| Delaware | 26-0414014 | |

| (State of Incorporation) | (I.R.S. Employer Identification Number) | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

2018

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| Delaware | 26-0414014 | |

| (State of Incorporation) | (I.R.S. Employer Identification Number) | |

| Title of each class | Name of each exchange on which registered | |

| Common Stock, $0.01 par value | New York Stock Exchange | |

| Large accelerated filer | x | Accelerated filer | ||||

| Non-accelerated filer | Smaller reporting company | |||||

| Emerging growth company | ☐ | |||||

29, 2018.

| Page | ||||

| Item 1. | 3-16 | |||

| Item 1A. | 17-29 | |||

| Item 1B. | 30 | |||

| Item 2. | 30 | |||

| Item 3. | 30 | |||

| Item 4. | 30 | |||

| Item 5. | 31-32 | |||

| Item 6. | 33 | |||

| Item 7. | 34-49 | |||

| Item 7A. | 50 | |||

| Item 8. | 51-97 | |||

| Item 9. | 98 | |||

| Item 9A. | 98 | |||

| Item 9B. | 98 | |||

| Item 10. | 99 | |||

| Item 11. | 99 | |||

| Item 12. | 99 | |||

| Item 13. | 99 | |||

| Item 14. | 99 | |||

| Item 15. | 100-104 | |||

| Item 16. | 105 | |||

| PART I. |

OUTSIDE NORTH AMERICA ON- HIGHWAY HYBRID BUS ON- HIGHWAY PARTS, OTHER 2015 NET SALES (IN MILLIONS) % OF TOTAL • #1 supplier of fully-automatic transmissions • A leading supplier of hybrid-propulsion systems • A leading independent supplier • #1 supplier of fully-automatic transmissions in China and India • Established presence in Western Europe • A leading independent supplier • #1 supplier of transmissions for the U.S. Department of Defense • Approximately 1,400 dealers and distributors worldwide • Distribution • Emergency • Refuse • Construction • Utility • School, transit, shuttle and coach buses • Motorhome • Metro tractors • Hybrid transit bus • Hybrid shuttle bus • Energy • Mining • Construction • Specialty vehicle • Distribution • Emergency • Refuse • Construction • Utility • Transit, shuttle and coach buses • Energy • Mining • Construction • Specialty vehicle • Medium- and heavy-tactical wheeled platforms • Tracked combat platforms • Parts • Support equipment • Remanufactured transmissions • Fluids 2018. customers. CLASS 4-5 TRUCKS CLASS 6-7 TRUCKS • Ford • Manual Transmissions • AMTs • Ford • Manual Transmissions • AMTs • Ford • Ford America. DOD. markets. From time to time, we also acquire certain licenses to provide us with technology to complement our portfolio of products and product initiatives.ITEM 1. BusinessOverviewAllison Transmission Holdings, Inc. and its subsidiaries (“Allison,” the “Company” or “we”) design and manufacture commercial and defense fully-automatic transmissions. The business was founded in 1915 and has been headquartered in Indianapolis, Indiana since inception. Allison was an operating unit of General Motors Corporation (“Old GM”) from 1929 until 2007, when Allison once again became a stand-alone company. In March 2012, Allison began trading on the New York Stock Exchange under the symbol “ALSN”.We have approximately 2,7002,900 employees and 1312 different transmission product lines. Although approximately 81%77% of revenues were generated in North America in 2015,2018, we have a global presence by serving customers in Europe, Asia, South America and Africa. We serve customers through an independent network of approximately 1,400 independent distributor and dealer locations worldwide.Our BusinessWe are the world’s largest manufacturer of fully-automatic transmissions for medium- and heavy-duty commercial vehicles and medium- and heavy-tactical U.S. defense vehicles. Allison transmissions are used in a wide variety of applications, including on-highway trucks (distribution, refuse, construction, fire and emergency), buses (primarily school, transit and electric hybrid-transit), motorhomes, off-highway vehicles and equipment (primarily energy, mining and construction) and defense vehicles (wheeled and tracked). We estimate that globally, in 2015,2018, we sold approximately 63%60% of all fully-automatic transmissions for medium- and heavy-duty on-highway commercial vehicle applications. We believe the Allison brand is one of the most recognized in our industry as a result of the performance, reliability and fuel efficiency of our transmissions and is associated with high quality, durability, vocational value, technological leadership and superior customer service.We introduced the world’s first fully-automatic transmission for commercial vehicles over 60 years ago. Since that time, we have driven the trend in North America and Western Europe towards increasing automaticity by targeting a diverse range of commercial vehicle vocations. Allison transmissions are optimized for the unique performance requirements of end users, which typically vary by vocation. Our products are highly engineered, requiring advanced manufacturing processes, and employ complex software algorithms for our transmission controls to maximize end user performance. We have developed over 100 different models that are used in more than 2,500 different vehicle configurations and are compatible with more than 500 combinations of engine brands, models and ratings (including diesel, gasoline, natural gas and other alternative fuels). Additionally, we have created thousands of unique Allison-developed calibrations available to be used with our transmission control modules.Our IndustryCommercial vehicles typically employ one of three transmission types: manual, automated manual transmissions (“AMT”) or fully-automatic. Manual and automated manual transmissions ("AMT") are the most prevalent transmission type used in Class 8 tractors in North America andAmerica. Manual transmissions are the most prevalent in medium- and heavy-duty commercial vehicles, generally, outside North America. Manual transmissions utilize a disconnect clutch causing power to be interrupted during each gear shift resulting in energy loss-related inefficiencies and less work being accomplished for a given amount of fuel consumed. In long-distance trucking, this power interruption is not a significant factor, as the manual transmission provides its highest degree of fuel economy during steady-state cruising. However, steady-state cruising is only one part of the duty cycle. When the duty cycle requires a high degree of “start and stop” activity or speed transients, as is common in many vocations as well as in urban environments, we believe manual transmissions result in reduced performance, lower fuel efficiency, lower average speed for a given amount of fuel consumed and inferior ride quality. Moreover, the clutches must be replaced regularly, resulting in increased maintenance expense and vehicle downtime. Manual transmissions also require a skilled driver to operate the disconnect clutch when launching the vehicle and shifting gears. AMTs are manual transmissions that feature automated operation of the disconnect clutch. Fully-automatic transmissions utilize technology that smoothly shifts gears instead of a disconnect clutch, thereby delivering uninterrupted power to the wheels during gear shifts and requiring minimal driver input. These transmissions deliver superior acceleration, higher productivity, increased fuel efficiency, reduced operating costs, less driveline shock and smoother shifting relative to both manual transmissions and AMTs in vocations with a high degree of “start and stop” activity, as well as in urban environments.Emerging technologies in commercial-duty transmissions and powertrains include dual clutch transmissions (“DCT”) and electric drive powertrains. DCTs are variants of manual transmissions and AMTs that incorporate a “dual clutch” mechanism to facilitate shifting the manual transmission gearbox. Electric drive powertrains are also emerging in certain end markets, such as transit buses, and are in part driven by efforts to reduce fuel consumption and greenhouse gas emissions. Electric drive powertrains differ from “electric hybrid” powertrains because they only propel the vehicle with an electric motor; while “electric hybrids” generally utilize both a conventional internal combustion power source and powertrain as well as the means to propel the vehicle electrically. While both emerging technologies are gaining use in niche automotive markets, they are just beginning to evolve and become proven in commercial vehicle markets.Fuel efficiency, reduction in fuel consumption and greenhouse gasreduced emissions are important considerations for commercial vehicles everywhere and they tend to go together. We believe fuel efficiency, the measure of work performed for a given amount of fuel consumed, is the best method to assess fuel consumption of commercial vehicles as compared to the more commonly-used fuel economy metric of miles-per-gallon (“MPG”). MPG is inadequate for commercial vehicles because it does not encompass two key elements of efficiency that we believe are important to vehicle owners and operators: payload and transport time. For example, if more work can be completed or more payload hauled using the same amount of fuel and/or over a shorter period of time, then we believe the vehicle is more fuel efficient. Since fuel economy and its MPG metric only accounts for distance traveled and fuel consumed, ignoring time and work performed, we believe it is therefore an inferior metric to fuel efficiency when it comes to assessing commercial vehicles. Markets, regulations, policies and technology continue to evaluateevolve with respect to these topics.Our Served MarketsWe sell our transmissions globally for use in medium- and heavy-duty on-highway commercial vehicles, off-highway vehicles and equipment and defense vehicles. In addition to the sale of transmissions, we also sell branded replacement parts, support equipment and other products necessary to service the installed base of vehicles utilizing our transmissions. The following table provides a summary of our business by end market, for the fiscal year ended December 31, 2015. NORTH AMERICA DEFENSE SERVICE END MARKET

TRANSIT OFF-

HIGHWAY OFF-

HIGHWAY

SUPPORT

EQUIPMENT

& $1,059 $73 $55 $262 $35 $113 $389 53% 4% 3% 13% 2% 6% 19% MARKET POSITION VOCATIONS OR END USE END MARKET NORTH AMERICA OUTSIDE NORTHAMERICADEFENSE SERVICE PARTS, SUPPORT EQUIPMENT& OTHERON-HIGHWAYOFF-HIGHWAYON-HIGHWAYOFF-HIGHWAY2018 NET SALES(IN MILLIONS)$1,317 $93 $383 $129 $158 $633 % OF TOTAL 49% 3% 14% 5% 6% 23% MARKET POSITION • #1 supplier of fully-automatic transmissions • A leading independent supplier • #1 supplier of fully-automatic transmissions in China • Established presence in Western Europe• A leading independent supplier • #1 supplier of transmissions for the U.S. Department of Defense • Approximately 1,400 dealers and distributors worldwide VOCATIONS OR END USE • Construction• Distribution • Electric hybrid transit and shuttle bus• Emergency • Metro Tractors • Motorhome• Refuse • School, transit, shuttle and coach buses• Utility • Construction• Energy • Mining • Specialty vehicle• Construction• Distribution • Emergency • Refuse • Transit, shuttle and coach buses • Utility • Construction• Energy • Mining • Specialty vehicle• Medium- and heavy-tactical wheeled platforms • Tracked combat platforms• Fluids• Parts• Remanufactured transmissions • Support equipmentRefer to NOTE 18, “Concentration of Risk” and NOTE 22, “Geographic Information” in Part II, Item 8, of this Annual Report on Form 10-K for additional information on our significant original equipment manufacturer (“OEM”) customers and net sales by geographical areas.North AmericaOn-Highway.We are the largest manufacturer of fully-automatic transmissions for the on-highway medium- and heavy-duty commercial vehicle market in North America. The following is a summary of our on-highway net sales by vehicle class in North America.

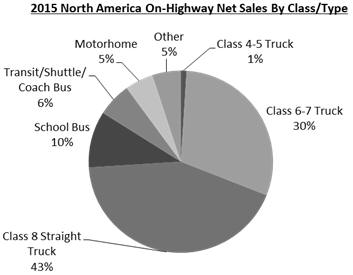

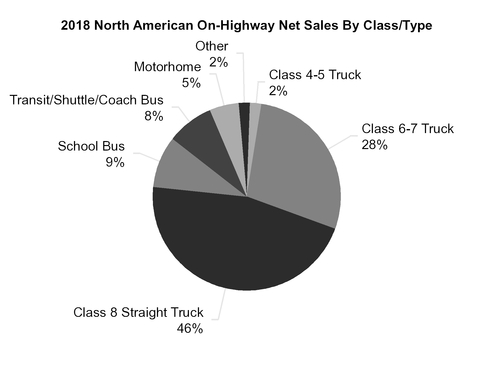

Our core North American on-highway market includes Class 4-5, Class 6-7 and Class 8 straight trucks, conventional transit, shuttle and coach buses, school buses and motorhomes. Class 8 trucks are subdivided into two markets: straight and tractor. Class 8 straight trucks are those with a unified body (e.g., refuse, construction, and dump trucks), while tractors have a vehicle chassis that is separable from the trailer they pull. We have been supplying transmissions for Class 8 straight trucks for decades, and it is a core end market for us. Today, we have very limited exposure to the Class 8 line-haul tractor market because lower priced manual transmissions and AMTs generally meet the needs of these vehicles which are primarily used in long distance hauling.

Our core North American on-highway market includes Class 4-5, Class 6-7 and Class 8 straight trucks, conventional transit, shuttle and coach buses, school buses and motorhomes. Class 8 trucks are subdivided into two markets: straight and tractor. Class 8 straight trucks are those with a unified body (e.g., refuse, construction, and dump trucks), while tractors have a vehicle chassis that is separable from the trailer they pull. We have been supplying transmissions for Class 8 straight trucks for decades, and it is a core end market for us. Today, we have very limited exposure to the Class 8 line-haul tractor market because lower priced manual transmissions and AMTs generally meet the needs of these vehicles which are primarily used in long distance hauling. However, we have identified a portionWe also provide electric hybrid-propulsion systems for transit buses within the North American on-highway market. The interest in conserving fuel and reducing greenhouse gas emissions is driving demand for more fuel efficient commercial vehicles. Our customers are typically city, state and federal governmental entities. We compete primarily with BAE Systems plc and manufacturers of the Class 8 tractor market that we call metro tractors that are usedelectric drive systems in urban environments the majority of the time and developed a fully-automatic transmission (the “TC10”) that meets the unique duty cycle requirements of the Class 8 metro tractorthis market. Combining the startability and continuous, uninterrupted power qualities of a fully-automatic transmission with the cruising aspects of a manual transmission, the TC10 offers an alternative to traditional manual and automated manual transmissions in tractor applications.We sell substantially all of our transmissions in the North American on-highway market to OEMs. These OEMs, in turn, install our transmissions in vehicles in which our transmission is either the exclusive transmission available or is specifically requested by end users who are choosing between a manual transmission, an AMT or a fully-automatic transmission.users. In 2015,2018, OEM customers representing over 90%95% of our North American on-highway unit volume participated in long-term supply agreements (“LTSA”) with us. Generally, these supply agreementsLTSAs offer the OEM customer defined levels of mutual commitment with respect to growing Allison’s presence in the OEMs’ products and promotional efforts, pricing and sharing of commodity cost risk. The length of our customer agreementsLTSAs is typically between three and five years. We often compete in this market against independent manufacturers of manual transmissions, AMTs, DCTs, electric drive systems, fully-automatic transmissions manufactured by Ford Motor Company (“Ford”), ZF Friedrichshafen AG (“ZF”) and Voith GmbH, (“Voith”), and against vertically integrated OEMs in certain weight classes that use their own internally manufactured transmissions in certain vehicles.The following table presents a summary of our competitive position by vehicle class in the North America on-highwayOn-Highway end market. CLASS 8 STRAIGHT

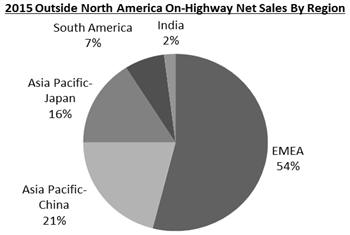

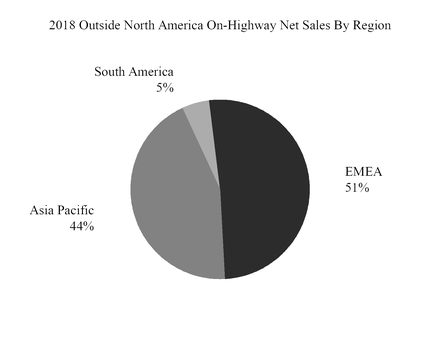

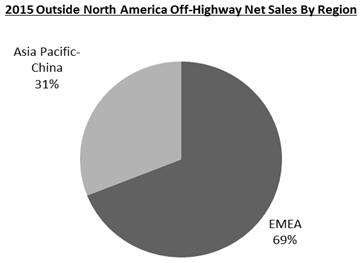

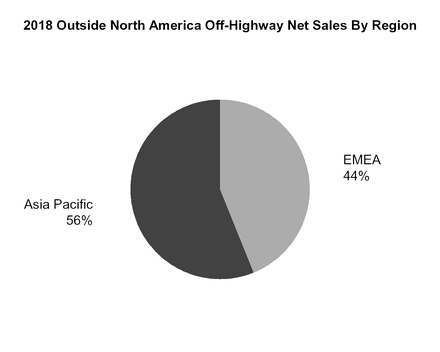

TRUCKS SCHOOL BUSES MOTORHOMES 2015 SHARE 5% 77% 61% 98% 40% PRIMARY COMPETITION Hybrid Transit Buses.The interest in conserving fuel and reducing greenhouse gas emissions is driving demand for more fuel efficient commercial vehicles. In North America, we sold approximately 60% of all units for the hybrid transit bus market in 2015. Our customers in this North American end market are typically city, state and federal governmental entities, which utilize government funds to subsidize a portion of the purchase price for the transit buses containing our hybrid-propulsion system. In this market, we compete primarily with BAE Systems plc (“BAE”). CLASS 4-5TRUCKSCLASS 6-7TRUCKSCLASS 8 STRAIGHTTRUCKSSCHOOL BUSES MOTORHOMES 2018 SHARE7% 74% 70% 88% 39% PRIMARY COMPETITION• Ford • Manual Transmissions• AMTs• Ford• Manual Transmissions• AMTs• Ford • Ford Off-Highway.We have provided products used in vehicles and equipment that serve energy, mining and construction applications in North America for over 5060 years. Off-highway energy applications include hydraulic fracturing equipment, well-stimulation equipment, pumping equipment, and well-servicing rigs, which often use a fully-automatic transmission to propel the vehicle and drive auxiliary equipment. We maintain a leadership position in this end market, with nearly all producers of well-stimulation and well-servicing equipment utilizing our heavy duty off-highway transmissions. Additionally, we sell kits that can increase the horsepower of our existing off-highway products. Competition includes Caterpillar Inc. (“Caterpillar”) and Twin Disc, Inc. (“Twin Disc”).We also provide heavy-duty transmissions used in mining trucks, specialty vehicles and construction vehicles. Mining applications include trucks used to haul various commodities and other products, including rigid dump trucks, underground trucks and long-haul tractor trailer trucks with load capacities between 40 to 110 tons. Our major competitors in this end market are Caterpillar and Komatsu Ltd. (“Komatsu”), both of which are vertically integrated and manufacture fully-automatic transmissions for their own vehicles. Specialty vehicles using our heavy-duty transmissions include airport rescue and firefighting vehicles and heavy-equipment transporters. Our major competitor in this end market is Twin Disc. Construction applications include articulated dump trucks, with Caterpillar, Volvo Group (“Volvo”) and ZF as competitors.Outside North AmericaOutside North America we serve several different markets, including: Europe, Middle East, Africa (“EMEA”(collectively, “EMEA”), Asia-Pacific and South America and India.On-Highway.We are the largest manufacturer of fully-automatic transmissions for the commercial vehicle market outside of North America. While the use of fully-automatic transmissions in the medium- and heavy-duty commercial vehicle market has been widely accepted in North America, the markets outside North America continue to be dominated by manual transmissions. In 2015,2018, fully-automatic transmission-equipped medium- and heavy-duty commercial vehicles represented less than 5% of the vehicles in markets outside North America and are concentrated in certain vocational end markets. The following is a summary of our on-highway net sales by region outside of North America.

Europe, Middle East, Africa. EMEA is composed of several different markets, each of which differs

Europe, Middle East, Africa. EMEA is composed of several different markets, each of which differs significantly from our core North American market by the degree of market maturity, sophistication and acceptance of fully-automatic transmission technology. Within Europe, we serve Western European developed markets, as well as Russian and Eastern European emerging markets, principally in the refuse, emergency, bus, coach, distribution and utility markets. Competition in Western Europe is most notably characterized by a high level of vertical powertrain integration with OEMs often utilizing their own manual transmissions and AMTs in their vehicles. The Middle East and Africa regions are generally characterized by very limited local vehicle production, with imports from the U.S., South America, Turkey, China, India and Europe accounting for the majority of vehicles.Asia-Pacific. Our key Asia-Pacific markets include China, Japan, Australia,India, and South Korea; however, we actively participate in several other important Asia-Pacific countries including Australia, Taiwan, Indonesia, Malaysia and Thailand, which are primarily importers of commercial vehicles. Within Asia-Pacific, our sales efforts are principally focused on the transit bus and vocational truck markets. Currently, manual transmissions are the predominant transmissions used in commercial vehicles in the Asia-Pacific region.South America. The South American region is characterized by a high level of OEM integration, with captive manual transmission and AMT manufacturing. Currently, manual transmissions are the predominant transmissions used in commercial vehicles in South America.India. Currently, manual transmissions are the predominant transmission used in commercial vehicles in India.Off-Highway.The following is a summary of our off-highway net sales by region outside of North America.

Europe, Middle East, Africa.Our off-highway markets in EMEA are mining and construction. Our major off-highway competitors are Caterpillar and Komatsu, both of which are vertically integrated manufacturers of off-highway mining vehicles, including the specific fully-automatic transmission used in their mining trucks. A typical construction application is the articulated dump truck, with competition from Caterpillar, Volvo and ZF transmissions.Asia-Pacific. Off-highway markets in Asia are shared by energy, mining and construction applications. Our primary competitors are Caterpillar, Danyang Winstar Auto Parts Co., Ltd. and Twin Disc in energy

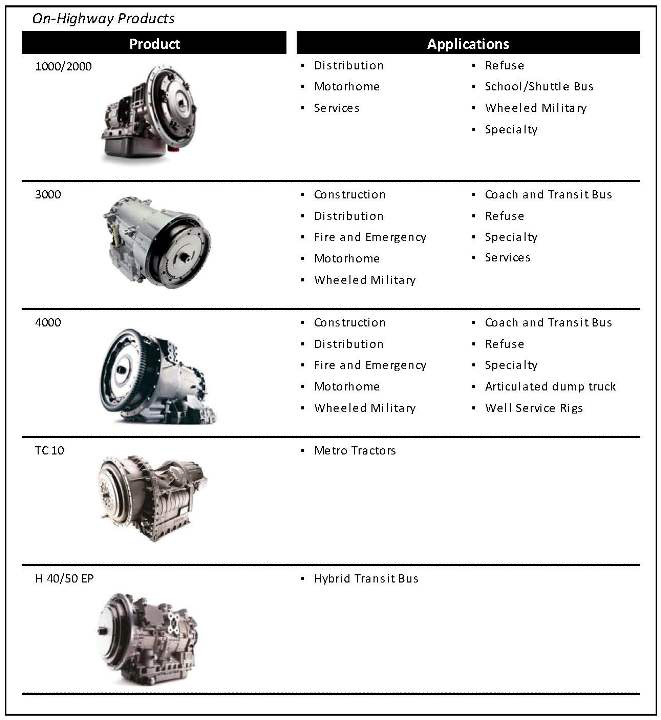

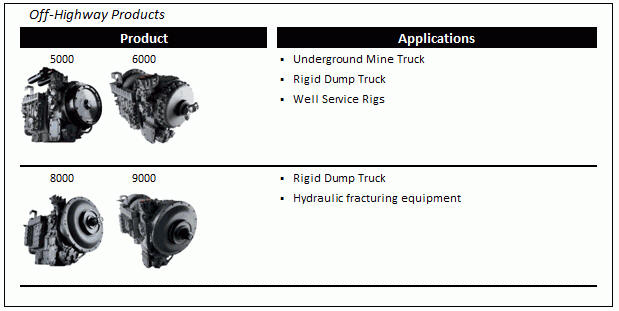

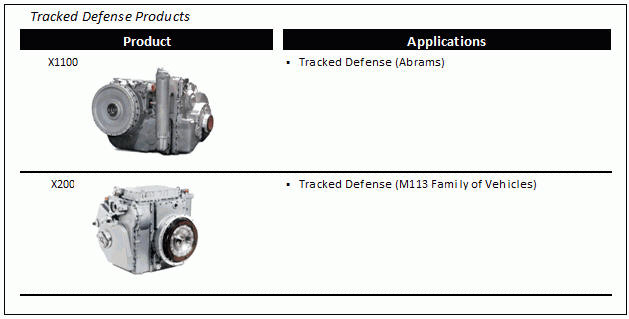

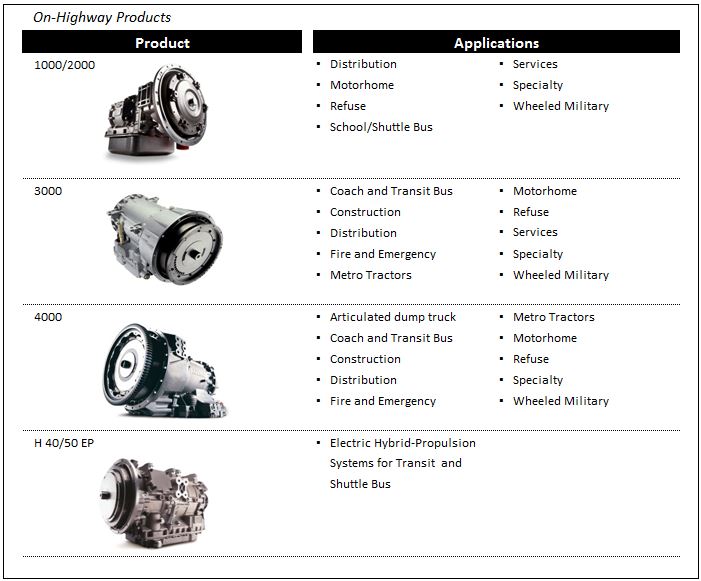

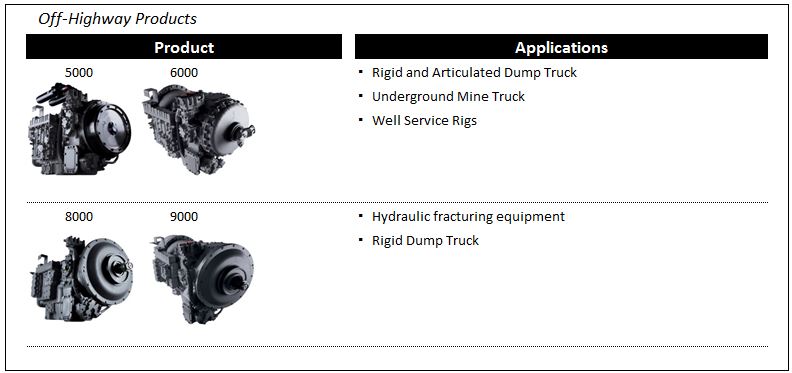

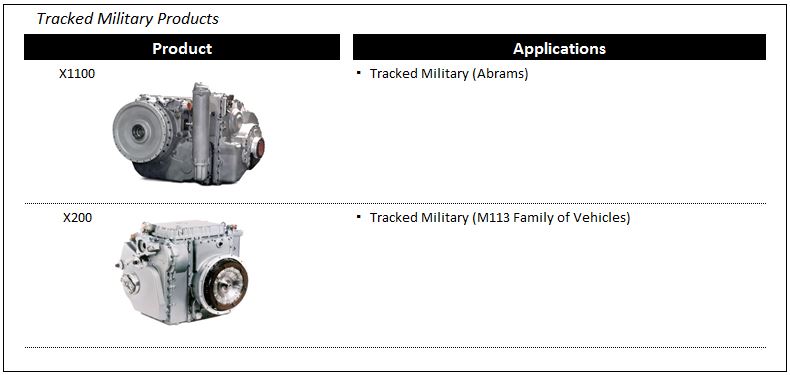

Europe, Middle East, Africa.Our off-highway markets in EMEA are mining and construction. Our major off-highway competitors are Caterpillar and Komatsu, both of which are vertically integrated manufacturers of off-highway mining vehicles, including the specific fully-automatic transmission used in their mining trucks. A typical construction application is the articulated dump truck, with competition from Caterpillar, Volvo and ZF transmissions.Asia-Pacific. Off-highway markets in Asia are shared by energy, mining and construction applications. Our primary competitors are Caterpillar, Danyang Winstar Auto Parts Co., Ltd. and Twin Disc in energy applications,applications; Caterpillar, Komatsu and KomatsuDanyang Winstar Auto Parts Co., Ltd. in mining applicationsapplications; and Caterpillar, Volvo and ZF in construction applications.DefenseWe have a long-standing relationship with the U.S. Department of Defense (“DOD”), dating back to 1946, when we began developing our first-generation tank transmission. Today, we sell substantially all of the transmissions for medium- and heavy-tactical wheeled vehicle platforms including the Family of Medium Tactical Vehicles, Armored Security Vehicles, Heavy Expanded Mobility Tactical Trucks, Heavy Equipment Transporters, Palletized Loading Systems, M915 Series Trucks, Medium Tactical Vehicle Replacements and the Logistic Vehicle System Replacement. Additionally, we supplied transmissions for the majority of Mine-Resistant Ambush Protected (“MRAP”) Vehicles, and the MRAP All-Terrain Vehicle and for the Joint Light Tactical Vehicles,Vehicle, which is the replacement vehicle for Humvee personnel transport. Transmissions for our wheeled vehicle platforms are typically sold to OEMs.We are also the supplier on two of the three key tracked vehicle platforms, the Abrams tank and the M113 family of vehicles, which are sold directly to the DOD. Additionally, we sell parts kits to licensees for the production of transmissions for tracked vehicles manufactured outside North America. Overall, we have seenSee Part I, Item 1A, “Risk Factors” of this Annual Report on Form 10-K for a discussion of risks associated with our contracts with the demand for U.S. defense vehicles decrease as the funding for defense vehicles declines. Additionally, the DOD budgets and supplemental spending have allowed them to recapitalize and reset many vehicle systems, which has reduced the average age of the fleet and the need to procure new vehicles.Globally, we face competition for the supply of our transmissions in tracked defense vehicles primarily from L-3 Communications Corporation,L3 Technologies, Inc., Renk AG and ZF. Additionally, we face limited competition from Caterpillar and ZF in certain defense wheeled vehicle platforms.Service Parts, Support Equipment and OtherThe aftermarket provides us with a relatively stable source of revenues as the installed base of vehicles and equipment utilizing our transmissions continues to grow. The need for replacement parts is driven by normal vehicle and equipment maintenance requirements and is not significantly impacted by economic cycles.requirements. Uninterrupted operation is generally critical for end users’ profitability. End users focus on getting the vehicle or equipment back in service, which in some cases results in the aftermarket purchase decision being less price-sensitive.The sale of Allison-branded parts and fluids, remanufactured transmissions and support equipment is fundamental to our brand promise. We have assembled a worldwide network of approximately 1,400 independent distributor and dealer locations to sell, service and support our transmissions. As part of our brand strategy, our distributors and dealers are required to sell genuine Allison-branded parts. Within the aftermarket, we offer remanufactured transmissions under our ReTran brand, which provides a cost-effective alternative for transmission repairs and replacements. We also provide support equipment to our OEMs to assist in installing new Allison transmissions into vehicles, and, therefore, sales of support equipment are dependent upon sales of new transmissions.Over the last few years, traditional aftermarket sales have been tempered by improvements in product quality and durability. While traditional aftermarket sales are expected to grow, support equipment sales fluctuate with the introduction of new transmissions. The competition for service parts and ReTran transmissions comes from a variety of smaller-scale companies sourcing non-genuine “will-fit” parts from unauthorized manufacturers. These “will-fit” parts often do not meet our product specifications, and therefore may be of lesser quality than genuine Allison parts.Our Product OfferingsAllison transmissions are sold under the Allison Transmission brand name and remanufactured transmissions are sold under the ReTran brand name. The following is a summary of our 1312 transmission product lines.

Product Development and EngineeringWe maintain product development and engineering capability dedicated to the design, development, refinement and support of our fully-automatic transmissions and electric hybrid-propulsion systems. We believe our customers expect our products to provide unparalleled performance and value defined in various ways, including delivering maximum cargo in minimum time, using the least amount of fuel possible while employing the fewest vehicles possible and experiencing maximum vehicle uptime. In response to those needs and the evolving customer focus on fuel efficiency, we provide vehicle specification guidelines, transmission control software and mechanical components to optimize fuel economy while delivering desired vehicle performance. Further, we are developing new technology to improve fuel efficiency and fuel economy by allowing engines to operate more efficiently and at lower speeds to avoid consuming fuel without compromising performance. Building on our engineering capabilities, we pioneered electric hybrid-propulsion in commercial vehicles and are developing new alternative technologies for use in our global commercial vehicle

Product Development and EngineeringWe maintain product development and engineering capability dedicated to the design, development, refinement and support of our fully-automatic transmissions and electric hybrid-propulsion systems. We believe our customers expect our products to provide unparalleled performance and value defined in various ways, including delivering maximum cargo in minimum time, using the least amount of fuel possible while employing the fewest vehicles possible and experiencing maximum vehicle uptime. In response to those needs and the evolving customer focus on fuel efficiency, we provide vehicle specification guidelines, transmission control software and mechanical components to optimize fuel economy while delivering desired vehicle performance. Further, we are developing new technology to improve fuel efficiency and fuel economy by allowing engines to operate more efficiently and at lower speeds to avoid consuming fuel without compromising performance. Building on our engineering capabilities, we pioneered electric hybrid-propulsion in commercial vehicles and are developing new alternative technologies for use in our global commercial vehicle markets; however, decreased fuel costs, alternative fuels and other technologies have resulted in deteriorating market conditions for hybrid-propulsion vehicles in recent years. For the years ended December 31, 2015, 2014 and 2013, we have invested $92.5 million, $103.8 million and $97.1 million in engineering – research and development expense, respectively.initiatives, such as our engineering development agreement with Torotrak plc and our development agreement with Fallbrook Technologies, Inc. For the years ended December 31, 2015, 2014 and 2013, we have invested $0.2 million, $6.1 million and $6.0 million, respectively, in engineering – research and development expense related to technology-related licenses.We maintain test tracks on our Indianapolis, Indiana campus and at our location in Szentgotthard, Hungary for vehicle drive, testing and calibration activities in addition to being a demonstration venue for customers. We also use test track facilities in New Carlisle, Indiana and Apache Junction, Arizona.Sales and Marketing OrganizationOur sales and marketing effort is organized along geographic and customer lines and is comprised of marketing, sales and service professionals, supported by application engineers worldwide. In North America, selling efforts in the on-highway end market are organized by distributor area responsibility, OEM sales and, national accounts, for our large end users.users, national accounts. Outside North America, we manage our sales, marketing, service and application engineering professionals through regional areas of responsibility. These regional management teams distribute OEM service and application engineering resources globally. We manage our defense products sales, marketing, service and application engineering through professionals based in Indianapolis, Indiana and Detroit, Michigan.We have developed a marketing strategy to reach OEM customers as well as end users. We target our end users primarily through marketing activities by our sales staff, who directly call on end users and attend local trade shows, targeting specific vocations globally and through our plant tour programs, where end users may test our products on the Indianapolis test track and our enhanced customer experience demonstration track at our Hungary facility.While our marketing management uses the term “customer” interchangeably for OEMs and end users, the primary objective of our marketing strategy is to create demand for fully-automatic transmissions through:OEM promotion of our products and incorporation of fully-automatic transmissions in their commercial vehicle product offerings;

In addition, in conjunction with the sale of Allison (the “Acquisition Transaction”) by Old GM, we acquired

Allison trademarks.

Under

During the third quarter of 2015, the EPA determined that GM’s remedial activities were complete and that the migration of any contamination is under control, and published a public notice seeking comment on a draft final decision, the issuance of which would result in us assuming responsibility for operating, monitoring and maintaining the ongoing Corrective Action activities throughinto an anticipated agreedadministrative order of consent (“AOC”) with the EPA. As a result of the publishing of the draft final decision, we determinedEPA that appropriate liabilities for operating, monitoring and maintaining the ongoing remedial activities could be reasonably estimated and recorded approximately $14.0 million for the estimated undiscounted liabilitiesrequires us to be paid out over the next 30 years. The recorded liabilities will be adjusted periodically as remediation efforts progress or as additional technical, regulatory or legal information becomes available. We expect to fund the expenditures for these activities from operating cash flow.

On January 27, 2016, the EPA issued a final decision. With the AOC,provide financial assurance is required by the EPA to complete the operation, monitoring and maintenance activities in the event we fail to do so. This financial assurance can take a variety of forms including, but not limited to meeting certain financial metrics, providingWe currently have a letter of credit or securing a bond or an insurance policy. Thewith the EPA in the amount and method by which we will be required to provide financial assurance is expected to be determined in 2016.

of $15 million.

ITEM 1A. Risk FactorsThe following is a cautionary discussion of risks, uncertainties and assumptions that we believe are significant to our business. In addition to the factors discussed elsewhere in this Annual Report on Form 10-K, the following are some of the important factors that, individually or in the aggregate, we believe could make our actual results differ materially from those described in any forward-looking statements. It is impossible to predict or identify all such factors and, as a result, you should not consider the following factors to be a complete discussion of risks, uncertainties and assumptions.Risks Related to Our BusinessWe participate in markets that are competitive, and our competitors’ actions could have a material adverse effect on our business, results of operations and financial condition.Our business operates in competitive markets. We compete against other existing or new global manufacturers of transmissions for commercial vehicles on the basis of product performance, quality, price, distribution capability and service in addition to other factors. In addition, we compete with manufacturers developing alternative technologies, including electric drivetrains, that may or may not require a transmission. In addition, subsidies offered by governmental entities continue to drive the development and adoption of various alternative technologies. Actions by our competitors could lead to downward pressure on prices and/or a decline in our market share, either or both of which could adversely affect our results.In addition, some of our customers or future customers are OEMs that manufacture or could in the future manufacture transmissions or alternate technologies, including electric drive powertrains, for their own products. Despite their transmission manufacturing abilities,capabilities, our existing OEM customers have chosen to purchase certain transmissions from us due to customer demand, resulting from the quality of our transmission products and in order to reduce fixed costs, eliminate production risks and maintain company focus. However, we cannot be certain these customers will continue to purchase our products in the future. Increased levels of production insourcing by these customers could result from a number of factors, such as shifts in our customers’ business strategies, acquisition by a customer of another transmission manufacturer, the inability of third-party suppliers to meet specifications and the emergence of low-cost production opportunities in foreign countries. As a result, these OEMs may use transmissions produced internally or by another manufacturer and no longer choose to purchase transmissions from us. A significant reduction in the level of external sourcing of transmission production by our OEM customers could significantly impact our net sales and cash flows and, accordingly, have a material adverse effect on our business, results of operations and financial condition.Certain of our end users operate in highly cyclical industries, which can result in uncertainty and significantly impact the demand for our products, which could have a material adverse effect on our business, results of operations and financial condition.Some of the markets in which we operate, including energy, mining, construction, distribution and motorhomes, exhibit a high degree of cyclicality. Decisions to purchase our transmissions are largely a result of the performance of these and other industries we serve. If demand for output in these industries decreases, the demand for our products will likely decrease. Demand in these industries is impacted by numerous factors including prices of commodities, rates of infrastructure spending, housing starts, real estate equity values, interest rates, consumer spending, fuel costs, energy demands, municipal spending and commercial construction, among others. Increases or decreases in these variables globally may significantly impact the demand for our products, which could have a material adverse effect on our business, results of operations and financial condition. If we are unable to accurately predict demand, we may be unable to meet our customers’ needs, resulting in the loss of potential sales, or we may manufacture excess products, resulting in increased inventories and overcapacity in our production facilities, increasing our unit production cost and decreasing our operating margins.Continued volatilityVolatility in and disruption to the global economic environment could adversely affectand changes in the ability of customersregulatory and suppliers to obtain credit andbusiness environments in which we operate may have a material adverse effect on our business, results of operations and financial condition.The commercial vehicle industry as a whole has been more adversely affected by volatile economic conditions than many other industries, as the purchase or replacement of commercial vehicles, which are durable items, can be deferred for many reasons, including reduced spending by end users. Future changes in the regulatory and business environments in which we operate may adversely affect our ability to sell our products or source materials needed to manufacture our products. Furthermore, financial instability or bankruptcy at any of our suppliers or customers could disrupt our ability to manufacture our products and impair our ability to collect receivables, any or all of which may have a material adverse effect on our business, results of operations and financial condition. In addition, some of our customers and suppliers may experience serious cash flow problems and, thus, may find it difficult to obtain financing, if financing is available at all. As a result, our customers’ need for and ability to purchase our products or services may decrease, and our suppliers may increase their prices, reduce their output or change their terms of sale. Any inability of customers to pay us for our products and services, or any demands by suppliers for different payment terms, may materially and adversely affect our results of operations and financial condition. Furthermore, our suppliers may not be successful in generating sufficient sales or securing alternate financing arrangements, and therefore may no longer be able to supply goods and services to us. In that event, we would need to find alternate sources for these goods and services, and there is no assurance we would be able to find such alternate sources on favorable terms, if at all. Any such disruption in our supply chain could adversely affect our ability to manufacture and deliver our products on a timely basis, and thereby affect our results of operations.We may not be successful in introducing our new products and technologies and responding to customer needs.We currently have new products and technologies under development. The development of new products and technologies is difficult and the timetable for commercial release is uncertain. Not all new product launches have been successful, and we may not be successful in the future in introducing other new products and responding to customer needs. In addition, it often takes significant time, in some cases multiple fleet buy cycles, before customers gain experience with new products and technologies and those new products and technologies become widely-accepted by the market, if at all. If we do not adequately anticipate the changing needs of our customers by developing and introducing new and effective products and technologies on a timely basis, our competitive position and prospects could be harmed. If our competitors are able to respond to changing market demands and adopt new technologies more quickly than we do, demand for our products could decline, our competitive position could be harmed, our future research and development activities may be constrained due to intellectual property rights of others and we will not be able to recoup a return on our development investments. Moreover, changing customer demands as well as evolving regulatory, safety and environmental standards could require us to adapt our products and technologies to address such changes. As a result, in the future we may experience delays in the introduction of some or all of our new products or modifications or enhancements of existing products. Furthermore, there may be production delays due to unanticipated technological setbacks, which may, in turn, delay the release of new products to our end users. If we experience significant delays or increased costs in the production, launch or acceptance of our products and technologies, our net sales and results of operations may be materially adversely affected.Our sales are concentrated among our top five OEM customers and the loss or consolidation of any one of these customers or the discontinuation of particular vehicle models for which we are a significant supplier could reduce our net sales and have a material adverse effect on our results of operations and financial condition.We have in the past and may in the future derive a significant portion of our net sales from a relatively limited number of OEM customers. For the years ended December 31, 2018, 2017 and 2016, our top five OEM customers accounted for approximately 49%, 49% and 52% of our net sales, respectively. Our top two customers, Daimler AG and PACCAR Inc. accounted for approximately 18% and 10%, respectively, of our net sales during 2018. The loss of, or consolidation of, any one of these customers, or a significant decrease in business from, one or more of these customers could harm our business. In addition, the discontinuation of particular vehicle models for which we are a significant supplier could reduce our net sales and have a material adverse effect on our results of operations.Our success depends on continued research and development efforts, the outcome of which is uncertain.Our success depends on our ability to improve the efficiency and performance of our transmissions, and we invest significant resources in research and development in order to do so. Nevertheless, the research and development process is time-consuming and costly, and offers uncertain results. We may not be able through our research and development efforts to keep pace with improvements and changes in transmission-related or vehicle propulsion technology of our competitors, and licenses for technologies that would enable us to keep pace with our competitors may not be available on commercially reasonable terms if at all. Finally, our research and development efforts, and generally our ability to introduce improved or new products in the marketplace, may be constrained by the patents and other intellectual property rights of competitors and others.We may not be able to identify or consummate acquisitions or achieve expected benefits from or effectively integrate acquisitions, which could harm our growth.From time to time we evaluate selective acquisitions and strategic investments to obtain additional technologies, complementary product lines and supply channels. Acquisitions involve many risks that could have an adverse effect on our business, financial condition or results of operations, including:our ability to identify suitable acquisition candidates, prevail against competing potential acquirers and negotiate and consummate acquisitions on terms attractive to us;difficulties in integrating personnel and sales forces, operations, manufacturing, logistics, research and development, information technology, communications, purchasing, accounting, marketing, administration and other systems and processes and otherwise assimilating the operations of the acquired company;the diversion of resources, including diverting management’s attention from our current operations;risks of entering new geographic or product markets in which we have limited or no direct prior experience;the potential loss of key customers, employees or suppliers of the acquired company or adverse effects on our existing business relationships with our suppliers and customers;the potential incurrence of indebtedness to fund the acquisition;the acquired business not achieving anticipated revenues, earnings, cash flow or market share;excess capacity;failure to achieve the expected synergies or cost savings resulting from the acquisition;the need for additional investments post-acquisition that could be greater than anticipated;the impact of U.S. and foreign competition laws and regulations on our ability to make certain acquisitions;inaccurate assessment of undisclosed, contingent or other liabilities or problems and unanticipated costs associated with the acquisition;incorrect estimates made in accounting for acquisitions, incurrence of non-recurring charges and write-off of significant amounts of goodwill that could adversely affect our financial results; anddilution of earnings.We may also face liability with respect to acquired businesses for violations of environmental or other laws occurring prior to the date of our acquisition, and some or all of these liabilities may not be covered by environmental or other insurance secured to mitigate the risk or by indemnification from the sellers from which we acquired these businesses. We could also incur significant costs, including, but not limited to, remediation costs, natural resources damages, civil or criminal fines and sanctions and third-party claims, as a result of past or future violations of, or liabilities associated with, environmental or other laws.We cannot offer any assurance that we will be able to consummate any future acquisitions, strategic investments or other business combinations. If we are unable to identify suitable acquisition candidates or to consummate and successfully integrate strategic acquisitions, our business and results of operations may be adversely affected as a result.Increases in cost, disruption of supply or shortage of raw materials or components used in our products could harm our business and profitability.Our products contain various raw materials, including corrosion-resistant steel, non-ferrous metals such as aluminum and nickel, and precious metals such as platinum and palladium. We use raw materials directly in manufacturing and in transmission components that we purchase from our suppliers. We generally purchase components with significant raw material content on the open market. The prices for these raw materials fluctuate depending on market conditions. Volatility in the prices of raw materials such as steel, aluminum and nickel could increase the cost of manufacturing our products. We may not be able to pass on these costs to our customers, andthis could have a material adverse effect on our business, results of operations and financial condition. Even in the event that increased costs can be passed through to customers, our gross margin percentages would decline. Additionally, our suppliers are also subject to fluctuations in the prices of raw materials and may attempt to pass all or a portion of such increases on to us. In the event they are successful in doing so, our margins would decline.In 2018, approximately 75% of our total spending on components was sourced from approximately 35 suppliers, some of which are the single source for such components. All of the suppliers from which we purchase materials and components used in our business are fully validated suppliers, meaning the suppliers’ manufacturing processes and inputs have been validated under a production part approval process (“PPAP”). Furthermore, there are only a limited number of suppliers for certain of the materials used in our business, such as corrosion-resistant steel. As a result, our business is subject to the risk of additional price fluctuations and periodic delays in the delivery of our materials or components if supplies from a validated supplier are interrupted and a new supplier, if one is available, must be validated or materials and components must be purchased from a supplier without a completed PPAP, which could increase our risk of purchasing non-conforming components. Any such price fluctuations or delays, if significant, could harm our profitability or operations. In addition, the loss of a supplier could result in significant material cost increases or reduce our production capacity. We also cannot guarantee we will be able to maintain favorable arrangements and relationships with these suppliers. An increase in the cost or a sustained interruption in the supply or shortage of some of these raw materials or components that may be caused by a deterioration of our relationships with suppliers or by events such as natural disasters, power outages, labor strikes, or the like could negatively impact our business, results of operations and financial condition. Although we have agreements with many of our customers that we will pass such price increases through to them, such contracts may be canceled by our customers and/or we may not be able to recoup the costs of such price increases. Additionally, if we are unable to continue to purchase our required quantities of raw materials on commercially reasonable terms, or at all, if we are unable to maintain or enter into purchasing contracts for commodities, or if delivery of materials from suppliers is delayed or non-conforming, our operations could be disrupted or our profitability could be adversely impacted.We could be materially adversely affected by any failure to maintain cost controls.We rely on our cost structure and operating discipline to achieve strong operating margins. There are many factors that could affect our ability to realize expected cost savings or achieve future cost savings that we are not able to control, including the need for unexpected significant capital expenditures; unexpected changes in commodity or component pricing, including an increase in export or import tariffs, that we are unable to pass on to our suppliers or customers; labor costs, including wages, benefits and healthcare; cost inflation; and our inability to maintain efficiencies gained from our workforce optimization initiatives. Additionally, we have substantial indebtedness of approximately $2,548 million as of December 31, 2018. Our inability to maintain our cost controls could adversely impact our operating margins.Our long-term growth prospects and results of operations may be impaired if the rate of adoption of fully-automatic transmissions in commercial vehicles outside North America does not increase.Our long-term growth strategy depends in part on an increased rate of automaticity outside North America. As part of that strategy, we have established manufacturing facilities in India and Hungary. We have also dedicated significant human resources to serve markets where we anticipate increased adoption of automaticity, including China, India, Brazil and Russia. However, manual transmissions remain the market leader outside North America and there can be no assurance that adoption of automatic transmissions will increase. Factors potentially impacting adoption of automatic transmissions outside of North America may include the large existing installed base of manual transmissions, customer preferences for manual transmissions, commercial vehicle OEM vertical integration into manual transmission and AMT manufacturing, increased competition from AMTs, DCTs, electric driving systems, and other alternative transmission technologies and failure to further develop the Allison brand. If the rate of adoption of fully-automatic transmissions does not increase as we have anticipated, our long-term growth prospects and results of operations may be impaired.Our sales are concentrated among our top five OEM customers and the loss or consolidation of any one of these customers or the discontinuation of particular vehicle models for which we are a significant supplier could reduce our net sales and have a materially adverse effect on our results of operations.We have in the past and may in the future derive a significant portion of our net sales from a relatively limited number of OEM customers. For the years ended December 31, 2015, 2014 and 2013, our top five customers accounted for approximately 52%, 45% and 48% of our net sales, respectively. Our top three customers, Daimler, Navistar and Volvo, accounted for approximately 21%, 10% and 10%, respectively, of our net sales during 2015. The commercial vehicle industry, including our customers and suppliers, continues to experience volatility and uncertainty. The loss of, or consolidation of any one of these customers, or a significant decrease in business from, one or more of these customers could harm our business. In addition, the discontinuation of particular vehicle models for which we are a significant supplier could reduce our net sales and have a material adverse effect on our results of operations.Sales of our hybrid-propulsion systems have been, and are expected to continue to be, negatively impacted by external factors, including fuel price trends, regulatory requirements, alternative technologies and governmental entities electing not to subsidize the purchase of such products by end users.External factors, including diesel and natural gas fuel price trends, emissions and on-board diagnostics regulatory requirements, availability of compatible engine calibrations from engine manufacturers and alternative emerging green technologies, have, and are expected to continue to, negatively impact sales of our hybrid-propulsion systems. In addition, the sales of our hybrid-propulsion systems for use in transit buses have been, and are expected to continue to be, negatively impacted by governmental entities electing not to subsidize the purchase of such products by end users. In 2015, we derived approximately 4% of our net sales from the sale of hybrid-propulsion systems for use in transit buses to city, state and federal governmental end users. Such end users may be eligible to receive certain subsidies as a result of their purchase of vehicles using hybrid-propulsion systems. For example, the Federal Transit Authority and the DOE provide funds for end users to pursue alternative fuel propulsion systems. While we do not directly receive these subsidies, if any of the subsidizing entities elect to curtail such subsidies to end users for any reason including governmental budget reductions and related fiscal matters, failure of our hybrid technology to qualify for such subsidies or redundancy by alternative technologies created by our competitors, our sales from our hybrid-propulsion systems may be negatively impacted. For the years ended December 31, 2015, 2014 and 2013, we experienced decreases in revenue generated from hybrid-propulsion systems for use in transit buses of 22%, 11% and 9%, respectively.A majority of our sales to the defenseDefense end market are to U.S. government entities and contractors for the U.S. government,and foreign governments, and the loss of a significant number of our contracts, or budgetary declines or future reductions or changes in spending by the U.S. government wouldor foreign governments could have a material adverse effect on our results of operations and financial condition.The majority of ourOur net sales to the defenseDefense end market are derived from contracts (revenue arrangements) with agencies of, and prime system contractors for, the U.S. government.government and foreign governments. If a significant number of our DODDefense contracts and subcontracts are simultaneously delayed or cancelled for budgetary, performance or other reasons, it would have a material adverse effect on our results of operations and financial condition. Approximately 6%, or $113$158 million, of our net sales for the year ended December 31, 20152018 were from our Defense end market.Sales in our defense end market have been, and we expect will continue to be, negatively impacted by declining DOD spending on wheeled and tracked vehicles. In addition to declines in defense budgets, ourOur future financial results may be adversely affected by:declines in, or uncertainty regarding, U.S. or foreign government defense budgets;curtailment of the U.S. government’s use of technology or other services and product providers, including curtailment due to government budget reductions, future government shutdowns and related fiscal matters;

Any events that impact our brand name, including if the products we manufacture or distribute are found to be defective, could have an adverse effect on our reputation, cause us to incur significant costs and negatively impact our business, results of operations and financial condition.

We face exposure to product liability claims in the event that the use of our products has, or is alleged to have, resulted in injury, death or other adverse effects. We currently maintain product liability insurance coverage, but we cannot be assured that we will be able to obtain such insurance on acceptable terms in the future, if at all, or that any such insurance will provide adequate coverage against potential claims. Product liability claims can be expensive to defend and can divert the attention of management and other personnel for long periods of time, regardless of the ultimate outcome. An unsuccessful product liability defense could have a material adverse effect on our business, results of operation, financial condition or prospects. If one of our products is determined to be defective, we may face substantial warranty costs and may be responsible for significant costs associated with a product recall or a redesign. We have had defect and warranty issues associated with certain of our products in the past, and we cannot give assurance similar product defects will not occur in the future. See NOTE 9 of Notes to Consolidated Financial Statements included in Part II, Item 8 of this Annual Report on Form 10-K for additional details regarding these warranty issues.

Furthermore, our business depends on the strong brand reputation we have developed. In addition to the risk of defective products we face with our new product installations, we also face significant risks in our efforts to penetrate new markets, where we have limited brand recognition. We also rely on our reputation with end users of our transmissions to specify our transmissions when purchasing new vehicles from our OEM customers. In the event we are not able to maintain or enhance our brand in these new markets or our reputation is damaged in our existing markets as a result of product defects or recalls, we may face difficulty in maintaining our pricing positions with respect to some of our products or experience reduced demand for our products, which could negatively impact our business, results of operations and financial condition.

Our brand and reputation are dependent on the continued participation and level of service of our numerous independent distributors and dealers.

We work with a network of approximately 1,400 independent distributors and dealers that provide post-sale service and parts and support equipment. Because we depend on the pull-through demand generated by end users for our products, any actions by the independent distributors or dealers, which are not in our control, may harm our reputation and damage the brand loyalty among our customer base. In the event that we are not able to maintain our brand reputation because of the actions of our independent distributors and dealers, we may face difficulty in maintaining our pricing positions with respect to some of our products or have reduced demand for our products, which could negatively impact our business, results of operations and financial condition. In addition, if a significant number of independent dealers were to terminate their contracts, it could adversely impact our business, results of operations and financial condition.

In the event of a catastrophic loss of our key manufacturing facility, our business would be adversely affected.

While we manufacture our products in several facilities and maintain insurance covering our facilities, including business interruption insurance, a catastrophic loss of the use of all or a portion of one of our manufacturing facilities due to accident, labor issues, weather conditions, acts of war, political unrest, terrorist activity, natural disaster or otherwise, whether short- or long-term, would have a material adverse effect on our business, results of operations and financial condition. Our most significant concentration of manufacturing is around our corporate headquarters in Indianapolis, Indiana where we produce approximately 90% of our transmissions. In addition to our Indianapolis manufacturing facilities, we currently operate manufacturing facilities in both Szentgotthard, Hungary and Chennai, India. In the event of a disruption at the Indianapolis facilities, our other facilities may not be adequately equipped to operate at a level sufficient to compensate for the volume of production at the Indianapolis facility due to their size and the fact that they have not yet been tested for such significant increases in production volume.

We may not be successful in introducing our new products and responding to customer needs.

We currently have new products and technologies under development. The development of new products and technologies is difficult and the timetable for commercial release is uncertain, and we may not be successful in introducing our new products and responding to customer needs. In addition, it often takes significant time, in some cases multiple fleet buy cycles, before customers gain experience with new products and technologies and those new products and technologies become widely-accepted by the market. If we do not adequately anticipate the changing needs of our customers by developing and introducing new and effective products and technologies on a timely basis, our competitive position and prospects could be harmed. If our competitors are able to respond to changing market demands and adopt new technologies more quickly than we do, demand for our products could decline, our competitive position could be harmed, and we will not be able to recoup a return on our development investments. Moreover, changing customer demands as well as evolving safety and environmental standards could require us to adapt our products and technologies to address such changes. As a result, in the future we may experience delays in the introduction of some or all of our new products or modifications or enhancements of existing products. Furthermore, there may be production delays due to unanticipated technological setbacks, which may, in turn, delay the release of new products to our end users. If we experience significant delays in production, our net sales and results of operations may be materially adversely affected.

Our success depends on continued research and development efforts, the outcome of which is uncertain.

Our success depends on our ability to improve the efficiency and performance of our transmissions, and we invest significant resources in research and development in order to do so. Nevertheless, the research and development process is time-consuming and costly, and offers uncertain results. We may not be able through our research and development efforts to keep pace with improvements in transmission-related technology of our competitors, and licenses for technologies that would enable us to keep pace with our competitors may not be available on commercially reasonable terms if at all. Finally, our research and development efforts, and generally our ability to introduce improved products in the marketplace, may be constrained by the patents and other intellectual property rights of competitors and others.

Our international operations, in particular our emerging markets, are subject to various risks which could have a material adverse effect on our business, results of operations and financial condition.Our business is subject to certain risks associated with doing business internationally, particularly in emerging markets. Outside-North America net sales represented approximately 19%23% of our net sales for 2015.2018. Most of our operations are in the U.S., but we also have manufacturing and customization facilities in India and Hungary with a services agreement with Opel Szentgotthard Automotive Manufacturing Ltd., formerly GM-PTH, and customization capability in Brazil, The Netherlands, China and Japan. Further, we intend to continue to pursue growth opportunities for our business in a variety of business environments outside the U.S., which could exacerbate the risks set forth below. Our international operations are subject to, without limitation, the following risks:the burden of complying with multiple and possibly conflicting laws and any unexpected changes in regulatory requirements;

Labor unrest

As

In addition to our unionized work force, manysome of our direct and indirect customers and vendors have unionized work forces. Strikes, work stoppages or slowdowns experienced by these customers or vendors or their other suppliers could result in slowdowns or closings of assembly plants that use our products or supply materials for use in the production of our products. Organizations responsible for shipping our products may also be impacted by strikes. Any interruption in the delivery of our products could reducehave reduced demand for our products, andwhich could have a material adverse effect on us.

In general, we consider our labor relations with all of our employees to be good. However, in the future we may be subject to labor unrest. The inability to reach a new agreement could delay or disrupt our operations in the affected regions, including the acquisition of raw materials and components, the manufacture, sales and distribution of products and the provision of services. If strikes, work stoppages or lock-outs at our facilities or at the facilities of our vendors or customers occur or continue for a long period of time,negatively impact our business, results of operations and financial conditioncondition. In addition, if a significant number of independent dealers were to terminate their contracts, it could adversely impact our business, results of operations and financial condition.

Increases in cost, disruption of supply or shortage of raw materials or components used in

Our products contain various raw materials, including corrosion-resistant steel, non-ferrous metals such as aluminum and nickel, and precious metals such as platinum and palladium. Weinterruption insurance, a catastrophic loss of the use raw materials directly inof all or a portion of one of our manufacturing and in transmission components that we purchase from our suppliers. We generally purchase components with significant raw material content on the open market. The prices for these raw materials fluctuate depending on market conditions. Volatility in the pricesfacilities due to accident, labor issues, weather conditions, acts of raw materials such as steel, aluminum and nickel could increase the cost of manufacturing our products. We may not be able to pass on these costs to our customers, and this couldwar, political unrest, terrorist activity, natural disaster or otherwise, whether short- or long-term, would have a material adverse effect on our business, results of operations and financial condition. EvenOur most significant concentration of manufacturing is around our corporate headquarters in the event that increased costs can be passed throughIndianapolis, Indiana, where we produce approximately 90% of our transmissions. In addition to customers, our gross margin percentages would decline. Additionally, our suppliers are also subject to fluctuationsIndianapolis manufacturing facilities, we currently operate manufacturing facilities in the prices of raw materialsboth Szentgotthard, Hungary and may attempt to pass all or a portion of such increases on to us.Chennai, India. In the event they are successful in doing so, our margins would decline.

In 2015, approximately 75% of our total spending on components was sourced from approximately 40 suppliers, some of which are the single source for such components. All of the suppliers from which we purchase materials and components used in our business are fully validated suppliers, meaning the suppliers’ manufacturing processes and inputs have been validated under a production part approval process (“PPAP”). Furthermore, there are only a limited number of suppliers for certain of the materials used in our business, such as corrosion-resistant steel. As a result, our business is subject to the risk of additional price fluctuations and periodic delays in the delivery of our materials or components if supplies from a validated supplier are interrupted and a new supplier, if one is available, must be validated or materials and components must be purchased from a supplier without a completed PPAP. Any such price fluctuations or delays, if significant, could harm our profitability or operations. In addition, the loss of a supplier could result in significant material cost increases or reducedisruption at the Indianapolis facilities, our production capacity. We also cannot guarantee we will be able to maintain favorable arrangements and relationships with these suppliers. An increase in the cost or a sustained interruption in the supply or shortage of some of these raw materials or components that may be caused by a deterioration of our relationships with suppliers or by events such as natural disasters, power outages, labor strikes, or the like could negatively impact our business, results of operations and financial condition. Although we have agreements with many of our customers that we will pass such price increases through to them, such contracts may be cancelled by our customers and/or weother facilities may not be ableadequately equipped to recoupoperate at a level sufficient to compensate for the costsvolume of production at the Indianapolis facility due to their size and the fact that they have not yet been tested for such price increases. Additionally, if we are unable to continue to purchase our required quantities of raw materials on commercially reasonable terms, or at all, if we are unable to maintain or enter into purchasing contracts for commodities, or if delivery of materials from suppliers is delayed or non-conforming, our operations could be disrupted or our profitability could be adversely impacted.

We could be materially adversely affected by any failure to maintain cost controls.

We rely on our cost structure and operating discipline to achieve strong operating margins. There are many factors that could affect our ability to realize expected cost savings or achieve future cost savings that we are not able to control, including the inability to meet demand through our low-cost country sourcing initiatives; the need for unexpected significant capital expenditures; unexpected changesincreases in commodity or component pricing that we are unable to pass on to our suppliers or customers; our inability to maintain efficiencies gained from our workforce optimization initiatives; and our failure to achieve and maintain expected cost savings from our multi-tier wage and benefit structure. Additionally, we have substantial indebtedness of approximately $2,402.8 million as of December 31, 2015. Our inability to maintain our cost controls could adversely impact our operating margins.

production volume.

is limited.

$93 million.

GM performed

The result of, or expiration of the statute of limitations for, such audits could have an impact on reported net income and cash flow from operations.

GM’s actions may materially affect our business and operating results.

Although we are an independent company as a result of the Acquisition Transaction, GM’s future actions may still have a material impact on our business and results of operations. Pursuant to the Cure Agreement after GM’s emergence from bankruptcy in 2009, GM has assumed certain agreements from its predecessor, including the asset purchase agreement, intellectual property and software license agreements and a hybrid co-branding agreement. GM’s failure to comply with any portion of these agreements for any reason, including the indemnities therein, could inhibit us from operating and expanding our business in the future.

Additionally, GM has received a non-exclusive, royalty-free, worldwide license to use the “Allison Transmission” name and certain related trademarks on GM’s line of A1000 transmissions for use primarily in Class 2 and 3 pick-up trucks. If GM, or any of its subsidiaries or affiliated entities, or any third party uses the trade name “Allison Transmission” in ways that adversely affect such trade name or trademark, our reputation could suffer damage, which in turn could have a material adverse effect on our business, results of operations and financial condition.

In connection with the Acquisition Transaction, we entered into a mutual non-compete agreement with GM that restricts GM from competing with us in non-defense vehicles in North America with gross vehicle weights above 5900 kilograms (typically Class 4 and higher) with some limited exceptions for certain GM light-duty pickup truck and van platforms. It also restricts GM from competing with us in defense vehicles globally and in non-defense vehicles outside North America that exceed 4250 kilograms (generally Class 3 to Class 4 and higher) with some limited exceptions. The non-compete periods extend until August 2017 globally, except in Europe, where they expired in 2012. Similarly, we are restricted from competing with GM in weight classes below the above mentioned thresholds for similar periods of time. Upon expiration of the non-competition periods, both Allison and GM will be permitted to compete with each other but such expiration will generally not affect Allison’s rights under the Patent and Technology License Agreement to use on an exclusive basis within its respective weight classes (subject to previously mentioned exceptions) the intellectual property that is licensed to Allison on an exclusive basis.

In addition, because of our current manufacturing services agreement with Opel Szentgotthard Automotive Manufacturing Ltd., a GM subsidiary, we may be materially adversely affected by the failure of GM to perform as expected. This non-performance may consist of delays or failures caused by production issues. The risk of non-performance may also result from the insolvency or bankruptcy of GM. GM’s ability to provide personnel and technical resources to us is also subject to a number of risks, including destruction of our equipment or work stoppages. In addition, our failure to provide an adequate facility, or order sufficient quantities of inventory, may increase the cost of production or may lead to GM refusing to provide resources to us at all. Our efforts to protect against and to minimize these risks may not always be effective.

Our annual goodwill impairment test for 2015 resulted in no goodwill impairment. Although our analysis regarding the fair value of goodwill indicates that it exceeds its carrying value, materially different assumptions regarding the future performance of our business could result in goodwill impairment losses. A review of our trade name in 2015 resulted in an impairment charge of $80.0 million. The impairment charge was triggered principally by lower forecasted net sales for certain of our end markets in the fourth quarter of 2015. The effects of the impairment did not result in any other charges to goodwill, other intangible assets or long-lived assets. See NOTE 2 “Summary of Significant Accounting Policies” and NOTE 56 “Goodwill and Other Intangible Assets” of Notes to Consolidated Financial Statements included in Part II, Item 8 of this Annual Report on Form 10-K for additional details.

Resources” of this Annual Report on Form 10-K.

Facility, the indenture governing the 5.0% Senior Notes and the indenture governing the 4.75% Senior Notes as well as any future agreements.

UNRESOLVED STAFF COMMENTSITEM 1B. Unresolved Staff CommentsNone.