0001059556mco:TwoThousandSeventeenFiveYearPrivatePlacementDueTwoThosandTwentyThreeMember2020-12-31

SECURITIES AND EXCHANGE COMMISSION

☑ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED

DECEMBERDecember 31,

20172021

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934FOR THE TRANSITION PERIOD FROM TO .

COMMISSION FILE NUMBER

1-14037(EXACT NAME OF REGISTRANT AS SPECIFIED IN ITS CHARTER) | | | | | |

DELAWAREDelaware | | 13-3998945 |

| (STATE OF INCORPORATION) | | (I.R.S. EMPLOYER IDENTIFICATION NO.) |

7 World Trade Center at 250 Greenwich Street,

NEW YORK, NEW YORKNew York, New York 10007

(ADDRESS OF PRINCIPAL EXECUTIVE OFFICES)

REGISTRANT’S TELEPHONE NUMBER, INCLUDING AREA CODE:

(212) 553-0300.SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

| | | | | | | | | | | | | | | | |

| TITLE OF EACH CLASS | | | | TRADING SYMBOL(S) | | NAME OF EACH EXCHANGE ON WHICH REGISTERED |

COMMON STOCK, PAR VALUE $.01 PER SHARECommon Stock, par value $0.01 per share | | NEW YORK STOCK EXCHANGE | | MCO | | New York Stock Exchange |

1.75% SENIOR NOTES DUESenior Notes Due 2027 | | NEW YORK STOCK EXCHANGE | | MCO 27 | | New York Stock Exchange |

| 0.950% Senior Notes Due 2030 | | | | MCO 30 | | New York Stock Exchange |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes

☑ No

☐Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes

☐ No

☑Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes

☑ No

☐Indicate by check mark whether the registrant has submitted electronically

and posted on its corporate Web site, if any, every Interactive Data File required to be submitted

and posted pursuant to Rule 405 of Regulation

S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit

and post such files). Yes

☑ No

☐Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer ☑ Accelerated Filer ☐Non-accelerated Filer ☐ Smaller reporting company ☐ Emerging growth company☐

| | | | | | | | | | | | | | | | | | | | | | | |

| Large Accelerated Filer | ☑ | Accelerated Filer ☐ | Non-accelerated Filer ☐ | Smaller reporting company | ☐ | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the

Registrantregistrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards

provided pursuant to Section 13(a) of the Exchange Act.

☐Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Act). Yes

☐ No

☑The aggregate market value of Moody’s Corporation Common Stock held by nonaffiliates* on June 30,

20172021 (based upon its closing transaction price on the

Composite TapeNew York Stock Exchange on such date) was approximately

$23.0$68 billion.

As of January 31,

2018, 191.12022, 185.2 million shares of Common Stock of Moody’s Corporation were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive proxy statement for use in connection with its annual meeting of stockholders scheduled to be held on April

24, 2018,26, 2022, are incorporated by reference into Part III of this Form

10-K.The Index to Exhibits is included as Part IV, Item 15(3) of this Form

10-K.*Calculated by excluding all shares held by executive officers and directors of the Registrant without conceding that all such persons are “affiliates” of the Registrant for purposes of federal securities laws.

** | Calculated by excluding all shares held by executive officers and directors of the Registrant without conceding that all such persons are “affiliates” of the Registrant for purposes of federal securities laws. | | | | | | | | | | | | | | | | |

| Auditor Name: | KPMG LLP | Auditor Location: | New York, NY | Auditor Firm ID: | 185 |

MOODY’S CORPORATION

INDEX TO FORM 10-K | | | | | | | | | | | |

| | MOODY’S 2017 10-KPage(s) |

| | | |

|

| Item 1. | | | |

MOODY’S CORPORATION

INDEX TO FORM10-K

| | | | | | | | | | | |

2 | | MOODY’S 2017 10-K | | | Page(s) |

| Item 9A. | |

| | |

| Item 9B. | | | |

| Item 9C. | | | |

| | Page(s) | |

| | |

| | PART III.

| | | | |

| Item 10. | | | | | 118 | |

| Item 11. | | | | | 118 | |

| Item 12. | | | | | 118 | |

| Item 13. | | | | | 118 | |

| Item 14. | | | | | 118 | |

| | |

| | PART IV.

| | | | |

| Item 15. | | | | | 119 | |

| |

SIGNATURES | | | 120 | |

| |

INDEX TO EXHIBITS | | | 121-124 | |

| | | | |

| | |

Exhibits

filed Herewith

| | |

10.2.1 | | 1998 Moody’s CorporationNon-Employee Directors’ Stock Incentive Plan (Adopted September 8, 2000; Amended and Restated as of December 11, 2012, October 20, 2015, December 14, 2015 and December 18, 2017) |

10.2.3 | | Form of Non-Employee Director Restricted Stock Unit Grant Agreement (for awards after 2017) for the 1998 Moody’s Corporation Non-Employee Directors’ Stock Incentive Plan (Adopted September 8, 2000; Amended and Restated as of December 11, 2012, October 20, 2015, December 14, 2015 and December 18, 2017) |

10.4.1 | | Amended and Restated 2001 Moody’s Corporation Key Employees’ Stock Incentive Plan (as amended, December 18, 2017) |

10.4.6 | | Form of Performance Share Award Letter (for awards granted after 2017) for the Amended and Restated 2001 Moody’s Corporation Key Employees’ Stock Incentive Plan. |

10.10 | | Moody’s Corporation Change in Control Severance Plan (as amended December 18, 2017). |

12 | | Statement of Computation of Ratios of Earnings to Fixed Charges |

21 | | SUBSIDIARIES OF THE REGISTRANT |

23.1 | | CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

31.1 | | Chief Executive Officer Certification Pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 |

31.2 | | Chief Financial Officer Certification Pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 |

32.1 | | Chief Executive Officer Certification Pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 |

32.2 | | Chief Financial Officer Certification Pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 |

101.DEF | | XBRL Definitions Linkbase Document |

101.INS | | XBRL Instance Document |

101.SCH | | XBRL Taxonomy Extension Schema Document |

101. CAL | | XBRL Taxonomy Extension Calculation Linkbase Document |

101.LAB | | XBRL Taxonomy Extension Labels Linkbase Document |

101.PRE | | XBRL Taxonomy Extension Presentation Linkbase Document |

GLOSSARY OF TERMS AND ABBREVIATIONS

The following terms, abbreviations and acronyms are used to identify frequently used terms in this report: | | | | | | | | |

| TERM | | DEFINITION |

| | |

TERM

| | DEFINITION

|

| | |

Acquisition-Related AmortizationAcquire Media (AM) | | An aggregator and distributor of curated real-time news, multimedia, data, and alerts; acquired by the Company on October 21, 2020 |

| | |

| Acquisition-Related Amortization | | Amortization of acquired definite-lived intangible assets acquired by the Company from all business combination transactions |

| | |

| Acquisition-Related Expenses | | Consists of expenses incurred over a multi-year period to complete and integrate the acquisition of Bureau van Dijk for which the integration will be a multi-year effort |

| | |

| Adjusted Diluted EPS | | Diluted EPS excluding the impact of certain items as detailed in Item 7 in the section entitled“Non-GAAP “Non-GAAP Financial Measures” |

| | |

| Adjusted Net Income | | Net Income excluding the impact of certain items as detailed in Item 7 in the section entitled“Non-GAAP “Non-GAAP Financial Measures” |

| | |

| Adjusted Operating Income | | Operating income excluding the impact of certain items as detailed in Item 7 in the section entitled“Non-GAAP "Non-GAAP Financial Measures”Measures" |

| | |

| Adjusted Operating Margin | | Adjusted Operating Income divided by revenue |

| | |

| Americas | | Represents countries within North and South America, excluding the U.S. |

| | |

AOCIAML | | Anti-money laundering |

| | |

| AOCI(L) | | Accumulated other comprehensive income (loss); a separate component of shareholders’ (deficit) equity |

| | |

ASC | | |

| | |

| ASC | | The FASB Accounting Standards Codification; the sole source of authoritative GAAP as of July 1, 2009 except for rules and interpretive releases of the SEC, which are also sources of authoritative GAAP for SEC registrants |

| | |

| Asia-Pacific | | Represents Australia and countries in Asia including but not limited to: Australia, China, India, Indonesia, Japan, Korea, Malaysia, Singapore, Sri Lanka and Thailand |

| | |

ASUASR | | Accelerated Share Repurchase |

| | |

| ASU | | The FASB Accounting Standards Update to the ASC. It also provides background information for accounting guidance and the bases for conclusions on the changes in the ASC. ASUs are not considered authoritative until codified into the ASC |

| |

Basel II | | Capital adequacy framework published in June 2004 by the Basel Committee on Banking Supervision |

| |

Basel IIIB&H | | A new global regulatory standard on bank capital adequacy and liquidity agreed by the membersBarrie & Hibbert Limited, an acquisition completed in December 2011; part of the Basel Committee on Banking Supervision. Basel III was developed in a response to the deficiencies in financial regulation revealed by the global financial crisis. Basel III strengthens bank capital requirements and introduces new regulatory requirements on bank liquidity and bank leverage |

| |

BlackBox | | BlackBox Logic;MA segment, a leading provider of Residential Mortgage-Backed securities loan level data. The Company acquired the customer base and products of BlackBox Logic in December 2015risk management modeling tools for insurance companies worldwide |

| | |

| Board | | The board of directors of the Company |

| | |

| BPS | | Basis points |

| | |

| Brexit | | The withdrawal of the United Kingdom from the European Union |

| | |

| Bureau van Dijk | | Bureau van Dijk Electronic Publishing, B.V.,; a global provider of business intelligence and company information; acquired by the companyCompany on August 10, 2017 via the acquisition of yellowYellow Maple I B.V., an indirect parent of Bureau van DijkDijk; part of the RD&A LOB |

| | |

CCARBitSight | | Comprehensive Capital AnalysisA provider of cybersecurity ratings, analytics, and Review; annual review by the Federal Reserveperformance management tools; Moody's acquired a minority investment in the U.S. to ensure that financial institutions have sufficient capitalBitSight in times of economic and financial stress and that they have robust, forward-looking capital-planning processes that account for their unique risks.2021 |

| | |

CCXICatylist | | A provider of commercial real estate (CRE) solutions for brokers; acquired by the Company on December 30, 2020 |

| | |

| CCXI | | China ChenCheng Xin International Credit Rating Co. Ltd.; China’s first and largest domestic credit rating agency approved by the People’s Bank of China; the Company acquired a 49% interest in 2006; currently Moody’s owns 30% of CCXI |

| | |

CCXI Gain | | In |

| CDP | | A not-for-profit charity that runs the first quarter of 2017 CCXI, as a part of a strategic business realignment, issued additional capitalglobal disclosure system for investors, companies, cities, states and regions to its majority shareholder in exchange for a ratings business wholly-owned by the majority shareholder and which has the right to rate a different class of debt instruments in the Chinese market. The capital issuance by CCXI in exchange for the ratings business diluted Moody’s ownership interest in CCXI to 30% of a larger business and resulted in a $59.7 millionnon-cash,non-taxable gainmanage their environmental impacts |

| | |

| | | | | | | | |

4 | | MOODY’S 2017 10-K | TERM | | | DEFINITION |

| | |

TERM

CFG | | DEFINITION

|

CFG

| | Corporate finance group; an LOB of MIS |

| | |

| CLO | | Collateralized loan obligation |

| | |

| CMBS | | Commercial mortgage-backed securities; part of the CREFan asset class within SFG |

| | |

CommissionCOLI | | European CommissionCorporate-Owned Life Insurance |

| | |

| Commission | | European Commission |

| | |

| Common Stock | | The Company’s common stock |

| | |

| Company | | Moody’s Corporation and its subsidiaries; MCO; Moody’s |

| | |

CopalContent | | Copal Partners; an acquisition completed in November 2011; partPrior to the second quarter of 2021, was a reporting unit within the MA segment; leading provider of offshoresegment that offered subscription-based research, data and analytical products, including credit ratings produced by MIS, credit research, quantitative credit scores and other analytical tools, economic research and analytical services to institutional investorsforecasts |

| | |

CouncilCortera | | CouncilA provider of North American credit data and workflow solutions; acquired by the European UnionCompany in March 2021 |

| | |

CPCOVID-19 | | Commercial paperAn outbreak of a novel strain of coronavirus resulting in an international public health crisis and a global pandemic |

| | |

| CP | | Commercial Paper |

| | |

| CP Notes | | Unsecured commercial paper issued under the CP Program |

| | |

| CP Program | | A program entered into on August 3, 2016 allowing the Company to privately place CP up to a maximum of $1 billion for which the maturity may not exceed 397 days from the date of issue.issue, and which is backstopped by the 2021 Facility. |

| | |

| CRAs | | Credit rating agencies |

| | |

CREFCRE | | Commercial real estate finance, which includes REITs, commercial real estate CDOs and mortgage-backed securities; part of SFGReal Estate |

| | |

CSIDBPPs | | CSI Global Education, Inc.; an acquisition completed in November 2010; part of the PS LOB and FSTC reporting unit within the MA segment; a provider of financial learning, credentials, and certification services primarily in CanadaDefined benefit pension plans |

| | |

CSPPDodd-Frank Act | | Corporate Sector Purchase Programme; quantitative easing program implemented by the ECB. This program allows the central bank to purchase bonds issued by European companies, as well as provide access to the secondary bond market in which existing corporate bonds tradeDodd-Frank Wall Street Reform and Consumer Protection Act |

| |

D&A | | Depreciation and amortization |

| |

DBPPsEBITDA | | Defined benefit pension plans |

| |

DBRS | | Dominion Bond Rating Service |

| |

DCF | | Discounted cash flow; a fair value calculation methodology whereby future projected cash flows are discounted back to their present value |

| |

Debt/EBITDA | | Ratio of Total Debt to EBITDA |

| |

Directors’ Plan | | The 1998 Moody’s CorporationNon-Employee Directors’ Stock Incentive Plan |

| |

Distribution Date | | September 30, 2000; the date which Old D&B separated into two publicly traded companies—Moody’s Corporation and New D&B |

| |

DOJ | | U.S. Department of Justice |

| |

E&P | | Earnings and profits |

| |

EBITDA | | Earnings before interest, taxes, depreciation and amortization |

| |

ECB | | European Central Bank |

| |

ECCA | | Economics and Consumer Credit Analytics; a business within the RD&A LOB which provides economic and consumer credit trend analytics |

| | | | | | |

| | MOODY’S 2017 10-K |

| EEO-1 | | | 5 | Data filing required by the U.S. Equal Employment Opportunity Commission that requires all private sector employers with 100 or more employees, and federal contractors with 50 or more employees meeting certain criteria, to submit demographic workforce data, including data by race/ethnicity, sex and job categories |

| | |

TERM

EMEA | | DEFINITION

|

| |

EMEA

| | Represents countries within Europe, the Middle East and Africa |

| | |

| EPS | | Earnings per share |

| |

Equilibrium | | A leading provider of credit rating and research services in Peru and Panama; acquired by Moody’s in May 2015 |

| |

| ERS | | The enterprise risk solutionsEnterprise Risk Solutions; an LOB within MA, which offers risk management software productssolutions as well as software implementation services and related risk management advisory engagements services |

| | |

| ESA | | Economics and Structured Analytics; part of the RD&A line of business within MA |

| | |

| ESG | | Environmental, Social and Governance |

| | |

| ESMA | | European Securities and Markets Authority |

| | |

ESPESPP | | Estimated Selling Price; estimate of selling price, as defined in the ASC, at which the vendor would transact if the deliverable were sold by the vendor regularly on a stand-alone basisEmployee stock purchase plan |

| | |

ESPPETR | | The 1999 Moody’s Corporation Employee Stock Purchase PlanEffective tax rate |

| | |

ETREU | | Effective tax rateEuropean Union |

| | |

EUEUR | | European UnionEuros |

| | |

EUREURIBOR | | EurosThe Euro Interbank Offered Rate |

| | |

European Ratings PlatformEurozone | | Central credit ratings website administered by ESMAMonetary union of the EU member states which have adopted the euro as their common currency |

| | |

| | | | | | | | |

| TERM | | DEFINITION |

| | |

| Excess Tax Benefits | | The difference between the tax benefit realized at exercise of an option or delivery of a restricted share and the tax benefit recorded at the time the option or restricted share is expensed under GAAP |

| | |

| Exchange Act | | The Securities Exchange Act of 1934, as amended |

| | |

FASBExternal Revenue | | Revenue excluding any intersegment amounts |

| | |

| FASB | | Financial Accounting Standards Board |

| | |

FIGFermat | | Fermat International; an acquisition completed in October 2008; part of the MA segment; a provider of risk and performance management software to the global banking industry |

| | |

| FIG | | Financial institutions group; an LOB of MIS |

| |

Fitch | | Fitch Ratings, a part of the Fitch Group |

| |

Financial Reform Act | | Dodd-Frank Wall Street Reform and Consumer Protection Act |

| | |

| Four Twenty Seven | | A provider of data, intelligence, and analysis related to physical climate risks; acquired by the Company in July 2019 |

| | |

| Free Cash Flow | | Net cash provided by operating activities less cash paid for capital additions |

| | |

FSTCFTSE | | Financial Services Training and Certifications; part of the PS LOB and a reporting unit within the MA reportable segment; consists ofon-line and classroom-based training services and CSITimes Stock Exchange |

| | |

| FX | | Foreign exchange |

| | |

| GAAP | | U.S. Generally Accepted Accounting Principles |

| | |

| GBP | | British pounds |

| | |

| GDP | | Gross domestic product |

| | |

GGYGDPR | | Gilliland Gold Young; a leading provider of advanced actuarial software for the global insurance industry. The Company acquired GGY on March 1, 2016; Part of the ERS LOB and reporting unit within the MA reportable segmentEuropean Union’s General Data Protection Regulation |

| | |

| ICRA | | ICRA Limited; a leading provider of credit ratings and research in India. The Company previously held 28.5% equity ownership and in June 2014, increased that ownership stake to just over 50% through the acquisition of additional shares |

| |

ICRA Acquisition | | The June 2014 purchase of an additional interest in ICRA resulting in a majority ownership of ICRA; ICRAs results are consolidated into Moody’s financial statements on a three-month lag and accordingly the Company began including the results of operations for ICRA in its consolidated financial statements beginning in the fourth quarter of 2014 |

| | |

TERM

| | DEFINITION

|

| |

ICRA Gain

| | Gain relating to the ICRA Acquisition; U.S. GAAP requires the remeasurement to fair value of the previously heldnon-controlling shares upon obtaining a controlling interest in a step-acquisition. This remeasurement of the Company’s equity investment in ICRA to fair value resulted in apre-tax gain of $102.8 million ($78.5 million after tax) in the second quarter of 2014

|

| |

ICTEAS | | ICRA Techno Analytics; formerly a wholly-owned subsidiary of ICRA; divested by ICRA in the fourth quarter of 2016 |

| | |

Intellectual PropertyINR | | The Company’s intellectual property, including but not limited to proprietary information, trademarks, research, software tools and applications, models and methodologies, databases, domain names, and other proprietary materialsIndian National Rupee |

| | |

| IRS | | Internal Revenue Service |

| |

IT | | Information technology |

| | |

KIS | | |

| KIS | | Korea Investors Service, Inc;Inc.; a leading Korean rating agency and consolidated subsidiary of the Company |

| | |

| KIS Pricing | | Korea Investors Service Pricing, Inc;Inc.; a leading Korean provider of fixed income securities pricing and consolidated subsidiary of the Company |

| | |

| KIS Research | | Korea Investors Service Research; a Korean provider of financial research and consolidated subsidiary of the Company |

| | |

| Korea | | Republic of South Korea |

| | |

Legacy Tax Matter(s)KYC | | Exposures to certain potential tax liabilities assumed in connection with the Company’sspin-off from Dun & Bradstreet in 2000Know-your-customer |

| | |

LIBOR | | |

| | |

| LIBOR | | London Interbank Offered Rate |

| | |

| LOB | | Line of business |

| |

M&A | | Mergers and acquisitions |

| |

| MA | | Moody’s Analytics—a reportable segment of MCO formed in January 2008MCO; a global provider of: i) data and information; ii) research and insights; and iii) decision solutions, which provides a wide range of productshelp companies make better and services that support financial analysis and risk management activities of institutional participants in global financial markets;faster decisions; consists of threetwo LOBs—RD&A ERS and PSERS |

| | |

| Make Whole Amount | | The prepayment penalty amount relating to the Series 2007-1 Notes, 2010certain Senior Notes, 2012 Senior Notes, 2013 Senior Notes, 2014 Senior Notes (5-year), 2014 Senior Notes (30-year), 2015 Senior Notes, 2017 Senior Notes, 2017 Private Placement Notes Due 2023 and 2028 which is a premium based on the excess, if any, of the discounted value of the remaining scheduled payments over the prepaid principal |

| | |

| MAKS | | Moody’s Analytics Knowledge Services; formerly known as Copal Amba; providesprovided offshore research and analytic services to the global financial and corporate sectors; business was divested in the fourth quarter of 2019 and was formerly part of the PS LOB and a reporting unit within the MA reportable segmentsegment. |

| | |

MCOMALS | | Moody’s Analytics Learning Solutions; prior to the second quarter of 2021, was a reporting unit within the MA segment that offered on-line and classroom-based training services as well as credentialing and certification services |

| | |

| MCO | | Moody’s; Moody’s Corporation and its subsidiaries; the Company; Moody’sCompany |

| | |

| | | | | | | | |

| TERM | | DEFINITION |

| | |

| MD&A | | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

| | |

MIS | | |

| | |

| MIS | | Moody’s Investors Service—a reportable segment of MCO; consists of five LOBs—SFG, CFG, FIG, PPIF and MIS Other |

| | |

| MIS Other | | Consists ofnon-ratings revenue from ICRA, KIS Pricing and KIS Research.Research revenue as well as revenue from providing ESG research, data and assessments. These businesses are components of MIS; MIS Other is an LOB of MIS |

| | |

| Moody’s | | Moody’s Corporation and its subsidiaries; MCO; the Company |

| | |

| Moody's Local | | A ratings platform focused on providing credit rating services in local capital markets |

| | |

| MSS | | Moody's Shared Services; primarily consists of information technology and support staff such as finance, human resources and legal that support both MIS and MA. |

| | |

| NAV | | Net asset value |

| | |

| Net Income | | Net income attributable to Moody’s Corporation, which excludes net income from consolidated noncontrolling interests belonging to the minority interest holder |

| |

New D&B | | The New D&B Corporation—which comprises the D&B business after September 30, 2000 |

| | |

TERM

New Credit Losses Accounting Standard | | DEFINITION

Updates to the ASC pursuant to ASU No. 2016-13, “Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments”. This new accounting guidance requires the use of an “expected credit loss” impairment model for most financial assets reported at amortized cost, which requires entities to estimate expected credit losses over the lifetime of the instrument. |

| | |

NM

New Lease Accounting Standard | | Updates to the ASC pursuant to ASU No. 2016-02, “Leases (ASC Topic 842)”. This new accounting guidance requires lessees to recognize a right-of-use asset and lease liability on the balance sheet for all leases with terms of more than 12 months. Recognition, measurement and presentation of expenses and cash flows depend on classification as either a finance or operating lease |

| | |

| NM | | Percentage change is not meaningful |

| | |

| Non-GAAP | | A financial measure not in accordance with GAAP; these measures, when read in conjunction with the Company’s reported results, can provide useful supplemental information for investors analyzingperiod-to-period comparisons of the Company’s performance, facilitate comparisons to competitors’ operating results and to provide greater transparency to investors of supplemental information used by management in its financial and operational decision making |

| | |

| NRSRO | | Nationally Recognized Statistical Rating Organization, which is a credit rating agency registered with the SEC. |

| | |

| OCI | | Other comprehensive income (loss); includes gains and losses on cash flow and net investment hedges, unrealized gains and losses on available for sale securities, certain gains and losses relating to pension and other retirement benefit obligations and foreign currency translation adjustments |

| |

Old D&B | | The former Dun and Bradstreet Company which distributed New D&B shares on September 30, 2000, and was renamed Moody’s Corporation |

| | |

| | |

| Operating segment | | Term defined in the ASC relating to segment reporting; the ASC defines an operating segment as a component of a business entity that has each of the three following characteristics: i) the component engages in business activities from which it may recognize revenue and incur expenses; ii) the operating results of the component are regularly reviewed by the entity’s chief operating decision maker; and iii) discrete financial information about the component is available. |

| | |

Other Retirement PlanPlans | | The U.S. retirement healthcare and U.S. retirement life insurance plans |

| | |

PPIFPassFort | | A U.K. SaaS-based workflow platform for identity verification, customer onboarding, and risk analysis; acquired by the Company on November 30, 2021. |

| | |

| PCS | | Post-Contract Customer Support |

| | |

| PPIF | | Public, project and infrastructure finance; an LOB of MIS |

| | |

| Profit Participation Plan | | Defined contribution profit participation plan that covers substantially all U.S. employees of the Company |

| | |

| | | | | | | | |

PSTERM | | DEFINITION |

| | |

| PS | | Professional Services, ana former LOB within MA consistingwhich consisted of MAKS and FSTCMALS that providesprovided offshore researchanalytical and analyticalresearch services as well as financial traininglearning solutions and certification programsprograms. Subsequent to the divestiture of MAKS in 2019, revenue from the MALS reporting unit, which previous to 2020 was reported in the PS LOB, is now reported as part of the RD&A LOB. Prior periods have not been reclassified as the amounts were not material. |

| | |

Purchase Price HedgeRealXData | | Foreign currency collarA provider of CRE lease-level portfolio management with benchmarking and forward contracts enteredrent forecasting capabilities; acquired by the Company to economically hedge the Bureau van Dijk euro denominated purchase pricein September 2021 |

| |

Purchase Price Hedge Gain | | Gain on foreign currency collars to economically hedge the Bureau van Dijk euro denominated purchase price |

| |

| RD&A | | Research, Data and Analytics; an LOB within MA that produces, sells and distributesoffers: subscription based research, data and related content. Includesanalytical products, generatedincluding credit ratings produced by MIS, such as analyses on major debt issuers, industry studies, and commentary on topicalMIS; credit events. Also includes economic research, data,research; quantitative riskcredit scores and other analytical tools that are produced within MAtools; economic research and forecasts; business intelligence and company information productsproducts; commercial real estate data and analytical tools; and on-line and classroom-based training services as well as credentialing and certification services |

| |

Reform Act | | Credit Rating Agency Reform Act of 2006 |

| |

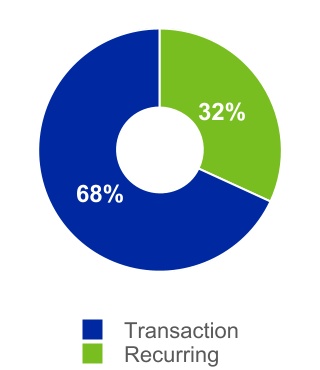

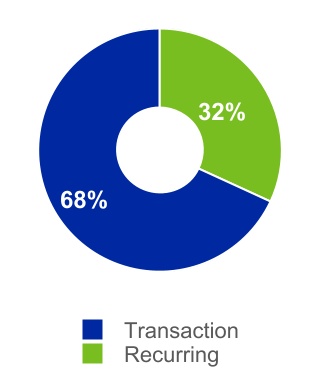

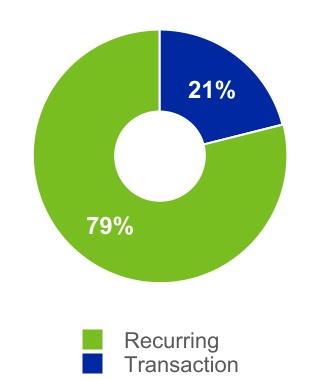

REITRecurring Revenue | | Real Estate Investment Trust |

| |

Relationship Revenue | | For MIS, represents recurring monitoring fees of a rated debt obligation and/or entities that issue such obligations, as well as revenue from programs such as commercial paper, medium-term notes and shelf registrations. For MIS Other represents subscription-based revenue. For MA, represents subscription-based licenserevenue and software maintenance revenue |

| | |

| Reform Act | | Credit Rating Agency Reform Act of 2006 |

| | |

| Regulatory Data Corporation (RDC) | | A provider of anti-money laundering (AML) and know-your-customer (KYC) data and due diligence services; the Company acquired RDC in February 2020 |

| | |

| REIT | | Real Estate Investment Trust |

| | |

| Reis, Inc. (Reis) | | A provider of U.S. commercial real estate (CRE) data; acquired by the Company in October 2018; part of the RD&A LOB and prior to the second quarter of 2021 a reporting unit within the MA reportable segment. |

| | |

| Reporting unit | | The level at which Moody’s evaluates its goodwill for impairment under U.S. GAAP; defined as an operating segment or one level below an operating segment |

| | |

| Retirement Plans | | Moody’s funded and unfunded pension plans, the healthcare plans and life insurance plans |

| | |

S&PRevenue Accounting Standard | | S&P Global Ratings,Updates to the ASC pursuant to ASU No. 2014-09, “Revenue from Contracts with Customers (ASC Topic 606)”. This accounting guidance significantly changed the accounting framework under U.S. GAAP relating to revenue recognition and to the accounting for the deferral of incremental costs of obtaining or fulfilling a division of S&P Global Inc.contract with a customer |

| |

SAV | | Structured Analytics and Valuation; a business within the RD&A LOB which provides data and analytics for securitized assets |

| |

SCDM | | SCDM Financial, a leading provider of analytical tools for participants in securitization markets. Moody’s acquired SCDM’s structured finance data and analytics business in February 2017 |

| | |

SECRMBS | | Residential mortgage-backed securities; an asset class within SFG |

| | |

| RMS | | A global provider of climate and natural disaster risk modeling and analytics; acquired by the Company in September 2021 |

| | |

| ROU Asset | | Assets recorded pursuant to the New Lease Accounting Standard which represent the Company’s right to use an underlying asset for the term of a lease |

| | |

| SaaS | | Software-as-a-Service |

| | |

| SEC | | U.S. Securities and Exchange Commission |

| | |

| Securities Act | | Securities Act of 1933, as amended |

| |

Series2007-1 Notes | | Principal amount of $300 million, 6.06% senior unsecured notes due in September 2017 pursuant to the 2007 Agreement; prepaid in March 2017 |

| | |

TERM

SFG | | DEFINITION

|

| |

Settlement Charge

| | Charge of $863.8 million recorded in the fourth quarter of 2016 related to an agreement entered into on January 13, 2017 with the U.S. Department of Justice and the attorneys general of 21 U.S. states and the District of Columbia to resolve pending and potential civil claims related to credit ratings that MIS assigned to certain structured finance instruments in the financial crisis era

|

| |

SFG | | Structured finance group; an LOB of MIS |

| | |

| SG&A | | Selling, general and administrative expenses |

| | |

Solvency IISOFR | | EU directive 2009/138/EC that codifies the amount of capital that EU insurance companies must hold to reduce insolvencySecured Overnight Financing Rate |

| |

Stock Plans | | The Old D&B’s 1998 Key Employees’ Stock Incentive Plan and the Restated 2001 Moody’s Corporation Key Employees’ Stock Incentive Plan |

| | |

| | |

| SSP | | Standalone selling price |

| | |

| T&M | | Time-and-Material |

| | |

| Tax Act | | The “Tax Cuts and Jobs Act” enacted into U.S. law on December 22, 2017, which significantly amends the tax code in the U.S. |

| | |

| TCFD | | Task Force on Climate-Related Financial Disclosures |

| | |

| | | | | | | | |

| TERM | | DEFINITION |

| | |

| Total Debt | | All indebtedness of the Company as reflected on the consolidated balance sheets |

| |

TPE | | Third party evidence, as defined in the ASC, used to determine selling price based on a vendor’s or any competitor’s largely interchangeable products or services in standalone sales transactions to similarly situated customers |

| |

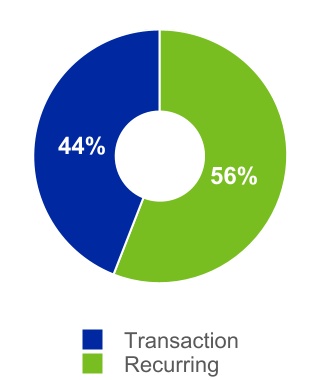

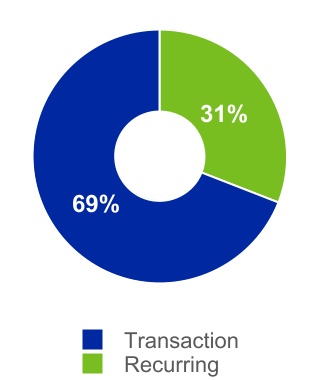

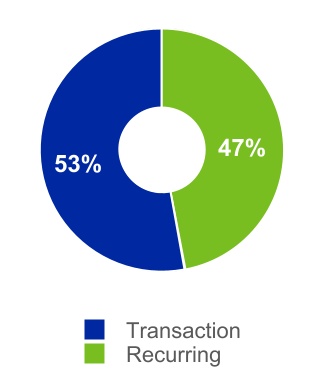

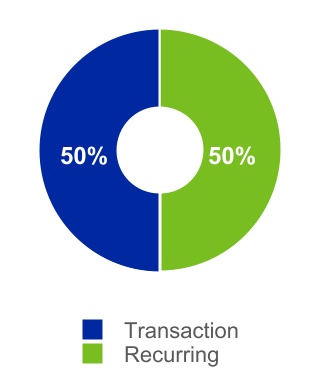

| Transaction Revenue | | For MIS, represents the initial rating of a new debt issuance as well as otherone-time fees. For MIS Other, represents revenue from professional services as well as data services, research and analytical engagements. For MA, represents perpetual software license fees and revenue from software implementation services, risk management advisory projects, training and certification services, and research and analytical engagements |

| | |

| U.K. | | United Kingdom |

| | |

| U.S. | | United States |

| | |

| USD | | U.S. dollar |

| | |

UTBsUTPs | | UnrecognizedUncertain tax benefitspositions |

| | |

UTPsVigeo Eiris (VE) | | Uncertain tax positionsA provider of ESG research, data and assessments; acquired by the Company in April 2019 |

| | |

VSOEVisibleRisk | | Vendor specific objective evidence; as defined in the ASC, evidence of selling price limited to either of the following: the price charged forA cyber risk ratings joint venture created by Moody’s and Team8, a deliverable when it is sold separately, or for a deliverable not yet being sold separately, the price established by management having the relevant authorityglobal venture group |

| | |

| WACC | | Weighted average costAverage Cost of capitalCapital |

| | |

1998 PlanZM Financial Systems (ZMFS) | | Old D&B’s 1998 Key Employees’ Stock Incentive PlanA provider of risk and financial management software for the U.S. banking sector; acquired by the Company in December 2020 |

| | |

2001 Plan2018 Restructuring Program | | The AmendedRestructuring program approved by the chief executive officer of Moody’s on October 26, 2018. This program included relocation of certain functions from high-cost to lower-cost jurisdictions, a reduction of staff, including from acquisitions and Restated 2001 Moody’s Corporation Key Employees’ Stock Incentive Planpursuant to a review of the business criticality of certain positions, and the rationalization and exit of certain real estate leases due to consolidation of various business activities. |

| | |

2007 Agreement2020 MA Strategic Reorganization Restructuring Program | | Note purchase agreement dated September 7, 2007,Restructuring program approved by the chief executive officer of Moody’s on December 22, 2020, relating to a strategic reorganization in the Series2007-1 NotesMA reportable segment. |

| | |

2010 Indenture2020 Real Estate Rationalization Restructuring Program | | Supplemental indenture and related agreements dated August 19, 2010, relatingRestructuring program approved by the chief executive officer of Moody’s on July 29, 2020, primarily in response to the 2010 Senior NotesCOVID-19 pandemic which revolves around the rationalization and exit of certain real estate leases. |

| |

2010 Senior Notes | | Principal amount of $500 million, 5.50% senior unsecured notes due in September 2020 pursuant to the 2010 Indenture |

| |

2012 Facility | | Revolving credit facility of $1 billion entered into on April 18, 2012; was replaced with the 2015 Facility |

| |

2012 Indenture | | Supplemental indenture and related agreements dated August 18, 2012, relating to the 2012 Senior Notes Due 2022 |

| |

2012 Senior Notes | | Principal amount of $500 million, 4.50% senior unsecured notes due in September 2022, pursuant tobut early repaid by the 2012 IndentureCompany in 2021 |

| |

2013 Indenture | | Supplemental indenture and related agreements dated August 12, 2013, relating to the 2013 Senior Notes |

| | |

TERM

| | DEFINITION

|

| |

| 2013 Senior Notes Due 2024 | | Principal amount of the $500 million, 4.875% senior unsecured notes due in February 2024 pursuant to the 2013 Indenture |

| | |

2014 Indenture | | Supplemental indenture and related agreements dated July 16, 2014, relating to the 2014 Senior Notes Due 2044 |

| |

2014 Senior Notes(5-Year) | | Principal amount of $450 million, 2.75% senior unsecured notes due in July 2019 |

| |

2014 Senior Notes(30-Year) | | Principal amount of $600 million, 5.25% senior unsecured notes due in July 2044 |

| | |

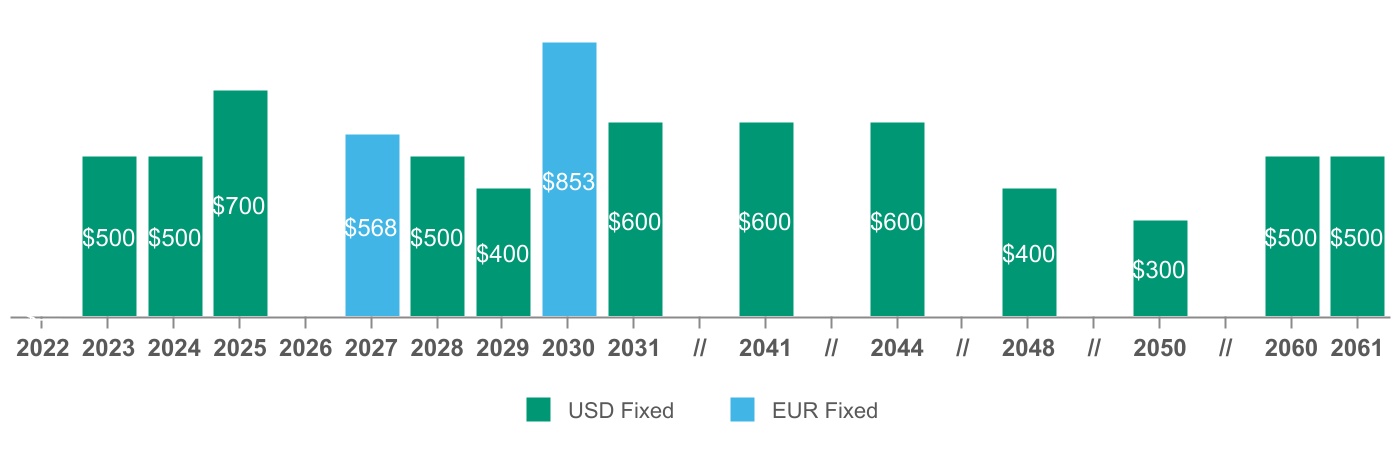

2015 FacilitySenior Notes Due 2027 | | Principal amount of €500 million, 1.75% senior unsecured notes due in March 2027 |

| | |

| 2017 Senior Notes Due 2023 | | Principal amount of $500 million, 2.625% senior unsecured notes due January 15, 2023 |

| | |

| 2017 Senior Notes Due 2028 | | Principal amount of $500 million, 3.25% senior unsecured notes due January 15, 2028 |

| | |

| | |

| | |

| 2018 Facility | | Five-year unsecured revolving credit facility, with capacity to borrow up to $1 billion; backstops CP issued under the CP Program. The 2021 Facility replaces the 2012 FacilityCompany's $1 billion 2018 Credit Facility. |

| |

2015 Indenture | | Supplemental indenture and related agreements dated March 9, 2015, relating to the 2015 Senior Notes |

| | |

2015 | | |

| 2018 Senior Notes Due 2029 | | Principal amount€500 of $400 million, 1.75%4.25% senior unsecured notes issued March 9, 2015 and due in March 2027February 1, 2029 |

| | |

2017 Bridge Credit Facility | | Bridge Credit Agreement entered into in May 2017 pursuant to the definitive agreement to acquire Bureau van Dijk; this facility was terminated in June 2017 upon issuance of the 2017 Private Placement2018 Senior Notes Due 2023 and 20282048 | | Principal amount of $400 million, 4.875% senior unsecured notes due December 17, 2048 |

| | |

2017 Floating Rate2019 Senior Notes Due 2030 | | Principal amount of €750 million, 0.950% senior unsecured notes due February 25, 2030 |

| | |

| | | | | | | | |

| TERM | | DEFINITION |

| | |

| 2020 Senior Notes Due 2025 | | Principal amount of $700 million, 3.75% senior unsecured notes due March 24, 2025 |

| | |

| 2020 Senior Notes Due 2050 | | Principal amount of $300 million, floating rate3.25% senior unsecured notes due in September 2018May 20, 2050 |

| | |

2017 Indenture | | Collectively the Supplemental indenture and related agreements dated March 2, 2017, relating to the 2017 Floating Rate2020 Senior Notes and 2017 Senior Notes and the Supplemental indenture and related agreements dated June 12, 2017, relating to the 2017 Private Placement Notes Due 2023 and 20282060 |

| |

2017 Private Placement Notes due 2023 | | Principal amount of $500 million, 2.625%2.55% senior unsecured notes due January 15, 2023August 18, 2060 |

| | |

2017 Private Placement2021 Facility | | Five-year unsecured revolving credit facility, with capacity to borrow up to $1.25 billion; backstops CP issued under the CP Program. |

| | |

2021 Senior Notes Due 20282031 | | Principal amount $500of $600 million, 3.250%2.00% senior unsecured notes due January 15, 2028August 19, 2031 |

| | |

20172021 Senior Notes Due 2041 | | Principal amount of $600 million, 2.75% senior unsecured notes due August 19, 2041 |

| | |

| 2021 Senior Notes Due 2061 | | Principal amount of $500 million, 2.75%3.10% senior unsecured notes due December 2021November 15, 2061 |

| |

2017 Term Loan | | $500 million, three-year term loan facility entered into on June 6, 2017 for which the Company drew down $500 million on August 8, 2017 to fund the acquisition of Bureau van Dijk |

| |

| 7WTC | | The Company’s corporate headquarters located at 7 World Trade Center in New York, NY |

ITEM 1. BUSINESS

As used in this report, except where the context indicates otherwise, the terms “Moody’s” or the “Company” refer to Moody’s Corporation, a Delaware corporation, and its subsidiaries. The Company’s executive offices are located at 7 World Trade Center at 250 Greenwich Street, New York, NY 10007 and its telephone number is

(212) 553-0300.

Company Overview

Moody’s is a

provider of (i) credit ratings; (ii) credit, capital marketsglobal integrated risk assessment firm that empowers organizations and

economic research, data and analytical tools; (iii) software solutions that support financial risk management activities; (iv) quantitatively derived credit scores; (v) financial services training and certification services; (vi) offshore financial research and analytical services; and (vii) company information and business intelligence products.investors to make better decisions. Moody’s reports in two

reportable segments: MIS and MA. Financial information and operating results of these segments, including revenue, expenses and

operating income,Adjusted Operating Income, are included in Part II, Item 8. Financial Statements of this annual report and are herein incorporated by reference.

MIS

| | | | | | | | | | | | | | | | | |

| | | | | |

|

| |

| Independent provider of credit rating opinions and related information for over 100 years | | Global integrated risk assessment firm providing credit rating opinions, analytical solutions and insights that empower organizations to make better, faster decisions | | Provider of financial intelligence and analytical tools supporting customers’ growth, efficiency and risk management objectives |

| | | | | |

| | | | | | | | | | | | | | |

| Moody's has evolved over the last 15 years as our customers' needs have changed and we expanded our capabilities |

| | | | |

| | | 2007 - 2016 | |

| | Expanded beyond ratings agency | |

| | •Established Moody’s Analytics •Built the ERSbusiness (e.g., Fermat, B&H) •Expanded ratings to China (i.e., CCXI) | |

| | | | |

| | | 2017 - 2021 | |

| | Built out substantial data and analytics capabilities | |

| | •Complemented ERS business with private company information(i.e., BvD) •Accelerated capability expansion (e.g., company database, CRE data, ESG data) •Invested in insurance data and analytics capabilities, including weather and disaster modeling (i.e., RMS) | |

| | | | |

| | | 2022 and Beyond | |

| | Positioned to serve a wide range of risk assessment markets | |

| | •Competitive differentiator: integration of data and analytics combined with expertise and technology enablement •Further investment in data and analytics capabilities such as private company, CRE and ESG to serve high growth risk assessment use cases (e.g., KYC and compliance) | |

Moody's Investors Service Overview

Moody's Investors Service (MIS) publishes credit ratings and provides assessment services on a wide range of debt obligations, programs and facilities, and the entities that issue such obligations in markets worldwide, including various corporate, financial institution and governmental obligations, and structured finance securitiessecurities. A rating from MIS enables issuers to create timely, go-to-market debt strategies with the ability to capture wider investor focus and commercial paper programs. deeper liquidity options.

| | | | | | | | | | | | | | | | | | | | |

| The Benefits of a Moody's Rating |

| Investors seek Moody's opinions and particularly value the knowledge of its analysts and the depth of Moody's research |

| | | | | | |

| Access to capital | | Transparency, credit comparison and market stability | | Planning and budgeting | | Analytical capabilities |

•Moody’s opinions on credit are used by institutional investors throughout the world, making an issuer’s debt potentially more attractive to a wide range of buyers. | | •Signals a willingness by issuers to be transparent and provides issuers with an independent assessment against which to compare creditworthiness. | | •May help issuers when formulating internal capital plans and funding strategies. | | •Among ratings advisors, Moody’s has a strong position and is well-recognized for the depth and breadth of its analytical capabilities. |

| | | | | | |

•A Moody’s rating may facilitate access to both domestic and international debt capital.

| | •Moody’s ratings and research reports may help to maintain investor confidence, especially during periods of market stress. | | | | |

Ratings revenue is derived from the originators and issuers of such transactions who use MIS ratings to support the distribution of their debt issues to investors. MIS provides ratings in more than 120 countries. Ratings are disseminated via press releases to the public primarily through a variety of print and electronic media, including the Internetinternet and real-time information systems widely used by securities traders and investors. As of December 31, 2017,

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| MIS by the Numbers |

| | | | | | | | | |

| 35,000+ | | | | | | | |

| Rated Organizations and Structured Deals | | | | |

| | | | | | | | | |

| | 5,300+ | | | 3,500+ | | | 15,500+ | |

| Rated Non-Financial Corporates | | Rated Financial Institutions | | Rated Public Finance Issuers | |

| | | | | | | | | |

| | 9,000+ | | | 1,000+ | | | 445 | |

| Rated Structured Finance Deals | | Rated Infrastructure & Project Finance Issuers | | Rated Sub-Sovereigns

| |

| | | | | | | | | |

| | 145 | | | 49 | | | $73 trillion | |

| Rated Sovereigns | | Rated Supranational Institutions | | Total rated debt outstanding | |

| | | | | | | | | |

| | 190 | | | | | | | |

| Rating Methodologies | | | | | | |

MIS

had the following ratings relationships:» | | Approximately 4,700 ratednon-financial corporate issuers; |

» | | Approximately 4,100 rated financial institutions issuers; |

» | | Approximately 18,000 rated public finance issuers (including sovereign,sub-sovereign and supranational issuers); |

» | | Approximately 11,000 rated structured finance transactions; and |

» | | Approximately 1,000 rated infrastructure and project finance issuers. |

Additionally, MISalso earns revenue from certainnon-ratings-related operations, which primarily consist of financial instruments pricing services in the Asia-Pacific region, as well as revenue from ICRAnon-ratingESG research, data and assessments and revenue from ICRA's non-ratings operations. The revenue from these operations is included in the MIS Other LOB and is not material to the results of the MIS segment.

The MA segment develops

Moody's Analytics Overview

Moody's Analytics (MA) is a

wide range of productsglobal provider of: i) data and

services that support financial analysis and risk management activities of institutional participants in global financial markets. Within its Research, Data and Analytics business, MA distributesinformation; ii) research and

data developed by MISinsights; and iii) decision solutions, which help companies make better and faster decisions. MA leverages its industry expertise across multiple risks such as

partcredit, market, financial crime, supply chain, catastrophe and climate to deliver integrated risk assessment solutions that enable business leaders to identify, measure and manage the implications of

its ratings process, includingin-depth research on major debt issuers, industry studies, commentary on topical credit related events. The RD&A LOB also provides economicinterrelated risks and opportunities. MA’s proprietary data, research and

credit data and analyticalanalytics combined with cloud-based software tools

suchdeliver solutions to meet customer needs as

quantitative credit risk scores as well as business intelligence and company information products. Within its Enterprise Risk Solutions business, MA provides software solutions as well as related risk management services. Within its Professional Services business it provides offshore research and analytical services along with financial training and certification programs. MA customers represent more than 10,500 institutions worldwide operatingthey arise. MA’s subscription businesses provide a significant base of recurring revenue to mitigate cyclical changes in

over 155 countries. During 2017 Moody’s research website was accessed by over 252,000 individuals including 36,000 customer users.PROSPECTS FOR GROWTH

Over recent decades, global fixed-income markets have grown significantly bothdebt issuance volumes that may result in terms of the amount and types of securities or other obligations outstanding. Beginningvolatility inmid-2007, there was a severe market disruption and associated financial crisis both in the devel-

MIS’s revenues. | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Curated Data Combined with Analytics are the Foundation of MA's Integrated Risk Assessment Strategy |

| | | | | | | | | | | | | | | |

| | MOODY’S 2017 10-K | | | 11Domain Expertise | | | | | |

| | | | | | | | | |

| | | | | | | | | | | | | | | |

| Curated Data | | | | | Best in Class Analytics |

| | | |

| Proprietary data assets allow companies to inform and perform many critical business activities with trust and confidence | | | | | | | | | | | | | MA's approach to deepening available data sets and ability to combine with research, analytic tools and software is driving a more integrated understanding of risks and opportunities |

| | | | | | | |

| | | | | |

| | | | | |

| | | | | | | | | | | |

| Transparency | ç | | | | | | | è | Benchmarks | |

| Efficiency | Better Decisions | Analytics | |

| Convenience | | | | | | | Insights | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| MA Customers by the Numbers |

| | | | | | | | | |

| 14,900 + | | | | | | | |

| Total MA customers | | | | |

| | | | | | | | | |

| | 1,800+ | | | 2,300+ | | | 3,600+ | |

| Asset Managers | | Commercial Banks | | Corporations | |

| | | | | | | | | |

| | 200+ | | | 900+ | | | 5,300+ | |

| Securities Dealers and Investment Banks | | Insurance Companies | | Government & Other Entities | |

| | | | | | | | | |

| | 800+ | | | 165 | | | 29,000+ | |

| Real Estate Entities | | Countries where MA customers operate | | Customer users accessed the Moody's research website in 2021 | |

| | | | | | | | | |

| | 244,000+ | | | | | | | |

| Individuals accessed the Moody's research website | | | | | | | |

oped

Sustainability

Moody’s manages its business with the goal of delivering value to all of its stakeholders, including its customers, employees, business partners, local communities and emerging markets resultingstockholders. As part of this effort, Moody’s advances sustainability by considering environmental, social, and governance (“ESG”) factors throughout its operations and products and services. The Company uses its expertise and assets to make a positive difference through technology tools, research and analytical services that help other organizations and the investor community better understand the links between sustainability considerations and the global markets. Moody’s efforts to promote sustainability-related thought leadership, assessments and data to market participants include adhering to the policies of recognized sustainability organizations that develop standards or frameworks and/or evaluate and assess performance, including: the Global Reporting Initiative; Sustainability Accounting Standards Board; and the World Economic Forum’s Stakeholder Capitalism metrics. Moody's also issues an annual report on Stakeholder Sustainability and on how the Company has implemented the Task Force on Climate-related Financial Disclosures (“TCFD”) recommendations. Moody’s sustainability-related achievements in 2021 included the following:

–Established three goals to increase representation of women and employees of racial and ethnic underrepresented groups; published our EEO-1 data;

–Accelerated our net-zero commitment to 2040, a decade earlier than the Paris Agreement goal;

–Received an ‘A’ score from CDP on climate action for the second consecutive year; and

–Became a founding member of the Net Zero Financial Services Provider Alliance, part of the Glasgow Financial Alliance for Net Zero (GFANZ) and joined the Taskforce on Nature-related Financial Disclosures (TNFD).

The Board oversees sustainability matters, with assistance from the Audit, Governance & Nominating and Compensation & Human Resources Committees, as part of its oversight of management and the Company’s overall strategy. The Board also oversees Moody’s policies for assessing and managing our exposure to risk, including climate-related risks such as business continuity disruption or reputational and credibility concerns stemming from incorporation of climate-related risks into the credit methodologies and credit ratings of MIS.

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Pillars of Moody's Sustainability Strategy |

| | | | | | | |

| | | | |

| Better Business | | Better Lives | | Better solutions |

| For Moody's operations and value chain | | For Moody's people and communities | | For market transformation |

| Strive to embed responsible, sustainable decision-making in everything Moody's does. | | Aim to create a forward-thinking, inclusive culture across Moody's people and communities. | | Build/develop products to help our customers identify risks and opportunities and provide meaningful performance measurements and insights |

HUMAN CAPITAL

Moody’s purpose is to bring clarity, knowledge and fairness to an interconnected world. The Company’s success in achieving its purpose is only possible through the collective contributions of its global employee population whose members possess the unique combination of skills, professional experience and diversity of backgrounds needed to advance the Company’s business and contribute to the communities in which it operates. Moody’s believes that it is essential to: i) create a workplace where its employees feel valued and inspired; ii) provide an environment that fosters a culture of independence, inclusion and intellectual leadership; and iii) support peer collaboration and professional growth.

As a global integrated risk assessment firm, attracting, supporting and retaining skilled talent is essential to the Company’s success. Moody’s addresses these goals by:

–championing diversity, equity and inclusion among employees;

–seeking to provide market-competitive compensation and benefits and rewarding employees for their contributions to the Company’s strategic and operational goals;

–offering wellness programs;

–supporting employee learning, development and skills enhancement; and

–advancing employee engagement.

Diversity, Equity and Inclusion

Moody's believes it is imperative to be visible champions of diversity, equity and inclusion because differing thoughts and perspectives help to enrich the Company’s offerings to its many stakeholders and improve performance. The key objectives for which the Company focuses with respect to these items include:

–incorporating diversity, equity and inclusion into Moody’s business strategy;

–establishing leadership accountability with respect to diversity, including through executive compensation programs;

–working to increase diverse representation (e.g., women and ethnic groups);

–continuing to advance women and ethnically diverse employees in leadership roles;

–enhancing employee training in diversity, equity and inclusion matters;

–promoting equal employment opportunities in all aspects of employment;

–designing the Company’s compensation practices to provide equal pay for equal work; and

–incorporating market standards, role, experience and performance into compensation decisions.

The executive leadership team’s focus on these items is vital to attract, support and retain its skilled talent.

Moody’s has numerous diversity programs and eight active business resource groups (“BRGs”) including:

–EnAble BRG: advocates for an inclusive, accessible and stigma-free workplace in which employees with disabilities are valued for their talents and have the opportunity to advance and thrive professionally

–Generational BRG: seeks to leverage the insights and experiences of our multi-generational workforce in order to cultivate an inclusive work environment that fosters greater connectedness, supports the development of all generational groups and delivers business value to the firm

–Inclusion BRG: supports all areas of diversity and inclusion combining Moody's BRG chapters. Inclusion creates opportunities for all employees regardless of office size to engage with a BRG

–Minds BRG: seeks to foster a culture at Moody’s where all employees are empowered to discuss and manage their mental health

–Multicultural BRG: seeks to leverage diverse talent by promoting recruitment, professional development and networking opportunities for all ethnically diverse employees at Moody's

–Pride BRG: advocates for a work environment that respects, welcomes and supports lesbian, gay, bisexual and transgender professionals, enabling them to perform to their fullest potential and contribute to the greater goals of the Company

–Veterans BRG: recognizes and supports veterans, active-duty military personnel and military families both at Moody's and in our communities

–Women's BRG: seeks to enhance the recruitment, retention, and professional development of female professionals by implementing programs that foster greater interaction among peers as well as the broader community, while acting as a collective voice for raising women's issues to senior management and enhancing the employment brand

The BRGs represent 44 chapters and more than 6,600 memberships globally as of December 31, 2021. An employee can hold membership in multiple BRGs in a single region.

The Company’s diversity programs include its TIDE program (Talent Aspirations & Alignment, Insights, Development & Career Planning and Exposure & Expansion), which is a high potential employee diversity initiative aimed at elevating women and ethnically diverse employees into leadership positions.

The Company provides and periodically updates information on its BRGs and other diversity, inclusion and equity programs in its various sustainability and stakeholder reports and on its Diversity & Inclusion microsite. See moodys.com/sustainability and moodys.com/diversity for these items. The content of those websites is not incorporated by reference herein.

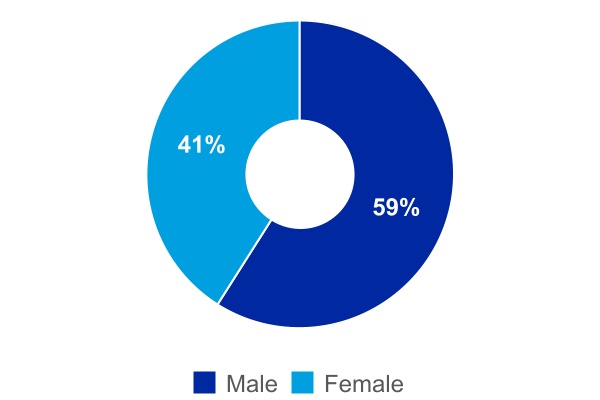

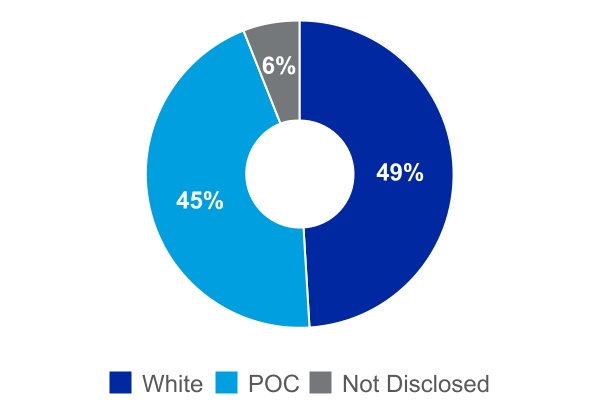

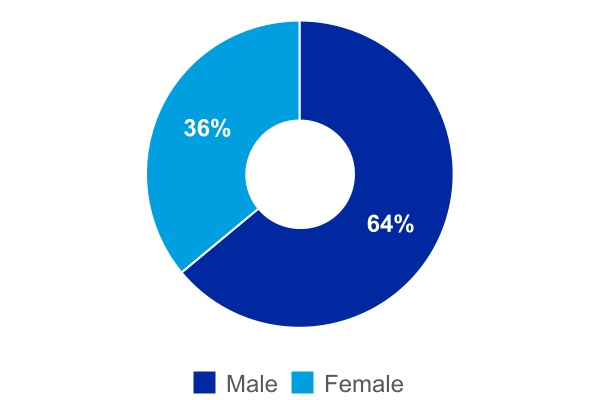

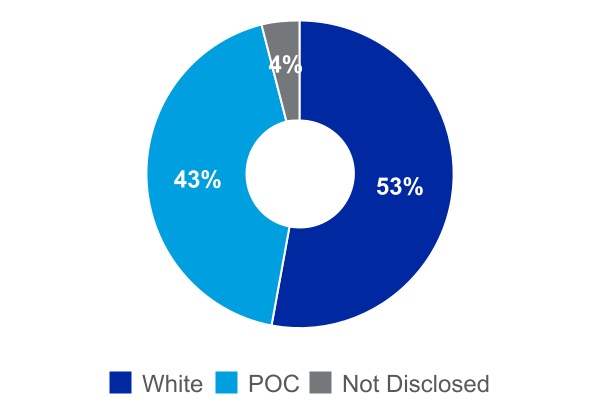

The charts below present additional information regarding the diversity of the Company's workforce as of December 31, 2021. The percentage for people of color ("POC") includes those who identified as Asian, Hispanic, Black, American Indian/Alaskan Native, Hawaiian/Other Pacific Island or two or more races. Officers and Managers are calculated using the job categories: executives, senior managers, mid-level managers, and first-level managers. The following data is based on Company records and may involve estimates or assumptions.

| | | | | | | | | | | | | | |

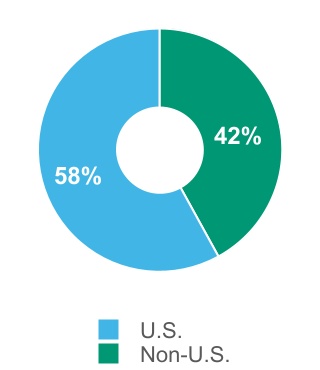

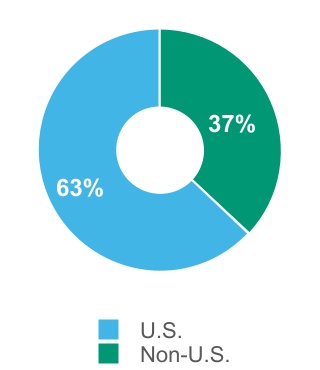

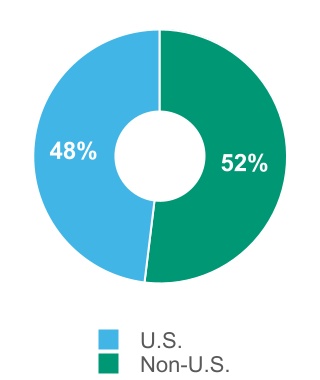

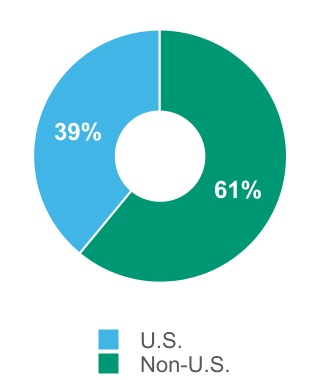

| Total Workforce: Gender | | U.S. Workforce: Ethnicity |

| | | | | | | | | | | | | | |

Total Officers and Managers: Gender (1) | | U.S. Officers and Managers: Ethnicity |

(1) Total officers and managers by gender represents approximately 90% of employees (excludes certain non-wholly-owned subsidiaries and newly acquired companies for which this data was not available)

Compensation

Moody’s compensation programs are designed to foster and maintain a strong, capable, experienced and motivated global declineworkforce. An important element of the Company’s compensation philosophy is aligning compensation to local market standards so that Moody's can attract and retain the highly-skilled talent needed to thrive. The Company’s compensation packages include market-competitive salaries, annual bonuses and equity grants for certain employees.

Benefits and Wellness Programs

With respect to benefits, the Company views investments in debt issuance activitybenefits as an investment in its people. Moody’s is committed to providing competitive benefits programs designed to care for some significant asset classesall employees and weak economictheir families. The Company’s comprehensive programs offer resources for physical and mental health that promote preventive care, awareness and support a healthy lifestyle. The Company also promotes financial wellness and provides for flexible work arrangements, which support the Company’s efforts to create a work atmosphere in which people feel valued and inspired to give their best. Beyond delivering health, welfare, retirement benefits, and paid vacation and sick days, Moody’s extends other benefits to support its employees and their families. To provide competitive benefits, the Company periodically adjusts the nature and extent of benefits, such as parental leave, workplace flexibility and educational support.

Employee Population

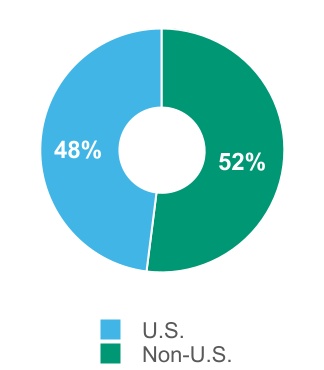

As of December 31, 2021 and 2020, the number of Moody’s employees was as follows:

| | | | | | | | | | | | | | | | | | | | | | | | | |

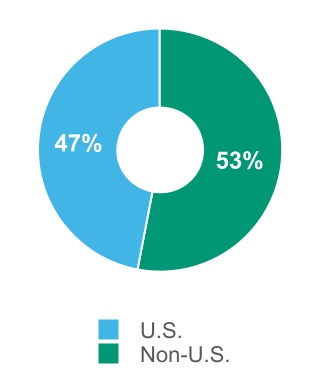

| | | December 31, | | | | Change |

| Global Headcount | | 2021 | | 2020 | | | | % |

| | | | | | | | | |

| MIS | | | | | | | | |

| U.S. | | 1,459 | | | 1,518 | | | | | (4) | % |

| Non-U.S. | | 3,836 | | | 3,533 | | | | | 9 | % |

| Total | | 5,295 | | | 5,051 | | | | | 5 | % |

| | | | | | | | | |

| MA | | | | | | | | |

| U.S. | | 2,647 | | | 2,012 | | | | | 32 | % |

| Non-U.S. | | 3,882 | | | 2,996 | | | | | 30 | % |

| Total | | 6,529 | | | 5,008 | | | | | 30 | % |

| | | | | | | | | |

| MSS |

| U.S. | | 728 | | | 704 | | | | | 3 | % |

| Non-U.S. | | 908 | | | 724 | | | | | 25 | % |

| Total | | 1,636 | | | 1,428 | | | | | 15 | % |

| | | | | | | | | |

| Total MCO | | | | | | | | |

| U.S. | | 4,834 | | | 4,234 | | | | | 14 | % |

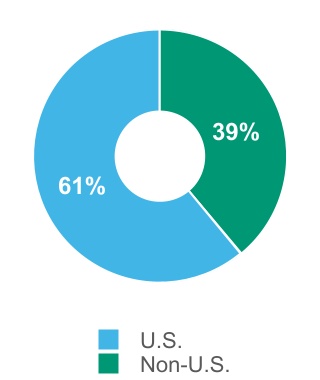

| Non-U.S. | | 8,626 | | | 7,253 | | | | | 19 | % |

| Total | | 13,460 | | | 11,487 | | | | | 17 | % |

The MIS employee population primarily consists of credit analysts, data and operations analysts, credit strategy and methodology professionals, software engineers, sales and sales operations, and international strategy teams.

MA’s employee population primarily consists of software engineers, data and operation analysts, advisory and implementation teams and economists, as well as sales and sales support professionals.

The MSS employee population primarily consists of information technology professionals and other professional support staff such as finance, human resources and legal that support both MIS and MA.

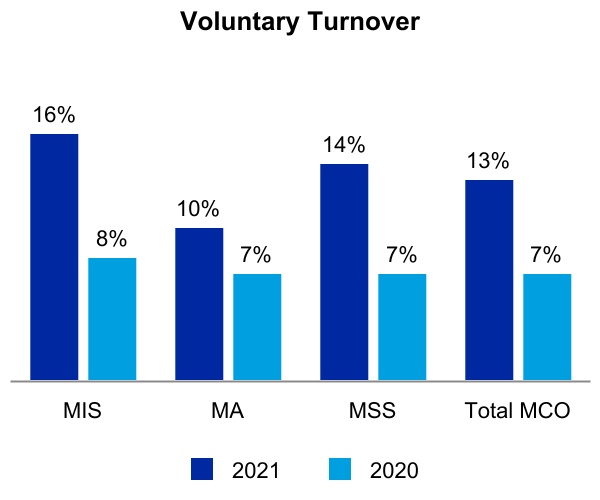

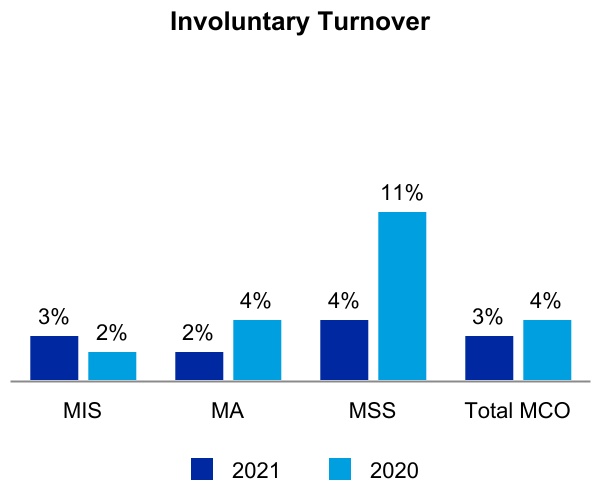

Management monitors employee turnover rates as presented in the chart below:

The increase in the Company's voluntary turnover rates in 2021 compared to 2020 are likely due to the effects of COVID-19 on the labor market. Additionally, MSS involuntary turnover figures in 2020 in the chart above includes employees who separated pursuant to a third-party outsourcing arrangement relating to certain back-office functions. A majority of these employees were hired by the third-party outsourcing provider.

Employee Engagement, Learning and Development

As a result of the COVID-19 pandemic, the Company enhanced its digital communications with its employees beginning in 2020. These enhanced communications have allowed senior management to continue to interact with employees regarding evolving priorities and its focus on the health, safety and well-being of Moody’s employees during this challenging time.

Learning & Development is one element of Moody’s talent management framework, which includes talent acquisition, performance in advanced economies. Since this financial crisis, many marketsmanagement, total rewards, succession planning and economies have recoveredleadership development. Each of these areas supports the Company’s business strategy and Moody’s culture as a diverse, equitable and inclusive place to work. Moody's views learning and education as an investment in its people that aligns their professional goals and interests with the success of the Company, and helps to retain talent over the longer-term. A number of training programs are available, including leadership development, professional skills development, technical skills, as well as compliance training.

CLIMATE CHANGE

Climate change is a defining issue of our time, and while Moody’s operations have a limited direct environmental impact and we are not considered a major emitter of greenhouse gas (GHG) emissions, we do nonetheless have an important role to play in demonstrating proactive corporate responsibility, setting industry standards and demonstrating best practices when it comes to climate change mitigation. As such, the Company is taking steps to advance climate action by publishing its TCFD report on an annual basis, issuing its decarbonization plan with science-based targets and a comprehensive roadmap and accelerating its commitment to achieve net-zero emissions across its operations and value chain by 2040.

Moody’s Decarbonization Plan outlines tangible strategies for realizing its climate ambitions, including the procurement of 100% of renewable electricity in the Company’s office spaces and optimizing efficiencies in its operations through a “Workplace of the Future” program. The Decarbonization Plan was subject to a vote at Moody’s 2021 Annual Meeting of Stockholders with 93% of votes in favor of the proposal, which underscored that climate considerations and action are now an integral part of the Company’s business strategy, governance, and corporate performance. The costs associated with the implementation of the Decarbonization Plan are not expected to be material.

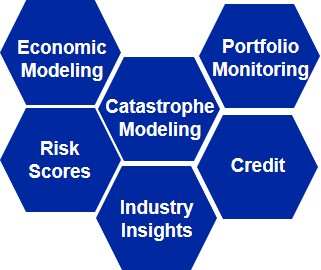

Furthermore, Moody’s has invested in acquisitions that expand its climate capabilities further, including RMS, Four Twenty Seven and Vigeo Eiris. To integrate these capabilities into our existing offerings, Moody’s is enhancing its technology infrastructure to provide our analysts and researchers with streamlined access to consistent and high-quality ESG and climate insights. These enhancements will allow Moody’s to seamlessly integrate climate considerations into our products and solutions for the benefit of our customers and the capital markets at large.

MOODY’S STRATEGY

Moody’s corporate mission is to provide trusted insights and standards that help decision-makers act with confidence. Moody’s will continue to invest with intent to defend and enhance its core businesses and expand into strategic adjacencies and new geographies.

| | | | | | | | | | | | | | | | | | | | |

| Vision | To promote progress through better decisions |

| | | | | | |

| Objective | Deliver global integrated risk assessment platform and solutions |

| | | | | | |

| Growth Strategy | Invest with intent to grow and scale |

| | | | | |

| | | |

Invest with intent to grow and strengthen our core business with a foundation of credibility, transparency, technology, data and analytics | | Invest in integrated solutions to allow customers to manage multiple risks, bringing the best of Moody's capabilities | | Invest to successfully scale in priority growth markets with highly differentiated products and services |

| | | | | |

| Investment in high growth markets |

| | | | | | |

| Execution Priorities | How we will get it done |

| | | | | |

| | | | |

Sharpen focus on

customers | | Develop our people and culture | | Collaborate, modernize and innovate |

| | | | | | |

Moody’s invests in initiatives to implement the Company’s strategy, including internally led organic development and targeted acquisitions. Illustrative examples include:

| | | | | | | | | | | | | | |

| | | | |

| Enhancements to ratings quality and product extensions | Investments that extend ownership and participation in joint ventures and strategic alliances | Expansion in emerging markets | New products, services, content and technology capabilities to meet customer demands | Selective bolt-on acquisitions that accelerate the ability to scale and grow Moody’s businesses |

During 2021, Moody’s continued to invest in and acquire complementary businesses as further described below:

| | | | | | | | | | | | | | |

| Date | Business | Company | Stake | Strategic Commentary |

| | | | |

| November 2021 | KYC | PassFort | 100% | A U.K. SaaS-based workflow platform for identity verification, customer onboarding, and risk analysis. The integration of PassFort’s platform into Moody’s suite of KYC and compliance offerings will create a more holistic workflow solution, allowing customers to incorporate Moody’s data, including credit, cyber, ESG, and climate analytics, directly into their proprietary processes.

|

| | | | |

| November 2021 | KYC | Bogard AB | 100% | A provider of data and information on politically exposed persons (PEPs) in the Nordic region. The acquisition advances Moody’s ability to help customers perform KYC screening and research to address financial crime.

|

| | | | |

| October 2021 | Cyber | BitSight | Minority | A provider of cybersecurity ratings, analytics, and performance management tools. In 2021, BitSight acquired VisibleRisk, a cyber risk ratings joint venture created by Moody’s and Team8, a global venture group. The investment enhances BitSight’s offerings and capabilities, to create a comprehensive, integrated, industry-leading cybersecurity risk platform. Moody’s will leverage BitSight’s extensive cyber risk data and research across its growing suite of integrated risk assessment product offerings.

|

| | | | |

| September 2021 | Insurance | Risk Management Solutions (RMS) | 100% | A global provider of climate and natural disaster risk modeling and analytics. The acquisition expands Moody’s insurance data and analytics business and accelerates the development of the Company’s global integrated risk capabilities to address the next generation of risk assessment.

|

| | | | |

| September 2021 | Commercial Real Estate | RealXData | 100% | A provider of CRE lease-level portfolio management with benchmarking and rent forecasting capabilities. The acquisition advances Moody's ability to help customers manage their real estate portfolio, analyze performance, and define a strategy in one platform.

|

| | | | |

| March 2021 | KYC | Cortera | 100% | A provider of North American credit data and workflow solutions. The acquisition enhances Moody’s integrated risk assessment capabilities and significantly extends its coverage in the small and medium enterprise segment. Cortera augments Moody’s extensive Orbis database of private company information and enhances its know-your-customer, commercial lending, and supply chain solutions.

|

PROSPECTS FOR GROWTH

Moody’s believes

that the overall long-term outlook remains favorable for continued growth of the global fixed-income market and related financial information market, which includes information such as credit opinions, research, data, analytics, risk management tools and related services.

Moody’s growth is influenced by a number of trends that impact financial information markets including:

» | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | |

Health of the world’s major economies; |

»economies | | Debt capital markets activity; |

»activity | | Disintermediation of credit markets; |

»markets | | Fiscal and monetary policy of governments;governments | | Expansion of market for integrated data and |

» analytics solutions | | Business investment spending, including mergers and acquisitions.acquisitions |

In an environment of increasing financial complexity and heightened attention to credit analysis and risk management, Moody’s is well positioned to benefit from continued growth in global fixed-income market activity and

a more widespread use of credit ratings, research and related analytical products. Moody’s expects that these developments will support continued long-term demand for high quality, independent credit opinions, research, data, analytics, risk management tools and related services.

Strong secular trends should continue to provide long-term growth opportunities. For MIS, key growth drivers include debt market issuance driven by global GDP growth, continued disintermediation of fixed-income markets in both developed and emerging economies driving issuance and demand for new ratings products and services. Growth in MA is likely to be driven by deeper and broader penetration of its customer base as regulatory compliance and other analytical requirements drive demand for MA’s products and expertise. Moreover, pricing opportunities aligned with customer value creation and advances in information technology present growth opportunities for Moody’s.

Moody’s operations are subject to various risks, as more fully described in Part I, Item 1A “Risk Factors,” inherent in conducting business on a global basis. Such risks include currency fluctuations and possible nationalization, expropriation, exchange and price controls, changes in the availability of data from public sector sources, limits on providing information across borders and other restrictive governmental actions.