UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

| | |

(Mark One) |

þx | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20112013

Or

|

| | |

or |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

|

For the transition period from to

Commission file number: 000-53206File Number: 001-35568 (Healthcare Trust of America, Inc.)

Commission File Number: 333-190916 (Healthcare Trust of America Holdings, LP)

HEALTHCARE TRUST OF AMERICA, INC.

HEALTHCARE TRUST OF AMERICA HOLDINGS, LP

(Exact name of registrant as specified in its charter)

|

| |

| Maryland (Healthcare Trust of America, Inc.) | 20-4738467 |

Delaware (Healthcare Trust of America Holdings, LP) | 20-4738347 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| |

16435 N. Scottsdale Road, Suite 320, Scottsdale, Arizona | 85254 |

| (Address of principal executive offices) | 85254

(Zip Code) |

Registrant’s telephone number, including area code: (480) 998-3478

Securities registered pursuant to Section 12(b) of the Act:

|

| |

| Title of each class | Name of each exchange on which registered |

NoneClass A common stock, par value $0.01 per share | NoneNew York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.01 par value per shareNone

(TitleIndicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of Class)the Securities Act.

|

| | | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405Healthcare Trust of the Securities Act.America, Inc. | Yesx ¨Yes

| No¨ þNo

| |

| Healthcare Trust of America Holdings, LP | ¨ Yes | x No | |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

|

| | | |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d)Healthcare Trust of the Act.America, Inc. | Yes¨ ¨Yes

| Nox þNo

| |

| Healthcare Trust of America Holdings, LP | ¨ Yes | x No | |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

|

| | | |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d)Healthcare Trust of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.America, Inc. | Yesx þYes

| No¨ ¨No

| |

| Healthcare Trust of America Holdings, LP | x Yes | ¨ No | |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

|

| | | |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405Healthcare Trust of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).America, Inc. | Yesx þYes

| ¨ No | |

| Healthcare Trust of America Holdings, LP | x Yes | ¨ No | |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

|

| |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. | þ |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

| | | |

Large accelerated filer | ¨ | Accelerated filer | ¨ |

Non-accelerated filerHealthcare Trust of America, Inc. | þLarge-accelerated filer (Dox

| Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ |

| | | (Do not check if a smaller reporting company) | |

| Healthcare Trust of America Holdings, LP | Large-accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer x | Smaller reporting company¨ |

| ¨ | | (Do not check if a smaller reporting company) | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

|

| | | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2Healthcare Trust of the Act).America, Inc. | Yes¨ ¨Yes

| Nox þNo

| |

| Healthcare Trust of America Holdings, LP | ¨ Yes | x No | |

While there is no established market for the registrant’s common stock, theThe aggregate market value of the registrant’sHealthcare Trust of America, Inc.’s Class A common stock held by non-affiliates of the registrant as of June 30, 2011,28, 2013, the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $1,624,601,000, assuming a market value of $10.00 per share which was$1,879,465,000, computed by reference to the closing price per share in our recently-completed offering.as reported on the New York Stock Exchange.

As of March 23, 2012February 19, 2014, there were 229,502,006237,291,846 shares of Class A common stock of the registrantHealthcare Trust of America, Inc. outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant'sRegistrant’s definitive Proxy Statementstatement for the Annual Meeting of Stockholders to be held in July 2012 are incorporated by reference into Part III, Items 10 through 1410-14 of this Annual Report on Form 10-K.

Explanatory Note

This report combines the Annual Reports on Form 10-K for the year ended December 31, 2013 of Healthcare Trust of America, Inc., a Maryland corporation, and Healthcare Trust of America Holdings, LP, a Delaware limited partnership. Unless otherwise indicated or unless the context requires otherwise, all references in this report to “we,” “us,” “our,” “the Company” or “our Company” refer to Healthcare Trust of America, Inc. and Healthcare Trust of America Holdings, LP, collectively.

Healthcare Trust of America, Inc. (“HTA”) operates as a real estate investment trust, or REIT, and is the general partner of Healthcare Trust of America Holdings, LP (“HTALP”). As of December 31, 2013, HTA owned a 98.94% partnership interest in HTALP, and other limited partners, including some of HTA’s directors, executive officers and their affiliates, owned the remaining partnership interest (including the long term incentive plan, or LTIP, units) in HTALP. As the sole general partner of HTALP, HTA has the full, exclusive and complete responsibility for HTALP’s day-to-day management and control, including its compliance with Securities and Exchange Commission filing requirements.

We believe it is important to understand the few differences between HTA and HTALP in the context of how we operate as an integrated consolidated company. HTA operates in an umbrella partnership REIT structure in which HTALP and its subsidiaries hold substantially all of the assets. HTA’s only material asset is its ownership of partnership interests of HTALP. As a result, HTA does not conduct business itself, other than acting as the sole general partner of HTALP, issuing public equity from time to time and guaranteeing certain debts of HTALP. HTALP conducts the operations of the business and has no publicly traded equity. Except for net proceeds from public equity issuances by HTA, which are generally contributed to HTALP in exchange for partnership units, HTALP generates the capital required through its operations, and by direct or indirect incurrence of indebtedness or through the issuance of partnership units.

Redeemable noncontrolling interests of limited partners, stockholders’ equity and partners’ capital are the primary areas of difference between the consolidated financial statements of HTA and HTALP. Limited partner units in HTALP are accounted for as partners’ capital in HTALP’s consolidated balance sheets and as noncontrolling interest reflected within equity or redeemable noncontrolling interest of limited partners reflected outside of equity in HTA’s consolidated balance sheets. The differences between HTA’s stockholders’ equity and HTALP’s partners’ capital is due to the differences in the equity issued by HTA and HTALP, respectively.

The Company believes combining the Annual Reports on Form 10-K of HTA and HTALP, including the notes to the consolidated financial statements, into this single report results in the following benefits:

enhances stockholders’ understanding of HTA and HTALP by enabling stockholders to view the business as a whole in the same manner that management views and operates the business;

eliminates duplicative disclosure and provides a more streamlined and readable presentation since a substantial portion of the disclosure in this report applies to both HTA and HTALP; and

creates time and cost efficiencies through the preparation of a single combined report instead of two separate reports.

In order to highlight the material differences between HTA and HTALP, this report includes sections that separately present and discuss areas that are materially different between HTA and HTALP, including:

the market for registrant’s common equity, related stockholder matters and issuer purchase of equity securities in Item 5 of this report;

the selected financial data in Item 6 of this report;

the funds from operations and normalized funds from operations in Item 7 of this report;

the controls and procedures in Item 9A of this report;

the consolidated financial statements in Item 15 of this report;

certain accompanying notes to the consolidated financial statements, including Note 3 - Business Combinations, Note 11 - Stockholders’ Equity and Partners’ Capital, Note 13 - Per Share Data of HTA, Note 14 - Per Unit Data of HTALP, Note 18 - Selected Quarterly Financial Data of HTA and Note 19 - Selected Quarterly Financial Data of HTALP;

the certifications of the Chief Executive Officer and the Chief Financial Officer included as Exhibits 31 and 32 to this report; and

the statement regarding the computation of the ratio of earnings to fixed charged included as Exhibit 12.1 to this report.

In the sections of this report that combine disclosure for HTA and HTALP, this report refers to actions or holdings as being actions or holdings of the Company. Although HTALP (directly or indirectly through one of its subsidiaries) is generally the entity that enters into contracts, holds assets, and issues or incurs debt, management believes this presentation is appropriate for the reasons set forth above and because the business of the Company is a single integrated enterprise operated through HTALP.

Healthcare Trust of America, Inc.

(A Maryland Corporation)

HEALTHCARE TRUST OF AMERICA, INC. AND HEALTHCARE TRUST OF AMERICA HOLDINGS, LP

TABLE OF CONTENTS

|

| | |

| | | Page |

|

| | |

| | |

| | |

| | |

| | |

| | |

| | |

|

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

|

| | |

| | |

| | |

| | |

| | |

| | | |

|

| | |

| |

EX-21.1 |

EX-23.1 |

EX-31.1 |

EX-31.2 |

EX-32.1 |

EX-32.2 |

PART I

The use of the words “we,” “us” or “our” refers to Healthcare Trust of America, Inc. (“HTA”), a Maryland corporation, and its subsidiaries, including Healthcare Trust of America Holdings, LP (“HTALP”), a Delaware limited partnership, were incorporated or our operating partnership, except where the context otherwise requires.formed, as applicable, on April 20, 2006.

BUSINESS OVERVIEW

We areHTA is a fully integrated, self-administered and self-managed real estate investment trust, or REIT. We acquire, ownREIT, and operate medical office buildingsone of the largest dedicated owners and other facilities that serve the healthcare industry. Since January 2007, we have been an active, disciplined buyeroperators of medical office buildings in the United States. Our primary objective is to generate stockholder value through consistent and other facilities that serve the healthcare industry, acquiring properties with an aggregate purchase pricegrowing dividends and appreciation of real property value. The Company has invested approximately $2.3$3.0 billion and building key industry relationships with significant healthcare systems and quality tenants. We are one to form a portfolio of the largest owners ofpredominately medical office buildings based onlocated in core, critical locations in key markets throughout the United States that we believe are positioned to provide healthcare services over the long term.

We invest in medical office buildings because we believe they provide stable cash flows with relatively low vacancy risk, while still allowing for potentially higher returns through their exposure to the fast growing healthcare sector. Healthcare is the fastest growing segment of the U.S. economy with expenditures expected to grow 5.9% per annum and account for 19.2% of gross domestic product, or GDP, by 2020 according to the U.S. Centers for Medicare & Medicaid Services. Similarly, healthcare is experiencing the fastest employment growth in the U.S., a trend that is expected to continue through 2020. These high levels of demand are driven by the aging of the U.S. population and the long term impact of the Affordable Care Act. As importantly, these healthcare services are increasingly being provided in the lower cost and more convenient outpatient settings such as medical office buildings.

As of December 31, 2013, our portfolio consisted of 14.1 million square feet of gross leasable area, or GLA, inGLA. Approximately 96% of our portfolio is located on the United States. Ourcampuses of or affiliated with nationally or regionally recognized healthcare systems. We believe these key locations and affiliations create significant demand from healthcare related tenants for our properties. Further, the portfolio is primarily concentrated within major U.S. metropolitan areas and located primarily on or adjacent to campuses of nationally recognized healthcare systems.

As of December 31, 2011, approximately 57% of our annualized base rent was derived from tenants or their parent companies that have a credit rating as determined by a nationally recognized rating agency. Approximately 38% of our annualized base rent was derived from tenants that have an investment grade credit rating as determined by nationally recognized rating agencies, including, but not limited to, Greenville Hospital System, Community Health Systems, Aurora Healthcare, West Penn Allegheny Health System, Indiana University Health, Hospital Corporation of America, and Banner Health. As of December 31, 2011, our portfolio contains approximately 11.2 million square feet of GLA with an occupancy rate of approximately 91%, including leases signed but which have not yet commenced. Approximately 95% of our portfolio (based on GLA) is located on, adjacent to, or anchored by the campuses of nationally and regionally recognized healthcare systems. Our portfolio is diversified geographically, across 25 states, with no state having more than 13% of the GLA of our portfolio. As of December 31, 2011, none of our tenants at our properties accounted for 7.0% or more of our aggregate annual rental revenue. Our portfolio consisted of 248 medical office buildings and other facilities that serve the healthcare industry, as well as two mortgage loans receivable.

We invest primarily in medical office buildings based on fundamental healthcare and real estate economics. Medical office buildings serve a critical role in the national healthcare delivery system, and we believe there are key dynamics within the healthcare industry that increase the need for, and the value of, medical office buildings. As hospitals and other facilities that serve the healthcare industry and physicians continue to collaborate, we believe an increasing number of healthcare services will be undertaken in medical offices. Further, with healthcare reform projected to expand coverage to over 30 million additional patients by 2019, we believe the performance of office-based services will play a key role in providing quality healthcare while also allowing for the recognition of cost efficiencies. In addition, as the emphasis within the healthcare industry moves toward preventative care, rather than responsive care, we expect that more healthcare services will be undertaken at medical offices.

Another key reason that we invest in medical office buildings is that we believe there is generallywill grow economically and demographically over the potential for higher returns with lower vacancy risk relative to other types of real estate investing. Like traditional commercial office property, as we renew leases and lease new space, we expect that the recovering economy will allow us to earn higher rents. Unlike commercial office space, however, medical office tenants, primarily physicians, hospitals and other healthcare providers, typically do not move or relocate, thus providing for stable tenancies and an ongoing demand for medical office space.coming years.

We are a Maryland corporation, formed in April 2006. Since that time, we have raised equity capital to finance our real estate investment activities through two public offerings of our common stock. Our offerings raised an aggregate of approximately $2.2 billion in gross offering proceeds, excluding proceeds associated with shares issued under our distribution reinvestment plan, or DRIP. Our principal executive offices are located at 16435 North Scottsdale Road, Suite 320, Scottsdale, AZ 85254 and our telephone number is (480) 998-3478. We maintain a web site at www.htareit.com at which there isyou may find additional information about us. The contents of that site are not incorporated by reference in, or otherwise a part of this filing. We make our periodic and current reports, as well as any amendments to such reports, available at www.htareit.com as soon as reasonably practicable after such materials are electronically filed with the Securities Exchange Commission, or the SEC. They are also available for printing forin hard copy to any stockholder upon request.

HIGHLIGHTS

During the year ended December 31, 2013, we acquired $397.8 million of high quality medical office buildings, representing an expansion of almost 15% by investment, based on purchase price. These acquisitions totaled approximately 1.5 million square feet of GLA. These properties are located in the key markets of Dallas, Denver, Miami, Tampa and West Palm Beach.

In 2013, we consistently achieved Same-Property Adjusted NOI growth of 3% or more each quarter.

In December 2013, our credit rating was upgraded which decreased the interest rate on our variable rate term loans and revolving credit facility. Taking into account the January 2014 amendment to the unsecured credit agreement, the total interest expense savings based on the current outstanding balances on these facilities is expected to be approximately $2.5 million in 2014.

During 2013, HTA generated returns that exceeded the SNL US REIT Healthcare Index by approximately 1,100 basis points and the MSCI US REIT (RMS) Index by approximately 230 basis points.

During 2013, we declared cash dividends of $0.575 per share that were paid to stockholders in equal quarterly installments.

During the year ended December 31, 2013, HTA issued and sold approximately 21.9 million shares of Class A common stock at an average price of $11.22 per share under HTA’s equity at-the-market, or ATM, program.

In March 2013, we issued and sold $300.0 million of 10-year unsecured senior notes at a rate of 3.70% per annum.

In November 2013, the last of HTA’s shares of Class B common stock converted to shares of Class A common stock, providing full liquidity to all of our stockholders.

As of December 31, 2013, we had a strong and flexible balance sheet with total liquidity of $613.1 million, including cash and cash equivalents of $18.1 million and $595.0 million available on our unsecured revolving credit facility. Our leverage ratio of total debt to total capitalization was 34.0%.

The occupancy rate on our portfolio increased 50 basis points during the year, ending at approximately 91.6% as of December 31, 2013. This included month-to-month leases and leases that have been executed, but which have not yet commenced.

In 2013, we consistently achieved tenant retention of 82% or more each quarter, and tenant retention for the year of 85%.

BUSINESS STRATEGIES

Our primary objectiveCorporate Strategies

Invest in and maintain a portfolio of properties that are well positioned for the long term future of healthcare delivery

The Company is focused on building and maintaining a portfolio of primarily medical office buildings that allow for the efficient delivery of healthcare over the long term. We believe that properties that are well located and efficient should increase in value over the long term. To date, we have invested over $3.0 billionto enhance stockholder value with disciplined growth through strategic investments and to provide an attractive total risk-adjusted return for our stockholders by consistently increasing our cash flow. The strategies we intend to execute to achieve this objective include:

Achieve Growth through Targeted Acquistions. We employ an acquisition philosophy that focuses primarilycreate one of the largest portfolios of healthcare real estate focused on mid-sized, relationship-driventhe medical office building targetssector in the United States. As a result, we look to allocate capital to properties that are located in established markets and that complement our existing portfolio. We emphasize building long-term relationships with healthcare systems, owners, operators, and otherexhibit the following key industry participants as a core aspect of our acquisition strategy. We believe our focusattributes:

Located on building such a strong, relationship-based network fosters opportunities for future growth of our company. We intend to grow through the strategic acquisition of high-quality medical office buildings and other facilities that serve the healthcare industry:

with stabilized occupancy that are located on or adjacent to the campuses of nationally recognizedor affiliated with leading healthcare systems in major U.S. metropolitan areas. On-campus locations provide for better tenant retention rates and rental rate growth as comparedthe United States. We seek to unaffiliated facilities;

that are affiliatedinvest with the country's top healthcare systems, which attract the top physicians. We will seek healthcare systems with dominant market share, and high credit quality;quality and those who are investing capital into their campuses. We believe our affiliations with these health systems help ensure long term tenant demand. At December 31, 2013, approximately 96% of our portfolio was located on-campus or affiliated with these health systems.

that are locatedIn attractive markets. We seek to own MOBs in high-growth primary and secondary markets with attractive demographics and favorable regulatory environments in business-friendly states or those with high barriers to entry;entry, especially those in which we can achieve operational and leasing efficiency. At December 31, 2013, over 50% of our GLA was located in 12 key markets throughout the U.S.

Well occupied with limited near term leasing risks. We have elected not to have an active development platform. As a result, we seek to invest in and maintain well occupied properties that create anbenefit from existing demand. We believe this positions us for long term value as hospitals and physicians are reluctant to move or relocate, as evidenced by our 2013 retention rate of 85%.

Occupied by credit-worthy tenants. Our primary tenants are the healthcare systems which maintain credit ratings with national rating agencies. At December 31, 2013, approximately 56% of our annual base rent comes from credit-rated tenants. A significant amount of our remaining rent comes from physicians and physician groups that are credit-worthy but do not have the size to benefit from a credit rating. We believe this helps ensure the stability of our rental income, and that we are invested in buildings that are attractive to the long term providers of healthcare.

Provide balanced mix of credit-rated tenants with long-term, triple-nettenants. We actively invest in both multi-tenant properties, which have shorter leases with fixed, scheduled rental growthon smaller spaces, and multi-tenantsingle-tenant properties, which have longer term leases. The multi-tenanted buildings with greater market-driven growth opportunities.

provide for lower lease rollover risks in any particular year and regularly allow for rents to be re-set to current market rates. We believe we have relationships and a proven track record of acquiring properties in off-market transactions at accretive cap rates. We will continue to focus our acquisition activity primarily on high quality medical officesingle tenanted buildings which we believe comprise the majority of our current property portfolio. We believe our pure focus on the medical office building sector of healthcare related real estate will provide insulation from the impact of certain governmental regulatory actions, such as the recently-passed cut in 2012 Medicare payments to skilled nursing facilities. This is because medical office buildings typically have a diversified payer mix composed largely of private health insurance companies.

Actively Manage Our Balance Sheet Strength and Flexibility. Our conservative balance sheet, with approximately 27.9% leverage as of December 31, 2011, and flexibility with our unused $575 million unsecured credit facility is crucial to our strategic growth. We actively manage our balance sheet to maintain conservative leverage with carefully staged debt maturities. This positions us to take advantage of strategic investment opportunities. We intend to utilize our unsecured line of credit for acquisition opportunities on a short-term basis. We have a number of sources of liquidity available to effectively manage our long-term leverage strategy, such as unsecured bank debt, mortgage financing, public debt, and private equity. We may also attempt to access the public equity markets to repay our secured debt maturities orsteady long term cash flow, but generally provide for future acquisition opportunities.more limited long term growth.

Maximize Internal Growth through Proactive Asset Management, Leasing and Property Management Oversight. Oversight

Our internal asset management focuses onteam operates approximately 85% of our total portfolio, a definedsignificant increase from approximately 70% a year ago. We believe this direct approach allows us to maximize our internal growth strategy, seizing on opportunities to achieve more profitable internal and external growth. Our strategy focuses on increasingby improving occupancy, optimizing rental rates, while maximizingand improving operating efficiencies at our properties. Specific components of our overall strategy include:

migrating towardMaintaining regional offices in markets where we have a significant presence, which enables our HTA-dedicatedin-house property management and leasing platform to (i) create closer relationships with national and regional healthcare systems and other tenants, and (ii) better respond to their needs. Our regional offices are located in geographic areas in which we have significant portfolio concentrations;Albany, Atlanta, Boston, Charleston, Dallas, Indianapolis, Pittsburgh and Scottsdale.

obtaining accretiveIncreasing our average rental rates, on our lease rolloversmaintaining or increasing renewal rates and actively leasing our vacant space, at a time when there is limited supply of medical office space in a slow-recovering economy;which contributed to our 3% or more Same-Property Adjusted NOI growth each quarter during 2013.

leveraging and proactively managing the best property management and leasing companies in markets not currently managed by our property management platform;

improvingImproving the quality of service provided to our tenants by being attentive to their needs, managing expenses, and strategically investing capital;capital. During 2013, we consistently achieved tenant retention of 82% or more each quarter, and tenant retention for the year of 85%.

maintainingMaintaining the high quality of our properties and building on our marketing initiative to brand our companyreputation as the landlord of choice;

maintaining regional offices in markets in which we have a significant presence;desirable and

purchasing in volume and using market expertise to continually reduce our operating costs.

COMPANY HIGHLIGHTS

In May 2011, we successfully increased our unsecured revolving credit facility to an aggregate maximum principal amount of $575,000,000 from $275,000,000 as well as extended its maturity date from November 2013 to May 2014.

As of December 31, 2011, we had a strong, flexible balance sheet with total assets of $2,291,629,000, cash on hand of $69,491,000, and a leverage ratio of our mortgage and secured term loans payable debt to total assets of approximately 27.9%.

In July 2011, we received ratings by two nationally recognized rating agencies. We believe these ratings, along with our strong balance sheet and conservative leverage, will allow us access to multiple sources of liquidity, such as unsecured bank debt, mortgage financing, and public debt.

We completed the sale of 21,564,900 shares of our common stock for $215,649,000 during the first quarter of 2011 pursuant to our follow-on offering and closed this offering on February 28, 2011, except for the DRIP.

For the year ended December 31, 2011, net income increased by 170.6% to $5,593,000 from a loss of $7,919,000 for the year ended December 31, 2010, and by 122.6% from a loss of $24,773,000 for the year ended December 31, 2009.

For the year ended December 31, 2011, Funds from Operations, or FFO, has increased by 60.2% to $113,135,000 from $70,642,000 for the year ended December 31, 2010, and by 292.5% from $28,822,000 for the year ended December 31, 2009. FFO is a non-GAAP financial measure. For a reconciliation of FFO to net income (loss), see Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations, "Funds from Operations and Normalized Funds from Operations".

During the year ended December 31, 2011, we transitioned a significant portion of our Indiana property portfolios to a regionally-focused property management platform with HTA-dedicated property management personnel. The addition of this market complemented the 34% of our overall portfolio that we had already been successfully managing with our asset management team. We believe such a platform provides us with the potential to reduce costs while enhancing our relationships with our hospital systems and physician tenants. Further, it allows us to improve the efficiency and effectiveness of property management and leasing. Following the success experienced with transitioning our Indiana portfolios, based on cost savings and enhanced tenant relations, we have begun the transition of properties in Arizona as well as in several east coast markets to our HTA-dedicated property management platform. Upon completion of these markets currently in transition, approximately 61% of our portfolio will be managed internally. We will continue to evaluate additional markets in which to expand our internal property management migration efforts in the future, based on concentrations of properties.

Our total portfolio of properties achieved an occupancy rate, including leases signed but not yet commenced, of approximately 91% as of December 31, 2011.

During the year ended December 31, 2011, we completed two new portfolio acquisitions and expanded two of our existing portfolios through the purchase of additional medical office buildings within each for an aggregate purchase price of $68,314,000. These purchases consist of six buildings comprised of approximately 306,000 square feet of GLA, bringing our total portfolio value, based on purchase price, to $2,334,673,000 as of December 31, 2011. These acquisitions possessed a weighted average acquisition-day occupancy rate of approximately 90%.

In February 2012, J.P. Morgan Securities, LLC, Deutsche Bank Securities Inc., and Wells Fargo Securities, LLC signed engagement letters to serve as Joint Lead Arrangers for a new credit facility of at least $825,000,000. As of March 23, 2012, the Joint Lead Arrangers and other additional lenders had committed in excess of that amount to the new credit facility. The credit facility, which will replace our existing credit facility, will have an initial term of four years, with one twelve-month extension. We anticipate closing the facility in the near future. The terms of this facility have not been finalized and there can be no assurance that we will enter into such facility on the terms or timing described herein or at all.landlord.

On February 14, 2012,Using market knowledge and economies of scale to seek to continually reduce our operating costs.

Achieve External Growth through Targeted Acquisitions

We plan to grow externally through targeted acquisitions that improve the quality of our portfolio and are accretive to our cost of capital. To achieve this growth in competitive markets, we completed the acquisitionseek:

| |

| ▪ | Mid-sized acquisitions in the $25 million to $75 million range. These transactions tend to be less competitive than larger transactions, but also allow us to exhibit meaningful growth given our current mid-market size. |

| |

| ▪ | Long term relationships with key industry participants. We plan to continue to emphasize building long-term relationships, cultivated by our senior management team, with key industry participants, including health systems and local and regional developers, which have traditionally provided us with valuable sources of potential investment opportunities. In this regard, approximately 73% of our acquisitions since January 2009, based on purchase price, were either sourced directly from hospitals and developers or were not marketed for sale. |

| |

| ▪ | Local knowledge through our internal asset management platform. Our local personnel are able to stay in touch with local industry activities which can provide insightful information on potential opportunities. |

Actively Maintain Strong, Flexible Capital Structure and Balance Sheet

We seek to actively manage our balance sheet to maintain our investment grade credit rating, to maintain conservative leverage, and to preserve financing flexibility. This positioning will allow us to take advantage of St. John Providence MOB, an approximately 203,000 square foot on-campus medical office building locatedstrategic investment opportunities. We have access to multiple forms of capital, including public debt and equity, unsecured bank loans and secured property-level debt. In addition, we may also pursue dispositions of properties that we believe no longer align with our strategic objectives in Novi, Michiganorder to redeploy capital. The strength of our balance sheet is demonstrated by our investment grade credit ratings, which we first received in an all-cash transaction for approximately $51,320,000. The St. John Providence MOB,July 2011 and which was 99% leasedmost recently upgraded in December 2013. To maintain our strong and flexible balance sheet, we:

Continue to maintain high liquidity primarily through our unsecured revolving credit facility. During 2013, we increased our unsecured revolving credit facility to $650.0 million, of which $595.0 million was available as of December 31, 2013.

Limit the dateamount of acquisition, is connected directlysecured debt. During 2013, the percentage of secured debt, including net premiums to the Providence Park Hospital via an enclosed walkway. Providence Park Hospital is parttotal capitalization decreased to 11.4% from 16.1% in 2012.

Maintain a low leverage ratio. Our leverage ratio of Ascension Health Systems (Moody's Investors Services rated Aa1).

On March 6, 2012, we completed the acquisition of Penn Avenue Place in Pittsburgh, Pennsylvania for a purchase price of approximately $54,000,000 in an all-cash transaction. Penn Avenue Place is an eight story, 558,000 square foot, Class A office building whichtotal debt to total capitalization was completely renovated in 1997. The building was approximately 99.6% occupied34.0% as of December 31, 2013.

Maintain well laddered debt maturities. As of December 31, 2013, we had $7.7 million, $74.0 million and $477.5 million of debt principal payments due in 2014, 2015 and 2016, respectively. After refinancing our $300.0 million term loan in January 2014, our principal payments due in 2016 was reduced to $177.5 million. During 2013, we increased the dateweighted average remaining term of acquisition and is anchored by Highmark, Inc. (Standard & Poor's Rating Services rated A). Highmark, Inc., which leases and occupies 92.4% of the building, is one of the largest Blue Cross affiliates in the nation. On January 1, 2012, Highmark, Inc. renewed its lease for an additional 10-year term.

On March 9, 2012, we entered into a purchase and sale agreement for a medical office buildingour debt portfolio located in the eastern United States for an aggregate purchase price of $100,000,000. The portfolio, which is expected to be master leased on a triple net basis, consists of a combination of on-campus assets and off-campus medical office buildings. We anticipate closing this acquisition in the near future, though there can be no assurance that the acquisition will close on our expected schedule, if at all.5.2 years, including extension options.

HEALTHCARE INDUSTRY

Healthcare Sector Growth

We operate in the healthcare industry because we believe this sector is benefiting from several macroeconomic events, including the demandAffordable Care Act, aging population, increases in healthcare employment, and increased healthcare spending.

The Affordable Care Act is a broad-based initiative that has the potential to expand health insurance coverage for healthcare real estatemany Americans, further increasing the number of people who are able to utilize medical services. The Congressional Budget Office estimates an additional 25 million individuals will continuegain access to insurance coverage by 2016 as a result of this reform. The Affordable Care Act’s focus on preventative care is expected to increase consistent with health spending in the United States. According toutilization of outpatient care into the U.S. Departmentfuture.

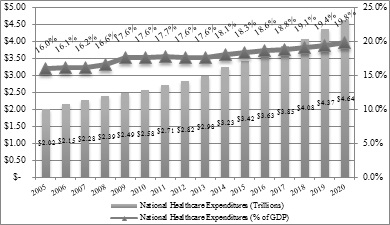

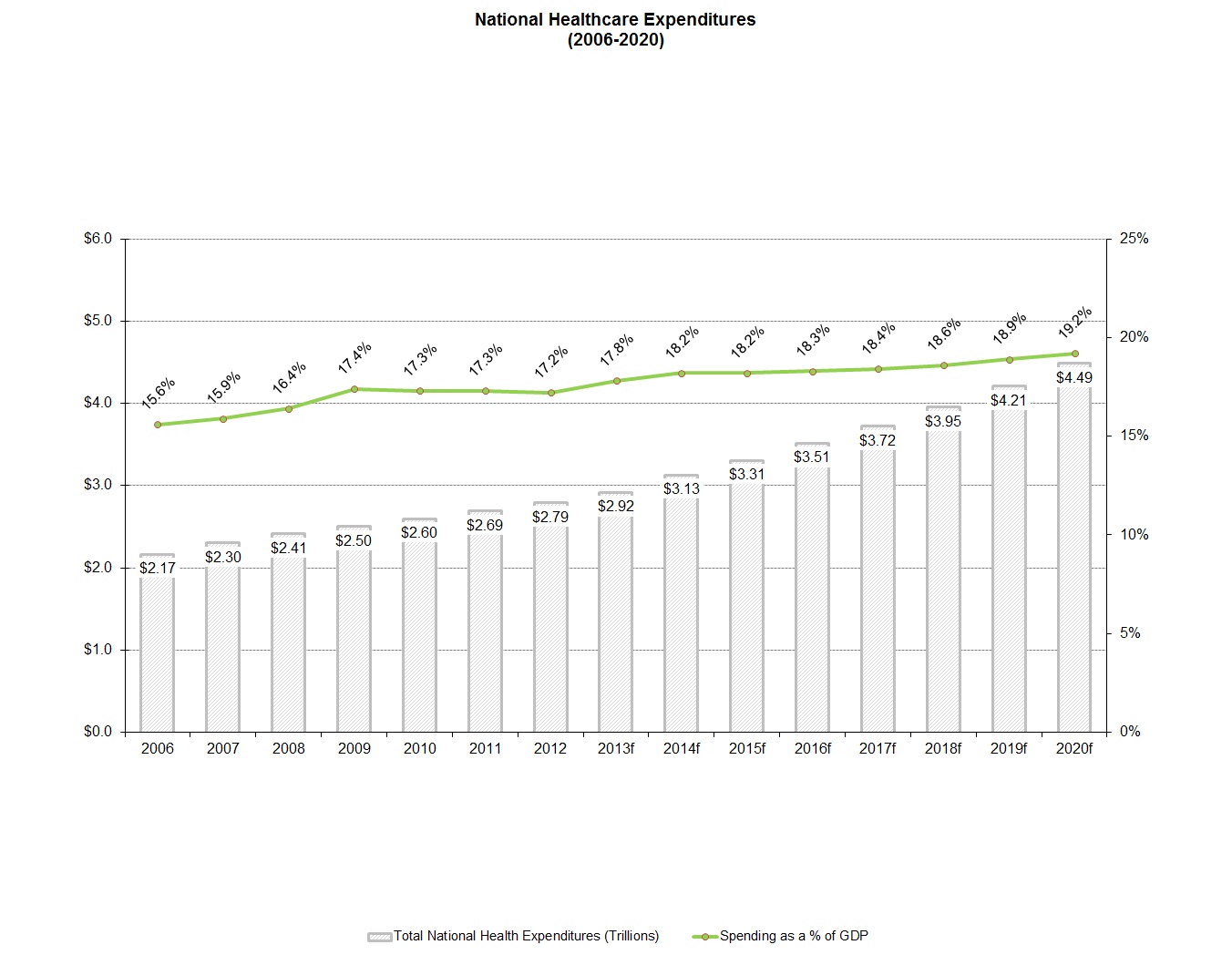

National Healthcare Expenditures

(2005-2020)

Source: U.S. Department of HealthCongressional Budget Office and Human Services. Centers for Medicare & Medicaid Services. Office of the Actuary. National Health ExpendituresRosen Consulting Group.

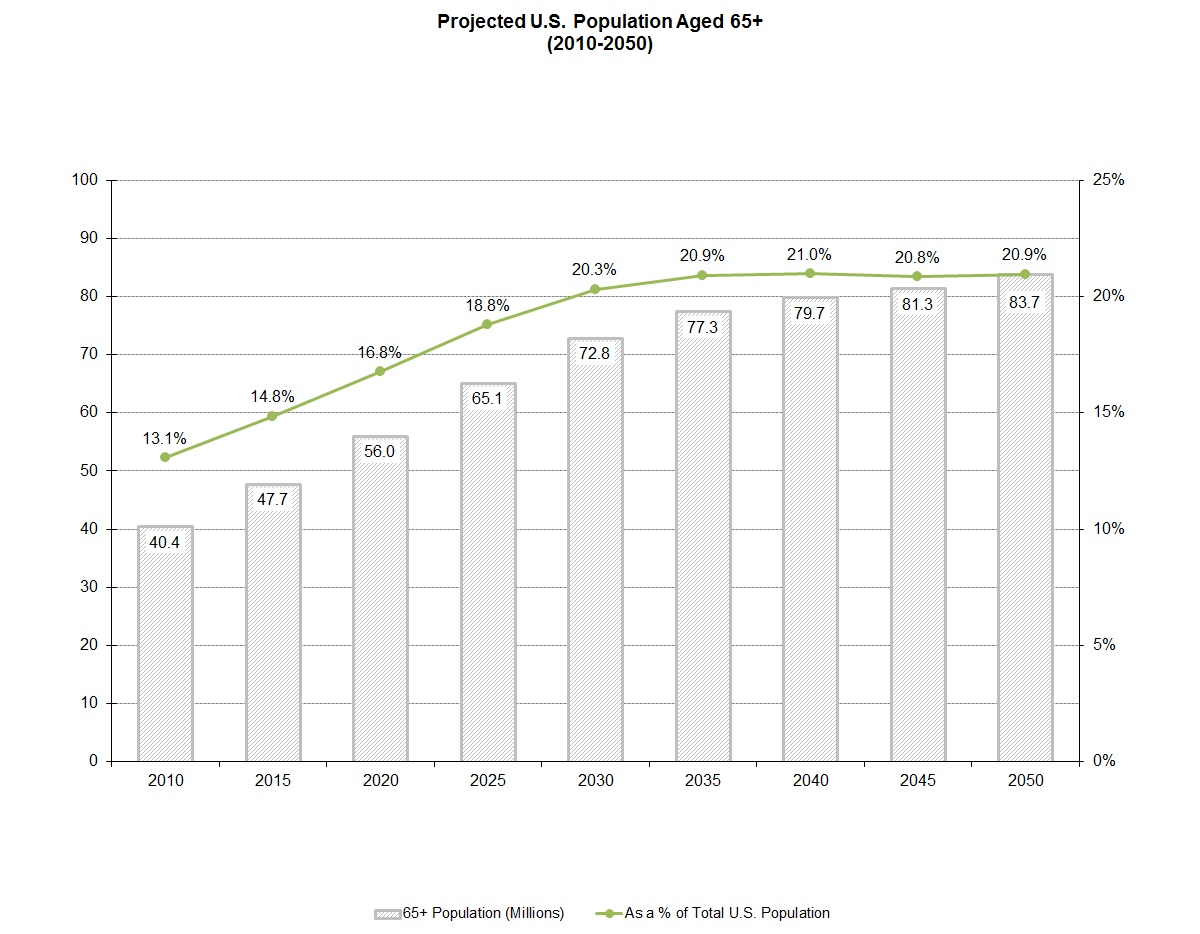

Advancements in medical technology and Selected Economic Indicators. Levelschanges in treatment methods have enabled people to live longer and Annual Percent Change: Calendar Years 2005-2020 (based on the version of the National Health Expenditures releasedhas resulted in January 2011).

a growing elderly population. Between 2010 and 2050, the U.S. population over 65 years of age is projected to more than double from 40.240.4 million to nearly 88.583.7 million people, as reflected in the below chart. Similarly, the 85 and older population is expected to more than triple, from 5.7 million in 2010 to 19.0 million between 2010 and 2050. The number of older Americans is also growing as a percentage of the total U.S. population as the “baby boomers” enter their 60s.people. The number of persons older than 65 years of age was estimated to comprise 13.0%13.1% of the total U.S. population in 2010 and is projected to grow to 20.2%20.9% by 2050, as reflected in the below chart.

Projected U.S. Population Aged 65+

(2010-2050)

Source: U.S. Census Bureau, Population Division, August 14, 2008.

Based on the information above, we believe that healthcare expenditures for the population over 65 years of age will continue to rise as a disproportionate share of healthcare dollars is spent on older Americans.2050. According to the 20102012 Consumer Expenditure Survey, persons agedbetween 65 toand 74 years of age spent the highest amount annually for healthcare with more than $4,900$5,200 in annual personal expenditures including health insurance premiums. Those agedpersons more than 75 years of age followed closely with nearly $4,800$4,900 spent on healthcare per year. In contrast, persons aged less than 25 years of age spent only $775approximately $1,000 per year on healthcare. The older population group will increasingly require treatment and management of chronic and acute health ailments. We believe that this increased demand for healthcare services will create a substantial need for the development of additional medical office buildings and other facilities that serve the healthcare industry in many regions of the United States. Additionally, we believe that there will likely be a focus on lower cost outpatient care to support the aging U.S. population, which will continue to support medical office building demand in the long term.

Source: U.S. Census Bureau and Rosen Consulting Group.

Employment in the healthcare industry has steadily increased for at least 20 years despite three recessions. Healthcare-related jobs are among the fastest growing occupations, projected to increase 22% between 2012 and 2022, significantly higher than the general U.S. employment growth of 10.8% according to the Bureau of Labor Statistics. Additionally, healthcare related jobs are projected to account for eleven of the twenty fastest growing occupations. These occupations are estimated to grow by between 36% and 48% between 2012 and 2022, according to the most recent Bureau of Labor Statistics projections. Additionally, the Bureau of Labor Statistics projects seven out of the top twelve occupations with the highest demand for workers will be in the healthcare sector. We expect the increased growth in the healthcare industry will correspond with a growth in demand for medical office buildings and other facilities that serve the healthcare industry.

Source: Bureau of Labor Statistics and Rosen Consulting Group.

According to the latest data from 2012, Americas spent nearly $2.8 trillion, or 17.2% of total GDP, on healthcare expenditures, an increase of 3.7% from the previous year. The U.S. Centers for Medicare & Medicaid Services project that the total healthcare expenditures will reach approximately $5.0 trillion by 2022. Healthcare expenditures are projected to grow by 5.9% annually through 2022 and account for 19.2% of GDP by 2020. With healthcare costs remaining high, we believe thisinsurance providers will result in a substantial increase in suitable, quality properties meeting our acquisition criteria.encourage patients to transition to cost efficient, outpatient settings.

Source: U.S. Centers for Medicare & Medicaid Services and Rosen Consulting Group.

Medical Office Building Supply and Demand

We invest primarily in medical office buildings. We believe that healthcare-related real estate rents and valuations are less susceptible to changes in the general economy than general commercial real estate due to demographic trends and the resistance of rising healthcare expenditures to economic downturns. For this reason, we believe medical office building investments could potentially offer a more stable return to investors compared to other types of real estate investments. We believe that demand for medical office buildings and other facilities that serve the healthcare industry will increase due to a number of factors, including:

Evolution in the healthcare industry is a contributing factor, with procedures that have traditionally been performed in hospitals, such as surgery, moving to outpatient facilities as a result of shifting consumer preferences, limited space in hospitals, and lower costs. In addition, increased specialization within the medical field is driving the demand for medical office buildings suited specifically toward a particular specialty. Finally, some hospital systems have begun divesting their real estate holdings in order to better focus on the delivery of care.

An increase in medical office visits due to the overall rise in healthcare utilization has in turn driven hiring within the healthcare sector. This has increased the need for expansion of medical office facilities. Additionally, the increased dissemination of health research through media outlets, marketing of healthcare products, and availability of advanced screening techniques and medical procedures have contributed to a more engaged population of healthcare users. This has created a surge in demand for customized facilities providing specialized, preventive, and integrative medicine. Additionally, the rate of employment growth in physicians'physicians’ offices and outpatient care facilities has outpaced employment growth in hospitals during the past decade, further supporting the trend of increased utilization of healthcare services outside of the hospital. These factors, in combination with changing consumer preferences and limitations on hospital expansion, have resulted in the increased utilization of medical office space, a trend which is expected to continue over the long term. According to the Bureau of Labor Statistics, employment in physicians'physicians’ offices is expected to increase by a cumulative 36.4%38.4% from 20102012 to 2020, as compared with a projected 25.9%21.5% increase in all healthcare professions and a forecasted increase of 14.3%10.8% in total employment.employment during this time.

Advances in medical technology will continue to enable healthcare providers to identify and treat once fatal ailments and will improve the survival rate of critically ill and injured patients who will require continuing medical care. Along with these technical innovations, the U.S. population is growing older and living longer. In addition, according to the Centers for Disease Control and Prevention,Census Bureau, from 19501980 to 2005,2012, the average life expectancy at birth increased from 68.274 years to 77.978 years. By 2050,2020, the average life expectancy at birth is projected to increase to 82.680 years, according to the U.S. Census Bureau.

Construction of medical office buildings has been relatively constrained with little developable land and high-cost barriers to development.

Strong rent growth is forecasted as market conditions tighten due to limited development, a decline in vacancy rates, growth in healthcare employment, and a larger number of baby boomers entering retirement age. Beginning in 2013, rent growth for medical office buildings is expected to outpace rent growth for traditional office properties as healthcare employment increases at a faster pace than employment in traditional office-using industries.

Healthcare Industry TrendsSource: U.S. Census Bureau (as of Q3 2013) and OutlookRosen Consulting Group.

The current healthcare environment is impacted by several factors, each of which will inform the industry outlook over the long term:

According to the United States Department of Labor’s Bureau of Labor Statistics, the healthcare industry was the largest industry in the United States in 2006, providing 14 million jobs. Healthcare-related jobs are among the fastest growing occupations, accounting for ten of the 20 fastest growing occupations. The Bureau of Labor and Statistics estimates that healthcare will generate three million new wage and salary jobs between 2008 and 2018, more than any other industry. Wage and salary employment in the healthcare industry is projected to increase 22% through 2018, compared with 11% for all industries combined. Despite the downturn in the economy and widespread job losses in most industries, the healthcare industry has not been impacted. We expect the increased growth in the healthcare industry will correspond with a growth in demand for medical office buildings and other facilities that serve the healthcare industry.

Complex state and federal regulations govern physician hospital referrals. Patients typically are referred to particular hospitals by their physicians. To restrict hospitals from inappropriately influencing physicians to refer patients to them, federal and state governments adopted Medicare and Medicaid anti-fraud laws and regulations. One aspect of these complex laws and regulations addresses the leasing of medical office space by hospitals to physicians. One intent of the regulations is to restrict medical institutions from providing facilities to physicians at below market rates or on other terms that may present an opportunity for undue influence on physician referrals. The regulations are complex, and adherence to the regulations is time consuming and requires significant documentation and extensive reporting to regulators. The costs associated with regulatory compliance have encouraged many hospital and physician groups to seek third-party ownership and/or management of their healthcare-related facilities.

Physicians are increasingly forming group practices. To increase the numbers of patients they can see and thereby increase market share, physicians have formed and are forming group practices. By doing so, physicians can gain greater influence in negotiating rates with managed care companies and hospitals in which they perform services. Also, the creation of these groups allows for the dispersion of overhead costs over a larger revenue base and gives physicians the financial ability to acquire new and expensive diagnostic equipment. Moreover, certain group practices may benefit from certain exceptions to federal and state self-referral laws, permitting them to offer a broader range of medical services within their practices and to participate in the facility fee related to medical procedures. This increase in the number of group practices has led to the construction of new medical facilities in which the groups are housed and medical services are provided.

We believe that healthcare-related real estate rents and valuations are less susceptible to changes in the general economy than general commercial real estate due to demographic trends and the resistance of rising healthcare expenditures to economic downturns. For this reason, we believe healthcare-related real estate investments could potentially offer a more stable return to investors compared to other types of real estate investments.

We believe the confluence of these factors over the last several years, in combination with low interest rates and continued increases in the selling price of medical office buildings, has led to the following trends, which encourage third-party ownership of existing and newly developed medical properties:

Decentralization and Specialization. There is a continuing evolution toward delivery of medical services through smaller outpatient facilities located near patients and designed to treat specific diseases and conditions. In order to operate profitably within a managed care environment, physician practice groups and other medical services providers are aggressively trying to increase patient populations, while maintaining lower overhead costs by building new healthcare facilities in areas of population or patient growth. Continuing population shifts and ongoing demographic changes create a demand for additional properties, including an aging population requiring and demanding more medical services.

Hospital Consolidation and Recapitalization. Hospitals continue to consolidate in an effort to secure or expand market share, gain access to capital, and/or to achieve various economies of scale. Historically, these have been in the form of the expansion of investor-owned health systems through acquisitions or the merger of one or more tax-exempt health systems. Recently, new entrants include private equity firms that have either acquired hospital assets or are investing capital into existing tax-exempt organizations. We believe that accessing capital will continue to be a major area of focus for healthcare organizations, both in the short and long term.

Increasing Regulation. Evolving regulatory factors affecting healthcare delivery create an incentive for providers of medical services to focus on patient care, leaving real estate ownership and operation to third-party real estate professionals. Third-party ownership and management of hospital-affiliated medical office buildings substantially reduces the risk that hospitals will violate complex Medicare and Medicaid fraud and abuse statutes.

Modernization. Hospitals are modernizing by renovating existing properties and building new properties and becoming more efficient in the face of declining reimbursement and changing patient demographics. This trend has led to the development of new, smaller, specialty healthcare-related facilities as well as improvements to existing general acute care facilities. As a result, we believe hospitals will monetize their assets to redeploy needed capital.

Redeployment of Capital. Medical providers are increasingly focused on wisely investing their capital in their medical business. A growing number of medical providers have determined that third-party ownership of real estate with long term leases is an attractive alternative to investing their capital in bricks-and-mortar. Increasing use of expensive medical technology has placed additional demands on the capital requirements of medical services providers and physician practice groups. By selling their real estate assets and relying on third-party ownership of new healthcare properties, medical services providers and physician practice groups can generate the capital necessary to acquire the medical technology needed to provide more comprehensive services to patients and improve overall patient care.

Physician Practice Ownership. Many physician groups have reacquired their practice assets and real estate from national physician management companies or otherwise formed group practices to expand their market share. Other physicians have left hospital-based or HMO-based practices to form independent group practices. These physician groups are interested in new healthcare properties that will house medical businesses that regulations permit them to own. In addition to existing group practices, there is a growing trend for physicians in specialties, including cardiology, oncology, women’s health, orthopedics and urology, to enter into joint ventures and partnerships with hospitals, operators and financial sponsors to form specialty hospitals for the treatment of specific diseases. In general, we believe a significant number of these types of organizations have a limited interest in owning real estate and are aggressively looking for third-parties to own their healthcare properties.

The current regulatory environment remains an ongoing challenge for healthcare providers, who are under pressure to comply with complex healthcare laws and regulations designed to prevent fraud and abuse. These regulations, for example, prohibit physicians from referring patients to entities in which they have ownership or investment interests and prohibit hospitals from leasing space to physicians at below market rates. As a result, healthcare providers seek reduced liability costs and have an incentive to dispose of real estate to third parties, thus reducing the risk of violating fraud and abuse regulations. This environment creates investment opportunities for owners, acquirers and joint venture partners of healthcare real estate who understand the needs of healthcare professionals and can help keep tenant costs low. While the current regulatory environment is positive for healthcare operators, there is uncertainty as to the future of government policies and its potential impact on healthcare provider profitability.

PORTFOLIO OF PROPERTIES

As of December 31, 2011,2013, our portfolio consisted of 229269 medical office buildings and 19 other facilities that serve the healthcare industry, as well as two mortgage loans receivable.real estate notes receivable secured by medical office buildings. Our portfolio consistedis comprised of approximately 11.214.1 million square feet of GLA, with an occupancy rate of approximately 91.6%, including month-to-month leases signedand leases we have executed, but which have not yet commenced,commenced.

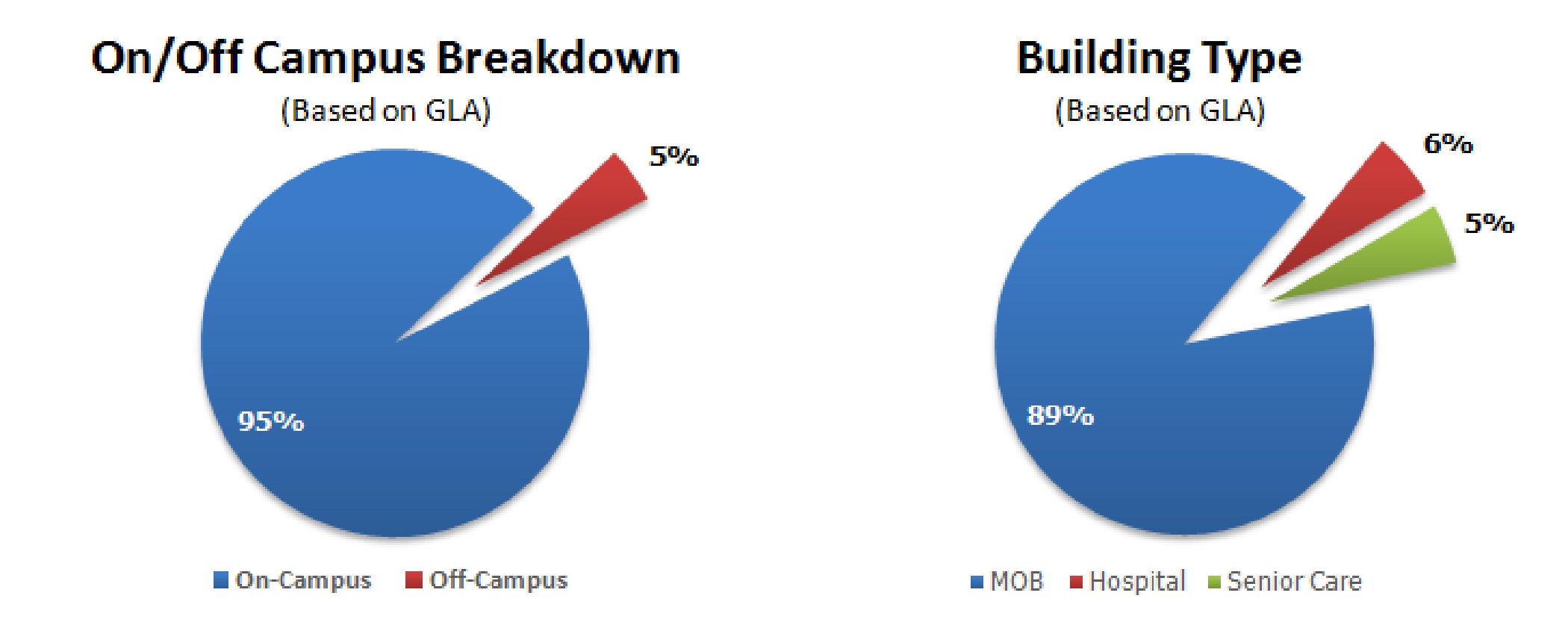

Our properties are primarily located onon-campus or adjacent to, or are anchored by, the campuses ofaligned with nationally and regionally recognized healthcare systems in the United States, including some of the largest in the United States,healthcare systems, such as AdventistForest Park Medical Center, Greenville Hospital System, Highmark, Hospital Corporation of America, Indiana University Health, Systems, AscensionPiedmont Healthcare, Steward Health Banner HealthCare System, Catholic Healthcare Partners, Catholic Healthcare West, Community Health Systems, HCA, Inc. and Tenet Healthcare Corporation.System. As of December 31, 2011,2013, approximately 95%96% of our portfolio, based on GLA, is located onon-campus or adjacent to, or was anchored by, the campuses of suchaligned with nationally and regionally recognized healthcare systems.

The following charts depict 1) the proportion of our portfolio that is located on or is aligned with the campuses of nationally recognized healthcare systems; and 2) the composition of our overall portfolio as of December 31, 2011:

|

| | | | | | | | | | | | | | | | | |

| Portfolio by Type | # of Buildings | | Annualized Base Rent (1) | | % of Total

Annualized Base Rent | | Purchase Price | | % of

Aggregate

Purchase Price | | Number of States |

| Medical office buildings | | | |

| | |

| | |

| | |

| | |

| Single-tenant, net lease | 55 | | $ | 41,205,000 |

| | 19.9 | % | | $ | 488,915,000 |

| | 20.9 | % | | 15 |

| Single-tenant, gross lease | 7 | | $ | 6,308,000 |

| | 3.1 | % | | $ | 70,504,000 |

| | 3.0 | % | | 4 |

| Multi-tenant, net lease | 73 | | $ | 52,558,000 |

| | 25.4 | % | | $ | 650,411,000 |

| | 27.9 | % | | 15 |

| Multi-tenant, gross lease | 94 | | $ | 77,765,000 |

| | 37.6 | % | | $ | 739,388,000 |

| | 31.7 | % | | 16 |

| Other facilities that serve the healthcare industry | | | |

| | |

| | |

| | |

| | |

| Hospitals, single-tenant, net lease | 10 | | $ | 20,692,000 |

| | 10.0 | % | | $ | 241,720,000 |

| | 10.4 | % | | 4 |

| Seniors housing, single-tenant, net lease | 9 | | $ | 8,236,000 |

| | 4.0 | % | | $ | 91,600,000 |

| | 3.9 | % | | 3 |

| Mortgage loans receivable | | | N/A |

| | N/A |

| | $ | 52,135,000 |

| | 2.2 | % | | 2 |

| TOTALS | 248 | | $ | 206,764,000 |

| | 100.0 | % | | $ | 2,334,673,000 |

| | 100.0 | % | | |

|

| | | | | | | | | | | |

| Portfolio Diversification by Type | | Number of Buildings | | GLA (1) | | Percent of

Total GLA | | Number of States |

| Medical office buildings: | | |

| | |

| | |

| | |

| Single-tenant | | 76 |

| | 3,159 |

| | 22.4 | % | | 17 |

| Multi-tenant | | 193 |

| | 9,685 |

| | 68.8 |

| | 23 |

| Other healthcare facilities: | | | | | | |

| | |

| Hospitals | | 10 |

| | 655 |

| | 4.7 |

| | 4 |

| Seniors housing | | 9 |

| | 581 |

| | 4.1 |

| | 3 |

| Total | | 288 |

| | 14,080 |

| | 100.0 | % | | |

________________________

SIGNIFICANT TENANTS

As of December 31, 2013, none of the tenants at our properties accounted for more than 6% of our annualized base rent. The table below depicts our top 15 health system relationships.

|

| | | | | | | | | | | | | | | | |

| Tenant | | Weighted Average Remaining Years in Lease Term | | Total Leased GLA (1) | | Percent of Leased GLA | | Annualized Base Rent (1) (2) | | Percent of Annualized Base Rent |

| Highmark | | 8 |

| | 856 |

| | 6.6 | % | | $ | 15,713 |

| | 5.7 | % |

| Greenville Hospital System | | 10 |

| | 761 |

| | 5.9 |

| | 13,724 |

| | 5.0 |

|

| Hospital Corporation of America | | 5 |

| | 329 |

| | 2.5 |

| | 7,583 |

| | 2.8 |

|

| Community Health Systems | | 5 |

| | 327 |

| | 2.5 |

| | 7,128 |

| | 2.6 |

|

| Steward Health Care System | | 13 |

| | 317 |

| | 2.5 |

| | 7,124 |

| | 2.6 |

|

| Aurora Health Care | | 10 |

| | 315 |

| | 2.4 |

| | 6,684 |

| | 2.4 |

|

| Indiana University Health | | 4 |

| | 294 |

| | 2.3 |

| | 4,739 |

| | 1.7 |

|

| Deaconess Health System | | 10 |

| | 261 |

| | 2.0 |

| | 4,011 |

| | 1.5 |

|

| Banner Health | | 2 |

| | 201 |

| | 1.6 |

| | 4,599 |

| | 1.7 |

|

| Capital District Physicians Health Plan | | 3 |

| | 198 |

| | 1.5 |

| | 3,026 |

| | 1.1 |

|

| Catholic Health Partners | | 4 |

| | 177 |

| | 1.4 |

| | 2,770 |

| | 1.0 |

|

| Wellmont Health System | | 9 |

| | 160 |

| | 1.2 |

| | 2,694 |

| | 1.0 |

|

| Rush University Medical Center | | 6 |

| | 137 |

| | 1.1 |

| | 4,425 |

| | 1.6 |

|

| Diagnostic Clinic Medical Group | | 16 |

| | 119 |

| | 0.9 |

| | 3,173 |

| | 1.2 |

|

| Forest Park Medical Center | | 7 |

| | 112 |

| | 0.9 |

| | 3,090 |

| | 1.1 |

|

| Total | | | | 4,564 |

| | 35.3 | % | | $ | 90,483 |

| | 33.0 | % |

________________________

| |

| (2) | Annualized base rent is based on thecalculated by multiplying contractual base rent in effect as of December 31, 2011, excluding2013 by 12 (excluding the impact of renewals, future step-ups in rent, abatements, concessions, and straight-line rent.rent). |

SIGNIFICANT TENANTS

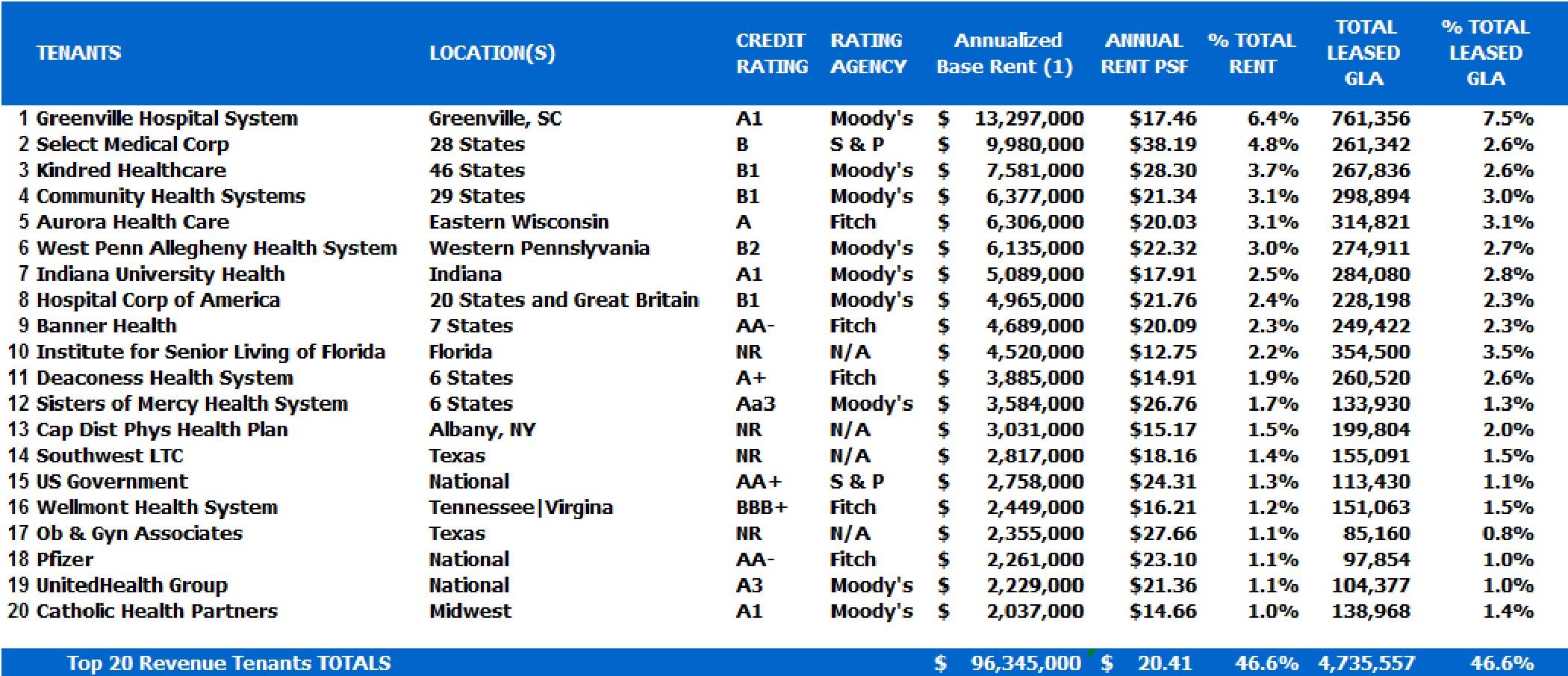

As of December 31, 2011, none of our tenants at our properties accounted for 10.0% or more of our aggregate annual rental revenue. The chart below depicts credit rating, annual rent, and GLA information for our top 20 tenants as determined by annualized base rent:

| |

(1) | Annualized base rent is based on the contractual base rent in effect as of December 31, 2011, excluding the impact of renewals, future step-ups in rent, abatements, concessions, and straight-line rent. |

| |

(2) | Credit ratings of our tenants or their parent companies. |

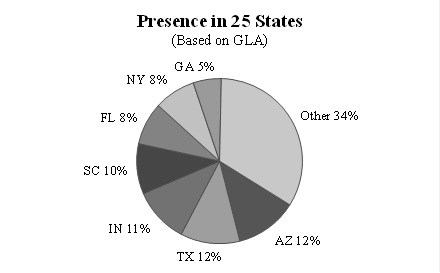

GEOGRAPHIC CONCENTRATION

As of December 31, 2011,2013, our portfolio was comprised of approximately 11.214.1 million square feet of GLA and was concentrated in locationskey markets that we have determined to be strategic based on demographic trends and projected demand for healthcare. We have concentrations in the following key markets: Phoenix, Arizona; Greenville, South Carolina; Indianapolis, Indiana; Albany, New York; Houston, Texas; Atlanta, Georgia; Pittsburgh, Pennsylvania; Dallas, Texas; Raleigh, North Carolina and Oklahoma City, Oklahoma.

The chart belows depicts our geographic presence based on GLA as of December 31, 2011:

|

| | | | | | |

| Market | | GLA (1) | | Percent of Portfolio |

| Phoenix, AZ | | 1,152 |

| | 8.2 | % |

| Pittsburgh, PA | | 1,094 |

| | 7.8 |

|

| Greenville, SC | | 965 |

| | 6.9 |

|

| Albany, NY | | 879 |

| | 6.3 |

|

| Indianapolis, IN | | 850 |

| | 6.1 |

|

| Houston, TX | | 692 |

| | 4.9 |

|

| Dallas, TX | | 682 |

| | 4.8 |

|

| Atlanta, GA | | 597 |

| | 4.2 |

|

| Miami, FL | | 591 |

| | 4.2 |

|

| Boston, MA | | 359 |

| | 2.5 |

|

| Total | | 7,861 |

| | 55.9 | % |

________________________

FINANCIAL INFORMATION ABOUT INDUSTRY SEGMENTS

Financial Accounting Standards Board, or FASB, Accounting Standard Codification, or ASC, 280, Segment Reporting, or ASC 280, establishes standards for reporting financial and descriptive information about an enterprise’s reportable segment.segments. We have determined that we have one reportable segment, with activities related to investing in medical office buildings, healthcare-related facilities and other facilities that serve the healthcare industry, and mortgage loans receivable.real estate related assets. Our investments in real estate and other real estate relatedestate-related assets are geographically diversified and our chief operating decision maker evaluates operating performance on an individual asset level. As each of our assets has similar economic characteristics, tenants, and products and services, our assets have been aggregated into one reportable segment. See our accompanying consolidated financial statements for further information.

COMPETITION

We compete with many other real estate investment entities, including financial institutions, institutional pension funds, real estate developers, other REITs, other public and private real estate companies and private real estate investors for the acquisition of medical office buildings and other facilities that serve the healthcare industry. During the acquisition process, we compete with others who may have a comparativecompetitive advantage in terms of size, capitalization, depth of experience, local knowledge of the marketplace, and extended contacts throughout the region. Any combination of these factors may result in an increased purchase price for real properties or other real estate related assets which may reduce the number of opportunities available to us that meet our investment criteria. If the number of opportunities that meet our investment criteria are limited, our ability to increase stockholder value may be adversely impacted.

We face competition in leasing available medical office buildings and other facilities that serve the healthcare industry to prospective tenants. As a result, we may have to provide rent concessions, incur charges for tenant improvements, offer other inducements, or we may be unable to timely lease vacant space in our properties, all of which may have an adverse impact on our results of operations. At the time we elect to dispose of our properties, we will also be in competition with sellers of similar properties to locate suitable purchasers.purchase opportunities.

We believe our focus on medical office buildings, and other facilities that serve the healthcare industry, our experience and expertise, and our ongoing relationships with healthcare providers provide us with a competitive advantage. We have established an asset identification and acquisition network with healthcare providers and local developers, which provides for the early identification of and access to acquisition opportunities. In addition, we believe this broad network allows for us to effectively lease available medical office space, retain our tenants, and maintain and improve our assets.

GOVERNMENT REGULATIONS

Healthcare-relatedHealthcare-Related Regulations

Overview. The healthcare industry is heavily regulated by federal, state and local governmental bodies. Our tenants generally are subject to laws and regulations covering, among other things, licensure, certification for participation in government programs, and relationships with physicians and other referral sources. Changes in these laws and regulations could negatively affect the ability of our tenants to satisfy their contractual obligations, including making lease payments to us.

Healthcare Legislation. On March 23, 2010, the President signed into law theThe Patient Protection and Affordable Care Act of 2010, or the Patient Protection and Affordable Care Act, and on March 30, 2010, the President signed into law the Health Care and Education Reconciliation Act of 2010, or the Reconciliation Act, which in part modified the Patient Protection and Affordable Care Act. Together, the two lawsAct, together serve as the primary vehicle for comprehensive healthcare reform in the U.S.United States and will become effective through a phased approach, which began in 2010 and will conclude in 2018. The laws are intended to reduce the number of individuals in the United States without health insurance and significantly change the means by which healthcare is organized, delivered and reimbursed. The Patient Protection and Affordable Care Act includes program integrity provisions that both create new authorities and expand existing authorities for federal and state governments to address fraud, waste and abuse in federal healthcare programs. In addition, the Patient Protection and Affordable Care Act expandsexpanded reporting requirements and responsibilities related to facility ownership and management, patient safety and care quality.quality of care. In the ordinary course of their businesses, our tenants may be regularly subjected to inquiries, investigations and audits by federal and state agencies that oversee these laws and regulations. If they do not comply with the additional reporting requirements and responsibilities, our tenants’ ability to participate in federal healthcare programs may be adversely affected. Moreover, there may be other aspects of the comprehensive healthcare reform legislation for which regulations have not yet been adopted, which, depending on how they are implemented, could materially and adversely affect our tenants and their ability to meet their lease obligations.obligations to us.

On June 28, 2012, the U.S. Supreme Court ruled on the constitutionality of the two laws generally upholding the entirety of the Patient Protection and Affordable Care Act, including holding that the “individual mandate” -- the centerpiece of the legislation that requires all individuals to purchase some form of health insurance -- is permissibly construed as a tax imposed on those who do not obtain health insurance. Notably, the portions of the health reform laws addressing fraud, waste and abuse remain intact. The only aspect of the two laws that was held unconstitutional is the mandated Medicaid expansion that would have required states to cover nonelderly persons with incomes up to 133% of the poverty level. The Supreme Court held that Congress could not require states to implement such an expansion or risk losing all federal Medicaid funding. As a result of the Supreme Court’s decision, states may opt to expand Medicaid coverage in accordance with the two laws, but they are not required to do so. In fact, more than one dozen states have decided to opt out of the Medicaid expansion. Despite the Supreme Court’s decision, it remains difficult to predict the impact of these laws on us due to their complexity, lack of implementing regulations or interpretive guidance, and the gradual implementation of the laws over a multi-year period. In addition, there have been numerous Congressional attempts to amend and repeal the laws both prior to and subsequent to the Supreme Court’s ruling; we cannot predict whether any of these attempts to repeal or amend the laws will be successful. Moreover, the launch of the federal and state health exchanges on October 1, 2013, received significant public scrutiny for perceived technical shortcomings affecting the ability of individuals to enroll in health plans as mandated by the Affordable Care Act. Consequently, it remains difficult to foresee how individuals and business will respond to the choices afforded them by law. Because of the many variables involved, we are unable to predict how these laws may impact our tenants’ operations or the net effect of these laws on us. Both our tenants and us may be adversely affected by these laws.

Reimbursement Programs. Sources of revenue for our tenants may include the federal Medicare program, state Medicaid programs, private insurance carriers, health maintenance organizations, preferred provider arrangements, self-insured employers and the patients themselves, among others. Medicare and Medicaid programs, as well as numerous private insurance and managed care plans, generally require participating providers to accept government-determined reimbursement levels as payment in full for services rendered, without regard to a facility’s charges. Changes in the reimbursement rate or methods of payment from third-party payors, including Medicare and Medicaid, could result in a substantial reduction in our tenants’ revenues. In fact, legislation governing Medicare physician fee-for-service reimbursements has, for a number of years, called for significant reductions in such rates. Congress, however, has repeatedly enacted superseding legislation postponing the implementation of physician rate cuts, most recently postponing the effective date of such cuts until April 1, 2014. There are a number of Congressional proposals to further postpone implementation of the cuts or to permanently address the issue, however, we cannot predict whether any of these attempts will be successful. Efforts by such payors to reduce healthcare costs will likely continue, which may result in reductions or slower growth in reimbursement for certain services provided by some of our tenants. Further, revenue realizable under third-party payor agreements can change after examination and retroactive adjustment by payors during the claims settlement processes or as a result of post-payment audits. Payors may disallow requests for reimbursement based on determinations that certain costs are not reimbursable or reasonable or because additional documentation is necessary or because certain services were not covered or were not medically necessary. The recently enacted healthcare reform law and regulatory changes could impose further limitations on government and private payments to healthcare providers. In some cases, states have enacted or are considering enacting measures designed to reduce their Medicaid expenditures and to make changes to private healthcare insurance. In addition, the failure of any of our tenants to comply with various laws and regulations could jeopardize their ability to continue participating in Medicare, Medicaid and other government sponsored payment programs. The financial impact on our tenants could restrict their ability to make rent payments to us.

Fraud and Abuse Laws. There are various federal and state laws prohibiting fraudulent and abusive business practices by healthcare providers who participate in, receive payments from or are in a position to make referrals in connection with government-sponsored healthcare programs, including the Medicare and Medicaid programs. Our lease arrangements with certain tenants may also be subject to these fraud and abuse laws. These laws include, but are not limited to:

the Federal Anti-Kickback Statute, which prohibits, among other things, the offer, payment, solicitation or receipt of any form of remuneration in return for, or to induce, the referral or recommendation for the ordering of any item or service reimbursed by a federal healthcare program, including Medicare or Medicaid;

the Federal Physician Self-Referral Prohibition, commonly referred to as the Stark Law, which, subject to specific exceptions, restricts physicians from making referrals for specifically designated health services for which payment may be made under Medicare or Medicaid programs to an entity with which the physician, or an immediate family member, has a financial relationship;

the False Claims Act, which prohibits any person from knowingly presenting or causing to be presented false or fraudulent claims for payment to the federal government, including claims paid by the Medicare and Medicaid programs;

the Civil Monetary Penalties Law, which authorizes the U.S. Department of Health and Human Services to impose monetary penalties for certain fraudulent acts and to exclude violators from participating in federal healthcare programs; and

the Health Insurance Portability and Accountability Act, as amended by the Health Information Technology for Economic and Clinical Health Act of the American Recovery and Reinvestment Act of 2009, which protects the privacy and security of personal health information.