UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 20172019

Oror

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE

ACT OF 1934

For the transition period from to

Commission File Number: 000-02040

CARBON NATURAL GAS COMPANYENERGY CORPORATION

(Exact Name of Registrant as Specified in Its Charter)

| State of incorporation:Delaware | I.R.S. Employer Identification No.26-0818050 | |

| 1700 Broadway, Suite 1170, Denver, Colorado | 80290 | |

| (Address of Principal Executive Offices) | (Zip Code) |

Registrant’s telephone number, including area code:(720) 407-7030

Securities registered pursuant to Section 12(b) of the Act:None

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||

| None |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, Par Value $0.01 Per Share

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | Smaller reporting company | ☒ | |

| Emerging growth company | ☐ | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the registrant’s voting and non-voting common stock held by non-affiliates of the registrant asof June 30, 2017,28, 2019, the last business day of the registrant’s most recently completed second fiscal quarter, was $10.0approximately $19.2 million (based on the closing price of such common stock of $10.50$8.00 as reported on otcmarkets.com on such date).

As ofMarch 23, 2018, there were 7,533,411 issued and outstanding16, 2020, the registrant had 7,816,420 shares of the Company’s common stock $0.01 par value.outstanding.

Documents incorporated by reference: None

Certain information required by Part III of Form 10-K is incorporated by reference to the Registrant’s definitive information statement for the 2020 Annual Meeting of Stockholders, which will be filed within 120 days of December 31, 2019.

CARBON NATURAL GAS COMPANYENERGY CORPORATION

TABLE OF CONTENTS

i

Forward-Looking Statements

The information in this Annual Report on Form 10-K includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “1933 Act”“Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “1934 Act”“Exchange Act”). Forward-looking statements are statements other than statements of historical or present facts, that address activities, events, outcomes, and other matters that Carbonthe Company (as defined herein) plans, expects, intends, assumes, believes, budgets, predicts, forecasts, projects, estimates, or anticipates (and other similar expressions) will, should, or may occur in the future. Generally, the words “expects,” “anticipates,” “targets,” “goals,” “projects,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “may,” “will,” “could,” “should,” “future,” “potential,” “continue,” variations of such words, and similar expressions identify forward-looking statements. These forward-looking statements are based on our current expectations and assumptions about future events and are based on currently available information as to the outcome and timing of future events.

These forward-looking statements appear in a number ofseveral places in this Annual Report on Form 10-K and include statements with respect to, among other things:

| ● | estimates of our oil, natural gas liquids, and natural gas reserves; |

| ● | estimates of our future oil, natural gas liquids, and natural gas production, including estimates of any increases or decreases in our production; |

| ● | our future financial condition and results of operations; |

| ● | our future revenues, cash flows, and expenses; |

| ● | our access to capital and our anticipated liquidity; |

| ● | our future business strategy and other plans and objectives for future operations and acquisitions; |

| ● | our outlook on oil, natural gas liquids, and natural gas prices; |

| ● | the amount, nature, and timing of future capital expenditures, including future development costs; |

| ● | our ability to access the capital markets to fund capital and other expenditures; |

| ● | our assessment of our counterparty risk and the ability of our counterparties to perform their future obligations; and |

| ● | the impact of federal, state and local political, regulatory, and environmental developments in the United |

We believe the expectations and forecasts reflected in our forward-looking statements are reasonable, but we can give no assurance that they will prove to be correct. We caution you that these forward-looking statements can be affected by inaccurate assumptions and are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which are beyond our control, incident to the exploration for and development, production, and sale of oil, natural gas and natural gas.gas liquids. SeePart I, Item 1 —-“Business—CompetitionBusiness-Competition” and —“- “Business—RegulationBusiness-Regulation,” as well asPart I, Item 1A—1A -" “Risk Factors,” andPart II, Item 7—7 -" “Management'sManagement’s Discussion and Analysis of Financial Condition and Results of Operations-Liquidity and Capital Resources” for a description of various, but by no means all, factors that could materially affect our ability to achieve the anticipated results described in the forward-looking statements.

We caution you not to place undue reliance on these forward-looking statements, which speak only as of the date of this report, and we undertake no obligation to update this information to reflect events or circumstances after the filing of this report with the Securities and Exchange Commission (“SEC”), except as required by law. All forward-looking statements, expressed or implied, included in this Annual Report on Form 10-K and attributable to us are expressly qualified in their entirety by this cautionary statement. This cautionary statement should also be considered in connection with any subsequent written or oral forward-looking statements that we may make or persons acting on our behalf may issue.

ii

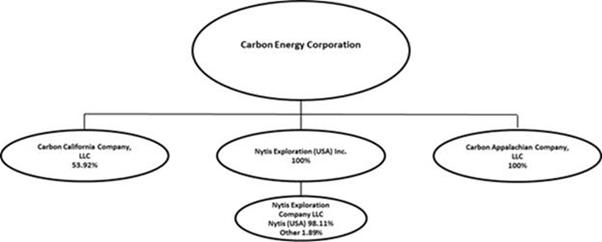

Throughout this Annual Report on Form 10-K, we use the terms “Carbon,” “Company,” “we,” “our,” and “us” to refer to Carbon Natural Gas CompanyEnergy Corporation and our wholly-owned and majority-owned subsidiaries. Additionally, we refer to Carbon Appalachian Company, LLC as “Carbon Appalachia” and Carbon California Company, LLC as “Carbon California,” and we refer to Carbon Appalachia and Carbon California, togetherwith our proportionate share of 53.92%, as our “equity investees.“majority-owned subsidiary.” We refer to Carbon Appalachian Company, LLC as “Carbon Appalachia”. In the following discussion, we make statements that may be deemed “forward-looking” statements within the meaning of Section 27A of the Securities Act, of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”).Act. See “Forward-Looking Statements,” above, for more details. We also use a number of terms used in the oil and gas industry. See “Glossary of Oil and Gas Terms” for the definition of certain terms.

Item 1. Business.Items 1 and 2. Business and Properties

GeneralOverview

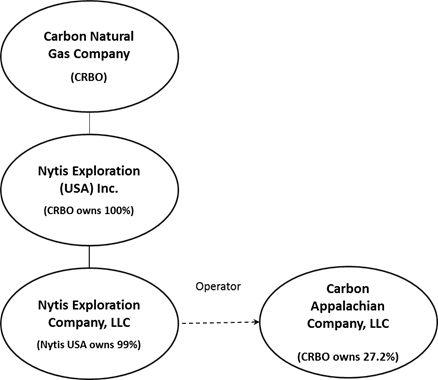

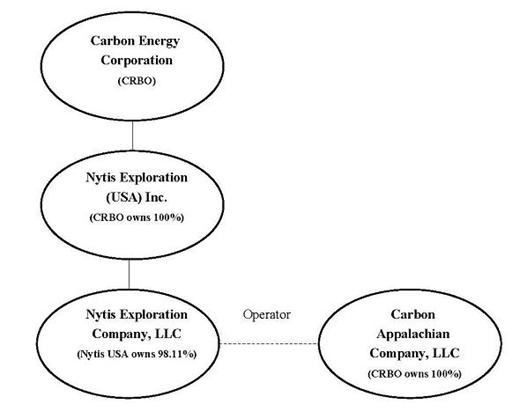

Carbon Natural Gas Company,Energy Corporation, a Delaware corporation formed in 2007, is an independent oil and natural gas company engaged in the acquisition, exploration, development and production of oil, natural gas and natural gas liquids (“NGLs”) properties located in the United States. We currently develop and operate oil and gas properties in the Appalachian Basin in Kentucky, Ohio, Tennessee, Virginia and West Virginia, andin the Illinois Basin in Illinois and Indiana, and in the Ventura Basin in California through our wholly-owned and majority-owned subsidiaries. We own 100% of the outstanding sharesinterests of Carbon Appalachia, and Nytis Exploration (USA) Inc., a Delaware corporation (“Nytis USA”USA”), which in turn owns 98.1%98.11% of Nytis Exploration Company LLC, a Delaware limited liability company (“Nytis LLC”LLC”). Nytis LLC holds interests in our operating subsidiaries, which include 46 consolidated partnerships and 18 non-consolidated partnerships.

subsidiaries. We also develop and operate oil and gas properties in the Appalachian Basin in Kentucky, Tennessee, Virginia and West Virginia and the Ventura Basin in California through our investments in Carbon Appalachia andown 53.92% of Carbon California respectively.which we consolidate for financial reporting purposes as a majority-owned subsidiary. We focus on conventional and unconventional reservoirs, including shale, tight sands and coalbed methane.

As of December 31, 2017, we held a 17.81% and 27.24% proportionate share of the profits interests of Carbon California and Carbon Appalachia, respectively. This proportionate share amount reflects our aggregated sharing percentage based on all classes of ownership interests held in each equity investee. These proportionate share amounts assume each equity investee is operating as a going concern, and no adjustments have been made that could be required based on priority of units and hurdle rates upon liquidation or distributions.

As of December 31, 2017,2019, directly and through our 53.92% proportionate share in our equity investees,of Carbon California, we own working interests in approximately 7,7007,200 gross wells (6,600 net) and, royalty interests in approximately 6001,100 wells and have leasehold positions in approximately 995,700314,000 net developed acres and approximately 590,6001,257,000 net undeveloped acres.

The chart belowfollowing table shows a summary of reserve and production data as of and for the year ended December 31, 2017 for us and our 17.81% and 27.24% proportionate share in Carbon California and Carbon Appalachia, respectively:2019:

| Estimated Total Proved Reserves | Average Net Daily | Average | ||||||||||||||||||||||

| Oil (MMBbls) | NGLs (MMBbls) | Natural Gas (Bcf) | Total (Bcfe) | Production (Mcfe/D) | Reserve Life (years) | |||||||||||||||||||

| Carbon | 0.9 | - | 78.7 | 84.2 | 14,559 | 17.6 | ||||||||||||||||||

| Carbon Appalachia | 0.1 | - | 90.8 | 91.2 | 13,196 | 20.7 | ||||||||||||||||||

| Carbon California (1) | 1.6 | 0.2 | 3.0 | 14.1 | 5,286 | 30.4 | ||||||||||||||||||

| Total | 2.6 | 0.2 | 172.5 | 189.4 | 33,041 | 21.2 | ||||||||||||||||||

| Estimated Total Proved Reserves(1) | Average Production (Mcfe/D) | Average Reserve Life (years) | ||||||||||||||||||||

| Oil (MMBbls) | NGLs (MMBbls) | Natural Gas (Bcf) | Total (Bcfe) | |||||||||||||||||||

| 17.7 | 1.3 | 450.4 | 564.9 | 68,993 | 22.8 | |||||||||||||||||

| (1) |

An illustrative organizational chart as of December 31, 2017 is below:

Recent DevelopmentsAcquisition Highlights

InvestmentsWe pursue acquisitions for investment which meet our criteria for investment returns, and which are consistent with our field development strategy. The acquisition of properties in Affiliatesour existing operating areas enable us to leverage our cost control abilities, technical expertise and existing land and infrastructure positions. Our acquisition program is focused on acquisitions of properties which have relatively low base decline, field development opportunities and undeveloped acreage.

Carbon Appalachia

Carbon Appalachia was formed in 2016 by us, entities managed by Yorktown Energy Partners XI, L.P. (“Yorktown”), a majority stockholder of ours, and entities managed by Old Ironsides Energy, LLC (“Old Ironsides”), to acquire producing assets in the Appalachian Basin in Kentucky, Tennessee, Virginia and West Virginia. Substantial operations commenced in April 2017. Prior to November 1, 2017, Yorktown held 7.95% of the voting interest and 7.87% of the profits interest in Carbon Appalachia. On November 1, 2017, Yorktown exercised a warrant, pursuant to which Yorktown obtained additional shares of common stock in us in exchange for the transfer and assignment by Yorktown of all of its rights in Carbon Appalachia. Following the exercise of this warrant by Yorktown, we ownowned 26.50% of the voting interest and 27.24% of the profits interest, and Old Ironsides holdsheld the remainder of the interests in Carbon Appalachia.

Carbon Appalachia’s board

On December 31, 2018, we acquired all of directors is composed of four members. We have the right to appoint one member to the board of directors, and Patrick R. McDonald, our Chief Executive Officer, is our designee to the board of directors. We currently serve as the managerClass A Units of Carbon Appalachia and operate its day-to-day administration, pursuantowned by Old Ironsides for a purchase price of $58.2 million, subject to the termspurchase price adjustments (“OIE Membership Acquisition”). As a result of the limited liability company agreementOIE Membership Acquisition, we now own 100% of the voting and profit interests of Carbon Appalachia, along with its direct and indirect subsidiaries. The acquisition was funded with cash, debt and the management services agreement between Carbon Appalachia and us, subjectissuance of notes to certain approval rights held byOld Ironsides. See Note 3 to the board of directors of Carbon Appalachia.consolidated financial statements.

As of December 31, 2017, Carbon Appalachia owns working interests in approximately 4,400 gross well (3,800 net) and has leasehold positions in approximately 804,400 net developed acres and approximately 360,200 net undeveloped acres.

Carbon California

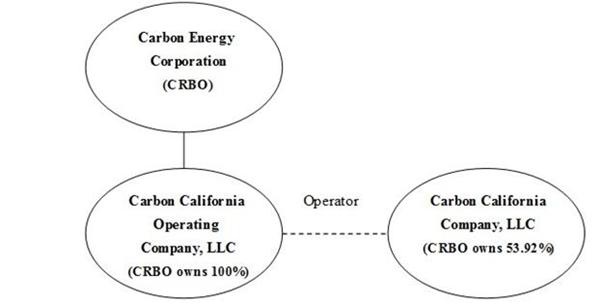

Carbon California was formed in 2016 by us, Yorktown and Prudential Capital Energy Partners, L.P. (“Prudential”), to acquire producing assets in the Ventura Basin in California. Prior to February 1, 2018, we held 17.81% of the voting and profits interests, Yorktown held 38.59% of the voting and profits interests and Prudential held 43.59% of the voting and profits interests in Carbon California. On February 1, 2018, Yorktown exercised a warrant, pursuant to which Yorktown obtained additional shares of common stock in us in exchange for the transfer and assignment by Yorktown of all of its rights in Carbon California. Following the exercise of this warrant by Yorktown, we own 56.41% of the voting and profits interests, and Prudential holds the remainder of the interests, in Carbon California.

Carbon California’s board of directors is composed of five members. We have the right to appoint one member to the board of directors, and Patrick R. McDonald, our Chief Executive Officer, is our designee. We currently serve as the manager of Carbon California and operate its day-to-day administration, pursuant to the terms of the limited liability company agreement of Carbon California and the management services agreement between Carbon California and us, subject to certain approval rights held by the board of directors of Carbon California.

Prior to February 1, 2018, we held 17.81% of the voting and profits interests, Yorktown held 38.59% of the voting and profits interests and Prudential Capital Energy Partners, L.P. held 43.59% of the voting and profits interests in Carbon California. On February 1, 2018, Yorktown exercised a warrant, pursuant to which Yorktown obtained additional shares of common stock in us in exchange for the transfer and assignment by Yorktown of all of its rights in Carbon California (the “California Warrant”). As of December 31, 2017,February 1, 2018, we consolidate Carbon California owns working interests approximately 200 gross wells (200 net) and has leasehold positions in approximately 2,300 net developed acres and approximately 8,000 net undeveloped acres.

Following the transactions described above, Yorktown currently owns 64.6% of the outstanding shares of our common stock.for financial reporting purposes.

Pending and Recent Acquisitions

We, through our equity investees, have made, or entered into definitive agreements to make, numerous acquisitions during 2017. When Carbon Appalachia andIn May 2018, but effective as of October 1, 2017, Carbon California make acquisitions, we contribute our pro rata portion ofacquired 309 operated and one non-operated oil wells covering approximately 6,800 gross acres (6,600 net), and fee interests in and to certain lands, situated in the Ventura Basin, together with associated wells, pipelines, facilities, equipment and other property rights for a purchase price to fund such acquisitions. In 2017 and 2016, we contributed an aggregate of $15.9$43.0 million to Carbon Appalachia, Carbon California and Nytis USA in connection with our and our equity investees’ acquisition activities. While Carbon Appalachia and Carbon California made other insignificant acquisitions that are not specifically listed, the acquisitions described below most meaningfully affect the financial condition of Carbon Appalachia and Carbon California, and, therefore, us. Seefrom Seneca Resources Corporation (the “—Seneca Acquisition and Divestiture Activities” for more information about our acquisitions and divestitures.

Reverse Stock Split

Our shareholders and board of directors approved a reverse stock split of our common stock, effective March 15, 2017, pursuant to which every 20 shares of issued and outstanding common stock became one share of common stock and no fractional shares were issued. All references to the number of shares of common stock and per share amounts give retroactive effect to the reverse stock split for all periods presented. In connection with the reverse stock split, the number of authorized shares of our common stock was decreased from 200,000,000 to 10,000,000.

Preferred Stock Issuance to Yorktown

In connection with the anticipated closing of the 2018 Ventura Acquisition, Yorktown expects to make a contribution to us in an amount equal to our portion of the purchase price forwith the 2018 Ventura Acquisition in exchange for preferred stock in us. The Yorktown contribution is subjectremainder funded by debt. We raised the $5.0 million through the issuance of 50,000 shares of Series B Convertible Preferred Stock, par value $0.01 per share (the “Preferred Stock”), to negotiation and preparation of definitive transaction documents pending closingYorktown.

Following the exercise of the 2018 Ventura Acquisition.California Warrant by Yorktown and the Seneca Acquisition, we own 53.92% of the voting and profits interests and Prudential Legacy Insurance Company of New Jersey and Prudential Insurance Company of America or its affiliates (“Prudential”) owns 46.08% voting and profits interest in Carbon California.

Strategy

We continuously evaluate our portfolio of oil and gas assets and make acquisitions, investments and divestitures as part of our strategic plan. In the current environment, we are actively analyzing options such as selling assets, including potentially our Appalachian business, primarily in order to reduce indebtedness and, to a lesser extent, to fund higher value acquisition or development opportunities. Any decision to divest would be made based upon several criteria, including but not limited to the value we could obtain for such assets, the outlook for commodity prices, our expected return on invested capital and the impact on our overall leverage.

Our primary business objective is to create stockholder value through consistent growth in cash flows, production and reserves through drilling ondevelopment of our existing oil and gas properties and through the acquisition of complementary properties. We focus on the development of our existing leaseholds, which consist primarily of low risk, repeatable resource plays. We invest significantly in technical staff and geological and engineering technology to enhance the value of our properties.

We intend to accomplish our objective by executing the following strategies:

| ● | Capitalize on the development of our oil and gas properties. Our |

| ● | Acquire complementary |

| ● | Reduce operating costs |

| ● | Replace reserves and production through |

Some of our estimated proved reserves and resources are classified as unconventional, including fractured shale formations, tight gas sands, and coalbed methane. Our technical team has significant experience in drilling vertical, horizontal and directional wells, as well as fracture stimulation of unconventional formations.wells. We utilize geological, drilling and completion technologies that enhance the predictability and repeatability of finding and recovering hydrocarbons in these unconventional plays.throughout our asset base.

| ● | Maintain financial flexibility.We expect to fund |

| ● | Acquire and develop reserves |

| ● | Control operating decisions and capital program. At December 31, |

| ● | Manage commodity price exposure through an active hedging program. We maintain a hedging program designed to reduce exposure to fluctuations in commodity prices. |

In addition to our hedging program, we also maintain active hedging programs at Carbon California and Carbon Appalachia.

| ● | Manage midstream assets, storage facilities and |

Operational Areas

Our oilAppalachian and gas properties and those of our equity investees are located in the Appalachia, Illinois and Ventura Basins.

Appalachian BasinBasins

As of December 31, 2017,2019, we directly own working interests in approximately 3,0006,650 gross wells (2,600(6,070 net) and royalty interests located in Illinois, Indiana, Kentucky, Ohio, Tennessee, Virginia and West Virginia, and have leasehold positions in approximately 189,000304,700 net developed acres and approximately 222,4001,249,000 net undeveloped acres. As of December 31, 2017, net production was approximately 13,100 Mcfe per day. These interests are located in the Berea Sandstone, Devonian Shale, Seelyville Coal Seam and Lower Huron Shale formations and other zones which produce oil and natural gas.

As of December 31, 2017, Carbon Appalachia owns working interests in approximately 4,400 gross wells (3,800 net) located in Kentucky, Tennessee, Virginia and West Virginia, and has leasehold positions in approximately 804,400 net developed acres and approximately 360,200 net undeveloped acres. As of December 31, 2017, net oil and natural gas sales were approximately 12,100 Mcfe per day. These interests are located in the Devonian Shale, Chattanooga Shale, Lower Huron Shale, Monteagle and Big Line formations and other zones which produce oil and natural gas.

The chart below showsfollowing table is a summary of our and our 27.24% proportionate share in Carbon Appalachia’s reserve and production data in the Appalachian Basinand Illinois Basins as of and for the year ended December 31, 2017:2019:

| Estimated Total Proved Reserves | Average Net Daily | Average | ||||||||||||||||||

| Oil (MMBbls) | Natural Gas (Bcf) | Total (Bcfe) | Production (Mcfe/D) | Reserve Life (years) | ||||||||||||||||

| Carbon | 0.9 | 78.7 | 84.2 | 14,559 | 17.6 | |||||||||||||||

| Carbon Appalachia | 0.1 | 90.8 | 91.2 | 13,196 | 20.7 | |||||||||||||||

| Total | 1.0 | 169.5 | 175.4 | 27,755 | 20.0 | |||||||||||||||

| Estimated Total Proved Reserves | Average Net Daily | Average | ||||||||||||||||

| Oil (MMBbls) | Natural Gas (Bcf) | Total (Bcfe) | Production (Mcfe/D) | Reserve Life (years) | ||||||||||||||

| 1.2 | 430.3 | 437.8 | 59,399 | 20.7 | ||||||||||||||

Ventura Basin

As of December 31, 2017,2019, Carbon California owns working interests in approximately 200550 gross wells (200(530 net) located in the Ventura Basin of California and has leasehold positions in approximately 2,3009,200 net developed acres and approximately 8,0007,900 net undeveloped acres. As of December 31, 2017, net oil and natural gas sales were approximately 7,100 Mcfe per day. These interests are located in the Miocene-Age formation and other zones which produce oil and natural gas.

The chart below showsfollowing table is a summary of our 17.81% proportionate share in Carbon California’s reserve and production data in the Ventura Basin as of and for the year ended December 31, 2017:

| Estimated Total Proved Reserves | Average Net Daily | Average | ||||||||||||||||||||||

| Oil (MMBbls) | NGLs (MMBbls) | Natural Gas (Bcf) | Total (Bcfe) | Production (Mcfe/D) | Reserve Life (years) | |||||||||||||||||||

| Carbon California (1) | 1.6 | 0.2 | 3.0 | 14.1 | 941 | 30.4 | ||||||||||||||||||

Illinois Basin

As of December 31, 2017, we directly own working interests in 58 gross (29 net) coalbed methane wells in the Illinois Basin and have a leasehold position in approximately 1,900 net developed acres and approximately 58,000 net undeveloped acres. As of December 31, 2017, net natural gas sales were approximately 500 Mcf per day. These interests are located in the Seelyville Coal Seam formation and other zones which produce oil and natural gas.2019:

The chart below shows a summary of our reserve and production data in the Illinois Basin as of and for the year ended December 31, 2017:

| Estimated Total Proved Reserves | Average Net Daily | Average | ||||||||||||||||||

| Oil (MMBbls) | Natural Gas (Bcf) | Total (Bcfe) | Production (Mcfe/D) | Reserve Life (years) | ||||||||||||||||

| Carbon | - | 0.4 | 0.4 | 465 | 3 | |||||||||||||||

| Estimated Total Proved Reserves(1) | Average Net Daily | Average | ||||||||||||||||||||

| Oil (MMBbls) | NGLs (MMBbls) | Natural Gas (Bcf) | Total (Bcfe) | Production (Mcfe/D) | Reserve Life (years) | |||||||||||||||||

| 16.5 | 1.3 | 20.1 | 127.1 | 9,594 | 35.3 | |||||||||||||||||

Acquisition and Divestiture Activities

We pursue acquisitions for investment by us or our equity investees which meet our criteria for investment returns and which are consistent with our field development strategy. The acquisition of properties in our or our equity investees’ existing operating areas enable us to leverage our cost control abilities, technical expertise and existing land and infrastructure positions. Our acquisition program is focused on acquisitions of properties which have relatively low base decline, preferable field development opportunities and undeveloped acreage. The following is a summary of our acquisitions and divestitures for 2017 and 2016. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note 4 to the consolidated financial statements for more information on our acquisitions.

Acquisitions – Appalachian Basin

Cabot Acquisition. On September 29, 2017, but effective April 1, 2017 for oil and gas properties and September 29, 2017 for the corporate entity, a wholly-owned subsidiary of Carbon Appalachia completed the acquisition of natural gas producing properties, including associated mineral interests, certain gathering system assets, associated vehicles and equipment, and all of the outstanding shares of Cranberry Pipeline, which operates certain pipeline assets, located predominantly in the state of West Virginia from Cabot Oil & Gas Corporation. The purchase price was $41.3 million, subject to normal and customary adjustments. We contributed approximately $2.9 million to Carbon Appalachia to fund this acquisition. The acquired assets consisted of the following:

Enervest Acquisition. On August 15, 2017, but effective as of May 1, 2017, a wholly-owned subsidiary of Carbon Appalachia completed the acquisition of natural gas producing properties, the associated mineral interests, gas wells and associated facilities and vehicles and equipment located predominantly in the state of West Virginia from Enervest Energy Institutional Fund XII-A, L.P., Enervest Energy Institutional Fund XII-WIB, L.P., Enervest Energy Institutional Fund XII-WIC, L.P. and Enervest Operating, L.L.C. The purchase price was $21.5 million, subject to normal and customary adjustments. We contributed approximately $3.7 million to Carbon Appalachia to fund this acquisition. The acquired assets consisted of the following:

CNX Acquisition. On April 3, 2017, but effective as of February 1, 2017 for oil and gas properties and April 3, 2017 for the corporate entity, a wholly-owned subsidiary of Carbon Appalachia completed the acquisition of all of the issued and outstanding shares of Coalfield Pipeline and all of the membership interest in Knox Energy from CNX Gas Company, LLC. Coalfield Pipeline and Knox Energy own producing assets in Tennessee. The purchase price for the acquired assets was $20.0 million. We contributed approximately $0.2 million to Carbon Appalachia to fund this acquisition. The acquired assets consisted of the following:Commodity Price Risk Management

EXCO Acquisition. In October 2016, Nytis LLC completed an acquisition consisting of producing natural gas wells and natural gas gathering facilities. The purchase price for the acquired assets was $9.0 million, subject to customary closing adjustments, plus certain assumed obligations, from Exco Production Company (WV), LLC, BG Production Company (WV), LLC and Exco Resources (PA) LLC (the “EXCO Acquisition”). We contributed approximately $9.0 million to Nytis USA for it to fund its portion of the purchase price to Nytis LLC to fund this acquisition. The acquired assets consisted of the following:

Acquisitions – Ventura Basin

2018 Ventura Acquisition. On October 20, 2017, Carbon California entered into a Purchase and Sale Agreement to acquire operated and non-operated oil and gas leases covering lands, and fee interests in and to certain lands situated in the Ventura Basin, together with associated wells, pipelines, facilities, equipment and other property rights. The purchase price is $42.0 million, subject to customary and standard purchase price adjustments. We expect to contribute approximately $5.0 million to Carbon California to fund our portion of the purchase price, which amount Yorktown will contribute to us in exchange for preferred stock in us. The remainder of the purchase price is expected to be funded with contributions from other equity members and debt. The transaction is expected to close on May 1, 2018, subject to negotiation and preparation of definitive transaction documents and other customary closing conditions.

Mirada Acquisition.On February 15, 2017, but effective as of January 1, 2017, Carbon California completed the acquisition of oil and gas leases, the associated mineral interests and gas wells and vehicles and equipment from Mirada Petroleum, Inc. The purchase price was $4.5 million. We were not required to contribute any cash to Carbon California to fund this acquisition. The acquired assets consisted of the following:

CRC Acquisition.On February 15, 2017 Carbon California also completed the acquisition of oil and gas leases, the associated mineral interests, oil and gas wells and associated facilities, a field office building, land and vehicles and equipment from California Resources Petroleum Corporation and California Resources Production Corporation. The purchase price was $34.0 million. We were not required to contribute any cash to Carbon California to fund this acquisition. The acquired assets consisted of the following:

Equity Investments in Affiliates

Carbon Appalachia

Our Carbon Appalachia Ownership Interests

We own 26.50% of the voting interest and 27.24% of the profits interest in Carbon Appalachia through our ownership of Class A Units and Class C Units in Carbon Appalachia. In addition, we own 100% of the Class B Units in Carbon Appalachia, which do not currently participate in distributions from Carbon Appalachia. Pursuant to the terms of the Amended and Restated Limited Liability Company Agreement of Carbon Appalachia, once the holders of the Class A Units have received a full return of their aggregate capital contributions plus an internal rate of return of 10%, the Class B Units begin participating in distributions from Carbon Appalachia, with 80% of distributions allocated to the holders of the Class A Units and Class C Units and 20% of the distributions allocated to the holders of Class B Units. Carbon Appalachia does not currently pay distributions to its members, including us.

Carbon Appalachia Credit Facility

In connection and concurrently with the CNX Acquisition, Carbon Appalachia Enterprises, LLC, a Delaware limited liability company and indirect subsidiary of Carbon Appalachia (“Carbon Appalachia Enterprises”), entered into a 4-year $100.0 million senior secured asset-based revolving credit facility with LegacyTexas Bank, which has been used to partially fund each of Carbon Appalachia’s acquisitions. The current borrowing base under the credit facility is $50.0 million. We are not a guarantor of this credit facility. As of December 31, 2017, there was approximately $38.0 million outstanding under the credit facility. The ability of Carbon Appalachia to make distributions to its owners, including us, is dependent upon the terms of Carbon Appalachia Enterprises’ credit facility, which currently prohibits distributions unless they are agreed to by the lender. See Note 5 to the Carbon Appalachia consolidated financial statements.

Carbon Appalachia Accounting Treatment

Based on our ownership of 26.50% of the voting interest and 27.24% of the profits interest, our ability to appoint a member to the board of directors and our role as manager of Carbon Appalachia, we account for our investment in Carbon Appalachia under the equity method of accounting as we believe we can exert significant influence on Carbon Appalachia. We use the hypothetical liquidation at book value (“HLBV”) method to determine our share of profits or losses in Carbon Appalachia and adjust the carrying value of our investment accordingly. The HLBV method is a balance-sheet approach that calculates the amount each member of an entity would receive if the entity were liquidated at book value at the end of each measurement period. The change in the allocated amount to each member during the period represents the income or loss allocated to that member. From the commencement of operations on April 3, 2017 through December 31, 2017, Carbon Appalachia generated net income, of which our share is approximately $1.1 million.

Carbon California

Our Carbon California Ownership Interests

As of December 31, 2017, we own 17.81% of the voting and profits interests in Carbon California through our ownership of Class A Units and Class B Units in Carbon California. The Class A Units and Class B Units participate pro rata in distributions from Carbon California.Carbon California does not currently pay distributions to its members, including us.

Carbon California Senior Revolving Notes and Subordinated Notes

In connection with the CRC Acquisition, Carbon California (i) entered into a Note Purchase Agreement (the “Note Purchase Agreement”) for the issuance and sale of Senior Secured Revolving Notes to Prudential Legacy Insurance Company of New Jersey and Prudential Insurance Company of America with a revolving borrowing capacity of $25.0 million (the “Senior Revolving Notes”) which mature on February 15, 2022 and (ii) entered into a Securities Purchase Agreement (the “Securities Purchase Agreement”) with Prudential for the issuance and sale of $10.0 million of Senior Subordinated Notes (the “Subordinated Notes”) due February 15, 2024. We are not a guarantor of the Senior Revolving Notes or the Subordinated Notes. The closing of the Note Purchase Agreement and the Securities Purchase Agreement on February 15, 2017, resulted in the sale and issuance by Carbon California of (i) Senior Revolving Notes in the principal amount of $10.0 million and (ii) Subordinated Notes in the original principal amount of $10.0 million. The maximum principal amount available under the Senior Revolving Notes is based upon the borrowing base attributable to Carbon California’s proved oil and gas reserves which is to be determined at least semi-annually. The current borrowing base is $15.0 million, of which $11.0 million is outstanding as of December 31, 2017. The ability of Carbon California to make distributions to its owners, including us, is dependent upon the terms of the Note Purchase Agreement and Securities Purchase Agreement, which currently prohibit distributions unless they are agreed to by Prudential Legacy Insurance Company of New Jersey and Prudential Insurance Company of America.

Borrowings under the Senior Revolving Notes and net proceeds from the Subordinated Notes issuances were used to fund the Mirada Acquisition and the CRC Acquisition. Additional borrowings from the Senior Revolving Notes may be used to fund field development projects and to fund future complementary acquisitions and for general working capital purposes of Carbon California. See Note 5 to the Carbon California financial statements.

As of December 31, 2017, Carbon California was in breach of its covenants; however, it obtained a waiver for the December 31, 2017 and March 31, 2018 covenants. It is anticipated that covenants will be met in the future. SeeLiquidity and Management’s Plans within Note 1 to the Carbon California financial statements.

Carbon California Accounting Treatment

Based on our ownership of 17.81% of the voting and profits interests as of December 31, 2017, our ability to appoint a member to the board of directors and our role of manager of Carbon California, we account for our investment in Carbon California under the equity method of accounting as we believe we can exert significant influence. We use the HLBV method to determine our share of profits or losses in Carbon California and adjust the carrying value of our investment accordingly. From February 15, 2017 (inception) through December 31, 2017, Carbon California incurred a net loss, of which our share (as a holder of Class B units for that period) is zero. Should Carbon California generate net income in future periods, we will not record income (or losses) until our share of such income exceeds the amount of our share of losses not previously reported.

Crawford County Gas Gathering Company

We have a 50% interest in Crawford County Gas Gathering Company, LLC (“CCGGC”) which owns and operates pipelines and related gathering and treatment facilities which service our natural gas production in the Illinois Basin. We account for our investment in CCGGC under the equity method of accounting, and our share of income or loss is recognized in our consolidated statement of operations. During the twelve months ended December 31, 2017 and 2016, we recorded equity method income of approximately $37,000 and equity method loss of approximately $17,000, respectively, related to this investment. In addition, during the years ended December 31, 2017 and 2016, we received cash distributions from CCGGC of approximately $68,000 and $340,000, respectively.

Risk Management

We and our equity investees hedge a portion of forecasted oil and gas production to reduce exposure to fluctuations in the prices of oil and natural gas and provide long-term cash flow predictability to pay dividends or distributions, respectively, service debt and manage our and their businesses.predictability. By removing a portion of the price volatility associated with future production, we and our equity investees expect to mitigate, but not eliminate, the potential effects of variability in cash flow from operations due to adverse fluctuations in commodity prices.

While there are many different types of derivatives available, we and our equity investeesWe generally utilize swaps and collars designed to manage price risk more effectively.

The following tables reflect our and our equity investees’ outstanding derivative hedges as of December 31, 2017:

��

Carbon Natural Gas Company

| Natural Gas Swaps | Natural Gas Collars | Oil Swaps | ||||||||||||||||||||||

| Weighted | Weighted | Weighted | ||||||||||||||||||||||

| Average | Average Price | Average | ||||||||||||||||||||||

| Year | MMBtu | Price (a) | MMBtu | Range (a) | Bbl | Price (b) | ||||||||||||||||||

| 2018 | 3,390,000 | $ | 3.01 | 90,000 | $3.00 - $3.48 | 63,000 | $ | 53.55 | ||||||||||||||||

| 2019 | 2,596,000 | $ | 2.86 | - | - | 48,000 | $ | 53.76 | ||||||||||||||||

Carbon Appalachia(1)

| Natural Gas Swaps | Natural Gas Collars | Oil Swaps | ||||||||||||||||||||||

| Weighted | Weighted | Weighted | ||||||||||||||||||||||

| Average | Average Price | Average | ||||||||||||||||||||||

| Year | MMBtu | Price (a) | MMBtu | Range (a) | Bbl | Price (b) | ||||||||||||||||||

| 2018 | 9,100,000 | $ | 2.99 | 3,630,000 | $2.96 - $3.85 | 15,000 | $ | 51.74 | ||||||||||||||||

| 2019 | 11,515,000 | $ | 2.86 | 960,000 | $2.85 - $3.19 | 12,000 | $ | 50.35 | ||||||||||||||||

| 2020 | 3,792,000 | $ | 2.83 | - | - | - | $ | - | ||||||||||||||||

Carbon California(1)

| Natural Gas Swaps | Natural Gas Collars | Oil Swaps | ||||||||||||||||||||||

| Weighted | Weighted | Weighted | ||||||||||||||||||||||

| Average | Average Price | Average | ||||||||||||||||||||||

| Year | MMBtu | Price (a) | MMBtu | Range (a) | Bbl | Price (b) | ||||||||||||||||||

| 2018 | 360,000 | $ | 3.03 | - | - | 149,247 | $ | 53.12 | ||||||||||||||||

| 2019 | - | - | 360,000 | $2.60 - $3.03 | 139,797 | $ | 51.96 | |||||||||||||||||

| 2020 | - | - | - | - | 73,147 | $ | 50.12 | |||||||||||||||||

Reserves

The tables below summarize our estimated proved oil and gas reserves and the estimated proved oil and gas reserves of our equity investees as of December 31, 2017. Our estimated proved reserves increased in 2017 primarily due to revisions of previous estimates.risk.

Carbon Natural Gas CompanyReserves

The following table summarizes our estimated quantities of proved reserves as of December 31, 20172019 and 2016 after consolidating the 46 partnerships in which we have a controlling interest through our subsidiaries.2018, inclusive of all non-controlling interests:

Carbon Natural Gas CompanyEnergy Corporation

Estimated Consolidated Proved Reserves

Including Non-Controlling Interests of Consolidated Partnerships

| December 31, | December 31, | |||||||||||||||

| 2017 | 2016 | 2019 | 2018 | |||||||||||||

| Proved developed reserves: | ||||||||||||||||

| Natural gas (MMcf) | 81,702 | 74,265 | 444,104 | 450,424 | ||||||||||||

| Oil and liquids (MBbl) | 903 | 851 | 13,908 | 15,808 | ||||||||||||

| Total proved developed reserves (MMcfe) | 87,120 | 79,371 | 527,555 | 545,272 | ||||||||||||

| Proved undeveloped reserves: | ||||||||||||||||

| Natural gas (MMcf) | - | - | 6,261 | 4,976 | ||||||||||||

| Oil and liquids (MBbl) | 16 | 31 | 5,180 | 5,013 | ||||||||||||

| Total proved undeveloped reserves (MMcfe) | 96 | 186 | 37,338 | 35,054 | ||||||||||||

| Total proved reserves (MMcfe) | 87,216 | 79,557 | 564,893 | 580,326 | ||||||||||||

| Percent developed | 99.9 | % | 99.8 | % | 93.4 | % | 94.0 | % | ||||||||

| Average natural gas price used (per Mcf) | $ | 2.93 | $ | 2.41 | $ | 2.58 | $ | 3.24 | ||||||||

| Average oil and liquids price used (per Bbl) | $ | 48.94 | $ | 40.40 | $ | 55.69 | $ | 69.20 | ||||||||

The estimated quantities of proved developed reserves for the non-controlling interest of Carbon California as of December 31, 2019 and 2018 are approximately 58.6 Bcfe and 47.8 Bcfe, respectively, which is approximately 10.4% and 8.2%, respectively, of total consolidated proved reserves. The estimated quantities of proved undeveloped reserves for the non-controlling interest of Carbon California as of December 31, 2019 and 2018 are approximately 17.2 Bcfe and 16.2 Bcfe, respectively, which is approximately 3.1% and 2.8%, respectively, of total consolidated proved reserves.

The estimated quantities of proved developed reserves for the non-controlling interests of the consolidated partnerships (not including Carbon California) as of December 31, 20172019 and 2018 are approximately 3.03.4 Bcfe and 3.3 Bcfe, respectively, which is approximately 3%1.0% of total consolidated proved reserves. There were no proved undeveloped reserves associated with the non-controlling interests of the consolidated partnerships (not including Carbon California) as of December 31, 2019 and 2018.

The following table summarizes our estimated quantities of proved reserves, excluding the non-controlling interests, of the consolidated partnerships, as of December 31, 20172019 and 2016.2018:

Carbon Natural Gas CompanyEnergy Corporation

Estimated Consolidated Proved Reserves

Excluding Non-Controlling Interests of Consolidated Partnerships

| December 31, | ||||||||

| 2017 | 2016 | |||||||

| Proved developed reserves: | ||||||||

| Natural gas (MMcf) | 78,665 | 71,125 | ||||||

| Oil and liquids (MBbl) | 903 | 851 | ||||||

| Total proved developed reserves (MMcfe) | 84,802 | 76,231 | ||||||

| Proved undeveloped reserves: | ||||||||

| Natural gas (MMcf) | - | - | ||||||

| Oil and liquids (MBbl) | 16 | 31 | ||||||

| Total proved undeveloped reserves (MMcfe) | 94 | 186 | ||||||

| Total proved reserves (MMcfe) | 84,176 | 76,417 | ||||||

| Percent developed | 99.9 | % | 99.7 | % | ||||

| Average natural gas price used (per Mcf) | $ | 2.93 | $ | 2.41 | ||||

| Average oil and liquids price used (per Bbl) | $ | 48.94 | $ | 40.40 | ||||

| December 31, | ||||||||

| 2019 | 2018 | |||||||

| Proved developed reserves: | ||||||||

| Natural gas (MMcf) | 431,498 | 439,234 | ||||||

| Oil and liquids (MBbl) | 5,687 | 9,161 | ||||||

| Total proved developed reserves (MMcfe) | 465,618 | 494,199 | ||||||

| Proved undeveloped reserves: | ||||||||

| Natural gas (MMcf) | 3,376 | 2,684 | ||||||

| Oil and liquids (MBbl) | 2,793 | 2,703 | ||||||

| Total proved undeveloped reserves (MMcfe) | 20,133 | 18,901 | ||||||

| Total proved reserves (MMcfe) | 485,751 | 513,100 | ||||||

| Percent developed | 95.9 | % | 96.3 | % | ||||

| Average natural gas price used (per Mcf) | $ | 2.58 | $ | 3.24 | ||||

| Average oil and liquids price used (per Bbl) | $ | 55.69 | $ | 69.20 | ||||

The following table shows a summary of the changes in quantities of our estimated proved oil and gas reserves for the year ended December 31, 2017.2019:

| 2017 | ||||||||||||||||||||||||

| Oil | Natural Gas | Total | Oil & Liquids | Natural Gas | Total | |||||||||||||||||||

| MBbls | MMcf | MMcfe | MBbls | MMcf | MMcfe | |||||||||||||||||||

| Proved reserves, beginning of year | 882 | 74,265 | 79,557 | 20,821 | 455,400 | 580,326 | ||||||||||||||||||

| Revisions of previous estimates | 107 | 12,195 | 12,835 | (1,713 | ) | 69,295 | 59,019 | |||||||||||||||||

| Extensions and discoveries | 16 | 138 | 232 | 2,194 | 22,218 | 35,380 | ||||||||||||||||||

| Production | (86 | ) | (4,896 | ) | (5,414 | ) | (625 | ) | (21,436 | ) | (25,182 | ) | ||||||||||||

| Purchases of reserves in-place | - | - | - | |||||||||||||||||||||

| Demotions from proved | (1,544 | ) | (63,980 | ) | (73,247 | ) | ||||||||||||||||||

| Sales of reserves in-place | - | - | - | (45 | ) | (11,132 | ) | (11,403 | ) | |||||||||||||||

| Proved reserves, end of year | 919 | 81,702 | 87,210 | 19,088 | 450,365 | 564,893 | ||||||||||||||||||

Carbon Appalachia

The following table summarizes Carbon Appalachia’s estimated quantities of proved reserves and our 27.24% proportionate share in Carbon Appalachia’s estimated quantities of proved reserves as of December 31, 2017.

Carbon Appalachia

Estimated Proved Reserves

| December 31, 2017 | ||||||||

| Carbon Appalachia | Carbon’s Share | |||||||

| Proved developed reserves: | ||||||||

| Natural gas (MMcf) | 333,175 | 90,757 | ||||||

| Oil and liquids (MBbl) | 264 | 72 | ||||||

| Total proved developed reserves (MMcfe) | 334,759 | 91,189 | ||||||

| Proved undeveloped reserves: | ||||||||

| Natural gas (MMcf) | - | - | ||||||

| Oil and liquids (MBbl) | - | - | ||||||

| Total proved undeveloped reserves (MMcfe) | - | - | ||||||

| Total proved reserves (MMcfe) | 334,759 | 91,189 | ||||||

| Percent developed | 100 | % | 100 | % | ||||

| Average natural gas price used (per Mcf) | $ | 2.96 | $ | 2.96 | ||||

| Average oil and liquids price used (per Bbl) | $ | 48.60 | $ | 48.60 | ||||

The following table shows a summary of the changes in quantities of estimated proved oil and gas reserves for the period from April 3, 2017 (inception) through December 31, 2017.

| 2017 | ||||||||||||

| Oil | Natural Gas | Total | ||||||||||

| MBbls | MMcf | MMcfe | ||||||||||

| Proved reserves, inception | - | - | - | |||||||||

| Purchases of reserves in-place (1) | 278 | 338,479 | 340,147 | |||||||||

| Production | (14 | ) | (5,304 | ) | (5,388 | ) | ||||||

| Proved reserves, end of year | 264 | 333,175 | 334,759 | |||||||||

Carbon California

The following table summarizes Carbon California’s estimated quantities of proved reserves and our 17.81% proportionate share in Carbon California’s estimated quantities of proved reserves as of December 31, 2017.

Carbon California

Estimated Proved Reserves

| December 31, 2017 | ||||||||

| Carbon California | Carbon’s Share | |||||||

| Proved developed reserves: | ||||||||

| Natural gas (MMcf) | 12,319 | 2,194 | ||||||

| Oil and liquids (MBbl) | 6,563 | 1,169 | ||||||

| Total proved developed reserves (MMcfe) | 51,697 | 9,208 | ||||||

| Proved undeveloped reserves: | ||||||||

| Natural gas (MMcf) | 4,590 | 818 | ||||||

| Oil and liquids (MBbl) | 3,827 | 682 | ||||||

| Total proved undeveloped reserves (MMcfe) | 27,554 | 4,908 | ||||||

| Total proved reserves (MMcfe) | 79,251 | 14,117 | ||||||

| Percent developed | 65 | % | 65 | % | ||||

| Average natural gas price used (per Mcf) | $ | 3.07 | $ | 3.07 | ||||

| Average oil and liquids price used (per Bbl) | $ | 50.98 | $ | 50.98 | ||||

The following table shows a summary of the changes in quantities of estimated proved oil and gas reserves for the period of February 15, 2017 (inception) through December 31, 2017.

| 2017 | ||||||||||||||||

| Oil | Natural Gas | NGL | Total | |||||||||||||

| MBbls | MMcf | MBbls | MMcfe | |||||||||||||

| Proved reserves, inception | - | - | - | - | ||||||||||||

| Purchases of reserves in-place | 9,260 | 17,260 | 1,294 | 80,586 | ||||||||||||

| Production | (141 | ) | (351 | ) | (23 | ) | (1,335 | ) | ||||||||

| Proved reserves, end of year | 9,119 | 16,909 | 1,271 | 79,251 | ||||||||||||

Preparation of Reserves Estimates

Our estimates of proved oil, and natural gas and NGL reserves as of December 31, 20172019 and 2016 and our equity investees’ estimates of proved oil and natural gas reserves as of December 31, 20172018, were based on the average fiscal-year prices for oil, and natural gas and NGL (calculated as the unweighted arithmetic average of the first-day-of-the month price for each month within the 12-month period ended December 31, 20172019 and 2016,2018, respectively). Proved developed oil, gas and gasNGL reserves are reserves that can be expected to be recovered through existing wells with existing equipment and operating methods. Proved undeveloped oil, gas and gasNGL reserves are reserves that are expected to be recovered from new wells on undrilled acreage, or from existing wells where a relatively major expenditure is required for recompletion. Proved undeveloped reserves on undrilled acreage are limited to those locations on development spacing areas that are offsetting economic producers that are reasonably certain of economic production when drilled. Proved undeveloped reserves for other undrilled development spacing areas are claimed only where it can be demonstrated with reasonable certainty that there is continuity of economic production from the existing productive formation. Proved undeveloped reserves are included when they are scheduled to be drilled within five years.

SEC rules dictate the types of technologies that a company may use to establish reserve estimates including the extraction of non-traditional resources, such as natural gas extracted from shales as well as bitumen extracted from oil sands. See Note 1817 to the consolidated financial statements in Item 8 for additional information regarding our estimated proved reserves.

Uncertainties are inherent in estimating quantities of proved reserves, including many factors beyond our control. Reserve engineering is a subjective process of estimating subsurface accumulations of oil and natural gas that cannot be measured in an exact manner, and the accuracy of any reserve estimate is a function of the quality of available data and its interpretation. As a result, estimates by different engineers often vary, sometimes significantly. In addition, physical factors such as the results of drilling, testing, and production subsequent to the date of an estimate, as well as economic factors such as changes in product prices or development and production expenses, may require revision of such estimates. Accordingly, quantities of oil and natural gas ultimately recovered will vary from reserve estimates. See “Risk Factors,” for a description of some of the risks and uncertainties associated with our business and reserves.

Reserve estimates are based on production performance, data acquired remotely or in wells, and are guided by petrophysical, geologic, geophysical and reservoir engineering models. Estimates of our proved reserves were based on deterministic methods. In the case of mature developed reserves, reserve estimates are determined by decline curve analysis and in the case of immature developed and undeveloped reserves, by analogy, using proximate or otherwise appropriate examples in addition to volumetric analysis. The technologies and economic data used in estimating our proved reserves include empirical evidence through drilling results and well performance, well logs and test data, geologic maps and available downhole and production data. Further, the internal review process of our wells and related reserve estimates includes but is not limited to the following:

| ● | A comparison is made and documented of actual data from our accounting system to the data utilized in the reserve database. Current production, revenue and expense information obtained from our accounting records is subject to external quarterly reviews, annual audits and additional internal controls over financial reporting. This process is designed to create assurance that production, revenues and expenses are accurately reflected in the reserve database. |

| ● | A comparison is made and documented of land and lease records to ownership interest data in the reserve database. This process is designed to create assurance that the costs and revenues utilized in the reserves estimation match actual ownership interests. |

| ● | A comparison is made of property acquisitions, disposals, retirements or transfers to the property records maintained in the reserve database to verify that all are accounted for accurately. |

| ● | Natural gas pricing for the first flow day of every month is obtained from Platts Gas Daily. Oil pricing for the first flow day of every month is obtained from the U.S. Energy Information Administration. At the reporting date, 12-month average prices are determined. Regional variations in pricing and related deductions are similarly obtained and a 12-month average is calculated at year end. |

For the years ended December 31, 20172019 and 2016 for us and the year ended December 31, 2017 for our equity investees,2018, the independent engineering firm, Cawley, Gillespie & Associates, Inc. (“CGA”) reviewed with us, technical personnel field performance and future development plans. Following these reviews, we furnished our internal reserve database and supporting data to CGA in order for them to prepare their independent reserve estimates and final report. We restrict access to our database containing reserve information to select individuals from our engineering department.and corporate development departments. CGA’s independent reserve estimates and final report are for our and our equity investees’ interests in the respective oil and gas properties and represents 100% of the total proved hydrocarbon reserves owned by us and our equity investees or 96%99% of the consolidated proved hydrocarbon reserves presented in our consolidated financial statements. CGA’s report does not include the hydrocarbon reserves owned by the non-controlling interests of our consolidated partnerships. We calculated the estimated reserves of the non-controlling interests of the consolidated partnerships’ oil and gas properties by multiplying CGA’s independent reserve estimates for such properties by the respective non-controlling interests in those properties.

Our Vice PresidentDirector of Engineering, Richard Finucane,Corporate Planning and our manager of Acquisitions and Divestitures,Development, Todd Habliston, areis responsible for overseeing the preparation of the reserve estimates with consultations from our internal technical and accounting staff. Mr. FinucaneHabliston started his career with ARCO Oil and Gas in 1983, has been involved in reservoir engineering inserved as Adjunct Professor of Economics at the Appalachian Basin since 1982Colorado School of Mines, and has worked as an oil and natural gas engineer since 1978 and holds a B.S. in Civil Engineering from the University of Tennessee (highest honors) and is admitted as an expert in oil and natural gas matters in civil and regulatory proceedings in Kentucky, Virginia and West Virginia. Mr. Habliston has over 3035 years of oil and gas experience in all aspects of reservoir and has served as Adjunct Professor at the Colorado School of Mines.production engineering. Mr. Habliston earned a B.S. in Chemical and Petroleum Refining Engineering from the Colorado School of Mines and an MBA from Purdue University. He is a registered Professional Engineer and is a member of SPE, SPEE, AAPG API and IPAA.API.

Drilling Activities

Based on oilDuring 2019, we drilled two oil-related wells associated with our Carbon California assets. One well was completed in the fourth quarter of 2019 and natural gas prices during 2017, we reduced our and our equity investees’the other well was completed in the first quarter of 2020. We completed no drilling activities to manage and optimizein the utilization of our and our equity investees’ capital resources. During 2017, ourAppalachian or Illinois Basins. Our 2019 capital expenditures consisted principally of oil-related drilling, remediation, return to production and recompletion projects in California and the optimization and streamlining of our natural gas gathering and compression facilities in Appalachia to provide more efficient and lower cost operations and greater flexibility in moving our production to markets with more favorable pricing.

Carbon Natural Gas Company

The following table summarizes the number of wells drilled for the years ended December 31, 2017, 20162019, 2018 and 2015.2017. Gross wells reflect the sum of all wells in which we own an interest. Net wells reflect the sum of our working interests in gross wells.

| Year Ended December 31, | ||||||||||||||||||||||||

| 2017 | 2016 | 2015 | ||||||||||||||||||||||

| Gross | Net | Gross | Net | Gross | Net | |||||||||||||||||||

| Development wells: | ||||||||||||||||||||||||

| Productive (1) | 2 | 1.2 | - | - | - | - | ||||||||||||||||||

| Non-productive (2) | - | - | - | - | - | - | ||||||||||||||||||

| Total development wells | 2 | 1.2 | - | - | - | - | ||||||||||||||||||

| Exploratory wells: | ||||||||||||||||||||||||

| Productive (1) | - | - | - | - | - | - | ||||||||||||||||||

| Non-productive (2) | - | - | - | - | - | - | ||||||||||||||||||

| Total exploratory wells | - | - | - | - | - | - | ||||||||||||||||||

| Year Ended December 31, | ||||||||||||||||||||||||

| 2019 | 2018 | 2017 | ||||||||||||||||||||||

| Gross | Net | Gross | Net | Gross | Net | |||||||||||||||||||

| Development wells: | ||||||||||||||||||||||||

| Productive (1) | 1 | 1 | - | - | 2 | 1.2 | ||||||||||||||||||

| Non-productive (2) | - | - | - | - | - | - | ||||||||||||||||||

| Total development wells | 1 | 1 | - | - | 2 | 1.2 | ||||||||||||||||||

Exploratory wells: | ||||||||||||||||||||||||

| Productive (1) | - | - | - | - | - | - | ||||||||||||||||||

| Non-productive (2) | - | - | - | - | - | - | ||||||||||||||||||

| Total exploratory wells | - | - | - | - | - | - | ||||||||||||||||||

| (1) | A well classified as productive does not always provide economic levels of activity. |

| (2) | A non-productive well is a well found to be incapable of producing either oil or natural gas in sufficient quantities to justify completion as an oil or natural gas well; also known as a dry well (or dry hole). |

Carbon Appalachia

No wells were drilled for the year ended December 31, 2017.

Carbon California

The following table summarizes our 17.81% proportionate share in the number of wells drilled for the year ended December 31, 2017. Gross wells reflect the sum of all wells in which Carbon California owns an interest. Net wells reflect the sum of Carbon California’s working interests in gross wells.

| Year Ended December 31, | ||||||||

| 2017 | ||||||||

| Gross | Net | |||||||

| Development wells: | ||||||||

| Productive (1) | 1 | 1 | ||||||

| Non-productive (2) | - | - | ||||||

| Total development wells | 1 | 1 | ||||||

| Exploratory wells: | ||||||||

| Productive (1) | - | - | ||||||

| Non-productive (2) | - | - | ||||||

| Total exploratory wells | - | - | ||||||

Oil and Natural Gas Wells and Acreage

Productive Wells

Productive wells consist of producing wells and wells capable of production, including shut-in wells. A well bore with multiple completions is counted as only one well. The following table summarizes our and our proportionate share in our equity investees’ productive wells as of December 31, 2017.2019:

| December 31, 2017 | December 31, 2019 | |||||||||||||||

| Gross | Net | Gross | Net | |||||||||||||

| Carbon Natural Gas Company | ||||||||||||||||

| Gas | 2,555 | 2,165 | 6,696 | 5,275 | ||||||||||||

| Oil | 474 | 420 | 901 | 843 | ||||||||||||

| Total | 3,029 | 2,585 | 7,597 | 6,118 | ||||||||||||

| Carbon Appalachia | ||||||||||||||||

| Gas | 4,378 | 3,802 | ||||||||||||||

| Oil | 33 | 24 | ||||||||||||||

| Total | 4,411 | 3,826 | ||||||||||||||

| Carbon California | ||||||||||||||||

| Gas | - | - | ||||||||||||||

| Oil | 208 | 207 | ||||||||||||||

| Total | 208 | 207 | ||||||||||||||

Acreage

Carbon Natural Gas Company

The following table summarizes our gross and net developed and undeveloped acreage by state as of December 31, 2017.2019. Acreage related to royalty, overriding royalty and other similar interests is excluded from this summary, as well as acreage related to any options held by us to acquire additional leasehold interests.

| December 31, 2017 | December 31, 2019 | |||||||||||||||||||||||||||||||||||||||||||||||

| Developed Acres | Undeveloped Acres | Total Acres | Developed Acres | Undeveloped Acres(1) | Total Acres | |||||||||||||||||||||||||||||||||||||||||||

| Gross | Net | Gross | Net | Gross | Net | Gross | Net | Gross | Net | Gross | Net | |||||||||||||||||||||||||||||||||||||

| California | 11,476 | 9,148 | 8,013 | 7,896 | 19,489 | 17,044 | ||||||||||||||||||||||||||||||||||||||||||

| Indiana | - | - | 43,364 | 43,364 | 43,364 | 43,364 | - | - | 9,079 | 9,079 | 9,079 | 9,079 | ||||||||||||||||||||||||||||||||||||

| Illinois | 3,758 | 1,879 | 24,216 | 14,608 | 27,974 | 16,487 | 3,758 | 1,879 | 20,225 | 12,613 | 23,983 | 14,492 | ||||||||||||||||||||||||||||||||||||

| Kentucky | 10,778 | 9,710 | 95,159 | 69,333 | 105,937 | 79,043 | 10,540 | 10,415 | 78,172 | 76,881 | 88,712 | 87,296 | ||||||||||||||||||||||||||||||||||||

| Ohio | 338 | 338 | 6,703 | 6,703 | 7,041 | 7,041 | 3,103 | 374 | 6,703 | 7,366 | 9,806 | 7,740 | ||||||||||||||||||||||||||||||||||||

| Tennessee | 160 | 40 | 45,904 | 45,896 | 46,064 | 45,936 | 69,095 | 65,847 | 115,883 | 115,761 | 184,978 | 181,608 | ||||||||||||||||||||||||||||||||||||

| Virginia | 732 | 679 | - | - | 732 | 679 | 10,541 | 1,385 | 117,768 | 124,569 | 128,309 | 125,954 | ||||||||||||||||||||||||||||||||||||

| West Virginia | 187,858 | 176,326 | 54,021 | 42,497 | 241,879 | 218,823 | 1,093,266 | 224,837 | 240,103 | 902,748 | 1,333,369 | 1,127,585 | ||||||||||||||||||||||||||||||||||||

| Total | 203,624 | 188,972 | 269,367 | 222,401 | 472,991 | 411,373 | 1,201,779 | 313,885 | 595,946 | 1,256,913 | 1,797,725 | 1,570,798 | ||||||||||||||||||||||||||||||||||||

| (1) | As of December 31, 2019, approximately 16,000, 3,000 and 2,000 net acres of undeveloped acreage are scheduled to expire by December 31, 2020, 2021 and 2022, respectively. |

Carbon Appalachia

The following table summarizes our 27.24% proportionate share in Carbon Appalachia’s gross and net developed and undeveloped acreage by state as of December 31, 2017. Acreage related to royalty, overriding royalty and other similar interests is excluded from this summary, as well as acreage related to any options held by Carbon Appalachia to acquire additional leasehold interests.

| December 31, 2017 | ||||||||||||||||||||||||

| Developed Acres | Undeveloped Acres | Total Acres | ||||||||||||||||||||||

| Gross | Net | Gross | Net | Gross | Net | |||||||||||||||||||

| Ohio | 986 | 290 | - | - | 986 | 290 | ||||||||||||||||||

| Virginia | 2,212 | 2,045 | 32,113 | 32,113 | 34,325 | 34,159 | ||||||||||||||||||

| West Virginia | 230,817 | 198,863 | 46,448 | 45,070 | 277,265 | 243,932 | ||||||||||||||||||

| Tennessee | 18,778 | 17,926 | 20,977 | 20,925 | 39,755 | 38,851 | ||||||||||||||||||

| Total | 252,793 | 219,124 | 99,538 | 98,108 | 352,331 | 317,232 | ||||||||||||||||||

Carbon California

The following table summarizes our 17.81% proportionate share in Carbon California’s gross and net developed and undeveloped acreage by state as of December 31, 2017. Acreage related to royalty, overriding royalty and other similar interests is excluded from this summary, as well as acreage related to any options held by Carbon California to acquire additional leasehold interests.

| December 31, 2017 | ||||||||||||||||||||||||

| Developed | Undeveloped | Total | ||||||||||||||||||||||

| Acres | Acres | Acres | ||||||||||||||||||||||

| Gross | Net | Gross | Net | Gross | Net | |||||||||||||||||||

| California | 415 | 415 | 1,427 | 1,425 | 1,842 | 1,840 | ||||||||||||||||||

| Total | ||||||||||||||||||||||||

Undeveloped Acreage Expirations

Carbon Natural Gas Company

The following table sets forth our gross and net undeveloped acres by state as of December 31, 2017 which are scheduled to expire through December 31, 2020 unless production is established within the spacing unit covering the acreage prior to the expiration date or we extend the terms of a lease by paying delay rentals to the lessor.

| December 31, 2017 | ||||||||||||||||||||||||

| 2018 | 2019 | 2020 | ||||||||||||||||||||||

| Gross | Net | Gross | Net | Gross | Net | |||||||||||||||||||

| Indiana | - | - | 34,285 | 34,285 | - | - | ||||||||||||||||||

| Illinois | 6,143 | 3,071 | 2,908 | 1,454 | 3,099 | 1,549 | ||||||||||||||||||

| Kentucky | 8,471 | 5,083 | 10,223 | 6,290 | 9,648 | 8,175 | ||||||||||||||||||

| West Virginia | - | - | 3,625 | 3,625 | 11,574 | 11,574 | ||||||||||||||||||

| Total | 14,614 | 8,154 | 51,041 | 45,654 | 24,321 | 21,298 | ||||||||||||||||||

Carbon Appalachian

The following table sets forth our 27.24% proportionate share in Carbon Appalachia’s gross and net undeveloped acres by state as of December 31, 2017 which are scheduled to expire through December 31, 2020 unless production is established within the spacing unit covering the acreage prior to the expiration date or Carbon Appalachia extends the terms of a lease by paying delay rentals to the lessor.

| December 31, 2017 | ||||||||||||||||||||||||

| 2018 | 2019 | 2020 | ||||||||||||||||||||||

| Gross | Net | Gross | Net | Gross | Net | |||||||||||||||||||

| Ohio | - | - | - | - | - | - | ||||||||||||||||||

| Tennessee | 1,416 | 1,416 | 478 | 457 | 58 | 48 | ||||||||||||||||||

| Virginia | 2 | 2 | - | - | - | - | ||||||||||||||||||

| West Virginia | 3,790 | 3,255 | 1,422 | 1,362 | 1,793 | 1,793 | ||||||||||||||||||

| Total | 5,207 | 4,673 | 1,901 | 1,819 | 1,851 | 1,851 | ||||||||||||||||||

Carbon California

Carbon California does not have any scheduled undeveloped acres to expire from December 31, 2017 through December 31, 2020.

Production, Average Sales Prices and Production Costs

Carbon Natural Gas Company

The following table reflects our production, average sales price, and production cost information for the years ended December 31, 2017, 20162019, 2018 and 2015.2017:

| Year Ended December 31, | Year Ended December 31, | |||||||||||||||||||||||

| 2017 | 2016 | 2015 | 2019 | 2018(1) | 2017(1) | |||||||||||||||||||

| Production data: | ||||||||||||||||||||||||

| Natural gas (MMcf) | 4,896 | 2,823 | 2,040 | 21,436 | 5,320 | 4,896 | ||||||||||||||||||

| Oil and condensate (Bbl) | 86,277 | 79,044 | 101,255 | |||||||||||||||||||||

| Oil (MBbl) | 589 | 451 | 86 | |||||||||||||||||||||

| Natural gas liquids (MBbl) | 36 | 33 | - | |||||||||||||||||||||

| Combined (MMcfe) | 5,414 | 3,297 | 2,646 | 25,182 | 8,223 | 5,414 | ||||||||||||||||||

| Gas and oil production revenue (in thousands) | $ | 19,511 | $ | 10,443 | $ | 10,708 | ||||||||||||||||||

| Commodity derivative (loss) gain (in thousands) | $ | 2,928 | $ | (2,259 | ) | $ | 852 | |||||||||||||||||

| Gas, oil and natural gas liquids production revenue (in thousands) | $ | 93,841 | $ | 48,052 | $ | 19,511 | ||||||||||||||||||

| Commodity derivative gain (in thousands) | $ | 3,044 | $ | 4,894 | $ | 2,928 | ||||||||||||||||||

| Prices: | ||||||||||||||||||||||||

| Average sales price before effects of hedging; | ||||||||||||||||||||||||

| Natural gas (per Mcf) | $ | 2.53 | $ | 2.53 | $ | 2.78 | $ | 2.63 | $ | 3.01 | $ | 3.12 | ||||||||||||

| Oil and condensate (per Bbl) | $ | 41.95 | $ | 41.95 | $ | 49.83 | ||||||||||||||||||

| Average sale price after effects of hedging: | ||||||||||||||||||||||||

| Oil (per Bbl) | $ | 62.50 | $ | 68.53 | $ | 48.83 | ||||||||||||||||||

| Natural gas liquids (per Bbl) | $ | 16.18 | $ | 34.55 | $ | - | ||||||||||||||||||

| Average sale price after effects of hedging(2): | ||||||||||||||||||||||||

| Natural gas (per Mcf) | $ | 3.12 | $ | 1.89 | $ | 3.01 | $ | 2.80 | $ | 2.96 | $ | 3.25 | ||||||||||||

| Oil and condensate (per Bbl) | $ | 48.84 | $ | 36.14 | $ | 53.48 | ||||||||||||||||||

| Oil (per Bbl) | 62.38 | $ | 60.65 | $ | 50.38 | |||||||||||||||||||

| Natural gas liquids (per Bbl) | $ | 16.18 | $ | 34.55 | $ | - | ||||||||||||||||||

| Average costs per Mcfe: | ||||||||||||||||||||||||

| Lease operating costs | $ | 1.13 | $ | 0.96 | $ | 1.10 | $ | 1.18 | $ | 1.94 | $ | 1.13 | ||||||||||||

| Transportation costs | $ | 0.40 | $ | 0.50 | $ | 0.65 | $ | 0.24 | $ | 0.54 | $ | 0.40 | ||||||||||||

| Production and property taxes | $ | 0.24 | $ | 0.25 | $ | 0.33 | $ | 0.22 | $ | 0.22 | $ | 0.24 | ||||||||||||

| (1) | The 2018 and 2017 activity shown above includes only that which is included in the consolidated financial statements. Therefore, the above represents all of Carbon’s activities for the years ended December 31, 2018 and 2017 and only the activity of Carbon California for the period February 1, 2018 through December 31, 2018. It does not include any activity for Carbon Appalachia as the OIE Membership Acquisition, which resulted in consolidation of Carbon Appalachia, did not occur until December 31, 2018. |

| (2) | Includes effect of settled commodity derivative gains and losses. |

10

Carbon Appalachia

Present Activities

The following table reflects our 27.24% proportionate share in Carbon Appalachia’s production, average sales price, and production cost information for the period endedAt December 31, 2017.

| Period from Inception Through December 31, | ||||

| 2017 | ||||

| Production data: | ||||

| Natural gas (MMcf) | 5,304 | |||

| Oil and NGLs (Bbl) | 14 | |||

| Combined (MMcfe) | 5,390 | |||

| Gas, oil and NGL production revenue (in thousands) | $ | 16,813 | ||

| Commodity derivative (loss) gain (in thousands) | $ | 2,545 | ||

| Prices: | ||||

| Average sales price before effects of hedging; | ||||

| Natural gas (per Mcf) | $ | 3.04 | ||

| Oil and NGLs (per Bbl) | $ | 47.94 | ||

| Average sale price after effects of hedging: | ||||

| Natural gas (per Mcf) | $ | 3.14 | ||

| Oil and NGLs (per Bbl) | $ | 47.41 | ||

| Average costs per Mcfe: | ||||

| Lease operating costs | $ | 0.98 | ||

| Transportation costs | $ | 0.35 | ||

| Production and property taxes | $ | 0.27 | ||

Carbon California2019, we have successfully drilled and completed one well and we were actively completing a second well in the Ventura Basin.

The following table reflects our 17.81% proportionate share in Carbon California’s production, average sales price, and production cost information for the year ended December 31, 2017.

| Period Inception Through December 31, | ||||

| 2017 | ||||

| Production data: | ||||

| Natural gas (MMcf) | 351 | |||

| Oil and condensate (Bbl) | 165 | |||

| Combined (MMcfe) | 1,339 | |||

| Gas and oil production revenue (in thousands) | $ | 8,616 | ||

| Commodity derivative (loss) gain (in thousands) | $ | (1,382 | ) | |

| Prices: | ||||

| Average sales price before effects of hedging; | ||||

| Natural gas (per Mcf) | $ | 2.95 | ||

| Oil and condensate (per Bbl) | $ | 46.04 | ||

| Average sale price after effects of hedging: | ||||

| Natural gas (per Mcf) | $ | 3.26 | ||

| Oil and condensate (per Bbl) | $ | 35.18 | ||

| Average costs per Mcfe: | ||||

| Lease operating costs | $ | 16.70 | ||

| Transportation costs | $ | 6.46 | ||

| Production and property taxes | $ | 2.37 | ||

Present Activities

Our current focus is on growth through acquisition of producing wells, rather than drilling wells.

Our current drilling program includes only those wells required to be drilled under certain agreements.

Marketing and Delivery Commitments

Our and our equity investees’ oil andAs of December 31, 2019, we have delivery commitments of approximately 1,289,000 Btu of natural gas production is generally sold onthrough February 2020 as part of a month-to-month basis in the spot market, priced in referencestorage contract. These delivery commitments were fulfilled subsequent to published indices. We believe that the loss of one or more of our or our equity investees’ purchasers would not have a material adverse effect on our or our equity investees’ ability to sell our production, because any individual purchaser could be readily replaced by another purchaser, absent a broad market disruption.

We currently do not have any delivery commitments.year-end.