| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

28, 2017

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| Bermuda | 77-0481679 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

Title of each class | Name of each exchange on which registered | |

Common shares, $0.002 par value per share | The NASDAQ Stock Market LLC | |

Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ | |||

(Do not check if a smaller reporting company) | ||||||

None

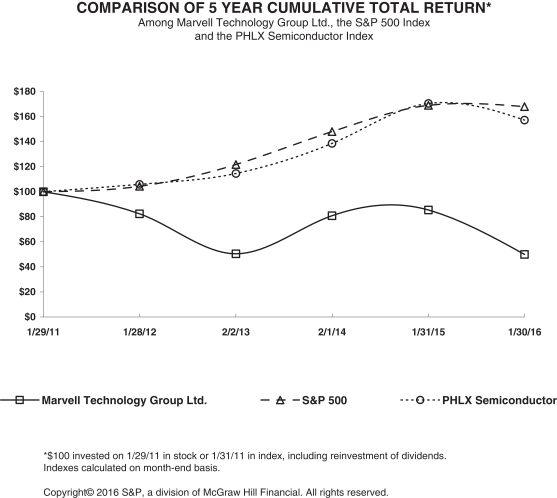

Item 5. Item 6. Item 7. Item 7A. Item 8. Item 9. Item 10. Item 11. Item 12. Item 13. Item 14. Item 15. The integration of these various technologies onto a single piece of silicon is referred to as SoC. Storage Mobile and Wireless Networking Other Total We are a leading HDD controller supplier and currently supply products to all of the major hard drive manufacturers. Our HDD controllers with advanced Our advanced HDD controller SoCs are designed incorporating the latest Marvell IPs using leading advanced semiconductor process Solid-State Drive Controllers We are a leading supplier of SSD controllers across a range of customers and market segments. Our advanced SSD controller SoCs Our SSD controllers are complemented by our fully featured complete customer solution. & Custom ASIC Internet of Things solutions. See “Risk Factors” under Item 1A of this Annual Report on Form 10-K for a discussion of the risks associated with our international operations. groups. End Customer: Western Digital Seagate Distributor: Wintech an industry practice that allows customers to cancel or change orders prior to the scheduled shipment dates; an increasing portion of our revenue comes from products shipped to customers using third-party logistics providers, or “hubs” wherein the product can be pulled at any time by the customer and is therefore never reflected in backlog; and scheduled future shipments include shipments to distributors for which we do not recognize revenue until the products are sold to end customers. lowest power. We devote a significant portion of our resources to expanding our product portfolio based on a broad intellectual property portfolio with designs that enable high-performance, reliable communications over a variety of physical transmission media. We are also focused on incorporating functions currently provided by stand-alone integrated circuits into our integrated platform solutions to reduce our customers’ overall system costs. development expenses in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, of this Annual Report on Form 10-K for further information. property. acquiring existing technology. We believe that our ability to compete successfully in the rapidly evolving markets for our products depends on a number of factors, including, The performance, features, quality and price of our products; The timing and success of new product introductions by us, our customers and our competitors; Our ability to obtain adequate foundry The number and nature of our competitors in a given market. for our products include Broadcom Limited, Cavium, Inc., MediaTek, Inc., QUALCOMM, Inc., Quantenna Communications Inc. and Silicon Motion Technology Corporation. We expect increased competition in the future from emerging or established companies, or alliances among competitors, customers or other third parties, any of which could acquire significant market share. changes in general economic and political conditions and specific conditions in the end markets we address, including the continuing volatility in the technology sector and semiconductor industry; the highly competitive nature of the end markets we serve, particularly within the semiconductor industry; our dependence on a few customers for a significant portion of our revenue; cancellations, rescheduling or deferrals of significant customer orders or shipments, as well as the ability of our customers to manage inventory; gain or loss of a design win or key customer; seasonality in sales of consumer devices in which our products are incorporated; failure to qualify our products or our suppliers’ manufacturing lines; our ability to develop and introduce new and enhanced products in a timely and effective manner, as well as our ability to anticipate and adapt to changes in technology; failure to protect our intellectual property; impact of a significant natural disaster, including earthquakes, floods and tsunamis, particularly in certain regions in which we operate or own buildings, such as Santa Clara, California and where our third party suppliers operate, such as Taiwan and elsewhere in the Pacific Rim; and our ability to attract and retain a highly skilled workforce, especially managerial, engineering, sales and marketing personnel. As the technology inflections happen, our competitors may get ahead of us and negatively impact our market share. Unlike in the HDD industry, SSD customers may develop their own controllers, which could pose a challenge to our market share in the SSD space. substantially and our results of operations and financial condition may be harmed. condition. customer relationships. In addition, any future significant cancellations or deferrals of product orders or the return of previously sold products could materially and adversely affect our profit margins, increase product obsolescence and restrict our ability to fund our operations. The occurrence of any or a combination of the additional risks described below would significantly and negatively impact our business and results of operations. 2016. complying (including the costs of any investigations, auditing and monitoring) with these laws could adversely affect our current or future business. In addition, future regulations may become more stringent or costly and our compliance costs and potential liabilities could increase, which may harm our current or future business. As we carry only limited insurance coverage, any incurred liability resulting from uncovered claims could adversely affect our financial condition and results of operations. be no assurance that we will effect on our share price. include authorizing the issuance of preferred shares without shareholder First Quarter Second Quarter Third Quarter Fourth Quarter Marvell Technology Group Ltd. S&P 500 PHLX Semiconductor 2015. of $15.91. Consolidated Statements of Operations Data: Net revenue Cost of goods sold Research and development Operating income (loss) Net income (loss) Net income (loss) per share: Basic Diluted Weighted average shares: Basic Diluted Consolidated Balance Sheet Data: Cash, cash equivalents and short-term investments Working capital Total assets Total shareholders’ equity Other Data: Cash dividends declared per share Number of employees Restructuring. In $105.2 million. In Capital Return Program.We believe our financial position is strong and we remain committed to deliver shareholder value through our share repurchase and dividend programs. Our cash, cash equivalents and short-term investments were 28, 2017. We Consequently, if anticipated sales and shipments in any quarter do not occur when expected, expenses and inventory levels could be disproportionately high, and our operating results for that quarter and future quarters may be adversely affected. realized. Using available evidence and judgment, we establish a valuation allowance for deferred tax assets, when it is determined that it is more likely than not that they will not be realized. Valuation allowances have been provided primarily against the U.S. research and development credits. Valuation allowances have also been provided against certain acquired operating losses and the deferred tax assets of future product demand, any significant unanticipated changes in demand or technological developments could have a significant impact on the value of our inventory and our results of operations. significant decreases in the market price of the asset; significant adverse changes in the business climate or legal factors; accumulation of costs significantly in excess of the amount originally expected for the acquisition or construction of the asset; current period cash flow or operating losses combined with a history of losses or a forecast of continuing losses associated with the use of the asset; and current expectation that the asset will more likely than not be sold or disposed of significantly before the end of its estimated useful life. significant underperformance relative to historical or projected future operating results; significant changes in the manner of our use of the acquired assets or the strategy for our overall business; significant negative industry or economic trends; a significant decline in our stock price for a sustained period; and Page Page Item 1. Item 1A. Item 1B. Item 2. Item 3. Item 4. Item 1.2Item 1A.12Item 1B.31Item 2.32Item 3.32Item 4.32PART II3336375557Item 9A. Item 9B. 110Item 9A.110Item 9B.115PART III118122154157 159PART IV 161162EXPLANATORY NOTEAs previously reported, we were unable to timely file our Quarterly Reports on Form 10-Q for the second and third quarters of fiscal 2016 ended August 1, 2015 and October 31, 2016, respectively, and our Annual Report on Form 10-K for the fiscal year ended January 30, 2016, as a result of the resignation of our independent registered public accounting firm and an Audit Committee investigation as described herein. As previously reported and further set forth herein, we retained Deloitte & Touche LLP as our independent registered public accounting firm and the Audit Committee subsequently completed its investigation. This Form 10-K is being filed concurrently with our Quarterly Reports on Form 10-Q for the periods ended August 1, 2015 and October 31, 2015, respectively.•our dependence upon the hard disk drive and wireless markets, which are highly cyclical and intensely competitive;•the outcome of pending or future litigation and legal proceedings;•our dependence on a small number of customers;•our ability and the ability of our customers to successfully compete in the markets in which we serve;•our reliance on independent foundries and subcontractors for the manufacture, assembly and testing of our products;•our ability and our customers’ ability to develop new and enhanced products and the adoption of those products in the market;•decreases in our gross margin and results of operations in the future due to a number of factors;•our ability to estimate customer demand and future sales accurately;•our ability to scale our operations in response to changes in demand for existing or new products and services;•the impact of international conflict and continued economic volatility in either domestic or foreign markets;•the effects of transitioning to smaller geometry process technologies;•the risks associated with manufacturing and selling a majority of our products and our customers’ products outside of the United States;•the impact of any change in our application of the United States federal income tax laws and the loss of any beneficial tax treatment that we currently enjoy;•the effects of any potential acquisitions or investments;•our ability to protect our intellectual property;•our ability to regain compliance with our NASDAQ listing qualifications;•the impact and costs associated with changes in international financial and regulatory conditions; and•our maintenance of an effective system of internal controls.Item 1. Business and System-in-a-Package (“SiP”) devices, leveraging our extensive technology portfolio of intellectual property in the areas of analog, mixed-signal, digital signal processing, and embedded and standalone integrated circuits. The majority of our product portfolio leverages embedded central processing unit technology. We also develop platforms that we define as integrated hardware platforms along with software that incorporates digital computing technologies designed and configured to provide an optimized computing solution. Our broad product portfolio includes devices for data storage, enterprise-class Ethernet data switching, Ethernet physical-layer transceivers (“PHY”), wireless connectivity, Internet-of-Things (“IoT”) devicesnetworking and multimedia solutions.connectivity. We were incorporated in Bermuda in January 1995.Italy, Japan, Malaysia, Singapore, South Korea, Spain, SwitzerlandTaiwan and Taiwan.Vietnam. Our fiscal year ends on the Saturday nearest January 31. For example, the fiscal year ended January 30, 2016 is referred to as fiscal 2016.inon our website does not form any part of this Annual Report on Form 10-K. However, we10-K and is not incorporated by reference herein. We make available free of charge through our website our annual reports on Form 10-K, our quarterly reports on Form 10-Q, our current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), as soon as reasonably practicable after we electronically file this material with, or furnish it to, the U.S. Securities and Exchange Commission (“SEC”).solution compared to individual components.solution. Our solutions have become increasingly integrated, with more and more components resulting in an all-in-one solution for a given customer’s end product. The demand for such highly integrated platform solutions is generally driven by technological changes and anticipation of the future needs of device manufacturers and end users, as well as,including enterprises, campus and service provider networks and, to an increasing extent, service providers, including cellular network carriers and Internet-based applicationsdata center providers.high-definition graphics processing, high-definition video and audio, and power management. These platforms will often cross multipletechnologies leveraged from one end market product into products for other end markets, integrating components and technologies traditionally associated with one end market with components and technologies from another end market. For example, we may integrate an applications processor, traditionally associated with the mobile and wireless end market, with software and other components in an end user product targeting the home cloud. Therefore, it has become critical that our products across multiple end markets work together seamlessly. The development of SoCs became in high demand over the past decade, with strong market presence in networkingand cloud infrastructure, storage, multimedia and custom specific product solutions. We believe the development of SoCs will continue to grow as more complex chips can be delivered to the different end markets in the years to come.expectbelieve software towill become even more relevant as the market expects hardware and software to be delivered as aan integrated solution offering. On-chip software, which acts as the “driver” for the functionality of the chip, has always been a critical part of our business. However, the software and application-level software that we deliver with our chipproducts has become significantly more complex as the range of uses and the needs in application-level software havehas increased. For example, a chipsolution that we develop for storage or networking can contain software that already has a range of functionalities included, or itbuilt in. Alternatively, our solution can offer abilities thatallow our customers to deploy in their operative systemsystems on top of our chip, as well as deploying indeploy their application software on top of it.The products that we developour SoC.targeted for several key end markets and applications:primarily in three broad product groups: storage, networking and cloud infrastructure, wireless connectivity, multimedia and IoT.connectivity. In storage, we are a market leader in data storage controller solutions spanning consumer, mobile, desktop and enterprise markets. Our storage solutions enable customers to engineer high-volume products for hard disk drives and solid state drives. In IoT, we develop flexibleOur networking products address end markets in cloud, enterprise, small and cost-effective platforms that enable original equipment manufacturers (“OEM”)medium business and original design manufacturers (“ODM”) to quicklyservice provider networks. Our connectivity products address end markets in consumer, enterprise, desktop, service provider networks and cost-effectively reach the market with new, innovative products in this rapidly growing space. We provide a range of silicon and software solutions that enable applications such as wearables, home automation, home security, smart appliances and automotive. For networking and cloud infrastructure, our products and solutions are designed for reliability and resiliency. From robust enterprise networking applications to consumer and small business solutions, our cloud services products power every point in the cloud and networking ecosystem. Our storage, networking multimedia, wirelessand connectivity and video processing products power cutting-edge consumernetworks and digital entertainmentdata centers around the world. The networking & connectivity product groups were previously referred to as smart networked devices empowering consumers to manage and consume content at home or onsolutions.go.AllNovember 2016 announcement of our products are built on the foundation of innovation,plan to restructure our operations to refocus our research and development, increase operational efficiency and improve profitability, we also plan to divest certain businesses and we continuebegan an active program to develop newlocate buyers for several businesses. As of January 28, 2017, two of these businesses were classified as discontinued operations. As required, we retrospectively recast our consolidated statements of operations and cutting-edge technologybalance sheets for all periods presented to enablereflect these businesses as discontinued operations. Unless noted otherwise, the following discussion refers to our customers’ applications. In fiscal 2016, we developed two technologies that have the potential to revolutionize integrated circuit design by decreasing the cost, complexity, power and form factor of next-generation systems and chips. Our Final-Level Cache (“FLCTM”) architecture redefines the main memory hierarchy by substantially reducing the amount of dynamic random access memory needed in a system. Our Modular Chip (“MoChi TM”) technology enables the building of virtual SoCs by connecting together a set of MoChi TM in a modular fashion to implement a final product. Both FLC TM and MoChi TM technologies may become integral parts of our product evolution in the future.Our current product offerings are primarily in three broad end markets: storage, networking, and mobile and wireless.continuing operations. Our net revenue by end marketproduct group for the last three fiscal years is as follows: Year Ended January 30,

2016 January 31,

2015 February 1,

2014 (in millions, except for percentages) $ 1,201 44 % $ 1,745 47 % $ 1,682 49 % 786 29 % 1,072 29 % 839 25 % 552 20 % 675 18 % 670 20 % 187 7 % 215 6 % 213 6 % $ 2,726 $ 3,707 $ 3,404 Year Ended January 28, 2017 January 30, 2016 January 31, 2015 (in millions, except for percentages) Storage $ 1,158 50 % $ 1,201 45 % $ 1,745 48 % Networking 590 25 % 532 20 % 661 18 % Connectivity 318 14 % 441 17 % 530 15 % Other 252 11 % 475 18 % 701 19 % Total $ 2,318 $ 2,649 $ 3,637 (“HDD”("HDD") controllers provide high-performance input/output (“I/O”)(I/O) interface control between the HDD and the host system. We support a variety of host system interfaces, including serial advanced technology attachment (“SATA”), statistical analysis system (“SAS”), peripheral component interconnect express (“PCIe”)SATA (Serial Advanced Technology Attachment) and universal serial bus (“USB”)SAS (Serial Attached SCSI), which supportssupport the complete range of enterprise, desktop and mobile HDDs.1 terabyte-per-platter technology for mobile HDDs provide a technological advantage that enablesenable a higher level of data storage on smaller form factors and higher volumetric densities.nodes, including Taiwan Semiconductor Manufacturing Company’s (“TSMC”) 16nm FinFet Compact (“FFC”) process node, resulting in the smallest die size, lowest power dissipation and highest performance.•We provide advanced Hybrid HDD controller solutions based on our solid state drive (“SSD”) forward flash based concepts utilizing our SSD controller SoCs and Marvell’s differentiated and patented FLC and MoChiTM technologies. Our Hybrid SSDs provide SSD like performance with HDD cost structures.Our Hybrid HDD solutions incorporate hardware accelerated advanced caching algorithms and are supported by our full turnkey (“FTK”) software system solutions.SSDsolid-state- drive ("SSD") controller SoCs are targeted at the fast growing market for flash-based storage systems, for the cloud, enterprise, consumer and mobile computing markets, as well as for smartphones and tablets.markets. We support a variety of host system interfaces, including SAS, SATA, PCIe,peripheral component interconnect express ("PCIe"), and non-volatile memory express (“NVMe”("NVMe") and emerging mobile standards..are designed incorporatingincorporate the latest Marvell technology using leading advanced process nodes, including TSMC’s 16nm FFC process node, resulting to the smallest die size, lowest power dissipation and leading performance.softwareSDK (software development kitkit) and FTK (Full Turnkey software solutions. We are currently in production using our controllers and FTKs with a number of customers.•We are also designing future SSD controllers incorporating our differentiated and patented FLC and MoChiTM technologies.2016,2017, Marvell re-entered the HDD preamps and motor combo drivers business. We are working with a number of customers in developing and qualifying our components.software enabledsoftware-enabled silicon solutions for enterprise, data centers and cloud computing businesses. The solutions include SATA port multipliers, bridges, SATA, SAS and NVMe redundant array of independent disksdisk controllers and converged storage processors.aSwitchesswitches with market optimized advancedmarket-optimized innovative features, such as audio video bridgingadvanced tunneling and network traffic management,routing, high throughput forwarding and packet processing that make networks more effective at delivering content, and rangecontent. Our Ethernet switch product portfolio ranges from low-power, five portfive-port switches to highly integrated, multi terabitmulti-terabit Ethernet SoC devices that can be interconnected to form massive network solutions;aA broad selection of Ethernet Transceiversphysical-layer transceivers for both fiber and copper interconnect with advanced power management, link security and time synchronization features that complement our Ethernet Switchswitch and Embedded Communication Processors;embedded communication processors; andaA family of single-chip network interface devices offered in ultra-small form factor with low-power consumption and targeted for client-server network interface cards.multi-processor architecturesmulti-core ARM processor architecture optimized to consume low power while simultaneously delivering high-performance per watt. They provide a combination of I/O peripherals, including Ethernet, SATA, SAS, PCIe and USBuniversal serial bus and are ideally suited tofor a range of end-customer networking applications, such as home gateways, networked storage, point-of-service terminals,control plane applications, routers, switches and wireless applicationaccess points and base stations.Network ProcessorsOur family of Network Processors offers high-performance-per-watt programmable solutions ideally suited to applications where flexible functionality for differentiated, value-add solutions and enhanced quality of service are essential, such as in carrier Ethernet access, aggregation, mobile backhaul, transport and mobile cloud platforms. They also offer 1G through 100G Ethernet connectivity into a multi-hundred gigabit Ethernet pipeline that has deterministic performance and ideally suited for software-defined networking.Mobile and WirelessCommunications and Applications ProcessorsWe offer “thin modems,” highly optimized multi-mode baseband modem devices without an application processor. In September 2015, we announced a significant restructuring of our mobile platform business in order to focus research and development on more profitable opportunities and align our expenses with corporate targets. As a result, we have discontinued the development and marketing of our communications and applications processors targeted for mobile handsets.varietybroad portfolio of connectivity solutions, including Wi-Fi, and Wi-Fi/Bluetooth global positioning system (“GPS”) and ZigBee.integrated SOCs. These products are integrated into a wide variety of end devices, such as enterprise access points, home gateways, multimedia devices, gaming, devices, printers, enterprise solutions, video dongles tablets, in-carautomotive infotainment and telematics units, and smart appliances.industrial devices. Our products are well positionedwell-positioned to deliver low-power and high-performance functionality with cutting-edge technologies, and to lead the latest technologies that follow evolutionfast-paced developments of IEEE 802.11standards. We have a broad wirelessWi-Fi 802.11 and Bluetooth standards. Our connectivity product portfolio that includes a single stream 1x1, as well as multi-stream 2x2 and 4x4 multiple input multiple output (“MIMO”) devices,devices. We deliver both the radio control and we are developing��58x8 MIMO 802.11ax solutions. Asprocessing as well as the RF components for a result of the restructuring of our mobile platform business announced in September 2015, our connectivity solutions are no longer being targeted for mobile phones.Mobile ComputingWe offer high-performance applications processors that are designed to deliver advanced integration, excellent multimedia performance and superior power consumption savings for mobile computing products. These products have been incorporated into tablets, notebooks, eReaders, gaming devices, scanners and educational devices.Other TechnologiesWe incorporate a variety of other technologies into our platforms, depending on the needs of our customers and their end products, including power management, GPS, radio frequency (“RF”) and memory. As a result of the restructuring of our mobile platform business announced in September 2015, we have also discontinued development and marketing of our power management, GPS, RF and memory into mobile platform designs.printerapplication-specific integrated circuits.Smart Home Productssmart home products are designed to enable the next generationseparate line of connected consumer platforms,application processors is targeted for non-mobile applications and to enhance the eco-friendly “Connected Lifestyle” throughout the home,deliver leading-edge performance for today’s embedded and include platforms for set-top boxes, video dongles such as Google Chromecast and smart appliances. business segment: the design, development and sale of integrated circuits. For information regarding our revenue by geographic area, and property and equipment by geographic area, please see “Note 13 — Segment and Geographic Information” in our Notes to the Consolidated Financial Statements set forth in Part II, Item 8 of this Annual Report on Form 10-K.As a fabless semiconductor company, ourOEMsoriginal equipment manufacturers and ODMs,original design manufacturers, both of which design and manufacture end market devices. Our sales force is strategically aligned along key customer lines in order to offer fully integrated platforms to our customers. In this way, we believe we can more effectively offer a broader set of content into our key customers’ end products, without having multiple product groups separately engage the same customer. We complement and support our direct sales force with manufacturers’ representatives for our products in North America, Europe and Asia. In addition, we have distributors who support our sales and marketing activities in the United States, Europe and Asia. We also use third-party logistics providers who maintain warehouses in close proximity to our customers’ facilities. We expect that a significant percentage of our sales will continue to come from direct sales to key customers.We believe that superior field applications engineering support plays a pivotal role in building long-term relationships withcustomers by improving our customers’ time-to-market, maintaining a high level of customer satisfaction and encouraging customers to use our next-generation products. Our marketing team works in conjunction with our field sales and application engineering force, and is organized around our product applications and end markets. Year Ended January 30,

2016 January 31,

2015 February 1,