UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20162017

or

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 001-37428

RITTER PHARMACEUTICALS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 26-3474527 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

1880 Century Park East, Suite 1000 Los Angeles, California | 90067 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (310) 203-1000

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange on Which Registered | |

| Common Stock, par value $0.001 per share | NASDAQ Capital Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”filer,” “smaller reporting company,” and “smaller reporting“emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | [ ] | Accelerated filer | [ ] |

| Non-accelerated filer | [ ] (Do not check if a smaller reporting company) | Smaller reporting company | [X] |

| Emerging growth company | [X] |

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

As of June 30, 20162017 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of the registrant’s common stock held by non-affiliates was approximately $8.1 million based upon the closing price for shares of the registrant’s common stock of $1.53$0.55 as reported by the NASDAQ Capital Market on that date. For purposes of this calculation, the registrant has assumed that its directors, executive officers and holders of 5% or more of the outstanding common stock are affiliates.

As of February 22,March 19, 2018, there were 11,619,19749,406,521 shares outstanding of the registrant’s common stock, par value $0.001 per share.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of Ritter Pharmaceuticals, Inc.’s Proxy Statement to be filed with the Securities and Exchange Commission pursuant to Regulation 14A for the 2017 Annual Meeting of Stockholders are incorporated by reference in Part III of this Annual Report on Form 10-KNone.

RITTER PHARMACEUTICALS, INC.

ANNUAL REPORT ON FORM 10-K

For the Year Ended December 31, 20162017

Table of Contents

| 2 |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS AND INDUSTRY DATA

This Annual Report on Form 10-K (“Annual Report”) contains forward-looking statements that involve substantial risks and uncertainties. All statements other than statements of historical facts contained in this Annual Report, including statements regarding our strategy, future operations, future financial position, future revenue, projected costs, prospects, plans, objectives of management and expected market growth are forward-looking statements. The words “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “should,” “target,” “will,” “would” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. These statements involveare subject to known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements.

Some of the factors that we believe could cause actual results to differ from those anticipated or predicted include:

| ● | our ability to obtain additional | |

| ● | the accuracy of our estimates regarding expenses, future revenues and capital requirements; | |

| ● | the success and timing of our preclinical studies and clinical trials; | |

| ● | our ability to obtain and maintain regulatory approval of RP-G28 and any other product candidates we may develop, and the labeling under any approval we may obtain; | |

| ● | regulatory developments in the United States and other countries; | |

| ● | the performance of third-party manufacturers; | |

| ● | our ability to develop and commercialize | |

| ● | our ability to obtain and maintain intellectual property protection for | |

| ● | the successful development of our sales and marketing capabilities; | |

| ● | the potential markets for | |

| ● | the rate and degree of market acceptance of | |

| ● | the success of competing drugs that are or become available; and | |

| ● | the loss of key scientific or management personnel. |

By their nature, forward-looking statements involve risks and uncertainties because they relate to events, competitive dynamics, and healthcare, regulatory and scientific developments and depend on the economic circumstances that may or may not occur in the future or may occur on longer or shorter timelines than anticipated. Although we believe that we have a reasonable basis for each forward-looking statement contained in this Annual Report, we caution you that forward-looking statements are not guarantees of future performance and that our actual results of operations, financial condition and liquidity, and the development of the industry in which we operate may differ materially from the forward-looking statements contained in this Annual Report. In addition, even if our results of operations, financial condition and liquidity, and the development of the industry in which we operate are consistent with the forward-looking statements contained in this Annual Report, they may not be predictive of results or developments in future periods.

Any forward-looking statement that we make in this Annual Report speaks only as of the date of such statement,this Annual Report, and we undertake no obligation to update such statements to reflect events or circumstances after the date of this Annual Report. You should also read carefully the factors described in the “Risk Factors” section of this Annual Report to better understand the risks and uncertainties inherent in our business and underlying any forward-looking statements.

This Annual Report includes statistical and other industry and market data that we obtained from industry publications and research, surveys and studies conducted by third-parties. Industry publications and third-party research, surveys and studies generally indicate that their information has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. While we believe these industry publications and third-party research, surveys and studies are reliable, we have not independently verified such data.

| 3 |

Overview

Ritter Pharmaceuticals, Inc. develops novel therapeutic products that modulate the human gut microbiome to treat gastrointestinal diseases. We are advancing human gut health research by exploring the metabolic capacity of the gut microbiota and translating the functionality of prebiotic-based therapeutics into applications intended to have a meaningful impact on a patient’s health.

Our first novel microbiome modulator, RP-G28, an orally administered, high purity galactooligosaccharide (“GOS”),galacto-oligosaccharide, is currently under development for the reductiontreatment of symptoms associated with lactose intolerance. RP-G28 is designed to selectively stimulate the growth of lactose-metabolizing bacteria in the colon, thereby effectively adapting the gut microbiome to assist in digesting the lactose (the sugar found in milk) that reaches the large intestine. RP-G28 has the potential to become the first drug approved by the Food and Drug Administration (“FDA”) for the reductiontreatment of symptoms associated with lactose intolerance. RP-G28 has been studied in a Phase 2a and Phase 2b clinical trial and an adaptive design Phase 2b/3 clinical trialtrials and is a first-in-class compound.

On October 17, 2016,March 28, 2017, we announced that the last patient had completed dosing and all monitoring visits intop-line results from our Phase 2b/32b clinical trial of RP-G28 for the treatment of lactose intolerance. Topline results of the trial are expected to be announced in the first quarter of 2017. The Phase 2b/32b trial iswas a double-blind, placebo-controlled, three arm, multicenterthree-arm, multi-center study evaluating safety, efficacy and tolerability of two dosing regimens of RP-G28 in patients with moderate to severe lactose intolerance symptoms.intolerance. Enrollment was initiated in March 2016 and the last patient completed dosing in August 2016, achieving our projected enrollment time period.October 2016. The study aimsaimed to evaluate a patient’s ability to consume dairy foods post-treatment with improved tolerance and reduced digestive symptoms. A total of 377368 subjects were enrolledrandomized in the trial with 18 clinical sites participating throughout the United States. Patients underwent a screening period and a 30-day treatment period, followed by a 30-day post-treatment evaluation“real world” observation of milk and dairy tolerance. product consumption period.

A subset of subjects have been rolledenrolled into a 12-month extension study to evaluate long-term durability of treatment. The extension study will also evaluateevaluated each participant’s microbiome, expanding knowledge of the effects that RP-G28 may have on adapting the gut microbiota in a beneficial manner. The subjects are expected to complete the 12-month evaluation duringWe completed this study in the fourth quarter of 2017.

We have had communications with the FDA regarding our clinical program and regulatory path towards getting RP-G28 adequately studied and eventually approved. We intend to hold two meetings with the FDA in the near future about our Phase 2b/3 study, includingheld a Type C meeting as well aswith the FDA’s Division of Gastroenterology and Inborn Errors Products in March 2017, prior to the unblinding of our Phase 2b data, to discuss our development plans and Phase 2b clinical trial. The focus of the meeting was to obtain the FDA’s feedback on our Phase 2b clinical trial, including our statistical analysis plan (“SAP”), prior to unblinding any data.

We held an End of PhaseEnd-of-Phase 2 meeting bothwith the FDA’s Division of whichGastroenterology and Inborn Errors Products in August 2017. The purpose of the meeting was to obtain the FDA’s feedback on our Phase 3 program. We reached general consensus with the FDA has encouraged us to schedule. These meetingson certain elements of our current Phase 3 program and communications are typical for development stage companieshave received clear guidance and includerecommendations on many necessary components of our Phase 3 program; including the clinical, pathway, regulatorynon-clinical, and chemistry, manufacturing and controls (CMC) requirements statistical planneeded to support an NDA submission.

We have incorporated much of this guidance into our Phase 3 program. Our current Phase 3 clinical program will consist of two confirmatory clinical trials of similar trial design as our Phase 2b clinical trial and endpoints and similar matters.will include additional components that may allow for claims for durability of effect. These additional trials may be run in parallel. We anticipate that the first Phase 3 clinical trial will begin in the second quarter of 2018.

The Gut Microbiome

The human gut is a relatively under-explored ecosystem but provides a great opportunity for using dietary intervention strategies to reduce the impact of gastrointestinal disease. The human body carries about 100 trillion microorganisms in the intestines, which is 10 times greater than the number of cells in the human body. This microbial population is responsible for a number of beneficial activities such as fermentation, strengthening the immune system, preventing growth of pathogenic bacteria, providing nutrients, and providing hormones. The increasing knowledge of how these microbial populations impact human health provides opportunities for novel therapies to treat an assortment of diseases such as neurological disease, cardiovascular disease, obesity, irritable bowel syndrome, inflammatory bowel disease, colon cancer, allergies, autism and depression.

Platform ApproachLactose Intolerance

Our platformLactose intolerance is based on selectively colonizing microbiota (increasing beneficial bacteria)a common condition attributed to the absence or insufficient levels of the enzyme lactase, which is needed to properly digest lactose, a complex sugar found in the colon,milk and thus changing the colon’s composition of microbiota. This process has been shown to stimulate the growth of endogenous bifidobacteria, which after a short feeding period become predominant in the colon. The result is believed to reduce inflammation and improve digestion, thereby potentially reducing digestive symptoms.milk-containing foods.

RP-G28 selectively increases colonization of lactose-metabolizing bacteria in the colon, such as bifidobacteria and lactobacilli, without increasing the growth of harmful bacteria, such as Escherichia coli (“E. coli”). Increased colonization of lactose-metabolizing colonic microbiota is associated with increased lactase activity, thereby increasing the fermentation of lactose into galactose, glucose and short chain fatty acids. We believe this process could reduce lactose-derived gas production and thereby mitigate the symptoms of lactose intolerance.

| 4 |

Lactose Intolerance

Studies have suggested that lactose intolerance is a widespread condition affecting over one billion people worldwide and over 40 million people in the United States (or 15% of the U.S. population), with an estimated nine million of those individuals demonstrating moderate to severe symptoms.

Current annual spending on over-the-counter lactose intolerance aids in the United States has been estimated at approximately $2.45 billion.However, these options are limited and there is no long-term treatment available.

LactoseUnlike many common gastrointestinal conditions, such as irritable bowel syndrome, inflammatory bowel diseases, gastroesophageal reflux disease, or dyspepsia (among many others), lactose intolerance develops insymptoms can be completely abated by avoiding dietary lactose. In this regard, lactose maldigesters when consuming too much lactose or when lactose is added to a previously low-lactose diet. People with lactose maldigestion have a low activity level of lactase, the enzyme responsible for breaking down human lactose, located in the brush border membrane of the small intestine. Lactose intolerance is characterized by onean avoidance condition, similar to celiac sprue, food intolerances, or morevarious environmental allergies. However, dairy avoidance may lead to inadequate calcium and vitamin D intake, which can predispose individuals to decreased bone accrual, osteoporosis, hypertension, rickets, osteomalacia, and possibly certain cancers. Although supplements and calcium-rich foods are available, several studies have shown that lactose intolerance patients had an average calcium intake of only 300-388 mg/day, significantly less than the cardinal symptoms; including abdominal pain/cramps, bloating, gas, and diarrhea following1000-1200 mg/day adult dietary recommended levels. The 2010 National Institutes of Health conference on lactose intolerance highlighted the ingestionlong-term consequences of lactose or lactose-containing foods.

In lactose maldigesters, unhydrolyzed lactose passes intodairy avoidance demonstrating both the large intestine, where it is fermented byimportance of treating the indigenous microflora into gases and short chain fatty acids. The excessive gas productioncondition and the osmotic effects of excessive undigested lactose cause the symptoms of lactose intolerance. Symptoms begin about 30 minutesneed to two hours after eating or drinking foods containing lactose. The severity of symptoms depends on many factors, including the amount of lactose a person can tolerate and a person’s age, ethnicity, and digestion rate. The symptoms of lactose intolerance are caused by gases and toxins produced by anaerobic bacteria in the large intestine. The problem of lactose intolerance has been exacerbated because many foods and drinks contain traces of lactose without lactose being clearly stated on the product’s label.find improved solutions for patients.

Diagnosis

Lactose intolerance is often diagnosed by evaluating an individual’s clinical history, which reveals a relationship between lactose ingestion and onset of symptoms. Hydrogen breath tests may also be utilized to diagnose lactose malabsorption and a milk challenge may be used to differentiate between lactose malabsorption and lactose intolerance. Further tests can be conducted to rule out other digestive diseases or conditions, including: stool examination to document the presence of a parasite, blood tests to determine the presence of celiac disease, and intestinal biopsies to determine mucosal problems leading to malabsorption, such as inflammatory bowel disease or ulcerative colitis.

Health Consequences

Substantial evidence indicates that lactose intolerance is a major factor in limiting calcium intake in the diet of individuals who are lactose intolerant. Studies suggest that these individuals avoid milk and dairy products, resulting in an inadequate intake of calcium and significant nutritional and health risks.

At the 2010 National Institute of Health (“NIH”) Consensus Development Conference: Lactose Intolerance and Health, the NIH highlighted numerous health risks tied to lactose intolerance such as: osteoporosis; hypertension; and low bone density.There is substantial evidence indicating that lactose intolerance is a major factor in limiting calcium and nutrient intake in the diet of people who are lactose intolerant. Adequate calcium intake is essential to reducing the risks of osteoporosis and hypertension.In addition, chronic calcium depletion has been linked to increased arterial blood pressure, thereby establishing a relationship between hypertension and low calcium intake.Moreover, there is evidence of a correlation between calcium intake and both colon and breast cancer.

Decreased Calcium Intake Increases the Risk for Hypertension

Numerous published reports show that chronic calcium depletion may lead to increased arterial blood pressure. Many additional papers have corroborated this relationship between hypertension and a low calcium intake.

A growing body of evidence indicates that a nutritionally sound diet rich in fruits, vegetables and a generous component of low-fat dairy foods (sometimes referred to as the DASH diet) is optimal for reducing the risk of hypertension. Several reports have confirmed this finding in middle-aged and elderly women. Further, it appears that the DASH diet with generous low-fat dairy is associated with low prevalence of metabolic syndrome. Studies have suggested that the levels of dairy foods (three to four servings per day) required to achieve these effects are well above current U.S. averages and even further above those of lactose intolerant individuals who are avoiding dairy due to symptoms.

Our History

We were formed as a Nevada limited liability company on March 29, 2004 under the name Ritter Natural Sciences, LLC. Our first prototype, Lactagen™, was an alternative lactose intolerance treatment method. In 2004, clinical testing was conducted, which included a 60 subject61-subject double-blind placebo controlled clinical trial. The results were published in the Federation of American Societies for Experimental Biology in May 2005 and demonstrated Lactagen™ to be an effective and safe product for reducing symptoms for nearly 80% of the clinical participants who were on Lactagen™.

| 5 |

In 2008, we expanded our focus by developing a prescription drug development program. We initiated the program by developing RP-G28, a second generation edition of Lactagen™. We believe that RP-G28 enables us to state stronger claims, garner more medical community support and reach a wider market in the effort to treat lactose intolerance.

To help fund the development of RP-G28, we were awarded a grant from the United States government’s Health Care Bill program, the Qualifying Therapeutic Discovery Project, in 2008. The grant program provides support for innovative projects that are determined by the U.S. Department of Health and Human Services to have reasonable potential to result in new therapies that treat areas of unmet medical need and/or prevent, detect or treat chronic or acute diseases and conditions.

On September 16, 2008, we converted into a Delaware corporation under the name Ritter Pharmaceuticals, Inc.

We completed our initial public offering in June 2015. Our common stock is traded on the Nasdaq Capital Market under the trading symbol “RTTR”.

Our Leading Product Candidate — RP-G28

Overview

RP-G28 is a novel highly purified GOS, which is synthesized enzymatically. The product is being developed to reducefor the symptoms and frequencytreatment of episodes of abdominal pain associated with lactose intolerance. The therapeutic is taken orally (a powder solution mixed in water) for 30 consecutive days. The proposed mechanism of action of RP-G28 is to increase the intestinal growth and colonization of bacteria that can metabolize lactose to compensate for a patient’s intrinsic inability to digest lactose. Once colonization of bacteria has occurred, it is hypothesized that patients will continue to tolerate lactose as long as they maintain their microflora balance. RP-G28 has the potential to become the first FDA-approved drug for the reduction of symptoms associated with lactose intolerance.

GalactooligosaccharidesGalacto-oligosaccharides (GOS)

RP-G28 is a >95% purified GOS product.product derived from a commercially available GOS food ingredient, which is designated as generally recognized as safe (GRAS) by the FDA. GOS refers to a group of compounds containing β-linkages of 1 to 6 galactose units with a single glucose on the terminal end and are found at low levels in human milk. GOS is purified to a pharmaceutical grade by minimizing residual glucose, lactose, galactose and other impurities. Further processing includes ultra-filtration, nano-filtration, decolorization, deionization, and concentration to yield GOS 95 syrup, which is the starting material for RP-G28.

GOS products resist hydrolysis by salivary and intestinal enzymes because of the configuration of their glycosidic bonds and reach the colon virtually intact. The undigested GOS enhances the growth of beneficial, lactose metabolizing, colonic bacteria that already exist in the subject’s digestive track, including multiple species and strains of bifidobacteria and lactobacilli. Once colonies of these bacteria have increased, continued lactose exposure should maintain tolerability of lactose without further exposure to RP-G28.

While formal nonclinical studies evaluating the safety of RP-G28 have not been performed, other commercially available GOS products have been evaluated in acute and repeat-dose general toxicology studies, reproductive toxicology studies, juvenile toxicology studies, genetic toxicology studies, and in long-term safety studies.

Clinical studies of GOS products were reviewed as part of the safety evaluation to support the Investigational New Drug Application (“IND”) for RP-G28. These include studies in adults (including pregnant women and geriatrics), children, infants and newborns (preterm and full term). The safety of GOS products in humans has been evaluated in 1316 adults at doses of 2.5 to 20 g/day for up to 12 months, and in 1125 children > 1 year of age at doses of 2.0 to 12 g/day for up to 1 year. Overall, no safety concerns attributable to the consumption of GOS were reported. Where side effects were observed, they were typically mild and limited to increased flatulence, abdominal discomfort, and changes in stool consistency and frequency; however, effects were not consistently observed in all studies. Similar observations of increased flatulence have been reported following the consumption fructo-oligosaccharies (FOS) (15 g/day) over a 7-day period (Alles, 1996), and this symptom represents a localized effect that is expected in association with the consumption of indigestible fiber in large quantities. There were no reports of events in other System Organ Class (SOC) suggestive of systemic toxicity.

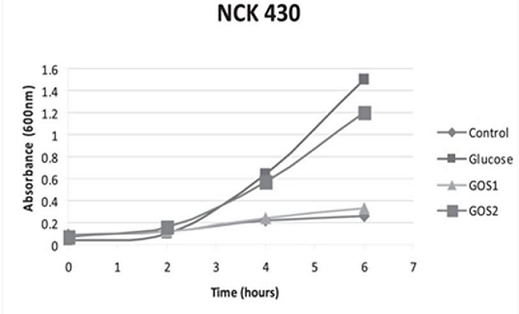

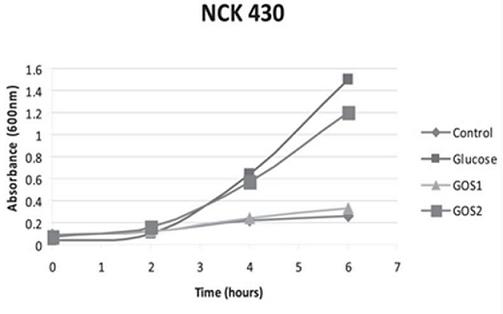

The significance of a higher purity GOS, namely RP-G28, was highlighted in a 2010 study by Klaenhammer. The in vitro study concluded that RP-G28 promoted growth of lactobacilli and bifidobacteria, but did not promote multiple strains of E. coli. In contrast, lower purity GOS stimulated both bifidobacteria as well as the strains of E. coli evaluated. (As seen below in Figure 1, NCK 430 (e. coli) grew in the presence of low purity GOS (GOS 2). Alternatively, the higher purity GOS (RP-G28/GOS 1) did not promote the growth of E. coli.).

| 6 |

Figure 1

Mechanism of Action

RP-G28 selectively increases colonizationis understood to resist hydrolysis by salivary and intestinal enzymes due to the configuration of their glycosidic bonds and consequently reach the colon virtually intact. The product is then broken down intracellularly by galactosidases, and eventually β-galactosidase hydrolyzes the terminal lactose. This leads to selective alterations in the composition and activity of the microbiome in which RP-G28 enhances the growth of lactose-metabolizing bacteria, including species of Bifidobacteria and Lactobacilli (30). In our Phase 2a Clinical Trial (G28-001), shifts in the colon, such as bifidobacteriafecal microbiome in 82% of participants on treatment and lactobacilli, withoutincreases in relative abundance of both Bifidobacteria and Lactobacilli were reported. RP-G28 had a bifidogenic effect in 90% of responders, which included species Bifidobacterium longum, Bifidobacterium adolenscentis, Bifidobacterium catenulatum, Bifidobacterium breve, and Bifidobacterium dentium (30). The understood mechanism of action is that by increasing the growth of harmfullactose-metabolizing bacteria, such as E. coli.Increased colonization of lactose-metabolizing colonic bacterialess undigested lactose is associated with increased lactase activityfermented, and GOS utilization, thereby increasing the fermentation of lactose into galactose, glucose and short chain fatty acids. Digestion of lactosethus reduces lactose-derived gas production and thereby mitigatesrelated LI symptoms. Data correlating bacterial taxa and symptom metadata support this proposed hypothesis. In the symptomsG28-001 study, microbiome changes correlated with clinical outcomes of improved lactose intolerance.

Safety & Toxicology of GOS

Clinical studies of GOS products were reviewed as part of the safety evaluation to support our Investigational New Drug (“IND”) Application for RP-G28. The safety of GOS productstolerance in humans has been evaluatedwhich an increase in 486 adults at doses of 2.5 to 15 gm/day for up to 14 weeks, 342 children at doses of 2.0 – 2.4 gm/day for up to 1 year,Bifidobacterium was associated with decreased pain and in 2415 newborns and infants for up to 6 months. Overall, no reports of severe adverse events attributable to the consumption of GOS were reported in the literature.cramping outcomes.

Among the studies that included tolerance endpoints, side effects were limited to reports of flatulence, fullness, gastronintestinal symptoms, and changes in stool consistency and frequency when GOS was consumed on a repeat basis at quantities of between 5.5 to 15 g/day (Ito 1990; Deguchi 1997; Teuri 1998); however, this effect was not consistently reported in all studies (Teuri and Korpela 1998; Depeint 2008; Drakoularako 2010; van de Heuval 1998; van Dokkum 1999; Bouhnik 2004; Sairanen and Piirainen 2007; Shadid 2007). Similar observations of increased flatulence have been reported following the consumption of fructooligosaccharides (15 gm/day) over a 7-day period (Alles 1996), and this symptom represents a localized effect that is expected in association with the consumption of indigestible fiber in large quantities. There were no reports of events in other System Organ Class (“SOC”) suggestive of systemic toxicity.

RP-G28 Clinical Safety

In addition to the nonclinical studies evaluating GOS products, the safety of RP-G28 for clinical investigation is supported by clinical safety results from our Phase 2a study, G28-001. In this study, RP-G28 was escalated from 1.5 grams per day to 15 grams per day over a 35-day dosing period.

RP-G28 was well-tolerated. There were no serious adverse effects. The most common adverse effects were headache, dizziness, nausea, upper respiratory tract infection, nasal congestion and pain. All adverse effects were mild or moderate in severity, and event occurrence was distributed over the treatment and post-treatment follow-up phase. No clinically significant changes or findings were noted from clinical lab evaluations, vital sign measurements, physical exams, or 12-lead electrocardiograms.

Our Market Opportunity

Unmet Medical Needs

Lactose intolerance is a challenging condition to manage. According to a market research study conducted by Objective Insights in April 2012, approximately 60% of lactose intolerant sufferers reported experiencing symptoms daily, or bi-weekly. Not only can symptoms be painful and embarrassing, they can also dramatically affect one’s quality of life, social activities, and health. Currently there are few reliable, or effective, treatments available that provide consistent or satisfactory relief.

Currently, there is no approved prescription treatment for lactose intolerance. Most persons with lactose intolerance avoid ingestion of milk and dairy products while others substitute non-lactose-containing foods in their diet. However, complete avoidance of lactose-containing foods is difficult to achieve (especially for those with moderate to severe symptoms) and can lead to significant long-term morbidity (i.e., dietary deficiencies of calcium and vitamin D).

| 7 |

At the 2010 National Institute of Health (“NIH”) Consensus Development Conference: Lactose Intolerance and Health, the NIH highlighted numerous health risks tied to lactose intolerance such as: osteoporosis; hypertension; and low bone density.There is substantial evidence indicating that lactose intolerance is a major factor in limiting calcium and nutrient intake in the diet of people who are lactose intolerant. Adequate calcium intake is essential to reducing the risks of osteoporosis and hypertension.In addition, chronic calcium depletion has been linked to increased arterial blood pressure in over 30 published reports, thereby establishing a relationship between hypertension and low calcium intake.Moreover, there is evidence of a correlation between calcium intake and both colon and breast cancer.

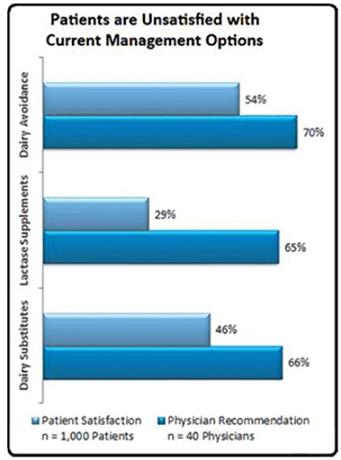

Treatment Options

Doctors generally recommend the following treatments for the management of lactose intolerance: (1) dairy avoidance; (2) lactase supplements; (3) probiotics/dietary supplements; and (4) dairy substitutes/lactose free products. Despite educating their patients on all viable treatment options, physicians tend to advise their patients to refrain from consuming any dairy products whatsoever. However, in a 2008 survey conducted by Engage Health, 47% of lactose intolerance sufferers reported that this method was not effective (largely due to hidden dairy products in ingredients), and only 30% of lactose intolerance sufferers reported lactase supplements as being effective in managing their lactose intolerance.Further, while probiotics/dietary supplements have been demonstrated to aid and support one’s digestive system, helping break down general foods consumed, they don’t directly help with lactose intolerance. The 2008 survey by Engage Health suggests that the majority of lactose intolerance patients are dissatisfied with current treatment options.

Patients Unsatisfied with Current Management Options

Growing Awareness

Lactose intolerance is a condition that continues to expand as society advances and evolves. It has been estimated that gastroenterologists see approximately 15 new patients with lactose intolerance each month. Education and awareness have increased, and the American diet has greatly changed over the past decade to include more dairy-based goods. As the populace is growing older, the prevalence of lactose intolerance is increasing because more people tend to develop lactose intolerance later in life. Increased education and diagnosis is making more people aware of their allergies and digestive conditions. Physicians may compound the growth of lactose intolerance prevalence and its associated disorders by recommending individuals to avoid dairy products, a practice which in and of itself may increase severity of the intolerance.

| 8 |

Doctors tend to diagnose lactose intolerance in a patient before the patient is able to self-diagnose it.However, patients tend to initiate discussion about lactose intolerance with their doctors. This is indicative of broad public awareness of lactose intolerance. Doctors often administer two tests for diagnosing lactose intolerance: (i) a symptom history test and (ii) a hydrogen breath test.

Our Competitive Strengths

Market Opportunity

RP-G28 has the potential to become the first approved drug in the United States and Europe for the reductiontreatment of symptoms associated with lactose intolerance.

Renowned Scientific Team and Management Team

Our leadership team has extensive biotechnology/pharmaceutical expertise in discovering, developing, licensing and commercializing therapeutic products. We have attracted a scientific team comprised of innovative researchers who are renowned in their knowledge and understanding of the host-microbiome in the field of lactose intolerance and gastroenterology.

Substantial Patent Portfolio and Product Exclusivity

We have an issued patent in the United Kingdom directed to the composition of non-digestible carbohydrates, and we have issued patents in the United States, in select countries in Europe (Germany, the United Kingdom, France, Spain, the Netherlands, Spain), and in other jurisdictions, directed to pharmaceutical compositions, methods of making such compositions, and methods of using such compositions for the treatment of lactose intolerance and certain of its symptoms. Additional worldwide patent applications are pending. The patent applications include claims covering pharmaceutical compositions, methods of making, methods of use, formulations and packaging.

In addition, in July 2015 we acquired the rights, title and interest to certain patents and related patent applications with claims covering a process for producing ultra highultra-high purity GOSgalacto-oligosaccharide active pharmaceutical ingredients, including RP-G28 from our supplier. See “Business—Clinical Supply and Cooperation Agreement with Ricerche Sperimentali Montale and Inalco SpA”“Manufacturing” for additional details regarding the second amendment to the exclusive supply agreement and our exercise of the exclusive option.

See “Business—Intellectual“Intellectual Property” for additional information regarding our patent portfolio.

Our Growth Strategy

In order to achieve our objective of developing safe and effective applications to treat conditions associated with microbiome dysfunctions,disfunctions, our near-term and long-term strategies include the following:

| ● | ||

| ● | ||

| ● | develop and commercialize RP-G28 either by ourselves or in collaboration with others throughout the world; | |

| ● | explore the use of RP-G28 for additional potential therapeutic indications and orphan indications; | |

| ● | establish ourselves as a leader in developing therapeutics that modulates the human gut microbiome; | |

| ● | continue to develop a robust and defensible patent portfolio, including those we own and those we plan to in-license in the future; and | |

| ● | continue to optimize our product development and manufacturing capabilities both internally and externally through outside manufacturers. |

Clinical and Regulatory

IND Application/Phase 1

We submitted anThe IND application for RP-G28 to the FDA in June 2010. Because the safety and tolerability profile, pharmacokinetics and dose response curve of GOS products is generally well understood, as part of our IND submission, we proposed that the data supporting the IND was sufficientactivated initially to support a Phase 2 proof-of-concept2a safety, tolerability and efficacy study in a small number of lactose-intolerantlactose intolerant patients. The FDA agreed with this proposal and the typicalStandard Phase 1 clinical programsingle and repeat dose safety and tolerability studies in healthy volunteers was replaced withwere not needed because other GOS products that contain similar GOS constituents are generally regarded as safe (GRAS) and therefore supported the safety of RP-G28 in humans.

| 9 |

In 2018, a Phase 2a program in subjects with lactose intolerance.

On June 28, 2010, we received an advice letter from1 study will be conducted to understand the FDA regarding our IND submission. The FDA suggested that we (1) consider expanding our inclusion criteria to include femalespotential for systemic absorption of childbearing potential who are willing to use appropriate contraception throughoutRP-G28 and any impact the durationpresence of food may have on the protocol; (2) follow the FDA’s guidance regarding Patient-Reported Outcome Measures; and (3) include a pharmacokinetic profile of RP-G28. A Phase 1 QT/QTc study in our proposed Phase 2a trial to determine the extent ofmay be needed if there is measurable systemic exposure of RP-G28. Phase 1 systemic drug-drug-interaction (DDI) studies may also be needed if there is measurable systemic exposure of RP-G28, or if DDI potential within the gut is suggested by the results of in vitro DDI studies.

Phase 2a Study

In June 2011, we beganWe completed a double-blinded, randomized, multi-center, placebo-controlled Phase 2a clinical trial on RP-G28 to validate the efficacy, safety and tolerance of RP-G28 compared to placebo when administered to subjects with symptoms of lactose intolerance. The clinical results from the study, which concluded at the end of 2011, showed that RP-G28 improved lactose digestion versus placebo as measured by the improvement in digestive symptoms associated with lactose intolerance and decline in hydrogen production present in a hydrogen breath test.

On June 12, 2013, we announced positive data from our Phase 2a first-in-human, proof of concept clinical study of RP-G28. The purpose of the study was to assess the effectiveness, safety and tolerability of RP-G28 compared to a placebo when administered to subjects with symptoms associated with lactose intolerance. The results were presented at Digestive Diseases Week and the New York Academy of Sciences Conference on Probiotics, Prebiotics and the Host Microbiome: The Science of Translation, and co-sponsored by the Sackler Institute for Nutrition Science and the International Scientific Association of Probiotics and Prebiotics.

The clinical microbiome data from this Phase 2a clinical trial of RP-G28 in patients with lactose intolerance was published in theProceedings of the National Academy of Science (“PNAS-Plus”) PNAS 2017; Early Edition, published ahead of print January 3, 2017. The paper titled, “Impact of short-chain galactooligosaccharides on the gut microbiome of lactose-intolerant individuals,” reports findings on our lead therapeutic candidate, RP-G28, a short-chain GOS. The data validates RP-G28’s mechanism of action and supports the product as a potential treatment for lactose intolerance. The newly published microbiome data provides further insight into RP-G28’s Phase 2a 2013 clinical trial.

The double-blinded, randomized, multi-center, placebo-controlled Phase 2a studyplacebo. We evaluated RP-G28 in 62 patients with lactose intolerance over a treatment period of 35 consecutive days. Post-treatment, subjects reintroduced dairy into their diets and were followed for an additional 30 days to evaluate lactose digestion, as measured by hydrogen production and symptom improvements. In order to confirm lactose intolerance and study participation, subjects underwent a 25-gram lactose challenge in the clinic. Lactose intolerance symptoms and hydrogen production via hydrogen breath test were assessed for six hours post-lactose dose. Eligible subjects were required to demonstrate a minimum symptom score and a “positive” hydrogen breath test in order to be eligible for randomization. A “positive” breath test was defined as a hydrogen gas elevation of 20 parts per million (ppm) at two time-points within the six hours following a lactose-loading dose. The primary endpoints included tracking patients’ gastrointestinal symptoms via a patient-reported symptom assessment instrument (a Likert Scale, measuring individual symptoms of flatulence, bloating, cramping, abdominal pain and diarrhea, on a scale of 0 (none) to 10 (worst)) at baseline, day 36 and day 66; as well as the measurement of hydrogen gas levels in their breath following a 25-gram lactose challenge.

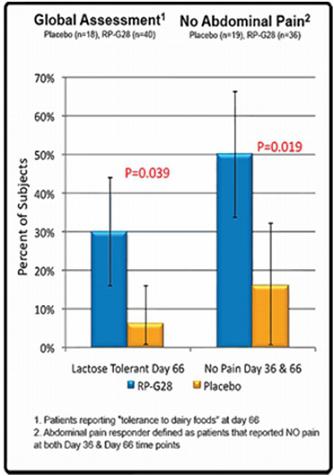

RP-G28 was well tolerated, with no significant adverse events reported. The Phase 2a study demonstrated clinically meaningful benefits to patients on treatment, whereas treated subjects reported increased tolerance to lactose and dairy foods: reduced lactose intolerance symptoms (gas, bloating, cramping and abdominal pain) were reported in subjects on RP-G28, a durable reduction in abdominal pain (p=0.019) was reported, and treated patients were six times more likely to describe themselves as lactose tolerant (p=0.039). In sum, positivePositive trends were seen when the entire per protocol study population was analyzed, including some statistically significant subgroup analysis, suggesting that a therapeutically positive effect is seen.effect. Although there were few primary and secondary efficacy endpoints with statistically significant results, the combined data suggest that RP-G28 is exerting a positive therapeutic effect. We believe these positive drug effect trends combined with the benign safety profile support continued drug development of RP-G28.

Key findings of the Phase 2a study include:clinical trial included:

| ● | RP-G28 was well tolerated with no significant study-drug related adverse effects. The benign adverse event safety profile of RP-G28 with dose levels up to 15 gm/day observed in this study is consistent with the known safety of GOS products administered up to 20 gm/day reported in literature. | |

| ● | Subjects in the RP-G28 group reported a reduction in total symptoms after treatment. Reported symptom improvement continued 30 days post-treatment. Improvement in symptoms was assessed in the study using several different measures, including a pain Likert scale and a patient global assessment. Subjects receiving RP-G28 had greater improvement in most of their symptoms (cramps, bloating and gas) following lactose challenge compared to placebo, but the differences were not statistically significant given the small cohort size. However, a clinically meaningful reduction in abdominal pain was seen in subjects receiving RP-G28 compared to placebo. | |

| ● | An analysis of “responders” for abdominal pain (defined as subjects who reported a score of zero in abdominal pain severity following a lactose challenge at Day 36/Hour 6 and Day 66/Hour 6) was performed. In the 55 subjects who noted abdominal pain following the baseline (Day 0) lactose challenge, 50% of RP-G28-treated subjects reported no abdominal pain compared to 17% of the placebo-treated subjects. This difference was statistically significant (p = 0.0190). See Figure 2 below. | |

| ● | An analysis of “responders” for abdominal pain (defined as subjects who reported a greater than 50% decrease in abdominal pain severity following lactose challenge between Day 0/Hour 6 and Day 36/Hour 6) was performed. In the 55 subjects who noted abdominal pain following the baseline (Day 0) lactose challenge, 72.2% of RP-G28-treated subjects reported a >50% reduction in abdominal pain severity compared to 42.1% of the placebo-treated subjects. This difference was also statistically significant (p=0.0288). | |

| ● |

| ● |

Figure 2

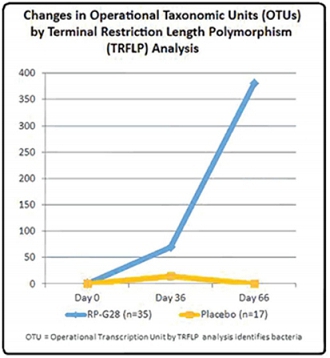

In the Phase 2a study, changes in the fecal microbiome were investigated using both Terminal Restriction Fragment Length Polymorphisms (“TRFLP”), a molecular biology technique for profiling microbial communities based on the position of a restriction site closest to a labeled end of an amplified gene, and microme analysis of 16S rRNA genex by pyrosequencing, a method of DNA sequencing (determining the order of nucleotides in DNA).

| 10 |

Figure 32

In addition, Principal Component Analysis (“PCA”), a multivariate method that helps transform a number of possibly correlated variables into a smaller number of uncorrelated variables called principal components, thereby reducing the dimensions of a complex dataset, showed statistically significant shifts in the microbiome of subjects fed RP-G28, compared to placebo, at 66 days. Specifically, RP-G28 significantly altered the microbiomes of 82% of the study participants who received the treatment. See Figure 3 above.

| 11 |

Pre-treatment, three distinct clusters were identified, whereas post-treatment (Day 66) two distinct clusters were identified, showing a clear shift in certain species represented before and after treatment.

Principal Coordinates Analysis (“PCoA”), a multivariate method that helps visualize similarities and dissimilarities in large datasets, was also utilized to analyze the microbiome data. For analysis of 16S amplicon sequencing data, we created Unweighted Unifrac similarity matrices (that is we conducted PCoA) and applied ANOSIM (Analysis of Similarities) and PERMANOVA (Permutational Analysis of Variance) statistical analyses. Our analysis showed a significant association between Day (day 0 or baseline, and day 36 and 66 as categories) and microbiome composition (ANOSIM R = 0.218, P = 0.0001, PERMANOVA Pseudo-F = 3.4318, P = 0.0001). These data indicate that RP-G28 and subsequent introduction of lactose into the diet had impacted the fecal microbiome of participants. Further, lactose metabolizing bacteria were shown to increase in the treatment group.

The clinical results of our Phase 2a study were published in Nutrition Journal in a manuscript entitled “Improving lactose digestion and symptoms of lactose intolerance with a novel galactooligosaccharidegalacto-oligosaccharide (RP-G28): a randomized, double-blind clinical trial.” The microbiome results were published in the Proceedings of the National Academy of Science in a manuscript entitled“Impact of short-chain galacto-oligosaccharides on the gut microbiome of lactose-intolerant individuals.”

Type C Meeting with the FDA

We held a Type C meeting with the FDA’s Division of Gastroenterology and Inborn Errors Products on February 20, 2013. The purpose of the meeting was to obtain the FDA’s feedback on the planned Phase 2 program and Phase 3 programs, inform the FDA of our ongoing development plans, gain feedback on relevant clinical trial design and end points related to patient meaningful benefits, and to inform the FDA of the status of our product characterization. We believe that this meeting

Phase 2b Clinical Trial

Enrollment in our Phase 2b clinical trial of RP-G28 was initiated in March 2016 and completed in August 2016. The final patient completed dosing and all monitoring visits in October 2016.

The Phase 2b trial was a significant step forward in streamliningmulti-center, randomized, double-blind, placebo-controlled, parallel-group trial of 368 subjects designed to determine the pathway to initial U.S. approvalefficacy, safety, and tolerability of two dosing regimens of RP-G28 in subjects with moderate to reduce symptomssevere lactose intolerance. Two hundred and frequency of symptomatic episodes associatedforty-seven (247) subjects received RP-G28 while 121 subjects received placebo. Twenty-four (24) subjects were discontinued prematurely from the study and 344 (91.2%) completed the study.

The trial assessed patients with lactose intolerance.intolerance symptoms as measured on a Likert scale after a lactose challenge. Entry criteria in the Phase 2b trial included a hydrogen breath test to validate lactase deficiency. The meetingPhase 2b trial design included a screening period, a 30-day course treatment period, and official meeting minutes provided valuable guidance ona 30-day post-treatment “real world” observation period during which subjects were followed while lactose containing food products were re-introduced into their diets. The study was designed to escalate the development pathdose beyond the 15 gm/day dose level evaluated in the Phase 2a study. Study subjects abstained from lactose containing food products and were then randomized evenly (1:1:1) to receive one of RP-G28:two doses of RP-G28 or placebo for 30 days.

The primary endpoint for the Phase 2b clinical trial was a LI symptom composite score response at day 31. A response was based on change from baseline (Day -7, visit 1) to end of treatment period at day 31 (visit 5), combined average of four maximum symptom scores taken over 0.5, 1, 2, 3, 4, and 5 hours for each symptom (abdominal pain, cramping, bloating, and gas movement) after a lactose challenge test. A response was defined as a 4-point or greater decrease from baseline or a composite score of zero at day 31. The Phase 2b trial further required the collection of fecal samples from patients enrolled to evaluate the baseline and changes to the patient’s microbiome that correlate to symptom reduction and lactose tolerance.

| 12 |

We held a Type C meeting with the FDA in March 2017, to discuss our development plans and Phase 2b clinical trial. The focus of the meeting was to obtain the FDA’s feedback on our Phase 2b clinical trial, including our SAP, prior to unblinding any data.

In order to gather long-term data on subjects exposed to RP-G28, we also offered enrollment in an observational 12-month extension study, G28-003XA, to subjects who completed the Phase 2b protocol. As RP-G28 is expected to provide extended relief from lactose intolerance symptoms beyond the initial 30-day treatment phase, this extension study for the Phase 2b program will assess the long-term treatment effect. The study is also evaluating each participant’s microbiome, expanding our knowledge of the effects that RP-G28 may have on adapting the gut microbiota in a beneficial manner. We completed this study in the fourth quarter of 2017. We intend for the results from this study to support durability of treatment and guide the need to evaluate an additional 30-day course of treatment in subjects who experience the return of lactose intolerance symptoms after an initial course of RP-G28.

Topline results of the Phase 2b clinical trial were announced in March 2017. Due to inconsistent data results from one study site, the data from this site was excluded from the primary analysis population (Efficacy Subset mITT). After excluding the data from the one anomalous study site, results showed a clinically meaningful benefit to subjects in the reduction of lactose intolerance symptoms across a variety of outcome measures. The majority of analyses showed positive outcome measures and the robustness of the data point to a clear drug effect. Treatment patients not only reported meaningful reduced symptoms, but also 30-days after taking the treatment, patients reported adequate relief from lactose intolerance symptoms and satisfaction with the results of the treatment, with RP-G28 preventing or treating their lactose intolerance symptoms. Greater milk and dairy product consumption was also reported by patients.

Because the efficacy data from one study site was found to be significantly different from that of the other study sites, the data from this site was excluded from the primary analysis population (Efficacy Subset mITT. n=296). It was decided that, in addition to the efficacy analysis for the mITT Population, the Efficacy Subset mITT population would be used to perform all efficacy analyses.

In the Efficacy Subset mITT Analysis group, the primary endpoint met statistical significance, (39.7% of the pooled dosing group compared to 25.8% of the placebo group responded (p=0.0159)). Because the primary analysis was statistically significant, the primary endpoint comparison between the high dose group and the placebo group was then tested and also met statistical significance (38.1% of the high dose group, compared to 25.8% of the placebo group responded (p=0.0294)). The comparison between the low dose group and the placebo group further met statistical significance (p=0.0434).

In the entire study population (mITT population), including patients from the excluded study site, taking at least one dose of drug (n=368), the comparison between the pooled treatment groups and the placebo group narrowly missed statistical significance (p=0.0618), (40.1% of the pooled treatment group responded compared to 31.4% of the placebo group). Both low dose and high dose group arms demonstrated a higher proportion of responders than the placebo group.

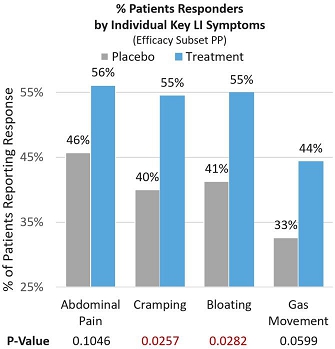

In the Efficacy Subset Per-protocol population (Efficacy Subset PP), significant and meaningful symptom improvement was consistently seen across key individual lactose intolerance symptoms by patients reporting a ≥4-point improvement from baseline (proportion of subjects on treatment that reported improvement in severity of each symptom). Of the treatment patients, 56.1% reported significant improvement in abdominal pain compared to 45.7% in the placebo group (p=0.1046). Of the treatment patients, 54.5% reported statistically significant improvement in cramping compared to 40.2% in the placebo group (p=0.0257). Of the treatment patients, 55% reported statistically significant improvement in bloating compared to 41.3% in the placebo group (p=0.0282). Finally, 44.4% of treatment patients reported significant improvement in gas movement compared to 32.6% in the placebo group (p=0.0599). See Figure 4 below.

| 13 |

Figure 4

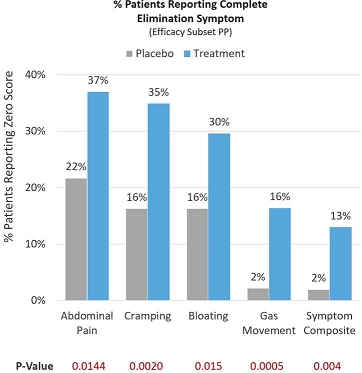

In a more stringent assessment, many patients reported that they experienced complete elimination of lactose intolerance symptoms, scoring a 0 out of 10 on a Likert pain scale post-treatment (Efficacy Subset PP). Of the treatment patients, 37.0% reported complete elimination of abdominal pain compared to 21.7% in the placebo group (p=0.0144). Of the treatment patients, 34.9% reported complete elimination of cramping compared to 16.3% in the placebo group (p=0.0020). Of the treatment patients, 29.6% reported complete elimination of bloating compared to 16.3% in the placebo group (p=0.015). Of the treatment patients, 16.4% reported complete elimination of gas movement compared to 2.2% in the placebo group (p=0.0005). Symptoms of abdominal pain, cramping, bloating and gas movement were then combined into a composite endpoint representing the key symptoms of lactose intolerance. Of the treatment patients, 13% experienced complete elimination of lactose intolerance symptoms compared to 2% in the placebo group (p=0.004). See Figure 5 below.

Figure 5

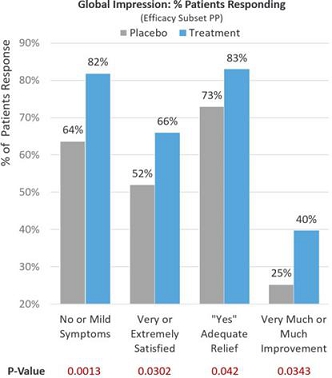

Observing global patient-reported assessments (Efficacy Subset PP) on multiple aspects of their symptom severity and treatment benefit experience 30 days after treatment and adding dairy and milk products back into their diets, 81.9% of treatment patients reported no or mild lactose intolerance symptoms compared to 63.7% in the placebo group (p=0.0013). Of the treatment patients, 66.3% reported being very or extremely satisfied with RP-G28 preventing or treating their lactose intolerance symptoms compared to 51.6% in the placebo group (p=0.0302). Of the treatment patients, 83.2% reported adequate relief from lactose intolerance symptoms compared to 72.5% in the placebo group (p=0.042). Of the treatment patients, 39.7% reported much or very much improvement in their lactose intolerance symptoms compared to 25.3% in the placebo group (p=0.0343). See Figure 6 below.

| 14 |

Figure 6

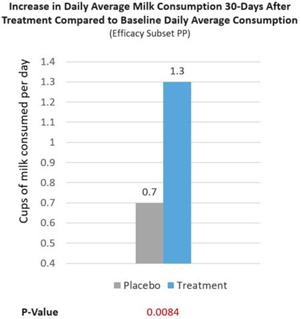

Further, a real-world milk intake assessment was conducted on treatment and placebo group patients (Efficacy Subset PP). At baseline, lactose intolerance patients reported consuming 0.2 cups/d of milk. After RP-G28, treatment patients increased their milk consumption to 1.5 cups/d of milk, consuming 1.3 cups/d more of milk (p=0.0084), 39% more milk consumed per day than placebo patients reported consuming (See Figure 7 below). We believe this is significant because the USDA recommends healthy individuals to consume 1.5 cups/d of milk. Overall, 62% of treatment patients consumed ≥1 cups/d of milk after being treated (p=0.0095). The increase in milk consumption is meaningful for dairy avoiders because it reflects increased lactose tolerance and may lead to more dietary calcium intake post-treatment as milk contains a higher percentage of one’s daily intake of calcium.

Figure 7

No serious adverse events related to treatment were reported and the number of adverse events reported was similar between treatment and placebo groups.

| 15 |

End-of-Phase 2 Meeting with the FDA

We held an End-of-Phase 2 meeting with the FDA’s Division of Gastroenterology and Inborn Errors Products in August 2017. The purpose of the meeting was to obtain the FDA’s feedback on our planned Phase 3 program. We reached general consensus with the FDA on certain elements of our Phase 3 program and have received clear guidance and recommendations on many necessary components of our Phase 3 program; including the clinical, non-clinical, and chemistry, manufacturing and controls (CMC) requirements needed to support an NDA. We have incorporated much of this guidance into our Phase 3 program.

Elements of our Phase 3 program are expected to include the following:

| ● | Trial Design: Will consist of two confirmatory clinical trials of similar trial design and size as our Phase 2b clinical trial and will include additional components that may allow for claims for durability of effect. The trials may be run in parallel. | |

| ● | Protocol design: Will consist of multi-center, randomized, doubled-blind, placebo-controlled, parallel-group trials designed to determine the efficacy, safety and durability of RP-G28 compared to a placebo in subjects with lactose intolerance. The protocol designs include screening to determine lactose intolerance, 30-day course of treatment, and 6-months of post-treatment observation. | |

| ● | Primary endpoint: Will evaluate a patient’s LI symptom composite score (including abdominal pain, cramping, bloating and gas) after a lactose challenge, comparing the mean difference between baseline symptom score to 30-days post-treatment symptom score. | |

| ● | Secondary endpoints: Will evaluate LI signs and symptoms and global assessment outcomes to evaluate and assess a patient’s continued meaningful treatment benefit. |

In preparation for Phase 3, we have had regular communications with the FDA and have received feedback from the FDA on the Phase 3 protocols, the statistical analysis plan (SAP), non-clinical matters, chemistry and controls, as well as other items.

The FDA has provided the following recommendations with respect to our revised Phase 3 protocols, SAP and other items (all of which we intend to implement):

| ● | The FDA |

| ● | ||

| ● | The FDA |

| ● |

Following analysis of the Phase 2a clinical trial, discussions with the FDA in 2013 about our clinical development plan, and further discussions with our regulatory consultants, we initiated a Phase 2b/3 clinical trial of RP-G28 in March 2016. We believe this trial could serve as one of two pivotal trials should the resulting data and the FDA be supportive of this trial as a pivotal trial. We did not discuss the Phase 2b/3 study design and development plan with the FDA before initiating the study in March 2016, though we did submit a supplement to the IND detailing the protocols for the adaptive study and intend to hold two meetings with the FDA in the near future.

Nonclinical Safety Plans

Given the established safety profile of GOS in humans and the lack of significant safety concerns with RP-G28 administered to subjects in the Phase 2a study,and Phase 2b clinical trials, it was agreed with the FDA (August 2017 End-of-Phase 2 meeting) that no additional non-clinical safety studies are plannedrequired to support continued evaluation of RP-G28 in the Phase 23 program. The FDA also agreed that no rat fertility, rat peri-post natal reproductive toxicity, genotoxicity or, importantly, rodent carcinogenicity studies are needed for the NDA submission.

Guidelines adoptedAs recommended by the FDA, and established by ICH require nonclinical studies that specifically address female fertility to be completed before the inclusion of women of child bearing potential in large-scale or long-duration clinical trials (e.g., Phase 3 trials). In the United States, such assessments of embryo-fetal development can be deferred until before Phase 3 using precautions to prevent pregnancy in clinical trials. As the FDA recommended in their June 28, 2010 advice letter, we will continue to evaluate females of child-bearing potential who are willing to use appropriate contraception throughout the duration of any study.

Phase 2b/3 Study

Enrollment in our Phase 2b/3 clinical trial ICH-compliant embryo-fetal development toxicology studies of RP-G28 was initiated in March 2016 and completed in August 2016. The final patient completed dosing and all monitoring visits in October 2016. Topline results of this trial are expected to be announced in the first quarter of 2017.

The Phase 2b/3 study was designed as a multi-center double-blinded, placebo controlled clinical trial of approximately 377 subjectsrat and rabbit will be conducted to determinesupport the maximum tolerated dose and optimal dose-escalation schedule for RP-G28. The trial assessed patients with moderate to severe abdominal pain as measured by a pain Likert scale after a lactose challenge. The Phase 2b/3 clinical trial was intended to measure additional lactose intolerance symptoms (gas, bloating, diarrhea, cramps) as secondary endpoints. Entry criteria in the Phase 2b/3 study included a hydrogen breath test to validate lactase deficiency. The Phase 2b/3 study design included a screening phase; a 30-day course treatment phase and a 30-day post-treatment evaluation phase. The study was designed to gradually escalate the dose beyond the 15 gm/day dose level evaluated in the Phase 2a study. Study subjects abstained from lactose containing food products and were then randomized evenly (1:1:1:1) to receive one of three doses of RP-G28 or placebo for 30 days. Subjects were then followed post-treatment for an additional 30 days while lactose containing food products were re-introduced into their diets. The primary endpoint for the Phase 2b/3 clinical study was a durable reduction in abdominal pain, with secondary endpoints measuring changes in individual lactose intolerance symptoms (gas, bloating, diarrhea, cramps). The Phase 2b/3 study wasNDA submission. Additional general toxicity studies may also designed to include collection of blood samples to assess systemic exposure to RP-G28 using measurement of serum concentrations of a trisaccharide. This was monitored as a surrogate to assess the systemic bioavailability of orally administered RP-G28. Additionally, the study required the collection of fecal samples from patients enrolled to evaluate the baseline and changes to the patient’s microbiome that correlate to symptom reduction and lactose tolerance.

In order to gather long-term data on subjects exposed to RP-G28, we also offered enrollment in an observational extension study, G28-004, to subjects who completed the Phase 2b/3 protocol. As RP-G28 is expected to provide extended relief from lactose intolerance symptoms beyond the initial 30-day treatment phase, this extension study for the Phase 2b/3 program will assess the long-term treatment effect. We intend for the results from this study to guide the need to evaluate an additional 30-day course of treatment in a Phase 3 clinical trial in subjects who experience the return of lactose intolerance symptoms after an initial course of RP-G28.

Adaptive seamless phase 2b/3 designs, such as the Phase 2b/3 pivotal clinical trial for RP-G28, are aimed at interweaving the two phases of full development by combining them into one single, uninterrupted study conducted in two steps. Adaptive seamless phase 2b/3 designs enable a clinical trial to be conducted in steps with the sample size calculation selected on the basis of data observed in the first step to continue along to the second step. The main statistical challenge in such a design is ensuring control of the type I error rate. Most methodology for such trials is based on the same endpoint being used for interim and final analyses. A type I error is one in which the adaptation process leads to design, analysis, or conduct flaws that introduce bias that increases the chance of a false conclusion that a treatment is effective (a type I error). Controlling type I error can be accomplished by prospectively specifying and including in the statistical analysis plan all possible adaptation plans that may be considered during the course of the trial. We worked with Covance, Inc. (“Covance”), a contract research organization (“CRO”) to control a type I error in our Phase 2b/3 study.

We did not discuss the Phase 2b/3 study design and development plan with the FDA before initiating the study in March 2016, though we did submit a supplement to the IND detailing the protocols for the adaptive study and have subsequently had communications with the FDA regarding our clinical program. We intend to hold two meetings with the FDA in the near future about our Phase 2b/3 study, including a Type C meeting as well as an End of Phase 2 meeting, both of which the FDA has encouraged us to schedule. These meetings and communications are typical for development stage companies and include the clinical pathway, regulatory requirements, statistical plan and endpoints and similar matters.

Master Service Agreement

On December 30, 2015, we entered into a Master Service Agreement with Covance, with an effective date of December 29, 2015. Pursuant to the terms of the Master Service Agreement, Covance (or one or more of its affiliates) will provide Phase 1, 2, 3, and 4 clinical services for a clinical study or studies to us, and, at our request, assist us with the design of such studies, in accordance with the terms of separate individual project agreements to be entered into by the parties. The term of the agreement is for three years and will renew automatically for successive one year periods unless Covance is no longer providing services under the agreement or either party has terminated the agreement upon written notice. We may terminate the Master Service Agreement or any individual project agreement entered into under the Master Service Agreement prior to the applicable study’s completion at any time for any reason upon 30 days written notice to Covance, except when the reason for termination is the safety of subjects, in which case it may be terminated immediately. Covance may not terminate any individual project agreement without cause, except when the reason for the termination is the safety of subjects, in which case it may be terminated immediately. In the event of a termination of the Master Service Agreement, Covance will be entitled to full payment for (i) work performed on the applicable project upon through the date work on such project is concluded and (ii) reimbursement for all non-cancellable and non-refundable expenses and financial obligations which Covance (or an affiliate) has incurred or undertaken on our behalf.NDA submission.

Manufacturing

We do not own or operate manufacturing facilities, for the production of RP-G28 or any other product candidates we may develop, nor do we have plans to develop our own manufacturing operations in the foreseeable future. We have an exclusive worldwide agreement (the “Supply Agreement”) to manufacture a higher purity form of GOS (referred to as “Improved GOS”) with Ricerche Sperimentali Montaleor (“RSM”) in connection with theour clinical and nonclinical studies we will need to conduct prior to receiving regulatory approval for RPG-28. RSM has also agreed that it will not, except as necessary for RSM to perform its obligations under the Supply Agreement, market or sell Improved GOS, or any GOSgalacto-oligosaccharides that are of greater purity to any third party.

| 16 |

Pursuant to the terms of the Supply Agreement, as amended on July 24, 2015, we purchased the exclusive worldwide assignment of all right, title and interest to the Improved GOS (the “Improved GOS IP”) on July 30, 2015 for $800,000. We also issued 100,000 shares of our common stock to RSM pursuant to a stock purchase agreement. The shares issued to RSM are subject to a lock-up agreement, pursuant to which RSM has agreed that it will not sell these shares for a period ending on the earlier of (i) the public release by us of the final results of our Phase 2b/3 clinical trial of RP-G28 and (ii) the filing of a Form 10-Q with the SEC for the fiscal quarter in which we receive the results of our Phase 2b/3 clinical trial of RP-G28.

Under the terms of the Supply Agreement, as amended, if we fail to make any future option payment to RSM required under the terms of the Supply Agreement, we may be required to return the Improved GOS IP to RSM. The terms of the Supply Agreement, as amended, require us to pay RSM $400,000 within 10 days following FDA approval of a new drug application for the first product owned or controlled by us using Improved GOS as its active pharmaceutical ingredient and to pay RSM the sum of $250 per kilo for clinical supply of Improved GOS.ingredient.

Commercialization

Given our stage of development, we have not yet established a commercial organization or distribution capabilities. RP-G28, if approved, is intended to be prescribed to patients suffering from lactose intolerance. These patients are normally under the care of a gastroenterologist and/or a primary care physician. Our current plan is to evaluate a possible partnership to commercialize RP-G28 for the reductiontreatment of symptoms associated with lactose intolerance in patients in the United States and Europe if it is approved. We may also build our own commercial infrastructure or utilize contract reimbursement specialists, sales people and medical education specialists, and take other steps to establish the necessary commercial infrastructure at such time as we believe that RP-G28 is approaching marketing approval. Outside of the United States and Europe, subject to obtaining necessary marketing approvals, we will likely seek to commercialize RP-G28 through distribution or other collaboration arrangements for patients suffering from lactose intolerance.

Competition

The biopharmaceutical industry is characterized by intense competition and rapid innovation. Although we know of no drug candidate, other than RP-G28, in advanced clinical trials for treating lactose intolerance, other biopharmaceutical companies may be able to develop compounds or drugs that are able to achieve similar or better results. Our potential competitors include major multinational pharmaceutical companies, established biotechnology companies, specialty pharmaceutical companies and universities and other research institutions. Some of the pharmaceutical and biotechnology companies we expect to compete with include microbiome-based development companies such as Second Genome, Inc., Seres Health, Inc., Enterome SA, Vedanta Biosciences, Inc., and Rebiotix, Inc. Smaller or early-stage companies may also prove to be significant competitors, particularly through collaborative arrangements with large, established companies. We will also compete with providers of a wide variety of lactase supplements (the most widely used supplement in the United States being Lactaid®), probiotic/dietary supplements, and lactose-free and dairy-free products. We believe the key competitive factors that will affect the development and commercial success of our product candidates are efficacy, safety and tolerability profile, reliability, convenience of dosing, price and reimbursement.

Intellectual Property

The proprietary nature of, and protection for, our product candidates and our discovery programs, processes and know-how are important to our business. We have sought patent protection in the United States and internationally for uses of RP-G28 and our discovery programs, and any other inventions to which we have rights, where available and when appropriate. Our policy is to pursue, maintain and defend patent rights, whether developed internally or licensed from third parties, and to protect the technology, inventions and improvements that are commercially important to the development of our business. We also rely on trade secrets that may be important to the development of our business. We do not have composition of matter patent protection in the United States for RP-G28, which may result in competitors being able to offer and sell products so long as these competitors do not infringe any other patents that we hold, including patents directed to methods of manufacturing and purified RP-G28 or directed to methods of using RP-G28.

Our commercial success will depend in part on obtaining and maintaining patent protection and trade secret protection of RP-G28 and any future product candidates and the methods used to develop and manufacture them, as well as successfully defending these patents against third-party challenges. Our ability to stop third parties from making, using, selling, offering to sell or importing our products depends on the extent to which we have rights under valid and enforceable patents or trade secrets that cover these activities. We cannot be sure that patents will be granted with respect to any of our pending patent applications or with respect to any patent applications filed by us in the future, nor can we be sure that any of our existing patents or any patents that may be granted to us in the future will be commercially useful in protecting our product candidates, discovery programs and processes from commercial competition. Furthermore, we cannot be sure that issued patents will not be challenged in court as invalid or in the Patent Office as unpatentable. For this and more comprehensive risks related to our intellectual property, please see “Risk Factors — Risks Relating to Our Intellectual Property.”

| 17 |

Patents and Proprietary Rights Covering Our Drug Candidates