(Mark One)

| ☑ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

2021

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

Inc.

Delaware | 62-1096725 | |||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification | |||||||

6210 Ardrey Kell Road, Suite 600 Charlotte, North Carolina | ||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

code)

Title of each class | Trading symbol | Name of each exchange on which registered | ||||||||||||

| Common Stock, par value $0.01 | NNBR | The | ||||||||||||

(Title of class)

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

| Large accelerated filer | ☐ | Accelerated filer | ☑ | ||||||||||||

| Non-accelerated filer | Smaller reporting company | ☑ | |||||||||||||

| ☐ | |||||||||||||||

The number of $7.35. Solely for purposes of making this calculation, shares of the registrant’s common stock outstanding onheld by named executive officers, directors and 5% or greater stockholders of the registrant as of such date have been excluded because such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for any other purposes.

4, 2022, there were 43,297,653 shares of the registrant’s common stock, par value $0.01 per share, outstanding.

Such proxy statement will be filed with the Securities and Exchange Commission within 120 days of the registrant’s fiscal year ended December 31, 2021.

PART I

| Page | ||||||||

All dollar amounts presented in tables that follow are in thousands (except for share data) unless otherwise indicated.

Our business is aggregated into three reportable segments, the Precision Bearing Components Group, the Precision Engineered Products Group and the Autocam Precision Components Group. Our business segments and acquisition activity are described further below.

Acquisition Activity

2015

On May 29, 2015, we completed the acquisition of Caprock Manufacturing, Inc. and Caprock Enclosures, LLC (collectively referred to as “Caprock”). Caprock was a privately held plastic components supplier located in Lubbock, Texas. Caprock serves multiple end markets; including aerospace, medical and general industrial. The acquisition provided further balancing of our end markets and represented the first step in our strategic plan related to transforming our plastics business. The results of Caprock have been consolidated with NN since the date of acquisition as part of the Precision Engineered Products Group.

On October 19, 2015, we completed the acquisition (the “PEP Acquisition”) of Precision Engineered Products Holdings, Inc. (“PEP”). As a result of the PEP Acquisition, PEP became a wholly owned subsidiary of NN. PEP is a global manufacturer of highly engineered precision customized solutions serving the medical, electrical, automotive and aerospace end markets. PEPthat combines in-depth materials science expertise with advanced engineering and production capabilities to design and manufacture a broad range of high-precision metal and plastic components and assemblies and finished devices. Following the PEP Acquisition and the divestiture of Delta Rubber Company (described below), we combined the operations of PEP with our Plastics and Rubber Components Group, and renamed the group as the Precision Engineered Products Group.

On November 30, 2015, we completed the divestiture of Delta Rubber Company, a wholly owned subsidiary (“Delta Rubber”). The sale of Delta Rubber was in furtherance of our strategic plan and provided further balance to our portfolio of businesses.

2014

On January 20, 2014, we acquired V-S Industries (“V-S”), a manufacturer of precision metal components with locations in Wheeling, Illinois and Juarez, Mexico. The acquisition of V-S provided us with a broader product offering, allowing for penetration into adjacent markets. V-S’s products serve a variety of industries including electric motors, HVAC, power tools, automotive and medical. V-S’s operations were integrated withend markets on a global basis. As used in this Annual Report on Form 10-K (this “Annual Report”), the Autocam Precision Components Group.

On June 20, 2014, we acquired RFK Industries (“RFK”terms “NN,” the “Company,” “we,” “our,” or the “Konjic Plant”), a manufacturer of tapered rollers located in Konjic, Bosnia and Herzegovina. RFK’s products are complementary“us” refer to our existing roller bearing products and broaden our product offerings and allows penetration into adjacent markets. RFK currently exports all of its products to customers serving the European truck, industrial vehicle and railway markets. RFK’s operations were integrated with our Precision Bearing Components Group.

On July 15, 2014, we acquired Chelsea Grinding Company (“Chelsea”)NN, Inc., a manufacturer of cylindrical rollers used primarily in the hydraulic pump industry. Following the acquisition of Chelsea, we relocated Chelsea’s operations to our Erwin, Tennessee plant. Chelsea’s operations were integrated with the Precision Bearing Components Group.

On August 29, 2014, we acquired Autocam Corporation (“Autocam”), a manufacturer of high precision metal components serving primarily the automotive and commercial vehicle HVAC and fluid power industries. Based in Kentwood, Michigan, Autocam manufactures and assembles highly complex, system critical components for fuel systems, engines, transmission, power steering and electric motors. Autocam and its subsidiaries employ over 2,100 employees with 15 manufacturingsubsidiaries. We have 31 facilities in the U.S.,North America, Europe, South America, and Asia. With

Corporate Information

We were founded in October 1980Power Solutions groups and are incorporatedbased principally on the end markets they serve.

Business Segments

Net sales, income from operations and assets for each of our business segments is presented in Management’s Discussion and Analysis of Financial Condition Results of Operations and Note 12 of the Notes to the Consolidated Financial Statements. Additional information regarding our three business segments (Precision Bearing Components Group, Precision Engineered Products Group and Autocam Precision Components Group) is presented below.

Precision Bearing Components Group

Within our Precision Bearing Components Group, we manufacture and supply high precision bearinginternal combustion engine vehicles. The group currently manufactures components consisting of balls, cylindrical rollers, tapered rollers, spherical rollers and metal retainers, for leading bearing and CV-joint manufacturers on a global basis. We are a leading independent manufacturer of precision steel bearing ballshigh-volume basis for use in power steering, braking, transmissions, and rollers forgasoline fuel system applications, along with components utilized in heating, ventilation and air conditioning and diesel injection and diesel emissions treatment applications. This expertise has been gained through investment in technical capabilities, processes and systems, and allows us to provide skilled program management and product launch capabilities.

Precision Engineered Products Group

Following the PEP Acquisition, we combined the operations of PEP with our Plastics and Rubber Components Segment. Within our Precision Engineered Products Group,this group we combine materials science expertise with advanced engineering and production capabilities to design and manufacture a broad range of high-precision metal and plastic components, assemblies, and finished devices for the medical, electrical, automotive and aerospace end markets.

Autocam Precision Components Group

Within our Autocam Precision Components Group, we manufacture highly engineered, difficult-to-manufacture precision metal components and subassemblies for the automotive, HVAC, fluid power and diesel engine end markets. Our entry into the precision metal components market began in 2006 with the acquisition of Whirlaway Corporation. We dramatically expanded the segment in 2014 with the acquisitions of Autocam and V-S. These acquisitions furthered our strategy to diversify our end markets and build upon our core manufacturing competency of high-precision metal machining.

Products

Precision Bearing Components Group

Precision Steel Balls. At our Precision Bearing Components Group facilities (with the exception of our Veenendaal plant), we manufacture and sell high quality, precision steel balls. Our steel balls are used primarily by manufacturers of anti-friction bearings and constant velocity joints where precise spherical, tolerance and surface finish accuracies are required.

Steel Rollers. We manufacture tapered rollers at our Veenendaal, Erwin, and Konjic plants and cylindrical rollers at our Erwin plant. Rollers are an alternative rolling element used instead of balls in anti-friction bearings that typically have heavier loading or different speed requirements. Our roller products are used primarily for applications similar to those of our precision steel ball product line, plus certain non-bearing applications such as hydraulic pumps and motors. Tapered rollers are a component in tapered roller bearings that are used in a variety of applications including automotive gearbox applications, automotive wheel bearingsranging from power control to flight control and a wide variety of industrial applications. Most cylindrical rollers are made to specific customer requirements for diameter and length and are used in a variety of industrial applications.

Metal Retainers. We manufacture and sell precision metal retainers for roller bearings used in a wide variety of industrial applications. Retainers are used to separate and space the rolling elements within a fully assembled bearing. We manufacture metal retainers at our Veenendaal plant.

Precision Engineered Products Group

Precision Solutions.military devices. We manufacture a variety of components, assemblies and instruments, such as surgical knives, bioresorbable implants, surgical staples, orthopedic system tools, laparoscopic devices, drug delivery devices and catheter components for the medical end market,products including electrical contacts, connectors, contact assemblies, and precision stampings for the electrical control end market, precision components, assemblies and electrical contacts for the automotive end market and a variety of engineered materialshigh precision products for the aerospace and defense end market includingutilizing our extensive process technologies for optical grade plastics, thermally conductive plastics, and titanium, Inconel, magnesium, and gold electroplating. At our Lubbock plant, we manufacture and sell precision plastic retainers for ball and roller bearings used inOur medical business includes the production of a wide variety of industrial applications. We also manufacturetools and sell a wide range of specialized plastic products including automotive under-the-hood components, electronic instrument casesinstruments for the orthopaedics and precision electronic connectors and lenses.

Autocam Precision Components Group

Precision Components. We sell a wide range of highly engineered, extremely close tolerance, precision-machined metal components and subassemblies primarily to the consumer transportation, industrial technology, HVAC, fluid power and diesel enginemedical/surgical end markets.

Research and Development and Product Engineering

Our research and development and product engineering efforts focus on enhancingbelieve our existing products and developing patented products, particularlyability to produce high-precision parts at high production volumes is among the best in the medical industry,market. Our technology platform consists of high precision machining, progressive stamping, injection molding, laser welding, material science, assembly, and design optimization. In-house tool design and process know-how create trade secrets that can be presentedenable consistent production tolerances of less than one micron while producing millions of parts per day. Parts are manufactured to application-specific customer design and soldco-design standards that are developed for a specific use. The high-precision capabilities are part of our zero-defect design process which seeks to eliminate variability and manufacturing defects throughout the entire product lifecycle. We believe our production capabilities provide a competitive advantage as few other manufacturers are capable of meeting tolerance demands at any volume level requested by our customers. As the need for tight-tolerance precision parts, subassemblies, and devices continues to increase, we believe that our production capabilities will place us at the forefront of the industry. We have differentiated ourselves among our competitors by providing customers engineered solutions and a broad reach and breadth of manufacturing capabilities. We believe it is for these reasons, and because of our proven ability to produce high-quality, precision parts and components on a cost-effective basis, that customers choose us to meet their manufacturing needs.

grow the business.

See Note 12 of the Notes to Consolidated Financial Statements and “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Results of Operations” for additional segment financial information.

The following table presents a breakdown

| 2016 | 2015 | 2014 | ||||||||||

Precision Bearing Components Group | $ | 248,534 | $ | 261,837 | $ | 278,026 | ||||||

Percentage of Total Sales | 30 | % | 39 | % | 57 | % | ||||||

Precision Engineered Products Group | 258,816 | 77,183 | 33,351 | |||||||||

Percentage of Total Sales | 31 | % | 12 | % | 7 | % | ||||||

Autocam Precision Components Group | 326,138 | 328,260 | 177,224 | |||||||||

Percentage of Total Sales | 39 | % | 49 | % | 36 | % | ||||||

|

|

|

|

|

| |||||||

Total | $ | 833,488 | $ | 667,280 | $ | 488,601 | ||||||

|

|

|

|

|

| |||||||

Percentage of Total Sales | 100 | % | 100 | % | 100 | % | ||||||

During 2015, followingqualified individuals in the PEP Acquisition and the divestiture of Delta Rubber,communities in which we combined the operations of PEP with our Plastics and Rubber Components Group, and renamed the segment as the Precision Engineered Products Group. The Precision Engineered Products Group includes the Plastic and Rubber Components Group as presented in our previous filings. Net sales for the fiscal years 2014 solely relate to our former Plastic and Rubber Components Segment.

Employees

operate.

Competition

Precision Bearing Components Group

We believe that competition within the Precision Bearing Components Group is based principally on quality, priceour employees and the abilitycommunities in which we operate. Our team monitors country, state, and local guidance, and uses these to consistently meet customer delivery requirements. Management believes that our competitive strengths are our precision manufacturing capabilities, our wide product assortment, our reputationimplement best practice guidelines for consistent qualityemployees and reliability,visitors. Throughout the pandemic, NN has increased communications, including the addition of virtual “town hall” style meetings at the group and organizational level. This has helped employees across our global manufacturing footprint and the productivitystay connected, whether working from home or at one of our workforce.

Precision Engineered Products Group

manufacturing sites.

Our primary competitors in the plastic bearing retainer market are Nakanishi Manufacturing Corporationcontext and Precimold, Inc. Domestically, National Plastics and Sales, Inc., Nypro, Inc., Thermotec, Inc., GW Plastics, Inc., C&J Industries, Inc., and Nyloncraft, Inc., are amongst the largest players in the precision plastic components markets. Our primary competitors in the medical device market are Tecomet, Inc., Lake Region Medical, Inc., and Vention Medical, Inc. Our primary competitors in the electrical market are Deringer-Ney, Inc., Doduco GmbH and Metalor Technologies International. Our primary competitors in the automotive and aerospace market are Interplex Industries, Inc. and Accu-Mold, LLC.

We believe that competition within the plastic injection molding, plastic bearing retainer, precision plastic components, medical device, electrical, automotive and aerospace markets is based principally on quality, price, design capabilities and speed of responsiveness and delivery. Management believes that our competitive strengths are product development, tool design, fabrication, and tight tolerance molding processes. With these strengths, we have built our reputation in the marketplace ashelp them build a quality producer of technically difficult products.

Autocam Precision Components Group

long-term career path.

Raw Materials

development and global platform, as well as on quality, price, and service.

The primary raw material used in our core ball and roller business of the Precision Bearing Components Group is 52100 Steel, which is high quality chromium steel. Our other steel requirements include metal strip, stainless steel, and type S2 rock bit steel.

The Precision Bearing Components Group businesses purchase substantially all of their 52100 Steel requirements from suppliers in Europe and Japan, and all of their metal strip requirements from European suppliers and traders.Machining. We purchase steel on the basis of composition, quality, availability and price. For precision steel balls, the pricing arrangements with our suppliers are typically subject to adjustment every three to six months in North America and contractually adjusted on an annual basisbelieve that competition within the European locations forelectrical and aerospace and defense end markets is based principally on quality, price, design capabilities, and speed of responsiveness and delivery. We believe that our competitive strengths are product development, tool design, fabrication, tight tolerance processes, and customer solutions. With these strengths, we have built our reputation in the base steel price and quarterly for surcharge adjustments. If any of our current suppliers were unable to supply 52100 Steel to us, higher costs and/or production interruptions could occurmarketplace as a resultquality producer of obtaining 52100 Steel from alternate sources. Our operating results would be negatively affected in the event that North American or European governments impose any significant quotas, tariffs or other duties or restrictions on the importtechnically difficult products.

Precision Engineered Products Group

The Precision Engineered Products Group uses a wide variety of metals in various forms, including precious metals like gold, silver, palladium and platinum. Through our diverse network of suppliers, we minimize supplier concentration risk and provide a stable supply of raw materials at competitive pricing. This group also procures resins and metal stampings from several domestic and foreign suppliers.

For the Precision Engineered Products Group, we base purchase decisions on quality, service and price. Generally, we do not enter into written supply contracts with our suppliers or commit to maintain minimum monthly purchases of materials. However, we carefully manage raw material price volatility, particularly with respect to precious metals, through the use of consignment agreements. In effect, we lease the precious metals for our own stock and buy the raw materials on the same day customer shipments are priced, thereby eliminating speculation. In addition, our products with precious metal content are priced with a margin on the raw material cost to further protect against raw material price volatility and to provide incremental profit.

Autocam Precision Components Group

The Autocam Precision Components GroupContent

Most of the raw materials we use are purchased from various suppliers and are typically available from numerous sources, some of which are located in China and Europe. The ongoing COVID-19 pandemic has impacted our suppliers, and we continue to monitor the effect of these impacts on our supply chain in order to maintain regular and timely supply of raw materials to our business segments.

Historically, we

may divert management attention from other business concerns.

Matters

Based on information compiled to date, management believes that our current operations are in substantial compliance with applicable environmental laws and regulations, the violation of which could have a material adverse effect on our business and financial condition. We have assessed conditional asset retirement obligations and have found them to be immaterial to the consolidated financial statements. We cannot assure that currently unknown matters, new laws and regulations, or stricter interpretations of existing laws and regulations will not materially affect our business or operations in the future. More specifically, although we believe that we dispose of waste in material compliance with applicable environmental laws and regulations, we cannot be certain that we will not incur significant liabilities in the future in connection with the clean-up of waste disposal sites.

FDA Compliance

As a contract manufacturer of medical devices, certain of our subsidiaries, including PEP, are required to register as such with the U.S. Food and Drug Administration (“FDA”). Each of our facilities that manufacture finished medical devices is registered with the FDA. To maintain our registration, we deploy a robust quality management system across all of our manufacturing facilities.

Content

sExecutive Officers

date hereof, compliance with these laws and regulations has not had a material effect on our capital expenditures, results of operations, and competitive position. For additional information, see “Item 1A - Risk Factors.”

Name | Age | Position | ||||||||||||

| President and Chief Executive Officer | ||||||||||||||

| Senior Vice President – Chief Financial Officer | ||||||||||||||

| John R. Buchan | 60 | Executive Vice President – Mobile Solutions and Power Solutions | ||||||||||||

| Matthew S. Heiter | Senior Vice President and General Counsel | |||||||||||||

| Senior Vice President | ||||||||||||||

| Senior Vice President | ||||||||||||||

Set forth below is certain additional information with respect to each of our executive officers.

Richard D. Holder joined us as

J. Robert Atkinson joined us as Vice President, Corporate Treasurer and Manager of Investor Relations in 2014. Prior to joining us, Mr. Atkinson was with Regions Bank, one of the nation’s largest full-service providers of consumer and commercial banking, wealth management, mortgage, and insurance products and services. He most recently served as vice president and commercial relationship manager in Regions Corporate Bank Group, where he was responsible for marquee corporate relationships, developing treasury management solutions and negotiating terms and conditions for new and renewal credit facilities. Prior to that position, he served as Vice President of business services. Mr. Atkinson also served as a project coordinator for the Electrical Group of Eaton Corporation. Mr. Atkinson is a member of the Association of Financial Professions and earned his certified treasury professional designation.

Thomas C. Burwell, Jr. joined us as Corporate Controller in September 2005. He was promoted to Vice President Chief Accounting Officer and Corporate Controller in 2011, and to Senior Vice President and Chief Financial Officer in November 2016. Prior to joining NN, Mr. Burwell held various positions at Coats, PLC from 1997 to 2005 ultimately becoming the Vice President of Finance for the U.S. Industrial Division. From 1992 to 1997, Mr. Burwell held various positions at the international accounting firm BDO Seidman, LLP. Mr. Burwell is a Certified Public Accountant.

Matthew S. Heiter joined us as Senior Vice President and General Counsel in July 2015. Prior to joining us, Mr. Heiter was a shareholder in the law firm of Baker, Donelson, Bearman, Caldwell and Berkowitz, PC from May 1996 to December 1999 and from July 2002 to July 2015, where he served as chairman of the firm’s Securities and Corporate Governance Practice Group. From January 2000 to July 2002, Mr. Heiter served as the Executive Vice President, General Counsel and Secretary of Internet Pictures Corporation, a publicly traded internet technology company.

L. Jeffery Manzagol joined us as Senior Vice President—General Manager of the Precision Bearing Components Group in October 2014. Manzagol stepped into his role with more than 36 years of metal bearings and high precision manufacturing experience. He most recently served as President of the Bearings Division at Kaydon Corporation. Previously, Manzagol held various leadership positions at SKF Group, including President and General Manager at the Armada, Michigan facility.

John Manzi joined us as Senior Vice President—General Manager of Precision Engineered Products Group in October 2015 in connection with the completion of the PEP Acquisition. Previously, Mr. Manzi served as the President and Chief Executive Officer of PEP. Mr. Manzi was instrumental in leading PEP’s development and, together with PEP’s management team, has successfully enhanced PEP’s end market reach, expanded its product breadth and executed on key strategic acquisitions. Mr. Manzi has 20 years of experience with PEP. Prior to joining PEP’s management team, Mr. Manzi held various positions including President of PEP’s Attleboro operations, Vice President of Operations, and Engineering Manager.

Warren Veltman joined us as Senior Vice President and General Manager of our former Autocam Precision Components Group in September 2014.Group. Prior to the acquisition, Mr. Veltman served as Chief Financial Officer of Autocam Corporation from 1990 and Secretary and Treasurer since 1991. Prior to Mr. Veltman’s service at Autocam, Mr. Veltman was an Audit Manager with Deloitte & Touche LLP.

James

COVID-19 pandemic.Item 1A.Risk FactorsThe following are risk factors that affect our business, prospects, financial condition, results of operations, and cash flows, some of which are beyond our control. These risk factors should be considered in connection with evaluating the forward-looking statements contained in this Annual Report on Form 10-K. If any of the events described below were to actually occur, our business, prospects, financial condition, results of operations, or cash flows could be adversely affected, and results could differ materially from expected and historical results.Risks Related to Our OperationsA recession impactingThe COVID-19 pandemic and mitigation efforts to control the spread of the disease have impacted, and are expected to continue to materially impact, our business and our financial condition, results of operations and cash flows could be materially adversely affected by factors directly or indirectly relating to the COVID-19 pandemic.The COVID-19 pandemic has created significant volatility in the global economy, led to significant reduced market and economic activity, and disrupted, and may continue to disrupt, the end markets we serve. In response, various governmental bodies and private enterprises implemented numerous measures to contain the pandemic, such as travel bans and restrictions, quarantines, “shelter-in-place” orders and shutdowns. While many of the restrictions have eased across the globe, some areas have re-imposed closures and other restrictions due to increased rates of COVID-19 cases. No assurance can be given that these new closures and restrictions will not continue to occur. New and more easily transmitted variants of COVID-19, such as the Delta and Omicron variants, have emerged and spread in the U.S. and across the globe.The impact of these variants cannot be predicted at this time and could depend on numerous factors, including vaccination rates among the population, the efficacy of COVID-19 vaccines against the new variants, and the response by governmental bodies and regulators.Further surges in COVID-19 infection rates could result in the reinstatement of directives and mandates requiring businesses to again curtail or cease normal operations.The COVID-19 pandemic and the geographic regionsresponses by governmental bodies and regulators thereto have created a disruption in which we orour manufacturing, product distribution, overall supply chain, and other business activities, and that of our customers, operatesuppliers, co-manufacturers, and distributors. A significant number of our customers, suppliers, co-manufacturers, distributors, and manufacturing facilities are located in regions that have been affected by the pandemic and those operations have been, and may continue to be, materially affected by restrictive measures implemented in response to the pandemic. As a result we have experienced, and may continue to experience, delays in the production and distribution of our products and the loss of sales to our customers. Any delay or shortage in the supply of raw materials or delay in the manufacturing or distribution of our products may result in our inability to satisfy customer demand in a timely manner or at all, which could result in the loss of a portion of or all of the customer’s business and damage our reputation. Additionally, if the global economic effects caused by11the COVID-19 pandemic continue or increase, overall customer demand may continue to decrease, which could have a material adverse effect on our ability to finance our operations and implement our growth strategy.During the three month period ended December 31, 2008 and the year ended December 31, 2009, we experienced a sudden and significant reduction in customer orders driven by reductions in automotive and industrial end market demand across all our businesses. Additionally, during the latter part of 2011 and all of 2012, we experienced the impacts of a European recession in our European businesses. Prior to this time, we had never been affected by a recession that had impacted both of our key geographic markets of the U.S. and Europe simultaneously. If we are impacted by a global recession in the future, this could have a material adverse effect on our business, prospects,results of operations, and financial condition.Further, the COVID-19 pandemic could adversely impact our ability, and the ability of our suppliers, co-manufacturers, distributors, and customers, to retain key employees and ensure the continued service and availability of skilled personnel necessary to run our, and their, operations. To the extent our management or other personnel, or the management or other personnel of our suppliers, co-manufacturers, distributors, and customers, are impacted in significant numbers by the pandemic and are not available to perform their job duties, we could experience delays in, or the suspension of, our manufacturing operations, distribution of our products, and other important corporate functions.The ongoing COVID-19 pandemic and the current volatility in the global economy, reduced market and economic activity, and disruptions in the end markets we serve present material risks and uncertainties for us.The extent of the impact that the COVID-19 pandemic will have on our business, results of operations, and financial condition will depend largely on future developments relating to the duration and scope of the COVID-19 pandemic, including the continued emergence, persistence, severity and transmissibility of variants of the virus, the efficacy of vaccines, the pace at which governmental restrictions are eased or lifted, and the implementation of new or additional mitigation efforts by governmental authorities to control the spread of the disease, such as “stay-at-home” orders, business closures, and vaccine mandates. To the extent the COVID-19 pandemic adversely affects our business, financial condition, results of operations, oroperation, and cash flows, and could lead to additional restructuring and/or impairment charges being incurred and our ability to implement our growth strategy.The cyclical demand for our products andit may also have the seasonality impact on our production could adversely affect our revenues.The end markets for fully assembled bearings and industrial and automotive components are cyclical and tend to decline in response to overall declines in industrial and automotive production. As a result, the market for the bearing components and precision metal and industrial plastic products we sell is also cyclical and impacted by overall levelseffect of industrial and automotive production. Our sales have been, and can beheightening other risks disclosed below. In addition, if in the future negatively affected by adverse conditions in the industrial and/there is an outbreak of another highly infectious or automotive production sectors of the economycontagious disease or by adverse global or national economic conditions generally. Similarly, any inflation in oil prices and any resulting increase in gasoline prices could have a negative impact on demand for our products as a result of consumer and corporate spending reductions.In addition, seasonality may have a negative impact on our production. Due to the typical slower summer manufacturing season in Europe,similar public health crisis, we expect that revenues in the third fiscal quarter of each year willwould be lower than in the other quarters of the year.We depend on a very limited number of sources for our primary raw material and are subject to similar risks of shortages and price fluctuation.The steel that we use to manufacture our precision bearing components is of an extremely high quality and is available from only a limited number of producers on a global basis. Due to quality constraints inas posed by the U.S. steel industry, we obtain substantially all of the steel used in our U.S. operations of our Precision Bearing Components Group from non-U.S. suppliers. In addition, we obtain most of the steel used in our European operations from a single European source. If we had to obtain steel from sources other than our current suppliers, we could face higher prices and automotive costs, increased duties or taxes and shortages of steel. Problems in obtaining steel, particularly 52100 chrome steel in the quantities that we require, on commercially reasonable terms, could increase our costs and have a material adverse effect on our business, prospects, financial condition, results of operations, or cash flows.We depend heavily on a relatively limited number of customers, and the loss of any major customer would have a material adverse effect on our business.Sales to various U.S. and foreign divisions of SKF, one of the largest bearing manufacturers in the world, accounted for approximately 13% of consolidated net sales in 2016. No other customers accounted for more than 10% of sales. During 2016,2021, sales to various U.S. and foreign divisions of our ten largest customers accounted for approximately 48%43% of our consolidated net sales. The loss of all or a substantial portion of sales to these customers would cause us to lose a substantial portion of our revenue and would lower our operating profit margin and cash flows from operations.Work stoppages or similar difficulties and unanticipated business disruptions could significantly disrupt our operations, reduce our revenues and materially affect our earnings.A work stoppage at one or more of our facilities could have a material adverse effect on our business, prospects, financial condition, results of operations, or cash flows. Also, if one or more of our customers were to experience a work stoppage, that customer would likely halt or limit purchases of our products,products. For example, increased demand for semiconductor chips in 2020, due in part to the COVID-19 pandemic and an increased use of laptop computers, 5G phones, gaming systems and other IT equipment that use these chips, has resulted in a severe shortage of chips in early 2021 and is ongoing. These same chips are used in automobiles in a variety of parts and information and entertainment systems. As a result, various automotive manufacturers have been forced to delay or stall new vehicle production. If efforts to address the chip shortage by the industry and the U.S government are unsuccessful, there may be further delays in new vehicle production, which could have a material adverse effect on our business, prospects, financial condition, results of operations, or cash flows.We have a complex network of suppliers, owned and leased manufacturing locations, co-manufacturing locations, distribution networks, and information systems that support our ability to consistently provide our products to our customers. Factors that are hard to predict or beyond our control, such as weather, raw material shortages, natural disasters, fires or explosions, political unrest, terrorism, generalized labor unrest, or health pandemics, such as COVID-19, could damage or disrupt our operations or our customers’, suppliers’, co-manufacturers’ or distributors’ operations. These disruptions may require additional resources to restore our supply chain or distribution network. If we cannot respond to disruptions in our operations, whether by finding alternative suppliers or replacing capacity at key manufacturing or distribution locations, or if we are unable to quickly repair damage to our information, production, or supply systems, we may be late in delivering, or be unable to deliver, products to our customers and may also be unable to track orders, inventory, receivables, and payables. If that occurs, our customers’ confidence in us and long-term demand for our products could decline. Any of these events could materially and adversely affect our product sales, financial condition, and operating results.We operate in and sell products to customers outside the U.S. and are subject to several risks related to doing business internationally.Because weWe obtain a majority of our raw materials from overseas suppliers, actively participate in overseas manufacturing operations and sell to a large number of international customers. During the year ended December 31, 2021, sales to customers located outside of the U.S. accounted for approximately 39% of our consolidated net sales. As a result of doing business internationally, we face risks associated with the following:•changes in tariff regulations, which may make our products more costly to export or import;

Our growth strategy depends in part on companies outsourcing critical components, and if outsourcing does not continue, our business could be adversely affected.

Our growth strategy depends in part on major customers continuing to outsource components and expanding the number of components being outsourced. This requires manufacturers to depart significantly from their traditional methods of operations. If major customers do not continue to expand outsourcing efforts or determine to reduce their use of outsourcing, our ability to grow our business could be materially adversely affected.

Our production capacity has been expanded geographically in recent years to operate in the same markets as our customers.

We have expanded our precision bearing components production facilities and capacity over the last several years. Historically, precision bearing component production facilities have not always operated at full capacity. Over the past several years, we have undertaken steps to address a portion of the capacity risk including closing or ceasing operations at certain plants and downsizing employment levels at others. As such, the risk exists that our customers may exit the geographic markets in which our production capacity is located and/or develop vendors in lower cost countries in which we do not have production capacity.

Recent developments relating to the United Kingdom’s referendum vote in favor of leaving the European Union could adversely affect us.

The United Kingdom held a referendum in June 2016 in which a majority voted for the United Kingdom’s withdrawal from the European Union. As a result of this vote, negotiations are expected to commence to determine the terms of the United Kingdom’s withdrawal from (“Brexit”) the European Union as well as its relationship with the European Union going forward, including the terms of trade between the United Kingdom and the European Union. The effects of Brexit have been and are expected to continue to be far-reaching. Brexit, and the perceptions as to its impact, may adversely affect business activity and economic conditions in Europe and globally and could continue to contribute to instability in global financial and foreign exchange markets. The full effects of Brexit are uncertain and will depend on any agreements the United Kingdom may make to retain access to European Union markets. Lastly, as a result of the Brexit, other countries in the European Union may seek to conduct referenda with respect to their continuing membership with the European Union. Given these possibilities and others we may not anticipate, as well as the lack of comparable precedent, the full extent to which our business, prospects, financial condition, results of operations, or cash flows could be adversely affected by Brexit is uncertain.

Changes in legislation, regulation and government policy as a result of the 2016 U.S. presidential and congressional elections may have a material adverse effect on our business in the future.

The recent presidential and congressional elections in the United States could result in significant changes in, and uncertainty with respect to, legislation, regulation and government policy directly affecting our business or indirectly affecting us because of impacts on our customers and suppliers. Legislative and regulatory proposals discussed during and after the election that could have a material direct or indirect impact on us include, but are not limited to, a disallowance of the deduction for net interest expense, a tax on existing unrepatriated foreign earnings, restrictions on imports and exports, modifications to international trade policy, including withdrawal from trade agreements, environmental regulation, changes to immigration policy, changes to health insurance legislation and the imposition of tariffs and other taxes on imports. We are currently unable to predict whether such changes will occur and, if so, the ultimate impact on our business. To the extent that such changes have a negative impact on us, our suppliers or our customers, including as a result of related uncertainty, these changes may materially and adversely impact our business, prospects, financial condition, results of operations, or cash flows.

We have identifiedmaterialweaknessesin our internalcontrol over financialreporting which could,if not remediated, resultinmaterial misstatements in ourfinancialstatements.

Our management is responsible for establishing and maintaining adequate internal control over financial reporting as defined in Rule 13a-15(f) under the Exchange Act. As disclosed in Item 9A, management identified certain material weaknesses in our internal control over financial reporting. Because of these material weaknesses, our management concluded that we did not maintain effective internal control over financial reporting as of December 31, 2016. With the oversight of senior management and the audit committee, we have begun taking steps to remediate the underlying cause of these material weaknesses and improve the design of controls.

While we expect to take the measures necessary to address the underlying causes of these material weaknesses, we cannot at this time estimate how long it will take and our efforts may not prove to be successful in remediating these material weaknesses. While we have not incurred and do not expect to incur material expenses specifically related to the remediation of these material weaknesses, actual expenses may exceed our current estimates and overall costs of compiling the system and processing documentation necessary to assess the effectiveness of our internal control over financial reporting may be material.

If we are unable to successfully remediate these material weaknesses in our internal control over financial reporting, or identify any additional material weaknesses that may exist, the accuracy and timing of our financial reporting may be adversely affected, we may be unable to maintain compliance with securities law requirements regarding timely filing of periodic reports in addition to applicable stock exchange listing requirements, and our stock price may decline materially as a result, all of which could have a material adverse effect on our business, prospects, financial condition, results of operations, or cash flows.

We have had difficulty with purchase accounting and other aspects related to the accounting for our acquisitions, which resulted in material weaknesses in our internal control over financial reporting. Although we have remediated these material weaknesses, there can be no assurances we will not face similar issues with respect to any future acquisitions.

We have and will continue to incur expenses in relation to our acquisitions and the integration of our acquired companies.

We have and will continue to incur expenses in relation to our acquisitions and the integration of our acquired companies. While we have assumed that a certain level of expenses will be incurred, there are many factors beyond our control that could affect the total amount or the timing of the integration expenses. Moreover, many of the expenses that will be incurred are, by their nature, difficult to estimate accurately. These integration expenses may result in us taking charges against earnings, and the amount of any future charges are uncertain at present.

We may be unable to realize the anticipated cost or capital expenditure savings or may incur additional and/or unexpected costs in order to realize them.

There can be no assurance that we will be able to realize the anticipated cost or capital expenditure savings from our acquisitions in the anticipated amounts or within the anticipated timeframes or at all. We anticipate implementing a series of cost savings initiatives that we expect to result in recurring, annual run-rate cost savings. We expect to incur one-time, non-recurring costs to achieve such synergies, including certain costs during 2015 and 2016. These or any other cost or capital expenditure savings that we realize may differ materially from our estimates. We cannot provide assurances that these anticipated savings will be achieved or that our programs and improvements will be completed as anticipated or at all. In addition, any cost savings that we realize may be offset, in whole or in part, by reductions in revenues or through increases in other expenses.

Our projections and assumptions related to cost savings are based on our current estimates, but they involve risks, uncertainties, projections and other factors that may cause actual results, performance or achievements to be materially different from any future results, performance or achievements, express or implied. Neither our independent auditors nor any other independent auditors, have examined, compiled or performed any procedures with respect to these projections, nor have they expressed any opinion, or any other form of assurance on such information or their achievability. Assumptions relating to our projections involve subjective decisions and judgments with respect to, among other things, the estimated impact of certain operational adjustments, including Six Sigma/OpEx optimization programs, product grouping and rationalization, facility rationalization and shared services cost savings and other cost and savings adjustments, as well as future economic, competitive, industry and market conditions and future business decisions, all of which are inherently uncertain and may be beyond the control of our management.

Failure to realize the expected costs savings and operating synergies related to our acquisitions could result in increased costs and have an adverse effect on our business, prospects, financial condition, results of operations, or cash flows.

Our future results could suffer if we cannot effectively manage our expanded operations, which are significantly larger and more complex following our acquisitions.

As a result of our acquisitions over the past few years, the size and scope of our operations were significantly increased. Our future success depends, in part, upon our ability to manage the expanded operations, which will pose challenges for management, including challenges related to the management and monitoring of new operations and associated increased costs and complexity. We may not have the expertise, experience and resources to pursue or successfully operate all of our businesses at once. The administration of our businesses requires implementation and oversight of appropriate operations, management, compliance and financial reporting systems and controls. We may experience difficulties in effectively implementing and overseeing these and other systems. Such implementation and initial oversight will require the focused attention of our management team, including a significant commitment of its time and resources. The need for management to focus on these matters could have a material and adverse impact on our revenues and operating results. There can be no assurance that we will be successful or that we will realize any operating efficiencies, cost savings, revenue enhancements or other benefits currently anticipated from our acquisitions.

Any divestitures and discontinued operations could negatively impact our business and retained liabilities from businesses that we may sell could adversely affect our financial results.As part of our portfolio management process, we review our operations for businesses which may no longer be aligned with our strategic initiatives and long-term objectives. Divestitures pose risks and challenges that could negatively impact our business, including required separation or carve-out activities and costs, disputes with buyers, or potential impairment charges. We may also dispose of a business at a price or on terms that are less than we had previously anticipated. After reaching an agreement with a buyer for the disposition of a business, we are also subject to satisfaction of pre-closing conditions, as well as necessary regulatory and governmental approvals on acceptable terms, which may prevent us from completing a transaction. Dispositions may also involve continued financial involvement, as we may be required to retain responsibility for, or agree to indemnify buyers against contingent liabilities related to a businesses sold, such as lawsuits, tax liabilities, lease payments, product liability claims, or environmental matters. Under these types of arrangements, performance by the divested businesses or other conditions outside of our control could affect future financial results.General Risk FactorsDamage to our reputation could harm our business, including our competitive position and business prospects.Our ability to attract and retain customers, suppliers, investors, and employees is impacted by our reputation. Harm to our reputation can arise from various sources, including employee misconduct, security breaches, unethical behavior, litigation, or19regulatory outcomes. The consequences of damage to our reputation include, among other things, increasing the number of litigation claims and the size of damages asserted or subjecting us to enforcement actions, fines, and penalties, all of which would cause us to incur significant defense related costs and expenses.Changes in U.S. tax laws could have a material adverse effect on our business, cash flow, results of operations, and financial condition.The U.S. tax laws and regulations, as well as the administrative interpretations of those laws and regulations, are constantly under review and may be changed at any time, possibly with retroactive effect. No assurance can be given as to whether, when, or in what form changes to the U.S. tax laws applicable to us may be enacted. Changes in U.S. tax laws, tax rulings, or interpretations of existing laws could materially affect our business, cash flow, results of operations, and financial condition.Item 1B.Unresolved Staff Comments

None

Precision Bearing Componentsfacilities by segment.

| Country | Owned or Leased | ||||||||||||||||||

| Leased | ||||||||||||||||||||

| Brazil | Leased | |||||||||||||||||||

| U.S.A. | Owned | |||||||||||||||||||

| Leased | ||||||||||||||||||||

| Poland | Owned | |||||||||||||||||||

| Leased | ||||||||||||||||||||

| U.S.A. | Leased | |||||||||||||||||||

| Kentwood, Michigan | Plant 3, Warehouse | U.S.A. | Leased | |||||||||||||||||

| Kentwood, Michigan | Office | U.S.A. | Owned | |||||||||||||||||

| Marnaz, France | Plant | France | Owned | |||||||||||||||||

| Marshall, Michigan | Plant 1 | U.S.A. | Leased | |||||||||||||||||

| Marshall, Michigan | Plant 2 | U.S.A. | Leased | |||||||||||||||||

| Sao Joao da Boa Vista, Brazil | Plant 1 | Brazil | Leased | |||||||||||||||||

| Sao Joao da Boa Vista, Brazil | Plant 2 | Brazil | Leased | |||||||||||||||||

| Wellington, Ohio | Plant 1 | U.S.A. | Leased | |||||||||||||||||

| Wellington, Ohio | Plant 2 | U.S.A. | Leased | |||||||||||||||||

| Wuxi, China | Plant | China | Leased | |||||||||||||||||

Precision Engineered Products

| Country | Owned or Leased | ||||||||||||||||||

| Algonquin, | U.S.A. | Owned | ||||||||||||||||||

| Attleboro, Massachusetts | Plant 1 | U.S.A. | Owned | |||||||||||||||||

| Attleboro, Massachusetts | Plant 2 | U.S.A. | ||||||||||||||||||

| Attleboro, | Owned | |||||||||||||||||||

| Owned | ||||||||||||||||||||

| Leased | ||||||||||||||||||||

| Leased | ||||||||||||||||||||

| Owned | ||||||||||||||||||||

| Mexico | Owned | |||||||||||||||||||

| Owned | ||||||||||||||||||||

| U.S.A. | Leased | |||||||||||||||||||

| Leased | ||||||||||||||||||||

Autocam Precision Components Group

| Country | Owned or Leased | ||||||||||||||||||

Joint Venture

| Plant | ||||||||||||

| ||||||||||||

For more information, please see “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources.”

All

Partapplicable.

The following table sets forth the high and low closing sales prices of the common stock, as reported by NASDAQ for our two most recent fiscal years.

| Close Price | ||||||||

| High | Low | |||||||

2016 | ||||||||

First Quarter | $ | 14.90 | $ | 10.58 | ||||

Second Quarter | 19.16 | 12.77 | ||||||

Third Quarter | 18.81 | 13.48 | ||||||

Fourth Quarter | 20.21 | 13.65 | ||||||

2015 | ||||||||

First Quarter | $ | 28.18 | $ | 19.49 | ||||

Second Quarter | 29.86 | 22.50 | ||||||

Third Quarter | 26.97 | 18.29 | ||||||

Fourth Quarter | 19.54 | 12.92 | ||||||

$2.42.

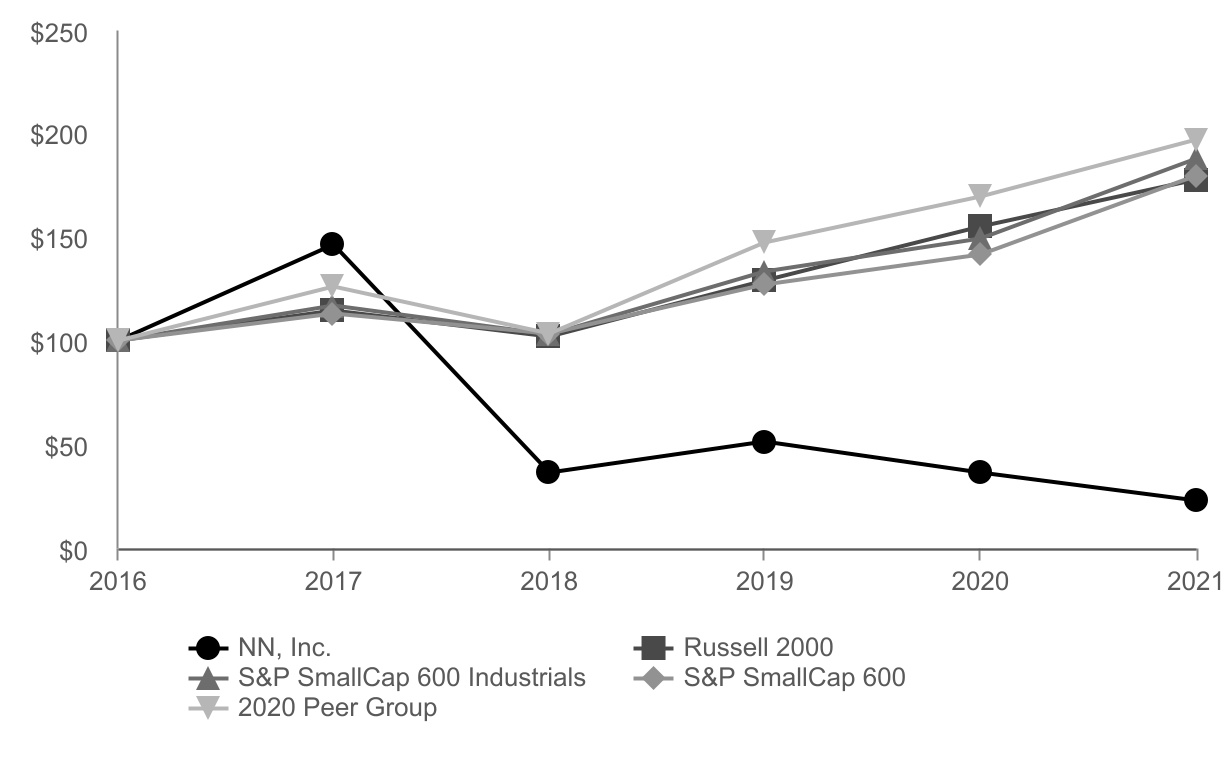

In our Annual Report on Form 10-K for the year ended December 31, 2014, we used the Standard & Poors 500 Stock Index as our broad equity market index and the Machinery Index as our line of business index for our performance graph comparison. However, we have determined that the Standard & Poors SmallCap 600 is a more appropriate broad equity market index because it has more companies that have a market capitalization similar to us. Additionally we have determined that the Peer Group is a more appropriate comparative group than the Machinery Index, as the companies comprising the Peer Group include diversified industrial manufacturers like NN. In light of the diversification of our end markets and the broadening of our portfolio of products, services and solutions over the last two years, primarily due to the acquisitions of Autocam and PEP, we believe the Peer Group is comprised of companies that better reflect our current business.

NN Inc., S&P 500, S&P 600, Value Line Machinery and Peer Group

December 31, 2021)

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | ||||||||||||||||||||||||||||||

| NN, Inc. | $ | 100.00 | $ | 146.51 | $ | 36.31 | $ | 51.31 | $ | 36.45 | $ | 22.74 | |||||||||||||||||||||||

| Russell 2000 | $ | 100.00 | $ | 114.65 | $ | 102.03 | $ | 129.10 | $ | 155.20 | $ | 177.73 | |||||||||||||||||||||||

| S&P SmallCap 600 Industrials | $ | 100.00 | $ | 117.21 | $ | 102.97 | $ | 133.49 | $ | 149.47 | $ | 188.18 | |||||||||||||||||||||||

| S&P SmallCap 600 | $ | 100.00 | $ | 113.21 | $ | 103.59 | $ | 127.24 | $ | 141.61 | $ | 179.60 | |||||||||||||||||||||||

| 2020 Peer Group | $ | 100.00 | $ | 126.26 | $ | 103.48 | $ | 147.62 | $ | 169.44 | $ | 197.34 | |||||||||||||||||||||||

2016 | Dividend | |||

First Quarter | $ | 0.07 | ||

Second Quarter | $ | 0.07 | ||

Third Quarter | $ | 0.07 | ||

Fourth Quarter | $ | 0.07 | ||

2015 | Dividend | |||

First Quarter | $ | 0.07 | ||

Second Quarter | $ | 0.07 | ||

Third Quarter | $ | 0.07 | ||

Fourth Quarter | $ | 0.07 | ||

The following selected financial data has been derived from our audited financial statements. The selected financial data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the audited Consolidated Financial Statements, including the Notes thereto.

| Year ended December 31, | ||||||||||||||||||||

| 2016 | 2015 | 2014 | 2013 | 2012 | ||||||||||||||||

Statement of Income Data: | ||||||||||||||||||||

Net sales | $ | 833,488 | $ | 667,280 | $ | 488,601 | $ | 373,206 | $ | 370,084 | ||||||||||

Cost of products sold (exclusive of depreciation shown separately below) | 621,022 | 525,993 | 384,889 | 295,136 | 294,859 | |||||||||||||||

Selling, general and administrative | 80,266 | 51,745 | 43,756 | 33,281 | 31,561 | |||||||||||||||

Acquisition related costs excluded from selling, general and administrative | — | 11,682 | 9,248 | — | — | |||||||||||||||

Depreciation and amortization | 62,488 | 44,482 | 22,146 | 16,957 | 17,643 | |||||||||||||||

(Gain) loss on disposal of assets | 288 | (687 | ) | — | 5 | (17 | ) | |||||||||||||

Restructuring and integration | 10,024 | 7,268 | 875 | — | 967 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Income from operations | 59,400 | 26,797 | 27,687 | 27,827 | 25,071 | |||||||||||||||

Interest expense | 63,154 | 29,899 | 10,895 | 2,374 | 3,878 | |||||||||||||||

Write-off of unamortized debt issuance cost | 3,089 | 18,673 | 1,398 | — | — | |||||||||||||||

Derivative payments on interest rate swap | 609 | — | — | — | — | |||||||||||||||

Derivative losses on change in interest rate swap fair value | 2,448 | — | — | — | — | |||||||||||||||

Other (income) expense, net | (2,591 | ) | 1,175 | 2,222 | 275 | 852 | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Income before provision (benefit) for income taxes | (7,309 | ) | (22,950 | ) | 13,172 | 25,178 | 20,341 | |||||||||||||

Provision (benefit) for income taxes | (9,313 | ) | (10,518 | ) | 5,786 | 8,000 | (3,927 | ) | ||||||||||||

Share of net income from joint venture | 5,938 | 5,001 | 831 | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net income (loss) | $ | 7,942 | $ | (7,431 | ) | $ | 8,217 | $ | 17,178 | $ | 24,268 | |||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Basic income per share: | ||||||||||||||||||||

Net income (loss) | $ | 0.29 | $ | (0.35 | ) | $ | 0.46 | $ | 1.00 | $ | 1.43 | |||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Diluted income per share: | ||||||||||||||||||||

Net income (loss) | $ | 0.29 | $ | (0.35 | ) | $ | 0.45 | $ | 1.00 | $ | 1.42 | |||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Dividends paid | $ | 0.28 | $ | 0.28 | $ | 0.28 | $ | 0.18 | $ | — | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Weighted average number of shares outstanding—Basic | 27,016 | 21,181 | 17,887 | 17,176 | 17,009 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Weighted average number of shares outstanding – Diluted | 27,154 | 21,181 | 18,253 | 17,260 | 17,114 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Balance Sheet Data: Current assets Current liabilities Total assets Long-term debt Stockholders’ equity As of December 31, 2016 2015 2014 2013 2012 $ 280,555 $ 280,181 $ 242,799 $ 125,674 $ 127,296 138,616 133,351 137,598 69,384 58,758 1,360,386 1,380,567 712,713 262,402 265,343 785,713 795,400 328,026 26,000 63,715 315,199 313,881 173,699 152,760 128,560

The year ended December 31, 2016 reflects fully all the acquisition activity from 2015 and 2014. Line items such as Selling, general and administrative costs, Depreciation and amortization, Restructuring and impairment charges, excluding goodwill impairment, and Interest expense all increased because of increased basis in assets and higher debt and employee levels. There were no acquisitions made during 2016.

The year ended December 31, 2015 was significantly impacted by certain costs related to the PEP Acquisition and to a lesser extent the Caprock acquisition completed in 2015, as well as the issuance of shares of our common stock. The total impact of these costs was $43.0 million (before tax) and $29.4 million (after tax). The balance sheet for the year ended December 31, 2015 includes the impact of these costs. With these acquisitions, we acquired current assets and total assets of $71.2 million and $741.6 million, respectively, and assumed current liabilities and total liabilities of $21.7 million and $111.3 million, respectively.

On July 1, 2015 we closed a registered follow-on offering of public common stock. The total number of shares of common stock sold was approximately 7.6 million at a public offering price of $24.00 per share. The net proceeds received from the offering, after deducting underwriter discounts, commissions and offering expenses, were approximately $173.1 million. Of these proceeds, $148.7 million was used for repayment of principal and interest on existing debt.

On October 19, 2015, concurrent with the PEP Acquisition, we: (i) entered into a new senior secured term loan credit facility in the amount of up to $525.0 million (with a $100.0 million accordion feature) and a seven year maturity (as amended, supplemented and/or restated from time to time, the “Term Loan Credit Facility”); (ii) entered into a new senior secured revolving credit facility in the amount of up to $100.0 million with a five year maturity (as amended, supplement and/or restated from time to time, the “Senior Secured Revolving Credit Facility”, and together with the Term Loan Credit Facility, the “Senior Credit Facilities”); and (iii) issued $300.0 million of 10.25% senior notes due 2020 (the “Senior Notes”). Proceeds from the Term Loan Credit Facility and the Senior Notes were used to finance the purchase price of the PEP Acquisition and pay down debt. The Senior Credit Facilities replaced our existing credit facilities. On November 9, 2015, an incremental term loan of $50.0 million was drawn on the Term Loan Credit Facility, and the proceeds were used to repurchase approximately $50.0 million of the Senior Notes. On September 30, 2016, we amended and restated the Senior Credit Facilities, which lowered the interest rate and rate floor on the Company’s Senior Secured Term Loan B (the “Term Loan B”). The new applicable rate for the Term Loan B is London Inter Bank Offering Rate (“LIBOR”), subject to a 0.75% rate floor, plus 4.25%, which in combination is 75 basis points lower (or 0.75%) than the previous rate. Concurrent with the amended and restated Term Loan B, the Senior Secured Revolving Credit Facility was upsized from $100 million to $133 million. Proceeds were drawn under the Senior Secured Revolving Credit Facility to pay down debt under the Term Loan B, reducing the debt under the Term Loan B to $545 million. During October 2016, an incremental amendment was executed increasing the $133 million Senior Secured Revolving Credit Facility to $143 million. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note 7 of the Notes to Consolidated Financial Statements for more information. Additional details regarding the financing of the PEP Acquisition may be found in our Current Report on Form 8-K filed with the Securities and Exchange Commission on October 20, 2015.

The year ended December 31, 2014 was significantly impacted by certain costs related to the Autocam acquisition and to a lesser extent the three other acquisitions completed in 2014. The total impact of these costs was $14.8 million (before tax) and $13.6 million (after tax). In addition, related to the Autocam acquisition, we discontinued use of certain trade names and incurred a $0.9 million impairment charge. The balance sheet for the year ended December 31, 2014 includes the impact of four acquisitions closed during 2014. With these acquisitions, we acquired current assets and total assets of $92.9 million and $433.9 million, respectively, and assumed current liabilities and total liabilities of $52.9 million and $124.4 million, respectively. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for more information.

The year ended December 31, 2012 was impacted by a favorable tax benefit of a net $7.3 million from removing valuation allowances on deferred tax assets in the U.S. Additionally, results for the year ended December 31, 2012 were negatively impacted by impairments of $1.0 million and after tax foreign exchange losses of $1.1 million related to intercompany notes.

Management generally focuses on these trends and relevant market indicatorsGlobal industrial growth•Trends related to the geographic migration of competitive manufacturing, electric vehicles, and economics;electrification;

•Changes in tariff regulations.23Management generally focuses on the following key indicators of operating performance•Sales growth;

Estimates

Business Combinations. We allocate the total purchase price of the acquired tangible and intangible assets acquired and liabilities assumed based on their estimated fair values as of the business combination date, with the excess purchase price recorded as goodwill. The purchase price allocation process required us to use significant estimates and assumptions, including fair value estimates, as of the business combination date. Although we believe the assumptions and estimates we have made are reasonable and appropriate, they are based in part on historical experience and information obtained from management of the acquired company, in part based on valuation models that incorporate projections of expected future cash flows and operating plans and are inherently uncertain. Valuations are performed by management or third party valuation specialists under management’s supervision. In determining the fair value of assets acquired and liabilities assumed in business combinations, as appropriate, we may use one of the following recognized valuation methods: the income approach (including discounted cash flows from relief from royalty and excess earnings model), the market approach and/or the replacement cost approach.

Examples of significant estimates used to value certain intangible assets acquired include but are not limited to:

However, different assumptions regarding projected performance and other factors associated with the acquired assets may affect the amount recorded under each type of assets and liabilities, mainly between property plant and equipment, intangibles assets, goodwill and deferred income tax liabilities and subsequent assessment could result in future impairment charges. The purchase price allocation process also entails us to refine these estimates over a measurement period not to exceed one year to reflect new information obtained surrounding facts and circumstances existing at acquisition date.

Goodwill and Acquired Intangibles. For new acquisitions, we use estimates, assumptions and appraisals to allocate the purchase price to the assets acquired and to determine the amount of goodwill. These estimates are based on market analyses and comparisons to similar assets. Annual procedures are required to be performed to assess whether recorded goodwill is impaired. The annual tests requireprinciples requires management to make estimates and assumptions with regardabout future events that affect the amounts reported in the financial statements and accompanying notes. Actual results could differ significantly from those estimates. We believe that the following discussion addresses our most critical accounting estimates, which are those that are most important to the futureportrayal of our financial condition and results of operations of its reporting units, and the expected cash flows that they will generate. These estimatesrequire management’s most difficult, subjective, and assumptions could impact the recorded value of assets acquired in a business combination, including goodwill, and whether or not there is any subsequent impairment of the recorded goodwill and the amount of such impairment.

complex judgments.

Generally accepted accounting principles in the U.S. (“GAAP”) prescribes a quantitative two-step process of testing for goodwill impairments. The first step is to determine if the carrying value of the reporting unit with goodwill is less than the related fair value of the reporting unit. We considered three main approaches to value (cost, market and income) the fair value of the reporting unit and market based multiples of earning and sales methods obtained from a grouping of comparable publicly trading companies. We believe this methodology of valuation is consistent with how market participants would value reporting units. The discount rate and market based multiples used are specifically developed for the units tested regarding the level of risk and end markets served. Even though we do use other observable inputs (Level 2 inputs under the GAAP hierarchy), the calculation of fair value for goodwill would be most consistent with Level 3 under the GAAP hierarchy. We conducted tests for goodwill impairment for the years ended December 31, 2016 and 2015 and concluded no impairment of goodwill had occurred.

As of fourth quarter testing, the PEP Acquisition (the “PEP reporting unit”) had an estimated fair value that exceeded the carrying value including goodwill by 4 percent. As of December 31, 2016,2021 and 2020, there was no remaining goodwill of $368.3 million is allocated to the PEP reporting unit. Cash flows from the PEP reporting unit are susceptible to changes in demandbalance due to cyclicality and timingimpairments recognized during the year ended December 31, 2020. An impairment charge was calculated based on a reporting unit’s carrying amount in excess of customer project completions primarily in the electrical and medical markets. Weakened demand in these markets could decrease the estimatedits fair value (i.e., step 1 of the PEP reporting unit. Two of the most critical assumptions used in the calculation of the fair value of the PEP reporting unit are the target market long-term growth rate and the discount rate. Although management believes its estimate of fair value is reasonable, if the PEP reporting unit’s financial performance falls below expectation or there are negative revisions to key assumptions, the Company may be required to recognize antwo-step impairment charge.

test). If the carrying value of the reporting unit including goodwill iswas less than the fair value of the reporting unit, the goodwill iswas not considered impaired. IfReporting units for the carrying value is greater than fair value, then the potential for impairmentpurpose of goodwill exists. The potential impairment is determined by allocatingtesting were the fair value of the reporting unit among the assetssame as our operating segments (Mobile Solutions and liabilities based on a purchase price allocation methodology as if the reporting unit was acquired in a business combination. The fair value of the goodwill is implied from this allocation and compared to the carrying value with an impairment loss recognized if the carrying value is greater than the implied fair value.

Our indefinite lived intangible asset is accounted for similarly to goodwill. This asset is tested for impairment at least annually by comparing the fair value to the carrying value, using the relief from royalty rate method, and if the fair value is less than the carrying value, an impairment charge is recognized for the difference. The indefinite lived intangible asset was impaired during the year ended December 31, 2014, as management is in the process of phasing out the use of the trade name as a result of the Autocam acquisition.

Power Solutions).

Valuation allowances are recorded to reduce deferred tax assets when it is more likely than not that a tax benefit will not be realized. Provision has been made for income taxes on unremitted earnings of certain foreign subsidiaries as these earnings are not deemed to be permanently reinvested. We recognize income tax positions that meet the more likely than not threshold and accrue interest and potential penalties related to unrecognized income tax positions which are recorded as a component of the provision (benefit) for income taxes. We eliminate disproportionate tax effects from accumulated other comprehensive income (loss) when the circumstances upon which they are premised cease to exist.

We did not record a U.S. deferred tax liability for the excess of the book basis over the tax basis of our investments in foreign subsidiaries to the extent the foreign earnings meet the indefinite reversal criteria. As of the year ended December 31, 2016, we consider the unremitted foreign earnings of our foreign subsidiaries to be reinvested indefinitely. We base this assertion on two factors. First, our intention to invest in foreign countries that are strategically important to our Precision Bearing Components Group, Autocam Precision Components Group and customers. With the acquisitions completed in 2015 and 2014, we have expanded our domestic and international base of operations adding subsidiaries in Mexico and China, which will require more foreign investment. Second, we have sufficient access to funds in the U.S. through projected free cash flows and the availability of our credit facilities to fund currently anticipated domestic operational and investment needs. As such, we do not expect unrepatriated foreign earnings to become subject to U.S. taxation.

During

Devaluation2020.

The euro devalued against the U.S. dollar beginning in the latter part of the third quarter of 2014 and accelerated during the fourth quarter of 2014 and into the first quarter of 2015. During these periods, the euro to U.S. dollar dropped from approximately $1.36 in June 2014 to $1.08 in March 2015, representing an approximate 21% decline in value. The exchange rate ranged between $1.08 and $1.12 for the remainder of the 2015. The exchange rates ranged between $1.05 and $1.09 during 2016, with $1.05 being the exchange rate at December 31, 2016. The devaluation of the euro significantly impacted the translation of our euro denominated sales and costs when comparing year over year activity. The euro translation impact, and the translation impact of other currencies, is highlighted below in the overall results as “foreign exchange effects”. In addition to translation effects, the devaluation of the euro impacted the value of certain intercompany loan receivables denominated in euros.

Net Sales

The following table sets forth for the periods indicated selected financial data andpresents the percentage of our net sales represented by each income statement of operations line item presented.

As a Percentageitem.

| Years Ended December 31, | ||||||||||||||||||||

| 2021 | 2020 | 2019 | ||||||||||||||||||

| Net sales | 100.0 | % | 100.0 | % | 100.0 | % | ||||||||||||||

| Cost of sales (exclusive of depreciation and amortization shown separately below) | 81.7 | % | 80.4 | % | 80.2 | % | ||||||||||||||

| Selling, general, and administrative expense | 10.8 | % | 13.6 | % | 14.1 | % | ||||||||||||||

| Depreciation and amortization | 9.7 | % | 10.7 | % | 9.2 | % | ||||||||||||||

| Goodwill impairment | — | % | 21.7 | % | — | % | ||||||||||||||

| Other operating expense (income), net | (0.2) | % | 1.1 | % | 0.2 | % | ||||||||||||||

| Loss from operations | (1.9) | % | (27.5) | % | (3.6) | % | ||||||||||||||

| Interest expense | 2.7 | % | 4.4 | % | 2.7 | % | ||||||||||||||

| Loss on extinguishment of debt and write-off of debt issuance costs | 0.5 | % | — | % | 0.1 | % | ||||||||||||||

| Derivative payments on interest rate swap | 0.4 | % | 1.0 | % | — | % | ||||||||||||||

| Loss on interest rate swap | 0.4 | % | 2.7 | % | — | % | ||||||||||||||

| Other expense (income), net | (1.1) | % | — | % | 0.2 | % | ||||||||||||||

| Loss from continuing operations before benefit (provision) for income taxes and share of net income from joint venture | (4.7) | % | (35.6) | % | (6.6) | % | ||||||||||||||

| Benefit (provision) for income taxes | 0.4 | % | 2.1 | % | (0.1) | % | ||||||||||||||