For comparison purposes in the table below, we use freight revenue, or total revenue less fuel surcharges, in addition to total revenue when discussing changes as a percentage of revenue. We believe excluding this sometimes volatile source of revenue affords a more consistent basis for comparing our results of operations from period to period. Freight revenue excludes $68.2 million, $158.1 million, $109.9 million, and $111.6$109.9 million of fuel surcharges in 2009, 2008, 2007, and 2006,2007, respectively.

The following table sets forth the percentage relationship of certain items to total revenue and freight revenue:

| | | 2009 | | 2008 | | 2007 | | | | 2009 | | 2008 | | 2007 |

| | | | | | | | | | | | | | | |

| Total revenue | | 100.0% | | 100.0% | | 100.0% | | Freight revenue (1) | | 100.0% | | 100.0% | | 100.0% |

| Operating expenses: | | | | | | | | Operating expenses: | | | | | | |

Salaries, wages, and related expenses | | 36.7 | | 34.1 | | 38.0 | | Salaries, wages, and related expenses | | 41.5 | | 42.8 | | 44.9 |

Fuel expense | | 24.4 | | 33.7 | | 29.6 | | Fuel expense (1) | | 14.6 | | 16.7 | | 16.8 |

Operations and maintenance | | 6.0 | | 5.5 | | 5.7 | | Operations and maintenance | | 6.8 | | 6.9 | | 6.7 |

Revenue equipment rentals and purchased transportation | | 13.0 | | 11.8 | | 9.3 | | Revenue equipment rentals and purchased transportation | | 14.7 | | 14.8 | | 11.0 |

Operating taxes and licenses | | 2.1 | | 1.7 | | 2.0 | | Operating taxes and licenses | | 2.3 | | 2.1 | | 2.3 |

Insurance and claims | | 5.4 | | 4.9 | | 5.1 | | Insurance and claims | | 6.1 | | 6.1 | | 6.0 |

Communications and utilities | | 1.0 | | 0.9 | | 1.0 | | Communications and utilities | | 1.1 | | 1.1 | | 1.2 |

General supplies and expenses | | 4.0 | | 3.2 | | 3.3 | | General supplies and expenses | | 4.5 | | 4.3 | | 3.9 |

Depreciation and amortization, including net gains on disposition of equipment (2) | | 8.2 | | 8.2 | | 7.5 | | Depreciation and amortization, including net gains on disposition of equipment (2) | | 9.3 | | 10.3 | | 8.9 |

Goodwill impairment (3) | | 0.0 | | 3.2 | | 0.0 | | Goodwill impairment (3) | | 0.0 | | 4.0 | | 0.0 |

| Total operating expenses | | 100.8 | | 107.2 | | 101.5 | | Total operating expenses | | 100.9 | | 109.1 | | 101.8 |

| Operating loss | | (0.8) | | (7.2) | | (1.5) | | Operating loss | | (0.9) | | (9.1) | | (1.8) |

| Other expense, net (4) | | 4.3 | | 1.4 | | 1.6 | | Other expense, net (4) | | 4.9 | | 1.7 | | 1.9 |

| Loss before income taxes | | (5.1) | | (8.6) | | (3.1) | | Loss before income taxes | | (5.8) | | (10.8) | | (3.7) |

| Income tax benefit | | (0.9) | | (1.7) | | (0.8) | | Income tax benefit | | (1.0) | | (2.1) | | (0.9) |

| Net loss | | (4.2)% | | (6.9)% | | (2.3)% | | Net loss | | (4.8)% | | (8.7)% | | (2.8)% |

| | | | | | | | | | | | | | | |

| | | 2008 | | 2007 | | 2006 | | | | 2008 | | 2007 | | 2006 |

| | | | | | | | | | | | | | | |

| Total revenue | | 100.0% | | 100.0% | | 100.0% | | Freight revenue (1) | | 100.0% | | 100.0% | | 100.0% |

| Operating expenses: | | | | | | | | Operating expenses: | | | | | | |

Salaries, wages, and related expenses | | 34.1 | | 38.0 | | 38.4 | | Salaries, wages, and related expenses | | 42.8 | | 44.9 | | 45.8 |

Fuel expense | | 33.7 | | 29.6 | | 28.4 | | Fuel expense (1) | | 16.7 | | 16.8 | | 14.5 |

Operations and maintenance | | 5.5 | | 5.7 | | 5.3 | | Operations and maintenance | | 6.9 | | 6.7 | | 6.3 |

Revenue equipment rentals and purchased transportation | | 11.8 | | 9.3 | | 9.3 | | Revenue equipment rentals and purchased transportation | | 14.8 | | 11.0 | | 11.1 |

Operating taxes and licenses | | 1.7 | | 2.0 | | 2.1 | | Operating taxes and licenses | | 2.1 | | 2.3 | | 2.5 |

Insurance and claims | | 4.9 | | 5.1 | | 5.0 | | Insurance and claims | | 6.1 | | 6.0 | | 6.0 |

Communications and utilities | | 0.9 | | 1.0 | | 1.0 | | Communications and utilities | | 1.1 | | 1.2 | | 1.2 |

General supplies and expenses | | 3.2 | | 3.3 | | 3.1 | | General supplies and expenses | | 4.3 | | 3.9 | | 3.7 |

Depreciation and amortization, including net gains on disposition of equipment (2) | | 8.2 | | 7.5 | | 6.0 | | Depreciation and amortization, including net gains on disposition of equipment (2) | | 10.3 | | 8.9 | | 7.2 |

| Goodwill impairment (3) | | 3.2 | | 0.0 | | 0.0 | | Goodwill impairment (3) | | 4.0 | | 0.0 | | 0.0 |

| Total operating expenses | | 107.2 | | 101.5 | | 98.6 | | Total operating expenses | | 109.1 | | 101.8 | | 98.3 |

| Operating income (loss) | | (7.2) | | (1.5) | | 1.4 | | Operating income (loss) | | (9.1) | | (1.8) | | 1.7 |

| Other expense, net | | 1.4 | | 1.6 | | 0.9 | | Other expense, net | | 1.7 | | 1.9 | | 1.1 |

| Income (loss) before income taxes | | (8.6) | | (3.1) | | 0.5 | | Income (loss) before income taxes | | (10.8) | | (3.7) | | 0.6 |

| Income tax expense (benefit) | | (1.7) | | (0.8) | | 0.7 | | Income tax expense (benefit) | | (2.1) | | (0.9) | | 0.8 |

| Net loss | | (6.9)% | | (2.3)% | | (0.2)% | | Net loss | | (8.7)% | | (2.8)% | | (0.2)% |

| (1) | Freight revenue is total revenue less fuel surcharges. In this table, fuel surcharges are eliminated from revenue and subtracted from fuel expense. The amounts were $68.2 million, $158.1 million, and $109.9 million in 2009, 2008, and $111.6 million in 2008, 2007, and 2006, respectively. |

| (2) | Includes a $9.4 million pre-tax impairment charge for held and used equipment and $6.4 million of pre-tax impairment charges for equipment held for sale in the year ended December 31, 2008, which together represent 2.0% of total revenue and 2.6% of freight revenue. Includes a $1.7 million pre-tax impairment charge for equipment held for sale in the year ended December 31, 2007. See the discussion abovebelow under "Additional Information Concerning ImpairmentNon-Cash Charges" for a more extensive description of these impairments. |

| (3) | Represents a $24.7 million non-cash impairment charge to write off the goodwill associated with the acquisition of our Star Transportation subsidiary. See the discussion abovebelow under "Additional Information Concerning ImpairmentNon-Cash Charges" for a more extensive description of this impairment. |

| (4) | Includes an $11.5 million non-cash loss on the sale of the investment in and note receivable from Transplace in 2009. See the discussion below under "Additional Information Concerning Non-Cash Charges" for a more extensive description of the loss. |

Comparison of Year Ended December 31, 2009 to Year Ended December 31, 2008

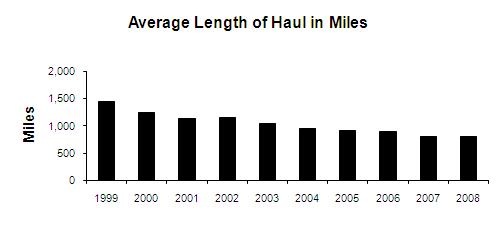

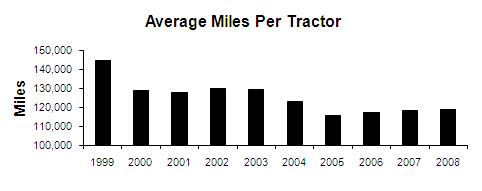

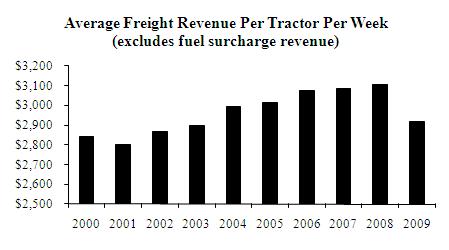

Total revenue decreased $185.2 million, or 23.9%, to $588.7 million in 2009, from $773.9 million in 2008. Freight revenue excludes $68.2 million of fuel surcharge revenue in 2009 and $158.1 million in 2008. Freight revenue (total revenue less fuel surcharges) decreased $95.3 million, or 15.5%, to $520.5 million in 2009, from $615.8 million in 2008. For comparison purposes, we use freight revenue (total revenue less fuel surcharge revenue) when discussing changes as a percentage of revenue. We believe removing this sometimes volatile source of revenue affords a more consistent basis for comparing the results of operations from period to period. As previously discussed, the rate environment was difficult in 2009, and freight volumes were significantly lower than 2008 as a result of the overall weak economic environment. The decreased level of freight revenue was primarily attributable to weak freight demand, excess tractor and trailer capacity in the truckload industry, and significant rate pressure from customers and freight brokers. Through mid-year 2009, we continued to reduce the size of our tractor fleet to achieve greater utilization of the remaining tractors in our fleet and attempt to improve profitability. With the assistance of this fleet reduction, we experienced a 0.7% increase in average miles per tractor versus the 2008 period. Average freight revenue per tractor per week, our primary measure of asset productivity, decreased 6.0% to $2,920 in 2009, from $3,105 in 2008, while total miles were down 9.3% from 2008. As the economy has begun to show signs of improvement in 2010, we expect customer demand to increase at a modest rate in the second half of the year.

Salaries, wages, and related expenses decreased $47.6 million, or 18.1%, to $216.2 million in 2009, from $263.8 million in 2008. As a percentage of freight revenue, salaries, wages, and related expenses decreased to 41.5% in 2009, from 42.8% in 2008. Driver pay decreased $33.7 million to $147.1 million in 2009, from $180.8 million in the 2008 period. The decrease was attributable to a 38.4 million reduction in truck miles, a decrease in driver pay per mile, and an increase in participation in our driver per diem pay program. Our payroll expense for employees, other than over-the-road drivers, decreased $6.1 million to $39.4 million from $45.4 million, due to a reduction in our non-driver work force. Additionally, workers' compensation and group health costs were $3.1 million and $0.9 million lower, respectively, in the 2009 period than the 2008 period, primarily as a result of reduced miles and head count along with favorable development in workers' compensation claims. If the economy continues to show signs of recovery, our ability to hold in place prior reductions in salaries and wages could be limited. Accordingly, these expenses could increase in absolute terms (and as a percentage of revenue absent an increase in revenue to offset increased costs).

Fuel expense, net of fuel surcharge revenue of $68.2 million in 2009 and $158.1 million in 2008, decreased $26.9 million to $75.6 million in 2009, from $102.6 million in 2008. As a percentage of freight revenue, net fuel expense declined to 14.6% in 2009 from 16.7% in 2008. Lower average fuel prices in 2009 versus 2008, multiple operating improvements, and the continued addition of auxiliary power units and more fuel efficient engines improved fuel efficiency and contributed to these decreases.

During 2009, fuel prices were less volatile than in 2008, contributing to the decrease in net fuel expense and the related percentage of revenue. After reaching unprecedented record fuel high fuel prices during most of 2008, diesel fuel prices started to fall in the fourth quarter of 2008 and continued through the first quarter of 2009. Significant fluctuations in fuel prices impact recovery of surcharges because we purchase fuel daily, while the U.S. Department of Energy ("DOE") index on which the surcharges are based resets weekly.

The Company receives a fuel surcharge on its loaded miles from most shippers; however, this may not cover the entire cost of high fuel prices for several reasons, including the following: surcharges cover only loaded miles, surcharges do not cover miles driven out-of-route by our drivers, and surcharges typically do not cover refrigeration unit fuel usage or fuel burned by tractors while idling. Additionally, fuel surcharges vary in the percentage of reimbursement offered, and not all surcharges fully compensate for fuel price increases even on loaded miles. The rate of fuel price increases and decreases also can have an impact. Most fuel surcharges are based on the average fuel price as published by the DOE for the week prior to the shipment. In times of decreasing fuel prices, the lag time causes under-recovery. Accordingly, volatility in fuel prices could cause volatility in our results of operations.

Operations and maintenance, consisting primarily of vehicle maintenance, repairs, and driver recruitment expenses, decreased $7.1 million to $35.4 million in 2009, from $42.5 million in 2008. As a percentage of freight revenue, operations and maintenance decreased to 6.8% in 2009, from 6.9% in 2008. The decrease resulted from decreased tractor and trailer maintenance costs, as a result of fewer tractors and less miles. Additionally, tire expense decreased due to a somewhat newer average fleet age. Finally, expenses related to tolls and unloading were less in the 2009 period than the 2008 period, due to the reduction in miles, and driver recruitment expenses were less as a result of the decreased demand for drivers. As a percentage of freight revenue, operations and maintenance remained relatively constant, as this mostly variable cost tracked our decrease in revenue, and the modest benefit from a somewhat younger tractor fleet was offset by an older trailer fleet and fixed costs. With the adverse economic environment in 2009, we had less difficulty recruiting and retaining drivers. If the economy improves, we could face more difficulty recruiting and retaining drivers, which could impact this expense category going forward. Further, the new Comprehensive Safety Analysis initiative could limit the pool of available drivers and increase these costs.

Revenue equipment rentals and purchased transportation decreased $14.5 million, or 15.9%, to $76.5 million in 2009, from $91.0 million in 2008. The decrease was a result of payments to third-party transportation providers associated with our Solutions subsidiary, which decreased to $40.0 million in 2009, from $45.3 million in 2008, primarily due to decreased loads and lower fuel costs passed on to those providers. In addition, we had a $3.8 million reduction in payments to independent contractors, which decreased to $10.3 million in 2009, from $14.1 million in 2008, mainly due to a decrease in the size of the independent contractor fleet and the reduction in fuel surcharges passed through that are a component of the related expense. Additionally, tractor and trailer equipment rental and other related expenses decreased to $25.9 million in 2009, compared with $31.2 million in 2008. We had financed approximately 236 tractors and 5,987 trailers under operating leases at December 31, 2009, compared with 646 tractors and 5,706 trailers under operating leases at December 31, 2008. As a percentage of freight revenue, revenue equipment rentals and purchased transportation expense remained relatively constant at 14.7% in 2009, and 14.8% in 2008. This expense category will fluctuate with the number of loads hauled by independent contractors and handled by Solutions and the percentage of our fleet financed with operating leases, as well as the amount of fuel surcharge revenue passed through to the independent contractors and third-party carriers. Because we anticipate adding new equipment over the next twelve months through on-balance sheet financing, the percentage of our tractor fleet financed with operating leases is expected to decrease in the near term. If the economy continues to improve, we may need to increase the amounts we pay to independent contractors and third-party transportation providers, which could increase this expense category absent an offsetting increase in revenue.

Operating taxes and licenses decreased $1.0 million, or 7.4%, to $12.1 million in 2009, from $13.1 million in 2008. As a percentage of freight revenue, operating taxes and licenses increased slightly to 2.3% in the 2009 period, from 2.1% in the 2008 period. This increase as a percentage of freight revenue resulted from increased costs per tractor as various taxing authorities increased their rates, as well as lower revenue per tractor, which less effectively covered this fixed cost.

Insurance and claims, consisting primarily of premiums and deductible amounts for liability, physical damage, and cargo damage insurance and claims, decreased $5.6 million, or 15.0%, to approximately $32.0 million in 2009, from approximately $37.6 million in 2008. The costs on a per mile basis were approximately half a cent per mile lower when comparing 2009 to 2008 because of a lower accident rate and slightly higher miles per tractor. The Company's overall safety performance has improved as our DOT reportable accidents dropped to the lowest level per million miles since 2001, giving us the best overall safety performance in at least nine years (based on DOT reportable accidents per million miles). As a percentage of freight revenue, insurance and claims remained constant at 6.1% in 2009 and 2008 because the decline in average freight revenue per mile offset the improvements in cost per mile. With our significant self-insured retention, insurance and claims expense may fluctuate significantly from period to period, and any increase in frequency or severity of claims could adversely affect our financial condition and results of operations.

Communications and utilities decreased to $5.7 million in 2009, from $6.7 million in 2008. As a percentage of freight revenue, communications and utilities remained constant at 1.1% in 2009 and 2008.

General supplies and expenses, consisting primarily of headquarters and other terminal facilities expenses, decreased $2.8 million to $23.6 million in 2009, from $26.4 million in 2008. As a percentage of freight revenue, general supplies and expenses increased slightly to 4.5% in 2009, from 4.3% in 2008. The increase as a percentage of revenue was primarily due to certain of these costs being fixed in nature, which were less efficiently spread over a reduced revenue base when comparing the 2009 period to the 2008 period.

Depreciation and amortization, consisting primarily of depreciation of revenue equipment, decreased $15.1 million or 23.9%, to $48.1 million in 2009, from $63.2 million in 2008. As a percentage of freight revenue, depreciation and amortization decreased to 9.3% in 2009, from 10.3% in 2008. The decreases were related to a $15.8 million revenue equipment impairment charge that was recorded in 2008 with no similar charge in 2009. See "Additional Information Concerning Non-Cash Charges" below for a further description of impairment charges affecting our operating results. Additionally, included in depreciation and amortization was $1.9 million of losses on the sale of property and equipment in 2008, with only $0.1 million of losses in 2009. Excluding the impairment charge and the losses on sale of equipment, depreciation and amortization increased $2.5 million in 2009 compared to 2008 as a result of having more owned tractors on our balance sheet as opposed to leased, as we owned 2,784 and 2,555 tractors at December 31, 2009 and 2008, respectively. Excluding the impairment charge and the losses on sale of equipment, as a percentage of revenue, depreciation and amortization increased to 9.2% in 2009, from 7.5% in 2008, as a result of lower revenue per tractor, which less effectively covered this fixed cost. We anticipate purchasing additional equipment through on-balance sheet financing over the next twelve months, which will likely cause an increase in depreciation and amortization in the near term.

Goodwill impairment in 2008 related to the $24.7 million write-off of all goodwill associated with our 2006 acquisition of Star Transportation, while there was no similar charge in 2009. This amount was non-cash and non-deductible for tax purposes. See "Additional Information Concerning Non-Cash Charges" below for a further description of impairment charges affecting our operating results.

The other expense category includes interest expense, interest income, and other miscellaneous non-operating items. Other expense, net, increased $14.8 million, to $25.3 million in the 2009 period, from $10.5 million in the 2008 period. The increase is primarily attributable to the loss on the sale of the investment in and note receivable from Transplace, which provided for $11.5 million of the increase. The remainder of the increase is a result of higher interest costs in the 2009 period, compared to the 2008 period, resulting from a period-over-period increase in debt and the increase in our average interest rate on our Credit Facility, as amended, compared to the average interest rates in the 2008 period.

Our income tax benefit was $5.0 million in 2009 compared to $12.8 million in 2008. The effective tax rate is different from the expected combined tax rate as a result of permanent differences primarily related to a per diem pay structure implemented in 2001. Due to the partial nondeductible effect of the per diem payments, our tax rate will fluctuate in future periods as income fluctuates. Additionally, the loss on the sale of the investment in Transplace and goodwill impairment in 2009 and 2008, respectively, were not deductible.

Primarily as a result of the factors described above, net loss was approximately $25.0 million in 2009, compared with a net loss of $53.4 million in 2008. As a result of the foregoing, our net loss as a percentage of freight revenue improved to (4.8%) in 2009, from (8.7%) in 2008.

Comparison of Year Ended December 31, 2008 to Year Ended December 31, 2007

Total revenue increased $61.4 million, or 8.6%, to $773.9 million in 2008, from $712.5 million in 2007. Freight revenue excludes $158.1 million of fuel surcharge revenue in 2008 and $109.9 million in 2007. Freight revenue (total revenue less fuel surcharges) increased $13.2 million, or 2.2%, to $615.8 million in 2008, from $602.6 million in 2007. For comparison purposes, we use freight revenue (total revenue less fuel surcharge revenue) when discussing changes as a percentage of revenue. We believe removing this sometimes volatile source of revenue affords a more consistent basis for comparing the results of operations from period to period.

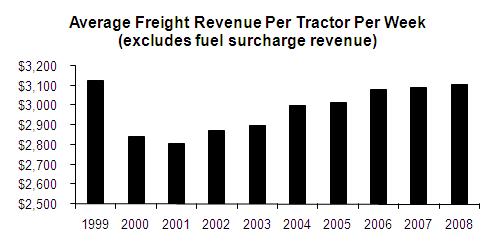

Average freight revenue per tractor per week our primary measure of asset productivity, increased 0.6% to $3,105 in 2008, from $3,088 in 2007. The increase was primarily generated by a 0.7% increase in average miles per tractor. The average miles per tractor increase was attributable to a 7 percentage point increase in the percentage of our fleet operated by driver teams (which usually generate higher miles than a solo-driver truck). The increase in teams offset aoffsets deterioration in miles per truck in our solo fleets. We continued to constrain the size of our tractor fleet to achieve greater fleet utilization and attempt to improve profitability. Weighted average tractors decreased 4.6% to 3,456 in 2008, from 3,623 in 2007.

Our Solutions revenue increased approximately 176% to $54.7 million in 2008 from $19.8 million in 2007, primarily due to an increase in fuel surcharge collection, much of which is passed on to the third party carriers, and an increase in brokerage loads to 27,117 in 2008 from 10,743 loads in 2007. As a result, average revenue per load increased approximately 9.4% to $2,017 in 2008 from $1,843 per load in 2007.

Salaries, wages, and related expenses decreased $6.6 million, or 2.5%, to $263.8 million in 2008, from $270.4 million in 2007. As a percentage of freight revenue, salaries, wages, and related expenses decreased to 42.8% in 2008 from 44.9% in 2007. Driver pay decreased $7.7 million to $180.8 million in 2008, from $188.5 million in the 2007 period. The decrease was attributable to lower driver wages as more drivers have opted onto our driver per diem pay program. Our payroll expense for employees, other than over-the-road drivers, decreased $1.8 million to $45.4 million from $47.2 million, due to a reduction in non-driver work force comparable to the percentage reduction in tractor fleet. These reductions were partially offset by an increase in workers' compensation expense related to unfavorable development of some outstanding claims during 2008, as well as increases in our group health expenses and additional office salary expense related to severance payments.

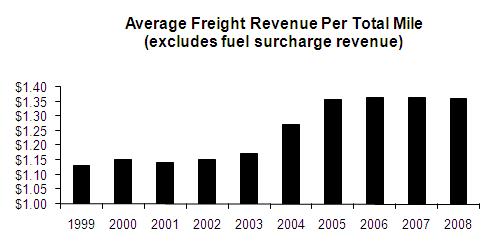

Fuel expense, net of fuel surcharge revenue of $158.1 million in 2008 and $109.9 million in 2007, increased $1.5 million to $102.6 million in 2008, from $101.1 million in 2007. As a percentage of freight revenue, net fuel expense was essentially constant at 16.7% in 2008 and 16.8% in 2007. Net fuel expense was highly volatile during the year,2008, however, amounting to 19.0% of freight revenue during the second quarter and dropping to 11.5% of freight revenue in the fourth quarter. Fuel surcharges amounted to $0.384 per total mile in 2008, compared to $0.257 per total mile in 2007. We received a fuel surcharge on our loaded miles from most shippers. However, this does not cover the entire cost of high fuel prices for several reasons, including the following: surcharges cover only loaded miles, not the approximately 11% of non-revenue miles we operated in 2008; surcharges do not cover miles driven out-of-route by our drivers; and surcharges typically do not cover refrigeration unit fuel usage or fuel burned by tractors while idling. In addition, fuel surcharges vary in the percentage of reimbursement offered, and not all surcharges fully compensate for fuel price increases even on loaded miles.

The rate of fuel price increases also can have an impact. Most fuel surcharges are based on the average fuel price as published by the DOE for the week prior to the shipment. In times of decreasing fuel prices, the lag time causes additional recovery. Lag time was a factor to additional recovery during the second half of 2008, as fuel prices decreased rapidly during the period.

We have established several initiatives to combat the cost of fuel. We have invested in auxiliary power units for a percentage of its fleet and is evaluating the payback on additional units where idle time is already lower. We have also reduced the maximum speed of many of our trucks, implemented strict idling guidelines for our drivers, encouraged the use of shore power units in truck stops, and imposed standards for accepting broker freight that include a minimum combined rate and assumed fuel surcharge component. This combination of initiatives contributed to a significant improvement in fleetwide average fuel mileage. We will continue to review shipper's overall freight rate and fuel surcharge program. Fuel costs may continue to be affected in the future by price fluctuations, volume purchase commitments, the terms and collectibility of fuel surcharges, the percentage of miles driven by independent contractors, and lower fuel mileage due to government mandated emissions standards that have resulted in less fuel efficient engines. At December 31, 2008, we had no derivative financial instruments to reduce our exposure to fuel price fluctuations.

Operations and maintenance, consisting primarily of vehicle maintenance, repairs, and driver recruitment expenses, increased $2.0 million to $42.5 million in 2008, from $40.4 million in 2007. The increase resulted from increased tractor and trailer maintenance costs, as well as increased tire expense associated with a somewhat older average fleet age and the associated tire replacement cycle. As a percentage of freight revenue, operations and maintenance increased to 6.9% in 2008, from 6.7% in 2007.

Revenue equipment rentals and purchased transportation increased $24.5 million, or 36.8%, to $91.0 million in 2008, from $66.5 million in 2007. As a percentage of freight revenue, revenue equipment rentals and purchased transportation expense increased to 14.8% in 2008, from 11.0% in 2007. These increases were primarily driven by increased payments to third-party transportation providers associated with Solutions, our brokerage subsidiary, which increased to $45.7 million in 2008 from $16.3 million in 2007. This was offset by a $3.7 million reduction in payments to independent contractors, which decreased to $14.1 million in 2008, from $17.8 million in 2007, mainly due to a decrease in the independent contractor fleet and a decrease in tractor and trailer equipment rental and other related expenses to $31.2 million in 2008 compared with $32.5 million in 2007. We had financed approximately 646 tractors and 5,706 trailers under operating leases at December 31, 2008, compared with 693 tractors and 6,322 trailers under operating leases at December 31, 2007. This expense category will fluctuate with the number of loads hauled by independent contractors and handled by Solutions and the percentage of our fleet financed with operating leases, as well as the amount of fuel surcharge revenue passed through to the independent contractors and third-party carriers.

Operating taxes and licenses decreased $1.0 million, or 7.3%, to $13.1 million in 2008 from $14.1 million in 2007. As a percentage of freight revenue, operating taxes and licenses remained essentially constant at 2.1% in 2008 and 2.3% in 2007.

Insurance and claims consisting primarily of premiums and deductible amounts for liability, physical damage, and cargo damage insurance and claims, increased $1.2 million, or 3.3%, to approximately $37.6 million in 2008, from approximately $36.4 million in 2007. As a percentage of freight revenue, insurance and claims remained essentially constant at 6.1% in 2008 and 6.0% in 2007.

The Company's overall safety performance has improved as our DOT reportable accidents dropped to the lowest level per million miles since 2000, giving us the best overall safety performance in at least eight years (based on DOT reportable accidents per million miles). During 2008, there werewas a small number of severe accidents late in the year that resulted in a negative impact of approximately $5.4 million. During 2007, there were unfavorable developments on two prior-period claims that increased our accrual for casualty claims in 2007 by $5.2 million. The 2007 increase was partially offset by the receipt of a $1.0 million refund from our insurance carrier related to achieving certain monetary claim targets for our casualty policy in the 2007 policy year. The insurance refund in 2008 was approximately $0.4 million. With our significant self-insured retention, insurance and claims expense may fluctuate significantly from period to period, and any increase in frequency or severity of claims could adversely affect our financial condition and results of operations.

Communications and utilities decreased to $6.7 million in 2008, from $7.4 million in 2007. As a percentage of freight revenue, communications and utilities remained essentially constant at 1.1% in 2008 and 1.2% in 2007.

General supplies and expenses, consisting primarily of headquarters and other terminal facilities expenses increased $3.0 million to $26.4 million in 2008, from $23.3 million in 2007. As a percentage of freight revenue, general supplies and expenses increased to 4.3% in 2008, from 3.9% in 2007. The increase was primarily due to increased sales agent commissions from our growing brokerage subsidiary, which increased $2.5 million to $3.8 million in 2008, compared to $1.3 million in 2007.

Depreciation and amortization, consisting primarily of depreciation of revenue equipment increased $9.7 million or 18.1%, to $63.2 million in 2008, from $53.5 million in 2007. As a percentage of freight revenue, depreciation and amortization increased to 10.3% in 2008, from 8.9% in 2007. The increase was related to a $15.8 million revenue equipment impairment charge that was recorded in 2008, as compared to a $1.7 million impairment charge recorded in 2007. Excluding the impairment charges, depreciation and amortization decreased $4.4 million in 2008 and, as a percentage of freight revenue, decreased to 7.7% in 2008, from 8.6% in 2007. These decreases were primarily the result of our efforts to eliminate excess equipment and terminals over the past year. We haveduring 2008, and we reduced theour fleet by approximately 263 tractors and 390 trailers. Depreciation and amortization expense includes any gain or loss on the disposal of equipment, which was an approximately $1.9 million loss in 2008 and a $1.7 million loss in 2007. Please seeSee "Additional Information Concerning ImpairmentNon-Cash Charges" abovebelow for a further description of impairment charges affecting our operating results.

Goodwill impairment in 2008 related to the $24.7 million write-off of all goodwill associated with our 2006 acquisition of Star Transportation. This amount is non-cash and non-deductible. Please seeSee "Additional Information Concerning ImpairmentNon-Cash Charges" abovebelow for a further description of impairment charges affecting our operating results.

Our income tax benefit was $12.8 million in 2008 compared to $5.6 million in 2007. The effective tax rate is different from the expected combined tax rate as a result of permanent differences primarily related to a per diem pay structure implemented in 2001. Due to the nondeductible effect of per diem, our tax rate will fluctuate in future periods as income fluctuates. In addition, weWe reversed a contingent tax accrual during 2007, based on the recommendation by an IRS appeals officer that the IRS concede a case in our favor. This concession resulted in recognition of approximately $0.4 million of income tax benefit for 2007.

Primarily as a result of the factors described above, net income decreased approximately $36.7 million to a net loss of $53.4 million in 2008, from a net loss of $16.7 million in 2007. As a result of the foregoing, our net loss as a percentage of freight revenue declined to (8.7%) in 2008, from (2.8%) in 2007.

Comparison of Year Ended December 31, 2007 to Year Ended December 31, 2006SEGMENT OPERATIONS

Total revenue increased $28.7 million, or 4.2%We operate two reportable business segments. Our Asset-Based Truckload Services ("Truckload") segment consists of Covenant Transport, Inc., SRT, and Star Transportation. Our Brokerage Services segment consists of Covenant Transport Solutions, Inc. ("Solutions"). The operation of each of these businesses is described in our notes to $712.5 million in 2007, from $683.8 million in 2006. Freight revenue excludes $109.9 millionthe "Business Section." Unallocated corporate overhead includes costs that are incidental to our activities and are not specifically allocated to one of fuel surcharge revenue in 2007the segments. The following tables summarize financial and $111.6 million in 2006.operating data by segment:

On September 14, 2006, we acquired 100% of the outstanding stock of Star, a short-to-medium haul dry van regional truckload carrier based in Nashville, Tennessee. The acquisition included 614 tractors and 1,719 trailers. Star's operating results have been accounted for in the Company's results of operations since the acquisition date. Star's total revenue for the year ended December 31, 2007 totaled approximately $96.2 million, which is included in our consolidated statements of operations for the year ended December 31, 2007. Star's cost structure is similar to that of our additional operating subsidiaries, and therefore has a minimal impact on expenses as a percentage of freight revenue.| | | Twelve months ended December 31, | |

| (in thousands) | | 2009 | | | 2008 | | | 2007 | |

| Revenues: | | | | | | | | | |

| | | | | | | | | | |

| Asset-Based Truckload Services | | $ | 541,325 | | | $ | 719,220 | | | $ | 692,722 | |

| Brokerage Services | | | 47,362 | | | | 54,694 | | | | 19,804 | |

| | | | | | | | | | | | | |

| Total | | $ | 588,687 | | | $ | 773,914 | | | $ | 712,526 | |

| Operating Income (Loss): | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Asset-Based Truckload Services | | $ | 10,552 | | | $ | (37,091 | ) | | $ | (7,011 | ) |

| Brokerage Services | | | 155 | | | | 466 | | | | 1,031 | |

| Unallocated Corporate Overhead | | | (15,429 | ) | | | (19,054 | ) | | | (4,701 | ) |

| | | | | | | | | | | | | |

| Total | | $ | (4,722 | ) | | $ | (55,679 | ) | | $ | (10,681 | ) |

Freight revenue (total revenue less fuel surcharges) increased $30.4 million, or 5.3%, to $602.6 million in 2007, from $572.2 million in 2006. Average freight revenue per tractor per week, our primary measure of asset productivity, increased 0.4% to $3,088 in 2007 from $3,077 in 2006. The increase was primarily generated by a 0.5% increase in average miles per tractor and a 1.1% increase in our average freight revenue per loaded mile. Excluding the acquisition of Star, we continued to constrain the size of our tractor fleet to achieve greater fleet utilization and improved profitability. In general, the changes in freight mix as a result of the realignment expanded the portions of our business with longer lengths of haul, more miles per tractor, and generally lower rate structures, while reducing the regional service offering, which had the highest rate structure but significantly lower miles per tractor. The lackluster freight environment continued to impact every subsidiary and service offering.

Salaries, wages, and related expenses increased $8.1 million, or 3.1%, to $270.4 million in 2007, from $262.3 million in 2006. As a percentage of freight revenue, salaries, wages, and related expenses decreased to 44.9% in 2007 from 45.8% in 2006. Driver pay increased $7.5 million to $188.5 million in 2007, from $181.0 million in the 2006 period, as improved driver retention resulted in higher wages for more experienced drivers. This resulted in increased driver pay on a cost per mile basis of 1.0% in the 2007 period over the 2006 period. Our employee benefits, decreased $1.9 million to $34.7 million in 2007 from $36.6 million in 2006, attributable to favorable health insurance expense of $1.3 million and reduced workers' compensation exposure resulting in a $1.3 million reduction in related expense, offset by increased payroll taxes of $0.8 million related to increased salaries and wages. These benefit expenses decreased to 5.8% of freight revenue in 2007 from 6.4% of freight revenue in 2006.

Fuel expense, net of fuel surcharge revenue of $109.9 million in 2007 and $111.6 million in 2006, increased $18.4 million to $101.1 million in 2007 from $82.8 million in 2006. As a percentage of freight revenue, net fuel expense increased to 16.8% in 2007 from 14.5% in 2006. Fuel surcharges amounted to $0.257 per total mile in 2007 compared to $0.266 per total mile in 2006. In 2007, we had a lower surcharge collection rate due primarily to three factors: 1) the increase in freight obtained through brokers, 2) less compensatory fuel surcharge programs, and 3) an increase in the percentage of non-revenue miles, due to the decrease in freight demand. Our total miles increased approximately 2.7% while our fuel surcharge revenue decreased 1.5%. The resulting net effect was that our fuel expense, net of surcharge, increased approximately $.038 per total mile. Fuel costs may be affected in the future by price fluctuations, volume purchase commitments, the terms and collectibility of fuel surcharges, the percentage of miles driven by independent contractors, and lower fuel mileage due to government mandated emissions standards that have resulted in less fuel efficient engines. At December 31, 2007, we had no derivative financial instruments to reduce our exposure to fuel price fluctuations.

Operations and maintenance, consisting primarily of vehicle maintenance, repairs, and driver recruitment expenses, increased $4.3 million to $40.4 million in 2007 from $36.1 million in 2006. As a percentage of freight revenue, operations and maintenance increased slightly to 6.7% in 2007 from 6.3% in 2006. The increase resulted in part from higher unloading costs, tractor and trailer maintenance costs, and tire expense, but was offset by reduced driver recruiting expense and tolls.

Revenue equipment rentals and purchased transportation increased $3.0 million, or 4.7%, to $66.5 million in 2007, from $63.5 million in 2006. As a percentage of freight revenue, revenue equipment rentals and purchased transportation expense remained essentially flat at 11.0% in 2007 and 11.1% in 2006. Payments to third-party transportation providers primarily from Solutions, our brokerage subsidiary, were $16.3 million in 2007, compared to $3.4 million in 2006. Tractor and trailer equipment rental and other related expenses decreased $8.5 million, to $32.5 million in 2007 compared with $41.0 million in 2006. We had financed approximately 693 tractors and 6,322 trailers under operating leases at December 31, 2007, compared with 1,116 tractors and 7,575 trailers under operating leases at December 31, 2006. Payments to independent contractors decreased $1.3 million to $17.8 million in 2007 from $19.1 million in 2006, mainly due to a decrease in the independent contractor fleet.

Operating taxes and licenses decreased $0.4 million, or 2.8%,

Comparison of Year Ended December 31, 2009 to $14.1 million in 2007 from $14.5 million in 2006. As a percentage of freight revenue, operating taxes and licenses remained essentially constant at 2.3% in 2007 and 2.5% in 2006.Year Ended December 31, 2008

Insurance and claims, consisting primarily of premiums and deductible amounts for liability, physical damage, and cargo damage insurance and claims, increased $2.3 million, or 6.7%Our asset-based truckload services segment revenue decreased 24.7%, to approximately $36.4$541.3 million for the twelve-month period ended December 31, 2009, compared to $719.2 million for the comparable period in 2008. Lower fuel prices resulted in fuel surcharge revenue of $68.2 million in 2007 from approximately $34.1the twelve months ended December 31, 2009, versus $158.1 million in 2006.the 2008 period. The increase was thedecrease in freight revenue is related to a decrease in rates and miles as a result of unfavorable developments on two separate claims occurringthe weakened economy in 20042009. In 2009, management decreased the fleet size approximately 10% in response to weak demand. Excluding unallocated corporate overhead, the segment generated an operating income of $10.6 million for the twelve months ended December 31, 2009, compared to an operating loss of $37.1 million for the same 2008 period, primarily due to certain non-cash charges in 2008 totaling $40.5 million related to the impairment of certain property and 2005,equipment and Star's goodwill, both of which were ultimately settled duringare discussed in more detail below. Excluding these charges in 2008, the second quarterTruckload segment generated operating income of 2007, increasing our accrual for casualty claims by $5.2 million. Our frequency and severity$3.4 million, representing an increase in operating income in 2009 from 2008, with the exclusion of accidents during 2007 has improved versus 2006, andthe impairments, as a percentageresult of freight revenue, insurancelower net fuel expenses and claims remained essentially constant at 6.0% in 2007 and 2006.cost savings initiatives.

In general,Our brokerage segment revenue decreased 13.4% to $47.3 million for casualty claims, we have insurance coverage upthe twelve months ended December 31, 2009, compared to $50.0$54.7 million per claim. In 2006for the same period in the prior year. The decreases were primarily attributable to a reduction in the portion of revenue attributable to fuel surcharges given fuel was at historic highs throughout much of 2008 and through February 28, 2007, we were self-insuredless volume due to the closure of a large company store in October 2008. Excluding unallocated corporate overhead, operating income for personal injury and property damage claimsour brokerage segment was $0.2 million for amounts up to $2.0 million per occurrence, subjectthe twelve-month period ended December 31, 2009, compared to an additional $2.0operating income of $0.5 million self-insured aggregate amount, whichfor the comparable 2008 period. The decreases are a result of an increase in bad debt expense of $0.3 million from the comparable 2008 period due to several large bankruptcies, an increase in purchased transportation expense per revenue dollar, and an increase in depreciation expense of approximately $0.3 million related to accelerating the depreciation of certain software that will be abandoned in 2010. These increases were partially off-set by various reductions in selling, general, and administrative expenses as a result of cost savings initiatives.

Comparison of Year Ended December 31, 2008 to Year Ended December 31, 2007

Our asset-based truckload services segment revenue increased 3.9%, to $719.2 million for the twelve-month period ended December 31, 2008, compared to $692.3 million for the comparable period in 2007. Higher fuel prices resulted in fuel surcharge revenue of $158.1 million in the twelve months ended December 31, 2008, versus $109.9 million in the 2007 period. The decrease in freight revenue is related to a decrease in rates, total self-insured retentionmiles, and fleet size, specifically in the third and fourth quarters, related to the onset of upthe recession in 2008. Excluding unallocated corporate overhead, an operating loss of $37.1 million for the twelve months ended December 31, 2008 compared to $4.0operating loss of $7.0 million untilfor the $2.0same 2007 period. The fluctuations are primarily due to certain non-cash charges in 2008 totaling $40.5 million aggregate threshold was reached. We renewed our casualty program asrelated to the impairment of February 28,certain property and equipment and Star's goodwill and a $1.7 million impairment charge related to a corporate aircraft in 2007, each of which is discussed in more detail below. Excluding these charges, the Truckload segment generated operating income of $3.4 million in 2008 and an operating loss of $5.3 million in 2007. In conjunctionThe increase in operating income from 2007 to 2008, with the renewal, we are self-insuredexclusion of the impairments, is primarily a result of a $6.6 million reduction in salaries and wages due to more drivers participating in the per diem plan and a reduction in our non-driving workforce.

Our brokerage segment revenue increased 176.3% to $54.7 million for personal injury and property damage claimsthe twelve months ended December 31, 2008, compared to $19.8 million for amounts upthe same period in the prior year, primarily due to an increase in fuel surcharge collection, much of which is passed on to the first $4.0 million. We are self-insuredthird-party carriers, and an increase in brokerage loads to 27,117 in 2008, from 10,743 loads in 2007. As a result, average revenue per load increased approximately 9.4% to $2,017 in 2008, from $1,843 per load in 2007. Excluding unallocated corporate overhead, operating income for cargo loss and damage claimsour brokerage segment was $0.5 million for amounts upthe twelve-month period ended December 31, 2008, compared to an operating income of $1.0 million per occurrence. Insurancefor the comparable 2007 period. The decrease is a result of an increase in legal expense of $0.8 million related to litigation surrounding the closure of a large Company store in 2008, partially offset by a more efficient spreading of fixed costs due to the increase in loads year-over-year.

Additional Information Concerning Non-Cash Charges

Transplace

From July 2001 to December 2009, we owned approximately 12.4% of Transplace, Inc. ("Transplace"), a global logistics provider. During the first quarter of 2005, we loaned Transplace approximately $2.6 million through a 6% interest-bearing note receivable. After receiving an offer to purchase our 12.4% equity ownership and claims expense varies basedrelated note receivable that was accepted by a majority of Transplace's shareholders, we determined, pursuant to the guidance provided by the Financial Accounting Standards Board ("FASB") Accounting Standards Codification 325, that the value of our equity investment had become completely impaired in the third quarter of 2009, and the value of the note receivable had become impaired by approximately $0.9 million. As a result, we recorded a non-cash impairment charge of $11.6 million during the third quarter of 2009.

The transaction closed in December 2009, whereby the proceeds of $1.9 million provided for a recovery of $0.1 million of the previously impaired amount in the fourth quarter of 2009 and thus an $11.5 million non-cash loss on the frequencysale of our investment and severity of claims,related note receivable. There was no tax benefit recorded in connection with the premium expense, and the level of self-insured retention, the development of claims over time, and other factors. With our significant self-insured retention, insurance and claims expense may fluctuate significantly from period to period, and any increase in frequency or severity of claims could adversely affect our financial condition and results of operations.

Communications and utilities increased to $7.4 million in 2007 from $6.7 million in 2006. As a percentage of freight revenue, communications and utilities remained constant at 1.2% in 2007 and 2006.

General supplies and expenses, consisting primarily of headquarters and other terminal facilities expenses, increased $1.9 million to $23.3 million in 2007 from $21.4 million in 2006. As a percentage of freight revenue, general supplies and expenses increased to 3.9% in 2007 from 3.7% in 2006. Of this increase, $0.7 million was for additional building rent paidloss on our headquarters building and surrounding property in Chattanooga, Tennessee for which we completed a sale leaseback transaction effective April 2006 as described more fully in the following paragraph. Sales agent commissions, primarily from our growing brokerage subsidiary, increased $1.1 million to $1.3 million in 2007, compared to $0.2 million in 2006.

In April 2006, we entered into a sale leaseback transaction involving our corporate headquarters, a maintenance facility, and approximately forty-six acres of surrounding property in Chattanooga, Tennessee (collectively, the "Headquarters Facility"). We received proceeds of approximately $29.6 million from the sale of the Headquarters Facility,investment, given a full valuation allowance was established for the related capital loss.

Goodwill

In light of changes in market conditions and the related declining market outlook for the Star Transportation operating subsidiary, which is included in our Truckload segment, noted in the fourth quarter of 2008, we engaged an independent third party to assist us in the completion of valuations used to pay down borrowings under our Credit Facilityin the impairment testing process. The completion of this work concluded that the goodwill previously recorded for the Star acquisition was fully impaired and to purchase revenue equipment. In the transaction, we entered into a twenty-year lease agreement, whereby we will lease back the Headquarters Facility at an annual rental rate of approximately $2.5 million, subject to annual rent increases of 1.0%, resulting in annual straight-line rental expense of approximately $2.7 million. The transaction resulted in a gain$24.7 million, or $1.75 per basic and diluted share, non-cash goodwill impairment charge, recorded in the fourth quarter of approximately $2.4 million, which is being amortized ratably over2008. There was no tax benefit associated with this nondeductible charge. Pursuant to applicable accounting standards, we conducted our 2009 annual impairment test for goodwill in the life of the leasesecond quarter and recorded as an offset to general supplies and expenses (specifically to building rent) on our consolidated statements of operations.did not identify any impairment.

DepreciationRevenue Equipment, including Assets Held For Sale

As a result of sharply lower economic indicators, a worsening credit market, and amortization, consisting primarilysignificantly lower prices received for disposals of depreciationour owned used revenue equipment, all of which deteriorated substantially during the fourth quarter of 2008, we recorded a $9.4 million asset impairment charge to write-down the carrying values of tractors and trailers in-use in our Truckload segment which were expected to be traded or sold in 2009 or 2010. The carrying values for revenue equipment scheduled for trade in 2011 and beyond were not adjusted because those tractors and trailers were not required to be impaired based on recoverability testing using the expected future cash flows and disposition values of such equipment.

Similarly, we recorded a $6.4 million asset impairment charge ($1.2 million was recorded in the third quarter and $5.2 million was recorded in the fourth quarter) to write down the carrying values of tractors and trailers held for sale in our Truckload segment, which were expected to be traded or sold in future periods.

Although we do not expect to be required to make any current or future cash expenditures as a result of these impairment charges, cash proceeds of future disposals of revenue equipment increased $12.4 million, or 30.1%,are anticipated to $53.5 million in 2007 from $41.2 million in 2006. As a percentagebe lower than expected prior to the impairment charges.

Our evaluation of freight revenue, depreciation and amortization increasedthe future cash flows compared to 8.9% in 2007 from 7.2% in 2006. The increase related to several factors, including an increase in the numbercarrying value of ownedthe tractors and trailers in-use in 2007; a softer market2009 has not resulted in any additional impairment charges. Additionally, there were no indicators triggering an evaluation for used equipment resulting in a lossimpairment of $1.7 million in 2007 compared to a gain of $2.1 million in 2006;assets held for sale during the 2009 period, as evidenced by our minimal gains and increased amortization expense of $1.5 million related to the identifiable intangibles acquired with our Star acquisition on September 14, 2006. Depreciation and amortization expense is net of any gain or losslosses on the disposal of tractors and trailers.revenue equipment, including assets held for sale.

TheAircraft

In addition, our 2007 asset impairment charge relateswas related to our decision to sell our corporate aircraft to reduce ongoing operating costs. We recorded an impairment charge of $1.7 million, reflecting the unfavorable fair market value of the airplane as compared to the combination of the estimated payoff of the long-term operating lease and current book value of related airplane leasehold improvements.

The other expense category includes interest expense, interest income, and pre-tax non-cash gains or losses related to the accounting for interest rate derivatives under SFAS No. 133, Accounting for Derivative Instruments and Hedging Activities, as amended ("SFAS No. 133"). Other expense, net, increased $5.2 million, to $11.6 million in 2007 from $6.4 million in 2006. The increase relates primarily to increased net interest expense of $4.9 million resulting from the additional borrowings related to the Star acquisition, along with increased average interest rates. However a portion of this increase has been offset by a reduction in overall balance sheet debt since the Star acquisition.

Our income tax benefit was $5.6 million in 2007 compared to income tax expense of $4.6 million in 2006. The effective tax rate is different from the expected combined tax rate as a result of permanent differences primarily related to a per diem pay structure implemented in 2001. Due to the nondeductible effect of per diem, our tax rate will fluctuate in future periods as income fluctuates. In addition, we received a net tax benefit in 2007, as compared with the 2006 period because we reversed a contingent tax accrual effective March 31, 2007, based on the recommendation by an IRS appeals officer that the IRS concede a case in our favor. This concession resulted in recognition of approximately $0.4 million of income tax benefit in 2007.

Primarily as a result of the factors described above, net income decreased approximately $15.3 million to a net loss of $16.7 million in 2007 from a net loss of $1.4 million in 2006. As a result of the foregoing, our net loss as a percentage of freight revenue declined to (2.8%) in 2007 from (0.2%) in 2006.

LIQUIDITY AND CAPITAL RESOURCES

Our business requires significant capital investments over the short-term and the long-term. In recent years,Recently, we have financed our capital requirements with borrowings under our credit facilities,Credit Facility, cash flows from operations, long-term operating leases, capital leases, and secured installment notes with finance companies. Our primary sources of liquidity at December 31, 2008,2009, were funds provided by operations, proceeds from the sale of used revenue equipment, borrowings under our Credit Agreement,Facility, borrowings from the Daimler Facility, other secured installment notes, (each as defined in Note 7 to our consolidated financial statements contained herein), andcapital leases, operating leases of revenue equipment. Although turmoil inequipment, and cash and cash equivalents. We had a working capital (total current assets less total current liabilities) deficit of $17.8 million at December 31, 2009, and a working capital surplus of $16.3 million at December 31, 2008. Working capital deficits are common to many trucking companies that expand by financing revenue equipment purchases through borrowing or capitalized leases. When we finance revenue equipment through borrowing or capitalized leases, the economyprincipal amortization scheduled for the next twelve months is categorized as a current liability, although the revenue equipment is classified as a long-term asset. Consequently, each purchase of revenue equipment financed with borrowing or capitalized leases decreases working capital. We believe our working capital deficit had little impact on our liquidity. Based on our expected financial condition, results of operations, net capital expenditures, a material refund of previously paid federal income taxes as a result of net operating loss carry backs pursuant to the Worker, Homeownership, and inBusiness Assistance Act of 2009, and net cash flows during the financial and credit markets has made availability of financing less certain, based upon our assumptions for 2009 described above,next twelve months, which contemplate an improvement compared with the past twelve months, we believe our working capital and sources of financing, together with additional financing we may be able to access and secure with available real estate,liquidity will be adequate to meet our current and projected needs both for at least the shortnext twelve months. On a longer-term basis, based on our anticipated financial condition, results of operations, and long term.cash flows, and continued availability of our Credit Facility, secured installment notes, and other sources of financing that we expect will be available to us, we do not expect to experience material liquidity constraints in the foreseeable future.

The Company has had significant losses from 2007 through 2009, attributable to operations, impairments, and other charges. The Company has managed its liquidity during this time through a series of cost reduction initiatives, refinancing, amendments to credit facilities, and sales of assets. We have had difficulty meeting budgeted results in the past. If we are unable to meet budgeted results or otherwise comply with our Credit Facility, we may be unable to obtain a further amendment or waiver under our Credit Facility, or we may incur additional fees.

Cash Flows

Net cash provided by operating activities was $30.9 million in 2009 and $40.3 million in 2008. Excluding the effects of $40.4 million in non-cash charges in 2008 and $33.7$11.5 million in 2007. Our2009, our cash from operating activities was higherlower in 20082009 primarily due to improved collectionan $11.5 million net change from 2009 to 2008 related to cash payments for insurance and claims accruals resulting from the payment of receivables which resulteda large volume of claims in an approximately $14.7 million increase in cash from operating activities in 2008.

Net cash used in investing activities was $62.6 million in 2008 and $11.1 million in 2007. The increase in net cash used in investing activities was primarily the2009, including several large claims. Additionally, as a result of an increase in our acquisition of revenue equipment using balance sheet debt as opposed to operating leases, accelerated depreciation for tax purposes provided for an increase in the deferred tax provision, which resulted in an $8.7 million adjustment to net loss for the related non-cash activity in 2009 versus $2.5 million in the corresponding 2008 period. The decrease in our cash from operating activities was partially offset by an increase in our collections of receivables, primarily resulting from the impact of fuel prices on revenue and accounts receivable, which resulted in a $2.9 million increase in cash from operating activities in 2009.

Net cash used in investing activities was $63.0 million in 2009 and $62.6 million in 2008. In 2009, gross capital expenditures increased approximately $24 million, consistent with proceeds from our Daimler Facility and a decreasedispositions. The increase in proceeds from the sale of revenue equipment. We currently project netgross capital expenditures for 2009 will be in the rangewas primarily due to increasing our percentage of $65 to $80 million; however, such projection is subject to a number of uncertainties, including our plans for equipment replacementowned tractors and fleet size for 2009, which are still being finalized, as well as the prices obtained for used equipment.reducing tractors under operating leases.

Net cash provided by financing activities was $38.0 million in 2009, compared to $24.1 million in 2008 compared to $23.5 million used inprovided by financing activities in 2007. In2008. The primary contributors to the differences in our net cash provided by financing activities and net borrowings in the 2009 period, as compared to the 2008 we entered intoperiod, were the new Daimler Facility. At December 31, 2008, the Company had outstandingpurchase of additional tractors in 2009 using balance sheet debt as opposed to operating leases and fluctuations in checks outstanding in excess of $167.0 million, primarily consisting of $159.8 million drawn under the Daimler Facility and approximately $3.8 millionbank balances resulting from the Credit Agreement. At December 31, 2008, interest rates on thistiming of certain payments, partially off-set by lower debt ranged from 4.0% to 6.2%. At December 31, 2008, we had approximately $38.9 million of available borrowing remaining under our Credit Agreement.refinancing costs given the Company's new credit facilities in 2008.

We havehad a stock repurchase plan for up to 1.3 million Company shares to be purchased in the open market or through negotiated transactions subject to criteria established by the Board. No shares were purchased under this plan during 2008. At December 31, 2008, there were 1,154,100 shares still available to purchase under this plan,2009, which expiresexpired on June 30, 2009. However, ourwe remitted approximately $0.1 million to the proper taxing authorities in satisfaction of the employees' minimum statutory withholding requirements related to employees' vesting in restricted share grants. The tax withholding amounts paid by the Company have been accounted for as a repurchase of shares. Our Credit AgreementFacility now prohibits the repurchase of any shares.

shares, except those purchased to off-set an employee's minimum statutory withholding requirements upon the vesting of equity awards, without obtaining approval from the lenders. Material Debt Agreements

Credit Agreement

In September 2008, Covenant Transport, Inc., a Tennessee corporation ("CTI"), CTGL, Covenant Asset Management, Inc., a Nevada corporation ("CAM"), Southern Refrigerated Transport, Inc., an Arkansas corporation ("SRT"), Covenant Transport Solutions, Inc., a Nevada corporation ("Solutions"), Star Transportation, Inc., a Tennessee corporation ("Star";the Company and collectively with CTI, CTGL, CAM, SRT, and Solutions, the "Borrowers"; and each of which is a direct or indirect wholly-owned subsidiary of Covenant Transportation Group, Inc.), and Covenant Transportation Group, Inc.substantially all its subsidiaries entered into a Third Amended and Restated Credit AgreementFacility with Bank of America, N.A., as agent (the "Agent"), JPMorgan Chase Bank, N.A. ("JPM"), and Textron Financial Corporation ("Textron"; and collectively(collectively with the Agent and JPM, the "Lenders") that matures September 2011 (the "Credit Agreement"Facility").

The Credit AgreementFacility is structured as an $85.0 million revolving credit facility, with an accordion feature that, so long as no event of default exists, allows the BorrowersCompany to request an increase in the revolving credit facility of up to $50.0 million. Borrowings under the Credit Agreement are classified as either "base rate loans" or "LIBOR loans". As of December 31, 2008, base rate loans accrued interest at a base rate equal to the Agent's prime rate plus an applicable margin that adjusted quarterly between 0.625% and 1.375% based on average pricing availability. LIBOR loans accrued interest at LIBOR plus an applicable margin that adjusted quarterly between 2.125% and 2.875% based on average pricing availability. The applicable margin was 2.625% at December 31, 2008. The Credit AgreementFacility includes, within its $85.0 million revolving credit facility, a letter of credit sub facility in an aggregate amount of $85.0 million and a swing line sub facility in an aggregate amount equal to the greater of $10.0 million or 10% of the Lenders' aggregate commitments under the Credit AgreementFacility from time to time.

Borrowings under the Credit Facility are classified as either "base rate loans" or "LIBOR loans." Base rate loans accrue interest at a base rate equal to the greater of the prime rate, the federal funds rate plus 0.5%, or LIBOR plus 1.0%, plus an applicable margin that is adjusted quarterly between 2.5% and 3.25% based on average pricing availability. LIBOR loans accrue interest at the greater of 1.5% or LIBOR, plus an applicable margin that is adjusted quarterly between 3.5% and 4.25% based on average pricing availability. The unused line fee is adjusted quarterly between 0.25%0.5% and 0.375%0.75% of the average daily amount by which the Lenders' aggregate revolving commitments under the Credit AgreementFacility exceed the outstanding principal amount of revolver loans and the aggregate undrawn amount of all outstanding letters of credit issued under the Credit Agreement.Facility. The obligations of the Borrowers under the Credit AgreementFacility are guaranteed by Covenant Transportation Group, Inc.the Company and secured by a pledge of substantially all of the Borrowers'Company's assets, with the notable exclusion of any real estate or revenue equipment financed with purchase money debt,pledged under other financing agreements, including without limitation, tractors financed through our $200.0 million line of credit from Daimler Truck Financial.revenue equipment installment notes and capital leases.

Borrowings under the Credit AgreementFacility are subject to a borrowing base limited to the lesser of (A) $85.0 million, minus the sum of the stated amount of all outstanding letters of credit; or (B) the sum of (i) 85% of eligible accounts receivable, plus (ii) the lesser of (a) 85% of the appraised net orderly liquidation value of eligible revenue equipment, (b) 95% of the net book value of eligible revenue equipment, or (c) 35% of the Lenders' aggregate revolving commitments under the Credit Agreement,Facility, plus (iii) the lesser of (a) $25.0 million or (b) 65% of the appraised fair market value of eligible real estate. The borrowing base is limited by a $15.0 million availability block, plus any other reserves as the Agent may establish in its judgment. WeThe Company had approximately $3.8$12.7 million in borrowings outstanding under the Credit AgreementFacility as of December 31, 2008, and had2009, undrawn letters of credit outstanding of approximately $40.6$42.0 million, and available borrowing capacity of $27.7 million. The weighted average interest rate on outstanding borrowings was 6.25%.

The Credit Agreement includes usual and customary events of default for a facility of this nature and provides that, upon the occurrence and continuation of an event of default, payment of all amounts payable under the Credit Agreement may be accelerated, and the Lenders' commitments may be terminated. The Credit Agreement contains certain restrictions and covenants relating to, among other things, dividends, liens, acquisitions and dispositions outside of the ordinary course of business, and affiliate transactions. The Credit Agreement contains a single financial covenant, which requires us to maintain a consolidated fixed charge coverage ratio of at least 1.0 to 1.0. The financial covenant became effective October 31, 2008, we were in compliance at December 31, 2008, and such covenant was thereafter amended as described below.

On March 27, 2009, wethe Company obtained an amendment to ourits Credit Agreement,Facility, which among other things, (i) retroactively to January 1, 2009 amended the fixed charge coverage ratio covenant for January and February 2009 to the actual levels achieved, which cured our default of that covenant for January 2009, (ii) restarted the look back requirements of the fixed charge coverage ratio covenant beginning on March 1, 2009, (iii) increased the EBITDAR portion of the fixed charge coverage ratio definition by $3,000,000$3.0 million for all periods between March 1 to December 31, 2009, (iv) increased the base rate applicable to base rate loans to the greater of the prime rate, the federal funds rate plus 0.5%, or LIBOR plus 1.0%, (v) setsets a LIBOR floor of 1.5%, (vi) increased the applicable margin for base rate loans to a range between 2.5% and 3.25%3.25 % and for LIBOR loans to a range between 3.5% and 4.25%, with 3.0% (for base rate loans) and 4.0% (for LIBOR loans) to be used as the applicable margin through September 2009, (vii) increased ourthe Company's letter of credit facility fee by an amount corresponding to the increase in the applicable margin, (viii)(vii) increased the unused line fee to a range between 0.5% and 0.75%, and (ix) increased the maximum number of field examinations per year from three to four. In exchange for these amendments, wethe Company agreed to the increases in interest rates and fees described above and paid fees of approximately $544,000. Our$0.5 million.

The Credit Facility includes usual and customary events of default for a facility of this nature and provides that, upon the occurrence and continuation of an event of default, payment of all amounts payable under the Credit Facility may be accelerated, and the Lenders' commitments may be terminated. The Credit Facility contains certain restrictions and covenants relating to, among other things, dividends, liens, acquisitions and dispositions outside of the ordinary course of business, and affiliate transactions. The Credit Facility contains a single financial covenant, which required the Company to maintain a consolidated fixed charge coverage ratio will beof at least 1.0 to 1.0. The fixed charge coverage covenant became effective October 31, 2008, and the Company was in compliance with the covenant as follows after the amendment:of December 31, 2009.

On February 25, 2010, the Company obtained an additional amendment to its Credit Facility, which, among other things (i) amended certain defined terms in the Credit Facility, (ii) retroactively to January 1, 2010, amended the fixed charge coverage ratio covenant through June 30, 2010, to the levels set forth in the table below, which prevented a default of that covenant for January 2010, (iii) restarted the look back requirements of the fixed coverage ratio covenant beginning on January 1, 2010, and (iv) required the Company to order updated appraisals for certain real estate described in the Credit Facility. In exchange for these amendments, we agreed to pay the Agent, for the pro rata benefit of the Lenders, a fee equal to 0.125% of the Lenders' total commitments under the Credit Facility, or approximately $0.1 million. Following the effectiveness of the amendment, our fixed charge coverage ratio covenant requirement will be as follows:

One month ending March 31, 2009 | 1.00 to 1.0 |

Two months ending April 30, 2009 | 1.00 to 1.0 |

Three months ending May 31, 2009 | 1.00 to 1.0 |

Four months ending June 30, 2009 | 1.00 to 1.0 |

Five months ending July 31, 2009 | 1.00 to 1.0 |

Six months ending August 31, 2009 | 1.00 to 1.0 |

Seven months ending September 30, 2009 | 1.00 to 1.0 |

Eight months ending October 31, 2009 | 1.00 to 1.0 |

Nine months ending November 30, 2009 | 1.00 to 1.0 |

Ten months ending December 31, 2009 | 1.00 to 1.0 |

Eleven months ending January 31, 2010 | 1.00.80 to 1.01.00 |

TwelveTwo months ending February 28, 2010 | .65 to 1.00 |

| Three months ending March 31, 2010 | .72 to 1.00 |

| Four months ending April 30, 2010 | .80 to 1.00 |

| Five months ending May 31, 2010 | .85 to 1.00 |

| Six months ending June 30, 2010 | .90 to 1.00 |

| Seven months ending July 31, 2010 | 1.00 to 1.01.00 |

| Eight months ending August 31, 2010 | 1.00 to 1.00 |

| Nine months ending September 30, 2010 | 1.00 to 1.00 |

| Ten months ending October 31, 2010 | 1.00 to 1.00 |

| Eleven months ending November 30, 2010 | 1.00 to 1.00 |

| Twelve months ending December 31, 2010 | 1.00 to 1.00 |

| Each rolling twelve-month period thereafter | 1.00 to 1.01.00 |

Daimler Facility

On June 30, 2008, we securedCapital lease obligations are utilized to finance a $200.0 million lineportion of credit from Daimler Financial (the "Daimler Facility").our revenue equipment and are entered into with certain finance companies who are not parties to our Credit Facility. The Daimler Facility is securedleases terminate in January 2015 and contain guarantees of the residual value of the related equipment by both newthe Company, and used tractors and is structuredthe residual guarantees are included in the related debt balance as a combinationballoon payment at the end of retail installment contractsthe related term as well as included in the future minimum lease payments. These lease agreements require us to pay personal property taxes, maintenance, and TRAC leases.operating expenses.

Pricing for the Daimler Facility is (i)revenue equipment installment notes are quoted by Daimlerthe respective financial captives of our primary revenue equipment suppliers at the funding of each group of equipment acquired and consists ofinclude fixed annual rates for new equipment under retail installment contractscontracts. Approximately $185.6 million and (ii) a rate of 6% annually on used equipment financed on June 30, 2008. Approximately $159.8 million waswere reflected on our balance sheet under the Daimler Facilityfor these installment notes at December 31, 2008.2009 and 2008, respectively. The notes included in the Daimler funding are due in monthly installments with final maturities at various dates ranging from DecemberJanuary 2010 to December 2011.June 2013. The Daimler Facility containsnotes contain certain requirements regarding payment, insurance of collateral, and other matters, but doesdo not have any financial or other material covenants or events of default.

Additional borrowings underfrom the Daimler Facilityfinancial captives of our primary revenue equipment suppliers are available to fund new tractors expected to be delivered in 2009. Following relatively modest capital expenditures in 2007 and in the first half of 2008, we increased net capital expenditures in the last half of 2008 and we expect net capital expenditures (primarily consisting of revenue equipment) to increase significantly over the next 12 to 18 months consistent with our expected tractor replacement cycle. The Daimler Facility includes a commitment to fund most or all of the expected tractor purchases. The annual interest rate on the new equipment is approximately 200 basis points over the like-term rate for U.S. Treasury Bills, and the advance rate is 100% of the tractor cost. A leasing alternative is also available.2010.

Contractual Obligations and Commercial Commitments (1)

The following table sets forth our contractual cash obligations and commitments as of December 31, 2008:2009:

Payments due by period: (in thousands) | | Total | | | 2010 | | | 2011 | | | 2012 | | | 2013 | | | 2014 | | | There-after | |

| Credit Facility, including interest (2) | | $ | 12,686 | | | | - | | | $ | 12,686 | | | | - | | | | - | | | | - | | | | - | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Revenue equipment and property installment notes, including interest (3) | | $ | 207,837 | | | $ | 77,176 | | | $ | 59,409 | | | $ | 67,450 | | | $ | 3,802 | | | | - | | | | - | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Operating leases (4) | | $ | 81,989 | | | $ | 22,898 | | | $ | 9,650 | | | $ | 7,668 | | | $ | 5,358 | | | $ | 3,216 | | | $ | 33,199 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Capital leases (5) | | $ | 18,052 | | | $ | 2,177 | | | $ | 2,177 | | | $ | 2,177 | | | $ | 2,177 | | | $ | 8,064 | | | $ | 1,280 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Lease residual value guarantees | | $ | 23,594 | | | $ | 12,714 | | | $ | 10,880 | | | | - | | | | - | | | | - | | | | - | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Purchase obligations (6) | | $ | 98,014 | | | $ | 97,607 | | | $ | 407 | | | | - | | | | - | | | | - | | | | - | |

| Total contractual cash obligations | | $ | 442,172 | | | $ | 212,572 | | | $ | 95,209 | | | $ | 77,295 | | | $ | 11,337 | | | $ | 11,280 | | | $ | 34,479 | |

Payments due by period: (in thousands) | | Total | | | 2009 | | | 2010 | | | 2011 | | | 2012 | | | 2013 | | | There- after | |

| Credit Facility, including interest (2) | | $ | 3,940 | | | $ | 3,940 | | | | - | | | | - | | | | - | | | | - | | | | - | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Revenue equipment installment notes, including interest (3) | | $ | 175,067 | | | $ | 67,217 | | | $ | 59,405 | | | $ | 36,485 | | | $ | 11,960 | | | | - | | | | - | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Operating leases (4) | | $ | 98,959 | | | $ | 23,857 | | | $ | 19,658 | | | $ | 8,572 | | | $ | 7,290 | | | $ | 4,834 | | | $ | 34,748 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Lease residual value guarantees | | $ | 26,212 | | | | - | | | $ | 9,864 | | | $ | 16,348 | | | | - | | | | - | | | | - | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Diesel fuel and purchase obligations (5) | | $ | 67,000 | | | $ | 67,000 | | | | | | | | | | | | | | | | | | | | | |