| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) | |

| OF THE SECURITIES EXCHANGE ACT OF 1934. |

| Spirit Realty Capital, Inc. | Maryland | 20-1676382 | ||

| Spirit Realty, L.P. | Delaware | 20-1127940 | ||

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |||

| (972) 476-1900 | ||||

| (Address of principal executive offices; zip code) | (Registrant’s telephone number, including area code) | |||

| Title of each class: | Name of exchange on which registered: | |||

| Spirit Realty Capital, Inc. | Common Stock, $0.01 par value | New York Stock Exchange | ||

| Spirit Realty, L.P. | None | None | ||

| Spirit Realty Capital, Inc. | None | |

| Spirit Realty, L.P. | None | |

| Large accelerated filer | x | Accelerated filer | o | ||||

| Non-accelerated filer | o | Smaller reporting company | o | ||||

| Large accelerated filer | o | Accelerated filer | x | Non-accelerated filer | o | Smaller reporting company | o |

| PART I | ||

| Item 1. | Business | |

| Item 1A. | Risk Factors | |

| Item 1B. | Unresolved Staff Comments | |

| Item 2. | Properties | |

| Item 3. | Legal Proceedings | |

| Item 4. | Mine Safety Disclosure | |

| PART II | ||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |

| Item 6. | Selected Financial Data | |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | |

| Item 8. | Financial Statements and Supplementary Data | |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |

| Item 9A. | Controls and Procedures, As Restated | |

| Item 9B. | Other Information | |

| PART III | ||

| Item 10. | Directors, Executive Officers and Corporate Governance | |

| Item 11. | Executive Compensation | |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | |

| Item 14. | Principal Accountant Fees and Services | |

| PART IV | ||

| Item 15. | Exhibits, Financial Statement Schedules | |

| SIGNATURES | ||

| Definitions: | |

| 1031 Exchange | Tax-deferred like-kind exchange of properties held for business or investment purposes, pursuant to Section 1031 of the Code |

| 2013 Credit Facility | $400.0 million secured credit facility pursuant to the credit agreement between the Operating Partnership and certain lenders dated July 17, 2013 |

| 2015 Credit Facility | $800.0 million unsecured credit facility pursuant to the Credit Agreement |

| 2019 Notes | $402.5 million convertible notes of the Corporation due in 2019 |

| 2021 Notes | $345.0 million convertible notes of the Corporation due in 2021 |

| 401(k) Plan | Defined contribution retirement savings plan qualified under Section 401(k) of the Code |

| ACM | Asbestos-Containing Materials |

| ADA | Americans with Disabilities Act |

| Additional Collateral Deposit | A cash reserve deposit or letter of credit in the amount of $8.0 million required pursuant to an amendment of a certain CMBS loan agreement |

| AFFO | Adjusted Funds From Operations |

| Amended Incentive Award Plan | Amended and Restated Spirit Realty Capital, Inc. and Spirit Realty, L.P. 2012 Incentive Award Plan |

| AOCL | Accumulated Other Comprehensive Loss |

| ASC | Accounting Standards Codification |

| ASU | Accounting Standards Update |

| ATM Program | At the Market equity distribution program, pursuant to which the Corporation may offer and sell registered shares of common stock from time to time |

| CMBS | Commercial Mortgage Backed Securities |

| Code | Internal Revenue Code of 1986, as amended |

| Cole II | Cole Credit Property Trust II, Inc. |

| Cole II Merger | Acquisition on July 17, 2013 of Cole II by the Company, in which the Company merged with and into the Cole II legal entity |

| Collateral Pools | Pools of collateral assets that are pledged to the indenture trustee for the benefit of the noteholders and secure obligations of issuers under the Spirit Master Funding Program |

| Company | The Corporation and its consolidated subsidiaries |

| Convertible Notes | The 2019 Notes and 2021 Notes, together |

| Corporation | Spirit Realty Capital, Inc., a Maryland corporation |

| CPI | Consumer Price Index |

| Credit Agreement | 2015 credit facility agreement between the Operating Partnership and certain lenders dated March 31, 2015, as amended or otherwise modified from time to time |

| EBITDA | Earnings Before Interest, Taxes, Depreciation and Amortization |

| EBITDAR | Earnings Before Interest, Taxes, Depreciation, Amortization and Rent |

| EDF | Expected Default Frequency |

| Excess Cash | Rent received in excess of debt service obligations |

| Exchange Act | Securities Exchange Act of 1934, as amended |

| FASB | Financial Accounting Standards Board |

| FFO | Funds From Operations |

| Fitch | Fitch Ratings |

| GAAP | Generally Accepted Accounting Principles in the United States |

| IASB | International Accounting Standards Board |

| IFRS | International Financial Reporting Standards |

| IPO | Initial Public Offering |

| Definitions: | |

| IRS | Internal Revenue Service |

| LIBOR | London Interbank Offered Rate |

| Line of Credit | $40.0 million secured revolving credit facility pursuant to the loan agreement between an indirect wholly-owned subsidiary of the Corporation and a certain lender dated March 27, 2013, as amended |

| Master Trust 2013 | The net-lease mortgage securitization trust established in 2013 under the Spirit Master Funding Program |

| Master Trust 2014 | The net-lease mortgage securitization trust established in 2005 and amended and restated in 2014 under the Spirit Master Funding Program |

| Master Trust Exchange Costs | Legal, accounting and financial advisory services costs incurred in connection with the Exchange Offer |

| Master Trust Notes | The Master Trust 2013 and Master Trust 2014, together |

| Master Trust Release | Proceeds from the sale of assets securing the Master Trust Notes held in restricted accounts until a qualifying substitution is made |

| Merger | The transaction in which the Corporation's prior legal entity merged into the Cole II legal entity |

| Merger Exchange Ratio | Merger exchange ratio of 1.9048 |

| MGCL | Maryland General Corporation Law |

| Moody's | Moody's Investor Services |

| NAREIT | National Association of Real Estate Investment Trusts |

| Normalized Rental Revenue | Total rental revenues and earned income from direct financing leases from our owned properties during the final month of the reporting period, adjusted to exclude amounts from properties sold during that period and to include a full month of rental revenues for properties acquired during that period. |

| NYSE | New York Stock Exchange |

| OP Holdings | Spirit General OP Holdings, LLC |

| Operating Partnership | Spirit Realty, L.P., a Delaware limited partnership |

| PATH Act | Protecting Americans from Tax Hikes Act of 2015 |

| REIT | Real Estate Investment Trust |

| Revolving Credit Facilities | The 2013 Credit Facility, the 2015 Credit Facility and Line of Credit, together |

| S&P | Standard & Poor's Rating Services |

| SEC | Securities and Exchange Commission |

| Securities Act | Securities Act of 1933, as amended |

| Senior Unsecured Notes | $300 million aggregate principal amount of senior notes issued in August 2016 |

| Shopko | Specialty Retail Shops Holding Corp. and certain of its affiliates |

| Spirit Master Funding Program | The Company's asset-backed securitization program that comprises Master Trust 2013 and Master Trust 2014 |

| Term Loan | $420.0 million senior unsecured term facility pursuant to the Term Loan Agreement |

| Term Loan Agreement | Term loan agreement between the Operating Partnership and certain lenders dated November 3, 2015, as amended or otherwise modified from time to time |

| Total Debt | Principal debt outstanding before discounts, premiums or deferred financing costs |

| TRS | Taxable REIT Subsidiaries |

| TSR | Total Shareholder Return |

| U.S. | United States |

| ◦ | Leases for Operationally Essential Real Estate with Relatively Long Terms. We seek to own properties that are operationally essential to our tenants, thereby reducing the risk that the tenant would choose not to renew an expiring lease or reject a lease in bankruptcy. In addition, we seek to enter into leases with relatively long terms, typically with non-cancelable initial terms of 15 to 20 years and tenant renewal options for additional terms with attractive rent escalation provisions. |

| ◦ |

| ◦ | Active Management and Monitoring of Risks Related to Our Investments. When monitoring existing investments or evaluating new investments, we typically consider two broad categories of risk: (1) tenant financial distress risk; and (2) lease renewal risk. We seek to measure these risks through various processes, including the use of a credit modeling product that we license from Moody’s Analytics that estimates the performance of the leased properties relative to rental payments due under the leases and a review of current market data and our historical recovery rates on re-leased properties and property dispositions. Our underwriting and risk management processes are designed to structure new investments |

| ◦ | Portfolio Diversification. We monitor and manage the diversification of our real estate investment portfolio in order to reduce the risks associated with adverse developments affecting a particular tenant, property, industry or region. Our strategy emphasizes a portfolio that (1) derives no more than 10% of its annual rent from any single tenant |

Tenant (2) | Number of Properties | Total Square Footage (in thousands) | Percent of Total Revenue (1) | ||||||

| Specialty Retail Shops Holding Corp. (Shopko) | 181 | 13,502 | 14.0 | % | |||||

| Walgreen Company | 67 | 969 | 3.7 | ||||||

| 84 Properties, LLC | 109 | 4,118 | 3.1 | ||||||

| Cajun Global, LLC (Church's Chicken) | 201 | 257 | 2.3 | ||||||

| Academy Sports + Outdoors | 8 | 1,852 | 2.0 | ||||||

| Alimentation Couche-Tard, Inc. (Circle K) | 83 | 251 | 2.0 | ||||||

| CVS Caremark | 37 | 413 | 1.6 | ||||||

| CarMax, Inc. | 9 | 368 | 1.4 | ||||||

| Carmike Cinemas, Inc. | 13 | 625 | 1.3 | ||||||

| Rite Aid Corp | 30 | 357 | 1.3 | ||||||

| Other | 1,626 | 34,249 | 67.3 | ||||||

| Total | 2,364 | 56,961 | 100.0 | % | |||||

(1) Total revenue for the quarter ended December 31, 2014. | |||||||||

(2) Tenants represent legal entities ultimately responsible for obligations under the lease agreements. Other tenants may operate certain of the same business concepts or brands set forth above, but represent distinct tenant credits. | |||||||||

Tenant (1) | Number of Properties | Total Square Feet (in thousands) | Percent of Normalized Rental Revenue | |||||

| Shopko | 116 | 7,798 | 8.2 | % | ||||

| Walgreen Company | 49 | 722 | 2.7 | |||||

| AMC Entertainment, Inc. | 17 | 862 | 2.3 | |||||

| Cajun Global, LLC | 192 | 271 | 2.2 | |||||

| AB Acquisition, LLC | 23 | 1,030 | 2.1 | |||||

| Alimentation Couche-Tard, Inc. | 83 | 250 | 1.9 | |||||

| Academy, LTD | 6 | 2,769 | 1.9 | |||||

| Regal Entertainment Group | 15 | 656 | 1.5 | |||||

| GPM Investments, LLC | 105 | 272 | 1.5 | |||||

| CVS Caremark Corporation | 36 | 405 | 1.5 | |||||

| Other | 1,853 | 35,823 | 74.2 | |||||

| Vacant | 46 | 2,029 | — | |||||

| Total | 2,541 | 52,887 | 100.0 | % | ||||

| Industry | Number of Properties | Total Square Footage (in thousands) | Percent of Total Rent (1) | Number of Properties | Total Square Feet (in thousands) | Percent of Normalized Rental Revenue | ||||||||||||

| General Merchandise | 228 | 14,841 | 15.9 | % | 156 | 9,224 | 9.9 | % | ||||||||||

| Restaurants - Casual Dining | 389 | 2,505 | 9.8 | 339 | 2,041 | 8.9 | ||||||||||||

| Restaurants - Quick Service | 546 | 1,473 | 7.5 | 588 | 1,359 | 8.1 | ||||||||||||

| Movie Theaters | 60 | 3,012 | 7.4 | |||||||||||||||

| Convenience Stores | 347 | 1,100 | 7.0 | |||||||||||||||

| Grocery | 66 | 3,127 | 6.2 | |||||||||||||||

| Drug Stores / Pharmacies | 134 | 1,739 | 6.8 | 111 | 1,560 | 5.3 | ||||||||||||

| Convenience Stores / Car Washes | 210 | 743 | 6.5 | |||||||||||||||

| Medical / Other Office | 122 | 1,293 | 4.8 | |||||||||||||||

| Sporting Goods | 29 | 4,209 | 4.2 | |||||||||||||||

| Health and Fitness | 45 | 1,800 | 4.0 | |||||||||||||||

| Automotive Parts and Service | 185 | 1,338 | 3.7 | |||||||||||||||

| Entertainment | 23 | 1,129 | 2.9 | |||||||||||||||

| Home Furnishings | 33 | 2,305 | 2.8 | |||||||||||||||

| Education | 54 | 821 | 2.6 | |||||||||||||||

| Building Materials | 177 | 5,750 | 5.6 | 64 | 2,291 | 2.5 | ||||||||||||

| Movie Theatres | 44 | 2,178 | 5.1 | |||||||||||||||

| Medical / Other Office | 98 | 1,071 | 3.9 | |||||||||||||||

| Apparel | 13 | 2,321 | 2.5 | |||||||||||||||

| Specialty Retail | 30 | 1,630 | 2.4 | |||||||||||||||

| Automotive Dealers | 23 | 665 | 2.3 | |||||||||||||||

| Home Improvement | 13 | 1,656 | 2.0 | |||||||||||||||

| Distribution | 17 | 4,077 | 3.8 | 13 | 1,372 | 1.9 | ||||||||||||

| Automotive Parts & Service | 151 | 1,280 | 3.2 | |||||||||||||||

| Grocery | 49 | 1,846 | 3.1 | |||||||||||||||

| Apparel | 11 | 2,261 | 2.9 | |||||||||||||||

| Home Furnishings | 31 | 1,922 | 2.6 | |||||||||||||||

| Health & Fitness | 24 | 933 | 2.5 | |||||||||||||||

| Education | 41 | 1,054 | 2.4 | |||||||||||||||

| Home Improvement | 10 | 1,492 | 2.3 | |||||||||||||||

| Sporting Goods | 23 | 1,223 | 2.3 | |||||||||||||||

| Automotive Dealers | 22 | 657 | 2.3 | |||||||||||||||

| Entertainment | 10 | 661 | 1.9 | |||||||||||||||

| Car Washes | 37 | 217 | 1.6 | |||||||||||||||

| Manufacturing | 27 | 4,094 | 1.7 | 19 | 2,662 | 1.4 | ||||||||||||

| Specialty Retail | 23 | 870 | 1.7 | |||||||||||||||

| Dollar Stores | 83 | 859 | 1.3 | |||||||||||||||

| Consumer Electronics | 16 | 1,270 | 1.5 | 10 | 529 | 1.1 | ||||||||||||

| Pet Supplies & Service | 5 | 1,126 | 1.0 | |||||||||||||||

| Pet Supplies and Service | 4 | 1,016 | * | |||||||||||||||

| Wholesale Clubs | 4 | 393 | * | |||||||||||||||

| Office Supplies | 20 | 546 | 1.0 | 17 | 400 | * | ||||||||||||

| Financial Services | 4 | 422 | * | 4 | 372 | * | ||||||||||||

| Wholesale Clubs | 3 | 355 | * | |||||||||||||||

| Dollar Stores | 41 | 449 | * | |||||||||||||||

| Other | 10 | 123 | * | 3 | 157 | * | ||||||||||||

| Vacant | 46 | 2,029 | — | |||||||||||||||

| Total | 2,364 | 56,961 | 100.0 | % | 2,541 | 52,887 | 100.0 | % | ||||||||||

| * Less than 1% | ||||||||||||||||||

(1) Total rental revenue for the month ended December 31, 2014 for properties owned at December 31, 2014. | ||||||||||||||||||

| Asset Type | Number of Properties | Total Square Footage (in thousands) | Percent of Total Rent (1) | Number of Properties | Total Square Feet (in thousands) | Percent of Normalized Rental Revenue | |||||||||||

| Retail | 2,170 | 43,426 | 85.7 | % | 2,345 | 39,553 | 86.0 | % | |||||||||

| Industrial | 80 | 11,376 | 8.2 | 73 | 11,069 | 8.0 | |||||||||||

| Office | 114 | 2,159 | 6.1 | 123 | 2,265 | 6.0 | |||||||||||

| Total | 2,364 | 56,961 | 100.0 | % | 2,541 | 52,887 | 100.0 | % | |||||||||

(1) Total rental revenue for the month ended December 31, 2014 for properties owned at December 31, 2014. | |||||||||||||||||

| Location | Number of Properties | Total Square Footage (in thousands) | Percent of Total Rent (1) | Number of Properties | Total Square Feet (in thousands) | Percent of Normalized Rental Revenue | ||||||||||||

| Texas | 270 | 6,101 | 12.0 | % | 313 | 6,475 | 12.5 | % | ||||||||||

| Georgia | 187 | 3,378 | 6.3 | |||||||||||||||

| Illinois | 126 | 3,694 | 6.7 | 118 | 3,626 | 5.8 | ||||||||||||

| Florida | 151 | 1,439 | 5.3 | |||||||||||||||

| California | 59 | 1,483 | 5.2 | |||||||||||||||

| Ohio | 129 | 2,417 | 4.6 | |||||||||||||||

| Wisconsin | 63 | 5,047 | 5.5 | 52 | 3,464 | 4.1 | ||||||||||||

| Georgia | 167 | 1,944 | 4.9 | |||||||||||||||

| Florida | 136 | 2,195 | 4.9 | |||||||||||||||

| Ohio | 127 | 2,144 | 4.3 | |||||||||||||||

| California | 49 | 1,065 | 3.5 | |||||||||||||||

| Missouri | 74 | 1,272 | 3.0 | |||||||||||||||

| Minnesota | 52 | 1,704 | 2.9 | 56 | 2,276 | 3.4 | ||||||||||||

| Michigan | 140 | 1,921 | 3.4 | |||||||||||||||

| Tennessee | 118 | 1,772 | 2.9 | 109 | 1,403 | 2.9 | ||||||||||||

| Indiana | 80 | 1,493 | 2.8 | 81 | 1,253 | 2.7 | ||||||||||||

| Missouri | 91 | 1,389 | 2.7 | |||||||||||||||

| North Carolina | 66 | 1,517 | 2.7 | 71 | 1,408 | 2.7 | ||||||||||||

| Alabama | 110 | 830 | 2.5 | |||||||||||||||

| Arizona | 57 | 753 | 2.5 | |||||||||||||||

| South Carolina | 47 | 1,024 | 2.7 | 46 | 962 | 2.1 | ||||||||||||

| Michigan | 82 | 1,759 | 2.6 | |||||||||||||||

| Alabama | 103 | 818 | 2.5 | |||||||||||||||

| Nebraska | 21 | 1,972 | 2.4 | |||||||||||||||

| Pennsylvania | 71 | 1,657 | 2.3 | |||||||||||||||

| Arizona | 51 | 799 | 2.2 | |||||||||||||||

| Kansas | 40 | 973 | 2.1 | |||||||||||||||

| Virginia | 47 | 1,546 | 2.0 | 61 | 1,371 | 2.0 | ||||||||||||

| Colorado | 29 | 774 | 1.6 | 33 | 1,040 | 1.9 | ||||||||||||

| Utah | 16 | 1,494 | 1.5 | |||||||||||||||

| Pennsylvania | 55 | 1,119 | 1.8 | |||||||||||||||

| Kansas | 40 | 852 | 1.7 | |||||||||||||||

| Nevada | 6 | 1,039 | 1.6 | |||||||||||||||

| New Mexico | 39 | 548 | 1.6 | |||||||||||||||

| Oklahoma | 53 | 536 | 1.5 | 68 | 559 | 1.5 | ||||||||||||

| New York | 39 | 738 | 1.5 | |||||||||||||||

| Kentucky | 49 | 635 | 1.5 | |||||||||||||||

| Washington | 25 | 726 | 1.5 | |||||||||||||||

| Arkansas | 52 | 618 | 1.2 | |||||||||||||||

| New Jersey | 15 | 895 | 1.2 | |||||||||||||||

| Massachusetts | 4 | 1,125 | 1.1 | |||||||||||||||

| Oregon | 14 | 453 | 1.1 | |||||||||||||||

| Idaho | 17 | 1,235 | 1.5 | 16 | 679 | 1.1 | ||||||||||||

| New York | 45 | 945 | 1.4 | |||||||||||||||

| Washington | 22 | 950 | 1.4 | |||||||||||||||

| Massachusetts | 8 | 1,390 | 1.3 | |||||||||||||||

| Nevada | 5 | 1,039 | 1.3 | |||||||||||||||

| Location | Number of Properties | Total Square Footage (in thousands) | Percent of Total Rent (1) | Number of Properties | Total Square Feet (in thousands) | Percent of Normalized Rental Revenue | ||||||||||||

| New Mexico | 33 | 330 | 1.2 | |||||||||||||||

| Iowa | 39 | 732 | 1.2 | 35 | 638 | 1.0 | ||||||||||||

| Kentucky | 45 | 952 | 1.2 | |||||||||||||||

| Oregon | 13 | 364 | 1.0 | |||||||||||||||

| Mississippi | 34 | 410 | * | 46 | 422 | 1.0 | ||||||||||||

| Arkansas | 35 | 643 | * | |||||||||||||||

| New Hampshire | 16 | 640 | * | |||||||||||||||

| Louisiana | 30 | 315 | * | 28 | 224 | * | ||||||||||||

| New Hampshire | 16 | 852 | * | |||||||||||||||

| Maryland | 19 | 242 | * | |||||||||||||||

| Nebraska | 14 | 521 | * | |||||||||||||||

| Connecticut | 5 | 686 | * | |||||||||||||||

| South Dakota | 11 | 522 | * | 9 | 395 | * | ||||||||||||

| Montana | 7 | 430 | * | |||||||||||||||

| West Virginia | 28 | 568 | * | 18 | 297 | * | ||||||||||||

| Maryland | 22 | 409 | * | |||||||||||||||

| New Jersey | 13 | 463 | * | |||||||||||||||

| Montana | 7 | 512 | * | |||||||||||||||

| Utah | 9 | 806 | * | |||||||||||||||

| North Dakota | 5 | 250 | * | 5 | 236 | * | ||||||||||||

| Maine | 26 | 79 | * | 26 | 79 | * | ||||||||||||

| Wyoming | 9 | 185 | * | |||||||||||||||

| Rhode Island | 4 | 128 | * | 4 | 117 | * | ||||||||||||

| Connecticut | 2 | 171 | * | |||||||||||||||

| Wyoming | 9 | 186 | * | |||||||||||||||

| Alaska | 1 | 38 | * | |||||||||||||||

| Delaware | 3 | 86 | * | 1 | 50 | * | ||||||||||||

| Virgin Islands | 1 | 5 | * | |||||||||||||||

| Vermont | 2 | 42 | * | 2 | 2 | * | ||||||||||||

| Virgin Islands | 1 | 38 | * | |||||||||||||||

| Alaska | 1 | 50 | * | |||||||||||||||

| Total properties owned | 2,364 | 56,961 | 100.0 | % | ||||||||||||||

| * Less than 1% | ||||||||||||||||||

(1) Total rental revenue for the month ended December 31, 2014 for properties owned at December 31, 2014. | ||||||||||||||||||

| Total | 2,541 | 52,887 | 100.0 | % | ||||||||||||||

| Leases Expiring In: | Number of Properties | Expiring Annual Rent (in thousands) (1) | Total Square Footage (in thousands) | Percent of Total Expiring Annual Rent | Number of Properties | Normalized Rental Revenue Annualized (in thousands) (1) | Total Square Feet (in thousands) | Percent of Expiring Annual Rental Revenue | |||||||||||||||||

| 2015 | 47 | $ | 14,194 | 2,439 | 2.4 | % | |||||||||||||||||||

| 2016 | 47 | 22,746 | 2,390 | 3.8 | |||||||||||||||||||||

| 2017 | 63 | 19,515 | 2,021 | 3.3 | 69 | $ | 3,052 | 23,501 | 3.6 | % | |||||||||||||||

| 2018 | 77 | 24,271 | 2,141 | 4.0 | 70 | 1,885 | 22,184 | 3.4 | |||||||||||||||||

| 2019 | 117 | 22,900 | 2,376 | 3.8 | 106 | 1,920 | 19,868 | 3.1 | |||||||||||||||||

| 2020 | 74 | 25,957 | 1,685 | 4.3 | 74 | 1,674 | 20,669 | 3.2 | |||||||||||||||||

| 2021 | 193 | 43,345 | 4,839 | 7.2 | 188 | 3,905 | 47,012 | 7.3 | |||||||||||||||||

| 2022 | 103 | 25,163 | 1,997 | 4.2 | 97 | 2,148 | 26,296 | 4.1 | |||||||||||||||||

| 2023 | 89 | 34,832 | 3,274 | 5.8 | 109 | 3,440 | 34,444 | 5.3 | |||||||||||||||||

| 2024 | 64 | 18,795 | 874 | 3.1 | 58 | 1,207 | 21,106 | 3.3 | |||||||||||||||||

| 2025 and thereafter | 1,453 | 347,633 | 30,978 | 58.1 | |||||||||||||||||||||

| 2025 | 78 | 2,116 | 37,254 | 5.8 | |||||||||||||||||||||

| 2026 | 200 | 5,311 | 47,094 | 7.3 | |||||||||||||||||||||

| Thereafter | 1,446 | 24,200 | 346,502 | 53.6 | |||||||||||||||||||||

| Vacant | 37 | — | 1,947 | — | 46 | 2,029 | — | — | |||||||||||||||||

| Total owned properties | 2,364 | $ | 599,351 | 56,961 | 100.0 | % | 2,541 | $ | 52,887 | 645,930 | 100.0 | % | |||||||||||||

(1) Total rental revenue for the month ended December 31, 2014 for properties owned at December 31, 2014 multiplied by twelve. | |||||||||||||||||||||||||

| Price Per Share | ||||||||||||

of Common Stock (1) | Distributions | |||||||||||

| High | Low | Declared (1) | ||||||||||

| 2014 | ||||||||||||

| First quarter | $ | 11.43 | $ | 9.83 | $ | 0.16625 | ||||||

| Second quarter | 11.49 | 10.62 | 0.16625 | |||||||||

| Third quarter | 12.02 | 10.92 | 0.16625 | |||||||||

| Fourth quarter | 12.02 | 11.06 | 0.17000 | |||||||||

| Total | $ | 0.66875 | ||||||||||

| 2013 | ||||||||||||

| First quarter | $ | 10.78 | $ | 9.06 | $ | 0.16406 | ||||||

| Second quarter | 12.11 | 8.94 | 0.16406 | |||||||||

| Third quarter | 10.05 | 8.53 | 0.16406 | |||||||||

| Fourth quarter | 10.50 | 9.12 | 0.16625 | |||||||||

| Total | $ | 0.65843 | ||||||||||

Price Per Share of Common Stock | Dividends | ||||||||||

| High | Low | Declared | |||||||||

| 2016 | |||||||||||

| First quarter | $ | 11.25 | $ | 9.10 | $ | 0.17500 | |||||

| Second quarter | 12.77 | 10.87 | 0.17500 | ||||||||

| Third quarter | 13.88 | 12.78 | 0.17500 | ||||||||

| Fourth quarter | 13.10 | 10.26 | 0.18000 | ||||||||

| Total | $ | 0.70500 | |||||||||

| 2015 | |||||||||||

| First quarter | $ | 12.99 | $ | 11.66 | $ | 0.17000 | |||||

| Second quarter | 12.40 | 9.67 | 0.17000 | ||||||||

| Third quarter | 10.55 | 9.04 | 0.17000 | ||||||||

| Fourth quarter | 10.40 | 9.33 | 0.17500 | ||||||||

| Total | $ | 0.68500 | |||||||||

| Distributions Declared | |||

| 2016 | |||

| First quarter | $ | 0.17500 | |

| Second quarter | 0.17500 | ||

| Third quarter | 0.17500 | ||

| Fourth quarter | 0.18000 | ||

| Total | $ | 0.70500 | |

| 2015 | |||

| First quarter | $ | 0.17000 | |

| Second quarter | 0.17000 | ||

| Third quarter | 0.17000 | ||

| Fourth quarter | 0.17500 | ||

| Total | $ | 0.68500 | |

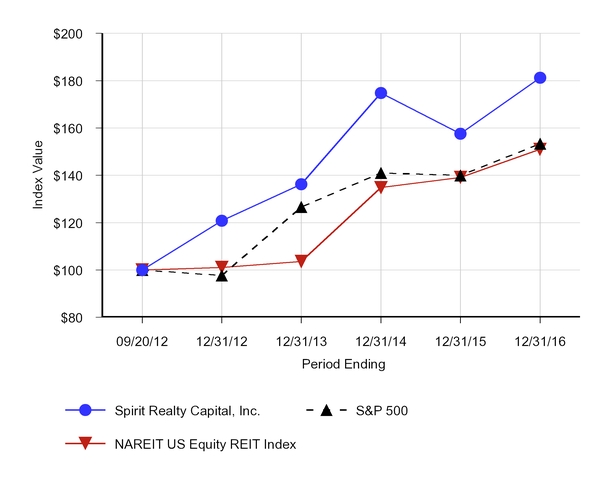

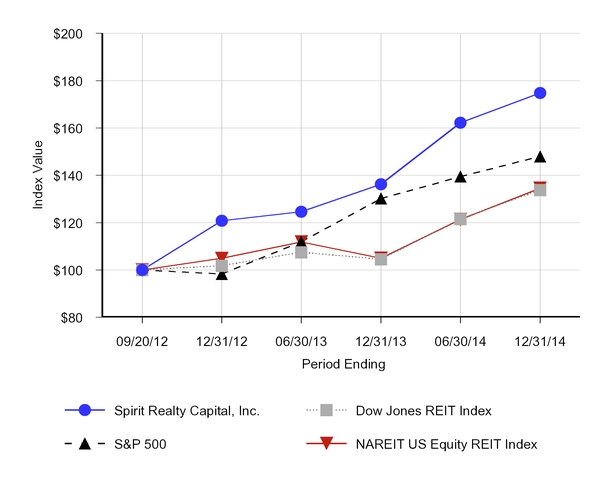

| Period Ended | Period Ended | |||||||||||||||||||||||||||||||||||

| Index: | 9/20/2012 | 12/31/2012 | 6/30/2013 | 12/31/2013 | 6/30/2014 | 12/31/2014 | 9/20/2012 | 12/31/2012 | 12/31/2013 | 12/31/2014 | 12/31/2015 | 12/31/2016 | ||||||||||||||||||||||||

| Spirit Realty Capital, Inc. | $ | 100 | $ | 121 | $ | 125 | $ | 136 | $ | 162 | $ | 175 | $ | 100 | $ | 121 | $ | 136 | $ | 175 | $ | 158 | $ | 181 | ||||||||||||

| S&P 500 | $ | 100 | $ | 98 | $ | 112 | $ | 130 | $ | 139 | $ | 148 | $ | 100 | $ | 98 | $ | 127 | $ | 141 | $ | 140 | $ | 153 | ||||||||||||

| NAREIT US Equity REIT Index | $ | 100 | $ | 105 | $ | 112 | $ | 105 | $ | 121 | $ | 135 | $ | 100 | $ | 101 | $ | 104 | $ | 135 | $ | 139 | $ | 151 | ||||||||||||

| Dow Jones REIT Index | $ | 100 | $ | 102 | $ | 107 | $ | 104 | $ | 122 | $ | 134 | ||||||||||||||||||||||||

| (Dollars in thousands, except share and per share data) | |||||||||||||||||||

| Years Ended December 31, | |||||||||||||||||||

2014 (1) | 2013 (1) | 2012 | 2011 | 2010 | |||||||||||||||

| Operating Data: | |||||||||||||||||||

| Revenues: | |||||||||||||||||||

| Rentals | $ | 574,456 | $ | 404,402 | $ | 266,567 | $ | 255,672 | $ | 255,148 | |||||||||

| Interest income on loans receivable | 7,239 | 5,928 | 5,696 | 6,772 | 9,572 | ||||||||||||||

| Earned income from direct financing leases | 3,343 | 1,572 | — | — | — | ||||||||||||||

| Tenant reimbursement income | 13,085 | 5,637 | — | — | — | ||||||||||||||

| Interest income and other | 4,748 | 1,928 | 852 | 786 | 14,473 | ||||||||||||||

| Total revenues | 602,871 | 419,467 | 273,115 | 263,230 | 279,193 | ||||||||||||||

| Expenses: | |||||||||||||||||||

| General and administrative | 44,252 | 35,146 | 36,252 | 27,854 | 19,575 | ||||||||||||||

| Litigation | — | — | — | — | 22,282 | ||||||||||||||

| Finance restructuring charges | 13,022 | 717 | — | — | — | ||||||||||||||

| Merger costs | — | 56,644 | — | — | — | ||||||||||||||

| Property costs | 23,383 | 11,760 | 5,176 | 4,693 | 2,631 | ||||||||||||||

| Real estate acquisition costs | 3,631 | 1,718 | 1,054 | 553 | — | ||||||||||||||

| Interest | 220,070 | 179,267 | 156,220 | 169,343 | 172,500 | ||||||||||||||

| Depreciation and amortization | 247,966 | 164,054 | 104,984 | 103,179 | 103,409 | ||||||||||||||

| Impairments (recoveries) | 36,019 | (185 | ) | 8,918 | 5,646 | 20,291 | |||||||||||||

| Total expenses | 588,343 | 449,121 | 312,604 | 311,268 | 340,688 | ||||||||||||||

| Income (loss) from continuing operations before other expense and income tax expense | 14,528 | (29,654 | ) | (39,489 | ) | (48,038 | ) | (61,495 | ) | ||||||||||

| Other (expense) income: | |||||||||||||||||||

| Loss on debt extinguishment | (64,750 | ) | (2,405 | ) | (32,522 | ) | — | — | |||||||||||

| Gain on debt repurchases | — | — | — | — | 9,455 | ||||||||||||||

| Loss on sale of loans receivable | — | — | — | — | (12,565 | ) | |||||||||||||

| Total other expense | (64,750 | ) | (2,405 | ) | (32,522 | ) | — | (3,110 | ) | ||||||||||

| Loss from continuing operations before income tax expense | (50,222 | ) | (32,059 | ) | (72,011 | ) | (48,038 | ) | (64,605 | ) | |||||||||

| Income tax expense (benefit) | 673 | 1,113 | 504 | (60 | ) | 239 | |||||||||||||

| Loss from continuing operations | (50,895 | ) | (33,172 | ) | (72,515 | ) | (47,978 | ) | (64,844 | ) | |||||||||

Discontinued operations: (2) | |||||||||||||||||||

| Income (loss) from discontinued operations | 3,368 | (2,077 | ) | (369 | ) | (13,149 | ) | (21,302 | ) | ||||||||||

| Gain (loss) on dispositions of assets | 488 | 36,926 | (3,349 | ) | (2,736 | ) | (391 | ) | |||||||||||

| Income (loss) from discontinued operations | 3,856 | 34,849 | (3,718 | ) | (15,885 | ) | (21,693 | ) | |||||||||||

| (Loss) income before dispositions of assets | (47,039 | ) | 1,677 | (76,233 | ) | (63,863 | ) | (86,537 | ) | ||||||||||

| Gain on dispositions of assets | 13,240 | — | — | — | — | ||||||||||||||

| Net (loss) income | (33,799 | ) | 1,677 | (76,233 | ) | (63,863 | ) | (86,537 | ) | ||||||||||

| Less: preferred dividends | — | — | (63 | ) | (16 | ) | (15 | ) | |||||||||||

| Net (loss) income attributable to common stockholders | $ | (33,799 | ) | $ | 1,677 | $ | (76,296 | ) | $ | (63,879 | ) | $ | (86,552 | ) | |||||

| Net (loss) income per share of common stock—basic and diluted: | |||||||||||||||||||

| Continuing operations | $ | (0.10 | ) | $ | (0.14 | ) | $ | (0.92 | ) | $ | (0.97 | ) | $ | (1.32 | ) | ||||

| Discontinued operations | 0.01 | 0.14 | (0.05 | ) | (0.33 | ) | (0.44 | ) | |||||||||||

| Net (loss) income per share attributable to common stockholders—basic and diluted | $ | (0.09 | ) | $ | 0.00 | $ | (0.97 | ) | $ | (1.30 | ) | $ | (1.76 | ) | |||||

| Weighted average common shares outstanding: | |||||||||||||||||||

Basic and diluted common shares (3) | 386,809,746 | 255,020,565 | 78,625,102 | 49,265,701 | 49,265,701 | ||||||||||||||

(1) As a result of the Merger completed on July 17, 2013, Operating Data includes the results of operations from the acquired properties for less than half a year in 2013 and for a full year in 2014. | |||||||||||||||||||

(2) Includes gains, losses and results of operations from all property dispositions and from properties classified as held for sale at the end of the period for all periods prior to 2014. During 2014, only those properties classified as held for sale as of December 31, 2013 are reported as discontinued operations and will continue to be reported as such until they are disposed of. | |||||||||||||||||||

(3) Historical weighted average number of shares of common stock outstanding (basic and diluted) have been adjusted for the Merger Exchange Ratio. No potentially dilutive securities were included as their effect would be anti-dilutive on results from continuing operations. | |||||||||||||||||||

| Years Ended December 31, | |||||||||||||||||||

2016 (1) | 2015 (1) | 2014 (1) | 2013 (1) | 2012 | |||||||||||||||

| (Dollars in thousands, except share and per share data) | |||||||||||||||||||

| Operating Data: | |||||||||||||||||||

| Revenues: | |||||||||||||||||||

| Rentals | $ | 648,363 | $ | 634,151 | $ | 574,456 | $ | 404,402 | $ | 266,567 | |||||||||

| Interest income on loans receivable | 5,253 | 6,948 | 7,239 | 5,928 | 5,696 | ||||||||||||||

| Earned income from direct financing leases | 2,742 | 3,024 | 3,343 | 1,572 | — | ||||||||||||||

| Tenant reimbursement income | 14,125 | 15,952 | 13,085 | 5,637 | — | ||||||||||||||

| Other income | 15,491 | 7,260 | 4,748 | 1,928 | 852 | ||||||||||||||

| Total revenues | 685,974 | 667,335 | 602,871 | 419,467 | 273,115 | ||||||||||||||

| Expenses: | |||||||||||||||||||

| General and administrative | 52,615 | 47,730 | 42,637 | 35,146 | 36,252 | ||||||||||||||

| Restructuring charges | 6,341 | 7,056 | — | — | — | ||||||||||||||

| Finance restructuring costs | — | — | 13,022 | 717 | — | ||||||||||||||

| Merger costs | — | — | — | 56,644 | — | ||||||||||||||

| Property costs | 30,839 | 27,715 | 23,383 | 11,760 | 5,176 | ||||||||||||||

| Real estate acquisition costs | 3,229 | 2,739 | 3,631 | 1,718 | 1,054 | ||||||||||||||

| Interest | 196,586 | 222,901 | 220,070 | 179,267 | 156,220 | ||||||||||||||

| Depreciation and amortization | 262,276 | 260,633 | 247,966 | 164,054 | 104,984 | ||||||||||||||

| Impairments (recoveries) | 88,275 | 70,695 | 37,598 | (185 | ) | 8,918 | |||||||||||||

| Total expenses | 640,161 | 639,469 | 588,307 | 449,121 | 312,604 | ||||||||||||||

| Income (loss) from continuing operations before other expense and income tax expense | 45,813 | 27,866 | 14,564 | (29,654 | ) | (39,489 | ) | ||||||||||||

| Other expense: | |||||||||||||||||||

| Gain (loss) on debt extinguishment | 233 | (3,162 | ) | (64,750 | ) | (2,405 | ) | (32,522 | ) | ||||||||||

| Total other income (expense) | 233 | (3,162 | ) | (64,750 | ) | (2,405 | ) | (32,522 | ) | ||||||||||

| Income (loss) from continuing operations before income tax expense | 46,046 | 24,704 | (50,186 | ) | (32,059 | ) | (72,011 | ) | |||||||||||

| Income tax expense | (965 | ) | (601 | ) | (673 | ) | (1,113 | ) | (504 | ) | |||||||||

| Income (loss) from continuing operations | 45,081 | 24,103 | (50,859 | ) | (33,172 | ) | (72,515 | ) | |||||||||||

Discontinued operations: (2) | |||||||||||||||||||

| Income (loss) from discontinued operations | — | 98 | 3,368 | (4,530 | ) | (369 | ) | ||||||||||||

| Gain (loss) on disposition of assets | — | 590 | 325 | 36,086 | (3,349 | ) | |||||||||||||

| Income (loss) from discontinued operations | — | 688 | 3,693 | 31,556 | (3,718 | ) | |||||||||||||

| (Dollars in thousands) | |||||||||||||||||||

| Years Ended December 31, | |||||||||||||||||||

2014 (1) | 2013 (1) | 2012 | 2011 | 2010 | |||||||||||||||

| Balance Sheet Data (end of period): | |||||||||||||||||||

| Gross investments including related lease intangibles | $ | 8,044,363 | $ | 7,235,732 | $ | 3,654,925 | $ | 3,582,870 | $ | 3,610,834 | |||||||||

| Net investments | 7,317,560 | 6,743,439 | 3,119,608 | 2,867,302 | 2,979,496 | ||||||||||||||

| Cash and cash equivalents | 176,181 | 66,588 | 73,568 | 49,536 | 88,341 | ||||||||||||||

| Total assets | 8,017,001 | 7,231,045 | 3,247,677 | 3,231,561 | 3,396,842 | ||||||||||||||

| Debt obligations, net | 4,369,634 | 3,778,218 | 1,894,878 | 2,627,146 | 2,730,994 | ||||||||||||||

| Total liabilities | 4,698,900 | 4,113,011 | 1,994,234 | 2,705,201 | 2,806,741 | ||||||||||||||

Total stockholders' equity (2) | 3,318,101 | 3,118,034 | 1,253,443 | 526,360 | 590,101 | ||||||||||||||

| Other Data: | |||||||||||||||||||

FFO (3) | $ | 236,490 | $ | 139,487 | $ | 52,830 | $ | 69,766 | $ | 70,548 | |||||||||

AFFO (3) | $ | 320,785 | $ | 208,853 | $ | 119,248 | $ | 99,574 | $ | 113,206 | |||||||||

| Number of properties in investment portfolio | 2,509 | 2,186 | 1,207 | 1,153 | 1,161 | ||||||||||||||

| Owned properties occupancy at period end (based on number of properties) | 98 | % | 99 | % | 99 | % | 98 | % | 96 | % | |||||||||

| Income (loss) before gain on disposition of assets | 45,081 | 24,791 | (47,166 | ) | (1,616 | ) | (76,233 | ) | |||||||||||

| Gain on disposition of assets | 52,365 | 68,421 | 10,221 | — | — | ||||||||||||||

| Net income (loss) | 97,446 | 93,212 | (36,945 | ) | (1,616 | ) | (76,233 | ) | |||||||||||

| Less: preferred dividends | — | — | — | — | (63 | ) | |||||||||||||

| Net income (loss) attributable to common stockholders | $ | 97,446 | $ | 93,212 | $ | (36,945 | ) | $ | (1,616 | ) | $ | (76,296 | ) | ||||||

| Net income (loss) per share of common stock—basic: | |||||||||||||||||||

| Continuing operations | $ | 0.21 | $ | 0.21 | $ | (0.11 | ) | $ | (0.14 | ) | $ | (0.92 | ) | ||||||

| Discontinued operations | — | — | 0.01 | 0.13 | (0.05 | ) | |||||||||||||

| Net income (loss) per share attributable to common stockholders—basic | $ | 0.21 | $ | 0.21 | $ | (0.10 | ) | $ | (0.01 | ) | $ | (0.97 | ) | ||||||

| Net income (loss) per share of common stock—diluted: | |||||||||||||||||||

| Continuing operations | $ | 0.21 | $ | 0.21 | $ | (0.11 | ) | $ | (0.14 | ) | $ | (0.92 | ) | ||||||

| Discontinued operations | — | — | 0.01 | 0.13 | (0.05 | ) | |||||||||||||

| Net income (loss) per share attributable to common stockholders—diluted | $ | 0.21 | $ | 0.21 | $ | (0.10 | ) | $ | (0.01 | ) | $ | (0.97 | ) | ||||||

| Weighted average shares of common stock outstanding: | |||||||||||||||||||

Basic common shares (3) | 469,217,776 | 432,222,953 | 386,809,746 | 255,020,565 | 78,625,102 | ||||||||||||||

Diluted common shares (3) | 469,246,265 | 432,545,625 | 386,809,746 | 255,020,565 | 78,625,102 | ||||||||||||||

Dividends declared per common share issued (4) | $ | 0.70500 | $ | 0.68500 | $ | 0.66875 | $ | 0.65843 | $ | 0.17480 | |||||||||

(1) As a result of the Merger completed on July 17, 2013, Operating Data includes the results of operations from the acquired properties for a full year in 2016, 2015 and 2014 and for less than half a year in 2013. | |||||||||||||||||||

(2) Includes gains, losses and results of operations from all property dispositions and from properties classified as held for sale at the end of the period for all periods prior to 2014. During 2015 and 2014, only those properties classified as held for sale as of December 31, 2013 were reported as discontinued operations. | |||||||||||||||||||

(3) Historical weighted average number of shares of common stock outstanding (basic and diluted) have been adjusted for the Merger Exchange Ratio. No potentially dilutive securities were included as their effect would be anti-dilutive on results from continuing operations. | |||||||||||||||||||

(4) Dividends declared per common share issued for the years ended December 31, 2013 and 2012 have been adjusted for the Merger. | |||||||||||||||||||

| Years Ended December 31, | |||||||||||||||||||

2016 (1) | 2015 (1) | 2014 (1) | 2013 (1) | 2012 | |||||||||||||||

| (Dollars in thousands) | |||||||||||||||||||

| Balance Sheet Data (end of period): | |||||||||||||||||||

| Gross investments, including related lease intangibles | $ | 8,247,654 | $ | 8,302,688 | $ | 8,043,497 | $ | 7,235,732 | $ | 3,654,925 | |||||||||

| Net investments | 7,272,655 | 7,425,719 | 7,316,694 | 6,743,439 | 3,119,608 | ||||||||||||||

| Cash and cash equivalents | 10,059 | 21,790 | 176,181 | 66,588 | 73,568 | ||||||||||||||

Total assets (3) | 7,677,971 | 7,891,039 | 7,964,230 | 7,207,775 | 3,245,938 | ||||||||||||||

Total debt, net (3) | 3,664,628 | 4,092,787 | 4,323,302 | 3,758,241 | 1,893,139 | ||||||||||||||

Total liabilities (3) | 3,995,863 | 4,429,165 | 4,652,568 | 4,093,034 | 1,992,495 | ||||||||||||||

Total stockholders' equity (2) | 3,682,108 | 3,461,874 | 3,311,662 | 3,114,741 | 1,253,443 | ||||||||||||||

| Other Data: | |||||||||||||||||||

FFO (4) | $ | 394,952 | $ | 354,686 | $ | 238,105 | $ | 139,487 | $ | 52,830 | |||||||||

AFFO (4) | $ | 412,999 | $ | 378,050 | $ | 322,400 | $ | 208,853 | $ | 119,248 | |||||||||

| Number of properties in investment portfolio | 2,615 | 2,629 | 2,509 | 2,186 | 1,207 | ||||||||||||||

| Owned properties occupancy at period end (based on number of properties) | 98 | % | 99 | % | 98 | % | 99 | % | 99 | % | |||||||||

| (Dollars in thousands) | Years Ended December 31, | |||||||||||||||||||||||||||||||||||||

| Years Ended December 31, | 2016 | 2015 | 2014 | 2013 | 2012 | |||||||||||||||||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | 2010 | (Dollars in thousands) | |||||||||||||||||||||||||||||||||

Net (loss) income attributable to common stockholders (1) | $ | (33,799 | ) | $ | 1,677 | $ | (76,296 | ) | $ | (63,879 | ) | $ | (86,552 | ) | ||||||||||||||||||||||||

Net income (loss) attributable to common stockholders (1) | $ | 97,446 | $ | 93,212 | $ | (36,945 | ) | $ | (1,616 | ) | $ | (76,296 | ) | |||||||||||||||||||||||||

| Add/(less): | ||||||||||||||||||||||||||||||||||||||

| Portfolio depreciation and amortization | ||||||||||||||||||||||||||||||||||||||

| Continuing operations | 247,587 | 163,874 | 104,929 | 103,086 | 103,237 | 261,799 | 260,257 | 247,587 | 163,874 | 104,929 | ||||||||||||||||||||||||||||

| Discontinued operations | — | 3,545 | 7,116 | 8,691 | 10,239 | — | — | — | 3,545 | 7,116 | ||||||||||||||||||||||||||||

| Portfolio impairment | ||||||||||||||||||||||||||||||||||||||

| Portfolio impairments | ||||||||||||||||||||||||||||||||||||||

| Continuing operations | 36,013 | 183 | 9,098 | 2,546 | 18,771 | 88,072 | 70,197 | 37,592 | 183 | 9,098 | ||||||||||||||||||||||||||||

| Discontinued operations | 417 | 7,134 | 4,634 | 16,586 | 24,462 | — | 34 | 417 | 9,587 | 4,634 | ||||||||||||||||||||||||||||

Realized (gain) loss on sales of real estate (2) | (13,728 | ) | (36,926 | ) | 3,349 | 2,736 | 391 | (52,365 | ) | (69,014 | ) | (10,546 | ) | (36,086 | ) | 3,349 | ||||||||||||||||||||||

| Total adjustments | 270,289 | 137,810 | 129,126 | 133,645 | 157,100 | 297,506 | 261,474 | 275,050 | 141,103 | 129,126 | ||||||||||||||||||||||||||||

| Funds from operations (FFO) attributable to common stockholders | $ | 236,490 | $ | 139,487 | $ | 52,830 | $ | 69,766 | $ | 70,548 | ||||||||||||||||||||||||||||

| FFO | $ | 394,952 | $ | 354,686 | $ | 238,105 | $ | 139,487 | $ | 52,830 | ||||||||||||||||||||||||||||

| Add/(less): | ||||||||||||||||||||||||||||||||||||||

| Loss (gain) on debt extinguishment | ||||||||||||||||||||||||||||||||||||||

| (Gain) loss on debt extinguishment | ||||||||||||||||||||||||||||||||||||||

| Continuing operations | 64,750 | 2,405 | 32,522 | — | — | (233 | ) | 3,162 | 64,750 | 2,405 | 32,522 | |||||||||||||||||||||||||||

| Discontinued operations | — | (1,028 | ) | — | — | — | — | — | — | (1,028 | ) | — | ||||||||||||||||||||||||||

| Restructuring charges | 6,341 | 7,056 | — | — | — | |||||||||||||||||||||||||||||||||

| Loss on derivative instruments related to term note extinguishment | — | — | 8,688 | 1,025 | — | 3,629 | — | — | — | 8,688 | ||||||||||||||||||||||||||||

| Expenses incurred to secure lenders’ consents to the IPO | — | — | 4,743 | 374 | — | — | — | — | — | 4,743 | ||||||||||||||||||||||||||||

| Expenses incurred to amend term note | — | — | — | 7,226 | — | — | — | — | — | — | ||||||||||||||||||||||||||||

| Litigation | — | — | — | 151 | 22,282 | — | — | — | — | — | ||||||||||||||||||||||||||||

Cole II Merger related costs (3) | — | — | — | 66,700 | — | |||||||||||||||||||||||||||||||||

| Master Trust Exchange Costs | — | — | 13,022 | 717 | — | |||||||||||||||||||||||||||||||||

| Real estate acquisition costs | 3,229 | 2,739 | 3,631 | 1,718 | 1,054 | |||||||||||||||||||||||||||||||||

| Non-cash interest expense | 15,380 | 10,367 | 5,175 | 8,840 | 16,495 | |||||||||||||||||||||||||||||||||

| Non-cash revenues | (26,333 | ) | (20,930 | ) | (16,732 | ) | (18,755 | ) | (3,015 | ) | ||||||||||||||||||||||||||||

| Accrued interest and fees on defaulted loans | 4,740 | 7,649 | 3,103 | — | — | |||||||||||||||||||||||||||||||||

Swap termination costs (4) | 1,724 | — | — | — | — | |||||||||||||||||||||||||||||||||

| Non-cash compensation expense | 9,570 | 13,321 | 11,346 | 8,769 | 5,931 | |||||||||||||||||||||||||||||||||

| Total adjustments to FFO | 18,047 | 23,364 | 84,295 | 69,366 | 66,418 | |||||||||||||||||||||||||||||||||

AFFO (8) | $ | 412,999 | $ | 378,050 | $ | 322,400 | $ | 208,853 | $ | 119,248 | ||||||||||||||||||||||||||||

| FFO per share of common stock | ||||||||||||||||||||||||||||||||||||||

Diluted (5) (6) | $ | 0.84 | $ | 0.82 | $ | 0.61 | $ | 0.54 | $ | 0.57 | ||||||||||||||||||||||||||||

| AFFO per share of common stock | ||||||||||||||||||||||||||||||||||||||

Diluted (5) (7) | $ | 0.88 | $ | 0.87 | $ | 0.83 | $ | 0.81 | $ | 1.14 | ||||||||||||||||||||||||||||

| Weighted average shares of common stock outstanding: | ||||||||||||||||||||||||||||||||||||||

| Basic | 469,217,776 | 432,222,953 | 386,809,746 | 255,020,565 | 78,625,102 | |||||||||||||||||||||||||||||||||

| Diluted | 469,246,265 | 432,545,625 | 387,585,580 | 255,210,757 | 112,509,283 | |||||||||||||||||||||||||||||||||

Cole II merger related costs (5) | — | 66,700 | — | — | — | ||||||||||||||

| Finance restructuring charges | 13,022 | 717 | — | — | — | ||||||||||||||

| Real estate acquisition costs | 3,631 | 1,718 | 1,054 | 553 | — | ||||||||||||||

| Non-cash interest expense | 5,175 | 8,840 | 16,495 | 22,704 | 19,554 | ||||||||||||||

| Non-cash revenues | (16,732 | ) | (18,755 | ) | (3,015 | ) | (2,225 | ) | (2,288 | ) | |||||||||

| Accrued interest on defaulted loans | 3,103 | — | — | — | — | ||||||||||||||

| Non-cash compensation expense | 11,346 | 8,769 | 5,931 | — | — | ||||||||||||||

| Other expense (income) | — | — | — | — | 3,110 | ||||||||||||||

| Total adjustments to FFO | 84,295 | 69,366 | 66,418 | 29,808 | 42,658 | ||||||||||||||

| Adjusted funds from operations (AFFO) attributable to common stockholders | $ | 320,785 | $ | 208,853 | $ | 119,248 | $ | 99,574 | $ | 113,206 | |||||||||

| FFO per share of common stock | |||||||||||||||||||

Diluted (3) | $ | 0.61 | $ | 0.54 | $ | 0.57 | $ | 1.42 | $ | 1.43 | |||||||||

| AFFO per share of common stock | |||||||||||||||||||

Diluted (4) | $ | 0.82 | $ | 0.81 | $ | 1.14 | $ | 2.02 | $ | 2.30 | |||||||||

| Weighted average shares of common stock outstanding: | |||||||||||||||||||

| Basic | 386,809,746 | 255,020,565 | 78,625,102 | 49,265,701 | 49,265,701 | ||||||||||||||

| Diluted | 387,585,580 | 255,210,757 | 112,509,283 | 49,265,701 | 49,265,701 | ||||||||||||||

(1) Amount is net of distributions paid to preferred stockholders. | |||||||||||||||||||

(2) Includes amounts related to discontinued operations. | |||||||||||||||||||

(3) FFO per share for the years ended December 31, 2014 and 2013 deducts dividends paid to participating stockholders of $1,099 and $1,291, respectively, in its computation. Earnings per share for 2012 adds back cash and non-cash interest savings under the "if converted method" of $11,578 for assumed conversion of the term note in the computation of diluted earnings per share. | |||||||||||||||||||

(4) AFFO per share for the years ended December 31, 2014 and 2013 deducts dividends paid to participating stockholders of $1,099 and $1,291, respectively, in its computation. Earnings per share for 2012 adds back cash interest savings under the "if converted method" of $9,020 for assumed conversion of the term note in the computation of diluted earnings per share. | |||||||||||||||||||

(5) Includes $10.1 million of interest expense charges related to the Merger. | |||||||||||||||||||

| Contractual rent from date of rejection through either sale or December 31, 2016 | $ | 1.3 | ||

| Three months of prepaid rent for the 3 stores subsequently sold | 0.5 | |||

| Total included in AFFO | $ | 1.8 | ||

| December 31, | |||||||

| 2016 | 2015 | ||||||

| (in thousands) | |||||||

| Revolving credit facilities | $ | 86,000 | $ | — | |||

| Term loan, net | 418,471 | 322,902 | |||||

| Senior unsecured notes | 295,112 | — | |||||

| Mortgages and notes payable, net | 2,162,403 | 3,079,787 | |||||

| Convertible notes, net | 702,642 | 690,098 | |||||

| 3,664,628 | 4,092,787 | ||||||

| Add/(less): | |||||||

| Unamortized debt discount, net | 52,894 | 52,203 | |||||

| Unamortized deferred financing costs | 37,111 | 41,577 | |||||

| Cash and cash equivalents | (10,059 | ) | (21,790 | ) | |||

| Cash reserves on deposit with lenders as additional security classified as other assets | (11,757 | ) | (24,660 | ) | |||

| Total adjustments | 68,189 | 47,330 | |||||

Adjusted Debt (1) | $ | 3,732,817 | $ | 4,140,117 | |||

| Three Months Ended December 31, | |||||||

| 2016 | 2015 | ||||||

| (Dollars in thousands) | |||||||

| Net income attributable to common stockholders | $ | 988 | $ | 6,301 | |||

Add/(less): (2) | |||||||

| Interest | 46,744 | 54,147 | |||||

| Depreciation and amortization | 68,049 | 65,173 | |||||

| Income tax (benefit) expense | 33 | (106 | ) | ||||

| Total adjustments | 114,826 | 119,214 | |||||

| EBITDA | $ | 115,814 | $ | 125,515 | |||

Add/(less): (2) | |||||||

| Restructuring charges | 615 | 6,956 | |||||

| Other non-routine costs in G&A associated with headquarter relocation | 187 | — | |||||

| Real estate acquisition costs | 1,137 | 617 | |||||

| Impairments | 46,379 | 13,691 | |||||

| Realized gain on sales of real estate | (13,144 | ) | (2,131 | ) | |||

| Loss on debt extinguishment | 93 | 5,651 | |||||

| Total adjustments to EBITDA | 35,267 | 24,784 | |||||

Adjusted EBITDA (3) | $ | 151,081 | $ | 150,299 | |||

Annualized Adjusted EBITDA (4) | $ | 604,324 | $ | 601,196 | |||

Adjusted Debt / Annualized Adjusted EBITDA (5) | 6.2 | 6.9 | |||||

| December 31, | ||||||||

| 2014 | 2013 | |||||||

| Revolving credit facilities | $ | 15,181 | $ | 35,120 | ||||

| Mortgages and notes payable, net | 3,658,496 | 3,743,098 | ||||||

| Convertible Notes | 695,957 | — | ||||||

| 4,369,634 | 3,778,218 | |||||||

| Add/(less): | ||||||||

| Preferred stock | — | — | ||||||

| Unamortized debt discount/(premium) | 51,586 | (1,669 | ) | |||||

| Cash and cash equivalents | (176,181 | ) | (66,588 | ) | ||||

| Cash collateral deposits for the benefit of lenders classified as other assets | (29,483 | ) | (16,927 | ) | ||||

| Total adjustments | (154,078 | ) | (85,184 | ) | ||||

Adjusted Debt (1) | $ | 4,215,556 | $ | 3,693,034 | ||||

| Three Months Ended December 31, | ||||||||

| 2014 | 2013 | |||||||

| Net income (loss) attributable to common stockholders | $ | 34,113 | $ | 43,586 | ||||

| Add/(less): | ||||||||

| Interest | 56,144 | 52,890 | ||||||

Depreciation and amortization (2) | 63,380 | 59,263 | ||||||

| Income tax expense | 87 | 168 | ||||||

| Total adjustments | 119,611 | 112,321 | ||||||

| Earnings before interest, income tax, and depreciation and amortization expenses ("EBITDA") | $ | 153,724 | $ | 155,907 | ||||

Add/(less): (2) | ||||||||

| Merger related costs | — | 16 | ||||||

| Finance restructuring costs | — | 717 | ||||||

| Real estate acquisition costs | 1,259 | 1,030 | ||||||

| Impairments | (5,631 | ) | 1,282 | |||||

| Losses / (gains) on sales of assets | (11,557 | ) | (35,700 | ) | ||||

| Losses on debt extinguishment | 254 | 2,405 | ||||||

| Total adjustments to EBITDA | (15,675 | ) | (30,250 | ) | ||||

Adjusted EBITDA (3) | $ | 138,049 | $ | 125,657 | ||||

Annualized Adjusted EBITDA (4) | $ | 552,196 | $ | 502,628 | ||||

Leverage (5) (Adjusted Debt / Annualized Adjusted EBITDA) | 7.6 | 7.3 | ||||||

(1) Adjusted Debt represents interest bearing debt (reported in accordance with GAAP) adjusted to include preferred stock and exclude unamortized debt discount, as further reduced for cash and cash equivalents and cash collateral deposits retained by lenders. We believe that including preferred stock in Adjusted Debt is appropriate because it is an equity security that has properties of a debt instrument not possessed by common stock. Additionally, by excluding unamortized debt discount, cash and cash equivalents, and cash collateral deposits retained by lenders, the result provides an estimate of the contractual amount of borrowed capital to be repaid which we believe is a beneficial disclosure to investors. | ||||||||

(2) Adjustments include all amounts charged to continuing and discontinued operations. | ||||||||

| ◦ | Issued |

| ◦ |

| ◦ |

| ◦ |

| ◦ |

| ◦ | Extinguished |

| ◦ | Unencumbered assets totaled $4.8 billion at December 31, 2016, or approximately 58.8% of |

| Years Ended December 31, | Years Ended December 31, | ||||||||||||||||||||||||||||

| 2014 | 2013 | Change | % | 2016 | 2015 | Change | % Change | ||||||||||||||||||||||

| (in thousands) | (in thousands) | ||||||||||||||||||||||||||||

| Revenues: | |||||||||||||||||||||||||||||

| Rentals | $ | 574,456 | $ | 404,402 | $ | 170,054 | 42.1 | % | $ | 648,363 | $ | 634,151 | $ | 14,212 | 2.2 | % | |||||||||||||

| Interest income on loans receivable | 7,239 | 5,928 | 1,311 | 22.1 | % | 5,253 | 6,948 | (1,695 | ) | (24.4 | )% | ||||||||||||||||||

| Earned income from direct financing leases | 3,343 | 1,572 | 1,771 | 112.7 | % | 2,742 | 3,024 | (282 | ) | (9.3 | )% | ||||||||||||||||||

| Tenant reimbursement income | 13,085 | 5,637 | 7,448 | 132.1 | % | 14,125 | 15,952 | (1,827 | ) | (11.5 | )% | ||||||||||||||||||

| Interest income and other | 4,748 | 1,928 | 2,820 | 146.3 | % | ||||||||||||||||||||||||

| Other income | 15,491 | 7,260 | 8,231 | NM | |||||||||||||||||||||||||

| Total revenues | 602,871 | 419,467 | 183,404 | 43.7 | % | 685,974 | 667,335 | 18,639 | 2.8 | % | |||||||||||||||||||

| Expenses: | |||||||||||||||||||||||||||||

| General and administrative | 44,252 | 35,146 | 9,106 | 25.9 | % | 52,615 | 47,730 | 4,885 | 10.2 | % | |||||||||||||||||||

| Finance restructuring charges | 13,022 | 717 | 12,305 | NM | |||||||||||||||||||||||||

| Merger costs | — | 56,644 | (56,644 | ) | NM | ||||||||||||||||||||||||

| Restructuring charges | 6,341 | 7,056 | (715 | ) | (10.1 | )% | |||||||||||||||||||||||

| Property costs | 23,383 | 11,760 | 11,623 | 98.8 | % | 30,839 | 27,715 | 3,124 | 11.3 | % | |||||||||||||||||||

| Real estate acquisition costs | 3,631 | 1,718 | 1,913 | 111.4 | % | 3,229 | 2,739 | 490 | 17.9 | % | |||||||||||||||||||

| Interest | 220,070 | 179,267 | 40,803 | 22.8 | % | 196,586 | 222,901 | (26,315 | ) | (11.8 | )% | ||||||||||||||||||

| Depreciation and amortization | 247,966 | 164,054 | 83,912 | 51.1 | % | 262,276 | 260,633 | 1,643 | 0.6 | % | |||||||||||||||||||

| Impairment (recoveries) | 36,019 | (185 | ) | 36,204 | NM | ||||||||||||||||||||||||

| Impairment | 88,275 | 70,695 | 17,580 | 24.9 | % | ||||||||||||||||||||||||

| Total expenses | 588,343 | 449,121 | 139,222 | 31.0 | % | 640,161 | 639,469 | 692 | 0.1 | % | |||||||||||||||||||

| Income (loss) from continuing operations before other expense and income tax expense | 14,528 | (29,654 | ) | 44,182 | 149.0 | % | |||||||||||||||||||||||

| Other expense: | |||||||||||||||||||||||||||||

| Loss on debt extinguishment | (64,750 | ) | (2,405 | ) | (62,345 | ) | NM | ||||||||||||||||||||||

| Total other expense | (64,750 | ) | (2,405 | ) | (62,345 | ) | NM | ||||||||||||||||||||||

| Loss from continuing operations before income tax expense | (50,222 | ) | (32,059 | ) | (18,163 | ) | (56.7 | )% | |||||||||||||||||||||

| Income from continuing operations before other income (expense) and income tax expense | 45,813 | 27,866 | 17,947 | 64.4 | % | ||||||||||||||||||||||||

| Other income (expense): | |||||||||||||||||||||||||||||

| Gain (loss) on debt extinguishment | 233 | (3,162 | ) | 3,395 | NM | ||||||||||||||||||||||||

| Total other income (expense) | 233 | (3,162 | ) | 3,395 | NM | ||||||||||||||||||||||||

| Income from continuing operations before income tax expense | 46,046 | 24,704 | 21,342 | NM | |||||||||||||||||||||||||

| Income tax expense | 673 | 1,113 | (440 | ) | (39.5 | )% | (965 | ) | (601 | ) | (364 | ) | (60.6 | )% | |||||||||||||||

| Loss from continuing operations | $ | (50,895 | ) | $ | (33,172 | ) | $ | (17,723 | ) | (53.4 | )% | ||||||||||||||||||

| Income from continuing operations | $ | 45,081 | $ | 24,103 | $ | 20,978 | NM | ||||||||||||||||||||||

| Gain on disposition of assets | $ | 52,365 | $ | 68,421 | $ | (16,056 | ) | (23.5 | )% | ||||||||||||||||||||

| Years Ended December 31, | |||||||

| 2014 | 2013 | ||||||

| (in thousands) | |||||||

Interest expense – revolving credit facilities (1) | $ | 3,597 | $ | 3,037 | |||

| Interest expense – mortgages and notes payable | 196,246 | 157,903 | |||||

| Interest expense – Convertible Notes | 15,046 | — | |||||

| Interest expense – other | 6 | 475 | |||||

Amortization of deferred financing costs (2) | 5,899 | 13,188 | |||||

| Amortization of net losses related to interest rate swaps | 125 | 11 | |||||

| Amortization of debt (premium)/discount, net | (849 | ) | 4,653 | ||||

| Total interest expense | $ | 220,070 | $ | 179,267 | |||

(1) Includes interest expense associated with non-utilization fees of approximately $1.2 million and $0.7 million for the years ended December 31, 2014 and 2013, respectively. | |||||||

(2) Includes $9.5 million arising from financing commitments related to the Merger for the year ended December 31, 2013. | |||||||

| Years Ended December 31, | |||||||

| 2016 | 2015 | ||||||

| (in thousands) | |||||||

| Interest expense – Revolving Credit Facilities (1) | $ | 3,314 | $ | 2,698 | |||

| Interest expense – Term Loan | 5,218 | 888 | |||||

| Interest expense – mortgages and notes payable | 143,233 | 184,439 | |||||

Interest expense – Convertible Notes (2) | 24,509 | 24,509 | |||||

| Interest expense – Unsecured Senior Notes | 4,932 | — | |||||

| Non-cash interest expense: | |||||||

| Amortization of deferred financing costs | 9,070 | 7,937 | |||||

| Amortization of net losses related to interest rate swaps | 93 | 108 | |||||

| Amortization of debt discount/(premium), net | 6,217 | 2,322 | |||||

| Total interest expense | $ | 196,586 | $ | 222,901 | |||

| Years Ended December 31, | Years Ended December 31, | |||||||||||||

| 2014 | 2013 | 2016 | 2015 | |||||||||||

| (in thousands) | (in thousands) | |||||||||||||

| Depreciation of real estate assets | $ | 194,383 | $ | 130,285 | $ | 215,443 | $ | 210,395 | ||||||

| Other depreciation | 379 | 180 | 475 | 375 | ||||||||||

| Amortization of lease intangibles | 53,204 | 33,589 | 46,358 | 49,863 | ||||||||||

| Total depreciation and amortization | $ | 247,966 | $ | 164,054 | $ | 262,276 | $ | 260,633 | ||||||

| Years Ended December 31, | |||||||

| 2016 | 2015 | ||||||

| (in thousands) | |||||||

| Real estate and intangible asset impairment | $ | 80,390 | $ | 68,531 | |||

| Write-off of lease intangibles due to lease terminations, net | 7,683 | 1,666 | |||||

| Loans receivable impairment | 176 | 324 | |||||

| Total impairments from real estate investment net assets | 88,249 | 70,521 | |||||

| Other impairment | 26 | 174 | |||||

| Total impairment loss | $ | 88,275 | $ | 70,695 | |||

| Years Ended December 31, | ||||||||||||||

| 2015 | 2014 | Change | % Change | |||||||||||

| (in thousands) | ||||||||||||||

| Revenues: | ||||||||||||||

| Rentals | $ | 634,151 | $ | 574,456 | $ | 59,695 | 10.4 | % | ||||||

| Interest income on loans receivable | 6,948 | 7,239 | (291 | ) | (4.0 | )% | ||||||||

| Earned income from direct financing leases | 3,024 | 3,343 | (319 | ) | (9.5 | )% | ||||||||

| Tenant reimbursement income | 15,952 | 13,085 | 2,867 | 21.9 | % | |||||||||

| Other income | 7,260 | 4,748 | 2,512 | 52.9 | % | |||||||||

| Total revenues | 667,335 | 602,871 | 64,464 | 10.7 | % | |||||||||

| Expenses: | ||||||||||||||

| General and administrative | 47,730 | 42,637 | 5,093 | 11.9 | % | |||||||||

| Restructuring charges | 7,056 | — | 7,056 | NM | ||||||||||

| Finance restructuring costs | — | 13,022 | (13,022 | ) | (100.0 | )% | ||||||||

| Property costs | 27,715 | 23,383 | 4,332 | 18.5 | % | |||||||||

| Real estate acquisition costs | 2,739 | 3,631 | (892 | ) | (24.6 | )% | ||||||||

| Interest | 222,901 | 220,070 | 2,831 | 1.3 | % | |||||||||

| Depreciation and amortization | 260,633 | 247,966 | 12,667 | 5.1 | % | |||||||||

| Impairment | 70,695 | 37,598 | 33,097 | 88.0 | % | |||||||||

| Total expenses | 639,469 | 588,307 | 51,162 | 8.7 | % | |||||||||

| Income from continuing operations before other expense and income tax expense | 27,866 | 14,564 | 13,302 | 91.3 | % | |||||||||

| Other expense: | ||||||||||||||

| Loss on debt extinguishment | (3,162 | ) | (64,750 | ) | 61,588 | �� | 95.1 | % | ||||||

| Total other expense | (3,162 | ) | (64,750 | ) | 61,588 | 95.1 | % | |||||||

| Income (loss) from continuing operations before income tax expense | 24,704 | (50,186 | ) | 74,890 | NM | |||||||||

| Income tax expense | (601 | ) | (673 | ) | 72 | 10.7 | % | |||||||

| Income (loss) from continuing operations | $ | 24,103 | $ | (50,859 | ) | $ | 74,962 | NM | ||||||

| Gain on disposition of assets | $ | 68,421 | $ | 10,221 | $ | 58,200 | NM | |||||||

| Years Ended December 31, | |||||||

| 2015 | 2014 | ||||||

| (in thousands) | |||||||

| Interest expense – Revolving Credit Facilities (1) | $ | 2,698 | $ | 3,597 | |||

| Interest expense – Term Loan | 888 | — | |||||

| Interest expense – mortgages and notes payable | 184,439 | 196,246 | |||||

Interest expense – Convertible Notes (2) | 24,509 | 15,046 | |||||

| Interest expense – other | — | 6 | |||||

| Non-cash interest expense: | |||||||

| Amortization of deferred financing costs | 7,937 | 5,899 | |||||

| Amortization of net losses related to interest rate swaps | 108 | 125 | |||||

| Amortization of debt discount/(premium), net | 2,322 | (849 | ) | ||||

| Total interest expense | $ | 222,901 | $ | 220,070 | |||

| Years Ended December 31, | |||||||

| 2015 | 2014 | ||||||

| (in thousands) | |||||||

| Depreciation of real estate assets | $ | 210,395 | $ | 194,383 | |||

| Other depreciation | 375 | 379 | |||||

| Amortization of lease intangibles | 49,863 | 53,204 | |||||

| Total depreciation and amortization | $ | 260,633 | $ | 247,966 | |||

| Years Ended December 31, | Years Ended December 31, | |||||||||||||

| 2014 | 2013 | 2015 | 2014 | |||||||||||

| (in thousands) | (in thousands) | |||||||||||||

| Real estate and intangible asset impairment | $ | 40,311 | $ | 182 | $ | 68,531 | $ | 41,890 | ||||||

| Write-off of lease intangibles due to lease terminations, net | (4,820 | ) | — | 1,666 | (4,820 | ) | ||||||||

| Loan receivable impairment recovery | — | (367 | ) | |||||||||||

| Loans receivable impairment | 324 | — | ||||||||||||

| Total impairments from real estate investment net assets | 70,521 | 37,070 | ||||||||||||

| Other impairment | 528 | — | 174 | 528 | ||||||||||

| Total impairment loss (recovery) | $ | 36,019 | $ | (185 | ) | |||||||||

| Total impairment loss | $ | 70,695 | $ | 37,598 | ||||||||||

| Years Ended December 31, | |||||||||||||||

| 2013 | 2012 | Change | % | ||||||||||||

| (in thousands) | |||||||||||||||

| Revenues: | |||||||||||||||

| Rentals | $ | 404,402 | $ | 266,567 | $ | 137,835 | 51.7 | % | |||||||

| Interest income on loans receivable | 5,928 | 5,696 | 232 | 4.1 | % | ||||||||||

| Earned income from direct financing leases | 1,572 | — | 1,572 | NM | |||||||||||

| Tenant reimbursement income | 5,637 | — | 5,637 | NM | |||||||||||

| Interest income and other | 1,928 | 852 | 1,076 | 126.3 | % | ||||||||||

| Total revenues | 419,467 | 273,115 | 146,352 | 53.6 | % | ||||||||||

| Expenses: | |||||||||||||||

| General and administrative | 35,146 | 36,252 | (1,106 | ) | (3.1 | )% | |||||||||

| Finance restructuring charges | 717 | — | 717 | NM | |||||||||||

| Merger costs | 56,644 | — | 56,644 | NM | |||||||||||

| Property costs | 11,760 | 5,176 | 6,584 | 127.2 | % | ||||||||||

| Real estate acquisition costs | 1,718 | 1,054 | 664 | 63.0 | % | ||||||||||

| Interest | 179,267 | 156,220 | 23,047 | 14.8 | % | ||||||||||

| Depreciation and amortization | 164,054 | 104,984 | 59,070 | 56.3 | % | ||||||||||

| Impairment (recoveries) | (185 | ) | 8,918 | (9,103 | ) | (102.1 | )% | ||||||||

| Total expenses | 449,121 | 312,604 | 136,517 | 43.7 | % | ||||||||||

| Loss from continuing operations before other expense and income tax expense | (29,654 | ) | (39,489 | ) | 9,835 | 24.9 | % | ||||||||

| Other expense: | |||||||||||||||

| Loss on debt extinguishment | (2,405 | ) | (32,522 | ) | 30,117 | 92.6 | % | ||||||||

| Total other expense | (2,405 | ) | (32,522 | ) | 30,117 | 92.6 | % | ||||||||

| Loss from continuing operations before income tax expense | (32,059 | ) | (72,011 | ) | 39,952 | 55.5 | % | ||||||||

| Income tax expense | 1,113 | 504 | 609 | 120.8 | % | ||||||||||

| Loss from continuing operations | (33,172 | ) | (72,515 | ) | 39,343 | 54.3 | % | ||||||||

| Years Ended December 31, | |||||||

| 2013 | 2012 | ||||||

| (in thousands) | |||||||

| Interest expense – term note payable | $ | — | $ | 19,925 | |||

Interest expense – revolving credit facilities (1) | 3,037 | 108 | |||||

| Interest expense – mortgages and notes payable | 157,903 | 119,196 | |||||

| Interest expense – other | 475 | 10 | |||||

Amortization of deferred financing costs (2) | 13,188 | 2,819 | |||||

| Amortization of net losses related to interest rate swap | 11 | 3,415 | |||||

| Amortization of debt (premium) or discount, net | 4,653 | 10,747 | |||||

| Total interest expense | $ | 179,267 | $ | 156,220 | |||

(1) Includes interest expense associated with non-utilization fees of approximately $0.7 million and $0.1 million for the years ended December 31, 2013 and 2012, respectively. | |||||||

(2) Includes $9.5 million arising from financing commitments related to the Merger for the year ended December 31, 2013. | |||||||

| Years Ended December 31, | |||||||

| 2013 | 2012 | ||||||

| (in thousands) | |||||||

| Depreciation of real estate assets | $ | 130,285 | $ | 86,905 | |||

| Other depreciation | 180 | 54 | |||||

| Amortization of lease intangibles | 33,589 | 18,025 | |||||

| $ | 164,054 | $ | 104,984 | ||||

| Years Ended December 31, | |||||||

| 2013 | 2012 | ||||||

| (in thousands) | |||||||

| Real estate and intangible asset impairment | $ | 182 | $ | 7,267 | |||

| Write-off of lease intangibles due to lease terminations | — | 1,831 | |||||

| Loan receivable impairment (recovery) expense | (367 | ) | (180 | ) | |||

| Total impairment (recovery) loss | $ | (185 | ) | $ | 8,918 | ||

Stated Rates (1) | Remaining Term | December 31, 2016 | December 31, 2015 | |||||||||

| (in Years) | (in Thousands) | |||||||||||

| Series 2014-1 Class A1 | 5.1 | % | 3.5 | $ | 53,919 | $ | 65,027 | |||||

| Series 2014-1 Class A2 | 5.4 | % | 3.5 | 253,300 | 253,300 | |||||||

| Series 2014-2 | 5.8 | % | 4.2 | 226,283 | 229,674 | |||||||

| Series 2014-3 | 5.7 | % | 5.2 | 311,820 | 312,276 | |||||||

| Series 2014-4 Class A1 | 3.5 | % | 3.1 | 150,000 | 150,000 | |||||||

| Series 2014-4 Class A2 | 4.6 | % | 13.1 | 360,000 | 360,000 | |||||||

| Total Master Trust 2014 notes | 5.1 | % | 6.5 | 1,355,322 | 1,370,277 | |||||||

| Series 2013-1 Class A | 3.9 | % | 2.0 | 125,000 | 125,000 | |||||||

| Series 2013-2 Class A | 5.3 | % | 7.0 | 192,384 | 196,817 | |||||||

| Total Master Trust 2013 notes | 4.7 | % | 5.0 | 317,384 | 321,817 | |||||||

| Total Master Trust Notes | 1,672,706 | 1,692,094 | ||||||||||

| Debt discount, net | (18,787 | ) | (22,909 | ) | ||||||||

| Deferred financing costs, net | (16,376 | ) | (19,345 | ) | ||||||||

| Total Master Trust Notes, net | $ | 1,637,543 | $ | 1,649,840 | ||||||||

| Industry | Properties | Net Book Value | Monthly Base Rent | Principal Outstanding | Monthly Debt Service | Stated Interest Rate | Maturity Date | ||||||||||||||||

| Building Materials | 109 | $ | 199,022 | $ | 1,493 | $ | 139,389 | $ | 916 | 6.17 | % | May 5, 2017 | |||||||||||

| Year of Maturity | Number of Loans | Number of Properties | Stated Interest Rate Range | Weighted Average Stated Rate | Scheduled Principal | Balloon | Total | |||||||||||||||

| 2017 | 18 | 15 | 5.51%-6.52% | 5.72 | % | $ | 4,222 | $ | 161,373 | $ | 165,595 | |||||||||||

| 2018 | 4 | 10 | 3.90%-4.65% | 4.03 | % | 3,853 | 57,779 | 61,632 | ||||||||||||||

| 2019 | 1 | 5 | 4.61%-4.61% | 3.32 | % | 3,905 | 10,000 | 13,905 | ||||||||||||||

| 2020 | — | — | — | — | 4,100 | — | 4,100 | |||||||||||||||

| 2021 | — | — | — | — | 4,365 | — | 4,365 | |||||||||||||||

| Thereafter | 6 | 100 | 4.67%-6.00% | 5.77 | % | 11,891 | 240,380 | 252,271 | ||||||||||||||

| Total | 29 | 130 | 5.37 | % | 32,336 | 469,532 | 501,868 | |||||||||||||||

| Industry | Properties | Net Book Value | Monthly Base Rent | Outstanding Principal | Restricted Cash (3) | Stated Rate | Default Rate | Accrued Interest | |||||||||||||||||||||

| Drug Stores / Pharmacies | 1 | $ | 1,032 | $ | — | $ | 1,247 | $ | 78 | 5.67 | % | 9.67 | % | $ | 61 | (1) | |||||||||||||

| Home Furnishings | 1 | 3,315 | 36 | 17,026 | 3,537 | 6.88 | % | 10.88 | % | 1,168 | (1) | ||||||||||||||||||

| Sporting Goods | 1 | 3,375 | — | 4,133 | 609 | 5.52 | % | 9.52 | % | 260 | (1) | ||||||||||||||||||

| Manufacturing | 9 | 39,034 | 83 | 53,184 | 9,497 | 5.85 | % | 9.85 | % | 1,614 | (1) | ||||||||||||||||||

| 12 | $46,756 | $ | 119 | $ | 75,590 | $ | 13,721 | 6.06 | % | (2) | 10.06 | % | (2) | $ | 3,103 | ||||||||||||||

(1) Interest accrued or capitalized to principal that remains unpaid. | |||||||||||||||||||||||||||||

(2) Weighted average interest rate. | |||||||||||||||||||||||||||||

(3) Represents restricted cash controlled by the lender that may be applied to reduce the outstanding principal balance. | |||||||||||||||||||||||||||||

| Industry | Properties | Net Book Value | Monthly Base Rent | Pre-Default Outstanding Principal | Capitalized Interest (1) | Total Debt Outstanding | Restricted Cash (2) | Stated Rate | Default Rate | Accrued Interest (1) | ||||||||||||||||||||||||||

| Sporting Goods | 1 | $ | 6,351 | $ | — | $ | 6,321 | $ | 30 | $ | 6,351 | $ | 376 | 5.62 | % | 10.62 | % | $ | 58 | |||||||||||||||||

| Manufacturing | 3 | 20,206 | — | 10,730 | 9,476 | 20,206 | — | 5.85 | % | 9.85 | % | 216 | ||||||||||||||||||||||||

| 4 | $ | 26,557 | $ | — | $ | 17,051 | $ | 9,506 | $ | 26,557 | $ | 376 | 5.80 | % | 10.04 | % | $ | 274 | ||||||||||||||||||

Scheduled Principal | Balloon Payment | Total | |||||||||

| 2015 | $ | 31,552 | $ | 321,372 | $ | 352,924 | |||||

| 2016 | 30,167 | 289,045 | 319,212 | ||||||||

| 2017 | 29,667 | 839,977 | 869,644 | ||||||||

| 2018 | 43,750 | 248,851 | 292,601 | ||||||||

| 2019 | 45,771 | 452,000 | 497,771 | ||||||||

| Thereafter | 289,752 | 1,799,316 | 2,089,068 | ||||||||

| $ | 470,659 | $ | 3,950,561 | $ | 4,421,220 | ||||||

| Total | 2017 | 2018 | 2019 | 2020 | 2021 | Thereafter | |||||||||||||||||||||

| Term Loan | $ | 420,000 | $ | — | $ | 420,000 | $ | — | $ | — | $ | — | $ | — | |||||||||||||

| 2015 Credit Facility | 86,000 | — | — | 86,000 | — | — | — | ||||||||||||||||||||

| Master Trust Notes | 1,672,706 | 21,893 | 163,262 | 40,420 | 448,202 | 236,046 | 762,883 | ||||||||||||||||||||

CMBS - fixed-rate (1) | 528,427 | 192,154 | 61,632 | 13,905 | 4,100 | 4,365 | 252,271 | ||||||||||||||||||||

| Convertible Notes | 747,500 | — | — | 402,500 | — | 345,000 | — | ||||||||||||||||||||

| Unsecured Senior Notes | 300,000 | — | — | — | — | — | 300,000 | ||||||||||||||||||||

| $ | 3,754,633 | $ | 214,047 | $ | 644,894 | $ | 542,825 | $ | 452,302 | $ | 585,411 | $ | 1,315,154 | ||||||||||||||

| Payment due by period | Payment due by period | |||||||||||||||||||||||||||||||||||||||

| More than | More than | |||||||||||||||||||||||||||||||||||||||

| Less than 1 | 1-3 years | 3-5 years | 5 years | Less than 1 | 1-3 years | 3-5 years | 5 years | |||||||||||||||||||||||||||||||||

| Contractual Obligations | Total | Year (2015) | (2016-2017) | (2018-2019) | (after 2019) | Total | Year (2017) | (2018-2019) | (2020-2021) | (after 2021) | ||||||||||||||||||||||||||||||

| Debt - Principal | $ | 4,421,220 | $ | 352,924 | $ | 1,188,856 | $ | 790,372 | $ | 2,089,068 | $ | 3,754,633 | $ | 214,047 | $ | 1,187,719 | $ | 1,037,713 | $ | 1,315,154 | ||||||||||||||||||||

Debt - Interest (1) | 1,077,028 | 211,465 | 351,678 | 242,257 | 271,628 | |||||||||||||||||||||||||||||||||||

Debt - Interest (1) (3) | 796,059 | 158,651 | 273,111 | 180,096 | 184,201 | |||||||||||||||||||||||||||||||||||

Acquisitions Under Contract (2) | 288,738 | 288,738 | — | — | — | 45,598 | 45,598 | — | — | — | ||||||||||||||||||||||||||||||

| Capital Improvements | 4,235 | 4,235 | — | — | — | 53,085 | 52,759 | 326 | — | — | ||||||||||||||||||||||||||||||

| Operating Lease Obligations | 23,979 | 1,743 | 3,584 | 3,814 | 14,838 | 38,918 | 2,912 | 6,047 | 6,009 | 23,950 | ||||||||||||||||||||||||||||||

| Total | $ | 5,815,200 | $ | 859,105 | $ | 1,544,118 | $ | 1,036,443 | $ | 2,375,534 | $ | 4,688,293 | $ | 473,967 | $ | 1,467,203 | $ | 1,223,818 | $ | 1,523,305 | ||||||||||||||||||||

(1) Excludes interest on defaulted mortgage loans. | ||||||||||||||||||||||||||||||||||||||||

(2) Contracts contain standard cancellation clauses contingent on results of due diligence. | ||||||||||||||||||||||||||||||||||||||||

| Years Ended | |||||||||||

| December 31, | |||||||||||

| 2016 | 2015 | Change | |||||||||

| Net cash provided by operating activities | $ | 361,409 | $ | 371,986 | $ | (10,577 | ) | ||||

| Net cash used in investing activities | (117,251 | ) | (385,696 | ) | 268,445 | ||||||

| Net cash used in financing activities | (255,889 | ) | (140,681 | ) | (115,208 | ) | |||||

| Net (decrease) increase in cash and cash equivalents | $ | (11,731 | ) | $ | (154,391 | ) | $ | 142,660 | |||

| Years Ended | |||||||||||

| December 31, | |||||||||||

| 2015 | 2014 | Change | |||||||||

| Net cash provided by operating activities | $ | 371,986 | $ | 218,571 | $ | 153,415 | |||||

| Net cash used in investing activities | (385,696 | ) | (878,030 | ) | 492,334 | ||||||

| Net cash provided by financing activities | (140,681 | ) | 769,052 | (909,733 | ) | ||||||

| Net increase (decrease) in cash and cash equivalents | $ | (154,391 | ) | $ | 109,593 | $ | (263,984 | ) | |||

| Carrying Value | Estimated Fair Value | ||||||

| Revolving credit facilities | $ | 15,181 | $ | 15,254 | |||

| Mortgages and notes payable, net | 3,658,496 | 3,899,950 | |||||

Convertible Notes, net (1) | 695,957 | 729,231 | |||||

(1) The carrying value of the Convertible Notes is net of an embedded conversion premium totaling $51.5 million. | |||||||

| Carrying Value | Estimated Fair Value | ||||||

| 2015 Credit Facility | $ | 86,000 | $ | 87,718 | |||

Term Loan, net (1) | 418,471 | 428,441 | |||||

Senior Unsecured Notes, net (1) | 295,112 | 283,473 | |||||

Mortgages and notes payable, net (1) | 2,162,403 | 2,282,142 | |||||

Convertible Notes, net (1) | 702,642 | 784,175 | |||||

| December 31, 2014 | December 31, 2013 | December 31, 2016 | December 31, 2015 | |||||||||||

| Assets | ||||||||||||||

| Investments: | ||||||||||||||

| Real estate investments: | ||||||||||||||

| Land and improvements | $ | 2,614,630 | $ | 2,330,510 | $ | 2,704,010 | $ | 2,710,888 | ||||||

| Buildings and improvements | 4,579,166 | 4,188,783 | 4,775,221 | 4,816,481 | ||||||||||

| Total real estate investments | 7,193,796 | 6,519,293 | 7,479,231 | 7,527,369 | ||||||||||

| Less: accumulated depreciation | (752,210 | ) | (590,067 | ) | (940,005 | ) | (860,954 | ) | ||||||

| 6,441,586 | 5,929,226 | 6,539,226 | 6,666,415 | |||||||||||

| Loans receivable, net | 109,425 | 117,721 | 66,578 | 104,003 | ||||||||||

| Intangible lease assets, net | 590,073 | 618,121 | 470,276 | 526,718 | ||||||||||

| Real estate assets under direct financing leases, net | 56,564 | 58,760 | 36,005 | 44,324 | ||||||||||

| Real estate assets held for sale, net | 119,912 | 19,611 | 160,570 | 84,259 | ||||||||||

| Net investments | 7,317,560 | 6,743,439 | 7,272,655 | 7,425,719 | ||||||||||

| Cash and cash equivalents | 176,181 | 66,588 | 10,059 | 21,790 | ||||||||||

| Deferred costs and other assets, net | 231,839 | 129,597 | 140,917 | 179,180 | ||||||||||

| Goodwill | 291,421 | 291,421 | 254,340 | 264,350 | ||||||||||

| Total assets | $ | 8,017,001 | $ | 7,231,045 | $ | 7,677,971 | $ | 7,891,039 | ||||||

| Liabilities and stockholders’ equity | ||||||||||||||

| Liabilities: | ||||||||||||||

| Revolving credit facilities | $ | 15,181 | $ | 35,120 | $ | 86,000 | $ | — | ||||||

| Term loan, net | 418,471 | 322,902 | ||||||||||||

| Senior unsecured notes | 295,112 | — | ||||||||||||

| Mortgages and notes payable, net | 3,658,496 | 3,743,098 | 2,162,403 | 3,079,787 | ||||||||||

| Convertible Notes, net | 695,957 | — | ||||||||||||

| Convertible notes, net | 702,642 | 690,098 | ||||||||||||

| Total debt, net | 3,664,628 | 4,092,787 | ||||||||||||

| Intangible lease liabilities, net | 205,968 | 220,114 | 182,320 | 193,903 | ||||||||||

| Accounts payable, accrued expenses and other liabilities | 123,298 | 114,679 | 148,915 | 142,475 | ||||||||||

| Total liabilities | 4,698,900 | 4,113,011 | 3,995,863 | 4,429,165 | ||||||||||

| Commitments and contingencies (see Note 10) | ||||||||||||||