(“CODM”) utilizes information provided to allocate resources and make decisions. Our two reportable segments are the similarityVacuum & Analysis segment and the Light & Motion segment. The Vacuum & Analysis segment represents the legacy MKS business and the Light & Motion segment represents the legacy Newport business.

The Vacuum & Analysis segment provides a broad range of product function. These three groups of products are: Instruments, Controlinstruments, components and Vacuum Products; Power and Reactive Gas Products; and Analytical Solutions Products. Our productssubsystems which are derived from our core competencies in pressure measurement and control, materialsflow measurement and control, gas and vapor delivery, gas composition analysis, residual gas analysis, leak detection, control technology, ozone generation and information technology,delivery, RF & DC power, and reactive gas generation and vacuum technology. OurThe Light & Motion segment provides a broad range of instruments, components and subsystems which are derived from our core competencies in lasers, photonics,sub-micron positioning, vibration control, and optics.

We group our products are used in diverse markets, applications and processes. Our primary served markets are manufacturers of capital equipment for semiconductor devices, and for other thin film applications, including flat panel displays, solar cells light emitting diodes (“LEDs”), data storage media, and other advanced coatings. We also leverage our technology in other markets with advanced manufacturing applications, including medical equipment, pharmaceutical manufacturing, energy generation and environmental monitoring.

Effective January 1, 2015, we changed the structure of our reportable segmentsinto six product groups based upon how the information is provided to our Chief Operating Decision Maker. Our four reportable segments prior to the change in structure were: Advanced Manufacturing Capital Equipment, Analytical Solutions Group, Europe Region Sales & Service and Asia Region Sales & Service. Our current structure still reflects four reportable segments, however, the compositionsimilarity of the segments has changed.

Our current reportable segmentsproduct function, type of product and manufacturing processes. These six groups are: Analytical and Controls Solutions Products; Power, Plasma and Reactive Gas Solutions Products; Vacuum Solutions Products; Photonics Products; Optics Products; and Laser Products. The Analytical and Controls Solutions Products, the Power, Plasma and Reactive Gas Solutions Products and the Vacuum Solutions Products are Advanced Manufacturing Capital Equipment, Global Service, Asia Region Sales and Other. The primary change to the segment structure was to separate worldwide service from product sales and create a separate reportable segment known as Global Service. Product salesincluded in the Advanced Manufacturing Capital Equipment segment remained with that segment. Asia product sales became a separate reportable segment. The product sales from the operating segments that made up the Analytical Solutions Group and Europe Region Sales were combined into the OtherVacuum & Analysis segment and the Photonics Products, Optics Products and Laser Products are not reported separately, as they are individually immaterial and collectively remain belowincluded in the separate segment guidelines. We report corporate expenses and certain intercompany pricing transactions in a Corporate and Eliminations reconciling column.Light & Motion segment.

The Advanced Manufacturing Capital Equipment segment includes the development, manufacture and sales of instruments, control and vacuum products; and power and reactive gas products, all of which are utilized in semiconductor processing and other similar advanced manufacturing processes. Sales in this segment include both external sales and intercompany product sales, which are recorded at transfer prices in accordance with applicable tax requirements. The Global Service segment includes the worldwide servicing of instruments,

control and vacuum products, power and reactive gas products and certain other product groups, all of which are utilized in semiconductor processing and other similar advanced manufacturing processes. The Asia Region Sales segment mainly includes sale of products that are re-sold from the Advanced Manufacturing Capital Equipment and Other segments into Asia regions. The Other segment includes operating segments that are not required to be reported separately as reportable segments and includes sales of products that are re-sold from the Advanced Manufacturing Capital Equipment into Europe regions as well as sales from other operating segments.

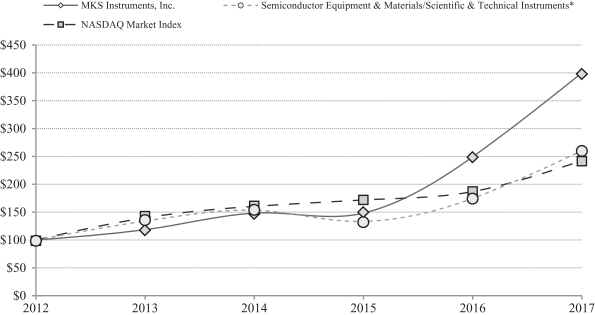

For further information on our segments, please see Note 2119 to the Notes to the Consolidated Financials contained in this Annual Report on Form10-K.

Since our inception, we have focused on satisfying the needs of our customers by establishing long-term, collaborative relationships. We have a diverse base of customers that includes manufacturers of semiconductor capital equipment and semiconductor devices; thin film equipment, process industries, environmental monitoring, life science and other advanced manufacturing companies, as well as university, government and industrial research laboratories.

We file reports, proxy statements and other documents with the Securities and Exchange Commission (“SEC”). You may read and copy any document we file at the SEC Headquarters at the Office of Investor Education and Assistance,SEC’s Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. You should call1-800-SEC-0330 for more information on the public reference room. Our SEC filings are also available to you on the SEC’s internet site at http://www.sec.gov.

Our internet addresswebsite is http://www.mksinst.com. We are not including the information contained in our website as part of, or incorporating it by reference into, this annual report on Form10-K. We make available free of charge through our internet site our annual reportsAnnual Reports on Form10-K, quarterly reports Quarterly Reports on Form10-Q, current reports Current Reports on Form8-K and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), as soon as reasonably practicable after we electronically file such materials with, or furnish them to, the SEC.

Recent Events

On February 23, 2016, we announced that we had entered into a definitive agreement to acquire Newport Corporation (“Newport”), a worldwide leader in photonics solutions. Pursuant to the merger agreement, and subject to the terms and conditions contained therein, at the closing of the acquisition, we will acquire all of the outstanding shares of Newport for a purchase price of approximately $980 million in cash. The parties’ obligations to consummate the acquisition are subject to customary closing conditions, including required approvals for the transaction from governmental authorities and approval from Newport’s shareholders. Our obligations under the merger agreement are not subject to any financing condition.

Markets and Applications

We areSince our inception, we have focused on improving process performancesatisfying the needs of our customers by establishing long-term collaborative relationships. We have a diverse base of customers and productivity by measuring, controlling, powering, monitoringour primary served markets are manufacturers of capital equipment for semiconductor manufacturing, industrial technologies, life and analyzing advanced manufacturing processes in semiconductor, thin filmhealth sciences, as well as research and certain other advanced market sectors.defense. Approximately 69%57%, 70%56% and 68%69% of our net revenues for the years 2015, 20142017, 2016 and 2013,2015, respectively, were from sales to semiconductor capital equipment manufacturers and semiconductor device manufacturers. As a result of our acquisition of Newport, we estimate that sales to semiconductor capital equipment manufacturers and semiconductor device manufacturers could account for more than 50% of our total sales in future periods.

Approximately 31%43%, 30%44% and 32%31% of our net revenues in the years 2015, 20142017, 2016 and 2013,2015, respectively, were from other advanced manufacturing applications. These include, but are not limited to, thin film processing equipment applications such as flat panel displays; LEDs, solar cells, data storage mediaindustrial technologies, life and other thin film coatings;health sciences, as well as medical equipment, pharmaceutical manufacturing, energy generationresearch and environmental monitoring processes; other industrial manufacturing; and university, government and industrial research laboratories.defense.

DuringA significant portion of our net revenues are from sales to customers in international markets. For the years 2015, 20142017, 2016 and 2013,2015, international net revenues accounted for approximately 44%50%, 43%48% and 46%44% of our total net revenues, respectively. NetA significant portion of our international net revenues from ourwere in South Korea, Japan, Israel