SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ | |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended September 30, 20132016

OR

☐ | |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from __________ to ___________ |

Commission File No. | Name of Registrant, State of Incorporation, Address of Principal Offices, and Telephone No. | IRS Employer Identification No. | ||

001-34757 | ||||

Spectrum Brands Holdings, Inc. ( | ||||

| a Delaware corporation) 3001 Deming Way Middleton, (608) 275-3340 www.spectrumbrands.com | 27-2166630 | |||

333-192634-03 | SB/RH Holdings, LLC ( 3001 Deming Way Middleton, WI 53562 (608) 275-3340 | 27-2812840 | ||

Securities registered pursuant to Section 12(b) of the Act:

Registrant | ||||

Title of each class | Name of each exchange on which registered | |||

Spectrum Brands Holdings, Inc. | Common Stock, Par Value $0.01 | New York Stock Exchange | ||

SB/RH Holdings, LLC | None | None |

Securities registered pursuant to Section 12(g) of the Act:

None

1

Indicate by check mark if the registrant is aregistrants are well-known seasoned issuer,issuers, as defined in Rule 405 of the Securities Act. Yes

Spectrum Brands Holdings, Inc. | Yes | ☒ | No | ☐ | ||

SB/RH Holdings, LLC | Yes | ☐ | No | ☒ |

Indicate by check mark if the registrant isregistrants are not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes

Spectrum Brands Holdings, Inc. | Yes | ☐ | No | ☒ | ||

SB/RH Holdings, LLC | Yes | ☐ | No | ☒ |

Indicate by check mark whether the registrantregistrants (1) hashave filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes

Spectrum Brands Holdings, Inc. | Yes | ☒ | No | ☐ | ||

SB/RH Holdings, LLC | Yes | ☒ | No | ☐ |

Indicate by check mark whether the registrant hasregistrants have submitted electronically and posted on itstheir corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes

Spectrum Brands Holdings, Inc. | Yes | ☒ | No | ☐ | ||

SB/RH Holdings, LLC | Yes | ☒ | No | ☐ |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Spectrum Brands Holdings, Inc. | ☐ | |||||

SB/RH Holdings, LLC | ☐ |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Registrant | Large Accelerated Filer | |||||||

Accelerated filer | ||||||||

Non-accelerated filer | Smaller reporting company | |||||||

Spectrum Brands Holdings, Inc. | X | |||||||

SB/RH Holdings, LLC | X | |||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

Spectrum Brands Holdings, Inc. | Yes | ☐ | No | ☒ | ||

SB/RH Holdings, LLC | Yes | ☐ | No | ☒ |

The aggregate market value of the voting stock held by non-affiliates of the registrantSpectrum Brands Holdings, Inc. was approximately $1,228,779,585$2,677,495,424 based upon the closing price on the last business day of the registrant's most recently completed second fiscal quarter (March 31, 2013)(April 3, 2016).* As of November 25, 201314, 2016, there were outstanding 52,423,49259,410,438 shares of the registrant'sSpectrum Brands Holdings, Inc.’s Common Stock, par value $0.01 per share.

SB/RH Holdings, LLC meets the conditions set forth in General Instruction I(1)(a) and (b) of Form 10-K and has therefore omitted the information otherwise called for by Items 10 to 13 of Form 10-K as allowed under General Instruction I(2)(c).

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’sSpectrum Brands Holdings, Inc.’s definitive proxy statement to be filed within 120 days of September 30, 20132016 are incorporated by reference in this Annual Report on Form 10-K in response to Part III, Items 10, 11, 12, 13 and 14.

2

SPECTRUM BRANDS HOLDINGS, INC.

SB/RH HOLDINGS, LLC

Page | |||||

PART I | |||||

| 17 | |||||

| ITEM 1B. | 35 | ||||

| 35 | |||||

| 37 | |||||

| ITEM 4. | 37 | ||||

PART II | |||||

| 38 | |||||

| 40 | |||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 41 | ||||

| 58 | |||||

| 59 | |||||

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 59 | ||||

| 59 | |||||

| 60 | |||||

PART III | |||||

| 61 | |||||

| 61 | |||||

| ITEM 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 61 | |||

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS AND DIRECTOR INDEPENDENCE | 62 | ||||

| 62 | |||||

PART IV | |||||

| 63 | |||||

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS AND FINANCIAL STATEMENT SCHEDULE | 64 | ||||

| 122 | |||||

| EXHIBIT INDEX | 124 | ||||

3

Forward-Looking Statements

We have made or implied certain forward-looking statements in this Annual Report on Form 10-K.report. All statements, other than statements of historical facts included in this Annual Report,report, including the statements under Item 7. Management’s“Management’s Discussion and Analysis of Financial Condition and Results of OperationsOperations” regarding our business strategy, future operations, financial condition, estimated revenues, projected costs, projected synergies, prospects, plans and objectives of management, as well as information concerning expected actions of third parties, are forward-looking statements. When used in this Annual Report,report, the words “anticipate,” “intend,” “plan,” “estimate,” “believe,” “expect,” “project,” “could,” “will,” “should,” “may”anticipate, intend, plan, estimate, believe, expect, project, could, will, should, may and similar expressions are also intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words.

Since these forward-looking statements are based upon our current expectations of future events and projections and are subject to a number of risks and uncertainties, many of which are beyond our control and some of which may change rapidly, actual results or outcomes may differ materially from those expressed or implied herein, and youundue reliance should not place undue reliancebe placed on these statements. Important factors that could cause our actual results to differ materially from those expressed or implied herein include, without limitation:

· | the impact of our indebtedness on our business, financial condition and results of operations; |

· | the impact of restrictions in our debt instruments on our ability to operate our business, finance our capital needs or pursue or expand business strategies; |

· | any failure to comply with financial covenants and other provisions and restrictions of our debt instruments; |

· | the impact of actions taken by significant stockholders; |

· | the impact of expenses resulting from the implementation of new business strategies, divestitures or current and proposed restructuring activities; |

· | our inability to successfully integrate and operate new acquisitions at the level of financial performance anticipated; |

· | the unanticipated loss of key members of senior management; |

· | the impact of fluctuations in commodity prices, costs or availability of raw materials or terms and conditions available from suppliers, including suppliers’ willingness to advance credit; |

· | interest rate and exchange rate fluctuations; |

· | our ability to utilize our net operating loss carry-forwards to offset tax liabilities from future taxable income; |

· | the loss of, significant reduction in, or dependence upon, sales to any significant retail customer(s); |

· | competitive promotional activity or spending by competitors, or price reductions by competitors; |

· | the introduction of new product features or technological developments by competitors and/or the development of new competitors or competitive brands; |

· | the effects of general economic conditions, including inflation, recession or fears of a recession, depression or fears of a depression, labor costs and stock market volatility or changes in trade, monetary or fiscal policies in the countries where we do business; |

· | changes in consumer spending preferences and demand for our products; |

· | our ability to develop and successfully introduce new products, protect our intellectual property and avoid infringing the intellectual property of third parties; |

· | our ability to successfully implement, achieve and sustain manufacturing and distribution cost efficiencies and improvements, and fully realize anticipated cost savings; |

· | the cost and effect of unanticipated legal, tax or regulatory proceedings or new laws or regulations (including environmental, public health and consumer protection regulations); |

· | public perception regarding the safety of products that we manufacture and sell, including the potential for environmental liabilities, product liability claims, litigation and other claims related to products manufactured by us and third parties; |

· | the impact of pending or threatened litigation; |

· | the impact of cybersecurity breaches or our actual or perceived failure to protect company and personal data; |

· | changes in accounting policies applicable to our business; |

· | government regulations; |

· | the seasonal nature of sales of certain of our products; |

· | the effects of climate change and unusual weather activity; and |

· | the effects of political or economic conditions, terrorist attacks, acts of war or other unrest in international markets. |

Some of the above-mentioned factors are described in further detail in the sectionsections entitled “Risk Factors” set forth below.in our annual and quarterly reports (including this report), as applicable. You should assume the information appearing in this Annual Report on Form 10-Kreport is accurate only as of

4

PART I

This combined Form 10-K is being filed separately by Spectrum Brands Holdings, Inc., a Delaware corporation (“SB Holdings” orSBH”) and SB/RH Holdings, LLC (“SB/RH”) (collectively, the “Company”). SB/RH is a wholly-owned subsidiary of SBH and represents a majority of its assets, liabilities, revenues, expenses and operations. Thus, all information contained in this report relates to, and is filed by, SBH. Information that is specifically identified in this report as relating solely to SBH, such as its financial statements and its common stock, does not relate to and is not filed by SB/RH. SB/RH makes no representation as to that information. The terms “the Company,” “we,” and “our” as used in this report, refer to both SBH and its consolidated subsidiaries and SB/RH and its consolidated subsidiaries, unless otherwise indicated. The terms “SBH” and “SB/RH” refer to Spectrum Brands Holdings, Inc. and SB/RH Holdings, LLC, respectively.

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to reports filed pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), isare made available free of charge on or through our website at www.spectrumbrands.com as soon as reasonably practicable after such reports are filed with, or furnished to the SEC. You may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains an Internet site that contains our reports, proxy statements and other information at www.sec.gov. In addition, copies of our (i) Corporate Governance Guidelines, (ii) charters for the Audit Committee, Compensation Committee and Nominating and Corporate Governance Committee, (iii) Code of Business Conduct and Ethics and (iv) Code of Ethics for the Principal Executive Officer and Senior Financial Officers are available at our Internet site at www.spectrumbrands.com under “Investor Relations—Corporate Governance.” Copies will also be provided to any stockholder upon written request to the Vice President, Investor Relations & Corporate Communications, Spectrum Brands, Inc. at 3001 Deming Way, Middleton, Wisconsin 53562 or via electronic mail at investorrelations@spectrumbrands.com, or by contacting the Vice President, Investor Relations & Corporate Communications by telephone at (608) 275-3340.

General

We are a diversified global branded consumer products company. Spectrum Brands, Inc. (“Spectrum Brands”), is a wholly owned subsidiary of SB Holdings. SB Holdings' common stock trades on the New York Stock Exchange (the “NYSE”) under the symbol “SPB.”

Our operating performance is influenced by a number of factors including: general economic conditions; foreign exchange fluctuations; trends in consumer markets; consumer confidence and preferences; our overall product line mix, including pricing and gross margin, which vary by product line and geographic market; pricing of certain raw materials and commodities; energy and fuel prices; and our general competitive position, especially as impacted by our competitors’ advertising and promotional activities and pricing strategies. See Management’s Discussion and Analysis of Financial Condition and Results of Operations, included elsewhere in this Annual Report on Form 10-K, for further discussion of the consolidated operating results.

5

Our Products

Our mission is to achieve superior shareholder returns through above-market organic growth, with a focus on building sustainable free cash flow and further acquisitions. Our vision is to be the preferred strategic partner to our customers with an expanding portfolio of innovative and superior-value consumer batteries; small appliances; pet supplies; electric shaving and grooming; electric personal care; home and garden controls; and hardware and home improvement. Our broad line of products include:

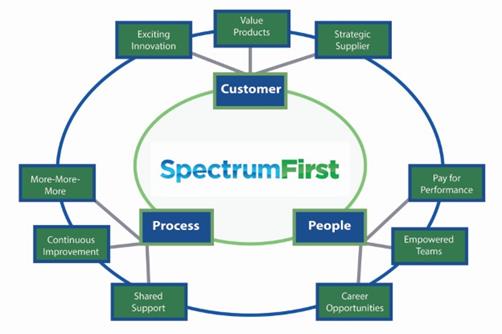

The Spectrum First growth accelerators; Customer, Process, and herbicides;People; provide the roadmap for how we intend to execute this strategy. Each growth accelerator has three drivers. These accelerators and their respective drivers are collectively known as the “Spectrum First 3x3.”

· | Customer – Our first growth accelerator focuses on strengthening strategic partnerships with customers. Our objective is for our retail partners to think of Spectrum Brands first when identifying how best to compete for consumers’ attention to bring them into their stores and online platforms with exciting product innovation, converting interest to sales through value products, and being a strategic supplier through total-cost reduction initiatives. |

· | Process – Our process growth accelerator is intended to drive continuous improvements in our products, costs and processes to generate healthy margins through sales growth with our “more-more-more” strategy to achieve above-market sales growth, which means entering into more countries, serving more channels and launching more categories. We also seek to drive continuous improvement over performance, quality and costs, and provide superior and efficient services through our shared services and “Centers of Excellence” model. |

· | People – Employees represent the third Spectrum First growth accelerator. We are working to be a preferred employer by empowering our teams and providing long-term career opportunities and pay-for-performance through focusing on retention and collaboration; driving empowered teams with trust, competence and speed; supporting alignment and providing more paths for employees to embrace new challenges and advance their careers across the global organization. |

6

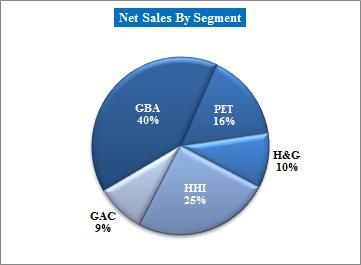

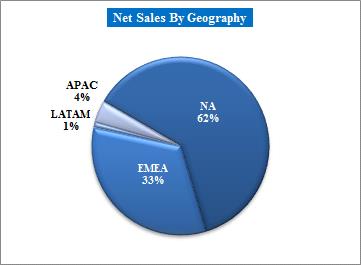

Global Batteries and home improvement products, including residential locksets, builders hardware and plumbing products.

The following is an overview of the GBA segment net sales of eachby product category and geographic region sold (based upon destination) as a percentage of net sales of our consolidated operations, is set forth below.

Percentage of Total Company Net Sales for the Fiscal Year Ended September 30, | |||||||||

| 2013 | 2012 | 2011 | |||||||

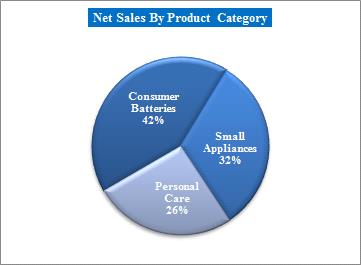

| Consumer batteries | 23 | % | 29 | % | 30 | % | |||

| Hardware and home improvement products | 21 | % | — | % | — | % | |||

| Small appliances | 18 | % | 24 | % | 24 | % | |||

| Pet supplies | 15 | % | 19 | % | 18 | % | |||

| Home and garden control products | 10 | % | 12 | % | 11 | % | |||

| Electric shaving and grooming products | 7 | % | 8 | % | 9 | % | |||

| Electric personal care products | 6 | % | 8 | % | 8 | % | |||

| 100 | % | 100 | % | 100 | % | ||||

The consumer batteries product category consists of alkaline batteries, (AA, AAA, C, Dzinc carbon batteries, nickel metal hydride (NiMH) rechargeable batteries and 9-volt sizes) to both retail and industrial customers. Our alkaline batteries are marketed and soldbattery chargers primarily under the RayovacRayovac® and VARTAVARTA® brands. We alsoAdditionally, we manufacture alkaline batteries for third parties who sell the batteries under their own private labels. Our zinc carbon batteries are also marketed and sold primarily under the Rayovac and VARTA brands and are designed for low and medium drain battery powered devices.

The small appliances product category consists of small kitchen appliances under the Black & Decker®, Russell Hobbs®, George Foreman®, Juiceman® and Breadman® brands, including toaster ovens, toasters, sandwich makers, coffeemakers, coffee grinders, can openers, electric knives, grills, deep fryers, food choppers, food processors, slow cookers, hand mixers, blenders, juicers, bread makers, kettles, rice cookers and steamers. We also sell small home product appliances, including hand-held irons, vacuum cleaners, air purifiers, clothes shavers and heaters, primarily under the Black & Decker® and Russell Hobbs® brands.

The personal care product category includes a broad line of electric shaving and grooming products under the Remington® brand name, including men’s rotary and foil shavers, beard and mustache trimmers, body, nose and ear trimmers, women’s shavers, haircut kits and intense pulsed light hair removal systems. Other personal care products include hand-held dryers, curling irons, straightening irons, brush irons, hair setters, facial brushes, skin appliances, electric toothbrushes and hair accessories.

We manage our GBA sales teams by geographic region and product category. We sell primarily to large retailers, online retailers, wholesalers, distributors, warehouse clubs, food and drug chains and specialty trade or retail outlets such as consumer electronics stores, department stores, discounters and other specialty stores. We maintain separate sales teams to service (i) our retail sales and distribution channels; (ii) our hearing aid professionals channel; and (iii) our industrial distributors and OEM sales and distribution channel. International distribution varies by region and is often executed on a country-by-country basis. We utilize a network of independent brokers to service participants in selected distribution channels.

See Management’s Discussion and Analysis of Financial Condition and Results of Operations, included elsewhere in this Annual Report on Form 10-K, for further discussion of the segment’s operating results.

7

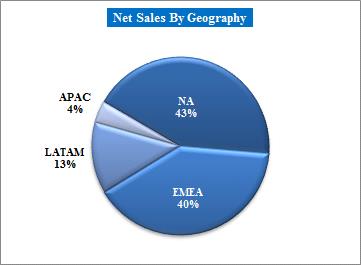

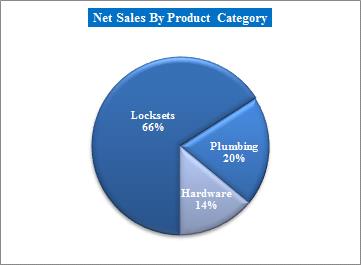

Hardware and Home Improvement Products

The following is an overview of the hardware and home improvementHHI segment net sales by product category we market and sellgeographic region sold (based upon destination) as a percentage of net sales for the segment for the year ended September 30, 2016:

The lockset product category includes a broad range of residential locksets and door hardware including knobs, levers, deadbolts, handlesetshandle sets and electronics. We offer our security hardwareelectronics under three main brands, Kwikset, Weiser and Baldwin. On a global basis we are one of the largest producers of tubular residential locksets. Kwikset includes opening to mid-price pointbrands: (i) Kwikset®, residential door hardware sold primarily in the U.S. retail and wholesale channels. Products are offered under the three brands Safe Lock, Kwikset and Kwikset Signature Series. Weiser offers opening to mid-price point; (ii) Weiser®, residential door hardware sold primarily in the Canadian retailCanada; and wholesale channels. Baldwin offers high price point(iii) Baldwin®, luxury hardware sold globally through the showroom and lumber yard channels.

The plumbing product line is largely harmonized between the brands, the dual branding approach has been utilized to protect legacy business with key customers and avoid channel conflict.

The hardware product category we marketincludes hinges, security hardware, screen and storm door products, garage door hardware, window hardware and floor protection under the National Hardware® and Stanley® brand names throughout the U.S. and Canada. The product line is largely harmonized between these brands and the dual-branding approach has been utilized to protect legacy business with key customers and avoid channel conflict.

On October 1, 2014, the Company acquired privately owned Tell Manufacturing, Inc. (“Tell”), a U.S. manufacturer and distributor of commercial doors, locks and hardware. Tell provides the HHI segment with an established commercial security sales position through a well-recognized brand, along with a platform to expand our patented SmartKey® and Kevo® residential lock technologies into commercial channels. The Tell acquisition also added doors and hollow metal door manufacturing capabilities, a strategically important adjacent category.

The sales force of the HHI business is aligned by customer and geographic region. We sell a variety of leading branded pet supplies for fish, dogs, cats, birdsprimarily to large retailers, home improvement centers, hardware stores, non-retail distributors, home builders, commercial contractors, and other small domestic animals. We haveretailers.

See Management’s Discussion and Analysis of Financial Condition and Results of Operations, included elsewhere in this Annual Report on Form 10-K, for further discussion of the segment’s operating results.

8

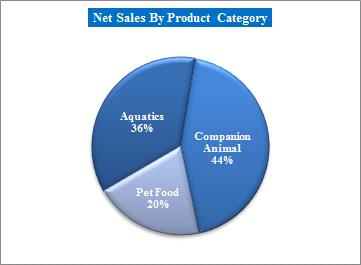

Global Pet Supplies (PET)

The following is an overview of the PET segment net sales by product category and geographic region sold (based upon destination) as a percentage of net sales for the segment for the year ended September 30, 2016:

The aquatics product category includes a broad line of consumer and commercial aquatics products, including integrated aquarium kits, stand-alone tanks and stands, aquatics equipment such as filtration systems, heaters, and pumps, and other equipment,aquatics consumables such as fish food, water treatments and water treatment products.conditioners. Our largest aquatics brands are Tetra, Marineland, Whisper, JungleTetra®, Marineland®, Whisper®, Jungle® and Instant Ocean. We also sellOcean®.

The companion animal product category includes a variety of specialty pet products including rawhide chews, dog and cat treats, small animal food and treats, clean upclean-up and training aid products, health and grooming aids, bedding products, and consumable accessories including privacy tents, litter carpets, crystal litter cartridges, charcoal filters, corn-based litter and replaceable waste receptacles. Our largest specialty pet brands include FURminator, 8-in-1, Dingo,FURminator®, 8-in-1®, Dingo®, Nature’s Miracle,Miracle®, Wild HarvestHarvest® and Littermaid.Littermaid®.

The pet food product category includes wet and dry pet food for dogs and cats under the IAMS®, Eukanuba® and 8-in-1® brand names in European markets. On December 31, 2014, we completed the acquisition of Procter & Gamble’s European pet food business, consisting of the IAMS® and Eukanuba® brands for dogs and cats. Eukanuba® is a popular brand with breeders and veterinarians in Europe; and IAMS® is a premium brand with broad customer appeal primarily in the United Kingdom with opportunities to grow further across Europe and is positioned for consumers who treat their pets as family members and view the food they feed their pets as a way to make them happy.

Additionally, on January 16, 2015, we acquired Salix Animal Health, a vertically integrated producer and distributor of natural rawhide dog chews, treats and snacks, offering a comprehensive line of chews made from beef hides, pork, chicken, beef and other various proteins. Its two flagship brands are Healthy-Hide® that is marketed across the Good’n’Fun®, Good’n’Fit®, and Good’n’Tasty® family of brands; and Digest-eeze®. Salix will provide the segment with increased optionality for low-cost global rawhide production and supply, and expand our Dingo® dog treats business with complementary product offerings.

Our PET sales force is aligned by customer type, geographic region and product category. We sell primarily to mass merchandisers, grocery stores and drug chains, pet superstores, independent pet stores, warehouse clubs and other specialty retailers. International distribution varies by region and is often executed on a country-by-country basis.

See Management’s Discussion and Analysis of Financial Condition and Results of Operations, included elsewhere in this Annual Report on Form 10-K, for further discussion of the segment’s operating results.

9

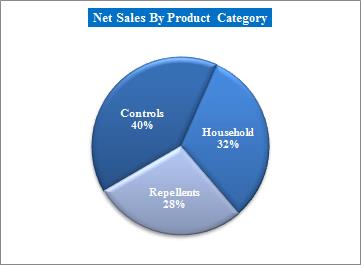

Home and Garden Control Products

The following is an overview of the home, lawnH&G segment net sales by product category and garden products geographic region sold (based upon destination) as a percentage of net sales for the segment for the year ended September 30, 2016:

The controls product category we currently sell and marketincludes a variety of leadingoutdoor insect and weed control solutions, and animal repellents under the brand names Spectracide®, Black Flag®, Garden Safe®, EcoLogic® and Liquid Fence®. Our line of outdoor control solutions are designed to assist consumers in controlling insects, weeds and animals when tackling lawn and landscaping projects themselves. From selective and non-selective herbicides to pest-specific solutions, our outdoor products including are available as aerosols, granules, ready-to-use or hose-end ready-to-sprays designed to fulfill a variety of consumer needs.

The household insecticides, insect repellents, and lawn insect and weed control solutions. We offer product category includes a broad array of household pest control solutions, such as spider and scorpion killers; roach and ant killers; flying insect killers; insect foggers; wasp and hornet killers; bedbug, flea and tick control products; and roach and ant baits. We also offer powerful rodent traps and rodenticides with discreet designs that are easy to refill and reuse. Our largest brands in the household insect control and rodenticide category are Hot ShotShot® and Black Flag.

The repellents product category includes personal use pesticides for protection from various outdoor nuisance pests, especially mosquitoes. These products include both personal repellents available in a variety of formulas (suchsuch as aerosols, lotions, pump sprays and wipes)wipes to match consumers’ dynamic needs,needs; as well as area repellents (suchsuch as yard sprays, citronella candles and patio lanterns) that letlanterns to allow consumers to enjoy the outdoors without bothersome pests. Our brands in the insect repellents category are CutterCutter® and Repel.

Repel®.

The Home and Garden business sales force is geographically aligned with our key customers. We sell primarily to home improvement centers, mass merchandisers, dollar stores, hardware stores, home and garden distributors, and food and drug retailers, primarily in the U.S.

See Management’s Discussion and Analysis of Financial Condition and Results of Operations, included elsewhere in this Annual Report on Form 10-K, for further discussion of the segment’s operating results.

10

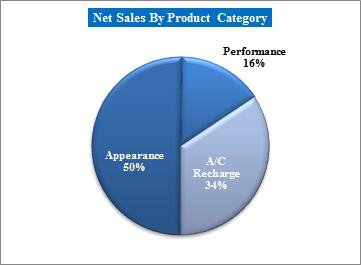

Global Auto Care (GAC)

The following is an overview of the GAC segment net sales by product category and geographic region sold (based upon destination) as a percentage of net sales for the segment for the year ended September 30, 2016:

We entered the GAC segment through our lineacquisition of outdoor insectArmored Auto Group (“AAG”) on May 21, 2015, which consists of products within the automotive aftermarket appearance, performance chemicals, and weed control solutions allows consumers to conquer bugsdo-it-yourself automotive air conditioner recharge product categories.

The appearance product category includes protectants, wipes, tire and weeds,wheel care products, glass cleaners, leather care products, air fresheners and tackle their biggest lawn and landscaping projects themselves. From selective and non-selective herbicides to pest-specific solutions, our outdoor products are available in easy-to-use formulations (such as aerosols, granules, ready-to-use or hose-end ready-to-sprays)washes designed to fulfillclean, shine, refresh and protect interior and exterior automobile surfaces under the brand name Armor All®. Armor All® is a variety of consumer needs. Our outdoor insecticideleader in the automotive aftermarket appearance products category based upon its recognized brand name, convenient application methods and herbicide brands include Spectracideproduct innovation.

The performance product category includes STP® branded fuel and Garden Safe.

The A/C recharge product category includes do-it-yourself automotive air conditioner recharge products under the RemingtonA/C PRO® brand name, including men’s rotaryalong with other refrigerant and foil shavers, beardoil recharge kits, sealants and mustache trimmers, body, noseaccessories.

The GAC business sales force is geographically aligned with key customers and ear trimmers, women’s shavers, haircut kitssupply chains. We sell primarily to big-box auto, auto specialty retail, mass retailers, food and intense pulsed light hair removal systems.

See Management’s Discussion and Analysis of productsFinancial Condition and Results of Operations, included elsewhere in this Annual Report on Form 10-K, for further discussion of the branded small household appliances category under the George Foreman, Black & Decker, Russell Hobbs, Farberware, Juiceman, Breadmansegment’s operating results.

11

Other Information

Sales, Distribution and Toastmaster brands, including grills, bread makers, sandwich makers, kettles, toaster ovens, toasters, blenders, juicers, can openers, coffee grinders, coffeemakers, electric knives, deep fryers, food choppers, food processors, hand mixers, rice cookers and steamers. We also market small home product appliances, including hand-held irons, vacuum cleaners, air purifiers, clothes shavers and heaters, primarily under the Black & Decker and Russell Hobbs brands.

We sell our products through a variety of trade channels, including retailers, wholesalers and distributors, hearing aid professionals, industrial distributorsconstruction companies and OEMs. Our sales generally are made through the use of individual purchase orders, consistent with industry practice. Retail sales of the consumer products we market have been increasingly consolidated on a worldwide basis into a small number of regional and national mass merchandisers. This trend towards consolidation is occurring on a worldwide basis. As a result of this consolidation, amerchandisers and e-commerce companies that generally have strong negotiating power with their suppliers. A significant percentage of our sales are attributable to a very limited group of retailer customers, including Wal-Mart,(in alphabetical order), Amazon, Argos, Autozone, Dollar General, Lowe’s, PetCo, PetSmart, Target, The Home Depot, Lowe’s, Carrefour, Target, PetSmart, Canadian Tire, PetCo and Gigante.Wal-Mart. Our sales to our largest customer, Wal-Mart, represented approximately 1518%% of our consolidated net sales for the fiscal year ended September 30, 2013.2016. No other customer accounted for more than 10% of our consolidated net sales in the fiscal year ended September 30, 20132016..

Factors influencing product sales include brand name recognition, perceived quality, price, performance, product packaging, design innovation, and total assetsconsumer confidence and preferences as well as information concerning our revenues and long-lived assets by geographic location for the last three fiscal years is set forth in Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and Note 11, "Segment Information", in Notes to Consolidated Financial Statements included in this Annual Report on Form 10-K.

· | Strong Diversified Global Brand Portfolio. We have a global portfolio of well-recognized consumer product brands. We believe that the strength of our brands positions us to extend our product lines and provide our retail customers with strong sell-through to consumers. |

· | Strong Global Retail Relationships. We have well-established business relationships with many of the top global retailers, distributors and wholesalers, which have assisted us in our efforts to expand our overall market penetration and promote sales. |

· | Expansive Distribution Network. We distribute our products in approximately 160 countries through a variety of trade channels, including retailers, wholesalers and distributors, hearing aid professionals, construction companies and OEMs. |

· | Innovative New Products, Packaging and Technologies. We have a long history of product and packaging innovations in each of our product categories and continually seek to introduce new products both as extensions of existing product lines and as new product categories. |

· | Experienced Management Team. Our management team has substantial consumer products experience. On average, each senior management team member has more than 20 years of experience at Spectrum Brands, VARTA, Remington, Russell Hobbs or other branded consumer product companies such as Newell Brands and Honeywell. |

Within our GBA segment, primary competitors for consumer batteries include Energizer Holdings, Inc. (Energizer); Berkshire Hathaway (Duracell); Matsushita (Panasonic) and private label brands of major geographic territories, Northretailers. Primary competitors for small appliances include Newell Brands (Oster, Sunbeam, Mr. Coffee, Crockpot, Rival, Breville), General Electric (GE), De’Longhi America Latin America(DeLonghi, Kenwood, Braun), SharkNinja f/k/a Euro-Pro (Shark, Ninja), NACCO Industries (Hamilton Beach, Proctor Silex), SEB S.A.(T-fal, Krups, Rowenta), Whirlpool Corporation (Kitchen Aid, Waring), Conair Corporate (Cuisinart), Koninklijke Philips N.V. (Philips), Glen Dimplex (Morphy Richards) and Europeprivate label brands for major retailers. Primary competitors in personal care include are Koninklijke Philips Electronics N.V. (Norelco), The Procter & Gamble Company (Braun), Conair Corporation, Wahl Clipper Corporation and Helen of Troy Limited.

Within our HHI segment, primary competitors in residential locksets include Allegion (Schlage) and private label import brands such as Defiant. Primary competitors for hardware include The Hillman Group, Hampton Hardware, Crown Bolt and private label competitors. Primary competitors for plumbing include Kohler, Masco, Fortune Brands (Moen), American Standard, Glacier Bay, AquaSource, and the restprivate label brands of the world (“Europe/ROW”). Within each major geographic territory, we have additional subdivisions designed to meetretailers.

Primary competitors in our customers’ needs.

Primary competitors in our H&G segment are The Scotts Miracle-Gro Company (Scotts, Ortho, Roundup, Miracle-Gro, Tomcat); Central Garden & Pet (AMDRO, Sevin) and Bayer A.G. (Bayer Advanced), S.C. Johnson & Son, Inc. (Raid, OFF!); and Henkel AG & Co. KGaA (Combat).

Primary competitors in our GAC segment include Valvoline, Prestone, Turtle Wax, Black Magic, Energizer, Newell Brands and private label brands. We manage our sales force in North Americaalso encounter competition from similar and alternative products, many of which are produced and marketed by distribution channel. We maintain separate sales groups to service (i) our retail salesmajor multinational or national companies, including Mothers, Meguiars, Lucas, and distribution channel, (ii) our hearing aid professionals channel and (iii) our industrial distributors and OEM sales and distribution channel. In addition, we utilize a network of independent brokers to service participants in selected distribution channels.

12

Seasonality

On a consolidated basis our financial results are approximately equally weighted across our quarters, however, sales force servingof certain product categories tend to be seasonal. Sales from our GBA segment, primarily from consumer battery and electric personal care product categories tend to increase during the December holiday season (the Company’s first fiscal quarter), while small appliances sales increase from July through December primarily due to the increased demand by customers in Europe/ROW is supplemented by an international networkthe late summer for “back-to-school” sales (the Company’s fourth fiscal quarter) and in December for the holiday season. Sales from our HHI segment primarily increase during the spring and summer construction period (the Company’s third and fourth fiscal quarters). Sales from our PET segment remain fairly consistent throughout the year with little variation. Sales from our H&G segment and GAC segment typically peak during the first six months of distributorsthe calendar year (the Company’s second and third fiscal quarters) due to promote the salecustomer seasonal purchasing patterns and timing of our products.promotional activities. Our sales operations throughout Europe/ROW are organized by geographic territoryquarter as a percentage of annual net sales during the years ended September 30, 2016, 2015 and the following sales channels: (i) food/retail, which includes mass merchandisers, discounters and drug and food stores; (ii) specialty trade, which includes clubs, consumer electronics stores, department stores, photography stores and wholesalers/distributors; and (iii) industrial, government, hearing aid professionals and OEMs.

|

|

|

|

|

|

|

|

|

|

|

| 2016 |

| 2015 |

| 2014 | |||

First Quarter |

|

| 24% |

|

| 23% |

|

| 25% |

Second Quarter |

|

| 24% |

|

| 23% |

|

| 23% |

Third Quarter |

|

| 27% |

|

| 26% |

|

| 25% |

Fourth Quarter |

|

| 25% |

|

| 28% |

|

| 27% |

Manufacturing, Raw Materials and Suppliers

The principal raw materials used in manufacturing our products—include zinc, electrolytic manganese dioxide used in our consumer batteries products; brass and steel—steel used in our HHI products; and refrigerant R-134a used in our GAC A/C recharge products; that are sourced either on a global or regional basis. The prices of these raw materials are susceptible to price fluctuations due to supply and demand trends, energy costs, transportation costs, government regulations and tariffs, changes in currency exchange rates, price controls, general economic conditions and other unforeseen circumstances. We have regularly engaged in forward purchase and hedging derivative transactions in an attempt to effectively manage thecertain raw material costs we expect to incur over the next 12 to 24 months.

Substantially all of our rechargeable batteries and chargers, portable lighting products, hair care and other personal care products and our electric shaving and grooming products and small appliances are manufactured by third party suppliers that are primarily located in the Asia/PacificAsia-Pacific region. We maintain ownership of most of the tooling and molds used by our suppliers.

We continually evaluate our manufacturing facilities’ capacity and related utilization. As a result of such analyses, we have closed a number of manufacturing facilities during the past five years. In general, we believe our existing facilities are adequate for our present and foreseeable needs.

Patents and Development

We use and development strategy is focused on new product development and performance enhancementsmaintain a number of our existing products. We plan to continue to use our strongpatents, trademarks, brand names established customer relationships and trade names that are, in the aggregate, important to our businesses. We seek trademark protection in the U.S. and in foreign countries. The Company’s most significant research and development efforts to introduce innovative products that offer enhanced value to consumers through new designs and improved functionality.registered trademarks are:

Segment | Trademarks | |

GBA | Rayovac®, VARTA®, Remington®, Black & Decker®, George Foreman®, Russell Hobbs®, Farberware®, Toastmaster®, Breadman®, Juiceman® | |

HHI | Kwikset®, Weiser®, Baldwin®, National Hardware®, Stanley®, Fanal®, Pfister®, Tell® | |

PET | Tetra®, 8-in-1®, Dingo®, Nature’s Miracle®, Wild Harvest®, Marineland®, Furminator®, Littermaid®, Birdola®, Healthy Hide®, Digest-eeze®, Iams®, Eukanuba® | |

H&G | Spectracide®, Cutter®, Hot Shot®, Real Kill®, Ultra Kill®, Black Flag®, Liquid Fence®, Rid-a-bug®, TAT®, Garden Safe®, Repel® | |

GAC | Armor All®, STP®, A/C PRO® |

We own or license from third parties a significant number of patents and patent applications throughout the world relating to products we sell and manufacturing equipment we use. We hold a license that expires in March 2022 for certain alkaline battery designs, technology and manufacturing equipment from Matsushita Electrical Industrial Co., Ltd. (“Matsushita”), to whom we pay a royalty.

patented SmartKey® technology, which enables customers to easily rekey their locks without hiring a locksmith.

13

We acquired the October 2002 sale by VARTA AG of substantially all of its consumer battery business to us and VARTA AG’s subsequent sale of its automotive battery business to Johnson Controls, Inc. (“Johnson Controls”), we acquired rights to the VARTAVARTA® trademark in the consumer battery category and Johnson Controls Inc. acquired rights to the trademark in the automotive battery category.category from VARTA AG. VARTA AG continues to have rights to use the trademark with travel guides and industrial batteries and VARTA Microbattery GmbH has the right to use the trade marktrademark with micro batteries. We are party to a Trademark and Domain Names Protection and Delimitation Agreement that governs ownership and usage rights and obligations of the parties relative to the VARTA ® trademark.

We license the Black & DeckerDecker® brand in North America, Latin America (excluding Brazil) and the Caribbean for four core categories of household appliances: beverage products, food preparation products, garment care products and cooking products. Russell Hobbs has licensed the Black & Decker brand since 1998 for use in marketing various household small appliances. In July 2011, Russell Hobbs andproducts through a trademark license agreement with The Black &and Decker Corporation (“BDC”) extended the trademark license agreement for a fourth time through December 2015.2018. Under the agreement, as extended, Russell HobbsSpectrum agreed to pay BDC royalties based on a percentage of sales, with minimum annual royalty payments of $15.0 million from calendar year 2011 through calendar year 2015.2018. The agreement also requires us to comply with maximum annual return rates for products.

We own the patented SmartKey technology,rights to use the Remington® trademark for electric shavers, shaver accessories, grooming products and personal care products; and Remington Arms Company, Inc. (“Remington Arms”) owns the rights to use the trademark for firearms, sporting goods and products for industrial use, including industrial hand tools. The terms of a 1986 agreement between Remington Products, LLC and Remington Arms provides for the shared rights to use the trademark on products which enables customers to easily rekey their locks without hiring a locksmith.

We license the Stanley® and Black & Decker® marks and logos in the HHI segment for limited shelf spacesuch products as residential locksets, builder’s hardware, padlocks, and consumer acceptance. Factors influencing product sales include brand name recognition, perceived quality, price, performance, product packaging, design innovation,door hardware through a transitional trademark license agreement with Stanley Black & Decker Corporation. Under the agreement and consumer confidence and preferences as well as creative marketing, promotion and distribution strategies.

Research and gardenDevelopment

Our research and development strategy is focused on new product category face competition from The Scotts Miracle-Gro Company (“Scotts Company”), which markets lawndevelopment and garden products under the Scotts, Ortho, Roundup, Miracle-Gro, and Tomcat brand names; Central Garden & Pet, which markets garden products under the AMDRO and Sevin brand names; and Bayer A.G., which markets home and garden products under the Bayer Advanced brand name.

Governmental Regulations and Environmental Matters

Due to the nature of our operations, our facilities are subject to a broad range of federal, state, local and foreign legal and regulatory provisions relating to the environment, including those regulating the discharge of materials into the environment, the handling and disposal of solid and hazardous substances and wastes and the remediation of contamination associated with the releases of hazardous substances at our facilities. We believe that compliance with the federal, state, local and foreign laws and regulations to which we are subject will not have a material effect upon our capital expenditures, financial condition, earnings or competitive position.

From time to time, we have been required to address the effect of historic activities on the environmental condition of our properties. We have not conducted invasive testing at all facilities to identify all potential environmental liability risks. Given the age of our facilities and the nature of our operations, it is possible that material liabilities may arise in the future in connection with our current or former facilities. If previously unknown contamination of property underlying or in the vicinity of our manufacturing facilities is discovered, we could incur material unforeseen expenses, which could have a material adverse effect on our financial condition, capital expenditures, earnings and competitive position. Although we are currently engaged in investigative or remedial projects at some of our facilities, we do not expect that such projects, taking into account established accruals, will cause us to incur expenditures that are material to our business, financial condition or results of operations; however, it is possible that our future liability could be material.

14

We have been, and in the future may be, subject to proceedings related to our disposal of industrial and hazardous material at off-site disposal locations or similar disposals made by other parties for which we are held responsible as a result of our relationships with such other parties. In the U.S., these proceedings are under the Federal Comprehensive Environmental Response, Compensation and Liability Act of 1980 (“CERCLA”) or similar state laws that hold persons who “arranged for” the disposal or treatment of such substances strictly liable for costs incurred in responding to the release or threatened release of hazardous substances from such sites, regardless of fault or the lawfulness of the original disposal. Liability under CERCLA is typically joint and several, meaning that a liable party may be responsible for all costs incurred in investigating and remediating contamination at a site. As a practical matter, liability at CERCLA sites is shared by all of the viable responsible parties. We occasionally are identified by federal or state governmental agencies as being a potentially responsible party for response actions contemplated at an off-site facility. At the existing sites where we have been notified of our status as a potentially responsible party, it is either premature to determine whether our potential liability, if any, will be material or we do not believe that our liability, if any, will be material. We may be named as a potentially responsible party under CERCLA or similar state laws for other sites not currently known to us, and the costs and liabilities associated with these sites may be material.

It is difficult to quantify with certainty the potential financial impact of actions regarding expenditures for environmental matters, particularly remediation, and future capital expenditures for environmental control equipment. Nevertheless, based upon the information currently available, we believe that our ultimate liability arising from such environmental matters, taking into accountconsidering established accruals of

Electronic and electrical products that we sell in Europe, particularly products sold under the RemingtonRemington® brand name, VARTAVARTA® battery chargers, certain portable lighting and all of our batteries, are subject to regulation in European Union (“EU”) markets under three key EU directives. The first directive is the Restriction of the Use of Hazardous Substances in Electrical and Electronic Equipment (“RoHS”) which took effect in EU member states beginning July 1, 2006. RoHS prohibits companies from selling products which contain certain specified hazardous materials in EU member states. We believe that compliance with RoHS willdoes not have a material effect on our capital expenditures, financial condition, earnings or competitive position. The second directive is entitled the Waste of Electrical and Electronic Equipment (“WEEE”). WEEE makes producers or importers of particular classes of electrical goods financially responsible for specified collection, recycling, treatment and disposal of past and future covered products. WEEE assigns levels of responsibility to companies doing business in EU markets based on their relative market share. WEEE calls on each EU member state to enact enabling legislation to implement the directive. To comply with WEEE requirements, we have partnered with other companies to create a comprehensive collection, treatment, disposal and recycling program. As EU member states pass enabling legislation we currently expect our compliance system to be sufficient to meet such requirements. Our current estimated costs associated with compliance with WEEE are not significant based on our current market share. However, we continue to evaluate the impact of the WEEE legislation as EU member states implement guidance and as our market share changes and, as a result, actual costs to our company could differ from our current estimates and may be material to our business, financial condition or results of operations. The third directive is the Directive on Batteries and Accumulators and Waste Batteries, which was adopted in September 2006 and went into effect in September 2008 (the “Battery Directive”). The Battery Directive bans heavy metals in batteries by establishing maximum quantities of those heavy metals in batteries and mandates waste management of batteries, including collection, recycling and disposal systems. The Battery Directive places the costs of such waste management systems on producers and importers of batteries. The Battery Directive calls on each EU member state to enact enabling legislation to implement the directive. We currently believe

Certain of our products and facilities in each of our business segments are regulated by the United States Environmental Protection Agency (the “EPA”) and the United States Food and Drug Administration (the “FDA”) or other federal consumer protection and product safety agencies and are subject to the regulations such agencies enforce, as well as by similar state, foreign and multinational agencies and regulations. For example, in the U.S., all products containing pesticides must be registered with the EPA and, in many cases, similar state and foreign agencies before they can be manufactured or sold. Our inability to obtain or the cancellation of any registration could have an adverse effect on our business, financial condition and results of operations. The severity of the effect would depend on which products were involved, whether another product could be substituted and whether our competitors were similarly affected. We attempt to anticipate regulatory developments and maintain registrations of, and access to, substitute chemicals and other ingredients. We may not always be able to avoid or minimize these risks.

The Food Quality Protection Act (“FQPA”) established a standard for food-use pesticides, which is that a reasonable certainty of no harm will result from the cumulative effect of pesticide exposures. Under the FQPA, the EPA is evaluating the cumulative effects from dietary and non-dietary exposures to pesticides. The pesticides in certain of our products continue to be evaluated by the EPA as part of this program. It is possible that the EPA or a third party active ingredient registrant may decide that a pesticide we use in our products will be limited or made unavailable to us. We cannot predict the outcome or the severity of the effect of the EPA’s continuing evaluations of active ingredients used in our products.

15

Certain of our products and packaging materials are subject to regulations administered by the FDA. Among other things, the FDA enforces statutory prohibitions against misbranded and adulterated products, establishes ingredients and manufacturing procedures for certain products, establishes standards of identity for certain products, determines the safety of products and establishes labeling standards and requirements. In addition, various states regulate these products by enforcing federal and state standards of identity for selected products, grading products, inspecting production facilities and imposing their own labeling requirements.

Certain A/C products containing R-134a are subject to regulation in the U.S. markets under the EPA’s Significant New Alternative Policy ("SNAP Program"), which implements international agreements restricting the use of certain refrigerants. The EPA has identified use of R-134a in new automotive air conditioning systems as an approved use up to the 2020 automotive model year. The EPA has not yet approved a replacement refrigerant under the SNAP program for sale in small cans for automotive use for automobiles produced beginning with the 2021 model year, and future rulemakings from the agency are anticipated. We hadcurrently believe that compliance with current and future SNAP regulations will not have a material effect on our capital expenditures, financial condition, earnings or competitive position. However, until such time as future regulations are issued and future alternate refrigerants are approved for sale in small cans, a full evaluation of these costs cannot be completed. We will continue to evaluate the impact of the SNAP Program as the EPA issues additional guidance.

Employees

We have approximately

16

ITEM 1A.www.spectrumbrands.com as soon as reasonably practicable after such reports are filed with, or furnished to, the United States Securities and Exchange Commission (the “SEC”). You may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains an Internet site that contains our reports, proxy statements and other information at www.sec.gov . In addition, copies of our (i) Corporate Governance Guidelines, (ii) charters for the Audit Committee, Compensation Committee and Nominating and Corporate Governance Committee, (iii) Code of Business Conduct and Ethics and (iv) Code of Ethics for the Principal Executive Officer and Senior Financial Officers are available at our Internet site at www.spectrumbrands.com under “Investor Relations—Corporate Governance.” Copies will also be provided to any stockholder upon written request to the Vice President, Investor Relations & Corporate Communications, Spectrum Brands, Inc. at 3001 Deming Way, Middleton, Wisconsin 53562 or via electronic mail at investorrelations@spectrumbrands.com, or by contacting the Vice President, Investor Relations & Corporate Communications by telephone at (608) 275-3340.

Any of the following factors could materially and adversely affect our business, financial condition and results of operations and theoperations. The risks described below are not the only risks that we may face. Additional risks and uncertainties not

Our substantial indebtedness may limit our financial and operating flexibility, and we may incur additional debt, which could increase the risks associated with our substantial indebtedness.

We have, and we expect to continue to have, a significant amount of indebtedness. As of

September 30,· | require us to dedicate a large portion of our cash flow to pay principal and interest on our indebtedness, which will reduce the availability of our cash flow to fund working capital, capital expenditures, research and development expenditures and other business activities; |

· | increase our vulnerability to general adverse economic and industry conditions; |

· | limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; |

· | restrict our ability to make strategic acquisitions, dispositions or to exploit business opportunities; |

· | place us at a competitive disadvantage compared to our competitors that have less debt; and |

· | limit our ability to borrow additional funds (even when necessary to maintain adequate liquidity) or dispose of assets. |

Under the Senior Secured Facilitiessenior secured facilities and the indentures governing the Notesnotes (together, the “Indentures”), we may incur additional indebtedness. If new debt is added to our existing debt levels, the related risks that we now face would increase.

Furthermore, a substantial portion of our debt bears interest at variable rates. If market interest rates increase, the interest rate on our variable rate debt will increase and will create higher debt service requirements, which would adversely affect our cash flow and could adversely impact our results of operations. While we may enter into agreements limiting our exposure to higher debt service requirements, any such agreements may not offer complete protection from this risk.

Restrictive covenants in the Senior Secured Facilitiessenior secured facilities and the Indentures may restrict our ability to pursue our business strategies.

The Senior Secured Facilitiessenior secured facilities and the Indentures each restrict, among other things, asset dispositions, mergers and acquisitions, dividends, stock repurchases and redemptions, other restricted payments, indebtedness and preferred stock, loans and investments, liens and affiliate transactions. The Senior Secured Facilitiessenior secured facilities and the Indentures also contain customary events of default. These covenants could, among other things, limit our ability to fund future working capital and capital expenditures, engage in future acquisitions or development activities, or otherwise realize the value of our assets and opportunities fully because offully. In addition, the needsenior secured facilities and the Indentures require us to dedicate a portion of cash flow from operations to payments on debt. In addition,debt and also contain borrowing restrictions based on, among other things, our fixed charge coverage ratio. Furthermore, the Senior Secured Facilities containcredit agreement governing our senior secured facilities contains a financial covenantscovenant relating to maximum leverageleverage. Such requirements and minimum interest coverage. Such covenants could limit the flexibility of our restricted entities in planning for, or reacting to, changes in the industries in which they operate. Our ability to comply with these covenants is subject to certain events outside of our control. If we are unable to comply with these covenants, the lenders under our Senior Secured Facilitiessenior secured facilities could terminate their commitments and the lenders under our Senior Secured Facilitiessenior secured facilities or the holders of the Notesnotes could accelerate repayment of our outstanding borrowings and, in either case, we may be unable to obtain adequate refinancing of outstanding borrowings on favorable terms or at all. If we are unable to repay outstanding borrowings when due, the lenders under the Senior Secured Facilitiessenior secured facilities will also have the right to proceed against the collateral granted to them to secure the indebtedness owed to them. If our obligations under the Senior Secured Facilitiessenior secured facilities are accelerated, we cannot assure you that our assets would be sufficient to repay in full such indebtedness.

17

The sale or other disposition by HarbingerHRG Group, Inc. (“HRG”), the holder of a majority of the outstanding shares of our common stock, to non-affiliates of a sufficient amount of the common stock of SB Holdingsthe Company would constitute a change of control under the agreements governing Spectrum Brands’the Company’s debt.

Harbinger Group Inc. (“HRG”)HRG owns a majority of the outstanding shares of the common stock of SB Holdings.the Company. The sale or other disposition by HRG to non-affiliates of a sufficient amount of the common stock of SB Holdingsthe Company could constitute a change of control under certain of the agreements governing Spectrum Brands'the Company's debt, including any foreclosure on or sale of SB Holdings'the Company's common stock pledged as collateral by HRG pursuant to the indenture governing HRG's 7.875% Senior Secured Notes due 2019. Under the Term Loan and the ABL Revolving Credit Facility,senior secured facilities, a change of control is an event of default and, if a change of control were to occur, Spectrum Brandsthe Company would be required to get an amendment toamend these agreementsfacilities to avoid a default. If Spectrum Brandsthe Company was unable to get such an amendment,amend these facilities, the lenders could accelerate the maturity of each of the Spectrum Brands Term Loan and the ABL Revolving Credit Facility.any outstanding debt under these facilities. In addition, under the indentures governing the Notes,Indentures, upon a change of control of SB Holdings, Spectrum Brandsthe Company, the Company is required to offer to repurchase such notes from the holders at a price equal to 101% of the principal amount of the notes plus accrued interest or obtain a waiver of default from the holders of such notes. If Spectrum Brands wasthe Company were unable to make the change of control offer, or to obtain a waiver of default, it would be an event of default under the indentures that could allow holders of such notes to accelerate the maturity of the notes. See “Risks Related to SB Holdings' Common Stock-The Harbinger Partiesthe risk factor entitled “HRG and HRGits significant stockholders exercise significant influence over us and their interests in our business may be different from the interests of our stockholdersstockholders”” in this Form 10-K.

We face risks related to the current economic environment.

The current economic environment and related turmoil in the global financial system hasin recent years had and may continue to have an impact on our business and financial condition.

Global economic conditions have significantly impacted economic markets within certain sectors, with financial services and retail businesses being particularly impacted. Our ability to generate revenue depends significantly on discretionary consumer spending. It is difficult to predict new general economic conditions that could impact consumer and customer demand for our products or our ability to manage normal commercial relationships with our customers, suppliers and creditors. The recent continuation of aA number of negative economic factors, including constraints on the supply of credit to households, uncertainty and weakness in the labor market and general consumer fears of a continuingnew economic downturn could have a negative impact on discretionary consumer spending. If the economy continues to deterioratedeteriorates or fails to further improve, our business could be negatively impacted, including as a result of reduced demand for our products or supplier or customer disruptions. Any weakness in discretionary consumer spending could have a material adverse effect on our revenues, results of operations and financial condition. In addition, our ability to access the capital markets may be restricted at a time when it could be necessary or beneficial to do so, which could have an impact on our flexibility to react to changing economic and business conditions.

In the last few years, concern over continuing high unemployment, stagnant economic performance and government debt levels in many European Union countries has caused significant fluctuations of the Euro relative to other currencies, such as the U.S. Dollar. Criticism of excessive national debt among certain European Union countries has led to credit downgrades of the sovereign debt of several countries in the region, and uncertainty about the future status of the Euro. DestabilizationContinued weakness of the European economy could lead to a decrease in consumer confidence, which could cause reductions in discretionary spending and demand for our products. Furthermore, sovereign debt issues could also lead to further significant, and potentially longer-term, economic issues such as reduced economic growth and devaluation of the Euro against the U.S. Dollar, any of which could adversely affect our business, financial conditions and operating results.

We depend on key personnel and may not be able to retain those employees or recruit additional qualified personnel.

We are highly dependent on the continuing efforts of our senior management team and other key personnel. Our business, financial condition and results of operations could be materially adversely affected if we lose any of these persons and are unable to attract and retain qualified replacements.

18

We participate in very competitive markets and we may not be able to compete successfully, causing us to lose market share and sales.

We compete with our competitors for consumer acceptance and limited shelf space based upon brand name recognition, perceived product quality, price, performance, product features and enhancements, product packaging and design innovation, as well as creative marketing, promotion and distribution strategies, and new product introductions. Our ability to compete in these consumer product markets may be adversely affected by a number of factors, including, but not limited to, the following:

· | We compete against many well-established companies that may have substantially greater financial and other resources, including personnel and research and development, and greater overall market share than us. |

· | In some key product lines, our competitors may have lower production costs and higher profit margins than us, which may enable them to compete more aggressively in offering retail discounts, rebates and other promotional incentives. |

· | Technological advancements, product improvements or effective advertising campaigns by competitors may weaken consumer demand for our products. |

· | Consumer purchasing behavior may shift to distribution channels, including to online retailers, where we and our customers do not have a strong presence. |

· | Consumer preferences may change to lower margin products or products other than those we market. |

· | We may not be successful in the introduction, marketing and manufacture of any new products or product innovations or be able to develop and introduce, in a timely manner, innovations to our existing products that satisfy customer needs or achieve market acceptance. |

In the consumer battery product category, our primary competitors are Duracell (a brand of Berkshire Hathaway), Energizer and Panasonic (a brand of Matsushita). In the personal care product category, our primary competitors are Braun (a licensed brand of Procter & Gamble), Norelco (a brand of Philips), and Conair, Wahl, and Helen of Troy. In our PET business, our primary competitors are Central Garden & Pet, Mars and Hartz. In the H&G business, our principal national competitors are Scotts, Central Garden & Pet and S.C. Johnson. Our principal national competitors within our small appliances product category include Newell Brands, DeLonghi America, SharkNinja (f/k/a Euro-Pro Operating LLC), NACCO Industries, Inc. and SEB S.A. In the HHI business, our principal competitors are Fortune Brands, Allegion, Masco, Kohler and American Standard. In the GAC business, our primary competitors are Valvoline, Prestone, Turtle Wax, Black Magic, Energizer and store brands.

In addition, in a number of our product lines, we compete with our retail customers, who use their own private label brands, and with distributors and foreign manufacturers of unbranded products. Significant new competitors or increased competition from existing competitors may have lower production costsadversely affect our business, financial condition and higher profit margins than us, which may enable them to compete more aggressively in offering retail discounts, rebates and other promotional incentives.

Some competitors may be willing to reduce prices and accept lower profit margins to compete with us. As a result of this competition, we could lose market share and sales, or be forced to reduce our prices to meet competition. If our product offerings are unable to compete successfully, our sales, results of operations and financial condition could be materially and adversely affected.

We face risks relating to the United Kingdom’s 2016 referendum, which called for its exit from the European Union.

The announcement of products. The acquisition of a business or the rights to market specific products or use specific product names may involve a financial commitment by us, eitherreferendum regarding the United Kingdom’s (“UK”) membership in the formEuropean Union (“EU”) on June 23, 2016 (referred to as “Brexit”), advising for the exit of the UK from the EU, has adversely impacted global markets and foreign currencies. In particular, the value of the Pound Sterling has sharply declined as compared to the US Dollar and other currencies. This volatility in foreign currencies is expected to continue as the UK negotiates and executes its exit from the EU, but there is uncertainty over what time period this will occur. A significantly weaker Pound Sterling compared to the US Dollar could have a significant negative effect on the Company’s business, financial condition and results of operations. The decrease in value to the Pound Sterling and impacts across global markets and foreign currencies may influence trends in consumer confidence and discretionary spending habits, but given the lack of precedent and uncertainty, it is unclear how the implications will affect us.

The UK is expected to remain a member of the EU for some period of time and there is generally not expected to be any immediate change in either EU or UK law as a consequence of the “leave” vote. However, we can provide no assurances that such consequences will not occur. Negotiations will commence to determine the future terms of the UK relationship with the EU, including, among other things, the terms of trade between the UK and the EU. The effects of Brexit will depend on many factors, including any agreements that the UK makes to retain access to EU markets either during a transitional period or more permanently. Brexit could lead to legal uncertainty and potentially divergent national laws and regulations as the UK determines which EU laws to replace or replicate. Any of these effects of Brexit and others we cannot anticipate, could materially and adversely affect our business, business opportunities, results of operations, financial condition, liquidity and cash or equity consideration. In the caseflows.

19

Sales of certain of our products are seasonal and may cause our operating results and working capital requirements to fluctuate.

On a consolidated basis our financial results are approximately equally weighted betweenacross our quarters, however, sales of certain product categories tend to be seasonal. Sales in thefrom our GBA segment, primarily from consumer battery electric shaving and grooming and electric personal care product categories particularly in North America, tend to be concentrated inincrease during the December holiday season (Spectrum’s(the Company’s first fiscal quarter). Demand for hardware and home improvement products increases during the spring and summer construction period (Spectrum's third and fourth fiscal quarters) and demand for pet supplies products remains fairly constant throughout the year. Demand for home and garden control products typically peaks during the first six months of the calendar year (Spectrum’s second and third fiscal quarters). Small Appliances peaks, while small appliances sales increase from July through December primarily due to the increased demand by customers in the late summer for “back-to-school” sales (the Company’s fourth fiscal quarter) and in the fallDecember for the holiday season. Sales from our HHI segment primarily increase during the spring and summer construction period (the Company’s third and fourth fiscal quarters). Sales from our PET segment remain fairly consistent throughout the year with little variation. Sales from our H&G segment and GAC segment typically peak during the first six months of the calendar year (the Company’s second and third fiscal quarters) due to customer seasonal purchasing patterns and timing of promotional activities. As a result of this seasonality, our inventory and working capital needs fluctuate significantly throughout the year. In addition, orders from retailers are often made late in the period preceding the applicable peak season, making forecasting of production schedules and inventory purchases difficult. If we are unable to accurately forecast and prepare for customer orders or our working capital needs, or there is a general downturn in business or economic conditions during these periods, our business, financial condition and results of operations could be materially and adversely affected.

Adverse weather conditions during our peak selling seasonseasons for our home and garden control and auto care products could have a material adverse effect on our Homehome and Garden Business.

Weather conditions in the U.S. have a significant impact on the timing and volume of sales of certain of our lawn and garden and household insecticide and repellent products. For example, periods of dry, hot weather can decrease insecticide sales, while periods of cold and wet weather can slow sales of herbicides. Adverse weather conditions during the first six months of the calendar year (the Company’s second and third fiscal quarters), when demand for home and garden control products typically peaks, could have a material adverse effect on our home and garden business and our financial results during such period. Weather can also influence customer behavior for our auto care products, especially with appearance and A/C recharge products, which sell best during warm, dry weather. There could be a material adverse effect on the auto care segment if the weather is cold or wet, during the spring and summer seasons when demand typically peaks.

We are subject to significant international business risks that could hurt our business and cause our results of operations to fluctuate.

Approximately 36% of our net sales for the fiscal year ended September 30, 2016 were to customers outside of the U.S. Our pursuit of international growth opportunities may require significant investments for an extended period before returns on these investments, if any, are realized. Our international operations are subject to risks including, among others:

· | currency fluctuations, including, without limitation, fluctuations in the foreign exchange rate of the Euro, British Pound, Brazilian Real, Canadian Dollar, Australian Dollar, Japanese Yen and the Mexican Peso; |

· | changes in the economic conditions or consumer preferences or demand for our products in these markets; |

· | the risk that because our brand names may not be locally recognized, we must spend significant amounts of time and money to build brand recognition without certainty that we will be successful; |

· | labor unrest; |

· | political and economic instability, as a result of war, terrorist attacks, pandemics, natural disasters or otherwise; |

· | lack of developed infrastructure; |