our ability to successfully integrate operations of our acquisitions and sentencing policies.);realize projected returns resulting therefrom;

Any or all of our forward-looking statements in this Annual Report may turn out to be inaccurate. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may

3

affect our financial condition, results of operations, business strategy, and financial needs. TheyOur statements can be affected by inaccurate assumptions we might make or by known or unknown risks, uncertainties and assumptions, including the risks, uncertainties, and assumptions described in “Risk Factors.”"Risk Factors" included elsewhere in this Annual Report and in other reports, documents, and other information we file with the Securities and Exchange Commission, or the SEC, from time to time.

3

In light of these risks, uncertainties and assumptions, the forward-looking events and circumstances discussed in this Annual Report may not occur and actual results could differ materially from those anticipated or implied in the forward-looking statements. When you consider these forward-looking statements, you should keep in mind the risk factors and other cautionary statements in this Annual Report, including in “Management’s"Management's Discussion and Analysis of Financial Condition and Results of Operations”Operations," "Business" and “Business.”"Risk Factors."

Our forward-looking statements speak only as of the date made. We undertake no obligation to publicly update or revise forward-looking statements, whether as a result of new information, future events or otherwise. All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained in this Annual Report.

4

We are a diversified government solutions company with the nation’s largest ownerscale and experience needed to solve tough government challenges in flexible, cost-effective ways. Through three business offerings, CoreCivic Safety, CoreCivic Properties, and CoreCivic Community, we provide a broad range of privatized correctionalsolutions to government partners that serve the public good through corrections and detention management, government real estate solutions, and a growing network of residential reentry centers to help address America's recidivism crisis. We have been a flexible and dependable partner for government for more than 30 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good.

Structured as a REIT, we are one of the nation's largest owners of partnership correctional, detention, and residential reentry facilities and one of the largest prison operators in the United States. We also believe we are the largest private owner of real estate used by government agencies. As of December 31, 2014,2017, we owned or controlled 52and managed 70 correctional, detention, and detentionresidential reentry facilities, and managed an additional 12seven correctional and detention facilities owned by our government partners, with a total design capacity of approximately 84,50078,000 beds in 19 statesstates. In addition, as of December 31, 2017, we owned 12 properties leased to third parties and the District of Columbia.used by government agencies, totaling 1.1 million square feet in five states.

We are a Real Estate Investment Trust, or REIT, specializing in owning, operating, and managing prisons and other correctional facilities and providing residential, community re-entry, and prisoner transportation services for governmental agencies. In addition to providing fundamental residential services, our correctional, detention, and residential reentry facilities offer a variety of rehabilitation and educational programs, including basic education, faith-based services, life skills and employment training, and substance abuse treatment. These services are intended to help reduce recidivism and to prepare offenders for their successful re-entryreentry into society upon their release. We also provide or make available to offenders certain health care (including medical, dental, and mental health services), food services, and work and recreational programs.

We are a Maryland corporation formed in 1983. Our principal executive offices are located at 10 Burton Hills Boulevard, Nashville, Tennessee, 37215, and our telephone number at that location is (615) 263-3000. Our website address is www.cca.com.www.corecivic.com. We make our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, definitive proxy statements, and amendments to those reports under the Securities Exchange Act of 1934, as amended, (the “Exchange Act”),or the Exchange Act, available on our website, free of charge, as soon as reasonably practicable after these reports are filed with or furnished to the Securities and Exchange Commission, or the SEC. Information contained on our website is not part of this Annual Report.

We began operating as a REIT for federal income tax purposes effective January 1, 2013. Since that date, we have provided correctionalWe provide services and conductedconduct other operationsbusiness activities through taxable REIT subsidiaries, or TRSs. A TRS is a subsidiary of a REIT that is subject to applicable corporate income tax and certain qualification requirements. Our use of TRSs enables us to comply with REIT qualification requirements while providing correctional services at facilities we own and at facilities owned by our government partners and to engage in certain other business operations. A TRS is not subject to the distribution requirements applicable to REITs so it may retain income generated by its operations for reinvestment.

As a REIT, we generally are not subject to federal income taxes on our REIT taxable income and gains that we distribute to our stockholders, including the income derived from providing prison bed capacityour real estate and dividends we earn from our TRSs. However, our TRSs will be required to pay income taxes on their earnings at regular corporate income tax rates.

As a REIT, we generally are required to distribute annually to our stockholders at least 90% of our REIT taxable income (determined without regard to the dividends paid deduction and excluding net capital gains). Our REIT taxable income will not typically include income earned by our TRSs except to the extent our TRSs pay dividends to the REIT. Prior to our REIT reorganization, we operated as a C-corporation for federal income tax purposes. A REIT is not permitted to retain earnings and profits accumulated during the periods it was taxed as a C-corporation, and must make one or more distributions to stockholders that equal or exceed those accumulated amounts. To satisfy this requirement, on April 8, 2013, our

5

Board of Directors declared a special dividend to stockholders of $675.0 million, or $6.66 per share of common stock to distribute our accumulated earnings and profits attributable to tax periods ending prior to January 1, 2013. We paid the special dividend on May 20, 2013 to stockholders of record on April 19, 2013. The special dividend was composed of cash and shares of our common stock, at each stockholder’s election, subject to a cap on the total amount of cash equal to 20% of the aggregate amount of the special dividend, or $135.0 million. The balance of the special dividend was paid in the form of 13.9 million additional shares of our common stock.

Management and Operation of Correctional and Detention Facilities

Our customers primarily consist of federal, state, and local correctional and detention authorities. Federal correctional and detention authorities primarily consist of the Federal Bureau of Prisons, or the BOP, the United

5

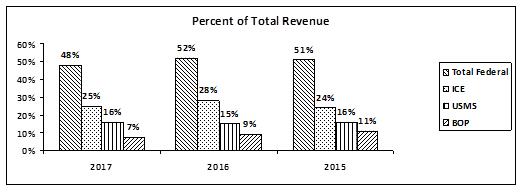

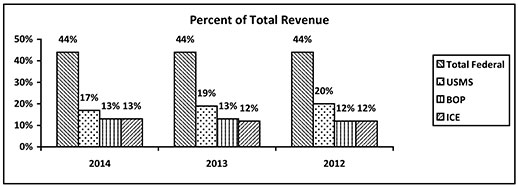

States Marshals Service, or the USMS, and the U.S. Immigration and Customs Enforcement, or ICE. Payments by federal correctional and detention authorities represented 44%48%, 52%, and 51% of our total revenue for each of the years ended December 31, 2014, 2013,2017, 2016, and 2012.2015, respectively.

Our customer contracts typically have terms of three to five years and contain multiple renewal options. Most of our facility contracts also contain clauses that allow the government agency to terminate the contract at any time without cause, and our facility contracts and government lease agreements are generally subject to annual or bi-annual legislative appropriations of funds.

We are compensated for providing prison bed capacity and correctional, detention, and residential reentry services at an inmatea per diem rate based upon actual or minimum guaranteed occupancy levels. Occupancy rates for a particular facility are typically low when first opened or immediately following an expansion. However, beyond the start-up period, which typically ranges from 90 to 180 days, the occupancy rate tends to stabilize. For the years 2014, 2013, and 2012, theThe average compensated occupancy of our facilities, based on rated capacity was 84%as follows for the years 2017, 2016, and 2015:

|

| 2017 |

|

| 2016 |

|

| 2015 |

| |||

Owned and managed facilities |

|

| 77 | % |

|

| 76 | % |

|

| 80 | % |

Managed-only facilities |

|

| 94 | % |

|

| 95 | % |

|

| 94 | % |

Total operating facilities |

|

| 80 | % |

|

| 79 | % |

|

| 83 | % |

The average compensated occupancy of our owned and managed facilities, excluding idled facilities, was 89%, 85%87%, and 88%89% for 2017, 2016, and 2015, respectively.

We also lease facilities to governmental agencies and third-party operators where our occupancy percentage is based on leased square feet rather than bed capacity. These facilities generated 6%, 5%, and 5% of our facility net operating income, which we define as a facility's operating income or loss from operations before interest, taxes, asset impairments, depreciation, and amortization, in 2017, 2016, and 2015, respectively, and the occupancy of these facilities was as follows for allthe years 2017, 2016, and 2015:

|

| 2017 |

|

| 2016 |

|

| 2015 |

| |||

Leased portfolio |

|

| 100 | % |

|

| 100 | % |

|

| 100 | % |

We also provide transportation services to governmental agencies through TransCor America, LLC, or TransCor, a subsidiary of our wholly-owned TRS. During the facilities we ownedyears ended December 31, 2017, 2016, and 2015, TransCor generated total revenue of $2.3 million, $2.6 million, and $4.1 million, respectively, or managed, exclusiveapproximately 0.1%, 0.1%, and 0.2% of facilitiesour total consolidated revenue in 2017, 2016, and 2015, respectively. We believe TransCor provides a complementary service to our core business that have been presented as discontinued operations.enables us to respond quickly to our customers' transportation needs.

Operating Procedures and Offender Services for Correctional, Detention, and Residential Reentry Facilities

Pursuant to the terms of our customer contracts, we are responsible for the overall operations of our facilities, including staff recruitment, general administration of the facilities, facility maintenance, security, and supervision of the offenders. We are required by our customer contracts to maintain certain levels of insurance coverage for general liability, workers’workers' compensation, vehicle liability, and property loss or damage. We also are also required to indemnify our customers for claims and costs arising out of our operations and, in certain cases, to maintain performance bonds and other collateral requirements. Approximately 90% of the eligible facilities we operated at December 31, 2014 were accredited by the American Correctional Association Commission on Accreditation. The American Correctional Association, or ACA, is an independent organization comprised of corrections professionals that establishes accreditation standards for correctional and detention institutions.

We arebelieve a focus on inmate reentry provides great benefits for our communities – more people living healthy and productive lives and contributing to strong families and local economies. We have committed to equipping offendersevolving our model to focus more and more on reentry services, and we are working hard to equip the men and women in our care with the services, support, and resources necessarythey need to return to the community as productive, contributing members of society. be successful.

6

To that end, we provide a wide range of evidence-based re-entryreentry programs and activities atin our facilities. At most of the facilities we manage, offenders have the opportunity to enhance their basic education from literacy through the acquisition of theearning a high school equivalency diploma endorsed by thetheir respective state and, instate. In some cases,

6

we also provide opportunities for postsecondary educational achievements. In aachievements and chances to participate in college correspondence classes. A number of our facilities and in conjunction with the Mexican government, wethat house non-citizens offer an adult education curriculumcurricula recognized by a number ofseveral nations to which these offenders may return.return, including a curriculum offered in conjunction with the Mexican government. We also provide the Adult Education in Spanish program for offenders with that specific language need.

For the offenders who are close to taking their high school equivalency exam (either the GED or the HiSET), we have invested in the equipment needed to use the GED/HiSET Academy software program, which is an offline software program providing over 200 hours of individualized lessons up to the 12th grade. The GED/HiSET Academy incorporates teaching best practices and provides an atmosphere to engage and motivate students to learn everything they need to know to pass the GED/HiSET exam. As an example of the impact we are having, during 2017, the number of offenders in our facilities who passed high school equivalency exams totaled 1,684, an increase of 3% from 2016. In 2017, our Crowley County Correctional Facility and Coffee Correctional Facility led the state systems in Colorado and Georgia, respectively, in GED completions. According to research from the independent RAND Corporation, "Evaluating the Effectiveness of Correctional Education" published in 2013, inmates who obtain GEDs while in prison are 30% less likely to return to prison.

In addition, we offer a broad spectrum of vocational/career/technical education opportunities to equiphelp individuals withlearn marketable job skills. Our trade programs are certified by the National Center for Construction Education and Research, or NCCER. NCCER establishes the curriculum and certification for over 4,000 construction and trade organizations. Graduates of these programs enter the job market with certified skills that significantly enhance employability. During 2017, 4,483 offenders in facilities we manage earned career and technical education certificates. We are proud of the educational programs we offer and intend to maintain and develop such programs. For example, near the end of 2016, in coordination with the Georgia Department of Corrections, we developed programs at two facilities in the state to offer courses in welding and diesel truck maintenance, enabling students to earn trade certificates from nearby community colleges. In 2017, 93 students graduated from these programs.

For those with assessed substance use disorder needs,disorders, we offer cognitive evidence-based treatment programs with proven clinical outcomes, such as the Residential Drug Addictions TreatmentAbuse Program. We offer both Residential Therapeutic Community models and intensive outpatient programs. We also offer drug and alcohol use education/DWI programs at some of our locations. Our goal in providing substance use treatment is to stimulate internal motivation for change and progress through the stages of change so that lasting behavioral alterations can occur. Our drug and alcohol education programs help participants understand their relationships with drugs and the links between drug use and crime, as well as assisting them in making better choices that can lead to healthier relationships in their lives. In 2017, 1,839 offenders completed substance use disorder programming.

Additional program offerings include our Victim Impact Programs, available at a number of our facilities, which seek to educate offenders about the negative effects their criminal conduct can have on others. In 2017, seven facilities received training to offer Victim Impact Programs to offenders in both secure and community sites. In addition, in 2017, 455 offenders successfully completed Victim Impact Programs. All of our facilities offer opportunities for worship and/or study for a wide range of faith traditions represented in our populations. Additionally, in many facilities, we offer faith-based programs, with an emphasis on reentry, character development, and spiritual growth. During 2017, we transitioned to the Threshold Program, or RDAP, with proven clinical outcomes. a multi-faith, evidence-based model, for our faith-based reentry component.

Our life skillsReentry and Life Skills programs prepare individuals for life after incarceration by teaching offendersthem how to successfully conduct a job search, how to manage their budget and financial matters, parenting skills, and relationship and family skills. Equally significant, we offer cognitive behavioral programs aimed at changing anti-social attitudes and behaviors ofin offenders, with a focus on altering the level of criminal thinking. We recently introduced a comprehensive reentry strategy we call "Go Further", a forward thinking, of offenders. Our Victim Impact Programs, available atsystems approach to reentry. "Go Further" embraces all facility reentry programs, adds a numberproprietary cognitive/behavioral curriculum, and encourages staff and offenders to take a collaborative approach to assist in reentry preparation. "Go Further" is currently in place in five of our facilities, seekwith plans to educate offenders on the negative effects upon others resulting from their criminal conduct. At a number of ouradd additional facilities we provide faith-based programs to those seeking spiritual growth and character development. Our facilities offer opportunities for religious worship and study for a variety of faith groups and belief systems. in 2018.

7

Across the country, these programs incorporateour dedicated staff, along with the useassistance of thousands of volunteers, along with our staff, who assist in providingwork to provide guidance, direction, and post-incarceration services to offenders.the men and women in our care. We believe, that together these effortscritical reentry programs help us achieve reductions in recidivism.fight the serious challenge of recidivism facing the United States.

Through our community corrections facilities, we provide an array of services to defendants and offenders who are serving their full sentence, the last portion of their sentence, waiting to be sentenced, or awaiting trial while supervised in a community environment. We also offer services for alternative sentencing options that provide governmental agencies and the courts the ability to place sentenced offenders in a community corrections facility thereby allowing them the opportunity to maintain their employment. We offer housing and programs with a key focus on employment, job readiness, and life skills and various substance abuse treatment programs, in order to help offenders successfully re-enter the communityreenter their communities and reduce the risk of recidivism.

In addition, in some of our community corrections facilities, we offer housing and program services to parolees who have completed their sentence but lack a viable reentry plan. Through a focus on employment and skill development, we provide a means for these parolees to successfully reintegrate into their communities.

Lastly, we provide day-reporting and outpatient substance abuse treatment programs at some of our community corrections facilities. These programs, depending on the needs of the offender, can provide cognitive behavioral-based programs to assist in the offender's successful reentry while holding the individual accountable while living in the community.

Ultimately, the work we do is about giving people the tools to reintegrate with their communities for good. We are proud of the teachers, counselors, case managers, chaplains, and other inmate support service professionals who provided these extensive services to the men and women entrusted in our care.

The American Correctional Association, or ACA, is an independent organization comprised of corrections professionals that establishes accreditation standards for correctional and detention institutions. Outside agency standards, such as those established by the ACA, provide us with the industry’sindustry's most widely accepted operational guidelines. ACA accredited facilities must be audited and re-accredited at least every three years. We have sought and received ACA accreditation for 4735, or approximately 90%, of the eligible facilities we operated as of December 31, 2014.2017, excluding our residential reentry facilities. During 2017, nine of the facilities we manage were re-accredited by the ACA with an average score of 99.4%, making our portfolio average 99.5%.

Beyond the standards provided by the ACA, our facilities are operated in accordance with a variety of company and facility-specific policies and procedures, as well as various contractual requirements. TheseMany of these policies and procedures reflect the high standards generated by a number of sources, including the ACA, The Joint Commission, the National Commission on Correctional Healthcare, the Occupational Safety and Health Administration, as well as federal, state, and local government codes and regulations establishedand longstanding correctional procedures, and company-wide policies and procedures that may exceed these guidelines.procedures.

In addition, our facilities are operated in compliance with the Prison Rape Elimination Act, or PREA, regulations were published in June 2012 andstandards, which became effective in August 2013. All confinement facilities covered under the PREA standards must be audited at least every three years to be considered compliant with the PREA standards, with one-third of each facility type operated by an agency, or private organization on behalf of an agency, audited each year. ThesePREA. Covered facilities include adult prisons and jails, juvenile facilities, lockups (housing detainees overnight), and community confinement facilities, whether operated by the United States Department of Justice, or unit ofDOJ, or by a state, local, corporate, or nonprofit authority.We utilize DOJ-certified PREA auditors to help ensure that all facilities operate in compliance with applicable PREA regulations.

7

Our facilities not only operate under these established standards, policies, and procedures, but theyand also are consistently challengedsubject to annual audits by our management to exceed them. This challenge is presented, in large part, through our extensive Quality Assurance Program. Our Quality Assurance Division, or QAD, independentlywhich operates under the auspices of, and reports directly to, our Office of General Counsel. WeCounsel and independently from our Operations Division. Through the QAD, we have devoted significant resources to meetingensuring that our facilities meet outside agency and accrediting organization standards and guidelines. Our QAD provides governance for all efforts by our facilities to deliver high quality services and operations, with a commitment to continuous quality improvement.

The QAD collects and analyzes performance metrics across multiple databases. Through rigorous reporting and analyses of comprehensive, comparative statistics across disciplines, divisions, business units and our company as a whole, the QAD provides timely, independently generated performance and trend data to senior management.

The QAD also employs a team of full-time auditors, who are subject matter experts from all major disciplines within institutional operations. Annually, without advance notice, theseQAD auditors conduct rigorous, on siteon-site evaluations of each facility we operate. Theoperate using specialized audit tools, typically containing more than 1,000 audit indicators across all major operational areas. In most instances, these audit tools are tailored to facility and partner specific

8

requirements. In addition, audit teams use highly specialized, discipline-specific audit tools, containing over 1,600 audited items across fourteen major operational areas, in this detailed, comprehensive process. The results of these on-site evaluations are used to discern areas of operational strength and areas in need of management attention. The audit findings also comprise a major part of our continuous operational risk assessment and management process. Audit teams are also made available tooften work with facilities into address specific areas of need, such as meeting requirements of new partner contracts or providing detailed training of new departmental managers.

The QAD management team coordinates overall operational auditing and compliance efforts across all CCA facilities.correctional, detention, and residential reentry facilities we manage. In conjunction with subject matter experts and other stakeholders having risk management responsibilities, the QAD management team develops performance measurement tools used in facility audits. The QAD management team also provides governance of the corporatecorrective action plan process for any items of action process which helps to ensure swift resolution of issuesnonconformance identified through internal and external facility reviews. Our QAD also contracts with teams of seasoned, ACA certified correctional auditors to help ensure continuousevaluate compliance with ACA standards at accredited facilities and to help ensure that our facilities are operating at the highest possible levels.facilities. Similarly, the QAD coordinates the workroutinely incorporates a review of certified PREA auditors to help ensure that all facilities operate infacility compliance with these important regulations.key PREA regulations during audits of company facilities.

Prisoner Transportation Services

We currently provide transportation services to governmental agencies through our wholly-owned TRS, TransCor America, LLC, or TransCor. During the years ended December 31, 2014, 2013, and 2012, TransCor generated total revenue of $4.4 million, $2.7 million, and $2.5 million, respectively, or approximately 0.3% of our total consolidated revenue in 2014 and 0.2% in both 2013 and 2012. We believe TransCor provides a complementary service to our core business that enables us to respond quickly to our customers’ transportation needs.

8

We are currently the nation’s largest owner and provider of outsourced correctional facilities and management services. We believe we manage nearly 41% of all beds under contract with private operators of correctional and detention facilities in the United States, most of which are in facilities we own and provide to our governmental customers. We believe we own approximately 61%58% of all privately owned prison beds in the United States.States, manage nearly 39% of all privately managed prison beds in the United States, and are currently the second largest private owner and provider of community corrections services in the nation. We also believe that we are the largest private owner of real estate used by government agencies. Under the direction of our partnership development department, and senior management, we market our facilities and services to government agencies responsible for federal, state, and local correctional, detention, and detentionresidential reentry facilities in the United States. Under the direction of our strategic developmentreal estate department, we pursue asset acquisitionsintend to continue pursuing the acquisition and development of additional correctional, detention, and residential reentry facilities, as well as other government-leased real estate assets with a bias toward those used to provide mission-critical governmental services that we believe have a favorable investment return, diversify our cash flows, and increase value to our stockholders.

We execute cross-departmental efforts to market CoreCivic Safety solutions to government partners that seek corrections and detention management services, CoreCivic Properties solutions to customers that need real estate and maintenance services, and CoreCivic Community solutions to government partners seeking residential reentry services. We also offer government partners a combination of these business combination transactions.offerings, and currently have two government partners utilizing all three.

As indicated by the following chart, business from our federal customers, including primarily the BOP, USMS, and ICE, continues to be a significant component of our business. The BOP, USMS, and ICE were the only federal partners that accounted for 10% or more of our total revenue during the last three years.

Certain of our contracts with federal partners contain “take-or-pay” clauses that guarantee the federal partner access to a minimum bed capacity in exchange for a fixed monthly payment. However, these contracts also generally provide the government the ability to cancel the contract for non-appropriation of funds or for convenience.

BusinessThe decline in federal revenue from 2016 to 2017 was primarily a result of an amendment to the inter-governmental service agreement, or IGSA, associated with our South Texas Family Residential Center, which became effective in the fourth quarter of 2016. See "Management's Discussion and Analysis of Financial Condition and Results of

9

Operations - Results of Operations" for a further discussion regarding our contract at the South Texas Family Residential Center. In addition, populations in federal facilities, particularly within the BOP system nationwide, have declined over the past three years. Inmate populations in the BOP system declined due, in part, to the retroactive application of changes to sentencing guidelines applicable to certain federal drug trafficking offenses.

Despite this decline, we continue to believe utilization of private sector bed capacity and management services provides our federal partners with flexible and cost-effective solutions essential to their missions. For example, in November 2016, we announced that the BOP exercised a two-year renewal option at our 1,978-bed McRae Correctional Facility. The amended agreement commenced on December 1, 2016, and provides for caring for up to 1,724 federal inmates with a fixed monthly payment for 1,633 beds, compared to our previous contract which contained a fixed payment for 1,780 beds. In addition, in July 2017, the BOP exercised a two-year renewal option at our 2,232-bed Adams County Correctional Center. For the year ended December 31, 2017, we generated 5% of our total revenue through the remaining contracts with the BOP at these two correctional facilities.

Further, we believe our ability to provide flexible solutions and fulfill emergent needs of ICE would be very difficult and costly to replicate in the public sector, demonstrated by the contract with ICE at our 2,400-bed South Texas Family Residential Center, which was amended and extended in October 2016. The October 2016 amendment extended the term of the contract through September 2021 and can be further extended by bi-lateral modification. In addition, in December 2016, we announced a new award to provide detention capacity to ICE at our 2,016-bed Northeast Ohio Correctional Center, and in April 2017, we announced a new contract award to provide up to 996 beds to the state customers, whichof Ohio at this same facility. We previously housed inmates from the BOP at the Northeast Ohio facility under a contract that expired in May 2015. We believe these contracts provide further examples of the marketability of our real estate assets across multiple government customers.

State revenues from contracts at correctional, detention, and residential reentry facilities that we operate constituted 48%41%, 49%38%, and 49%40% of our total revenue during the years 2014, 2013,2017, 2016, and 2012,2015, respectively, decreased 4.2%and increased 2.4% from $826.1$710.4 million during 20132016 to $791.8$727.8 million during 2014. The State2017. Approximately 6%, 6%, and 10% of our total revenue for 2017, 2016, and 2015, respectively, was generated from the California Department of Corrections and Rehabilitation, or CDCR, accounted for 14%, 12%, and 12%in facilities housing inmates outside the state of total revenue for 2014, 2013, and 2012, respectively, including revenue generated under an operating lease that commenced December 1, 2013, at our California City facility.California. The CDCR was our only state partner that accounted for 10% or more of our total revenue during these years.

Several of our state partners are projecting modest increases in tax revenues and improvements in their budgets which has resulted in our ability tohelped us secure recent per diem increases at certain facilities. Further, several of our existing state partners, as well as prospective state partners, are experiencing growth in inmate populations and overcrowded conditions. Although we can provide no assurance that we will enter into any new contracts, we believe we are well positioned to provide them with needed bed capacity, as well as the programming and reentry services they are seeking.

We believe the long-term growth opportunities of our business remain very attractive as certain statesgovernments consider efficiency and savingstheir emergent needs, as well as the efficiency and offender programming opportunities we can provide, as a toolflexible solutions to reduce recidivism.satisfy our partners' needs. Further, we expect our partners to continue to face challenges in maintaining old facilities, and developing new facilities, and expanding current facilities for additional capacity, which could result in future demand for the solutions that we provide.

10

9

We believe that we can further develop our business by, among other things:

Maintaining and expanding our existing customer relationships and continuing to fillfilling existing beds within our facilities, while maintaining an adequate inventory of available beds that we believe provides us with flexibility and a competitive advantage when bidding for new management contracts;

Pursuing mission-critical real estate solutions for government agencies including, but not limited to, corrections and detention real estate assets;

Pursuing other asset acquisitions and business combinations through transactions with non-government third parties;

We generally receive inquiries from or on behalf of government agencies that are considering outsourcing the ownership and/or management of certain facilities or that have already decided to contract with a private enterprise. When we receive such an inquiry, we determine whether there is an existing need for our correctional, detention, and residential reentry facilities and/or services and whether the legal and political climate in which the inquiring party operates is conducive to serious consideration of outsourcing. Based on these findings, an initial cost analysis is conducted to further determine project feasibility.

Frequently, government agencies responsible for correctional, detention, and detentionresidential reentry facilities and services procure space and services through solicitations or competitive procurements. As part of our process of responding to such requests, members of our management team meet with the appropriate personnel from the agency making the request to best determine the agency’sagency's needs. If the project fits within our strategy, we submit a written response. A typical solicitation or competitive procurement requires bidders to provide detailed information, including, but not limited to, the space and services to be provided by the bidder, its experience and qualifications, and the price at which the bidder is willing to provide the facility and services (which services may include the purchase, renovation, improvement or expansion of an existing facility or the planning, design and construction of a new facility). The requesting agency selects a firm believed to be able to provide the requested bed capacity, if needed, and most qualified to provide the requested services and then negotiates the price and terms of the contract with that firm.

11

In 2017, we entered into a number of new contracts, renewed several other significant contracts, and completed numerous other transactions and milestones, including the following:

Completed the acquisition of Arapahoe Community Treatment Center, a 135-bed residential reentry center in Colorado.

Completed the acquisition of the Stockton Female Community Corrections Facility, a 100-bed residential reentry center in California, which is leased to a third-party operator. The lessee separately contracts with the CDCR.

Announced a new contract with the state of Ohio to care for up to an additional 996 offenders at our 2,016-bed Northeast Ohio Correctional Center. The initial term of the contract continues through June 2032 with unlimited renewal options, subject to appropriations and mutual agreement.

Completed the acquisition of the real estate operated by Center Point, Inc., or Center Point, a California-based non-profit organization. We consolidated a portion of Center Point's operations into our preexisting residential reentry center portfolio and assumed ownership and operations of a 200-bed residential reentry center in Oklahoma.

Executed a new three-year contract with the City of Mesa, Arizona to care for up to 200 offenders at our 4,128-bed Central Arizona Florence Correctional Complex.

Completed the acquisition of New Beginnings Treatment Center, Inc., an Arizona-based community corrections company. In connection with the acquisition, we assumed a contract with the BOP to provide reentry services at a 92-bed residential reentry center in Arizona.

Completed the acquisition of a portfolio of four properties, including a 230-bed residential reentry center leased to the state of Georgia and three properties in North Carolina and Georgia leased to the General Services Administration, or GSA, an independent agency of the United States government, two of which are occupied by the Social Security Administration, or SSA, and one of which is occupied by the Internal Revenue Service, or IRS.

Completed the offering of $250.0 million principal amount of unsecured notes with a fixed stated interest rate of 4.75%, due October 15, 2027. We used net proceeds from the offering, after underwriter's fees and offering expenses, to pay down a portion of our revolving credit facility, reducing our exposure to variable rate debt, extending our weighted average maturity, and increasing the availability of borrowings under our revolving credit facility that is used to fund growth opportunities that require capital deployment.

Executed a new contract with the state of Nevada to care for up to 200 offenders at our 1,896-bed Saguaro Correctional Facility in Arizona.

Launched a nationwide initiative to advocate for a range of government policies that will help former inmates successfully reenter society and stay out of prison. We also committed to a series of accountability measures, including publicly reporting related advocacy activities on an annual basis and making support for recidivism-reducing policies one of our criteria for evaluating political contributions.

Completed the acquisition of Time to Change, Inc., a Colorado-based community corrections company. In connection with the acquisition, we assumed contracts to provide residential reentry services in three facilities located in Colorado containing a total of 422 beds.

Announced a new contract with Hamilton County, Tennessee to continue management, operation, and maintenance of the 1,046-bed Silverdale Detention Center. The initial term of the new contract is four years, renewable for four additional four-year periods.

Announced a new contract with the Commonwealth of Kentucky Department of Corrections to house medium and close-security offenders at our previously idled 816-bed Lee Adjustment Center in Kentucky. The contract commenced on November 19, 2017, and has an initial term expiring June 30, 2019, with two additional one-year extension options.

12

General

Our correctional, detention, and residential reentry facilities can generally be classified according to the level(s) of security at such facility. Secure facilities are facilities having cells, rooms, or dormitories, a secure perimeter, and some form of external patrol. Non-secure facilities are facilities having open housing that

10

inhibit movement by their design. Minimum security facilities have open housing within an appropriately designed and patrolled institutional perimeter. Medium security facilities have either cells, rooms or dormitories, a secure perimeter, and some form of external patrol. Maximum security facilities have cells, a secure perimeter, and external patrol. Multi-security facilities have various areas encompassing minimum, medium or maximum security.

Our facilities can also be classified according to their primary function. The primary functional categories are:

Correctional Facilities. Correctional facilities house and provide contractually agreed upon programs and services to sentenced adult prisoners, typically prisoners on whom a sentence in excess of one year has been imposed.

Detention Facilities. Detention facilities house and provide contractually agreed upon programs and services to (i) individuals being detained by ICE, (ii) individuals who are awaiting trial who have been charged with violations of federal criminal law (and are therefore in the custody of the USMS) or state criminal law, and (iii) prisoners who have been convicted of crimes and on whom a sentence of one year or less has been imposed.

Residential Facilities. Residential facilities provide space and residential services in an open and safe environment to adults with children who have been detained by ICE and are awaiting the outcome of immigration hearings or the return to their home countries. As contractually agreed upon, residential facilities offer services including, but not limited to, educational programs, medical care, recreational activities, counseling, and access to religious and legal services.

Community Corrections. Community corrections/residential reentry facilities offer housing and programs to offenders who are serving the last portion of their sentence or who have been assigned to the facility in lieu of a jail or prison sentence, with a key focus on employment, job readiness, and life skills.

Leased Facilities. Leased facilities are properties that are owned and leased to third parties and used by government agencies.

13

Facilities and Facility Management Contracts

As of December 31, 2014,2017, we owned or controlled 52and managed 70 correctional, detention, and residential reentry facilities, and managed an additional seven correctional and detention facilities in 16 states and the Districtowned by our government partners. In addition, as of Columbia, three of whichDecember 31, 2017, we owned 12 properties leased to third-party operators. Additionally, we managed 12 correctionalthird parties and detention facilities ownedused by government agencies. We also owned two corporate office buildings. Owned and managed facilities include facilities placed into service that we own or control via a long-term lease and manage. Managed-only facilities include facilities we manage that are owned by a third party. The segment disclosures are included in Note 16 of the Notes to the Consolidated Financial Statements.government authority. The following table sets forth all of the facilities that, as of December 31, 2014,2017, we (i) owned and managed, (ii) owned, but were leased to another operator,a third party, and (iii) managed but are owned by a government authority. The table includes certain information regarding each facility, including the term of the primary customer contract related to such facility, or, in the case of facilities we owned but leased to a third-party operator, the term of such lease.

11

Facility Name | Primary | Design Capacity (A) | Security Level | Facility Type (B) | Term | Remaining Renewal (C) | ||||||||||||||||||

Owned and Managed Facilities: | ||||||||||||||||||||||||

Central Arizona Florence Correctional Complex | USMS | 4,128 | Multi | Detention | Sep-18 | (2) 5 year | ||||||||||||||||||

Florence, Arizona | ||||||||||||||||||||||||

Eloy Detention Center | ICE | 1,500 | Medium | Detention | Indefinite | — | ||||||||||||||||||

Eloy, Arizona | ||||||||||||||||||||||||

| ||||||||||||||||||||||||

La Palma Correctional Center | State of California | 3,060 | Multi | Correctional | Jun-19 | Indefinite | ||||||||||||||||||

Eloy, Arizona | ||||||||||||||||||||||||

Oracle Transitional Center | BOP | 92 | — | Community | Feb-18 | (1) 1 year | ||||||||||||||||||

Tucson, Arizona | Corrections | |||||||||||||||||||||||

Red Rock Correctional Center (D) | State of Arizona | 2,024 | Medium | Correctional | Jul-26 | (2) 5 year | ||||||||||||||||||

Eloy, Arizona | ||||||||||||||||||||||||

Saguaro Correctional Facility | State of Hawaii | 1,896 | Multi | Correctional | Jun-19 | (2) 1 year | ||||||||||||||||||

Eloy, Arizona | ||||||||||||||||||||||||

CAI Boston Avenue | State of California | 120 | — | Community | Jun-18 | (3) 1 year | ||||||||||||||||||

San Diego, California | Corrections | |||||||||||||||||||||||

CAI Ocean View | BOP | 483 | — | Community | May-18 | (3) 1 year | ||||||||||||||||||

San Diego, California | Corrections | |||||||||||||||||||||||

Leo Chesney Correctional Center | — | 240 | — | — | — | — | ||||||||||||||||||

Live Oak, California | ||||||||||||||||||||||||

Otay Mesa Detention Center | ICE | 1,482 | Minimum/ | Detention | Jun-20 | (1) 3 year | ||||||||||||||||||

San Diego,

| Medium | |||||||||||||||||||||||

Adams Transitional Center | Adams County | 102 | — | Community | Jun-18 | — | ||||||||||||||||||

Denver, Colorado | Corrections | |||||||||||||||||||||||

Arapahoe Community Treatment Center | Arapahoe County | 135 | — | Community Corrections | Jun-18 | — | ||||||||||||||||||

Englewood, Colorado | ||||||||||||||||||||||||

Bent County Correctional Facility | State of Colorado | 1,420 | Medium | Correctional | Jun-18 | — | ||||||||||||||||||

Las Animas, Colorado | ||||||||||||||||||||||||

14

Facility Name | Primary Customer | Design Capacity (A) | Security Level | Facility Type (B) | Term | Remaining Renewal Options (C) | ||||||||||||||||||

Center | Boulder County | 69 | — | Community Corrections | Dec-18 | — | ||||||||||||||||||

Boulder, Colorado | ||||||||||||||||||||||||

Centennial Community Transition Center | Arapahoe County | 107 | — | Community Corrections | Jun-18 | — | ||||||||||||||||||

Englewood, Colorado | ||||||||||||||||||||||||

Columbine Facility | Denver County | 60 | — | Community | Jun-18 | — | ||||||||||||||||||

Denver, Colorado | Corrections | |||||||||||||||||||||||

Commerce Transitional Center | Adams County | 136 | — | Community | Jun-18 | — | ||||||||||||||||||

Commerce City, Colorado | Corrections | |||||||||||||||||||||||

Crowley County Correctional Facility | State of Colorado | 1,794 | Medium | Correctional | Jun-18 | — | ||||||||||||||||||

Olney Springs, Colorado | ||||||||||||||||||||||||

Dahlia Facility | Denver County | 120 | — | Community | Jun-18 | — | ||||||||||||||||||

Denver, Colorado | Corrections | |||||||||||||||||||||||

Fox Facility and Training Center | Denver County | 90 | — | Community | Jun-18 | — | ||||||||||||||||||

Denver, Colorado | Corrections | |||||||||||||||||||||||

Henderson Transitional Center | Adams County | 184 | — | Community | Jun-18 | — | ||||||||||||||||||

Henderson, Colorado | Corrections | |||||||||||||||||||||||

Huerfano County Correctional Center | — | 752 | Medium | Correctional | — | — | ||||||||||||||||||

Walsenburg, Colorado | ||||||||||||||||||||||||

Kit Carson Correctional Center | — | 1,488 | Medium | Correctional | — | — | ||||||||||||||||||

Burlington, Colorado | ||||||||||||||||||||||||

Longmont Community Treatment Center | Boulder County | 69 | — | Community Corrections | Dec-18 | — | ||||||||||||||||||

Longmont, Colorado | ||||||||||||||||||||||||

Ulster Facility | Denver County | 90 | — | Community | Jun-18 | — | ||||||||||||||||||

Denver, Colorado | Corrections | |||||||||||||||||||||||

Coffee Correctional Facility | State of Georgia | 2,312 | Medium | Correctional | Jun-18 | (16) 1 year | ||||||||||||||||||

Nicholls, Georgia | ||||||||||||||||||||||||

Jenkins Correctional Center | State of Georgia | 1,124 | Medium | Correctional | Jun-18 | (17) 1 year | ||||||||||||||||||

Millen, Georgia | ||||||||||||||||||||||||

McRae Correctional Facility | BOP | 1,978 | Medium | Correctional | Nov-18 | (2) 2 year | ||||||||||||||||||

McRae, Georgia | ||||||||||||||||||||||||

Stewart Detention Center | ICE | 1,752 | Medium | Detention | Indefinite | — | ||||||||||||||||||

Lumpkin, Georgia | ||||||||||||||||||||||||

Wheeler Correctional Facility | State of Georgia | 2,312 | Medium | Correctional | Jun-18 | (16) 1 year | ||||||||||||||||||

Alamo, Georgia | ||||||||||||||||||||||||

15

Facility Name | Primary Customer | Design Capacity (A) | Security Level | Facility Type (B) | Term | Remaining Renewal Options (C) | ||||||||||||||||||

Leavenworth Detention Center | USMS | 1,033 | Maximum | Detention | Dec-21 | (1) 5 year | ||||||||||||||||||

Leavenworth, Kansas | ||||||||||||||||||||||||

Lee Adjustment Center | Commonwealth of | 816 | Multi | Correctional | Jun-19 | (2) 1 year | ||||||||||||||||||

Beattyville, Kentucky |

| Kentucky | ||||||||||||||||||||||

12

| |||||||||||||||||||||||||||||||

Marion Adjustment Center | — | 826 | Minimum/ | Correctional | — | — | |||||||||||||||||||||||||

St. Mary, Kentucky | Medium | ||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||

Southeast Kentucky Correctional Facility (F) | — | 656 | Minimum/ Medium | Correctional | — | — | |||||||||||||||||||||||||

Wheelwright, Kentucky |

| ||||||||||||||||||||||||||||||

Prairie Correctional Facility | — | 1,600 | Medium | Correctional | — | — | |||||||||||||||||||||||||

Appleton, Minnesota | |||||||||||||||||||||||||||||||

Adams County Correctional Center | BOP | 2,232 | Medium | Correctional | Jul-19 | — | |||||||||||||||||||||||||

Adams County, Mississippi | |||||||||||||||||||||||||||||||

Tallahatchie County Correctional Facility | State of California | 2,672 | Multi | Correctional | Jun-19 | Indefinite | |||||||||||||||||||||||||

Tutwiler, Mississippi |

| ||||||||||||||||||||||||||||||

Crossroads Correctional Center | State of Montana | 664 | Multi | Correctional | Jun-17 | (1) 2 year | |||||||||||||||||||||||||

Shelby, Montana |

| ||||||||||||||||||||||||||||||

Nevada Southern Detention Center | USMS | 1,072 | Medium | Detention | Sep-20 | (2) 5 year | |||||||||||||||||||||||||

Pahrump, Nevada | |||||||||||||||||||||||||||||||

Elizabeth Detention Center | ICE | 300 | Minimum | Detention | Aug-18 | (3) 1 year | |||||||||||||||||||||||||

Elizabeth, New Jersey | |||||||||||||||||||||||||||||||

Cibola County Corrections Center | ICE | 1,129 | Medium | Detention | Oct-21 | Indefinite | |||||||||||||||||||||||||

Milan, New Mexico | |||||||||||||||||||||||||||||||

Northwest New Mexico Correctional | State of New Mexico | 596 | Multi | Correctional | Jun-20 | — | |||||||||||||||||||||||||

Grants, New Mexico |

| ||||||||||||||||||||||||||||||

Torrance County Detention Facility | — | 910 | Multi | Detention | — | — | |||||||||||||||||||||||||

Estancia, New Mexico | |||||||||||||||||||||||||||||||

Lake Erie Correctional Institution | State of Ohio | 1,798 | Medium | Correctional | Jun-32 | Indefinite | |||||||||||||||||||||||||

Conneaut, Ohio | |||||||||||||||||||||||||||||||

Northeast Ohio Correctional Center | State of Ohio | 2,016 | Medium | Correctional | Jun-32 | Indefinite | |||||||||||||||||||||||||

Youngstown, Ohio | |||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||

Carver Transitional Center | State of Oklahoma | 494 | — | Community | Jun-18 | (4) 1 year | |||||||||||||||||||||||||

Oklahoma City, Oklahoma | Corrections | ||||||||||||||||||||||||||||||

16

Facility Name | Primary Customer | Design Capacity (A) | Security Level | Facility Type (B) | Term | Remaining Renewal Options (C) | ||||||||||||||||||

State of Oklahoma | 1,692 | Multi | Correctional | Jun-18 | (1) 1 year | |||||||||||||||||||

Cushing, Oklahoma | ||||||||||||||||||||||||

Davis Correctional Facility | State of Oklahoma | 1,670 | Multi | Correctional | Jun-18 | (1) 1 year | ||||||||||||||||||

Holdenville, Oklahoma | ||||||||||||||||||||||||

Diamondback Correctional Facility | — | 2,160 | Multi | Correctional | — | — | ||||||||||||||||||

Watonga, Oklahoma | ||||||||||||||||||||||||

| ||||||||||||||||||||||||

Oklahoma City Transitional

| State of Oklahoma | 200 | — | Community Corrections | Jun-18 | |||||||||||||||||||

(4) 1 year | ||||||||||||||||||||||||

| ||||||||||||||||||||||||

Tulsa Transitional Center | State of Oklahoma | 390 | — | Community | Jun-18 | (4) 1 year | ||||||||||||||||||

Tulsa, Oklahoma | Corrections | |||||||||||||||||||||||

Turley Residential Center | State of Oklahoma | 289 | — | Community | Jun-18 | (4) 1 year | ||||||||||||||||||

Tulsa, Oklahoma | Corrections | |||||||||||||||||||||||

Shelby Training Center | — | 200 | — | — | — | — | ||||||||||||||||||

Memphis, Tennessee | ||||||||||||||||||||||||

13

| ||||||||||||||||||||||||

Trousdale Turner Correctional Center | State of Tennessee | 2,552 | Multi | Correctional | Jan-21 | — | ||||||||||||||||||

Hartsville, Tennessee | ||||||||||||||||||||||||

West Tennessee Detention Facility | USMS | 600 | Multi | Detention | Sep-19 | (5) 2 year | ||||||||||||||||||

Mason, Tennessee | ||||||||||||||||||||||||

Whiteville Correctional Facility | State of Tennessee | 1,536 | Medium | Correctional | Jun-21 | — | ||||||||||||||||||

Whiteville, Tennessee | ||||||||||||||||||||||||

Austin Residential Reentry Center | BOP | 116 | — | Community | Feb-18 | — | ||||||||||||||||||

Del Valle, Texas | Corrections | |||||||||||||||||||||||

Austin Transitional Center | State of Texas | 460 | — | Community | Aug-18 | (2) 1 year | ||||||||||||||||||

Del Valle, Texas | Corrections | |||||||||||||||||||||||

Corpus Christi Transitional Center | State of Texas | 160 | — | Community Corrections | Aug-19 | — | ||||||||||||||||||

Corpus Christi, Texas | ||||||||||||||||||||||||

Dallas Transitional Center | State of Texas | 300 | — | Community | Aug-18 | (2) 1 year | ||||||||||||||||||

Hutchins, Texas | Corrections | |||||||||||||||||||||||

Eden Detention Center | — | 1,422 | Medium | Correctional | — | — | ||||||||||||||||||

Eden, Texas | ||||||||||||||||||||||||

El Paso Multi-Use Facility | State of Texas | 360 | — | Community | Aug-18 | (2) 1 year | ||||||||||||||||||

El Paso, Texas | Corrections | |||||||||||||||||||||||

17

Facility Name | Primary Customer | Design Capacity (A) | Security Level | Facility Type (B) | Term | Remaining Renewal Options (C) | |||||||||||||||||||||||||

El Paso, Texas | State of Texas | 224 | — | Community Corrections | Aug-18 | (2) 1 year | |||||||||||||||||||||||||

Fort Worth Transitional Center | State of Texas | 248 | — | Community | Aug-18 | (2) 1 year | |||||||||||||||||||||||||

Fort Worth, Texas | Corrections | ||||||||||||||||||||||||||||||

Houston Processing Center | ICE | 1,000 | Medium | Detention | Apr-18 | (5) 2 month | |||||||||||||||||||||||||

Houston, Texas | |||||||||||||||||||||||||||||||

Laredo Processing Center | ICE | 258 | Minimum/ | Detention | Jun-18 | — | |||||||||||||||||||||||||

Laredo, Texas | Medium | ||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||

South Texas Family Residential Center |

| ICE | 2,400 | — | Residential | Sep-21 | — | ||||||||||||||||||||||||

Dilley, Texas | |||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||

T. Don Hutto Residential Center | ICE | 512 | Medium | Detention | Jan-20 | Indefinite | |||||||||||||||||||||||||

Taylor, Texas | |||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||

Webb County Detention Center |

| USMS | 480 | Medium | Detention | Feb-18 | — | ||||||||||||||||||||||||

Laredo, Texas | |||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||

Cheyenne Transitional Center | State of Wyoming | 116 | — | Community | Jun-18 | Indefinite | |||||||||||||||||||||||||

Cheyenne, Wyoming | Corrections | ||||||||||||||||||||||||||||||

Managed Only Facilities: | |||||||||||||||||||||||||||||||

Citrus County Detention Facility | Citrus County, FL | 760 | Multi | Detention | Sep-20 | Indefinite | |||||||||||||||||||||||||

Lecanto, Florida | |||||||||||||||||||||||||||||||

Lake City Correctional Facility | State of Florida | 893 | Medium | Correctional | Jun-18 | Indefinite | |||||||||||||||||||||||||

Lake City, Florida |

| ||||||||||||||||||||||||||||||

Marion County Jail | Marion County, IN | 1,030 | Multi | Detention | Dec-27 | — | |||||||||||||||||||||||||

Indianapolis, Indiana | |||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||

Hardeman County Correctional Facility | State of Tennessee | 2,016 | Medium | Correctional | May-18 | — | |||||||||||||||||||||||||

Whiteville, Tennessee | |||||||||||||||||||||||||||||||

Metro-Davidson County Detention Facility | Davidson County, TN | 1,348 | Multi | Detention | Jan-20 | — | |||||||||||||||||||||||||

Nashville, Tennessee | |||||||||||||||||||||||||||||||

Silverdale Facilities | Hamilton County, | 1,046 | Multi | Detention | Sep-21 | (4) 4 year | |||||||||||||||||||||||||

Chattanooga, Tennessee | TN | ||||||||||||||||||||||||||||||

South Central Correctional Center | State of Tennessee | 1,676 | Medium | Correctional | Jun-18 | — | |||||||||||||||||||||||||

Clifton, Tennessee | |||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||

|

|

| |||||||||||||||||||||||||||||

|

|

| |||||||||||||||||||||||||||||

|

|

| |||||||||||||||||||||||||||||

18

| Primary Customer |

| Design Capacity (A) |

|

| Square Footage |

|

| Property Type (B) |

| Term |

| Remaining Renewal Options (C) | |||

Leased Properties: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

California City Correctional Center |

| State of California |

|

| 2,560 |

|

|

| 522,000 |

|

| Correctional |

| Nov-20 |

| Indefinite |

California City, California |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Long Beach Community Corrections Center |

| The GEO Group, Inc. |

| 112 |

|

|

| 16,000 |

|

| Community Corrections |

| Jun-20 |

| (1) 5 year | |

Long Beach, California |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stockton Female Community Corrections Facility |

| WestCare California, Inc. |

| 100 |

|

|

| 15,000 |

|

| Community Corrections |

| Apr-21 |

| (1) 5 year | |

Stockton, California |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Augusta Transitional Center |

| Georgia Department |

| 230 |

|

|

| 29,000 |

|

| Community |

| Jun-18 |

| (5) 1 year | |

Augusta, Georgia |

| of Corrections |

|

|

|

|

|

|

|

|

| Corrections |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Milledgeville |

| GSA - Social Security |

| - |

|

|

| 9,000 |

|

| Government- |

| Jan-20 |

| - | |

Milledgeville, Georgia |

| Administration |

|

|

|

|

|

|

|

|

| Leased |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Greenville |

| GSA - Internal |

| - |

|

|

| 13,000 |

|

| Government- |

| Mar-24 |

| - | |

Greenville, North Carolina |

| Revenue Service |

|

|

|

|

|

|

|

|

| Leased |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rockingham |

| GSA - Social Security |

| - |

|

|

| 8,000 |

|

| Government- |

| Mar-25 |

| - | |

Rockingham, North Carolina |

| Administration |

|

|

|

|

|

|

|

|

| Leased |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

North Fork Correctional Facility |

| State of Oklahoma |

|

| 2,400 |

|

|

| 466,000 |

|

| Correctional |

| Jul-21 |

| Indefinite |

Sayre, Oklahoma |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Broad Street Residential Reentry Center |

| The GEO Group, Inc. |

|

| 150 |

|

|

| 18,000 |

|

| Community Corrections |

| Jul-19 |

| (4) 5 year |

Philadelphia, Pennsylvania |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Chester Residential Reentry Center |

| The GEO Group, Inc. |

|

| 135 |

|

|

| 18,000 |

|

| Community |

| Jul-19 |

| (4) 5 year |

Chester, Pennsylvania |

|

|

|

|

|

|

|

|

|

|

| Corrections |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Roth Hall Residential Reentry Center |

| The GEO Group, Inc. |

| 160 |

|

|

| 18,000 |

|

| Community Corrections |

| Jul-19 |

| (4) 5 year | |

Philadelphia, Pennsylvania |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Walker Hall Residential Reentry Center |

| The GEO Group, Inc. |

| 160 |

|

|

| 18,000 |

|

| Community Corrections |

| Jul-19 |

| (4) 5 year | |

Philadelphia, Pennsylvania |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14

| (A) | |||||||||||||

|

|

| ||||||||||||

| ||||||||||||||

| ||||||||||||||

| ||||||||||||||

| ||||||||||||||

| Design capacity measures the number of beds, and accordingly, the number of offenders each facility is designed to accommodate. Facilities housing detainees on a |

(B) | We manage numerous facilities that have more than a single function |

(C) | Remaining renewal options represents the number of renewal options, if applicable, and the term of each option renewal. |

(D) | Pursuant to the terms of a contract awarded by the state of Arizona in September 2012, the state of Arizona has an option to purchase the Red Rock facility at any time during the term of the contract, including extension options, based on an amortization schedule starting with the fair market value and decreasing evenly to zero over the |

(E) | These facilities are subject to purchase options held by the Georgia Department of Corrections, or GDOC, which grants the GDOC the right to purchase the facility for the lesser of the |

(F) | The facility is subject to a deed of conveyance with the city of Wheelwright, Kentucky which includes provisions that would allow assumption of ownership by the city of Wheelwright under the following occurrences: (1) we cease to operate the facility for more than two years, (2) our failure to maintain at least one employee for a period of sixty consecutive days, or (3) a conversion to a maximum security facility based upon classification by the Kentucky Corrections Cabinet. |

(G) | The facility is subject to a purchase option held by the Tallahatchie County Correctional Authority which grants Tallahatchie County Correctional Authority the right to purchase the facility at any time during the contract at a price generally equal to the cost of the premises less an allowance for amortization originally over a |

(H) | The state of Montana has an option to purchase the facility generally at any time during the term of the contract with us at fair market value less the sum of a pre-determined portion of |

(I) | The state of Ohio has the irrevocable right to repurchase the facility before we may resell the facility to a third party, or if we become insolvent or are unable to meet our obligations under the management contract with the state of Ohio, at a price generally equal to the fair market |

15

(J) | These facilities are subject to purchase options held by the Oklahoma Department of Corrections, or |

(K) | The state of Tennessee has the option to purchase the facility in the event of our bankruptcy, or upon an operational or financial breach |

Facilities Under Construction or Development

As more fully described hereafter in “Management’s Discussion and Analysis of Financial Condition and Results of Operations, or MD&A, – Liquidity and Capital Resources”, we have three facilities under construction or development. The 1,492-bed Otay Mesa Detention Center is being constructed in San Diego, California, and is expected to be completed in the third quarter of 2015. We plan to offer the Otay Mesa facility to house the existing federal inmate populations at the San Diego Correctional Facility upon expiration of the ground lease at that facility on December 31, 2015. The 2,552-bed Trousdale Turner Correctional Center is being constructed in Trousdale County, Tennessee, and is expected to be completed in the fourth quarter of 2015. Under an agreement with Trousdale County, we expect the intake of inmate populations from the state of Tennessee to begin at this facility in the first quarter of 2016. We lease the South Texas Family Residential Center and the site upon which it is being constructed from a third-party lessor. In addition to the lease payments under the lease agreement, we are investing in certain leasehold improvements and furniture, fixtures, and equipment at the facility. We expect to complete these additions by the end of the second quarter of 2015 when the 2,400-bed South Texas facility is expected to be ready for full occupancy.20

WeUnder our three business offerings, CoreCivic Safety, CoreCivic Community, and CoreCivic Properties, we offer multiple solutions to unique challenges, allowing government organizations to address their various needs while customizing the solution based on their unique circumstances. Accordingly, we believe that we benefit from the following competitive strengths:

The First and Largest Private Prison Operator. Our recognition asOwner. Under our CoreCivic Safety platform, we are the nation’s leadingnation's largest private prison owner and operatorone of the largest prison operators in the United States, which provides us with significant credibility with our current and prospective clients. We believe we manage nearly 41%own approximately 58% of all privately managedowned prison beds in the United States. We believe we own approximately 61%States and manage nearly 39% of all privately ownedmanaged prison beds in the United States. We pioneered modern-day private prisons with a list of notable accomplishments, such as being the first company to design, build, and operate a private prison, the first company to manage a private maximum-security facility under a direct contract with the federal government, and, most recently, the first company to purchase a government-owned correctional facility from a governmental agency in the United States and to manage the facility for the government agency.agency, the first company to lease a private prison to a state government, and with an award from the state of Kansas in January 2018, we will be the first company to develop a privately-owned, build-to-suit correctional facility to be operated by a government agency through a long-term lease agreement. In addition to providing us with extensive experience and institutional knowledge, our size also helps us deliver value to our customers by providing purchasing power and allowing us to achieve certain economies of scale.

Available Beds within Our Existing Facilities.As of December 31, 2014,2017, we had approximately 6,0009,800 beds at five coreeight prison facilities that are vacant and immediately available to use. We consider our core facilities to be those that were designed for adult secure correctional purposes. We have staff throughout the organizationare actively engaged in

16

marketing this available capacity to existing and prospective customers. Historically, we have been successful in substantially filling our inventory of available beds and the beds that we have constructed. Filling these available beds wouldcould provide substantial growth in revenues, cash flow, and earnings per share. We expect the Commonwealth of Kentucky to utilize one of our previously idled prison facilities containing 816 beds beginning in the second quarter of 2018 pursuant to a new management contract we executed in November 2017.

Well-Established Community Corrections Platform. Under our CoreCivic Community and CoreCivic Properties platforms, we have a rapidly growing network of community corrections facilities we own and manage, as well as facilities we own and lease to third-party operators. Community corrections facilities offer housing and programs, with a key focus on employment, job readiness and life skills in order to help offenders successfully re-enter the community and reduce the risk of recidivism.

We are the second largest community corrections owner and operator in the United States, with 33 residential reentry centers containing a total of 6,261 beds. We believe this recognition provides us with a platform for further growth. We acquired eight residential reentry centers during 2017, which added an additional 1,179 beds to our existing residential reentry portfolio. See "2017 Accomplishments" for a summary of certain of our growth transactions completed during the year ended December 31, 2017. We acquired the residential reentry centers as strategic investments that further expand the network of reentry assets we own and the reentry services we provide. Acquisitions of residential reentry centers prior to 2017 include the following:

Acquisition of Correctional Management, Inc., or CMI, in April 2016 (7 facilities with 605 beds);

Acquisition of a residential reentry center in Long Beach, California in June 2016 (112 beds);

Acquisition of Avalon Correctional Services, Inc., or Avalon, in October 2015 (11 facilities with 3,157 beds);

Acquisition of four community corrections facilities in Pennsylvania in August 2015 (605 beds); and

Acquisition of Correctional Alternatives, Inc., or CAI, in July 2013 (2 facilities with 603 beds).

We believe the demand for the housing and programs that community corrections facilities offer will continue to grow as offenders are released from prison and due to an increased awareness of the important role these programs play in an offender's successful transition from prison to society. We expect to continue to pursue opportunities to acquire additional community corrections facilities in order to provide these services to parolees, defendants, and offenders who are serving their full sentence, the last portion of their sentence, waiting to be sentenced, awaiting

21

trial while supervised in a community environment, or as an alternative to incarceration. We also believe we have the opportunity to maximize utilization of available beds within our community corrections portfolio that would further increase the number of individuals benefiting from the services we provide in such facilities.

Attractive REIT Profile.Key characteristics of our business make us a highly attractive REIT. As of December 31, 2014,2017, we owned or controlled 52 correctional and detention82 facilities containing approximately 1414.8 million square feet which, for the year ended December 31, 2014,2017, generated 97%99% of our net operating income, or our operating income before general and administrative expenses, asset impairments, depreciation, and amortization. Land and buildings comprise overapproximately 90% of our gross fixed assets. These valuable assets are located in areas with high barriers to entry, particularly due to the unique permitting and zoning requirements for correctional and detentionthese facilities. Further, thesethe majority of our assets are constructed primarily of concrete and steel, generally requiring lower maintenance capital expenditures than other types of commercial properties.

Since our inception,We believe we have constructed dozensare the largest developer of facilities, manymission-critical, criminal justice center real estate projects over the past 15 years. We also believe we are the largest private owner of which we subsequently expanded.real estate used by government agencies. We provide space and services under contracts with federal, state, and local government agencies that generally have credit ratings of single-A or better. In addition, a majority of our contracts have terms between one and five years, and we have historically experienced customer retention in excess of 90%approximately 91%, which contributes to our relatively predictable and stable revenue base. This stream of revenue combined with our low maintenance capital expenditure requirement translates into steady, predictable cash flow. We believe the REIT structure also provides us with greater access to capital and flexibility to pursue growth opportunities.opportunities, and provides a high dividend yield to our shareholders compared with other investments.

DevelopmentFlexible Real Estate Solutions and Expansion Opportunities.Attractive Real Estate Portfolio. Under our CoreCivic Properties platform, we offer our customers an attractive portfolio of facilities that can be leased for various needs as an alternative to providing "turn-key" correctional, detention, and residential reentry bed space and services to our government partners. In May 2016, we entered into a lease with the ODOC for our previously idled 2,400-bed North Fork Correctional Facility. The demandlease agreement commenced on July 1, 2016, and includes a five-year base term with unlimited two-year renewal options. The lease of the North Fork facility, along with the lease of our California City Correctional Center to the CDCR originating in 2013, exemplify our ability to react quickly to our partners' needs with innovative and flexible solutions that make the best use of taxpayer dollars. We intend to pursue additional opportunities to lease prison facilities to government and other third-party operators in need of correctional capacity.