UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 20202023 or

☐ Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Commission File Number 0-53713

OTTER TAIL CORPORATION

(Exact name of registrant as specified in its charter)

| | | | | |

Minnesota (State or other jurisdiction of incorporation or organization) | 27-0383995 (I.R.S. Employer Identification No.) |

| |

215 South Cascade Street, Box 496, Fergus Falls, Minnesota (Address of principal executive offices) | 56538-0496 (Zip Code) |

Registrant's telephone number, including area code: 866-410-8780

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Shares, par value $5.00 per share | OTTR | The Nasdaq Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | | | | | | | | | | | | |

| | Large Accelerated Filer ☑ | | Accelerated Filer ☐ | | |

| | Non-Accelerated Filer ☐ | | Smaller Reporting Company ☐ | | Emerging Growth Company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange ActAct. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued

its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

TheAs of June 30, 2023, the aggregate market value of common stock held by non-affiliates computed by reference to the last sales price on June 30, 2020 was$1,546,518,975. $3,646,181,401.

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of the latest practicable date:

41,510,45541,710,521 Common Shares ($5 par value) as of February 16, 2021.January 31, 2024.

DOCUMENTS INCORPORATED BY REFERENCE

The Registrant's definitive Proxy Statement for its 20212024 Annual Meeting of Shareholders is incorporated by reference into Part III of this Form 10-K.

| | | | | | | | |

| | Description | Page |

| | |

| | | |

| | |

| | |

| | |

| ITEM 1. | | |

| ITEM 1A. | | |

| ITEM 1B. | | |

| ITEM 1C. | | |

| ITEM 2. | | |

| ITEM 3. | | |

| ITEM 3A. | | |

| ITEM 4. | | |

| | |

| ITEM 5. | | |

| ITEM 6. | | |

| ITEM 7. | | |

| ITEM 7A. | | |

| ITEM 8. | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| ITEM 9. | | |

| ITEM 9A. | | |

| ITEM 9B. | | |

| ITEM 9C. | | |

| | |

| ITEM 10. | | |

| ITEM 11. | | |

| ITEM 12. | | |

| ITEM 13. | | |

| ITEM 14. | | |

| | |

| ITEM 15. | | |

| ITEM 16. | | |

| | |

The following abbreviations or acronyms are used in the text. | | | | | | | | | | | | | | |

ACE | Affordable Clean Energy | | MNDOC | Minnesota Department of Commerce |

| AFUDC | Allowance for Funds Used During Construction | | MPCAkwh | Minnesota Pollution Control Agencykilowatt-hour |

| AME | Available Maximum Energy | | LSA | Lignite Sales Agreement |

| ARO | Asset Retirement Obligation | | MPUCMDT | Minnesota Public Utilities CommissionMetering and Distribution Technology |

| ARP | Alternative Revenue Program | | MISO | Midcontinent Independent System Operator |

| ASC | Accounting Standards Codification | | MW | Megawatt |

| BTD | BTD Manufacturing, Inc. | | MPUC | MVP | Multi-Value ProjectMinnesota Public Utilities Commission |

| CCMC | Coyote Creek Mining Company, L.L.C. | | MWNAV | megawattsNet Asset Value |

COCCS2

| carbon dioxideCarbon Capture and Sequestration | | NDDEQ | North Dakota Department of Environmental Quality |

ECRCDD | Environmental Cost RecoveryCooling Degree Day | | NDPSC | North Dakota Public Service Commission |

EEICIS | Edison Electric InstituteCritical Security Controls | | NERC | North American Electric Reliability Corporation |

EEPCO2

| Carbon dioxide | | Energy Efficiency Plan | Northern Pipe | Northern Pipe Products, Inc. |

EPACOSO | Committee of Sponsoring Organizations of the Treadway Commission | | OTC | Environmental Protection AgencyOtter Tail Corporation |

| ECO | Energy Conservation and Optimization Rider | | OTP | Otter Tail Power Company |

| EEI | Edison Electric Institute | | Paris Agreement | United Nations Framework Convention on Climate Change |

| EEP | Energy Efficiency Plan | | PFAS | Polyfluoroalkyl substances |

| EGU | Electric Generating Unit | | PIR | Phase-in Rider |

| EPA | Environmental Protection Agency | | PSLRA | Private Securities Litigation Reform Act of 1995 |

| ERISA | Employee Retirement Income Security Act of 1974 | | PTCs | Production tax credits |

| ESSRP | Executive Survivor and Supplemental Retirement Plan | | PACEPVC | Partnership in Assisting Community ExpansionPolyvinyl chloride |

| EUIC | Electric Utility Infrastructure Costs Rider | | RHR | Regional Haze Rule |

| FASB | Financial Accounting Standards Board | | ROE | Return on equity |

| FCA | Fuel Clause Adjustment | | REC | Renewable Energy Certificate |

| FERC | Federal Energy Regulatory Commission | | PTCsRRR | Production tax creditsRenewable Resource Rider |

GCRFOB | Generation Cost RecoveryFree on Board | | PVC | Polyvinyl chloride |

GHG | Greenhouse Gas | | RHR | Regional Haze Rule |

IRP | Integrated Resource Plan | | ROE | Return on equity |

kV | kiloVolt | | SDPUC | South Dakota Public Utilities Commission |

kWGCR | kiloWattGeneration Cost Recovery Rider | | SRECsSEC | Solar renewable energy creditsSecurities and Exchange Commission |

kwhGHG | kilowatt-hourGreenhouse Gas | | SIP | State implementation plan |

| HDD | Heating Degree Day | | SOFR | Secured Overnight Financing Rate |

| ICSP | Information and Cybersecurity Program | | T.O. Plastics | T.O. Plastics, Inc. |

LSAIRP | Lignite Sales AgreementIntegrated Resource Plan | | TCR | Transmission Cost Recovery Rider |

MerricourtITCs | Merricourt Wind Energy CenterInvestment Tax Credits | | TSR | Total Shareholder Return |

VaristarkV | Varistar CorporationkiloVolt | | VIE | Variable Interest Entity |

MISOkW | Midcontinent Independent System Operator, Inc.kiloWatt | | Vinyltech | Vinyltech Corporation |

| MNCIP | Minnesota Conservation Improvement Program | | |

| | | | |

| | | | | | | | |

| WHERE TO FIND MORE INFORMATION | | |

We make available free of charge at our website (www.ottertail.com) our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy and information statements, Forms 3, 4 and 5 filed on behalf of directors and executive officers and any amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as soon as reasonably practicable after such material is electronically filed with or furnished to the Securities and Exchange Commission (SEC). These reports are also available on the SEC's website (www.sec.gov). Information on our and the SEC's websites is not deemed to be incorporated by reference into this report on Form 10-K. | | |

| FORWARD-LOOKING INFORMATION |

This report on Form 10-K contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (the Act)PSLRA). When used in this Form 10-K and in future filings by the Company with the SEC, in the Company’s press releases and in oral statements, words such as “anticipate,” “believe,” “could,"can,"“could,” “estimate,” “expect,” "future," "goal," “intend,” "likely," “may,” “outlook,” “plan,” “possible,” “potential,” "predict," "probable," "projected ," “should,” "target," “will,” “would” or similar expressions are intended to identify forward-looking statements within the meaning of the Act.PSLRA. Such statements are based on current expectations and assumptions and entail various risks and uncertainties that could cause actual results to differ materially from those expressed in such forward-looking statements. Such risks and uncertainties include the various factors set forth in Item 1A. Risk Factors of this report on Form 10-K and in our other SEC filings.

PART I

Otter Tail Corporation (OTC) has interests in diversified operations that include an electric utility and manufacturing and plastic pipe businesses with corporate offices located in Fergus Falls, Minnesota and Fargo, North Dakota.

We classify our five operating companies into three reportable segments consistent with our business strategy and management.management structure. The following table depicts our three segments and the subsidiary entities included within each segment:

| | | | | | | | | | | | | | |

| ELECTRIC SEGMENT | | MANUFACTURING SEGMENT | | PLASTICS SEGMENT |

| Otter Tail Power Company (OTP) | | BTD Manufacturing, Inc. (BTD) | | Northern Pipe Products, Inc. (Northern Pipe) |

| | T.O. Plastics, Inc. (T.O. Plastics) | | Vinyltech Corporation (Vinyltech) |

Electric includes the generation, purchase, transmission, distribution and sale of electric energy in western Minnesota, eastern North Dakota and northeastern South Dakota. OTP,Otter Tail Power (OTP), our largest operating subsidiary and primary business since 1907, serves more than 133,000 customers in 422more than 400 communities across a predominantly rural and agricultural service territory.

Manufacturing consists of businesses engaged in the following manufacturing activities: contract machining; metal parts stamping,stamping; fabrication and painting; and production of plastic thermoformed horticultural containers, life science and industrial packaging, material handling components and extruded raw material stock. These businesses have manufacturing facilities in Georgia, Illinois and Minnesota and sell products primarily in the United States.

Plastics consists of businesses producing polyvinyl chloride (PVC) pipe at plants in North Dakota and Arizona. The PVC pipe is sold primarily in the western half of the United States and Canada.

Throughout the remainder of this report, we use the terms "Company", "us", "our", or "we" to refer to Otter Tail CorporationOTC and its subsidiaries collectively. We will also refer to our Electric, Manufacturing and Plastics segments and our individual subsidiaries as indicated above.

INVESTMENT AND GROWTH STRATEGY

We maintain a moderate risk profile by investing in rate base growth opportunities in our Electric segment and organic growth opportunities in our Manufacturing and Plastics segments.segments (collectively, our manufacturing platform). This strategy and risk profile are designed to provide a more predictable and growing earnings stream, maintainsupport quality credit ratings, and provide for dividend payments.

Our long-term focus remains on executing our credit qualitystrategy to grow our business and preserveachieving operational, commercial and talent excellence to strengthen our ability to fund our dividend.position in the markets we serve. Our goal is to deliverlong-term financial objectives include achieving a compounded annual growth rate in earnings per share between fivein the range of 5 - 7%, with a long-term earnings mix of approximately 65% from our Electric segment and seven percent over35% from our manufacturing platform. We also are targeting an annual increase in our dividend to be in the next several years, using 2020 diluted earnings per share as the base for measurement.range of 5 - 7%. We expect our earnings growth and cash flow generation to come frombe driven by rate base investments in our Electric segment and from planned earnings growth arising from existing capacities and planned investments within our Manufacturing and Plastics segments.

Over the past three years, we delivered earnings growth well in excess of our 5 - 7% target due to unique industry conditions within the PVC pipe industry, which led to extraordinary revenue, earnings and cash flow growth in our Plastics Segment. We expect these industry conditions to gradually normalize over the course of 2024 and into 2025. As they do, we expect earnings and cash flow generation within our Plastics segment to moderate from current levels. Once these industry conditions have normalized, we expect to achieve our long-term financial objectives as outlined above.

We will continue to review our business portfolio to identify additional opportunities to improve our risk profile, enhance our credit metrics and generate additional sources of cash to support the organic growth opportunities in our electric utility.Electric, Manufacturing, and Plastics segments. We will also evaluate opportunities to allocate capital to potential acquisitions withinacquisitions. We are a committed long-term owner and do not acquire companies in pursuit of short-term gains. However, we will divest of businesses which no longer fit into our Manufacturingstrategy and Plastics segments.risk profile over the long term.

We maintain a set of criteria used in evaluating the strategic fit of our operating businesses. The operating company should:

•Maintain a minimum level of net earnings and a return on invested capital in excess of the Company’s weighted averageweighted-average cost of capital,

•Have a strategic differentiation from competitors and a sustainable cost advantage,

•Operate within a stable and growing industry and be able to quickly adapt to changing economic cycles, and

•Have a strong management team committed to operational and commercial excellence.

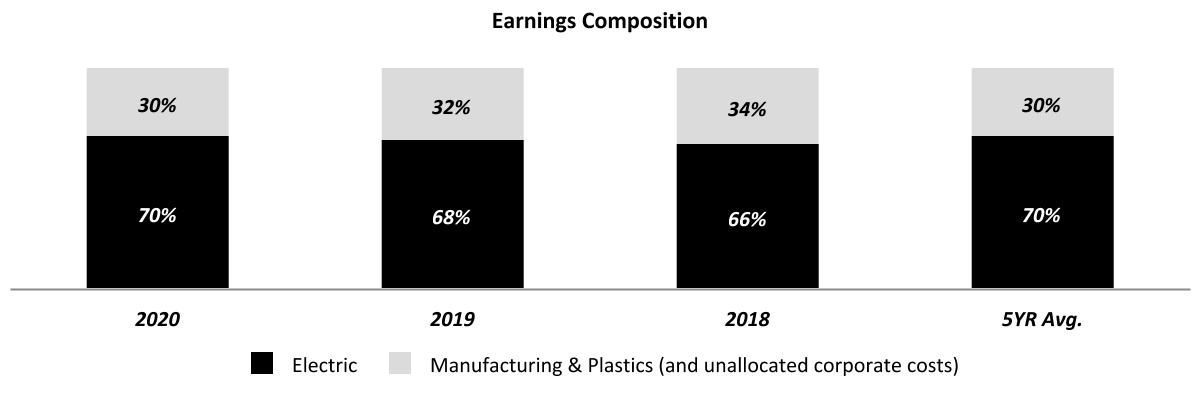

Over time, we expect our Electric segment will provide approximately 75% of our overall earnings and our Manufacturing and Plastics segments will collectively provide approximately 25% of our overall earnings and continue to be a fundamental part of our strategy.

Our actual mix of earnings in 2020, 2019, 2018and the average for the five-year periodyears ended December 31, 2020 is2023, 2022 and 2021 was as follows:

HUMAN CAPITAL

Our employees are a critical resource and an integral part of our success. We strive to provide an environment of opportunity and accountability where people are valued and empowered to do their best work. We are focused on the health and safety of our employees and creating a culture of inclusion, excellence and learning. Our human capital management efforts include monitoringlearning, and our executive annual incentive plan reflects those commitments. We monitor various metrics and objectives associated with i) employee safety, ii) workforce stability, iii) management and workforce demographics, including gender, racial and ethnic diversity, iv) leadership development and succession planning and v) productivity. We have established the following programs in furtherance of these efforts:

•Safety -Safety is one of our core values. We engageIn managing our business, we focus on the safety of our employees and have implemented safety programs and management practices to promote a third party to conduct conformity assessments annually.culture of safety. Safety is also a metric used and evaluated in determining annual incentive compensation. We continually monitor the Occupational Safety and Health Administration Total Recordable Incident Rate (number of work-related injuries per 100 employees for a one-year period) and Lost Time Incident Rate.Rate (number of employees who lost time due to work-related injuries per 100 employees for a one-year period). New cases are reported and evaluated for corrective action during monthly safety callsmeetings attended by safety professionals at all locations. Our 2023 Total Recordable Incident Rate was 1.70, compared to 2.08 in 2022 and our Lost Time Incident Rate was 0.53 in 2023, compared to 0.49 in 2022.

•Employee and Leadership Development, Succession Planning and Training Programs - We extend leadershipinvest in training and professional development intofor various levels of employees, management and leaders throughout the organizationCompany to ensure all have the necessary training and skills to perform their work well, and to build enterprise-wide understanding of our culture, strategy and processes. Annual succession planning, individual development planning, mentoring, and supervisory and leadership development programs all play a role in ensuring a capable leadership team now and in the future. Our skill progression and technical training programs help ensure we haveto retain a skilledstable and stableskilled workforce.

•Workforce Stability - Recruiting, retaining and developing employees is an important factor in our continued success and growth. We regularly evaluate our recruiting programs, employee retention and turnover rates.

Employee Engagement - To enhance productivity and employee engagement,the effectiveness of our workforce and to help our companies continue to be places where our employees choose to work and thrive, we have undertaken a multi-year series of employee engagement surveys. We use the feedback to help shape the futureemployee programs of our organization.

•Human Rights - We are committed to the protection of our employee’s freedom of expression and freedom of organization and assembly.

Diversity, Equity, and Inclusion -We communicate annuallyexpect, and are committed to, diversity, equity and inclusion as part of who we are, what we value, and how we achieve individual, business and community success. We hold every employee accountable for their behavior in maintaining a workplace free of discrimination and harassment. We have implemented education initiatives for all employees, aimed at inclusive leadership and a respectful workplace, focused on identities and culture, unconscious bias, the power of diverse teams and culturally sensitive conversations. We have implemented initiatives to improve upon our demographic profile, including revised hiring processes and a commitment to diverse slates of interview candidates.

Code of ConductBusiness Ethics -We require employees to help ensure understandingcomplete training on several topics associated with our code of the common principlesbusiness ethics to reinforce our commitment to compliance with laws, regulations and values that guide who we are and how we do business.

Across our operating companies and including our corporate team as

As of December 31, 2020,2023, we employed 2,0742,655 full-time employees:employees as shown in the table below:

| | | | | |

| Segment/Organization | Employees |

| |

| Electric Segment | |

OTP(1) | 790 | | 647 |

| Manufacturing Segment | |

| BTD | 1,0471,458 | |

| T.O. Plastics | 163192 | |

| Segment Total | 1,2101,650 | |

| Plastics Segment | |

| Northern Pipe | 10098 | |

| Vinyltech | 7980 | |

| Segment Total | 179178 | |

| Corporate | 3837 | |

| Total | 2,0742,655 | |

(1) Includes all full-time employees of Otter Tail Power Company, including employees working at jointly owned facilities. Labor costs associated with employees working at jointly owned facilities are allocated to each of the co-owners based on their ownership interest. | |

At December 31, 2020, 3722023, 378 employees of OTP arewere represented by local unions of the International Brotherhood of Electrical Workers under two separate collective bargaining agreements expiring on August 31, 20232026 and October 31, 2023.2026. OTP has not experienced any strike, work stoppage or strike vote, and considers its present relations with employees to be good.

None of the employees of our other operating companies are represented by local unions.

| | | | | | | | | | | |

| % Female | | % Racially and Ethnically Diverse |

| | | |

| Board of Directors | 36 | % | | 9 | % |

| CEO Direct Reports | 33 | % | | — | % |

| Management | 21 | % | | 4 | % |

| Non-Management Employees | 15 | % | | 15 | % |

| | | |

| | | | | |

| ELECTRIC | Contribution to Operating Revenues: 50% (2020)39% (2023), 50% (2019)38% (2022), 49% (2018)40% (2021) |

OTP, headquartered in Fergus Falls, Minnesota, is a vertically integrated, regulated utility with generation, transmission and distribution facilities to serve its more than 133,000 residential, industrialcommercial and commercialindustrial customers in a service area encompassing approximately 70,000 square miles of western Minnesota, eastern North Dakota and northeastern South Dakota.

CUSTOMERS

Our service territory is predominantly rural and agricultural and includes over 400 communities, most of which have populations of less than 10,000. While our customer base includes relatively few large customers, sales to commercial and industrial customers are significant, with one industrial customertwo customers accounting for 11%21% of segment operating revenues for the year ended December 31, 2020.2023 and 16% for the year ended December 31, 2022.

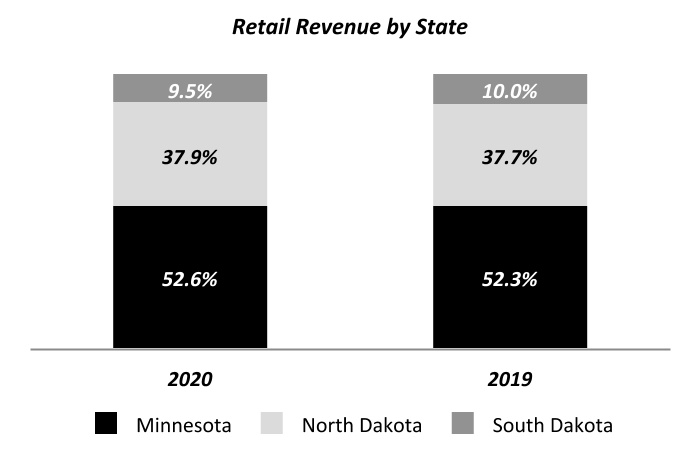

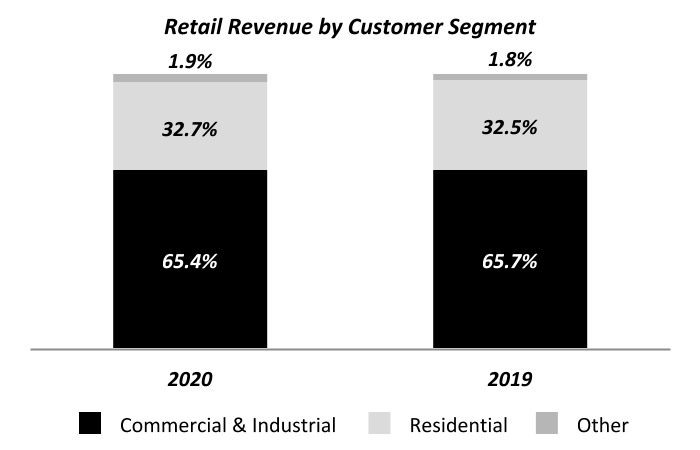

The following summarizescharts summarize our retail electric revenues by state and by customer segment for the years ended December 31, 20202023 and 2019:2022:

In addition to retail revenue, our Electric segment also earnsgenerates operating revenues from the transmission of electricity for others over the transmission assets we wholly or jointly own with other transmission service providers, and from the sale of electricity we generate and sell into the wholesale electricity market.

COMPETITIVE CONDITIONS

Retail electric sales are made to customers in assigned service territories. As a result, most retail customers do not have the ability to choose their electric supplier. Competition is present in some areas from municipally owned systems, rural electric cooperatives and, in certain respects, from on-site generators and co-generators. Electricity also competes with other forms of energy.

The degree of competition may vary from time to time depending on relative costs and supplies of other forms of energy and advances in technology; however, we believe OTP is well positioned to be successful in a competitive environment. A comparison of OTP's electric retail rates to the rates of other investor-owned utilities, cooperatives and municipals in the states OTP serves indicates OTP's rates are competitive.

Competition also arises from customers supplying their own power through distributed generation, which is the generation of electricity on-site or close to where it is needed in small facilities designed to meet local needs. Distributed energy resources are utility- or customer-owned resources on the distribution grid that can include combined heat and power, solar photovoltaic, wind, battery storage, thermal storage and demand-response technologies.

The degree of competition may vary from time to time depending on relative costs and supplies of other forms of energy and advances in technology. Irrespective of the competitive environment, we are focused on providing value to our customers and ensuring our retail rates remain among the lowest in the region and in the nation.

The following table presents our average retail rate per kilowatt-hour (kwh) by customer class and in total for the years ended December 31, 2023 and 2022:

| | | | | | | | | | | |

| Revenue per kwh | 2023 | | 2022 |

| | | |

| Residential | 10.82 | ¢ | | 10.99 | ¢ |

| Commercial & Industrial | 7.02 | ¢ | | 7.54 | ¢ |

| Total Retail | 7.90 | ¢ | | 8.41 | ¢ |

Wholesale electricity markets are competitive under the FERC'sFederal Energy Regulatory Commission (FERC) open access transmission tariffs, which require utilities to provide nondiscriminatory access to all wholesale users. In addition, the FERC has established a competitive process for the construction and operation of certain new electric transmission facilities whereby electricunder federal regulation. Certain states have laws which provide the incumbent transmission providers, includingowner the Midcontinent Independent System Operator, Inc. (MISO), of which OTP is a member, are required to remove from their tariffs a federal right of first refusal to construct and own new transmission facilities selected in a regional transmission plan for purposes of cost allocation.

Franchisesfacilities.

OTP has franchises to operate as an electric utility in substantially all of the incorporated municipalities it serves. Franchise rights generally require periodic renewal. No franchises are required to serve unincorporated communities in any of the three states that OTP serves.

GENERATION AND PURCHASED POWER

OTP primarily relies on company-owned generation, supplemented by power purchase power agreements, to supply the energy to meet our customer needs. Wholesale market purchases and sales of electricity are used as necessary to balance supply and demand. Our mix of owned generation and wholesale market energy purchases to meet customer demand as seasonal or other variations occur.are impacted by wholesale energy prices and the relative cost of each energy source.

As of December 31, 2020,2023, OTP’s wholly or jointly owned plants and facilities, as well as in place power purchase agreements, and their dependable kilowatt (kW) capacity was:were: | | | | | | | | |

| | Capacity /

Purchased Power

in kW |

| | |

| Owned Generation: | | |

| Baseload Plants | | |

Big Stone Plant(1) | | 256,000256,900 | |

Coyote Station(2) | | 149,000148,400 | |

Hoot Lake Plant | | 143,100 | |

Total Baseload Net PlantPlants | | 548,100405,300 | |

| Combustion Turbine and Small Diesel Units | | |

| Astoria Station | | 107,900249,700 | |

Hydroelectric FacilitiesAll Other | | 2,500102,800 | |

| Total Combustion Turbine and Small Diesel Units | | 352,500 | |

| Owned Wind Facilities (rated at nameplate) | | |

Merricourt Wind Energy Center (75 turbines) | | 150,000 | |

| Ashtabula III | | Luverne Wind Farm (33 turbines)62,400 | |

| Luverne | | 49,500 | |

Ashtabula Wind Center (32 turbines) | | 48,000 | |

Langdon Wind Center (27 turbines) | | 40,500 | |

| Total Owned Wind Facilities | | 288,000350,400 | |

TotalHoot Lake Solar | | 946,50049,900 | |

(1) Hydroelectric Facilities

| | 2,600Reflects OTP's 53.9% ownership percentage of jointly-owned facility | | |

(2) Total Owned Generation Capacity

| | 1,160,700Reflects OTP's 35.0% ownership percentage of jointly-owned facility | | |

In addition to the owned facilities described above, OTP had the following purchased power agreements in place on December 31, 2020:

| | | | | |

| Power Purchase Agreements: | | Purchased Power

in kW

| |

| Purchased Wind Power (rated at nameplate and greater than 2,000 kW) | |

Ashtabula Wind III | 62,400 | |

| Edgeley | | 21,000 | |

| Langdon | | 19,500 | |

| Total Purchased Wind | | 102,90040,500 | |

Purchase ofTotal Generating Capacity (in excess of 1 year and 500 kW) | |

Great River Energy (through May 2021)

| 50,0001,201,200 | |

| | |

(1) Reflects OTP's 53.9% ownership percentage of jointly owned facility. | | |

(2) Reflects OTP's 35.0% ownership percentage of jointly owned facility. | | |

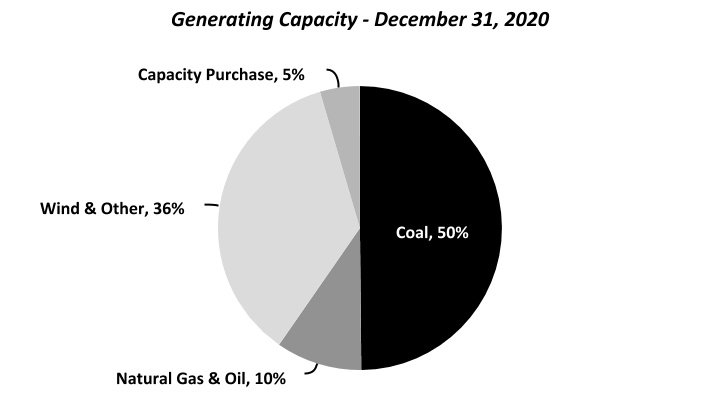

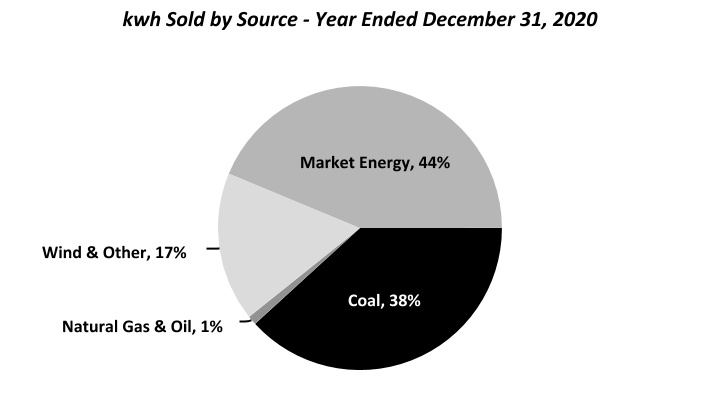

The following summarizescharts summarize the percentage of our generating capacity by source, including owned and jointly-ownedjointly owned facilities and through power and capacity purchase arrangements, as of December 31, 2020,2023 and the percentage of retail kilowatt-hours (kwh) sold by source during the year ended December 31, 2020:2022:

Under MISOMidcontinent Independent System Operator (MISO) requirements, OTP is required to haveprovide sufficient capacity through wholly or jointly-ownedjointly owned generating capacity or purchased power purchase agreements to meet its monthly weather-normalized forecast demand, plus a reserve obligation. OTP met its obligation forMISO operates under a seasonal resource adequacy construct in which generation resources are accredited and planning reserve margin requirements are implemented on a seasonal basis. Current planning reserve margin requirements range between 7.4% and 25.5%, depending on the 2019-2020 planning year and anticipates meeting this obligation prospectively.season.

The following charts summarize the percentage of retail kwh sold by source during the years ended December 31, 2023 and 2022:

Capacity Retirements and Additions

Hoot Lake Plant, our 142-meagwatt coal-fired power plant in Fergus Falls, Minnesota is approved for retirement in mid-2021.

As part of our investment plan to meet our future energy needs, we have the following projects at various stages of planning and construction or have been recently completed:undertaken, completed, or acquired:

MerricourtAshtabula III Wind Energy Center (Merricourt)Farm is a 150-megawatt62-megawatt (MW) wind farm located in southeasterneastern North Dakota. ConstructionThe facility was purchased for approximately $50 million in January 2023. Prior to the purchase of the wind farm commenced in 2019 andassets, we were purchasing the facility was in commercial operation in December 2020 atwind-generated electricity from the wind farm pursuant to a cost of approximately $260.0 million.

Astoria Station Natural Gas Plant (Astoria) is a 245-megawatt simple cycle natural gas combustion turbine generation facility near Astoria, South Dakota. Construction began in 2019 and we anticipate the facility will be substantially complete in the first quarter of 2021. We anticipate total project costs will be $152.5 million.power purchase agreement.

Hoot Lake Plant Solar (HLP Solar) is a 49-megawatt49-MW solar farm under development on landconstructed on and around our Hoot Lake Plant property in Fergus Falls, Minnesota. The project will include up to 150,000 solar panels at an anticipatedMinnesota, with a total cost of $60.0approximately $60 million. The facility was placed into commercial operation in August 2023.

Wind Energy Facility Upgrades consisting of the replacement and upgrade of hubs, gearboxes, blades, generators and other components of our Ashtabula, Ashtabula III, Langdon and Luverne wind facilities at a total cost of approximately $230 million. Once complete, we expect the increased energy production from these facilities will be equivalent to an additional 40-MW of generation. We anticipate subject to permitting and regulatory approval, the repowering of our Langdon facility will be completed in commercial operation no later2024 and the remaining facilities to be completed in 2025. Once complete, the energy production from each of these facilities is eligible for production tax credits (PTCs) over a ten-year period. We expect these projects will lower customer costs through a combination of fuel savings and the tax credit benefits afforded to our customers.

ENERGY TRANSITION

OTP is committed to transitioning to a lower-carbon and increasingly clean energy future, while maintaining affordable and reliable electricity to serve our customers. We have developed the following goals in furtherance of our efforts to support the energy transition:

Own or purchase energy generation that is 55% renewable by 2030.

Reduce carbon emissions from owned generation resources 50% by 2030 from 2005 levels.

Reduce carbon emissions from owned generation resources 97% by 2050 from 2005 levels.

We have based these goals on our December 2023 supplemental Integrated Resource Plan (IRP) filing in Minnesota. While modified from our previously published goals, they reflect current market conditions, including the impact of higher natural gas prices, and higher than originally forecasted dispatch levels of our co-owned, coal-fired power plants.

We have undertaken numerous initiatives to reduce our carbon footprint and mitigate greenhouse gas (GHG) emissions in the endprocess of 2023.generating electricity for our customers. Our recent initiatives include retiring the 140-MW coal-fired Hoot Lake Plant, adding the 150-MW Merricourt Wind Energy Center and the 49-MW Hoot Lake Solar facility to our resource mix and sponsoring energy conservation programs. We anticipate our Minnesota retail sales will be 80% carbon free by 2030, in compliance with Minnesota clean energy requirements.

From 2005 through 2023, we have reduced our carbon dioxide (CO2) emissions approximately 39% and increased the amount of renewable generation resources we own or purchase through power purchase agreements by approximately 420-MW. We currently own or contract energy generation that is 37% renewable.

The following chart depicts our energy resource mix, which is the electricity we used to serve our customers in 2005 and 2023, and the projected mix in 2030 and 2050. The amounts include energy generated from owned resources, procured through power purchase agreements and energy purchased in the wholesale market:

RESOURCE MATERIALS

Coal is the principal fuel burned at our jointly owned Big Stone and Coyote and Hoot LakeStation generating plants. Coyote Station, a mine-mouth facility, burns North Dakota lignite coal. Hoot Lake Plant and Big Stone Plant burnburns western subbituminous coal transported by rail. We source coal for our coal-fired power plants through requirements contracts which do not include minimum purchase requirements but do require all coal necessary for the operation of the respective plant to be purchased from the counterparty. Our coal supply contracts for our Hoot Lake Plant, Big Stone Plant and Coyote Station have expiration dates in 2023, 20222024 and 2040, respectively.

The supply agreement between the Coyote Station owners, including OTP, and the coal supplier includes provisions requiring the Coyote Station owners to purchase the membership interests and pay off or assume loan and lease obligations of the coal supplier, as well as complete mine closing and post-mining reclamation, in the event of certain early termination events and at the expiration of the coal supply agreement in 2040. See below and Note 1 to our consolidated financial statements included in this report on Form 10-K for additional information.

Coal is transported to our non-mine-mouth facilities, Big Stone Plant and Hoot Lake Plant by rail and is provided under a common carrier rate which includes a mileage-based fuel surcharge.

We purchase natural gas for use at our combustion turbine facilities based on anticipated short-term resource needs. We procure natural gas from multiple vendors at spot prices in a liquid market primarily under firm delivery contracts.

TRANSMISSION AND DISTRIBUTION

Our transmission and distribution assets deliver energy from energy generation sources to our customers. In addition, we earn revenue from the transmission of electricity over our wholly or jointly owned transmission assets for others under approved rate tariffs. As of December 31, 2020,2023, we were the wholesole or partialjoint owner of over 8,900approximately 14,000 miles of transmission and distribution lines.

Midcontinent Independent System Operator Inc. (MISO)

MISO is an independent, non-profit organization that operates the transmission facilities owned by other entities, including OTP, within its regional jurisdiction and administers energy and generation capacity markets. MISO has operational control of our transmission facilities above 100 kV.kilovolts (kV). MISO seeks to optimize the efficiency of the interconnected system, provide solutions to regional planning needs and minimize risk to reliability through its security coordination, long-term regional planning, market monitoring, scheduling and tariff administration functions.

Transmission Additions

In 2022, MISO approved several projects within the first tranche of its long-range transmission plan, which includes two new 345 kV transmission projects. OTP will have a varying level of ownership interest in these projects, which will be completed over several years and are at various stages of planning and development:

Jamestown-Ellendale includes the construction of a new 345 kV transmission line in southeastern North Dakota spanning approximately 95 miles from Jamestown, North Dakota to Ellendale, North Dakota. This project is in the initial stages of planning and development. This jointly owned project is expected to be completed in 2028 and our capital investment is estimated to be approximately $230 million.

Big Stone South-Alexandria-Big Oaks includes the construction of a new 345 kV transmission line in eastern South Dakota and western Minnesota and the addition of a second circuit to an existing 345 kV line in central Minnesota. The new transmission line will span approximately 100 miles between Big Stone, South Dakota and Alexandria, Minnesota. A second circuit will be added to the existing transmission line spanning from Alexandria, Minnesota to Big Oaks, Minnesota. This project is in the initial stages of planning and development. This jointly owned project is expected to be completed in 2031 and our capital investment is estimated to be approximately $190 million.

SEASONALITY

Electricity demand is affected by seasonal weather differences, with peak demand occurring in the summer and winter months. As a result, our Electric segment operating results mayregularly fluctuate on a seasonal basis. In addition, fluctuations in electricity demand within the same season but

between years can impact our operating results. We monitor the level of heating and cooling degree days in a period to assess the impact of weather-related effects on our operating results between periods.

PUBLIC UTILITY REGULATION

OTP is subject to regulation of rates and other matters in each of the three states in which it operates and by the federal government for, certainamong other matters, the interstate operations.transmission of electricity. OTP operates under approved retail electric tariff rates in all three states it serves. Tariff rates are designed to recover plant investments, a return on those investments, and operating costs. In addition to determining rate tariffs, state regulatory commissions also authorize ROE,return on equity (ROE), capital structure, and depreciation rates of our plant investments. Decisions by our regulators can significantly impact our operating results, financial position, and cash flows.

Below is a summary of the regulatory agencies with jurisdiction of electric rates over OTP along with the percentage of electric revenue for the year ended December 31, 2020 covered by each regulatory agency:

| | | | | | | | | | | | | | |

| Regulatory | | | % of | |

| Agency | | | Revenue | Areas of Regulation |

| | | | |

Minnesota Public Utilities Commission

(MPUC)

| | | 47% | Retail rates, issuance of securities, depreciation rates, capital structure, public utility services, construction of major facilities, establishment of exclusive assigned service areas, contracts with subsidiaries and other affiliated interests and other matters. Selection or designation of sites for new generating plants (50,000 kW or more) and routes for transmission lines (100 kV or more). Review and approval of fifteen-year Integrated Resource Plan. |

North Dakota Public Service Commission

(NDPSC) | | | 34% | Retail rates, certain issuances of securities, construction of major utility facilities and other matters. Approval of site and routes for new electric generating facilities (500(>500 kW or more for wind generating facilities; 50,000>50,000 kW for non-wind generating facilities) and high voltage transmission lines (115 kV or more)(>115 kV). Review and approval of ten-year facility plan.fifteen-year Integrated Resource Plan. |

South Dakota Public Utilities Commission

(SDPUC) | | | 9% | Retail rates, public utility services, construction of major facilities, establishment of assigned service areas and other matters. Approval of sites and routes for new electric generating facilities (100,000 kW or more) and most transmission lines (115 kV or more). |

Federal Energy Regulatory Commission

(FERC) | | | 10% | Wholesale electricity sales, transmission and sale of electric energy in interstate commerce, interconnection of facilities, hyrdoelectrichydroelectric licensing and accounting policies and practices. Compliance with NERCNorth American Electric Reliability Corporation (NERC) reliability standards, including standards on cybersecurity and protection of critical infrastructure. |

In addition to base rates, which are established through periodic rate case proceedings within each state jurisdiction, there are other mechanisms for recovery of plantour capital investments including a return on investment, and operating expenses.expenses between rate cases. The following is a summary oftable summarizes these recovery mechanisms:

| | | | | | | | | | | | | | |

| Recovery Mechanism | | Jurisdiction(s) | | Additional Information |

| | | | |

| Fuel Clause Adjustment (FCA) | | MN, ND, SD | | Provides for periodic billing adjustments for changes in prudently incurred costs of fuel and purchased power. In North and South Dakota, fuel and purchased power costs are generally adjusted on a monthly basis with over or under collections from the previous month applied to the next monthly billing.basis. In Minnesota, fuel and purchased power costs are estimated on an annual basis and the accumulated difference between actual and estimated cost per kwh areis refunded or recovered, subject to regulatory approval, in subsequent periods. |

| Transmission Cost Recovery Rider (TCR) | | MN, ND, SD | | Provides for the recovery of costs outside of a general rate case for investments in new or modified electric transmission or distribution assets. |

Environmental Cost Recovery Rider (ECR) | | MN, ND, SD | | Provides for recovery of costs outside of a general rate case for investments inassets and certain environmental improvement projects.MISO transmission service and related costs. |

| Renewable Resource Rider (RRR) | | MN, ND | | Provides for the recovery of costs outside of a general rate case for investments in certain new renewable energy projects. |

| Energy Conservation and Optimization Rider (ECO) | | MN | | Under Minnesota law, OTP is required to save 1.75% of its gross retail energy revenues through the energy conservation and optimization program. Recovery of these costs outside of a general rate case occurs through the ECO rider. |

| Electric Utility Infrastructure Costs Rider (EUIC) | | MN | | Provides for the recovery of costs for investments made to replace or modify existing infrastructure if the replacement or modification conserves energy or uses energy more efficiently. |

| Metering and Distribution Technology Cost Recovery Rider (MDT) | | ND | | Provides for the recovery of costs for advanced metering infrastructure, outage management systems and demand response projects. |

| Generation Cost Recovery Rider (GCR) | | ND | | Provides for the recovery of costs outside of a general rate case for investments in new generation facilities. |

| Energy Efficiency Plan (EEP) | | SD | | Provides for the recovery of costs from energy efficiency investments. |

| Phase-In Rider (PIR) | | SD | | Provides for the recovery of costs outside of a general rate case for investments in new generation facilities. |

Conservation Improvement Program (CIP) | | MN | | Under Minnesota law, OTP is required to invest at least 1.5% of its gross operating revenues on energy conservation improvements. Recovery of these costs outside of a general rate case occurs through the CIP. |

Energy Efficiency Plan (EEP) | | SD | | Provides for the recovery of costs from energy efficiency investments.facilities and advanced grid infrastructure. |

Renewable Energy Standard

Minnesota has a renewable energy standard requiring utilities to generate or procure sufficient renewable generation such that the following percentages of total retail electric sales to Minnesota customers come from qualifying renewable sources: 17% by 2016; 20% by 2020 and 25% by 2025. We met the current renewable sources requirements with a combination of owned renewable generation and purchases from renewable generation sources. Minnesota law also requires 1.5% of total Minnesota electric sales by public utilities to be supplied by solar energy by 2020. For a public utility with between 50,000 and 200,000 retail electric customers, such as OTP, at least 10% of the 1.5% requirement must be met by solar energy generated by or procured from solar photovoltaic devices with a nameplate capacity of 40 kWs or less. OTP has purchased sufficient solar renewable energy credits (SRECs) to meet 100% of its 2020 obligation and approximately 70% of its 2021 obligation.

Under certain circumstances and after consideration of costs and reliability issues, the MPUC may modify or delay implementation of the standards. We are evaluating potential options for maintaining compliance and meeting the solar energy standard beyond 2021.

Integrated Resource Plan (IRP)Planning

Under Minnesota law, utilities are required to submit for approval by the MPUCMinnesota Public Utilities Commission (MPUC) a 15-year advance IRP.Integrated Resource Plan (IRP). An IRP is a set of resource options a utility could use to meet the service needs of its customers over the forecast period, including an explanation of the utility’s supply and demand circumstances, and the extent to which each resource option would be used to meet those service needs. The MPUC’s findings of fact and conclusions regarding IRPs are considered to be prima facie evidence, subject to rebuttal, in future rate reviews and other proceedings. Typically, IRPs are submitted every two years.

On April 26, 2017In 2021, the MPUC approved OTP’s 2017-2031North Dakota Legislative Assembly enacted a provision requiring investor-owned electric utilities to submit an IRP filing with modificationsto the North Dakota Public Service Commission (NDPSC) and setting requirementsgranted the NDPSC the authority to adopt rules and regulations for the next IRP.preparation and submission of IRPs. The approvedNDPSC's rules and regulations were finalized and became effective on January 1, 2023. Under the finalized regulation, utilities are required to submit a 15-year advance IRP with modifications included the following items:every three years.

•The addition of 200 MW of wind resources in the 2018 to 2020 timeframe.

•The addition of 30 MW of solar resources by 2020 to comply with Minnesota's Solar Energy Standard.

•The addition of up to 250 MW of peaking capacity in 2021.

•Average annual energy savings of 46.8 gigawatt-hours (1.6% of retail sales).

•The addition of 100 MW to 200 MW of wind resources in the 2022 to 2023 timeframe.

The MPUC has granted us an extension for filing our next IRP to September 1, 2021. The extension provides additional time to assess the potential impact of two key Environmental Protection Agency (EPA) regulations: the federal Regional Haze Rule (RHR) and the Affordable Clean Energy (ACE) Rule. In connection with the extension, OTP made a supplemental filing on December 31, 2020 summarizing the results of scenario modeling evaluating RHR compliance cost options and a Coyote Station 2028 retirement scenario. The filing indicated, when modeled with externalities, that capital investments in additional environmental controls at Coyote Station does not result in the lowest-cost mix of resources for our customers. This IRP supplemental filing includes only a subset of our resource planning analysis and it is not conclusive. In addition, we cannot conclude how RHR will impact Coyote Station as key milestones remain in developing the state implementation plan in North Dakota. Finally, OTP is one of four partners in Coyote Station and cannot make a unilateral decision on its future. We expect to have more definitive information about the most cost-effective resource mix to meet customer needs when the next IRP is filed on September 1, 2021.

Capital Structure Petition

Minnesota law requires an annual filing of a capital structure petition with the MPUC. In this filing the MPUC reviews and approves OTP's capital structure. Once approved, OTP may issue securities without further petition or approval, provided the issuance is consistent with the purposes and amounts set forth in the approved petition. The MPUC approved OTP’s most recentcurrent capital structure petitionapproved by the MPUC on July 15, 2020, allowingAugust 29, 2023, allows for an equity-to-total-capitalization ratio between 47.5%48.3% and 58.1%59.1%, with total capitalization not to exceed $1.70 billion until$1.958 billion.

Renewable Energy Standard

Minnesota has a renewable energy standard requiring utilities to generate or procure sufficient renewable generation such that the following percentages of total retail electric sales to Minnesota customers come from qualifying renewable sources: 25% by 2025 and 55% by 2035. Qualifying renewable sources are classified as wind, hydropower, hydrogen, and certain biomass generation. We met the current renewable sources requirements with a combination of owned renewable generation and purchases from renewable generation sources. Minnesota law also requires 1.5% of total Minnesota retail electric sales by public utilities to be supplied by solar energy. For a public utility with between 50,000 and 200,000 retail electric customers, such as OTP, at least 10% of the 1.5% requirement must be met by solar energy generated by or procured from solar photovoltaic devices with a nameplate capacity of 40 kW or less. We met the current solar requirement with a combination of owned solar generation and solar renewable energy certificate (REC) purchases. We plan to comply with the requirements of this standard in the future through a combination of our existing and projected renewable generation fleet and the purchase of RECs.

Minnesota Clean Energy Bill

In February 2023, Minnesota enacted the Clean Energy Bill, which requires electric utilities to generate or procure sufficient electricity from carbon-free resources, to provide retail customers in Minnesota with at least the following percentages of carbon-free electric energy: 80% by 2030, 90% by 2035, and 100% by 2040. Carbon-free resources include wind, solar, hydropower, and nuclear generation. To provide flexibility, the law allows electric utilities to use RECs to offset carbon emissions and for the MPUC issuesto consider whether a new capital structure order for 2021.regulated utility's requirement to meet established standards should be delayed due to affordability or reliability impacts. We expect to meet these requirements based on our existing and projected renewable generation fleet and the purchase of RECs.

ENVIRONMENTAL REGULATION

OTP is subject to stringent federal and state environmental standards and regulations regarding, among other things, air, water and solid waste pollution. OTP's facilities have been designed, constructed and, as necessary, updated to operate in compliance with applicable environmental regulations. However, new or amended laws and regulations or changes in interpretations of current laws and regulations may require additional pollution control equipment or emission reduction measures, and there can be no assurance that our facilities will remain economic to operate. Prudent expenditures incurred to comply with environmental regulations are eligible to be recovered in rates grantedauthorized by regulators in jurisdictions in which we operate; however, there can be no assurance that future costs will be grantedauthorized for recovery. Alternatively, additional pollution control equipment or other emission reduction measures may prove to be uneconomic, withpotentially leading to the potentialexiting of a facility earlier than originally planned. As it relates to leadour jointly owned facilities, we may determine it is necessary to antransfer, sell or otherwise divest of our ownership, or the ownership group may determine the early closure or repurposing of a facility.facility is necessary.

Financial Impacts

For the five-year period ended December 31, 2020,2023, OTP invested approximately $13.5$6.6 million including $0.4 million in 2020, in environmental control facilities. Our 2021 and 2022 construction budgets include approximatelyfacilities, including $1.4 million and $1.2in 2023. Our construction budget for the next five years includes approximately $7.5 million for such expenditures.of capital investments in environmental control equipment. The timing and amount of our expenditures may change as the regulatory environment changes.

Among current regulatory requirements,Emerging Regulation

The Environmental Protection Agency (EPA) adopted the Regional Haze Rule (RHR) could have the most significant impact on our operating results, financial condition and cash flows.

The EPA adopted the RHR in 1999 as an effort to improve visibility in national parks and wilderness areas. The RHR requires states, in coordination with the EPA and other governmental agencies, to develop and implement state implementation plans to(SIPs) that work towards achieving natural visibility conditions by the year 2064.2064; to set goals to ensure reasonable progress is being made; and periodically evaluate whether those goals and progress are on track or whether additional emission reductions are appropriate. The second RHR implementation period covers the years 2018-2028, with state implementation plans to be submitted to the EPA by July 31, 2021. States are required to assess reasonable progress with the RHR and determine what additional emission reductions are appropriate, if any. 2018-2028.

Coyote Station OTP's co-owned coal-fired power plant in North Dakota is subject to assessment in the second implementation period under the North Dakota state implementation plan.SIP for the RHR. The North Dakota Department of Environmental Quality (NDDEQ) submitted its proposed RHR SIP to the EPA for approval in August 2022. In its plan, the NDDEQ concluded it is not reasonable to require additional emission controls during this planning period. The EPA submitted comments during the development of the SIP requesting NDDEQ to reassess its determination for Coyote Station. See Note 13 to our consolidated financial statements included in the report on Form 10-K for additional information.

In April 2023, the EPA released a proposal to tighten aspects of the Mercury and Air Toxics Standards, including the reduction of emissions limits for filterable particulate matter, and requiring the use of continuous emissions monitoring systems to demonstrate compliance. Until the EPA takes final action on this rulemaking, we are unable to predict the ultimate impact, however, there could be a cost of compliance which could have a material impact on our operating results, financial condition and liquidity.

Climate Change and Greenhouse Gas Regulation

Present and future federal, state, regional and international environmental regulations to address globalGlobal climate change and reduce greenhouse gas (GHG) emissions may havepresents a significant impact on our utility business.energy and environmental policy challenge. Combustion of fossil fuels for the generation of electricity is a considerable source of CO2 emissions, which is the primary GHG emitted by our utility operations. The federal government and many states are pursuing climate policies to regulate GHG emissions as part of a broad-based effort to limit global warming.

RegulatoryIn February 2021, the U.S. rejoined the United Nations Framework Convention on Climate Change (the Paris Agreement), which is a legally binding international treaty on climate change adopted by over 190 countries. The goal of the Paris Agreement is to limit the global temperature increase to well below 2° Celsius compared to pre-industrial levels and to pursue efforts to limit the temperature increase to 1.5° Celsius. The Biden Administration set goals of reducing GHG emissions by 50% to 52% from 2005 levels in 2030 and reaching 100% carbon pollution-free electricity by 2035 as part of the U.S. plan to achieve the goals under the Paris Agreement.

In February 2023, Minnesota enacted the Clean Energy Bill, which requires electric utilities to generate or procure sufficient electricity from carbon-free resources to provide retail customers in Minnesota with at least the following percentages of carbon-free electric energy: 80% by 2030, 90% by 2035, and 100% by 2040.

The implementation of climate change programs, such as the Paris Agreement, the Minnesota Clean Energy Bill, and other federal or state regulations targeting GHG emissions may have a significant impact on our utility business. Specific regulatory measures to address climate change continue to evolve.

In May 2023, the EPA proposed new regulations under Section 111 of the Clean Air Act to regulate GHG emissions from existing and new fossil fuel-based electric generating units (EGU). The proposal provides requirements for different types of fossil fuel-based EGUs with various compliance dates.

•For existing coal-fired steam generating units that were in operation before January 2021,8, 2014 and that plan to operate past December 31, 2039, the EPA's Affordable Clean Energy Rule (ACE Rule) was vacatedproposal would (subject to certain exceptions) set emissions standards that reflect the use of carbon capture and sequestration (CCS) with 90% capture of CO2 emissions beginning in 2030.

•For existing coal-fired steam generating units that are scheduled to be retired between January 1, 2032 and December 31, 2039, the proposed rule would, in general, set emissions standards that reflect the use of co-firing 40% natural gas with coal beginning in 2030.

•For existing coal-fired steam generating units that will either (a) retire by January 1, 2032, or (b) retire between 2032 and December 21, 2034 and will operate at a 20% annual capacity factor limit in the U.S. Courtmeantime, the proposed rule would simply require routine maintenance and no increase in emission rate.

The proposal also includes emission standards for existing large (greater than 300 mega-watt), frequently used (those that operate at a capacity factor over 50%) natural gas combustion turbines, including which emission standard would reflect the use of Appeals forCCS by 2035 or co-firing with low-GHG hydrogen at incremental portions in 2032 (30% of volume) and 2038 (96% of volume). Under the District of Columbia Circuit and remandedproposed rule, each state must submit a plan to the EPA for further consideration. Future federal regulatory measures, including in response to implement standards that are at least as stringent as the vacatedEPA’s emission guidelines, unless states demonstrate that due to remaining useful life and other factors, a facility cannot reasonably achieve the standards. The EPA is proposing to require states to submit their plans within 24 months of the effective date of the final regulation. This proposed rule ACE Rule, will be impacted byhas the Biden administration's prioritiespotential to impact the emissions controls needed at OTP’s coal-fired power plants, which could have an impact on our operating results, financial condition and objectives. While the eventual outcome of GHG regulation is unknown, we are taking steps to reduce our carbon footprint and mitigate CO2 emission levels in the process of generating electricity for our customers. Our initiatives include increasing the efficiency of our plants, adding renewable energy to our resource mix, and sponsoring energy conservation programs.liquidity.

While the future financial impact of any current, proposed, or pending litigation or regulation of GHG or other emissions is unknown at this time, any capital or operating costs incurred for additional pollution control equipment or emission reduction measures could materially adversely impact our future operating results, financial position, and cash flowsliquidity unless such costs could be recovered through related rates and/or future market prices for energy.

| | | | | |

| MANUFACTURING | Contribution to Operating Revenues: 30% (2023), 27% (2020)(2022), 30% (2019), 29% (2018)28% (2021) |

Manufacturing consists of businesses engaged in the following activities: contract machining, metal parts stamping, fabrication and painting, and production of plastic thermoformed horticultural containers, life science and industrial packaging, and material handling components and extruded raw material stock. The following is a brief description of each of these businesses:

BTD Manufacturing, Inc. (BTD), with headquarters locatedfacilities in Detroit Lakes and Lakeville, Minnesota, Washington, Illinois and Dawsonville, Georgia, provides metal fabrication services for custom machine parts and metal components through metal stamping, tool and die, machining, tube bending, welding and assembly in its facilities in Detroit Lakes and Lakeville, Minnesota, Washington, Illinois and Dawsonville, Georgia.assembly.

T.O. Plastics, Inc. (T.O. Plastics), with facilities in Otsego and Clearwater, Minnesota, manufactures extruded and thermoformed plasticplastics products, including custom parts for customers in several industries and its own line of horticulture containers. Examples ofcontainers and custom packaging products produced include clamshell packing, blister packs, returnable palletsfor the medical and handling trays for shipping and storing odd-shaped or difficult-to-handle parts.industrial product markets.

CUSTOMERS

Our metal fabrication business primarily serves Midwestern and Southeastern U.S. manufacturers in the recreational vehicle, agricultural, oil and gas, lawn and garden, agricultural, construction, and industrial and energy equipment end markets. Our plastic products business serves primarily U.S. customers in the

horticulture, medical and life sciences, industrial, recreational and electronics industries. The principal method of production distribution is by direct shipment to our customers through direct customer pick-up or common carrier ground transportation.

No single customer or product of our manufacturingManufacturing segment businesses accounted for 10% or more of our consolidated operating revenuerevenues in 2020.2023. However, the top threetwo customers combined to account for 46%30% of our 2020 Manufacturing segment operating revenue.revenues for the year ended December 31, 2023 and 40% for the year ended December 31, 2022.

COMPETITIVE CONDITIONS

The various marketsWe compete in which we compete are characterized by intensea highly fragmented market with competition from both foreigndomestic and domestic manufacturers. Theseinternational entities. Our competitors vary in size, ranging from small companies focused on certain end markets or geographical area, to large companies with broad manufacturing capabilities and geographical reach. Competition can be geographically regionalized as customers procure products locally to manage cost and minimize logistical complexities. Certain competitors may have many established manufacturers with broader product lines, more manufacturing capacity, and greater distribution capabilities greater capital resources, excess capacity, labor advantages and larger marketing, research and development staffs and facilities than our own.we do.

We believe the principal competitive factors in our Manufacturing segment are product performance, quality, price, technical innovation, cost effectiveness, customer service and breadth of product line. We intend to continue to compete based on high-performancehigh quality products, innovative production technologies, cost-effective manufacturing techniques, close customer relations and support, and increasing product offerings.

RESOURCE MATERIALS

We use raw materials in the products we manufacture, including, among others, steel, aluminum, and polystyrene and other plastics resins. Managing price volatility and ensuring raw material availability are important aspects of our business. We attempt to pass increases in the costs of these raw materials onthrough to our customers. Increases in the costs of raw materials that cannot be passed on to customers could have a negative effect on profit margins. Additionally, a certain amount of residual material (scrap) is a by-product of the manufacturing and production processes. Declines in commodity prices for these scrap materials due to weakened demand or excess supply can negatively impact the profitability of our Manufacturing segment as it reduces their ability to mitigate the costcosts associated with excess material.

ENVIRONMENTAL REGULATION

Our manufacturing businesses are subject to environmental, health and safety laws and regulations, including those governing discharges to air and water, the management and disposal of hazardous substances, the cleanup of contaminated sites and health and safety matters.

| | | | | |

| PLASTICS | Contribution to Operating Revenues: 23% (2020)31% (2023), 20% (2019)35% (2022), 22% (2018)32% (2021) |

Plastics consists of businesses producing PVC pipe at plants in North Dakota and Arizona. The following is a brief description of these businesses:

Northern Pipe Products, Inc. (Northern Pipe), located in Fargo, North Dakota, manufactures and sells PVC pipe for municipal water, rural water, wastewater, storm drainage systems and other uses in the northern, midwestern, south-central and western regions of the United States as well as central and western Canada.

Vinyltech Corporation (Vinyltech), located in Phoenix, Arizona, manufactures and sells PVC pipe for municipal water, wastewater, water reclamation systems and other uses in the western, northwest and south-central regions of the United States.

PVC pipe is manufactured through aan extrusion process, known as extrusion. During this process,during which PVC compound (a dry powder-like substance) is introduced into an extrusion machine, where it is heated to a molten state and then forced through a sizing apparatus to produce the pipe. The newly extruded pipe is pulled through a series of water-cooling tanks, marked to identify the type of pipe and cut to finished lengths. Together our Plastic segment businesses have the current capacity to produce approximately 300 million pounds of PVC pipe annually.

CUSTOMERS

PVC pipe products are marketed through a combination of independent sales representatives, company salespersons and customer service representatives. Customers for our PVC pipe products consist primarily of wholesalers and distributors, and the principal method for distribution of our products is by common carrier ground transportation. No single customer of the PVC pipe companies accounted for 10% or more of our consolidated operating revenues in 2020.2023. However, two customers, both of which are distributors of PVC pipe, combined to account for 45%36% of our 2020 Plastics segment operating revenue.revenues for the year ended December 31, 2023 and 46% for the year ended December 31, 2022.

COMPETITIVE CONDITIONS

The plastic pipe industry is fragmented and competitive due to the number of producers, the small number of raw material suppliers and the fungible nature of the product. Due to shipping costs, competition is usually regional instead of national in scope. The principal factors of competition are price, customer service and product performance. We compete not only against other plastic pipe manufacturers, but also ductile iron, high-density polyethylene, steel and concrete pipe producers. Pricing pressure will continue to affect our operating margins in the future.

We will continue to compete based on our high-quality products, cost-effective production techniques and close customer relations and support.support, including our responsiveness and reliability.

RESOURCE MATERIALS

PVC resins are acquired in bulk and shipped to our facilities by rail. There are four vendors from which we can source our PVC resin requirements. Two vendors provided over 99%In 2023 we sourced all of totalour PVC resin from three vendors. Our contractual arrangements to acquire resin generally include estimated annual order quantities with no required minimum purchases, in 2020.and include variable pricing based on market prices for resin. The supply of PVC resin may also be limited primarily due to manufacturing capacity and the limited availability of raw material components. Most U.S. resin production plants are located in the Gulf Coast region. These plants are subject to the risk of damage and production shutdowns because of exposure to hurricanes or other extreme weather events that occur in this part of the United States. The loss of a key vendor, or any interruption or delay in the supply of PVC resin could disrupt the ability of theour Plastics segment businesses to manufacture products, cause customers to cancel orders or result in increased expenses for obtaining PVC resin from alternative sources, if such sources were available. We believe we have good relationships with our key raw material vendors.

Due to the commodity nature of PVC resin and PVC pipe and the dynamic supply and demand factors worldwide, historically the markets for both PVC resin and PVC pipe have been very cyclical with significant fluctuations in prices and gross margins.

In addition to PVC resin, we use certain other materials, such as stabilizers, gaskets and lumber, in the process of manufacturing and shipping our PVC pipe products. We generally source these materials from a limited number of suppliers, and supply chain constraints or disruptions related to these materials could disrupt our ability to manufacture or ship products and could result in increased costs.

Demand for our PVC pipe products can be impacted by seasonal weather differences, with generally lower sales volumes realized in the first quarter of the year when cold temperatures and frozen ground across the northern portion of our footprint can delay or prevent construction activity and consequently delay or prevent customer orders of PVC pipe.

ENVIRONMENTAL REGULATION

Our plastics businesses are subject to environmental, health and safety laws and regulations, including those governing discharges to air and water, the management and disposal of hazardous substances, the cleanup of contaminated sites and health and safety matters.

RISK FACTORS AND CAUTIONARY STATEMENTS

Our businesses are subject to various risks and uncertainties. Any of the risks described below or elsewhere in this report on Form 10-K or in our other SEC filings could materially adversely affect our business, operating results, financial condition operating results and cash flows.liquidity. Additional risks and uncertainties we are not presently aware of or that we currently consider immaterial may also affect our business, operating results, financial condition operating results and cash flows.

Oversight of Risk and Related Processes

A key accountability of the Board of Directors is the oversight of material risk. Management and the Board of Directors have responsibility for overseeing the identification and mitigation of top risks. Management identifies and analyzes risks to determine the impact and other attributes such as timing, likelihood and management control. Identification and analysis occur formally through a top risk assessment conducted by senior management, the financial disclosure process, and internal auditing and compliance with financial and operational controls. Management also identifies and analyzes risk through development of goals and key performance indicators, which include risk identification to determine barriers to implementing our strategy. We promote a culture of compliance, including tone at the top. The process for risk mitigation includes adherence to our code of conduct and compliance policies, operation of formal risk management structures and overall business management to mitigate the risks inherent in the implementation of strategy. We manage and further mitigate risks through formal risk management structures, including a management executive risk committee and services such as internal audit/business risk management and legal. Management communicates regularly with our Board of Directors and key stakeholders regarding risk. Senior management presents and communicates a periodic risk assessment to our Board of Directors which provides information on the risks management believes are material, including the earnings impact, timing, likelihood and management control. The Board of Directors approaches oversight, management and mitigation of risk as an integral and continuous part of its governance of Otter Tail Corporation. The Board of Directors regularly reviews management’s top risk assessment and analyzes areas of existing and future risks and opportunities. Finally, the Board of Directors conducts an annual strategy session where our future plans and initiatives are reviewed.liquidity.

OPERATIONAL RISKS

The economic effects of the COVID-19 pandemic and measures taken to arrest its spread, as well as any emergency measures we take in response, could adversely impact our business, including our operating results, financial condition and liquidity.

The outbreak and global spread of COVID-19, which has been declared a pandemic by the World Health Organization, has adversely impacted economic activity and conditions worldwide and is currently impacting our business operations. The extent to which COVID-19 will continue to impact our business is highly uncertain and will depend on future developments, including the efficacy and availability of vaccines, the spread of COVID-19 variants and the extent of federal, state and local government responses affecting the economy. In particular, the COVID-19 pandemic could, among other things:

•reduce customer demand in our Manufacturing segment, where we experienced a significant but temporary decline in orders in 2020 as many of our customers temporarily closed their plants, which led to actions to reduce our operations, including furloughing of employees and eliminating positions;

•reduce customer demand in our Electric segment, including demand from commercial and industrial customers;

•reduce customer demand in our Plastics segment;

•result in lower PVC pipe sales due to potential delays or cancellation of public water and wastewater infrastructure projects caused by funding shortfalls;

•lead to disruptions of our workforce;

•force us to temporarily close certain plants or construction sites if precautions to prevent the spread of the virus at those locations are not effective;

•increase our bad debt expenses, particularly in our Electric segment;

•increase our future pension benefit cost and funding requirements;

•increase health insurance premiums;

•disrupt the supply chains, delivery systems or construction workforce related to our Electric segment maintenance requirements and capital expenditure plans, resulting in further delays and increased costs;

•disrupt global financial markets, reducing our ability to access capital necessary to finance such expenditures, and which could in the future negatively affect our liquidity; and

•result in a recession or market correction that could materially affect our business and the value of our common stock.

We continue to monitor developments involving our workforce, customers, construction contractors, suppliers and vendors and take steps to mitigate against additional impacts, but given the unprecedented and evolving nature of these circumstances, we cannot predict the full extent of the impact that COVID-19 will have on our operating results, financial condition and liquidity.

Our strategy includes large capital investments, which are subject to risks.