CAUTIONARY NOTE REGARDING FORWARD LOOKING STATEMENTS

Certain oral and written statements made by Vystar Corporation about future events and expectations, including statements in this Annual Report on Form 10-K (the “Report”) contain forward-looking statements, within the meaning of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) and the Securities Act of 1933, as amended ( the(the “Securities Act”), that involve risks and uncertainties. For those statements, we claim the protection of the safe-harbor for forward-looking statements contained in the Private Securities Litigation Act of 1995. In some cases, forward-looking statements are identified by words such as “believe,” “anticipate,” “expect,” “intend,” “plan,” “will,” “may” and similar expressions. You should not place undue reliance on these forward-looking statements, which speak only as of the date of this Report or the statement. All of these forward-looking statements are based on information available to us at this time, and we assume no obligation to update any of these statements. Actual results could differ from those projected in these forward-looking statements as a result of many factors, including those identified in “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere. We urge you to review and consider the various disclosures made by us in this Report, and those detailed from time to time in our filings with the Securities and Exchange Commission (the “SEC”), that attempt to advise you of the risks and factors that may affect our future results. We qualify any forward-looking statements entirely by these cautionary factors.

The above-mentioned risk factors are not all-inclusive. Given these uncertainties and that such statements, speak only as of the date made; you should not place undue reliance on forward-looking statements. We undertake no obligation to update publicly or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

3

| ITEM 1. | BUSINESS |

Products and Services

For more information, visitwww.vytex.com, www.vystarcorp.com.

Natural Rubber Latex

Vystar Corporation (“Vystar”, the “Company”, “we”, “us”, or “our”)is based in Worcester, Mass., Vystar® Corp is the exclusive creator and exclusive owner of the innovative technology to produce Vytex®Vytex Natural Rubber Latex (NRL), a multi-patented, all-natural, raw material that contains significantly reduced levels of the proteins found in natural rubber latex and can be used in over 40,000 products, and the owner of RxAir UV light air purification products. Vytex NRL is a 100% renewable resource, environmentally safe, “green” and fully biodegradable. Vystar is working with manufacturers across a broad range of consumer and medical products bringing Vytex NRL to market in adhesives, gloves, balloons, condoms, other medical devices and natural rubber latex foam mattresses, toppers, and pillows.

Vytex is currently used in multiple mattress lines, including Natura™ and Gold Bond®; Jeffco manufactured components for toppers and mattresses, which are sold to multiple manufacturers; and private label toppers, pillows and mattresses sold online via sites such as Amazon and Bed Bath & Beyond. Vytex is also used in industrial adhesives, apparel padding and threads, shoes, sports equipment and electrical gloves and Vytex 3D printed fabrics available through partners like Tami Care. Liquid Vytex can be ordered wholesale through Halcyon Agri’s RCMA and CentroTrade.

About RxAir

RxAir promotes a healthy lifestyle through the use of its innovative, patented ViraTech air purification technology, thereby improving the quality of life of each and every customer. Independently tested by EPA- and FDA-certified laboratories, the RxAir has been proven to destroy greater than 99% of bacteria and viruses and reduce concentrations of odors and Volatile Organic Compounds (“NRL”VOCs”). The RxAir uses high-intensity germicidal UV lamps that destroy bacteria and viruses instead of just trapping them, setting it apart from ordinary air filtration units. RxAir® and ViraTech ® are registered trademarks of UV Flu Technologies, Inc. For more information, visit http://www.RxAir.com

The Vytex Division contains our global multi-patented technology that reduces antigenic and total protein in natural rubber latex products to virtually undetectable levels. Vytex NRL, our “ultra-low protein” natural rubber latex has been introduced throughout the worldwide marketplace that uses NRL or latex substitutes as a raw material for end products. Natural rubber latex or latex substitutes are used in an extensive range of products including balloons, textiles, footwear and clothing (threads), adhesives, foams (mattresses, pillows, mattress toppers, etc.), furniture (foam and adhesives), carpet, paints, coatings, protective equipment, sporting equipment, and, especially health care products such as condoms, surgical and exam gloves, among others. Our challenge has been that a manufacturer’s conversion from the use of standard latex or synthetic raw material to Vytex NRL involves a protracted sales cycle ranging from eighteen to thirty-six months. We have seen that same cycle apply to the newest version of Vytex NRL, a dry rubber sampling targeted for the tire and tubing industries. Additionally, in the past, our primary method of distribution was via toll manufacturing. We now have several licensing agreements in place for global distribution that have allowed us to focus on and transition to sales and marketing with a technical oversight.

Natural rubber latex is an agricultural product produced from the sap of the rubber tree,Hevea brasiliensis. In presentations at the 5th World Elastomer Conference held in Dusseldorf, Germany during early March 2018 it was noted that there was a slowing growth rate in global NR consumption and it was predicted demand would fall over the next two years. The numbers 1 and 2 producers (Thailand and Indonesia) had a modest fall in production while Malaysia, China and India showed a large negative gap between output and capacity mainly based on current low prices. Vietnam continues at 85 to 95% capacity. There is a huge natural rubber capacity surplus until the early 2030s and prices will remain flat through 2025. With growing substitution of synthetics, that an uptick in prices may not occur and based on the pricing of synthetics the market share competition may weigh more to synthetics.

Substantially all the latex processors are in Southeast Asia, India, Africa and Latin America and are owned by local groups or large multinational corporations. This future demand is awakening interest in other areas of the world where the climate is suitable, particularly in Guatemala, where focus now shifts to certifications from the Forestry Stewardship Council and Rainforest Alliance, as a specialty latex. In addition to the resurgence of Central and South America in natural rubber latex production, countries such as Vietnam, Cambodia and Cameroon have launched major efforts to meet the needs of the global liquid natural rubber latex market. Vietnam is now a major processor of our Vytex NRL and severalNRL. Several trial runs of the specialty offerings discussed below that are in place for manufacturer trials and wetrials. We now have two producers in Guatemala, one in the trial phase.

Our initial product portfolio included Vytex NRL in high ammonia (HA) and low ammonia (LA) formulations. New specialized formulations are projected to come to market over the next year with trials in ultra-low ammonia, pre-vulcanized and low nitrosamine versions currently taking place. Vystar has used its technology to work with customers to solve production issues and provide them with a point of difference and guidance as research using Vytex has headed into directions previously thought to be off-limits to natural rubber latex. It appears to be the removal of the vast majority of the proteins, the carotenoids and the non-rubbers that affords Vytex NRL this opportunity.

Board of Directors Member and Research & Development Director Ranjit K. Matthan, Ph.D., revealed ongoing developments in the formulation of Vytex NRL with reduced or no ammonia and nitrosamines at the International Latex Conference (ILC) session titled “Advances in Environmentally Friendly Ultra Low Protein Natural Rubber Specialty Latices” on August 12, 2015. The significant advances in aluminum hydroxide-treated Vytex NRL properties and applications are potential game-changers for the issues of volatile organic content and nitrosamines for some critical latex products, such as balloons, catheters, condoms, and other medical devices, as well as enabling cleaner and more sustainable work environments. The expanded Vystar product grades make it applicable in a wider range of latex products with the advantage of improved environmental impact through reduced leachables/extractables. The advances deliver a simplified, sustainable, totally safe raw material that Vystar can offer for several applications without reservations about nitrosamines. Vystar has initiated a scale up to lab production of all three newer versions of Vytex NRL and has commenced a sample fulfillment mode with a significant manufacturer of women’s intimate apparel who is in the final testing stages of two of the grades (no ammonia and ultra-low ammonia) as possible replacements of their current raw materials.

Recently at the Nuremberg Toy Show (Speilwarenmesse) Vytex NRL was a targeted product for manufacturers of balloons, masks, etc. On the main page of the European Balloons and Party Council web sitewebsite there is still a Yahoo video still plus a recent press release that discusses the benefits of Vytex NRL in items such as balloons. As there is a new proposal for limits on protein content of balloons by virtue of an EN listing, Vytex has now gone in to full prevulcanized testing to start the sampling process in selected areas based on manufacturing needs.

Over the course of several years, our technical groups have presented technical papers of varying topics that still hold relevance. Vytex NRL is produced at the latex processor level and can be integrated into the current processing environments without additional capital equipment investment. The protein removal and modification process that leads to Vytex NRL allows manufacturers to lower manufacturing costs with the benefit of reduced protein levels. Reduced leaching times and resulting reductions in energy, water and material handling consumption can lead to realized cost savings.

Also, the article “Eco-Friendly Manufacturing of High Performance Latex using Ultra Low Antigenic Protein Latex” reviewed some of the learnings Vystar had made since commercializing Vytex NRL. Among these discoveries were: improved air and helium retention in balloons; reduced leaching needs for some dipped products; truer colors for dyed dipped products (such as balloons); and low latex odor in foams, which has now led to unique research into areas previously considered off-limits to NRL. Vystar published and presented a paper, “Further Development of Vytex® Natural Rubber Latex Leads to Strong Niche Market Advances”, that added additional learnings related to slow release (memory) foam formulations and other technical improvements helping customers solve their new product development challenges.

Vystar has transitioned from toll manufacturing agreements to licensing agreements that eliminate the need to maintain a costly infrastructure along with the other investment and regulatory compliance costs to develop and operate a processing or manufacturing facility. All of these costs are or will be borne by our manufacturing and distribution contractors and/or customers. This means we must show the NRL producers and product manufacturers the economic value proposition of including Vytex NRL in their product lines, hence the technical paper presentations we have made and continue to make. In addition, as an all-natural raw material, Vytex NRL puts the main component in gloves and other products back in the environmentally friendly arena.

To implement our licensing model, in March 2010 we signed a licensing agreement with Pica de Hule Natural, a division of Grupo Agroindustrial de Occidente (“Occidente”), located in Guatemala. Occidente is the largest processor of natural rubber latex in Latin America and the largest exporter serving more than 15 countries. Under the agreement, Occidente will manufacture, sell and market Vytex NRL throughout Latin America as well as supply Vytex NRL to North America and Europe. This agreement was continued in 2017 and remains in place currently.

Additionally, in 2017, Vystar began trials to process various Vytex offerings, including pre-vulcanized grades, at Forteleza’s new facility in Guatemala with initial good results. This is an important strategic maneuver to handle demand in the North, Central and South American regions as well as certain areas of Southeast Asia. This will lead to a new agreement between the two companies upon successful completion of the trials.

In addition, in January 2009, we entered into a Distribution Agreement with Centrotrade Minerals & Metals, US and Centrotrade Deutschland, GmbH, Germany, a leading global distributor of latex raw materials, to create a worldwide distribution network that will further enhance our ability to cost effectively reach and service manufacturer customers in these key manufacturing areas. This provides an expansive distribution network that facilitates both the licensing and toll manufacturing models and can assist with various processors in taking their products to market. On December 19, 2012, we amended our agreement with Centrotrade to expand Vytex NRL distribution rights to the world’s largest NRL consuming markets in Southeast Asia, specifically Malaysia and Thailand. Under this new license agreement, Centrotrade controls production scheduling of Vytex NRL, inventory in Thailand, sales, pricing and customer financing, while Vystar will focus on marketing, customized product development, as noted above, and support activities. Vystar currently has no exclusive areas under contract as RCMA, a Dutch based distributor was added in 2016.

In December 2017 Halcyon Agri, the owners of Centrotrade, announced that they had acquired RCMA’s polymer group and would operate it under the Wurfbain label.

The paper entitled, “The Non-Enzymatic Deproteinization of Natural Rubber Latex (DPNRL) Enabling the Greater Versatility in End Product Applications” discussed improvements that extend beyond the ultra-low allergenicity of the DPNRL and include improved color, absence of rubber odor, and improved physicochemical attributes. Improved air and helium retentions results were reported. The potential to extend applications into other non-conventional areas other than latex end products was discussed and we are currently in the final retail test market stages for the United States based manufacturing of mattresses, pillows and toppers to key furniture stores and buying groups, primarily in the Northeastern United States and signed a 5 year renewable agreement in January 2015 with Nature’s Home Solutions (NHS) to exclusively distribute these products in the United States. In September 2016, the Vystar Board of Directors voted to end the January 2015 NHS agreement and replace it with a global exclusive for foam manufactured with Vytex and sold into the home furnishings industry. This change reflects the global nature of the mattress, topper and pillow businesses, the need for local warehousing, and access to container loads of foam cores and pillows for European and Asian manufacturers.

In April of 2018 Vystar acquired the assets of NHS Holdings, LLC (NHS) executing on the first part of the Company’s vision to move into direct product offerings made from Vytex® latex. NHS was the exclusive U.S. distributor of Vystar’s Vytex® natural rubber latex foam to manufacturers for use in over 200 home furnishings products, including mattresses, toppers, pillows and upholstery, sold through multiple channels. This acquisition provides Vystar with roll packing and cutting equipment to support our bedding manufacturing partners, while lowering the cost of Vytex to the manufacturer by eliminating the middleman.

Now unified under the Vytex brand, we anticipate developing additional product offerings and solidifying partnerships with multiple major manufacturing partners throughout the home furnishings industry. We anticipate our new offerings will include cushions and padding for use in seating and other products which we believe will achieve higher margins.

NHS was a related party transaction for Vystar, approved by NHS members, who are also major Vystar shareholders, business partners and insiders. Notable NHS members include:

| ● | Lam Ngoc Minh, CEO of Lien ‘A, which is one of the world’s largest latex foam manufacturers, and a major producer of Vytex foam. Lien ‘A has worked closely with NHS to develop traditional and innovative new foam products; | |

| ● | Keith Osborn, MD; member of Vystar Board of Directors, orthopedic spine surgeon and Vystar’s largest shareholder; | |

| ● | Bryan Stone, MD, member of Vystar Board of Directors, nephrologist and CEO of Fluid Energy Conversion; | |

| ● | Joseph Allegra, MD, Director at Oncology Molecular Imaging LLC, a Director & Owner at Cyber Logistics, Inc., a Founder at Diamond Investments II LLC and an Owner at Lincoln Lee Investments LLC; and | |

| ● | Steven Rotman, now CEO of Vystar, and CEO of Rotmans Furniture and Carpet, a large independent furniture retailer. |

On April 18, 2018, Vystar acquired assets of NHS for 27,769,500 shares of restricted common stock of Vystar valued at approximately $1.1 million. NHS assets included: current inventory, equipment and intellectual property related to product development.

Vytex is considered by many as one the best foam product in the world, as it is sustainably sourced; biodegradable; purer and more resilient and durable than competitors’ latex; virtually free of odor, VOCs and allergenic proteins; and competitively priced for a wide array of over 40,000 products. Vytex is available in many offerings such as low/no ammonia and low/no nitrosamine formulations, which are now being required in certain countries and by certain manufacturers. Vystar anticipates fulfilling this multi-billion-dollar market need with Vytex.

Vystar has also expanded licensing arrangements into the consumer arena, with the licensing of foam products produced with and labeled as “Made with Vytex NRL”. Specifically working with partners, to introduce foam made with Vytex into the mattress, mattress topper and pillow arenas aligning with key foam manufacturers, mattress, mattress toppers and pillow producers, and furniture stores in specific areas of the Unites States. In May 2018, Vystar announced the signing of the aforementioned exclusive global distribution agreementacquisition with Worcester, MA based NHS who sources eco-friendly materials and technologies for use in furnishings and other markets. NHS has completed several trials with Vietnamese, European and Indian makers of foam products to use its Vytex NRL raw material in their current offerings in their own areas as well as to supply added needs for foam cores in both the mattress and topper arenas globally. The current requests from major mattress manufactures for Vytex foam trials involves different densities especially those used on the upper levels of mattresses. The samples have been presented to the manufacturers and feedback has been very positive with names such as Gold Bond, King CoilKoil (Natura) and SpringAirSpring Air (Nature’s Rest) adding Vytex to their current offerings. A similar trial occurred in October 2016 in Thailand focusing on specific densities and pillows, and a meeting with a Belgian foam maker using a unique drying concept occurred in May 2016 with discussions ongoing. In addition, with the acquisition of NHS and working with NHS and a large Vietnamese foam manufacturer, Lien A, the group attended the International Sleep Products Association (ISPA) in Orlando in March 2016 and has followed that joint effort with ISPA 2018 in Charlotte, North Carolina.and 2019. The significance of ISPA is the focus on components for use with major mattress and pillow manufacturers, which takes Vytex foam to an additional audience.

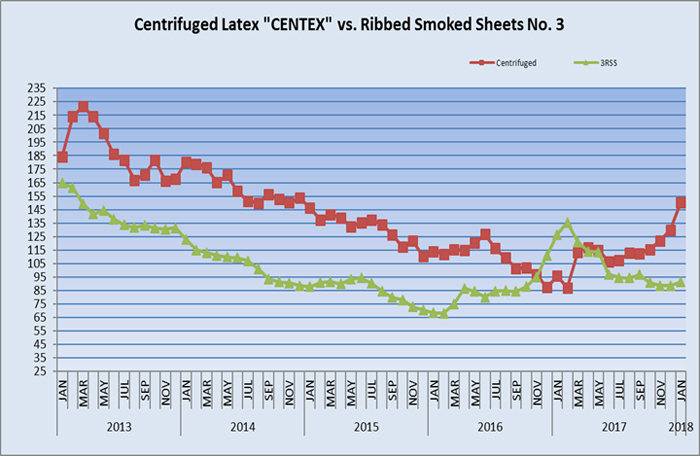

Pricing of materials in the rubber and latex industries continues to fluctuate as noted by the graph below courtesy of Centrotrade. Prices of centrifuged latex, thus Vytex, have risen throughout 2016, 2017, and into early 2018 due to various factors such as floods in southern Thailand, removal of older tress and replanting which is a seven-year process, newer plantations coming online, etc.Competition

Competition

Natural Rubber Latex

Synthetic raw materials such as ethylene, propylene, styrene and butadiene compete with NRL. Currently, it is estimated that NRL processors have lost one-half of the overall latex market to synthetic latex. Despite the switch to non-latex alternatives, it is estimated that almost 70% of exam gloves and nearly 80% of surgical gloves used in U.S. hospitals are still made with NRL.

During 2017 and 2018 Vystar contracted with varioustwo consultants and manufacturers to make exam and surgical gloves on an OEM basis. The testing and results were encouraging and led to further efforts prepare for a potential launch of these lines in 2018.2019. The company is going to proceed with testing and subsequent filing with the USFDA to obtain 510(k) allowances. With this new OEM structure, the Company will bring several versions (surgical, exam, household, etc) of the gloves to market under its own OEM brand label.

Several attempts, including new source crops, synthetic lattices and various treatment methods, have been made by competitors to eliminate problem proteins from Hevea NRL by biological, physical and/or chemical methods that act on proteins. One approach has been to introduce the latex articles to multiple leaching steps and chlorination. While it does reduce the protein levels in the finished product, it weakens the latex film thus compromising the desirable physical properties of the product. Another attempt to reduce proteins in NRL is the use of proteolytic enzymes to degrade the proteins in the latex solution but this approach introduces another protein (the enzyme) to the latex, which may itself be allergenic. Attempts to commercialize two other non-Hevea NRL materials have been made in the United States: guayule rubber latex and Taraxacum kok-saghyz, also known as the Russian dandelion. These materials are reported to be higher in cost compared to natural rubber latex and presently are available only in limited quantities.

These facts, coupled with the uncomplicated transition to the utilization of Vytex NRL, make it very attractive for processors to regain lost business by switching to Vytex NRL. We believe our unique patented technology offers a viable alternative to the marketplace. The licensing model will allow the message to spread through more sales channels than we could reach in the past.

Intellectual Property

Vystar has four issued patents by the United States Patent Trademark Office (“USPTO”) that were issued in 2005 (Patent No. 6,906,126), 2006 (Patent No. 7,056,970), 2011 (Patent No. 8,048,951) and 2012 (Patent No. 8,324,312). International patents include one issued patent from the Republic of South Africa in 2009 (2008/00886)(2008/00886), a second foreign patent issued by China in 2011 (No. 200580051526.1)200580051526.1), a third foreign patent issued by Japan in 2012 (No. 4944885) and a fourth foreign patent issued by Hong Kong in 2013 (HK1125959). In 2005, we sought international patent protection of our application that would become our U.S. Patent No. 6,906,126 pursuant to the Patent Cooperation Treaty (“PCT”) (No. PCT/US2005/025018), and this application has been nationalized in the following countries and regions: The European Union (No.05775523.3)(No.05775523.3), Canada (No. 2,614,945), India (No.295/DELNP/2008), and Sri Lanka (No.14827). Additionally, this PCT was nationalized back into the United States to expand our protection to both method and composition claims (No.11/988,498). We expect patents to be issued in these countries without objection.

On January 18, 2012, we converted the provisional patent filed January 18, 2011 (No. 61/433,853) to full utility applications based on new discoveries and unexpected results (No. 13/374,851). We also sought international protection for the new developments and unexpected results reflected in this 2009 USPTO patent application through another PCT application (No. PCT/US2009/031445). This PCT application was nationalized in the following countries in 2010: the European Union (No. 09702339.4)09702339.4), Brazil (No. PI0906513-0), Guatemala (No. 2010-000208)2010-000208), India (No.2487/KOLNP/2010), Indonesia (No. W-00201002436), and Malaysia (No. PI2010003317). In addition, we filed the same patent application that was the subject of our USPTO patent application No. 12/356,355 and PCT/US2009/031445 directly into Thailand (No. 0901000201)0901000201). Thailand has informed us our patent application is now published for open comments and Vystar has responded to various questions by Thailand’s patent office and is awaiting their response.

On January 18, 2017 Vystar was informed that the Indian Patent Office approved our application (2487/KOLNP/2010) entitled, “Natural Rubber Latex Having Reduced Allergenicity and Method of Making” under Patent Number 279323.

On February 8, 2017 Vystar received notice of grant from the Guatemalan Patent Office for application number 2010-000208 entitled, “Natural Rubber Latex Having Reduced Allergenicity and Method of Making” and is awaiting a grant number.

On October 27, 2017 Vystar was granted its second Indian patent (288824) from Application No.: 295/DELNP/2008 entitled: “Decreasing Allergenicity of Natural Latex Rubber Prior to Vulcanization.” The European Patent Office issued a Decision to Grant Vystar’s patent application under European Patent Number 1 902 089 titled “Decreasing Allergenicity of Natural Latex Rubber Prior to Vulcanization” greatly expanding the territory covered by the Company’s intellectual property portfolio. The mention of the grant was published in the European Patent Bulletin 13/35 dated 28 August 2013. Vystar selected the United Kingdom (065143-011612/UK)(065143-011612/UK), Germany (065143-011611/DE)(065143-011611/DE), and Austria (065143-001610/AT)(065143-001610/AT) as validation points for this specific patent. There is a

In March 2019 Vystar Corp.was granted European, EP Patent No. 2238183 (its second patent application still inEuropean patent) entitled “Natural Rubber Latex Having Reduced Allergenicity and Method of Making Same.” Vystar now holds 13 foreign and 4 U.S. patents related to its latex deproteinization process for the production of Vytex®, a natural rubber latex (NRL) that is virtually free of allergen-causing latex proteins, for products including balloons, examination and surgical gloves, condoms, breather bags, latex tubing, probe covers, catheters, threads, foams, cold seal and pressure sensitive adhesives. Vystar has now broadened its protected areas in Europe that can expandto include additional manufacturing areas in Germany, the countries that are validated.United Kingdom, France, Spain and Italy, which account for much of latex product manufacturing in Europe for another ten years.

On December 9, 2016 Vystar was notified by our Singaporean IP Counsel that Malaysia Application No PI 2010003317 entitled “Natural Rubber Latex Having Reduced Allergenicity and Method of Making” was cleared for issuance and that a Notice of Grant will be issued.

Vystar filed and has received registered trademark protected status in the United States for the marks “Vystar”, “Vytex” and “Created by Nature. Recreated by Science.” In 2010 Vystar filed for international trademark protection of “Vytex” in Malaysia (No.2010013149)(No.2010013149) and India (No. 1992991)1992991), which was granted in India. On November 18, 2014, the Company was informed that the “VYTEX” trademark was registered in Malaysia effective May 30, 2014. The aforementioned trademarks have been renewed successfully in each period as required.

While we believe that the pending patent and trademark applications will be granted without objection, there are no guarantees that all such patents or trademarks will be granted by each relevant governing body. No assurance can be given that such patent and trademark protection will provide substantial protection from competition. We realize that the market for Vytex NRL is an industrialized world concern and we are committed to aggressively challenging any infringements of our patents and/or trademarks. As of December 31, 2017,2018, Vystar has expended, since inception, approximately $290,195$370,245 on such patent and trademark costs and has budgeted approximately $25,000$55,000 more for the year ended December 31, 20182019 to continue to pursue and maintain its patents and trademarks around the world.

Research and Developmentworld

Vytex NRL has produced protein test results on finished products that are both “below detection” and “not detectable” in termsRXAIR Intellectual Property

In May of 2018, Vystar acquired substantially all of the amountassets of proteins remaining in these finished goods made with Vytex NRL. These results have been reproduced in many subsequent tests. From inception through December 31, 2017, Vystar’s researchUV Flu Technologies, Inc., formerly traded on the OTC under the ticker UVFT, whose patented ViraTech™ UV light air purification technology destroys greater than 99% of airborne bacteria, viruses and development costs have been approximately $2.4 million. These efforts pastother microorganisms and future have beenvirtually eliminates concentrations of odors and will continue to be patented and/or trademarked.volatile organic compounds (VOCs).

UV Flu’s product line includes:

| ● | RXair™ Residential Filterless Air Purifier |

| ● | UV400 ™ FDA cleared Class II Filterless Air Purifier |

| ● | RX3000™ Commercial FDA cleared Class II Air Purifier (news video with RX3000) |

Vystar acquired all UV Flu intellectual property, multiple patents, product lines, tooling, FDA clearances, research data, websites and other assets related to the business.

Government Regulation

In the United States, healthcare and many food and food-based packaging products are subject to regulation by the Food and Drug Administration (FDA). Vystar is not directly subject to regulation by the FDA due to the fact that it does not manufacture a finished medical device or other product, but only provides Vytex NRL as a component or raw material to healthcare or other product manufacturers. However, there will be FDA regulation of the labeling of healthcare and food-based packaging products that are produced with Vytex NRL and the FDA has promulgated standards for good manufacturing practices for manufacturing the end products, which makes the end product manufacturers responsible for seeing that all of their components and component manufacturers, including Vytex NRL, are produced using goodquality manufacturing processes. Additionally, the FDA prohibits the use of the term “hypoallergenic” or “low protein” on any natural rubber latex product it regulates. In order to make any such claim, the latex product manufacturer must seek a waiver from the FDA of such regulatory prohibitions. Commentary by the FDA in its guidance documents and other rulings indicate that the prohibition on the use of the “hypoallergenic” or “low protein” label is based, at least in part, on the fact that, although the use of such terms in such labeling may be intended to indicate that the risk of allergic reaction to residual levels of processing chemicals has been reduced, consumers may interpret the labeling to mean that the risk of allergic reactions to any component in the device would be minimal. Thus the hypoallergenic or low protein label is deemed misleading. There can be no assurance, however, that we will succeed in securing FDA approval for any claim regarding the “hypoallergenic” “low protein” or reduced allergy potential of latex produced with the Vytex NRL process. Failure to secure, if required, such FDA approval, could delay or otherwise detrimentally affect our introduction to natural rubber latex healthcare and/or food packaging products regulated by the FDA. Notwithstanding, the medical or food packaging manufacturer will be able to use the Vytex NRL trademark on its label if size permits to indicate only that the Vytex NRL component was used in the production of the healthcare product, and what protein levels the end product does contain, but no further claim is asserted. We have been able to provide sufficient testing data to the FDA to support our protein level claims with respect to the natural rubber latex antigenic and total proteins present in end products made with Vytex NRL. On May 1, 2009, a condom manufactured from Vytex NRL received 510(k) clearance from the U.S. Food and Drug Administration. This was the first medical product available in the U.S. made from Vytex NRL, which had less than 2 micrograms/dm2, virtually undetectable levels, of the antigenic proteins that cause an allergic response, while retaining and improving upon all of the desirable qualities of latex. While the product is no longer available, thisThis condom is a predicate device for future products and the 510(k) is still in existence. Vystar continues to seek other U.S. and global manufacturers interested in pursuing similar claims for products.

On July 22, 2009, a non-powdered medical exam glove manufactured with Vytex NRL received 510(k) clearance from the FDA, with an approved claim of less than 50 micrograms/gram of total proteins. As with the condom product, Vystar continues to pursue U.S. and global manufacturers using this exam glove as a predicate device and to help fill pending exam glove business. Late in 2016 the FDA banned the use of powder in medical gloves which took effect early in 2017 positioningadvantaging the position of the Vytex non-powdered exam glove in an excellent position.glove..

Inflation and Seasonality

We do not believe that our operations are significantly impacted by inflation. Our NRL business is not seasonal in nature but is subject to commodity pricing. Our NRL product is a commodity-based raw material and prices for such material fluctuate from day-to-day, though this will have less impact as we transition to sales via licensing fees.

Employees

As of December 31, 2017,2018, Vystar had a total of one associate.associate, Steven Rotman, CEO.

Corporate Information

Vystar Corporation is a Georgia corporation that was incorporated in 2003. Our predecessor company, Vystar LLC, was formed by our founder, Travis Honeycutt, in February 2000 as a Georgia limited liability company.

Our principal mailing address is 101 Aylesbury Rd., Worcester, MA 01609. Our website address is www.vytex.com. www.vytex.com & www.vystarcorp.com.

The information contained on, or that can be accessed through, our website is not a part of this Report. We have links on our website to reports, information statements, and other information that we file electronically with the Securities and Exchange Commission, or SEC, at the Internet website maintained by the SEC, www.sec.gov. In addition to visiting our website and the SEC’s website, you may read and copy public reports we file with or furnish to the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330.

| ITEM 1A. | RISK FACTORS |

Our business is subject to a number of risks and uncertainties — many of which are beyond our control — that may cause our actual operating results or financial performance to be materially different from our expectations. If one or more of the events discussed in the following risksbelow were to occur, actual outcomes could differ materially from those expressed in or implied by any forward-looking statements we make in this report or our other filings with the SEC, and our business, financial condition, results of operations or liquidity could be materially adversely affected; furthermore, the trading price of our common stock could decline and our shareholders could lose all or part of their investment.

Vystar presently does not generate the cash needed to finance its current and anticipated operations.

The Company has had very limited revenue in its history prior to 2011 and transitioned from the development stage to the operational stage during the fourth quarter of 2009. The Company is still in the early stage of establishing our business including attracting new customers and increasing sales; oursales. Our financial success will be dependent upon the soundness of our business concept, our management’s ability to successfully and profitably execute our plan, and our ability to raise additional capital.

Our limited operating history makes it difficult to evaluate our business. We expect to make significant future operating expenditures to develop and expand our business into areas such as OEM product lines and offerings in the mattress and furniture arenas. We may incur significant losses in the future for a number of reasons, including due to the other risks described in this Report, and we may encounter unforeseen expenses, difficulties, complications and delays and other unknown events. Accordingly, we may not be able to achieve or maintain profitability, and we may incur significant losses for the foreseeable future. See additional discussion under Liquidity and Capital Resources.

At December 31, 20172018 our cash position was $50,052 and we had $13,502 cash on hand and an accumulated deficit of $27,999,122.$34,072,553. We plan to finance our operations for the next twelve (12) months through the use of cash on hand, stock warrant exercises from existing shareholders, raising of capital through private placements and the possible acquisition of a cash flow positive foam business in key areas of the furniture world that includes finished mattresses, component cores, topper cores and pillows. You should consider, among other factors, our prospects for success in light of the risks and uncertainties encountered by companies that, like us, have not generated net earnings on an annual basis. Various factors, such as economic conditions, regulatory and legislative considerations, and competition, may also impede our ability to expand our market presence. We may not successfully address these risks and uncertainties or successfully implement our operating strategies. If we fail to do so, it could materially harm our business and impair the value of our common stock. Even if we accomplish these objectives, we may not generate positive cash flows or profits we anticipate in the future.

The following risk factors apply to our Vytex Division:

Our Vytex operating results could fluctuate and differ considerably from our financial forecasts.

Our business model is based on assumptions derived from (i) the experience of the principals of the Company, and (ii) third party market information and analysis. There are no assurances that these assumptions will prove to be valid for our future operations or plans.

Our operating results may fluctuate significantly as a result of a variety of factors, including:

| ● | Acceptance by manufacturers of the Vytex Natural Rubber Latex technology; | |

| ● | Our ability to achieve and sustain profitability; | |

| ● | Consumer confidence in products manufactured using our Vytex Natural Rubber Latex technology; | |

| ● | Our ability to raise additional capital. |

Our Vytex NRL Division business is totally dependent on market demand for, and acceptance of, the Vytex Natural Rubber Latex process.

We expect to derive most of our Vytex NRL Division revenue from the sales of our Vytex Natural Rubber Latex raw material to various manufacturers of rubber and rubber end products using NRL through our distribution agreement with Centrotrade Deutschland. We pay natural rubber latex processors a fee for the service of manufacturing and creating Vytex NRL for us under our toll manufacturing agreements. Conversely, Vystar collects a fee under the Centrotrade and Occidente (PICA) licensing models. The agreement in the bedding and furniture industries with NHS also provides income based on a license model. Our Vytex NRL product operates within broad, diverse and rapidly changing markets. As a result, widespread acceptance and use of product is critical to our future growth and success. If the market for our product fails to grow or grows more slowly than we currently anticipate, demand for our product could be negatively affected.

Our ability to generate significant revenue in the Vytex Division is substantially dependent upon the willingness of consumers to make discretionary purchases and the willingness of manufacturers to utilize capital for research and development and the retooling of their manufacturing process, both of which are impacted by the state of the economy.

The current state of the world economy has and likely will in the future impact upon our ability to increase revenue. Certain of the products that we anticipate will be manufactured with our Vystar NRL process, such as mattresses and sponge products, are considered discretionary consumer purchases which decline during economic downturns. Additionally, certain manufacturers who might otherwise utilize the Vytex NRL process in the manufacturing of products with NRL have determined not to expend capital to complete the research of the Vytex NRL process or to retool their manufacturing process because of the general downturn in the economy. As part of a strategy to increase awareness of the Vytex NRL brand, the Company has been aggressively seeking to have end products produced and labeled “made with Vytex NRL” such as mattresses, toppers and pillows. As these products enter the market, the Company plans to create consumer awareness of these end products and in so doing begin to develop consumer demand pull through as part of the Company’s efforts to complete the push-pull cycle using an ingredient branding strategy.

Assertions by a third party that our Vytex process infringes its intellectual property, whether or not correct, could subject us to costly and time-consuming litigation or expensive licenses.

There is frequent litigation based on allegations of infringement or other violations of intellectual property rights. As we face increasing competition and become increasingly visible as an operating company, the possibility of intellectual property rights claims against us may grow.

Any intellectual property rights claim against us or our customers, with or without merit, could be time-consuming, expensive to litigate or settle and could divert management attention and financial resources. An adverse determination also could prevent us from offering our process, require us to pay damages, require us to obtain a license or require that we stop using technology found to be in violation of a third party’s rights or procure or develop substitute services that do not infringe, which could require significant resources and expenses.

The latex market in which we will participate is competitive and if we do not compete effectively, our operating results may be harmed.

The markets for our product are competitive and rapidly changing. With the introduction of new technologies, increasing scrutiny of alternative lattices such as Russian dandelion, and new market entrants, we expect competition to intensify in the future. In addition, pricing pressures and increased competition generally could result in reduced sales, reduced margins or the failure of our products to achieve or maintain widespread market acceptance.

While early interest was strong in a new innovative product in the natural rubber latex industry, pricing and regulatory approvals remain a key selling factor especially in the exam glove arena. There is no exam glove manufacturer signed to date that has accepted Vytex NRL into its product mix.

Our Vytex revenue will vary based on fluctuations in commodity prices for NRL.

NRL is a commodity and, as such, its price fluctuates on a daily basis. Our raw material revenue including licensing fees and cost of goods will also fluctuate upward or downward based upon changing market prices for the raw material used to produce Vytex NRL. Prolonged periods of lowered market prices can also cause manufacturers to review synthetic price drops as they look for even lower cost alternatives to NRL. A current example of the fluctuations is shown above in the Centrifuged Latex graph

While Vytex NRL has received 510(k) clearance from the FDA for condoms and exam gloves, there is no assurance that future applications will be cleared.

In order for Vytex to be used in medical device applications, the manufacturer of the end product must submit an application to the FDA. If the device is classified by the FDA as Class II (e.g., condoms, surgical gloves, and most non-cardiac and non-renal/dialysis catheters) and in some cases Class I (e.g., exam gloves), a 510(k) application must be filed with the FDA seeking clearance to market the device based on the fact that there is at least one other predicate or similar device already marketed. If the product is classified as a Class III product (e.g., most cardiac and renal/dialysis catheters, certain adhesives and other in vivo devices), or is otherwise a new device with no predicate on the market already, then the manufacturer of the end product must submit a Pre-Market Approval (“PMA”) application seeking approval by the FDA to market the device. The PMA approval process is much more in depth and lengthy and requires a greater degree of clinical data and FDA review than does a 510(k) clearance process.

Since Vytex is a raw material and not an end-product, Vystar is not the entity that files with the FDA for any clearance or approval to market a device. Instead, the end-product manufacturers who will be selling and marketing the device(s) must submit applications and seek FDA clearance or approval depending upon the device classification. Vystar’s role in this process is only as background support to the manufacturers to supply information and any technical or test data regarding the Vytex raw material if and to the extent needed.material.

An American manufacturer of condoms and exam gloves had been engaged in production work and had completed required testing and received FDA clearance for using Vytex NRL in their condom and exam glove lines. However, this manufacturer is not currently producing products made with Vytex NRL or any other type of raw material. Notwithstanding such approvals, we have no assurance that future products will provide acceptable test results and even if they do, there is no certainty that the FDA will approve the applications.

Each of the above mentioned 510(k)s have been sold to other manufacturers hence the need to pursue 510(k)s for the newer manufacturing facilities.

Vytex may seek to have lower protein claims than what is currently on the market today for exam gloves and may ultimately seek to have latex warnings removed from or modified on all FDA-regulated products, but it cannot guarantee that either of such actions will be approved by the FDA.

The FDA heavily scrutinizes any and all claims categorizing the protein levels and other claims of an NRL product. Currently, the FDA has allowed claims only stating the level of less than 50 micrograms/gram of total extractable proteins pursuant to only one of two FDA-recognized standards on exam or surgical gloves. Vystar intends to claim protein levels pursuant to both of the two FDA-recognized standards, which will result in claiming the lowest level of antigenic proteins for a Hevea NRL product currently on the market. Although the FDA has cleared such claims on the condom using Vytex NRL, the FDA rejected those claims for the exam glove. There is no guarantee that the FDA will ultimately or ever allow these claims on an exam glove.

Additionally, for many years, the FDA has required warnings on products containing latex due to the latex allergy issue that exists. Vystar plans on petitioning the FDA to have that label removed from or modified on products manufactured with Vytex NRL, by filing a Citizen’s Petition. The Petition will be filed when we see that the benefits of filing will far outweigh the costs since such Petition is likely to require clinical test results indicating acceptable allergic reactions associated with Vytex NRL. There are no assurances that the FDA will grant that request.

Manufacturers are implementing trials of Vytex NRL in their facilities but final data areis not yet available from all these manufacturers on its viability for their particular environments.

Over the past several years, samples of Vytex NRL have been made available to over 50 natural rubber latex and latex substitute end product manufacturers, 30 of which have been in place since early 2009. Since the completion of the Vytex NRL Standard Operation Procedures (SOPs), Vytex has been produced at Revertex (Malaysia), Occidente (Guatemala), KAPVL (India) and most recently Mardec-Yala (Thailand) and MMG (Thailand). Manufacturers that have signed a ‘sampling’’sampling’ agreement with us have been provided with samples of Vytex NRL for validating its use in their manufacturing processes. To date, a number of manufacturers have completed those runs and feedback is often minimal. Although most feedback to date has been positive, there is no assurance that such feedback continueswill continue to be satisfactory.

Another risk is the validity of the customer as testing completes. Recently Vystar has completed more than three years of a specialized version of Vytex NRL only to have the end product manufacturer fail to upgrade their production line and fulfill their own contract.

As part of the Company’s learnings, we have found that in listening closely to customer challenges and needs, our technical team has been able to develop solutions. The Company has come to realize that what we offer is not just a raw material but often a technology solution to a production or product development challenge.

While many of these new formulations look promising, there is no guarantee that these technological innovations will be successfully scaled up or successfully implemented by the customer.

The following risk factors apply to our company as a whole:whole:

Because our stock price may be volatile due to factors beyond our control, you could lose all or part of your investment.

Price and volume of stock, including additional stock issuances may cause price decline and dilution.

If we do not attract and retain highly qualified employees, we may not be able to grow effectively.

Our ability to compete and grow depends in large part on the efforts and talents of our executive officers or employees. We require the key employee(s) to enter into employment agreements, but in the U.S. employees are free to leave an employer at any time without penalties. The loss of key employees or the inability to hire additional skilled employees as necessary could result in significant disruptions of our business, and the integration of replacement personnel could be time-consuming and expensive and cause us additional disruptions.

We do not expect to declare any dividends in the foreseeable future.

We do not anticipate declaring any cash dividends to holders of our common stock in the foreseeable future. Consequently, shareholders must rely on sales of their common stock after price appreciation, which may never occur, as the only way to realize any future gains on their investment. Investors seeking cash dividends should not purchase our common stock.

There is no assurance that any significant public market for our shares of common stock will develop.

While our shares of common stock trade on the OTC Bulletin Board under the symbol “VYST”, there is currently no significant public market for our common stock and there is no assurance that there will be any such significant public market for our common stock in the future.

The utilization of our tax losses could be substantially limited if we experience an ownership change as defined in the Internal Revenue Code.

Because of net operating losses we have experienced for federal income tax purposes at December 31, 2017,2018, we had federal net operating loss (“NOL”) carry-forwards of approximately $18.6$20.0 million ($17.818.4 million for 2016) pretax2017) available to offset future taxable income. Our ability to utilize NOL carry-forwards to reduce future taxable income may be limited under Section 382 of the Internal Revenue Code if certain ownership changes in our Company occur during a rolling three-year period. These ownership changes include purchases of common stock under share repurchase programs, the offering of stock by us, the purchase or sale of our stock by 5% shareholders, as defined in the Treasury regulations, or the issuance or exercise of rights to acquire our stock. If such ownership changes by 5% shareholders result in aggregate increases that exceed 50 percentage points during the three-year period, then Section 382 imposes an annual limitation on the amount of our taxable income that may be offset by our NOL carry-forwards or tax credit carry-forwards at the time of ownership change. The limitation may affect the amount of our deferred income tax asset and, depending on the limitation, a significant portion of our NOL carry-forwards or tax credit carry-forwards could expire before we are able to use them. In such an event, our business, financial condition, results of operations or cash flows could be adversely affected.

We believe we have not experienced an ownership change under Section 382 of the Internal Revenue Code as of December 31, 2017;2018; however, the amount by which our ownership may change in the future could be affected by purchases and sales of stock by 5% shareholders and new issuances of stock by us, should we choose to do so.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None

| ITEM 2. | PROPERTIES |

Although we believe that our current space is adequate for the foreseeable future, if additional office space is required, we believe that suitable space will be available at market rates.

| ITEM 3. | LEGAL PROCEEDINGS |

None

On February 19, 2019, EMA Financial, Inc. filed a lawsuit in the Southern District of New York against the Company. The lawsuit alleged various breaches of an underlying convertible promissory note and stock purchase agreement, and sought four claims for relief: (i) specific performance to enforce a stock conversion and contractual obligations; (ii) breach of contract; (iii) permanent injunction to enforce the stock conversion and contractual obligations; and (iv) legal fees and costs of the litigation. The complaint was filed with a motion seeking: (i) a preliminary injunction seeking an immediate resolution of the case through the stock conversion; (ii) a consolidation of the trial with the preliminary injunctive hearing; and (iii) summary judgment on the first and third claims for relief. As of December 31, 2018, there was no accurate assumption of liability to be accrued.

The Company filed an opposition to the motion and at oral argument the motion for injunctive relief was denied. The Court issued a decision permitting a motion for summary judgment to proceed and permitted the Company the opportunity to supplement its opposition papers together with the plaintiff who was also provided opportunity to submit reply papers. On April 5, 2019, the Company filed the opposition papers as well as a motion to dismiss the first and third causes of action in the complaint.

| ITEM 4. | MINE SAFETY DISCLOSURES |

Not applicable

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND PURCHASES OF EQUITY SECURITIES |

Market Price Information

Our common stock is traded in the United States on the Over the Counter Bulletin Board (OTCBB) under the symbol “VYST.” The following table shows the range of high and low closing prices for our common stock.

| December 31, 2016 | High | Low | ||||||||||||||

| December 31, 2017 | High | Low | ||||||||||||||

| First Quarter | $ | 0.19 | $ | 0.09 | ||||||||||||

| Second Quarter | $ | 0.18 | $ | 0.10 | ||||||||||||

| Third Quarter | $ | 0.11 | $ | 0.05 | ||||||||||||

| Fourth Quarter | $ | 0.07 | $ | 0.04 | ||||||||||||

| December 31, 2018 | ||||||||||||||||

| First Quarter | $ | 0.10 | $ | 0.06 | $ | 0.08 | $ | 0.02 | ||||||||

| Second Quarter | $ | 0.08 | $ | 0.03 | $ | 0.08 | $ | 0.04 | ||||||||

| Third Quarter | $ | 0.12 | $ | 0.02 | $ | 0.08 | $ | 0.01 | ||||||||

| Fourth Quarter | $ | 0.22 | $ | 0.10 | $ | 0.03 | $ | .0006 | ||||||||

| December 31, 2017 | ||||||||||||||||

| First Quarter | $ | 0.19 | $ | 0.09 | ||||||||||||

| Second Quarter | $ | 0.18 | $ | 0.10 | ||||||||||||

| Third Quarter | $ | 0.11 | $ | 0.05 | ||||||||||||

| Fourth Quarter | $ | 0.07 | $ | 0.04 | ||||||||||||

Holders

As of December 31, 2017,2018, there were 238437 holders of record of our common stock.

Dividends

We have never paid or declared any cash dividends on our common stock and we do not intend to pay or declare dividends on our common stock in the near future. We presently expect to retain any future earnings to fund continuing development and growth of our business. Our payment of dividends is subject to the discretion of our board of directors and will depend on earnings, financial condition, capital requirements and other relevant factors.

Issuer Purchases of Equity Securities

We did not make any repurchases of our equity securities during the 20172018 fiscal year.

Securities Authorized for Issuance Under Equity Compensation Plans

Information concerning our equity compensation plans is set forth in Item 12 of Part III of this Annual Report on Form 10-K.

Recent Sales of Unregistered Securities

Common Stock and Warrant Grants

From January 1, 20172018 through December 31, 2017,2018, we issued 7,244,2251,928,571 shares of our common stock valued at $490,000$90,000 for services rendered to the Company in 2017 and 9,503,9932018, 54,999,997 shares were issued in investments andfor cash for $165,000, 8,333,333 shares were issued to convert payables valued at $44,167, 721,408 shares were issued upon exercise of cashless conversion of options and warrants valued at $384,500.$34,806, and 55,687,500 shares were to be issued as part of a private placement valued at $2,931,019. During the period, 1,109,406203,267,791 shares of common stock valued at $55,359$1,444,320 were issued upon the conversion of convertible notes.notes and accrued interest.

From January 1, 20172018 through December 31, 2017,2018, we issued 1,240,250411,875 warrants to purchase shares of common stock for services rendered to the Company per the following:

| Warrants | Exercise Price per Share | ||||

| $ | |||||

| $ | |||||

Stock Option Grants

From January 1, 20172018 through December 31, 2017,2018, we issued 1,500,00021,800,000 options to purchase common stock to Board members and employeesconsultants valued at $1,161,132.

Proceeds from loans and shareholder, convertible and contingently convertible notes payable

On November 2, 2012, the Company executed a $1,500,000 unsecured line of credit agreement with CMA Investments, LLC, a related party and a Georgia limited liability company (the “CMA Note”). Three of the directors of the Company (“CMA directors”) were initially the members of CMA. Pursuant to the terms of the CMA Note, interest is computed at LIBOR plus 5.25% (8.22% at December 31, 2018) on amounts drawn and fees. The weighted average interest rate in effect on the borrowings for the year ended December 31, 2018 was 7.99%. There are no available borrowings under the CMA note at December 31, 2018. During the year ended December 31, 2018, the Company recorded approximately $123,000 of interest expense.

During the year ended December 31, 2018 certain investors have guaranteed $100,000 each with Fidelity Bank to establish a $500,000 revolving line of credit. At the present time, the Company is paying interest only at a rate of 4.5% per annum, with a balloon payment of $500,000 due in 2033.

From January 1, 2018 to February 9, 2018, the following:Company issued contingently convertible promissory notes (the “Notes”) for contract work performed by other entities in lieu of compensation and expense reimbursement in the amount of $195,635. The Notes are (i) unsecured, (ii) bear interest at an annual rate of five percent (5%) per annum from date of issuance, and (iii) are convertible at the Company’s option post April 19, 2018. The Notes mature one year from issuance but may be extended one (1) additional year by the Company. If converted, the Notes plus accrued interest are convertible into shares of the Company’s common stock at the prior twenty (20) day average closing price with a 50% discount.

From January 1, 2018 and through the date of these financial statements, the Company has issued certain convertible and contingently convertible promissory notes in varying amounts, in the aggregate of $710,000. The face amount of the notes represents the amount due at maturity along with the accrued interest, at which time that amount may be converted into shares of the Company stock based on the lowest 2 day closing price for the trailing 20 days prior to conversion and carrying a 35% discount. The contingently convertible notes provide for interest to accrue at an interest rate equal to 12% per annum or the maximum rate permitted under applicable law after the occurrence of any event of default as provided in the notes. At any time after 180 days from the issue date, the holder, at its option, may convert the outstanding principal balance and accrued interest into shares of common stock of the Company. The initial conversion price for the principal and interest in connection with voluntary conversions by a holder of the convertible notes ranges from $0.05 to $0.10 per share, subject to adjustment as provided therein. If the total outstanding balance of the contingent convertible notes were convertible as of December 31, 2018, they would have been convertible into approximately 343 million shares of the Company’s common stock. Based on the variable conversion price, the Company recorded initial derivative liabilities of $465,905, debt discount of $430,579 and interest expense related to the excess fair value of $35,326 upon the date such notes became convertible.

In connection with the issuance of the convertible notes, the Company issued warrants to purchase 411,875 shares of the Company’s common stock. The exercise term of the warrants ranges from issuance to any time on or after the six (6) month anniversary or prior to the maturity of the related note. The exercise price of the warrants is $0.40 per share of the Company’s common stock, as may be adjusted from time to time pursuant to the antidilution provisions of the related warrant. Pursuant to ASU 2017-11, such antidilution features do not subject the Company to derivative accounting pursuant to ASC 815.

During the year ended December 31, 2018, the Company entered into a financing agreement with Peak One Opportunity Fund, L.P. to receive $435,000 of original issue discount notes in three tranches as follows:

| 1. |

| 2. | September 14, 2018: $150,000 principal $135,000 net. |

| November 13, 2018: a final $200,000 principal, $180,000 net. |

Peak One Opportunity Fund is entitled to convert the note into common stock at a price equal to 65% of the lowest traded price for the twenty trading days immediately preceding the date of the date of conversion. The Company has the option to redeem the note at varying prices based upon the redemption date.

13

During the year ended December 31, 2018, the Company entered into a financing agreement with Crown Bridge Partners, LLC to receive $100,000 of original issue discount notes in two tranches as follows:

| 1. | August 6, 2018: principal $50,000 bearing interest at 8%, discounted by 10%, and $2,000 for legal fees, for a net of $43,000 due one year from the funding date; |

| 2. | The remaining tranche may be funded at the holder’s discretion. |

Crown Bridge Partners is entitled to convert the note into common stock at a price equal to 65% of the average of the two lowest traded prices for the twenty-five trading days immediately preceding the date of the date of conversion.

As of December 31, 2018, only the first tranche had been received and none of it has been converted to stock.

In addition, the following notes are convertible after six months from the issue date:

| Face | Interest | Net Cash | Amount | |||||||||||||||||

| Issue Date and Name | Amount | Rate | Maturity | Proceeds | Converted | |||||||||||||||

| Jan 29, 2018 EMA | $ | 80,000 | 12 | % | Jan 29, 2019 | $ | 72,300 | $ | 79,348 | |||||||||||

| Feb 14, 2018 Auctus | 80,000 | 12 | % | Nov 14, 2018 | 72,500 | 70,625 | ||||||||||||||

| Feb 13, 2018 FirstFire Global | 76,500 | 5 | % | Nov 13, 2018 | 72,500 | 81,500 | ||||||||||||||

| May 2, 2018 Power Up | 83,000 | 12 | % | May 23, 2019 | 80,000 | 83,000 | ||||||||||||||

| Jun 20, 2018 Power Up | 68,000 | 12 | % | Jun 25, 2019 | 65,000 | — | ||||||||||||||

During the year ended December 31, 2018 approximately $418,117 of the convertible notes and approximately $28,000 of accrued interest were exchanged for approximately 203,267,791 shares of common stock. In addition, approximately $75,000 of the notes have been subsequently converted to approximately 24,288,000 of common stock and 15,000,000 shares of common stock for CMA were still being held in escrow as of December 31, 2018.

Application of Securities Laws and Other Matters

No underwriters were involved in the foregoing sales of securities. The securities described above were issued to investors in reliance upon the exemption from the registration requirements of the Securities Act, as set forth in Section 4(2)4 (2) under the Securities Act and Regulation D promulgated thereunder, as applicable, relative to sales by an issuer not involving any public offering, to the extent an exemption from such registration was required.

The issuance of stock options as described above were issued pursuant to written compensatory plans or arrangements with our employees, directors and consultants, in reliance on the exemption provided by Rule 701 promulgated under the Securities Act. All recipients either received adequate information about us or had access, through employment or other relationships, to such information.

All of the foregoing securities are deemed restricted securities for purposes of the Securities Act. All certificates representing the issued shares of common stock, warrants and options described above included appropriate legends setting forth that the securities had not been registered and the applicable restrictions on transfer.

| ITEM 6. | SELECTED FINANCIAL DATA |

As a smaller reporting company, we are not required to provide the information required by this Item pursuant to 301(c) of Regulation S-K.

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

This analysis of our results of operations should be read in conjunction with the accompanying financial statements, including notes thereto, contained in Item 8 of this Report. This Report contains certain forward-looking statements within the meaning of Section 27A of the Securities Act, and Section 21E of the Exchange Act. Statements that are predictive in nature and that depend upon or refer to future events or conditions are forward-looking statements. Although we believe that these statements are based upon reasonable expectations, we can give no assurance that projections will be achieved. Please refer to the discussion of forward-looking statements included in Part I of this Report.

Overview

Vystar LLC, the predecessor to the Company, was formed February 2, 2000, as a Georgia limited liability company by Travis W. Honeycutt. Operations under the LLC entity were focused substantially on the research, development and testing of the Vytex® Natural Rubber Latex (“NRL”) process, as well as attaining intellectual property rights. In 2003, the Company reorganized as Vystar Corporation, a Georgia corporation, at which time all assets and liabilities of the limited liability company became assets and liabilities of Vystar Corporation, including all intellectual property rights, patents and trademarks.

We are the creator and exclusive owner of the innovative technology to produce Vytex NRL. This technology reduces antigenic protein in natural rubber latex products to virtually undetectable levels in both liquid NRL and finished latex products. The process also removes many of the naturally occurring non-rubber particles superfluous to end product function, resulting in a cleaner latex base material. We have introduced Vytex NRL, our “ultra-low protein” natural rubber latex, throughout the worldwide marketplace that uses NRL or latex substitutes as a component of manufactured products. Natural rubber latex is used in an extensive range of products including balloons, textiles, footwear and clothing (threads), adhesives, foams, furniture, carpet, paints, coatings, protective equipment, sporting equipment, and especially health care products such as condoms, surgical and exam gloves. We produce Vytex through licensing agreements and have introduced Vytex NRL into the supply channels with aggressive, targeted marketing campaigns directed to the end users.

We transitioned from a development stage company to the operating stage during the last quarter of 2009. During the period of 2010 to 2015, our financial condition and results of operations have experienced substantial fluctuations as we provided introductory pricing in 2010 and then began to switch to a licensing rather than a toll model in 2011. Our licensing model will continue in 20182019 for the raw material business and we will continue our focus in 2019 onward on the licensing contracts associated with the foam and furniture offerings. Accordingly, the financial condition and results of operations reflected in our historical financial statements are not expected to be indicative of our future financial condition and results of operations.

We believe that the key for increased Vytex NRL product acceptance is to focus on companies seeking solutions to production challenges or ways to differentiate their product offering. Vystar’s technical team has been successful in developing customized formulations to meet specific manufacturer needs. Some of these formulations will become new line extensions. Vystar is becoming less of a raw material provider and more of a technology innovator through its technical consultation and formulation activities.

In addition to this technology focus, we are determined to have the “made with Vytex” claim added to products made using various forms of Vytex NRL. To help drive this effort we’re focusing on products that benefit from Vytex NRL low non-rubber features. As part of this effort, we are working with a licensee to launch a line of foam core products used in various bedding products including pillows, mattresses and mattress toppers.

In January 2015 Vystar announced that it had entered into an exclusive agreement with NHS to distribute mattresses, mattress toppers and pillows made with its multi-patented Vytex NRL raw material. NHS is a distribution company led by SteveSteven Rotman of Rotman’sRotmans Furniture and as of December 18, 2017 is the CEO of Vystar and focuses on innovative, sustainably sourced, eco-friendly material and technologies for use in furnishings and other markets. Our Vytex NRL fits the needs of this unique new distributor which has already attracted such firms as mattress manufacturer Gold Bond that was formed in 1899 to manufacture and then distribute mattresses, toppers and pillows along with a plan to reach specific segments of the United States by targeting other manufacturers. Vystar has focused on these segments since 2015 and will continue into 20182019 as we display at furniture and mattress conventions and attend and sell at sleep products meetings such as ISPA 2016 (International Sleep Products Association) held in Orlando, FL and ISPA 2017 in Tampa, FL and attendingattended ISPA 2018 in Charlotte, NC. Vystar will also continue to develop specialty versions of Vytex NRL after presenting to the International Latex Conference in Akron OH in July 2016 and 2017 and sending out samples for lab trials. Vystar is currently producing Vytex thread samples for an entry into the thread marketplace. In September 2016, the Vystar Board of Directors voted to end the January 2015 agreement with NHS and replace it with a global exclusive for foam manufactured with Vytex and sold into the home furnishings industry. This change reflects the global nature of the mattress, topper and pillow businesses.

In April of 2018 Vystar acquired the assets of NHS Holdings, LLC (NHS) executing on the first part of the company’s vision to move into direct product offerings made from Vytex® latex. NHS was the exclusive U.S. distributor of Vystar’s Vytex® natural rubber latex foam to manufacturers for use in over 200 home furnishings products, including mattresses, toppers, pillows and upholstery, sold through multiple channels. This acquisition provides Vystar with roll packing and cutting equipment to support our bedding manufacturing partners, while lowering the cost of Vytex to the manufacturer by eliminating the middleman.

Now unified under the Vytex brand, we anticipate developing additional product offerings and solidifying partnerships with multiple major manufacturing partners throughout the home furnishings industry. We anticipate our new offerings will include cushions and padding for use in seating and other products which we believe will achieve higher margins.

In May of 2018 Vystar acquired substantially all of the assets of UV Flu Technologies, Inc., formerly traded on the OTC under the ticker UVFT, whose patented ViraTech™ UV light air purification technology destroys greater than 99% of airborne bacteria, viruses and other microorganisms and virtually eliminates concentrations of odors and volatile organic compounds (VOCs).

As part of Vystar’s mission to offer eco-friendly, sustainable materials and products that create a better environment for consumers and workers throughout the product lifecycle, UV Flu Technologies is an excellent counterpart to our Vytex materials and Vytex bedding products. Vystar products will help create a perfect natural sleep environment starting with Vytex bedding made from the purest latex in the world and UV Flu’s RxAir™ air purifier ensuring every breath is free of harmful pathogens, VOCs and odors.”

UV Flu products use 48 inches of high-intensity germicidal UV lamps that destroy bacteria, viruses and other germs instead of just trapping them, setting it apart from ordinary air filtration units. RxAir is one of the few UV air purifiers that have been proven in independent EPA- and FDA-certified testing laboratories to destroy on the first pass 99.6% of harmful airborne viruses and bacteria. In addition to inactivating airborne viruses that cause influenza (flu) and colds, RxAir’s device disarms the airborne pathogens that cause MRSA (staph), strep (whooping cough), tuberculosis (TB), measles, pneumonia and a myriad of other antibiotic-resistant and viral infections. (see news video with RX3000 in use)

UV Flu’s product line includes:

| ● | RXair™ Residential Filterless Air Purifier | |

| ● | UV400 ™ FDA cleared Class II Filterless Air Purifier | |

| ● | RX3000™ Commercial FDA cleared Class II Air Purifier (news video with RX3000) |

Vystar acquired all UV Flu intellectual property and multiple patents, product lines, tooling, FDA clearances, research data, websites and other assets related to the business for the purchase price of $975,000 or 27,918,000 shares of Vystar restricted common stock which may not be assigned or sold by UV Flu for 12 months.

Manufacturing, Distribution and Sales

Vystar will continue production of UV Flu product lines with BOI, a world-class manufacturer. Vystar plans to sell RxAir residential and commercial units via Distributors, online and through retail channels.

Vystar is assembling the distribution network to relaunch sales of UV400 and Rx3000 units to the healthcare and medical markets, which UV Flu had ceased due to sales force, distribution and cash flow constraints. Once production and sales are firmly re-established, Vystar expects that the air purification products will produce margins of approximately 75%.

UV Flu’s products have world class engineering, are made to the highest quality standards and are extremely effective in settings ranging from homes to offices, healthcare facilities, salons, restaurants and nursing homes.

About RxAir

RxAir promotes a healthy lifestyle through the use of its innovative, patented ViraTech air purification technology, thereby improving the quality of life of each and every customer. Independently tested by EPA- and FDA-certified laboratories, the RxAir has been proven to destroy greater than 99% of bacteria and viruses and reduce concentrations of odors and VOCs. The RxAir uses high-intensity germicidal UV lamps that destroy bacteria and viruses instead of just trapping them, setting it apart from ordinary air filtration units. RxAir® and ViraTech® are registered trademarks of Vystar Corp. For more information, visit http://www.RxAir.com

Critical Accounting Policies and Estimates