding as trustee, whicha result of a decrease in the total number of voting securities outstanding. Until such time, the Voting Trust Agreement will remain in full force and effect.The Voting Trust Agreement provides that, for both strategic and other transactions requiring at least two-thirds of the voting power to approve, the trusteeTrustee will vote shares as follows: (i) for a certain percentageStrategic Transaction, vote shares that exceed 20% of MAK Capital’sthe outstanding shares in favor of, against, or abstaining from voting in the same proportion as all other shares voted by shareholders (including MAK Capital’sreporting persons’ shares that do not beingexceed the 20% threshold); and (ii) for Other Transactions, vote shares that exceed 25% of the outstanding shares in favor of, against, or abstaining from voting in the same proportion as all other shares voted by shareholders (including reporting persons’ shares that do not exceed the trustee)25% threshold). If theThe Voting Trust Agreement as amended, that MAK entered into with Computershare wereterminates (i) if the vote necessary to terminate for any reason, MAK Capital would have a level of control that would highly influence the approval or disapprovalapprove all forms of transactions requiring under Ohio lawis lowered to the approvalaffirmative vote of two-thirdsholders of the outstanding common shares, such as a business combination, or majority share acquisition involving the issuance of common shares entitling the holdersthem to exercise one-sixth or moreat least a majority of the voting power of Agilysys, each of which requires approval by two-thirds ofon the outstanding common shares. MAK Capital might also be able to initiate or substantially assist any such transaction. Even with the limitations on MAK Capital’s voting power imposed by the Voting Trust Agreement, as amended, it would be more difficult for the other shareholdersproposal to approve such a transactiontransactions (from two-thirds); (ii) if MAK Capital opposed it,Fund and MAK Capital’s interests may differ from thosePaloma are no longer members of other shareholders.Item 1B. UnresolvedStaff Comments.None.Item 2. Properties.Agilysys’ corporate services are located in Alpharetta, Georgia where we lease approximately 23,000 square feet of office space. In addition, we lease approximately 27,000 square feet of office space in Las Vegas, Nevada and 77,500 square feet of warehouse and office space in Taylors, South Carolina. Our major leases contain renewal options for periods of up to 10 years. We believe that our current facilities and office space are sufficient to meet our needs and do not anticipate any difficulty securing additional space as needed.Item 3. LegalProceedings.We are involved in legal actions that arise in the ordinary course of business. It is the opinion of management that the resolution of any current pending litigation will not have a material adverse effect on our financial position or results of operations.On April 6, 2012, Ameranth, Inc. filed a complaint against us for patent infringement in the United States District Court for the Southern District of California. The complaint alleges, among other things, that point-of-sale and property management and other hospitality information technology products, software, components and/or systems sold by us infringe three patents owned by Ameranth purporting to cover generation and synchronization of menus, including restaurant menus, event tickets, and other products across fixed, wireless and/or internet platforms as well as synchronization of hospitality information and hospitality software applications across fixed, wireless and internet platforms. The complaint seeks monetary damages, injunctive relief, costs and attorneys fees. We dispute the allegations of wrongdoing and intend to vigorously defend ourselves in this matter.Item 4. MineSafety Disclosures.Not applicable.13Part IIItem 5.Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities.Our common shares, without par value, are traded on the NASDAQ Stock Market LLC under the symbol “AGYS”. The high and low sales prices for the common shares for each quarter during the past two fiscal years are presented in the table below.Fiscal 2012 High Low $ 9.60 $ 6.92 $ 9.00 $ 6.50 $ 10.00 $ 6.60 $ 8.62 $ 4.43 Fiscal 2011 High Low $ 6.50 $ 4.74 $ 7.45 $ 4.66 $ 8.31 $ 4.30 $ 12.50 $ 6.09 The closing price of the common shares on June 1, 2012, was $7.25 per share. There were 1,999 shareholders of record.We did not pay dividends in fiscal 2012 or fiscal 2011 and are unlikely to do so in the foreseeable future. The current policy of the Board of Directors is to retain any available earnings for use in the operations of our business.Repurchase of Common SharesThe following table sets forth repurchases during the fourth quarter of fiscal 2012: Total Number

of Shares

Purchased (1) Average

Price Paid

Per Share Total Number of

Shares Purchased

as Part of Publicly

Announced Plans (2) Maximum Number of

Shares That May Yet

Be Purchased Under

the Plans 112,957 $ 8.07 112,957 16,087 16,087 $ 8.31 16,087 — 5,924 $ 8.99 — — 134,968 $ 8.14 — — (1)The total number of shares includes shares purchased under our share repurchase plan described below and shares surrendered by employees to Agilysys to satisfy tax withholding obligations in connection with the vesting of restricted stock total 5,924 shares in March 2012, which do not count against shares authorized under the share repurchase plan.(2)In August 2011, we announced that our Board of Directors provided authorization to repurchase up to 1.6 million of our common shares. As of March 31, 2012, we had repurchased all our common shares under this plan. No repurchases of common shares were made by us or on our behalf during fiscal 2011.14Shareholder Return Performance PresentationThe following chart compares the value of $100 invested in our common shares, including reinvestment of dividends, with a similar investment in the Russell 2000 Index (the “Russell 2000”) and with the companies listed in the SIC Code 5045-Computer and Computer Peripheral Equipment and Software for the period March 31, 2007 through March 31, 2012. The stock price performance in this graph is not necessarily indicative of the future performance of our common shares.Comparison of 5 Year Cumulative Total Return

INDEXED RETURNS Fiscal Years Ended March 31, Company Name / Index Base Period 2007 2008 2009 2010 2011 2012 $ 100.00 $ 51.97 $ 19.68 $ 51.69 $ 26.57 $ 41.61 $ 100.00 $ 87.01 $ 54.38 $ 88.51 $ 111.34 $ 111.13 $ 100.00 $ 80.67 $ 60.08 $ 87.11 $ 107.02 $ 95.98 This performance graph shall not be deemed “filed”“group” for purposes of Section 1813(d) of the Securities Exchange Act, of 1934, as amended or incorporated by reference intothen the Voting Trust Agreement terminates with respect to any of our filings under the Securities Act of 1933, as amended,MAK Fund and Paloma that beneficially owns not more than 20% of the Exchange Act, except as shall be expressly set forth by specific reference in such filing.15