UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

xAnnual Report Pursuant to Section 13 OR 15(d) of the Securities Exchange Act of 1934

| |

| x | Annual Report Pursuant to Section 13 OR 15(d) of the Securities Exchange Act of 1934 |

For the Fiscal Year Ended December 31, 20102013

oTransition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

| |

| o | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to .

Commission File Number:

000-51515

CORE-MARK HOLDING COMPANY, INC.

(Exact name of registrant as specified in its charter)

|

| |

| Delaware | 20-1489747 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| | |

395 Oyster Point Boulevard, Suite 415 South San Francisco, California 94080 | (650) 589-9445 |

| (Address of Principal Executive Offices, including Zip Code) | (Registrant's Telephone Number, including Area Code) |

Securities Registered Pursuant to Section 12(b) of the Act:

|

| |

Title of each class | Name of each exchange on which registered |

| Common Stock, par value $0.01 per share | NASDAQ Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ox No xo

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ox No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. |

| |

Large accelerated filer ox | Accelerated filer xo |

Non-accelerated filer o | Smaller reporting company o |

(Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of June 30, 201028, 2013, the last business day of the registrant's most recently completed second fiscal quarter: $289,526,950.$711,883,006

As of February 28, 201114, 2014, the Registrantregistrant had 11,282,05611,532,968 shares of its common stock issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

See PartsThe information called for by Part III and IV. Registrant's Proxy Statement for the 2011 Annual Meeting of Stockholders isthis Form 10-K will be included in an amendment to this Form 10-K or incorporated by reference to Part III in this Form 10-K.the registrant's 2014 definitive proxy statement to be filed pursuant to Regulation 14A.

FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2013

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Except for historical information, the statements madeStatements in this Annual Report on Form 10-K that are not statements of historical fact are forward-looking statements made pursuant to the safe-harbor provisions of the Private Securities Litigation ReformExchange Act of 1995. Forward-looking statements are based on certain assumptions or estimates, discuss future expectations, describe future plans1934 and strategies, contain projectionsthe Securities Act of results of operations or of financial conditions or state other forward-looking information. Our ability to predict results or the actual effect of future plans or strategies is inherently uncertain.1933.

Although we believe that the expectations reflected in such forward-looking statements are based on reasonable assumptions, actual results and performance could differ materially from those set forth in the forward-looking statements. Forward-looking statements in some cases can be identified by the use of words such as “may,” “will,” “should,” “potential,” “intend,” “expect,” “seek,” “anticipate,” “estimate,” “believe,” “could,” “would,” “project,” “predict,” “continue,” “plan,” “propose” or other similar words or expressions. These forward-lookingForward-looking statements are made only as of the date of this Form 10-K and are based on theour current intent, beliefs, plans and expectations of our management and are subject to certainexpectations. They involve risks and uncertainties that could cause actual results to differ materially from historical results or those discusseddescribed in or implied by such forward-looking statements.

FactorsA detailed discussion of risks and uncertainties that mightcould cause or contributeactual results and events to differ materially from such differences include, but are not limited to, our dependence on the convenience retail industry for our revenues; uncertain economic conditions; competition; price increases; our dependence on relatively few suppliers; the low-margin nature of cigarette and consumable goods distribution; certain distribution centers' dependence on a few relatively large customers; competitionforward-looking statements is included in the labor market; product liability claims and manufacturer recalls of products; fuel price increases; our dependence on our senior management; our ability to successfully integrate acquired businesses; currency exchange rate fluctuations; our ability to borrow additional capital; governmental regulations and changes thereto, including the Family Smoking Prevention and Tobacco Control Act which was signed into law in June 2009 and granted the U.S. Food & Drug Administration the authority to regulate the production and marketing of tobacco products in the U.S.; earthquake and natural disaster damage; failure or disruptions to our information systems; a greater decline than anticipated in cigarette sales volume; our ability to implement marketing strategies; our reliance on manufacturer discount and incentive programs; tobacco and other product liability claims; and competition from sales of deep-discount cigarette brands and illicit and other low priced sales of cigarettes. Refer to Part I, Item 1A, “Risk Factors” of this Form 10-K. Except as providedrequired by law, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

SEC Regulation G - Non-GAAP Information

The financial statements in this Annual Report are prepared in accordance with generally accepted accounting principles in the United States of America (“GAAP”). Core-Mark Holding Company, Inc. (“Core-Mark”) uses certain non-GAAP financial measures including remaining gross profit, remaining gross profit margin, Adjusted EBITDA and net sales, less excise taxes. We believe these non-GAAP financial measures provide meaningful supplemental information for investors regarding the performance of our business and facilitate a meaningful period to period evaluation. Management uses these non-GAAP financial measures in order to have comparable financial results to analyze changes in Core-Mark’s underlying business. These non-GAAP measures should be considered as a supplement to, and not as a substitute for, or superior to, financial measures calculated in accordance with GAAP.

PART I

ITEM 1. BUSINESS

Unless the context indicates otherwise, all references in this Annual Report on Form 10-K to Core-Mark, the Company, we, us,“Core-Mark”, “the Company”, “we”, “us”, or our“our” refer to Core-Mark Holding Company, Inc. and its subsidiaries.

Company Overview

Core-Mark is one of the largest marketers of fresh and broad-line supply solutions to the convenience retail industry in North America, in terms of annual sales, providing sales and marketing, distribution and logistics services to customer locations across the U.S. and Canada. Our origins date back to 1888, when Glaser Bros., a family-owned-and-operated candy and tobacco distribution business, was founded in San Francisco, California.

Core-Mark offers retailers the ability to participate intake advantage of manufacturer and Company-sponsored sales and marketing programs, merchandising and product category management services as well asand the use of information systems and data services that are focused on minimizing retailers' investment in inventory, while seeking to maximize their sales.sales and profits. In addition, our wholesale distributing capabilities provide valuable services to both manufacturers of consumer products and convenience retailers. Manufacturers benefit from our broad retail coverage, inventory management, efficiency in processing small orders and efficient processingfrequency of small orders.deliveries. Convenience retailers benefit from our distribution capabilities by gaining access to a broad product line, optimizing inventory management and accessing trade credit.

We operate in an industry where, in 2009,2012, based on the NACSNational Association forof Convenience and Petroleum Retailing 2010Stores (NACS) 2013 State of the Industry (“SOI”) Report, total in-store sales at convenience retail locations in the U.S. increased 4.9%2.2% to approximately $182.4$199 billion and were generated through an estimated 145,000approximately 149,000 stores. According to a more recent report from NACS, the number of convenience stores across thegrew 1.4% in 2013 to approximately 151,000 stores. The U.S. We estimate that approximately 50% of the products that these stores sell are supplied by wholesale distributors such as Core-Mark. The convenience retail industry gross profit for in-store sales wasdecreased 1.3% to approximately $58.6$62.5 million in 2012 from $63.3 billion in 2009 and $55.6 billion in 2008.2011. Over the ten years from 19992003 through 2009,2013, U.S. convenience in-store sales increased by a compounded annual growth rate of 6.2%5.5%. In Canada, based on the Canadian Convenience Store Association (CCSA) 2013 Industry Report, we estimate that total in-store sales at convenience locations were approximately $23.1 billion generated through approximately 23,100 stores.

We operate a network of 28 distribution centers (excluding two distribution facilities we operate as a third party logistics provider) in the U.S. and Canada, which distribute a diverse line of national, regional and private label convenience store products to approximately 26,000over 30,000 customer locations in all 50 states ofin the U.S. and five Canadian provinces. The products we distribute include cigarettes, other tobacco products, candy, snacks, fast food, groceries, fresh products, dairy, bread, non-alcoholic beverages, general merchandise and health and beauty care products. Cigarettes comprised approximately 68.0% of our total net sales in 2013, while approximately 70.5% of our gross profit in 2013 was generated from our food/non-food products.

We service traditional convenience stores as well as alternative outlets selling consumer packaged goods. We estimate that on average 45% to 50% of the products sold in convenience products.stores are supplied by broad-line wholesale distributors such as Core-Mark. Our traditional convenience store customers include many of the major national and super-regional convenience store operators, as well as thousands of multi- and single-store customers. Our alternative outlet customers comprise a variety of store formats, including druggrocery stores, grocerydrug stores, liquor stores, cigarette and tobacco shops, hotel gift shops, military exchanges, college bookstores,and corporate campuses, casinos, movie theaters, hardware stores, airport concessions and airport concessions.other specialty and small format stores that carry convenience products.

We operate a network of 24 distribution centers (excluding two distribution facilities we operate as a third party logistics provider) in the U.S. and Canada. We distribute approximately 43,000 Stock Keeping Units ("SKUs") of packaged consumable goods to our customers and also provide an array of information and data services that enable our customers to better manage retail product sales and marketing functions.

In 2010, our consolidatedOur net sales increased grew from $7.3 billion in 2010 to $9.8 billion in 2013, yielding an annual compounded growth rate of approximately 10%, while our annual Adjusted EBITDA11.3%(1) increased from $70.0 million to $7,266.8$109.5 million, from $6,531.6 million in 2009. Cigarettes comprisedor approximately 70.5%16%, compounded annually during the same period. Our growth has been driven primarily by our business strategies described more fully below. We believe these strategies have positioned us to continue to grow our approximate 4% market share of total netin-store sales within the convenience store channel in 2010, while approximately 69.0%North America and to take advantage of our gross profit was generated from food/non-food products.growth opportunities with other retail store formats.

| |

| (1) | Adjusted EBITDA is a non-GAAP financial measure and should be considered as a supplement to, and not as a substitute for, or superior to, financial measures calculated in accordance with GAAP. Adjusted EBITDA is equal to net income adding back net interest expense, provision for income taxes, depreciation and amortization, LIFO expense, stock-based compensation expense and net foreign currency transaction losses. |

Competitive Strengths

We believe we have the following fundamental competitive strengths, which areform the foundation offor our business strategy:

Experience in the Industry. Our origins date back to 1888, when Glaser Bros., a family-owned-and-operated candy and tobacco distribution business, was founded in San Francisco, California. The executive management team, as of the end of 2013, comprised of our CEO and 14 senior managers, hashad an average tenure of over 1520 years and applies theirapplied its expertise to critical functional areas including logistics, sales and marketing, purchasing, information technology, finance, business development, human resources and retail store support.

Innovation &and Flexibility. Wholesale distributors typically provide convenience retailers access to a broad product line, the ability to place small quantity orders, inventory management and access to trade credit. As a large, full-service wholesale distributor, we offer retailers the ability to participate ina wide array of manufacturer and Company-sponsored sales and marketing programs, merchandising and product category management services as well asand the use of information systems that are focused on minimizing retailers' investment in inventory, while seeking to maximize their sales.sales and profit.

Distribution Capabilities. The wholesale distribution industry is highly fragmented and historically has consisted of a large number of small, privately-owned businesses and a small number of large, full-service wholesale distributors serving multiple geographic regions. Relative to smaller competitors, large distributors such as Core-Mark benefit from several competitive advantages including: increased purchasing power, the ability to service large national chain accounts, economies of scale in sales and operations, the ability to spread fixed costs over a larger revenue base and the resources to invest in information technology and other productivity enhancing technology.productivity-enhancing technologies.

Business Strategy

Our objective is to increase overall return to shareholdersstockholders by growing our market share, revenues and profitability. To achieve that objective, we have becomeAs one of the largest marketers of fresh and broad-line supply solutions to the convenience retail industry in North America. In orderAmerica, with the proven capability of effectively selling into other retail channels, we are well-positioned to continue meeting this objective. Our business strategy also includes the following initiatives, designed to further enhance the value we provide to our value to the retailer, we plan to:retail customers:

DriveLeverage our Vendor Consolidation Initiative (“VCI”). We expect our VCI program will allow us to continue to grow our sales by capitalizing on the highly fragmented nature of the distribution channelsupply chain that services the convenience retail industry. A convenience retailer generally receives store merchandise through a large number of uniquedirect-store deliveries. This represents a highly inefficient and costly process for the individual stores.retailers. Today, we estimate that Core-Mark sells on average 45% to 50% of what a convenience retailer purchases from their vendors. Our VCI program offers convenience retailersthe retailer the ability to receive one deliverymultiple weekly deliveries for the bulk of their products, including dairy and other perishable items, thus simplifyingmerchandise they would historically purchase from direct-store-delivery companies. This simplifies the supply chain and eliminatingprovides retailers with an opportunity to improve inventory turns and working capital, eliminate operational costs.and transaction costs, and greatly diminish their out-of-stocks on best-selling items.

Deliver Fresh Products. We believe there is an increasing trend among consumers to purchase fresh food and dairy products from convenience stores.and other retail formats. To meet this expected demand, we have modified and upgraded our refrigerated capacity, including investing in chill docks state-of-the-art ordering devices and tri-temperature trailers, which enables usprovides the infrastructure to deliver a significant range of chilled items including milk, produce and other fresh foods to retail outlets. We have also established partnerships with strategically locatedstrategically-located dairies, fresh kitchens and bakeries and commissaries to further enable us to deliver the freshest product possible.possible, with premium consumer items such as sandwiches, wraps, cut-fruit, parfaits, pastries, doughnuts, bread and home meal replacement solutions. We continue to expand the deliveryarray of fresh products through the development of unique and comprehensive marketing programs and we have rebrandedequipment programs that assist the Company to properly reflect the role this freshretailer in showcasing their “fresh” product line will play in our and the industry's future.offering. We believe our investments in infrastructure, and branding, combined with our strategically located suppliers and in-house expertise, position us as the leader in providing fresh products and programs to the convenience stores.retail industry. Proper execution of VCI, with the cornerstone being dairy distribution, provides Core-Mark the critical mass necessary to offer retailers a multiple weekly delivery platform, which facilitates the proper handling and dating of "Fresh" products.

Expand our Presence Eastward. We believe there is significant opportunity for us to increase our market sharepresence and revenue growth by continuing to expand our presence east of the Mississippi.Mississippi River. According to The Association for Convenience & Petroleum Retailing 2010the 2013 SOI Report, during 2009,2012, aggregate U.S. traditional convenience retail in-store sales were approximately $182.4$199 billion through approximately 145,000149,000 stores with the majority61% of those stores located eastin the eastern portion of the Mississippi.country. We believe our continued expansion eastwardin the Eastern U.S. will be accomplished through acquisitions and by acquiringgaining new customers, both national and regional, through a combination of exemplary service, VCI programs, fresh product deliveries, innovative marketing strategies, and competitive pricing.

In January 2008,Some of our recent expansion activities include:

On May 7, 2013, we openedsigned a three year distribution agreement with Turkey Hill, a subsidiary of the Kroger Co. (“Kroger”) and the largest of Kroger's convenience divisions, to service all their convenience stores, which are located across

Pennsylvania, Ohio and Indiana. With the addition of the Turkey Hill stores, we serviced approximately 700 Kroger convenience locations as of December 31, 2013.

On December 17, 2012, we acquired J.T. Davenport & Sons, Inc. (“Davenport”), a large convenience wholesaler based in North Carolina, which services customers in the eight states of North Carolina, South Carolina, Georgia, Maryland, Ohio, Kentucky, West Virginia and Virginia. This acquisition increased our market presence primarily in the Southeastern United States and further enhanced our ability to cost effectively service national and regional retailers.

On September 7, 2011, we signed a distribution agreement (“the Customer Agreement”) with Alimentation Couche-Tard Inc. ("Couche-Tard") to service Couche-Tard corporate stores, under the Circle K brand, within Couche-Tard's Southeast, Gulf Coast and Florida markets. We added a new distribution facility near Toronto, Ontario. This facility expanded our existing market geographylocated in Canada. Tampa, Florida in 2011 as a result of the Customer Agreement. As of December 31, 2013, we serviced nearly 1,000 Circle K stores in these markets.

In addition to organic growth, we intend to explore select acquisitions of other wholesale distributors which complement our business. In June 2008,May 2011, we acquired Auburn Merchandise Distributors, Inc.Forrest City Grocery Company (“AMD” or “New England”) to further expand our presence and infrastructure in the Northeastern region of the U.S. In August 2010, we acquired Finkle Distributors, Inc. (“FDI”FCGC”), a convenience wholesalerregional wholesale distributor providing Core-Mark with additional infrastructure and market share by servicing customers in New York, PennsylvaniaArkansas, Mississippi, Tennessee and the surrounding states, to continue to expand our market share in the Northeastern region of the U.S. (see Note 3 -- Acquisitions to our consolidated financial statements).states.

Continue Building Sustainable Competitive Advantage. We believe our ability to increase sales and profitability with existing and new customers is highly dependent upon our ability to deliver consistently high levels of service, innovative marketing programs, and information technology solutions and logistics support. To that fundamental end, we are committed to further improving operational efficiencies in our distribution centers while containing our costs in order to enhance profitability. To further enhance our competitive advantage, we have beenWe were one of the first to recognize emerging trends and to offer retailers our unique marketing programsstrategic solutions such as VCI and Fresh. In addition, we continue to leverage our Focused Marketing Initiative (“FMI”), which is designed to drive deeper entrenchment with our customer base and to further differentiate us in the market place. The FMI program is centered on increasing the sales and profitability of the independent store through improved category insights, optimized retail price strategy, demographic decision-making along with providing Core-Mark's marketing solutions to create a complete retail marketing strategy. We believe this innovationour innovative approach, which focuses on building a trusted partnership with our customers, has established us as the market leader in providing valuable marketing and supply chain solutions into the convenience retail industry.

Customers, Products and Suppliers

We service approximately 26,000over 30,000 customer locations in all 50 states ofin the U.S. and five Canadian provinces. Our customers represent manyprimary customer base consists of the large national, regional, and regionalindependent convenience retailers in the U.S. and CanadaCanada. In addition, we are expanding our distribution into alternative channels including drug stores and leading alternative outlet customers.large-scale retailers. Our top ten customers accounted for approximately 32.6%35.4% of our net sales in 2010, and no single2013 including Couche-Tard, our largest customer, which accounted for 10% or more14.7% of our total sales in 2010.net sales.

Below is a comparison of our net sales mix by primary product category for the last three years (in millions):

| | | | Year ended December 31, | | | | | | | | | | | | | |

| | | 2010 | | 2009 | | 2008 | Year Ended December 31, |

| | | Net Sales | | % of Net Sales | | Net Sales | | % of Net Sales | | Net Sales | | % of Net Sales | 2013 | | 2012 | | 2011 |

| Product Category | | Net Sales | | % of Net Sales | | Net Sales | | % of Net Sales | | Net Sales | | % of Net Sales |

| Cigarettes | | $ | 5,119.7 | | | 70.5 | % | | $ | 4,589.1 | | | 70.3 | % | | $ | 4,124.8 | | | 68.2 | % | $ | 6,642.0 |

| | 68.0 | % | | $ | 6,139.4 |

| | 69.0 | % | | $ | 5,710.6 |

| | 70.4 | % |

| Food | | 840.9 | | | 11.6 | % | | 738.0 | | | 11.3 | % | | 710.1 | | | 11.7 | % | 1,342.3 |

| | 13.7 |

| | 1,178.6 |

| | 13.4 |

| | 995.7 |

| | 12.3 |

|

| Candy | | 426.0 | | | 5.8 | % | | 405.0 | | | 6.2 | % | | 401.3 | | | 6.7 | % | 527.2 |

| | 5.4 |

| | 489.5 |

| | 5.5 |

| | 459.8 |

| | 5.7 |

|

| Other tobacco products | | 503.6 | | | 6.9 | % | | 434.0 | | | 6.6 | % | | 402.7 | | | 6.7 | % | 787.8 |

| | 8.1 |

| | 687.8 |

| | 7.7 |

| | 607.9 |

| | 7.5 |

|

| Health, beauty & general | | 220.6 | | | 3.0 | % | | 209.5 | | | 3.2 | % | | 220.1 | | | 3.6 | % | 327.3 |

| | 3.4 |

| | 269.2 |

| | 3.0 |

| | 237.5 |

| | 2.9 |

|

| Non-alcoholic beverages | | 152.0 | | | 2.1 | % | | 151.7 | | | 2.3 | % | | 180.9 | | | 3.0 | % | |

| Beverages | | 139.1 |

| | 1.4 |

| | 125.6 |

| | 1.4 |

| | 100.9 |

| | 1.2 |

|

| Equipment/other | | 4.0 | | | 0.1 | % | | 4.3 | | | 0.1 | % | | 5.0 | | | 0.1 | % | 1.9 |

| | — |

| | 2.3 |

| | — |

| | 2.5 |

| | — |

|

| Total food/non-food products | | 2,147.1 | | | 29.5 | % | | 1,942.5 | | | 29.7 | % | | 1,920.1 | | | 31.8 | % | 3,125.6 |

| | 32.0 |

| | 2,753.0 |

| | 31.0 |

| | 2,404.3 |

| | 29.6 |

|

| Total net sales | | $ | 7,266.8 | | | 100.0 | % | | $ | 6,531.6 | | | 100.0 | % | | $ | 6,044.9 | | | 100.0 | % | $ | 9,767.6 |

| | 100.0 | % | | $ | 8,892.4 |

| | 100.0 | % | | $ | 8,114.9 |

| | 100.0 | % |

Cigarette Products. We purchase cigarette products from major U.S. and Canadian manufacturers. With cigarettes accounting for approximately $5,119.7$6,642.0 million, or 70.5%68.0% of our total net sales, and 31.0%29.5% of our total gross profit in 2010,2013, we control major purchases of cigarettes centrally in order to optimize inventory levels and purchasing opportunities. The daily replenishment of inventory and brand selection is controlled by our distribution centers.

In the U.S., legislation was introduced in 2008 to fund the State Children's Health Insurance Program (“SCHIP”) by raising the federal cigarette excise tax from 39¢ to $1.01 per pack. Federal excise tax is included as a component of our product cost charged by the manufacturer. The legislation, which was signed into law in February 2009, became effective April 1, 2009. As a result, our net cigarette sales were inflated in 2009, due primarily to the significant price increases from manufacturers in response to the SCHIP legislation.

U.S. and Canadian cigarette consumption has generallysteadily declined over the last ten years.from 2002 to 2012. Based on 2010the 2012 statistics provided by the Tobacco Merchants Association (“TMA”) published in early 2011 and2013 compiled from the U.S. Department of Agriculture-EconomicAgriculture - Economic Research Service, total cigarette consumption in the U.S. declined from 456425 billion cigarettes in 20002002 to 299294 billion cigarettes in 2010,

2012, or 34%a compounded annual decline of approximately 3.6%. PriorTotal cigarette consumption also declined in Canada from 37 billion cigarettes in 2002 to 2007, we had benefited from25 billion cigarettes in 2012, or a shift in cigarette and tobacco sales to the convenience retail segmentcompounded annual decline of approximately 3.8%, based on statistics reportedprovided by NACS. In 2010, convenience retailers were the largest trade class for cigarette sales accounting for approximately 70% ofTMA. Our total industry volume according to the R.J. Reynolds' 2010 Industry Report. The shift in cigarette carton sales from other channelsincreased 7.6% in 2013 attributable primarily to our acquisition of Davenport in December of 2012 and net market gain shares. Excluding the acquisition of Davenport, our carton sales in the U.S. declined 1.8%. Our carton sales in Canada decreased 7.5% in 2013 on a comparative basis to the convenience retail segment may no longer be adequateprior year due primarily to compensate forthe loss of two non-major customers in the fourth quarter of 2012. Although we anticipate overall cigarette consumption declines. However,will continue to decline, we expect to offset the majority of the impact from these declines through market share expansion, growth in our non-cigarette categories and incremental gross profit that resultsfrom cigarette manufacturer price increases. We expect cigarette manufacturers will continue to raise prices as carton sales decline in order to maintain or enhance their overall profitability.

Total cigarette consumption also declined in Canada from 43 billion cigarettes in 2000 to 25 billion cigarettes in 2010, or a 42% reduction in consumption, based on the 2010 statistics provided by TMA.

In 2010, our carton sales in the U.S. increased 1.1%, excluding the impact resulting from the acquisition of Finkle Distributors, Inc., in August 2010. Our carton sales in Canada increased 7.5% primarily through market share gains driven by our expansion in the Toronto market.

We have no long-term cigarette purchase agreements and buy substantially all of our products on an as neededas-needed basis. Cigarette manufacturers historically have offeredoffer structured incentive programs to wholesalers based on maintaining market share and executing promotional programs. These programs are subject to change by the manufacturers without notice.

In addition to exciseExcise taxes are levied by the federal government, excise taxes on cigarettes and other tobacco products by the U.S. and Canadian federal governments and are also imposed by the various states, localities and provinces. We collect state, local and provincial excise taxes from our customers and remit these amounts to the appropriate authorities.authorities based on the credit terms, if applicable, extended by each jurisdiction. Excise taxes are a significant component of our revenuenet sales and cost of sales. During 2010, we included in2013, net sales and cost of sales included offsetting amounts of approximately $1,756.5$2,050.8 million ofrelated to state, local and provincial excise taxes. As of December 31, 2010,2013, state cigarette excise taxes in the U.S. jurisdictions we serve ranged from $0.17 per pack of 20 cigarettes in the state of Missouri to $4.35 per pack of 20 cigarettes in the state of New York. In the Canadian jurisdictions we serve, provincial excise taxes ranged from C$2.47 per pack of 20 cigarettes in Ontario to C$5.485.80 per pack of 20 cigarettes in the Northwest Territories.

Manitoba. Federal excise taxes are levied on the manufacturers who pass the tax on to us as part of the product cost and thus are not a component of our excise taxes.

Food/Non-food Products. Our food products include fast food, candy, snacks, groceries, non-alcoholic beverages and fresh products such as sandwiches, juices, salads, produce, dairy and bread. Our non-food products include cigars, tobacco, health and beauty care products, general merchandise and equipment. SalesNet sales of the combined food/non-food product categories grew 10.5%13.5% in 20102013 to $2,147.1$3,125.6 million, which was 29.5%32.0% of our total net sales. More specifically, sales in the food category grew 13.9% to $1,342.3 million, by far the largest contributor to our overall food/non-food sales improvement. This is consistent with our strategy to grow food/non-food products at a faster pace than cigarettes through a combination of market share gains and execution of our VCI, Fresh, FMI and acquisition strategies.

Gross profitsprofit for food/non-food categories grew $6.7$52.8 million, or 2.6%16.2%, to $265.9$378.6 million in 2013, which was 69.0%70.5% of our total gross profit. Food/non-food products generated gross margins of 13.40%13.0% excluding excise taxes in 2010,2013, while the cigarette category generated gross margins of 3.39%3.3% excluding excise taxes. Gross margin growth in our food/non-food categories was negatively impacted by a $5.3 million reduction in floor stock income dueIn order to lower manufacturers' price inflation.

Due totake advantage of the significantly higher margins earned by food/non-food products, two of our key business strategies, VCI and ourthe delivery of fresh initiative,products, focus primarily on the higherhighest margin categories in the foodfood/non-food group. TheseThere is a special emphasis on fresh categories, which include items such as milk, fresh bread, fresh sandwiches, fresh fruit, fresh produce, fresh baked goods, healthy snackshome meal replacements and home replacement meals. This drive toward more healthy andother fresh foods being sold in the convenience markets is a recognized major trend in the industry.products. We have invested amade significant amount of capital investments over the years to position our Company to havecreate the proper infrastructure to successfully deliver these highly perishable items. Our objective

Another primary aspect of our VCI strategy is to consolidatetake cost out of the current fragmented naturesupply chain by putting more of convenience store vendor distribution by consolidating suchthe product that the retailers purchase on our delivery trucks. We targeted $100 million of incremental sales for the last five years, which contributed to the growth in our food/non-food sales and gross profit dollars. In addition, our FMI strategy was created to assist our independent retailer to sell more food/non-food items as dairy and bread and to increase profitability.

We completed five acquisitions between 2006 and 2012. At the time of acquisition, most of these companies generally had a higher index of cigarette sales than our company-wide average; however, through our marketing programs we are able to grow “fresh food”the higher margin food/non-food categories of these acquired businesses as we bring our strategies to their customers. In addition, our market share forhas grown steadily over the customers we service as they fight forlast several years, due, in part, to our capability to deliver fresh and perishable categories. We believe that fresh items are increasingly driving consumer “share of stomach” fordecisions, and fresh foods with other retailers. Ultimately the defragmentation of vendor deliveries coupled with market share gains in fresh foods for the stores we serviceproducts will increase our customers' sales and profits and in turn improve our sales and profits.

continue to be an important category going forward.

Our Suppliers. We purchase products for resale from approximately 4,4004,700 trade suppliers and manufacturers located across the U.S. and Canada. In 2010,2013, we purchased approximately 62%64% of our products from our top 20 suppliers, with our top two suppliers, Philip Morris USA, Inc. and R.J. Reynolds representingTobacco Company, accounting for approximately 28% and 13%14% of our purchases, respectively. We coordinate our purchasing from suppliers by negotiating, on a corporate-wide basis, special arrangements to obtain volume discounts and additional incentives, while also taking advantage of promotional and marketing incentives offered to us as a wholesale distributor. In addition, buyers in each of our distribution facilities purchase products, particularly food, directly from the manufacturers, improving product mix and availability for individual markets.

Seasonality

We typically generate slightly higher revenuesnet sales and higher gross profits during the warm weather months (May(April through September) than in other times throughout the year. We believe this occurs because the convenience store industry which we serve tends to be busier during this period due to vacationvacations and travel. Duringother travel by consumers. We generated approximately 53%, 52% and 53% of our net sales during the second and third quarters of 2010, 20092013, 2012, and 2008, we generated approximately 53% of our net sales for each fiscal year.2011, respectively.

Operations

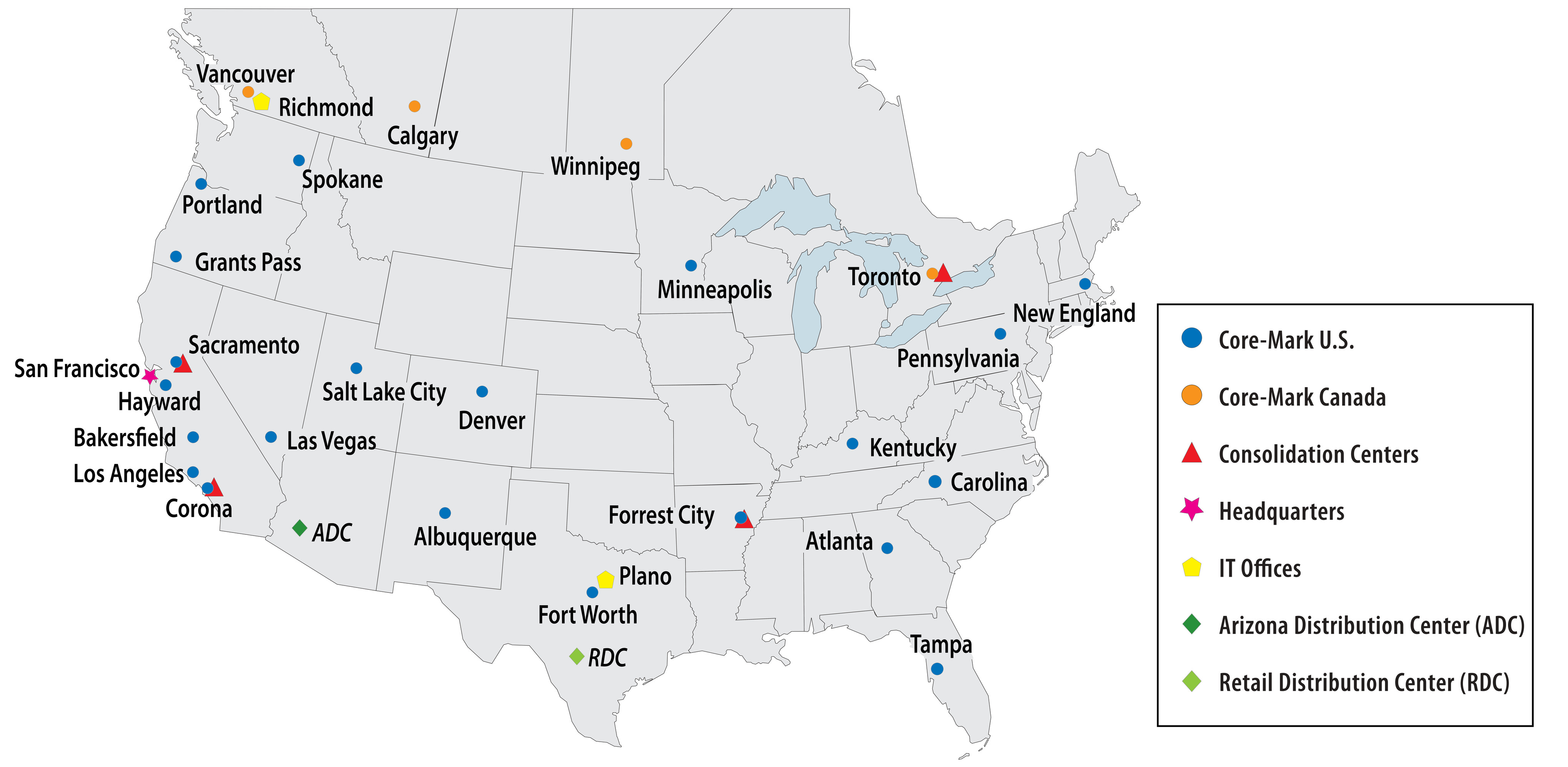

We operate a network of 2428 distribution centers in the U.S. and Canada (excluding two distribution facilities we operate as a third party logistics provider). TwentyTwenty-four of our distribution centers are located in the U.S. and four are located in Canada. The map below depicts the scope of our operations and the names of our distribution centers.

Map of Operations

Two of the facilities weWe operate four consolidation centers, including one that opened in Toronto, Canada in the U.S., Artic Cascade and Allied Merchandising Industry, are consolidating warehousesfourth quarter of 2013, which buy products from our suppliers in bulk quantities and then distribute the products to many of our other distribution centers. By using Artic Cascade, located in Sacramento, California, to obtainThe products at lower cost frompurchased by our consolidation centers include frozen product vendors, we are able to offer a broader selection of quality products to retailers at more competitive prices. Allied Merchandising Industry, located in Corona, California, purchases the majority of our non-food products, other than cigarettes and tobacco products, for our distribution centers, enabling us to reduce our overall general merchandise andchilled items, health and beauty care product inventory.and general merchandise products. The new center in Toronto was launched with an exclusive distribution arrangement with a retail beverage manufacturer. We expect to obtain additional consolidated purchasing opportunities for Canada in 2014. We operate two additional facilities as a third party logistics provider. One distribution facility located in Phoenix, Arizona, referred to as the Arizona Distribution Center (“ADC”), is dedicated solely to supporting the logistics and management requirements of one of our major customers, Alimentation Couche-Tard Inc.Couche-Tard. The second distribution facility located in San Antonio, Texas, referred to as the Retail Distribution Center (“RDC”), is dedicated solely to supporting another major customer, CST Brands, Inc. (formerly, Valero Energy Corporation.Corporation).

We purchase a variety of brand name and private label products, totaling approximately 43,000in excess of 53,000 SKUs, including approximately 1,700 cigarette products, from our suppliers and manufacturers. Cigarette products represent less than 5% of our total SKUs purchased. We offer customers a variety of food and food/non-food products, including fast food, candy, snacks, groceries, fresh products, dairy, bread, non-alcoholic beverages, other tobacco products, general merchandise and health and beauty care products.

A typical convenience store order consists of a mix of dry, frozen and chilled products. Our receivers, stockers, order selectors, stampers, forklift drivers and loaders received, storedstocked and picked approximately 454615 million, 426551 million and 435476 million items (a carton of 10 packs of cigarettes is one item) or 7196 million, 6586 million and 6671 million cubic feet of product, during the years ended December 31, 2010, 20092013, 2012 and 2008,2011, respectively, while limiting the service error rate to approximately twoless than 2.7 errors per thousand items shipped in 2010.

Our proprietary Distribution Center Management System ("DCMS") platform provides our distribution centers with the flexibility to adapt to our customers' information technology requirements in an industry that does not have a standard information technology platform. Actively integrating our customers onto our platform is a priority which enables fast, efficient and reliable service.2013.

Our proprietary Distribution Center Management System platform provides our distribution centers with the flexibility to adapt rapidly to changing business needs and allows them to provide our customers with necessary information technology requirements and integration capabilities.

Distribution

At December 31, 2010,2013, we had approximately 9911,300 transportation department personnel, including delivery drivers, shuttle drivers, routers, training supervisors and managers who focus on achieving safe, on-time deliveries. Our daily orders are picked and loaded nightly in reverse order of scheduled delivery. At December 31, 2010,2013, our trucking fleet consisted of approximately 700over 800 tractors, trucks and vans, of which nearlymostly all were leased. We have made a significant investment over the past few years in upgrading our trailer fleet to tri-temperature (“tri-temp”), which gives us the capability to deliver frozen, chilled and non-refrigerated goods in one delivery. As of December 31, 2010,2013, approximately 70%80% of our trailers were tri-temp, with the remainder capable of delivering refrigerated and non-refrigerated foods. This provides us the multiple temperature zone capability needed to support our focus on delivering fresh products to our customers. In addition, in 2013, we began converting portions of our fleet to tractors, which use compressed natural gas ("CNG"). At December 31, 2013, we had 57 CNG tractors. We plan to convert a large portion of our fleet to CNG tractors in order to lower our fuel costs with the added benefit of reducing carbon emissions. Our fuel consumption costs for 2010in 2013 totaled approximately $9.5$16.9 million, net of fuel surcharges passed on to customers, which represented an increase of approximately $4.6 million,16%, from $4.9$14.6 million in 2009,2012, due primarily to higher fuel prices, a 6.9%11.9% increase in miles driven excluding FDI,due to the addition of Davenport and the acquisition of FDI.growth in our business.

Competition

We estimate that, as of December 31, 2010,2013, there were overapproximately 300 wholesale distributors serving traditional convenience retailers in the U.S. and Canada. We believe that McLane Company, Inc., a subsidiary of Berkshire Hathaway, Inc., and Core-Mark are the two largest convenience wholesale distributors measured(measured by annual sales,sales) in North America. There are alsotwo other large regional companies that provide products to specific regionsareas of the country, such as The H.T. Hackney Company in the Southeast and Eby-Brown Company in the Midwest and Mid-Atlantic and Southeast and GSC Enterprises, Inc. in Texas and surrounding states, andregions. In addition there are several hundred local distributors serving small regional chains and independent convenience retailers. In Canada, there are feweris one large national company, Wallace & Carey, Inc., one regional company, which services the Ontario market, Karrys Bros., Limited, and more recently one large national grocery wholesaler, Sobeys Inc., aside from Core-Mark, that make up the competitive landscape.

Beyond the traditional wholesale distributors compared to the U.S. In addition,supply channels, we face potential competition from at least three other supply avenues. First, certain manufacturers such as The Coca Cola Company, Hostess Brands, Inc., Frito- Lay North America, Inc.Budweiser, Miller-Coors, Coca-Cola, Frito-Lay and PepsiCo Inc. deliver their products directly to convenience retailers. Secondly, club wholesalers such as Costco and Sam's Club provide a limited selection of products at generally competitive prices; however, they often have limited delivery options and limited services. Finally, some large convenience retail chains self-distribute products due to the geographic density of their stores and their belief that they can economically service such locations.

Competition within the industry is based primarily on the range and quality of the services provided, price, variety of products offeredproduct selection and the reliability of deliveries.wholesalers' logistics. We operate from a perspective that focuses heavily on flexibility and providing outstanding customer service through our distribution centers, order fulfillment rates, on-time delivery performance using delivery equipment sized for the small format store, innovative marketing solutions and merchandising support, as well as competitive pricing. We believe this represents a contrast to some large competitors whothat offer a standardized logistics approach, with emphasis on uniformity of product lines, and company determined delivery schedules using large delivery equipment designed for large format stores, while also providing competitive order fulfillment rates and pricing. Thestores. While this emphasis on thea standardized logistics approach while responsive toallows for competitive pricing, iswe do not in our opinionbelieve it is best suited for retailers looking for more customized solutions and support from their supply partners in addition to competitive pricing. SomeAlternatively, some small competitors focus on customer service and long standinglong-standing customer relationships but often times lack the range of offerings of the larger distributor.distributors. We believe that our unique combination of service, marketing solutions and price is a compelling combination that is highly attractive to customersretailers and mayhelps to enhance their growth and profitability.

WeIn the U.S. we purchase cigarettes primarily from manufacturers covered by the tobacco industry's Master Settlement Agreement (“MSA”), which was signed in November 1998. Competition amongst cigarette wholesalers is based primarily on service, price and variety, whereas competition amongst manufacturers for cigarette sales is based primarily on brand positioning, price, product attributes, consumer loyalty, promotions, marketing and retail presence. Cigarette brands produced by the major tobacco product manufacturers generally require competitive pricing, substantial marketing support, retail programs and other financial incentives to maintain or improve a brand's market position. Historically, major tobacco product manufacturers have had a competitive advantage in the U.S. because significant cigarette marketing restrictions and the scale of investment required to compete made gaining consumer awareness and trial of new brands difficult.

We also face competition from the diversion into the U.S. and Canadian markets of cigarettes intended for sale outside of such markets, including the sale of cigarettes in non-taxable jurisdictions, inter-state/provincial and international smuggling of cigarettes,

the sale of counterfeit cigarettes by third parties, increased imports of foreign low priced brands, the sale of cigarettes by third parties over the internet and by other means designed to avoid collection of applicable taxes, including the saletaxes. The competitive environment has been characterized by a continued influx of cigarettes in non-taxable jurisdictions, importscheap products that challenge sales of foreign, low-priced brandshigher priced and the diversion into the U.S. market of cigarettes intended for sale outside the U.S. fully taxed cigarettes.

We also believe the competitive environment has been impacted by alternative smoking products, such as snus, electronic cigarettes and snuff, higherthe emergence of nicotine consumption through vapor devices. In addition, cigarette prices continue to rise due to higher federal and statecontinuing pressure on taxing jurisdictions to raise revenues through excise taxes andtaxes. Further, cigarette list price increasesprices have historically increased for cigarettes manufactured bythose manufacturers who are parties to the MSA, and the impact of restrictions on marketing imposed by the U.S. Food and Drug Administration ("FDA").MSA. As a result, the lowestlower priced products of numerous small share brands manufactured by companies that are not parties to the MSAnon-MSA participants have held their market share, putting profitability pressure on the profitability of premium cigarettes.MSA products.

Working Capital Practices

We sell products on credit terms to our customers that averaged, as measured by days sales outstanding, about nine days for 2010, 2009each of 2013, 2012 and 2008.2011. Credit terms may impact pricing and are competitive within our industry. An increasing number of our

customers remit payment electronically, which facilitates efficient and timely monitoring of payment risk. Canadian days sales outstanding in receivables tend to be lower as Canadian industry practice is for shorter credit terms than in the U.S.

We maintain our inventory of products based on the level of sales of the particular product and manufacturer replenishment cycles. The number of days a particular item of inventory remains in our distribution centers varies by product and is principally driven by the turnover of that product and economic order quantities. We typically order and carry in inventory additional amounts of certain critical products to assure high order fulfillment levels for these items. Periodically, we may carry higher levels of inventory to take advantage of anticipated manufacturer price increases. The number of days of cost of sales in inventory averaged about 1516 days during 2010, 2009in each of 2013, 2012 and 2008.

2011 with the cigarette category averaging 10 days and food/non-food categories averaging 30 days. We obtain terms from our vendors and certain taxing jurisdictions based on industry practices, and consistent with our credit standing. We take advantage of the full complement of term offerings, which may include enhanced cash discounts for earlier payment.payment or prepayment. Terms for our accounts payable and cigarette and tobacco taxes payable range anywhere from three days prepaid to 60 days credit. Days payable outstanding for both categories, excluding the impact of prepayments, during 2010each of 2013, 2012 and 20092011 averaged about 11 days, compared to 12 days in 2008.days.

Employees

The following chart provides a breakdown of our employees by function and geographic region (including employees at our third party logistic facilities) as of December 31, 2010:2013:

TOTAL EMPLOYEES BY BUSINESS FUNCTIONS

| | | | | U.S. | | Canada | | Total | U.S. | | Canada | | Total |

| Sales and Marketing | | 1,091 | | | 83 | | | 1,174 | | 1,256 |

| | 65 |

| | 1,321 |

|

| Warehousing and Distribution | | 2,376 | | | 267 | | | 2,643 | | 3,255 |

| | 297 |

| | 3,552 |

|

| Management, Administration, Finance and Purchasing | | 478 | | | 104 | | | 582 | | 628 |

| | 116 |

| | 744 |

|

| Total Categories | | 3,945 | | | 454 | | | 4,399 | | 5,139 |

| | 478 |

| | 5,617 |

|

Three of our distribution centers, Hayward, Las Vegas and Calgary, have employees who are covered by collective bargaining agreements with local affiliates of The International Brotherhood of Teamsters (Hayward and Las Vegas) and United Food and Commercial Workers (Calgary). Approximately 213210 employees, or 4.8%4% of our workforce, are unionized. There have been no disruptions in customer service, strikes, work stoppages or slowdowns as a result of union activities, and we believe we have satisfactory relations with our employees.

Regulation

As a distributor of food products in the U.S., we are subject to the Federal Food, Drug and Cosmetic Act and regulations promulgated by the FDA.U.S. Food and Drug Administration (“FDA”). The FDA regulates the holding requirements for foodsfood products through its current good manufacturing practice regulations, specifies the standards of identity for certain foods and prescribes the format and content of certain information required to appear on food product labels. A limited number of the over-the-counter medications that we distribute are subject to the regulations of the U.S. Drug Enforcement Administration.Administration (“DEA”). In Canada, similar standards related to food and over-the-counter medications are governed by Health Canada. The products we distribute are also subject to federal, state, provincial and local regulation through such measures as the licensing of our facilities, enforcement by state, provincial and local health agencies of relevant standards for the products we distribute and regulation of our trade practices in connection with the sale of our products. Our facilities are inspected periodically by federal, state, provincial and local authorities, including the Occupational Safety and Health Administration under the U.S. Department of Labor (“OSHA”), which require us to comply with certain health and safety standards to protect our employees.

We are also subject to regulation by numerous other federal, state, provincial and local regulatory agencies including, but not limited to, the U.S. Department of Labor, which sets employment practice standards for workers, the U.S. and Canadian Departments of Transportation, which regulate transportation of perishable goods, and similar state, provincial and local agencies. Non-compliance with, or significant changes to, these laws or the implementation of new laws, could have a material effect on our results of operations.

In September 2011, the Tobacco Products Labeling Regulations (Cigarettes and Little Cigars) came into force in Canada with strengthened labeling requirements for cigarettes and little cigar packages. The requirements include graphic health warnings and health information messages which are prominently displayed on the front and back of most tobacco packages and focus primarily on the health hazards posed by tobacco use.

We voluntarily participate in random quality inspections of all of our distribution centers, conducted by the American Institute of Baking (“AIB”). The AIB publishes standards as a tool to permit operators of distribution centers to evaluate the food safety risks within their operations and determine the levels of compliance with the standards. AIB conducts an inspection, which is composed of food safety and quality criteria. AIB conducts its inspections based on five categories: adequacy of the company's

food safety program, pest control, operational methods and personnel practices, maintenance of food safety and cleaning practices. Within these five categories, the AIB evaluates over 100 criteria items. AIB's independent evaluation is summarized and posted on its website for our customers' review. In 2010, nearly 97%2013, 96.8% of the audits of our distribution centers received the highest rating from the AIB with the remaining 3% receiving the second highest rating.

a score of 900 or greater (on a possible 1,000 point scale).

Registered Trademarks

We have registered trademarks including the following: Arcadia Bay®, Arcadia Bay Coffee Company®, BOONDOGGLES™, Cable Car®, Core-Mark®, Core-Mark International®, EMERALD®,, Java Street®, QUICKEATS®, Richland ValleyTM, SmartStock®, and Tastefully Yours®..

Segment and Geographic Information

We operate in two reportable geographic segmentsareas -- the U.S. and Canada. See Note 15 --16 - Segment and Geographic Information to our consolidated financial statements.

Corporate and Available Information

The office of ourOur corporate headquarters is located at 395 Oyster Point Boulevard, Suite 415, South San Francisco, California, 94080 and theour telephone number is (650) 589-9445.

Our internet website address is www.core-mark.com. We provide free access to various reports that we file with or furnish to the U.S. Securities and Exchange Commission (“SEC”) through our website, as soon as reasonably practicable after they have been filed or furnished. These reports include, but are not limited to, our annual reports on Form 10-K, quarterly reports on Form 10-Q and any amendments to those reports. Our SEC reports can be accessed through the “Investor Relations” section of our website under “Financials and Filings”, or through www.sec.gov. Also available on our website are printable versions of Core-Mark's Audit Committee Charter, Compensation Committee Charter, Nominating and Corporate Governance Committee Charter, Code of Business Conduct and Ethics, and Corporate Governance Guidelines and Principles.Principles and other corporate information. Copies of these documents may also be requested from:

Core-Mark International

395 Oyster Point Blvd, Suite 415

South San Francisco, CA 94080

Attention: Investor Relations

Corporate Governance-Governance---CodeCode of Business Conduct and Ethics and Whistle Blower Policy:

Our Code of Business Conduct and Ethics is designed to promote honest, ethical and lawful conduct by all employees, officers and directors and is postedavailable on the “Investor Relations” section of our website at www.core-mark.com under “Corporate Governance.”

Additionally, the Audit Committee (“Audit Committee”) of the Board of Directors of Core-Mark has established procedures to receive, retain, investigate and act on complaints and concerns of employees, shareholdersstockholders and others regarding accounting, internal accounting controls and auditing matters, including complaints regarding attempted or actual circumvention of internal accounting controls or complaints regarding violations of the Company's accounting policies. The procedures are also described inon our website address at www.core-mark.com under Corporate Governance“Corporate Governance” in the “Investor Relations” section.

ITEM 1. A. RISK FACTORS

You should carefully consider the following risks together with allOur business is subject to a variety of risks. Set forth below are certain of the other information contained in this Annual Report on Form 10-K. Additionalimportant risks and uncertainties not currently known to us may also materially adversely affect our business, financial condition or resultsthat we face, the occurrence of operations.

This Annual Report on Form 10-K contains forward-looking statements that involve risks and uncertainties. Our actual results may differ significantly from the results discussed in the forward-looking statements. Factors that might cause such differences include, but are not limited to, the risk factors set forth below(see Special Note Regarding Forward-Looking Statements prior to Item 1. Business).

Risks Related to the Economy and Market Conditions

Current difficult economic conditions may reduce demand for our products and increase credit risks.

Continuing difficult economic conditions, including increased unemployment and underemployment rates, significant declines in real estate values, large losses to consumer retirement and investment accounts and increases in food prices, have resulted in reduced consumer confidence and curtailed consumer spending. If these economic conditions persist or deteriorate further, we expect that convenience retail operators will experience continued weakness and further reductions in same store sales, which will adversely affect demand for our products and lead to reduced sales and increased pressures on margins. In addition, ongoing uncertainty in the financial markets and the resulting pressures on liquidity may place a number of our convenience retail customers under financial stress, which could increase our credit risk and potential bad debt exposure. These economic and market conditions may have a material adverse effect on our business, and operating results.

Our business is sensitive to gasoline prices and related transportation costs, whichfinancial condition or results of operations. These risks are not the only ones we face. We could adversely affect business.

Our operating results are sensitive to, and mayalso be adversely affected by unexpected increases in fuel or other transportation-related costs, including costs from the use of third party carriers, temporary staff and overtime. Our retailers have reportedadditional factors that are presently unknown to us or that when gasoline prices increased they have experienced a decrease in the proportion of their customers' expenditures on food/non-food products comparedwe currently believe to customers' expenditures on cigarettes. The shift in expenditures may place pressure on our sales and gross margins since sales of food/non-food products result in higher margins than sales of cigarettes do.

Historically, we have been able to pass on a substantial portion of increases in our own fuel or other transportation costsbe immaterial to our customers in the form of fuel surcharges, but our ability to continue to pass through price increases, either from manufacturers or costs incurred in the business, including fuel costs, is not assured. If we are unable to continue to pass on fuel and transportation-related cost increases to our customers, our operating results could be materially and adversely affected.

As a result of recent recessionary economic conditions, our pension plan is currently underfunded and we will be required to make cash payments to the plan, reducing the cash available for our business.

We record a liability associated with the underfunded status of our pension plans when the benefit obligation exceeds the fair value of the plan assets. Included in claims liabilities on our balance sheet as of December 31, 2010 is $8.5 million related to the underfunded pension obligation compared with $11.6 million as of December 31, 2009. The decrease in the underfunded status of our pension plans from 2009 to 2010 is due primarily to an increase in Company contributions and a higher return than expected on invested plan assets for 2010. If the performance of the assets in the plan does not meet our expectations, or if other actuarial assumptions are modified, our future cash payments to the plan could be substantially higher than we expect. We contributed $3.4 million to our plan in 2010, compared to $0.2 million and $0.4 million in 2009 and 2008, respectively. The pension plan is subject to the Employee Retirement Income Security Act of 1974 ("ERISA"). Under ERISA, the Pension Benefit Guaranty Corporation ("PBGC") has the authority to terminate an underfunded pension plan under limited circumstances. In the event our pension plan is terminated for any reason while it is underfunded, we will incur a liability to the PBGC that may be equal to the entire amount of the underfunding in the pension plan.

Risks Related to Our Business and Industry

We are dependent on the convenience retail industry, for our revenues, and our results of operations wouldcould suffer if there isit experiences an overall decline or consolidation in the convenience retail industry.consolidation.

The majority of our sales are made under purchase orders and short-term contracts with convenience retail stores which inherently involve significant risks. These risks include declining sales in the convenience retail industry due to general economic conditions, credit exposureincluding rising gasoline prices, which may impact “in store” retail sales, competition from our customers,grocery stores and other retail outlets, termination of customer relationships without notice,and consolidation of our customer basebase. Such events could cause us to experience decreases in revenues and consumer movement toward purchasing from club stores. Anyput pressure on our margins. In addition, any decline in the convenience store industry may place a number of these factorsour convenience retail customers under financial stress, which could negatively affectincrease our resultscredit risk and potential bad debt exposure.

Many of operations.

We face competitionthe markets in our distribution marketswhich we compete are highly competitive and if we are unable to compete effectively in any distribution market, we may lose market share and suffer a decline in sales and profitability.profitability in these markets if we are unable to outperform our competition.

Our distribution centers operate in highly competitive markets. We face competition from local, regional and national tobacco and consumable products distributors on the basis of service, price, reliability, delivery schedules, and variety of products offered, schedulesoffered. We also face competition from club stores and reliability of deliveries and the range and quality of services provided.alternate sources that sell consumable products to convenience retailers. Some of our competitors, including aMcLane Company, Inc. (a subsidiary of Berkshire Hathaway Inc., McLane Company, Inc., the largest convenience wholesale distributor in the U.S.), have substantial financial resources and long standinglong-standing customer relationships. In addition, heightened competition among our existing competitors, or by new entrants into the distribution market, could create additional competitive pressures that may reduce our margins and adversely affect our business. If we fail to successfully respond to these competitive pressures or to implement our strategies effectively, we may lose market share and our results of operations could suffer.

IncreasingOur failure to maintain relationships with large customers could potentially harm our business.

We have relationships with many large regional and national convenience store chains. While we expect to maintain these relationships for the growth and profitability of our distribution business is particularly dependent upon our ability to retain existing customers and attract additional customers. The ability to attract additional customers through our existing network of distribution centers is especially important because it enables us to leverage our distribution centers and other fixed assets. Our ability to retain existing customers and attract new customers is dependent upon our ability to provide industry-leading customer service, offer competitive products at low prices, maintain high levels of productivity and efficiencyforeseeable future, any termination, non-renewal or reduction in distributing products to our customers while integrating new customers into our distribution system, and offer marketing, merchandising and ancillary services that we provide value to such customers could cause our customers. If we are unablerevenues and operating results to execute these tasks effectively, we may not be able to attract a significant number of new customers and our existing customer base could decrease, either or both of which could have an adverse impact on our results of operations.suffer.

We may lose business if cigarettemanufacturers or other manufacturers decidelarge retail customers convert to engage in direct distribution of their products.

In the past, certain large manufacturers and customers have elected to engage in direct distribution or third party distribution of their products and eliminate wholesale distributors such as Core-Mark. If other manufacturers or retail customers make similar decisionselections in the future, our revenues and profits would be adversely affected and there can be no assurance that we will be able to take actionmitigate such losses.

Our business is sensitive to compensate for such losses.fuel prices and related transportation costs, which could adversely affect our business.

Our operating results are sensitive to, and may be adversely affected by, unexpected increases in fuel or other transportation-related costs, including costs from the use of third party carriers, temporary staff and overtime. Historically, we have been able to pass on a substantial portion of increases in our own fuel or other transportation costs to our customers in the form of fuel or delivery surcharges, but our ability to continue to pass through these increases, is not assured. If we are unable to continue to pass on fuel and transportation-related cost increases to our customers or do not realize the benefits we expect from converting a large percentage of our trucks to operate on natural gas, our operating results could be materially and adversely affected.

Cigarette and consumable goods distribution is a low-margin business sensitive to economic conditions.inflation and deflation.

We derive most of our revenues from the distribution of cigarettes, other tobacco products, candy, snacks, fast food, groceries, fresh products, dairy, non-alcoholic beverages, general merchandise and health and beauty care products. Our industry is characterized by a high volume of sales with relatively low profit margins. Our food/non-food sales are at prices that aregenerally priced based on the manufacturer's cost of the product plus a percentage markup. As a result, our profit levels may be negatively impacted during periods of cost deflation or stagnation for these products, even though our gross profit as a percentage of the price of goods sold may remain relatively constant. Alternatively,In addition, periods of product cost inflation may also have a negative impact on our gross profit margins and earnings with respect to sales of cigarettes. Grosscigarettes because gross profit on cigarette sales are generally fixed on a cents per carton basis. Therefore, as cigarette prices

increase, gross profit generally decreases as a percentpercentage of sales. In addition, if the cost of the cigarettes that we purchase increases due to manufacturer price increases, reduced or eliminated manufacturer discounts and incentive programs or increases in applicable excise tax rates, our inventory carrying costs and accounts receivable could rise. To the extent that we are unable to passrise, placing pressure on product cost increases to our customers, our profit margins and earnings could be negatively impacted.working capital requirements.

We rely on funding from manufacturer discount and incentive programs and cigarette excise stamping allowances;allowances, and any material changes in these programs could adversely affect our results of operations.

We receive payments from the manufacturers ofon the products we distribute for allowances, discounts, volume rebates and other merchandising and incentive programs. These payments are a substantial benefit to us. The amount and timing of these payments are affected by changes in the programs by the manufacturers, our ability to sell specified volumes of a particular product, attaining specified levels of purchases by our customers and the duration of carrying a specified product. In addition, we receive discounts from statescertain taxing jurisdictions in connection with the purchasecollection of excise stamps for cigarettes.taxes. If the manufacturers or statestaxing jurisdictions change or discontinue these programs or change the timing of payments, or if we are unable to maintain the volume of our sales required by such programs, our results of operations could be negatively affected.

We depend on relatively few suppliers for a large portion of our products, and any interruptions in the supply of the products that we distribute could adversely affect our results of operations.

We obtain the products we distribute from third party suppliers. At December 31, 2010,2013, we had approximately 4,4004,700 vendors, and during 20102013 we purchased approximately 62%64% of our products from our top 20 suppliers, with our top two suppliers, Philip Morris USA, Inc. and R. J.R.J. Reynolds Tobacco Company, representing approximately 28% and 13%14% of our purchases, respectively. We do not have any long-term contracts with our suppliers committing them to provide products to us. Our suppliers may not provide the products we distribute in the quantities we request on favorable terms, or at all. We are also subject to delays caused by interruption in production due to conditions outside our control, such as job actionsslow-downs or strikes by employees of suppliers, inclement weather, transportation

interruptions, regulatory requirements and natural disasters or other catastrophic events.disasters. Our inability to obtain adequate supplies of the products we distribute could cause us to fail to meet our obligations to our customers and reduce the volume of our sales and profitability.

SomeOur ability to operate effectively could be impaired by the risks and costs associated with expansion activities.

Market share growth is one of our distribution centers are dependentkey company initiatives. To accomplish this growth we have focused on strategic acquisitions and securing large regional and national customers as key elements of success. Any significant expansion activity comes with inherent risks. Acquisitions may entail various risks such as identifying suitable candidates, realizing acceptable rates of return on the investment, identifying potential liabilities, obtaining adequate financing, negotiating acceptable terms and conditions, and successfully integrating operations and converting systems post acquisition. Integrating a few relatively large customers,new customer has similar risks of realizing acceptable returns on invested working capital, negotiating acceptable pricing and service levels, while managing resources and business interruptions as we integrate the new business into our failurecurrent infrastructure. We may realize higher costs or lower margins than originally anticipated and may experience disruption to maintain our relationships with these customers could substantially harm ourbase business, and prospects.

Some of our distribution centers are dependent on relationships with a single customermay not realize the anticipated benefits or a few customers, and we expect our reliance on these relationshipssavings from expansion activities to continue for the foreseeable future. Any terminationextent or non-renewal of customer relationships could severely and adversely affectin the revenues generated by certain of our distribution centers. Any future termination, non-renewal or reduction in services that we provide to these select customers would cause our revenues to decline and our operating results to suffer.time frame expected.

We may be subject to product liability claims and counterfeit product claims which could materially adversely affect our business, and our operations could be subject to disruptions asbusiness.

As a result of manufacturer recalls of products.

Core-Mark, as with other distributorsdistributor of food and consumer products, faceswe face the risk of exposure to product liability claims in the event that the use of productsa product sold by us causes injury or illness. With respect to product liability claims, we believeIn addition, certain products that we have sufficient liability insurance coverage and indemnities from manufacturers. However, product liability insurance may not continue to be available at a reasonable cost, or, if available, may not be adequate to cover all of our liabilities. We generally seek contractual indemnification and insurance coverage from parties supplying the products we distribute but this indemnification or insurance coverage is limited, as a practical matter, to the creditworthiness of the indemnifying party and the insured limits of any insurance provided by suppliers. Some of our local suppliers are relatively small companies with limited financial resources. If we do not have adequate insurance, if contractual indemnification is not available or if a party cannot fulfill its indemnification obligation, product liability relating to defective products could materially adversely impact our results of operations.

In addition, we may be requiredsubject to manage a recall of products on behalf of a manufacturer. Managing a recall could disrupt our operations as we might be required to devote substantial resources toward implementing the recall, which could materially adversely affect our ability to provide quality service to our customers.

Adverse publicity or lack of confidence in our products could adversely affect reputation and reduce earnings.