Valence, France

| Leased | ||||||||||||

| 3,900 | Office for Industrial segment

| |||||||||||

Rödermark, Germany | Leased | 8,600 | Warehouse and office for Industrial segment

| |||||||||

Milan, Italy | Leased | 7,500 | Office and warehouse for Industrial segment

| |||||||||

Sibiu, Romania | Leased | 31,000 | Manufacturing for Industrial segment

| |||||||||

St. Gallen, Switzerland | Owned | 78,000 | Manufacturing, warehouse, office, product development and application laboratory for Industrial segment

| |||||||||

St. Gallen, Switzerland | Leased | 9,000 | Manufacturing for Industrial segment

| |||||||||

Poole, Dorset, United Kingdom | Leased | 3,500 | Office and warehouse for Industrial segment | |||||||||

| ||||||||||||

| Denton, Manchester, United Kingdom | Leased | 2,500 | Manufacturing, warehouse and office for Industrial segment |

| Stoke-on-Trent, Staffordshire, United Kingdom | Leased | 7,300 | Manufacturing, warehouse, office and product development for Industrial segment | ||||||||||

| Brighouse, West Yorkshire, United Kingdom | Leased | 18,000 | Manufacturing, warehouse, office and product development for Industrial segment | ||||||||||

| Brighouse, West Yorkshire, United Kingdom | Leased | 10,800 | Manufacturing, warehouse and office for Industrial segment | ||||||||||

| Brighouse, West Yorkshire, United Kingdom | Leased | 6,000 | Warehouse for Industrial segment | ||||||||||

Asia Pacific | |||||||||||||

| Bundoora, Australia | Leased | 2,500 | Office

| ||||||||||

| Derrimut, Australia | Leased | 7,500 | Warehouse

| ||||||||||

| Shanghai, P.R.C. | Leased | Office; Asia Pacific training, testing and education center

| |||||||||||

Shanghai Waiqaoqiao Pilot Free Trade Zone, P.R.C. | Leased | Warehouse

| |||||||||||

Shanghai, P.R.C. | Leased | 27,000 | Office and warehouse for Industrial segment | ||||||||||

| Suzhou, P.R.C. | Owned | 79,000 | Manufacturing, warehouse, office and product development

| ||||||||||

Yokohama, Japan | Leased | 18,500 | Office

| ||||||||||

Boon Lay Way, Singapore | Leased | ||||||||||||

| Warehouse and office for Industrial segment | |||||||||||||

Anyang, South Korea | Leased | 5,100 | Office

| ||||||||||

| Gwangjoo, South Korea | Leased | 10,700 | Warehouse | ||||||||||

Our Company is engaged in routine litigation, administrative proceedings and regulatory reviews incident to our business. It is not possible to predict with certainty the outcome of these unresolved matters, but management believes that they will not have a material effect upon our operations or consolidated financial position.

Item 4. Mine Safety DisclosuresSafetyDisclosures

Not applicable.

Executive Officers of Our Company

The following are all the executive officers of Graco Inc. as of February 18, 2014:17, 2015:

Patrick J. McHale, 52,53, is President and Chief Executive Officer, a position he has held since June 2007. He served as Vice President and General Manager, Lubrication Equipment Division from June 2003 to June 2007. He was Vice President, Manufacturing and Distribution Operations from April 2001 to June 2003. He served as Vice President, Contractor Equipment Division from February 2000 to April 2001. From September 1999 to February 2000, he was Vice President, Lubrication Equipment Division. Prior to September 1999, he held various manufacturing management positions in Minneapolis, Minnesota; Plymouth, Michigan; and Sioux Falls, South Dakota. Mr. McHale joined the Company in 1989.

David M. Ahlers, 55,56, became Vice President, Human Resources and Corporate Communications in April 2010. From September 2008 through March 2010, he served as the Company’s Vice President, Human Resources. Prior to joining Graco, Mr. Ahlers held various human resources positions, including, most recently, Chief Human Resources Officer and Senior Managing Director of GMAC Residential Capital, from August 2003 to August 2008. He joined the Company in 2008.

Caroline M. Chambers, 49,50, was elected Vice President, Corporate Controller and Information Systems on December 6, 2013. She has also served as the Company’s principal accounting officer since September 2007. From April 2009 to December 2013, she was Vice President and Corporate Controller. She served as Vice President and Controller from December 2006 to April 2009. She was Corporate Controller from October 2005 to December 2006 and Director of Information Systems from July 2003 through September 2005. Prior to becoming Director of Information Systems, she held various management positions in the internal audit and accounting departments. Prior to joining Graco, Ms. Chambers was an auditor with Deloitte & Touche in Minneapolis, Minnesota and Paris, France. Ms. Chambers joined the Company in 1992.

Mark D. Eberlein, 53,54, is Vice President and General Manager, Process Division, a position he has held since January 2013. From November 2008 to December 2012, he was Director, Business Development, Industrial Products Division. He was Director, Manufacturing Operations, Industrial Products Division from January to October 2008. From 2001 to 2008, he was Manufacturing Operations Manager of a variety of Graco business divisions. Prior to joining Graco, Mr. Eberlein worked as an engineer at Honeywell and at Sheldahl. He joined the Company in 1996.

Karen Park Gallivan, 57,58, became Vice President, General Counsel and Secretary in September 2005. She was Vice President, Human Resources from January 2003 to September 2005. Prior to joining Graco, she was Vice President of Human Resources and Communications at Syngenta Seeds, Inc. from January 1999 to January 2003. From 1988 through January 1999, she was the general counsel of Novartis Nutrition Corporation. Prior to joining Novartis, Ms. Gallivan was an attorney with the law firm of Rider, Bennett, Egan & Arundel, L.L.P. She joined the Company in 2003.

James A. Graner, 69,70,became Chief Financial Officer in September 2005, a position he held in conjunction with Treasurer from September 2005 to June 2011. He served as Vice President and Controller from March 1994 to September 2005. He was Treasurer from May 1993 through February 1994. Prior to becoming Treasurer, he held various managerial positions in the treasury, accounting and information systems departments. He joined the Company in 1974. Mr. Graner has announced his intention to retire in 2015.

Dale D. Johnson, 59,60,became Vice President and General Manager, Contractor Equipment Division in April 2001. From January 2000 through March 2001, he served as President and Chief Operating Officer. From December 1996 to January 2000, he was Vice President, Contractor Equipment Division. Prior to becoming the Director of Marketing, Contractor Equipment Division in June 1996, he held various marketing and sales positions in the Contractor Equipment division and the Industrial Equipment division. He joined the Company in 1976.

Jeffrey P. Johnson, 54,55, became Vice President and General Manager, EMEA in January 2013. From February 2008 to December 2012 he was Vice President and General Manager, Asia Pacific. He served as Director of Sales and Marketing, Applied Fluid Technologies Division, from June 2006 until February 2008. Prior to joining Graco, he held various sales and marketing positions,

including, most recently, President of Johnson Krumwiede Roads, a full-service advertising agency, and European sales manager at General Motors Corp. He joined the Company in 2006.

David M. Lowe, 58,59, became Executive Vice President, Industrial Products Division in April 2012. From February 2005 to April 2012, he was Vice President and General Manager, Industrial Products Division. He was Vice President and General Manager, European Operations from September 1999 to February 2005. Prior to becoming Vice President, Lubrication Equipment Division in December 1996, he was Treasurer. Mr. Lowe joined the Company in 1995.

Bernard J. Moreau, 53,54, is Vice President and General Manager, South and Central America, a position he has held since January 2013. From November 2003 to December 2012, he was Sales and Marketing Director, EMEA, Industrial/Automotive Equipment Division. From January 1997 to October 2003, he was Sales Manager, Middle East, Africa and East Europe. Prior to 1997, he

worked in various Graco sales engineering and sales management positions, mainly to support Middle East, Africa and southern Europe territories. He joined the Company in 1985.

Peter J. O’Shea, 49,50,became Vice President and General Manager, Asia Pacific in January 2013. From January 2012 until December 2012, he was Director of Sales and Marketing, Industrial Products Division, and from 2008 to 2012, he was Director of Sales and Marketing, Industrial Products Division and Applied Fluid Technologies Division. He was Country Manager, Australia - New Zealand from 2005 to 2008, and from 2002 to 2005 he served as Business Development Manager, Australia - New Zealand. Prior to becoming Business Development Manager, Australia - New Zealand, he worked in various Graco sales management positions. Mr. O’Shea joined the Company in 1995.

Charles L. Rescorla, 62,63,was elected Vice President, Corporate Manufacturing, Distribution Operations and Corporate Development on December 6, 2013. From June 2011 to December 2013, he was Vice President, Corporate Manufacturing, Information Systems and Distribution Operations. He was Vice President, Manufacturing, Information Systems and Distribution Operations from April 2009 to June 2011. He served as Vice President, Manufacturing and Distribution Operations from September 2005 to April 2009. From June 2003 to September 2005, he was Vice President, Manufacturing/Distribution Operations and Information Systems. From April 2001 until June 2003, he was Vice President and General Manager, Industrial/Automotive Equipment Division. Prior to April 2001, he held various positions in manufacturing and engineering management. Mr. Rescorla joined the Company in 1988.

Christian E. Rothe, 40,41,became Vice President and Treasurer in June 2011. Prior to joining Graco, he held various positions in business development, accounting and finance, including, most recently, at Gardner Denver, Inc., a manufacturer of highly engineered products, as Vice President, Treasurer from January 2011 to June 2011, Vice President - Finance, Industrial Products Group from October 2008 to January 2011, and Director, Strategic Planning and Development from October 2006 to October 2008. Mr. Rothe joined the Company in 2011.

Mark W. Sheahan, 49,50, became Vice President and General Manager, Applied Fluid Technologies Division in February 2008. He served as Chief Administrative Officer from September 2005 until February 2008, and was Vice President and Treasurer from December 1998 to September 2005. Prior to becoming Treasurer in December 1996, he was Manager, Treasury Services. He joined the Company in 1995.

Brian J. Zumbolo, 44,45, became Vice President and General Manager, Lubrication Equipment Division in August 2007. He was Director of Sales and Marketing, Lubrication Equipment and Applied Fluid Technologies, Asia Pacific, from November 2006 through July 2007. From February 2005 to November 2006, he was the Director of Sales and Marketing, High Performance Coatings and Foam, Applied Fluid Technologies Division. Mr. Zumbolo was the Director of Sales and Marketing, Finishing Equipment from May 2004 to February 2005. Prior to May 2004, he held various marketing positions in the Industrial Equipment division. Mr. Zumbolo joined the Company in 1999.

Except as otherwise noted above, the Board of Directors elected or re-elected the above executive officers to their current positions on December 7, 2012, effective January 1, 2013.

Item 5. Market for the Company’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities

Graco Common Stock

Graco common stock is traded on the New York Stock Exchange under the ticker symbol “GGG.” As of February 4, 2014,3, 2015, the share price was $67.67$71.65 and there were 60,862,15458,991,622 shares outstanding and 2,7672,788 common shareholders of record, which includes nominees or broker dealers holding stock on behalf of an estimated 42,00078,000 beneficial owners.

High and low sales prices for the Company’s common stock and dividends declared for each quarterly period in the past two years were as follows:

| First Quarter | Second Quarter | Third Quarter | Fourth Quarter | |||||||||||||||||||||||||||||

2014 | ||||||||||||||||||||||||||||||||

Stock price per share | ||||||||||||||||||||||||||||||||

High | $ | 78.97 | $ | 77.82 | $ | 79.88 | $ | 81.93 | ||||||||||||||||||||||||

Low | 65.18 | 70.39 | 72.29 | 67.06 | ||||||||||||||||||||||||||||

Dividends declared per share | 0.28 | 0.28 | 0.28 | 0.30 | ||||||||||||||||||||||||||||

| First Quarter | Second Quarter | Third Quarter | Fourth Quarter | |||||||||||||||||||||||||||||

2013 | ||||||||||||||||||||||||||||||||

Stock price per share | ||||||||||||||||||||||||||||||||

High | $ | 59.81 | $ | 65.43 | $ | 74.70 | $ | 79.66 | $ | 59.81 | $ | 65.43 | $ | 74.70 | $ | 79.66 | ||||||||||||||||

Low | 52.45 | 53.90 | 62.84 | 72.39 | 52.45 | 53.90 | 62.84 | 72.39 | ||||||||||||||||||||||||

Dividends declared per share | 0.25 | 0.25 | 0.25 | 0.28 | 0.25 | 0.25 | 0.25 | 0.28 | ||||||||||||||||||||||||

2012 | ||||||||||||||||||||||||||||||||

Stock price per share | ||||||||||||||||||||||||||||||||

High | $ | 53.25 | $ | 56.66 | $ | 52.69 | $ | 53.25 | ||||||||||||||||||||||||

Low | 39.79 | 43.19 | 41.09 | 44.91 | ||||||||||||||||||||||||||||

Dividends declared per share | 0.23 | 0.23 | 0.23 | 0.25 | ||||||||||||||||||||||||||||

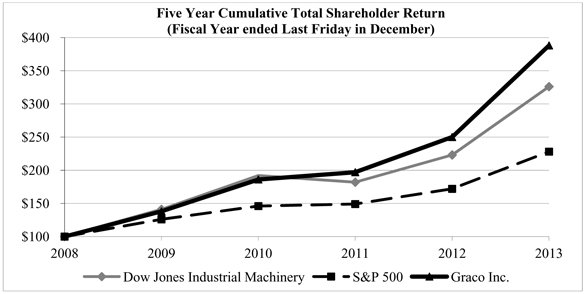

The graph below compares the cumulative total shareholder return on the common stock of the Company for the last five fiscal years with the cumulative total return of the S&P 500 Index and the Dow Jones US Industrial Machinery Index over the same period (assuming the value of the investment in Graco common stock and each index was $100 on December 26, 2008,25, 2009, and all dividends were reinvested).

| 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | |||||||||||||

Dow Jones Industrial Machinery | 100 | 141 | 192 | 182 | 223 | 326 | ||||||||||||||||||

Dow Jones US Industrial Machinery | 100 | 136 | 129 | 158 | 231 | 228 | ||||||||||||||||||

S&P 500 | 100 | 126 | 146 | 149 | 172 | 228 | 100 | 115 | 117 | 136 | 180 | 205 | ||||||||||||

Graco Inc. | 100 | 138 | 186 | 197 | 250 | 388 | 100 | 135 | 143 | 181 | 281 | 299 | ||||||||||||

Issuer Purchases of Equity Securities

On September 14, 2012, the Board of Directors authorized the Company to purchase up to 6,000,000 shares of its outstanding common stock, primarily through open-market transactions. The authorization expires on September 30, 2015.

In addition to shares purchased under the Board authorization, the Company purchases shares of common stock held by employees who wish to tender owned shares to satisfy the exercise price or tax withholding on stock option exercises.

Information on issuer purchases of equity securities follows:

Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs (at end of period) | ||||||||||||

Sep 28, 2013 - Oct 25, 2013 | 100,000 | $ | 75.70 | 100,000 | 5,469,918 | |||||||||||

Oct 26, 2013 - Nov 22, 2013 | 200,000 | $ | 77.63 | 200,000 | 5,269,918 | |||||||||||

Nov 23, 2013 - Dec 27, 2013 | 229,800 | $ | 76.59 | 229,800 | 5,040,118 | |||||||||||

Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs (at end of period) | ||||||||||||

Sep 27, 2014 - Oct 24, 2014 | 277,035 | $ | 71.11 | 277,035 | 2,887,377 | |||||||||||

Oct 25, 2014 - Nov 21, 2014 | 200,000 | $ | 78.52 | 200,000 | 2,687,377 | |||||||||||

Nov 22, 2014 - Dec 26, 2014 | 230,000 | $ | 79.59 | 230,000 | 2,457,377 | |||||||||||

Item 6. Selected Financial Data

Graco Inc. and Subsidiaries (in thousands, except per share amounts)

| 2013 | 2012 | 2011 | 2010 | 2009 | 2014 | 2013 | 2012 | 2011 | 2010 | |||||||||||||||||||||||||||||||

Net sales | $ | 1,104,024 | $ | 1,012,456 | $ | 895,283 | $ | 744,065 | $ | 579,212 | $ | 1,221,130 | $ | 1,104,024 | $ | 1,012,456 | $ | 895,283 | $ | 744,065 | ||||||||||||||||||||

Net earnings | 210,822 | 149,126 | 142,328 | 102,840 | 48,967 | 225,573 | 210,822 | 149,126 | 142,328 | 102,840 | ||||||||||||||||||||||||||||||

Per common share | ||||||||||||||||||||||||||||||||||||||||

Basic net earnings | $ | 3.44 | $ | 2.47 | $ | 2.36 | $ | 1.71 | $ | 0.82 | $ | 3.75 | $ | 3.44 | $ | 2.47 | $ | 2.36 | $ | 1.71 | ||||||||||||||||||||

Diluted net earnings | 3.36 | 2.42 | 2.32 | 1.69 | 0.81 | 3.65 | 3.36 | 2.42 | 2.32 | 1.69 | ||||||||||||||||||||||||||||||

Cash dividends declared | 1.03 | 0.93 | 0.86 | 0.81 | 0.77 | 1.13 | 1.03 | 0.93 | 0.86 | 0.81 | ||||||||||||||||||||||||||||||

Total assets | $ | 1,327,228 | $ | 1,321,734 | $ | 874,309 | $ | 530,474 | $ | 476,434 | $ | 1,544,778 | $ | 1,327,228 | $ | 1,321,734 | $ | 874,309 | $ | 530,474 | ||||||||||||||||||||

Long-term debt (including current portion) | 408,370 | 556,480 | 300,000 | 70,255 | 86,260 | 615,000 | 408,370 | 556,480 | 300,000 | 70,255 | ||||||||||||||||||||||||||||||

Net sales in 2012 included $93 million from Powder Finishing operations acquired in April 2012. The Company used long-term borrowings and available cash balances to complete the $668 million purchase of Powder Finishing and Liquid Finishing businesses in 2012.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following Management’s Discussion and Analysis reviews significant factors affecting the Company’s consolidated results of operations, financial condition and liquidity. This discussion should be read in conjunction with our financial statements and the accompanying notes to the financial statements. The discussion is organized in the following sections:

Overview

Graco designs, manufactures and markets systems and equipment to pump, meter, mix and dispense a wide variety of fluids and coatings. The Company specializes in equipment for applications that involve difficult-to-handle materials with high viscosities, materials with abrasive or corrosive properties and multiple-component materials that require precise ratio control. Graco sells primarily through independent third-party distributors worldwide to industrial and contractor end-users.end users. More than half of our sales are outside of the United States. Graco’s business is classified by management into three reportable segments, each responsible for product development, manufacturing, marketing and sales of their products.

Graco’s key strategies include developing and marketing new products, leveraging products and technologies into additional, growing end user markets, expanding distribution globally and completing strategic acquisitions that provide additional channel and technologies. Long-term financial growth targets accompany these strategies, including our expectation of 10 percent revenue growth and 12 percent consolidated net earnings growth. In 2013, the Process division was created within the Industrial segment to provide specific focus on development of product and channel related to industrial in-plant applications. In addition, a regional management team was formed to focus on building commercial resources in South and Central America. We continued to develop new products in each operating division including products that are expected to drive incremental sales growth, such as the development of equipment for packaging applications as well as continued refresh and upgrades of existing product lines. We

In January 2014, the Company paid $65 million cash to acquire QED Environmental Systems, a manufacturer of fluid management solutions for environmental monitoring and remediation, markets where Graco had little or no previous exposure. Results of operations are included in the Company’s Industrial segment starting from the date of acquisition.

In October 2014, we acquired EcoQuipthe stock of Alco Valves Group (“Alco”) for £72 million cash. Alco is a United Kingdom based manufacturer of high quality, high pressure valves used in the oil and QED, with combined annual revenuesnatural gas industry and in other industrial processes. Alco’s products and business relationships will enhance Graco’s position in the oil and natural gas industry and complement Graco’s core competencies of approximately $30 million. Both acquisitions were completeddesigning and manufacturing advanced flow control technologies. Results of Alco operations are included in December 2013, although the QED acquisition closed subsequent to fiscal year end.Company’s Industrial segment starting from the date of acquisition.

Manufacturing is a key competency of the Company. Our management team in Minneapolis provides strategic manufacturing expertise, and is also responsible for factories not fully aligned with a single division. Our primary manufacturing facilities are in the United States and Switzerland, and our primary distribution facilities are located in the United States, Belgium, Switzerland, United Kingdom, P.R.C., Japan, Korea and Australia.

Acquisition and Planned Divestiture of ITW Liquid Finishing Brands AcquisitionBusinesses

OnIn April 2, 2012, we completedpurchased the Finishing Brandsfinishing businesses of ITW. The acquisition includingincluded finishing equipment operations, technologies and brands of the Powder Finishing operations and Liquid Finishing operations.businesses. Results of the Powder Finishing businessbusinesses have been included in the Industrial segment since the date of acquisition. In March 2012, the FTC issued an order to hold the Liquid Finishing assets separate from our other businesses. In May 2012, the FTC issued a proposed decision and order that required us to sell the held separate Liquid Finishing business assets no later than 180 days from the date the order becomes final. The FTC approved a final decision and order that became effective on October 9, 2014.

Pursuant to the hold separatefinal order, issued by the FTC,Graco must sell the Liquid Finishing business is being held separate fromassets within 180 days of the rest of Graco’s businesses untileffective date. On October 8, 2014, the FTC has issued its final order and the divestiture ofCompany announced it had signed a definitive agreement to sell the Liquid Finishing business assets for $590 million cash, subject to regulatory approval and other customary closing conditions. The sale transaction is completed.

We have retainedexpected to close in the servicesfirst half of an investment bank to help us market2015, in compliance with the Liquid Finishing businessesFTC’s final decision and identify potential buyers. While we seek a buyer, we mustorder. Graco will continue to hold the Liquid Finishing business assetsbusinesses separate from our other businesses and maintain them as viable and competitive. In accordance withcompetitive until the hold separate order, the Liquid Finishing businesses are managed independently by experienced Liquid Finishing business managers, under the supervision of a trustee appointed by the FTC, who reports directly to the FTC.sale process is complete.

Under terms of the hold separate order, the Company does not have the power to direct the activities of the Liquid Finishing businesses that most significantly impact the economic performance of those businesses. Therefore, we have determined that the Liquid Finishing businesses are variable interest entities for which the Company is not the primary beneficiary and that they should not be consolidated. Furthermore, the Company does not have a controlling interest in the Liquid Finishing businesses, nor is it able to exert significant influence over the Liquid Finishing businesses. Consequently, our investment in the shares of the Liquid Finishing businesses has been reflected as a cost-method investment on our Consolidated Balance Sheets as of December 27, 201326, 2014 and December 28, 2012,27, 2013, and their results of operations have not been consolidated with those of the Company. As a cost-method investment, income is recognized based on dividends received from current earnings of Liquid Finishing. Dividends of $28 million

received in 2014, $28 million received in 2013 and $12 million received in 2013 and 2012 respectively, are included in other expense (income) on the Consolidated Statements of Earnings. We evaluate our cost-method investment for other-than-temporary impairment at each reporting period. As of December 27, 2013,26, 2014, we evaluated our investment in the Liquid Finishing businesses and determined that there was no impairment.

Results of Operations

Net sales, operating earnings, net earnings and earnings per share were as follows (in millions except per share amounts):

| 2013 | 2012 | 2011 | 2014 | 2013 | 2012 | |||||||||||||||||||

Net Sales | $ | 1,104 | $ | 1,012 | $ | 895 | $ | 1,221 | $ | 1,104 | $ | 1,012 | ||||||||||||

Operating Earnings | 280 | 225 | 220 | 309 | 280 | 225 | ||||||||||||||||||

Net Earnings | 211 | 149 | 142 | 226 | 211 | 149 | ||||||||||||||||||

Diluted Net Earnings per Common Share | $ | 3.36 | $ | 2.42 | $ | 2.32 | $ | 3.65 | $ | 3.36 | $ | 2.42 | ||||||||||||

2014 Summary:

| • | The effective tax rate was 28 1⁄2 percent, up from 27 percent in 2013. The effective rate was lower in 2013 primarily because it included two years of federal R&D credit as the credit was reinstated in the first quarter of 2013 retroactive to the beginning of 2012. |

2013 Summary:

2012 Summary:

The following table presents net sales by geographic region (in millions):

| 2013 | 2012 | 2011 | 2014 | 2013 | 2012 | |||||||||||||||||||

Americas1 | $ | 595 | $ | 536 | $ | 476 | $ | 684 | $ | 595 | $ | 536 | ||||||||||||

EMEA2 | 283 | 257 | 211 | 305 | 283 | 257 | ||||||||||||||||||

Asia Pacific | 226 | 219 | 208 | 232 | 226 | 219 | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total | $ | 1,104 | $ | 1,012 | $ | 895 | $ | 1,221 | $ | 1,104 | $ | 1,012 | ||||||||||||

|

|

|

|

|

| |||||||||||||||||||

| 1 | North, South and Central America, including the United States. Sales in the United States were $577 million in 2014, $498 million in 2013 and $441 million in |

| 2 | Europe, Middle East and Africa |

In 2014, sales in the Americas increased by 15 percent in total, with increases of 18 percent in the Industrial segment, 12 percent in the Contractor segment and 13 percent in the Lubrication segment as compared to the prior year. Sales from acquired operations totaled $32 million in the Americas, contributing 6 percentage points of growth. All of the growth from acquisitions is included the Industrial segment. Excluding acquisitions the Industrial segment grew by 7 percent in the region, with strength broadly across industrial end user markets and successful new product launches. The Contractor segment continues to benefit from the recovery of the U.S. housing and construction markets. Sales in the Lubrication segment reflected double digit growth in both vehicle service applications and industrial lubrication customers.

In 2014, sales in EMEA increased by 8 percent (7 percent at consistent translation rates). Sales in the Industrial segment increased by 9 percent (8 percent at consistent translation rates). Sales increased by 5 percent in the Contractor segment (4 percent at consistent translation rates) and decreased by 1 percent in the Lubrication segment (2 percent at consistent translation rates). Growth in EMEA came primarily from the developed economies in the West. The emerging markets increased slightly over 2013, with gains in Eastern Europe and the Middle East, partially offset by declines in Russia.

In 2014, sales in Asia Pacific grew by 3 percent. Sales increased by 3 percent in the Industrial segment (4 percent at consistent translation rates). Sales in the Contractor segment decreased by 3 percent (4 percent at consistent translation rates) and sales in the Lubrication segment decreased by 7 percent (4 percent at consistent translation rates). China grew by 3 1⁄2 percent, with good growth in the automotive industry. However, we continue to see lack of growth in a number of other markets throughout the region and continue to see variability in bookings and billings by country and product line.

In 2013, sales in the Americas increased by 11 percent in total, with increases of 6 percent in the Industrial segment, 22 percent in the Contractor segment and flat in the Lubrication segment as compared to the prior year. The increase in the Americas was led by the Contractor segment, which benefited from growth in U.S. housing starts and construction spending. Increased sales in the Industrial segment were driven by improvement in a variety of general industrial, construction and process-related end-markets. Sales in the Lubrication segment reflected modest demand growth in vehicle service applications and a low rate of investment by industrial lubrication customers.

In 2013, sales in EMEA increased by 10 percent (8 percent at consistent translation rates). Sales in the Industrial segment increased by 12 percent (9 percent at consistent translation rates). Sales increased by 4 percent in the Contractor segment (2 percent at consistent translation rates) and increased by 14 percent in the Lubrication segment (12 percent at consistent translation rates). We continued to seesaw growth during 2013 in the emerging markets of EMEA, though end-markets in many industries remained weak in Western Europe throughout much of the year.

In 2013, sales in Asia Pacific grew by 3 percent (5 percent at consistent translation rates). Sales increased by 7 percent in the Industrial segment (10 percent at consistent translation rates). Sales in the Contractor segment decreased by 4 percent (3 percent at consistent translation rates) and sales in the Lubrication segment decreased by 13 percent (10 percent at consistent translation rates). Industrial project activity was strong in the fourth quarter, which brought the Industrial segment back to modest growth for the year. However, we continue to seesaw lack of growth in a number of end user markets throughout Asia Pacific, including shipyards, container manufacturing, heavy machinery, general manufacturing, housing, paint and mining, and we face an increased level of competition in the region.

In 2012, sales in the Americas increased by 13 percent, with increases of 19 percent in the Industrial segment, 5 percent in the Contractor segment and 13 percent in the Lubrication segment as compared to the prior year. Growth related to the acquired Powder Finishing business was 4 percentage points. The increase in the Americas reflected strength across a range of product lines with growth in a number of industrial end-markets as well as growth in the housing and construction industries.

In 2012, sales in EMEA increased by 22 percent (28 percent at consistent translation rates), primarily due to the sales from Powder Finishing of $52 million since the acquisition. Sales of legacy Graco products in the Industrial segment decreased by 2 percent during 2012 (increased by 3 percent at consistent translation rates). Sales decreased by 5 percent in the Contractor segment (flat at consistent translation rates) and increased by 2 percent in the Lubrication segment (7 percent at consistent translation rates). We continued to see growth during 2012 in the emerging markets of Eastern Europe and the Middle East, though end-markets in many industries remained weak in Western Europe.

In 2012, sales in Asia Pacific grew by 5 percent overall. Sales of Powder Finishing equipment were $22 million from the date of acquisition. Sales decreased by 7 percent in 2012 for legacy Graco products in the Industrial segment. Sales in the Contractor

segment grew by 4 percent and sales in the Lubrication segment decreased by 10 percent. Activity levels in many end-markets remained challenging throughout the region and across product categories throughout 2012.mining.

The following table presents components of net sales change:

| 2013 | 2014 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Segment | Region | Segment | Region | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Industrial | Contractor | Lubrication | Americas | Europe | Asia Pacific | Consolidated | Industrial | Contractor | Lubrication | Americas | Europe | Asia Pacific | Consolidated | |||||||||||||||||||||||||||||||||||||||||||||||

Volume and Price | 3 % | 14 % | - % | 10 % | 2 % | 1 % | 6 % | 6 % | 10 % | 9 % | 10 % | 5 % | 2 % | 7 % | ||||||||||||||||||||||||||||||||||||||||||||||

Acquisitions | 5 % | - % | - % | 1 % | 6 % | 4 % | 3 % | 6 % | - % | - % | 6 % | 2 % | 2 % | 4 % | ||||||||||||||||||||||||||||||||||||||||||||||

Currency | - % | 1 % | (1) % | - % | 2 % | (2) % | - % | - % | - % | (1)% | (1)% | 1 % | (1)% | - % | ||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||||||||||||||||||

Total | 8 % | 15 % | (1) % | 11 % | 10 % | 3 % | 9 % | 12 % | 10 % | 8 % | 15 % | 8 % | 3 % | 11 % | ||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||||||||||||||||||

| 2012 | 2013 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Segment | Region | Segment | Region | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Industrial | Contractor | Lubrication | Americas | Europe | Asia Pacific | Consolidated | Industrial | Contractor | Lubrication | Americas | Europe | Asia Pacific | Consolidated | |||||||||||||||||||||||||||||||||||||||||||||||

Volume and Price | 3 % | 4 % | 8 % | 9 % | 2 % | (5) % | 4 % | 3 % | 14 % | - % | 10 % | 2 % | 1 % | 6 % | ||||||||||||||||||||||||||||||||||||||||||||||

Acquisitions | 19 % | - % | - % | 4 % | 26 % | 10 % | 10 % | 5 % | - % | - % | 1 % | 6 % | 4 % | 3 % | ||||||||||||||||||||||||||||||||||||||||||||||

Currency | (2) % | (1) % | (1) % | - % | (6) % | - % | (1) % | - % | 1 % | (1)% | - % | 2 % | (2)% | - % | ||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||||||||||||||||||

Total | 20 % | 3 % | 7 % | 13 % | 22 % | 5 % | 13 % | 8 % | 15 % | (1)% | 11 % | 10 % | 3 % | 9 % | ||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||||||||||||||||||

The following table presents an overview of components of operating earnings as a percentage of net sales:

| 2013 | 2012 | 2011 | 2014 | 2013 | 2012 | |||||||||||||||||||

Net Sales | 100.0 % | 100.0 % | 100.0 % | 100.0 | % | 100.0 | % | 100.0 | % | |||||||||||||||

Cost of products sold | 45.0 | 45.6 | 44.1 | 45.4 | 45.0 | 45.6 | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Gross profit | 55.0 | 54.4 | 55.9 | 54.6 | 55.0 | 54.4 | ||||||||||||||||||

Product development | 4.7 | 4.8 | 4.7 | 4.4 | 4.7 | 4.8 | ||||||||||||||||||

Selling, marketing and distribution | 16.1 | 16.2 | 16.9 | 16.0 | 16.1 | 16.2 | ||||||||||||||||||

General and administrative | 8.9 | 11.2 | 9.8 | 8.9 | 8.9 | 11.2 | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Operating earnings | 25.3 | 22.2 | 24.5 | 25.3 | 25.3 | 22.2 | ||||||||||||||||||

Interest expense | 1.6 | 1.9 | 1.0 | 1.5 | 1.6 | 1.9 | ||||||||||||||||||

Other expense (income), net | (2.5) | (1.1) | 0.1 | (2.0) | (2.5) | (1.1) | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Earnings before income taxes | 26.2 | 21.4 | 23.4 | 25.8 | 26.2 | 21.4 | ||||||||||||||||||

Income taxes | 7.1 | 6.7 | 7.5 | 7.3 | 7.1 | 6.7 | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Net Earnings | 19.1 % | 14.7 % | 15.9 % | 18.5 | % | 19.1 | % | 14.7 | % | |||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

2014 Compared to 2013

Operating earnings as a percentage of sales were 25 percent in 2014, consistent with 2013. The impact of purchase accounting, acquisition and divestiture costs, and spending on regional and product expansion offset the improvement in operating expense leverage from higher sales.

Gross profit margin as a percentage of sales decreased approximately one-half percentage point from 2013. Acquisitions negatively impacted the margin rate in 2014, decreasing the rate by 0.2 percentage point for purchase accounting, and 0.3 percentage point for lower margins in the acquired businesses. The favorable effect of realized price increases and higher production volume offset the unfavorable effect of changes in product mix.

Operating expenses for 2014 increased $30 million. The increase included $15 million from acquired operations, $8 million from regional and product expansion initiatives and a $2 million increase in divestiture and acquisition costs. Product development spending increased $3 million (including approximately $1 million from acquired operations), and represents 4 percent of sales, down slightly from 2013.

Interest expense was $19 million in 2014, compared to $18 million in 2013. Other expense (income) included dividends received from the Liquid Finishing businesses that are held separate from the Company’s other businesses. These dividends totaled $28 million for the year, consistent with 2013.

The effective income tax rate was 28 1⁄2 percent in 2014, compared to 27 percent in 2013. Last year’s effective rate was lower primarily because it included two years of federal R&D credit as the credit was reinstated in the first quarter of 2013 retroactive to the beginning of 2012.

2013 Compared to 2012

Operating earnings as a percentage of sales were 25 percent in 2013 as compared to 22 percent in 2012. Expense leverage and reductions of acquisition and divestiture costs led to the improvements in operating earnings as a percentage of sales.

Gross profit margin as a percentage of sales was 55 percent in 2013 as compared to 54 percent in 2012. The favorable effect of realized price increases and higher production volume offset the unfavorable effect of changes in product mix, including increased sales of powder finishing equipment and Contractor segment sales. For 2012, non-recurring purchase accounting effects reduced the gross margin percentage by approximately 1 percentage point.

Operating expenses for the year increased $2 million over 2012 with business activity-related increases largely offset by decreases in acquisition and divestiture costs in 2013. Acquisition and divestiture costs were $2 million in 2013, as compared to $16 million in 2012. Overall, product development spending was 5 percent of sales in 2013, consistent with 2012.

Interest expense was $18 million in 2013, a decrease of $1 million from 2012. Other expense (income) included dividends received from the Liquid Finishing businesses that are held separate from the Company’s other businesses. Dividends for the year totaled $28 million in 2013 and $12 million in 2012.

The effective income tax rate was 27 percent for the year as compared to 31 percent in 2012. The lower rate for 2013 reflected the effects of higher after-tax dividend income received from the Liquid Finishing businesses and the federal R&D credit that was renewed in 2013, effective retroactive to the beginning of 2012. There was no R&D credit recognized in 2012.

2012 Compared to 2011

Operating earnings as a percentage of sales were 22 percent in 2012 as compared to 25 percent in 2011. The impact of purchase accounting related to the Powder Finishing acquisition, higher acquisition/divestiture costs and an increase in pension costs were partially offset by other operating improvements.

Gross profit margin as a percentage of sales was 54 percent in 2012 as compared to 56 percent in 2011. Non-recurring purchase accounting effects totaling $7 million related to acquired inventory with the Powder Finishing operations reduced the gross margin percentage by approximately 1 percentage point. Strong operating performance and cost management improved margins on the legacy Graco operations, partially offsetting the lower margin rates on acquired Powder Finishing operations.

Operating expenses for the year increased $45 million, including $25 million from Powder Finishing operations, an increase of $8 million for acquisition and divestiture costs, an increase of $5 million in product development spending and an increase of $5 million in pension expense. Overall, product development spending was 5 percent of sales in 2012, consistent with 2011.

The purchase of Powder Finishing and Liquid Finishing operations had significant impacts on interest expense (an increase of $10 million for the year) and other expense (income), which included dividend income of $12 million received from the Liquid Finishing businesses held as a cost-method investment.

The effective income tax rate was 31 percent for the year as compared to 32 percent in 2011. The 2012 effective tax rate was reduced by the effect of the investment income from the Liquid Finishing businesses held separate and the effect of a tax rate change on deferred liabilities related to a tax holiday received in a foreign jurisdiction.

Segment Results

The following table presents net sales and operating earnings by business segment (in millions):

| 2013 | 2012 | 2011 | 2014 | 2013 | 2012 | |||||||||||||||||||

Sales | ||||||||||||||||||||||||

Industrial | $ | 652 | $ | 603 | $ | 502 | $ | 727 | $ | 652 | $ | 603 | ||||||||||||

Contractor | 343 | 299 | 291 | 376 | 343 | 299 | ||||||||||||||||||

Lubrication | 109 | 110 | 102 | 118 | 109 | 110 | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total | $ | 1,104 | $ | 1,012 | $ | 895 | $ | 1,221 | $ | 1,104 | $ | 1,012 | ||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Operating Earnings | ||||||||||||||||||||||||

Industrial | $ | 211 | $ | 186 | $ | 174 | $ | 225 | $ | 211 | $ | 186 | ||||||||||||

Contractor | 72 | 54 | 51 | 82 | 72 | 54 | ||||||||||||||||||

Lubrication | 23 | 23 | 19 | 26 | 23 | 23 | ||||||||||||||||||

Unallocated corporate | (26) | (38) | (24) | (24 | ) | (26 | ) | (38 | ) | |||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total | $ | 280 | $ | 225 | $ | 220 | $ | 309 | $ | 280 | $ | 225 | ||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Management looks at economic and financial indicators relevant to each segment and geography to gauge the business environment, as noted in the discussion below for each segment.

Industrial

The following table presents net sales, components of net sales change and operating earnings as a percentage of sales for the Industrial segment (dollars in millions):

| 2013 | 2012 | 2011 | 2014 | 2013 | 2012 | |||||||||||||||||||

Sales | ||||||||||||||||||||||||

Americas | $ | 276 | $ | 261 | $ | 220 | $ | 327 | $ | 276 | $ | 261 | ||||||||||||

EMEA | 206 | 184 | 135 | 224 | 206 | 184 | ||||||||||||||||||

Asia Pacific | 170 | 158 | 147 | 176 | 170 | 158 | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total | $ | 652 | $ | 603 | $ | 502 | $ | 727 | $ | 652 | $ | 603 | ||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Components of Net Sales Change | ||||||||||||||||||||||||

Volume and Price | 3 % | 3 % | 20 % | 6 % | 3 % | 3 % | ||||||||||||||||||

Acquisitions | 5 % | 19 % | - % | 6 % | 5 % | 19 % | ||||||||||||||||||

Currency | - % | (2) % | 3 % | - % | - % | (2)% | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total | 8 % | 20 % | 23 % | 12 % | 8 % | 20 % | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Operating Earnings as a Percentage of Sales | 32 % | 31 % | 35 % | 31 % | 32 % | 31 % | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

In 2014, sales in the Industrial segment totaled $727 million, an increase of 12 percent from the prior year. Sales for the year increased 18 percent in the Americas, 9 percent in EMEA and 3 percent in Asia Pacific. Results for 2014 included the operations of EcoQuip, acquired at the end of 2013, QED Environmental Systems, acquired at the beginning of fiscal 2014, and Alco, acquired at the beginning of the fourth quarter. Acquired operations contributed $41 million (6 percentage points of growth) in the Industrial segment for the year.

Operating margin rates for 2014 decreased by 1 percentage point compared to last year due to lower margins on acquired operations, including the impact of acquisition-related inventory valuation adjustments, acquisition expense and spending on regional and product expansion.

In 2013, sales in the Industrial segment totaled $652 million, an increase of 8 percent from the prior year. First quarter 2013 sales from the acquired Powder Finishing operations contributed approximately 5 percentage points to the 2013 sales growth. Overall for the Industrial segment, sales increased by 6 percent in the Americas, increased 12 percent in EMEA (9 percent at consistent translation rates) and increased 7 percent in Asia Pacific (10 percent at consistent translation rates).

Operating earnings as a percentage of sales were 32 percent in 2013 as compared to 31 percent in 2012. The effects of purchase accounting related to inventory reduced the operating margin rate for 2012 by approximately 1 percentage point.

In 2012, sales in the Industrial segment totaled $603 million, an increase of 20 percent from the prior year, including $93 million from Powder Finishing operations acquired in April 2012. Without Powder Finishing, sales increased by 10 percent in the Americas, decreased 2 percent in EMEA (3 percent increase at consistent translation rates) and decreased 7 percent in Asia Pacific.

Operating earnings as a percentage of sales were 31 percent in 2012 as compared to 35 percent in 2011. Powder Finishing operations contributed to segment earnings, but at a lower rate on sales, which drove the decrease in the operating margin for the Industrial segment.

In this segment, sales in each geographic region are significant and management looks at economic and financial indicators in each region, including gross domestic product, industrial production, capital investment rates, automobile production, building construction and the level of the U.S. dollar versus the euro, the Swiss franc, the Canadian dollar, the Australian dollar and various Asian currencies.

Contractor

The following table presents net sales, components of net sales change and operating earnings as a percentage of sales for the Contractor segment (dollars in millions):

| 2013 | 2012 | 2011 | 2014 | 2013 | 2012 | |||||||||||||||||||

Sales | ||||||||||||||||||||||||

Americas | $ | 237 | $ | 194 | $ | 184 | $ | 265 | $ | 237 | $ | 194 | ||||||||||||

EMEA | 67 | 64 | 68 | 71 | 67 | 64 | ||||||||||||||||||

Asia Pacific | 39 | 41 | 39 | 40 | 39 | 41 | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total | $ | 343 | $ | 299 | $ | 291 | $ | 376 | $ | 343 | $ | 299 | ||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Components of Net Sales Change | ||||||||||||||||||||||||

Volume and Price | 14 % | 4 % | 11 % | 10 % | 14 % | 4 % | ||||||||||||||||||

Currency | 1 % | (1) % | 2 % | - % | 1 % | (1)% | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total | 15 % | 3 % | 13 % | 10 % | 15 % | 3 % | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Operating Earnings as a Percentage of Sales | 21 % | 18 % | 17 % | 22 % | 21 % | 18 % | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Sales in the Contractor segment increased 10 percent for the year, which included increases of 12 percent in the Americas, 5 percent in EMEA and 3 percent in Asia Pacific. The growth in the Contractor segment was led by the Americas, which continued to benefit from the recovery of the U.S. housing and construction markets.

Operating earnings as a percentage of sales were 22 percent, up 1 percentage point from 2013. Higher sales and the leverage on expenses drove improvements in operating earnings in the Contractor Segment.

In 2013, sales in the Contractor segment increased 15 percent as compared to 2012. By geography, sales increased by 22 percent in the Americas, increased 4 percent in Europe (2 percent at consistent translation rates) and decreased 4 percent in Asia Pacific.

Operating earnings as a percentage of sales were 21 percent in 2013 as compared to 18 percent in 2012. Higher sales and the leveraging of expenses drove the improvement of operating earnings as a percentage of sales.

In 2012, sales in the Contractor segment increased 3 percent. By geography, sales increased by 5 percent in the Americas, decreased 5 percent in Europe (flat at consistent translation rates) and increased 4 percent in Asia Pacific.

Higher sales and the leveraging of expenses led to improvements in operating earnings as a percentage of sales.

In this segment, sales in all regions are significant and management reviews economic and financial indicators in each region, including levels of residential, commercial and institutional construction, remodeling rates and interest rates. Management also reviews gross domestic product for the regions and the level of the U.S. dollar versus the euro and other currencies.

Lubrication

The following table presents net sales, components of net sales change and operating earnings as a percentage of sales for the Lubrication segment (dollars in millions):

| 2013 | 2012 | 2011 | 2014 | 2013 | 2012 | |||||||||||||||||||

Sales | ||||||||||||||||||||||||

Americas | $ | 82 | $ | 81 | $ | 72 | $ | 92 | $ | 82 | $ | 81 | ||||||||||||

EMEA | 10 | 9 | 8 | 10 | 10 | 9 | ||||||||||||||||||

Asia Pacific | 17 | 20 | 22 | 16 | 17 | 20 | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total | $ | 109 | $ | 110 | $ | 102 | $ | 118 | $ | 109 | $ | 110 | ||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Components of Net Sales Change | ||||||||||||||||||||||||

Volume and Price | - % | 8 % | 30 % | 9 % | - % | 8 % | ||||||||||||||||||

Currency | (1) % | (1) % | 2 % | (1)% | (1)% | (1)% | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total | (1) % | 7 % | 32 % | 8 % | (1)% | 7 % | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Operating Earnings as a Percentage of Sales | 21 % | 20 % | 18 % | 22 % | 21 % | 20 % | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

In 2014, sales in the Lubrication segment increased by 8 percent for the year. Sales increased 13 percent in the Americas, decreased 1 percent in EMEA and 7 percent in Asia Pacific.

Operating earnings increased by 1 percentage point in 2014. Higher sales volume and expense leverage led to higher operating margin in the Lubrication segment.

In 2013, sales in the Lubrication segment decreased by 1 percentage point compared to 2012. By geography, sales were flat in the Americas, increased 14 percent in EMEA, and decreased 13 percent in Asia Pacific.

In 2012, sales in the Lubrication segment increased 7 percent. By geography, sales increased by 13 percent in the Americas, 2 percent in Europe (7 percent at consistent translation rates) and decreased 10 percent in Asia Pacific.

Operating earnings were $23 million or 20 percent of sales as compared to $19 million or 18 percent of sales in 2011. Improved gross margin rates and leveraging of expenses led to improvement in operating earnings as a percentage of sales.

Although the Americas represent the substantial majority of sales for the Lubrication segment, and indicators in that region are the most significant, management monitors indicators such as levels of gross domestic product, capital investment, industrial production and mining activity worldwide.

Unallocated corporate

(in millions)

| 2013 | 2012 | 2011 | ||||||||||

Unallocated corporate (expense) | $ | (26) | $ | (38) | $ | (24) | ||||||

| 2014 | 2013 | 2012 | ||||||||||

Unallocated corporate (expense) | $ | (24 | ) | $ | (26 | ) | $ | (38 | ) | |||

Unallocated corporate includes such items such as stock compensation, non-service portiondivestiture and certain acquisition transaction costs, bad debt expense, charitable contributions, certain portions of pension expense, bad debtand in 2014, central warehouse startup expenses. In 2014, unallocated corporate expenses included $17 million of stock compensation expense, $3 million of acquisition and divestiture costs, and $2 1⁄2 million of contributions to the Company’s charitable foundation, and certain other charges or credits driven by corporate decisions, including expense$1 1⁄2 million related to acquisition/divestiture activities.the new central warehouse. In 2013, unallocated corporate included $16 million of stock compensation, $6 million related to the non-service cost portion of pension expense, $2 million related to acquisition/divestiture activities, and $2 million of contributions to the Company’s charitable foundation. In 2012, acquisition/divestiture expense totaled $16 million, stock compensation totaled $12 million, the non-service portion of pension expense was $8 million and contributions to the Company’s charitable foundation totaled $2 million.

Financial Condition and Cash Flow

Working Capital.The following table highlights several key measures of asset performance (dollars in millions):

| 2013 | 2012 | 2014 | 2013 | |||||||||||||

Working capital | $ | 624 | $ | 625 | $ | 685 | $ | 624 | ||||||||

Current ratio | 4.7 | 5.1 | 4.9 | 4.7 | ||||||||||||

Days of sales in receivables outstanding | 60 | 62 | 64 | 60 | ||||||||||||

Inventory turnover (LIFO) | 3.8 | 4.0 | 3.8 | 3.8 | ||||||||||||

InAccounts receivable and inventory balances increased in both 2014 and 2013 the Company’s financial condition was strong. Cash flows from operations were $243 million, a 28 percent increase over 2012. due to increases in business activity.

Changes in receivables and inventories increased in line with volume growth. Primary uses of cash included net payments on long-term debt of $148 million, share repurchases of $68 million, dividends of $61 million, capital expenditures of $23 million and business acquisitions of $12 million.

Cash flows from operations totaled $190 million in 2012. Changes in receivables and inventories moderated during 2012 after increasing in 2011. Primary uses of cash included investments in businesses held separately of $427 million, business acquisitions of $240 million, payments on long-term lines of credit of $393 million, capital expenditures of $18 million and dividends of $54 million.

Capital Structure.At December 26, 2014, the Company’s capital structure included current notes payable of $5 million, long-term debt of $615 million and shareholders’ equity of $596 million. At December 27, 2013, the Company’s capital structure included current notes payable of $10 million, long-term debt of $408 million and shareholders’ equity of $634 million. At December 28, 2012, the Company’s capital structure included current notes payable of $8 million, long-term debt of $556 million and shareholders’ equity of $454 million.

Shareholders’ equity increaseddecreased by $180$38 million in 2013.2014. The key components of changesdecreases in shareholders’ equity include current year earnings of $211 million, reduced by $70$195 million of shares repurchased, and $63$67 million of dividends declared, and increased by $42decreases of $54 million for shares issued and increases in other comprehensive income (loss) due mainly to pension and post-retirement medical liability adjustments.adjustments and foreign currency translation. The decreases in shareholders’ equity were offset by current year earnings of $226 million and $30 million for shares issued.

Liquidity and Capital Resources. The Company had cash totaling $24 million at December 26, 2014 and $20 million at December 27, 2013, and $31 million at December 28, 2012, held in deposit accounts.

There wereIn January 2014, the Company paid $65 million cash to acquire QED Environmental Systems, a manufacturer of fluid management solutions for environmental monitoring and remediation, markets where Graco had little or no changes toprevious exposure. The acquired business will expand and complement the Company’s credit agreements during 2013. Industrial segment.

On March 27, 2012,June 26, 2014, the Company’s $250 millionCompany executed an amendment to its revolving credit agreement, was terminated in connection withextending the executionexpiration date to June 26, 2019, and increasing the amount of credit available to $500 million, a new unsecured revolving$50 million increase. The credit agreement. The current credit agreementfacility is with a syndicate of

lenders and expires in March 2017. It provides up to $450 million of committed credit,

is available for general corporate purposes, working capital needs, share repurchases and acquisitions. The Company may borrow up to $50 million under the swingline portion of the facility for daily working capital needs.

Under terms of the revolving creditamended agreement, loans denominated in U.S. dollars bear interest, at the Company’s option, at either a base rate or a LIBOR-based rate. Loans denominated in currencies other than U.S. dollars bear interest at a LIBOR-based rate. The base rateapplied to borrowings is an annual rate equal to a margin ranging from zero percent to 0.875 percent (down from zero to 1 percent under the prior agreement), depending on the Company’s cash flow leverage ratio, (debt to earnings before interest, taxes, depreciation, amortization and extraordinary non-operating or non-cash charges and expenses) plus the highest of (i) the bank’s prime rate, (ii) the federal funds rate plus 0.5 percent or (iii) one-month LIBOR plus 1.5 percent. In general, LIBOR-based loans bear interest at LIBOR plus 1 percent to 1.875 percent (down from 1 to 2 percent,percent), depending on the Company’s cash flow leverage ratio. The Company is also required to pay a feeFees on the undrawn amount of the loan commitment at an annual rate rangingdecreased to a range of 0.15 percent to 0.30 percent (down from 0.15 percent to 0.40 percent,percent), depending on the Company’s cash flow leverage ratio.

The agreement requiresOn October 1, 2014, the Company used proceeds from its revolving line of credit to maintain certain financial ratios asacquire the stock of Alco Valves Group for £72 million cash, subject to cash flow leverage and interest coverage. The Companynormal post-closing purchase price adjustments. Alco is in compliance with all financial covenantsa United Kingdom based manufacturer of its debt agreements.

On April 2, 2012, the Company paid $660 million to complete the Finishing Brands acquisition, using available cash and $350 million of borrowings on the new credit agreement. In July 2012, the Company made an additional payment of $8 million, representing the difference between cash balances acquired and the amount estimated at the time of closing. Assets acquiredhigh quality, high pressure valves used in the acquisitionoil and natural gas industry and in other industrial processes. Alco’s products and business relationships will enhance Graco’s position in the oil and natural gas industry and complement Graco’s core competencies of designing and manufacturing advanced flow control technologies. Alco revenues for the most recent trailing twelve months were approximately £19 million. Results of Alco operations have been included $18 millionin the Company’s Industrial segment starting from the date of cash, of which $6 million was availableacquisition.

Pursuant to Powder Finishing operations.

In May 2012,a final order from the FTC issued a proposed decision and order which requiresthat became effective on October 9, 2014, Graco tomust sell the Liquid Finishing business assets including Liquid Finishing business activities related to the development, manufacture, and sale of products under the Binks, DeVilbiss, Ransburg and BGK brand names, no later thanacquired in 2012 within 180 days fromof the date the order becomes final. The FTC has not yet issued its final decision and order. The Company has retained the services of an investment bankeffective date. Graco will continue to help it markethold the Liquid Finishing businesses separate and identify potential buyers.maintain them as viable and competitive until a sale process is complete. The Company believes its investment in the Liquid Finishing businesses, carried atbusiness assets are held as a costcost-method investment on Graco’s balance sheet, and income is recognized based on dividends received from current earnings. Since the date of $422 million, is not impaired.

Under terms of the FTC’s hold separate order, the Company is required to provide sufficient resources to maintain the viability, competitiveness and marketability of the Liquid Finishing businesses, including general funds, capital, working capital and reimbursement of losses. To the extent that the Liquid Finishing businesses generate funds in excess of financial resources needed, the Company has access to such funds consistent with practices in place prior to the acquisition. During 2013 and 2012,acquisition, the Company received a total of $28$68 million and $12 million, respectively, of dividends from current earnings of the Liquid Finishing businesses.businesses, including $28 million in 2014. Once the Company completes the sale of its investment, there will be no further dividends from Liquid Finishing.

On October 8, 2014, the Company announced it had signed a definitive agreement to sell the Liquid Finishing business assets for $590 million cash, subject to regulatory approval and other customary closing conditions. The sale transaction is expected to close in the first half of 2015, in compliance with the FTC’s final decision and order. Graco expects to use the proceeds from the sale of the Liquid Finishing assets for reduction of outstanding debt, ongoing share repurchases, and to make investments in strategic acquisitions that provide synergistic opportunities.

On December 27, 2013,26, 2014, the Company had $502$550 million in lines of credit, including the $500 million revolving credit agreement noted above, of which $355$200 million was unused. Internally generated funds and unused financing sources are expected to provide the Company with the flexibility to meet its liquidity needs in 2014,2015, including its capital expenditure plan of approximately $25-30$35 million, planned dividends (estimated at $67$70 million) and acquisitions. In January 2015, the Company used proceeds from its revolving line of credit to acquire High Pressure Equipment Holdings, LLC (HiP) for $160 million. The Company completed two additional business acquisitions in January 2015, for cash consideration totaling approximately $20 million. If acquisition opportunities increase, the Company believes that reasonable financing alternatives are available for the Company to execute on those opportunities.

In December 2013,2014, the Company’s Board of Directors increased the Company’s regular common dividend from an annual rate of $1.00$1.10 to $1.10$1.20 per share, a 109 percent increase.

Cash Flow.A summary of cash flow follows (in millions):

| 2013 | 2012 | 2011 | ||||||||||

Operating Activities | $ | 243 | $ | 190 | $ | 162 | ||||||

Investing Activities | (31) | (695) | (28) | |||||||||

Financing Activities | (226) | 233 | 160 | |||||||||

Effect of exchange rates on cash | 3 | - | - | |||||||||

|

|

|

|

|

| |||||||

Net cash provided (used) | (11) | (272) | 294 | |||||||||

|

|

|

|

|

| |||||||

Cash and cash equivalents at year-end | $ | 20 | $ | 31 | $ | 303 | ||||||

|

|

|

|

|

| |||||||

| 2014 | 2013 | 2012 | ||||||||||

Operating Activities | $ | 241 | $ | 243 | $ | 190 | ||||||

Investing Activities | (217 | ) | (31 | ) | (695 | ) | ||||||

Financing Activities | (23 | ) | (226 | ) | 233 | |||||||

Effect of exchange rates on cash | 3 | 3 | - | |||||||||

|

|

|

|

|

| |||||||

Net cash provided (used) | 4 | (11 | ) | (272 | ) | |||||||

|

|

|

|

|

| |||||||

Cash and cash equivalents at year-end | $ | 24 | $ | 20 | $ | 31 | ||||||

|

|

|

|

|

| |||||||

Cash Flows From Operating Activities. Net cash provided by operating activities was $241 million in 2014 and $243 million in 2013. The increase in accounts receivable and inventories was $20 million higher in 2014 than the increase in the comparable period of 2013. Accounts receivable and inventory balances have increased since the end of 2013 due to increases in business activity.

Net cash provided by operating activities was $243 million in 2013 and $190 million in 2012. During 2013, changes in receivables and inventories increased in line with volume growth. Net cash provided by operating activities in 2013 was driven by net income of $211 million and adjustments for depreciation and amortization and share-based compensation.

Net cash provided by operating activities was $190 million in 2012 and $162 million in 2011. During 2012, changes in receivables and inventories moderated after increasing in 2011.

Cash Flows Used in Investing Activities. Cash flows used in investing activities totaled $217 million in 2014, compared to $31 million in 2013. During 2014, cash outflows consisted of acquisitions of $185 million and additions to property, plant and equipment of $31 million. During 2013, cash used in investing activities was $31 million compared to $695 million in 2012. During 2013, cash outflows consisted of $23 million of additions to property, plant and equipment, and business acquisitions of $12 million. During 2012, cash outflows included an investment in businesses held separate of $427 million, business acquisitions of $240 million and $18 million of additions of property, plant and equipment.

Cash Flows Used in Financing Activities. Cash flows used in financing activities totaled $24 million in 2014, compared to $226 million in 2013. Cash inflows were generated by borrowings on outstanding lines of credit of $202 million and share issuances of $30 million. This was offset by share repurchases of $195 million and dividends paid of $66 million. During 2013, cash used in financing activities was $226 million. Net payments on outstanding lines of credit were $148 million, share repurchases totaled $68 million and cash dividends paid were $61 million in 2013. These cash uses were offset by the issuance of stock of $42 million. During 2012, cash provided by financing activities was $233 million. We used $350 million of borrowings on a $450 million revolving credit facility to fund business acquisitions and investments. Net payments on outstanding lines of credit, subsequent to the acquisition transaction, were $94 million in 2012 and cash dividends paid totaled $54 million.

In September 2012, the Board of Directors authorized the Company to purchase up to 6 million shares of its outstanding stock, primarily through open-market transactions. This authorization will expire on September 30, 2015. Under the current authorization, 52.5 million shares remain available for purchase as of December 27, 2013.26, 2014.

The Company repurchased and retired 2.6 million shares at a cost of $195 million in 2014, compared to repurchasing nearly 1 million shares at a cost of $68 million in 2013. We made2013 and $1 million and $43 million of share repurchases in 2012 and 2011, respectively.2012. Share repurchases willare expected to continue in 2014.2015 with a goal of weighted average dilutive shares outstanding at or below 60 million shares.

Off-Balance Sheet Arrangements and Contractual Obligations. As of December 27, 2013,26, 2014, the Company is obligated to make cash payments in connection with its long-term debt, operating leases and purchase obligations in the amounts listed below. The Company has no significant off-balance sheet debt or other unrecorded obligations other than the items noted in the following table. In addition to the commitments noted in the following table, the Company could be obligated to perform under standby letters of credit totaling $3$2 million at December 27, 2013.26, 2014. The Company has also guaranteed the debt of its subsidiaries up to $10$9 million. All debt of subsidiaries is reflected in the consolidated balance sheets.

| Payments due by period (in millions) | Payments due by period (in millions) | |||||||||||||||||||||||||||||||||||||||

| Total | Less than 1 year | 1-3 years | 3-5 years | More than 5 years | Total | Less than 1 year | 1-3 years | 3-5 years | More than 5 years | |||||||||||||||||||||||||||||||

Long-term debt | $ | 408 | $ | - | $ | - | $ | 183 | $ | 225 | $ | 615 | $ | - | $ | - | $ | 390 | $ | 225 | ||||||||||||||||||||

Operating leases | 24 | 5 | 7 | 4 | 8 | 29 | 6 | 9 | 6 | 8 | ||||||||||||||||||||||||||||||

Purchase obligations1 | 100 | 100 | - | - | - | 112 | 112 | - | - | - | ||||||||||||||||||||||||||||||

Interest on long-term debt | 127 | 16 | 32 | 27 | 52 | 125 | 18 | 37 | 30 | 40 | ||||||||||||||||||||||||||||||

Unfunded pension and postretirement medical benefits2 | 30 | 2 | 5 | 6 | 17 | 30 | 2 | 5 | 6 | 17 | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

Total | $ | 689 | $ | 123 | $ | 44 | $ | 220 | $ | 302 | $ | 911 | $ | 138 | $ | 51 | $ | 432 | $ | 290 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

| 1 | The Company is committed to pay suppliers under the terms of open purchase orders issued in the normal course of business. The Company also has commitments with certain suppliers to purchase minimum quantities, and under the terms of certain agreements, the Company is committed for certain portions of the supplier’s inventory. The Company does not purchase, or commit to purchase, quantities in excess of normal usage or amounts that cannot be used within one year. |

| 2 | The amounts and timing of future Company contributions to the funded qualified defined benefit pension plan are unknown because they are dependent on pension fund asset performance. |

Critical Accounting Estimates

The Company prepares its consolidated financial statements in conformity with generally accepted accounting principles in the United States of America (“U.S. GAAP”). The Company’s most significant accounting policies are disclosed in Note A to the consolidated financial statements. The preparation of the consolidated financial statements, in conformity with U.S. GAAP, requires management to make estimates and judgments that affect the amounts reported in the consolidated financial statements and accompanying notes. Actual amounts will differ from those estimates. The Company considers the following policies to involve the most judgment in the preparation of the Company’s consolidated financial statements.

Excess and Discontinued Inventory. The Company’s inventories are valued at the lower of cost or market. Reserves for excess and discontinued products are estimated. The amount of the reserve is determined based on projected sales information, plans for discontinued products and other factors. Though management considers these balances adequate, changes in sales volumes due to unanticipated economic or competitive conditions are among the factors that would result in materially different amounts for this item.

Goodwill and Other Intangible Assets. The Company performs impairment testing for goodwill and other intangible assets annually, or more frequently if events or changes in circumstances indicate that the asset might be impaired. For goodwill, the Company performs impairment reviews for the Company’s reporting units using a fair-value method based on management’s judgments and assumptions. The Company estimates the fair value of the reporting units by an allocation of market capitalization value, cross-checked by a present value of future cash flows calculation. The estimated fair value is then compared with the carrying amount of the reporting unit, including recorded goodwill. Based on our most recent goodwill impairment assessment performed during the fourth quarter of 2013,2014, the fair value of each reporting unit significantly exceeded its carrying value.value, except for the businesses acquired in 2014. The fair value of those businesses still exceeded their carrying value, and the results related to the analyses for those businesses are in line with management’s expectations given the recent date of appraisal and purchase price allocation. Accordingly, step two of the impairment analysis was not required.

The Company also performs a separate impairment test for each other intangible asset with indefinite life, based on estimated future use and discounting estimated future cash flows. A considerable amount of management judgment and assumptions are required in performing the impairment tests. Though management considers its judgments and assumptions to be reasonable, changes in economic or market conditions, product offerings or marketing strategies could change the estimated fair values and result in impairment charges.

Product Warranty. A liability is established for estimated warranty claims to be paid in the future that relate to current and prior period sales. The Company estimates these costs based on historical claim experience, changes in warranty programs and other factors, including evaluating specific product warranty issues. The establishment of reserves requires the use of judgment and assumptions regarding the potential for losses relating to warranty issues. Though management considers these balances adequate, changes in the Company’s warranty policy or a significant change in product defects versus historical averages are among the factors that would result in materially different amounts for this item.

Income Taxes. In the preparation of the Company’s consolidated financial statements, management calculates income taxes. This includes estimating current tax liability as well as assessing temporary differences resulting from different treatment of items for tax and financial statement purposes. These differences result in deferred tax assets and liabilities, which are recorded on the balance sheet using statutory rates in effect for the year in which the differences are expected to reverse. These assets and liabilities are analyzed regularly and management assesses the likelihood that deferred tax assets will be recoverable from future taxable income. A valuation allowance is established to the extent that management believes that recovery is not likely. Liabilities for uncertain tax positions are also established for potential and ongoing audits of federal, state and international issues. The Company routinely monitors the potential impact of such situations and believes that liabilities are properly stated. Valuations related to amounts owed and tax rates could be impacted by changes to tax codes, changes in statutory rates, the Company’s future taxable income levels and the results of tax audits.

Retirement Obligations. The measurements of the Company’s pension and postretirement medical obligations are dependent on a number of assumptions including estimates of the present value of projected future payments, taking into consideration future events such as salary increase and demographic experience. These assumptions may have an impact on the expense and timing of future contributions.

The assumptions used in developing the required estimates for pension obligations include discount rate, inflation, salary increases, retirement rates, expected return on plan assets and mortality rates. The assumptions used in developing the required estimates for postretirement medical obligations include discount rates, rate of future increase in medical costs and participation rates.