UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

(Mark One)

☑ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 20202023

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____ to _____

Commission file number 000-54691

PHILLIPS EDISON & COMPANY, INC.

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | |

| Maryland | | 27-1106076 |

(State or other jurisdiction of

incorporation or organization) | | (I.R.S. Employer

Identification No.) |

| | | | |

| 11501 Northlake Drive, Cincinnati, Ohio | | 45249 |

| (Address of principal executive offices) | | (Zip Code) |

(513) 554-1110

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

NoneCommon stock, par value $0.01 per share | | NonePECO | | NoneNasdaq Global Select Market |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.01 par value per shareNone

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐☑ No ☑☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

| Large accelerated filer | ☐☑

| Accelerated filer | ☐

|

| | | |

| Non-accelerated filer | ☑☐ | Smaller reporting company | ☐

|

| | | |

| | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in rule 12b-2 of the Act). Yes ☐ No ☑

There is no established publicAs of June 30, 2023, the aggregate market for the registrant’s shares of common stock. On May 6, 2020, the Board of Directors of the registrant approved an estimated value per share of the registrant’s common stock held by non-affiliates of $8.75the registrant was $4.0 billion, based substantiallyon a closing price of $34.08 as reported on the estimated market value of its portfolio of real estate properties as of March 31, 2020. Prior to May 6, 2020, the estimated value per share was $11.10. For a full description of the methodologies used to establish the estimated value per share, see “Part II, Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters, and Issuer Purchases of Equity Securities - Market Information” of this filing on Form 10-K. Nasdaq Global Select Market.

As of June 30, 2020, the last business day of the Registrant’s most recently completed second fiscal quarter,February 5, 2024, there were approximately 289.8 million shares of common stock held by non-affiliates.

As of March 1, 2021, there were approximately 280.7122.2 million outstanding shares of common stock of the registrant.

Documents Incorporated by Reference: NoneCertain required information will be included in our definitive proxy statement to be filed with the SEC within 120 days after December 31, 2023 in connection with the Company's 2024 Annual Meeting of Stockholders, and is hereby incorporated by reference into Part III of this Form 10-K.

PHILLIPS EDISON & COMPANY, INC.

FORM 10-K

TABLE OF CONTENTS

| | | | | | | | | | | |

| TABLE OF CONTENTS |

| | PART I | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | | |

| | PART II | |

| | | |

| | | |

| | [RESERVED] | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | | |

| | PART III | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | | |

| | PART IV | |

| | | |

| | | |

| | | |

| | | | |

| |

| | | | | | | | | | | |

PHILLIPS EDISON & COMPANY DECEMBER 31, 2023 FORM 10-K | | | 1 |

Cautionary Note Regarding Forward-Looking Statements

Certain statements contained in this Annual Report on Form 10-K of Phillips Edison & Company, Inc. (“we,” the “Company,” “our,” or “us”) other than historical facts may be considered forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and the Private Securities Litigation Reform Act of 1995 (collectively with the Securities Act and the Exchange Act, the “Acts”). These forward-looking statements are based on current expectations, estimates, and projections about the industry and markets in which we operate, and beliefs of, and assumptions made by, management of our company and involve uncertainties that could significantly affect our financial results. We intend for all such forward-looking statements to be covered by the applicable safe harbor provisions for forward-looking statements contained in the Acts. Such forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “can,” “expect,” “intend,” “anticipate,” “estimate,” “believe,” “continue,” “possible,” “initiatives,” “focus,” “seek,” “objective,” “goal,” “strategy,” “plan,” “potential,” “potentially,” “preparing,” “projected,” “future,” “long-term,” “once,” “should,” “could,” “would,” “might,” “uncertainty,” or other similar words. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date this report is filed with the U.S. Securities and Exchange Commission.Commission (“SEC”). Such statements include, but are not limited to,to: (a) statements about our focus, plans, strategies, initiatives, and prospects; (b) statements about the COVID-19 pandemic, including its durationour underwritten incremental yields; and potential or expected impact on our tenants, our business, and our estimated value per share; (c) statements about a reverse stock split, our distributions, share repurchase program, and dividend reinvestment program; and (d) statements about our future results of operations, capital expenditures, and liquidity. Such statements are subject to known and unknown risks and uncertainties, which could cause actual results to differ materially from those projected or anticipated, including, without limitation: (i) changes in national, regional, or local economic climates; (ii) local market conditions, including an oversupply of space in, or a reduction in demand for, properties similar to those in our portfolio; (iii) vacancies, changes in market rental rates, and the need to periodically repair, renovate, and re-let space; (iv) changes in interest rates and the availability of permanent mortgage financing; (v) competition from other available propertiesshopping centers and the attractiveness of properties in our portfolio to our tenants; (vi)(v) the financial stability of our tenants, including, the ability of tenants to pay rent; (vii) changes in tax, real estate, environmental, and zoning laws; (viii) the concentration of our portfolio in a limited number of industries, geographies, or investments; (ix) the effects of the COVID-19 pandemic, including on the demand for consumer goods and services and levels of consumer confidence in the safety of visiting shopping centers as a result of the COVID-19 pandemic; (x) the measures taken by federal, state, and local government agencies and tenants in response to the COVID-19 pandemic, including mandatory business shutdowns, “stay-at-home” orders and social distancing guidelines; (xi) the impact of the COVID-19 pandemic on our tenants andwithout limitation, their ability to pay rent on time or at all, or to renew their leases and, in the case of non-renewal, our ability to re-lease the space at the same or more favorable terms or at all; (xii) the length and severity of the COVID-19 pandemic in the United States; (xiii) the pace of recovery following the COVID-19 pandemic given the current severe economic contraction and increase in unemployment rates; (xiv) our ability to implement cost containment strategies; (xv) our and our tenants’ ability to obtain loans under government programs; (xvi)rent; (vi) our ability to pay down, refinance, restructure, or extend our indebtedness as it becomes due; (vii) increases in our borrowing costs as a result of changes in interest rates and other factors; (viii) potential liability for environmental matters; (ix) damage to our properties from catastrophic weather and other natural events, and the physical effects of climate change; (x) our ability and willingness to maintain our qualification as a real estate investment trust (“REIT”) in light of economic, market, legal, tax, and other considerations; (xi) changes in tax, real estate, environmental, and zoning laws; (xii) information technology security breaches; (xiii) our corporate responsibility initiatives; (xiv) loss of key executives; (xv) the concentration of our portfolio in a limited number of industries, geographies, or investments; (xvi) the economic, political, and social impact of, and uncertainty relating to, pandemics or other health crises; (xvii) our ability to re-lease our properties on the same or better terms, or at all, in the event of non-renewal or in the event we exercise our right to replace an existing tenant; (xviii) the loss or bankruptcy of our tenants; (xix) to the extent we wereare seeking to dispose of properties, in the near term, significantly greater uncertainty regarding our ability to do so at attractive prices or at all; (xviii)(xx) the impact of the COVID-19 pandemicinflation on us and on our business, results of operations, financial condition,tenants; and liquidity; (xix) supply chain disruptions due to the COVID-19 pandemic; and (xx)(xxi) any of the other risks included in this Annual Report on Form 10-K, including those set forth in Part“Part I, Item 1A. Risk Factors.Factors”. Therefore, such statements are not intended to be a guarantee of our performance in future periods.

Except as required by law, we do not undertake any obligation to update or revise any forward-looking statements contained in this Form 10-K.

| | | | | | | | | | | |

PHILLIPS EDISON & COMPANY DECEMBER 31, 2023 FORM 10-K | | | 2 |

ITEM 1. BUSINESS

All references to “Notes” throughout this Annual Report on Form 10-K refer to the footnotes to the consolidated financial statements in “Part II, Item 8. Financial Statements and Supplementary Data”.

Overview

OVERVIEW—Phillips Edison & Company, Inc. (“we,” the “Company,” “PECO,” “our,” or “us”) is an internally-managed, a real estate investment trust (“REIT”) thatfounded in 1991, is one of the nation’s largest owners and operators of omni-channel grocery-anchored shopping centers. Additionally, we operate ana third-party investment management business providing property management and advisory services to third-party owned grocery-anchoredtwo unconsolidated institutional joint ventures, in which we have partial ownership interests, and one private fund (collectively, the “Managed Funds”). The majority of our revenues are lease revenues derived from our real estate.estate investments. Our portfolio primarily consists of well-occupied, grocery-anchored neighborhood and community shopping centers havinganchored by the #1 or #2 grocer tenants by sales within their respective formats by trade area. As of December 31, 2023, our portfolio was 97.4% leased. Our tenants, who we refer to as “Neighbors,” are a mix of national, regional, and local retailers providingthat primarily provide necessity-based goods and services. OurWe believe our locations are in fundamentally strong demographic markets throughout the United States provideStates. Our brick and mortar assets positively contribute to our Neighbors’ omni-channel retailers with a solution forstrategies and act as the last mile of delivery.delivery solution.

We were formed as a Maryland corporation in October 2009 and have elected to be taxed as a REIT for U.S. federal income tax purposes. Substantially all of our business is conducted through Phillips Edison Grocery Center Operating Partnership I, L.P. (“Operating(the “Operating Partnership”), a Delaware limited partnership formed in December 2009. We are a limited partner of the Operating Partnership, and our wholly-owned subsidiary, Phillips Edison Grocery Center OP GP I LLC, is the sole general partner of the Operating Partnership. The majority

As of our revenues are lease revenues derived from ourDecember 31, 2023, we wholly-owned 281 shopping centers. Additionally, we owned real estate investments. In October 2017, we internalized our management structure through the acquisition of Phillips Edison Limited Partnership (“PELP”).

In November 2018, we completed a merger (the “Merger”) with Phillips Edison Grocery Center REIT II, Inc. (“REIT II”), a public non-traded REIT that was advised and managed by us (see Note 4). In the same month, we also contributed or sold 17 properties14% interest in the formation of Grocery Retail Partners I LLC (“GRP I”), a joint venture with Northwestern Mutual Life Insurance Company, (“Northwestern Mutual”); see Note 7 for more detail.

On October 31, 2019, we completed a merger with Phillips Edison Grocery Center REIT III, Inc. (“REIT III”), a public non-traded REIT that was advised and managed by us, in a transaction valued at approximately $71 million. This resulted in the acquisition of three properties, as well as a 10% equity interest in Grocery Retail Partners II LLC (“GRP II”), a joint venture with Northwestern Mutual that owns three properties. On October 1, 2020, GRP I acquired GRP II, and our ownership in the combined entity was adjusted to approximately 14%; see Notes 5 and 7 for more detail.

As of December 31, 2020, we wholly-owned 283 real estate properties. Additionally, wewhich owned 20 shopping centers. We also owned a 20% equity interest in Necessity Retail Partners (“NRP”), a joint venture with an affiliate of TPG Real Estate that owned five properties, and a 14% interestEstate. In May 2022, we sold the final property in GRP I, which owned 20 properties.our NRP joint venture. In total, our managed portfolio of wholly-owned propertiesshopping centers and those owned through our unconsolidated joint ventures comprisesventure comprised approximately 34.4 million square feet located in 31 states.

Business Objectives and Strategies

BUSINESS OBJECTIVES AND STRATEGIES—Our business objective is to own, operate, and manage well-occupied grocery-anchored shopping centers which generatein order to deliver long-term growth and value creation to all stakeholders while acting as a responsible corporate citizen. We seek to achieve this objective by generating cash flows, income growth, and capital appreciation to create value for and continue paying distributions to, our stockholders. We seek to achieve this objectivestockholders through our focus on core operations; strategic growthdifferentiated and portfolio management; andfocused strategy, responsible balance sheet management. Altogether, ourmanagement, and integrated operating platform. Our goal is to providecreate great grocery-anchored shopping experiences and improve our communities, one center at a time.

In response to the COVID-19 pandemicDifferentiated and the resultingFocused Strategy—We believe our differentiated strategy drives strong financial and operational performance and future growth, including showing resiliency during economic downturn, we implemented various initiatives to mitigate the negative impactdown cycles.

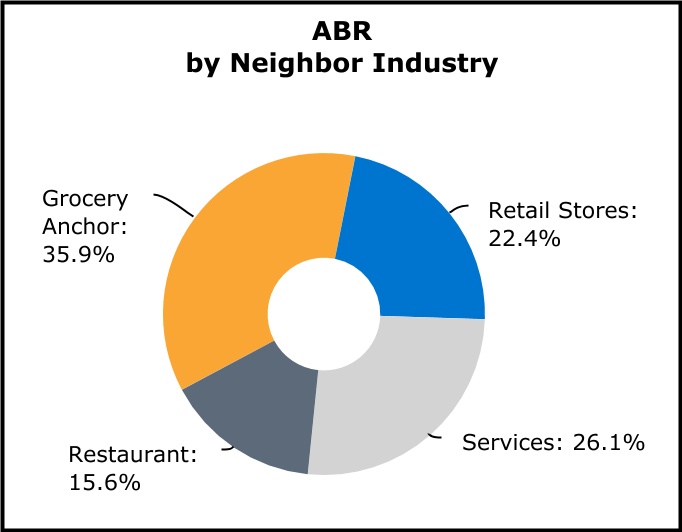

•Omni-Channel Grocery-Anchored Neighborhood Shopping Centers—We focus on our operations. Although we continue to address challenges brought aboutinvesting in omni-channel shopping centers anchored by the pandemic,#1 or #2 grocer by sales within their respective trade area. As of December 31, 2023, for our overall business objectiveswholly-owned shopping centers, 85% of our annualized base rent (“ABR”) was generated from shopping centers anchored by such grocers. Grocery-anchored shopping centers generally have strong foot traffic leading to high demand for leasing Neighbor spaces, which enhances our ability to increase lease revenue. These centers provide an attractive last-mile solution to residents of our communities by providing “Buy Online, Pick-Up in Store”, curbside pick-up, and strategies remain principally unchanged.grocery delivery options. We target investments with attractive going-in yields and growth potential in markets with demographic profiles that support necessity-based retail concepts.

Focus on Core Operations•Neighbor-Base—As of December 31, 2023, approximately 70% of our ABR, including the pro rata portion attributable to properties owned through our unconsolidated joint venture, is generated from Neighbors providing necessity-based goods and services. We believe our focus on necessity-based goods and services retailers limits our operating fundamentals will continueexposure to provide stabilitydistressed retailers and ultimately generate growth in our portfolioallows us to demonstrate resiliency during times of real estate and optimize returns for our stockholders.economic down cycles.

•Property Management Services—Targeted Portfolio—We add value by overseeing all aspectsfocus on owning centers in trade areas with favorable demographics that align with those of operations at our properties. Our property managers maintain a local presenceleading grocers. Further, we seek to invest in ordersmall format centers where leasing activity is concentrated in smaller tenant spaces and limits exposure to effectively manage costs while maintaining a pleasant, clean, and safe environment where retailers can be successful and customers canhigh-risk retailers. We believe that smaller centers provide higher growth potential because they enjoy a great shopping experience.positive leasing dynamic as: (i) we believe retailer demand is strongest for inline space, which contains less than 10,000 square feet of gross leasable area; (ii) there is less exposure to big box retailers, which we believe have higher risk because they require larger capital expenditures and have fewer leasing opportunities; and (iii) smaller centers typically have lower capital expenditures. We utilizeintend to grow our centralized accounting, billing,portfolio through targeted acquisitions that align with our differentiated and tax review platform to facilitate our daily operations.focused strategy.

•Leasing—Our national footprintMacroeconomic Trends—We continually monitor the macroeconomic environment to identify trends that are positive for the growth potential of experienced leasing professionals is dedicated toour shopping centers. We believe recent trends such as: (i) creating the optimal merchandising mix at our centers, (ii) increasing occupancy at our centers, (iii) maximizing rental income through capitalizing on below-market rent opportunities by means of increasing rents as leases expire, and (iv) executing leases with contractual rent increases. In responsepopulation shifts to the COVID-19 pandemic,Sun Belt and from urban to suburban communities in certain geographic locations; (ii) the continued presence of hybrid work initiatives; (iii) the importance of last mile delivery; (iv) low supply and lack of new construction coupled with high occupancy; and (v) continued consumer resilience will create additional leasing demand and growth opportunities for our capital expenditures were prioritized in part to support new leasing activity.shopping centers.

StrategicBalance Sheet Management Positioned for External Growth and Portfolio Management—Our goalstrategy is to identify growth opportunities withingrow our portfolio of properties as well through the use ofby pursuing acquisitions in a disciplined manner, while maintaining an attractive leverage profile and flexible balance sheet to preserve our existing management resources and knowledge.

•Development and Redevelopment—Our team of seasoned professionals identifies opportunities to unlock additional value at our properties through investments in our development and redevelopment program. Our strategies include outparcel development, footprint reconfiguration, anchor repositioning, and anchor expansion, among others. While our capital expenditures were prioritized in 2020 to support new leasing activity, we continue to look for development and redevelopment opportunities to increase the overall yield and value of our properties, which will allow us to generate higher returns for our stockholders while creating great grocery-anchored shopping center experiences.

| | | | | | | | | | | |

PHILLIPS EDISON & COMPANY DECEMBER 31, 2023 FORM 10-K | | | 3 |

•Investment Management—Our investment management business provides comprehensive real estate, asset management, and accounting and support services to third-party funds. Although the uncertainty surrounding the financial and real estate markets as a result of the COVID-19 pandemic has slowed the pace of joint venture and other growth opportunities, we believe that our investment management business will expand our platform and relationships while preserving our balance sheet and will afford us the opportunity to consider acquisitions in the future similar to what we have done historically.

Responsible Balance Sheet Management—Our strategy is to improve and monitor our leverage ratios and debt maturities and dispose of certain shopping centers in order to maximize our potential future valuation in the public equity markets.grade rating. We believe this is a critical part of maintaining access to multiple forms of capital, including common stock, unsecured debt, bank debt, and mortgage debt, to maximize availability and minimize our overall cost of capital.

•Disposition Program—Funding External Growth—We are actively evaluatinghave identified a target market of approximately 5,800 centers across the United States and believe we have a long runway for external growth. We believe our portfolio for opportunitieseffective shelf registration statement and At-the-Market offering (“ATM”) program allow us to disposeaccess equity and debt capital, further enhancing our financial flexibility and external growth potential. We believe our investment grade balance sheet and our available liquidity of assets that no longer meet$606.6 million under our growth and investment objectives due to stabilization or perceived future risk. These dispositionssenior unsecured revolving credit facility provide us with the financial capacity to pursue external growth initiatives in an accretive and prudently capitalized manner. Additionally, our investment management platform enables us to source and manage incremental sources of capital to fund acquisitions, fund redevelopment opportunities at owned properties, and reduce our leverage.through unconsolidated joint ventures, which provide us incremental fee revenue opportunities.

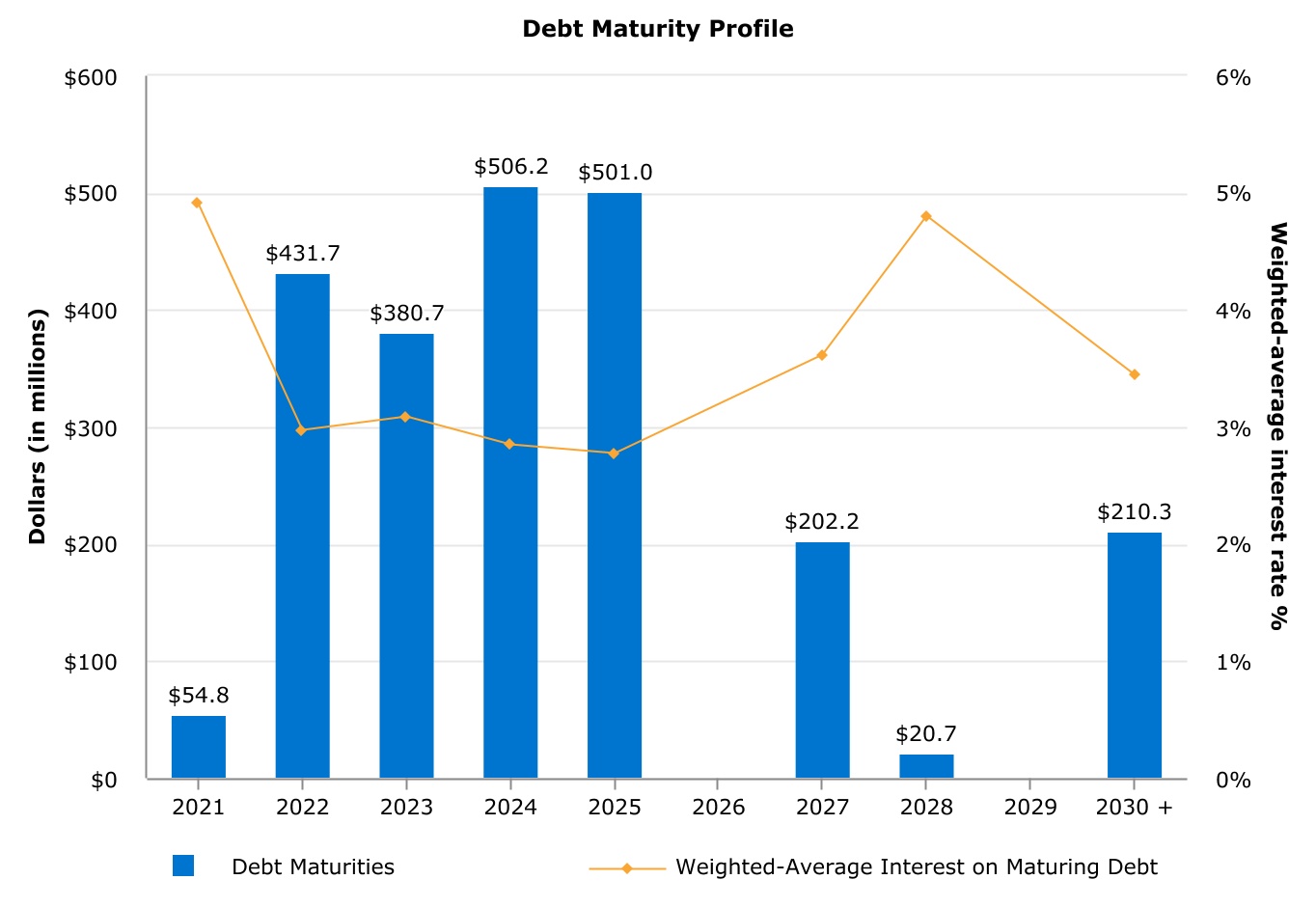

•Debt Maturity Profile—Profile—We believe we have prioritized maintainingmaintained an appropriately staggered debt maturity profile with no meaningful maturities in 2024, which will position us for long-term growth. Our outstanding debt obligations are composed primarily of (i) unsecured debt, including term loans, senior notes, and a revolving credit facility, and (ii) secured mortgage debt. Certain

•Investment Grade Ratings—Our current investment grade ratings are Baa3 (Outlook: Stable) with Moody’s Investors Services and BBB- (Outlook: Positive) with S&P Global Ratings.

Internal Growth Through Our Integrated Operating Platform—We believe our internally-staffed, vertically-integrated operating platform to lease and manage omni-channel grocery-anchored neighborhood shopping centers will continue to provide stability and generate growth in our existing portfolio, optimizing returns for our stockholders.

•Leasing—Our national footprint of experienced and Locally Smart™ leasing professionals is dedicated to increasing net operating income (“NOI”) at our centers by: (i) maximizing rental rates while improving the credit profile of our upcoming unsecured debt agreementsrental revenue; (ii) attracting high-quality retailers while improving the merchandising mix; (iii) capitalizing on below-market rent opportunities by increasing rents as leases expire; (iv) executing leases with contractual rent increases; and (v) increasing occupancy.

•Property Management Services—We believe we add value by overseeing all aspects of operations at our properties. Our Locally Smart™ property managers effectively manage costs while maintaining a pleasant, clean, and safe environment where retailers can be successful and customers can enjoy a great shopping experience. Further, we provide our Neighbors with responsive customer service and marketing tools, as well as other sophisticated solutions, such as a centralized accounting, billing, and tax review platform to facilitate our daily operations.

•Development and Redevelopment—Our team of seasoned professionals identify opportunities to unlock additional value at our properties through investments in our outparcel and redevelopment program. Our strategies include optionsoutparcel development, footprint reconfiguration, anchor repositioning, and anchor expansion, among others. These projects create opportunities to extend their maturities,increase the overall yield and value of our properties, which provide flexibility in managing refinancing through changing market conditions.we believe will allow us to deliver long-term growth and value creation to all stakeholders while creating great grocery-anchored shopping center experiences.

Competition

COMPETITION—Our business is inherently competitive. We believe that the competition is highly fragmented. We are subject to significantconsiderable competition in both seeking real estate investmentsshopping centers to acquire and tenants (whom we refer to as a “Neighbor” orattracting and retaining Neighbors in our “Neighbors”).existing shopping centers. We compete with many third parties engaged in real estate investment activities includinginstitutional investors and other REITs, specialty finance companies, savingsas well as local, regional, and loan associations, banks, insurance companies, mutual funds, institutional investors, investment banking firms, hedge funds,national owner-operators for property acquisitions. We compete with other properties including malls, lifestyle centers, power centers, community centers, neighborhood centers, free-standing retail, and other persons. Somemain street retail in attracting new Neighbors and retaining existing Neighbors when their leases expire. The competition for Neighbors varies depending on the characteristics of these competitors, including larger REITs, have greater financial resources than we doeach property.

We believe that the principal competitive factors in attracting and may potentially enjoy competitive advantages that primarily result from increased accessretaining Neighbors are the quality of the grocery anchor, location, trade area demographics, tenant mix, physical condition of the shopping center, and occupancy cost. These factors combine to capital, lower costdetermine the level of capital,occupancy and enhanced operating efficiencies. In addition to these entities, we also face competition from smaller landlords and companies at the local level in seeking Neighbors to occupy our shopping centers. This further increases the number of competitors we have and the type of competitionrental rates that we faceare able to achieve at our properties. We believe that the quality of our omni-channel grocery-anchored shopping centers enables us to compete effectively for Neighbors. We believe that we maintain a competitive position in seekingthe acquisition market due to execute on our business objectivestrack record and strategies.positive reputation.

Segment Data

SEGMENT DATA—Our principal business is the ownership and operation of community and neighborhood shopping centers. We do not distinguish our principal business or group our operations by geography or size for purposes of measuring performance. Accordingly, we have presented our results as a single reportable segment.

Government Regulation

COMPLIANCE WITH GOVERNMENT REGULATION—Compliance with various governmental regulations has an impact on our business, including our capital expenditures, earnings, and competitive position. The impact of these governmental regulations can be material to our business. We incur costs to monitor and take action to comply with governmental regulations that are applicable to our business, which include, among others: federal securities laws and regulations; REIT and other tax laws and regulations; environmental and health and safety laws and regulations; local zoning, usage, and other regulations relating to real property; and the Americans with Disabilities Act of 1990, as amended (“ADA”). See “Part I, Item“Item 1A. Risk Factors” of this filing on Form 10-Kbelow for a discussion of material risks to us (including those, to the extent material to our competitive position, relating to governmental regulations) and see “Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” of this filing on Form 10-K, together with our consolidated financial statements and accompanying footnotes, for a discussion of material information relevant to an assessment of our financial condition and results of operations (including, to the extent material, the effects that compliance with governmental regulations may have upon our capital expenditures and earnings).

Human Capital

As of December 31, 2020,2023, we are not aware of any environmental conditions or material costs of complying with environmental or other government regulations that would have a material adverse effect on our overall business. However, it

| | | | | | | | | | | |

PHILLIPS EDISON & COMPANY DECEMBER 31, 2023 FORM 10-K | | | 4 |

is possible that we are not aware of, or may become subject to potential environmental liabilities or material costs of complying with government regulations due to changes in requirements or otherwise that could be material to our business.

CORPORATE RESPONSIBILITY AND SUSTAINABILITY—Our corporate responsibility and sustainability program (“CRSP”), which we also refer to as our “PECO-ECO Promise™”, is designed to align with our corporate mission and strategic initiatives. With a mission of “creating great omni-channel grocery-anchored shopping center experiences and improving our communities, one shopping center at a time”, we strive to have a positive impact on all our stakeholders. Our CRSP is overseen by our full Board of Directors (the “Board”) reflecting our comprehensive approach to strong governance. In addition, we have a dedicated director liaison, Ms. Silfen, providing oversight to our PECO-ECO Team members based on her significant experience in energy innovation and sustainability. Our PECO-ECO Team is led by our General Counsel, who provides regular updates to the full Board on our CRSP.

Our PECO-ECO Promise™ is based on four pillars that are guided by our mission and our goal of driving long-term value creation for our stakeholders: our People and Culture, Environmental Stewardship, Community, and Oversight and Ethics:

PEOPLE AND CULTURE—At PECO, our associates are our greatest asset. We believe in fostering a work environment where every team member feels valued, respected, and empowered. To achieve this, our key areas of focus include:

•Engagement and Satisfaction: We empower our associates through personalized coaching and annual stock awards, intended to foster a resilient culture that has earned PECO the title of a Top Place to Work for seven consecutive years by Cincinnati Enquirer. By granting 100% of eligible associates service-based restricted stock units in PECO, we empower and encourage our associates to think and operate like owners, which we believe drives better decision making and strengthens our culture.

•Learning and Development: We are committed to continuous learning and the professional development of our associates. Established in 2007, PECO University is a hub for learning and development of our associates, encompassing our online learning platform, PECO U online, leadership development, mentoring programs, and more. PECO’s commitment to continuous learning includes an annual talent management process, workshops on development goal plans, and the PECO Mentor Match program, an internal mentoring program.

•Health and Well-Being: We strive to create a workplace that prioritizes the well-being of our associates. Our “Beyond Benefits” wellness program is integral to our Company’s culture and is designed to address our associates’ emotional, physical, and financial well-being. The program includes sponsoring wellness activities and challenges designed to improve the overall health of our associates.

•Inclusion and Belonging: At PECO, fostering connection and inclusivity is a core commitment of our culture. We established three associate-led resource groups, PECO Multicultural Opportunities, Resources & Education (“PECO MORE”), PECO Networking Opportunities for Women (“PECO NOW”), and PECO Connect to help further diversity, inclusion, collaboration, and communication throughout the Company.

As of December 31, 2023, we had approximately 300290 associates located in 20 states across the country, with concentrations in our corporate offices in Cincinnati, Ohio; Park City, Utah; and Atlanta, Georgia. Approximately 55%51% of our workforce is female and 45%49% is male. Our senior leadership team is 19%18% female and 81%82% male, while manager roles and above are approximately 40%39% female and 60%61% male. For the year ended December 31, 2020,2023, our overall turnover rate was 17%8%, with 6% voluntary turnover, beingcompared to our previous three year overall turnover average of 13%, with 10%. voluntary turnover.

Our human capital objectives include, as applicable, identifying, recruiting, retaining, developing, incentivizing, and integrating our existing and prospective employees. We provide associates with competitive salaries, bonuses, incentives, and opportunities for equity ownership. One unique aspectENVIRONMENTAL STEWARDSHIP—Environmental stewardship is an important component of our compensation philosophycommitment to sustainability, encapsulated in our PECO-ECO Promise™. We recognize that sustainable practices are not only beneficial for the environment but also important for our business success and contributing to the well-being of the communities we operate in. A key component of our sustainable practices is that each associatefocused on improving operational efficiencies and resource reductions within our portfolio. Our initiatives include calculating our Scope 1 and Scope 2 GHG emissions, participating in the organization, regardlessGlobal Real Estate Sustainability Benchmark ("GRESB") Real Estate Assessment, pursuing energy efficiency, developing on-site solar projects, and installing electric vehicle (“EV”) charging stations. We are also focused on attaining sustainable property certifications, implementing water conservation measures, and managing waste effectively.

We are proud to highlight the milestones below, as of level or tenure, has the opportunity for equity grants on an annual basis. During the year ended December 31, 2020,2023, in our ongoing sustainability journey:

•Exterior Lighting: Completed the retrofit of 98.1% of our wholly-owned portfolio to LED parking lot lighting, moving closer to our goal of retrofitting 100% of eligible associates received grantsour portfolio by 2025.

•Renewable Energy: Installed 14 solar array systems to date.

•Water Conservation: Conserved over 62 million gallons of service-based restricted stock unitswater in 2023 (through September) through the Company. Upon vesting, associates will receive actual sharesimplementation of common stock, which we believe encouragesxeriscaping and our employees to think like owners“Smart Water Control Program”, generating cost savings of the Company.over $200,000.

We recognize the importance of the health, safety, and environmental well-being•EV Charging Stations: Installed EV chargers at 17.7% of our employees,eligible properties to date.

•Waste Management: Achieved a waste diversion rate of approximately 26.0% at properties with a landlord-controlled waste program.

•Building Certifications: Secured WELL Health-Safety recertification for our company headquarters in Cincinnati, Ohio and are committedInstitute of Real Estate Management Certified Sustainable Property Certifications at 163 properties in 2023, bringing the total number of properties with certifications to providing172.

COMMUNITY—Through our mission of “creating great omni-channel grocery-anchored shopping center experiences and maintainingimproving our communities, one shopping center at a healthy work environment.time”, we strive to actively engage with our Neighbors and the local communities that we serve. Our 2020 all-associate engagement survey, which had an 89% participation rate, showed 84% overall engagement,focus is on being Locally Smart™ and 91%understanding the unique needs of associates reported they felt proud to tell people where they work, compared to an 80% global average as reported by Qualtrics XM, while 93% of associates felt they could be successful at the Company. In 2020, we were named a top place to work by the Cincinnati Enquirer for the fourth year in a row. We also won special recognition each of the past four years, including being recognized for “clued-in senior management” in 2020.

Our strong culture andcommunity. This commitment to inclusion is reinforced by two associate-led business resource groups: PECO MORE (Multicultural Opportunities, Resources & Education),our communities extends to its physical spaces, with initiatives like Front Row to Go® providing convenient curbside pickup for our local shoppers, and PECO NOW (Networking Opportunitiesa retailer mix that offers storefront windows and drive-through stores for Women). PECO MORE isadditional convenience for local shoppers.

| | | | | | | | | | | |

PHILLIPS EDISON & COMPANY DECEMBER 31, 2023 FORM 10-K | | | 5 |

dedicated

Our community commitment is also evident in our initiatives like our PECO Community Partnership, an award-winning, associate-led program that encourages community involvement and connects our associates to furthering diversitycauses they care about. In 2023, PECO Community Partnership sponsored 15 community service events and inclusion withincontributed over 440 service hours, including a volunteer day in partnership with Keep Cincinnati Beautiful at Green Man Park where 69 associates participated in a park cleanup and revitalization project.

PECO's partnership with communities also extends to disaster relief efforts, exemplified by our Incident Response Team. This team provides support to Neighbors and communities impacted by disasters, such as Hurricane Idalia in August 2023, as part of PECO's commitment to being there for its Neighbors and communities during challenging times.

OVERSIGHT AND ETHICS—Our governance framework guides our decision-making and accountability. Supported by an experienced executive management team, we maintain a robust system of corporate governance policies, designed to foster an ethical culture committed to the Company, the communities thatPECO-ECO Promise™ and to driving our goal of creating long-term value.

We believe our corporate governance structure closely aligns our interests with those of our stockholders. Notable features include: (i) each of our directors is subject to election annually, and our charter prevents us from classifying our Board unless we serve, and the commercial real estate industry. In June 2020, PECO MORE hosted “BEGIN” conversations, a series of 23 small group discussions, attended by approximately 50%receive prior stockholder approval; (ii) we have opted out of the workforce, designedbusiness combination and control share acquisition statutes in the Maryland General Corporation Law; (iii) we do not have a stockholder rights plan; (iv) we have a Stock Ownership Policy that requires each non-associate director, our CEO, and each other named executive officer to “begin” dialogue around diversity, inclusion,own a certain amount of our equity; and equity. PECO MORE’s programming has focused on providing education, raising awareness, and hosting events around Veterans Day,(v) our bylaws provide that our stockholders may alter or replace our bylaws upon the Chinese New Year, Black History Month, Pride Month, and Women’s History Month. PECO NOW’s missionaffirmative vote of a majority of the votes entitled to be cast.

We operate under the oversight of our Board, which is to provide leadership opportunities to women through advocacy, support, scholarship, and development. PECO NOW was recognized for excellencecomprised of nine directors, seven of whom meet the independence criteria set forth by the International CouncilNasdaq Global Select Market (“Nasdaq”) and U.S. Securities and Exchange Commission (“SEC”) rules. Our Audit, Nominating and Governance (“N&G”), and Compensation Committees are comprised solely of Shopping Centers in 2016.

“Always Keep Learning” is oneindependent directors who complete annual self-assessments. Our Board has adopted Corporate Governance Guidelines that, among other things, establish criteria and expectations for our directors, and our N&G Committee has responsibility for annually evaluating our Board and each of its committees. We are cognizant of “overboarding” and none of our core values. Each year, we sponsor an annual meeting that provides associatesdirectors serve on more than two other public company boards. We are compliant with the ability to hear directly from company leadershipNasdaq’s Board Diversity Rule and have three female directors and two directors who are members of underrepresented racial or ethnic minorities.

More information about our performance, goals, and strategy. We host external speakers to facilitate discussions on relevant industry topics, and educational roundtables are led by internal subject-matter experts. This annual learning event provides associates with the information needed to understand how their roles and responsibilities directly impact the Company’s performance and growth. Associates are also kept apprised of company information through town halls conducted throughout the year. While the COVID-19 pandemic impacted many planned learning opportunities in 2020, we focused on providing managers with skills-based training to coach their associates and navigate through tough conversations while addressing virtual team challenges. We look forward to returning to a regular learning cycle in 2021, adapted for the COVID-19 environment, with an inaugural virtual Core Values Week in February 2021.

Our “Beyond Benefits” wellness program focusesCRSP is available on our associates’ emotional, physical,website and financial well-being. Together with an external partner, we offer a full wellness platform providing Health Savings Account incentive contributionsin our Corporate Responsibility Report, which are not incorporated by reference and should not be considered part of this Annual Report on Form 10-K.

INFORMATION ABOUT OUR EXECUTIVE OFFICERS—The following table details information for biometric screening results, preventive care,our executive officers as of December 31, 2023:

| | | | | | | | | | | |

| Name | Age | Title | Joined PECO |

| Jeffrey S. Edison | 63 | Chairman & Chief Executive Officer | Co-Founder |

Devin I. Murphy(1) | 63 | President | 2013 |

Robert F. Myers(1) | 51 | Chief Operating Officer & Executive Vice President | 2003 |

| John P. Caulfield | 43 | Chief Financial Officer, Executive Vice President & Treasurer | 2014 |

| Tanya E. Brady | 56 | General Counsel, Executive Vice President & Secretary | 2013 |

(1)Devin Murphy stepped down as President effective December 31, 2023 and activity-based items such as step counts, nutrition tracking, and workout activity minutes. To keep remote associates engaged during 2020, we held six wellness challenges where individuals and teams could earn incentive dollars for winning competitions that tracked steps, workout activity, and water consumption. Such efforts have facilitated a continued dedication to wellness and preventive care among our associates, and as a result, we were recognized by Healthiest Employers LLC as onebecame Managing Director of the “Healthiest EmployersInvestment Management effective January 1, 2024 through his retirement date of Ohio” in 2020.June 30, 2024. Effective January 1, 2024, Robert Myers became President.

We are also committed to ensuring that the operations at all of our properties and corporate offices are conducted in a manner that safeguards the health and safety of employees, Neighbors, contractors, and members of the public who are either present at, or affected by, operations at these locations. This commitment increased in importance in 2020 due to the unique challenges posed by the COVID-19 pandemic, and we continue to work with all of our stakeholders to mitigate the pandemic’s impact.

In addition to the increased number of activity-based individual and team challenges, we maintained a proactive approach to all aspects of well-being during the COVID-19 pandemic, with a specific focus on mental health, including offering virtual Meditation and Mindfulness sessions throughout the spring and summer of 2020. We also maintained an intranet page with information related to COVID-19, work-from-home tips, and services available to associates, such as multiple free virtual fitness app memberships and a mental health, meditation and mindfulness app. Our communications team sent out regular company-wide emails to keep associates connected with helpful practical information, as well as fun topics such as healthy recipes and photos of our associates’ at-home office spaces and new “co-workers.”

Corporate Headquarters

CORPORATE HEADQUARTERS—Our corporate headquarters, located at 11501 Northlake Drive, Cincinnati, Ohio 45249, is where we conduct a majority of our management, leasing, construction, and investment activities, as well as administrative functions such as accounting and finance. Additionally, we maintain two regional offices located in Atlanta, Georgia and Park City, Utah.

Access to Company Information

ACCESS TO COMPANY INFORMATION—We electronically file our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, Proxy and Information statements, and all amendments to those reports with the U.S. Securities and Exchange Commission (“SEC”).SEC. The SEC maintains an Internetinternet site at www.sec.gov that contains the reports, proxy and information statements, and other information regarding issuers, including ours that are filed electronically.

We make available, free of charge, the Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and all amendments to those reports on our website, www.phillipsedison.com.www.phillipsedison.com. These reports are available as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. Also available on our website are (i) our Corporate Governance Guidelines, (ii) our Code of Business Conduct and Ethics, and (iii) our Whistleblower Policy. In the event of any changes to these documents, revised copies will be made available on our website. We intend to disclose on our website under “Investors - Governance - Governance Overview” any amendment to, or waiver of, any provisions of our Code of Business Conduct and Ethics applicable to the directors and/or officers of the Company that would otherwise be required to be disclosed under the rules of the SEC or Nasdaq. We also disclose, and intend to disclose, on our website under “Investors” material nonpublic information to comply with our disclosure obligations under Regulation FD. The contents of our website are not incorporated by reference.

| | | | | | | | | | | |

PHILLIPS EDISON & COMPANY DECEMBER 31, 2023 FORM 10-K | | | 6 |

ITEM 1A. RISK FACTORS

You should specifically consider the following material risks in addition to the other information contained in this Annual Report on Form 10-K. The occurrence of any of the following risks might have a material adverse effect on our business, operating results, financial condition, and cash flows. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may impair our business, operating results, financial condition, and cash flows.

Summary of Risk Factors

An investment in our common stock involves risks. You should carefully consider the risks summarized here and described more fully below.

Risks Related to Our StructureBusiness and an Investment in UsOperations

Because no public trading market for•Our revenues and cash flows will be affected by the success and economic viability of our shares currently existsanchor Neighbors.

•A significant percentage of our revenues is derived from non-anchor Neighbors, and our share repurchase program is limited, it is difficult for ournet income and ability to make distributions to stockholders may be adversely affected if these Neighbors are not successful.

•We may be unable to sell their shares and, if our stockholders are able to sell their shares, it may beshopping centers when desired, at a discount to the public offeringan attractive price, at which stockholders originally purchased the shares.

There is no public trading market for our shares of common stock. Until our shares of common stock are listed on a stock exchange, if ever, stockholders may not sell their shares unless the buyer meets the applicable suitability and minimum purchase standards.

Under the share repurchase program (“SRP”), any shares repurchased will be at the lesser of $5.75 per share or the most recent estimated value per share (“EVPS”) of our common stock. Currently, standard repurchases under the SRP are suspended and repurchases are limited to those upon a stockholder’s qualifying death, disability, or determination of incompetence. In addition, we may choose to repurchase fewer shares than have been requested in any particular month to be repurchased under the SRP, or none at all, in our discretion at any time. We may repurchase fewer shares than have been requested to be repurchased due to lack of readily available funds because of adverse market conditions beyond our control, the need to maintain liquidity for our operations, or because we have determined that paying off our debt or investing in real property or other investments or other items is a better use of our capital than repurchasing our shares. The Board of Directors (“Board”) may modify, suspend, or terminate the SRP at any time upon 30 days’ notice. In addition, because we are not required to authorize the recommencement of a suspension of the SRP, including the currently suspended standard repurchases, within any specified period of time, we may effectively terminate the SRP, or a portion of it, by suspending it indefinitely. As a result, your ability to have your shares repurchased by us may be limited, and at times, you may not be able to liquidate your investment.

Therefore, it is difficult for our stockholders to sell their shares promptly or at all. If a stockholder is able to sell his or her shares, it may be at a discount to the EVPS and to the public offering price at which the stockholder originally purchased the shares. It is also likely that our shares would not be accepted as the primary collateral for a loan. Because of the illiquid nature of our shares, investors should purchase our shares only as a long-term investment and be prepared to hold them for an indefinite period of time.

The EVPS of our common stock is based on a number of assumptions that may not be accurate or complete and the methodology used to calculate the EVPS is also subject to a number of limitations.

On May 6, 2020, our Board decreased the EVPS of our common stock to $8.75 based substantially on the estimated market value of our portfolio of real estate properties and our third-party investment management business as of March 31, 2020. The decrease was primarily driven by the negative impact of the COVID-19 pandemic on our non-grocery Neighbors resulting from social distancing and “stay-at-home” guidelines and the uncertainty of the duration and full effect on the overall economy. We engaged a third-party valuation firm to provide a calculation of the range in EVPS of our common stock as of March 31, 2020, which reflected certain balance sheet assets and liabilities as of that date. Previously, our EVPS was $11.10, based substantially on the estimated market value of our portfolio of real estate properties and our third-party investment management business as of March 31, 2019. Our EVPS is based upon a number of estimates and assumptions that may not be accurate or complete. Different parties with different assumptions and estimates could derive a different EVPS, and this difference could be significant. The EVPS is not audited and does not represent a determination of the fair value of our assets or liabilities based on accounting principles generally accepted in the United States (“GAAP”), nor does it represent a liquidation value of our assets and liabilities, the price a third party would pay to acquire us, the price at which our shares of common stock would trade in secondary markets, or the amount at which our shares of common stock would trade on a national securities exchange.

Accordingly, we can give no assurance that, (i) our shares would trade at or near the EVPS if listed on a national securities exchange; (ii) a stockholder would be able to resell his or her shares at the EVPS; (iii) a stockholder would ultimately realize distributions per share equal to the EVPS upon a liquidation of our assets and settlement of our liabilities; (iv) a stockholder would receive an amount per share equal to the EVPS upon a sale of the Company; (v) a third party would offer the EVPS in an arm’s-length transaction to purchase all or substantially all of our shares of common stock; (vi) another independent third-party appraiser or third-party valuation firm would agree with our EVPS; or (vii) the methodologies used to calculate our EVPS would be acceptable to the Financial Industry Regulatory Authority (“FINRA”) for use on customer account statements or that the EVPS will satisfy the applicable annual valuation requirements under the Employee Retirement Income Security Act of 1974 (“ERISA”).

Furthermore, we have not made any adjustments to the valuation of our EVPS for the impact of other transactions occurring subsequent to May 6, 2020, including, but not limited to, (i) acquisitions or dispositions of assets; (ii) the issuance of common stock under the DRIP; (iii) Net Operating Income (“NOI”) earned and dividends declared (see “Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations - Non-GAAP Measures - Same-Center Net Operating Income” of this filing on Form 10-K for the calculation of NOI); (iv) the repurchase of shares; and (v) changes in leases, tenancy, or other business or operational changes. The value of our shares of common stock will fluctuate over time in response to developments related to individual real estate assets, the management of those assets, and changes in the real estate and finance markets. Because of, among other factors, the high concentration of our total assets in real estate and the number of shares of our common stock outstanding, changes in the value of individual real estate assets or changes in valuation assumptions could have a very significant impact on the value of our shares of common stock. The EVPS also does not take into account any disposition costs or fees for real estate properties, debt prepayment penalties that could apply upon the prepayment of certain of our debt obligations, or the impact of restrictions on the assumption of debt. Accordingly, the EVPS may or may not be an accurate reflection of the fair market value of our stockholders’ investments and will not likely represent the amount of net proceeds that would result from an immediate sale of our assets.

The actual value of shares that we repurchase under the SRP, or any future tender offer, may be substantially less than the price we are willing to pay under this program.

Under the SRP, we repurchase eligible shares at the lesser of $5.75 per share or the most recent EVPS. The price we pay is likely to differ from the price at which a stockholder could resell his or her shares or the price at which our shares would trade if listed on a national securities exchange. Thus, when we repurchase shares of our common stock, the repurchase may be dilutive to our remaining stockholders.

If we do not successfully implement a liquidity transaction, stockholders may have to hold their investment for an indefinite period.

There currently is no public trading market for shares of our common stock, and our charter does not contain a requirement to effect a liquidity event by a specific date. In the future, our Board may consider various forms of liquidity, each of which is referred to as a liquidity event, including, but not limited to, (i) the listing of shares of common stock on a national securities

exchange; (ii) the sale of all or substantially alla property could cause significant tax payments.

•We face competition and other risks in pursuing acquisition opportunities that could increase the cost of our assets; (iii) a sale or merger that would provide stockholders with cashsuch acquisitions and/or securities of a publicly traded company; or (iv) the dissolution of the Company. However, there can be no assurance that we will cause a liquidity eventlimit our ability to occur. If we do not pursue a liquidity transaction, shares of our common stock may continue to be illiquidgrow, and stockholders may, for an indefinite period of time, be unable to easily convert their investment to cash and could suffer losses on their investments.

If we pay distributions from sources other than our cash flows from operations, we may not be able to sustaingenerate expected returns or successfully integrate completed acquisitions into our distribution rate,existing operations.

•We share ownership of our unconsolidated joint ventures and do not have exclusive decision-making power, and as such, we are unable to ensure that our objectives will be pursued.

•Our real estate assets may decline in value and be subject to significant impairment losses, which may reduce our net income.

•We actively reinvest in our portfolio in the form of development and redevelopment projects, which have inherent risks that could adversely affect our financial condition, cash flows, and results of operations.

•The continued shift in retail sales towards e-commerce may adversely affect our financial condition, cash flows, and results of operations.

•Actual incremental unlevered yields for our development and redevelopment projects may vary from our underwritten incremental unlevered yield range.

•Pandemics, epidemics, or other health crises may have fewer funds available for investment in properties and other assets,a negative effect on our and our stockholders’ overall returns may be reduced.Neighbors’ businesses, financial condition, results of operations, cash flows, and liquidity.

Risks Related to Our organizational documents permit us to pay distributions from any source without limit (other than those limits set forth under Maryland law). To the extent we fund distributions from borrowings, we willIndebtedness and Liquidity

•We have fewer funds available for investment in real estate propertiessubstantial indebtedness, and other real estate-related assets, and our stockholders’ overall returns may be reduced. At times, we may need to borrow funds to pay distributions,incur additional indebtedness, including recourse debt, in the future, which could increase the costsadversely affect our business, financial condition, and ability to operatemake distributions to our business. Furthermore, if we cannot cover our distributions with cash flows from operations, we may be unablestockholders.

Risks Related to sustain our distribution rate.

We cannot assure stockholders that we will be able to continue paying distributions at the rate currently paid.

We intend to evaluate distributions on a monthly basis throughout 2021. It is possible that stockholders may not receive distributions equivalent to those previously paid by us for various reasons, including the following:Our Corporate Structure and Organization

•we may not have enough cash to pay such distributions due to changes inWe and our cash requirements, indebtedness, capital spending plans, operating cash flows, or financial position;

•decisions on whether, when, and in what amounts to make any future distributions will remain at all times entirely atconsolidated subsidiary, the discretion of the Board, which reserves the right to change our distribution practices at any time and for any reason;

•our Board may elect to retain cash to maintain or improve our credit ratings; and

•the amount of distributions that our subsidiaries may distribute to us may be subject to restrictions imposed by state law, state regulators, and/or the terms of any current or future indebtedness that these subsidiaries may incur.

Stockholders have no contractual or other legal right to distributions that have not been authorized by the Board and declared by the Company.

We have agreed to nominate Mr. Jeffrey S. Edison, Chairman of the Board and Chief Executive Officer, to our Board for each annual meeting through 2027.

As part of the transaction to acquireOperating Partnership, entered into tax protection agreements with certain real estate assets and the third party investment management business of PELP in exchange for stock and cash (the “PELP transaction”), we agreed to nominate Mr. Jeffrey S. Edison to the Board for each annual meeting through 2027, subject to certain terminating events. As a result, it is possible that Mr. Edison may continue to be nominated as a director in circumstances when the independent directors would not otherwise have nominated or elected him.

The Operating Partnership’s limited partnership agreement grants certain rights and protections to the limitedprotected partners, which may prevent or delay a change of control transaction that might involve a premium price for our shares of common stock.

The Operating Partnership’s limited partnership agreement grants certain rights and protections to the limited partners, including granting them the right to consent to a change of control transaction. Furthermore, Mr. Edison currently has voting control over approximately 57% of the Operating Partnership’s limited partnership units (exclusive of those owned by us) and therefore could have a significant influence over votes on change of control transactions.

The tax protection agreement, during its term, could limit the Operating Partnership’s ability to sell or otherwise dispose of certain propertiesshopping centers and may require the Operating Partnership to maintain certain debt levels that otherwise would not be required to operate its business.

WeRisks Related to Our REIT Status and Other Tax Risks

•Failure to qualify as a REIT would cause us to be taxed as a regular C corporation, which would substantially reduce funds available for distributions to stockholders.

•If the Operating Partnership entered intofails to qualify as a tax protection agreement at the closing of the PELP transaction, pursuant to which if the Operating Partnership: (i) sells, exchanges, transfers, conveys or otherwise disposes of certain properties in a taxable transactionpartnership for a period of ten years commencing on the closing; or (ii) fails, prior to the expiration of such period, to maintain minimum levels of indebtedness that would be allocable to each protected partner forU.S. federal income tax purposes, we would fail to qualify as a REIT and would suffer adverse consequences.

•Complying with REIT requirements may cause us to forgo otherwise attractive opportunities or alternatively, failsliquidate otherwise attractive investments.

Risks Related to offer such protected partners the opportunityBusiness Continuity

•We and our Neighbors face risks relating to guarantee specific typescybersecurity attacks, which could cause loss of the Operating Partnership’s indebtednessconfidential information and other disruptions to business operations, and compliance with new laws and regulations regarding cybersecurity and privacy may result in ordersubstantial costs and may decrease cash available for distributions.

Risks Related to enable such partners to continue to defer certain tax liabilities, the Operating Partnership will indemnify each affected protected partner against certain resulting tax liabilities. Therefore, although itOur Common Stock

•The market price and trading volume of shares of our common stock may be involatile.

•The number of shares of our common stock available for future issuance or sale could adversely affect the stockholders’ best interest for us to cause the Operating Partnership to sell, exchange, transfer, convey or otherwise disposemarket price of one of these properties, it may be economically prohibitive for us to do so during the ten year protection period because of these indemnity obligations. Moreover, these obligations may require us to cause the Operating Partnership to maintain more or different indebtedness than we would otherwise require for our business. As a result, the tax protection agreement will, during its term, restrict our ability to take actions or make decisions that otherwise would be in our best interests.common stock.

| | | | | | | | | | | |

PHILLIPS EDISON & COMPANY DECEMBER 31, 2023 FORM 10-K | | | 7 |

If the fiduciary of an employee benefit plan subject to ERISA (such as a profit sharing, Section 401(k) or pension plan) or an owner of a retirement arrangement subject to Section 4975 of the Internal Revenue Code (such as an individual retirement account) fails to meet the fiduciary and other standards under ERISA or the Internal Revenue Code (“IRC”) as a result of an investment in our stock, the fiduciary could be subject to penalties and other sanctions.

There are special considerations that apply to employee benefit plans subject to ERISA (such as profit sharing, Section 401(k) or pension plans) and other retirement plans or accounts subject to Section 4975 of the IRC (such as an individual retirement account or “IRA”) that are investing in shares of our common stock. Fiduciaries and IRA owners investing the assets of such a plan or account in our common stock should satisfy themselves that:

•

the investment is consistent with their fiduciary and other obligations under ERISA and the IRC;

•the investment is made in accordance with the documents and instruments governing the plan or IRA, including the plan’s or account’s investment policy;

•the investment satisfies the prudence and diversification requirements of Sections 404(a)(1)(B) and 404(a)(1)(C) of ERISA and other applicable provisions of ERISA and the IRC;

•the investment in our shares, for which no public market currently exists, is consistent with the liquidity needs of the plan or IRA;

•the investment will not produce an unacceptable amount of “unrelated business taxable income” for the plan or IRA;

•our stockholders will be able to comply with the requirements under ERISA and the IRC to value the assets of the plan or IRA annually; and

•the investment will not constitute a prohibited transaction under Section 406 of ERISA or Section 4975 of the IRC.

Failure to satisfy the fiduciary standards of conduct and other applicable requirements of ERISA and the IRC may result in the imposition of civil and criminal penalties and could subject the fiduciary to claims for damages or for equitable remedies, including liability for investment losses, and if an investment in our shares constitutes a prohibited transaction under ERISA or the IRC, the fiduciary or IRA owner who authorized or directed the investment may be subject to the imposition of excise taxes with respect to the amount invested. In addition, the investment transaction must be undone. In the case of a prohibited transaction involving an IRA owner, the IRA may be disqualified as a tax-exempt account, and all of the assets of the IRA may be deemed distributed and subjected to tax. ERISA plan fiduciaries and IRA owners should consult with counsel before making an investment in our common stock.

If stockholders invested in our shares through an IRA or other retirement plan, they may be limited in their ability to withdraw required minimum distributions.

If stockholders established an IRA or other retirement plan through which they invested in our shares, federal law may require them to withdraw required minimum distributions (“RMDs”) from such plan in the future as they may not be able to have their shares repurchased at a time in which they need liquidity to satisfy the RMD requirements under their IRA or other retirement plan. A repurchase, if available, may be at a price that is less than the price at which the shares were initially purchased or the current EVPS. If stockholders fail to withdraw RMDs from their IRA or other retirement plan, they may be subject to certain tax penalties.

Risks Related to the Retail Industry

The ongoing COVID-19 pandemic has had,Our Business and is expected to continue to have, a negative effect on our and our Neighbors’ businesses, financial condition, results of operations, cash flows, and liquidity.

In March 2020, the World Health Organization declared COVID-19 a global pandemic. The COVID-19 pandemic has caused, and is expected to continue to cause, significant disruptions to the United States and global economy and has contributed to significant volatility and negative pressure in financial markets. The global impact of the outbreak is continually evolving and, as additional cases of the virus are identified, many countries, including the United States, reacted by instituting quarantines, restrictions on travel, and/or mandatory closures of businesses. Certain states and cities, including where our properties are located, also reacted by instituting quarantines, restrictions on travel, “shelter-in-place” or “stay-at-home” rules, restrictions on types of businesses that may continue to operate, and/or restrictions on the types of construction projects that may continue. In May 2020, many state and local governments began lifting, in whole or in part, the “stay-at-home” mandates, effectively removing or lessening the limitations on travel and allowing many businesses to reopen in full or limited capacity.

The COVID-19 pandemic has impacted our business and financial performance, and we expect this impact to continue. Our retail and service-based Neighbors depend on in-person interactions with their customers to generate unit-level profitability, and the COVID-19 pandemic has decreased, and may continue to decrease, customers’ willingness to frequent, and mandated “shelter-in-place” or “stay-at-home” orders may prevent customers from frequenting our Neighbors’ businesses, which may result in their inability to maintain profitability and make timely rental payments to us under their leases or to otherwise seek lease modifications or to declare bankruptcy. At the peak of the pandemic-related closure activity, for our wholly-owned properties and those owned through our joint ventures, our temporary closures reached approximately 2,100 Neighbors, or 37% of all Neighbor spaces, totaling 27% of our annualized base rent (“ABR”) and 22% of our gross leasable area (“GLA”). As of March 8, 2021, 98% of our occupied Neighbor spaces, totaling 99% of our ABR and GLA, are open for business. Certain Neighbors remain temporarily closed, have since closed after reopening, are limiting the number of customers allowed in their stores, or have modified their operations in other ways that may impact their profitability, either as a result of government mandates or self-elected efforts to reduce the spread of COVID-19. These actions could result in increased permanent store closings and could reduce the demand for leasing space in our shopping centers and result in a decline in average rental rates on expiring leases.

While most of our Neighbors have reopened, we cannot presently determine how many of the Neighbors that remain closed will reopen, or whether a portion of those that have reopened will be required by government mandates to temporarily close again or will encounter financial difficulties that require them to close permanently. We believe substantially all Neighbors,

including those that were required to temporarily close under governmental mandates, are contractually obligated to continue with their rent payments as documented in our lease agreements with them. However, we believe it is best to begin negotiation of relief only once a Neighbor has reopened and made payments toward rent and recovery charges accrued. As of March 8, 2021, inclusive of our prorated share of properties owned through our joint ventures, we have executed payment plans with our Neighbors agreeing to defer approximately $8.7 million in rent and related charges, and we granted rent abatements totaling approximately $4.2 million. These payment plans and rent abatements represented approximately 2% and 1% of portfolio ABR, respectively. The weighted-average remaining term over which we expect to receive payment on executed payment plans is approximately twelve months. We are in negotiations with additional Neighbors, which we believe will lead to more Neighbors repaying their past due charges. As of March 8, 2021, we have collected approximately 93% of rent and recoveries billed during the second quarter of 2020, approximately 95% of rent and recoveries billed during the third quarter, and over 95% of rent and recoveries billed during the fourth quarter. Further, as of March 8, 2021, our collections for January and February 2021 were approximately 94% in total. In the event of any default by a Neighbor under its lease agreement or relief agreement, we may not be able to fully recover, and/or may experience delays in recovering and additional costs in enforcing our rights as landlord to recover, amounts due to us under the terms of the lease agreement and/or relief agreement. Additionally, certain Neighbors have declared bankruptcy as a result of the effects of the pandemic. As of December 31, 2020, we have several Neighbors currently in bankruptcy proceedings who continue to occupy space in our centers where we have not yet received notice that the lease has been assumed or rejected, representing an exposure of less than 1% of our total ABR.

Moreover, the ongoing COVID-19 pandemic, restrictions intended to prevent and mitigate its spread, resulting consumer behavior, and the economic slowdown or recession could have additional adverse effects on our business, including with regards to:

•the ability and willingness of our Neighbors to renew their leases upon expiration, our ability to re-lease the properties on the same or better terms in the event of nonrenewal or in the event we exercise our right to replace an existing Neighbor, and obligations we may incur in connection with the replacement of an existing Neighbor, particularly in light of the adverse impact to the financial health of many retailers and service providers that has occurred and continues to occur as a result of the COVID-19 pandemic and the significant uncertainty as to when and the conditions under which certain potential Neighbors will be able to operate physical retail locations in the future;