UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

(Mark One)

| x | ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended January 31, 20122013

| o | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______________ to ________________

Commission File Number 000-52055

RED METAL RESOURCES LTD.

(Exact name of registrant as specified in its charter)

| Nevada | | 20-2138504 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

195 Park Avenue Thunder Bay, Ontario P7B 1B9

(Address of principal executive offices)

Registrant’s telephone number, including area code: (807) 345-7384

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | | Name of each exchange on which each is registered |

| N/A | | N/A |

Securities registered pursuant to Section 12(g) of the Act: Common Stock, $0.001 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes [ x ] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [ X ] No [ ] .

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company.

| Large accelerated filer [ ] | | Accelerated filer [ ] |

| Non-accelerated filer [ ] | | Smaller reporting company [X] |

| (Do not check if a smaller reporting company) | | |

Indicate by check mark whether the issuer is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. As of July 29, 2011,2012, the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the average bid and asked price of the common equity was $2,270,581.$2,793,881.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. The number of shares of the registrant’s common stock, $0.001 par value per share, outstanding as of March 21, 2012April 17, 2013 was 17,689,634.17,956,969.

GLOSSARY OF SELECTED MINING AND TECHNICAL TERMS | 1 |

| | | |

NOTE ABOUT FORWARD-LOOKING STATEMENTS | 2 |

| | | |

| 23 |

| | |

GENERAL | 2 |

UNPROVED MINERAL PROPERTIES | General | 3 |

| Unproved mineral properties | 4 |

COMPETITION | Competition | 23 |

| Raw materials | 23 |

| Dependence on major customers | 23 |

| Patents/Trademarks/Licenses/Franchises/Concessions/Royalty Agreements/Labor Contracts | 23 |

| Costs and effects of compliance with environmental laws | 24 |

RAW MATERIALS | Expenditures on research and development | 24 |

DEPENDENCE ON MAJOR CUSTOMERS | 25 |

PATENTS/TRADEMARKS/LICENSES/FRANCHISES/CONCESSIONS/ROYALTY AGREEMENTS/LABOR CONTRACTSNumber of total employees and number of full-time employees | 25 |

COSTS AND EFFECTS OF COMPLIANCE WITH ENVIRONMENTAL LAWS | 25 |

EXPENDITURES ON RESEARCH AND DEVELOPMENT | 25 |

NUMBER OF TOTAL EMPLOYEES AND NUMBER OF FULL-TIME EMPLOYEES | 2524 |

| | | |

| 2624 |

| | | |

| 30 |

| | | |

| 30 |

| | | |

| 30 |

| | | |

| 30 |

| | | |

| 30 |

| | |

| 31 |

| | |

ITEM 6: SELECTED FINANCIAL DATA. | 32 |

| |

| 3231 |

| | | |

| 4038 |

| | | |

| 4038 |

| | | |

INDEX TO FINANCIAL STATEMENTS | 40Index to Financial Statements | 38 |

| | | |

| 4139 |

| | | |

| 4139 |

| | | |

| 4240 |

| | | |

| 40 |

| | |

| 42 |

| | |

ITEM 11: EXECUTIVE COMPENSATION | 44 |

| |

| 4644 |

| | | |

| 4644 |

| | |

DIRECTOR INDEPENDENCE | 46 |

TRANSACTIONS WITH RELATED PERSONS | 46Director independence | 44 |

| Transactions with related persons | 45 |

| | | |

| 4847 |

| | | |

| 4948 |

GLOSSARY OF SELECTED MINING AND TECHNICAL TERMS

The following is a glossary of selected mining terms used in the United States and Canada and referenced in this Annual Report on Form 10-K that may be technical in nature:10-K:

Table 1. Glossary

| Term | Definition |

| Ag | Silver |

| Airborne survey | A survey made from an aircraft to obtain photographs, or measure magnetic properties, radioactivity, etc. |

| Assay | A chemical test performed on a sample of ores or minerals to determine the amount of valuable metals contained. |

| Au | Gold |

| Bulk sample | A large sample of mineralized rock, frequently hundreds of tonnes, selected in such a manner as to be representative of the potential mineral deposit (orebody) being sampled and used to determine metallurgical characteristics. |

| By-product | A secondary metal or mineral product recovered in the milling process. |

| Core | The long cylindrical piece of rock, about an inch in diameter, brought to surface by diamond drilling |

| Core sample | One or several pieces of whole or split parts of core selected as a sample for analysis or assay. |

| Cross-cut | A horizontal opening driven from a shaft and (or near) right angles to the strike of a vein or other orebody. The term is also used to signify that a drill hole is crossing the mineralization at or near right angles to it. |

| Cu | Copper |

| Cut-off grade | The lowest grade of mineralized rock that qualifies as ore grade in a given deposit, and is also used as the lowest grade below which the mineralized rock currently cannot be profitably exploited. Cut-off grades vary between deposits depending upon the amenability of ore to gold extraction and upon costs of production. |

| Diorite | An intrusive igneous rock composed chiefly of sodic plagioclase, hornblende, biotite or pyroxene. |

| Drift | A horizontal or nearly horizontal underground opening driven along a vein to gain access to the deposit. |

| Exploration | Prospecting, sampling, mapping, diamond drilling and other work involved in searching for or defining a mineral deposit. |

| Face | The end of a drift, cross-cut or stope in which work is taking place. |

| Fault | A break in the Earth'searth's crust caused by tectonic forces which have moved the rock on one side with respect to the other. |

| Grade | Term used to indicate the concentration of an economically desirable mineral or element in its host rock as a function of its relative mass. With gold or silver, this term may be expressed as grams per tonne (g/t) or ounces per tonne (opt or oz/t). |

| Gram | 0.0321507 troy ounces |

| g/t | Grams per metric tonne |

| Hydrothermal | Processes associated with heated or superheated water, especially mineralization or alteration. |

| Km | Kilometre(s). Equal to 0.62 miles. |

| Leaching | The separation, selective removal or dissolving-out of soluble constituents from a rock or ore body by the natural actions of percolating solutions. |

| M | Metre(s). Equal to 3.28 feet. |

| Metamorphic | Affected by physical, chemical, and structural processes imposed by depth in the earth’s crust. |

| Mine | An excavation on or beneath the surface of the ground from which mineral matter of value is extracted. |

| Net Smelter Return (“NSR”) | A payment made by a producer of metals based on the value of the gross metal production from the property, less deduction of certain limited costs including smelting, refining, transportation and insurance costs. |

| Orebody | A term used to denote the mineralization contained within an economic mineral deposit. |

| Outcrop | An exposure of rock or mineral deposit that can be seen on the surface, that is, not covered by soil or water. |

| Oxidation | A chemical reaction caused by exposure to oxygen that results in a change in the chemical composition of a mineral. |

| Oz | Ounce. A measure of weight in gold and other precious metals, correctly troy ounces, which weigh 31.1 grams as distinct from an imperial ounce which weigh 28.4 grams. |

| Shaft | A vertical passageway to an underground mine for moving personnel, equipment, supplies and material including ore and waste rock. |

| Strike | The direction, or bearing from true north, of a vein or rock formation measure on a horizontal surface. |

| Stringer | A narrow vein or irregular filament of a mineral or minerals traversing a rock mass. |

| Sulphides | A group of minerals which contains sulfur and other metallic elementelements such as copper and zinc. Gold is usually associated with sulphide enrichment in mineral deposits. |

| Tailings | Material rejected from a mill after most of the recoverable valuable minerals have been extracted. |

| Vein | A fissure, fault or crack in a rock filled by minerals that have travelled upwards from some deep source. |

| Zone | An area of distinct mineralization. |

NOTE ABOUT FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains “forward-looking statements”. These forward-looking statements are based on our current expectations, assumptions, estimates and projections about our business and our industry. Words such as “believe,” “anticipate,” “expect,” “intend,” “plan,” “may,” and other similar expressions identify forward-looking statements. In addition, any statements that refer to expectations, projections or other characterizations of future events or circumstances are forward-looking statements. These forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those reflected in the forward-looking statements. Factors that might cause such a difference include, but are not limited to, those discussed in the sections of this annual report titled “Risk Factors”, “Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, as well as the following:

| | · | general economic conditions, because they may affect our ability to raise money |

| | · | our ability to raise enough money to continue our operations |

| | · | changes in regulatory requirements that adversely affect our business |

| | · | changes in the prices for minerals that adversely affect our business |

| | · | political changes in Chile, which could affect our interests there |

| | · | other uncertainties, all of which are difficult to predict and many of which are beyond our control |

You are cautioned not to place undue reliance on these forward-looking statements, which relate only to events as of the date on which the statements are made. We undertake no obligation to publicly revise these forward-looking statements to reflect events or circumstances that arise after the date of this annual report. You should refer to and carefully review the information in future documents we file with the Securities and Exchange Commission.

General

Red Metal Resources Ltd. was incorporated in Nevada on January 10, 2005 as Red Lake Exploration, Inc. We changed our name to Red Metal Resources Ltd. on August 27, 2008.

On August 21, 2007, we formed Minera Polymet Limitada, a limited liability company, under the laws of the Republic of Chile. We own 99% of Polymet, which holds our Chilean mineral property interests. Under Chilean law, a resident of Chile must be a shareholder in a limitada. To meet this requirement, 1% of Polymet is owned by a Chilean resident, an experienced manager who has organized an office and other resources for us to use and is Polymet’s legal representative in Chile. Polymet’s office is located in Vallenar, III Region of Atacama, Chile. When we refer to “Red Metal”, the “company”, “we”, “us” or “our” in this report, we mean Red Metal Resources Ltd. together with Minera Polymet Limitada.

Our resident agent’s office is at 711 S. Carson Street, Suite 4, Carson City, Nevada, 89701. Our business office is at 195 Park Avenue, Thunder Bay, Ontario, Canada, P7B 1B9. Our telephone number is (807) 345-7384; our email address is info@redmetalresources.comadmin@redmetalresources.com; and our web address is www.redmetalresources.com. Information on our web site is not a part of this annual report.

We are a start-up exploration stage company without operations. We are in the business of acquiring and exploring mineral claims. All of our claims are located in the III Region of Atacama, Chile. We have not determined whether our claims contain mineral reserves that are economically recoverable. We have not produced revenues from our principal business and are considered an exploration stage company as defined by “Accounting and Reporting by Development Stage Enterprises.”

Our ability to realize a return on our investment in mineral claims depends upon whether we maintain the legal ownership of the claims. Title to mineral claims involves risks inherent in the process of determining the validity of claims and the ambiguous transfer history characteristic of many mineral claims. To the best of our knowledge, and after consultation with an attorney knowledgeable in the practice of mining, we believe that we have taken the steps necessary to ensure that we have good title to our mineral claims. We have had our contracts and deeds notarized, recorded in the registry of mines and published in the mining bulletin and we review the mining bulletin regularly to determine whether other parties have staked claims over our ground. We have discovered no such claims.

Chile’s mining and land tenure policies were established to secure the property rights of both domestic and foreign investors to stimulate development of mining in Chile. The government of Chile owns all mineral resources, but exploration and exploitation of these resources are permitted through exploration and mining concessions. A mineral concession must pass through three stages to become a permanent mining concession, namely, pedimento, manifestacion and mensura.

A pedimento is an initial exploration claim. It can be placed on any area, whereas the survey to establish a permanent mensura claim can only be completed on free areas where no other mensuras exist. A pedimento is valid for a maximum of two years. At the end of this period it may either be reduced in size by at least 50% and renewed for an additional two years or entered into the manifestacion process to establish a permanent mensura claim. New pedimentos can overlap existing pedimentos, but the pedimento with the earliest filing date takes precedence providing the claim holder maintains the pedimento in accordance with the mining code and the applicable regulations.

Manifestacion is the process by which a pedimento is converted to a permanent mining claim. At any stage during its two-year life, the holder of a pedimento can submit a manifestacion application, which is valid for 220 days. To begin the manifestacion process, the owner must request a survey (mensura) within 220 days. After the survey request is accepted, the owner has approximately 12 months to have the claim surveyed by a government-licensed surveyor, inspected and approved by the national mining service, and affirmed as a mensura (equivalent to a patented claim) by a judge. Thereafter, an abstract describing the claim is published in Chile’s official mining bulletin (published weekly) and 30 days later the claim is inscribed in the appropriate mining registry.

A mensura is a permanent property right that does not expire so long as the annual fees (patentes) are paid in a timely manner. Failure to pay the patentes for an extended period can result in the claim being listed for sale at auction, where a third party can acquire a claim for the payment of the back taxes owed and a penalty.

In Chile, we have both pedimento and mensura claims. We cannot guarantee that any of our pedimento claims will convert to mensura claims. Some of our pedimentos are still in the registration process and some are in the manifestacion stage. We may decide, for geologic, economic or other reasons, not to complete a registration or manifestacion or to abandon a claim after it is registered. Some of our pedimentos may have been staked over other owners’ claims as permitted by the Chilean mining code. Our pedimento rights in these claims will not crystallize unless the owners of the underlying claims fail to pay their taxes or otherwise forfeit their interests in their claims. Our purpose in over-staking is to claim free ground around others’ claims and to have the first right to forfeited claims if we want them. Over-staking is easier and less costly than staking available ground around claims and ensures that all available ground is covered that might otherwise be missed.

We have a close working relationship with Minera Farellon Limitada (“Minera Farellon”), a Chilean company owned equally by Kevin Mitchell, Polymet’s legal representative in Chile, and Richard Jeffs, the father of our president, who holds more than 5% of our shares of common stock (see Table 24 below)22). Minera Farellon investigates potential claims and often ties them up, by staking new claims, optioning or buying others’ claims, all at its own cost. This gives us an opportunity to review the claims to decide whether they are of interest to us. If we are interested, then we either proceed to acquire an interest in the property directly from the owner, or, if Minera Farellon has already obtained an interest, we take an option to acquire its interest. Minera Farellon, which is located in the city of Vallenar, also provides some of our logistical support in Vallenar under a month-to-month contract, which enables us to limit our operating expenses to those needed from time to time.

Unproved mineral properties

Due to a lack of operating capital, during the fiscal year ended January 31, 2013, we conducted no material exploratory operations on any of our properties. Until we are able to raise operating capital, which we cannot assure that we can do, we will not be able to initiate new exploration efforts or continue the exploration efforts we have begun. On February 11, 2013 we reported that we entered into a memorandum of understanding with Geoactiva Spa. ("Geoactiva") pursuant to which Geoactiva expressed an intention to acquire our Perth property, subject to the results of a due diligence investigation. See the section below titled, “Memorandum of Understanding with Geoactiva Spa”. The memorandum of understanding gives us confidence there is an opportunity to raise funds by selling some of our properties or by entering into joint venture agreements to develop some of our properties. We have fourthree active properties which we have assembled since the beginning of 2007— the Farellon, Perth, Mateo, and Veta Negra.Mateo. These properties consist of both mining and exploration claims and are grouped into two district areas – Carrizal Alto area properties and Vallenar area properties.

Active properties

| Table 2: Active properties | | |

| Property | Percentage, type of claim | Hectares |

| Gross area | Net areaa |

| Carrizal Alto area |

| Farellon | | | | |

| Farellon 1 – 8 claim | 100%, mensura | 66 | | |

| Farellon 3 claim | 100%, pedimento | 300 | | |

| Cecil 1 – 49 claim | 100%, mensura | 230 | | |

| Cecil 1 – 40 and Burghley 1 – 60 claims | 100%, mensura in process | 500 | | |

| | | 1,096 | | 1,096 |

| Perth | | | | |

| Perth 1 al 36 claim | 100%, mensura | 109 | | |

| Lancelot I 1 al 30 claim | 100%, mensura in process | 300 | | |

| Lancelot II 1 al 20 claim | 100%, mensura in process | 200 | | |

| Rey Arturo 1 al 30 claim | 100%, mensura in process | 300 | | |

| Merlin I 1 al 10 claim | 100%, mensura in process | 60 | | |

| Merlin I 1 al 24 claim | 100%, mensura in process | 240 | | |

| Galahad I 1 al 10 claim | 100%, mensura in process | 50 | | |

| Galahad IA 1 al 46 claim | 100%, mensura in process | 230 | | |

| Percival III 1 al 30 claim | 100%, mensura in process | 300 | | |

| Tristan II 1 al 30 claim | 100%, mensura in process | 300 | | |

| Tristan IIA 1 al 5 claim | 100%, mensura in process | 15 | | |

| Camelot claim | 100%, manifestacion | 300 | | |

| | | 2,404 | | |

| Overlapped claims (see Figure 4) | | (121) | | 2,283 |

Vallenar area |

Mateo | | | | |

Margarita claim | 100%, mensura | 56 | | |

Che 1 & 2 claims | 100%, mensura | 76 | | |

Irene & Irene II claims | 100% ,mensura | 60 | | |

Mateo 1, 2, 3, 9,10,12, 13, 14 claims | 100%, manifestacion | 2,100 | | |

| Mateo 4 and 5 claims | 100%, pedimento | 600 | | |

| | | 2,892 | | |

| Overlapped claims (see Figure 6) | | (469) | | 2,423 |

| | | | | |

| Veta Negra | | | | |

| Veta Negra 1 al 7 claim | Option to purchase, mensura | 28 | | |

| Exon 1 al 4 claim | Option to purchase, mensura | 16 | | |

| Trixy (19 claims) | 100%, manifestacion | 2,900 | | |

| Pibe | Option to purchase, mensura in process | 200 | | |

| | | 3,144 | | |

| Overlapped claims (see Figure 8) | | (238) | | 2,906 |

| | | | | |

| | | | | 8,708 |

a Some pedimentos and manifestacions overlap other claims. The net area is the total of the hectares we have in each property (i.e. net of our overlapped claims). |

| Table 2: Active properties | | | | |

| Property | Percentage, type of claim | | Hectares | |

| | Gross area | | | Net areaa | |

| Carrizal Alto area | |

| Farellon | | | | | | | |

| Farellon 1 – 8 claim | 100%, mensura | | | 66 | | | | |

| Farellon 3 claim | 100%, manifestacion | | | 300 | | | | |

| Cecil 1 – 49 claim | 100%, mensura | | | 230 | | | | |

| Teresita claim | 100%, mensura | | | 1 | | | | |

| Azucar 6 – 25 claim | 100%, mensura | | | 88 | | | | |

| Stamford 61 – 101 claim | 100%, mensura | | | 165 | | | | |

| Kahuna 1 – 40 claim | 100%, mensura | | | 200 | | | | |

| | | | | 1,050 | | | | 1,050 | |

| Perth | | | | | | | | | |

| Perth 1 al 36 claim | 100%, mensura | | | 109 | | | | | |

| Lancelot I 1 al 30 claim | 100%, mensura in process | | | 300 | | | | | |

| Lancelot II 1 al 20 claim | 100%, mensura in process | | | 200 | | | | | |

| Rey Arturo 1 al 30 claim | 100%, mensura in process | | | 300 | | | | | |

| Merlin I 1 al 10 claim | 100%, mensura in process | | | 60 | | | | | |

| Merlin I 1 al 24 claim | 100%, mensura in process | | | 240 | | | | | |

| Galahad I 1 al 10 claim | 100%, mensura in process | | | 50 | | | | | |

| Galahad IA 1 al 46 claim | 100%, mensura in process | | | 230 | | | | | |

| Percival III 1 al 30 claim | 100%, mensura in process | | | 300 | | | | | |

| Tristan II 1 al 30 claim | 100%, mensura in process | | | 300 | | | | | |

| Tristan IIA 1 al 5 claim | 100%, mensura in process | | | 15 | | | | | |

| Camelot claim | 100%, manifestacion | | | 300 | | | | | |

| | | | | 2,404 | | | | | |

Overlapped claims a | | | | (121 | ) | | | 2,283 | |

| Vallenar area | |

| Mateo | | | | | | | | | |

| Margarita claim | 100%, mensura | | | 56 | | | | | |

| Che 1 & 2 claims | 100%, mensura | | | 76 | | | | | |

| Irene & Irene II claims | 100% ,mensura | | | 60 | | | | | |

| Mateo 1, 2, 3, 9,10,12, 13, 14 claims | 100%, mensura in process | | | 2,100 | | | | | |

| Mateo 4 and 5 claims | 100%, pedimento | | | 600 | | | | | |

| | | | | 2,892 | | | | | |

Overlapped claims a | | | | (469 | ) | | | 2,423 | |

| | | | | | | | | | |

| | | | | | | | | 5,756 | |

a Some pedimentos and manifestacions overlap other claims. The net area is the total of the hectares we have in each property (i.e. net of our overlapped claims). | |

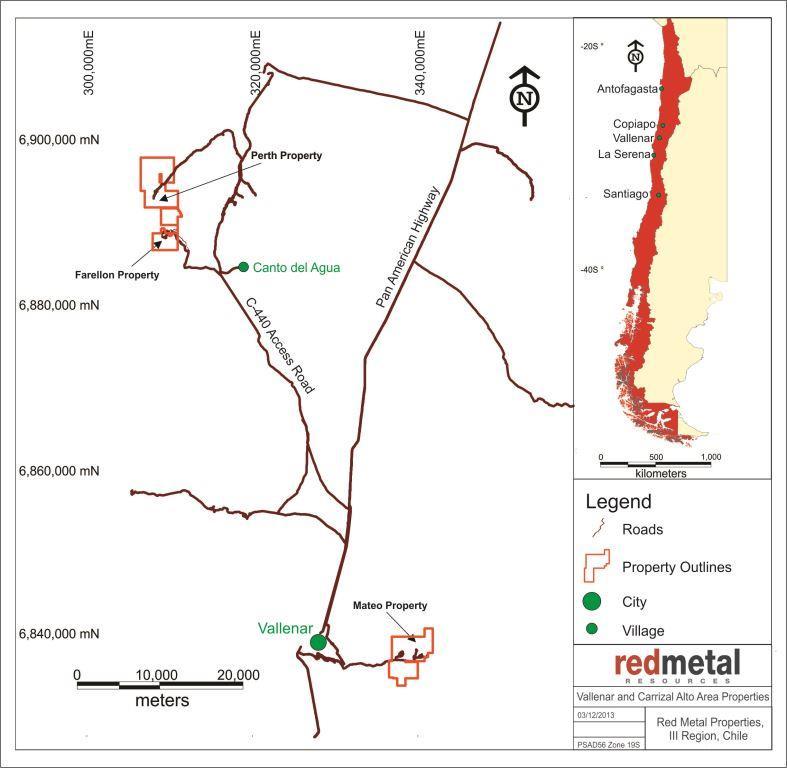

Our active properties as of the date of this filing are set out in Table 2.Figure 1. These properties are accessible by road from Vallenar as illustrated in Figure 1.1 below.

Figure 1: Location and access to active properties.

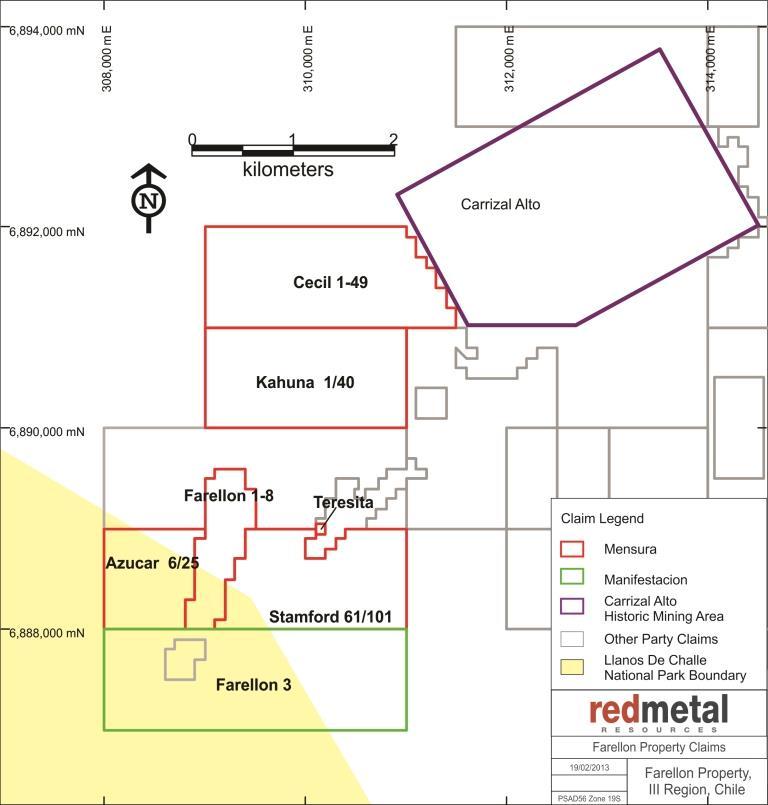

Farellon property

The Farellon property consists of two groups of claims—the Farellon claims and the Cecil and Burghley claims—which are not contiguous but lie within the historical Carrizal Alto mining district southwest of the Carrizal Alto mine. Table 3 describes the claims and Figure 2 illustrates them.

| Table 3: Farellon property | | | | | |

| | | Type | |

| Claim | | Mensura (ha) | | Pedimento (ha) | |

| Farellon 1 – 8 | | 66 | | | |

| Cecil 1 – 49 | | 230 | | | |

| Cecil 1 – 40 | | 200 | | | |

| Burghley 1 – 60 | | 300 | | | |

| Farellon 3 | | | | | 300 | |

| | | 796 | | | 300 | |

6

Table 3: Farellon property | | | | |

| | | | Type | |

| Claim | | | Mensura (ha) | | | | Manifestacion (ha) | | | | Pedimento (ha) | |

| Farellon 1 – 8 | | | 66 | | | | | | | | | |

| Cecil 1 – 49 | | | 230 | | | | | | | | | |

| Teresita | | | 1 | | | | | | | | | |

| Azucar 6 – 25 | | | 88 | | | | | | | | | |

| Stamford 61 – 101 | | | 165 | | | | | | | | | |

| Kahuna 1 – 40 | | | 200 | | | | | | | | | |

| Farellon 3 | | | | | | | 300 | | | | | |

| | | | 750 | | | | 300 | | | | | |

Figure 2: Farellon property

The Farellon 1 – 8 is the first mineral claim that we acquired in Chile. It covers 66 hectares and is centered about 309,150 east and 6,888,800 south UTM PSAD56 Zone 19 in Province of Huasco, Commune of Huasco, III Region of Atacama, Chile.

We acquired the claim on April 25, 2008, for $550,000 and owe a royalty equal to 1.5% of the net proceeds that we receive from the processor to a maximum of $600,000 with a monthly minimum of $1,000 when we start exploiting the minerals extractextracted from the claim. We can pay any unpaid balance of the royalty at any time. We have not yet exploited the claim.

On September 17, 2008, we bought the Cecil 1 – 49, Cecil 1 – 40 and Burghley 1 – 60 claims for $20,000. $27,676. On December 1, 2009, we initiated the manifestacion process when we applied to convert the Cecil 1 – 40 and Burghley 1 – 60 exploration claims to mining claims. In January 2013 we abandoned the manifestacion process for the Cecil 1-40 and Burghley 1-60 claims due to the fact that several mensuras underlying the claims covered the most prospective ground as outlined in our prospecting and mapping program completed in April 2012.

The Cecil and Burghley claims cover 730claim covers 230 hectares and areis centered at 311,500310,250 east and 6,890,0006,891,500 south UTM PSAD56 Zone 19 and lielies approximately 1.7 kilometers north of the Farellon 1 – 8 border. The claims coverclaim covers a 1.8-kilometre700 metre strike length of a mineralized vein interpreted to be part of the same mineralizing system as the Farellon 1 – 8 vein. An investigation completed during the Farellon 1 – 8 acquisition uncovered a broad regional reconnaissance sampling program completed in 1996 showing results from the areas covered by the Cecil and Burghley claims.claim. Results from the 1996 sampling show copper and gold grades similar to grades returned from the Farellon vein, indicating that the Cecil and Burghley claimsclaim could have similar mineralized bodies. On December 1, 2009, we initiated the manifestacion process when we applied to convert the Cecil 1 – 40 and Burghley 1 – 60 exploration (pedimento) claims to mining (mensura) claims.

Between July 2010 and November 2011 we registered seven pedimento, Farellon 3-9,3 through 9, at a cost of $2,408 to cover 1,800 hectares of ground around our Farellon 1 – 8 claim. In January 2013 we allowed the Farellon 4-9 are not included4 through 9 pedimentos to lapse due to underlying claims. In February 2013 we commenced the manifestacion process with the Farellon 3 pedimento.

On August 21, 2012, we acquired four mineral claims – Azucar 6-25, Kahuna 1-40, Stamford 61-101, and Teresita – through the government auction for a total price of $19,784. The Azucar claim is the most prospective of these claims as it covers a 1,200 metre strike length of a mineralized vein interpreted to be part of the same mineralizing system as the Farellon 1 – 8 vein. Three parallel veins have also been identified on the map until we confirm that underlying ground is open for staking. As permitted by Chilean law, Farellon 4-9 are currently overlapping other pedimentos.Azucar claim during the 2012 mapping and prospecting program and can be seen on Figure 3.

Location and means of access. The Farellon property is approximately 40 kilometers west of the Pan-American Highway, about 1 hour and 15 minutes by vehicle from the town of Vallenar which has a population of 40,000 and modern facilities. High-tension power lines and a fiber-optic communications line run along the highway and both power and rail are connected to the Cerro Colorado iron ore mine only 20 kilometers from the Farellon property. The area is serviced from Copiapó, a city of 70,000 with daily air and bus services to Santiago and other centers.

The Farellon property can be accessed by driving approximately 20 kilometers north on the Pan-American Highway from Vallenar then turning northwest towards Canto del Agua. From Canto del Agua, the Farellon property is approximately 10 kilometers along a well-maintained gravel road. There are numerous gravel roads in the area, so a guide is necessary to access the property the first time. All of the roads are well maintained and can support large machinery necessary to transport drills, backhoes and bulldozers. Water is readily available in Canto del Agua and could probably be found on the Farellon property where all of the historic drill holes intersected water.

Exploration history .The Farellon property is in the Carrizal Alto mining district and lies 5 kilometers along strike south of the center of the historic Carrizal Alto copper-gold mine. Veins of the Farellon property were exploited as part of the Carrizal Alto mines. We have located no hard data summarizing all of the past mining activity, but tailings, slag dumps and the size of the shafts and some of the shallow surface workings are evidence of extensive historical mining.

Mine workings of various sizes are all along the Farellon property, but only one modern exploration program has been completed. In 1996, the Farellon and two other veins, the Fortuna and the Theresa, were explored by an Australian junior mining company under the name Minera Stamford S.A. Their exploration included a large mapping and surface sampling program followed by a 34-hole RC drilling program. Of these 34 drill holes, 23 were drilled on the Farellon 1 – 8 claim. The RC drilling program on the Farellon claim consistently intersected oxide and sulphide facies mineralization along a 2 kilometer-long zone covering the Farellon claim and strike extents to the south. Mineralization is 2 to 35 meters wide with an average width of 5 meters. The mineralized zone consists of one or more discrete veins and, in places, stockwork veining and mineralization. While drilling covered the length of the property, gaps up to 350 meters are untested and infill drilling is required to confirm an economic ore body. Table 4 presents the significant intersections from the 23 holes drilled on the Farellon claim in the 1996 drilling.

| Table 4: Farellon historic significant intersections (1996) | |

| Drill hole | | | | Significant intervals (m) | | | | Assay results | |

| FAR–96 | | | | From | | | | To | | | Length | | | Gold (g/t) | | | Copper (%) | | | Cobalt (%) | |

| | 06 | | | | 49 | | | | 54 | | | | 5 | | | | 0.15 | | | | 0.73 | | | | 0.01 | |

| | 07 | | | | 25 | | | | 34 | | | | 9 | | | | 0.38 | | | | 1.05 | | | | 0.02 | |

| | 09 | | | | 57 | | | | 84 | | | | 27 | | | | 0.51 | | | | 0.91 | | | | 0.03 | |

| | 010 | | | | 31 | | | | 36 | | | | 5 | | | | 1.00 | | | | 0.68 | | | | 0.04 | |

| | 011 | | | | 20 | | | | 26 | | | | 6 | | | | 0.67 | | | | 0.46 | | | | 0.02 | |

| | 013 | | | | 86 | | | | 93 | | | | 7 | | | | 0.87 | | | | 1.68 | | | | 0.04 | |

| | 014 | | | | 77 | | | | 83 | | | | 6 | | | | 0.66 | | | | 0.85 | | | | 0.06 | |

| | 015 | | | | 59 | | | | 79 | | | | 20 | | | | 0.99 | | | | 0.98 | | | | 0.06 | |

| | | | | | 99 | | | | 109 | | | | 10 | | | | 0.18 | | | | 1.02 | | | | 0.03 | |

| | 016 | | | | 24 | | | | 26 | | | | 2 | | | | 0.95 | | | | 1.57 | | | | 0.02 | |

| | | | | | 64 | | | | 70 | | | | 6 | | | | 0.73 | | | | 0.81 | | | | 0.07 | |

| | 020 | | | | 14 | | | | 16 | | | | 2 | | | | 0.46 | | | | 1.85 | | | | 0.05 | |

| | | | | | 39 | | | | 43 | | | | 4 | | | | 0.75 | | | | 0.90 | | | | 0.03 | |

| | 021 | | | | 22 | | | | 25 | | | | 3 | | | | 4.17 | | | | 5.29 | | | | 0.11 | |

| | 022 | | | | 29 | | | | 39 | | | | 10 | | | | 1.53 | | | | 1.31 | | | | 0.04 | |

| | | | | | 100 | | | | 108 | | | | 8 | | | | 3.72 | | | | 2.49 | | | | 0.06 | |

| | | | | | 50 | | | | 53 | | | | 3 | | | | 0.48 | | | | 1.10 | | | | 0.06 | |

| | 023 | | | | 59 | | | | 64 | | | | 5 | | | | 0.28 | | | | 0.78 | | | | 0.03 | |

| | | | | | 132 | | | | 147 | | | | 15 | | | | 0.60 | | | | 1.42 | | | | 0.03 | |

| | 024 | | | | 33 | | | | 36 | | | | 3 | | | | 0.94 | | | | 2.89 | | | | 0.06 | |

| | 025 | | | | 65 | | | | 85 | | | | 20 | | | | 0.97 | | | | 1.22 | | | | 0.02 | |

| | 028 | | | | 55 | | | | 58 | | | | 3 | | | | 0.12 | | | | 0.52 | | | | 0.06 | |

| | 029 | | | | 30 | | | | 34 | | | | 4 | | | | 0.18 | | | | 1.15 | | | | 0.07 | |

| | | | | | 82 | | | | 87 | | | | 5 | | | | 0.09 | | | | 0.96 | | | | 0.01 | |

| Table 4: Farellon historic significant intersections (1996) |

Drill hole FAR–96 | Significant intervals (m) | | Assay results |

| From | To | Length | | Gold (g/t) | Copper (%) | Cobalt (%) |

| 06 | 49 | 54 | | 5 | | | 0.15 | 0.73 | 0.01 |

| 07 | 25 | 34 | | 9 | | | 0.38 | 1.05 | 0.02 |

| 09 | 57 | 84 | | 27 | | | 0.51 | 0.91 | 0.03 |

| 010 | 31 | 36 | | 5 | | | 1.00 | 0.68 | 0.04 |

| 011 | 20 | 26 | | 6 | | | 0.67 | 0.46 | 0.02 |

| 013 | 86 | 93 | | 7 | | | 0.87 | 1.68 | 0.04 |

| 014 | 77 | 83 | | 6 | | | 0.66 | 0.85 | 0.06 |

| 015 | 59 | 79 | | 20 | | | 0.99 | 0.98 | 0.06 |

| 99 | 109 | | 10 | | | 0.18 | 1.02 | 0.03 |

| 016 | 24 | 26 | | 2 | | | 0.95 | 1.57 | 0.02 |

| 64 | 70 | | 6 | | | 0.73 | 0.81 | 0.07 |

| 020 | 14 | 16 | | 2 | | | 0.46 | 1.85 | 0.05 |

| 39 | 43 | | 4 | | | 0.75 | 0.90 | 0.03 |

| 021 | 22 | 25 | | 3 | | | 4.17 | 5.29 | 0.11 |

| 022 | 29 | 39 | | 10 | | | 1.53 | 1.31 | 0.04 |

| 100 | 108 | | 8 | | | 3.72 | 2.49 | 0.06 |

| 023 | 50 | 53 | | 3 | | | 0.48 | 1.10 | 0.06 |

| 59 | 64 | | 5 | | | 0.28 | 0.78 | 0.03 |

| 132 | 147 | | 15 | | | 0.60 | 1.42 | 0.03 |

| 024 | 33 | 36 | | 3 | | | 0.94 | 2.89 | 0.06 |

| 025 | 65 | 85 | | 20 | | | 0.97 | 1.22 | 0.02 |

| 028 | 55 | 58 | | 3 | | | 0.12 | 0.52 | 0.06 |

| 029 | 30 | 34 | | 4 | | | 0.18 | 1.15 | 0.07 |

| 82 | 87 | | 5 | | | 0.09 | 0.96 | 0.01 |

Geology .Geology. The Farellon area has two major lithological units: Paleozoic metamorphic sediments consisting of schists, phyllites and quartzites; and the Franja Central diorites. The metamorphosed sediments outcrop in the western part of the property and have been metamorphosed to lower greenschist facies and then extensively overprinted by hydrothermal alteration. Hydrothermal alteration is directly associated with the shear zone. The diorite underlies the eastern part of the project area and has been extensively intruded by northeasterly trending intermediate mafic dykes. At the Farellon property, a small stock-like felsic body named Pan de Azucar intrudes the diorite. The intrusive relationship between the diorite and metamorphic sediments always appear to be tectonic. Within the property and at the main Carrizal Alto workings to the north, the major mineralization is intimately related to the south-southwest trending mylonitic sheared contact between the metamorphic sediments and the diorite. The shear is considered a splay of the main Atacama Fault Zone and dips 30º to 65º west. This contact parallels the regional geological trend and coincides with a major lineament which extends for hundreds of kilometers. The sheared contact is 50 meters to 200 meters wide over the 1.7-kilometre strike length of the Farellon property. Veins are typically 3 to 15 meters wide, striking south-southwest and dipping approximately 65 degrees to the northwest.

Mineralization . The Farellon property lies within the Candelaria iron oxide-copper-gold (IOCG) belt of Chile. Ore bodies in the belt occur in veins, breccias, stringer bodies and layer parallel replacement bodies and are typically associated with north-south trending faults related to the Atacama Fault Zone. All IOCG deposits have a strong association with iron oxides in the form of hematite or magnetite. In the Candelaria region, larger ore bodies are located where the fault zones intersect a lithological contact with significant rheological contrast such as a sedimentary and volcanic intrusive contact.

Economic IOCG deposits are generally polymetallic and can include iron, copper, gold, zinc, lead, uranium and cobalt among others. The Farellon property historically has been exploited for copper and to a lesser extent, gold. Cobalt mineralization was observed during the 1996–97 exploration work, but we have found no records of cobalt extraction.

Drilling (2009)(Fall 2009). In September 2009 we completed a 725-metre RC drilling program on the Farellon property. Table 5 summarizes the results of our drilling.

The drilling program was designed to confirm historic drilling results and test mineralization down dip of previous drilling. Of the five holes drilled, three holes—FAR–09–A, B and E—tested historic intersections FAR–96–09, 021 and 022 summarized in Table 3; and two—FAR–09–C and D—tested depth extents of the previously known mineralization. Results of the drilling show grades and widths of mineralization consistent with historic exploration results and have given us valuable geological information showing the possibility of a shallow, 30-degree dip of the mineralization.

| Table 5: Farellon drilling results (2009) |

Drill hole FAR – 09 | Assay interval (m) | | Assay grade |

| | From | To | Core length | | Gold (ppm) | Copper (%) |

| A | | 31 | 34 | 3.0 | | 0.81 | 1.99 |

| | 79 | 109 | 30.0 | | 0.18 | 0.62 |

| including | 97 | 106 | 9.0 | | 0.44 | 1.63 |

| B | | 56 | 96 | 40.0 | | 0.27 | 0.55 |

| including | 56 | 63 | 7.0 | | 0.22 | 0.66 |

| | 74 | 96 | 22.0 | | 0.42 | 0.79 |

| including | 75 | 86 | 11.0 | | 0.67 | 1.35 |

| C | | 73 | 103 | 30.0 | | 0.79 | 0.55 |

| including | 77 | 82 | 5.0 | | 4.16 | 2.57 |

| D | | 95 | 134 | 39.0 | | 0.11 | 0.58 |

| including | 95 | 103 | 8.0 | | 0.33 | 2.02 |

| E | | 25 | 30 | 5.0 | | 0.54 | 1.35 |

| 65 | 68 | 3.0 | | 0.58 | 1.46 |

| Table 5: Farellon drilling results (2009) | |

| | Drill hole | | Assay interval (m) | | | Assay grade | |

| | FAR – 09 | | | | From | | | To | | | Core length | | | Gold (ppm) | | | Copper (%) | |

| | | | | | | 31 | | | | 34 | | | | 3.0 | | | | 0.81 | | | | 1.99 | |

| | | A | | | | | 79 | | | | 109 | | | | 30.0 | | | | 0.18 | | | | 0.62 | |

| | | | | including | | | 97 | | | | 106 | | | | 9.0 | | | | 0.44 | | | | 1.63 | |

| | | | | | | | 56 | | | | 96 | | | | 40.0 | | | | 0.27 | | | | 0.55 | |

| | | | | including | | | 56 | | | | 63 | | | | 7.0 | | | | 0.22 | | | | 0.66 | |

| | | B | | | | | 74 | | | | 96 | | | | 22.0 | | | | 0.42 | | | | 0.79 | |

| | | | | including | | | 75 | | | | 86 | | | | 11.0 | | | | 0.67 | | | | 1.35 | |

| | | C | | | | | 73 | | | | 103 | | | | 30.0 | | | | 0.79 | | | | 0.55 | |

| | | | | including | | | 77 | | | | 82 | | | | 5.0 | | | | 4.16 | | | | 2.57 | |

| | | D | | | | | 95 | | | | 134 | | | | 39.0 | | | | 0.11 | | | | 0.58 | |

| | | | | including | | | 95 | | | | 103 | | | | 8.0 | | | | 0.33 | | | | 2.02 | |

| | | E | | | | | 25 | | | | 30 | | | | 5.0 | | | | 0.54 | | | | 1.35 | |

| | | | | | | | 65 | | | | 68 | | | | 3.0 | | | | 0.58 | | | | 1.46 | |

We commissioned Micon International Limited (“Micon”) to prepare a technical report that complies with Canadian National Instrument 43-101 summarizing the information obtained from this drilling program. Micon concluded that our drilling confirmed the general location and tenure of the mineralization identified during the 1996 drilling program and noted some minor disparities between historical 1996 gold and copper assays and the recent 2009 gold and copper assays in two of the drill holes—FAR–09–A and E. In FAR–09–E. Micon recommended that we investigate these disparities during the next phase of drilling.

The drilling identified that the copper and gold mineralization exhibited a direct correlation in both location and relative intensity and provided useful information for outlining the relative location and spacing of drill holes in our next exploration programs.

All of our 2009 drill holes intersected oxide facies mineralization with only minor amounts of sulphides observed in drill hole FAR–09–D. When we have established the general trend of the mineralization we can conduct some drilling to identify the oxide-sulphide interface.

Following the 2009 drilling program, Micon recommended that we conduct a two-phase drilling program. The first phase would consist of approximately 1,200 meters of diamond drilling to assist in defining the structural controls on the mineralization, which could have been misinterpreted in the past due to the limited geological information obtained from the historic RC drilling, and the depth and nature of the sulphide mineralization.

QA/QC, sampling procedures and analytical methods. We conducted sampling on one-meter intervals, which is generally the industry-standard sampling practice for RC drilling. Sampling started at the collar of the hole and proceeded to the toe or bottom of the drill hole on one-meter increments. Generally, the sample recovery was good to excellent for the 2009 drilling commenced in Julyprogram. Table 5 summarizes significant assay results. They are reported as drill lengths as we have not established the width of the mineralized zone.

Drilling (Summer 2011). During June through September 2011 we conducted a combined RC/diamond drill program on the Farellon property. The program was designed to continue to expand on the results of the 2009 drill program, as well as to continue confirming historical results along the strike. During this program we completed 11 drillholes for a total of 2,233m with the goal not only of better defining structural controls on mineralization but to examine the continuity of mineralization along strike and at depth. The target of the program was to outline a 700m mineralized strike length down to 200m vertical depth with approximate 75m intercept spacing, and to infill gaps 300m further to the North to increase intercepts to 150m150 m spacing.

Many of the existing intercepts in this area were from the 1996/97 drill program where no geological information can be located for these drill holes. By infilling the area with drilling at 75 meter pierce points the aim was to increase confidence in the continuity and increase knowledge of the nature and structural controls on mineralization to aid further exploration planning. 2011 drill results confirmed that mineralization is still present downdip of past drilling intercepts and still open at depth. Infill drilling confirmedcontinued to confirm the continuity of the mineralization is stilland aided in the development of economic grade and now starts the process of having consistent 75m spacing between drillholes.

a 3D model that will be used for any future drill planning.

2011 drilling confirmed the overall regional shear structural controls on mineralization occurring within the oblique fault contact between overlying Paleozoic Metasediments and underlying Jurassic intermediate intrusives. Supergene mineralization seems to occur within local faults not immediately within the lithological fault contact – possibly fault splays emanating off the main regional structure. In the 2011 drillholes, supergene copper-gold mineralization was intersected 50-150m downhole with abundant carbonate and iron oxide precipitation.

Hypogene mineralization occurred below 150m hosted in quartz and carbonate veins which appear closer to the main shear fault zone contact. Approximately within 20m downhole of intersected hypogene mineralized veins the lithological contact was encountered, passing through to the underlying intrusive package. The 2011 drill program was generally positive in better defining structural controls on mineralization and proving continuity of mineralization along strike and at depth. However, more drilling is needed to continue to expand on the mineralized zone along strike and at depth, and prove up infill targets for an initial resource estimation.

In spring of 2012 we commissioned Micon to complete a second 43-101 technical report. Micon now recommends that we conduct a much larger phase of exploration consisting of 5,000 meters of diamond drilling and 10,000 meters of RC drilling, and geophysical surveys and geological mapping. A geophysics survey using both magnetics and induced polarization will help to identify further mineralized structures on the property that may not have been noticed in the historic mapping. A phase two drill program would be at defined spacing to outline the continuity of mineralization leading to a 3D model andan initial resource estimation. The depth of the drilling would be dependent on the results of the phase one drilling program. The estimated cost of this phase is $1.9 million.

QA/QC, sampling procedures and analytical methods. We conducted sampling on one-meter intervals, which is generally the industry-standard sampling practice for RC drilling. Sampling started at the collar of the hole and proceeded to the toe or bottom of the drill hole on one-meter increments. Generally, the sample recovery was good to excellent for the 2009 drilling program. Table 5 summarizes significant assay results. They are reported as drill lengths as we have not established the width of the mineralized zone.

Drilling (2011)Table Of Contents. During June through September 2011 we conducted a combined RC/diamond drill program on the Farellon property. The program was designed to continue to expand on the results of the 2009 drill program, as well as to continue confirming historical results along the strike. During this program we completed 11 drillholes for a total of 2,233m. Significant results of assays from the 2011 drill program are presented in the Table 6 below.

Table 6: Farellon drilling results (2011)

| Drill Hole ID | Assay interval (m) | Assay grade |

| From | To | Length | Copper % | Gold g/t |

| FAR-11-001 | 36 | 49 | 13 | 2.51 | 0.35 |

| FAR-11-001 | 78 | 85 | 7 | 0.43 | 0.04 |

| FAR-11-002 | No Significant Intersections . Zone faulted off |

| FAR-11-003 | 150 | 155 | 5 | 0.40 | 0.28 |

| FAR-11-003 | 177 | 182 | 5 | 0.44 | 0.15 |

| FAR-11-004 | 141 | 145 | 4 | 0.73 | 0.01 |

| FAR-11-005 | 124 | 133 | 9 | 0.84 | 0.26 |

| FAR-11-006 | 80 | 112 | 32 | 1.35 | 0.99 |

| FAR-11-007 | 56 | 74 | 18 | 0.50 | 0.40 |

| FAR-11-008 | 98 | 102 | 4 | 0.85 | 0.26 |

| FAR-11-009 | 202 | 211.55 | 9.55 | 0.95 | 0.42 |

| FAR-11-010 | 179.13 | 183 | 3.87 | 0.50 | 0.39 |

| FAR-11-011 | 54 | 56 | 2 | 0.97 | 0.48 |

| | | Assay interval (m) | | | Assay grade | |

| Drill Hole ID | | From | | | To | | | Length | | | Copper % | | | Gold g/t | |

| FAR-11-001 | | | 36 | | | | 49 | | | | 13 | | | | 2.51 | | | | 0.35 | |

| FAR-11-001 | | | 78 | | | | 85 | | | | 7 | | | | 0.43 | | | | 0.04 | |

| FAR-11-002 | | No Significant Intersections . Zone faulted off | |

| FAR-11-003 | | | 150 | | | | 155 | | | | 5 | | | | 0.40 | | | | 0.28 | |

| FAR-11-003 | | | 177 | | | | 182 | | | | 5 | | | | 0.44 | | | | 0.15 | |

| FAR-11-004 | | | 141 | | | | 145 | | | | 4 | | | | 0.73 | | | | 0.01 | |

| FAR-11-005 | | | 124 | | | | 133 | | | | 9 | | | | 0.84 | | | | 0.26 | |

| FAR-11-006 | | | 80 | | | | 112 | | | | 32 | | | | 1.35 | | | | 0.99 | |

| FAR-11-007 | | | 56 | | | | 74 | | | | 18 | | | | 0.50 | | | | 0.40 | |

| FAR-11-008 | | | 98 | | | | 102 | | | | 4 | | | | 0.85 | | | | 0.26 | |

| FAR-11-009 | | | 202 | | | | 211.55 | | | | 9.55 | | | | 0.95 | | | | 0.42 | |

| FAR-11-010 | | | 179.13 | | | | 183 | | | | 3.87 | | | | 0.50 | | | | 0.39 | |

| FAR-11-011 | | | 54 | | | | 56 | | | | 2 | | | | 0.97 | | | | 0.48 | |

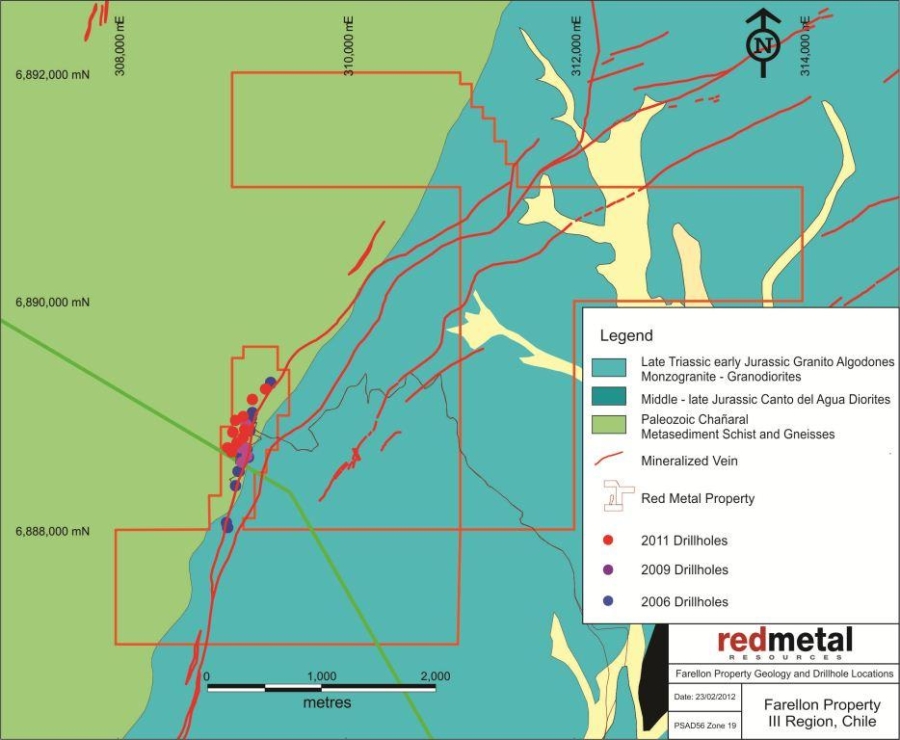

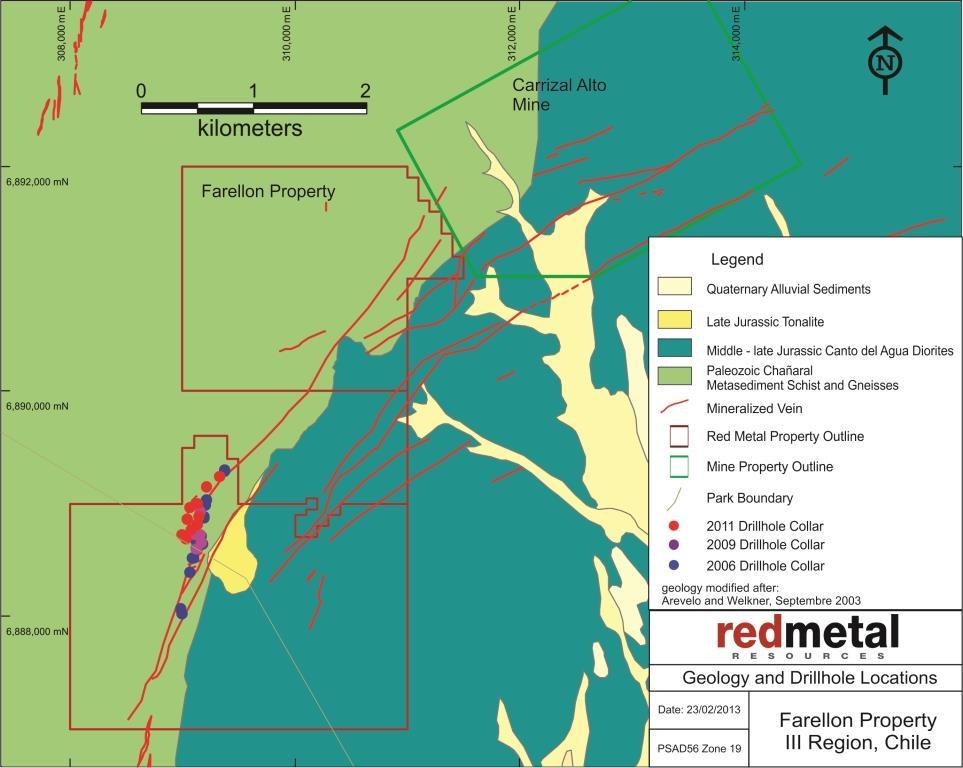

Figure 3 below illustrates the Farellon geology and the 2006, 2009 and 2011 drillhole collar locations as well as surface traces of mineralized vein systems:

Figure 3: Farellon property geology

QA/QC, sampling procedures and analytical methods. Samples were taken at intervals between 0.5 and 2 metres. Sampling started at the collar of the hole and proceeded to the toe or bottom of the drill hole. Samples were taken at two metre intervals outside the previously identified main zone of interest. Through the main zone of interest samples were taken at one metre intervals. Generally, the sample recovery was good to excellent for the 2011 drilling program. Table 56 above summarizes significant assay results. They are reported as drill lengths as we have not established the width of the mineralized zone.

Our quality assurance, quality control (QA/QC) protocol consists of the addition of standards, blanks and laboratory duplicates to the sample stream. We inserted these into the sample series using the same number sequence as the samples themselves. One of the QA/QC check samples is inserted every 25 samples and it alternates between standards, blanks and laboratory duplicates.

perth propertySpring 2012 mapping program: In April of 2012 we completed a detailed mapping, prospecting and rock sampling program over the Farellon Property. This program was designed to extend the known mineralized zone to the north and the south and to identify the best potential to expand on the known mineralized zone. As a result of the mapping program, new ground was acquired at public auction in August 2012 to cover the strike extent of the mineralized veins.

Perth Property

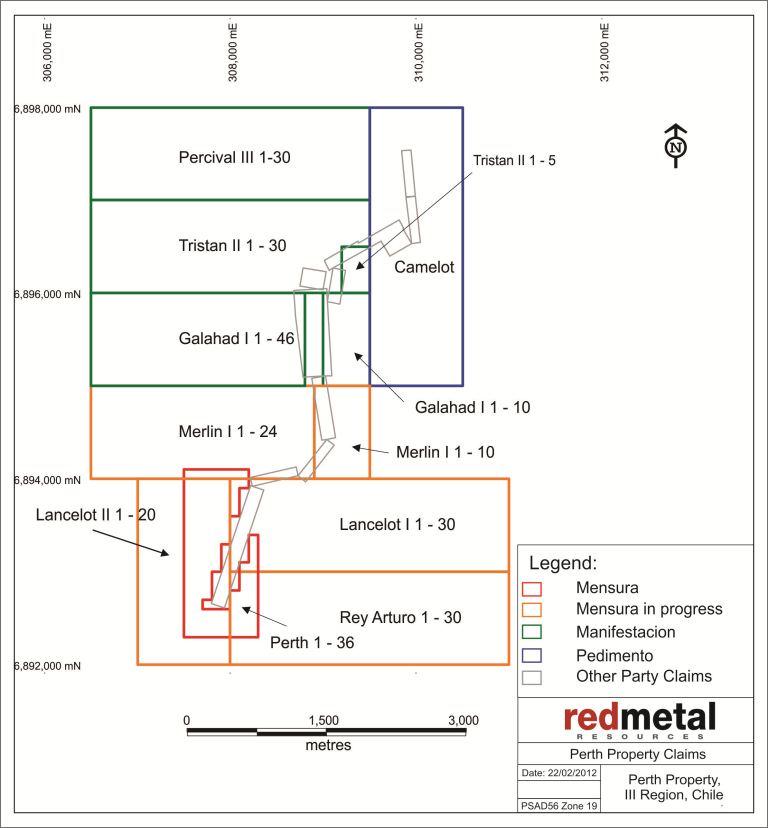

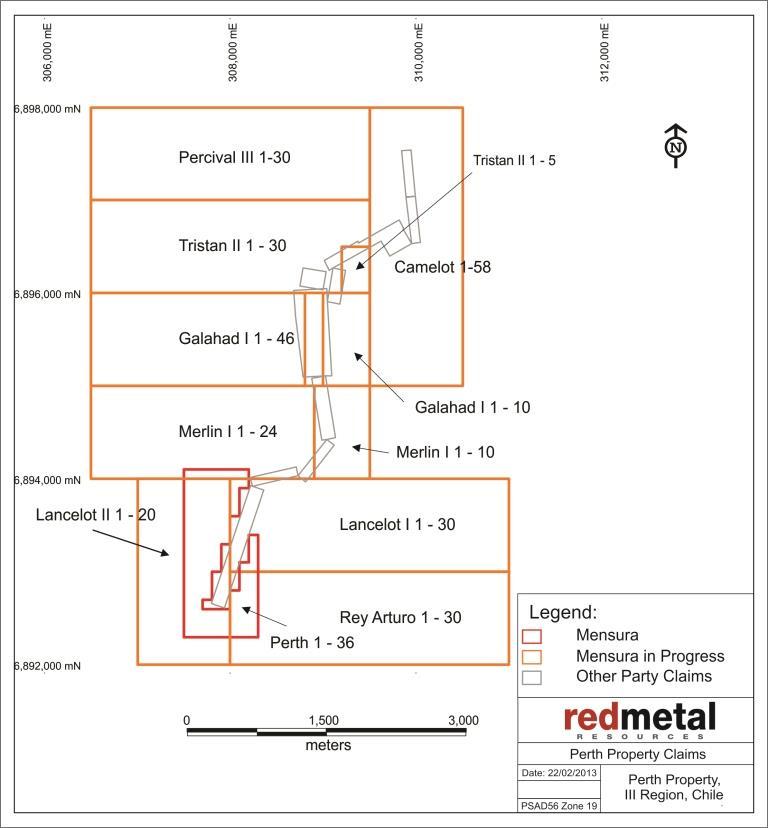

On March 10, 2011, we purchased for $35,000 a group of 12 claims (the Perth)“Perth”) as described in Table 7 and illustrated in Figure 4.

Table 7: Perth property

ClaimTable 7: Perth property | | | | |

| | | Type | |

| Claim | | | Mensura /Mensura in process (ha) | | | | Manifestacion (ha) | |

| Perth 1 al 36 claim | | | 109 | | | | | |

| Lancelot I 1 al 30 claim | | | 300 | | | | | |

| Lancelot II 1 al 20 claim | | | 200 | | | | | |

| Rey Arturo 1 al 30 claim | | | 300 | | | | | |

| Merlin I 1 al 10 claim | | | 60 | | | | | |

| Merlin I 1 al 24 claim | | | 240 | | | | | |

| Galahad I 1 al 10 claim | | | 50 | | | | | |

| Galahad I 1 al 46 claim | | | 230 | | | | | |

| Percival III 1 al 30 claim | | | 300 | | | | | |

| Tristan II 1 al 30 claim | | | 300 | | | | | |

| Tristan IIA 1 al 5 claim | | | 15 | | | | | |

| Camelot | | | | | | | 300 | |

| | | 2,104a | | | | 300a | |

|

aSome claims overlap others, reducing our net area to 2,283 hectares. See Figure 4.

Figure 4. The Perth property

Figure 4. The Perth property

The Perth property is adjacent to the west side of the historic Carrizal Alto mine and lies approximately 3.5 kilometers north of our Farellon project. It is a 45 minute drive from Vallenar city, with major road access, power and water supply close by. The project lies on a similar geologic contact as the Farellon and Carrizal Alto properties.

Location and means of access. The Perth property is centered about 308,750 east and 6,895,000 south UTM PSAD56 Zone 19 approximately 75 km northwest of the city of Vallenar with the highest point at approximately 925 meters above sea level. The property is accessible by road from Vallenar. The Perth Caliza Property is accessed by taking the Pan American Highway north from Vallenar for 20 kilometres, then turning west onto the road to Canto del Agua a distance of 35 kilometres. Then take the Cardones Canyon road for 15 kilometres, turn southwest towards Cerro Cachina Grande along a secondary gravel road for 14 kilometres to the property.

Exploration history. Exploration programs on the Perth property have historically been limited to surface sampling and mapping programs completed in 2007 and 2008. Mapping identified 12 individual veins on surface, significantSignificant results from historic channel samples across the veins are showshown in Table 8. Numerous artisanal mine workings on the property have previously been exploited for both copper and gold; however, no records of grade or tonnage can be located.

| Table 8: Perth historic significant intersections | |

| SAMPLE | | | Au g/t | | | Cu % | | | Co% | | | Length of Sample (m) | |

| | 521617 | | | | 2.5 | | | | 0.39 | | | | 0.03 | | | | 1.0 | |

| | 521796 | | | | 2.5 | | | | 0.21 | | | | 0.00 | | | | 1.0 | |

| | 521629 | | | | 2.8 | | | | 0.76 | | | | 0.19 | | | | 3.5 | |

| | 56905 | | | | 3.1 | | | | 1.00 | | | | 0.19 | | | | 1.0 | |

| | 521610 | | | | 3.5 | | | | 0.30 | | | | 0.02 | | | | 0.5 | |

| | 521622 | | | | 4.5 | | | | 1.72 | | | | 0.02 | | | | 1.0 | |

| | 521788 | | | | 4.5 | | | | 0.19 | | | | 0.00 | | | | 2.0 | |

| | 56858 | | | | 5.0 | | | | 0.42 | | | | 0.16 | | | | 1.0 | |

| | 521789 | | | | 5.5 | | | | 0.29 | | | | 0.00 | | | | 2.0 | |

| | 521628 | | | | 6.2 | | | | 0.59 | | | | 0.14 | | | | 1.3 | |

| | 521609 | | | | 10.7 | | | | 0.35 | | | | 0.07 | | | | 1.0 | |

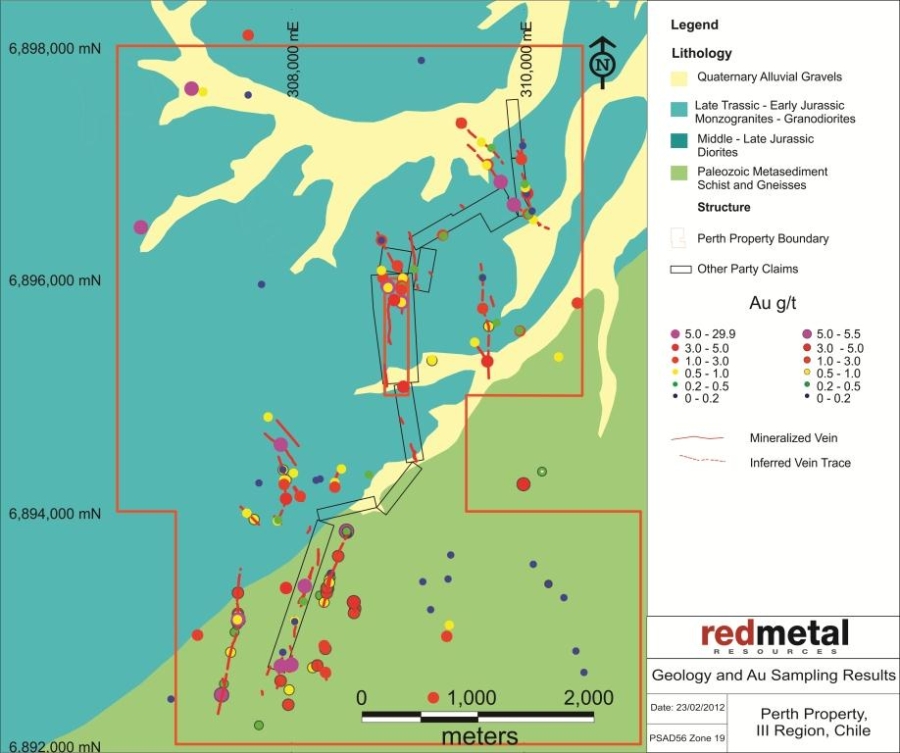

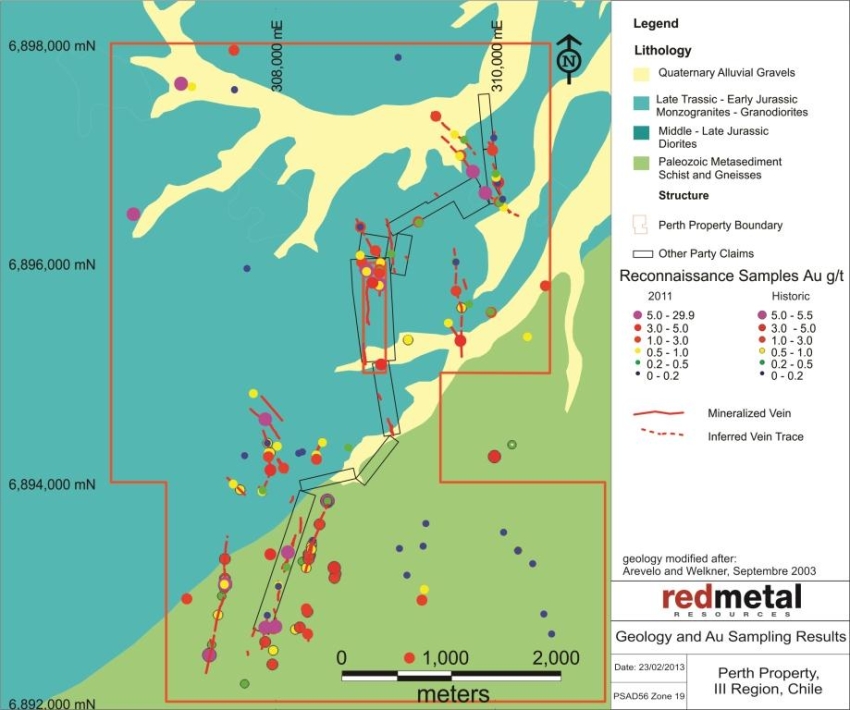

GeologyGeology. The Perth property overlies the contact between Paleozoic metamorphic sediments and a Cretaceous tonalitic batholith. A swarm of north northeast trending fault related copper gold bearing quartz veins crosscuts the property. Surface mapping and sampling records show twelve veins identified so far on the south end of the property. The veins average two metres wide but have been measured up to six metres wide.

In spring of 2011 we completed a reconnaissance mapping and sampling program on the Perth property. Geological mapping during the program identified four major areas where mineralization in veins appear to be concentrated. Sampling consisted of 129 reconnaissance samples taken of vein material where veins outcropped at surface. Significant results are summarized in Table 9 below.

Table 9: Perth 2011 significant reconnaissance samples | |

| SAMPLE | | | Au g/t | | | Cu % | |

| | 0003 | | | | 7.47 | | | | 1.73 | |

| | 0010 | | | | 7.37 | | | | 3.63 | |

| | 0016 | | | | 8.86 | | | | 2.29 | |

| | 0017 | | | | 29.93 | | | | 1.1 | |

| | 0033 | | | | 21.66 | | | | 2.85 | |

| | 0042 | | | | 0.9 | | | | 7.74 | |

| | 0077 | | | | 10.2 | | | | 2.43 | |

| | 0078 | | | | 8.39 | | | | 3.78 | |

| | 0097 | | | | 4.42 | | | | 0.14 | |

| | 0098 | | | | 10.27 | | | | 0.51 | |

| | 0099 | | | | 3.61 | | | | 0.19 | |

| | 0100 | | | | 6.37 | | | | 0.22 | |

| | 0110 | | | | 22.58 | | | | 1.51 | |

| | 0121 | | | | 11.12 | | | | 3.9 | |

Figure 5 below illustrates the Perth geology as well as the 2007historic and 2011 reconnaissance sample gold g/t assay results:

Figure 5 Perth Property Geology

TerminationMemorandum of Perth property joint venture earn-in agreementUnderstanding with Geoactiva Spa.

On March 14, 2011,February 11, 2013, we entered into ana Memorandum of Understanding (“MOU”) with Geoactiva Spa. The MOU confirmed Geoactiva’s intention to acquire 100% of the Perth mineral claims through the execution of a mining option purchase agreement on(the “Option Agreement”). Terms of the MOU are summarized below:

1. Option price. In order to maintain the option to purchase and to acquire the Perth property, with Revonergy Inc. Revonergy Inc. paid $35,000 on signingGeoactiva must pay us the agreement, which allowed Revonergy to earn a 35% interesttotal amount of $1,000,000 USD in the following instalments:

| | | |

| | Payment Price US$ | |

| Upon execution of Option Agreement (“Execution date”) | | | 37,500 | |

| 6 months after Execution date | | | 37,500 | |

| 12 months after Execution date | | | 50,000 | |

| 18 months after Execution date | | | 50,000 | |

| 24 months after Execution date | | | 100,000 | |

| 30 months after Execution date | | | 100,000 | |

| 36 months after Execution date | | | 125,000 | |

| 42 months after Execution date | | | 250,000 | |

| 48 months after Execution date | | | 250,000 | |

| Total | | | 1,000,000 | |

All of the above payments shall be made only if Geoactiva wishes to keep the Option Agreement in force and finally to exercise the option to purchase.

Upon exercise of the Option Agreement and once the commercial production begins, Geoactiva will pay us NSR of 1.5% from the sale of gold, copper, and cobalt extracted from the Perth property if it spent a minimumproperty. At any time after the exercise of $1,450,000 on a three phasethe Option Agreement and Geoactiva’s fulfilment of the investment commitment of $3,500,000 in exploration program,expenditure, Geoactiva may purchase 100% NSR as follows:

| · | Successful completion of a Phase I exploration program costing at least $115,000 one year from signing |

Gold: paying US $5 per inferred ounce of gold, according to the definition of Inferred Mineral Resource in the CIM Definition Standards on Mineral Resources and Mineral Reserves

Copper: US $0.005 per inferred ounce of copper, according to the definition of Inferred Mineral Resource in the CIM Definition Standards on Mineral Resources and Mineral Reserves

Cobalt: If Geoactiva acquires the NSR with respect to gold, copper, or both, the NSR relating to cobalt will be terminated

Upon execution of the Option Agreement, Geoactiva will incur exploration expenditures, as follows:

| | · | Successful completion of a Phase II exploration program costing at least $300,000 two years | |

| | US$ | |

Within 12 months from signingexecution date | | | 500,000 | |

| 12-24 months from execution date | | | 1,000,000 | |

| 24-36 months from execution date | | | 1,000,000 | |

| 36-48 months from execution date | | | 1,000,000 | |

| Total | | | 3,500,000 | |

| · | Successful completion of a Phase III exploration program costing at least $1,000,000 and that can justify completing a preliminary feasibility study three years from signing |

If Geoactiva fails to incur the required exploration expenditures during a specific period it may fulfill its obligations by paying us the outstanding amount in cash.

Revonergy failed2. Due diligence. Geoactiva had 60 days (“Due Diligence Period”) from February 11, 2013, to complete Phase Iconduct the legal, technical, and other background review of the exploration program withinPerth property. On April 5, 2013, we extended the term specified, thereforeDue Diligence Period until May 11, 2013. At any time during the agreement has terminated.Due Diligence Period, Geoactiva may communicate in writing of its decision to execute the Option Agreement. During the Due Diligence period and until the execution of the Option Agreement, we agreed to provide exclusivity rights to Geoactiva and refrain from any negotiations with third parties.

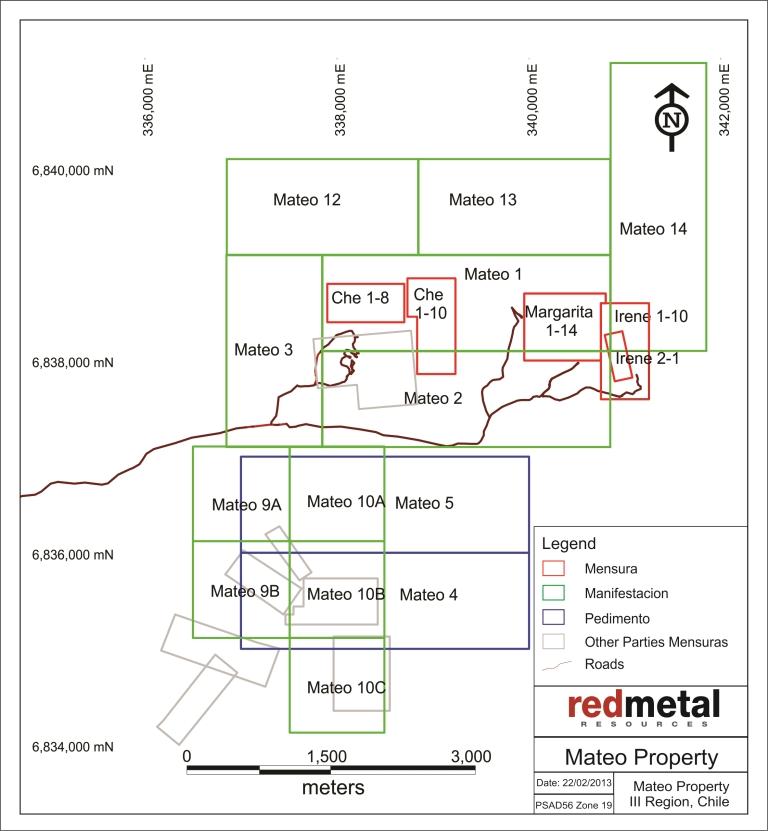

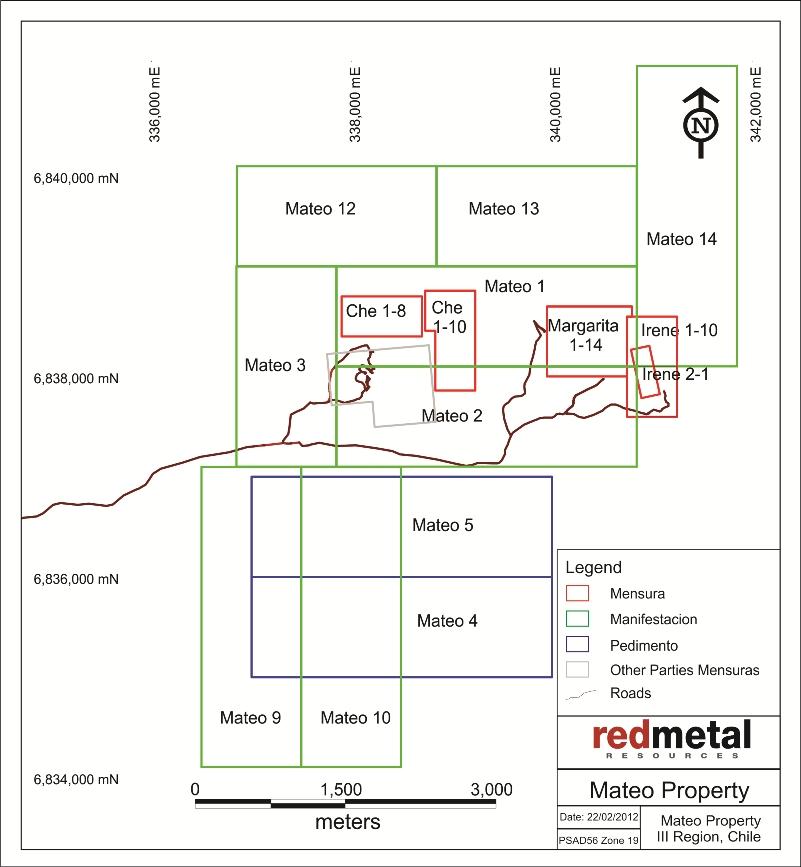

mateo propertyMateo Property

We have assembled a group of claims: the Che Uno and Che Dos, the Margarita, and the Irene Uno and Irene Dos mining claims, and the Mateo exploration claims as described in Table 910 and illustrated in Figure 6. The Mateo exploration claims overlap the Che, Margarita and Irene claims to secure the areas around the claims. Some of them may overlap others’ prior claims. We will acquire rights to these overlapped prior claims only if the owners forfeit their rights, and we will exercise our rights only if we want the property. We acquired all of these claims for the same geological reasons and consider them one property, which we call the Mateo property.

| Table 10: Mateo property | |

| Claim | | Type | |

| | Mensura (ha) | | | Mensura in processa (ha) | | | Pedimentoa (ha) | |

| Che Uno 1 – 8 | | | 32 | | | | | | | |

| Che Dos 1 – 10 | | | 44 | | | | | | | |

| Margarita 1 – 14 | | | 56 | | | | | | | |

| Irene Uno 1 – 2 | | | 10 | | | | | | | |

| Irene Dos 1 – 10 | | | 50 | | | | | | | |

Mateo 1, 2, 3, 9,10,12, 13, 14 | | | | | | | 2,100 | | | | |

| Mateo 4 | | | | | | | | | | | 300 | |

| Mateo 5 | | | | | | | | | | | 300 | |

| | | | 192 | | | | 2,100 | | | | 600 | |

| | |

a Some of the claims are staked over the mensuras to claim the ground surrounding them. See Figure 6.

| Table 9: Mateo property |

| Claim | Type |

Mensura (ha) | Manifestaciona (ha) | Pedimentoa (ha) |

| Che Uno 1 – 8 | 32 | | |

| Che Dos 1 – 10 | 44 | | |

| Margarita 1 – 14 | 56 | | |

| Irene Uno 1 – 2 | 10 | | |

| Irene Dos 1 – 10 | 50 | | |

| Mateo 1 | | 300 | |

| Mateo 2 | | 300 | |

| Mateo 3 | | 200 | |

| Mateo 4 | | | 300 |

| Mateo 5 | | | 300 |

| Mateo 9 | | 300 | |

| Mateo 10 | | 300 | |

| Mateo 12 | | 200 | |

| Mateo 13 | | 200 | |

| Mateo 14 | | 300 | |

| | 192 | 2,100 | 600 |

a Some of the claims are staked over the mensuras to claim the ground surrounding them. See Figure 6. |

Figure 6: Mateo property

che uno and che dos claims

On October 10, 2008 Minera Farellon Limitada granted us the option to purchase the Che Uno and Dos claims. The Che claims cover 76 hectares centered about 339,002 east and 6,838,450 south UTM PSAD56 Zone 19. They are in the northwest corner of the Mateo property. On April 12, 2011 we completed the acquisition of the Che claims by paying approximately $20,000 to Minera Farellon.

We continue to owe a royalty equal to 1% of the net proceeds that we receive from the processor to a maximum of $100,000 with no monthly minimum when we start exploiting the minerals we extract from the claim. We have not yet exploited the claim.

margarita claim

We bought the Margarita mining claim on November 27, 2008 through a public auction and at January 31, 2012 had spentfor a total of $17,528 (including legal and registration costs) for this claim.$15,984. The Margarita claim covers 56 hectares centered around 340,353 east and 6,838,347 south UTM PSAD56 Zone 19 located within the northeast corner of the Mateo claim.

irene uno and irene dos claims

On September 7, 2010, we entered into a purchase agreement with Minera Farellon to buy the Irene Uno and Irene Dos mining claims. Under the terms of the agreement, as amended, we paid $45,174 (equivalent of 21 million Chilean pesos) on May 10, 2011 to exercise the option and purchase the Irene claims. The Irene claims cover 60 hectares centered about 341,002 east and 6,838,101 south UTM PSAD56 Zone 19, are located within the northeast corner of the Mateo property, and share their western border with the Margarita claim.

mateo claims

The Mateo claims consist of eight manifestacionesmensura in process — Mateo 1 –3, 9-10,through 3, 9,10, and 12 –through 14, and two pedimentos — Mateo 4 and 5, covering 2,220 hectares, which we staked between November 2008 and November 2011. The claims are centered about 337,675 east and 6,837,600 south UTM PSAD56 Zone 19 and cover a five-kilometer strike length of intensely altered volcanics with significant massive sulphide mineralization.

Location and means of access. The Mateo property is centered about 337,675 east and 6,837,600 south UTM PSAD56 Zone 19 approximately 10 kilometers east of Vallenar with the highest point at approximately 1,050 meters above sea level. A well-used road leads from the city of Vallenar and crosses through the middle of the west half of the properties and along the southern border of the east half of the properties. Many unmarked dirt roads in the area provide reliable access to most areas of Mateo.

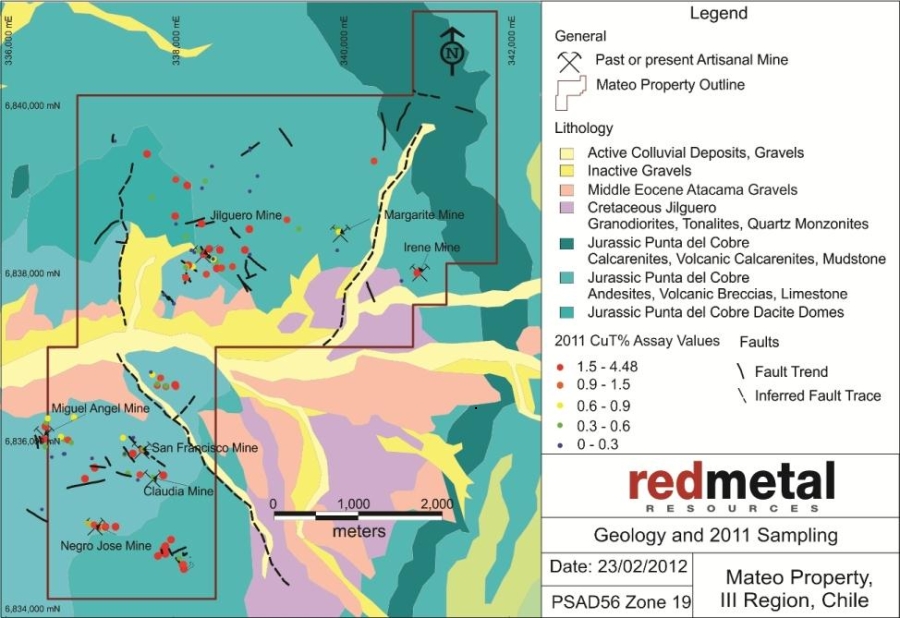

Description. The Mateo property is a copper-gold-silver project that lies in the Candelaria IOCG belt in the Chilean Coastal Cordillera. The Mateo property has undergone limited modern exploration including surface and underground RC drilling and artisanal mining on three separate mine sites, the Irene, Margarita and Santa Theresa mines. We have reviewed all available records of work completed to date, including some records of the mining activity. Our interpretation of the work completed to date indicates the potential for an economic ore body in mineralized mantos and skarn-style mineralization associated with IOCG deposits.

Exploration history. Historical work includes several drill programs completed by different Chilean private and public companies. Records exist from eight drillholes completed in 1994 on the Irene mine and include two full reports written by ENAMI (the Chilean national mining company) with interpretation of mineralization and recommendations for further exploration and mining work.

The Irene mine was investigated by ENAMI in 1994. Work completed during this time included surface RC drilling, including 490 meters in four RC drillholes, and underground diamond drilling, including 220 meters in four drillholes. We obtained ENAMI’s reports of mining activities from 1994 through 1997. Approximately 11,875 tonnes of rock were mined in that time averaging 4.3% copper, 61.9 grams per tonne silver, and 1.01 grams per tonne gold. During the period from June 2009 to December 2010 the vendor of the Irene, Minera Farellon, conducted small scale mining activities on a different area of the Irene claims and mined 1,705 tonnes grading 1.39% Cu, 1.39g/t Ag, 0.29g/t Au in sulphides and 1,477 tonnes grading 1.98% Cu in oxides. The difference in grade between the historic work and the recent work is not an indication that further high grade material will not be found on the Mateo property and further modeling and exploration work needs to be completed to determine the best place to drill.

A private Chilean company, Minera Taurus, drilled 16 RC holes on the east end of the Irene claim, but we have no record from this drilling. An unknown company built a portal 250 meters long and approximately three meters wide by three meters high. The portal leads to three mined-out chimneys connected to the surface providing ventilation channels. On a recent property visit with ENAMI’s geologists, we found an extension of the mineralized zone at the base of the tunnel below showing the potential for mineral resources.

Geology. Geologically, the Mateo property is located within the brittle-ductile north-south-trending Atacama Fault System that is known to host many of the major deposits in the Candelaria IOCG belt. Known mineralization is hosted in an andesitic volcaniclastic sequence assigned to the Bandurrias Formation. Widespread iron oxide and potassic alteration indicates an IOCG mineralizing system further supported by significant amounts of economic grade mineralization.

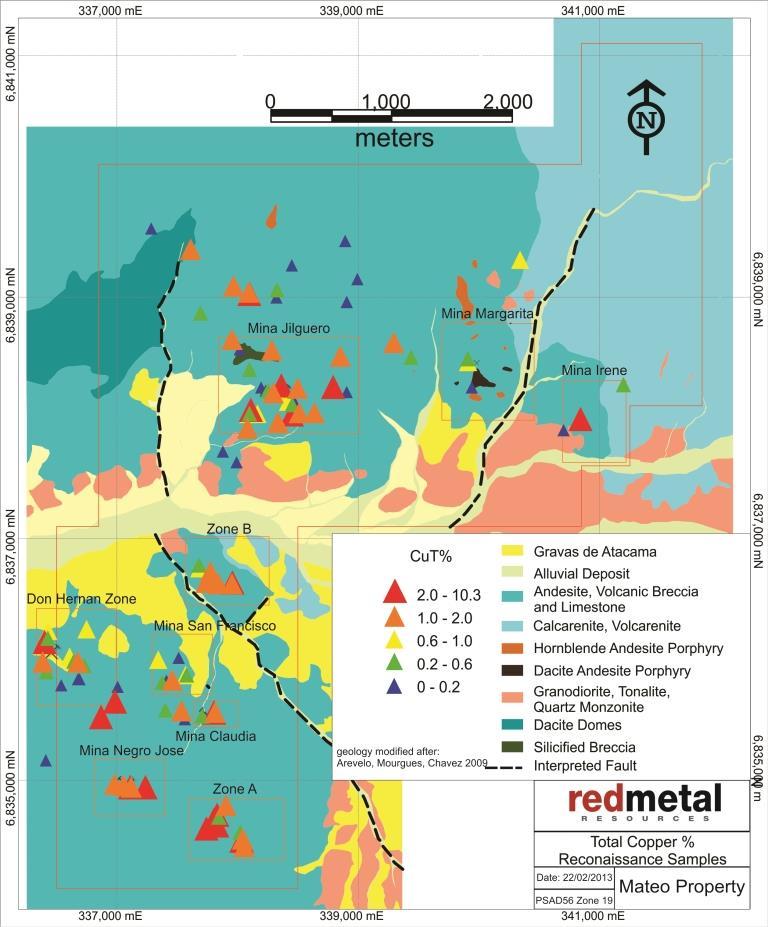

Exploration (2011). During August through October 2011 we carried out an in-depth geological mapping and sampling program on the Mateo property. The Mateo property has very diverse mineralization styles through the property which includes mantos, veins, breccias and porphyries with significant gold and copper. A total of 138 reconnaissance samples were collected over the property. The highest assay values returned from reconnaissance samples were 21g/t Au and 10.3% Cu but more common values were between 1-3g/t Au and 1-3% Cu. Table 1011 summarizes the significant assay results.

Table 10:11: Mateo significant intersections

| Sample | | | Cu% | | | Au g/t | |

| | 201272 | | | | 7.37 | | | | 1.12 | |

| | 202871 | | | | 2.63 | | | | 1.14 | |

| | 202852 | | | | 7.11 | | | | 1.18 | |

| | 202849 | | | | 10.3 | | | | 1.73 | |

| | 201220 | | | | 4.29 | | | | 2.07 | |

| | 201277 | | | | 9.39 | | | | 2.42 | |

| | 202850 | | | | 2.58 | | | | 2.46 | |

| | 202810 | | | | 2.44 | | | | 2.49 | |

| | 202882 | | | | 2.57 | | | | 3.08 | |

| | 202812 | | | | 0.50 | | | | 3.10 | |

| | 202815 | | | | 0.62 | | | | 3.57 | |

| | 202880 | | | | 1.46 | | | | 5.70 | |

| | 202826 | | | | 5.30 | | | | 6.85 | |

| | 201217 | | | | 3.46 | | | | 10.11 | |

| | 202813 | | | | 0.69 | | | | 21.72 | |

The detailed mapping identified nine significant mineralized zones where further work is recommended.

Figure 7 below illustrates the local Mateo geology including a thematic map of 2011 reconnaissance sample locations and corresponding percent copper assay ranges.

Figure 7: Mateo property geology

2011 Ground Magnetic Survey

During the month September 2011, we engaged Quantec International Project Services Ltd. to complete a ground magnetic survey on the Mateo Property. The ground magnetic survey consisted of 70 survey lines with an E-WEW orientation, and two control lines with a N-SNS orientation. The survey lines were separated by 100m, and data was collected at 10 m10m intervals on all lines. A total of 218.49 km218.49km of magnetic data was collected. The survey outlined areas of high and low magnetic response. Areas of high magnetic response indicated the presence of elevated levels of magnetic minerals such as magnetite, pyrotite and hematite whereas areas of low magnetic response may be caused by alteration processes such as magnetite destruction or may simply indicate rock types that never had magnetic minerals.

This ground magnetic survey demarcated the northern and western extent with a large, high magnetic anomaly with a southwest to northeast orientation. This magnetic high may correlate with the Jilguero Intermediate Intrusive formation which is only partially exposed on the property and underlies the Jurassic Punta Del Cobre volcanics, and mixed sedimentary sequence.

Two possible correlations with geology are drawn when looking at the magnetic geophysical response. Firstly, all artisanal mines, reconnaissance samples and documented surface mineralization isare exposed on the Western edge of the magnetic high in an area where magnetic high-low gradients are greatest transitioning from high to low. Secondly, magnetic highs appear to persist away from the main magnetic high body in a NW direction. Although these persisting magnetic highs are only small stringers in appearance they possibly correlate to dominant NW trending faults on the property that are often mineralized. Visual correlations between magnetic high/low contrasts and geology seem strong enough to suggest further exploration including sampling and drilling along the steepest gradient of magnetic high/low dropoff.

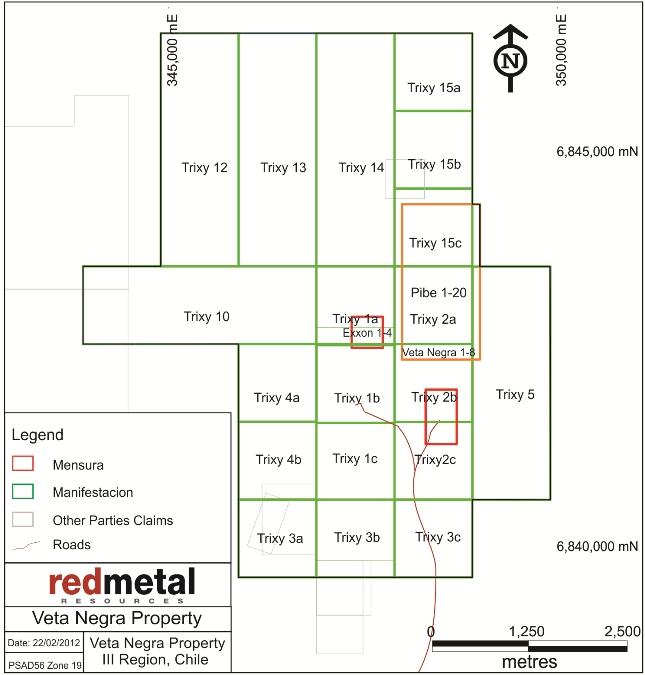

veta negra

The Veta Negra property is made up of 19 Trixy exploration claims and three mining claims.

Table 11: Veta Negra property.

| Claim | Mensura (ha) | Manifestaciona (ha) |

| Veta Negra 1-7 | 28 | |

| Exxon 1-4 | 16 | |

| Pibe 1-20 | 200 | |

| Trixy 1 (a,b,c) | | 300 |

| Trixy 2 (a,b,c) | | 300 |

| Trixy 3 (a,b,c) | | 300 |

| Trixy 4 (a,b) | | 200 |

| Trixy 5 | | 300 |

| Trixy 10 | | 300 |

| Trixy 12 | | 300 |

| Trixy 13 | | 300 |

| Trixy 14 | | 300 |

| Trixy 15(a,b,c) | | 300 |

| | 244 | 2,900 |

a Figure 8 below illustrates the Veta Negra claims. |

Figure 8: Veta Negra property

pibe claims

On November 25, 2011, we entered into an option to purchase agreement with Manuel Antonio Cortez Araya to purchase the Pibe 1 - 20 mining claims. The Pibe claims are located in Sierra la Chinchilla, community of Vallenar, Province of Huasco, Region of Atacama; they cover 200 hectares with UTM coordinates: East 348,500,000, North 6,843,300,000. The option to purchase has a term of 36 months, requiring us to make semi-annual payments totaling $500,000. We made our first payment of $40,000 on December 12, 2011.

The claims are also a subject to a 1.5% royalty on the net proceeds that we receive from the processor to a maximum of $1,000,000 with no monthly minimum. The payments are due once exploitation begins. We have not yet exploited the claim.

veta negra and exon claims

On June 30, 2011, we entered into an agreement with Minera Farellon to acquire its options to purchase the Veta Negra and Exon mining claims and the Trixy exploration claims for $107,500. Under the terms of the option, we agreed to transfer our interest in several generative claims with the net book value of $4,504. The claims are subject to a 1.5% royalty on the net sales of minerals extracted to a total of $500,000. The royalty payments are due monthly once exploitation begins. At January 31, 2012, we paid $10,000 in option payments and capitalized an additional $8,480 as cost of transferred generative claims.

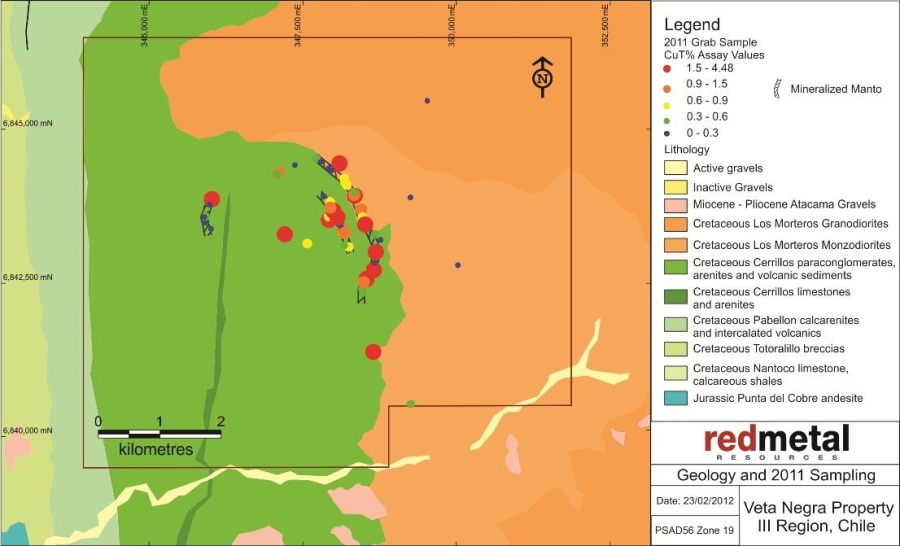

Location and means of access

The Veta Negra property is accessed from Vallenar by driving the Relincho, San Antonio, Los Morteros road east out of Vallenar along the Quebrada Jilgeuro Canyon to the 21km marker (before one reaches the village of San Antonio), there is black spray paint on rocks by the side of the road indicating the way to the Veta Negra and Exon mines at the UTM coordinates: East 338,097, North 6,839,203 at an altitude of 1,079 m above sea level. At this point turn north and drive for approximately 4 km until arriving at the Veta Negra artisanal mine.

The Veta Negra property is located approximately 25km from the Empresa Nacional de Mineria (ENAMI) crushing and processing facility.

Description

The Veta Negra property is a copper-gold project that lies in the Candelaria IOCG belt in the Chilean Coastal Cordillera. The Mateo property has undergone limited modern exploration, in the form of near surface artisanal mining. Mineralization occurs in tabular mantos or veins which trend approximately North-South through the property. There are 3 recognized mantos of approximately 4-6m in thickness, the longest of which extends for 2km on surface. The depth to which these mantos extend is unknown at this time. Supergene copper and gold mineralization within these mantos is very conspicuous as chrysocolla, malachite, atacamite, chalcocite, and minor cuprite. Sampling and mapping has been undertaken throughout the property

Exploration history

The Veta Negra property has been artisanally mined on the two mining concessions on the property, the Veta Negra 1-8 and Exxon 1-4 concessions. Many small pits and excavations on the property that do not have records of tonnage or grade are evident all along the surface traces of the exposed mantos.

Geology

The mineralization on the Veta Negra property is hosted in the middle Cretaceous Cerrillos formation composed of brecciated, flow, tuff, microcrystalline andesite, arenites and conglomerates. Abundant copper oxide mineralization is found on surface in distinct veins or ‘mantos’ deposited at the upper contact of a black altered andesite and an overlying vesicular iron oxidized andesite (some vesicular volcanics in the area exhibit hornfel metamorphic facies).

Primary structures on the Veta Negra property are made up of regional scale Cretaceous extension faults which predominantly dip to the East at 30-50 degrees. These faults likely provided accommodation space and fluid pathways along contacts of the Cerrillos volcanic units. There is also evidence of anticline structures which are not fully understood and later dip slip fault offsets seen where the mantos exhibit minor offset along strike.

Younger upper Cretaceous – Eocene intermediate composition Granodiorites and Monzonites are found in the Eastern and Northern region of the Veta Negra claim in contact with the Cerrillos volcanics to the South and West. These later units may have provided the hydrothermal heat and fluid source to produce mineralization which could have been injected into the faulted Cerrillos volcanics.

Beyond the claim boundaries to the West lies the lower Cretaceous Pabellon and Totoralillo bioclastic carbonates, volcanic and conglomerate formations. Beyond these formations – a few kilometers still - lies the Jurassic - lower Cretaceous Punta Del Cobre or Bandurrias formation composed of Dacites, andesites and carbonates.

Exploration (2011)