UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

|

| |

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 20142016

or

|

| |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period From to

Commission File Number: 001-33662

Forestar Group Inc.

(Exact Name of Registrant as Specified in Its Charter)

|

| | |

| Delaware | | 26-1336998 |

(State or Other Jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification No.) |

6300 Bee Cave Road

Building Two, Suite 500

Austin, Texas 78746-5149

(Address of Principal Executive Offices, including Zip Code)

Registrant’s telephone number, including area code: (512) 433-5200

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of Each Class | | Name of Each Exchange On Which Registered |

Common Stock, par value $1.00 per share Preferred Share Purchase Rights

| | New York Stock Exchange |

| Preferred Stock Purchase Rights | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

| | | | | | |

Large accelerated filer o | | Accelerated filer þ | | Non-accelerated filer o | | Smaller reporting company o |

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The aggregate market value of the Common Stock held by non-affiliates of the registrant, based on the closing sales price of the Common Stock on the New York Stock Exchange on June 30, 2014,2016, was approximately $457$210 million. For purposes of this computation, all officers, directors, and ten percent beneficial owners of the registrant (as indicated in Item 12) are deemed to be affiliates. Such determination should not be deemed an admission that such directors, officers, or ten percent beneficial owners are, in fact, affiliates of the registrant.

As of March 2, 2015,February 27, 2017, there were 33,618,52641,694,432 shares of Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Selected portions of the Company’s definitive proxy statement for the 20152017 annual meeting of stockholders are incorporated by reference into Part III of this Form 10-K.

TABLE OF CONTENTS

|

| | |

| | | Page |

| | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | | |

| | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| | | |

| | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| | | |

| | |

| Item 15. | | |

| | | |

| | |

PART I

Overview

Forestar Group Inc. is a residential and mixed-use real estate and oil and gasdevelopment company. WeIn our core community development business we own directly or through ventures 113,000interests in 50 residential and mixed-use projects comprised of 4,600 acres of real estate located in ten10 states and 13 markets, including about 102,000 acres with timber, primarily14 markets. In addition, we own interests in Georgia. We alsovarious other assets that have 960,000been identified as non-core that the company is divesting opportunistically over time. At year-end 2016, our remaining non-core assets principally include approximately 523,000 net acres of oil and gasowned mineral interests, consisting of fee ownership and leasehold interestsassets principally located in 16 statesTexas, Louisiana, Georgia and Alabama, 19,000 acres of timberland and undeveloped land (including mitigation banking), four multifamily assets and approximately 20,000 acres of groundwater leases in the continental U.S.central Texas. On February 17, 2017, we sold our owned mineral assets for $85.6 million. In 2014,2016, we had revenues of $307$197.3 million and net income of $17$58.6 million. Unless the context otherwise requires, references to “we,” “us,” “our” and “Forestar” mean Forestar Group Inc. and its consolidated subsidiaries. Unless otherwise indicated, information is presented as of December 31, 2014,2016, and references to acreage owned include approximate acres owned by us and ventures regardless of our ownership interest in a venture.

Key Initiatives

Reducing costs across our entire organization;

Reviewing entire portfolio of assets (complete non-core asset sales); and

Reviewing capital structure (allocate capital to maximize shareholder value).

2016 Transformation Highlights (including ventures):

Core Community Development:

Sold 1,940 residential lots for approximately $68,200 per lot

Approximately 2,100 lots under option contracts with builders at year-end 2016

Sold 298 commercial acres for approximately $44,600 per acre (principally non-core projects)

Sold 1,792 residential tract acres for approximately $8,700 per acre (principally non-core projects)

Cost Reductions:

Reduced SG&A, including discontinued operations, by over 28% compared with full year 2015

Divest Non-core Assets:

Executed non-core asset sales generating $481.9 million in pre-tax net proceeds:

|

| | | |

| Assets | Pre-Tax Net Proceeds |

| | (In millions) |

| Timberland and Undeveloped Land (bulk and retail, ~73,000 acres) | $ | 138.0 |

|

| Radisson Hotel & Suites | 128.8 |

|

| Multifamily properties (five properties) | 118.7 |

|

| Oil and Gas Working Interests | 77.1 |

|

| Non-core Community Development Projects (five projects) | 19.3 |

|

| | $ | 481.9 |

|

Reduced outstanding debt by $277.8 million in 2016 and $323.3 million since third quarter-end 2015

Business Segments

We manage our operations through three business segments:

Real estate,

Oil and gas,Mineral resources, and

Other natural resources.Other.

A summary of significant business segment assets at year-end 2014 follows:

Our real estate segment provided approximately 70%96% percent of our 20142016 consolidated revenues. We secure entitlementsare focused on maximizing real estate value through the entitlement and develop infrastructure, primarily for single-familydevelopment of strategically located residential and mixed-use communities. We own 92,000 acressecure entitlements by delivering thoughtful plans and balanced solutions that meet the needs of communities where we operate. Residential development activities target lot sales to local, regional and national home builders who build quality products and have strong and effective marketing and sales programs. The lots we develop in a broad area around Atlanta, Georgia, with the balance located primarilymajority of our communities are for mid-priced homes, predominantly in Texas.the first and second move up categories. We invest in projects principally in our strategic growth corridors, regions across the southern half of the United States that possess key demographic and growth characteristics that we believe make them attractive for long-term real estate investment. We also developA majority of our active real estate projects are developed on land we or our ventures acquired in the open market. In 2016, we announced that multifamily is a non-core business and own directly or through ventures,are opportunistically divesting our multifamily portfolio and will no longer allocate capital to new communities in this business. At year-end 2016, a multifamily site in Austin was classified as income producing properties, principally in our target markets.assets held for sale.

Our oil and gasmineral resources segment provided 27%three percent of our 20142016 consolidated revenues. We promote the exploration, development and production of oil and gas on our 960,000 owned and leasehold mineral interests. This includes 590,000These interests include 523,000 owned mineral acres and 370,000 net mineral acres leased from others.which we determined were non-core in 2016 and we are opportunistically divesting these assets over time. At year-end 2016, we classified our non-core mineral assets as held for sale. On February 17, 2017, we sold these assets for $85.6 million.

Our other natural resources segment, all of which is non-core, provided 3%one percent of our 20142016 consolidated revenues. We sell wood fiber from our land, primarily in Georgia, and lease land for recreational uses. We have about 102,000 real estate19,000 acres with timber we own directly or through ventures.of non-core timberland and undeveloped land that was classified as assets held for sale at year-end 2016. In addition, we have non-core water interests in about 1.5 million acres, including a 45 percent nonparticipating royalty interest in groundwater produced or withdrawn for commercial purposes or sold from approximately 1.4 million acres in Texas, Louisiana, Georgia and Alabama, and about 20,000 acres of groundwater leases in central Texas.

Our real estate origins date back to the 1955 incorporation of Lumbermen’s Investment Corporation, which in 2006 changed its name to Forestar (USA) Real Estate Group Inc. We have decades long legacy of residential and commercial real estate development operations, primarily in Texas. Our oil and gas origins date back to the mid-1940s when we started leasing our oil and gas mineral interests to third-party exploration and production companies. In 2007, Temple-Inland distributed all of the issued and outstanding shares of our common stock to its stockholders, which we will refer toTexas that were classified as the “spin-off”.assets held for sale at year-end 2016.

Our results of operations, including information regarding our business segments, are discussed in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, and in Item 8, Financial Statements and Supplementary Data.

Strategy

Our strategy is:

Recognizing and responsibly delivering the greatest value from every acre; and

Growing through strategic and disciplined investments.

We are focused on delivering the greatest real estate value from every acre through the entitlement and development of strategically-located residential and mixed-use communities. We secure entitlements by delivering thoughtful plans and balanced solutions that meet the needs of the communities where we operate. Moving land through the entitlement and development process creates significant real estate value. Residential development activities target lot sales to local, regional and national home builders who build quality products and have strong and effective marketing and sales programs. The lots we deliver in the majority of our communities are for mid-priced homes, predominantly in the first and second move-up categories. We also actively market and sell undeveloped land through our retail sales program. We develop multifamily commercial tracts ourselves as a merchant builder or we may venture with partners for the construction, operation, and sale of income producing properties.

We also seek to maximize value from our owned oil and gas mineral interests through promoting exploration, development and production activities by increasing the acreage leased, lease rates, royalty interests, negotiating additional interests in production and by entering into seismic exploration agreements and joint ventures. In addition, we lease mineral interests for oil and gas exploration and production and participate in working interests or may drill as an operator on both our owned and leased mineral interests.

We realize value from our undeveloped land by selling fiber and by managing it for future real estate development and conservation uses. We also generate cash flow and earnings through recreational leases. We are focused on creating value from our water interests by securing reservation and production supply agreements with various municipalities and water providers in our target markets.

We are committed to disciplined investment in our business. A majority of our real estate projects were acquired in the open market, with the remainder coming from entitlement efforts associated with our low basis lands principally located in and around Atlanta, Georgia. Our mineral interest investments are typically in conventional and unconventional oil and liquid-rich formations.

Our portfolio of assets in combination with our strategy, management expertise, stewardship and reinvestment in our business, position Forestar to maximize and grow long-term value for shareholders.

2014 Strategic Initiatives

On February 13, 2014, we announced Growing FORward, new strategic initiatives designed to further enhance shareholder value by:

Growing segment earnings through strategic and disciplined investments,

Increasing returns, and

Repositioning non-core assets.

On December 8, 2014, we announced that our Board of Directors, working together with our management team and financial advisor, is exploring strategic alternatives to enhance shareholder value. This analysis includes a review of alternatives with respect to our oil and gas business. There is no assurance that exploration of strategic alternatives will result in any transaction being pursued or consummated.

2014 Significant Highlights (including ventures)

Real Estate

Sold 2,343 developed residential lots, with the highest average annual gross profit per lot reported since 2006

Sold 22,137 acres of undeveloped land for almost $2,200 per acre

Sold 32 commercial acres for over $258,600 per acre

Sold 944 acres of residential tracts for over $8,500 per acre

Exchanged over 10,000 acres of timber leases into ownership of 5,400 acres of undeveloped land, generating a $10.5 million gain

Acquired partner's interest in Eleven multifamily venture for $21.5 million, generating a gain of $7.6 million

Received over $60 million from Cibolo Canyons Special Improvement District, generating a gain of $6.6 million

Oil and Gas

Increased proved reserves almost 20% to 10.1 MMBOE, with oil and liquids accounting for 76% of total reserves

Increased working interest oil and liquids production nearly 53% compared with 2013, principally due to working investments in the Bakken/Three Forks and Lansing-Kansas City formations

Production volumes related to royalty interests declined over 20% to approximately 310,300 BOE in 2014 which, in combination with lower lease bonus and delay rental revenues and higher operating costs, negatively impacted segment earnings by $6.1 million

Incurred non-cash impairment charges of $32.6 million associated with unproved leasehold interests and proved properties principally due to the significant decline in oil prices

Sold oil and gas properties primarily in Oklahoma and North Dakota for $17.7 million, generating gains of $8.5 million

Leased over 3,900 net mineral acres to third parties in Texas and Louisiana for over $1.2 million

Other Natural Resources

Generated $3.4 million gain related to termination of a timber lease in connection with the sale of the remaining 2,700 acres from the Ironstob venture

Sold nearly 330,000 tons of fiber for $14.93 per ton

Generated $1.1 million of revenue related to groundwater reservation agreement and almost $0.2 million gain associated with the sale of water rights related to a real estate community near Denver

Real Estate

In our real estate segment, we conduct a wide array of project planning and management activities related to the acquisition, entitlement, development and sale of real estate, primarily residential and mixed-use communities, which we refer to as community development. We own and manage our projects either directly or through ventures, which we use to achieve a variety of business objectives, including more effective capital deployment, risk management, and leveraging a partner’s local market contacts and expertise.

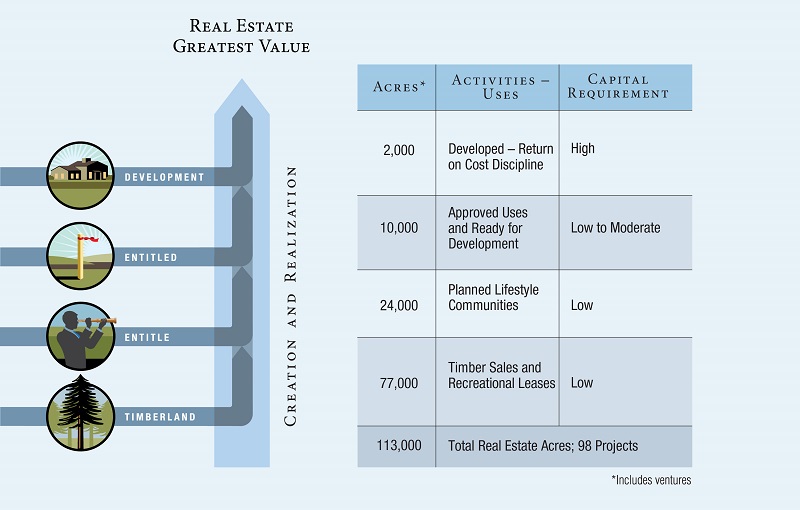

We have real estate in ten states and 13 markets encompassing 113,000 acres, including 92,000 acres located in a broad area around Atlanta, Georgia, with the balance located principally in Texas. Our development projects are principally located in the major markets of Texas.

Our strategy for creating value in our real estate segment is to move acres up the value chain by moving land located in growth corridors but not yet entitled, through the entitlement process, and into development. The chart below depicts our real estate value chain at year-end 2014:

We have approximately 77,000 undeveloped acres located in the path of population growth. As markets grow and mature, we intend to secure the necessary entitlements, the timing for which varies depending upon the size, location, use and complexity of a project, focusing first on those tracts that are more desirable for near-term development. We have 11two real estate projects representing 24,000approximately 730 acres currently in the entitlement process in California, which includes obtaining zoning and access to water, sewer and roads. In fourth quarter 2016, we classified 3,700 acres in Texas previously in the entitlement process as timberland and undeveloped land as it was determined it was unlikely this project would be entitled and developed in the future, and at year-end 2016 it was classified as assets held for sale. Additional entitlements, such as flexible land use provisions, annexation, and the creation of local financing districts generate additional value for our business and may provide us the right to reimbursement of major infrastructure costs. We have 75 entitled, developed or under development projects in eight states and 13 markets encompassing 12,000 entitled, developed and under development acres, planned for residential and commercial uses. We use return criteria, which include return on cost, internal rate of return, and cash multiples, and margin on sales when determining whether to invest initially or make additional investment in a project. When investment in development meets our return criteria, we will initiate the development process with subsequent sale of lots to home builders or for commercial tracts, internal development, sale to or venture with third parties.

We have 50 entitled, developed or under development projects in 10 states and 14 markets encompassing 4,600 acres planned for residential and commercial uses. We may sell land at any point within the value chain when additional time required for entitlement or investment in development will not meet our return criteria. In 2014,2016, we sold over 22,000nearly 73,000 acres of timberland and undeveloped land at an average price of almost $2,200$1,925 per acre.acre, of which 58,000 acres were bulk timberland and undeveloped land sales and 15,000 acres were retail land sales.

A summary of our real estate projects in the entitlement process(a) at year-end 20142016 follows:

|

| | | | | | | |

| Project | | County | | Market | | Project Acres (b) |

| California | | | | | | |

| Hidden Creek Estates | | Los Angeles | | Los Angeles | | 700 |

|

| Terrace at Hidden Hills | | Los Angeles | | 30 |

|

GeorgiaLos Angeles | | | | |

Ball Ground | | Cherokee | | 500 |

|

Crossing | | Coweta | | 230 |

|

Fincher Road | | Cherokee | | 3,890 |

|

Garland Mountain | | Cherokee/Bartow | | 350 |

|

Martin’s Bridge | | Banks | | 970 |

|

Mill Creek | | Coweta | | 770 |

|

Wolf Creek | | Carroll/Douglas | | 12,230 |

|

Yellow Creek | | Cherokee | | 1,060 |

|

Texas | | | | |

Lake Houston | | Harris/Liberty | | 3,70030 |

|

| Total | | | | 24,430 | | 730 |

|

_____________________

| |

(a) | A project is deemed to be in the entitlement process when customary steps necessary for the preparation of an application for governmental land-use approvals, likesuch as conducting pre-application meetings or similar discussions with governmental officials, have commenced, or an application has been filed. Projects listed may have significant steps remaining, and there is no assurance that entitlements ultimately will be received. |

| |

(b) | Project acres, which are the total for the project regardless of our ownership interest, are approximate. The actual number of acres entitled may vary. |

A summary of our non-core timberland and undeveloped land classified as assets held for sale at year-end 2016 follows:

|

| | | |

| | Acres |

| Timberland | | |

| Georgia | | 11,100 |

|

Texas (a) | | 7,900 |

|

| Total | | 19,000 |

|

_____________________

| |

(a) | Includes 3,700 acres in Houston that was previously in the entitlement process. |

Products

The majority of our projects are single-family residential and mixed-use communities. In some cases, commercial land uses within a project enhance the desirability of the community by providing convenient locations for resident support services. We sometimes undertake projects consisting exclusively of commercial tracts and, on occasion, we invest in a venture to develop a single commercial project.

We develop lots for single-family homes and develop multifamily properties on our commercial tracts or other developed sites we may purchase. We sell residential lots primarily to local, regional and national home builders. We have 10,0004,600 acres, principally in the major markets of Texas, comprised of land planned for over 18,000approximately 10,200 residential lots.lots and units. We generally focus our lot sales on the first and second move-up primary housing categories. First and second move-up segments are homes priced above entry-level products yet below the high-end and custom home segments. We also develop and own directly, or through ventures, multifamily communities as income producing properties, primarily in our target markets. Once these multifamily communities reach stabilization, we generally expect to market the properties for sale. We also actively market and sell undeveloped land through our retail sales program.

Commercial tracts are developed internally or ventured with commercial developers that specialize in the construction and operation of income producing properties, such as apartments, retail centers, or office buildings. We also sell land designated for commercial use to regional and local commercial developers. We have 2,000about 770 acres of entitled land designated for commercial use.

Cibolo Canyons is a significant mixed-use project in the San Antonio market area. Cibolo Canyons includes 2,100 acres planned to include 1,7691,791 residential lots, of which 9111,142 have been sold as of year-end 20142016 at an average price of $71,000$75,000 per lot. The residential component includes not only traditional single-family homes but also an active adult section, and is planned to include condominiums. The remaining 58 acres of commercial component includes over 150 acresis designated principally designated for multifamily and retail uses, of which 130 acres have been sold as of year-end 2014.uses. Located at Cibolo Canyons is the JW Marriott® San Antonio Hill Country Resort & Spa (Resort), a 1,002 room destination resort and two PGA Tour® Tournament Players Club® (TPC) golf courses designed by Pete Dye and Greg Norman. We have the right to receive from a legislatively createdthe Cibolo Canyons special improvement districtSpecial Improvement District (CCSID) nine percent of hotel occupancy revenues and 1.5 percent of other resort sales revenues collected as taxes by CCSID through 2034 and reimbursement of certain infrastructure costs related to the mixed-use development. The amount we receive is net of annual ad valorem tax reimbursements by CCSID to the third-party owners of the resort through 2020. In addition, these payments will be net of debt service on bonds issued in 2014 by CCSID as discussed below which are collateralized by hotel occupancy tax (HOT) and other resort sales tax through 2034.

In October 2014, we received $46,500,000$50,550,000 from CCSID under 2007 economic development agreements (EDA) in connection with development of the JW Marriott® Hill Country Resort & Spa. CCSID funded paymentprincipally related to us from its issuance

of $48,900,000 Hotel Occupancy Tax (HOT) and Sales and Use Tax Revenue Bonds.Bonds, resulting in recovery of our full Resort investment. These bonds are obligations solely of CCSID and are payable from HOT and sales and use taxes levied by CCSID. To facilitate the issuance of the bonds, we provided a $6,846,000 letter of credit to the bond trustee as security for certain debt service fund obligations in the event CCSID tax collections are not sufficient to support payment of the bonds in accordance with their terms. The letter of credit must be maintained until the earlier of redemption of the bonds or scheduled bond maturity in 2034. We also entered into an agreement with San Antonio Real Estate (SARE),the owner of the Resort to assign SARE’sits senior rights under the EDA to us in exchange for consideration provided by us, including a surety bond to be drawn if CCSID tax collections are not sufficient to support ad valorem tax rebates payable to SARE.payable. The surety bond has a balance of $9,010,000 at year-end 2014. The surety bond will decreasedecreases as CCSID makes annual ad valorem tax rebate payments, to SARE, which obligation is scheduled to be retired in full by 2020.

A summary of activity within our projects in the development process, which includes entitled,(a), developed and under development single-family and mixed-use projects, at year-end 20142016 follows:

| | | | | | | | | Residential Lots(c) | | Commercial Acres(d) | | | | | | Residential Lots/Units | | Commercial Acres |

| Project | | County | | Interest Owned(b) | | Lots Sold Since Inception | | Lots Remaining | | Acres Sold Since Inception | | Acres Remaining(e) | | County | | Interest

Owned (a) | | Lots/Units Sold

Since

Inception | | Lots/Units

Remaining | | Acres Sold

Since

Inception | | Acres

Remaining |

| Projects we own | | | | | | | | | | | |

| California | | | | | | | | | | | |

| San Joaquin River | | Contra Costa/Sacramento | | 100 | % | | — |

| | — |

| | — |

| | 288 |

| |

| Colorado | | | | | | | | | | | |

| Buffalo Highlands | | Weld | | 100 | % | | — |

| | 164 |

| | — |

| | — |

| |

| Johnstown Farms | | Weld | | 100 | % | | 281 |

| | 313 |

| | 2 |

| | 3 |

| |

| Pinery West | | Douglas | | 100 | % | | 45 |

| | 41 |

| | 20 |

| | 106 |

| |

| Stonebraker | | Weld | | 100 | % | | — |

| | 603 |

| | — |

| | — |

| |

| Tennessee | | | | | | | | | | | |

| Beckwith Crossing | | Wilson | | 100 | % | | — |

| | 99 |

| | — |

| | — |

| |

| Morgan Farms | | Williamson | | 100 | % | | 61 |

| | 112 |

| | — |

| | — |

| |

| Weatherford Estates | | Williamson | | 100 | % | | — |

| | 17 |

| | — |

| | — |

| |

| Projects with lots/units in inventory, under development or future planned development, projects with remaining commercial acres only and projects sold out in 2016 | | Projects with lots/units in inventory, under development or future planned development, projects with remaining commercial acres only and projects sold out in 2016 |

| Texas | | | | | | | | | | | | | | | | | | | | |

| Austin | | | | | | | | | | | |

| Arrowhead Ranch | | Hays | | 100 | % | | — |

| | 381 |

| | — |

| | 11 |

| | Hays | | 100 | % | | 6 |

| | 378 |

| | — |

| | 19 |

|

| The Colony | | | Bastrop | | 100 | % | | 566 |

| | — |

| | 27 |

| | — |

|

| Double Horn Creek | | | Burnet | | 100 | % | | 167 |

| | — |

| | — |

| | — |

|

| Hunter's Crossing | | | Bastrop | | 100 | % | | 510 |

| | — |

| | 54 |

| | 51 |

|

| La Conterra | | | Williamson | | 100 | % | | 202 |

| | — |

| | 3 |

| | — |

|

| Westside at Buttercup Creek | | | Williamson | | 100 | % | | 1,497 |

| | — |

| | 66 |

| | — |

|

| | | | | | 2,948 |

| | 378 |

| | 150 |

| | 70 |

|

| Corpus Christi | | | | | | | | | | | |

| Caracol | | | Calhoun | | 75 | % | | 65 |

| | — |

| | 14 |

| | — |

|

Padre Island (b) | | | Nueces | | 50 | % | | — |

| | — |

| | — |

| | 15 |

|

| Tortuga Dunes | | | Nueces | | 75 | % | | 95 |

| | — |

| | 4 |

| | — |

|

| | | | | | 160 |

| | — |

| | 18 |

| | 15 |

|

| Dallas-Ft. Worth | | | | | | | | | | | |

| Bar C Ranch | | Tarrant | | 100 | % | | 331 |

| | 774 |

| | — |

| | — |

| | Tarrant | | 100 | % | | 467 |

| | 654 |

| | — |

| | — |

|

| Barrington Kingwood | | Harris | | 100 | % | | 148 |

| | 32 |

| | — |

| | — |

| |

| Cibolo Canyons | | Bexar | | 100 | % | | 911 |

| | 858 |

| | 130 |

| | 56 |

| |

| Harbor Lakes | | Hood | | 100 | % | | 221 |

| | 228 |

| | 13 |

| | 8 |

| |

| Hunter’s Crossing | | Bastrop | | 100 | % | | 510 |

| | — |

| | 41 |

| | 62 |

| |

| Imperial Forest | | Harris | | 100 | % | | — |

| | 428 |

| | — |

| | — |

| |

| La Conterra | | Williamson | | 100 | % | | 202 |

| | — |

| | 3 |

| | 55 |

| |

| Keller | | | Tarrant | | 100 | % | | — |

| | — |

| | 1 |

| | — |

|

| Lakes of Prosper | | Collin | | 100 | % | | 97 |

| | 190 |

| | 4 |

| | — |

| | Collin | | 100 | % | | 187 |

| | 100 |

| | 4 |

| | — |

|

| Lantana | | Denton | | 100 | % | | 1,131 |

| | 650 |

| | 9 |

| | 3 |

| | Denton | | 100 | % | | 3,670 |

| | 432 |

| | 44 |

| | — |

|

| Maxwell Creek | | Collin | | 100 | % | | 935 |

| | 66 |

| | 10 |

| | — |

| | Collin | | 100 | % | | 1,001 |

| | — |

| | 10 |

| | — |

|

| Oak Creek Estates | | Comal | | 100 | % | | 226 |

| | 328 |

| | 13 |

| | — |

| |

| Parkside | | Collin | | 100 | % | | — |

| | 200 |

| | — |

| | — |

| | Collin | | 100 | % | | 138 |

| | 62 |

| | — |

| | — |

|

| The Preserve at Pecan Creek | | | Denton | | 100 | % | | 631 |

| | 151 |

| | — |

| | 7 |

|

| River's Edge | | | Denton | | 100 | % | | — |

| | 202 |

| | — |

| | — |

|

| Stoney Creek | | Dallas | | 100 | % | | 221 |

| | 487 |

| | — |

| | — |

| | Dallas | | 100 | % | | 320 |

| | 376 |

| | — |

| | — |

|

| Summer Creek Ranch | | Tarrant | | 100 | % | | 974 |

| | 277 |

| | 35 |

| | 44 |

| | Tarrant | | 100 | % | | 983 |

| | 245 |

| | 35 |

| | 44 |

|

| Timber Creek | | | Collin | | 88 | % | | 80 |

| | 521 |

| | — |

| | — |

|

| Village Park | | | Collin | | 100 | % | | 567 |

| | — |

| | 3 |

| | 2 |

|

| | | | | | 8,044 |

| | 2,743 |

| | 97 |

| | 53 |

|

| Houston | | | | | | | | | | | |

| Barrington Kingwood | | | Harris | | 100 | % | | 176 |

| | 4 |

| | — |

| | — |

|

| City Park | | | Harris | | 75 | % | | 1,468 |

| | — |

| | 58 |

| | 104 |

|

Harper's Preserve (b) | | | Montgomery | | 50 | % | | 588 |

| | 1,094 |

| | 30 |

| | 49 |

|

| Imperial Forest | | | Harris | | 100 | % | | 84 |

| | 347 |

| | — |

| | — |

|

Long Meadow Farms (b) | | | Fort Bend | | 38 | % | | 1,648 |

| | 149 |

| | 194 |

| | 99 |

|

Southern Trails (b) | | | Brazoria | | 80 | % | | 954 |

| | 41 |

| | 1 |

| | — |

|

| Spring Lakes | | | Harris | | 100 | % | | 348 |

| | — |

| | 25 |

| | 4 |

|

| Summer Lakes | | Fort Bend | | 100 | % | | 614 |

| | 455 |

| | 56 |

| | — |

| | Fort Bend | | 100 | % | | 780 |

| | 294 |

| | 56 |

| | — |

|

| Summer Park | | Fort Bend | | 100 | % | | 69 |

| | 130 |

| | 28 |

| | 68 |

| | Fort Bend | | 100 | % | | 125 |

| | 74 |

| | 34 |

| | 67 |

|

| The Colony | | Bastrop | | 100 | % | | 451 |

| | 1,434 |

| | 22 |

| | 31 |

| |

| The Preserve at Pecan Creek | | Denton | | 100 | % | | 534 |

| | 248 |

| | — |

| | 7 |

| |

| Village Park | | Collin | | 100 | % | | 756 |

| | — |

| | 3 |

| | 2 |

| |

| Westside at Buttercup Creek | | Williamson | | 100 | % | | 1,496 |

| | 1 |

| | 66 |

| | — |

| |

| Other projects (9) | | Various | | 100 | % | | 1,776 |

| | 228 |

| | 133 |

| | 7 |

| |

| Willow Creek Farms II | | | Waller / Fort Bend | | 90 | % | | 154 |

| | 111 |

| | — |

| | — |

|

| | | | | | 6,325 |

| | 2,114 |

| | 398 |

| | 323 |

|

| San Antonio | | | | | | | | | | | |

| Cibolo Canyons | | | Bexar | | 100 | % | | 1,142 |

| | 649 |

| | 97 |

| | 58 |

|

| Oak Creek Estates | | | Comal | | 100 | % | | 326 |

| | 227 |

| | 13 |

| | — |

|

| Olympia Hills | | | Bexar | | 100 | % | | 747 |

| | 7 |

| | 10 |

| | — |

|

Stonewall Estates (b) | | | Bexar | | 50 | % | | 378 |

| | 8 |

| | — |

| | — |

|

| | | | | | 2,593 |

| | 891 |

| | 120 |

| | 58 |

|

| Total Texas | | | | | 20,070 |

| | 6,126 |

| | 783 |

| | 519 |

|

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | |

|

| | | | | | | | | | | | | | | | | |

| | | | | | | Residential Lots(c) | | Commercial Acres(d) |

| Project | | County | | Interest Owned(b) | | Lots Sold Since Inception | | Lots Remaining | | Acres Sold Since Inception | | Acres Remaining(e) |

| | | | | | | | | | | | | |

| Georgia | | | | | | | | | | | | |

| Seven Hills | | Paulding | | 100 | % | | 780 |

| | 303 |

| | 26 |

| | 113 |

|

| The Villages at Burt Creek | | Dawson | | 100 | % | | — |

| | 1,715 |

| | — |

| | 57 |

|

| Other projects (18) | | Various | | 100 | % | | 297 |

| | 2,796 |

| | — |

| | 705 |

|

| Other | | | | | | | | | | | | |

| Other projects (3) | | Various | | 100 | % | | 534 |

| | 418 |

| | — |

| | — |

|

| | | | | | | 13,601 |

| | 13,976 |

| | 614 |

| | 1,626 |

|

| | | | | | | | | | | | | |

| Projects in entities we consolidate | | | | | | | | | | | | |

| Texas | | | | | | | | | | | | |

| City Park | | Harris | | 75 | % | | 1,311 |

| | 504 |

| | 50 |

| | 115 |

|

| Timber Creek | | Collin | | 88 | % | | — |

| | 601 |

| | — |

| | — |

|

| Willow Creek Farms II | | Waller/Fort Bend | | 90 | % | | 90 |

| | 160 |

| | — |

| | — |

|

| Other projects (2) | | Various | | Various |

| | 10 |

| | 198 |

| | — |

| | 18 |

|

| Georgia | | | | | | | | | | | | |

| The Georgian | | Paulding | | 75 | % | | 535 |

| | — |

| | — |

| | — |

|

| | | | | | | 1,946 |

| | 1,463 |

| | 50 |

| | 133 |

|

| Total owned and consolidated | | | | | | 15,547 |

| | 15,439 |

| | 664 |

| | 1,759 |

|

| Projects in ventures that we account for using the equity method | | | | | | | | | | |

| Texas | | | | | | | | | | | | |

| Entrada | | Travis | | 50 | % | | — |

| | 821 |

| | — |

| | — |

|

| Fannin Farms West | | Tarrant | | 50 | % | | 324 |

| | — |

| | — |

| | 12 |

|

| Harper’s Preserve | | Montgomery | | 50 | % | | 315 |

| | 1,413 |

| | 15 |

| | 64 |

|

| Lantana - Rayzor Ranch | | Denton | | 25 | % | | 1,163 |

| | — |

| | 16 |

| | 42 |

|

| Long Meadow Farms | | Fort Bend | | 38 | % | | 1,399 |

| | 405 |

| | 187 |

| | 118 |

|

| Southern Trails | | Brazoria | | 80 | % | | 794 |

| | 202 |

| | — |

| | 1 |

|

| Stonewall Estates | | Bexar | | 50 | % | | 342 |

| | 48 |

| | — |

| | — |

|

| Other projects (2) | | Various | | Various |

| | — |

| | — |

| | — |

| | 15 |

|

| Total in ventures | | | | | | 4,337 |

| | 2,889 |

| | 218 |

| | 252 |

|

| Combined Total | | | | | | 19,884 |

| | 18,328 |

| | 882 |

| | 2,011 |

|

|

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | Residential Lots/Units | | Commercial Acres |

| Project | | County | | Interest

Owned (a) | | Lots/Units Sold

Since

Inception | | Lots/Units

Remaining | | Acres Sold

Since

Inception | | Acres

Remaining |

| Colorado | | | | | | | | | | | | |

| Denver | | | | | | | | | | | | |

| Buffalo Highlands | | Weld | | 100 | % | | — |

| | 164 |

| | — |

| | — |

|

| Cielo | | Douglas | | 100 | % | | — |

| | 343 |

| | — |

| | — |

|

| Johnstown Farms | | Weld | | 100 | % | | 281 |

| | 317 |

| | 2 |

| | — |

|

| Pinery West | | Douglas | | 100 | % | | 86 |

| | — |

| | 20 |

| | 104 |

|

| Stonebraker | | Weld | | 100 | % | | — |

| | 603 |

| | — |

| | — |

|

| | | | | | | 367 |

| | 1,427 |

| | 22 |

| | 104 |

|

| Georgia | | | | | | | | | | | | |

| Atlanta | | | | | | | | | | | | |

| Harris Place | | Paulding | | 100 | % | | 22 |

| | 5 |

| | — |

| | — |

|

Montebello (b) | | Forsyth | | 90 | % | | — |

| | 224 |

| | — |

| | — |

|

| Seven Hills | | Paulding | | 100 | % | | 912 |

| | 341 |

| | 26 |

| | 113 |

|

| West Oaks | | Cobb | | 100 | % | | 6 |

| | 50 |

| | — |

| | — |

|

| | | | | | | 940 |

| | 620 |

| | 26 |

| | 113 |

|

| North & South Carolina | | | | | | | | | | | | |

| Charlotte | | | | | | | | | | | | |

| Ansley Park | | Lancaster | | 100 | % | | — |

| | 307 |

| | — |

| | — |

|

| Habersham | | York | | 100 | % | | 91 |

| | 96 |

| | — |

| | 6 |

|

| Moss Creek | | Cabarrus | | 100 | % | | — |

| | 84 |

| | — |

| | — |

|

| Walden | | Mecklenburg | | 100 | % | | — |

| | 384 |

| | — |

| | — |

|

| | | | | | | 91 |

| | 871 |

| | — |

| | 6 |

|

| Raleigh | | | | | | | | | | | | |

Beaver Creek (b) | | Wake | | 90 | % | | 31 |

| | 162 |

| | — |

| | — |

|

| | | | | | | 31 |

| | 162 |

| | — |

| | — |

|

| | | | | | | 122 |

| | 1,033 |

| | — |

| | 6 |

|

| Tennessee | | | | | | | | | | | | |

| Nashville | | | | | | | | | | | | |

| Beckwith Crossing | | Wilson | | 100 | % | | 32 |

| | 67 |

| | — |

| | — |

|

| Morgan Farms | | Williamson | | 100 | % | | 132 |

| | 41 |

| | — |

| | — |

|

| Scales Farmstead | | Williamson | | 100 | % | | 26 |

| | 171 |

| | — |

| | — |

|

| Weatherford Estates | | Williamson | | 100 | % | | 8 |

| | 9 |

| | — |

| | — |

|

| | | | | | | 198 |

| | 288 |

| | — |

| | — |

|

| Wisconsin | | | | | | | | | | | | |

| Madison | | | | | | | | | | | | |

Juniper Ridge/Hawks Woods (b) (d) | | Dane | | 90 | % | | 18 |

| | 196 |

| | — |

| | — |

|

Meadow Crossing II (b) (c) | | Dane | | 90 | % | | 7 |

| | 165 |

| | — |

| | — |

|

| | | | | | | 25 |

| | 361 |

| | — |

| | — |

|

| Arizona, California, Missouri, Utah | | | | | | | | | | | | |

| Tucson | | | | | | | | | | | | |

Boulder Pass (b) (d) | | Pima | | 50 | % | | 29 |

| | 59 |

| | — |

| | — |

|

| Dove Mountain | | Pima | | 100 | % | | — |

| | 98 |

| | — |

| | — |

|

| Oakland | | | | | | | | | | | | |

| San Joaquin River | | Contra Costa/Sacramento | | 100 | % | | — |

| | — |

| | 264 |

| | 25 |

|

| Kansas City | | | | | | | | | | | | |

| Somerbrook | | Clay | | 100 | % | | 185 |

| | — |

| | — |

| | — |

|

| Salt Lake City | | | | | | | | | | | | |

Suncrest (b) (c) | | Salt Lake | | 90 | % | | — |

| | 171 |

| | — |

| | — |

|

| | | | | | | 214 |

| | 328 |

| | 264 |

| | 25 |

|

| Total | | | | | | 21,936 |

| | 10,183 |

| | 1,095 |

| | 767 |

|

________________________________________

| |

(a) | AInterest owned reflects our total interest in the project, is deemed entitled when all major discretionary governmental land-use approvals have been received. Some projectswhether directly or indirectly, which may require additional permits and/or non-governmental authorizations for development.be different than our economic interest in the project. |

| |

(b) | Interest owned reflects our net equity interestProjects in the project, whether owned directly or indirectly. There are some projectsventures that have multiple ownership structures within them. Accordingly, portions of these projects may appear as owned, consolidated or accountedwe account for using the equity method. |

| |

(c) | Lots are for the totalVenture project regardless of our ownership interest. Lots remaining represent vacant developed lots, lots under developmentthat develops and future planned lots and are subject to change based on business plan revisions.sells homes. |

| |

(d) | Commercial acres are for the totalVenture project regardless of our ownership interest,that develops and are net developable acres, which may be fewer than the gross acres available in the project.sells lots and homes. |

| |

(e)

| Excludes acres associated with commercial and income producing properties. |

A summary of our significant commercial and income producingnon-core multifamily properties, excluding one multifamily site in Austin classified as held for sale, at year-end 20142016 follows:

|

| | | | | | | | | | | | |

| Project | | Market | | Interest Owned(a) | | Type | | Acres | | Description |

| Radisson Hotel | | Austin | | 100 | % | | Hotel | | 2 |

| | 413 guest rooms and suites |

| Eleven | | Austin | | 100 | % | | Multifamily | | 3 |

| | 257-unit luxury apartment |

Midtown(b) | | Dallas | | 100 | % | | Multifamily | | 13 |

| | 354-unit luxury apartment |

360°(b) | | Denver | | 20 | % | | Multifamily | | 4 |

| | 304-unit luxury apartment |

Acklen(b) | | Nashville | | 30 | % | | Multifamily | | 6 |

| | 320-unit luxury apartment |

HiLine(b) | | Denver | | 25 | % | | Multifamily | | 6 |

| | 385-unit luxury apartment |

Elan 99(b) | | Houston | | 90 | % | | Multifamily | | 14 |

| | 360-unit luxury apartment |

|

| | | | | | | | | | | | |

| Project | | Market | | Interest

Owned (a) | | Type | | Acres | | Description |

| Elan 99 | | Houston | | 90 | % | | Multifamily | | 17 |

| | 360-unit luxury apartment |

| Acklen | | Nashville | | 30 | % | | Multifamily | | 4 |

| | 320-unit luxury apartment |

| HiLine | | Denver | | 25 | % | | Multifamily | | 18 |

| | 385-unit luxury apartment |

| | | | | | | | | | | |

_____________________

| |

(a) | Interest owned reflects our net equitytotal interest in the project, whether owned directly or indirectly. |

| |

(b)

| Constructionindirectly, which may be different than our economic interest in progress.the project. |

Our net investment in owned and consolidated real estate projects by geographic location at year-end 20142016 follows:

| | | State | | Entitled, Developed, and Under Development Projects | | Undeveloped Land and Land in Entitlement | | Income Producing Properties | | Total | | Entitled, Developed, and Under Development Projects | | Undeveloped Land and Land in Entitlement | | Total |

| | | (In thousands) | | (In thousands) |

| Texas | | $ | 250,548 |

| | $ | 5,931 |

| | $ | 138,423 |

| | $ | 394,902 |

| | $ | 167,772 |

| | $ | 2,639 |

| | $ | 170,411 |

|

| Georgia | | 17,418 |

| | 63,653 |

| | — |

| | 81,071 |

| | 7,504 |

| | 409 |

| | 7,913 |

|

| North and South Carolina | | | 27,915 |

| | 117 |

| | 28,032 |

|

| California | | 8,915 |

| | 23,040 |

| | — |

| | 31,955 |

| | 1,667 |

| | 25,957 |

| | 27,624 |

|

| Tennessee | | | 23,624 |

| | 22 |

| | 23,646 |

|

| Colorado | | 25,334 |

| | 5 |

| | — |

| | 25,339 |

| | 29,514 |

| | — |

| | 29,514 |

|

| Tennessee | | 10,461 |

| | 540 |

| | 7,675 |

| | 18,676 |

| |

| North Carolina | | — |

| | 13 |

| | 15,203 |

| | 15,216 |

| |

| Other | | 8,597 |

| | — |

| | — |

| | 8,597 |

| | 5,863 |

| | — |

| | 5,863 |

|

| Total | | $ | 321,273 |

| | $ | 93,182 |

| | $ | 161,301 |

| | $ | 575,756 |

| | $ | 263,859 |

| | $ | 29,144 |

| | $ | 293,003 |

|

Approximately 6958 percent of our net investment in real estate is in the major markets of Texas.

Markets

Sales of new U.S. single-family homes roseaccording to U.S Census Bureau Department of Commerce declined 0.4% on a year over year basis as of December 31, 2016 and 10.4% below prior month's rate in December 2016, suggesting that the 40 basis point rise in mortgage rates and the return of winter weather affected December 2016 sales. Consumer confidence as measured by The Conference Board increased in December 2016 to its highest level since August 2001, registering 113.7 up from 109.4 in November 2016. The elevated monthly reading was attributed in part to increases in consumers' outlook for business conditions over the next six-months and more positive outlooks for the labor market and rising incomes. Builder confidence as measured by the NAHB/Wells Fargo Housing Market Index ended 2016 on a high note, jumping seven points to its highest reading since July 2005, largely attributable to a six-yearpost-election bounce. On a monthly basis, housing starts increased significantly in December 2016 due to volatile multifamily activity, while housing permit activity, viewed as a precursor to starts increased 1.9% year over year basis ending December 2016. Home prices as measured by S&P Corelogic Case-Shiller Home Price index hit a new high in September 2014, onNovember 2016 after rising at approximately a seasonally adjusted basis, but a sharp downward revision5.5% annual rate over the last two-and-a half years. As of the November 2016 reading, average home prices for the metropolitan statistical areas (MSAs) within the two composite indices were back to their winter 2007 levels. As of year-end 2016, finished vacant supply of new homes soldand vacant developed lot supply in November 2014 when compared with November 2013 indicatesMSAs in which Forestar's single family activity is located remained extremely tight, registering below the housing recovery remains tentative. Inventories of new homes are at historically low levels in many areas. In addition to declining finished lot inventoriestwo month and limited supply of economically developable raw land has increased demand for our developed lots. However, national and global economic weakness and uncertainty, and a restrictive mortgage lending environment continue to threaten a robust recovery in the housing market, despite low interest rates. Multifamily market conditions continue to be strong, with many markets experiencing healthy occupancy levels and positive rent growth. This improvement has been driven primarily by limited housing inventory, reduced single-family mortgage credit availability, and the increased propensity to rent among the 18 to 34 year old demographic of the U.S. population.

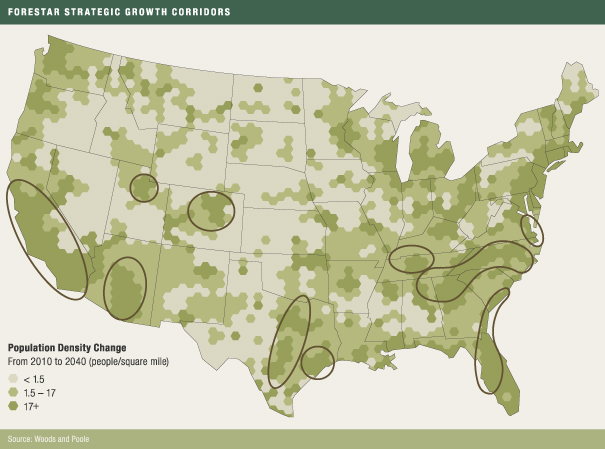

Forestar Strategic Growth Corridors

We target investments primarily in markets within our strategic growth corridors, which we define as areas possessing favorable growth characteristics for population, employment and household formation. These markets are generally located across the southern half of the U.S., and we believe they represent attractive long-term real estate investment opportunities. Demand for residential lots, single-family housing, and commercial land is substantially influenced by these growth characteristics, as well as by immigration and in-migration. Currently, most of our development projects are located within the major markets of Texas.

Our ten strategic growth corridors encompass 164,000 square miles, or approximately 4.6 percent of the total land area in the U.S. According to 2010 census data, 91.7 million people, or 30 percent of the U.S. total, reside in these corridors. The population density in these growth corridors is over six times the national average and is projected to grow to over 10 times the national average between 2010 and 2040. During that time, the target corridors are projected to garner approximately 49 percent of the nation’s population growth and 40 percent of total employment growth. Estimated housing demand from these ten growth corridors from 2010 to 2040 exceeds 24 million new homes.

Our value creation strategy includes both growth through strategic and disciplined investment in acquisitions that meet our investment criteria, and entitlement and development on our own lands. We continually monitor the markets in our strategic growth corridors for opportunities to acquire developed lots and land at prices that meet our return criteria.

Competition

We face significant competition for the acquisition, entitlement, development and sale of real estate in our markets. Our major competitors include other landowners who market and sell undeveloped land and numerous national, regional and local developers.developers, including home builders. In addition, our projects compete with other development projects offering similar

amenities, products and/or locations. Competition also exists for investment opportunities, financing, available land, raw materials and labor, with entities that may possess greater financial, marketing and other resources than us. The presence of competition may increase the bargaining power of property owners seeking to sell. These competitive market pressures sometimes make it difficult to acquire, entitle, develop or sell land at prices that meet our return criteria. Some of our real estate competitors are well established and financially strong, may have greater financial resources than we do, or may be larger than us and/or have lower cost of capital and operating costs than we have and expect to have.

The land acquisition and development business is highly fragmented, and we are unaware of any meaningful concentration of market share by any one competitor. Enterprises of varying sizes, from individuals or small companies to large corporations, actively engage in the real estate development business. Many competitors are local, privately-owned companies. We have a few regional competitors and virtually no national competitors other than national home builders that, depending on business cycles and market conditions, may enter or exit the real estate development business in some locations to develop lots on which they construct and sell homes. During periods when access to capital is restricted, participants with weaker financial conditions tend to be less active.

Oil Discontinued Operations

In 2016, we have divested substantially all of our oil and Gas

Ourgas working interest properties. As a result of this significant change in our operations, we have reported the results of operations and financial position of these assets as discontinued operations within our consolidated statements of income (loss) and comprehensive income (loss) and consolidated balance sheets for all periods presented. In addition, in second quarter 2016, we changed the name of the oil and gas segment to mineral resources to reflect the strategic shift from oil and gas working interests to owned mineral interests.

Mineral Resources

Our mineral resources segment is focused on maximizing the value from our owned oil and gas mineral interests through promoting exploration, development and production of oil and gas on our owned and leasehold mineral interests.

We typically lease our owned mineral interests to third parties for exploration and production of oil and gas. When we lease our mineral interests, we negotiate a lease bonus payment and retain a royalty interest and may take an additional working interest participation in production. Working interests refer to well interests in which we pay a share of the costs to drill, complete and operate a well and receive a proportionate share of the production revenues.

In 2012, we acquired 100 percent of the outstanding common stock of Credo in an all cash transaction for $14.50 per share, representing an equity purchase price of approximately $146.4 million. In addition, we paid in full $8.8 million of Credo’s outstanding debt at closing. Credo was an independent oil and gas exploration, development and production company based in Denver, Colorado. The acquired assets principally included leasehold interests in the Bakken and Three Forks formations of North Dakota, the Lansing – Kansas City formation in Kansas and Nebraska, and the Tonkawa and Cleveland formations in Texas.

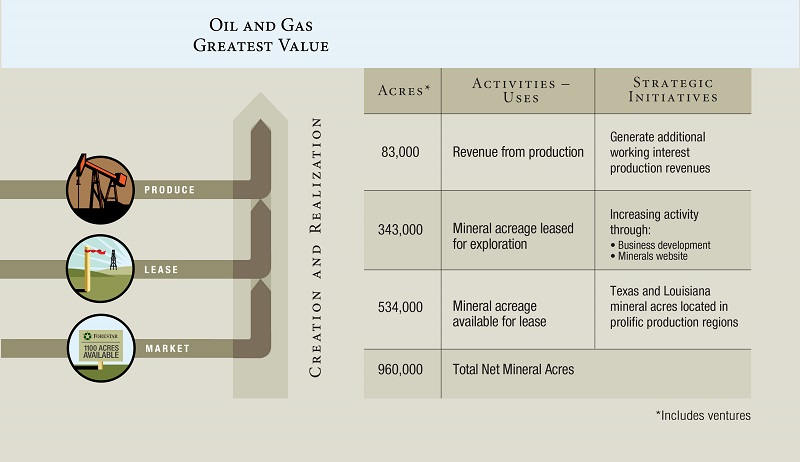

Our strategy for maximizing value from our owned and leased mineral interests is to move acres up the minerals value chainactivities by participating in working interests in the drilling, completion and production of oil and gas, increasing the net acreage leased, of our owned interests, the lease bonus amount per acrerates, and the size of retained royalty interests. The chart below depicts our minerals interests value chain:

Owned Mineral Interests

We own mineral interests beneath approximately 590,000 net acres located in the United States, principally in Texas, Louisiana, Georgia and Alabama. Our revenue from our owned mineral interests is primarily from oil and gas royalty interests, lease bonus payments and delay rentals received and other related activities. We engage in leasing certain portions of thesetypically lease our owned mineral interests to third parties for the exploration and production of oil and gas.

At year-end 2014, of our 590,0002016, we had approximately 523,000 net acres of owned mineral interests,acres that are classified as assets held for sale. On February 17, 2017, we sold substantially all of our remaining oil and gas assets for a total purchase price of $85,600,000. Please read Note 21 — Subsequent Events for additional information about 534,000 net acres are available for lease. We havethese items. At year-end 2016, we had about 56,00057,000 net acres leased for oil and gas exploration activities, of which about 36,00044,000 net acres arewere held by production from over 551473 gross oil and gas wells that arewere operated by others, in which we havehad royalty interest.interests. In addition, we havehad working interest ownership in 3331 of these wells. Many of these wells are part of an oil and gas unit, however; we count each well regardless of the unitization.

A summary of our non-core owned mineral acres(a) at year-end 20142016 follows:

| | | State | | Unleased | | Leased(b) | | Held By Production(c) | | Total(d) | | Unleased | | Leased (b) | | Held By Production (c) | | Total (d) |

Texas | | 208,000 |

| | 17,000 |

| | 27,000 |

| | 252,000 |

| | 210,000 |

| | 8,000 |

| | 34,000 |

| | 252,000 |

|

| Louisiana | | 132,000 |

| | 3,000 |

| | 9,000 |

| | 144,000 |

| |

Louisiana (e) (f) | | | 129,000 |

| | 5,000 |

| | 10,000 |

| | 144,000 |

|

| Georgia | | 152,000 |

| | — |

| | — |

| | 152,000 |

| | 84,000 |

| | — |

| | — |

| | 84,000 |

|

| Alabama | | 40,000 |

| | — |

| | — |

| | 40,000 |

| | 41,000 |

| | — |

| | — |

| | 41,000 |

|

| California | | 1,000 |

| | — |

| | — |

| | 1,000 |

| | 1,000 |

| | — |

| | — |

| | 1,000 |

|

| Indiana | | 1,000 |

| | — |

| | — |

| | 1,000 |

| | 1,000 |

| | — |

| | — |

| | 1,000 |

|

| | | 534,000 |

| | 20,000 |

| | 36,000 |

| | 590,000 |

| | 466,000 |

| | 13,000 |

| | 44,000 |

| | 523,000 |

|

_____________________

| |

(b) | Includes leases in primary lease term or for which a delayed rental payment has been received. In the ordinary course of business, leases covering a significant portion of leased net mineral acres may expire from time to time in a single reporting period. |

| |

(c) | Acres being held by production are producing oil or gas in paying quantities. |

| |

(d) | Texas, Louisiana, California and Indiana net acres are calculated as the gross number of surface acres multiplied by our percentage ownership of the mineral interest. Alabama and Georgia net acres are calculated as the gross number of surface acres multiplied by our estimated percentage ownership of the mineral interest based on county sampling. In fourth quarter |

A summary

2016, we sold approximately 58,300 acres of our Texastimberland and Louisianaundeveloped land in Georgia and Alabama which included selling any owned mineral acres(a) primarily in East Texas and Gulf Coast Basins by county or parish at year-end 2014 follows:

|

| | | | | | | | |

| Texas | | Louisiana(b) |

| County | | Net Acres | | Parish | | Net Acres |

| Trinity | | 46,000 |

| | Beauregard | | 79,000 |

|

| Angelina | | 42,000 |

| | Vernon | | 39,000 |

|

| Houston | | 29,000 |

| | Calcasieu | | 17,000 |

|

| Anderson | | 25,000 |

| | Allen | | 7,000 |

|

| Cherokee | | 24,000 |

| | Rapides | | 1,000 |

|

| Sabine | | 23,000 |

| | Other | | 1,000 |

|

| Red River | | 14,000 |

| | | | 144,000 |

|

| Newton | | 13,000 |

| | | | |

| San Augustine | | 13,000 |

| | | | |

| Jasper | | 12,000 |

| | | | |

| Other | | 11,000 |

| | | | |

| | | 252,000 |

| | | | |

_____________________minerals rights associated with these acres.

| |

(a)(e)

| Includes ventures. These owned mineral acre interests contain numerous oil and gas producing formations consisting of conventional, unconventional, and tight sand reservoirs. Of these reservoirs, we have mineral interests in and around production trends in the Wilcox, Frio, Cockfield, James Lime, Pettet,Petet, Travis Peak, Cotton Valley, Austin Chalk, Haynesville Shale, Barnett Shale and Bossier formations. |

| |

(b)(f)

| A significant portion of our Louisiana net mineral acres werewas severed from the surface estate shortly before our 2007 spin-off. Under Louisiana law, a mineral servitude that is not producing minerals or which has not been the subject of good-faith drilling operations will cease to burden the property upon the tenth anniversary of the date of its creation. The total number of net acres subject to prescription can fluctuate based on oil and gas development and production activities. Some or all of approximately 70,000 of our Louisiana net acres may revert to the surface owner unless drilling operations or production commences prior to October 2017. |

We engage in leasing certain portions of our owned mineral interests to third parties for the exploration and production of oil and gas. Leasing mineral acres for exploration and production can create significant value because we may negotiate a lease bonus payment and retain a royalty interest in all revenues generated by the lessee from oil and gas production. The significant terms of these arrangements include granting the exploration company the rights to oil or gas it may find and requiring that drilling be commenced within a specified period. In return, we may receive an initial lease payment (bonus), subsequent payments if drilling has not started within the specified period (delay rentals), and a percentage interest in the value of any oil or gas produced (royalties). If no oil or gas is produced during the required period, all rights are returned to us. Historically, our capital requirements for our owned mineral acres have been minimal.

Our royalty revenues are contractually defined and based on a percentage of production and are received in cash. Our royalty revenues fluctuate based on changes in the market prices for oil and gas, the decline in production in existing wells, and other factors affecting the third-party oil and gas exploration and production companies that operate wells on our minerals including the cost of development and production.

Most leases are for a three to five year term although a portion or all of a lease may be extended by the lessee as long as actual production is occurring. Financial terms vary based on a number of market factors including the location of the mineral interest, the number of acres subject to the agreement, proximity to transportation facilities such as pipelines, depth of formations to be drilled and risk.

Mineral Interests Leased

With the acquisition of Credo, we became an independent oil and gas exploration, development and production company. As of year-end 2014, our leasehold interests include 370,000 net mineral acres leased from others principally located in Nebraska and Kansas primarily targeting the Lansing – Kansas City formation, in Oklahoma primarily targeting the Anadarko Basin, in the Texas Panhandle primarily targeting the Tonkawa and Cleveland formations, and in North Dakota primarily targeting the Bakken and Three Forks formations. We have 47,000 net acres held by production and 393 gross oil and gas wells with working interest ownership, of which 153 are operated by us.

A summary of our net mineral acres leased from others as of year-end 2014 follows:

|

| | | | | | | | | |

| State | | Undeveloped(b) | | Held By Production | | Total |

| Nebraska | | 248,000 |

| | 11,000 |

| | 259,000 |

|

| Kansas | | 18,000 |

| | 8,000 |

| | 26,000 |

|

| Oklahoma | | 23,000 |

| | 18,000 |

| | 41,000 |

|

| Texas | | 10,000 |

| | 2,000 |

| | 12,000 |

|

| North Dakota | | 5,000 |

| | 4,000 |

| | 9,000 |

|

Other(a) | | 19,000 |

| | 4,000 |

| | 23,000 |

|

| | | 323,000 |

| | 47,000 |

| | 370,000 |

|

__________________

| |

(a)

| Excludes approximately 8,000 net acres of overriding royalty interests |

| |

(b)

| We have approximately 59,000 gross and 44,000 net undeveloped acres scheduled to expire in 2015, some of which we are currently evaluating for lease extension. |

Nebraska and Kansas

We have about 285,000 net mineral acres primarily located on or near the Central Kansas Uplift formations located in the western Kansas counties of Logan, Lane, Thomas, Rawlins and Gove and in the southwest portion of Nebraska in the counties of Dundy, Red Willow and Hitchcock. At year-end 2014, we own working interests in 139 gross producing wells with an average working interest of 51 percent.

Oklahoma

We have about 41,000 net mineral acres located in the Anadarko Basin. At year-end 2014, we own working interests in 88 gross producing wells with an average working interest of 38 percent.

Texas

We have about 12,000 net mineral acres primarily in Sabine, San Augustine, Lipscomb, Hemphill, Tyler and Fayette counties. We own working interests in 55 gross producing wells. These wells have an average working interest of 16 percent.

North Dakota

We have about 9,000 net acres in or near the core of the Bakken and Three Forks formations. Most of the acreage is located on the Fort Berthold Indian Reservation, south and west of the Parshall Field. We own working interests in 118 gross producing oil wells with an average working interest of 7 percent. Where a well has been drilled on a spacing unit, in many cases we expect additional development wells to be drilled on those spacing units in the future.

Most leases are for a three to five year term although a portion or all of a lease may be extended as long as production is occurring. Financial terms vary based on a number of factors including the location of the leasehold interest, the number of acres subject to the agreement, proximity to transportation facilities such as pipelines, depth of formations to be drilled and risk.

Estimated Proved Reserves (Including Discontinued Operations)

Our net estimated proved oil and gas reserves, all of which are located in the United States, as of year-end 2014,2016, 20132015 and 20122014 are set forth in the table below. We engaged independent petroleum engineers, Netherland, Sewell & Associates, Inc.(NSAI), to assist us in preparing estimates of our proved oil and gas reserves in accordance with the definitions and guidelines of the Securities and Exchange Commission (SEC).

Net quantities of proved oil and gas reserves related to our working and royalty interests follow:follow, including oil and gas working interest assets classified as discontinued operations in 2016:

| | | | Reserves | Reserves |

| | Oil(a) (Barrels) | | Gas (Mcf) | Oil (a) (Barrels) | | Gas (Mcf) |

| | (In thousands) | (In thousands) |

| Consolidated entities: | | | | | | |

| Proved developed | 5,269 |

| | 10,848 |

| 446 |

| | 3,836 |

|

| Proved undeveloped | 2,403 |

| | 1,801 |

| — |

| | — |

|

| Total proved reserves 2014 | 7,672 |

| | 12,649 |

| |

| Total proved reserves 2016 | | 446 |

| | 3,836 |

|

| Proved developed | 3,893 |

| | 11,385 |

| 5,179 |

| | 7,957 |

|

| Proved undeveloped | 1,931 |

| | 2,245 |

| — |

| | — |

|

| Total proved reserves 2013 | 5,824 |

| | 13,630 |

| |

| Total proved reserves 2015 | | 5,179 |

| | 7,957 |

|

| Proved developed | 2,416 |

| | 10,448 |

| 5,269 |

| | 10,848 |

|

| Proved undeveloped | 804 |

| | 1,274 |

| 2,403 |

| | 1,801 |

|

| Total proved reserves 2012 | 3,220 |

| | 11,722 |

| |

| Total proved reserves 2014 | | 7,672 |

| | 12,649 |

|

| Our share of ventures accounted for using the equity method: | | | | | | |

| Proved developed | — |

| | 1,751 |

| — |

| | 1,199 |

|

| Proved undeveloped | — |

| | — |

| — |

| | — |

|

| Total proved reserves 2014 | — |

| | 1,751 |

| |

| Total proved reserves 2016 | | — |

| | 1,199 |

|

| Proved developed | — |

| | 2,332 |

| — |

| | 1,263 |

|

| Proved undeveloped | — |

| | — |

| — |

| | — |

|

| Total proved reserves 2013 | — |

| | 2,332 |

| |

| Total proved reserves 2015 | | — |

| | 1,263 |

|

| Proved developed | — |

| | 2,572 |

| — |

| | 1,751 |

|

| Proved undeveloped | — |

| | — |

| — |

| | — |

|

| Total proved reserves 2012 | — |

| | 2,572 |

| |

| Total proved reserves 2014 | | — |

| | 1,751 |

|

| Total consolidated and our share of equity method ventures: | | | | | | |

| Proved developed | 5,269 |

| | 12,599 |

| 446 |

| | 5,035 |

|

| Proved undeveloped | 2,403 |

| | 1,801 |

| — |

| | — |

|

| Total proved reserves 2014 | 7,672 |

| | 14,400 |

| |

| Total proved reserves 2016 | | 446 |

| | 5,035 |

|

| Proved developed | 3,893 |

| | 13,717 |

| 5,179 |

| | 9,220 |

|

| Proved undeveloped | 1,931 |

| | 2,245 |

| — |

| | — |

|

| Total proved reserves 2013 | 5,824 |

| | 15,962 |

| |

| Total proved reserves 2015 | | 5,179 |

| | 9,220 |

|

| Proved developed | 2,416 |

| | 13,020 |

| 5,269 |

| | 12,599 |

|

| Proved undeveloped | 804 |

| | 1,274 |

| 2,403 |

| | 1,801 |

|

| Total proved reserves 2012 | 3,220 |

| | 14,294 |

| |

| Total proved reserves 2014 | | 7,672 |

| | 14,400 |

|

_____________________

| |

(a) | Includes natural gas liquids. |

The following summarizes the changes in proved reserves for 2014:2016:

| | | | Reserves | Reserves |

| | Oil (Barrels) | | Gas (Mcf) | Oil (Barrels) | | Gas (Mcf) |

| | (In thousands) | (In thousands) |

| Consolidated entities: | | | | | | |

| Year-end 2013 | 5,824 |

| | 13,630 |

| |

| Year-end 2015 | | 5,179 |

| | 7,957 |

|

| Revisions of previous estimates | 608 |

| | 293 |

| (11 | ) | | 631 |

|

| Extensions and discoveries | 2,191 |

| | 774 |

| 29 |

| | — |

|

| Acquisitions | 85 |

| | 31 |

| — |

| | — |

|

| Sales | (105 | ) | | (218 | ) | (4,460 | ) | | (3,756 | ) |

| Production | (931 | ) | | (1,861 | ) | (291 | ) | | (996 | ) |

| Year-end 2014 | 7,672 |

| | 12,649 |

| |

| Year-end 2016 | | 446 |

| | 3,836 |

|

| Our share of ventures accounted for using the equity method: | | | | | | |

| Year-end 2013 | — |

| | 2,332 |

| |

| Year-end 2015 | | — |

| | 1,263 |

|

| Revisions of previous estimates | — |

| | (382 | ) | — |

| | 79 |

|

| Extensions and discoveries | — |

| | — |

| — |

| | — |

|

| Production | — |

| | (199 | ) | — |

| | (143 | ) |

| Year-end 2014 | — |

| | 1,751 |

| |

| Year-end 2016 | | — |

| | 1,199 |

|

| Total consolidated and our share of equity method ventures: | | | | | | |

| Year-end 2014 | 7,672 |

| | 14,400 |

| |

| Year-end 2016 | | 446 |

| | 5,035 |

|

We do not have any estimated reserves of synthetic oil, synthetic gas or products of other non-renewable natural resources that are intended to be upgraded into synthetic oil and gas.

At year-end 2014,2016, we have approximately 2,703,000 barrelno barrels of oil equivalent (BOE) of proved undeveloped (PUD) reserves compared with 2,305,000because we have substantially divested all our non-core oil and gas working interest assets. At year-end 2015, we had no BOE of PUD reserves at year-end 2013. The increase in PUD reserves is principally due to (i) additionsour planned divestiture of 956,000 BOE from higher estimated recovery rates, lease acquisitions, extensionsoil and new discoveries, (ii) the conversion of 384,000gas working interest assets and not allocating capital to this non-core business. At year-end 2014, we had 2,703,000 BOE of PUD reserves to proved developed reserves, and (iii) downward revisions of 174,000 BOE related to lower oil prices. As a percent of our total proved reserves, PUD reserves were 27% at year-end 2014 and year-end 2013.reserves.

We did not participate in any drilling activity in 2016. In 2014,2015, we invested approximately $10,395,000 million, in addition to $383,000 of previous capital investments,$9,205,000 to convert 384,000610,000 BOE of PUD reserves into proved developed reserves.

All of our PUD reserves at year-end 2014 are expected to be developed over the next five years. Estimated future development costs related to the development of our 2,700,000 BOE at year-end 2014 PUD reserves are projected to be approximately $57 million.

Reserve estimates were based on the economic and operating conditions existing at year-end 2014, 20132016, 2015 and 2012.2014. Oil and gas prices arewere based on the twelve month unweighted arithmetic average of the first-day-of-the-month price for each month in the period January through December. For 2014,2016, 20132015 and 20122014, prices used for reserve estimates were $94.99, $96.91$42.75, $50.28 and $94.71$94.99 per barrel of West Texas Intermediate Crude Oil and gas prices of $4.35, $3.67$2.48, $2.59 and $2.76$4.35 per MMBTU per the Henry Hub spot market.spot. All prices were then adjusted for quality, transportation fees and regional price differentials. Since the determination and valuation of proved reserves is a function of the interpretation of engineering and geologic data and prices for oil and gas and the cost to produce these reserves, the reserves presented should be expected to change as future information becomes available. For an estimate of the standardized measure of discounted future net cash flows from proved oil and gas reserves, please read Note 19 — Supplemental Oil and Gas Disclosures (Unaudited) to our consolidated financial statements included in Part II, Item 8 of this Annual Report on Form 10-K.

The process of estimating oil and gas reserves is complex, involving decisions and assumptions in evaluating the available geological, geophysical, engineering and economic data. Accordingly, these estimates are imprecise. Actual future production, oil and gas prices, capital costs, operating costs, revenues, taxes and quantities of recoverable oil and gas reserves might vary from those estimated. Any variance could materially affect the estimated quantities and present value of proved reserves. In addition, estimates of proved reserves may be adjusted to reflect production history, development, prevailing oil and gas prices and other factors, many of which are beyond our control.

The primary internal technical person in charge of overseeing our reserves estimates has a Bachelor of Science in Physics and Mathematics and a MastersMaster's of Science in Civil Engineering. He has over 40 years of domestic and international experience in the exploration and production business including 3940 years of reserve evaluations. He has been a registered Professional Engineer for over 25 years.