UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K10-K

(Mark One)

| | | | | |

| ☑ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20202023

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission file number 001-32426

WEX INC.

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | | | | |

| Delaware | | 01-0526993 |

(State or other jurisdiction of

incorporation or organization) | | (I.R.S. Employer

Identification No.) |

| | |

| 1 Hancock St., | Portland, | ME | | 04101 |

| (Address of principal executive offices) | | (Zip Code) |

(207) 773-8171

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Common Stock, $0.01 par value | | WEX | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

þ Yes ¨ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

¨ Yes þ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

þ Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S–T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

þ Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b–2 of the Exchange Act.

| | | | | | | | | | | | | | | | | |

| Large accelerated filer | þ | | | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | | | Smaller reporting company | ☐ |

| | | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑þ

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b)

☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b–2 of the Act).

Act. ☐ Yes þ No

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant (assuming for the purpose of this calculation, but without conceding, that all directors, officers and any 10 percent or greater stockholders are affiliates of the registrant) as of June 30, 2020,2023, the last business day of the registrant’s most recently completed second fiscal quarter, was $7,140,251,666approximately $7.8 billion (based on the closing price of the registrant’s common stock on that date as reported on the New York Stock Exchange).

There were 44,190,99541,734,802 shares of the registrant’s common stock outstanding as of February 22, 2021.15, 2024.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Company’s definitive Proxy Statement to be delivered to stockholders in connection withproxy statement for the Company's 2021Company’s 2024 Annual Meeting of Stockholders (the "2021“2024 Proxy Statement"Statement”) are incorporated by reference into Part III of this 10–K. Such 2024 Proxy Statement will be filed with the Securities and Exchange Commission within 120 days of the Company’s fiscal year ended December 31, 2023. With the exception of the sections of the 20212024 Proxy Statement specifically incorporated herein by reference, the 20212024 Proxy Statement is not deemed to be filed as part of this Annual Report on 10–K.

| | | | | | | | |

| TABLE OF CONTENTS | |

| | |

| | |

| | |

| | |

| Business | | |

| Risk Factors | | |

| | |

| Properties | | |

| Legal Proceedings | | |

| Mine Safety Disclosures | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

Item 9A. | Controls and Procedures | |

Item 9B. | Other Information | |

Part III

|

Item 10.9A. | | |

| Executive Compensation | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| Form 10–K Summary

| | |

| | |

| |

Unless otherwise indicated or required by the context, the terms “we,” “us,” “our,” “WEX,” or the “Company,” in this Annual Report on Form 10–10–K mean WEX Inc. and all of its subsidiaries that are consolidated under Generally Accepted Accounting Principlesaccounting principles generally accepted in the United States.

FORWARD–LOOKING STATEMENTS

The Private Securities Litigation Reform Act of 1995 provides a “safe harbor” for statements that are forward-looking and are not statements of historical facts. This Annual Report on Form 10-K includes forward-looking statements including, but not limited to, statements about management’s planplans and goals and statements of strategic priorities included within the “Strategy” section of this Annual Report in Item 1.goals. Any statements in this Annual Report that are not statements of historical facts are forward-looking statements. When used in this Annual Report, the words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “project”“project,” “will,” “positions,” “confidence,” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such words. Forward-looking statements relate to our future plans, objectives, expectations and intentions and are not historical facts and accordingly involve known and unknown risks and uncertainties and other factors that may cause the actual results or performance to be materially different from future results or performance expressed or implied by these forward-looking statements. The following factors, among others, could cause actual results to differ materially from those contained in forward-looking statements made in this Annual Report and in oral statements made by our authorized officers:

•the extent to which the coronavirus (COVID-19) pandemic and measures taken in response thereto impact our business, results of operations and financial condition in excess of current expectations;

•the demand for worldwide travel as a result of COVID-19 and the length of time it may take for the travel industry to experience a rebound after the effects of the COVID-19 pandemic have subsided;

•the impact of fluctuations in demand for fuel and the volatility and prices of fuel, including fuel spreads in the impact of any continued reductions in fuel priceCompany’s international markets, and the resulting impact on ourthe Company’s margins, revenues, and net income;

•the effects of general economic conditions, including COVID-19, on fueling patterns, as well asa decline in demand for fuel, corporate payment services, travel related services, or healthcare related products and transaction processing activity;services;

•our compliance, or ourthe failure to comply with the applicable requirements of MasterCardMastercard or Visa;

•any limitation, reduction, or elimination of interchange fees;Visa contracts and rules;

•the impact of foreign currency exchange rates onextent to which unpredictable events in the locations in which the Company or the Company’s operations, revenue and income;

•changes in interest rates;

•the effects ofcustomers operate or elsewhere may adversely affect the Company’s employees, ability to conduct business, expansionresults of operations and acquisition efforts;

•potential adverse changes to business or employee relationships, including those resulting from the completion of an acquisition;

•competitive responses to any acquisitions;

•uncertainty of the expected financial performance of the combined operations following completion of an acquisition;

•the failure to complete or successfully integrate and realize anticipated benefits, synergies and cost savings from the Company’s acquisitions, including the recently competed eNett and Optal acquisition;

•unexpected costs, charges or expenses resulting from an acquisition;

•the Company’s failure to successfully acquire, integrate, operate and expand commercial fuel card programs;

•the failure of corporate investments to result in anticipated strategic value;condition;

•the impact and size of credit losses, including fraud losses, and other adverse effects if the Company fails to adequately assess and monitor credit risk or fraudulent use of our payment cards or systems;

•the impact of changes to the Company’s credit standards;

•limitations on, or compression of, interchange fees;

•the effect of adverse financial conditions affecting the banking system;

•the impact of increasing scrutiny with respect to our environmental, social and governance practices;

•failure to implement new technologies and products;

•the failure to realize or sustain the expected benefits from our cost and organizational operational efficiencies initiatives;

•the failure to compete effectively in order to maintain or renew key customer and partner agreements and relationships, or to maintain volumes under such agreements;

•the ability to attract and retain employees;

•the ability to execute the Company’s business expansion and acquisition efforts and realize the benefits of acquisitions we have completed;

•the failure to achieve commercial and financial benefits as a result of our strategic minority equity investments;

•the impact of foreign currency exchange rates on the Company’s operations, revenue and income and other risks associated with our operations outside the United States;

•the failure to adequately safeguard custodial HSA assets;

•the incurrence of impairment charges if the Company’s assessment of the fair value of certain of its reporting units changes;

•the uncertainties of investigations and litigation;

•the ability of the Company to protect its intellectual property and other proprietary rights;

•the impact of regulatory capital requirements and other regulatory requirements on the operations of WEX Bank or its ability to make payments to WEX Inc.;

| | | | | |

| Table of Contents | FORWARD-LOOKING STATEMENTS |

•the impact of the Company’s debt instruments on the Company’s operations;

•the impact of leverage on the Company’s operations, results or borrowing capacity generally;

•changes in interest rates, including those which we must pay for our deposits, and the rate of inflation;

•the ability to refinance certain indebtedness or obtain additional financing;

•the actions of regulatory bodies, including tax, banking and securities regulators, or possible changes in tax, banking or financial regulations impacting the Company’s industrial bank, the Company as the corporate parent or other subsidiaries or affiliates;

•the failure to comply with the Treasury Regulations applicable to non-bank custodians;

•the impact from breaches of, or other issues with, the Company’s technology systems or those of ourits third-party service providers and any resulting negative impact on ourthe Company’s reputation, liabilities or relationships with customers or merchants;

•the Company’s abilityimpact of regulatory developments with respect to successfully obtain new customersprivacy and commercial agreements, maintain key commercial agreements, or maintain customer volumes under such commercial agreements;

•failure to expand the Company’s technological capabilities and service offerings as rapidly as the Company’s competitors;

•failure to successfully implement the Company’s information technology strategies and capabilities in connection with its technology outsourcing and insourcing arrangements and any resulting cost associated with that failure;

•the regulation, supervision, and examination of our business or our entities by domestic and foreign governmental authorities, as well as litigation and regulatory actions;

•the effect of the United Kingdom’s departure from the European Union and the resulting trade agreement;data protection;

•the impact of any disruption to the transition from LIBOR as a global benchmarktechnology and electronic communications networks we rely on;

•the ability to a replacement rate;incorporate artificial intelligence in our business successfully and ethically;

•the ability to maintain effective systems of internal controls;

•the impact of the 2016 Credit Agreement, the Notesprovisions in our charter documents, Delaware law and the Convertible Notes onapplicable banking laws that may delay or prevent our operations;

•the impact of increased leverage on the Company’s operations, results or borrowing capacity generally, and asacquisition by a result of acquisitions specifically;

•the impact of sales or dispositions of significant amounts of our outstanding common stock into the public market, or the perception that such sales or dispositions could occur;

•the possible dilution to our stockholders caused by the issuance of additional shares of common stock or equity-linked securities, whether as a result of the Convertible Notes or otherwise;

•the incurrence of impairment charges if our assessment of the fair value of certain of our reporting units changes;

•the uncertainties of litigation;third party; as well as

•other risks and uncertainties identified in Item 1A of this Annual Report and in connection with such forward-looking statements.

Our forward-looking statements and these factors do not reflect the potential future impact of any alliance, merger, acquisition, disposition or stock repurchases. The forward-looking statements speak only as of the date of the initial filing of this Annual Report and undue reliance should not be placed on these statements. We disclaim any obligation to update any forward-looking statements as a result of new information, future events or otherwise.

RISK FACTOR SUMMARY

Investment in our securities involves risk. Below is a summary of what we believe to be the principal risks facing our business. You should carefully review and consider this summary along with the risks described more fully in Item 1A, “Risk Factors” of Part I of this Annual Report and other information included in this Annual Report. The risks and uncertainties described below are not the only risks and uncertainties we face. Additional risks and uncertainties not presently known to us or that we presently deem less significant may also impair our business operations.

If any of the following risks occurs, our business, financial condition, and results of operations and future growth prospects could be materially and adversely affected, and the actual outcomes of matters as to which forward-looking statements are made in this report could be materially different from those anticipated in such forward-looking statements.

•Our operations, business, and financial condition have been and are expected to continue to be adversely affected by the COVID-19 pandemic. COVID-19 has negatively impacted the business and consumer spending habits which result in revenues for us and has impacted our workforce and operations and the operations of our customers, suppliers and business partners.

•A significant portion of our revenues are related to the dollar amount of fuel purchased by or through our customers and from our fuel retailer partners, and, as a result, a reduction in the demand for fuel and other vehicle products and services and/or volatility in fuel prices could have a material adverse effect on our revenues and financial condition.

•If we fail to comply with the applicable requirements of MasterCard or Visa, they could seek to fine us, suspend us or terminate our registrations. We depend on MasterCard or Visa to process a large number of transactions and any disruption or elimination of that ability could have a material adverse effect on our revenues and business.

•A substantial portion of our revenue is generated by network processing fees, known as interchange fees, associated with transactions processed using our payment systems. Any limitation, reduction or elimination of these fees, whether by regulation or by private actions or otherwise could have a material adverse effect on our revenues and business.

•If we fail to adequately assess and monitor credit risks posed by our counterparties or there is fraudulent use of our payment cards or systems, we could experience an increase in credit loss and other intangible damages. This could affect our results from operations as well as our business reputation, among other things.

•The payments solutions industry is highly competitive. Such competition could have a material adverse effect on the fees we receive, our margins, and our ability to gain, maintain, or expand customer relationships, all on favorable terms.

•We may never realize the anticipated benefits of acquisitions we have completed or may undertake and we may encounter difficulties in trying to integrate such acquisitions and incur significant expenses or charges as a result of an acquisition. In December 2020, we consummated the acquisition of two travel focused electronic payments companies that were significantly impacted by the global COVID-19 pandemic. Given that the global COVID-19 pandemic has had, and will likely continue to have, a large effect on the travel industry, there can be no guarantee that we will achieve any of the anticipated benefits from this acquisition.

•Unpredictable events, including natural catastrophes or public health crises, dangerous weather conditions, technology failure, political unrest, and terrorist attacks in the locations in which we or our customers operate, or elsewhere, may adversely affect our ability to conduct business and could impact our results.

•WEX Bank operates under an industrial loan charter (ILC), which allows us to accept brokered deposits, which we believe provides us access to lower cost funds than many of our competitors, thus helping us to offer competitive products. The loss or suspension of WEX Bank's industrial loan charter, changes in applicable regulatory requirements, or an increase in the number or type of institutions eligible for an ILC could be disruptive to certain of our operations, increase costs, and increase competition.

•We currently have a substantial amount of indebtedness and may incur additional indebtedness, which could affect our flexibility in managing our business and could materially and adversely affect our ability to meet our debt service obligations.At December 31, 2020, we had approximately $3,026.8 million of debt outstanding, net of unamortized debt issuance costs and debt discount, including $152.7 million in current liabilities.

•We may want or need to refinance a significant amount of indebtedness or otherwise require additional financing to react to changing economic or business conditions or to replace maturing debt, fund working capital, capital expenditures, acquisitions, or other general corporate purposes. In addition, our access to lenders in the future is also dependent on, among other things, market conditions, which are variable and potentially volatile, and which could result in increased costs for obtaining and servicing our indebtedness. Accordingly, there is no guarantee, however, that we will be able to finance or obtain additional financing on favorable terms, or at all.

•Existing and new laws and regulations and enforcement activities could negatively impact our business and the markets we presently operate in or could limit our expansion opportunities.These regulations can negatively impact our revenues and increase our compliance costs. In addition, failure to comply with laws and regulations may result in the suspension or revocation of licenses or registrations, the limitation, suspension or termination of services, and/or the imposition of civil and criminal penalties, including fines, among other things.

•If the technologies we use in operating our business and interacting with our customers fail, are unavailable, or do not operate to expectations, or we fail to successfully implement technology strategies and capabilities in connection with our outsourcing arrangements, our business and results of operations could be adversely impacted.

•Our business is regularly subject to cyberattacks and attempted security and privacy breaches and we may not be able to adequately protect our information systems, including the data we collect about our customers, which could subject us to liability and damage our reputation.

•Provisions in our charter documents, Delaware law, applicable banking law and the Convertible Notes may delay or prevent our acquisition by a third party.

•The issuance by us of additional shares of common stock or equity-linked securities, including in connection with conversions of our outstanding Convertible Notes (as defined below), may cause dilution to our stockholders.

ACRONYMS AND ABBREVIATIONS

The acronyms and abbreviations identified below are used in this Annual Report including the accompanying consolidated financial statements and the notes thereto. The following is provided to aid the reader and provide a reference point when reviewing the Annual Report:

| | | | | | | | |

| |

| 2017 Tax Act | | Tax Cuts and Jobs Act of 2017 |

2016Adjusted free cash flow | A non-GAAP measure calculated as cash flows from operating activities, adjusted for net purchases of current investment securities, capital expenditures, the change in net deposits, changes in borrowings under the BTFP and borrowed federal funds and certain other adjustments. |

| Adjusted net income or ANI | A non-GAAP measure that adjusts net income (loss) attributable to shareholders to exclude all items excluded in segment adjusted operating income except unallocated corporate expenses, further excluding unrealized gains and losses on financial instruments, net foreign currency gains and losses, debt issuance cost amortization, tax related items and certain other non-operating items, as applicable depending on the period presented. |

| Amended and Restated Credit Agreement | | Amended and Restated Credit agreementAgreement entered into on JulyApril 1, 2016, as2021 (as amended from time to time,time) by and among the Company and certain of its subsidiaries, as borrowers, WEX Card Holding Australia Pty Ltd., as designated borrower, and Bank of America, N.A., as administrative agent on behalf of the lenders. |

| 2017 Tax Act | Tax Cuts and Jobs Act of 2017 |

Adjusted Net Income or ANIAscensus Acquisition | | A non-GAAP measure that adjusts net income attributable to shareholders to exclude unrealized gainsThe acquisition from Ascensus, LLC of certain entities, which comprised the health and losses on financial instruments, net foreign currency remeasurement gains and losses, acquisition-related intangible amortization, other acquisition and divestiture related items, loss on salebenefits business of subsidiary, stock-based compensation, restructuring and other costs, legal settlement, impairment charges, debt restructuring and debt issuance cost amortization, non-cash adjustments related to tax receivable agreement, similar adjustments attributable to our non-controlling interests and certain tax related items. |

AOC | | AOC Solutions and one of its affiliate companies, 3Delta Systems, Inc.Ascensus. |

| ASC | | Accounting Standards Codification |

| |

| |

| |

| | |

ASU 2014–09 | | Accounting Standards Update No. 2014–09 Revenue from Contracts with Customers (Topic 606) |

ASU 2016–01 | | Accounting Standards Update No. 2016–01 Financial Instruments–Overall (Subtopic 825–10): Recognition and Measurement of Financial Assets and Financial Liabilities

|

ASU 2016–02 | | Accounting Standards Update No. 2016–02 Leases (Topic 842)

|

| | |

ASU 2016–13 | | Accounting Standards Update No. 2016–13 Financial Instruments–Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments

|

| | |

ASU 2017–04 | | Accounting Standards Update 2017–04–Intangibles–Goodwill and Other (Topic 350): Simplifying the Test for Goodwill Impairment

|

| | |

| | |

Australian Securitization Subsidiary | | Southern Cross WEX 2015-1 Trust, a special purpose entity consolidated by the Company |

| |

| |

| |

| |

| |

| Average number of SaaS accounts | | Represents the average number of active consumer-directed health, COBRA, and billing accounts on our SaaS platforms. SaaS accounts include HSA accounts for which WEX Inc. serves as the non-bank custodian under designation by the U.S. Department of Treasury. |

| B2B | Business-to-Business |

| benefitexpress | Benefit Express Services, LLC, a provider of highly configurable, cloud-based benefits administration technologies and services, and its indirect and direct parents, which were acquired on June 1, 2021 and merged into WEX Health, Inc. on April 30, 2022. |

| BTFP | Business-to-businessThe Federal Reserve Bank Term Funding Program, which provides liquidity to U.S. depository institutions. |

| CDH | | Consumer-directedConsumer directed healthcare |

CompanyCFPB | Consumer Financial Protection Bureau |

| CODM | Chief Operating Decision Maker |

| Company | WEX Inc. and all entities included in the consolidated financial statementsstatements. |

| Consolidated EBITDA | A non-GAAP measure calculated in accordance with the terms of the Company’s Amended and Restated Credit Agreement. |

| Convertible Notes | | Convertible senior unsecured notes due on July 15, 2027 in an aggregate principal amount of $310$310.0 million with a 6.5 percent interest rate, issued July 1, 2020.2020, which were repurchased by the Company and canceled by the trustee at the instruction of the Company on August 11, 2023. |

COVID-19 or (“coronavirus”) | Corporate Cash | Calculated in accordance with the terms of our consolidated leverage ratio in the Company’s Amended and Restated Credit Agreement. |

| COVID-19 | An infectious disease caused by the SARS-CoV-2 virus.coronavirus. The World Health Organization declared the coronavirus outbreak a global pandemic on March 11, 2020. |

| | | | | |

| ACRONYMS AND ABBREVIATIONS |

| | | | | |

CFPBDCFM | | Consumer Financial Protection BureauDiscounted Cash Flow Method of valuation |

| Discovery Benefits | | Discovery Benefits, Inc.LLC, which was subsequently merged with and into WEX Health as of March 31, 2021. |

| DSUs | | Deferred stock units |

EBITDA | | A non-GAAP measure that adjusts income before income taxes to exclude interest, depreciation and amortizationStock Units held by non-employee directors. |

| EFS | | Electronic Funds Source, LLC, a provider of customized corporate payment solutions for fleet and corporate customers with a focus on the large and mid-sized over-the-road fleets. On July 1, 2016, the Company acquired WP Mustang Topco LLC, the indirect parent of Electronic Funds Source, LLC and Warburg Pincus Private Equity XI (Lexington), LLC, an affiliated entity, from investment funds affiliated with Warburg Pincus LLC. |

| | |

| eNett | | eNett International (Jersey) Limited |

European Fleet businessEVs | | WEX Fleet Europe and WEX Europe Services, collectively |

European Securitization Subsidiary | | Gorham Trade Finance B.V., a special purpose entity consolidated by the CompanyElectric Vehicles |

| FASB | | Financial Accounting Standards Board |

| FCPA | | U.S. Foreign Corrupt Practices Act |

| FDIC | | Federal Deposit Insurance Corporation |

FinCENFederal Reserve Bank Discount Window | Monetary policy that allows WEX Bank to borrow funds on a short-term basis to meet temporary shortages of liquidity caused by internal or external disruptions. |

| FinCEN | Financial Crimes Enforcement Network of the U.S. Department of the Treasury |

FRAFleetOne | FleetOne Holdings, LLC and its direct and indirect subsidiaries |

| FRA | Federal Reserve Act |

| FSA | | Flexible Spending Accounts |

| GAAP | | Generally Accepted Accounting Principles in the United States |

| GILTI | | Global Intangible Low Taxed Income |

WEX Fleet Europe (Go Fuel Card)GPCM | Guideline Public Company Method of valuation |

| GPCs | A fleet business in Europe acquired from EG Group on July 1, 2019Guideline Public Companies |

| HRA | | Health Reimbursement Arrangements |

| HSA | | Health Savings AccountsAccount |

ICSICE | | Insured Cash SweepInternal Combustion Engine |

IndentureLIBOR | | The Notes were issued pursuant to an indenture dated as of January 30, 2013 among the Company, the guarantors listed therein, and The Bank of New York Mellon Trust Company, N.A., as trustee |

Legal Settlement | | The settlement of legal proceedings and appeals related to the acquisition of eNett and Optal.London Interbank Offered Rate |

| NAV | | Net asset valueAsset Value |

Net payment processinginterchange rate | | TheRepresents the percentage of the dollar value of each payment processing transaction that WEX records as revenue from merchants, less certain discounts given to customers and network fees. |

| Net late fee rate | Net late fee rate represents late fee revenue as a percentage of fuel purchased by fleets that have a payment processing relationship with WEX. |

| Net payment processing rate | The percentage of each payment processing $ of fuel that the Company records as revenue from merchants less certain discounts given to customers and network feesfees. |

| | |

| | |

| | |

| Notes | | $400400.0 million senior notes with a 4.75%4.75 percent fixed rate, issued on January 30, 2013, |

Noventis | | Noventis, Inc. which were redeemed in full by the Company on March 15, 2021. |

| NYSE | | New York Stock Exchange |

| OFAC | | The United States Treasury’s Office of Foreign Assets Control |

OptalOperating cash flow | Net cash provided by (used for) operating activities |

| Operating interest | Interest expense incurred on the operating debt obtained to provide liquidity for the Company’s short-term receivables or used for investing purposes in fixed income debt securities. |

| Optal | Optal Limited |

Over-the-roadOTA | Online travel agency |

| Over-the-road | Typically, heavy trucks traveling long distances |

Pavestone Capital | | Pavestone Capital, LLCdistances. |

Payment processing $ of fuel spend | | Total dollar value of the fuel purchased by fleets that have a payment processing relationship with the CompanyWEX. |

| | | | | |

| ACRONYMS AND ABBREVIATIONS |

| | | | | |

| Payment processing transactions | | Total number of purchases made by fleets that have a payment processing relationship with the Company where the Company maintains the receivable for the total purchasepurchase. |

Payment solutions purchasePBRSUs | Performance-based restricted stock units |

| PO Holding | PO Holding, LLC, a wholly-owned subsidiary of WEX Inc. and the direct parent of WEX Health. |

| |

| Processing costs | Expenses related to processing transactions, servicing customers and merchants and costs of goods sold related to hardware and other product sales. |

| Purchase volume | | TotalPurchase volume in the Corporate Payments segment represents the total dollar value of all WEX-issued transactions that use WEX corporate card products and virtual card products |

PBRSUs | | Performance-based restricted stock units |

| | |

| products. Purchase volume | | Total U.S. in the Benefits segment represents the total dollar value of all transactions in the Health and Employee Benefit Solutions segment where interchange is earned by the CompanyWEX. |

| | | | | | | | |

| Redeemable non-controlling interest | | The portion of the U.S. HealthBenefits business’ net assets owned by a non-controlling interest subjectholder, SBI, prior to redemption rights held by the non-controllingMarch 7, 2022 acquisition of SBI’s remaining interest in PO Holding. |

| Revolving Credit Facility | The Company’s secured revolving credit facility under the Amended and Restated Credit Agreement. |

| RSUs | | Restricted stock units |

| SaaS | Software-as-a-Service |

| SBI | Software-as-a-serviceSBI Investments, Inc., which is owned by State Bankshares, Inc., and was a minority interest holder in PO Holding, LLC. |

| SEC | | Securities and Exchange Commission |

| Segment adjusted operating income | | A non-GAAP measure that adjusts operating income to exclude specified items that the Company’s management excludes in evaluating segment performance, including unallocated corporate expenses, acquisition-related intangible amortization, other acquisition and divestiture related expenses and adjustments including the acquisition related intangible amortization, impairment charges, stock-based compensation, restructuring and other costs,items, debt restructuring costs, stock-based compensation, other costs and unallocated corporate expenses.certain non-recurring or non-cash operating charges that are not core to our operations, as applicable depending on the period presented. |

| Service fees | | Costs incurred from third-party networks utilized to deliver payment solutions and other third-parties utilized in performing services directly related to generating revenue. |

| SOFR | Secured Overnight Financing Rate |

| SPE | Wholly-owned special purpose entity |

| Topic 320 | Accounting Standards Codification Section 320, Debt Securities |

| Topic 606 | Accounting Standards Codification Section 606, Revenue from Contracts with Customers |

| Total volume | Includes purchases on WEX-issued accounts as well as purchases issued by others, but using a WEX platform. |

| TSR | | Total shareholder return |

Transaction processing transactionsUDFI | | Unfunded payment transactions where the Company is the processor and only has receivables for the processing fee |

UNIK or WEX Latin America | | UNIK S.A., the Company’s Brazilian subsidiary, which is branded WEX Latin America. This subsidiary was sold on September 30, 2020 |

U.S. Health business | | WEX Health and Discovery Benefits, collectively |

Utah DFI | | Utah Department of Financial Institutions |

VCNU.S. Benefits business | (i) prior to March 31, 2021, WEX Health, Inc. and Discovery Benefits, LLC., collectively, (ii) from March 31, 2021 to June 1, 2021, WEX Health, Inc., (iii) from June 1, 2021 to April 30, 2022, WEX Health, Inc. and benefitexpress, collectively, and (iv) from April 30, 2022, WEX Health, Inc. |

| VCN | Virtual card number |

VPNWACC | | Virtual private networkWeighted Average Cost of Capital |

| WEX | | WEX Inc., and all of its subsidiaries that are consolidated under accounting principles generally accepted in the United States, unless otherwise indicated or required by the contextcontext. |

| WEX Australia | WEX Card Holdings Australia Pty Ltd and its subsidiaries |

| | | | | |

| ACRONYMS AND ABBREVIATIONS |

| | | | | |

| WEX Bank | An industrial bank organized under the laws of the State of Utah, and wholly owned subsidiary of WEX Inc. |

| WEX Europe Services | | AWEX Europe Service Limited, a European FleetMobility business acquired by the Company from ExxonMobil on December 1, 2014 |

| WEX Health | WEX Health, Inc., the Company’s healthcare technology and administration solutions provider/business. |

| WEX Payments | Legacy healthcare operations prior to the acquisition of Discovery Benefits

WEX Payments Inc. (formerly known as Noventis, Inc.) |

PART I

ITEM 1. BUSINESS

Our Company

WEX’s mission is focused on simplifying the business of running a business. WEX Inc.owns and operates a B2B ecosystem that helps our customers overcome highly manual processes and reconciliations, navigate the complexity of consumer driven healthcare benefits, and solve their administrative challenges. We believe that WEX offers the marketplace a unique combination of capabilities to simplify complexity, thereby setting WEX’s offerings apart from those of our competition, including:

•Global commerce platform. Our technology is engineered and operated with global scale and reliability. We have invested heavily, and expect to continue to invest, in technology. Using our technology, our customers have trusted us to conduct hundreds of billions of dollars in money movements in more than 20 currencies. We believe that our products and services play integral roles in the infrastructure of businesses.

•Personalized solutions, seamlessly embedded. We believe WEX is a leading financial technology service provider having simplifiedleader in our end markets with solutions shaped by customer focused innovation and deep industry expertise. Both in our direct-to-corporate and partner channels, our solutions focus on simplifying the complexitiesbusiness of payment systemsrunning a business by deeply embedding our solutions within our end customer workflows.

•Insights that power success. Customers look to WEX for a powerful combination of specialized expertise and rich data to assist them in driving better decisions, moving more quickly, and in dealing with risk. We put control in the hands of our customers.

The combination of our capabilities across continentssegments forms a diverse B2B ecosystem for us to provide products and industries. We currently operateservices to our customers, as depicted in the following graphic:

Our Ecosystem of Solutions

Incorporates the Best of Our Vertical Expertise and the Power of Our Commerce Platform

WEX Solutions Ecosystem

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| Simplify Benefits | Reimagine Mobility | Pay & Get Paid |

| | | | | | | | |

| | | | | | | | |

CDH Program

Management | Non-Bank

Custodian | Benefits

Administration | Analytics &

Controls | Proprietary

Network | EV & Mixed

Fleets | Expense

Management | Workflow

Automation | Fraud

Controls |

| | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| Global Commerce Platform |

| | | | | | |

| | | | | | |

| Payments | Access to Funds | API Integration | Flexible UIs | Global Omnichannel

Servicing | Scalable Data,

Analytics, AI | Risk & Security |

| | | | | | |

Leveraging these unique capabilities, WEX offers solutions that organizations use to drive efficiencies and manage risk. These solutions, which share and benefit from our underlying capabilities, are provided across the following three reportablebusiness segments: Fleet Solutions, Travel and Corporate Solutions, and Health and Employee Benefit Solutions, which are described in more detail below. The Company’s U.S. operations include WEX Inc., the majority-owned U.S. Health business (currently consisting of WEX Health and Discovery Benefits), and our wholly-owned subsidiaries

| | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| | | | | | |

Mobility WEX reimagines mobility across fleets of all sizes. WEX has more than 600,000 mobility customers worldwide. | | | Benefits WEX simplifies administration of benefits for employers, including consumer directed health accounts in the United States both directly and through partners. We serve more than half of the Fortune 1000 companies in the United States. | | | Corporate Payments WEX is both one of the largest commercial payment companies in the world as well as a trusted technology partner for some of the largest organizations in the world. WEX is unique in our space as we couple wholly owned market leading technology with a global issuing and funding capability. |

| | | | | | |

Our wholly owned subsidiary, WEX Bank, WEX FleetOne, Noventis and EFS. Our international operations include our wholly-owned operations including, WEX Fuel Cards Australia, WEX Prepaid Cards Australia, WEX Canada, WEX Asia, WEX Europe Limited, WEX Fleet Europe, and eNett and Optal and their respective operating subsidiaries, and a controlling interest in WEX Europe Services Limited and its subsidiaries.

WEX Bank, a Utah industrial bank incorporated in 1998, is an FDIC insured depository institution. The functions performed at WEX Bank contribute to the U.S. and Canadian operations of Fleet Solutions andcurrently funds the majority of operations of Travelour Mobility and Corporate Solutions by providingPayments operations, provides us with a funding mechanism, among other services. Withnumber of services, including credit adjudication, and is a depository institution for certain HSA cash assets. We believe that our ownership of WEX Bank we haveprovides us with a competitive advantage through access to low-costlow cost sources of capital. WEX Bank raises capital primarily through the issuanceand liquidity and enables us to design funding solutions for customers that complement our technology solutions.

Our ecosystem of brokered deposit accounts andsolutions provides the financingCompany with multiple and makes credit decisions that enablediverse levers and opportunities to help WEX achieve its financial and business goals. Current goals include winning new customers, growing our share of wallet, expanding and diversifying our offering, deepening our global presence, and executing strategic mergers and acquisitions. Our existing and evolving technology, talented workforce, and robust customer and partner footprint all continue to drive our business forward and we expect will help us achieve our goals. We have established a growth engine in large end markets and we are a leader in the Fleet Solutions and Travel and Corporate Solutions segments to extend credit to customers. WEX Bank approves customer applications, maintains appropriate credit lines for each customer, is the account issuer, and is the counterparty for the customer relationships for mostmarkets in which we participate.

Seasonality

Certain parts of our programsbusiness are affected by seasonal variations. For example, in a typical year, fuel prices are typically higher during the summer and online travel sales are typically higher during the third quarter. In addition, we experience seasonality in our Benefits segment as consumer spend is correlated with insurance deductibles, typically resulting in higher spend in the U.S. Operations such as sales, marketing, merchant relations, customer service, software development and IT are performed as a service within our organization but outside of WEX Bank. WEX Bank’s primary regulators are Utah DFI and the FDIC. The activities performed by WEX Bank are integrated into the operations of our Fleet Solutions and Travel and Corporate Solutions segments. The relationship between WEX Inc. and WEX Bank is governed under a master service agreement, which establishes the parametersearly part of the services described above.

Recent Developments

Acquisition of eNett and Optal

On January 24, 2020, the Company entered into a purchase agreement to purchase eNett, a leading provider of B2B payments solutions to the travel industry, and Optal, a company that specializes in optimizing B2B transactions, for an aggregate purchase price comprised of $1.3 billion in cash and 2.0 million shares of the Company’s common stock, subject to customary closing conditions, including the absence of a Material Adverse Effect (as defined in the purchase agreement between WEX, eNett and Optal, among others). The Company concluded that the COVID-19 pandemic and conditions arising in connection with it had a Material Adverse Effect on the eNett and Optal businesses, disproportionate to the effect on othersyear until employees meet their deductibles.

in the relevant industry. Because of this Material Adverse Effect, WEX formally advised eNett and Optal on May 4, 2020 that it was not required to close the transaction pursuant to the terms of the purchase agreement. On May 11, 2020, the shareholders of eNett and Optal each initiated separate legal proceedings in the High Court of Justice of England and Wales in the United Kingdom against the Company seeking a declaration that no Material Adverse Effect had occurred and an order for specific performance of WEX's obligations under the purchase agreement. From September 21, 2020 through September 29, 2020, a London court held a trial of certain preliminary issues. On October 12, 2020, the Court handed down its judgment, which concluded, among other things, that the Optal and eNett Groups operate in the payments industry and the B2B payments industry and that, for the purpose of the definition of the Material Adverse Effect clause, the relevant industry is the B2B payments industry. The Court found that there was no travel payments industry, as argued for by eNett and Optal. This finding meant that when determining whether eNett or Optal have been disproportionately impacted by the pandemic, a comparison would be made against other B2B payments companies. The Company and the claimants each sought permission to appeal certain portions of the Court’s judgment.On December 15, 2020, the Company entered into a Deed of Settlement (the “Settlement Deed”) with eNett, Optal and the other parties thereto providing for, among other things, (i) the dismissal with prejudice of the legal proceedings and appeals described above, (ii) the amendment of original purchase agreement and (iii) the release of all claims capable of arising out of, or in any way connected with or relating to the COVID-19 pandemic, but excluding any claims arising under the amended purchase agreement. The closing of the acquisition occurred concurrent with the execution of the Settlement Deed on December 15, 2020. The amended purchase agreement provided for, among other things, a reduction of the aggregate purchase price for the acquisition to $577.5 million (subject to certain adjustments) consisting entirely of cash, which the company paid with cash on hand, and the closing of the acquisition occurring concurrent with the execution of the Settlement Deed on December 15, 2020. The Company determined the aggregate purchase price represents consideration paid for the businesses acquired and for the settlement of legal proceedings described above. The preliminary fair value of the businesses acquired was estimated to be $415.0 million using a discounted cash flow analysis and guideline transaction method. Since the Company was not able to reliably estimate the fair value of the legal settlement, the residual value of $162.5 million has been allocated to the legal proceedings settlement, which has been included in legal settlement expense in the consolidated statement of operations for the year ended December 31, 2020.Key Developments

| | | | | |

| Renamed reportable segments •In connection with a rebranding initiative, during the first quarter of 2023 the Company renamed its existing reportable segments. The Fleet Solutions segment was renamed to Mobility, the Travel and Corporate Solutions segment was renamed to Corporate Payments and the Health and Employee Benefits Solutions segment was renamed to Benefits. There were no changes to the composition of our reportable segments. |

| |

| |

| EV-related initiatives •We have made progress against many of our EV-related initiatives, including our DriverDash® mobile app, which we recently expanded to include EV functionality. This means that, through their existing WEX portal, fleet managers can enable their cards for EV charging and use our integrated app, DriverDash®, to find, activate, pay for, and track charges all on one credit line, invoice, dataset, and management interface. This simplifies customer workflows while eliminating the need for drivers to have multiple fobs and apps in order to manage their mixed fleet. We have also launched an at-home reimbursement product in the U.S. We began rolling out the initial phase of this product during the fourth quarter of 2023, and expect to roll out depot functionality later in 2024. •During 2023, our Board of Directors authorized the Company to invest up to $100 million through 2025 in predominantly early-stage companies focused on the energy transition. To-date, the Company has invested a total of $7.5 million in three such minority investments and has entered into subscription and limited partnership agreements for the investment of up to an additional $10 million in two venture capital funds that invest in climate/alternative energy technologies. |

| |

| |

| Cloud migration •We accomplished our cloud migration goal with the full migration of the Benefits segment in the third quarter of 2023. All of our core technology is now cloud-based. In an effort to reduce our dependency on physical data centers, during the fourth quarter of 2023 we achieved our data center reduction goal of consolidating from 33 data centers in 2019 to seven by the end of 2023. We will continue our Cloud-first development philosophy, which enables improved data security, infrastructure resiliency, system availability, and speed to market. |

| |

| |

| Business acquisitions •During the third quarter of 2023, we acquired a collection of entities from Ascensus, LLC that provide employee health benefit accounts. We believe the technology of these acquired entities complements ours, while increasing our scale in the Benefits space and expanding our Benefits product offering with their Affordable Care Act compliance and dependent verification capabilities. •During the fourth quarter of 2023 we acquired Payzer, a leading cloud-native field service management software provider. We expect Payzer to strengthen our relationships with vertical customers in our Mobility segment, allowing us to match our payments capabilities with integrated software that creates durable value to our customer base. Payzer's high-growth, top-tier service offering and feature set, which includes end-to-end business management software and enables a wide range of payment solutions, is at the convergence of SaaS and payments. |

| |

| |

| AI experiments •We have conducted AI experiments across the enterprise, which have driven customer-focused outcomes, uncovered opportunities for workflow efficiencies, and identified many other opportunities for us to continue driving value by leveraging these technologies. We believe our efforts in using machine learning in credit adjudication and monitoring have helped reduce delinquencies significantly in 2023 as seen in our credit loss results. |

| |

| |

| Operational improvement efforts •By the end of 2023 we achieved $75 million in run-rate cost savings and are on track to generate $100 million by the end of 2024. We are reinvesting a portion of these cost savings in enhancing our capabilities, including digital products, technology and risk management capabilities and tools. |

On September 30, 2020, the Company sold its wholly-owned subsidiary UNIK S.A, (the "WEX Latin America" business). The operations of WEX Latin America were primarily included in the Health and Employee Benefit Solutions segment through the date of sale. A pre-tax loss on sale of subsidiary of $46.4 million, has been reflected in the consolidated statement of operations for the year ended December 31, 2020. The Company decided to sell UNIK S.A. because it no longer aligned with the strategic direction of the Company.

Our Business Segments

Overview

Our Fleet SolutionsWithin our Mobility segment, WEX is a leader in fleet vehicle payment solutions, transaction processing, services specifically designed forand information management services. We address the marketplace through three different business units.

•North American Fleet. Addresses the needs of large fleets, government fleets, over-the-road carriersbusinesses that utilize primarily light and small businesses. medium duty vehicles central to the operation of the service economy in North America.

•Over-the-Road. Addresses the needs of businesses that utilize primarily medium and heavy duty vehicles central to the operation of the freight economy in North America.

•International Fleet. Addresses the needs of businesses that utilize primarily light and medium duty vehicles central to the operation of the service economy outside of North America inclusive of our Fleet portfolios in Europe and Asia-Pacific.

As of December 31, 2020, 15.82023, more than 19 million vehicles useused our payment solutions for fleet management.

SalesSolution

We believe our key source of differentiation in the Mobility segment is the enhanced data and controls we provide fleet operators based on our proprietary closed loop payments network. This proprietary closed-loop network enables us to capture rich data, deploy custom controls, and establish the economics between fleets and merchants. Our data and tools allow fleet owners and managers to control spend and limit fraud while optimizing their fleet operations. At the point-of-sale, we capture an array of information. Examples of information captured, which varies by type of customer, include the amount of the purchase, the driver, the vehicle, the odometer reading, the fuel or vehicle maintenance provider, and the items purchased. We provide standard and personalized information to customers through vehicle analysis reports, custom reports, and our websites. We also alert customers of unusual transactions or those that fall outside of pre-established parameters. Customers can access their account information through our platform including account history and recent transactions and download the related details. In addition, fleet managers can elect to be notified when limits are exceeded in specified purchase categories, including limits on transactions within a time range and gallons per day. In the over-the-road space, we additionally offer fleets customizable payment solutions including real-time interactive and seamless interfaces delivering data integrity, alternative payment and money transfer options, comprehensive settlement solutions, real-time reports and analytics for compliance and cost-optimization and fuel reconciliation and mobile optimization tools.

In conjunction with the above, we offer our mobility customers the following additional products and services:

•Account activation and account retention: We provide activation and retention services that promote the adoption and use of our products.

•Authorization and billing inquiries and account maintenance: We handle authorization and billing questions, account changes, and other issues through our dedicated contact centers, which are available 24 hours a day, seven days a week. Self-service options are also provided through our online tools.

•Account management: We assign account managers to customers who operate large fleets. Our account managers have in-depth knowledge of both our programs and the objectives of the fleets they service.

•Credit and collections services: We extend short term credit in the majority of Mobility transactions. Related to this service we have developed proprietary account approval, underwriting, credit management, and collections programs.

•Merchant services: Our representatives work with fuel and vehicle maintenance providers to enroll these providers in our network, test all network technology, and provide training on our processes.

•Analytics solutions: We provide customers with access to analytics platforms and custom reporting tools targeted toward identifying cost savings opportunities and managing their fleet.

•Ancillary services and offerings: We provide a variety of ancillary services and tools to fleets to help them better manage expenses and capital requirements. Additionally, beginning in November 2023, we provide a cloud-native

software solution that has various capabilities, including scheduling, dispatch navigation, marketing and payment acceptance, to mobility field service customers in HVAC, roofing and other similar verticals.

Building upon our historical ICE-related fleet solutions, we are working on solutions we believe will ease the integration of EVs into mixed fleets. We are well positioned to help our customers transition to an expected mixed-fleet future. As fleet owners look to add vehicles powered by alternative energy sources, such as EVs, we are building on our deep experience in fleet and mobility in an attempt to develop and provide solutions to address specific customer needs, including charging, EV transition planning, and tools to successfully manage a mix of vehicle types ranging from connectivity to advanced route planning and carbon emissions reporting.

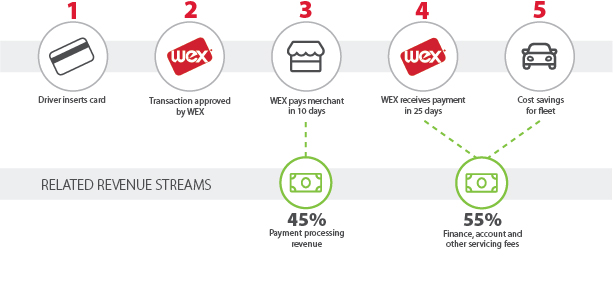

Payment processing transactions are the primary revenue source in Fleet Solutions and arethe Mobility segment. Revenue is earned based on a percentage of the aggregate dollar amount of the customer’s purchase, a fixed amount per transaction, or a combination of both. Normally, inIn a typical domestic payment processing transaction for which we extend short-term credit to the fleet cardholder, andwe pay the merchant within ten days, on average, for the purchase price, less the fees we retain and record as revenue.revenue according to their specific merchant agreement, which generally occurs within ten days. Revenue from our WEX Europe Services and Go Fuel Card operations is primarily derived from the difference between the negotiated price of the fuel from the supplier and the price charged to the fleet customer. In both types of transactions, weWe collect the total purchase price from the fleet customer, normallyour North America and international Mobility customers, typically within 2530 days from the billing date. In 2020, we processed approximately 464 million payment processing transactions, compared to approximately 505 million payment processing transactions in 2019.

The following illustration depicts our over-the-road fleet business, process for a typical closed-loop domestic fuel payment processing transaction and a breakdown of the related Fleet Solutions revenue streams:

At the point-of-sale, we capture an array of information including the amount of time between when we pay the expenditure,merchants and collect from our customers is significantly reduced relative to a typical North America or International Fleet transaction. There are instances, primarily within our over-the-road business, in which WEX processes a fleet customer transaction with the driver,merchant bearing the vehicle,credit risk and collecting the odometer reading,receivable from the fuel or vehicle maintenance provider and the items purchased. We provide standard and customized information to customers through monthly vehicle analysis reports, custom reports and our websites. We also alert customers of unusual transactions or transactions that fall outside of pre-established parameters. Customers can access their account information through our website including account history and recent transactions and download the related details. In addition, fleet managers can elect to be notified by email when limits are exceeded in specified purchase categories, including limits on transactions within a time range and gallons per day.fleet.

In the over-the-road space, we offer customizable payment solutions including real-time interactive and seamless interfaces delivering data integrity, alternative payment and money transfer options, comprehensive settlement solutions, real-time reports and analytics for compliance and cost-optimization and fuel reconciliation and mobile optimization tools.

In addition to revenue derived from payment processing transactions, we recognize account servicing revenue on fees charged to the cardholders, finance fee revenue on overdue accounts and other revenue through the followingon transaction processing revenue and miscellaneous other products and services:services.

•Customer service, account activation and account retention: We offer customer service, account activation and account retention services to fleets, fleet management companies and the fuel and vehicle maintenance providers on our network. Our services include promoting the adoption and use of our products and programs and account retention programs on behalf of our customers and partners.Distribution

•Authorization and billing inquiries and account maintenance: We handle authorization and billing questions, account changes and other issues for fleets through our dedicated customer contact centers, which are available 24 hours a day, seven days a week. Fleet customers also have self-service options available to them through our websites.

•Premium fleet services: We assign designated account managers to businesses and government agencies with large fleets. These representatives have in-depth knowledge of both our programs and the operations and objectives of the fleets they service.

•Credit and collections services: We have developed proprietary account approval, credit management and fraud detection programs. Our underwriting model produces a proprietary score, which we use to predict the likelihood of an account becoming delinquent at application and on an ongoing basis. We have developed a collections scoring model that we use to rank and prioritize past due accounts for collection activities. We also employ fraud specialists who monitor accounts, alert customers and provide case management expertise to minimize losses and reduce program abuse.

•Merchant services: Our representatives work with fuel and vehicle maintenance providers to enroll these providers in our network, test all network and terminal software and hardware, and to provide training on our sale, transaction authorization and settlement processes.

•Analytics solutions: We provide customers with access to web-based data analytics platforms and custom reporting tools that offer insights to fleet managers, including integrating and analyzing business fleet fuel purchases to uncover fraud, manage product type controls and identify cost saving opportunities.

•Ancillary services and offerings: We provide a variety of ancillary services and tools to fleets to help them better manage expenses and capital requirements including tracking driver performance, location and speed; mobile account maintenance and payment tools; tax reporting and permitting services.

Marketing Channels

We market our fleetMobility products and services both directly and indirectly to commercialbusinesses and government vehicle fleet customersagencies with small, medium and large fleets of commercial vehicles, including fleets of all sizes, and over-the-road, long haul fleets. Our direct product suite includes payment processing and transaction processing services, WEX branded fleet cards in North America, and Motorpass/Motorcharge-brandedMotorpass branded fleet cards in Australia. Additionally, our over-the-road line of business isthe WEX products and services are marketed under the EFS, EFS Transportation Services, T-Chek, and Fleet One network brands.

We also market our products and services using the WEX network indirectly through co-branded and private label relationships. With a co-branded relationship product, we market our products and services for, and in collaboration with, both fuel providers and fleet management companies using their brand names and our logo on a co-branded fleet card. These companies seek to offer our payment processing and information management services as a component of their total offering to their fleet customers.

Our private label programs market our products and services for, and in collaboration with, fuel retailers, using only their brand names. The fuel retailers with which we have formed strategic relationships offer our payment processing and information management products and services to their fleet customers in order to establish and enhance customer loyalty. These fleets use these products and services to purchase fuel at locations of the fuel retailer with whom we have the private label relationship.

TRAVEL AND CORPORATE SOLUTIONS SEGMENTCompetition

In general, our Mobility business competes with financial institutions that provide general payment services without the enhanced capabilities of our solution set. We also compete against similar more specialized offerings from Fleetcor, U.S. Bank Voyager, Radius Payment Solutions, DKV, and Edenred. We believe we compete favorably against these competitors and others through the combination of the breadth of our solution, the reach of our payments network, and our advantaged funding model through WEX Bank.

Overview

Our TravelBenefits segment simplifies the business of administering and Corporate Solutions segment provides innovative corporate purchasingmanaging employee benefit plans. We provide SaaS software with embedded payment solutions and plan administration services for consumer-directed health benefits, COBRA accounts, and benefit enrollment and administration. In addition, WEX Inc. and WEX Bank provide custodial and depository services, respectively, with respect to HSAs.

Solution

Our products simplify the process of navigating and managing employee benefits for plan administrators, employers, and plan participants and their families. Our solutions power a variety of benefit plans, including HSAs, FSAs, HRAs, Lifestyle Spending Accounts, COBRA accounts, wellness incentives, Medicare Advantage supplemental benefits, commuter benefits, and other account-based benefit plans. We also provide the software that enables employees to choose and enroll in their benefits and manage those benefits throughout the plan year. In addition, WEX Inc. is an IRS-designated non-bank custodian of HSA assets. As of December 31, 2023, WEX Inc. was the custodian to $5.4 billion in HSA assets, $1.5 billion of which were in investment funds at a third-party brokerage firm, and $3.9 billion of which were in cash.

The following summarizes our key products and services within the Benefits segment:

•Consumer-directed benefits. We provide a software platform for record-keeping and administration of account-based benefit plans, which reimburse eligible expenses incurred by plan participants and their eligible dependents. We also provide debit card processing services to enable immediate electronic reimbursement.

•Non-bank custodial services. We provide non-bank custodial services for HSAs, with consumer balances placed at a variety of bank depositories including WEX Bank.

•COBRA administration. We provide a software platform for the administration of COBRA plans. In addition, we collect and process consumer premium payments.

•Enrollment and benefits administration. We provide a software platform that guides employees through their benefits options and enables them to enroll in the plans and access and manage their benefits information throughout the year.

•Administrative services. We provide a wide range of benefit plan administration services, including employer and participant service, claims administration, and reporting.

We simplify plan administration and management by providing a feature-rich software platform that automates and streamlines processes for stakeholders. In addition, through robust data analytics, we help administrators and employers understand consumer usage and engagement and benchmark against firms of similar size, geography, and industry. These same capabilities enable us to help consumers navigate their choices and make informed decisions about how to use their benefits. Our ability to gain rich insights from our expansive database enables us to provide personalized, relevant messages to consumers that connect with them where they are. We also enable administrators to compare their performance against their peers on dozens of metrics related to growth, operating efficiency, and consumer experience. Our products are designed to reduce friction, lower administrative costs, and provide a more elegant user experience. Participants can use our web portal and mobile app to access and manage their benefits at anytime from anywhere.

Our platform supports a multitude of benefit plan types, enables customization of plan design, and is extendable to power new benefit offerings in a dynamic market, consistent with the increasing importance of choice in employer benefit strategy. Our solutions are deployed flexibly, from software-only to full benefit administration, with a wide range of options in between.

Our revenues derive primarily from three sources:

•Per participant per month fees charged for our software and administrative services.

•Interest on deposits and fees related to cash balances in HSAs over which WEX Inc. is the custodian.

•Interchange on debit cards used by plan participants and their dependents to pay for eligible expenses from their benefit plan.

Distribution

We distribute our software and payment capabilities thatsolutions through a variety of partners, such as third-party administrators, financial institutions, payroll providers, and health plans. These partners use our software and payment solutions in their administration of employee benefit plans for their employer clients. Our team works with these partners to help them deploy go-to-market strategies and tactics to grow their business. In addition, we provide business process outsourcing of administrative services on behalf of certain partners.

We distribute full administrative services to the employer market directly and through brokers and consultants. Our solutions can be fully white-labeled, co-branded, or WEX-branded.

Our flexible distribution capabilities enhance our ability to penetrate our addressable markets through hundreds of partners as well as direct to employer. We had an average of approximately 19.9 million SaaS accounts on our platform during the year ended December 31, 2023.

Competition

In our partner channel, we compete with other specialized providers of similar benefit solutions, such as Alegeus Technologies and Nations Benefits, providers of core banking platforms, such as FIS, Fiserv, and Jack Henry, as well as proprietary technology solutions developed and maintained in-house by plan administrators.

In our direct channel, we compete with providers of consumer-directed benefit and COBRA administration as well as providers of benefit enrollment software and services. Competitors in this segment include companies such as HealthEquity, Alight Technologies, Businessolver, and Inspira Financial. We believe we compete favorably against these competitors through the combination of the breadth of our solution, the feature-richness of our platform and the fact that our offerings can be deployed flexibly, from software-only to full benefit administration, with a wide range of options in between.

| | | | | |

| Corporate Payments Segment |

Overview

Our Corporate Payments segment focuses on the complex payment environment of global B2B payments. Our capabilities and solutions broadly fall into two categories:

•Embedded Payments. Our primary service offering is to enable customers to utilize our highly scalable and vertically integrated payments solutions to integrate into their own workflows. Customers access our capabilities primarily via our proprietary set of application programming interfaces (“APIs”). We combine wholly-owned and developed cloud-based technology along with our customers’ internal systemswholly-owned and operated global financial services capabilities, inclusive of WEX Bank and our various electronic money institutions around the world, to streamlinesatisfy the commercial payments needs of our customer base. Our end customers are primarily using our services to create and use virtual credit cards to satisfy payment obligations in their corporate payments,business models. Customers for this solution include OTAs, tour operators, and airlines, as well as non-travel customers such as financial technology firms that focus on spend management, accounts payable automation, insurance payments, and reconciliation processes.media payments.

Sales•Accounts Payable (AP) Automation and Spend Management. Built on top of our embedded payment capabilities, our AP Automation and Spend Management capabilities provide an enhanced user interface and Enterprise Resource Planning (“ERP”) software integration points for organizations to manage their AP Automation and Spend Management functions. Our solutions in this space address corporations of all sizes and are sold direct to customers and also white-labeled by leading financial institutions who license our technology.

Solution

The Travel and Corporate SolutionsPayments segment allows businesses to centralize purchasing, simplify complex supply chain processes, and eliminate the paper check writing associated with traditional purchase order programs. OurIt also enables technology companies and innovators across the globe to streamline their payment needs with a single, integrated technology and issuing partner.

At the core of our Corporate Payments product suite includes electronic payments and corporate cards offered across travel, insurance & warranty and other industries.

Our electronic payments product includesset is a virtual payments and integrated payables.card. Our virtual payments programcapability is used for transactions where no physical card is presented, including transactions conductedthat are increasingly completed online in a

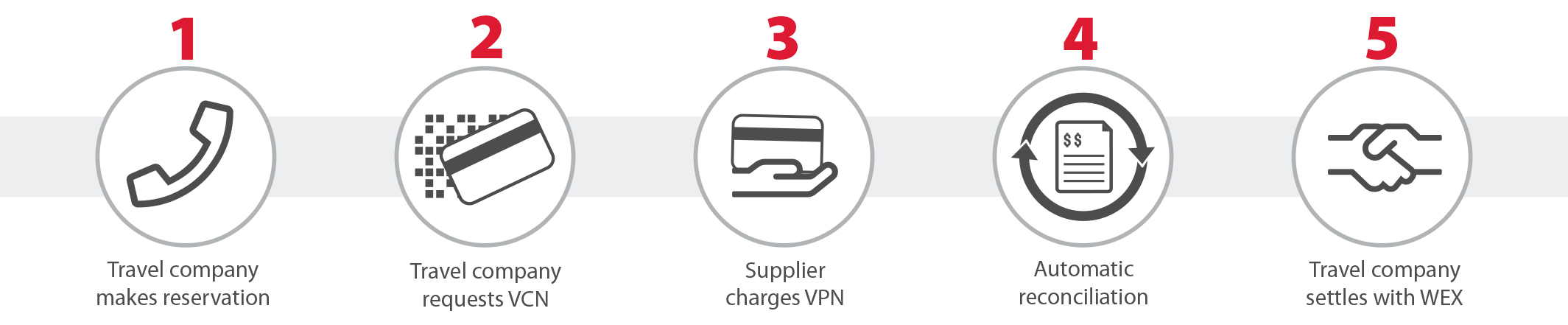

digitally connected world, but can also be used over the telephone, by mail, by faxemail, or on the Internet or for transactions that require pre-authorization, such as hotel reservations. Under our virtual payments program, eachby fax. Each transaction is assigned a unique account numberVCN on either of the Mastercard or Visa networks, with a customized creditspend limit, expiration date, and expiration date.various other purchase controls. These controls are in place to limit fraud and unauthorized spending. The unique account numberVCN limits purchase amounts and tracks, settles, and reconciles purchases more easily, creating efficiencies and cost savings for our customers. Our electronic accounts payablevirtual card solution combines (i) wholly-owned, end-to-end highly reliable technology, (ii) global currency capabilities with over 20 currencies active, and (iii) a wholly-owned global compliance and funding mechanism that allows WEX to be the issuer in addition to the payment processor. The use of a commercial virtual card is particularly appealing for its ability to easily reconcile, protect against fraud, provide chargeback protections, have global currency capabilities, and generate rebates through interchange economics.

We surround our core virtual card capabilities with a cloud-based web platformset of additional solution features to serve our customers. For our embedded payments solution, these capabilities include: (i) more than a dozen customized data fields that managesallow customers to tie together information such as invoice numbers, booking numbers, or purchase orders that enable industry-leading automated reporting and optimizes all accounts payable disbursements, regardlessreconciliation benefits, (ii) a wide variety of type. Automated clearing house,different virtual cards, electronic fundscard products with each of the card associations to optimize card acceptance and interchange yield, (iii) bank transfer and check payments are streamlinedissuance capabilities, (iv) modern, RESTful API, with associated, developer-focused explanation of use, and automated through(v) the ability to optimize our centralized application.

We offersystems and processes for bespoke solutions to large customer needs. For our AP automation and spend management solution, these capabilities include: (i) customizable integrations with different ERPs, (ii) enhanced AP data analysis and supplier enablement teams focused on increasing card acceptance, (iii) a wide variety of corporate cards, designed to combine all of a customer’s purchasing needs into a single integrated card, streamline the procure-to-pay process with a single card and control travel and entertainment spending and provide employees with greater flexibility.