UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | |||||

| ☒ | |||

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||

For the fiscal year ended December 31, 20192023

OR

| ☐ | |||||

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from _________ to _________

Commission File Number: 001-38984

CASTLE BIOSCIENCES, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 77-0701774 | |||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| 77546 | ||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

(866) 788-9007

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

| Common Stock, $0.001 par value per share | CSTL | The Nasdaq Global Market | ||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨☐ No x☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨☐ No x☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x☒ No ¨☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x☒ No ¨☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of ‘‘large accelerated filer,’’ ‘‘accelerated filer,’’ ‘‘smaller reporting company,’’ and ‘‘emerging growth company’’ in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | Accelerated filer | ||||||||||

| Non-accelerated filer | Smaller reporting company | ||||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨☐ No x☒

The registrant’saggregate market value of voting and non-voting common stock was not publicly tradedequity held by non-affiliates of the registrant as of theJune 30, 2023 (the last business day of the registrant’s most recently completed second fiscal quarter.quarter) was $311 million based on the closing price of the registrant’s common stock on June 30, 2023, as reported by the Nasdaq Global Market.

As of February 28, 2020,21, 2024, there were 17,192,35127,449,983 shares of common stock, $0.001 par value $0.001 per share, issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement to be filed with the Securities and Exchange Commission, or SEC, subsequent to the date hereof pursuant to Regulation 14A in connection with the registrant’s 20202024 Annual Meeting of Stockholders, are incorporated by reference into Part III of this Annual Report on Form 10-K. We intendThe registrant intends to file such proxy statement with the SEC not later than 120 days after the conclusion of the registrant’sits fiscal year ended December 31, 2019.

2023.

Table of Contents

| Page | |||||||||

| Item 1. | |||||||||

| Item 1A. | |||||||||

| Item 1B. | |||||||||

| Item | |||||||||

| Item 2. | |||||||||

| Item 3. | |||||||||

| Item 4. | |||||||||

| Item 5. | |||||||||

| Item 6. | |||||||||

| Item 7. | |||||||||

| Item 7A. | |||||||||

| Item 8. | |||||||||

| Item 9. | |||||||||

| Item | |||||||||

| Item 9B. | |||||||||

| Item 9C. | |||||||||

| Item 10. | |||||||||

| Item 11. | |||||||||

| Item 12. | |||||||||

| Item 13. | |||||||||

| Item 14. | |||||||||

| Item 15. | |||||||||

| Item 16. | |||||||||

F- | |||||||||

1

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements.statements within the meaning of the Private Securities Litigation Reform Act of 1995 that are subject to risks and uncertainties. The forward-looking statements are contained principally in the sections entitled “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business.” These statements relate to future events or to our future financial performance and involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Forward-looking statements include, but are not limited to, statements about:

•estimates of our total addressable market (“TAM”), future revenue and addressable patient populations, expenses, capital requirements and our needs for additional financing;

•expectations with respect to reimbursement for our products, including third-party payor reimbursement and coverage decisions;

•anticipated cost, timing and success of our products in development,product candidates, and our plans to research, develop and commercialize new tests;

•the impact of geopolitical and macroeconomic developments, such as the Israel-Hamas war, and the ongoing conflict between Ukraine and Russia and related sanctions on our business;

•our ability to obtain funding for our operations, including funding necessary to complete the expansion of our operations and development of our product candidates;pipeline products;

•the implementation of our business model and strategic plans for our products, technologies and businesses;business;

•expectations with respect to acquisitions of businesses, assets, products or technologies;

•our ability to manage and grow our business by expanding our sales to existing customers, or introducing our products to new customers;customers, addressing areas of high clinical need or reducing healthcare costs;

•our ability to develop and maintain sales and marketing capabilities;

•regulatory developments in the United States and foreign countries;

•the performance of our third-party suppliers;

•the success of competing diagnostic products that are or become available;

•our ability to attract and retain key personnel; and

•our expectations regarding our ability to obtain and maintain intellectual property protection for our products and our ability to operate our business without infringing on the intellectual property rights of others.

In some cases, you can identify these statements by terms such as “anticipate,” “believe,” “could,” “estimate,” “expects,” “intend,” “may,” “plan,” “potential,” “project,” “should,” “will,” “would” or the negative of those terms, and similar expressions that convey uncertainty of future events or outcomes. These forward-looking statements reflect our management’s beliefs and views with respect to future events and are based on estimates and assumptions as of the date of this Annual Report on Form 10-K and are subject to risks and uncertainties. In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based upon information available to us as of the date of this Annual Report on Form 10-K, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain and investors are cautioned not to unduly rely upon these statements. We discuss many of the risks associated with the forward-looking statements in this Annual Report on Form 10-K in greater detail underin the headingsection entitled “Risk Factors.” Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. Given these uncertainties, you should not place undue reliance on these forward-looking statements.

2

RISK FACTORS SUMMARY

We face many risks and uncertainties, as more fully described in this Annual Report on Form 10-K under the heading “Risk Factors.” Some of these risks and uncertainties are summarized below. The summary below does not contain all of the information that may be important to you, and you should read this summary together with the more detailed discussion of these risks and uncertainties contained in “Risk Factors.”

Risks Related to our Financial Condition

•A significant portion of our revenue comes from a small number of third-party payors.

•Due to how we recognize revenue, our quarterly and annual revenues may not reflect our underlying business.

•We have incurred significant losses since inception, and we may never achieve profitability.

•We are an early, commercial-stage company and have a limited operating history, which may make it difficult to evaluate our current business and predict our future performance.

•Our quarterly and annual operating results and cash flows may fluctuate in the future, which could cause the market price of our stock to decline substantially.

•If our internal control over financial reporting is not effective, we may not be able to accurately report our financial results or file our periodic reports in a timely manner, which may cause adverse effects on our business and may cause investors to lose confidence in our reported financial information and may lead to a decline in our stock price.

•We may need to raise additional capital to fund our existing operations, commercialize new products, or expand our operations.

Risks Related to our Business

•Our revenue currently depends primarily on sales of DecisionDx®-Melanoma and our other dermatologic tests, and we will need to generate sufficient revenue from this and other products to grow our business.

•Unfavorable U.S. and global economic conditions could adversely affect our business, financial condition, results of operations or cash flows.

•Public health crises, such as pandemics or similar outbreaks, could adversely impact our business.

•Billing for our products is complex and requires substantial time and resources to collect payment.

•We rely on third parties for sample collection, preparation and delivery.

•We rely on our database of samples for some of the development and improvement of our products. Depletion or loss of our samples could significantly harm our business.

•If our primary clinical laboratory facilities become damaged or inoperable, or we are required to vacate our existing facilities, our ability to perform our tests and pursue our research and development efforts may be jeopardized.

•New product development involves a lengthy and complex process, and we may be unable to develop and commercialize, or receive reimbursement for, on a timely basis, or at all, new products.

•We rely on limited or sole suppliers for some of the reagents, equipment, chips and other materials used by our products, and we may not be able to find replacements or transition to alternative suppliers.

•The sizes of the TAM for our current and future products have not been established with precision and may be smaller than we estimate.

•The diagnostic testing industry is subject to rapid change, which could make our current or future products obsolete.

Risks Related to Reimbursement and Government Regulation

•We generally have limited reimbursement coverage for our products, and if third-party payors, including government and commercial payors, do not provide sufficient coverage of, or adequate reimbursement for, our products, our commercial success, including revenue, will be negatively affected.

3

•We conduct business in a heavily regulated industry and failure to comply with federal, state and foreign laboratory licensing requirements including those established by the Centers for Medicare and Medicaid (“CMS”) and the applicable requirements of the U.S. Food and Drug Administration (“FDA”) or any other regulatory authority, could cause us to lose the ability to perform our tests, experience disruptions to our business, or become subject to administrative or judicial sanctions.

•Interim, topline and preliminary data from our clinical studies that we announce or publish from time to time may change as more data become available and are subject to audit and verification procedures that could result in material changes in the final data.

•Changes in healthcare policy, statutes or regulations, or our ability to comply with applicable healthcare requirements, could have a material adverse effect on our business and operations.

Risks Related to Intellectual Property

•If we are unable to obtain and maintain sufficient intellectual property protection for our technology, our ability to successfully commercialize our products may be impaired.

•Our commercial success depends significantly on our ability to operate without infringing upon the intellectual property rights of third parties.

•We depend on information technology systems that we license from third parties. Any failure of such systems or loss of licenses to the software that comprises an essential element of such systems could significantly harm our business.

Risks Related to Employee Matters and Managing Growth and Other Risks Related to Our Business

•We are highly dependent on the services of our key personnel, including our President and Chief Executive Officer.

•Our employees, clinical investigators, consultants, speakers, and vendors and any current or potential commercial partners may engage in misconduct or other improper activities, including non-compliance with regulatory standards and requirements and insider trading.

•We have engaged in, and may continue to engage in, strategic transactions, such as the acquisition of businesses, assets, products or technologies, which could be disruptive to our existing operations, divert the attention of our management team and adversely impact our liquidity, cash flows, financial condition and results of operations.

•Product or professional liability lawsuits against us could cause us to incur substantial liabilities and could limit our commercialization of our products.

•Our business could be adversely affected by natural disasters, public health crises and other events beyond our control.

Risks Related to Ownership of Our Common Stock

•The price of our common stock may be volatile or may decline regardless of our operating performance, and you may lose all or part of your investment.

•We have broad discretion in the use of working capital and may not use it effectively or in ways that increase our share price.

•We have and may continue to enter into related party transactions that create conflicts of interest, or the appearance of conflicts of interest, which may harm our business and cause our stock price to decline.

•The concentration of our stock ownership will likely limit your ability to influence corporate matters, including the ability to influence the outcome of director elections and other matters requiring stockholder approval.

•Delaware law and provisions in our amended and restated certificate of incorporation and amended and restated bylaws could make a merger, tender offer or proxy contest difficult, thereby depressing the trading price of our common stock.

•Our amended and restated certificate of incorporation provides that the Court of Chancery of the State of Delaware is the exclusive forum for certain disputes between us and our stockholders, which could limit our stockholders’ ability to obtain a favorable judicial forum for disputes with us or our directors, officers or employees.

4

PART I

Item 1. Business.

As used in this Annual Report on Form 10-K, unless the context indicates or otherwise requires, “Castle Biosciences,” “the Company,” “we,” “us,”Biosciences”, the “Company”, “we”, “us”, and “our” refer to Castle Biosciences, Inc., a Delaware Corporation.

Overview

Our Testing Solutions

Our tests are a commercial-stage dermatological cancer company focused on providing physicians and their patients withdesigned to deliver personalized clinically actionable genomic information to make more accurate treatmenthelp better inform care decisions. We believe that the traditional approachFor our tissue based tests, we use multi-analyte assays with algorithmic analysis (“MAAA”) to developing a treatment plan for certain cancers using clinical and pathology factors alone can be improved by incorporating personalized genomic information. Our non-invasive genomic products utilize proprietary algorithmscharacterize an individual patient’s biology to provide an assessment of a patient’sinform specific risk of metastasis or recurrenceprogression.

Test Portfolio and Market Overview

The foundation of theirour business is our dermatologic cancer allowing physiciansfranchise. We currently offer five commercially available proprietary MAAA tests for use in the dermatologic, gastroenterology and ocular fields and a proprietary pharmacogenomic (“PGx”) test to identifyguide optimal drug treatment for patients who are likelydiagnosed with depression, anxiety and other mental health conditions.

Maintaining commercial success for our existing test portfolio requires generating ongoing evidence, such as clinical use documentation, to benefit from an escalationsupport appropriate clinician adoption, reimbursement success and guideline inclusion. The clinical validity and utility of care as well as those who may avoid unnecessary medicalour test portfolio is supported by peer-reviewed publications and surgical interventions. Our lead product, ongoing clinical studies. Collectively, approximately 140 peer-reviewed articles have been published demonstrating the analytical validity, clinical validity and clinical utility of the tests in our portfolio.

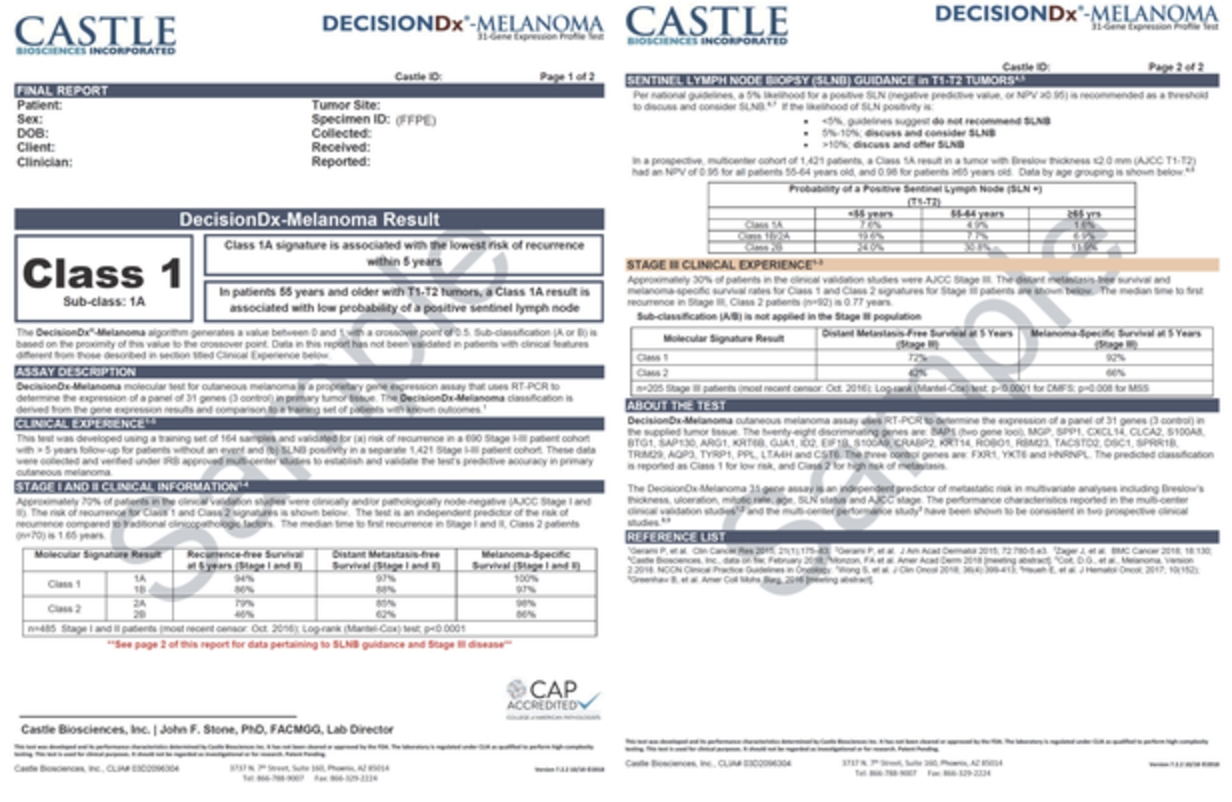

DecisionDx-Melanoma

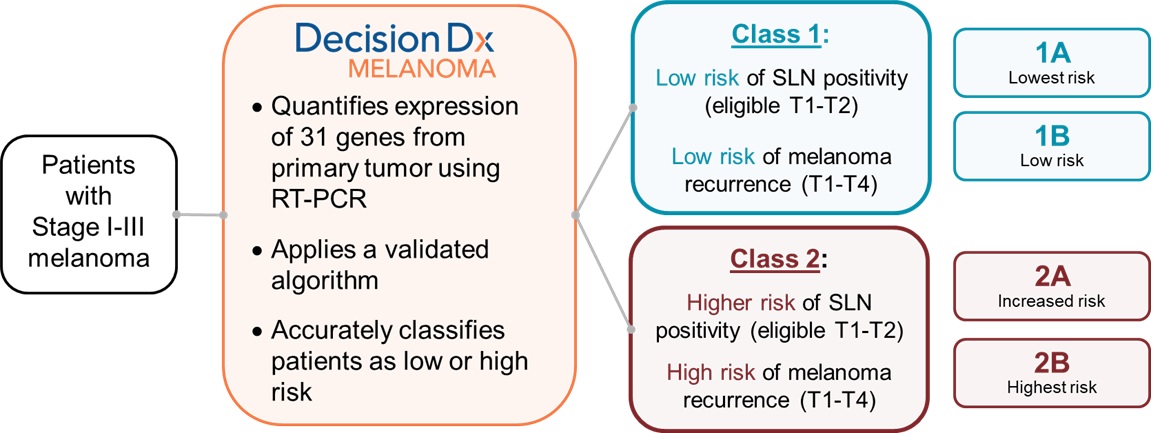

DecisionDx-Melanoma is aour proprietary multi-generisk stratification gene expression profile or GEP,(“GEP”) test that predicts the risk of metastasis, or recurrence, for patients diagnosed with invasive cutaneous melanoma (“CM”), a deadly skin cancer. We also market DecisionDx-UM,

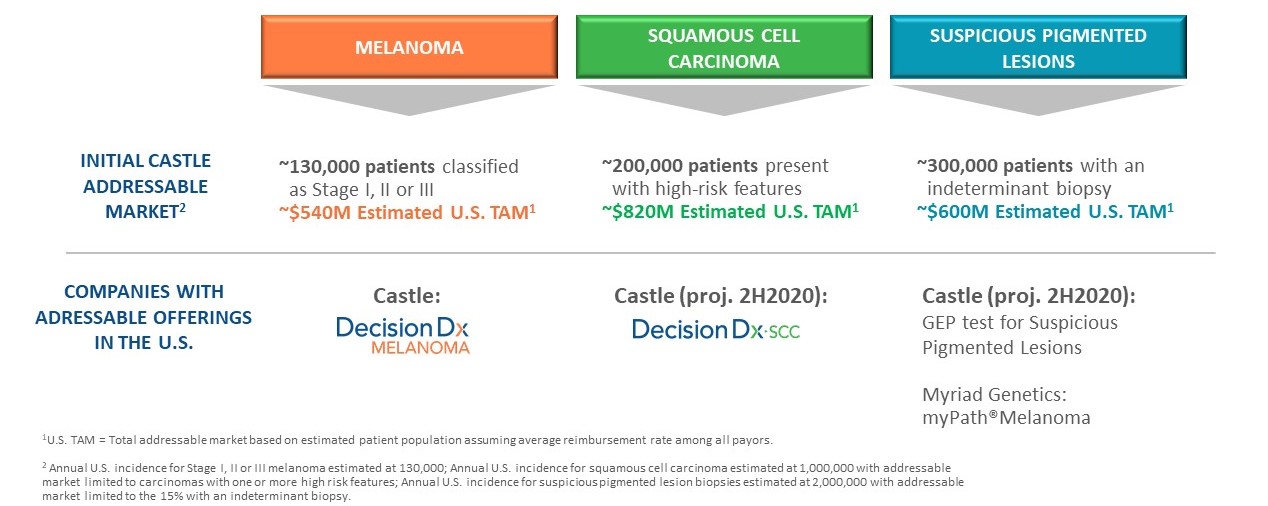

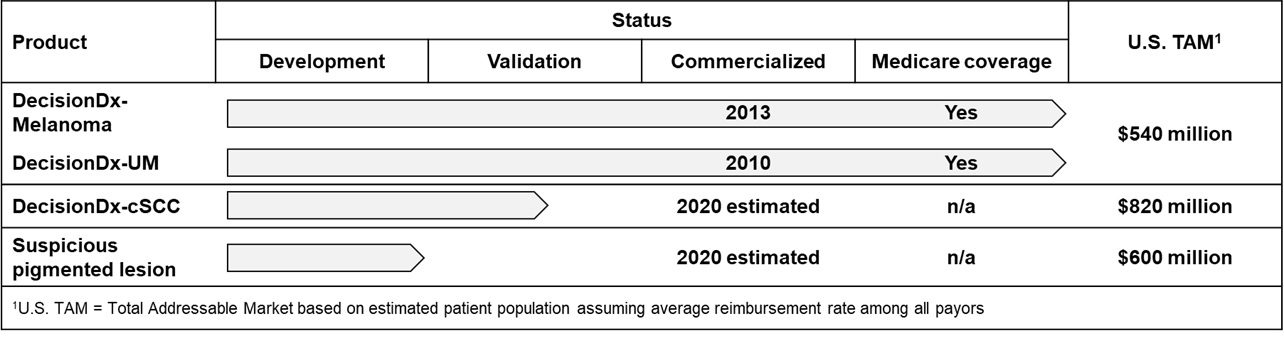

In a typical year, we estimate approximately 130,000 patients are diagnosed with invasive CM in the United States, representing an estimated U.S. TAM of approximately $540 million. This estimated annual incidence number is based upon a calculation using data from the U.S. Surveillance, Epidemiology, and End Results registries and subsequently adjusted for the documented underreporting of melanoma diagnoses which range from 30%-72%. Based on currently available data, we estimate the targetable clinician base treating melanoma is a proprietary GEP test that predicts the risk of metastasis for patients with uveal melanoma, a rare eye cancer.between 11,000 and 15,000. Based on the substantial clinical evidence that we have developed, we have received Medicare coverage for both of our products, which representsDecisionDx-Melanoma. We estimate that approximately 50% of our addressable patient population. We also have two proprietary products in late-stage development that address cutaneous squamous cell carcinoma, or SCC, and suspicious pigmented lesions, which are indications with high clinical need in dermatological cancer.

As of December 31, 2023, 49 peer-reviewed articles, six of which were published in 2023, support the clinical validity, clinical utility and impact on outcomes of our DecisionDx-Melanoma test. Based on our published data, we believe is underreported. In addition, our two late-stage proprietary products in development target approximately 200,000 patients diagnosed with SCC with high-risk features and approximately 300,000 patients with suspicious pigmented lesions without a definitive diagnosis of skin cancer. We estimatehave shown that the total addressable U.S. market for these three indications is approximately $2.0 billion.

5

DecisionDx-SCC

DecisionDx®‑SCC is our proprietary non-invasive genomic DecisionDx-Melanoma product to address this diagnostic discordance in patients with Stage I-III cutaneous melanoma. The product interrogates the biology of a patient’s tumor by analyzing the gene expression profile of 31 genes, a process made possible by our proprietary algorithm, developed using machine learning techniques. DecisionDx-Melanoma reports the risk of metastasis or recurrence for a patient’s melanoma into two classes and two subclasses, ranging from Class 1A, the lowest risk group, through Class 2B, the highest risk group, based on the genomics of the patient’s tumor. Physicians and patients use this additional tumor-specific genomic information, along with traditional staging criteria, to make better-informed decisions about how to manage the disease.

MyPath Melanoma

MyPath® Melanoma is our proprietary GEP test offering for patients with difficult-to-diagnose melanocytic lesions. Of the two million suspicious pigmented lesions are unusual-looking lesions that may be melanoma. There are approximately two million skin biopsies performed specifically for the diagnosis of melanomabiopsied annually in the United States. Approximately 15% of these biopsies are classified as indeterminate, in which case a pathologist cannot make a definitive diagnosis as to whether the biopsy is benign or malignant. Using a lower target reimbursement rate,States, we estimate the U.S. TAM at $600 million.

As of December 31, 2023, MyPath Melanoma has been clinically validated through three tissues comprising the uveal tractstudies and varyis supported by location17 peer-reviewed publications.

TissueCypher

TissueCypher® is our proprietary risk stratification spatial omics test designed to predict future development of high-grade dysplasia (“HGD”) and/or esophageal cancer in patients with non-dysplastic (“ND”), indefinite dysplasia (“IND”) or low-grade dysplasia (“LGD”) Barrett’s esophagus (“BE”).

There are approximately 90% occurring in choroid, 5%four million patients in the ciliary bodyU.S. currently diagnosed with BE and 5% inapproximately 415,000 patients annually undergo an endoscopic biopsy with a subsequent diagnosis of ND, IND or LGD BE, representing an estimated U.S. TAM of approximately $1 billion.

As of December 31, 2023, our TissueCypher test is supported by 14 peer-reviewed clinical validation and utility studies.

DecisionDx-UM

DecisionDx®-UM is our proprietary risk stratification GEP test that helps healthcare providers predict the iris. Uvealrisk of metastasis for patients with uveal melanoma may(“UM”), also be referred to as ocular melanoma.

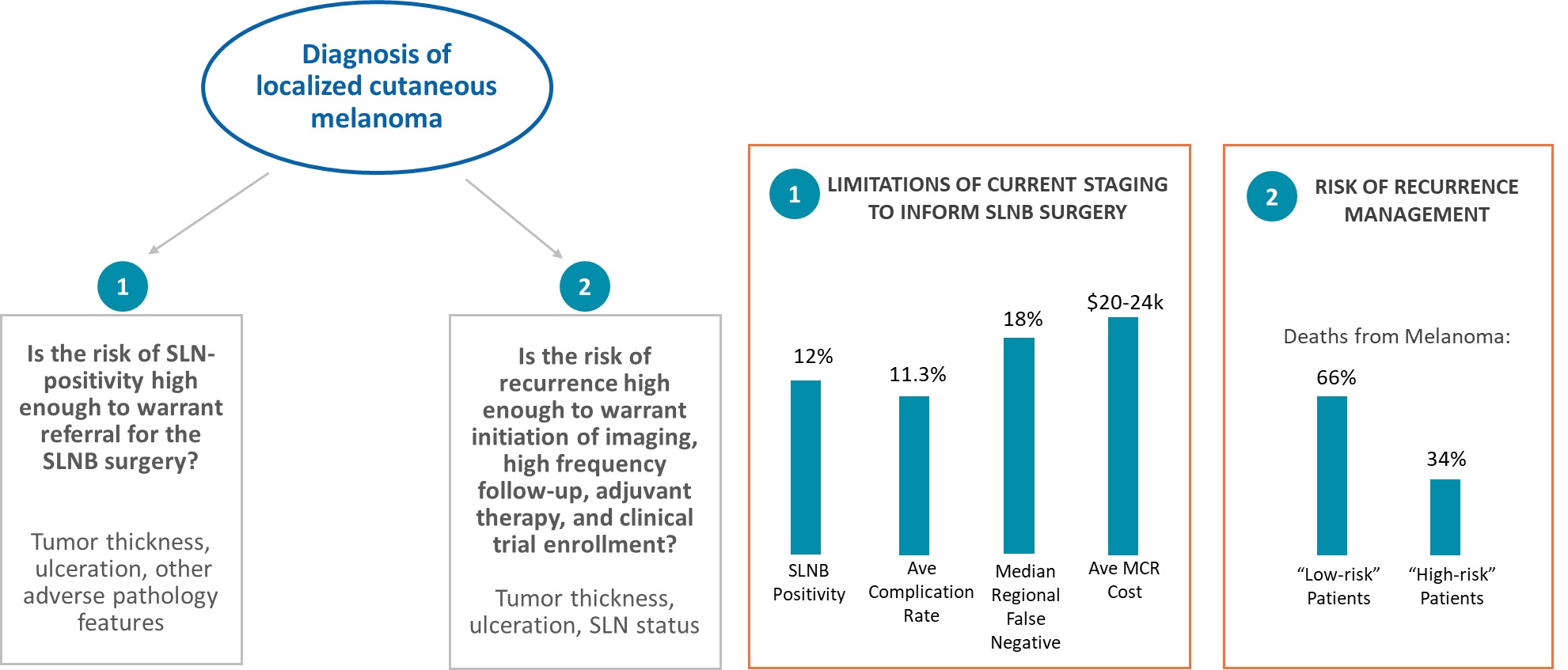

The dermatologic skin cancer market has significant unmet clinical needs, as clinical and pathology staging systems have traditionally applied a population-wide approachMedicare eligible population represents close to estimate an individual patient’s risk of metastasis and have not incorporated the genomics of a patient’s tumor biology. This is unlike the diagnostic process applied to other solid tumors, such as breast and prostate cancer, where the broader use of genomics to understand tumor biology has led to individualized patient treatment plans. Not incorporating tumor biology leads to a discordance between the estimated and actual risk of metastasis, which results in over- and under-treatment as well as increased healthcare costs.

DecisionDx-UM has been clinically validated by an independent prospective, multi-center study, by multiple retrospective and prospective single-center studies. As of December 31, 2023, our DecisionDx-UM test is supported by 25 peer-reviewed publications.

IDgenetix

IDgenetix® is our proprietary PGx test that helps guide optimal drug treatment for high-patients diagnosed with major depressive disorder, schizophrenia, bipolar disorder, anxiety disorders, social phobia, obsessive-compulsive personality disorder, post-traumatic stress disorder, and low-risk patients. For example, a 2014 study compared the AJCC version 7 and National Comprehensive Cancer Network, or NCCN, systemsattention deficit hyperactivity disorder. IDgenetix is designed to assess concordance between the AJCC and NCCN systems. The AJCC system classified 82% as low risk while the NCCN system classified 13% as low risk. As such, this level of discordance results in the risk assessment staging systems minimally impactingprovide important genetic information to clinicians to help guide personalized treatment plans with patients frequently being over- and under-treated.

We estimate a U.S. TAM of approximately $5 billion associated with this study, NCCNtest. We began offering the IDgenetix test following our acquisition of AltheaDx, Inc. (“AltheaDx”), in April 2022.

IDgenetix is supported by a published, peer-reviewed randomized controlled trial that demonstrated clinical utility over the standard of care when physicians used IDgenetix prior to prescribing a sensitivity of 96% while PPVmedication. The trial was 7% and NPV was 90.5%. The low PPV means that 93 out of 100 NCCN high risk SCC’s did not actually metastasize. AJCC and BWH demonstrated a sensitivity of 38.5% and 25%, respectively, PPV of 33% and 35%, respectively and NPV of 88% and 86%, respectively. If one relies just upon NCCN, the low PPV means that developing an adjuvant treatment plan that includes radiation, or chemotherapy or complete lymph surgical dissection, or a combination of these, for a high-risk patient may be appropriate for the one out of fourteen high-risk patients who will metastasize but not for the remaining thirteen patients who would not have metastasized. For AJCC and BWH, the PPV does improve but it also means that two out of three patients would be recommended for an adjuvant treatment plan who will not benefit. These accuracy metrics have created significant discordance in the approach to managing patients with high-risk features, from one of the spectrum being intervention for all high-risk patients to “watch and wait” for all high-risk patients. The end result is an unacceptableconducted across 20 independent clinical discordance in the approach to treatment plans and significant over- and under-treatment for a diagnosis that leads to the most skin cancer deaths insites within the United States.States specializing in psychiatry, internal medicine, obstetrics & gynecology, and family medicine. As of December 31, 2023, our IDgenetix test is supported by 19 peer-reviewed publications.

6

We usehave significant expertise in developing proprietary algorithms, conducting clinical studies and using the gene expression profile of an individual patient’s tumor biology to inform specific prognosis of metastasis or recurrence and aid the decision-making process of the treating physician and their patient to help optimize health outcomes and reduce healthcare costs.necessary instrumentation required for efficiently developing our pipeline products. Due to the biological complexity of skin cancers,diseases, developing accurate products takes scientific diligence, stringent clinical protocols, machine learning expertise, proprietary algorithms and significant investments of time and capital. In addition, the underlying tissue samples and associated clinical outcomes data required to develop and validate these products are difficult to obtain. Once successfully developed

In 2021, we announced the launch of our innovative pipeline initiative to develop a genomic test, or series of tests, aimed at predicting response to systemic therapy in patients with moderate to severe atopic dermatitis, psoriasis and validated, commercial success requiresrelated inflammatory skin conditions. In the generation of ongoing evidence such as clinical use documentation to support appropriate physician adoption, reimbursement success and guideline inclusion.

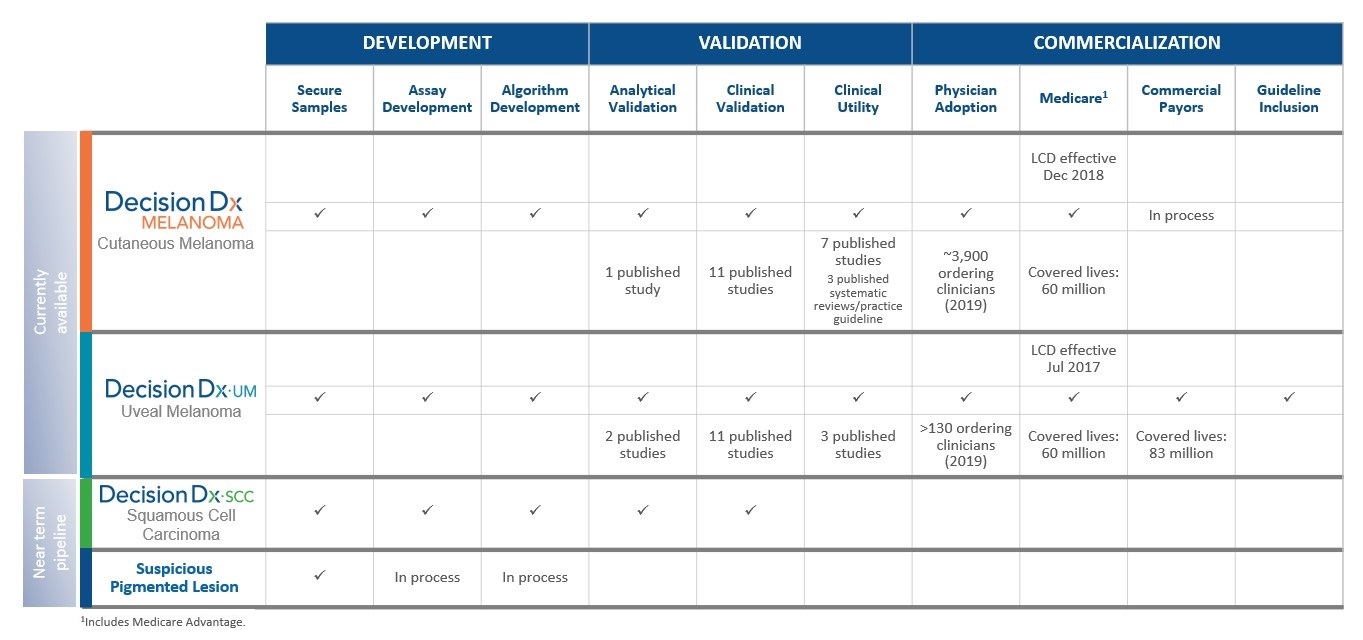

In addition to the U.S. TAM for both products have been published since completioneach of the initial clinical validation studies and have confirmedtests in our portfolio disclosed above, we estimate that the accuracy oftests in our products. Also, multiple clinical impact studies have demonstrated a significant impact on physician decisionspipeline add an additional estimated $5.7 billion to alter their treatment plan when the results of our test are considered in concert with the traditional clinical and pathology factors. Both of our currently marketed proprietary products are reimbursed by Medicare under positive coverage policies. In addition, we have received widespread positive private payor coverage and positive guideline inclusion for DecisionDx-UM, our first melanoma test. Since commercial launch, we have processed more than 60,000 clinical patient samples.

We expect to continue to pursue pipeline initiatives for tests that will branch out upstream, downstream and parallel to our test reports, physicians changed a patient’s treatmentexisting tests, within or adjacent to our established dermatological call points.

Acquisitions

From time to time, we may consider engaging in more than 50%transactions such as acquisitions of cases, indicating physician confidence in the evidence underlying our reports.

In April 2022, we acquired AltheaDx, a commercial-stage molecular diagnostics company specializing in the United States. We have received positive local coverage determinations, or LCDs, providing Medicare coveragefield of PGx testing services, for bothtotal consideration of $47.6 million, consisting of $30.5 million in cash and $17.1 million in shares of our common stock, adding the IDgenetix test to our portfolio.

In December 2021, we extended our commercial products. These LCDs facilitate reimbursementportfolio of proprietary tests into the gastroenterology market through our acquisition of Cernostics, Inc. (“Cernostics”) and the TissueCypher platform for total consideration of $49.0 million.

In May 2021, we acquired Myriad myPath, LLC and MyPath Melanoma test from Medicare, which represents approximately 50% of the addressable patient population. We also have third-party payor coverage for over 100 million lives for DecisionDx-UM and over 14 million lives for DecisionDx-Melanoma.

7

Test Report Volume and Revenue

The number of test reports we discovered, developed and completed validation for DecisionDx-Melanoma. This productgenerate is designeda key indicator that we use to help physicians identify high-risk patients with Stage I and II melanomas based on biological information, or expression, from 31 genes within their tumor tissue. DecisionDx-Melanoma does not change a physician’s standard diagnostic workflow for suspicious pigmented lesions, which includes performing the initial biopsy procedure and placing the biopsied tissue in formalin. The dermatopathologist then embeds the specimen in a paraffin block, cuts sections that are stained for viewing under a microscope and makes a diagnosis of invasive melanoma. We then extract and purify RNA from sections of the remaining specimen to runassess our test. We report test results in two classes and two subclasses. Class 1A represents the lowest risk group, Class 1B represents a low risk group, Class 2A represents an increased risk group and Class 2B represents the highest risk group.

| Study | Design | # of Patients | % Change in Management |

| Berger et al. CMRO 2016 | Prospectively tested cohort, multi-center. Retrospective pre test / post test management. | 156 | 53% |

| Dillon et al. SKIN J Cutan Med 2018 | Prospective, multi-center: pre test / post test management. | 247 | 49% |

| Farberg et al. J Drugs Derm 2017 | 169 physician impact study: patient vignettes with pre test / post test management. | n/a | 47-50% |

| Schuitevoerder et al. J Drugs Derm 2018 | Prospectively tested cohort, single center. Retrospective pre test / post test management; and modeling of prospective cohort. | 91 | 52% |

below:

| Years Ended December 31, | |||||||||||||||||||||||||||||

| 2023 | 2022 | 2021 | 2020 | 2019 | |||||||||||||||||||||||||

| DecisionDx-Melanoma | 33,330 | 27,803 | 20,328 | 16,232 | 15,529 | ||||||||||||||||||||||||

DecisionDx‑SCC(1) | 11,442 | 5,967 | 3,510 | 485 | — | ||||||||||||||||||||||||

Diagnostic GEP offering(2) | 3,962 | 3,561 | 2,662 | 73 | — | ||||||||||||||||||||||||

| Dermatologic Total | 48,734 | 37,331 | 26,500 | 16,790 | 15,529 | ||||||||||||||||||||||||

| DecisionDx-UM | 1,674 | 1,711 | 1,618 | 1,395 | 1,526 | ||||||||||||||||||||||||

TissueCypher(3) | 9,100 | 2,128 | 27 | — | — | ||||||||||||||||||||||||

IDgenetix(4) | 10,921 | 3,249 | — | — | — | ||||||||||||||||||||||||

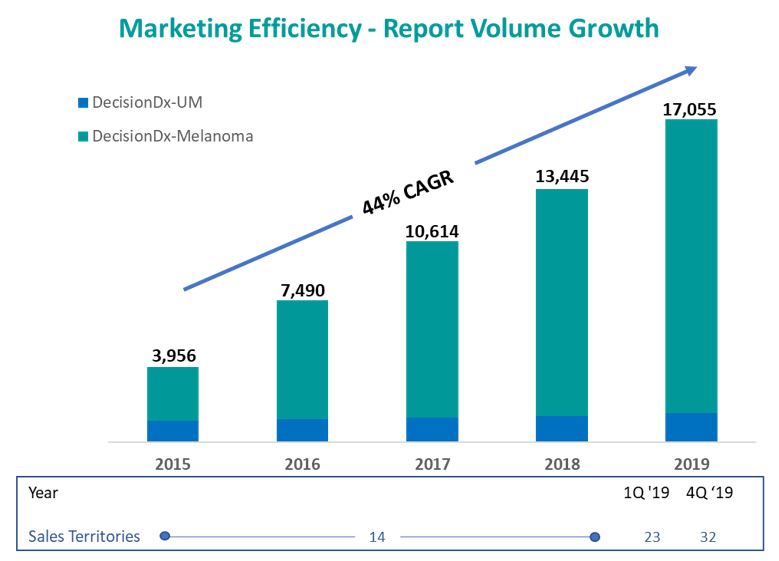

| Grand Total | 70,429 | 44,419 | 28,145 | 18,185 | 17,055 | ||||||||||||||||||||||||

| Net Revenues (in thousands) | $ | 219,788 | $ | 137,039 | $ | 94,085 | $ | 62,649 | $ | 51,865 | |||||||||||||||||||

(2)Includes MyPath Melanoma and provideDiffDx®-Melanoma. On November 2, 2020, we commercially launched our DiffDx-Melanoma test. We began offering MyPath Melanoma following our acquisition of the Myriad MyPath Laboratory on May 28, 2021. We offered both MyPath Melanoma and DiffDx-Melanoma under our Diagnostic GEP offering until February 2023 when we suspended the clinical offering of DiffDx-Melanoma.

(3)We began offering the TissueCypher on December 3, 2021, following our acquisition of Cernostics. Our TissueCypher test report volumes primarily derived from processed backlog orders. We temporarily paused accepting additional orders in July 2023 and resumed accepting new orders in a better PPV while maintaining similar NPV.phased approach in September 2023. We believe this product candidate will enable more informed clinical decisions regarding adjuvant intervention and other management decisions. We have ongoing multi-center studies involving more than 75 U.S. centers. Our development analysis has identified a proprietary gene expression profile algorithm that exhibits significant differential expression between non-recurrent and recurrent cases. Data fromcompleted processing of our initial validation study was presented at the American Society of Dermatologic Surgerypre-existing backlog orders in October 2019. 2023 and continue to accept new orders as of December 31, 2023.

(4)We have ongoing studiesbegan offering the IDgenetix test on April 26, 2022, following our acquisition of AltheaDx. Includes both single-gene and based upon our current progress we intend to commercially launch DecisionDx-SCC in the second half of 2020.multi-gene tests.

Our Commercial Channel

Sales and Marketing

Our sales and marketing efforts are currentlyprimarily focused on the United StatesU.S. skin cancer, market.gastroenterology and mental health markets. We employ a direct sales and marketing strategy to educate dermatologists, surgeonsclinicians and other physiciansassociated personnel on the clinical and economic benefits of our products. Our sales approach is highly technical, and our team is trained to articulate the scientific and clinical evidence behind our products and how they influence the clinical care pathway and ultimately improve patient outcomes. Our sales force is focused on educating and informing the entire patient care team, which consists of treating clinicians, nurses, laboratory and pathology personnel, and finance administrators, on the appropriate use and value of our test.

We increased our outside sales territories from 14 to 23 in the first quarter of 2019 and also added supporting inside sales associates, medical affairs and marketing staff. We believed that this increase in customer-facing personnel would increase the adoption of our products as we would be able educate more physicians on the clinical benefits of our products. We did see the promotion responsiveness that we anticipated and conducted a second expansion in December 2019 such that our outside sales territories now total 32. Based upon current knowledge, we believe that an optimally efficient dermatology salesforce to support our DecisionDx-Melanoma test ranges between 35 and 45 individuals. However, we will also continue to evaluate our mix of outside sales territories, inside sales support, marketingassess market response in determining further commercial expansions and medical affairs in the context of our DecisionDx-Melanoma test and our near-term pipeline product and adjust our investments based upon these evaluations.

Medical Affairs

We also deploy an experienced medical affairs group to assist education of treating physiciansclinicians and key opinion leaders, to identify and engage sites for our sponsored clinical studies and to evaluate collaborative study opportunities. Our medical affairs strategy complements our sales, and marketing and clinical research operations efforts.

We design our test reports with input from physicianswill continue to provide an easy to read risk classification and present specific actionable information to enable improved treatment decisions between patients and their physicians. We update our test reports as new data become available that may impact physicians’ treatment decisions based onassess the usemarket needs in determining further expansions of our tests. For example, the most recent update to our DecisionDx-Melanoma report incorporates data from our prospective multicenter 1,421 patient study showing how our tests can predict the likelihood of a patient experiencing an SLN-positive result from the SLNB surgery.medical affairs team.

Reimbursement

The primary source of revenue for our products is reimbursement from third-party payors, which includes government payors, such as Medicare, and commercial payors, such as insurance companies. Achieving broad coverage and reimbursement of our current products by third-party payors and continued Medicare coverage are key components of our financial success. De novo coverage by government and

We bill third-party payors for our pipeline tests will be important over time.

8

which meet certain criteria for Medicare and Medicare Advantage beneficiaries. A “covered life” means a public comment period that opened on October 7, 2019 and closed on November 21, 2019. Based upon our analysis from the close of the public comment period to issuance of the final LCD for other MolDX LCDs, we estimate that this expanded LCD may be final in the second half of 2020. However, there is no assurance that the timing of our LCD will match the recent experience of other MolDX LCDs.

The Medicare rates discussed below are prior to giving effect to applicable sequestration in effect from time to time as described in further detail under "Government Regulation and to guide surveillance and referral to medical oncology for those patients. Similar to cutaneous melanoma the median age at diagnosis for uveal melanoma is estimated at 58-62 years old, therefore the Medicare eligible population represents close to 45% of the addressable market.Product Approval—Healthcare Reform" included in Part 1, Item 1, “Business”, in this Annual Report on Form 10-K.

Commercial Third-Party Payors

We are actively engaged in efforts to achieve broad coverage and reimbursement for our current and future products, followed by contracting with commercial payors. Achieving positive coverage reduces the need for appeals and reduces failures to collect from the patient’s commercial insurance payor. Even with positive coverage decisions, we still experience delays in time to payment. Achieving in-network contracts with third-party payors can shorten the time required to receive payments. Implementing our strategy includes our managed care and medical affairs teams educating third-party payors regarding our strong clinical utility and outcomes data, which we believe validates the value of our products and will persuade more third-party payors to provide value-based reimbursement.

We have broad positive policy coverage for our DecisionDx-UM test weand have executed contracts with certain commercial payors. For our other tests, we engage third-party payors for positive coverage and anticipate increases in contracting in 2020 and 2021. We also have received positive policy recommendations from many third-party technical assessment review groups.

Dependence on Third-Party Payors

We receive a substantial portion of our revenue from a small number of third-party payors, primarily Medicare, BlueCross BlueShield affiliates and Medicare Advantage plans.payors. Our revenue from patients covered by Medicare Medicare Advantage plans, United Healthcare and BlueCross BlueShield plans, as a percentage of total revenue, was 49%, 29%, 6% and 6%, respectively, for the year ended December 31, 2023. Additionally, there was a commercial payor from which 14% of our revenue from patients was derived for the year ended December 31, 2023.

Government Payors

Medicare coverage is limited to items and services that are within the scope of a Medicare benefit category and that are reasonable and necessary for the diagnosis or treatment of an illness or injury. The controlling Medicare regulation for guiding the assessment of reasonable and necessary of diagnostic laboratory tests is 42 CFR. Section 410.32(a). Medicare Administrative Contractors (“MACs”) can provide coverage through evidentiary based reviews as well as more formal processes such as development of local coverage determinations (“LCD”).

Our laboratories are located in Phoenix, Arizona and Pittsburgh, Pennsylvania. The MAC responsible for administering claims for laboratory services located in Arizona is Noridian Healthcare Solutions, LLC (“Noridian”). Noridian has a joint operating agreement with Palmetto GBA MolDX (“Palmetto”) where Palmetto is responsible for reviewing genomic based tests. The MAC responsible for administering claims for laboratory services located in Pennsylvania is Novitas Solutions (“Novitas”).

Medicare

DecisionDx-Melanoma

Palmetto issued a final expanded test-specific LCD for DecisionDx-Melanoma, effective November 22, 2020. With this expanded LCD and the accompanying billing and coding articles, we estimate that a significant majority of the DecisionDx-Melanoma tests performed for Medicare patients will meet the coverage criteria. Noridian adopted the same coverage policy as Palmetto and also issued an expanded final LCD for DecisionDx-Melanoma, effective December 6, 2020. On May 19, 2022, Palmetto finalized an LCD that converted the DecisionDx-Melanoma test-specific LCD to a “foundational” LCD with Noridian issuing the same on June 16, 2022. The final LCDs did not result in any changes in coverage.

DecisionDx-UM

Palmetto issued a final test-specific LCD for DecisionDx-UM, which became effective in July 2017, and Noridian issued a similar LCD that became effective in September 2017. We estimate that a significant majority of the DecisionDx-UM tests performed for Medicare patients will meet the coverage criteria.

9

MyPath Melanoma and DiffDx-Melanoma

MyPath Melanoma was covered under a test-specific LCD policy through Noridian that became effective in June 2019. BlueCross BlueShield plansEffective August 6, 2023, Palmetto and Noridian issued LCDs that converted the test-specific MyPath Melanoma LCD to a “foundational” LCD and provided coverage for both MyPath Melanoma and DiffDx-Melanoma.

DecisionDx‑SCC

We issue our DecisionDx-SCC tests from our Pittsburgh and Phoenix labs, with a majority of tests being issued from our Pittsburgh lab. As previously discussed, Novitas is the MAC responsible for administering claims for test reports issued by our Pittsburgh laboratory.

We requested and received an evidentiary review of our DecisionDx-SCC by Novitas during the first quarter of 2022. Based upon this review, DecisionDx-SCC test began receiving coverage in April 2022.

On June 9, 2022, Novitas posted a draft oncology biomarker LCD that proposes to rely upon evidentiary reviews sourced from three databases for all oncology biomarker tests: ClinGen, OncoKB and National Comprehensive Cancer Network (“NCCN”). We believe the purpose of the proposals in this draft LCD are to streamline future reviews. Two of the databases do not review GEP tests and NCCN has not yet, to our knowledge, reviewed DecisionDx-SCC. If finalized as proposed, then DecisionDx-SCC would not have been included as a covered test in the associated billing and coding article. The comment period for the draft LCD ended on September 6, 2022.

On June 2, 2023, Novitas posted a finalized oncology biomarker LCD pursuant to which the DecisionDx-SCC test would no longer be covered by Medicare Advantage plans representeffective July 17, 2023. However, on July 6, 2023, Novitas suspended the final version of the LCD and announced its intent to post a new proposed LCD for comment and presentation at an aggregationopen meeting. On July 27, 2023, Novitas posted a nearly identical proposed oncology biomarker LCD that continues to intend to rely upon evidentiary reviews sourced from three databases: ClinGen, OncoKB and NCCN. The proposed LCD also recommends non-coverage for our DecisionDx-SCC test. The comment period for the proposed LCD ended on September 9, 2023. We cannot predict whether this LCD will be finalized as proposed or what the timing of any final LCD might be.

As previously discussed, the Palmetto MolDX program oversees MAAA tests that are reported from our Phoenix laboratory and Noridian is the MAC responsible for administering claims for test reports issued by our Phoenix laboratory. In the second quarter of 2020, we submitted our technical assessment dossier for DecisionDx-SCC to Palmetto and Noridian. The dossier was accepted as complete in the third quarter of 2020. On June 8, 2023, both Palmetto and Noridian posted a preliminary draft LCD recommending no coverage for DecisionDx-SCC. The comment period for the draft LCDs ended on July 22, 2023.

Advanced Diagnostic Laboratory Tests

Advanced Diagnostic Laboratory Test (“ADLT”) status is a designation granted by CMS for clinical diagnostic laboratory tests offered and furnished by a single laboratory and covered under Medicare Part B that meet one of the following criteria:

Criterion A: The test:

•Is an analysis of multiple payors making independentbiomarkers of DNA, RNA or proteins;

•When combined with an empirically derived algorithm, yields a result that predicts the probability a specific individual patient will develop a certain condition or conditions, or respond to a particular therapy or therapies;

•Provides new clinical diagnostic information that cannot be obtained from any other test or combination of tests; and

•May include other assays.

Criterion B: The test is cleared or approved by the FDA. Laboratories requesting ADLT status under this criterion are required to submit documentation of premarket approval (“PMA”) or premarket notification from the FDA.

All five of our commercially available proprietary MAAA tests have been reviewed by the CMS and have been granted ADLT status. ADLT status is not an indication of future coverage.

10

Medicare Reimbursement Rates

DecisionDx-Melanoma

On May 17, 2019, CMS determined that DecisionDx-Melanoma meets the criteria for “new ADLT” status. Our rate is set annually based upon the median private payor rate for the first half of the second preceding calendar year. For example, the rate for 2023 was set using median private payor rate data from January 1, 2021 to June 30, 2021. Our rate for 2022 and 2023 was $7,193 per test and is $7,193 for 2024.

DecisionDx-UM

On May 17, 2019, CMS determined that DecisionDx-UM meets the criteria for “existing advanced diagnostic laboratory test” status, also referred to as “existing ADLT” status. Our rate is set annually based upon the median private payor rate for the first half of the second preceding calendar year. For example, the rate for 2023 was set using median private payor rate data from January 1, 2021 to June 30, 2021. Our rate for 2022 and 2023 was $7,776 per test and is $7,776 for 2024.

MyPath Melanoma

On September 6, 2019, MyPath Melanoma was approved as a “new ADLT”. Our rate is set annually based upon the median private payor rate for the first half of the second preceding calendar year. Our rate for 2022 was $1,950 per test. Our 2023 rate was set at $1,755 per test, based on data submitted by the predecessor owner of the Myriad MyPath Laboratory relating to the first half of 2021. Our 2024 rate is set at $1,950 per test.

DiffDx-Melanoma

In the second quarter of 2022, we obtained a Proprietary Laboratory Analyses (“PLA”) code for DiffDx-Melanoma. In 2023, DiffDx-Melanoma went through the CMS gapfill process which concluded in September 2023 with CMS posting a final MAC-specific gapfill rate of $1,950 per test. Our rate for 2024 is $1,950 per test.

Diagnostic GEP Offering

Our Diagnostic GEP offering included MyPath Melanoma and DiffDx-Melanoma. We began offering MyPath Melanoma following our acquisition of the Myriad MyPath Laboratory on May 28, 2021. Our internal data indicates that we have improved the technical performance of MyPath Melanoma such that it is now comparable to the technical performance of DiffDx-Melanoma. As such, following an internal assessment of the clinical value of offering both tests, we made the decision to suspend the clinical offering of DiffDx-Melanoma in February 2023.

DecisionDx‑SCC

In the first quarter of 2022, we requested that Novitas conduct a medical review of our DecisionDx-SCC test. That review was completed towards the end of that quarter. In the second quarter of 2022, following the completion of a requested medical review and pricing of our DecisionDx-SCC test by Novitas, we obtained a PLA code and began receiving reimbursement decisions; however, these plans often basefrom Novitas for DecisionDx-SCC at a rate of $3,873 per test.

On June 30, 2023, CMS determined DecisionDx-SCC meets the criteria for “new ADLT” status. Effective July 1, 2023 and through March 31, 2024, CMS set the initial period rate equal to the list price of $8,500 per test. Effective April 1, 2024 and through December 31, 2025, the published CLFS rate for DecisionDx-SCC will be based on the median private payor rates received between July 1, 2023 and November 30, 2023. We submitted the median private payor data to CMS during the data reporting period in December 2023. Future rates will be set annually based upon the median private payor rate for the first half of the second preceding calendar year. ADLT status determines the process by which the rate is set and is not an indication of Medicare coverage.

11

TissueCypher

TissueCypher is processed in our Pittsburgh, Pennsylvania laboratory and falls under the Medicare jurisdiction managed by Novitas. From January 1, 2022 through March 31, 2022, we received payments for claims according to the published CLFS rate at $2,513 per test. On March 24, 2022, CMS determined TissueCypher meets the criteria for “new ADLT” status. ADLT status exempts TissueCypher from what is called the “14-day rule,” which simplifies the billing process for Medicare patients. From April 1, 2022 through December 31, 2022, CMS set the initial period rate equal to the original list price of $2,350 per test. Effective January 1, 2023, the published CLFS rate for TissueCypher was set at $4,950 per test, which will remain effective through December 31, 2024. This rate is based on the median private payor rates received between April 1, 2022 and August 31, 2022. Thereafter, the rate will be set annually based upon the median private payor rate for the first half of the second preceding calendar year.

IDgenetix

IDgenetix is currently covered under a Noridian LCD policy and accompanying billing and coding article developed by MolDX. The Medicare coverage includes depression and the following seven additional mental health conditions beyond major depressive disorder: schizophrenia, bipolar disorder, anxiety disorders, social phobia, obsessive-compulsive personality disorder, post-traumatic stress disorder and attention deficit hyperactivity disorder. IDgenetix has historically been billed to Medicare using an unspecified CPT code along with the IDgenetix test-specific MolDX Z-code (the “IDgenetix Z-Code”). We acquired AltheaDx and the IDgenetix test in April 2022 and received Medicare reimbursement decisions on common guidelinesat a rate of approximately $1,500 per test. In February 2023, MolDX notified us that as part of its annual CPT code updates, IDgenetix should shift billing to a different multi-test generic gene sequencing CPT code (the “New CPT Code”) and continue using the IDgenetix Z-Code beginning in March 2023. The New CPT Code was set at $917 per test while the test went through CMS’s Gapfill pricing process. We believed the new CPT Code, in conjunction with the IDgenetix Z-Code, did not describe all of the components of the IDgenetix test and thus, was not appropriate for IDgenetix. We subsequently obtained a test-specific PLA CPT code which can influence multiple plans simultaneously.became effective October 1, 2023. In November 2023, CMS posted its final CLFS determination which crosswalks our PLA CPT code to an existing PLA code at a rate of $1,336 per test effective January 1, 2024.

Competition

We are focused on providing high value diagnostic and prognostic solutions for dermatological cancers. We believe, today,improving health through innovative tests that there is limited existing competition for our products that provide evidence-based genomic solutions to physicians and their patients.guide patient care.

We believe the principal competitive factors in our target markets include:

•Proprietary, disciplined approach to genomic and proteomic analysis including the use of proprietary deep learning, machine learning, artificial intelligence and other techniques to identify and optimize genebiomarker selection and algorithmic approaches to answer the clinically important questions with accuracyaccurate tests. This involves the ability to design and efficiently conduct the right clinical studies at the right time;

•Research and development investments to document the quality, quantity, consistency and strength of the clinical validity data, the impact our products have on clinical use, and demonstration of net health outcome improvement that reduce health system costs;

•Maintaining a strong reputation with the treating physicianclinician by providing consistent, transparent, and clinically relevant information that will improve the appropriate management of their patients;

•Ease of use in accessing our products, reimbursement support for the physician and their patientour patients and laboratory reports that clearly communicate the clinically relevant data points;

•Demonstrated ability to work with, and secure coverage and reimbursement from, governmental and commercial payors;

•Ability to efficiently commercialize pipeline products to the same customer base asboth our current products.and our pipeline products

We believe we compete favorably on the factors described above.

Today, our principal competition for DecisionDx-Melanoma is existing traditional clinical and pathology staging criteria. While some clinical and pathology criteria have changed over time, this approach has been the standard of care in the United States for many years, and physiciansclinicians may be unwilling to accept the validity of the published data and adopt our test until it has become incorporated into national guidelines. In December 2019, we did see positive improvements in the NCCN guidelines as it related to our DecisionDx-Melanoma test. However, it is too early to understand the impact on physician adoption and commercial payer coverage. In addition, we currently face, or may in the near future,

12

face, competition from a limited number of companies who are working in this disease space, such as NeracareSkylineDx/Tempus/Quest, AMLo/Avero and SkylineDx.Neracare. In the future, we may face additional competitors.

We are unaware of late-stage work being performed to develop and validate a product that would compete with DecisionDx-SCC. We believe that the current primary competitor for DecisionDx-SCC is existing traditional clinical and pathology staging criteria. In the future, we may face additional competitors.

DecisionDx-UM competes with a subsidiary of LabCorp and several academic laboratories, all of which have had tests available for several years. To date, our data has demonstrated that DecisionDx-UM is clinically and statistically superior to these products. In the future, we may face additional competitors.

With respect to IDgenetix, our pipeline product for suspicious pigmented lesions suchcompetition arises from other parties using the same or similar methods as well as alternative methods of PGx testing. IDgenetix competes with Myriad Genetics. If we are successful in validating a clinically useful product, then we expect to compete favorably with them.Genetics’s GeneSight test, Genomind’s PGx test, and tests from numerous other commercial and academic laboratories.

Laboratory Operations

Raw Materials and Suppliers

We procure certain reagents, equipment, chips/cards and other materials used to perform our tests from sole suppliers such as ThermoFisher Scientific, Inc., and Qiagen, Inc. Some of these items are unique to these suppliers and vendors. While we have developed alternate sourcing strategies for these materials and vendors and while we have experienced no business interruption due to an inability to source these materials, we cannot be certain whether these strategies will be effective or whether alternative sources will be available when we need them. If these suppliers can no longer provide us with the materials we need to perform our test services, they do not meet our quality specifications, or we cannot obtain acceptable substitute materials, our business would likely be negatively affected.

License Agreement with The Washington University

In November 2009, we entered into a license agreement or the License Agreement,(the “License Agreement”) with WUSTLThe Washington University in St. Louis, Missouri (“WUSTL”) to license certain patent rights and technical information from WUSTL for the development of melanoma products or the Products,(the “Products”), and services or the Services.(the “Services”). The rights licensed under this agreement are used in DecisionDx-UM only.

Under the License Agreement, we obtain an exclusive, worldwide, royalty-bearing license to certain patent rights owned by WUSTL or the Patent Rights,(the “Patent Rights”) and a non-exclusive, worldwide license to certain technical information and research property owned by WUSTL, with the right to grant sublicenses under certain conditions, in order to develop the Products and the Services. WUSTL retains the right to use the Patent Rights for research purposes.

The Patent Rights that we license pursuant to the License Agreement have been generated through the use of U.S. government funding and are therefore subject to certain federal regulations. See “Risk Factors—Risks Related to Intellectual Property—Our in-licensed intellectual property has been discovered through government funded programs and thus may be subject to federal regulations such as “march-in” rights, certain reporting requirements

13

and a preference for U.S.-based companies, and compliance with such regulations may limit our exclusive rights, and limit our ability to contract with non-U.S. manufacturers.”

Under the License Agreement, we are required to use best efforts to carry out the activities under an agreed-upon development plan or the Development Plan,(the “Development Plan”) and meet any and all milestones set forth in the Development Plan. We are required to make milestone payments to WUSTL upon successful completion of development and commercialization milestones as set forth in the Development Plan. For each Product or Service that receives FDA approval, premarket approvalPMA or premarket notification, we are obligated to make a milestone payment to WUSTL in the mid-four digits. For the issuance of the first U.S. patent and the first foreign patent, we are obligated to make aggregate milestone payments to WUSTL in the low-five digits.

Under the License Agreement, we were obligated to pay WUSTL an initial license issue fee in the low-five digits. We are also obligated to make royalty payments to WUSTL equal to (i) a percentage in the mid-single digits of our and any of our affiliates’ or sub-licensees’ net sales of the Products and (ii) a percentage in the low-single digits of our and any of our affiliates’ or sub-licensees’ revenue from the Services. We are also obligated to make royalty payments to WUSTL in the low-to-mid single digit percentage of net sales, with minimum royalty payments to WUSTL every six-month period following the first commercial sale.

The term of the License Agreement will continue for ten years following the last-to-expire valid claim relating to the Patent Rights, unless terminated earlier. WUSTL may terminate the License Agreement upon written notice in the event of (i) our material breach if such breach remains uncured for 90 days, (ii) the exercise of certain rights by us with respect to the Patent Rights and/or the licensed technical information outside the scope of the License Agreement, or (iii) for certain insolvency-related events. We may terminate the License Agreement without cause upon written notice to WUSTL and payment of any amount due to WUSTL under the License Agreement.

Intellectual Property

Our core technology for our products is related to methods and devices for analysis of genetic expression. Using this technology, we are able to provide a more accurate prediction of a patient’s metastatic risk as compared to other methods. We have secured and continue to pursue intellectual property rights globally, including through patent protection covering analysis of metastasis in cutaneous melanoma, as well asthe treatment of cutaneous squamous cell carcinoma.SCC, BE and gastroenterology, and PGx for mental illness. We also rely on trademarks, trade secrets, know-how, continuing technological innovation and potential in-licensing opportunities to develop and maintain our proprietary position. For more information, please see “Risk Factors—Risks Related to Intellectual Property.”

14

Patents and Patent Applications

We have developed a global patent portfolio that as of the date of this Annual Report on Form 10-K,December 31, 2023, is comprised ofas follows:

| Number of Applications and Patents | ||||||||||||||||||||

| Commercial Focus | United States | International | Total | |||||||||||||||||

| Owned Patent Families | ||||||||||||||||||||

| Methods for predicting risk of metastasis in cutaneous melanoma | 3 | 19 | 22 | |||||||||||||||||

| Methods of diagnosing and treating patients with pigmented skin lesions | 1 | — | 1 | |||||||||||||||||

| Methods of diagnosing and treating patients with cutaneous squamous cell carcinoma | 2 | 19 | 21 | |||||||||||||||||

| Determining Prognosis and Treatment based on Clinical-Pathologic Factors and Continuous Multigene-Expression Profile Scores | 1 | — | 1 | |||||||||||||||||

| Diagnosing and Treating Atopic Dermatitis and/or Psoriasis | 2 | — | 2 | |||||||||||||||||

| Diagnosing and Treating Uveal Melanoma | 1 | — | 1 | |||||||||||||||||

| Genes and gene signatures for diagnosis and treatment of melanoma | 7 | 33 | 40 | |||||||||||||||||

| Method for automated tissue analysis | 2 | 3 | 5 | |||||||||||||||||

| Systems and compositions for diagnosing BE and methods of using same | 3 | 13 | 16 | |||||||||||||||||

| Methods of predicting progression of BE | 2 | 22 | 24 | |||||||||||||||||

| Expression profiling using microarrays | 1 | — | 1 | |||||||||||||||||

| Licensed Portfolio from WUSTL | ||||||||||||||||||||

| Method for predicting risk of metastasis | 2 | — | 2 | |||||||||||||||||

| Compositions and methods for detecting cancer metastasis | 2 | 2 | 4 | |||||||||||||||||

| Total | 29 | 111 | 140 | |||||||||||||||||

Included in the table above are 16 issued patents, including five issued U.S. patents and nine pending patent applications, including three U.S. applications. Our patent portfolio consists of three owned patent families and an exclusively in-licensed portfolio from WUSTL, which includes six pending and77 issued patents or patent applications across two families.international patents. This global patent portfolio has filing dates ranging from 20092007 to 2018,2023, and therefore are projected to expire between 20292027 and 2038,2043, subject to any patent term extension or patent term adjustment that might be available in a particular jurisdiction. The owned and licensed families contain issued patents and pending applications that relate to devices, systems, and methods for macromolecular analysis, and reflect our active and ongoing research programs. The commercial foci of these patent families are discussed below.

Individual patents extend for varying periods depending on the date of filing of the patent application or the date of patent issuance and the legal term of patents in the countries in which they are obtained. Generally, patents issued for regularly filed applications in the United States are granted a term of 20 years from the earliest effective non-provisional filing date. In addition, in certain instances, a patent term can be extended to recapture a period due to delay by the United States Patent and Trademark Office or USPTO(the “USPTO”) in issuing the patent as well as a portion of the term effectively lost as a result of the FDA regulatory review period. However, as to the FDA component, the restoration period cannot be longer than five years and the total patent term including the restoration period must not exceed 14 years following FDA approval. The duration of foreign patents varies in accordance with provisions of applicable local law, but typically is also 20 years from the earliest effective non-provisional filing date. However, the actual protection afforded by a patent varies on a product-by-product basis, from country to country, and depends upon many factors, including the type of patent, the scope of its coverage, the availability of regulatory-related extensions, the availability of legal remedies in a particular country and the validity and enforceability of the patent.

Trademarks and Trade Secrets

As of the date of this Annual Report on Form 10-K, our U.S. trademark portfolio contained seven16 trademark registrations.

We rely upon trade secrets, know-how, continuing technological innovation and potential in-licensing opportunities to develop and maintain our competitive position. We seek to protect our intellectual property and proprietary technology, in part, by entering into confidentiality agreements and intellectual property assignment agreements with our employees, consultants, corporate partners and, as applicable, our advisors. These agreements are designed to protect our proprietary information and, in the case of the invention assignment agreements, to grant us ownership of technologies that are developed through a relationship with an employee or a third party. These agreements may be breached, and we may not have adequate remedies for any breach. We additionally seek to preserve the

15

integrity and confidentiality of our data and trade secrets, such as our proprietary algorithms, by maintaining the physical security of our premises and physical and electronic security of our information technology systems. While we have confidence in these individuals, organizations and systems, agreements or security measures may be breached, and we may not have adequate remedies for any breach. In addition, our trade secrets may otherwise become known or be independently discovered by competitors. To the extent that our commercial partners, collaborators, employees and consultants use intellectual property owned by others in their work for us, disputes may arise as to the rights in related or resulting know-how and inventions.

Government Regulation and Product Approval

Regulations

Clinical Laboratory Improvement Amendments of 1988

As a clinical reference laboratory, we are required to hold certain federal, state and local licenses, certifications and permits to conduct our business. Under CLIA, we are required to hold a certificate applicable to the type of laboratory tests we perform and to comply with standards applicable to our operations, including test processes, personnel, facilities administration, equipment maintenance, recordkeeping, quality systems and proficiency testing. We must maintain CLIA compliance and certification to be eligible to bill for diagnostic services provided to Medicare beneficiaries.

To renew our CLIA certificate, we are subject to survey and inspection every two years to assess compliance with program standards. Because we areour Phoenix, Arizona laboratory is a College of American Pathologists, or CAP accredited laboratory, CMS does not perform thismay defer the survey and inspection and relies on our CAP survey and inspection.to those conducted by CAP. We may also be subject to additional unannounced inspections. The regulatory and compliance standards applicable to the testing we perform may change over time,periodically, and any such changes couldare published by CAP. Our SOPs, documents & records are updated accordingly and as needed. Any such changes may have a material effect on our business.

Penalties for non-compliance with CLIA requirements include suspension, limitation or revocation of the laboratory’s CLIA certificate, as well as directed plan of correction, state on-site monitoring, civil money penalties, civil injunctive suit or criminal penalties.

State Laboratory Licensing

In addition to federal certification requirements of laboratories under CLIA, CLIA provides that states may adopt laboratory regulations and licensure requirements that are more stringent than those under federal law. Such laws, among other things, establish standards for the day-to-day operation of a clinical reference laboratory, includingwhich includes ensuring personnel have the adequate knowledge and training and skills required of personnel andto maintain quality control. We currently provide laboratory services in all 50 states andstates. Additionally, we maintain out-of-state laboratory licenses in New York, California, Maryland, Pennsylvania and Rhode Island.

Because we receive specimens from the state of New York, our clinical reference laboratory is required to be licensed by New York, underhave a lab director with a specific certificate of qualification and is subject to biennial New York laws and regulations.state inspections to ensure the lab is compliant with New York lawlicensing standards. New York regulations also mandatesmandate proficiency testing for laboratories licensed under New York state law, regardless of whether such laboratories are located in New York. If a laboratory is out of compliance with New York statutory or regulatory standards, the New York State Department of Health or NYSDOH,(the “NYSDOH”) may suspend, limit, revoke or annul the laboratory’s New York license, censure the holder of the license, or assess civil money penalties. We have received writtenformal approval from the NYSDOH to offer the following of our proprietary DecisionDx-Melanoma DecisionDx-UM and DecisionDx-PRAME products in New York. If we wereassays to be found out of compliance with New York laboratory requirements,patients: DecisionDx-Melanoma, DecisionDx-CMSeq, DecisionDx-UM, DecisionDx-PRAME, DecisionDx-UMSeq, DecisionDx-SCC, MyPath Melanoma, and DiffDx-Melanoma. We have been given conditional approval for IDgenetix from the NYSDOH while we could be subjectwork through the formal review process. In July 2022, we submitted TissueCypher for review by the NYSDOH. We had been given clearance to such sanctions, which could harmtest New York state patients by the New York’s Clinical Laboratory Evaluation Program while our business.applications were under review. On September 12, 2023, we received our Clinical Laboratory Permit from NYSDOH for our Pennsylvania laboratory.

Federal Oversight of Laboratory Developed Tests

The laws and regulations governing the marketing of diagnostic products are evolving, extremely complex, and in many instances, there are no significant regulatory or judicial interpretations of these laws and regulations. Clinical laboratory tests are regulated under CLIA, as administered by CMS, as well as by applicable state laws. In addition, the Federal Food, Drug and Cosmetic Act or FDCA,(the “FDCA”) defines a medical device to include any instrument, apparatus, implement, machine, contrivance, implant, in vitro reagent, or other similar or related article, including a

16

component part, or accessory, intended for use in the diagnosis of disease or other conditions, or in the cure, mitigation, treatment, or prevention of disease, in man or other animals. Our in vitro testing products are considered by the FDA to be subject to regulation as medical devices. Among other things, pursuant to the FDCA and its implementing regulations, the FDA regulates the research, testing, manufacturing, safety, labeling, storage, recordkeeping, pre-market clearance or approval, marketing and promotion, and sales and distribution of medical devices in the United States to ensure that medical products distributed domestically are safe and effective for their intended uses. In addition, the FDA regulates the export of medical devices manufactured in the United States to international markets.

Although the FDA has statutory authority to assure that medical devices are safe and effective for their intended uses, the FDA has generally exercised its enforcement discretion and not enforced applicable regulations with respect to in vitro diagnostics that are designed, manufactured, and used within a single laboratory for use only in that laboratory. These tests are referred to as LDTs.Laboratory Developed Tests (“LDTs”). As a result, we believe our diagnostic services are currently subject to the FDA’s enforcement discretion and are not currently subject to the FDA’s oversight. However, reagents, instruments, software or components provided by third parties and used to perform LDTs may be subject to regulation.

In recent years, the FDA has stated its intention to modify its enforcement discretion policy with respect to LDTs. For example,Most recently, on July 31, 2014, the FDA notified Congress of its intent to modify, in a risk-based manner, its policy of enforcement discretion with respect to LDTs. On October 3, 2014,2023, the FDA issued two draft guidance documents entitled “Framework for Regulatory Oversight of Laboratory Developed Tests (LDTs),” or the Framework Guidance, and “FDA Notification and Medical Device Reporting for Laboratory Developed Tests (LDTs),” or the Reporting Guidance. The Framework Guidance states that FDA intends to modifyproposed regulations under which it would phase out its policy of enforcement discretion with respect to LDTs in a risk-based manner consistent with the classification of medical devices generally in Classes I through III. The Reporting Guidance would further enable FDA to collect information regarding the LDTs currently being offered for clinical use through a notification process, as well as to enforce its regulations for reporting safety issues and collecting information on any known or suspected adverse events related to the use of an LDT.

Medical Device Regulatory Framework