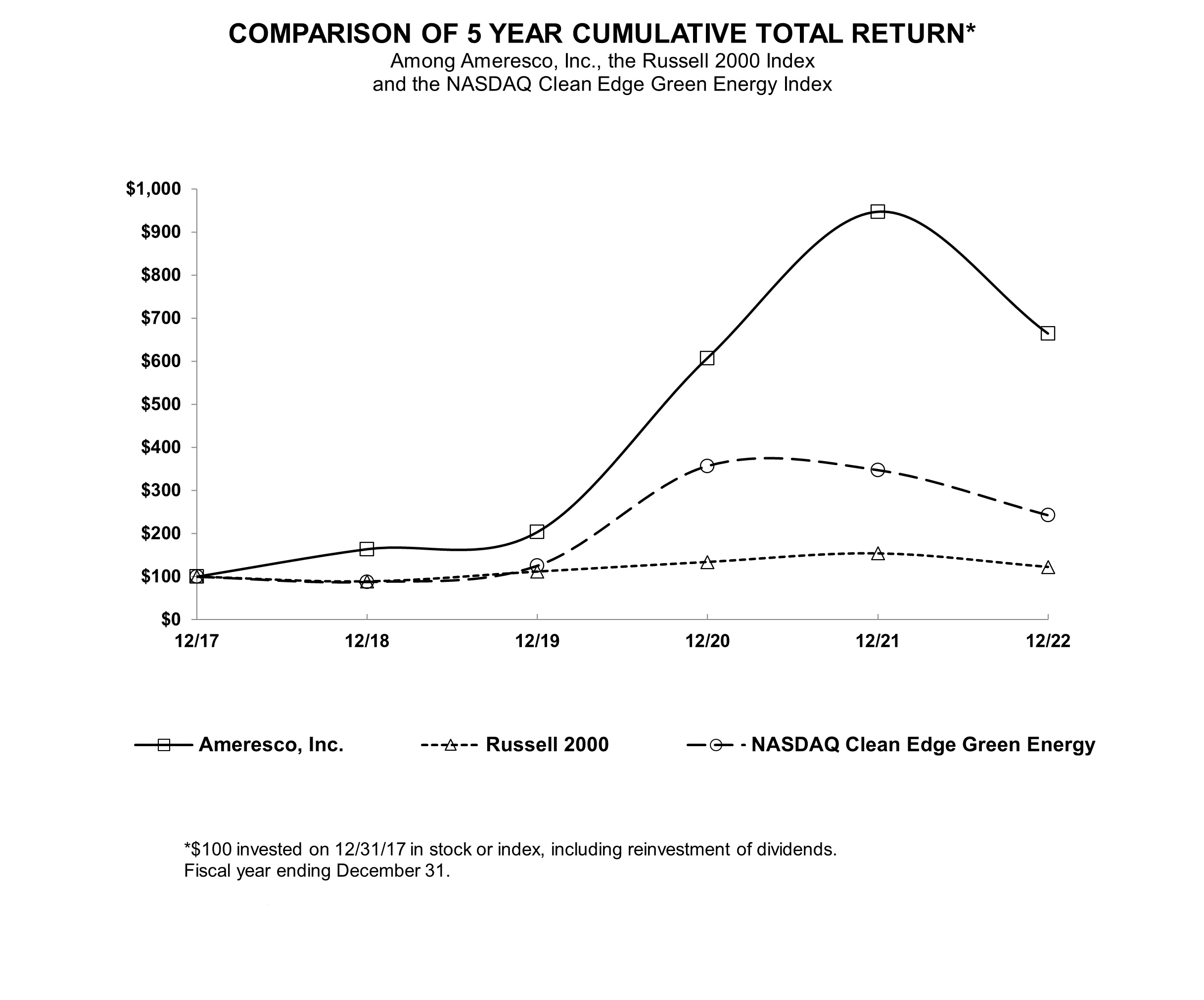

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

|

| | | | | | | |

þ☒ | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20192022

OR

|

| | | | | | | |

o☐ | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ___________ to ___________.

Commission File Number: 001-34811

Ameresco, Inc.

(Exact name of registrant as specified in its charter)

|

| | | | | | | |

| Delaware | | 04-3512838 |

(State or Other Jurisdiction of

Incorporation or Organization)

| | (I.R.S. Employer

Identification No.)

|

111 Speen Street, Suite 410 Framingham, Massachusetts | | 01701 |

| (Address of Principal Executive Offices) | | (Zip Code) |

(508) 661-2200

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

|

| | | | | | | |

| Title of each class | Trading Symbol | Name of each exchange on which registered |

Class A Common Stock, par value $0.0001 per share | AMRC | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o☑ No þ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o☐ No þ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes þ☑ No o☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ☑ No o☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Annual Report on Form 10-K or any amendment to this Annual Report on Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | | | | |

| Large Accelerated Filer | ☑ | Accelerated Filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | ☐ |

| Emerging growth company | ☐ | | | | | | |

Large Accelerated Filer o

| Accelerated Filer þ

| Non-accelerated filer o

| Smaller reporting company o

|

Emerging growth company o

| | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuentpursuant to Section 13(a) of the Exchange Act. o | |

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o☐ No þ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. Yes ☐ No ☑

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). Yes ☐ No ☑

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold on the New York Stock Exchange on June 28, 2019,30, 2022, the last business day of the registrant’s most recently completed second fiscal quarter, was $322,112,989.$1,447,717,111.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock as of the latest practicable date.

|

| | | | |

| Class | Shares outstanding as of March 2, 2020February 24, 2023 |

| Class A Common Stock, $0.0001 par value per share | 29,380,39533,948,362 |

| Class B Common Stock, $0.0001 par value per share | 18,000,000 |

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement for our 20202023 annual meeting of stockholders are incorporated by reference into Part III.

AMERESCO, INC.

TABLE OF CONTENTS

NOTE ABOUT FORWARD LOOKINGFORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (”Form 10-K” or “Report”) contains “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (“the Exchange Act”). All statements, other than statements of historical fact, including statements regarding our strategy, future operations, future financial position, future revenues, projected costs, prospects, plans, objectives of management, expected market growth and other characterizations of future events or circumstances are forward-looking statements. These statements are often, but not exclusively, identified by the use of words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “could,” “estimate,” “target,” “project,” “predict” or “continue,” and similar expressions or variations. These forward-looking statements include, among other things, statements about:

•our expectations as to the future growth of our business and associated expenses;expenses,

•our expectations as to revenue generation;generation,

•the future availability of borrowings under our revolving credit facility;facility,

•the expected future growth of the market for energy efficiency and renewable energy solutions;solutions,

•our backlog, awarded projects and recurring revenue and the timing of such matters;matters,

•our expectations as to acquisition activity;activity,

•the impact of any restructuring;restructuring,

•the uses of future earnings;earnings,

•our intention to repurchase shares of our Class A common stock;

•the expected energy and cost savings of our projects; andprojects,

•the expected energy production capacity of our renewable energy plants.plants,

•the impact of the ongoing macroeconomic challenges, including supply chain disruptions, and shortage of materials, and

•the impact of the U.S. Department of Commerce’s solar panel import investigation

•the impact of regulation, including the IRA

These forward-looking statements are based on current expectations and assumptions that are subject to risks, uncertainties, and other factors that could cause actual results and the timing of certain events to differ materially and adversely from the future results expressed or implied by such forward-looking statements. Risks, uncertainties, and factors that could cause or contribute to such differences include, but are not limited to, those discussed in the section titled “Risk Factors,” set forth in Item 1A of this Annual Report on Form 10-K and elsewhere in this report.Report. The forward-looking statements in this Annual Report on Form 10-K represent our views as of the date of this Annual Report on Form 10-K.Report. Subsequent events and developments may cause our views to change. However, while we may elect to update these forward-looking statements at some point in the future, we have no current intention of doing so and undertake no obligation to do so except to the extent required by applicable law. You should, therefore, not rely on these forward-looking statements as representing our views as of any date subsequent to the date of this Annual Report on Form 10-K.

ADDITIONAL NOTES

The terms “Ameresco,” “Company,” “we,” “our,” “us,” or “ourselves” included in this Report mean Ameresco, Inc. and its consolidated subsidiaries, collectively.

Rounding adjustments applied to individual numbers and percentages shown in this Report may result in these figures differing immaterially from their absolute values.

PART I

Item 1. Business

Company Overview

Founded in 2000, Ameresco Inc. is a leading independent provider ofclean technology integrator and renewable energy asset developer, owner, and operator. Our comprehensive energy services, includingportfolio includes energy efficiency, infrastructure upgrades, energy security and resilience, asset sustainability, and renewable energy solutions.

Our core offerings include the development, design, arrangement of financing, construction, and installation of solutions for businessesthat deliver measurable cost and organizations throughout North Americaenergy savings while enhancing the operations, energy security, infrastructure, and Europe. Ameresco’s sustainability services include capital and operationalresiliency of a facility. These solutions range from upgrades to a facility’s energy infrastructure andto the development, construction, ownership and operation of renewable energy plants. Ameresco has successfully completedAs a trusted sustainability partner, we are always on a mission to help customers lower their overall carbon footprint and reduce their environmental impact.

Our product independence coupled with our deep technical bench allows us to integrate best-in-class advanced technology solutions for the unique needs of each customer.

Drawing from decades of experience, we develop these tailored energy saving, environmentally responsible projects withfor federal, state, and local governments, educational and healthcare and educational institutions, airports, public housing authorities, commercial/industrial customers, transportation and commercialinfrastructure, and industrial customers. With its corporate headquarters in Framingham, MA, Ameresco has more than 1,100 employeesutilities across more than 70 offices providing local expertise in the United States, Canada, and the United Kingdom.Kingdom, and Europe.

StrategicWe have sourced and raised approximately $4.5 billion in project financing while delivering $13.0 billion in energy solutions since our inception. Our growth is driven by staying ahead of the curve and at the leading edge of innovation taking place in the energy sector, offering new products and services to new and existing customers.

In addition to organic growth, strategic acquisitions of complementary businesses and assets, haveand entering into joint venture arrangements has been, and continues to be an important part ofcomponent to our historical development. Since inception, we have completed numerous acquisitions, which have enabledgrowth strategy. These strategies enable us to broaden our service offerings and expand our geographical reach.

To best serve our expansive customer base, we have approximately 60 regional offices located throughout North America and the United Kingdom and more than 1,300 dedicated energy and business professionals with years of proven experience and a strong commitment to customer satisfaction. We offer our customers the resources needed to successfully plan, finance, execute and operate energy programs to create sustained economic and operating benefits to fulfill their unique requirements.

Our principalServices

Our portfolio of service isand product offerings aim to create value and provide energy efficient and renewable solutions to the organizations we serve in the pursuit of a sustainable future.

Energy Efficiency Measures & Upgrades

•Water management, efficiency and reclamation

•Renewable energy, storage & microgrids

•Heating, ventilation, cooling, building envelope

•Smart metering and controls

•Chillers and boilers

Renewable Energy, Storage & Microgrids

•Solar photovoltaic (“PV”)

•Combined heat and power (“CHP”) and co-generation plants

•Geothermal

•Renewable natural gas (“RNG”)

•Wind power

•Microgrid

•Battery storage

•EV charging infrastructure

•Hydrogen

Energy Infrastructure

•Smart building modernization and retrofits

•Design-build new construction

•Utilize a full range of technologies related to building systems, facility infrastructure, energy- and water-consuming systems

•Integrated project design and implementation

Energy Analytics & Supply

•Enterprise energy management services

•Proprietary asset management software

•Energy procurement services

Operations & Maintenance (“O&M”)

•End-to-end technical guidance

•Skilled technicians to operate and maintain renewable energy systems

Our core services are the development, design, engineering, and installation of projects thatdesigned to reduce the energy and operations and maintenance (“O&M”)&M costs of our customers’ facilities. These projects generally include a variety of measures that incorporate innovative technology and techniques, customized for the facility and designed to improve the efficiency of major building systems, such as heating, ventilation, cooling and lighting systems, while enhancing the comfort and usability of the buildings. Such measures may include a combination of the following: water reclamation, light-emitting diode (“LED”) lighting, smart metering, intelligent micro-grids, battery storage, combined heat and power (“CHP”) or the installation of renewable energy, such as solar photovoltaic (“PV”).

We also offer the ability to incorporate analytical tools thatdesigned to provide improved building energy management capabilities and enable customers to identify opportunities for energy cost savings. We typically commit to customers that our energy efficiency projects will satisfy agreed upon performance standards upon installation or achieve specified increases in energy efficiency. In most cases,Generally, the forecasted lifetime energy and operating cost savings of the energy efficiency measures we install willare designed to defray all or almost all of the cost of such measures. In many cases, we assist customers in obtaining private third-party financing, grants, or rebates for the cost of constructing the facility improvements, resulting in little or no upfront capital expenditure by the customer. After a project is complete, we may operate, maintain and repair the customer’s energy systems under a multi-year O&M contract, which providesdesigned to provide us with recurring revenue and visibility into the customer’s evolving needs.

We alsoIn addition, we serve certain customers by developing and building small-scale renewable energy plants located at or close to a customer’s site. Depending uponon the customer’s preference, we will either retain ownership of the completed plant or build it for the customer. Most of our small-scale renewable energy plants to date consist of solar PV installations and plants constructed adjacent to landfills, that use landfill gas (“LFG”) to generate energy. We have also designeddesign and built, as well asbuild, and own, operate and maintain plants that utilize biogas from wastewater treatment processes. Our largest renewable energy project that we operate for a customer uses biomass as the primary source of energy. In the case of most of the plants that we own, the electricity, thermal energy or processed renewable gas fuel generated by the plant is sold under a long-term supply contract with the customer, which is typically a utility, municipality, industrial facility or other purchaser of large amounts of energy. For information on how we finance the projects that we own and operate, please see the disclosures under Note 2, “Summary of Significant Accounting Policies”, Note 9, “Long-Term Debt”“Debt and Financing Lease Liabilities” and Note 11, “Investment Funds”“Variable Interest Entities and Equity Method Investments” to our Consolidated Financial Statements appearingconsolidated financial statements in Item 8 of this Annual Report on Form 10-K.Report.

As of December 31, 2019, we had backlog of approximately $1,107.6 million in expected future revenues under signed customer contracts for the installation or construction of projects, which we sometimes refer to as fully-contracted backlog. We also had been awarded projects for which we had not yet signed customer contracts, which we sometimes refer to as awarded projects, with estimated total future revenues of an additional $1,160.4 million. As of December 31, 2018, we had backlog of approximately $726.6 million in expected future revenues under signed customer contracts for the installation or construction of projects. We also had been awarded projects for which we had not yet signed customer contracts, with estimated total future revenues of an additional $1,241.4 million. As of December 31, 2017, we had backlog of approximately $572.5 million in expected future revenues under signed customer contracts for the installation or construction of projects. We also had been awarded projects for which we had not yet signed customer contracts with estimated total future revenues of an additional $1,199.0 million. The contracts reflected in our fully-contracted backlog typically have a construction period of 12 to 36 months and we typically expect to recognize revenue for such contracts over the same period. Where we have been awarded a project, but have not yet signed a customer contract for that project, we would not begin recognizing revenue unless and until a

customer contract has been signed and we treat the project as fully-contracted backlog. Recently, awarded projects typically have been taking 12 to 24 months from award to having a signed contract and thus convert to fully-contracted backlog. It may take longer, however, depending upon the size and complexity of the project. Generally, the larger and more complex the project, the longer it takes to take it from award to signed contract. Historically, approximately 90% of our awarded projects ultimately have resulted in a signed contract.

See “We may not recognize all revenues from our backlog or receive all payments anticipated under awarded projects and customer contracts” and “In order to secure contracts for new projects, we typically face a long and variable selling cycle that requires significant resource commitments and requires a long lead time before we realize revenues” in Item 1A, Risk Factors of this Annual Report on Form 10-K.

Revenues generated from backlog, which we refer to as project revenues, were $611.1 million, $545.1 million and $506.6 million for the twelve months ended December 31, 2019, 2018 and 2017, respectively.

We also expect to realize recurring revenues both from long-term O&M contracts and from energy output sales for renewable energy operating assets that we own. In addition, we expect to generate revenues from the sale of photovoltaic solar energy products and systems (“integrated-PV”) and other services, such as consulting services and enterprise energy management services. Information about revenues from these other service and product offerings may be found in Note 20, “Business Segment Information” of our Consolidated Financial Statements included in Item 8 of this Annual Report on Form 10-K, which information is incorporated herein by reference.

Ameresco’sOur Lines of Business

Smart Energy Solutions Projects

Our principal service isSmart Energy Solutions Projects are primarily energy efficiency projects, which entailsentail the design, engineering, and installation of and assisting with the arranging of financing for an ever-increasing array of innovative technologies and techniques designed to improve the energy efficiency and control the operation, of a building’s energy- and water- consumingwater-consuming systems. In certain projects, we also design and construct for a customer a central plant or cogeneration system providing power, heat and/or cooling to a building, or a small-scale plant that produces electricity, gas, heat or cooling from renewable sources of energy.energy for a customer, as well as battery energy storage. Our projects generally range in size and scope from a one-month project to design and retrofit a lighting system to a more complex 30-month36-month project to design and install a central plant or cogeneration system or other small-scale plant. Projects we have constructed or are currently working on include designing, engineering and installing energy conservation and resiliency measures across school buildings; buildings,

large, complex energy conservation, and energy security projects for the federal government;government, and municipal-scale street lighting projects incorporating smart-citysmart city controls.

O&M

After an energy efficiency or renewable energy project is completed, we often provide ongoing O&M services under a multi-year contract.contracts. These services offer end-to-end technical guidance and include operating, maintaining, and repairing facility energy systems, such as boilers, chillers, and building controls, as well as central power and other small-scale plants. For larger projects, we frequently maintain staff on-site to perform these services. In addition to providing O&M services for our own projects, we also provide similar services on projects we did not construct for various customers.

Ameresco-owned Energy Assets

Our service offering also includes the sale of electricity, processed renewable gas fuel, heat or cooling from the portfolio ofAmeresco-owned energy assets are small-scale power plants that we owndevelop, design, construct, finance and operate.own/operate and are included in our consolidated balance sheets. These assets may sell electricity, heat, cooling, processed biogas, or renewable biomethane fuel under short-or long-term contracts. We also offer Energy as a Service (“EaaS”), where we design, construct, finance and own/ operate various energy conservation measures on a customer’s site and sell them the output or availability of these items under a short-or long-term contract.

We have constructed and are currently developing, designing, and constructing a wide range of renewable energy plants using LFG,using:

•biogas (generated from landfills, wastewater treatment biogas, solar, plants, and the agricultural sector)

•advanced biofuels

•biomass and other bio-derived fuels

•solar PV

•wind and hydro sources of energy. energy

•battery storage

Most of our renewable energy projectsassets to date have involved the generation of and sale of:

•electricity from solar PV and LFG or battery storage

•electricity, thermal, renewable fuel, or biomethane using biogas as a feedstock

In the salecase of processed LFG. Weour biogas-fueled projects, we purchase the LFGbiogas that otherwise would be combusted or vented, process it, and either selluse it or use itas a renewable fuel source in our energy plants.plants to produce and sell electricity and/or thermal, or sell it as a renewable fuel source to a third party. We have also designeddesign and built, as well as own,build, and operate and maintain plantsfacilities that takeprocess biogas generated in the anaerobic digesters of wastewater treatment plants and turn it into biomethane (or renewable natural gas that is either used to generate energy on-site orgas) that can be soldtransported, primarily through the nation’s natural gas pipeline grid. Where we owngrid or in some cases through tanker trucks, and operate energy producing assets, we typically enter into a long-term power purchase agreement (“PPA”)sold to third parties. The rights to use the site for the saleplant and the purchase of raw feedstock fuel for the energy.plant are also obtained by us under long-term agreements with terms at least as long as the associated output supply agreement. Our supply agreements typically provide for fixed prices or prices that escalate at a fixed rate or vary based on a market benchmark. See “We may assume responsibility under customer contracts for factors outside our control, including, in connection with some customer projects, the risk that fuel prices will increase” in Item 1A, Risk Factors.

As of December 31, 2019,2022, we owned and operated 99162 small-scale renewable energy plants and solar PV installations. Of the owned plants, 23 are renewable LFG plants, 2 are wastewater biogas plants, and 74 are solar PV installations. The 99 small-

scale renewable energy plants andincluding solar PV installations that we own have the capacity towhich generate electricity or deliver renewable gas fuel producing an aggregatewith a combined capacity of more than 259approximately 389 megawatt equivalents.equivalents (“MWe”) and have energy assets in development and construction with a combined capacity of approximately 530 MWe, which includes 60 MWe attributable to a non-controlling interest.

The table below shows the type and number of plants we owned and operated as of December 31, 2022:

| | | | | |

| Plants Owned and Operated | Quantity |

| Biogas: RNG | 4 |

| Biogas: non-RNG | 22 |

| Solar and battery assets | 132 |

| Other | 4 |

| |

| Total plants owned and operated | 162 |

Other

Our serviceother lines of business include photovoltaic solar energy products and product offerings also include integrated-PV andsystems (“integrated-PV”), consulting, and enterprise energy management services.

Customer Arrangements

Energy Savings Performance Contracts (“ESPCs”)

For our energy efficiency projects, we typically enter into energy savings performance contracts (“ESPCs”),ESPCs, under which we agree to develop, design, engineer and construct a project for a customer and also commit that the project will satisfy agreed upon performance standards that vary from project to project. These performance commitments are typically based on the design, capacity, efficiency, or operation of the specific equipment and systems we install. Our commitments generally fall into three categories:

•Pre-agreed energy reduction commitment: our customer reviews the project design in advance and agrees that, upon or shortly after completion of the installation of the specified equipment comprising the project, the commitment will have been met.

•Equipment-level commitment: we commit to a level of energy use reduction based on the difference in use measured first with the existing equipment and then with the replacement equipment.

•Whole building-level commitment: requires demonstration of energy usage reduction for a whole building, often based on readings of the utility meter where usage is measured. Depending on the project, the measurement and demonstration may be required only once, upon installation, based on an analysis of one or more sample installations, or may be required to be repeated at agreed upon intervals generally over periods of up to 25 years. We often assist these customers in identifying and obtaining financing through rebate programs, grant programs, third-party lenders, and other sources.

Under our contracts, we typically do not take responsibility for a wide variety of factors outside of our control and exclude or adjust for such factors in commitment calculations. These factors include, among others, variations in energy prices and utility rates, weather, facility occupancy schedules, the amount of energy-using equipment in a facility, and the failure of the customer to operate or maintain the project properly. Typically, our performance commitments apply to the aggregate overall performance of a project rather than to individual energy efficiency measures. Therefore, to the extent an individual measure underperforms, it may be offset by other measures that overperform during the same period. In the event that an energy efficiency project does not perform according to the agreed upon specifications, our agreements typically allow us to satisfy our obligation by adjusting or modifying the installed equipment, installing additional measures to provide substitute energy savings or paying the customer for lost energy savings based on the assumed conditions specified in the agreement. Many of our equipment supply, local design, and installation subcontracts contain provisions that enable us to seek recourse against our vendors or subcontractors if there is a deficiency in our energy reduction commitment. See “We may have liability to our customers under our ESPCs if our projects fail to deliver the energy use reductions to which we are committed under the contract” in Item 1A, Risk Factors.

The projects that we perform for governmental agencies are governed by particular qualification and contracting regimes. Certain states require qualification with an appropriate state agency as a precondition to performing work or appearing as a qualified energy service provider for state, county, and local agencies within the state. For example, the Commonwealth of Massachusetts and the states of Colorado and Washington pre-qualify energy service providers and provide contract documents that serve as the starting point for negotiations with potential governmental clients.customers. Most of the work that we perform for the federal government is performed under indefinite delivery, indefinite quantityIndefinite Delivery, Indefinite Quantity (“IDIQ”) and Multiple Award Construction Contract agreements between government agencies and us or our subsidiaries.us. These IDIQ agreements allow us to contract with the relevant agencies to implement energy and infrastructure projects, but no work may be performed unless we and the agency agree on a task order or delivery order governing the provision of a specific project. The government agencies enter into contracts for specific projects on a competitive basis. We and our subsidiaries and affiliates are currently partyparties to an IDIQ agreement with the U.S. Department of Energy (“DOE”) expiring Aprilin 2026. We are also party to agreements with other federal agencies, including the U.S. Army Corps of Engineers, the Naval Facilities Engineering Command (NAVFAC) Mid-Atlantic, and the U.S. General Services Administration.

Payments by the federal government for energy efficiency measures are based on the services provided and the products installed but are limited to the savings derived from such measures, calculated in accordance with federal regulatory guidelines and the specific contract’s terms. The savings are typically determined by comparing energy use and other costs before and after the installation of the energy efficiency measures, adjusted for changes that affect energy use and other costs but are not caused by the energy efficiency measures.

Energy Supply Contracts

For the energy assets that we own and operate, we generally enter into (i) long-term power purchase agreements (“PPAs”) to supply electricity, (ii) long-term energy supply agreements (“ESAs”) to supply medium British Thermal Unit (“BTU”) biogas or thermal energy, (iii) gas purchase agreements (“GPAs”) to supply RNG, or (iv) EaaS contracts where we sell the output or availability of various energy conservation measures to third parties.

The third parties we enter into PPAs, ESAs, or EaaS contracts with include but are not limited to municipalities, the Federal government, commercial and industrial customers, or utilities. The third parties we sell RNG to include, but are not limited to, brokers, traders, utilities, municipalities, industrial facilities, or other large purchasers of energy.

Our Business Segments

Our company is primarily organized by region, where each region may perform our key services under our various lines of business. Our reportable business segments largely follow our regional segmentation. For the year ended December 31, 2022 our reportable business segments were as follows:

•U.S. Regions

•U.S. Federal

•Canada

•Alternative Fuels (formerly Non-Solar Distributed Generation)

•All Other

On January 1, 2022, we changed the structure of our internal organization and our “All Other” segment now includes our U.S.-based enterprise energy management services previously included in our U.S Regions segment and our U.S. Regions segment now includes U.S. project revenue and associated costs previously included in our former Non-Solar DG segment. As a result, previously reported amounts have been reclassified for comparative purposes.

Our U.S. Regions, U.S. Federal and Canada segments offer energy efficiency products and services which may be extended through December 2023.include the design, engineering, and installation of equipment and other measures to improve the efficiency and control the operation of a facility’s energy infrastructure, renewable energy solutions, and services and the development and construction of small-scale plants that we own or develop for customers that produce electricity, gas, heat, or cooling from renewable sources of energy and O&M services.

Our Alternative Fuels segment sells electricity and processed RNG derived from biomethane from small-scale plants that we own and operate, and provides O&M services for customer owned small-scale RNG plants.

The “All Other” category offers enterprise energy management services, consulting services, energy efficiency products and services outside of the U.S. and Canada, and the sale of solar PV energy products and systems which we refer to as integrated-PV.

The table below shows the percentage of revenues by segment for the last three years:

| | | | | | | | | | | | | | | | | |

| 2022 | | 2021 | | 2020 |

% of Revenues by Segment (1) | | | | | |

| U.S. Regions | 61.6 | % | | 45.3 | % | | 41.0 | % |

| U.S. Federal | 21.5 | % | | 32.3 | % | | 36.6 | % |

| Canada | 3.2 | % | | 4.1 | % | | 4.6 | % |

| Alternative Fuels | 6.3 | % | | 9.1 | % | | 8.1 | % |

| All Other | 7.4 | % | | 9.2 | % | | 9.7 | % |

| Total revenues | 100.0 | % | | 100.0 | % | | 100.0 | % |

| | | | | |

| (1) See Note 3 “Revenue from Contracts with Customers” for our disaggregated revenue and Note 20 “Business Segment Information” for additional information. |

Sales and Marketing

Our sales and marketing approach is to offer customers customized and comprehensive energy efficiency solutions tailored to meet their economic, operational, and technical needs. The sales, design and construction process for energy efficiency and renewable energy projects recently has been averaging from 18 to 54 months. We identify project opportunities through referrals, requests for proposals (“RFPs”), conferences and events, website, onlinedigital campaigns, telemarketing, and repeat business from existing customers. Our direct sales force develops and follows up on customer leads. As of December 31, 2019,2022, we had 135180 employees in direct sales.

In preparation for a proposal, our team typically conducts a preliminary audit of the customer’s needs and requirements and identifies areas to enhance efficiencies and reduce costs. We collect and analyze the customer’s utility bill and other data related

to energy use. If the bills are complex or numerous, we often utilize Ameresco’sour proprietary enterprise energy management software tools to scan, compile and analyze the information. Our experienced engineers visit and assess the customer’s current energy systems and infrastructure. Through our knowledge of the federal, state, and local governmental and utility environment,environments, we assess

the availability of energy, utility or environmental-based payments for usage reductions or renewable power generation, which helps us optimize the economic benefits of a proposed project for a customer. Once awarded a project, we perform a more detailed audit of the customer’s facilities, which serves as the basis for the final specifications of the project and final contract terms.

For renewable energy plants that are not built or located on a customer’s site or use sources of energy not within the customer’s control, the sales process also involves the identification of sites with attractive sources of renewable energy and obtaining necessary rights and governmental permits to develop a plant on that site. For example, for LFG projects, we start with gaining control of aan LFG resource located close to the prospective customer. For solar and wind projects, we look for sites where utilities are interested in purchasing renewable energy power at rates that are sufficient to make a project feasible. Where governmental agencies control the site and resource, such as a landfill owned by a municipality, the customer may be required to issue an RFP to use the site or resource. Once we believe we are likely to obtain the rights to the site and the resource, we seek customers for the energy output of the potential project, with whom we can enter into a long-term PPA.

Customers

We strive to be a trusted sustainability partner creating valued, single-sourced, efficient energy solutions delivered with passion, expertise, teamwork, and a relentless focus on customer satisfaction.

Our customers choose to prioritize efficiency and the development of clean, green energy sources and our solutions are customized to serve the specific needs of each customer and meaningfully reduce or offset their carbon footprint. From energy conservation through a variety of measures to the generation of green, renewable power, our customers and their communities reap the benefits of reducing energy consumption, costs, and associated carbon emissions.

In 2019,2022, we served customers throughout the United States, Canada, the United Kingdom (“U.K.”), and Greece. Historically, including for the years ended December 31, 2019, 2018 and 2017, approximately 75%Europe. Approximately 46.0% of our revenues have beenwere derived from federal, state, provincial, or local government entities, including public housing authorities, public universities, and public universities.municipal utilities. Our federal customers include various divisions of the U.S. federal government. The U.S. federal government which is considered a single customer and segment for reporting purposes constituted 33.2%, 31.3% and 32.0% of our consolidated revenues for the years ended December 31,2019, 2018 and 2017, respectively.(see table above under “Our Business Segments”). For the year ended December 31, 2019,2022, our largest 20 customers accounted for approximately 62.7%73.4% of our total revenues. Other than the U.S. federal government, no one customer represented more than 10%39.6% of our revenues during this period.

See “Provisions in our government contracts may harm our business, financial condition and operating results” in Item 1A, Risk Factors for a discussion of special considerations applicable to government contracting.contracting and “The loss of one of our significant customers or our failure to perform on our contract with that customer in accordance with its terms could adversely affect us” in Item 1A, Risk Factors for further discussion.

Competition

While we face significant competition from a large number of companies, we believe that few offer the objective technical expertise and full range of services that we provide.

do.

Our principal competitors for our core business includeinclude:

•Smart Energy Solutions: Constellation NewEnergy (andEnergy Group, Inc. (an Exelon Company)company), Energy Systems Group, Honeywell, Johnson Controls, NORESCO (a unit of Carrier Global Corporation), Schneider Electric, Siemens Building Technologies, and Trane.Trane Technologies (an Ingersoll-Rand company). We compete primarily on the basis of our comprehensive, independent offering of energy efficiency and renewable energy services and the breadth and depth of our expertise.

For•Energy Assets: In the LFG and RNG market our principal competitors primarily include large, national project developers and owners of landfills who self-develop projects using LFG from their own landfills, and other national renewable energy plants, wenatural gas developers/owners such as Archaea Energy, Montauk Renewables, Vanguard Renewables, Opal Fuels, and divisions of large multi-national oil and gas conglomerates. In the Solar PV and Battery Storage market our principal competitors include Borrego Solar Systems, BlueWave Solar, Citizens Energy Group, Nexamp Inc., SunPower Corp., Solect Energy, and Syncarpha Capital. We may also compete primarily with many large independent power producers and utilities, as well as a large number of smaller developers of renewable energy projects. In the LFG market,EaaS, our principal competitors include national project developersEngie, Enel X, Schneider Electric SE, and owners of landfills who self-develop projects using LFG from their landfills. In the solar PV market, our principal competitors are Borrego Solar, BlueWave Solar, Citizens Energy, Clean Energy Collective, Nexamp, SunPower Corp., Solect Energy, and Syncarpha Capital.Redaptive, Inc. We compete for renewable energy projects primarily on the basis of our experience, reputation, and ability to identify and complete high quality and cost-effective projects.

For •O&M services, our principal competitors areServices: EMCOR Group,Energy Services, Comfort Systems USA, Honeywell, Johnson Controls, and Veolia. In this area, we compete primarily on the basis of our expertise and quality of service.

See “We operate in a highly competitive industry, and our current or future competitors may be able to compete more effectively than we do, which could have a material adverse effect on our business, revenues, growth rates, and market share” in Item 1A, Risk Factors for further discussion of competition.

Regulatory

Various regulations affect the conduct of our business. Federal and state legislation and regulations enable us to enter into ESPCs with government agencies in the United States. The applicable regulatory requirements for ESPCs differ in each state and between agencies of the federal government.

We are also subject to local regulations in the international jurisdictions where we operate, including Canada, the United Kingdom, and Greece.

Our projects must conform to all applicable electric reliability, building and safety, and environmental regulations and codes, which vary from place to place and time to time. Various federal, state, provincial, and local permits are required to construct an energy efficiency project or renewable energy plant.

Renewable energy projects are also subject to specific governmental safety and economic regulation. States and the federal government typically do not regulate the transportation or sale of LFG unless it is combined with and distributed with natural gas, but this is not uniform among states and may change from time to time. States regulate the retail sale and distribution of natural gas to end-users, although regulatory exemptions from regulation are available in some states for limited gas delivery activities, such as sales only to a single customer. The sale and distribution of electricity at the retail level is subject to state and provincial regulation, and the sale and transmission of electricity at the wholesale level is subject to federal regulation. While we do not own or operate retail-level electric distribution systems or wholesale-level transmission systems, the prices for the products we offer can be affected by the tariffs, rules and regulations applicable to such systems, as well as the prices that the owners of such systems are able to charge. The construction of power generation projects typically is regulated at the state and provincial levels, and the operation of these projects also may be subject to state and provincial regulation as “utilities.” At the federal level, the ownership and operation of, and sale of power from, generation facilities may be subject to regulation under the Public Utility Holding Company Act of 2005 (“PUHCA”), the Federal Power Act (“FPA”), and Public Utility Regulatory Policies Act of 1978 (“PURPA”). However, because all of the plants that we have constructed and operated to date are small power “qualifying facilities” under PURPA, they are subject to less regulation under the FPA, PUHCA and related state utility laws than traditional utilities.

If we pursue projects employing different technologies or with a single project electrical capacity greater than 20 megawatts, we could become subject to some of the regulatory schemes which do not apply to our current projects. In addition, the state, provincial, and federal regulations that govern qualifying facilities and other power sellers frequently change, and the effect of these changes on our business cannot be predicted.

LFG power generation facilities require an air emissions permit, which may be difficult to obtain in certain jurisdictions. See “Compliance with environmental laws could adversely affect our operating results” in Item 1A, Risk Factors. Renewable energy projects may also be eligible for certain governmental or government-related incentives from time to time, including tax credits, cash payments in lieu of tax credits, and the ability to sell associated environmental attributes, including carbon credits. Government incentives and mandates typically vary by jurisdiction.

Some of the demand reduction services we provide for utilities and institutional clientscustomers are subject to regulatory tariffs imposed under federal and state utility laws. In addition, the operation of, and electrical interconnection for, our renewable energy projects are subject to federal, state, or provincial interconnection and federal reliability standards also set forth in utility tariffs. These tariffs specify rules, business practices, and economic terms to which we are subject. The tariffs are drafted by the utilities and approved by the utilities’ state, provincial, or federal regulatory commissions.

EmployeesSee our section entitled “Risks related to Regulations or Governmental Actions” in Item 1A, Risk Factors.

Human Capital Management

We believe our employees are Ameresco’s greatest resource, as they come together to creatively integrate our advanced technology portfolio and develop innovative, transformative energy solutions for our customers.

The diversity of our team coupled with our deep bench of technical expertise enables us to tackle the most complex energy opportunities. Supporting our employees and the communities in which we serve is paramount to our success.

We focus on team-based employee philanthropy, wellness-focused employee benefits, and donating our time to our local communities through education and training.

As of December 31, 2019,2022, we had a total of 1,1271,363 employees based in offices located in 3946 U.S. states, including the District of Columbia, foursix Canadian provinces, and four office locations throughout the U.K.United Kingdom

Philanthropic Activities

We actively participate in philanthropic activities that support our local communities and provide an opportunity for dynamic team building. During 2022, our employees were encouraged to use paid community service days to donate time and creative energy to the organizations that touch them personally and to give back to the environment and their communities. As a result, we experienced increased participation in both volunteer activities and employee match charitable giving.

Diversity, Equity, Inclusion and Justice

We welcome, support, and celebrate unique ways of thinking. We believe innovation demands diversity of thought, and Ameresco has done well by welcoming and celebrating employees from diverse backgrounds. We are proud to be an equal opportunity workplace and an Affirmative Action employer.

To educate, support, and promote the culture of diversity, equity, inclusion and justice at Ameresco, diversity in the workplace is discussed at all levels in the organization. Annual diversity in the workplace training is rolled out to all Ameresco employees. This comprehensive training is critical to ensuring we are focused on educating our teams and fostering a culture that is all-inclusive.

Recruiting is a key element in our commitment to diversity, equity, inclusion and justice. Our talent team focuses on attracting and recruiting a diverse workforce by partnering with organizations such as the National Society of Women in Construction, Browning The Green Space, New England Women in Energy and the Environment, Hire Heroes USA, and Dolce Center for Advancement of Veterans and Service Members.

During the year ended December 31, 2022, our global workforce is made up of 22% female, 77% male, and 1% not declared. In addition, 33% of our executive management team are female and 21% of our managers are female.

Benefits with a Purpose

The health, safety, and well-being of our employees continues to be a top priority at Ameresco. In addition to competitive salaries, we are committed to regularly evaluating a competitive benefits portfolio, striving to provide resources to our employees that assist with work-life balance.

While employee healthcare costs and access to a wide variety of doctors have always been at the top of our criteria list, we also continued to focus our 2022 benefit offerings on our mental health and well-being offerings. We wanted to ensure our employees have a variety of help and resources available, offered in platforms and services they felt comfortable using, should they need it.

In addition, we offered a comprehensive Employee Assistance Plan to all Ameresco employees and their family members should they need assistance with any life planning matters. And in support of some of the new applications and corporate programs, we rolled out memberships to Care.com, Gympass, and Headspace and Virgin Pulse mobile apps.

Energy Outside the Office

Whether it is through our philanthropic activities, our quest to provide an inclusive culture, or our focus on the well-being of our people, Ameresco benefits from the open communication seen between our employees. We encourage activities outside of our offices to enhance the employee experience.

Career Advancement

Ameresco strives to implement creative ways for our employees to support career advancement. To facilitate our employees’ career development with a focus on retention, we have improved on the frequency of career path discussions, training, and succession planning. To expand on the career training offered in 2021, we offered performance management training to employees and managers during 2022. The career path discussions identified specific training programs, mentorship opportunities, continued degree programs and certification programs – all of which will provide the tools necessary to assist our employees in their career development.

When it comes to the innovative solutions that we deliver to our customers, it is critical for the Ameresco team to be at the forefront. Every month our Corporate Marketing Team hosts a Center of Excellence in Advance Technology training session available to all employees. Each session features a different topic to cover various aspects of Ameresco’s solution portfolio and is presented by our internal subject matter experts. All employees are encouraged to attend live and participate in the Q&A.

In 2022, we continued to further integrate and invest in our Learning Management System (“LMS”) in our Workday Enterprise Management platform to centralize and have the capability to measure development metrics such as training hours per employee.

We provide a tuition reimbursement program to support career development within our organization. In addition, we support employee growth by investing in career advancing certification programs for our employees.

For more information on our initiatives noted above, please see our 2022 Environmental, Social and Governance Report which will be available at www.ameresco.com.

Seasonality

See “Our business is affected by seasonal trends and construction cycles, and these trends and cycles could have an adverse effect on our operating results” in Item 1A, Risk Factors and “Overview — Effects of Seasonality” in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations” for a discussion of seasonality in our business.

Segments and Geographic Information

Financial information about our domestic and international operations and about our segments may be found in Note 16, “Geographic Information” and 20, “Business Segment Information” respectively, of our Consolidated Financial Statementsconsolidated financial statements included in Item 8 of this Annual Report on Form 10-K, which information is incorporated herein by reference.

Additional Information

Ameresco was incorporated in Delaware in 2000 and is headquartered in Framingham, Massachusetts.

Periodic reports, proxy statements, and other information are available to the public, free of charge, on our website, www.ameresco.com, as soon as reasonably practicable after they have been filed with the Securities and Exchange Commission

(“SEC”), and through the SEC’s website, www.sec.gov. We include our website address in this report only as an inactive textual reference and do not intend it to be an active link to our website. None of the material on our website is part of this Annual Report on Form 10-K.Report.

Executive Officers

The following is a list of our executive officers, their ages as of March 1, 2020 and their principal positions.

|

| | | | | |

Name | | Age | | Position (s) |

George P. Sakellaris | | 73 |

| | Chairman of the Board of Directors, President and Chief Executive Officer |

David J. Anderson | | 59 |

| | Executive Vice President and Director |

Michael T. Bakas | | 51 |

| | Executive Vice President, Distributed Energy Systems |

Nicole A. Bulgarino | | 47 |

| | Executive Vice President and General Manager, Federal Solutions |

David J. Corrsin | | 61 |

| | Executive Vice President, General Counsel and Secretary and Director |

Louis P. Maltezos | | 53 |

| | Executive Vice President |

Spencer Doran Hole | | 51 |

| | Senior Vice President and Chief Financial Officer |

Mark A. Chiplock | | 50 |

| | Vice President of Finance and Chief Accounting Officer |

George P. Sakellaris: Mr. Sakellaris has served as chairman of our board of directors and our president and chief executive officer since founding Ameresco in 2000.

David J. Anderson: Mr. Anderson has served as our executive vice president as well as a director, since 2000 and oversees business development, government relations, strategic marketing and communications, as well as several U.S. business units and U.K. operations.

Michael T. Bakas: Mr. Bakas has served as our executive vice president, distributed energy systems, since November 2017. Mr. Bakas previously served as our senior vice president, renewable energy, from March 2010 to September 2017 and our vice president, renewable energy from 2000 to February 2010.

David J. Corrsin: Mr. Corrsin has served as our executive vice president, general counsel and secretary, as well as a director, since 2000.

Nicole A. Bulgarino: Ms. Bulgarino has served as our executive vice president and general manager of federal solutions since May 2017. Ms. Bulgarino previously served as our senior vice president and general manager of federal solutions from May 2015 to May 2017; vice president and general manager of federal solutions from February 2014 to May 2015; vice president, federal group operations from December 2012 to February 2014; director, implementation from May 2010 to December 2012; and senior engineer from June 2004 to May 2010.

Louis P. Maltezos: Mr. Maltezos has served as executive vice president since April 2009 and oversees Central and Northwest Regions and Canada operations. Mr. Maltezos has also served as the chief executive officer of Ameresco Canada since September 2015 and served as the president of Ameresco Canada from September 2014 to September 2015.

Spencer Doran Hole: Mr. Hole has served as our Senior Vice President and Chief Financial Officer since July 2019. Prior to joining Ameresco, Mr. Hole served as Chief Executive Officer, North America and Group Vice President - Strategy at ReneSola Ltd., a manufacturer and supplier of green energy products, since November 2017 and served as the Chief Financial Officer for the US division of ReneSola since December 2016. Prior to joining ReneSola, Mr. Hole was the founder of Coast to Coast Advisors, an independent financial consultancy practice, assisting investor, lender and developer clients with financing and asset sales. Mr. Hole also served as the Chief Financial Officer of Pristine Sun LLC, a small-scale solar developer, from November 2015 through April 2016, and as a Director at Deutsche Bank from April 2007 through October 2015.

Mark A. Chiplock: Mr. Chiplock has served as Vice President of Finance and Chief Accounting Officer since July 2019. Prior to that, Mr. Chiplock served as our Interim Chief Financial Officer and Treasurer from October 2018 through July 2019 and as our Corporate Controller from June 2014 to December 2019. Prior to Ameresco, he served as Vice President, Finance of GlassHouse Technologies, a data center infrastructure consulting firm, from June 2012 to May 2014.

Item 1A. Risk Factors

We face many risks. If any of the events or circumstances described below actually occur, we and our businesses, financial condition or results of operations could suffer, and the trading price of our Class A Common Stock could decline. Our business is subject to numerous risks. We caution you thatcurrent and potential investors should consider the following important factors, among others, could cause our actual results to differ materially from those expressed in forward-looking statements made by us or on our behalf in filings with the SEC, press releases, communications with investors and oral statements. Any or all of our forward-looking statements in this Annual Report on Form 10-K and in any other public statements we make may turn out to be wrong. They can be affected by inaccurate assumptions we might make or by known or unknown risks and uncertainties. Many factors mentioned in the discussion below will be important in determining future results. Consequently, no forward-looking statement can be guaranteed. Actual future results may differ materially from those anticipated in forward-looking statements. We undertake no obligationinformation contained under the heading “Cautionary Note Regarding Forward-Looking Statements” before deciding to update any forward-looking statements, whether as a result of new information, future events or otherwise, except to the extent required by applicable law. You should, however, consult any further disclosure we makeinvest in our reports filed with the SEC.securities.

Risks Related to Our Business

If demand for our energy efficiency and renewable energy solutions does not develop as we expect, our revenues will suffer, and our business will be harmed.

We believe, and our growth plans assume, that the market for energy efficiency and renewable energy solutions will continue to grow, that we will increase our penetration of this market and that our revenues from selling into this market will continue to increase over time. If our expectations as to the size of this market and our ability to sell our products and services in this market are not correct, our revenues will suffer, and our business will be harmed.

In order to secure contracts for new projects, we typically face a long and variable selling cycle that requires significant resource commitments and requires a long lead time before we realize revenues.

The sales design and construction processcycle for energy efficiency and renewable energy projects recently has been takingin general take from 18 to 5442 months, on average, with sales to federal government and housing authority customers tending to require the longest sales processes. Our sales cycle has been further lengthened as a result of macroeconomic conditions and we cannot predict the timeline for our selling cycle in the current conditions. Our existing and potential customers generally follow extended budgetingbudgeting and procurement processes, and sometimes must engage in regulatory approval processes related to our services. Our customers often use outside consultants and advisors, which contributes to a longer sales cycle. Most of our potential customers issue an RFP, as part of their consideration of alternatives for their proposed project. In preparation for responding to an RFP, we typically conduct a preliminary audit of the customer’s needs and the opportunity to reduce its energy costs. For projects involving a renewable energy plant that is not located on a customer’s site or that uses sources of energy not within the customer’s control, the sales process also involves the identification of sites with attractive sources of renewable energy, such as a landfill or a favorable site for solar PV, and it may involve obtaining necessary rights and governmental permits to develop a project on that site. If we are awarded a project, we then perform a more detailed audit of the customer’s facilities, which serves as the basis for the final specifications of the project. We then must negotiate and execute a contract with the customer. In addition, we or the customer typically need to obtain financing for the project.

This extended sales process requires the dedication of significant time by our sales and management personnel and our use of significant financial resources, with no certainty of success or recovery of our related expenses. A potential customer may go through the entire sales process and not accept our proposal. All of these factors can contribute to fluctuations in our quarterly financial performance and increase the likelihood that our operating results in a particular quarter will fall below investor expectations. These factors could also adversely affect our business, financial condition and operating results due to increased spending by us that is not offset by increased revenues.

We may not recognize all revenues from our backlog or receive all payments anticipated under awarded projects and customer contracts.

As of December 31, 20192022 and December 31, 2018,2021, we had backlog of approximately $1,107.6 million$1.0 billion and $726.6 million,$1.5 billion, respectively, in expected future revenues under signed customer contracts for the installation or construction of projects, which we sometimes refer to as fully-contracted backlog; and we also had been awarded projects for which we do not yet have signed customer contracts with estimated total future revenues of an additional $1,160.4 million$1.6 billion and $1,241.4 million, respectively .$1.5 billion, respectively. As of December 31, 2022 and 2021, we had O&M backlog of approximately $1.2 billion and $1.1 billion, respectively. Our O&M backlog represents expected future revenues under signed multi-year customer contracts for the delivery of O&M services, primarily for energy efficiency and renewable energy construction projects completed by us for our customers.

Our customers have the right under some circumstances to terminate contracts or defer the timing of our services and their payments to us. In addition, our government contracts are subject to the risks described below under “Provisions in government contracts may harm our business, financial condition and operating results.” The payment estimates for projects that have been awarded to us but for which we have not yet signed contracts have been prepared by management and are based upon a number

of assumptions, including that the size and scope of the awarded projects will not change prior to the signing of customer contracts, that we or our customers will be able to obtain any necessary third-party financing for the awarded projects, and that we and our customers will reach agreement on and execute contracts for the awarded projects. We are not always able to enter into a contract for an awarded project on the terms proposed. As a result, we may not receive all of the revenues that we include in the awarded projects component of our backlog or that we estimate we will receive under awarded projects. If we do not receive all of the revenue we currently expect to receive, our future operating results will be adversely affected. In addition, a delay in the receipt of

revenues, even if such revenues are eventually received, may cause our operating results for a particular quarter to fall below our expectations.

Our business depends in partIf we are not able to complete, perform or operate our projects on federal, state, provinciala profitable basis or as we have committed to our customers, we could become subject to liquidated damages, and local government support for energy efficiencyour reputation and renewable energy,our results of operations could be adversely impacted.

Development, installation, and a decline in such support could harmconstruction of our business.

We depend in part on legislation and government policies that support energy efficiency and renewable energy projects, that enhance the economic feasibilityand operation of our energy efficiency services and small-scale renewable energy projects. Thisprojects, entails many risks, including:

•failure or delays in receiving components and equipment that meet our requirements,

•failure or delays in obtaining all necessary rights to land access and use,

•failure or delays in receiving quality performance of contractors and other third-party service providers,

•increases (including as a result of inflation) in the cost of labor, equipment, and commodities needed to construct or operate projects,

•failure or delays in obtaining permitting and addressing other regulatory issues, license revocation, and changes in legal requirements,

•failure or delays in obtaining other governmental support includes legislationor approvals, or in overcoming objections from members of the public or adjoining land owners;

•shortages of equipment or skilled labor,

•unforeseen engineering problems,

•failure of a customer to accept or pay for renewable energy that we supply,

•weather interferences, catastrophic events including fires, explosions, earthquakes, droughts, and regulations that authorizeacts of terrorism; and regulateaccidents involving personal injury or the manner in which certain governmental entities do business with us; encourageloss of life,

•environmental, archaeological or subsidize governmental procurementgeological conditions

•health or similar issues, a pandemic, or epidemic, such as COVID-19,

•labor disputes and work stoppages,

•mishandling of hazardous substances and waste, and other events outside of our services; encouragecontrol.

Any of these factors could give rise to construction delays, costs in excess of our expectations or cause us not to meet commitments given to our customers. We have, for example, experienced disruptions in some casesdevelopment, installation and construction as a result of supply chain and logistics challenges, COVID-19 and the related quarantines, facility closures, and we may continue to experience such disruptions. In addition, the impacts of climate change have caused us to experience more frequent and severe weather interferences which has impacted our construction timelines, and this trend may continue. Furthermore, while the passage of the Inflation Reduction Act (“IRA”) may increase the demand for our service and project offerings, it may also increase demand and cost for labor, equipment and commodities needed for our projects. These factors and events could prevent us from completing construction of our projects, cause defaults under our financing agreements or under contracts that require other customerscompletion of project construction by a certain time, give rise to procure power from renewableliquidated damages or low-emission sources,penalties, cause projects to reduce their electricity usebe unprofitable for us, or otherwise to procure our services; and provide us with tax and other incentives that reduce our costs or increase our revenues. Without this support, on which projects frequently rely for economic feasibility, our ability to complete projects for existing customers and obtain project commitments from new customers could be adversely affected.

A substantial portion of our earnings are derived from the sale of renewable energy certificates (“RECs”) and other environmental attributes, and our failure to be able to sell such attributes could materially adversely affectimpair our business, financial condition, and resultsoperating results.

For example, our Turnkey Engineering, Procurement, Construction and Maintenance Agreement and the underlying purchase orders dated as of operation.

AOctober 21, 2021 (the “SCE Agreement”) with SCE obligated us to achieve certain substantial portioncompletion milestone dates for the facilities no later than August 1, 2022, and for at least two years thereafter meet specified availability and capacity guarantees. In 2022, SCE instructed us to adjust the project schedule into 2023. As previously disclosed, we made force majeure claims under the SCE Agreement as battery supply delays resulting from COVID-19 lockdowns in several regions around China, newly implemented Chinese transportation safety policies and related supply chain delays impacted our ability to achieve the August 1, 2022 completion date. We are in ongoing discussions with SCE about the applicability of our earnings are attributableforce majeure relief to our salethe project delays. If we fail to satisfy certain milestone obligations, fail to come to an agreement with SCE of renewable energy certificates (“RECs”) and other environmental attributes generated by our energy assets. These attributes are used as compliance purposes for state-specific or U.S. federal policy.

We own and operate solar PV installations which derive a significant portion of their revenues from the sale of solar renewable energy certificates (“SRECs”), which are produced as a result of generating electricity. The valueappropriate extensions of these SRECs is determined bymilestones and force majeure relief, or fail to meet the supplyavailability and demand of SRECs in the states in which the solar PV installations are installed. Supply is driven by the amount of installations and demand is driven by state-specific laws relating to renewable portfolio standards.

We also own and operate renewable natural gas plants that may deliver biofuels into to the nation’s natural gas pipeline grid. Such biofuel may qualify for certain environmental attribute mechanisms, such as renewable identification numbers (“RINs”) which are used for compliance purposes under the Renewable Fuel Standard (“RFS”) program. The RFS is a U.S. federal policy that requires transportation fuel to contain a minimum volume of renewable fuel. The U.S. Environmental Protection Agency (“EPA”) administers the RFS program and may periodically undertake regulatory action involving the RFS, including annual volume standards for renewable fuel.

We sometimes seek to sell forward a portion of our SRECs and other environmental attributes under contracts to fix the revenues from those attributes for financing purposes or hedge against future declines in prices of such environmental attributes. If our renewable energy facilities do not generate the amount of renewable energy attributes sold under such forward contracts or if for any reason the renewable energy we generate does not produce SRECs or other environmental attributes for a particular state,capacity guarantees, we may be requiredsubject to make upliquidated damages and under certain circumstances SCE may have a right to terminate the shortfallagreement.The requirement to pay liquidated damages or the loss of SRECs or other environmental attributes under such forward contracts through purchases on the open market or make payments of liquidated damages.

RECs are created through state law requirements for utilities to purchase a portion of their energybusiness from renewable energy sources and changes in state laws or regulation relating to RECs may adversely affect the availability of RECs or other environmental attributes and the future prices for RECs or other environmental attributes, whichSCE could have ana material adverse effect on our reputation, business financial condition andor results of operations.

A significant decline in the fiscal health of federal, state, provincial, and local governments could reduce demand for our energy efficiency and renewable energy projects.

Historically, including for the years ended December 31, 20192022 and 2018, more than 75%2021, 46% and 67%, respectively, of our revenues have been derived from sales to federal, state, provincial, or local governmental entities, including public housing authorities, public universities, and public universities.municipal utilities. We expect revenues from this market sector to continue to comprise a significant percentage of our revenues for the foreseeable future. A significant decline in the fiscal health of these existing and potential customers may make it difficult for them to enter into contracts for our services or to obtain financing necessary to fund such contracts, or may

cause them to seek to renegotiate or terminate existing agreements with us. In addition, if there is a partial or full shutdown of any federal, state, provincial or local governing body this may adversely impact our financial performance.

Provisions in our government contracts may harm our business, financial condition and operating results.

A significant majority of our fully-contracted backlog and awarded projects is attributable to customers that are governmental entities. Our contracts with the federal government and its agencies, and with state, provincial, and local governments, customarily contain provisions that give the government substantial rights and remedies, many of which are not typically found in commercial contracts, including provisions that allow the government to:

•terminate existing contracts, in whole or in part, for any reason or no reason;reason,

•reduce or modify contracts or subcontracts;subcontracts,

•decline to award future contracts if actual or apparent organizational conflicts of interest are discovered, or to impose organizational conflict mitigation measures as a condition of eligibility for an award;award,

•suspend or debar the contractor from doing business with the government or a specific government agency;agency, and

•pursue criminal or civil remedies under the False Claims Act, False Statements Act, and similar remedy provisions unique to government contracting.

Under general principles of government contracting law, if the government terminates a contract for convenience, the terminated company may recover only its incurred or committed costs, settlement expenses, and profit on work completed prior to the termination. If the government terminates a contract for default, the defaulting company is entitled to recover costs incurred and associated profits on accepted items only and may be liable for excess costs incurred by the government in procuring undelivered items from another source. In most of our contracts with the federal government, the government has agreed to make a payment to us in the event that it terminates the agreement early. The termination payment is designed to compensate us for the cost of construction plus financing costs and profit on the work completed.

In ESPCs for governmental entities, the methodologies for computing energy savings may be less favorable than for non-governmental customers and may be modified during the contract period. We may be liable for price reductions if the projected savings cannot be substantiated.

In addition to the right of the federal government to terminate its contracts with us, federal government contracts are conditioned upon the continuing approval by Congress of the necessary spending to honor such contracts. Congress often appropriates funds for a program on a September 30 fiscal-year basis even though contract performance may take more than one year. Consequently, at the beginning of many major Governmental programs, contracts often may not be fully funded, and additional monies are then committed to the contract only if, as and when appropriations are made by Congress for future fiscal years. Similar practices are likely to also affect the availability of funding for our contracts with Canadian, as well as state, provincial, and local government entities. If one or more of our government contracts were terminated or reduced, or if appropriations for the funding of one or more of our contracts is delayed or terminated, our business, financial condition and operating results could be adversely affected.

Our senior credit facility, project financing term loans and construction loans contain financial and operating restrictions that may limit our business activities and our access to credit.

Provisions in our senior credit facility, project financing term loans and construction loans impose customary restrictions on our and certain of our subsidiaries’ business activities and uses of cash and other collateral. These agreements also contain other customary covenants, including covenants that require us to meet specified financial ratios and financial tests.