• | improve our penetration of our existing markets by efficiently deploying marketing expenditures to attract new paid memberships and by retaining our existing paid memberships in these markets; |

• | maintain high levels of member engagement and the quality and integrity of our members’ reviews of local service providers; |

• | increase the number and variety of local service providers reviewed by our members and convince highly-rated local service providers to advertise with us; |

maintain high levels of member engagement and the quality and integrity of our members’ reviews of local service providers;

• | retain service providers that currently advertise with us and convince them to increase their advertising spending with us; |

increase the number and variety of local service providers reviewed by our members and convince highly-rated local service providers to advertise with us;

• | continue to develop and diversify our product offerings for local service providers; |

retain service providers that currently advertise with us and convince them to increase their advertising spending with us;

• | recruit, integrate and retain skilled and experienced sales personnel who can demonstrate our value proposition to service providers; |

continue to develop and diversify our product offerings for local service providers;

• | provide our members and local service providers with superior user experiences; |

recruit, integrate and retain skilled and experienced sales personnel who can demonstrate our value proposition to service providers;

• | react to changes in technology and challenges from existing and new competitors; and |

provide our members and local service providers with superior user experiences;

• | increase awareness of our brand. |

react to changes in technology and challenges from existing and new competitors; and

increase awareness of our brand.

We cannot assure you that our paid membership base or our service provider participation will continue to grow or will not decline as a result of increased competition and the maturation of our business. If our growth rates were to decline significantly or become negative, it could adversely affect our financial condition and results of operations. You should not rely on our historical rate of revenue growth as an indication of our future performance.

The Company’s inability to implement its strategic plan and growth initiatives may have an adverse impact on future results.

The Company’s ability to succeed in its strategic plan and growth initiatives could require significant capital investment and management attention, which may result in the diversion of these resources from the core business and other business issues and opportunities. Additionally, any new initiative is subject to certain risks, including customer acceptance, competition, product differentiation, challenges to economies of scale in merchandise sourcing and the ability to attract and retain qualified management and other personnel. There can be no assurance that the Company will be able to develop and successfully implement its strategic plan and growth initiatives to a point where they will become profitable or generate positive cash flow. If the Company cannot successfully execute its strategic plan and growth initiatives, the Company’s financial condition and results of operations may be adversely impacted.

Our future growth depends in part on our ability to effectively develop and sell additional products, services and features.

We invest in the development of new products, services and features with the expectation that we will be able to effectively offer them to consumers and local service providers. For example, we have introduced two e-commerce offerings, Angie’s List Big Deal and Storefront, which give our members the option to receive email alerts or search through service provider offerings on our website for deals. We plan to continue to develop additional advertising products for qualified local service providers. In addition, we may acquire vertical offerings that address additional “high cost of failure” segments of the market for local services.

Our future growth depends in part on our ability to sell these products and services, as well as additional features and enhancements to our existing offerings. As our new offerings evolve, we have adapted our sales and marketing strategies for them, and changes in these strategies may delay or prevent growth in these parts of our business. For example, we continue to refine our service provider eligibility criteria, pricing and our vendor credit and customer refund policies for our e-commerce offerings, which may cause our revenue from these offerings to fluctuate from period to period in the future. Further, many of our current and potential service provider advertisers have modest advertising budgets. Accordingly, we cannot assure you that the successful introduction of new products or services will not adversely affect sales of our current products and services or that those service providers that currently advertise with us will increase their aggregate spending as a result of the introduction of new products and services. If our efforts to effectively develop and sell additional products, services and features are not successful, our business may suffer.

12

We invest in features, functionality and customer support designed to drive traffic and increase engagement with members and service providers; however, these investments may not lead to increased revenue.

Our future growth and profitability will depend in large part on the effectiveness and efficiency of our efforts to convert consumers and local service providers who visit Angie’s List into paid memberships and participating service providers, respectively. We have made and will continue to make substantial investments in features and functionality for our website that are designed to drive online traffic and user engagement and in customer support for local service providers who do not advertise with us. These activities do not directly generate revenue, and we cannot assure you that we will reap any rewards from these investments. If the expenses that we incur in connection with these activities do not result in sufficient growth in paid members and participating service providers to offset their cost, our business, financial condition and results of operations will be adversely affected.

Our operating results may fluctuate, which makes our results difficult to predict and could cause our results to fall short of expectations.

Our revenue and operating results vary significantly from quarter to quarter and year to year because of a variety of factors, many of which are outside our control. As a result, comparing our operating results on a period to period basis may not be meaningful. In addition to other risk factors discussed in this “Risk Factors” section, factors that may contribute to the variability of our quarterly and annual results include:

our ability to retain our current paid memberships and build our paid membership base;

• | our ability to retain our current paid memberships and build our paid membership base; |

our ability to retain our service providers that currently advertise with us, and convince them to increase their advertising spending with us;

• | our ability to retain our service providers that currently advertise with us and convince them to increase their advertising spending with us; |

our revenue mix and any changes we make to our membership fees or other sources of revenue;

• | our revenue mix and any changes we make to our membership fees or other sources of revenue; |

our marketing costs or selling expenses;

• | our marketing costs or selling expenses; |

our ability to effectively manage our growth;

• | our ability to effectively manage our growth; |

the effects of increased competition in our business;

• | the effects of increased competition in our business; |

our ability to keep pace with changes in technology and our competitors;

• | our ability to keep pace with changes in technology and our competitors; |

• | costs associated with defending any litigation or enforcing our intellectual property rights; |

• | the impact of economic conditions in the United States on our revenue and expenses; and |

• | changes in government regulation affecting our business. |

From time to time we change the compensation plans for our intellectual property rights;

the impact of economic conditionssales personnel. For example, in the United States on our revenue and expenses; and

changes in government regulation affecting our business.

In the fourth quarter of 2012, we commenced the transitiontransitioned to a new compensation plan for our sales forcepersonnel responsible for new advertising originations whereby we have begunoriginations. Any future changes to pay commissions as cash is collected from our service providers rather than upfront at booking, as we have done historically. During this transition period, we expect to see higher selling expense as a percent of revenue in the near-term. In addition, the transitionsuch compensation plans could disrupt our sales forcepersonnel, adversely affecting sales and adversely affect new advertising sales, reducing our revenue. We cannot guarantee that we will accurately forecast the impact of the transitionfuture changes to such compensation plans on our operating results.

Seasonal variations in the behavior of our members and service providers also may cause fluctuations in our financial results. For example, we expect to experience some effects of seasonal trends in member and service provider behavior due to decreased demand for home improvement services in winter months. In addition, advertising expenditures by local service providers tend to be discretionary in nature and may be sporadic, reflecting overall economic conditions, the economic prospects of specific local service providers or industries, budgeting constraints and buying patterns and a variety of other factors, many of which are outside our control. We also expect revenue contributions from our e-commerce offerings to fluctuate from period to period as the offerings evolve and due to seasonality. While we believe seasonal trends have affected and will continue to affect our quarterly results, our trajectory of rapid growth may have overshadowed these effects to date. We believe that our business will be subject to seasonality in the future, which may result in fluctuations in our financial results.

13

Our revenue may be negatively affected if we are required to pay sales tax or other transaction taxes on all or a portion of our past and future sales in jurisdictions where we are currently not collecting and reporting tax.

We currently only pay sales or other transaction taxes in certain jurisdictions in which we do business. We do not separately collect sales or other transaction taxes. A successful assertion by any state, local jurisdiction or country in which we do not pay such taxes that we should be paying sales or other transaction taxes on the sale of our products or services, or the imposition of new laws requiring the payment of sales or other transaction taxes on the sale of our products or services, could result in substantial tax liabilities related to past sales, create increased administrative burdens or costs, discourage consumers and service providers from purchasing products or services from us, decrease our ability to compete or otherwise substantially harm our business and results of operations.

We depend on key personnel to operate our business, and if we are unable to retain, attract and integrate qualified personnel, our ability to develop and successfully grow our business could be harmed.

We believe that our future success depends in part upon the continued service of key members of our management team as well as our ability to attract and retain highly skilled and experienced sales, technical and other personnel. Our co-founders, William S. Oesterle and Angie Hicks, are critical to our overall management as well as the development of our culture and strategic direction. In particular, the reputation, popularity and talent of Ms. Hicks is an important factor in public perceptions of Angie’s List, and the loss of her services or any repeated or sustained shifts in public perceptions of her could adversely affect our business.

In addition, qualified individuals are in high demand in the Internet sector, and we may incur significant costs to attract them. Competition for these personnel is intense, and we may not be successful in attracting and retaining qualified personnel. Many of the companies with which we compete for experienced personnel have greater resources than us. In addition, in making employment decisions, particularly in the technology sector, job candidates often consider the value of the stock options they are to receive in connection with their employment.If we are unable to attract and retain our executive officers and key employees, we may not be able to achieve our strategic objectives, and our business could be harmed.

We have historically relied primarily on cash, rather than equity, compensation for the majority of our workforce. As such, we may have difficulty competing on a national scale for candidates focused on equity incentives. If we are unable to attract and retain executive officers and key personnel to our headquarters in Indianapolis, Indiana or integrate recently hired executive officers and key personnel, our business, operating results and financial condition could be harmed.

If we cannot maintain our corporate culture as we grow, we could lose the innovation, teamwork and focus that contribute crucially to our business.

We believe that a critical component of our success has been our corporate culture, which we believe fosters innovation, encourages teamwork, cultivates creativity and promotes focus on execution. We have invested substantial time, energy and resources in building a highly collaborative team that works together effectively in an environment designed to promote openness, honesty, mutual respect and the pursuit of common goals. As we continue to develop the infrastructure of a public company and continue to grow, we may find it difficult to maintain these valuable aspects of our corporate culture. Any failure to preserve our culture could negatively impact our future success, including our ability to attract and retain personnel, encourage innovation and teamwork and effectively focus on and pursue our corporate objectives.

We may require additional capital to pursue our business objectives and respond to business opportunities, challenges or unforeseen circumstances. If capital is not available to us, our business, operating results and financial condition may be harmed.

We may require additional capital to operate or expand our business. In addition, some of the strategic initiatives we have in early stages of development may require substantial additional capital resources before they begin to generate revenue. Additional funds may not be available when we need them, on terms that are

14

acceptable to us, or at all. For example, the loan and security agreement governing our term loan and revolving credit facility contains various restrictive covenants, including restrictions on our ability to dispose of assets, make acquisitions or investments, incur debt or liens, make distributions to our stockholders or enter into certain types of related party transactions, and any debt financing secured by us in the future could involve further restrictive covenants, which may make it more difficult for us to obtain additional capital and pursue business opportunities. If we raise additional funds through the issuance of equity or convertible securities, the percentage ownership of holders of our common stock could be significantly diluted,and these newly issued securities may have rights, preferences or privileges senior to those of holders of our common stock. Furthermore, volatility in the credit or equity markets may have an adverse effect on our ability to obtain debt or equity financing or the cost of such financing. If we do not have funds available to enhance our solutions, maintain the competitiveness of our technology and pursue business opportunities, we may not be able to service our existing members, acquire new members or attract or retain participating service providers, which could have an adverse effect on our business, operating results and financial condition.

If we fail to maintain proper and effective internal controls, our ability to produce accurate financial statements on a timely basis could be impaired, which would adversely affect our business and our stock price.

Ensuring that we have adequate internal financial and accounting controls and procedures in place to produce accurate financial statements on a timely basis is a costly and time-consuming effort that needs to be reevaluated frequently. We have in the past discovered, and may in the future discover, areas of our internal financial and accounting controls and procedures that need improvement.

Our management is responsible for establishing and maintaining adequate internal control over financial reporting to provide reasonable assurance regarding the reliability of our financial reporting and the preparation of financial statements for external purposes in accordance with U.S. general acceptedgenerallyaccepted accounting principles. Our management does not expect that our internal control over financial reporting will prevent or detect all errors and all fraud. A control system, no matter how well designed and operated, can provide only reasonable, not absolute, assurance that the control system’s objectives will be met. Because ofDue to the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that misstatements due to error or fraud will not occur or that all control issues and instances of fraud, if any, within our company will have beenbe detected.

Because we recognize membership revenue over the term of the membership and recognize service provider revenue ratably over the relevant contract period, downturns or upturns in membership or in service provider advertising may not be immediately reflected in our operating results.

We recognize membership revenue ratably over the term of a paid subscription and recognize service provider revenue ratably over the time period during which the advertisements are run. Because approximately 91%94% of our members subscribed on an annual or multi-year basis as of December 31, 2012,2013, a large portion of our membership revenue for each quarter reflects deferred revenue from memberships purchased in previous quarters. Similarly, because our service provider contracts run for an average term of more than one year, a large portion of our service provider revenue each quarter reflects purchasing decisions made in prior periods. Therefore, an increase or decrease in new or renewed memberships or new or renewed service provider contracts in any one quarter will not necessarily be fully reflected in our revenue for that quarter but will affect our revenue in future quarters. Accordingly, the effect of significant downturns or upturns in membership or advertising sales may not fully impact our results of operations until future periods.

We may suffer liability as a result of the ratings or reviews posted on our website.

Our terms of use specifically require members and non-members submitting reviews to represent that their ratings and reviews are based on their actual first-hand experiences and are accurate, truthful and complete in all respects and that they have the right and authority to grant us a license to publish their reviews. However, we do not have the ability to verify the accuracy of these representations on a case-by-case basis. There is a risk that a

15

review may be considered defamatory or otherwise offensive, objectionable or illegal under applicable law. Therefore, there is a risk that publication on our website of our ratings and reviews may give rise to a suit against us for defamation, civil rights infringement, negligence, copyright or trademark infringement, invasion of privacy, personal injury, product liability, breach of contract, unfair competition, discrimination, antitrust or other legal claims. From time to time, we are involved in claims and lawsuits based on the contents of the ratings and reviews posted on our website, including claims of defamation. To date, we have not suffered a material loss due to a claim of defamation. We expect that we will be subject to similar claims in the future, which may result in costly and time-consuming litigation, liability for money damages andor injury to our reputation.

If we fail to generate or maintain expected high quality reviews and reports from our members, we will be unable to provide members with the information they seek, which could negatively impact our membership retention and growth.

Our business depends on our ability to provide our members with the information they seek, which is directly dependent on the quality and quantity of the reviews and reports provided by our members. For example, we may be unable to offer our members adequate information on local service providers if our members do not contribute content that is helpful or relevant to the service category in a particular market. We may be unable to provide members with the information they seek if our members are unwilling to contribute reviews and reports because of concerns they will be sued or harassed by service providers they review, instances of which have occurred in the past and may occur again in the future. In addition, we may not be able to provide members with the information they seek if the information on our site is not updated. We do not remove older reviews, and members may view these reviews as less relevant, helpful or reliable. If our site does not provide current information about local service providers or members perceive reviews on our site as less relevant, our brand and business could suffer.

Membership growth is impacted by traffic to our website from search engines like such asGoogle, Bing and Yahoo!, some of which offer products and services that compete directly with our services. If our website fails to rank prominently in unpaid search results, traffic to our site could decline,and our business would be adversely impacted.

A portion of our website traffic comes from non-paid search results that appear on search engines such as Google and bing.Bing. For example, in fourth quarter of 2012, 2013,member sales from search engine optimization (“SEO”) efforts grew 185% year-over-year in the fourth quarter.57% as compared to 2012. While SEO has a much lower cost per acquisition compared to outbound channels like advertisingsuch asadvertising and has helped reduce our overall cost per member acquisition, our ability to maintain high organic search rankings is not within our control. As such, our competitors’ SEO efforts may result in their websites receiving a higher search result page ranking than ours. Separately, Internet search engines could revise their methodologies in a way that could adversely affect our search result rankings. For example, Google makes changes to its algorithm(s) every year, any one of which could potentially impact our rankings,which we are dependent upon to drive traffic and ultimately sales to our site. Our website has experienced fluctuations in search result rankings in the past, and we anticipate similar fluctuations in the future. Any reduction in the number of Internet users directed to our website through search engines could harm our business.

If local service providers rated on our website do not meet the expectations of our members, or engage in unethical or illegal conduct, we may suffer reputational harm, liability or adverse effects on our profitability and liquidity as a result.

Our business depends on our reputation for quality and integrity, which may be harmed by actions taken by local service providers that are outside our control. Because Given thatour members use our service to gather information about projects that carry a high risk of failure, and have the opportunity to purchase these services at a discounted rate through our Big Deal and Storefront offerings, if they are performed incompetently or if service providers fail to perform prepaid services, our reputation could be undermined. We cannot be certain that highly-rated local service providers will perform to the satisfaction of our members or that services purchased in advance through

16

our Big Deal or Storefront offerings will be performed to the satisfaction of our members or at all. In addition, unethical or illegal conduct by local service providers rated on our website could damage our reputation or expose us to liability arising from claims made by or on behalf of those harmed by such conduct.

We pay service providers in advance for all Big Deals and Storefront offerings purchased by members. Under this payment model, service providers are paid regardless of whether the Big Deal is redeemed or the Storefront services are performed. Subject to certain limitations, our members may request a refund from us on their e-commerce transactions. BecauseAs we do not have control over service providers and the quality of the services they deliver, we develop estimates for refund claims. Our actual level of refund claims could prove to be greater than the level of refund claims we estimate, particularly as our revenue from e-commerce offerings grows and we develop additional e-commerce products, services and features. Moreover, our members may make requests for refunds with respect to which we are unable to recover reimbursement from our service providers. An increase in our refund rates, or our inability to recover from our service providers, could adversely affect our profitability and liquidity.

Many people utilize smartphones and other mobile devices, as well as tablets, to access information about local service providers. If we are not successful in developing products through the use of these technologies,or our products are not widely adopted, our business could be adversely affected.

The number of people who seek information about local service providers through mobile devices, including smartphones and tablets, has increased significantly in the past few years. If our members are unable to access our ratings and reviews of service providers on their mobile devices, or if we otherwise fail to develop and maintain effective mobile advertising and e-commerce products and services or if our mobile products and services are not widely adopted by our members, our business may suffer. Additionally, as new mobile devices and platforms are released, it is difficult to forecast the problems that may arise, and we may need to devote significant resources to the development, support and maintenance of these products. Finally, if we experience problems with continued integration of our mobile application,applications, or mobile app,apps, into mobile devices, or weifwe have issues with providers of mobile operating systems or mobile application download stores, such as Apple, Inc. or Google, or if we facedface increased costs to distribute our mobile app,apps, our business could suffer.

Failure to comply with federal and state laws and regulations relating to privacy and security of personal information, including personal health information, could result in liability to us, damage our reputation and harm our business.

A variety of federal and state laws and regulations govern the collection, use, retention, sharing and security of personal information. We collect and utilize demographic and other information from and about our members as they interact with our service. We also may collect information from our members when they provide ratings and reviews of local service providers, participate in polls or contests or sign up to receive email newsletters. Further, we use tracking technologies, including “cookies,” to help us manage and track our members’ interactions with our service and deliver relevant advertising. Claims or allegations that we have violated laws and regulations related to privacy and data security could in the future result in negative publicity and a loss of confidence in us by our members and our participating service providers and may subject us to fines by credit card companies and the loss of our ability to accept credit and debit card payments. In addition, we have posted privacy policies and practices concerning the collection, use and disclosure of member data on our websites and mobile applications. Several Internet companies have incurred penalties for failing to abide by the representations made in their privacy policies and practices.

In rating and reviewing health care or wellness providers, our members may post personal health information about themselves or others, and the health care or wellness providers reviewed by members may submit responses that contain private or confidential health information about reviewing members or others. While we strive to comply with applicable privacy and security laws and regulations regarding personal health information, as well as our own posted privacy policies, any failure or perceived failure to comply may result in proceedings or actions against us by government entities or others or could cause us to lose members and participating service providers, which could adversely affect our business.

17

We have incurred, and will continue to incur, expenses to comply with privacy and security standards and protocols for personal information, including personal health information, imposed by law, regulation, self-regulatory bodies, industry standards and contractual obligations. However, such laws and regulations are evolving and subject to potentially differing interpretations, and federal and state legislative and regulatory bodies may expand current or enact new laws or regulations regarding privacy matters. We are unable to predict what additional legislation or regulation in the area of privacy of personal information could be enacted or its effect on our operations and business.

If our security measures are breached and unauthorized access is obtained to our members’ or service providers’data, our service may be perceived as not being secure,and members and service providers may curtail or terminate their use of our service.

In the ordinary course of business, we collect and store sensitive data, including intellectual property, our proprietary business information and that of our members and service providers and personally identifiable information of our members, service providers and employees in our data centers and networks. The secure processing, maintenance and transmission of this information is critical to our operations and business strategy. Our service involves the storage and transmission of our members’ and service providers’ proprietary information, such as credit card and bank account numbers, and security breaches could expose us to a risk of loss of this information, litigation and possible liability. Our payment services may be susceptible to credit card and other payment fraud schemes, including unauthorized use of credit cards, debit cards or bank account information, identity theft or merchant fraud.

If our security measures are breached as a result of third-party action, employee error, malfeasance or otherwise, and as a result, someone obtains unauthorized access to our members’ data, our reputation may be damaged, our business may suffer and we could incur significant liability. Because techniquesAstechniques used to obtain unauthorized access or to sabotage systems change frequently and generally are not recognized until launched against a target, we may be unable to anticipate these techniques or implement adequate preventative measures. If an actual or perceived breach of our security occurs, the public perception of the effectiveness of our security measures could be harmed,and we could lose members and service providers, which could adversely affect our business.

We are subject to a number of risks related to intentional business disruptions, cyber-attacks and piracy.

Despite a number of precautionary measures already in place and significant ongoing investments to protect against security risks, data protection breaches, cyber-attacks and other intentional disruptions of our products and offerings, we expect to be an ongoing target of attacks specifically designed to impede the performance of our products and offerings and harm our reputation as a company. Similarly, experienced third parties may attempt to penetrate our network security or the security of our website and misappropriate proprietary information or cause interruptions of our services. As the techniques used by such third parties to access or sabotage networks change frequently and may not be recognized until launched against a target, we may be unable to anticipate these techniques. The theft or unauthorized use or publication of our trade secrets and other confidential business information as a result of such an event could adversely affect our competitive position, reputation, brand and future sales of our products, and our customers may assert claims against us related to resulting losses of confidential or proprietary information. Our business could be subject to significant disruption, and we could suffer monetary and other losses and reputational harm, in the event of such incidents and claims.

We are subject to a number of risks related to accepting credit card and debit card payments.

We accept payments from our members primarily through credit and debit card transactions. For credit and debit card payments, we pay interchange and other fees, which may increase over time. An increase in those fees would require us to either increase the prices we charge for our service, which could cause us to lose members and membership revenue, or suffer an increase in our operating expenses, either of which could adversely affect our operating results.

If we or any of our processing vendors have problemsexperienceproblems with our billing software, or if the billing software malfunctions, it could have an adverse effect onadversely affect our member satisfaction and could cause one or more of the major credit card companies to disallow our continued use of their payment products. In addition, if our billing software fails to work properly and, as a result, we do not automatically charge our members’ credit cards on a timely basis or at all, we could lose membership revenue, which could harm our operating results.

We are also subject to payment card association operating rules, certification requirements and rules governing electronic funds transfers, including the Payment Card Industry Data Security Standard, or PCI DSS, a security standard with which companies that collect, store or transmit certain data regarding credit and debit cards, credit and debit card holders and credit and debit card transactions are required to comply. Our failure to comply fully with the PCI DSS may violate payment card association operating rules, federal and state laws and regulations and the terms of our contracts with payment processors and merchant banks. Such failure to comply fully also may subject us to fines, penalties, damages and civil liability and may result in the loss of our ability to accept credit and debit card payments. In addition, there is no guarantee that PCI DSS compliance will prevent illegal or improper use of our payment systems or the theft, loss or misuse of data pertaining to credit and debit cards, credit and debit card holders and credit and debit card transactions.

18

If we fail to adequately control fraudulent credit card transactions, we may face civil liability, diminished public perception of our security measures and significantly higher credit card-related costs, each of which could adversely affect our business, financial condition and results of operations.

If we are unable to maintain our chargeback rate at acceptable levels, our credit card fees for chargeback transactions or our fees for many or all categories of credit and debit card transactions, credit card companies and debit card issuers may increase our fees or terminate their relationship with us. Any increases in our credit card and debit card fees could adversely affect our results of operations, particularly if we elect not to raise our rates for our service to offset the increase. The termination of our ability to process payments on any major credit or debit card would significantly impair our ability to operate our business.

As we develop and sell new products, services and features, we may be subject to additional and unexpected regulations, which could increase our costs or otherwise harm our business.

As we develop and sell products and services that address new segments of the market for local services and expand our advertising services, we may become subject to additional laws and regulations, which could create unexpected liabilities for us, cause us to incur additional costs or restrict our operations. For example, our Angie’s List Health & Wellness offerings may become subject to complex federal and state health care laws and regulations, the application of which to specific products and services is unclear. Many existing health care laws and regulations, when enacted, did not anticipate the online health and wellness information and advertising products and services that we provide; nevertheless, they may be applied to our products and services.

We have e-commerce offerings, such as Angie’s List Big Deal and Storefront, which allow our members to purchase services or products from our service providers. Transactions between members and local service providers in connection with these offerings may be subject to regulation, in whole or in part, by federal, state and local authorities.

In addition, the application of certain laws and regulations to some of our promotions are uncertain. These include laws and regulations such as the Credit Card Accountability Responsibility and Disclosure Act of 2009, or the CARD Act, and unclaimed and abandoned property laws. If these promotions were subject to the CARD Act or any similar state or foreign law or regulation, we may be required to record liabilities with respect to unredeemed promotions,and we may be subject to additional fines and penalties.

From time to time, we may be notified of additional laws and regulations which governmental organizations or others may claim should be applicable to our business. Our failure to accurately anticipate the application of these laws and regulations, or other failure to comply, could create liability for us, result in adverse publicity or cause us to alter our business practices, which could cause our revenue to decrease, our costs to increase or our business otherwise to beotherwisebe harmed.

Our business depends on our ability to maintain and scale the network infrastructure necessary to operate our websites and applications.

Our members access reviews and other information through our websites and applications. Our reputation and ability to acquire, retain and serve our members and service providers are dependent upon the reliable performance of our websites and applications and the underlying network infrastructure. As our membership base and the amount of information shared on our websites and applications continue to grow, we will need an increasing amount of network capacity and computing power. We have made, and expect to continue to make, substantial investments in data centers, equipment and related network infrastructure to handle the traffic on our websites and the data submitted to us by our members. The operation of these systems is expensive and complex and could result in operational failures. In the event that our membership base or the amount of traffic on our websites and applications grows more quickly than anticipated, we may be required to incur significant additional costs. If we do not maintain or expand our network infrastructure successfully, or if we experience

19

operational failures, our reputation could be harmed,and we could lose current and potential members and participating service providers, which could harm our operating results and financial condition.

We may not be able to successfully prevent other companies, including copycat websites, from misappropriating our data in the future.

From time to time, third parties have attempted to misappropriate our member-generated ratings and reviews and other data regarding our service providers through website scraping, search robots or other means. We have deployed several technologies designed to detect and prevent such efforts. However, we may not be able to successfully detect and prevent all such efforts in a timely manner or assure that no misuse of our data occurs.

In addition, third parties operating “copycat” websites have attempted to misappropriate data from our network and to imitate our brand or the functionality of our website. When we have become aware of such efforts by other companies, we have employed technological or legal measures in an attempt to halt their operations. However, we may not be able to detect all such efforts in a timely manner, or at all, and even if we could, the technological and legal measures available to us may be insufficient to stop their operations. In some cases, particularly in the case of companies operating outside of the United States, our available remedies may not be adequate to protect us against the damage to our business caused by such websites. Regardless of whether we can successfully enforce our rights against the operation of these websites, any measures that we may take could require us to expend significant financial or other resources and have a significantly adverse effect on our brand.

Failure to adequately protect our intellectual property could substantially harm our business and operating results.

We rely on a combination of intellectual property rights, including trade secrets, copyrights and trademarks, as well as contractual restrictions, to safeguard our intellectual property. We do not have any patents or pending patent applications. Despite our efforts to protect our proprietary rights, unauthorized parties may attempt to copy our digital content, aspects of our solutions for members and service providers, our technology, software, branding and functionality, or obtain and use information that we consider proprietary. Moreover, policing our proprietary rights is difficult and may not always be effective. As we expand internationally, we may need to enforce our rights under the laws of countries that do not protect proprietary rights to as great an extent as do the laws of the United States.

Our digital content is not protected by any registered copyrights or other registered intellectual property. Rather, our digital content is protected by statutory and common law rights, user agreements that limit access to and use of our data and by technological measures. Compliance with use restrictions is difficult to monitor, and our proprietary rights in our digital content databases may be more difficult to enforce than other forms of intellectual property rights.

As of December 31, 2012,2013, we have registered 2324 trademarks in the United States, including “Angie’s List,” oneand two registered trademarks in Canada, as well as four pending trademark applicationapplications in the United States and one registered trademark and one pending trademark application in Canada.States. Some of our trade names may not be eligible to receive trademark protection. Trademark protection may also not be available, or sought by us, in every country in which our service may become available online. Competitors may adopt service names similar to ours or purchase our trademarks and confusingly similar terms as keywords in Internet search engine advertising programs, thereby impeding our ability to build brand identity and possibly confusing consumers and local service providers. Moreover, there could be potential trade name or trademark infringement claims brought by owners of other registered trademarks or trademarks that incorporate marks similar to our trademarks. In addition, in the past, some local service providers have used our trademarks inappropriately or without our permission, including our “Super Service Award,” which is available only to local service providers that have maintained superior service ratings. We have taken in the past and may in the future take action, including initiating litigation, to protect our intellectual property rights and the integrity of our brand, but these efforts may prove costly, ineffective or both.

20

We currently hold the “Angie’s List” Internet domain name and various other related domain names. Domain names generally are regulated by Internet regulatory bodies. If we lose the ability to use a domain name in the United States or any other country, we would be forced to incur significant additional expense to market our solutions, including the development of a new brand and the creation of new promotional materials, which could substantially harm our business and operating results. The regulation of domain names in the United States and in foreign countries is subject to change. Regulatory bodies could establish additional top-level domains, appoint additional domain name registrars or modify the requirements for holding domain names. As a result, we may not be able to acquire or maintain the domain names that utilize the “Angie’s List” name in all of the countries in which we currently intend to conduct business.

In order to protect our trade secrets and other confidential information, we rely in part on confidentiality agreements with our personnel, consultants and third parties with whom we have relationships. These agreements may not effectively prevent disclosure of trade secrets and other confidential information and may not provide an adequate remedy in the event of misappropriation of trade secrets or any unauthorized disclosure of trade secrets and other confidential information. In addition, others may independently discover trade secrets and confidential information, and in such cases, we could not assert any trade secret rights against such parties. Costly and time-consuming litigation could be necessary to enforce and determine the scope of our trade secret rights and related confidentiality and nondisclosure provisions, and failure to obtain or maintain trade secret protection, or our competitors being able to obtain our trade secrets or to independently develop technology similar to ours or competing technologies, could adversely affect our competitive business position.

Litigation or proceedings before the U.S. Patent and Trademark Office or other governmental authorities and administrative bodies in the United States and abroad may be necessary in the future to enforce our intellectual property rights, to protect our domain names and to determine the validity and scope of the proprietary rights of others. Our efforts to enforce or protect our proprietary rights may be ineffective, could result in substantial costs and diversion of resources and could substantially harm our operating results.

Assertions by third parties of infringement or other violation by us of their intellectual property rights could result in significant costs and substantially harm our business and operating results.

Internet, technology and media companies are frequently subject to litigation based on allegations of infringement, misappropriation or other violations of intellectual property rights. Some Internet, technology and media companies, including some of our competitors, own large numbers of patents, copyrights, trademarks and trade secrets, which they may use to assert claims against us. Third parties may in the future assert that we have infringed, misappropriated or otherwise violated their intellectual property rights, and as we face increasing competition, the possibility of intellectual property rights claims against us grows. We cannot assure you that we are not infringing or violating any third-party intellectual property rights.

We cannot predict whether assertions of third-party intellectual property rights or any infringement or misappropriation claims arising from such assertions will substantially harm our business and operating results. If we are forced to defend against any infringement or misappropriation claims, whether they are with or without merit, are settled out of court or are determined in our favor, we may be required to expend significant time and financial resources on the defense of such claims. Furthermore, an adverse outcome of a dispute may require us to pay damages, potentially including treble damages and attorneys’ fees, if we are found to have willfully infringed a party’s patent or copyright rights;rights, cease making, licensing or using solutions that are alleged to infringe or misappropriate the intellectual property of others;others, expend additional development resources to redesign our solutions;solutions, enter into potentially unfavorable royalty or license agreements in order to obtain the right to use necessary technologies, content or materials;materials and to indemnify our partners and other third parties. Royalty or licensing agreements, if required or desirable, may be unavailable on terms acceptable to us, or at all, and may require significant royalty payments and other expenditures. Any of these events could seriously harm our business, operating results and financial condition. In addition, any lawsuits regarding intellectual property rights, regardless of their success, could be expensive to resolve and would divert the time and attention of our management and technical personnel.

21

Some of our services and technologies may use “open source” software, which may restrict how we use or distribute our services or require that we release the source code of certain services subject to those licenses.

Some of our services and technologies may incorporate software licensed under so-called “open source” licenses, including, but not limited to, the GNU General Public License and the GNU Lesser General Public License. Such open source licenses typically require that source code subject to the license be made available to the public and that any modifications or derivative works to open source software continue to be licensed under open source licenses. These open source licenses typically mandate that proprietary software, when combined in specific ways with open source software, becomes subject to the open source license. If we combine our proprietary software with open source software, we could be required to release the source code of our proprietary software.

We take steps to ensure that our proprietary software is not combined with, nor incorporates, open source software in ways that would require our proprietary software to be subject to an open source license. However, few courts have interpreted open source licenses, and the manner in which these licenses may be interpreted and enforced is therefore subject to some uncertainty. Additionally, we rely on multiple software programmers to design our proprietary technologies, and although we take steps to prevent our programmers from including open source software in the technologies and software code that they design, write and modify, we do not exercise complete control over the development efforts of our programmers, and we cannot be certain that our programmers have not incorporated open source software into our proprietary products and technologies or that they will not do so in the future. In the event that portions of our proprietary technology are determined to be subject to an open source license, we could be required to publicly release the affected portions of our source code, re-engineer all or a portion of our technologies or otherwise be limited in the licensing of our technologies, each of which could reduce or eliminate the value of our services and technologies and materially and adversely affect our business, results of operations and prospects.

We rely on third parties to provide software and related services necessary for the operation of our business.

We incorporate and include third-party software into and with our product and service offerings and expect to continue to do so. The operation of our product and service offerings could be impaired if errors occur in the third-party software that we use. It may be more difficult for us to correct any defects in third-party software becauseas the development and maintenance of the software is not within our control. Accordingly, our business could be adversely affected in the event of any errors in this software. We cannot assure you that any third-party licensors will continue to make their software available to us on acceptable terms, or at all, or to invest the appropriate levels of resources in their software to maintain and enhance its capabilities or to remain in business. Any impairment in our relationships with these third-party licensors could have an adverse effect on our business, results of operations, cash flow and financial condition. These third-party in-licenses may expose us to increased risk, including risks associated with the assimilation of new technology sufficient to offset associated acquisition and maintenance costs. The inability to obtain any of these licenses could result in delays in development of solutions until equivalent technology can be identified and integrated. Any such delays in services could cause our business, operating results and financial condition to suffer.

We are involved in litigation matters that are expensive and time consuming, and, if resolved adversely, could harm our business, financial condition or results of operations.

We are involved in lawsuits, including a putative class action lawsuit brought by members and stockholder class action lawsuits, and we anticipate that we will continue to be a target for lawsuits in the future. Any negative outcome from such lawsuits could result in payment of substantial monetary damages or fines or undesirable changes to our products, services or business practices, and accordingly,our business, financial condition or results of operations could be materially and adversely affected. Although the results of such lawsuits and claims cannot be predicted with certainty, we currently believe that the final outcome of those matters that we currently face will not have a material adverse effect on our business, financial condition, results of operations or cash flows, except as otherwise recorded within the consolidated financial statements.However, there can be no assurance that a favorable final outcome will be obtained in all our cases, and regardless of the outcome, any lawsuit can have an adverse impact on us because of defense and settlement costs, diversion of management resources and other factors. Any lawsuit to which we are a party may result in an onerous or unfavorable judgment that may not be reversed upon appeal or in payments of substantial damages or fines, or we may decide to settle lawsuits on similarly unfavorable terms, which could adversely affect our business, financial conditions or results of operations.

Covenants in the loan and security agreement governing our term loan and revolving credit facility may restrict our operations, and if we do not effectively manage our business to comply with these covenants, our financial condition could be adversely affected.

The loan and security agreement governing our term loan and revolving credit facility contains various restrictive covenants, including restrictions on our ability to dispose of assets, make acquisitions or investments, incur debt or liens, make distributions to our stockholders or enter into certain types of related party transactions. We are also required to maintain certain financial covenants. Our ability to meet these restrictive covenants can be affected by events beyond our control, and we may be unable to do so. In addition, our failure to maintain effective internal controls to measure compliance with our financial covenants could affect our ability to take corrective actions on a timely basis and could result in our being in breach of these covenants. Our loan and

22

security agreement provides that our breach or failure to satisfy certain covenants constitutes an event of default. Upon the occurrence of an event of default, which includes a material adverse change, our lenders could elect to declare all amounts outstanding under one or more of our debt agreements to be immediately due and payable. If we are unable to repay those amounts, our financial condition could be adversely affected.

Because we generate substantially all of our revenue in the United States, a decline in aggregate demand for local services in the United States could cause our revenue to decline.

Substantially all of our revenue is from members and participating service providers in the United States. Consequently, a decline in consumer demand for local services, particularly in the home improvement and health and wellness segments, or for consumer ratings and reviews could have a disproportionately greater impact on our revenue than if our geographic mix of revenue was less concentrated. In addition, becauseas expenditures by service providers generally tend to reflect overall economic conditions, to the extent that economic growth in the United States remains slow, reductions in advertising by local service providers could have a serious impact on our service provider revenue and negatively impact our business.

If use of the Internet does not continue to increase, our growth prospects will be harmed.

Our future success is substantially dependent upon the continued use of the Internet as an effective medium of business and communication by consumers. Internet use may not continue to develop at historical rates, and consumers may not continue to use the Internet to research and hire local service providers. In addition, the Internet may not be accepted as a viable resource for a number of reasons, including:

actual or perceived lack of security of information or privacy protection;

• | actual or perceived lack of security of information or privacy protection; |

possible disruptions, computer viruses or other damage to Internet servers or to users’ computers; and

• | possible disruptions, computer viruses or other damage to Internet servers or to users’ computers; and |

• | excessive governmental regulation. |

excessive governmental regulation.

Our success will depend, in large part, upon third parties maintaining the Internet infrastructure to provide a reliable network backbone with the speed, data capacity, security and hardware necessary for reliable Internet access and services. Our growth prospects are also significantly dependent upon the availability and adoption of broadband Internet access and other high-speed Internet connectivity technologies.

We face many risks associated with our long-term plan to expand our operations outside of the United States.

Expanding our operations into international markets is an element of our long-term strategy. However, offering our products and services outside of the United States involves numerous risks and challenges. Most importantly, acquiring paid memberships in foreign countries and convincing foreign service providers to advertise with us would require substantial investment by us in local advertising and marketing, and there can be no assurance that we would succeed or achieve any return on this investment. In addition, international expansion would expose us to other risks such as:

the need to modify our technology and sell our products and services in non-English speaking countries;

• | the need to modify our technology and sell our products and services in non-English speaking countries; |

the need to localize our products and services to the preferences and customs of foreign consumers and local service providers;

• | the need to localize our products and services to the preferences and customs of foreign consumers and local service providers; |

difficulties in managing operations due to language barriers, distance, staffing, cultural differences and business infrastructure constraints;

• | difficulties in managing operations due to language barriers, distance, staffing, cultural differences and business infrastructure constraints; |

our lack of experience in marketing, and encouraging viral marketing, in foreign countries;

• | our lack of experience in marketing, and encouraging viral marketing, in foreign countries; |

23

application of foreign laws and regulations to us, including more stringent consumer and data protection laws;

• | application of foreign laws and regulations to us, including more stringent consumer and data protection laws; |

fluctuations in currency exchange rates;

• | fluctuations in currency exchange rates; |

risk of member or local service provider fraud;

• | risk of member or local service provider fraud; |

reduced or ineffective protection of our intellectual property rights in some countries; and

• | reduced or ineffective protection of our intellectual property rights in some countries; and |

• | potential adverse tax consequences associated with foreign operations and revenue. |

potential adverse tax consequences associated with foreign operations and revenue.

As a result of these obstacles, we may find it impossible or prohibitively expensive to enter foreign markets, or entry into foreign markets could be delayed, which could harm our business, operating results and financial condition.

We may acquire other companies or technologies, which could divert our management’s attention, result in additional dilution to our stockholders and otherwise disrupt our operations and harm our operating results.

Our success will depend, in part, on our ability to expand our product and service offerings and grow our business in response to changing technologies, member and service provider demands and competitive pressures. In some circumstances, we may determine to do so through the acquisition of complementary businesses or technologies rather than through internal development. We have limited experience acquiring other businesses and technologies. The pursuit of potential acquisitions may divert the attention of management and cause us to incur various expenses in identifying, investigating and pursuing suitable acquisitions, whether or not they are consummated. Furthermore, even if we successfully acquire additional businesses or technologies, we may not be able to integrate the acquired personnel, operations and technologies successfully or effectively manage the combined business following the acquisition. We also may not achieve the anticipated benefits from the acquired business or technology. In addition, we may unknowingly inherit liabilities from future acquisitions that arise after the acquisition and are not adequately covered by indemnities. Acquisitions could also result in dilutive issuances of equity securities or the incurrence of debt, which could adversely affect our operating results. If an acquired business or technology fails to meet our expectations, our operating results, business and financial condition may suffer.

Our ability to use our net operating loss carryforwards and certain other tax attributes may be limited.

At December 31, 2012 2013,we had federal net operating loss carryforwards of approximately $105.3 million and state net operating loss carryforwards of approximately $119.3$130.9 million. Under Sections 382 and 383 of the Internal Revenue Code of 1986, as amended, or the Code, if a corporation undergoes an “ownership change,” the corporation’s ability to use its pre-change net operating loss carryforwards and other pre-change tax attributes, such as research tax credits, to offset its post-change income and taxes may be limited. In general, an “ownership change” generally occurs if there is a cumulative change in our ownership by “5-percent shareholders” that exceeds 50 percentage points over a rolling three-year period. Similar rules may apply under state tax laws. We may have experienced an ownership change in the past and may experience ownership changes in the future as a result of future transactions in our stock, some of which may be outside our control. As a result, if we earn net taxable income, our ability to use our pre-change net operating loss carryforwards, or other pre-change tax attributes, to offset United States federal and state taxable income and taxes may be subject to limitations.

Our business is subject to the risks of tornadoes, floods, fires, earthquakes and other natural catastrophic events and to interruption by man-made problems such as computer viruses or terrorism.

Our systems and operations are vulnerable to damage or interruption from tornadoes, floods, fires, power losses, telecommunications failures, terrorist attacks, acts of war, human errors, break-ins or similar events. For example, a significant natural disaster, such as a tornado, fire or flood, could have a material adverse impact on our business, operating results and financial condition, and our insurance coverage may be insufficient to

24

compensate us for such losses that may occur. A portion of our technology team is located in the San Francisco Bay Area, a region known for seismic activity. In addition, acts of terrorism could cause disruptions in our business or the economy as a whole. Our servers may also be vulnerable to computer viruses, break-ins and similar disruptions from unauthorized tampering with our computer systems, which could lead to interruptions, delays, loss of critical data or the unauthorized disclosure of confidential customer data. We currently have limited disaster recovery capability, and our business interruption insurance may be insufficient to compensate us for losses that may occur. As we rely heavily on our servers, computer and communications systems and the Internet to conduct our business and provide high quality service to our members and service providers, such disruptions could negatively impact our ability to run our business, which could have an adverse effect on our operating results and financial condition.

Risks Related to Owning Our Common Stock

Our stock price may be volatile, and the value of an investment in our common stock may decline.

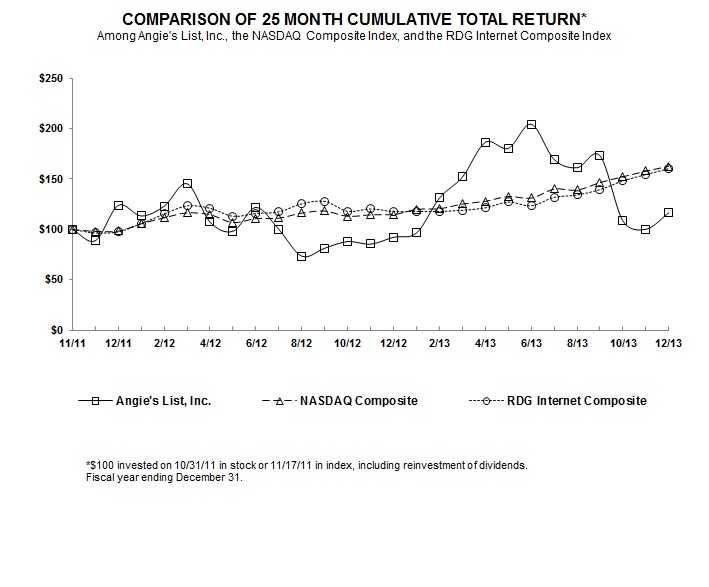

The trading price of our common stock has been, and is likely to continue to be volatile, and could decline substantially within a short period of time. For example, since shares of our common stock were sold in our initial public offering in November 2011 at a price of $13.00 per share, our trading price has ranged from $8.94 to $19.82.$28.32. The trading price of our common stock may be subject to wide fluctuations in response to various factors, some of which are beyond our control. In addition to the factors discussed in this “Risk Factors” section, these factors include:

our operating performance and the operating performance of similar companies;

• | our operating performance and the operating performance of similar companies; |

the overall performance of the equity markets;

• | the overall performance of the equity markets; |

the number of shares of our common stock publicly owned and available for trading;

• | the number of shares of our common stock publicly owned and available for trading; |

threatened or actual litigation;

• | threatened or actual litigation; |

changes in laws or regulations relating to our solutions;

• | changes in laws or regulations relating to our solutions; |

any major change in our board of directors or management;

• | any major change in our board of directors or management; |

publication of research reports about us or our industry or changes in recommendations or withdrawal of research coverage by securities analysts;

• | publication of research reports about us or our industry, changes in securities analysts’ projections or recommendations, withdrawal of research coverage, or our failure to meet analysts’ projections; |

large volumes of sales of shares of our common stock by existing stockholders; and

• | large volumes of sales of shares of our common stock by existing stockholders; and |

• | general political and economic conditions. |

general political and economic conditions.

In addition, the stock market has experienced extreme price and volume fluctuations that often have been unrelated or disproportionate to the operating performance of listed companies. Securities class action litigation has often been instituted against companies following periods of volatility in the overall market and in the market price of a company’s securities. This litigation, if institutedWe are currently the subject of multiple stockholder class action lawsuits. These lawsuits, and any future stockholder class action lawsuits initiated against us, could result in very substantial costs, divert our management’s attention and resources and harm our business, operating results and financial condition.

Future sales of our common stock by stockholders could depress the market price of our common stock.

As of December 31, 2012,2013, holders of approximately 16,478,94515,069,628 shares, or 29%26%, of our common stock vested stock options and options which vest within 60 days and their transferees have rights, subject to some conditions, to require us to file registration statements covering the sale of their shares or to include their shares in registration statements that we may file for ourselves or other stockholders. In addition, in November 2011, and March 2012 and October 2013, we filed registration statements on Form S-8 under the Securities Act to register an aggregate of 6,784,82710,830,475 shares of our common stock for issuance under our amended and restated omnibus incentive plan. This plan also provides for automatic increases in the shares

25

reserved for issuance under the plan. These shares may be sold in the public market upon issuance and,once vested, any restrictions providedareprovided under the terms of the applicable plan or award agreement. If these additional shares are sold, or if it is perceived that they will be sold, in the public market, the trading price of our common stock could decline.

We have incurred and will continue to incur increased costs as a result of becoming a reporting company.

We have faced and will continue to face increased legal, accounting, administrative and other costs as a result of becoming a reporting company. In additionWe are subject to Section 404 discussed above,the reporting requirements of the Securities Exchange Act of 1934, as amended, and related SEC rules implemented byand regulations, the SECDodd-Frank Act, the listing requirements of the NASDAQ Global Market and the Public Company Accounting Oversight Board have required changes in the corporate governance practices of public companies. We expectother applicable securities rules and regulations. Compliance with these rules and regulations to increasehas increased our legal and financial compliance costs and likely will continue to make legal, accounting and administrative activities more time-consuming and costly. For example, we expect to add independent directors and adopt policies regarding internal controls and disclosure controls and procedures. We are also incurring substantially higher costs to obtain directors’ and officers’ insurance than in prior periods.we did as a private company. In addition, as we gain experience with the costs associated with being a reporting company, we may identify and incur additional overhead costs.

If securities or industry analysts publish inaccurate or unfavorable research about our business, cease coverage of our company or make projections that exceed our actual results, our stock price and trading volume could decline.

The trading market for our common stock will be influenced by the research and reports that securities or industry analysts publish about us or our business. If one or more of the analysts who cover us downgrades our stock or publishes inaccurate or unfavorable research about our business, our stock price would likely decline. If one or more of these analysts ceases coverage of our company or fails to publish reports on us regularly, demand for our stock could decrease, which might cause our stock price and trading volume to decline.

Furthermore, such analysts publish their own projections regarding our actual results. These projections may vary widely from one another and may not accurately predict the results we actually achieve. Our stock price may decline if we fail to meet securities and analysts’ projections.

Concentration of ownership among our officers and directors and their affiliates may limit the influence of new investors on corporate decisions.

Our officers, directors and their affiliated funds beneficially own or control, directly or indirectly, approximately 29%27% of the outstanding shares of common stock. As a result, if some of these persons or entities act together, they will have significant influence over the outcome of matters submitted to our stockholders for approval, including the election of directors and approval of significant corporate transactions, such as a merger or other sale of our company or its assets. This concentration of ownership could limit the ability of other stockholders to influence corporate matters and may have the effect of delaying or preventing an acquisition or cause the market price of our stock to decline. Some of these persons or entities may have interests different from yours.

Certain provisions in our charter documents and Delaware law could discourage takeover attempts and lead to management entrenchment.

Our amended and restated certificate of incorporation and amended and restated bylaws contain provisions that could have the effect of delaying or preventing changes in control or changes in our management without the consent of our board of directors, including, among other things:

• | a classified board of directors with three year staggered terms, which could delay the ability of stockholders to replace a majority of our board of directors; |

• | no cumulative voting in the election of directors, which limits the ability of minority stockholders to elect director candidates; |

• | the ability of our board of directors to issue shares of preferred stock and to determine the price and other terms of those shares, including preferences and voting rights, without stockholder approval, which could be used to significantly dilute the ownership of a hostile acquiror; |

no cumulative voting in the election of directors, which limits the ability of minority stockholders to elect director candidates;

• | the exclusive right of our board of directors to elect a director to fill a vacancy created by the expansion of our board of directors or the resignation, death or removal of a director, which prevents stockholders from being able to fill vacancies on our board of directors; |

26

the ability of our board of directors to issue shares of preferred stock and to determine the price and other terms of those shares, including preferences and voting rights, without stockholder approval, which could be used to significantly dilute the ownership of a hostile acquiror;

• | a prohibition on stockholder action by written consent, which forces stockholder action to be taken at an annual or special meeting of our stockholders; |

the exclusive right of our board of directors to elect a director to fill a vacancy created by the expansion of our board of directors or the resignation, death or removal of a director, which prevents stockholders from being able to fill vacancies on our board of directors;

• | the requirement that a special meeting of stockholders may be called only by a majority vote of our Board of Directors, the Chairman of our Board of Directors, our Chief Executive Officer, our President or our Secretary, which could delay the ability of our stockholders to force consideration of a proposal or to take action, including the removal of directors; |

a prohibition on stockholder action by written consent, which forces stockholder action to be taken at an annual or special meeting of our stockholders;

• | the requirement for the affirmative vote of holders of at least 66 2/3% of the voting power of all of the then-outstanding shares of the voting stock, voting together as a single class, to amend the provisions of our amended and restated certificate of incorporation relating to the issuance of preferred stock and management of our business or our amended and restated bylaws, which may inhibit the ability of an acquiror to amend our amended and restated certificate of incorporation or amended and restated bylaws to facilitate a hostile acquisition; |

the requirement that a special meeting of stockholders may be called only by a majority vote of our Board of Directors, the Chairman of our Board of Directors, our Chief Executive Officer, our President or our Secretary, which could delay the ability of our stockholders to force consideration of a proposal or to take action, including the removal of directors;

• | the ability of our board of directors, by majority vote, to amend our amended and restated bylaws, which may allow our board of directors to take additional actions to prevent a hostile acquisition and inhibit the ability of an acquiror to amend our amended and restated bylaws to facilitate a hostile acquisition; and |