UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20202023

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-34028

AMERICAN WATER WORKS COMPANY, INC.

(Exact name of registrant as specified in its charter)

| | | | | |

| Delaware | 51-0063696 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

1 Water Street, Camden, NJ 08102-1658

(Address of principal executive offices) (Zip Code)

(856) 955-4001

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol | | Name of each exchange on which registered |

| Common stock, par value $0.01 per share | | AWK | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | | ☒ | | Accelerated filer | | ☐ |

| Non-accelerated filer | | ☐ | | Smaller reporting company | | ☐ |

| | | | Emerging growth company | | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

Common Stock, $0.01 par value—$20,390,800,00024,527,200,000 as of June 30, 20202023 (solely for purposes of calculating this aggregate market value, American Water has defined its affiliates to include (i) those persons who were, as of June 30, 2020,2023, its executive officers, directors or known beneficial owners of more than 10% of its common stock, and (ii) such other persons who were deemed, as of June 30, 2020,2023, to be controlled by, or under common control with, American Water or any of thesuch persons described in clause (i) above).

Indicate the number of shares outstanding of eacheach of the registrant’s classes of common stock as of the latest practicable date: Common Stock, $0.01 par value per share—181,439,255194,755,320 shares as of February 19, 2021.6, 2024.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the American Water Works Company, Inc. definitive proxy statement for the 2021 Annual2024 Annual Meeting of Shareholders to be filed with the Securities and Exchange Commission within 120 days after December 31, 20202023 are incorporated by reference into Part III of this report.

TABLE OF CONTENTS

| | | | | | | | |

| | | Page |

| |

| | | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 1C. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| Item 9C. | | |

| | | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| | | |

| Item 15. | | |

| Item 16. | | |

| |

| |

FORWARD-LOOKING STATEMENTS

Statements included in Item 1—Business, Item 1A—Risk Factors, and Item 7—Management’s Discussion and Analysis of Financial Condition and Results of Operations, and in other sections of this Annual Report on Form 10-K, or incorporated by reference into this Form 10-K,therein, are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and the Private Securities Litigation Reform Act of 1995. In some cases, these forward-looking statements can be identified by words with prospective meanings such as “intend,” “plan,” “estimate,” “believe,” “anticipate,” “expect,” “predict,” “project,” “propose,” “assume,” “forecast,” “likely,” “uncertain,” “outlook,” “future,” “pending,” “goal,” “objective,” “potential,” “continue,” “seek to,” “may,” “can,” “should,” “will” and “could” or the negative of such terms or other variations or similar expressions. Forward-looking statements may relate to, among other things: the Company’s future financial performance, liquidity and cash flows; the timing and amount of rate and revenue adjustments, including through general rate case filings, filings for infrastructure surcharges and other governmental agency authorizations and proceedings, and filings to address regulatory lag; the Company’s ability to execute its current and long-term business, operational, capital expenditures and growth plans and portfolio optimization strategies, includingstrategies; the timing and outcome of pending or future acquisition activity, the completion of the announced sale of the Company’s New York subsidiary and the amount of proceeds anticipatedability to be received therefrom;achieve organic customer growth; the ability of the Company’s California subsidiary to obtain adequate alternative water supplies in lieu of diversions from the Carmel River; the amount, allocation and allocationtiming of projected capital expenditures and related funding requirements; the Company’s ability to repay or refinance debt; the ability to execute its currentfuture impacts of increased or increasing financing costs, inflation and long-term business, operational and capital expenditures strategies; itsinterest rates; the Company’s ability to finance current and projected operations, capital expendituresexpenditure needs and growth initiatives by accessing the debt and equity capital markets;markets and sources of short-term liquidity; the outcome and impact on the Company of governmental and regulatory investigations and proceedings and related potential fines, penalties and other sanctions; the ability to meet or exceed the Company’s stated environmental and sustainability goals, including its greenhouse gas (“GHG”) emission reduction, water delivery efficiency and water system resiliency goals; the ability to complete, and the timing and efficacy of, the design, development, implementation and improvement of technology and other strategic initiatives; the impactsCompany’s ability to the Company of the current pandemic health event resulting from the novel coronavirus (“COVID-19”);comply with new and changing environmental regulations; the ability to capitalize on existing or future utility privatization opportunities; trends in the water and wastewater industries in which the Company operates, including macro trends with respect to the Company’s efforts related to customer, technology and work execution; regulatory, legislative, tax policy or legal developments; and impacts that future significant tax legislation may have on the Company and on its business, results of operations, cash flows and liquidity.

Forward-looking statements are predictions based on the Company’s current expectations and assumptions regarding future events. They are not guarantees or assurances of any outcomes, financial results, levels of activity, performance or achievements, and readers are cautioned not to place undue reliance upon them. These forward-looking statements are subject to a number of estimates, assumptions, known and unknown risks, uncertainties and other factors. The Company’s actual results may vary materially from those discussed in the forward-looking statements included herein as a result of the factors discussed under Item 1A—Risk Factors, and the following important factors:

•the decisions of governmental and regulatory bodies, including decisions to raise or lower customer rates and regulatory responses to the COVID-19 pandemic;rates;

•the timeliness and outcome of regulatory commissions’ and other authorities’ actions concerning rates, capital structure, authorized return on equity, capital investment, system acquisitions and dispositions, taxes, permitting, water supply and management, and other decisions;

•changes in customer demand for, and patterns of use of, water and energy, such as may result from conservation efforts, impacts of the COVID-19 pandemic, or otherwise;

•limitations on the availability of the Company’s water supplies or sources of water, or restrictions on its use thereof, resulting from allocation rights, governmental or regulatory requirements and restrictions, drought, overuse or other factors;

•a loss of one or more large industrial or commercial customers due to adverse economic conditions, the COVID-19 pandemic, or other factors;

•present and future proposed changes in laws, governmental regulations and policies, including with respect to environmental,the environment (such as, for example, potential improvements to existing Federal regulations with respect to lead and copper service lines and galvanized steel pipe), health and safety, data and consumer privacy, security and data privacy,protection, water quality and water quality accountability, contaminants of emerging concern (including without limitation per- and polyfluoroalkyl substances (“PFAS”)), public utility and tax regulations and policies, and impacts resulting from U.S., state and local elections and changes in federal, state and local executive administrations;

•the Company’s ability to collect, distribute, use, secure and store consumer data in compliance with current or future governmental laws, regulations and policies with respect to data and consumer privacy, security and protection;

•weather conditions and events, climate variability patterns, and natural disasters, including drought or abnormally high rainfall, prolonged and abnormal ice or freezing conditions, strong winds, coastal and intercoastal flooding, pandemics (including COVID-19) and epidemics, earthquakes, landslides, hurricanes, tornadoes, wildfires, electrical storms, sinkholes and solar flares;

•the outcome of litigation and similar governmental and regulatory proceedings, investigations or actions;

•the risks associated with the Company’s aging infrastructure, and its ability to appropriately improve the resiliency of or maintain, andupdate, redesign and/or replace, current or future infrastructure and systems, including its technology and other assets, and manage

the expansion of its businesses;

•exposure or infiltration of the Company’s technology and critical infrastructure systems, including the disclosure of sensitive, personal or confidential information contained therein, through physical or cyber attacks or other means;means, and impacts from required or voluntary public and other disclosures related thereto;

•the Company’s ability to obtain permits and other approvals for projects and construction, update, redesign and/or replacement of various water and wastewater facilities;

•changes in the Company’s capital requirements;

•the Company’s ability to control operating expenses and to achieve operating efficiencies;efficiencies, and the Company’s ability to create, maintain and promote initiatives and programs that support the affordability of the Company’s regulated utility services;

•the intentional or unintentional actions of a third party, including contamination of the Company’s water supplies or the water provided to its customers;

•the Company’s ability to obtain and have delivered adequate and cost-effective supplies of pipe, equipment (including personal protective equipment), chemicals, electricity,power and other fuel, water and other raw materials;materials, and to address or mitigate supply chain constraints that may result in delays or shortages in, as well as increased costs of, supplies, products and materials that are critical to or used in the Company’s business operations;

•the Company’s ability to successfully meet its operational growth projections, for the Regulated Businesses and the Market-Based Businesses (each as defined in this Form 10-K), either individually or in the aggregate, and capitalize on growth opportunities, including, among other things, with respect to:

•acquiring, closing and successfully integrating regulated operations and market-based businesses;operations;

•the Company’s Military Services Group (“MSG”) entering into new military installation contracts, price redeterminations, and other agreements and contracts, with or otherwise obtaining, new customers or partnerships in the Market-Based Businesses;U.S. government; and

•realizing anticipated benefits and synergies from new acquisitions;

•risks and uncertainties following the completion of the sale of the Company’s Homeowner Services Group (“HOS”), including:

•the Company’s ability to receive amounts due, payable and owing to the Company under the amended secured seller note when due; and

•the ability of the Company to redeploy successfully and timely the net proceeds of this transaction into the Company’s Regulated Businesses;

•risks and uncertainties associated with contracting with the U.S. government, including ongoing compliance with applicable government procurement and security regulations;

•cost overruns relating to improvements in or the expansion of the Company’s operations;

•the Company’s ability to successfully develop and implement new technologies and to protect related intellectual property;

•the Company’s ability to maintain safe work sites;

•the Company’s exposure to liabilities related to environmental laws and regulations, including those enacted or adopted and under consideration, and the substances related thereto, including without limitation lead and galvanized steel, PFAS and other contaminants of emerging concern, and similar matters resulting from, among other things, water and wastewater service provided to customers;

•the ability of energy providers, state governments and other third parties to achieve or fulfill their GHG emission reduction goals, including without limitation through stated renewable portfolio standards and carbon transition plans;

•changes in general economic, political, business and financial market conditions, including without limitation conditions and collateral consequences associated with the current pandemic health event resulting from COVID-19;conditions;

•access to sufficient debt and/or equity capital on satisfactory terms and when and as needed to support operations and capital expenditures;

•fluctuations in inflation or interest rates;rates, and the Company’s ability to address or mitigate the impacts thereof;

•the ability to comply with affirmative or negative covenants in the current or future indebtedness of the Company or any of its subsidiaries, or the issuance of new or modified credit ratings or outlooks by credit rating agencies with respect to the Company or any of its subsidiaries (or any current or future indebtedness thereof), which could increase financing costs or funding requirements and affect the Company’s or its subsidiaries’ ability to issue, repay or redeem debt, pay dividends or make distributions;

•fluctuations in the value of, or assumptions and estimates related to, its benefit plan assets and liabilities, including with respect to its pension and other post-retirement benefit plans, that could increase the Company’s costexpenses and plan funding requirements;

•changes in federal or state general, income and other tax laws, including (i) future significant tax legislation (ii) further rules,or regulations interpretations and guidance by the U.S. Department of the Treasury and state or local taxing authorities (collectively, the “Related Interpretations”)(including without limitation impacts related to the enactment of the Tax CutsCorporate Alternative Minimum Tax), and Jobs Act of 2017 (the “TCJA”), (iii)(ii) the availability of, or the Company’s compliance with, the terms of applicable tax credits and tax abatement programs, and (iv) the Company’s ability to utilize its U.S. federal and state income tax net operating loss (“NOL”) carryforwards;programs;

•migration of customers into or out of the Company’s service territories;territories and changes in water and energy consumption resulting therefrom;

•the use by municipalities of the power of eminent domain or other authority to condemn the systems of one or more of the Company’s utility subsidiaries, including without limitation litigation and other proceedings with respect to the water system assets of the Company’s California subsidiary (“Cal Am”) located in Monterey, California (the “Monterey system assets”), or the assertion by private landowners of similar rights against such utility subsidiaries;

•any difficulty or inability to obtain insurance for the Company, its inability to obtain insurance at acceptable rates and on acceptable terms and conditions, or its inability to obtain reimbursement under existing or future insurance programs and coverages for any losses sustained;

•the incurrence of impairment charges, changes in fair value and other adjustments related to the Company’s goodwill or the value of its other assets;

•labor actions, including work stoppages and strikes;

•the Company’s ability to retain and attract highly qualified employees;and skilled employees and/or diverse talent;

•civil disturbances or unrest, or terrorist threats or acts, or public apprehension about future disturbances, unrest, or terrorist threats or acts; and

•the impact of new, and changes to existing, accounting standards.

These forward-looking statements are qualified by, and should be read together with, the risks and uncertainties set forth above and the risk factors included in Item 1A—Risk Factors and other statements contained in this Annual Report on Form 10-K, and readers should refer to such risks, uncertainties and risk factors in evaluating such forward-looking statements. Any forward-looking statements the Company makes shall speak only as of the date this Annual Report on Form 10-K was filed with the U.S. Securities and Exchange Commission (“SEC”). Except as required by the federal securities laws, the Company does not have any obligation, and it specifically disclaims any undertaking or intention, to publicly update or revise any forward-looking statements, whether as a result of new information, future events, changed circumstances or otherwise. New factors emerge from time to time, and it is not possible for the Company to predict all such factors. Furthermore, it may not be possible to assess the impact of any such factor on the Company’s businesses, either viewed independently or together, or the extent to which any factor, or combination of factors, may cause results to differ materially from those contained in any forward-looking statement. The foregoing factors should not be construed as exhaustive.

PART I

ITEM 1. BUSINESS

The Company

With a history dating back to 1886, American Water is the largest and most geographically diverse, publicly-traded water and wastewater utility company in the United States, as measured by both operating revenues and population served. A holding company originally incorporated in Delaware in 1936, the Company employs approximately 7,0006,500 professionals who provide drinking water, wastewater and other related services to over 1514 million people in 4624 states. The Company conducts the majority of its business through regulated utilities that provide water and wastewater services, collectively presented as one reportable segment, referred to as the “Regulated Businesses.” The Company also operates market-basedother businesses that provide complementary services.water and wastewater services to the U.S. government on military installations, as well as municipalities. Individually, these other businesses do not meet the criteria of a reportable segment in accordance with generally accepted accounting principles in the United States (“GAAP”), and are collectively presented as the “Market-Based Businesses,throughout this Annual Report on Form 10-K within “Other,” which is consistent with how management assesses the results of these businesses.

Throughout this Annual Report on Form 10-K, unless the context otherwise requires, references to “we,” “us,” “our,” the “Company,” and “American Water” mean American Water Works Company, Inc. and its subsidiaries, taken together as a whole. References to “parent company” mean American Water Works Company, Inc., without its subsidiaries.

Regulated Businesses

The Company’s primary business involves the ownership of utilities that provide water and wastewater services to residential, commercial, industrial, public authority, fire service and sale for resale customers. The Company’s utilities operate in overapproximately 1,700 communities in 1614 states in the United States, with 3.5 million active customers in its water and wastewater networks. Services provided by the Company’s utilities are subject to regulation by multiple state utility commissions or other entities engaged in utility regulation, collectively referred to as public utility commissions (“PUCs”). Federal, state and local governments also regulate environmental, health and safety, and water quality and water accountability matters. The Company reports the results of the services provided by its utilities in the Regulated Businesses segment. Operating revenues for the Regulated Businesses were $3,255$3,920 million for 2020, $3,0942023, $3,505 million for 20192022 and $2,984$3,384 million for 2018,2021, accounting for 86%93%, 86%92% and 87%86%, respectively, of the Company’s total operating revenues for the same periods.

Presented in the table below is a geographic summary of the Regulated Businesses’ operating revenues and the number of customers the Company serves, by type of service, for and as of the year ended December 31, 2020:2023:

| | Operating Revenues (in millions) | | | Operating Revenues (in millions) | | Number of Customers (in thousands) |

| | Operating Revenues (in millions) | | Number of Customers (in thousands) | | Water (a) | | Wastewater | | Total | | % of Total | | Water | | Wastewater | | Total | | % of Total |

| | Water (a) | | Wastewater | | Total | | % of Total | | Water | | Wastewater | | Total | | % of Total |

| Pennsylvania | | Pennsylvania | $ | 810 | | | $ | 155 | | | $ | 965 | | | 24.6 | % | | 683 | | | 98 | | | 781 | | | 22.4 | % |

| New Jersey | New Jersey | $ | 753 | | | $ | 43 | | | $ | 796 | | | 24.5 | % | | 657 | | | 55 | | | 712 | | | 20.4 | % | New Jersey | 908 | | | 57 | | 57 | | | 965 | | 965 | | | 24.6 | | 24.6 | % | | 668 | | | 64 | | 64 | | | 732 | | 732 | | | 21.0 | | 21.0 | % |

| Pennsylvania | 663 | | | 70 | | | 733 | | | 22.5 | % | | 673 | | | 77 | | | 750 | | | 21.6 | % |

| Missouri | Missouri | 335 | | | 11 | | | 346 | | | 10.6 | % | | 472 | | | 15 | | | 487 | | | 13.9 | % | Missouri | 430 | | | 20 | | 20 | | | 450 | | 450 | | | 11.5 | | 11.5 | % | | 483 | | | 24 | | 24 | | | 507 | | 507 | | | 14.5 | | 14.5 | % |

| Illinois | Illinois | 293 | | | 32 | | | 325 | | | 10.0 | % | | 292 | | | 68 | | | 360 | | | 10.3 | % | Illinois | 366 | | | 61 | | 61 | | | 427 | | 427 | | | 10.9 | | 10.9 | % | | 299 | | | 72 | | 72 | | | 371 | | 371 | | | 10.6 | | 10.6 | % |

| California | California | 247 | | | 3 | | | 250 | | | 7.7 | % | | 183 | | | 3 | | | 186 | | | 5.3 | % | California | 300 | | | 4 | | 4 | | | 304 | | 304 | | | 7.8 | | 7.8 | % | | 190 | | | 3 | | 3 | | | 193 | | 193 | | | 5.5 | | 5.5 | % |

| Indiana | 234 | | | 2 | | | 236 | | | 7.3 | % | | 318 | | | 2 | | | 320 | | | 9.2 | % |

| West Virginia | 164 | | | 1 | | | 165 | | | 5.1 | % | | 168 | | | 1 | | | 169 | | | 4.8 | % |

Total—Top Seven States (b) | 2,689 | | | 162 | | | 2,851 | | | 87.7 | % | | 2,763 | | | 221 | | | 2,984 | | | 85.5 | % |

Total—Top Five States (b) | | Total—Top Five States (b) | 2,814 | | | 297 | | | 3,111 | | | 79.4 | % | | 2,323 | | | 261 | | | 2,584 | | | 74.1 | % |

Other (c) | Other (c) | 381 | | | 23 | | | 404 | | | 12.3 | % | | 481 | | | 31 | | | 512 | | | 14.5 | % | Other (c) | 779 | | | 30 | | 30 | | | 809 | | 809 | | | 20.6 | | 20.6 | % | | 865 | | | 37 | | 37 | | | 902 | | 902 | | | 25.9 | | 25.9 | % |

| Total Regulated Businesses | Total Regulated Businesses | $ | 3,070 | | | $ | 185 | | | $ | 3,255 | | | 100.0 | % | | 3,244 | | | 252 | | | 3,496 | | | 100.0 | % | Total Regulated Businesses | $ | 3,593 | | | $ | | $ | 327 | | | $ | | $ | 3,920 | | | 100.0 | | 100.0 | % | | 3,188 | | | 298 | | 298 | | | 3,486 | | 3,486 | | | 100.0 | | 100.0 | % |

(a)Includes other operating revenues consisting primarily of miscellaneous utility charges, fees and rents.

(b)The Company’s “Top SevenFive States” are determined based upon operating revenues.

(c)Includes the Company’s utility operations in the following states: Georgia, Hawaii, Indiana, Iowa, Kentucky, Maryland, Michigan, New York, Tennessee, Virginia and West Virginia and other revenue attributable collectively to the Regulated Businesses.

Customers

The Company’s Regulated Businesses have a large and geographically diverse customer base. A customer is defined as a person, business, municipality or any other entity that purchases the Company’s water or wastewater services as of the last business day of a reporting period. One single customer may purchase the Company’s services for use by multiple individuals or businesses. Examples of these customers are homes, apartment complexes, businesses and governmental entities.

The vast majority of the Company’s regulated water customers are metered, which allows the Company to measure and bill for its customers’ water usage, typically on a monthly basis. The Company employs a variety of methods of customer meter reading to monitor consumption. These methods range from meters with mechanical registers where consumption is manually recorded by meter readers, to meters with electronic registers capable of transmitting consumption data to proximity devices or via radio frequency to mobile or fixed network data collectors. The Company’s wastewater customers are billed either a flat rate or based upon their water consumption.

Residential customers make up a substantial portion of the Company’s customer base in all of the states in which it operates. The Company also serves (i) commercial customers, such as food and beverage providers, commercial property developers and proprietors, and energy suppliers, (ii) fire service customers, where the Company supplies water through its distribution systems to public fire hydrants for firefighting purposes and to private fire customers for use in fire suppression systems in office buildings and other facilities, (iii) industrial customers, such as large-scale manufacturers, mining and production operations, (iv) public authorities, such as government buildings and other public sector facilities, including schools and universities, and (v) other utilities and community water and wastewater systems in the form of bulk contracts for the supply of water or the treatment of wastewater for their own customers.

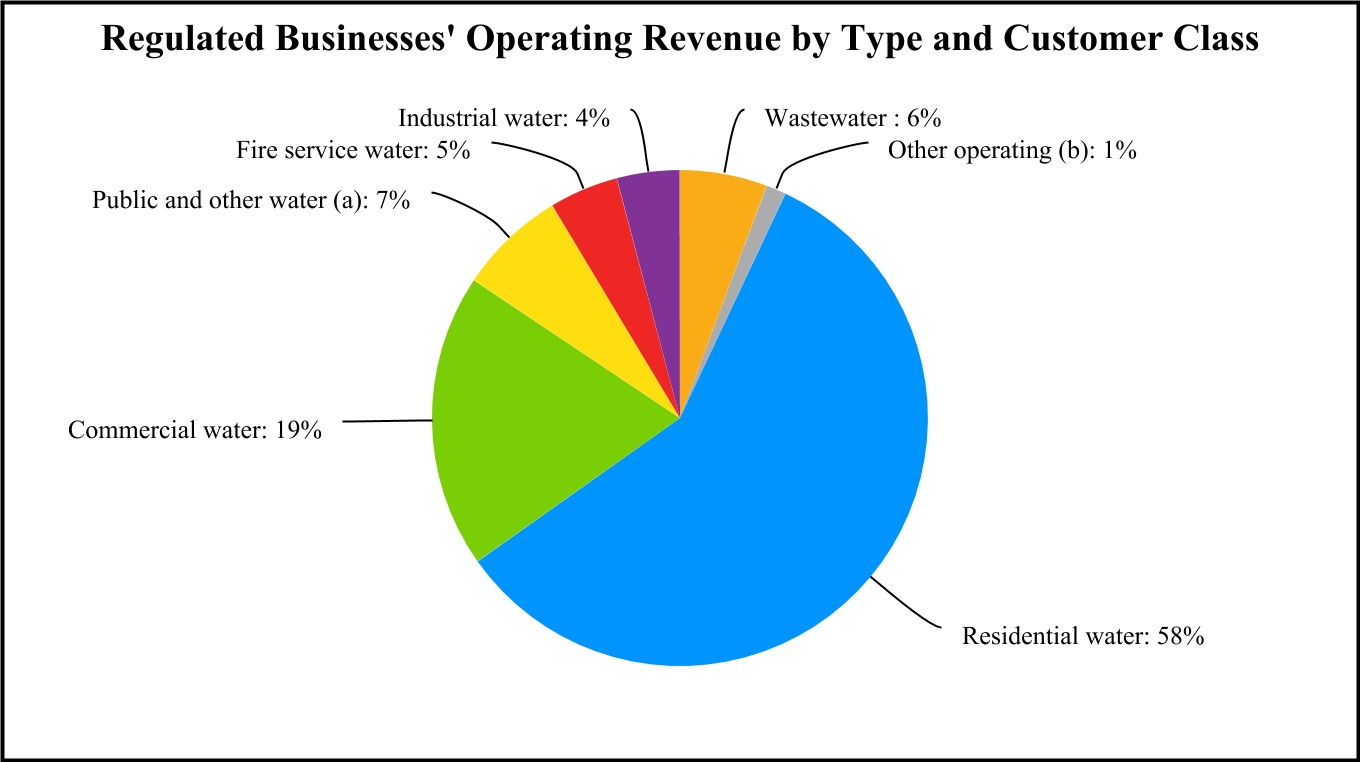

The following chart depictsPresented in the allocationtable below is a breakout of the Company’s Regulated Businesses’ operating revenue of $3,255 million by type, including a breakout of the total water services revenues by class of customer, for the yearyears ended December 31, 2020:2023, 2022 and 2021:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 2023 | | 2022 | | 2021 |

| (In millions) | Revenue | | Percentage of Revenue | | Revenue | | Percentage of Revenue | | Revenue | | Percentage of Revenue |

| Water services: | | | | | | | | | | | |

| Residential | $ | 2,143 | | | 55 | % | | $ | 1,941 | | | 55 | % | | $ | 1,935 | | | 57 | % |

| Commercial | 798 | | | 20 | % | | 710 | | | 20 | % | | 676 | | | 20 | % |

| Fire service | 158 | | | 4 | % | | 147 | | | 4 | % | | 151 | | | 5 | % |

| Industrial | 167 | | | 4 | % | | 153 | | | 4 | % | | 141 | | | 4 | % |

| Public and other water (a) | 284 | | | 7 | % | | 267 | | | 8 | % | | 239 | | | 7 | % |

| Wastewater | 327 | | | 8 | % | | 242 | | | 7 | % | | 208 | | | 6 | % |

| Other (b) | 43 | | | 2 | % | | 45 | | | 2 | % | | 34 | | | 1 | % |

| Total | $ | 3,920 | | | 100 | % | | $ | 3,505 | | | 100 | % | | $ | 3,384 | | | 100 | % |

(a)Includes water revenues from public authorities and other utilities, and community water systems under bulk contracts.contracts and alternative revenue programs.

(b)Includes other operating revenues consisting primarily of miscellaneous utility charges, fees and rents.

Presented in the table below is the number of water and wastewater customers the CompanyCompany’s Regulated Businesses’ served by class of customer as of December 31, 2020, 20192023, 2022 and 2018,2021, which represents approximately 1514 million people served as of December 31, 2020:2023:

| | | | 2020 | | 2019 | | 2018 | | 2023 | | 2022 | | 2021 |

| (In thousands) | (In thousands) | Water | | Wastewater | | Water | | Wastewater | | Water | | Wastewater | (In thousands) | Water | | Wastewater | | Water | | Wastewater | | Water | | Wastewater |

| Residential | Residential | 2,948 | | | 236 | | | 2,914 | | | 215 | | | 2,892 | | | 188 | |

| Commercial | Commercial | 225 | | | 15 | | | 222 | | | 13 | | | 222 | | | 11 | |

| Fire service | Fire service | 50 | | | — | | | 49 | | | — | | | 48 | | | — | |

| Industrial | Industrial | 4 | | | — | | | 4 | | | — | | | 4 | | | — | |

Public and other (a) | Public and other (a) | 17 | | | 1 | | | 16 | | | 1 | | | 16 | | | 1 | |

| Total | 3,244 | | | 252 | | | 3,205 | | | 229 | | | 3,182 | | | 200 | |

| Total (b) | |

(a)Includes public authorities and other utilities and community water and wastewater systems under bulk contracts. Bulk contracts, which are accounted for as a single customer in the table above, generally result in service to multiple customers.

(b)The Company completed the sale of its New York subsidiary on January 1, 2022 and the sale of its Michigan subsidiary on February 4, 2022.

Customer growth in the Company’s Regulated Businesses is primarily from (i) adding new customers to its customer base through acquisitions of water and/or wastewater utility systems, (ii) population growth in its authorized service areas, and (iii) sale of water to other water utilities and community water systems.

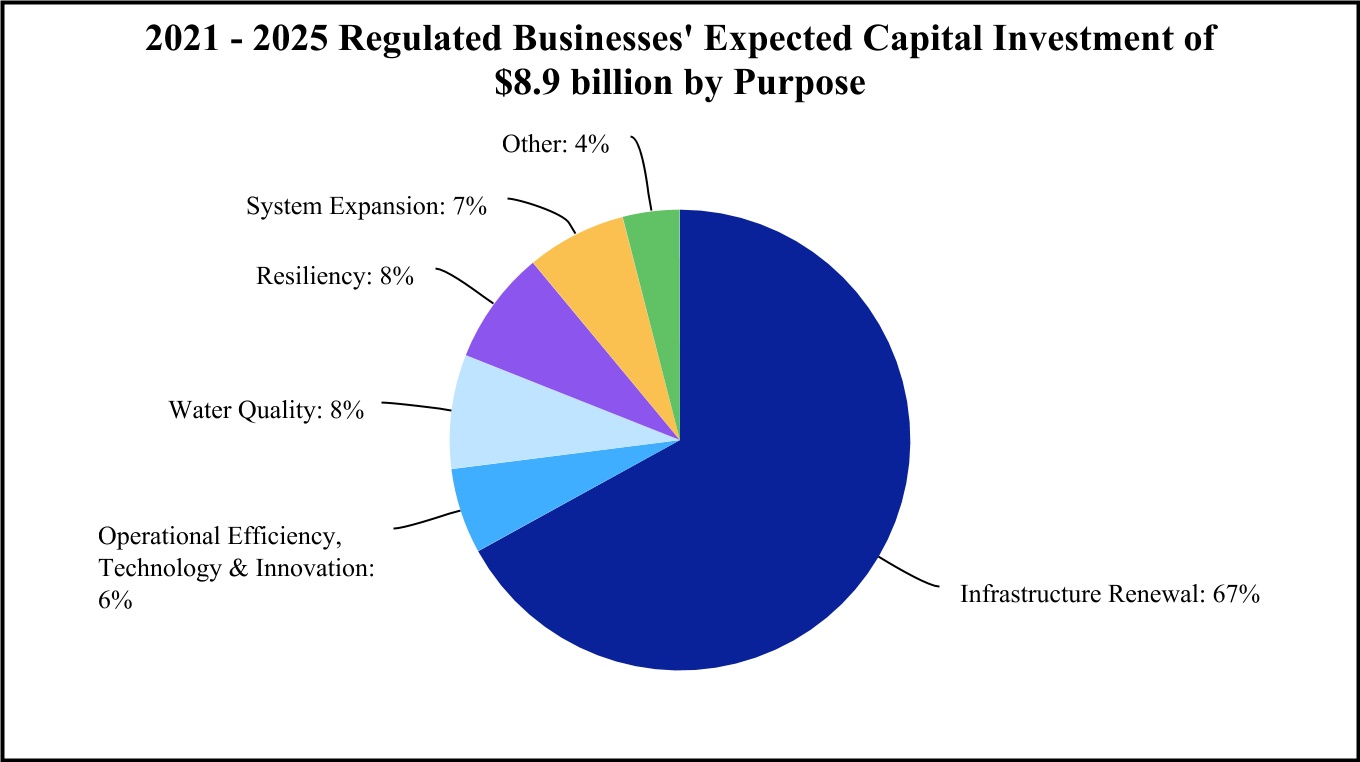

Capital Investment

The Company plans to invest between $22$34 billion and $25$38 billion over the next 10 years including acquisitions, for capital improvements, including acquisitions, to its Regulated Businesses’ water and wastewater infrastructure, largely for pipe replacement and upgrading aging water and wastewater treatment facilities. The Company has proactively improved its pipe renewal rate from a 250-year replacement cycle in 2009 to an expected 110-yearapproximate 125-year replacement cycle by 2025,2028, which it anticipates will enable the Company to replace nearly 2,2002,000 miles of mains and collection pipes between 20212024 and 2025.2028. In addition, from 20212024 to 2025,2028, the Company’s capital investment in treatment plants, storage tanks and other key, above-ground facilities is expected to increase, further addressingseeking to address infrastructure renewal, resiliency, water quality, operational efficiency, technology and innovation, and emerging regulatory compliance needs. Additionally, theThe Company continues to invest significantly in resiliency projects to address the impacts of climate and weather variability by hardening its assets. Recently completed projects include a $15 million emergency power generation system installation at New Jersey’s Raritan Millstone Water Treatment Plant which provides automated standby power in the event of a power failure, and $23 million and $27 million Water Treatment Plant Improvement projects to retire obsolete pumping and water treatment facilities located in 100-year floodplains in both Muncie and Richmond, Indiana, respectively.

Regulation and Rate Making

The operations of the Company’s Regulated Businesses are generally subject to regulation by PUCs in the states in which they operate, with the primary responsibility of the PUCs being the promotion of the overall public interest by balancing the interest of customers and utility investors. Specific authority might differ from state to state, but in most states, PUCs review and approve rates charged to customers, accounting treatments, long-term financing programs and cost of capital, operation and maintenance (“O&M”) expenses, capital expenditures, taxes, affiliated transactions and relationships, reorganizations, mergers and acquisitions, and dispositions, along with imposing certain penalties or granting certain incentives. Regulatory policies vary from state to state and can change over time. These policies will affect the timing, as well as the extent, of recovery of expenses and the realized return on invested capital.

Periodic changes in customer rates generally occur through the filing of a rate case by the utility with the PUC. The timing of rate case filings is typically determined by either periodic requirements in the regulatory jurisdiction or by the utility’s need to increase its revenue requirement to recover capital investment costs, changes in operating revenues, operating costs or other market conditions. The Company attempts to minimize “regulatory lag,” which is the time between the occurrence of an event that triggers a change in the utility’s revenue requirement and the recognition in rates of that change.

The Company’s Regulated Businesses support regulatory practices at the PUCs and state legislatures that mitigate the adverse impact of regulatory lag. Presented in the table below are examples of approved regulatory practices:

| | | | | | | | | | | | | | |

| Regulatory Practices | | Description | | States Allowed |

| Infrastructure replacement surcharge mechanisms | | Allows rates to change periodically, outside a general rate case proceeding, to reflect recovery of capital investments made to replace infrastructure necessary to sustain safe and reliable services for the Company’s customers. These mechanisms typically involve periodic filings and reviews to ensure transparency. | | IA, IL, IN, KY, MO, NJ, NY, PA, TN, VA, WV |

| Future test year | | A “test year” is a period used for setting rates, and a future test year describes the first 12 months that new rates are proposed to be effective. The use of a future test year allows current or projected revenues, expenses and capital investments to be collected on a more timely basis. | | CA, HI, IA, IL, IN, KY, NY, PA, TN, VA |

| Hybrid test year | | A historical test year sets rates using data from a 12-month period that ends prior to a general rate case filing. A hybrid test year allows an update to historical data for “known and measurable” changes that occur subsequent to the historical test year. | | MD, MO, NJ, WV |

| Utility plant recovery mechanisms | | Allows recovery of the full return on utility plant costs during the construction period, instead of capitalizing an allowance for funds used during construction (“AFUDC”). In addition, some states allow the utility to seek pre-approval of certain capital projects and associated costs. In this pre-approval process, the PUC may assess the prudency of such projects. | | CA, IL, KY, NY, PA, TN, VA |

| Expense mechanisms | | Allows changes in certain operating expenses, which may fluctuate based on conditions beyond the utility’s control, to be recovered outside of a general rate case proceeding or deferred until the next general rate case proceeding. | | CA, HI, IL, IN, MD, MO, NJ, NY, PA, TN, VA |

| Revenue stability mechanisms | | Adjusts rates periodically to ensure that a utility recovers the revenues authorized in its general rate case, regardless of sales volume, including recognition of declining sales resulting from reduced consumption, while providing an incentive for customers to use water more efficiently. | | CA, IL NY |

| Consolidated tariffs | | Use of a unified rate structure for water systems owned and operated by a single utility, which may or may not be physically interconnected. The consolidated tariff pricing structure may be used fully or partially in a state, and is generally used to moderate the price impact of periodic fluctuations in local costs, while lowering administrative costs for customers. Pennsylvania and West Virginia also permitspermit a blending of water and wastewater revenue requirements. | | CA, IA, IL, IN, KY, MD, MO, NJ, NY, PA, VA, WV |

| Deferred accounting | | A regulators’regulator’s willingness to defer recognition of financial impacts when setting rates for utilities. | | All |

The Company pursues enhancements to these regulatory practices to facilitate efficient recovery of its costs and capital investments and to continue to provide safe, clean, reliable and affordable services to its customers. The ability to seek regulatory treatment using the regulatory practices described above does not guarantee that the PUCs will accept the Company’s proposal in the context of a particular rate case, and these regulatory practices may reduce, but not eliminate, regulatory lag associated with traditional rate making processes. It is also the Company’s strategy to expand the use of these mechanisms in areas where they may not currently apply and enhance certain mechanisms where they already exist.

Acquisitions and Strategic Growth

The U.S. water and wastewater industries include investor-owned systems as well as municipal systems that are owned and operated by local governments or governmental subdivisions. According to the most recent study by the U.S. Environmental Protection Agency (“EPA”), as of 2017, approximately 84% of the water market is served by municipal systems and approximately 98% of the country’s wastewater systems are government owned. The EPA also estimates, as of 2017, that there are approximatelyover 50,000 community water systems and approximatelyover 15,000 community wastewater systems in the United States, with approximately 80% of the community water systems serving a population of 3,000 or less.

A fundamental aspect of the Company’s growth strategy is to pursue acquisitions of water and/or wastewater systems in geographic proximity to areas where the Company operates its Regulated Businesses.Businesses, see Item 7—Management’s Discussion and Analysis of Financial Condition and Results of Operations for additional information. The proximity of acquisition opportunities to the Company’s regulated footprint allows it to integrate and manage the acquired systems and operations primarily using the Company’s existing management (although the Company typically retains the majority, if not all, of the employees of the acquired systems) and to achieve operational efficiencies and prioritize capital investment needs. The Company’s current customer mix of 93%91% water and 7%9% wastewater also presents strategic opportunities for wastewater growth and systems consolidation, allowing the Company to add wastewater customers where it already serves water customers. The Company intends to continue to expand its regulated footprint geographically by acquiring water and wastewater systems in its existing markets and, if appropriate, pursuing acquisition opportunities in certain domestic markets where the Company does not currently operate its Regulated Businesses. Before entering new regulated markets, the Company will evaluate the business and regulatory climates to ensure that it will have the opportunity to achieve an appropriate rate of return on its investment while maintaining its high standards for providing safe, reliable and affordable services to its customers, as well ascustomers. The Company will also evaluate whether there is a line of sight to grow the Company’s base customers to sufficient scale in a new regulated market so that it can attain efficiencies and promote customer affordability after entering thea new domestic market.

Increasingly stringent environmental, health and safety, cybersecurity and water quality and water accountability regulations, the amount of infrastructure in need of significant capital investment, financial challenges and industry legislation are several elements, among others, that may drive more municipalities to consider selling their water and wastewater assets.

Sale of New York American Water Company, Inc.

On November 20, 2019,January 1, 2022, the Company andcompleted the Company’spreviously disclosed sale of its regulated utility operations in New York subsidiary entered into a Stock Purchase Agreement (the “Stock Purchase Agreement”) with Liberty Utilities Co. which it subsequently assigned to its indirect, wholly owned subsidiary Liberty Utilities (Eastern Water Holdings) Corp. (“Liberty”), pursuant to whichan indirect, wholly owned subsidiary of Algonquin Power & Utilities Corp. Liberty will purchasepurchased from the Company all of the capital stock of the Company’s New York subsidiary (the “Stock Purchase”) for an aggregatea purchase price of approximately $608 million in cash, subject to adjustment as provided in the Stock Purchase Agreement.cash. The Company’s regulated New York operations haverepresented approximately 125,000127,000 customers in the State of New York. Algonquin Power & Utilities Corp., Liberty’s ultimate parent company, executed and delivered an absolute and unconditional guaranty of the performance of the obligations of Liberty under the Stock Purchase Agreement. The Stock Purchase is subject to various conditions, including obtaining approvals and satisfying or waiving other closing conditions. The Stock Purchase Agreement has an initial termination date of June 30, 2021. Either party may extend the agreement beyond June 30, 2021, and the Company intends to extend the agreement, if necessary, provided all of the conditions to closing have been or are capable of being met, other than obtaining regulatory approvals. If not otherwise extended, the ultimate termination date is December 31, 2021. Liberty may also terminate the Stock Purchase Agreement if any governmental authority initiates a condemnation or eminent domain proceeding against a majority of the consolidated properties of the New York subsidiary, taken as a whole.

In the fourth quarter of 2020, the Governor of New York proposed legislation that, among other things, requires the New York State Department of Public Service (“NYSDPS”) to study whether private water suppliers should be placed under municipal control. On February 3, 2021, the Governor issued a press release announcing that he directed the NYSDPS Special Counsel to commence and lead a municipalization feasibility study to be completed by April 1, 2021. Meanwhile, the Company’s New York subsidiary continues to work constructively with the NYSDPS and is taking the actions necessary to complete the Stock Purchase. Subject to satisfying or waiving the various conditions to closing, and assuming no prior termination of the Stock Purchase Agreement by Liberty as described above, the Company remains confident that the Stock Purchase will be completed, though the date of the close of the transaction could be impacted by the timing of the work to be completed by the NYSDPS Special Counsel.

Industry Legislation

In 2017, New Jersey enacted2020 and 2021, the Water Quality AccountabilityUnited States Congress passed, and the President signed into law, legislation with water and wastewater provisions including the Infrastructure Investment and Jobs Act (the “WQAA”“IIJA”), which sets operational standardsthe Consolidated Appropriations Act of 2021 and the American Rescue Plan of 2021. The legislation provided funding for alla variety of initiatives to support water utilitiesand wastewater infrastructure, lead service line replacement, treatment of PFAS and other contaminants of emerging concern, and low-income water assistance (“LIHWAP”). LIHWAP expired in 2023.

The Company’s regulated subsidiaries in New Jersey, including municipalIndiana, and investor-ownedMissouri have versions of water quality or safety accountability acts which require operational or safety and security standards for water and wastewater utilities with more than 500 service connections. Thisserving a certain number of customers. In New Jersey, the law imposes requirements in areas such as cybersecurity, asset management, water quality reporting, remediation of notices of violation, and hydrant and valve maintenance. The WQAAmaintenance and cybersecurity. In Indiana, the law requires water and wastewater utilities to conduct rate analyses, develop capital asset management plans and conduct cybersecurity and water loss audits. In Missouri, the most senioract requires water manager, or either the executive director for municipal utility authorities or the mayor or chief executive officer for municipally owned public water systems,and wastewater utilities to certify that the system meets the requirements under the WQAA. In an effort to strengthen accountability under the WQAA, the New Jersey Senate held three hearings on the WQAA during 2020. The New Jersey Assembly has also heard legislation to strengthen the WQAA in one committee,create cybersecurity, valve inspection and referral to the Assembly Appropriations Committee is pending.hydrant inspection programs.

The Company’s regulated subsidiaries in California, Illinois, Indiana, Iowa, Kentucky, Maryland, Missouri, New Jersey, Pennsylvania, Tennessee, Virginia and West Virginia have access to fair market valueutility valuation legislation and regulation for private sector investment in public sector water and wastewater systems. The Company supports full optionality for municipalities, including state legislation that enables the consolidation of the largely fragmented water and wastewater industries through third-party fair market valuations of purchased property. Fair market value assessment of water and wastewater systems is an alternative to the traditional depreciated original cost method of valuation, which allows the Company to offer municipalities a purchase price for their system assets that is reflective of the assets’ fair market value, while providing the Company with increased opportunity to recover the purchase price over the life of the purchased system assets, subject to PUC approval.

In 2020, legislation in Indiana was passed2021, the Tennessee Public Utility Commission implemented acquisition valuation rules that created an appraisal processinclude a methodology to establish fair value for non-municipal utilities and a presumption that a purchase price not exceeding the appraised value is reasonable. That legislation also requires that all new municipal water and wastewater systems are subject toassets based upon the jurisdictionnew replacement cost of the utility regulatory commission for ten years. Separate legislation authorizes recovery for above ground infrastructure, without a full rate case, for service enhancements that are completed for health, safety or environmental concerns. That same legislation also removed relocations completed for road construction fromassets less the distribution system improvement charge recovery caps.depreciation, in addition to other valuation methodology options.

Consolidated tariffs use a unified rate structure for systems owned and operated by a single utility, which may or may not be physically interconnected. Consolidated tariff pricing moderates the impact of periodic fluctuations in local costs and promotes a more universal water infrastructure investment in a state.jurisdiction. As a result, consolidated tariffs can make it easier to incorporate new systems into an existing utility, support economies of scale for even the smallest of systems and prioritize capital needs across the state.jurisdiction. Overall, the Company believes that consolidated tariffs bring cost-effective, high qualityhigh-quality services to a larger number of customers. TwelveEleven of the Company’s regulated jurisdictions currently have some form of consolidated tariff pricing, including California, Illinois, Indiana, Iowa, Kentucky, Maryland, Missouri, New Jersey, New York, Pennsylvania, Virginia and West Virginia.

In 2020, legislation in West Virginia was passed that allows for expanded asset valuation in connection with the acquisition of a utility or utility assets, combined water and wastewater revenue requirements and the expansion of permitted uses by municipalities of proceeds from the sale of a water or wastewater system. The legislation also allows inclusion of contributed property in a system’s asset valuation and rate base recognition for the full purchase price approved by the Public Service Commission of West Virginia.

In December 2020, Congress passed and the President signed into law a $900 billion COVID-19 relief and $1.4 trillion U.S. government appropriations package for 2021, which included $638 million for a low-income water assistance program and $2.8 billion for capitalization grants under the Clean Water and Drinking Water State Revolving Funds. The Company is awaiting further guidance on the distribution of these funds.

Competition

The Company’s Regulated Businesses generally do not face direct competition in their existing markets because (i) the Company operates in those markets pursuant to franchises, charters, certificates of public convenience and necessity or similar authorizations (collectively, “CPCNs”) issued by state PUCs or other authorities, and (ii) the high cost of constructing a new water and wastewater system in an existing market creates a significant barrier to market entry. However, the Company’s Regulated Businesses do face increasing competition from governmental agencies, other investor-owned utilities, large industrial customers with the ability to provide their own water supply/treatment process and strategic buyers that are entering new markets and/or making strategic acquisitions. When pursuing acquisitions, the Company’s largest investor-owned competitors, based on a comparison of operating revenues and population served, include Essential Utilities, Inc. (formerly known as Aqua America, Inc.), Suez North America, American States Water Company and California Water Service Group. From time to time, the Company also faces competition from infrastructure funds, multi-utility companies and others, such as Algonquin Power and Utilities Corp., Eversource Energy, SouthWest Water Company and Corix.Corix Infrastructure, Inc.

Condemnation and Eminent Domain

All or portions of the Regulated Businesses’ utility assets could be acquired by state, municipal or other government entities through one or more of the following methods: (i) eminent domain (also known as condemnation); (ii) the right of purchase given or reserved by a municipality or political subdivision when the original CPCN was granted; and (iii) the right of purchase given or reserved under the law of the state in which the utility subsidiary was incorporated or from which it received its CPCN. The acquisition consideration related to such a proceeding initiated by a local government may be determined consistent with applicable eminent domain law, or may be negotiated or fixed by appraisers as prescribed by the law of the state or inthe jurisdiction of the particular CPCN.

As such, the Regulated Businesses are periodically subject to condemnation proceedings in the ordinary course of business. For example, a citizens group in Monterey, California successfully added “Measure J” to the November 2018 election ballot asking voters to decide whether the Monterey Peninsula Water Management District (the “MPWMD”) should conduct a feasibility study concerning the potential purchase of the Monterey water service system assets (the “Monterey system assets”) of the Company’s California subsidiary and, if feasible, to proceed with(“Cal Am”) are the subject of a purchase of those assets without an additional public vote. This service territory represents approximately 40,000 customers. Inpotential condemnation action by the Monterey Peninsula Water Management District (the “MPWMD”) stemming from a November 2018 Measure J was certified to have passed. In August 2019, the MPWMD’s General Manager issued a report that recommends that the MPWMD board (1) develop criteria to determine which water systems should be considered for acquisition; (2) examine the feasibility of acquiring the Monterey system assets and consider public ownership of smaller systems only if the MPWMD becomes the owner of a larger system; (3) evaluate whether the acquisition of the Monterey system assets by the MPWMD is in the public interest and sufficiently satisfies the criterion of “feasible” as provided in Measure J; (4) ensure there is significant potential for cost savings before agreeing to commence an acquisition; and (5) developballot initiative. For more fully alternate operating plans before deciding whether to consider a Resolution of Necessity.

In November 2019, the MPWMD issued a preliminary valuation and cost of service analysis report, finding in part that (1) an estimate of the Monterey system assets’ total value plus adjustments would be approximately $513 million, (2) the cost of service modeling results indicate significant annual reductions in revenue requirements and projected monthly water bills, and (3) the acquisition of the Monterey system assets by the MPWMD would be economically feasible. On June 12, 2020, the MPWMD issued a draft environmental impact report for the potential acquisition of the Monterey system assets and a related district boundary adjustment that would be required if the MPWMD were to acquire and operate certain of the Monterey system assets located outside the MPWMD’s boundaries. On September 15, 2020, the MPWMD gave notice of its intention to appraise the Monterey system assets and related property interests. On September 29, 2020, the Company’s California subsidiary declined to make the Monterey system assets and related property interests available for inspection or to comply with any of the other requests contained in the MPWMD’s notice. On October 7, 2020, the MPWMD issued a final environmental impact report (“FEIR”), andinformation on November 4, 2020, the MPWMD certified the FEIR, which purports to analyze the environmental impacts of the MPWMD’s project to (1) acquire the Monterey system assets through the power of eminent domain, if necessary, and (2) expand its geographic boundaries to include all parts of this system. On November 25, 2020, the Company’s California subsidiary filed a petition challenging this certification in court. Seematter, see Item 3—Legal Proceedings—ChallengeProposed Acquisition of Certification—Proposed Monterey System Final Environmental Impact Report.

The MPWMD will be required to file an application with the Local Agency Formation Commission of Monterey County (“LAFCO”) seeking approval to become a retail water provider and annex approximately 56 parcels of land into the MPWMD’s boundaries. Approval by LAFCO is a precondition to the MPWMD’s ability to file an eminent domain proceeding against the Company’s California subsidiary to acquire the Monterey system assets. If the MPWMD were to make a final determination that an acquisition of the Monterey system assets is feasible, it would then need to file a multi-year eminent domain proceeding against the Company’s California subsidiary. In that proceeding, it would first need to establish its right to take the Monterey system assets. If such right is established, the amount of just compensation to be paid to the California subsidiary for such assets would then need to be determined.

Also, five municipalities in the Chicago, Illinois area (approximately 30,300 customers in total) formed a water agency and filed an eminent domain lawsuit against the Company’s Illinois subsidiary in January 2013, seeking to condemn the water pipeline that serves those five municipalities. Before filing its eminent domain lawsuit, the water agency made an offer of $38 million for the pipeline. The parties have filed with the court updated valuation reports. Although the date of the valuation trial is not currently scheduled, it is not likely to commence until the second quarter of 2021.Assets — Potential Condemnation.

Furthermore, the law in certain jurisdictions in which the Regulated Businesses operate provides for eminent domain rights allowing private property owners to file a lawsuit to seek just compensation against a public utility, if a public utility’s infrastructure has been determined to be a substantial cause of damage to that property. In these actions, the plaintiff would not have to prove that the public utility acted negligently. In California, for example, lawsuits have been filed in connection with large-scale natural events such as wildfires. Some of these lawsuits have included allegations that infrastructure of certain utilities triggered the natural event that resulted in damage to the property. In some cases, the PUC has allowed certain costs or losses incurred by the utility to be recovered from customers in rates, but in other cases such recovery in rates has been disallowed. Also, the utility may have obtained insurance that could respond to some or all of such losses, although the utility would be at risk for any losses not ultimately subject to rate or insurance recovery or losses that exceed the limits of such insurance.

Water Supply and Wastewater Services

The Company’s Regulated Businesses generally own the physical assets used to store, pump, treat and deliver water to its customers and collect, treat, transport and recycle wastewater. Typically, the Company does not own the water, which is held in public trust and is allocated to the Company through contracts, permits and allocation rights granted by federal and state or multi-state agencies or through the ownership of water rights pursuant to local law. The Company is dependent on defined sources of water supply and obtains its water supply from surface water sources such as reservoirs, lakes, rivers and streams; from groundwater sources, such as wells and aquifers; and water purchased from third-party water suppliers. The level of water treatment the Company applies varies significantly depending upon the quality of the water source and customer stipulations. Surface water sources typically generally require significant treatment, while groundwater sources often require chemical treatment only.

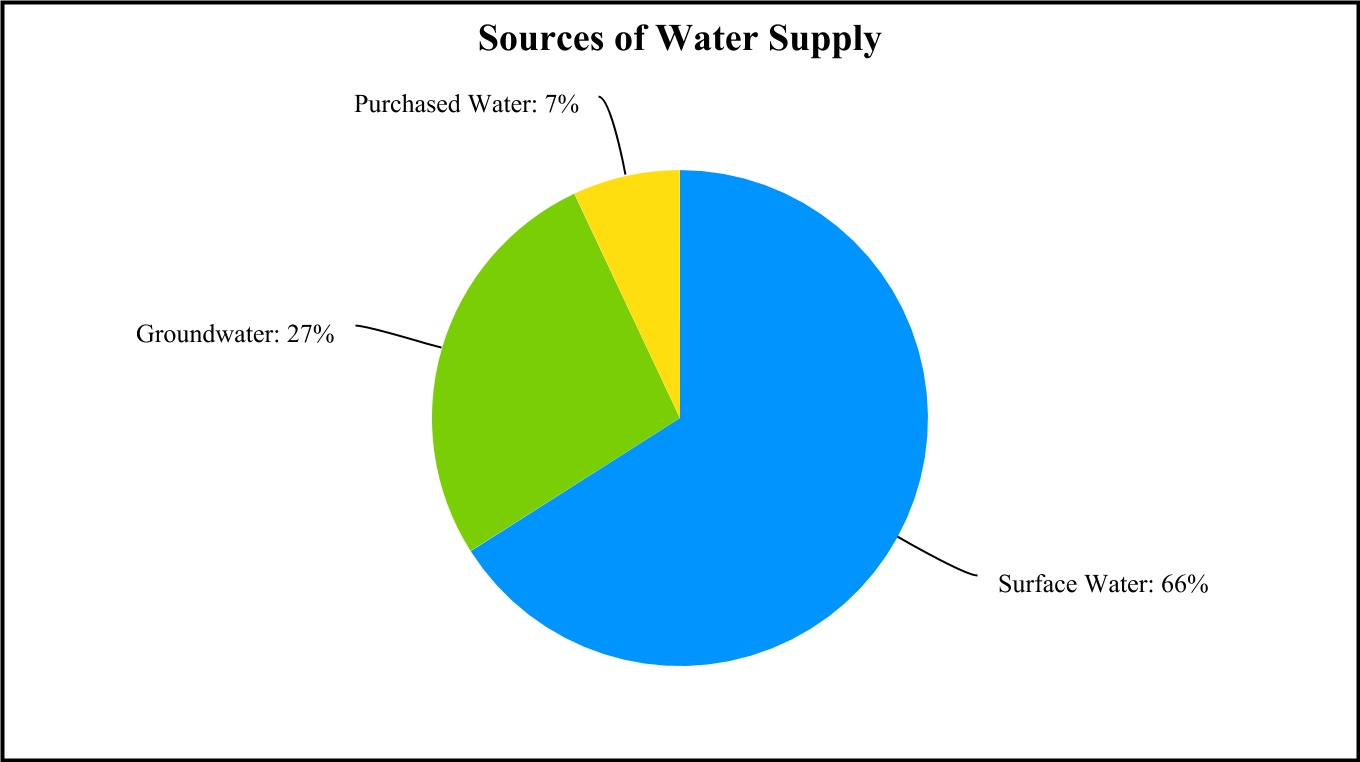

Presented in the chart below are the Company’s sources of water supply as of December 31, 2020:

Presented in the table below are the percentages of water supply by source type for the Company’s Top SevenFive States individually and the Regulated Businesses collectively for the year ended December 31, 2020:2023:

| | | | Surface Water | | Ground Water | | Purchased Water | | Surface Water | | Ground Water | | Purchased Water |

| New Jersey | New Jersey | 72% | | 24% | | 4% | New Jersey | 74% | | 20% | | 6% |

| Pennsylvania | Pennsylvania | 91% | | 7% | | 2% | Pennsylvania | 91% | | 7% | | 2% |

| Missouri | Missouri | 78% | | 21% | | 1% | Missouri | 84% | | 15% | | 1% |

| Illinois | Illinois | 54% | | 35% | | 11% | Illinois | 55% | | 35% | | 10% |

| California | California | — | | 62% | | 38% | California | —% | | 67% | | 33% |

| Indiana | 44% | | 56% | | — |

| West Virginia | 100% | | — | | — |

| Regulated Businesses | | Regulated Businesses | 71% | | 22% | | 7% |

The Company’s ability to meet the existing and future water demands of its customers depends on an adequate water supply. Drought, governmental restrictions, overuse of sources of water, the protection of threatened species or habitats, contamination or other factors may limit the availability of ground and surface water. The Company employs a variety of measures in an effort to obtain adequate sources of water supply, both in the short-term and over the long-term. The geographic diversity of the Company’s service areas may mitigate some of the economic effects on the water supply associated with weather extremes itthe Company might encounter in any particular service territory. For example, in any given summer, some areas may experience drier than average weather, which may reduce the amount of source water available, while other areas the Company serves may experience wetter than average weather.

The Company evaluates quality, quantity, growth needs and alternate sources of water supply as well as transmission and distribution capacity to provide water service to its customers. Water supply is seasonal in nature and weather conditions can have a pronounced effect on supply. In order to ensure that the Company has adequate water supply, it uses long-term planning processes and maintains contingency plans to minimize the potential impact on service caused by climate variability and a wide range of weather fluctuations. The Company reviews current climate science and global models related to temperature, precipitation and sea level rise on an ongoing basis. Where actionable forecasts are available, the Company will use this information in its comprehensive planning studies and asset management plans. These studies and plans, which are used by the Company to develop its asset management and system reliability strategies, assess the climate risk and resiliency of the Company’s water and wastewater systems over short-, medium- and long-term time horizons, and include evaluations of the availability of water supplies and system capacity against a number of different factors, projections and estimates.

In connection with supply planning for most surface or groundwater sources, the Company employs models to determine safe yields under different rainfall and drought conditions. Surface and ground water levels are routinely monitored so that supply capacity deficits may, to the extent possible, be predicted and mitigated through demand management and additional supply development. In California, where the state has recently experienced a multi-year drought, the Company utilizes multiple water supply options including numerous ground water wells in multiple aquifers as well as various long-term purchase water agreements with regional water suppliers to optimize supplies while assuring resiliency during dry years. An example of the Company’s use of long-term planning to ensure that it has adequate water supply is its involvement in the Monterey Peninsula Water Supply Project (the “Water Supply Project”) in California. The Water Supply Project includes the construction of a desalination plant, to be owned by the Company’s California subsidiary,Cal Am, and the construction of wells that would supply water to the desalination plant. In addition, the Water Supply Project also includes the California subsidiary’sCal Am’s purchase of water from a groundwater replenishment project (the “GWR Project”) between Monterey One Water (formerly known as the Monterey Regional Water Pollution Control Agency) and the MPWMD. The Water Supply Project is intended, among other things, to fulfill obligations of the California subsidiaryCal Am to eliminate unauthorized diversions from the Carmel River as required under orders of the California State Water Resources Control Board (the “SWRCB”). For more information, see Item 3—Legal Proceedings—Alternative Water Supply in Lieu of Carmel River Diversions and Note 17—16—Commitments and Contingencies—Contingencies—Alternative Water Supply in Lieu of Carmel River Diversions, in the Notes to the Consolidated Financial Statements.

Wastewater services involve the collection of wastewater from customers’ premises through sewer lines. The wastewater is then transported through a sewer network to a treatment facility, where it is treated to meet required regulatory standards for wastewater before being returned to the environment. The solid waste by-product of the treatment process is disposed of or recycled in accordance with applicable standards and regulations.

Seasonality

Customer demand for the Company’s water service is affected by weather and tends to vary with temperature and amount and frequency of rainfall. Customer demand is generally greater during the warmer months, primarily due to increased water usage for irrigation systems and other outdoor water use. As such, the Company typically expects its operating revenues to be the highest in the third quarter of each year. Weather that is hotterwarmer and/or drier than average generally increases operating revenues, whereas, weather that is cooler and/or wetter than average generally serves to suppresssuppresses customer water demand and can reduce water operating revenues. ThreeTwo of the Company’s jurisdictions, California Illinois and New York,Illinois, have adopted revenue stability mechanisms which permit the Company to collect state PUC-authorized revenue for a given period whichthat is not tied to the volume of water sold during that period, thereby lessening the impact of weather variability. See Regulated Businesses—Regulation—Regulation and Rate Making for additional information regarding revenue stability mechanisms.

Market-Based BusinessesAffordability

The Company supports the United Nations’ declaration of access to clean water and sanitation as a human right, regardless of economic status. As a water utility, the Company’s Market-Based Businesses provide home services primarily to residentialwater must be safe, efficient, reliable, accessible and smaller commercialaffordable. Through increased efficiency, conservation and low-income support programs, on average across the enterprise, the Company consistently achieves water costs that are significantly below the EPA’s suggested guidance of 2% of household income. Succeeding in water affordability positively affects the health and safety of the Company’s customers and contributes to the economic prosperity of the communities in which it operates.

The Company’s approach to water access and affordability consists of two key strategies. The first is to supply water that is safe, reliable and meets the needs of its customers. The second is to provide affordable water services to customers while protecting its customers’ right to clean water, regardless of economic status or geographic location. The Company also focuses on addressing water affordability by maximizing both supply-side and demand-side efficiency. Average residential water bills for the Company’s customers are approximately $55 to $65 per month, and the expected average annual rate increases across the Company’s footprint over the next five years is 5% to 6%. The Company continues to advocate for federal and state customer affordability support and monitors the number of customers enrolled in its assistance programs to make sure that it is effectively responding to customer needs.

Other

Other primarily includes the MSG business, which enters into long-term contracts with the U.S. government to provide water and wastewater services on military installations. The Contract Services Group (“CSG”), also included in Other, has three contracts with municipal customers to operate and manage water and wastewater facilities and provide other related services. Other also includes corporate costs that are not allocated to the U.S. government on military installations, as well as municipalities,Company’s Regulated Businesses, interest income related to the secured seller promissory note from the sale of HOS, income from assets not associated with the Regulated Businesses, eliminations of inter-segment transactions and utility customers. Thesefair value adjustments related to acquisitions that have not been allocated to the Regulated Businesses segment. The businesses included withinOther are not subject to regulation by state PUCs and the services provided generally do not require significant capital investment. Operating revenues for the Company’s Market-Based BusinessesOther were $540$314 million for 2020, $5392023, $287 million for 20192022 and $476$546 million for 2018,2021, accounting for 14%7%, 15%8% and 14%, respectively, of the Company’s total operating revenues for the same periods.

The Company’s primary Market-Based Businesses include the following operating segments:

•Homeowner Services Group (“HOS”), which provides various warranty protection programs and other home services to residential customers;

•Military Services Group (“MSG”), which enters into long-term contracts with the U.S. government to provide water and wastewater services on various military installations.

The Company also has five contracts with municipal customers to operate and manage water and wastewater facilities and provide other related services through its Contract Services Group (“CSG”).

Homeowner Services Group

The Company’s Homeowner Services Group, which includes the operations of Pivotal Home Solutions (“Pivotal”) acquired in June 2018, provides warranty protection programs and other home services to residential customers for interior and exterior water and sewer lines, interior gas and electric lines, heating and cooling systems, water heaters and other home appliances, as well as power surge protection and other related services. The Company develops partnerships with municipalities, utilities and other organizations to offer protection programs to customers serviced by, or affiliated with, those municipalities, utilities and organizations. The term of these partnership agreements with the municipalities, utilities and other organizations is typically three to five years, with mutual optional renewals. As of December 31, 2020, HOS had approximately 3 million customer contracts in 43 states.

Military Services Group

The Company’s Military Services GroupMSG operates on 1718 military installations under 50-year contracts with the U.S. government as part of its Utilities Privatization Program. The scope of these contracts generally includes the operation and maintenance of the installation’s water and wastewater systems and a capital program focused on asset replacement and, in certain instances, systems expansion. The replacement of assets assumed when a contract is awarded to MSG is completed either through a discrete set of projects executed in the first five years of the contract or through the long termlong-term recapitalization program performed over the life of the contract. Traditionally, both of these programs are funded from the contract fee. At times, new assets are required to support the installation’s mission, and the construction of these assets is funded by the U.S. government as separate modifications or amendments to the contract. The capital for these assets historically has not been funded through the Company’s debt or equity issuances; rather, the Company has used limited working capital for short-term needs under these contracts. In April 2018, theThe U.S. Army institutedhas a requirement that a bidder must offer financing in its proposal for these new capital projects under existing contracts, but the U.S. Army’s implementation of this requirement on existing contracts has limited the need for such financing. However, recent U.S. Army and Navy Utilities Privatization solicitations have included requirements for the successful bidder to finance discrete initial capital projects over either a five- or ten-year period after project completion. ThreeFour of MSG’s current contracts require such capital project financing, which the Company is currently addressing through internal sources of liquidity.

The contract price for sixfour of MSG’s contracts with the U.S. government is subject to redetermination two years after commencement of operations, and every three years thereafter. Price redetermination is a contract mechanism to periodically adjust the service fee in the next period, to reflect changes in contract obligations and anticipated market conditions. The remaining 1114 contracts with the U.S. government are subject to annual price adjustments under a mechanism called “Economic Price Adjustment.” All 1718 contracts could be terminated, in whole or in part, prior to the end of the 50-year term for convenience of the U.S. government, or as a result of default or non-performance by the MSG subsidiary performing the contract. In either event, pursuant to termination provisions applicable to all of these contracts, MSG would be entitled to recover allowable costs that it may have incurred under the contract, plus the contract profit margin on incurred costs. MSG’s backlog of revenue associated with its contracts with the U.S. government is approximately $6.2$7.1 billion, with an average remaining contract term of 4139 years.

Sale of Homeowner Services Group

On December 9, 2021 (the “Closing Date”), the Company sold all of the equity interests of the HOS subsidiaries for total consideration of approximately $1.275 billion. Prior to the Closing Date, the Company provided various warranty protection programs and other home services primarily to residential and smaller commercial customers through its HOS operations. See Item 7—Management’s Discussion and Analysis of Financial Condition and Results of Operations and Note 5—Acquisitions and Divestitures in the Notes to Consolidated Financial Statements for additional information.

Competition

The Company’s Market-Based Businesses faceMSG faces competition from a number of service providers, including HomeServe USA and Cinch Home Services in HOS, and American States Water Company Suez North America, and Veolia Environnement S.A. in MSG.

Environmental, Health and Safety, Water Quality and Other Regulation

The Company’s water and wastewater operations, including the services provided by both its Regulated Businesses, MSG and Market-Based Businesses,CSG, are subject to extensive federal, state and local laws and regulations governing the protection of the environment, health and safety, the provision of water and wastewater services, particularly with respect to the quality of water the Company delivers to its customers, and the manner in which it collects, treats, discharges, recycles and disposes of wastewater. In the United States, these regulations are developed under federal legislation including the Safe Drinking Water Act, the Reduction of Lead in Drinking Water Act and the Clean Water Act, and under a variety of applicable state laws. Environmental, health and safety, and water quality regulations are complex and may vary from state to state in those instances where a state has adopted a standard that is more stringent than the federal standard. For example, while the EPA has issued a non-enforceable Health Advisory for the combined level of two perfluorinated compounds (perfluorooctanoic acid, or PFOA, and perfluorooctane sulfonate, or PFOS), the New Jersey Department of Environmental Protection was the first state agency to establish a standard for perfluorononanoic acid, or PFNA, in 2018 and has since established maximum containment levels for PFOA and PFOS, with implementation occurring in January 2021. The Company is also subject to various federal, state, and local laws and regulations governing the storage of hazardous materials, the management and disposal of hazardous and solid wastes, discharges to air and water, the cleanup of contaminated sites, dam safety and other matters relating to the protection of the environment and health and safety. PUCs also set conditions and standards for the water and wastewater services the Company delivers.