UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

|

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) |

| OF THE SECURITIES EXCHANGE ACT OF 1934. |

For the fiscal year ended December 31, 20162017

Commission File Number 001-36004

SPIRIT REALTY CAPITAL, INC.

SPIRIT REALTY, L.P.

(Exact name of registrant as specified in its charter)

|

| | | | |

| Spirit Realty Capital, Inc. | | Maryland | | 20-1676382 |

| Spirit Realty, L.P. | | Delaware | | 20-1127940 |

| | | (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification Number) |

| | | 2727 North Harwood Street, Suite 300, Dallas, Texas 75201 | | (972) 476-1900 |

| | | (Address of principal executive offices; zip code) | | (Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

|

| | | | |

| | | Title of each class: | | Name of exchange on which registered: |

| Spirit Realty Capital, Inc. | | Common Stock, $0.01 par value per share | | New York Stock Exchange |

| | 6.000% Series A Cumulative Redeemable Preferred Stock, $0.01 par value per share | | New York Stock Exchange |

| Spirit Realty, L.P. | | None | | None |

Securities registered pursuant to Section 12(g) of the Act:

|

| | |

| Spirit Realty Capital, Inc. | | None |

| Spirit Realty, L.P. | | None |

| | | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Spirit Realty Capital, Inc. Yes x No o Spirit Realty, L.P. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Spirit Realty Capital, Inc. Yes o No x Spirit Realty, L.P. Yes x No o

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Spirit Realty Capital, Inc. Yes x No o Spirit Realty, L.P. Yes o No x

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Spirit Realty Capital, Inc. Yes x No o Spirit Realty, L.P. Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Spirit Realty Capital, Inc.

|

| | | | | | | |

| Large accelerated filer | x | Accelerated filer | o | Non-accelerated filer | o | Smaller reporting company | o |

Spirit Realty, L.P.

|

| | | | | | | |

| Large accelerated filer | o | Accelerated filer | x | Non-accelerated filer | o | Smaller reporting company | o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Spirit Realty Capital, Inc. o Spirit Realty, L.P. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Spirit Realty Capital, Inc. Yes o No x Spirit Realty, L.P. Yes o No x

As of June 30, 20162017 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of the Registrant'sSpirit Realty Capital, Inc's shares of common stock, $0.01 par value, held by non-affiliates of the Registrant, was $6.1$3.4 billion based on the last reported sale price of $12.77$7.41 per share on the New York Stock Exchange on June 30, 2016.2017.

There is no public trading market for the common units of limited partnership interest of Spirit Realty, L.P. As a result, the aggregate market value of the common units of limited partnership interest held by non-affiliates of Spirit Realty, L.P. cannot be determined.

The number of outstanding shares of Spirit Realty Capital, Inc.'s common stock, $0.01 par value, as of February 21, 2017,20, 2018, was 483,599,385448,835,524 shares.

Documents Incorporated by Reference

Certain specific portions of the definitive Proxy Statement for Spirit Realty Capital, Inc.'s 20172018 Annual Meeting of Stockholders to be filed pursuant to Regulation 14A are incorporated by reference into Part III, Items 10, 11, 12, 13 and 14 of this Annual Report on Form 10-K. Only those portions of the Proxy Statement which are specifically incorporated by reference herein shall constitute a part of this Annual Report on Form 10-K.

Explanatory NotesNote

This report combines the annual reports on Form 10-K for the year ended December 31, 20162017 of Spirit Realty Capital, Inc., a Maryland corporation, and Spirit Realty, L.P., a Delaware limited partnership. Unless otherwise indicated or unless the context requires otherwise, all references in this report to “we,” “us,” “our,” or the “Company” refer to Spirit Realty Capital, Inc. together with its consolidated subsidiaries, including Spirit Realty, L.P. Unless otherwise indicated or unless the context requires otherwise, all references to the “Operating Partnership” refer to Spirit Realty, L.P. together with its consolidated subsidiaries.

Spirit General OP Holdings, LLC ("OP Holdings") is the sole general partner of the Operating Partnership. The Company is a real estate investment trust, or REIT, and the sole member of OP Holdings, as well as the special limited partner of the Operating Partnership. As sole member of the general partner of our Operating Partnership, our Company has the full, exclusive and complete responsibility for our Operating Partnership’s day-to-day management and control.

We believe combining the annual reports on Form 10-K of our Company and Operating Partnership into a single report results in the following benefits:

enhancing investors’ understanding of our Company and Operating Partnership by enabling investors to view the business as a whole, reflective of how management views and operates the business;

eliminating duplicative disclosure and providing a streamlined presentation as a substantial portion of the disclosures apply to both our Company and Operating Partnership; and

creating time and cost efficiencies by preparing one combined report in lieu of two separate reports.

There are a few differences between our Company and Operating Partnership, which are reflected in the disclosures in this report. We believe it is important to understand these differences in the context of how we operate as an interrelated, consolidated company. Our Company is a REIT, the only material assets of which are the partnership interests in our Operating Partnership. As a result, our Company does not conduct business itself, other than acting as the sole member of the general partner of our Operating Partnership, issuing equity from time to time and guaranteeing certain debt of our Operating Partnership. Our Operating Partnership holds substantially all the assets of our Company. Our Company issued convertible notes and guarantees some of the debt of our Operating Partnership, see footnoteNote 4 to the combined, consolidated financial statements herein for further discussion. Our Operating Partnership conducts the operations of the business and is structured as a partnership with no publicly traded equity. Except for net proceeds from issuance of convertible notes and equity issuances by our Company, which are generally contributed to our Operating Partnership in exchange for partnership units of our Operating Partnership, our Operating Partnership generates the capital required by our Company’s business through our Operating Partnership’s operations or our Operating Partnership’s incurrence of indebtedness.

The presentation of stockholders’ equity and partners’ capital are the main areas of difference between the consolidated financial statements of our Company and those of our Operating Partnership. The partnership units in our Operating Partnership are accounted for as partners’ capital in our Operating Partnership’s consolidated financial statements. There are no non-controlling interests in the Company or the Operating Partnership.

To help investors understand the significant differences between our Company and our Operating Partnership, this report presents the consolidated financial statements separately for our Company and our Operating Partnership. All other sections of this report, including “Selected Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Quantitative and Qualitative Disclosures About Market Risk,” are presented together for our Company and our Operating Partnership.

In order to establish that the Chief Executive Officer and the Chief Financial Officer of each entity have made the requisite certifications and that our Company and Operating Partnership are compliant with Rule 13a-15 or Rule 15d-15 of the Securities Exchange Act of 1934, or the Exchange Act, and 18 U.S.C. §1350, this report also includes separate “Item 9A. Controls and Procedures” sections and separate Exhibit 31 and 32 certifications for each of our Company and our Operating Partnership.

SPIRIT REALTY CAPITAL, INC. and SPIRIT REALTY, L.P.

INDEX

|

| | |

| PART I | | |

| Item 1. | Business | |

| Item 1A. | Risk Factors | |

| Item 1B. | Unresolved Staff Comments | |

| Item 2. | Properties | |

| Item 3. | Legal Proceedings | |

| Item 4. | Mine Safety Disclosure | |

| PART II | | |

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |

| Item 6. | Selected Financial Data | |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | |

| Item 8. | Financial Statements and Supplementary Data | |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |

| Item 9A. | Controls and Procedures As Restated | |

| Item 9B. | Other Information | |

| PART III | | |

| Item 10. | Directors, Executive Officers and Corporate Governance | |

| Item 11. | Executive Compensation | |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | |

| Item 14. | Principal Accountant Fees and Services | |

| PART IV | | |

| Item 15. | Exhibits, Financial Statement Schedules | |

| SIGNATURES | | |

GLOSSARY

|

| |

| Definitions: | |

| 1031 Exchange | Tax-deferred like-kind exchange of properties held for business or investment purposes, pursuant to Section 1031 of the Code |

| 2013 Credit Facility | $400.0 million secured credit facility pursuant to the credit agreement between the Operating Partnership and certain lenders dated July 17, 2013 |

2015 Credit Facility2017 Tax Legislation | $800.0 million unsecured credit facility pursuant to the Credit AgreementTax Cuts and Jobs Act |

| 2019 Notes | $402.5 million convertible notes of the Corporation due in 2019 |

| 2021 Notes | $345.0 million convertible notes of the Corporation due in 2021 |

401(k) Plan | Defined contribution retirement savings plan qualified under Section 401(k) of the Code |

| ACM | Asbestos-Containing Materials |

| ADA | Americans with Disabilities Act |

Additional Collateral Deposit | A cash reserve deposit or letter of credit in the amount of $8.0 million required pursuant to an amendment of a certain CMBS loan agreement |

| AFFO | Adjusted Funds From Operations |

| Amended Incentive Award Plan | Amended and Restated Spirit Realty Capital, Inc. and Spirit Realty, L.P. 2012 Incentive Award Plan |

| AOCL | Accumulated Other Comprehensive Loss |

| ASC | Accounting Standards Codification |

| ASU | Accounting Standards Update |

| ATM Program | At the Market equity distribution program, pursuant to which the Corporation may offer and sell registered shares of common stock from time to time |

| CMBS | Commercial Mortgage Backed Securities |

| Code | Internal Revenue Code of 1986, as amended |

| Cole II | Cole Credit Property Trust II, Inc. |

Cole II Merger | Acquisition on July 17, 2013 of Cole II by the Company, in which the Company merged with and into the Cole II legal entity |

| Collateral Pools | Pools of collateral assets that are pledged to the indenture trustee for the benefit of the noteholders and secure obligations of issuers under the Spirit Master Funding Program |

| Company | The Corporation and its consolidated subsidiaries |

| Contractual Rent | Monthly contractual cash rent and earned income from direct financing leases, excluding percentage rents, from our properties owned fee-simple or ground leased, recognized during the final month of the reporting period, adjusted to exclude amounts received from properties sold during that period and adjusted to include a full month of contractual rent for properties acquired during that period |

| Convertible Notes | The 2019 Notes and 2021 Notes, together |

| Corporation | Spirit Realty Capital, Inc., a Maryland corporation |

| CPI | Consumer Price Index |

| Credit Agreement | 2015Revolving credit facility agreement between the Operating Partnership and certain lenders dated March 31, 2015, as amended or otherwise modified from time to time |

| EBITDA | Earnings Before Interest, Taxes, Depreciation and Amortization |

| EBITDAR | Earnings Before Interest, Taxes, Depreciation, Amortization and Rent |

| EDF | Expected Default Frequency |

Excess Cash | Rent received in excess of debt service obligations |

| Exchange Act | Securities Exchange Act of 1934, as amended |

| Exchange Offer | The May 2014 exchange of the outstanding principal balance of three series of existing net-lease mortgage notes for three series of newly issued 2014 Notes |

| FASB | Financial Accounting Standards Board |

| FFO | Funds From Operations |

| Fitch | Fitch Ratings |

| GAAP | Generally Accepted Accounting Principles in the United States |

| IASB | International Accounting Standards Board |

| IFRS | International Financial Reporting Standards |

IPOIRS | Initial Public OfferingInternal Revenue Service |

| LIBOR | London Interbank Offered Rate |

|

| |

| Definitions: | |

IRS | Internal Revenue Service |

LIBOR | London Interbank Offered Rate |

Line of Credit | $40.0 million secured revolving credit facility pursuant to the loan agreement between an indirect wholly-owned subsidiary of the Corporation and a certain lender dated March 27, 2013, as amended |

| Master Trust 2013 | The net-lease mortgage securitization trust established in 2013 under the Spirit Master Funding Program |

| Master Trust 2014 | The net-lease mortgage securitization trust established in 2005 and amended and restated in 2014 under the Spirit Master Funding Program |

| Master Trust Exchange Costs | Legal, accounting and financial advisory services costs incurred in connection with the Exchange Offer |

| Master Trust Notes | The Master Trust 2013 and Master Trust 2014, together |

| Master Trust Release | Proceeds from the sale of assets securing the Master Trust Notes held in restricted accounts until a qualifying substitution is made or until used for principal reduction |

| Merger | The transactionAcquisition on July 17, 2013 of Cole II by the Company, in which the Corporation's prior legal entityCompany merged with and into the Cole II legal entity |

| Merger Exchange Ratio | Merger exchange ratio of 1.9048 |

| MGCL | Maryland General Corporation Law |

| Moody's | Moody's Investor Services |

| NAREIT | National Association of Real Estate Investment Trusts |

Normalized Rental Revenue | Total rental revenues and earned income from direct financing leases from our owned properties during the final month of the reporting period, adjusted to exclude amounts from properties sold during that period and to include a full month of rental revenues for properties acquired during that period. |

| NYSE | New York Stock Exchange |

| OP Holdings | Spirit General OP Holdings, LLC |

| Operating Partnership | Spirit Realty, L.P., a Delaware limited partnership |

PATH Act | Protecting Americans from Tax Hikes Act of 2015 |

| REIT | Real Estate Investment Trust |

Revolving Credit FacilitiesFacility | The 2013$800.0 million unsecured credit facility pursuant to the Credit Facility, the 2015 Credit Facility and Line of Credit, togetherAgreement |

| S&P | Standard & Poor's Rating Services |

| SEC | Securities and Exchange Commission |

| Securities Act | Securities Act of 1933, as amended |

| Senior Unsecured Notes | $300 million aggregate principal amount of senior notes issued in August 2016 |

| Series A Preferred Stock | 6,900,000 shares of 6.000% Cumulative Redeemable Preferred Stock issued October 3, 2017, with a liquidation preference of $25.00 per share. |

| Shopko | Specialty Retail Shops Holding Corp. and certain of its affiliates |

| SMTA | Spirit MTA REIT, a Maryland real estate investment trust |

| Spin-Off | Creation of an independent, publicly traded REIT, SMTA, through contribution of properties leased to Shopko, assets that collateralize Master Trust 2014 and potential additional assets |

| Spirit Master Funding Program | The Company's asset-backed securitization program that comprises Master Trust 2013 and Master Trust 2014 |

| Term Loan | $420.0 million senior unsecured term facility pursuant to the Term Loan Agreement |

| Term Loan Agreement | Term loan agreement between the Operating Partnership and certain lenders dated November 3, 2015, as amended or otherwise modified from time to time |

Total Debt | Principal debt outstanding before discounts, premiums or deferred financing costs |

| TRS | Taxable REIT SubsidiariesSubsidiary, a corporation, other than a REIT, in which a REIT directly or indirectly holds stock and that has made a joint election with such REIT to be treated as a taxable REIT subsidiary |

| TSR | Total Shareholder Return |

| U.S. | United States |

| Vacant | Owned properties which are not economically yielding |

Unless otherwise indicated or unless the context requires otherwise, all references to the "registrant," the "Company," "Spirit Realty Capital," "we," "us" or "our" refer to the Corporation and its consolidated subsidiaries, including the Operating Partnership. Unless otherwise indicated or unless the context requires otherwise, all references to the "Operating Partnership" refer to Spirit Realty, L.P. and its consolidated subsidiaries.

PART I

The following discussion relates to our consolidated financial statements and should be read in conjunction with the consolidated financial statements and notes thereto appearing elsewhere in this Annual Report on Form 10-K. Statements contained in Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” that are not historical facts may be forward-looking statements. Such statements are subject to certain risks and uncertainties, which could cause actual results to differ materially from those projected. Some of the information presented is forward-looking in nature, including information concerning projected future occupancy rates, rental rate increases, property development timing and investment amounts. Although the information is based on our current expectations, actual results could vary from expectations stated in this report. Numerous factors will affect our actual results, some of which are beyond our control. These include the breadth and duration of the current economic environment and its impact on our tenants, the strength of commercial and industrial real estate markets, market conditions affecting tenants, competitive market conditions, interest rate levels, volatility in our stock price and capital market conditions. You are cautioned not to place undue reliance on this information, which speaks only as of the date of this report. We assume no obligation to update publicly any forward-looking information, whether as a result of new information, future events, or otherwise, except to the extent we are required to do so in connection with our ongoing requirements under federal securities laws to disclose material information. For a discussion of important risks related to our business, and related to investing in our securities, including risks that could cause actual results and events to differ materially from results and events referred to in the forward-looking information, see Item 1A. “Risk Factors - Special Note Regarding Forward-Looking Statements” and Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Liquidity and Capital Resources.” In light of these risks, uncertainties and assumptions, the forward-looking events discussed in this Annual Report on Form 10-K might not occur.

Available Information

The Corporation's principal executive offices are located at 2727 North Harwood Street, Suite 300, Dallas, Texas 75201. Our telephone number at that location is 972-476-1900. We maintain a website at www.spiritrealty.com. On the Investor Relations page of our website, we post the following filings as soon as reasonably practicable after they are electronically filed with or furnished to the SEC: our Annual Report on Form 10-K, our Quarterly Reports on Form 10-Q, our Current Reports on Form 8-K, and the Section 16 filings of our directors and officers, as well as any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act. All such filings on our Investor Relations page of our website are available to be viewed free of charge. Also available on our website, free of charge, are our corporate governance guidelines, the charters of the nominating and corporate governance, audit and compensation committees of our boardBoard of directorsDirectors and our code of business conduct and ethics (which applies to all directors and employees, including our principal executive officer, principal financial officer and principal accounting officer).

Information contained on or hyperlinked from our website is not incorporated by reference into and should not be considered part of this Annual Report on Form 10-K or our other filings with the SEC. A copy of this Annual Report on Form 10-K is available without charge upon written request to: Investor Relations, Spirit Realty Capital, Inc., 2727 North Harwood Street, Suite 300, Dallas, Texas 75201. All reports we file with the SEC are available free of charge on the SEC's Web sitewebsite at www.sec.gov. In addition, the public may read and copy materials we file with the SEC at the SEC’s public reference room located at 100 F Street, N.E., Washington, D.C. 20549. Shares of our common stock are traded on the NYSE under the symbol “SRC.”

Item 1. Business

The CompanyTHE COMPANY

The Corporation is a NYSE listed company under the symbol "SRC." We are a self-administered and self-managed REIT with in-house capabilities, including acquisition, portfolio management, asset management, investment, credit, research, real estate research, legal, finance, IT and accounting and capital markets.functions. We primarily invest in single-tenant, operationally essential real estate throughout the U.S., which is generally acquired through strategic sale-leaseback transactions and subsequently leased on a long-term, triple-net basis to high-quality tenants with business operations within predominantly retail, but also office and industrial property types.

As of December 31, 2016,2017, our undepreciated gross investment in real estate and loans totaled approximately $8.2$7.9 billion, representing investments in 2,6152,480 properties, including properties securing our mortgage loans. Of this amount,

99.2% 99.0% consisted of our gross investment in real estate, representing ownership of 2,5412,392 properties, and the remaining 0.8%1.0% consisted primarily of commercial mortgage loans receivable secured by 7488 real properties.

As of December 31, 2016,2017, our owned properties were approximately 98.2%99.2% occupied (based on number of economically yielding properties), and our leases had a weighted average non-cancelable remaining lease term (based on Normalized Rental Revenue)Contractual Rent) of approximately 10.710.0 years. Our leases are generally long-term, with non-cancelable initial terms of 15 to 20 years and tenant renewal options for additional terms. As of December 31, 2016,2017, approximately 89% of our single-tenant leases (based on Normalized Rental Revenue)Contractual Rent) provided for increases in future annual base rent. See Item 2. "Properties - Our Real Estate Investment Portfolio" for further information on our properties and tenants.

Our operations are carried out through the Operating Partnership. OP Holdings, one of our wholly-owned subsidiaries, is the sole general partner and owns approximately 1.0%1% of the Operating Partnership. We and one of our wholly-owned subsidiaries are the only limited partners and together own the remaining 99.0%99% of the Operating Partnership.

Although the Operating Partnership is wholly-owned by us, in the future, we may issue partnership interests in the Operating Partnership to third parties in exchange for assets owned by such third parties. In general, any partnership interests of the Operating Partnership issued to third parties would be exchangeable for cash or, at our election, shares of our common stock at specified ratios set when partnership interests in the Operating Partnership are issued.

As of December 31, 2016,2017, we had 8487 employees, as compared to 7184 employees as of December 31, 2015.2016. None of these employees are represented by a labor union.

History

We began operations through a predecessor legal entity in 2003. We became a public company in December 2004 and were subsequently taken private in August 2007 by a consortium of private investors. On September 25, 2012, we completed our IPOinitial public offering of 33.35 million shares of common stock (including shares issued on October 1, 2012 pursuant to the underwriters’ option to purchase additional shares).

On July 17, 2013, we completed the acquisition of Cole II through the Merger. Our boardBoard of directorsDirectors (including two additional members designated by Cole II) and executive team managed the surviving entity, which was renamed Spirit Realty Capital, Inc. and began trading on the NYSE under the symbol "SRC." Cole II was the "legal acquirer" in the Merger for certain legal and regulatory matters and the Corporation was deemed the "accounting acquirer" in the Merger for accounting and financial reporting purposes, including the financial information set forth herein.

Business and Growth StrategiesBUSINESS AND GROWTH STRATEGIES

Our objective is to maximize stockholder value by seeking superior risk-adjusted returns with an emphasis on stable rental revenue, primarily by investing in and managing a portfolio of single-tenant, operationally essential retail real estate throughout the U.S. that is generally acquired through strategic sale-leaseback transactions and subsequently leased on a long-term, triple-net basis. We generate revenue primarily by leasing our properties to our tenants. See Item 2. "Properties" for property information and Item 6. "Selected Financial Data" for additional financial and asset information.

Single-tenant, operationally essential real estate consists of properties that are generally free-standing, commercial real estate facilities where our tenants conduct activities essential to the generation of their sales and profits. Under a triple-net lease, the tenant is typically responsible for all improvements and is contractually obligated to pay all property operating expenses, such as real estate taxes, insurance premiums and repair and maintenance costs. In support of our primary business of owning and leasing real estate, we have also strategically originated or acquired long-term, commercial mortgage and other loans. We view our operations as one reporting segment consisting of net leasing operations. We intend to pursue our objective through the following business and growth strategies:

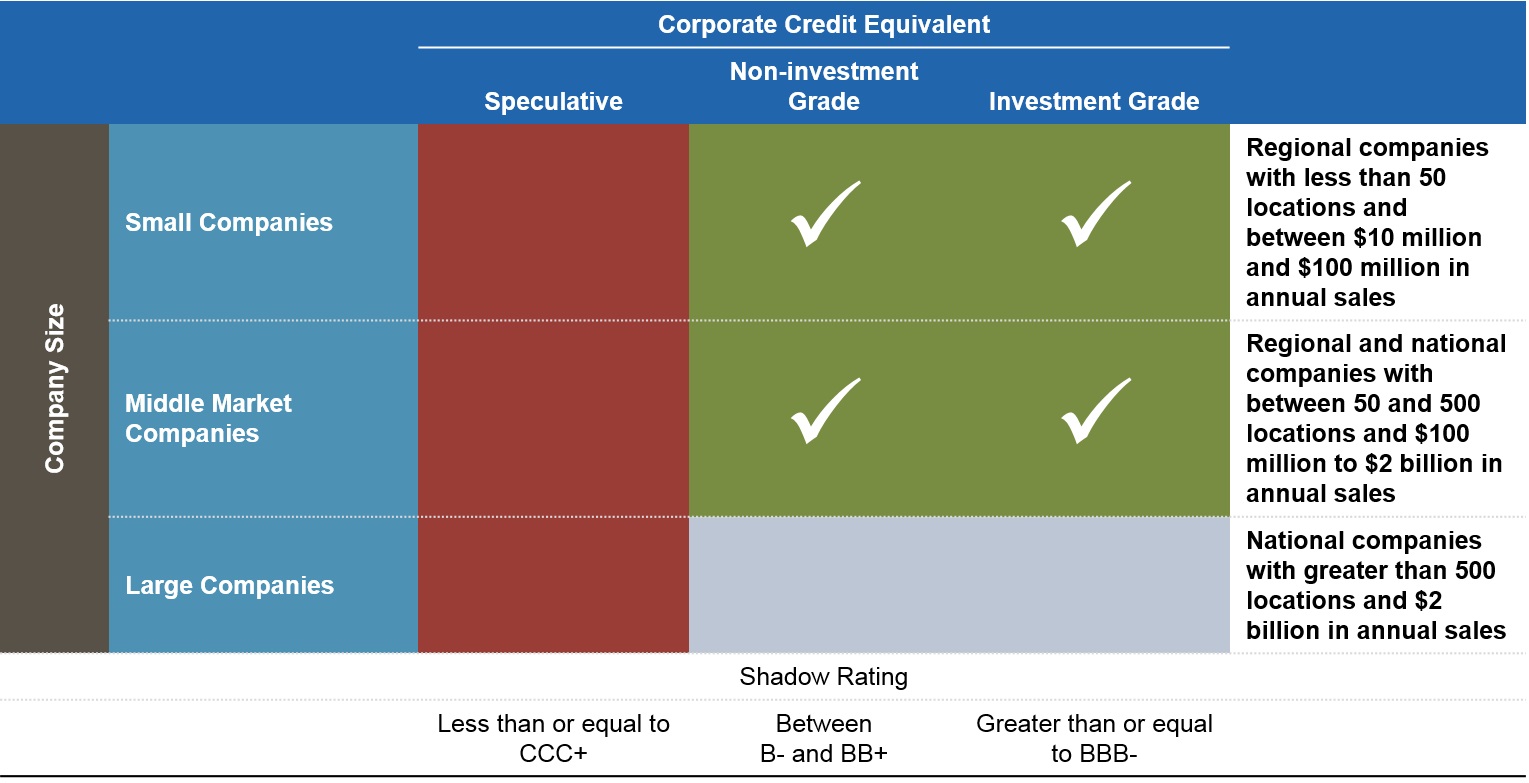

Focus on SmallIndustries Identified as Desirable in the Spirit Heat Map

Our investment strategy is based on increasing our exposure to industries we determine to be attractive based on our proprietary Spirit Heat Map. The Spirit Heat Map is used to analyze tenant industries across Porter’s Five Forces and Middle Market Companies. We primarily focus on investing in propertiespotential causes of technological disruption to identify tenant industries that we net leasebelieve to smallhave good fundamentals for future performance. The Spirit Heat Map is updated regularly to factor for changes in business and middle market companies withconditions, changes in technology and other trends. Desirable tenants have attractive credit characteristics and stable operating histories, but that may not carry a credit rating from a rating agency.histories. This strategy offers us the opportunity to achieve superior risk-adjusted returns when coupled with our intensive credit and real estate analysis, lease structuring and ongoing portfolio management. Small and middle market companies are often willing to enter into leases with structures and terms we consider attractive (such as master leases, leases with rental escalations and leases that require ongoing tenant financial reporting) and that we believe increase the security of rental payments. We may also

selectively acquire properties leased to large companies where we believe that we can achieve superior risk-adjusted returns.

The following chart highlights the tenants that we target based on company size and corporate credit equivalent:

Structure and Manage Our Portfolio Using Our Developed Underwriting and Risk Management Processes.Processes

We seek to maintain the stability of our rental revenue and the long-term return on our investments by using our developed underwriting and risk management processes to structure and manage our portfolio. In particular, our underwriting and risk management processes emphasize the following:

| |

| ◦ | Leases for Operationally Essential Real Estate with Relatively Long Terms. We seek to own properties that are operationally essential to our tenants, thereby reducing the risk that the tenant would choose not to renew an expiring lease or reject a lease in bankruptcy. In addition, we seek to enter into leases with relatively long terms, typically with non-cancelable initial terms of 15 to 20 years and tenant renewal options for additional terms with attractive rent escalation provisions. |

| |

| ◦ | Spirit Property Ranking Model. We use our proprietary ranking model annually to rank all properties in our portfolio, across twelve factors and weightings consisting of real estate quality scores, lease structure quality and credit underwriting criteria. The Spirit Property Rank Model is a key component of both the acquisition and disposition process as well as standard asset management activities. |

| |

| ◦ | Leases with a Master Lease Structure. Where appropriate, we seek to enter into master leases whereby we lease multiple properties to a single tenant on an “all or none” basis. In a master lease structure, a tenant is responsible for a single lease payment relating to the entire portfolio of leased properties, as opposed to separate lease payments relating to each individually leased properties.property. The master lease structure prevents a tenant from “cherry picking” locations, where it unilaterally gives up underperforming properties while maintaining its leasehold interest in well-performing properties. As of December 31, 2016,2017, we had 147131 active master leases with portfolios of leased properties ranging from 2 to 182172 and a weighted average non-cancelable remaining lease term (based on Normalized Rental Revenues)Contractual Rent) of 13.712.7 years. Master lease revenues contributed approximately 45% of our Normalized Rental Revenue.Contractual Rent. Our largest master lease, with Shopko, consisting of 2359 properties, contributed 2.9%6.8% of our Normalized Rental Revenue,Contractual Rent, and our smallest master lease, consisting of 5two properties, contributed less than 0.04%0.1% of our Normalized Rental RevenueContractual Rent for the month ended December 31, 2016.2017. As of December 31, 2016,2017, the majority of our master leases include between 2 and 10 properties. |

| |

| ◦ | Active Management and Monitoring of Risks Related to Our Investments. When monitoring existing investments or evaluating new investments, we typically consider two broad categories of risk: (1) tenant financial distress risk;risk and (2) lease renewal risk. We seek to measure these risks through various processes, including the use of a credit modeling product that we license from Moody’s Analytics that estimates the performance of the leased properties relative to rental payments due under the leases and a review of current market data and our historical recovery rates on re-leased properties and property dispositions. Our underwriting and risk management processes are designed to structure new investments and manage existing investments to address and mitigate each of the above risks and preserve the long-term return on our invested capital. Since our inception, our occupancy has never been below 96.1% (based on number of economically yielding properties), despite the economic downturn of 2008 through 2010. |

and manage existing investments to address and mitigate each of the above risks and preserve the long-term return on our invested capital. Since our inception, our occupancy has never been below 96.1% (based on number of properties), despite the economic downturn of 2008 through 2010.

| |

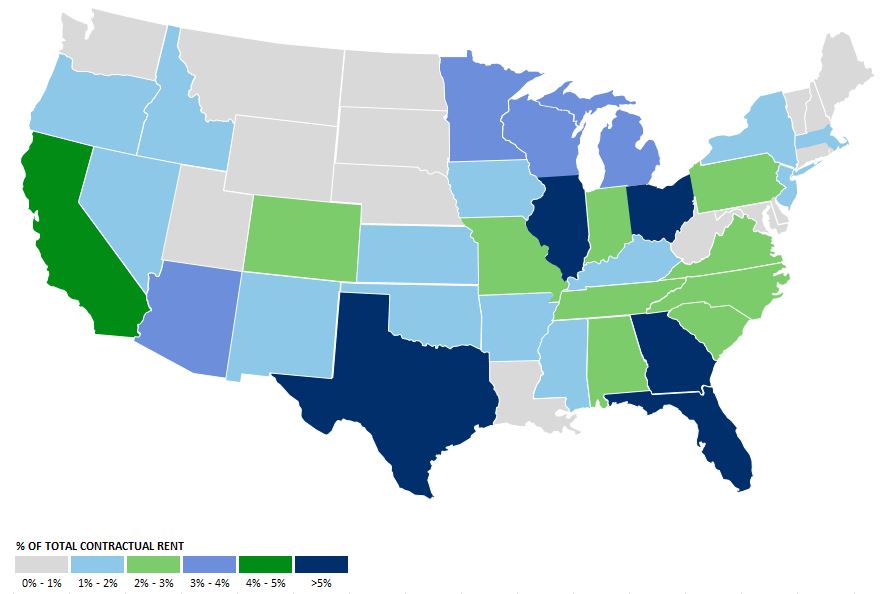

| ◦ | Portfolio Diversification. We monitor and manage the diversification of our real estate investment portfolio in order to reduce the risks associated with adverse developments affecting a particular tenant, property, industry or region. Our strategy emphasizes a portfolio that (1) derives no more than 10% of its annual rent from any single tenant and no more than 1.5%2.0% of its annual rent from any single property, (2) is leased to tenants operating in various industries and (3) is located across the U.S. without significant geographic concentration. While we consider the foregoing when making investments, we have made, and may make investments in the future that do not meet one or more of these criteria, and we may make additional investments that do not meet one or more of these criteria if we believe the opportunity is sufficiently attractive. |

Enhance Our Portfolio through Contractual Rental Growth.Growth

Approximately 89%89.2% of our single-tenant properties (based on Normalized Rental Revenue)Contractual Rent) contain contractual provisions that increase the rental revenue over the term of the lease. Generally, our rent escalators increase rent at specified

dates by: (1) a fixed amount; or (2) the lesser of (a) 1 to 1.252 times any increase in the CPI over a specified period, or (b) a fixed percentage, typically 1% to 2% per year.or (c) a fixed schedule.

Grow Our Portfolio through Selective Acquisitions.Acquisitions

We selectively make acquisitions that we believe will contribute to our business objective. We believe there will be ample acquisition opportunities in the single-tenant market fitting our underwriting and acquisition criteria, which may include improving our portfolio’s tenant, industry and geographic diversification, among other rationale. Acquisitions of such properties or portfolios may be subject to existing indebtedness or to new indebtedness which may be incurred in connection with acquiring or refinancing these investments.

Deleverage Our Portfolio.Portfolio

A significant amount of our secured debt is partially amortizing, and its principal amount will be reduced prior to the balloon payments due at maturity. Contractual amortization payments are scheduled to reduce our outstanding principal amount of indebtedness by $182.3$199.9 million prior to January 1, 2022.2023. We may selectively reduce our indebtedness using cash from operations in excess of our distributions or proceeds from asset dispositions and /or equity offerings. We may also strategically replace or refinance certain indebtedness with proceeds from new borrowings that represent a more attractive cost of capital. We believe contractual rent growth, selective growth through acquisitions and the ongoing deleveraging of our portfolio will contribute to our cash available for distributions.

Dispose of Select Assets.Assets

We typically retain and manage real estate assets that fit within our investment criteria, which criteria are subject to change without notice to or vote by our stockholders. Additionally, management may elect to dispose of assets when it believes appropriate in view of our business objective, considering criteria including, but not limited to, the Spirit Heat Map, the Spirit Property Rank, tenant concentration, tenant credit quality, unit financial performance, local market conditions and lease rates, associated indebtedness, asset location, tenant operation type (e.g., industry, sector, or concept/brand), and asset zoning, as well as potential capital appreciation, potential uses of proceeds and tax considerations, among others.

Financing StrategyFINANCING STRATEGY

Our long-term financing strategy is to maintain a leverage profile that creates operational flexibility and generates superior risk-adjusted returns for our stockholders. We finance our operations and investments using a variety of methods, including available unrestricted cash balances, property operating revenue, proceeds from property dispositions, available borrowings under our 2015Revolving Credit Facility and Term Loan, common and preferred stock issuances, and debt securities issuances, including mortgage indebtedness and senior unsecured debt. We determine the amount of equity and debt financing to be used when acquiring an asset by evaluating our cost of equity capital, terms available in the credit markets (such as interest rate, repayment provisions and maturity) and our assessment of the particular asset’s risk.

We may issue common stock when we believe that our share price is at a level that allows the offering proceeds to be accretively invested into additional properties, to permanently finance properties that were financed by our Revolving Credit FacilitiesFacility or Term Loan, or to repay outstanding debt at or before maturity.

In November 2016,September 2017, we filed a shelf registration statement with the SEC, which became immediately effective upon filing.filing and will remain effective for a term of three years with an expiration in September 2020. Under this shelf registration statement, we may offer shares of our common or preferred stock or debt securities from time to time in amounts,

at prices and on terms to be announced when and if such shares are offered. The specifics of any future offerings, along with the use of proceeds from any such offerings, will be described in detail in a prospectus supplement or other offering materials at the time of such offerings.

Historically, a significant portion of our debt has consisted of long-term borrowings secured by specific real estate assets or, more typically, pools of real estate assets. We have utilized our asset-backed securitization platform to raise capital through the issuance of non-recourse net-lease mortgage notes collateralized by commercial real estate, net-leases and mortgage loans under the Spirit Master Funding Program. In addition, we have issued senior unsecured debt securities and have obtained other senior unsecured debt at the Operating Partnership level. To the extent practicable, we expect to maintain a well-balanced debt profile with manageable and balanced maturities.

We expect to fund our operating expenses and other short-term liquidity requirements, including property acquisitions, payment of principal and interest on our outstanding indebtedness, property improvements, re-leasing costs, and cash distributions to common and preferred stockholders, primarily through cash provided by operating activities, borrowings under our available 2015Revolving Credit Facility and Term Loan and occasionallyperiodically through issuances of common stock and entering into secured and unsecured debt agreements.public securities.

We anticipate that we will continue to use a number of different sources to finance our acquisitions and operations going forward; however, we cannot assure you that we will have access to the capital and credit markets at times and at terms that are acceptable to us.

Recent DevelopmentsRECENT DEVELOPMENTS

Financing Activities

2015 Credit Facility

On April 27, 2016, the Company expanded the borrowing capacity under the 2015 Credit Facility from $600.0 million to $800.0 million by partially exercising the accordion feature under the terms of the Credit Agreement. The 2015 Credit Facility also includes a swing-line loan and letters of credit, which reduce availability under the 2015 Credit Facility on a dollar-for-dollar basis. In April 2016, the Corporation received a first time rating of BBB- from Fitch and was upgraded to a BBB- corporate issuer rating by S&P, allowing the Operating Partnership to elect to change the interest rate grid from leverage based pricing to credit based pricing. Under credit based pricing, the 2015 Credit Facility bears interest at a rate equal to LIBOR plus 0.875% to 1.55% per annum or a specified base rate plus 0.0% to 0.55% and requires a facility fee in an amount equal to the aggregate revolving credit commitments (whether or not utilized) multiplied by a rate equal to 0.125% to 0.30% per annum, in each case depending on the Corporation's credit rating.

Term Loan

In April 2016, the Corporation received a first time rating of BBB- from Fitch and was updated to a BBB- corporate issuer rating by S&P, allowing the Operating Partnership to elect to change the interest rate grid from leverage based pricing to credit based pricing. Under credit rating based pricing, borrowings bear interest at a rate equal to LIBOR plus 0.90% to 1.75% per annum or a specified base rate plus 0.0% to 0.75% per annum, in each case depending on the Corporation’s credit rating. On December 19, 2016, the Company increased the term facility from $370.0 million to $420.0 million.

Senior Unsecured Notes

In August 2016,The Company filed a registration statement with the Operating Partnership completed aSEC to exchange the private placement ofSenior Unsecured Notes for registered Senior Unsecured Notes with substantially identical terms, which became effective April 14, 2017. All $300.0 million aggregate principal amount of senior notes through a Rule 144A offering with registration rights, which are guaranteed by the Corporation. Theprivate Senior Unsecured Notes were issued at 99.378% of their principal amount, resultingtendered in net proceeds of $296.2 million, after deducting transaction fees and expenses. Thethe exchange for registered Senior Unsecured Notes accrue interest at a rate of 4.450% per year, payable on March 15 and September 15 of each year, until the maturity date of September 15, 2026.Notes.

Issuance of CommonPreferred Stock

In April 2016,October 2017, the CorporationCompany completed an underwritten public offering of 34.5 million6,900,000 shares of its common stock at $11.15 per share,6.000% Series A Preferred Stock, including 4.5 million900,000 shares issuedsold pursuant to the underwriter’sunderwriter's option to purchase additional shares. Gross proceeds raised were approximately $384.7 million and$172.5 million; net proceeds were approximately $368.9$166.2 million after deducting underwriter discounts and offering costs paid by the Corporation.Company. The net proceeds from the offering were initially used to reduce outstanding debt and for general operating purposes of the Company.

Master Trust 2014 Notes

In December 2017, the existing issuers under Master Trust 2014, collectively as co-issuers, completed the issuance of $674.4 million aggregate principal amount of net-lease mortgage notes comprised of $542.4 million of 4.36% amortizing notes and $132.0 million of 6.35% interest-only notes, both expected to be repaid in December 2022. The Operating Partnership retained $27.1 million in aggregate principal amount of Class A Notes and $6.6 million in aggregate principal amount of Class B Notes to satisfy its regulatory risk retention obligations. Net proceeds from the sale of the notes were initially used for general corporate purposes, including repayment of borrowings under its Revolving Credit Facility and Term Loan.

See Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Liquidity and Capital Resources - Description of Certain Debt” for further information on our debt and equity financings.

Company Spin-Off

On August 3, 2017, we announced a proposed Spin-Off of almost all of our interest in our properties leased to Shopko, assets that collateralize Master Trust 2014 and other additional assets into an independent, publicly traded REIT, Spirit MTA REIT, or SMTA. Pursuant to the plan, if the Spin-Off is completed, our stockholders would receive a distribution of common shares of beneficial interest issued by SMTA. The distribution will be treated as a taxable distribution to Spirit stockholders. The Spin-Off is subject to certain conditions, including declaration by the U.S. Securities and Exchange Commission that SMTA's registration statement on Form 10 is effective, customary third party consents, and final approval and declaration of the distribution by our Board of Directors. Such conditions and other unforeseen developments, including in the debt or equity markets or general market conditions, could delay or prevent the Spin-Off or cause the Spin-Off to occur on terms or conditions that are less favorable and/or different than those described herein. The transaction is expected to be completed in the first half of 2018. We may, at any time and for any reason until the proposed transaction is complete, abandon the Spin-Off or modify or change its terms, including the assets we plan to contribution to SMTA.

Real Estate Portfolio Activities

Tenant Concentration

Shopko is our most significant tenant, representing 7.7% and 8.2% of our Normalized Rental RevenueContractual Rent for the month ended December 31, 2016.2017and December 31, 2016, respectively. Shopko leases 11497 properties under 13three separate master

leases and two properties under individual groundsingle site leases with four indirect wholly-owned subsidiaries of ours. We took a number of steps during 2015 and 2014 to reduce the tenant concentration of Shopko assets below 10%, which we accomplished during the third quarter of 2015. We continue to take steps to decrease our concentration of Shopko assets as we grow our existing portfolio base and continue to effectthrough strategic dispositions.

During the month ended December 31, 2016,2017, no other tenant exceeded 3.0%5.0% of our Normalized Rental Revenue,Contractual Rent, and no one single property contributed more than 1.5%2.0% of our Normalized Rental Revenue.Contractual Rent. See Item 2. “Properties - Our Real Estate Investment Portfolio" for further information on our ten largest tenants and the composition of our tenant base.

AcquisitionAcquisitions and Dispositions

During the year ended December 31, 2016,2017, we purchased 26939 properties, representing an aggregate gross investment of $704.9$323.0 million, which includes $20.5$42.6 million in revenue producing follow-on investments in existing properties. The properties acquired had a weighted average lease term of 15.012.0 years. During the same period, we sold 213192 properties for $584.9$551.2 million in gross sales proceeds. See Note 3 to our Consolidated Financial Statementsconsolidated financial statements included in this Annual Report on Form 10-K for additional discussion of our investments.

Restatement and Remediation

In October 2016, we identified a deficiency in our internal control over financial reporting, which was considered to be a material weakness and led to the restatement of our audited consolidated financial statements for the year ended December 31, 2015 and our interim unaudited consolidated financial statements for the quarters ended March 31, 2015, June 30, 2015, September 30, 2015, March 31, 2016 and June 30, 2016. Management has concluded that the material weakness disclosed in the Company's Annual Report on Form 10-K/A, as amended, for the fiscal year ended December 31, 2015, has been fully remediated and that the Company's disclosure controls and procedures and internal control over financial reporting were effective at December 31, 2016, as discussed in detail in Item 9A. Controls and Procedures.

CompetitionCOMPETITION

We face competition for acquisitions from investors, including traded and non-traded public REITs, and private equity and institutional investment funds, some of which have greater financial resources than we do, a greater ability to borrow funds to acquire properties and the ability to accept more risk than we can prudently manage. This competition may increase the demand for the types of properties in which we typically invest and, therefore, reduce the number of suitable acquisition opportunities available to us and increase the prices paid for such. This competition will increase if investments in real estate become more attractive relative to other forms of investment.

As a landlord, we compete in the multi-billion dollar commercial real estate market with numerous developers and owners of properties, many of which own properties similar to ours in the same markets in which our properties are located. In operating and managing our portfolio, we compete for tenants based on a number of factors, including location, rental rates and flexibility. Some of our competitors have greater economies of scale, have lower cost of capital, have access to more resources and have greater name recognition than we do. If our competitors offer space at rental rates below current market rates or below the rental rates we currently charge our tenants, we may lose our tenants or prospective tenants and we may be pressured to reduce our rental rates or to offer substantial rent abatements, tenant improvement allowances, early termination rights or below-market renewal options in order to retain tenants when our leases expire.

RegulationREGULATION

General

Our properties are subject to various covenants, laws, ordinances and regulations, including regulations relating to common areas and fire and safety requirements. We believe that each of our properties has the necessary permits and approvals.

Americans With Disabilities Act

Pursuant to the ADA, our properties are required to meet federal requirements related to access and use by persons with disabilities. Compliance with the ADA, as well as a number of additional federal, state and local laws and regulations, may require modifications to properties we currently own and any properties we purchase, or may restrict renovations of those properties. Noncompliance with these laws or regulations could result in the imposition of fines or an award of damages to private litigants, as well as the incurrence of the costs of making modifications to attain compliance, and future legislation could impose additional financial obligations or restrictions on our properties. Although our tenants are generally responsible for all maintenance and repair costs pursuant to triple-net leases, including compliance with the ADA and other similar laws or regulations, we could be held liable as the owner of the property for a failure of one of our tenants to comply with such laws or regulations.

Environmental Matters

Federal, state and local environmental laws and regulations regulate, and impose liability for, releases of hazardous or toxic substances into the environment. Under various of these laws and regulations, a current or previous owner, operator or tenant of real estate may be required to investigate and clean up hazardous or toxic substances, hazardous wastes or petroleum product releases or threats of releases at the property, and may be held liable to a government entity or to third parties for property damage and for investigation, clean-up and monitoring costs incurred by those parties in connection with actual or threatened contamination. These laws typically impose clean-up responsibility and

liability without regard to fault, or whether or not the owner, operator or tenant knew of or caused the presence of the contamination. The liability under these laws may be joint and several for the full amount of the investigation, clean-up and monitoring costs incurred or to be incurred or actions to be undertaken, although a party held jointly and severally liable may seek contributions from other identified, solvent, responsible parties for their fair share toward these costs. These costs may be substantial, and can exceed the value of the property. The presence of contamination, or the failure to properly remediate contamination, on a property may adversely affect the ability of the owner, operator or tenant to sell or rent that property or to borrow using the property as collateral and may adversely impact our investment in that property.

Some of our properties contain, have contained, or are adjacent to or near other properties that have contained or currently contain storage tanks for the storage of petroleum products or other hazardous or toxic substances. Similarly, some of our properties are or were used for commercial or industrial purposes that involve or involved the use of petroleum products or other hazardous or toxic substances, or are adjacent to or near properties that have been or are used for similar commercial or industrial purposes. These operations create a potential for the release of petroleum products or other hazardous or toxic substances, and we could potentially be required to pay to clean up any contamination. In addition, strict environmental laws regulate a variety of activities that can occur on a property, including the storage of petroleum products or other hazardous or toxic substances, air emissions and water discharges. Such laws may impose fines or penalties for violations. As a result of the foregoing, we could be materially and adversely affected.

Environmental laws also govern the presence, maintenance and removal of ACM. Federal regulations require building owners and those exercising control over a building’s management to identify and warn, through signs and labels, of potential hazards posed by workplace exposure to installed ACM in their building. The regulations also have employee training, record keeping and due diligence requirements pertaining to ACM. Significant fines can be assessed for violation of these regulations. As a result of these regulations, building owners and those exercising control over a building’s management may be subject to an increased risk of personal injury lawsuits by workers and others exposed to ACM. The regulations may affect the value of a building containing ACM in which we have invested. Federal, state and local laws and regulations also govern the removal, encapsulation, disturbance, handling and/or disposal of ACM when those materials are in poor condition or in the event of construction, remodeling, renovation or demolition of a building. These laws may impose liability for improper handling or a release into the environment of ACM and may provide for fines to, and for third parties to seek recovery from, owners or operators of real properties for personal injury or improper work exposure associated with ACM.

When excessive moisture accumulates in buildings or on building materials, mold growth may occur, particularly if the moisture problem remains undiscovered or is not addressed over a period of time. Some molds may produce airborne toxins or irritants. Indoor air quality issues can also stem from inadequate ventilation, chemical contamination from indoor or outdoor sources, and other biological contaminants such as pollen, viruses and bacteria. Indoor exposure to airborne toxins or irritants above certain levels can be alleged to cause a variety of adverse health effects and symptoms, including allergic or other reactions. As a result, the presence of significant mold or other airborne contaminants at any of our properties could require us to undertake a costly remediation program to contain or remove the mold or other airborne contaminants from the affected property or increase indoor ventilation. In addition, the presence of significant mold or other airborne contaminants could expose us to liability from our tenants, employees of our tenants or others if property damage or personal injury occurs. We are not presently aware of any material adverse indoor air quality issues at our properties that have not been previously addressed or remediated by us.

Before completing any property acquisition, we obtain environmental assessments in order to identify potential environmental concerns at the property. These assessments are carried out in accordance with the Standard Practice for Environmental Site Assessments (ASTM Practice E 1527-05) as set by ASTM International, formerly known as the American Society for Testing and Materials, and generally include a physical site inspection, a review of relevant federal, state and local environmental and health agency database records, one or more interviews with appropriate site-related personnel, review of the property’s chain of title and review of historical aerial photographs and other information on past uses of the property. These assessments are limited in scope, however, if recommended in the initial assessments, we may undertake additional assessments such as soil and/or groundwater samplings or other limited subsurface investigations and ACM or mold surveys to test for substances of concern. A prior owner or operator of a property or historic operations at our properties may have created a material environmental condition that is not known to us or the independent consultants preparing the site assessments. Material environmental conditions may have arisen after the review was completed or may arise in the future, and future laws, ordinances or regulations may impose material additional environmental liability. If environmental concerns are not satisfactorily resolved in any initial or additional assessments, we may obtain environment insurance policies to insure against potential environmental risk or loss depending on the type of property, the availability and cost of the insurance and various other factors we

deem relevant (i.e., an environmental occurrence affects one of our properties where our lessee may not have the financial capability to honor its indemnification obligations to us).

Generally, our leases provide that the lessee will indemnify us for any loss or expense we incur as a result of the presence, use or release of hazardous materials on our property. However, our ultimate liability for environmental conditions may exceed the policy limits on any environmental insurance policies we obtain, if any. If we are unable to enforce the indemnification obligations of our lessees or if the amount of environmental insurance we carry is inadequate, our results of operations would be adversely affected.

InsuranceINSURANCE

Our tenants are generally required to maintain liability and property insurance coverage for the properties they lease from us pursuant to triple-net leases. Under such leases, our tenants are generally required to name us (and any of our lenders that have a mortgage on the property leased by the tenant) as additional insureds on their liability policies and additional named insured and/or loss payee (or mortgagee, in the case of our lenders) on their property policies. Tenants are required to maintain casualty coverage and most carry limits at 100% of replacement cost. Depending on the location of the property, losses of a catastrophic nature, such as those caused by earthquakes and floods, may be covered by insurance policies that are held by our tenant with limitations such as large deductibles or co-payments that a tenant may not be able to meet. In addition, losses of a catastrophic nature, such as those caused by wind/hail, hurricanes, terrorism or acts of war, may be uninsurable or not economically insurable. In the event there is damage to our properties that is not covered by insurance and such properties are subject to recourse indebtedness, we will continue to be liable for the indebtedness, even if these properties are irreparably damaged. See Item 1A. “Risk Factors - Risks Related to Our Business and Properties - Insurance on our properties may not adequately cover all losses and uninsured losses could materially and adversely affect us.”

In addition to being a co-insuredgenerally named as additional insureds on our tenants’ liability policies, we separately maintain commercial general liability coverage with per location limits of $1.0 million for each occurrence and $2.0 million general aggregate, and no policy maximum.aggregate. We also maintain primary property coverage on (i) all unleased properties, (ii) all properties for which such coverage is not required to be carried by a tenant and (iii) all properties for which we obtain such coverage but the costs of which are reimbursed by tenants. In addition, we maintain excess property coverage on all remaining properties and other property coverage as may be required by our lenders.

Item 1A. Risk Factors

Special Note Regarding Forward-Looking StatementsSPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the federal securities laws. In particular, statements pertaining to our businessSecurities Act and growth strategies, investment, financing and leasing activities and trends in our business, including trends inSection 21E of the market for long-term, triple-net leases of freestanding, single-tenant properties, contain forward-looking statements.Exchange Act. When used in this Annual Report on Form 10-K, the words “estimate,” “anticipate,” “expect,” “believe,” “intend,” “may,” “will,” “should,” “seek,” “approximately” or “plan,” or the negative of these words and phrases or similar words or phrases whichthat are predictions of or indicate future events or trends and which do not relate solely to historical matters are intended to identify forward-looking statements. You can also identify forward-looking statements by discussions of strategy, plans or intentions of management.

Forward-looking statements involve numerous risks and uncertainties and you should not rely on them as predictions of future events. Forward-looking statements depend on assumptions, data or methods which may be incorrect or imprecise and we may not be able to realize them. We do not guarantee that the transactions and events described will happen as described (or that they will happen at all).

The following risks and uncertainties, among others, could cause actual results and future events to differ materially from those set forth or contemplated in the forward-looking statements:

industry and economic conditions;

volatility and uncertainty in the financial markets, including potential fluctuations in the CPI;

our success in implementing our business strategy and our ability to identify, underwrite, finance, consummate, integrate and manage diversifying acquisitions or investments;

the financial performance of our traditional retail tenants and the demand for traditional retail space, particularly with respect to challenges being experienced by general merchandise retailers;

our ability to diversify our tenant base and reduce the concentration of our significant tenant;

the nature and extent of future competition;

increases in our costs of borrowing as a result of changes in interest rates and other factors;

our ability to access debt and equity capital markets;

our ability to pay down, refinance, restructure and/or extend our indebtedness as it becomes due;

our ability and willingness to renew our leases upon expiration and to reposition our properties on the same or better terms upon expiration in the event such properties are not renewed by tenants or we exercise our rights to replace existing tenants upon default;

the impact of any financial, accounting, legal or regulatory issues or litigation that may affect us or our major tenants;

our ability to manage our expanded operations;

our ability and willingness to maintain our qualification as a REIT;

uncertainties as to the completion and timing of our proposed Spin-Off, and the impact of the Spin-Off on our business; and

other risks inherent in the real estate business, including tenant defaults, potential liability relating to environmental matters, illiquidity of real estate investments and potential damages from natural disasters.

You are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date of this Annual Report on Form 10-K. While forward-looking statements reflect our good faith beliefs, they are not guarantees of future performance. We disclaim any obligation to publicly update or revise any forward-looking statement to reflect changes in underlying assumptions or factors, new information, data or methods, future events or other changes, except as required by law.

Set forth below are some (but not all) of the risk factors that could adversely affect our business and financial performance. Because we operate in a highly competitive and rapidly changing environment, new risk factors emerge from time to time, and it is not possible for management to predict all such risk factors, nor can management assess the impact of all such risk factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Given these risks and uncertainties, investors should not place undue reliance on forward-looking statements as a prediction of actual results.

Risks Related to Our Business and PropertiesRISKS RELATED TO OUR BUSINESS AND PROPERTIES

Risks related to commercial real estate ownership could reduce the value of our properties.

Our core business is the ownership of real estate that is leased to retail, service and distribution companies on a triple-net basis. Accordingly, our performance is subject to risks inherent to the ownership of commercial real estate, including:

inability to collect rent from tenants due to financial hardship, including bankruptcy;

changes in local real estate markets resulting in the lack of availability or demand for single-tenant retail space;

changes in consumer trends and preferences that reduce the demand for products/services of our tenants;

inability to lease or sell properties upon expiration or termination of existing leases;

environmental risks related to the presence of hazardous or toxic substances or materials on our properties;

subjectivity of real estate valuations and changes in such valuations over time;

illiquid nature of real estate compared to most other financial assets;

changes in laws and regulations, including those governing real estate usage and zoning;

changes in interest rates and the availability of financing; and

changes in the general economic and business climate.

The occurrence of any of the risks described above may cause the value of our real estate to decline, which could materially and adversely affect us.

Credit and capital market conditions may adversely affect our access to and/or the cost of capital.

Periods of volatility in the credit and capital markets negatively affect the amounts, sources and cost of capital available to us. We primarily use external financing to fund acquisitions and to refinance indebtedness as it matures. If sufficient sources of external financing are not available to us on cost effective terms, we could be forced to limit our acquisition activity and/or to take other actions to fund our business activities and repayment of debt, such as selling assets. To the extent that we access capital at a higher cost (reflected in higher interest rates for debt financing or lower stock price for equity financing), our acquisition yields, earnings per share and cash flow could be adversely affected.

Our tenants may fail to successfully operate their businesses, which could adversely affect us.

The success of our investments is materially dependent on the financial stability of our tenants’ financial condition and leasing practices. Adverse economic conditions such as high unemployment levels, interest rates, tax rates and fuel and energy costs may have an impact on the results of operations and financial condition of our tenants and result in a decline in rent or an increased incidence of default under existing leases. Such adverse economic conditions may also reduce overall demand for rental space, which could adversely affect our ability to maintain our current tenants and attract new tenants.

At any given time, our tenants may experience a downturn in their business that may weaken the operating results and financial condition of individual properties or of their business as whole. As a result, a tenant may delay lease commencement, decline to extend a lease upon its expiration, fail to make rental payments when due, become insolvent or declare bankruptcy. We depend on our tenants to operate the properties we own in a manner which generates revenues sufficient to allow them to meet their obligations to us, including their obligations to pay rent, maintain certain insurance coverage and pay real estate taxes and maintain the properties in a manner so as not to jeopardize their operating licenses or regulatory status. The ability of our tenants to fulfill their obligations under our leases may depend, in part, upon the overall profitability of their operations. Cash flow generated by certain tenant businesses may not be sufficient for a tenant to meet its obligations to us. Although our occupied properties are generally operationally essential to our tenants, meaning the property is essential to the tenant’s generation of sales and profits, this does not guarantee that a tenant’s operations at a particular property will be successful or that the tenant will be able to meet all of its obligations to us. Our tenants’ failure to successfully operate their businesses could materially and adversely affect us.

Single-tenant leases involve particular and significant risks related to tenant default.

Our strategy focuses primarily on investing in single-tenant triple-net leased properties throughout the U.S. The financial failure of, or default in payment by, a single tenant under its lease is likely to cause a significant reduction in, or elimination of, our rental revenue from that property and a reduction in the value of the property. We may also experience difficulty or a significant delay in re-leasing or selling such property. This risk is magnified in situations where we lease

multiple properties to a single tenant under a master lease.lease, such as our three master leases with Shopko. The failure or default of a tenant under a master lease could reduce or eliminate rental revenue from multiple properties and reduce the value of such properties. Although the master lease structure may be beneficial to us because it restricts the ability of tenants to individually remove underperforming properties from the portfolio of properties leased from us, there is no guarantee that a tenant will not default in its obligations to us or decline to renew its master lease upon expiration. The default of a tenant that leases multiple properties from us could materially and adversely affect us.

A substantial number of our properties are leased to one tenant, Shopko, which may result in increased risk due to tenant and industry concentration.

As of December 31, 2017, Shopko represents our most significant tenant. Currently we lease 11699 properties to Shopko, primarily pursuant to 13three master leases.leases (relating to 59, 34 and 4 properties, respectively) and two single site leases, under which we received approximately $3.9 million in Contractual Rent per month. The Shopko leases are guaranteed by Specialty Retail Shops Holding Corp., the parent company of Shopko. Revenues generated from Shopko represented 8.2%7.7% of our Normalized Rental RevenueContractual Rent for the month ended December 31, 2016.2017. Because a significant portion of our revenues are derived from rental revenues received from Shopko, any default, breach or delay in the payment of rent by Shopko may materially and adversely affect us.

As a result of the significant number of properties leased to Shopko, our results of operations and financial condition are closely tiedsignificantly impacted to Shopko's performance under its leases, which is ultimately tied to the performance of its stores and the retail industry in which it operates. Shopko operates as a multi-department general merchandise retailer and retail health services provider primarily in mid-size and large communities in the Midwest, Pacific Northwest, North Central and Western Mountain states. Shopko is subject to the following risks, as well as other risks that we are not currently aware of, that could adversely affect its performance and thus its ability to pay rent to us:

The retail industry in which Shopko operates is highly competitive, which could impair its operations and liquidity, limit its growth opportunities and reduce profitability. Shopko competes with other discount retail merchants as well as mass merchants, catalog merchants, internet retailers and other general merchandise, apparel and household merchandise retailers. It faces strong competition from large national discount retailers, such as Walmart, Kmart and Target, and mid-tier merchants such as Kohl’s and J.C. Penney.

Shopko stores are geographically concentrated in the Midwest, Pacific Northwest, North Central and Western Mountain states. As a result, adverse economic conditions in these regions may materially and adversely affect its results of operations and retail sales.

The seasonality in retail operations may cause fluctuations in Shopko’s quarterly performance and results of operations and could adversely affect its cash flows.

Shopko stores are dependent on the efficient functioning of its distribution networks. Problems that cause delays or interruptions in the distribution networks could materially and adversely affect its results of operations.

Shopko stores depend on attracting and retaining quality employees. Many employees are entry-level or part-time with historically high rates of turnover.

IfBased on our monitoring of Shopko's financial information and recent liquidity events and other challenges, including bankruptcies, impacting the retail industry generally relative to recent years, we continue to be concerned about Shopko's ongoing ability to meet its obligations to us under its leases. Although Shopko is current on all of its obligations to us under its lease arrangements with us as of February 20, 2018, we can give you no assurance that this will continue to be the case, particularly if Shopko (not just the stores subject to leases with us) experiences a further decline in its business, financial condition orand results of operations itor loses access to liquidity. If such events were to occur, Shopko may request discounts or deferrals on the rents it pays to us, seek to terminate its master leases with us or close certain of its stores, or file for bankruptcy, all of which could significantly decrease the amount of revenue we receive from it.

While we seek to reduce the tenant concentration of Shopko, we may have difficulty in selling or leasing to other tenants the properties currently leased byto Shopko, due to, among other things, market demand or tax constraints. Furthermore, we can provide no assurance that we will deploy the proceeds from the disposition of any Shopko properties in a manner that would produce comparable or better yields.

A substantial portion of our properties are leased to unrated tenants and the tools we use to measure the credit quality of such tenants may not be accurate.