PART I

ITEM 1.BUSINESS

We are a leading global chemical and ingredientsingredient distributor and provider of specialty services.value-added services to customers across a wide range of diverse industries. We purchase chemicals and ingredients from thousands of chemical producers worldwide andto warehouse, repackage, blend, dilute, transport and sell those chemicals to more than 100,000 customer locations across approximately 130 countries. Our specialized services include e-commerceWe operate an extensive worldwide chemical and digital marketingingredient distribution network, comprised of chemicals formore than 650 facilities and serviced by hundreds of tractors, railcars, tankers and trailers operating daily through our producers, chemical waste removalfacilities.

Chemical and ancillary services, on-site storage of chemicals for our customers, and support services for the agricultural and pest control industries. We derive competitive advantage from our scale, broad product offering, leading digital solutions, technical expertise, specialized services, long-standing relationships with leading chemical producers and our industry leading safety record.

The effects of market conditions on our operations are discussed in Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Recent Developments

On February 28, 2019, we generated $8.6 billionacquired Nexeo Solutions, Inc. (“Nexeo”), a leading global chemicals and plastics distributor. The acquisition expanded and strengthened our presence in netNorth America and provides expanded opportunities to create the largest North American sales net incomeforce in chemical and ingredients distribution coupled with a broad and deep product offering.

On March 29, 2019, we sold the plastics distribution business of $172.3 millionNexeo to an affiliate of One Rock Capital Partners, LLC and $640.4 million in Adjusted EBITDA. For a reconciliationon December 31, 2019, we sold our Environmental Sciences business to affiliates of Adjusted EBITDA to net income (loss), see “Selected Financial Data”AEA Investors LP.

See “Note 3: Business combinations” and “Note 4: Discontinued operations and dispositions” in Item 68 of this Annual Report on Form 10-K.

Our Segments

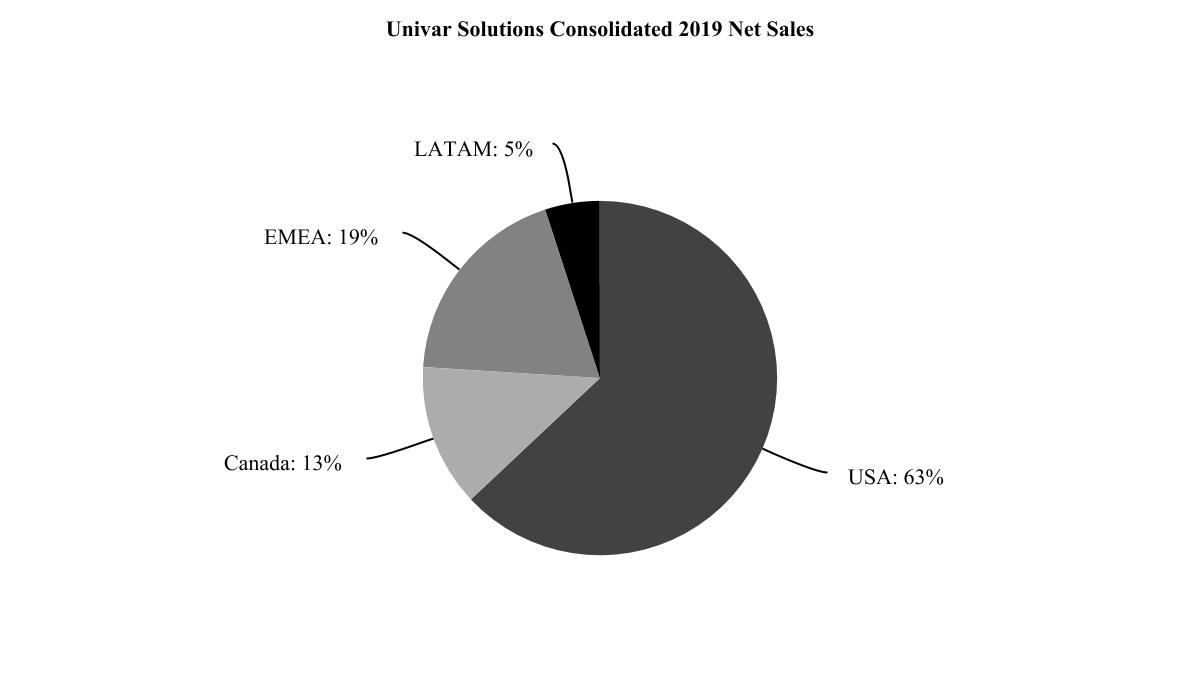

Our business is organized and managed in four geographical segments: Univar Solutions USA (“USA”), Univar Solutions Canada (“Canada”), Univar Solutions Europe and the Middle East and Africa (“EMEA”), and Rest of WorldUnivar Solutions Latin America (“Rest of World”LATAM”), which is predominantlyincludes developing businesses in Latin America.America (including Brazil and Mexico) and the Asia-Pacific region. For additional information on our geographical segments, see “Note 22:23: Segments” in Item 8 of this Annual Report on Form 10-K for additional information.

4

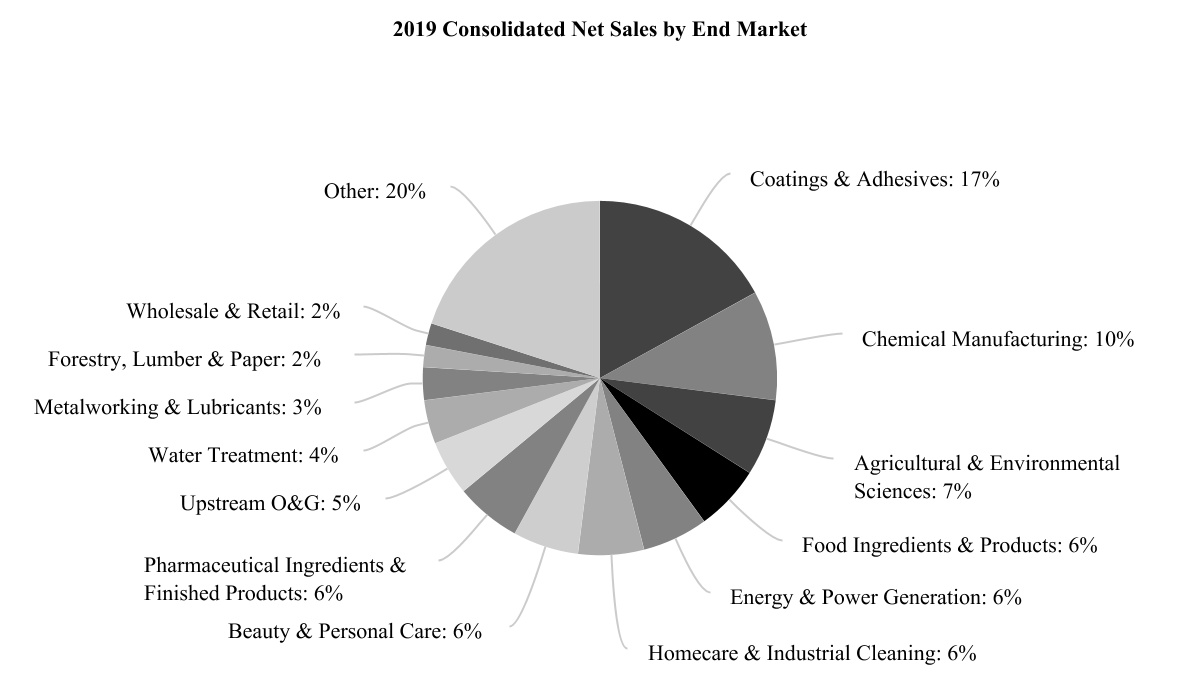

The following graph reflects the breakdown by segment of our 2019 consolidated net sales of $9.3 billion.

USA

We supply a broad offering of commodity and specialty chemicals and ingredients, as well as specialized services to a wide range of end markets, touching a majority of the manufacturing and industrial production sectors in the United States. OurWe believe our close proximity to customers, combined with our deep product knowledge and end market expertise, serves as a competitive advantage.

We repackage and blend bulk chemicals for shipment by our transportation fleet as well as common carriers. Our highly skilled salesforcesales force is deployed bythrough a geographic sales district model as well as by end-use market and industry e.g.(e.g., coatings and adhesives,adhesives), food ingredients and products, pharmaceutical ingredients and products, personal care, homecare and energy.industrial cleaning and energy (upstream, midstream and downstream).

Canada

Our Canadian operations are regionally focused, with a highly skilled salesforcesales force supplying a broad offering of commodity and specialty chemicals and specialized services. We sell into the industrial, agricultural and energy markets. In agriculture, we formulate and distribute inoculants, crop protection and fertilizer products to independent retailers and specialty applicators servicing the agricultural end markets in both Western Canada and Eastern Canada and we provide support services to agricultural chemical producers throughout the local customer base.country. In Eastern Canada, we primarily focus on industrial markets such as food ingredients, pharmaceutical ingredients, coatings and adhesives, and chemical manufacturing. We also service the cleaning and sanitation, personal care, mining, and energy markets. In Western Canada, we focus on forestry, chemical manufacturing, mining, and energy markets (e.g., midstream gas pipeline, oil sands processing and oil refining). Lastly, due to its

EMEA

We maintain a strong presence in the United Kingdom and Continentalcontinental Europe with sales offices in 2021 countries. We also have fourthree sales offices in the Middle East and Africa.

We execute primarily on a pan-European basis, leveraging centralized or shared information technology systems, raw materials procurement, logistics, route operations and the management of producer relationships where possible to benefit from economies of scale and improve cost efficiency. We have strong end market expertise and key account management capability across Europe to better support sales representatives in each country and for serving our key customer end markets, namelyin industrial production, pharmaceutical ingredients, and finished products, food ingredients, coating and adhesives and personal care.

We operateoffer generic and specialty chemicals and ingredients, as well as technical and market expertise, specialized services and key account management to a wide range of end markets including industrial production, personal care, coatings and adhesives, energy and agriculture through sales offices, Solution Centers and distribution sites in Mexico, Brazil, Colombia and

5

to a lesser extent the Asia-Pacific region. We continue to look for expansion opportunities throughout Latin America and opened a new sales center in Colombia, in 2018.

In addition to selling and distributing chemicals, we use our transportation and warehousing infrastructure, along with our broad knowledge of chemicals and hazardous materials handling to provide important distribution and specialized services for our producers and our customers.

We have state-of-the-art Solutions Centers at locations across the globe, consisting of formulation labs, development and research centers, and test kitchens, with specialized industry expertise and innovative technical capabilities to solve our customer's technical challenges and accelerate product development cycles.

Our key global end markets include:

•Agricultural. Within the agriculture industry we are a leading wholesale distributor of crop protection products to independent retailers and specialty applicators in Canada. To support this end market, we distribute herbicides, fungicides, insecticides, seed, seed treatments, inoculants, micronutrients, macronutrients, horticultural products and fertilizers among other products. In addition, we provide storage, packaging and logistics services for major crop protection companies.

•Beauty and Personal Care. We are a full-line distributor in the beauty and personal care industry providing a wide variety of specialty and basic chemicals and ingredients used in skin and hair care products.

•Chemical Manufacturing. We distribute a full suite of chemical products in support of the chemical manufacturing industry (organic, inorganic and polymer chemistries).

•Coatings and Adhesives. We sell resins, pigments, solvents, thickeners, dispersants and other additives used to make paints, inks, and coatings. Our product line includes epoxy resins, polyurethanes, titanium dioxide, fumed silica, esters, plasticizers, silicones and specialty amines.

•Energy (up, mid and downstream). We provide chemicals and service to midstream pipeline and downstream refinery operators primarily in the US and Canada, including oil sands production. We also service the upstream US shale hydraulic-fracturing sector, by providing bulk chemicals to drill sites.

•Food Ingredients and Products. We distribute a diverse portfolio of commodity and specialty products that are sold into the food industry. The major food and beverage markets we purchaseserve are meat processing, baked goods, dairy, grain mill products, processed foods, carbonated soft drinks, fruit drinks and alcoholic beverages.

•Forestry, Lumber, Paper.We serve the forest industry across Canada, supplying a complete range of chemical products for use at all stages of production, from sap stain prevention to pulp and paper manufacturing.

•Homecare & Industrial Cleaning. We offer an extensive range of quality ingredients for cleaners, detergents, and disinfectant products. We distribute chemicals manufactured by many of the industry’s leading producers of enzymes, surfactants, solvents, dispersants, thickeners, bleaching aides, builders, sealants, acids, alkalis and other chemicals that are used as ingredients and processing aids in bulk form,the manufacturing of cleaning and sanitation products.

•Metalworking & Lubricants. Our broad and diverse range of products include base stocks, performance-enhancing additives for both lubricants and metalworking fluids.

•Pharmaceutical Ingredients and Finished Products. Our portfolio includes products along the medicinal production chain, where we repackage them into various size containersoffer a broad portfolio of excipients, solvents, reactants, active pharmaceutical ingredients and intermediates to pharmaceutical ingredient producers.

•Water Treatment. We offer a broad portfolio of products for salewater treatment that includes pH adjusters, flocculants, coagulants, dechlorinators and distribution.disinfectants.

6

Commodity chemicals and ingredients represent the largest portion of our business by sales and volume. Our commodity portfolio includes acids and bases, surfactants, glycols, inorganic compounds, alcohols and general chemicals used extensively throughout most end markets. Our specialty chemicals and ingredient sales represent an important, high-value, higher-growth portion of the chemical distribution market. We typically sell specialty products in lower volumes, but at a higher profit than commodity products and our intent is to increase our presence in the specialty market. While many producers supply specialty products directly to customers, there is an increasing trend toward outsourcing the distribution of these specialized, lower volume products and ingredients. We believe that customers and producers value Univar’s ability to supply both commodity and specialty products, particularly as the markets continue to consolidate.

Services

In addition to selling and distributing chemicals, we use our transportation and warehousing infrastructure, along with our broad knowledge of chemicals and hazardous materials handling, to provide important distribution and specialized services for our producers and our customers. This intermediary role Univar plays is increasingly important, in particular due to the recent trend of increased outsourcing of distribution by chemical producers to satisfy their need for supply chain efficiency. These services include:

•Inventory Management. We manage our inventory in order to meet customer demands on short notice whenever possible. Our value as channel partners of chemical producers also enables us to obtain access to chemicals in times of short supply, when smaller chemical distributors may not be able to obtain or maintain stock. Further, our global distribution network permits us to stock products locally to enhance “just-in-time” delivery, providing outsourced inventory management to our customers in a variety of end markets.

•Mixing, Blending and Repackaging. We provide a full suite of blending and repackaging services for our customers across diverse industries. Additionally, we can fulfill small orders through our repackaging services, enabling customers to maintain smaller inventories.

•Specialized Formulation and Blending. Leveraging our technical expertise, we are able to utilize our blending and mixing capabilities to create specialty chemical formulations to meet specific customer performance demands for agriculture and energy products through our Future Group, Tagma,products.

Suppliers

We source materials from thousands of producers around the globe and Magnablend blending services.

7

Distribution Channels

Warehouse distribution

Our warehouse distribution channel is the core of our operations.operations and connects large producers with smaller volume customers whose consumption patterns tend to make them uneconomical to be served directly by producers. Thus, the core customer serviced via our warehouses is a small or medium-volume consumer of chemicals and ingredients. We purchase chemicals and ingredients in truck load or larger quantities from producers based on contracted demands of our customers and our estimates of anticipated customer purchases. Once received, products are stored in one or more of our distribution facilities for sale and distribution in smaller, less-than-truckload quantities to our customers. Our warehouses have various facilities for services such as repackaging, blending and mixing to create specialized solutions needed by our customers in ready-to-use formulations.

Direct distribution

Competition

The chemical and ingredient production, distribution and sales markets are highly competitive. Most of the products that we distribute are made to standard specifications and are either produced by or available from multiple sources.

Chemical and ingredient distribution itself is a fragmented market in which only a small number of competitors have substantial international operations. Our principal large international competitor is Brenntag, which has a particularly strong position in Europe.Europe due to its strong market position in Germany.

Many other chemical distributors operate on a regional, national or local basis and may have a strong relationship with local producers and customers that may give them a competitive advantage in their local market. Some of our competitors are either local or regional distributors with a broad product portfolio,market, while others are niche players which focus on a specific end market, either industry or product-based. In addition to Brenntag, some of our regional competitors in North America include Helm America, Hydrite Chemical, Azelis, IMCD and Maroon Group and some of our regional competitors in Europe include Azelis, Helm and IMCD.

Chemical and ingredient producers may also sell their products through a direct sales force or through multiple chemical distributors, limit their use of third party distributors, particularly with respect to higher margin products, or to partner with other chemical and ingredient producers for distribution. Each of which could increase our competition.

We compete on the basis of service, on-time delivery, product breadth and availability, product and market knowledge and insights, safety and environmental compliance, global reach, product price, as well as our ability to provide certain additional value-added services.

We operate in a number of jurisdictions and are subject to numerous foreign,international, federal, state and local laws and regulations related to the protection of the environment, human health and safety, including laws regulating discharges of hazardous substances into the soil, air and water, blending, managing, handling, storing, selling, transporting and disposing of hazardous substances, investigation and remediation of contaminated properties and protecting the safety of our employees and others. Some of these laws and regulations include the Comprehensive Environmental Response, Compensation and Liability Act (CERCLA or Superfund), the Toxic Substances Control Act (TSCA), the Resource Conservation and Recovery Act (RCRA), Registration, Evaluation, Authorization and Restriction of Chemicals (REACH), among others. Some of our operations are required to hold environmental permits and licenses to be compliant and certain of our services businesses are also impacted by these laws. The cost of complying with these

Information related to environmental health and safety laws, permits and licenses has, in some instances, been substantial.

We rely primarily on trademarks, copyrightsexpect that there will be a continued increase in demand for products, systems and trade secret lawsservices that meet growing customer sustainability standards, expectations and preferences. We recognize that our ability to establish and maintain our proprietary rights in our intellectual property including technology, creative works and products.continue to provide these

8

products and services including “ChemPoint.com,” “ChemCare,”requires our business to further advance environmentally and “PESTWEB.”socially responsible means of operating, reflecting the challenges and opportunities presented through increased legal requirements, climate parameters and market developments. We believe that our ability to meet these increased sustainability demands will be necessary to enhance our competitive position in the marketplace.

Patents, Licenses and Trademarks

We consider intellectual property, particularly trade secrets, proprietary technology and other similar intellectual property, as important to our success. We hold some patents and have registered numerous trademarks in multiple jurisdictions. Further, we have various patent and trademark applications pending in jurisdictions worldwide. Although we consider our patents, trademarks, trade secrets and licenses to constitute valuable assets, we do not regard any of our businesses as being materially dependent upon an individual patent, trademark, trade secret, or license.

Significant Customers

No single customer accounted for more than 10% of net sales in any of the years presented.

Employees

As of December 31, 2018,2019, we employed more than 8,500 personshad approximately 10,300 employees on a full-time equivalent basis worldwide.

Other

No material part of our business is subject to renegotiation of profits or termination of contracts or subcontracts at the election of any government.

Because we generally fill orders upon receipt, no segment has any significant order backlog.

Information about our Executive Officers

See Part III, Item 10, Directors, Executive Officers and Corporate Governance.

Available Information

We filemaintain a website at www.univarsolutions.com and make available free of charge at this website our Annual Report on Form 10-K, Quarterly Reportsquarterly reports on Form 10-Q, Current Reportscurrent reports on Form 8-K and anyall amendments to those reports as well as proxy statements and registration statements, with the Securities and Exchange Commission (the “SEC”). The SEC maintains a website at www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers, including us, that file electronically. We make our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act available free of charge on or through our website at www.univar.com as soon as reasonably practicable after we filethey are electronically filed with or furnish themfurnished to the SEC. The contents ofinformation on our website areis not, however,and will not be deemed to be, a part of this Annual Report on Form 10-K, or incorporated into any of our other filings with the SEC, filings.except where we expressly incorporated such information. If you wish to receive a paper copy of any exhibit to our reports filed with or furnished to the SEC, the exhibit may be obtained by writing to: Corporate Secretary, Univar Solutions Inc., 3075 Highland Parkway Suite 200, Downers Grove, Illinois 60515.

Item 1A. RISK FACTORS

We are affected by general economic conditions, particularly fluctuations in industrial production and consumption, and an economic downturn could adversely affect our operations and financial results.

We sell chemicals that are used in manufacturing processes and as components of or ingredients in other products. Our sales are correlated with and affected by fluctuations in the levels of industrial production, manufacturing output, and general economic activity. For example, demand for our oil, gas and mining products and services is affected by factors such as the level of exploration, drilling, development and production activity of, and the corresponding capital spending by, oil, gas and mining companies and oilfield service providers, and trends in oil, gas and mineral prices. Producers of commodity and specialty chemicals are likely to reduce their output in periods of significant contraction in industrial and consumer demand, while demand for the products we distribute depends largely on trends in demand in the end markets our customers serve. A majority of our sales are in North America and Europe and our business is therefore susceptible to downturns in those economies as well as, to a lesser extent, the economies in the rest of the world. Our profit margins, as well as overall demand for our products and services, could decline as a result of a large number of factors outside our control, including economic recessions, reduced customer demand (whether due to changes in production processes, consumer preferences, the industries in which the customer operates, laws and regulations affecting the chemicals industry and the manner in which they are enforced, or other factors), inflation, fluctuations in interest and currency exchange rates, and changes in the fiscal or monetary policies of governments in the regions in which we operate.

General economic conditions and macroeconomic trends, as well as the creditworthiness of our customers, could affect overall demand for chemicals. Any overall decline in the demand for chemicals could significantly reduce our sales and profitability. If the creditworthiness of our customers declines, we would face increased credit risk. In addition, volatility and

9

disruption in financial markets could adversely affect our sales and results of operations by limiting our customers’ ability to obtain financing necessary to maintain or expand their own operations.

A historical feature of past economic weakness has been significant destocking of inventories, including inventories of chemicals used in industrial and manufacturing processes. It is possible that an improvement in our net sales in a particular period may be attributable in part to restocking of inventories by our customers and represent a level of sales or sales growth that will not be sustainable over the longer term. Further economic weakness could lead to insolvencies among our customers or producers, as well as among financial institutions that are counterparties on financial instruments or accounts that we hold. Any of these developments could have a material adverse effect on our business, financial condition and results of operations.

Significant changes in the business strategies of producers could also disrupt our supply. Large chemical manufacturers may elect to sell certain products (or products in certain regions) directly to customers, instead of relying on distributors such as us. While we do not believe that our results depend materially on access to any individual producer’s products, a reversal of the trend toward more active use of distributors would likely result in increasing margin pressure or products becoming unavailable to us. Any

In addition, unpredictable events may have a significant impact on the industries in which many of these developmentsour customers operate, reducing demand for products that we normally distribute in significant volumes. Significant disruptions of supply and disruptions in customer industries could have a material adverse effect on our business, financial condition and results of operations.

The markets in which we operate are highly competitive.competitive and we may not be able to compete successfully.

The chemical distribution market is highly competitive. Chemicals can be purchased from a variety of sources, including traders, brokers, wholesalers and other distributors, as well as directly from producers. Many of the products we distribute or finish are essentially fungible with products offered by our competition, including emerging competitors. The competitive pressure we face is particularly strong in sectors and markets where local competitors have strong positions or where new competitors can easily enter. Increased competition from distributors of products similar to or competitive with ours could result in price reductions, reduced margins and a loss of market share.

We expect to continue to experience significant and increasing levels of competition in the future. We must also compete with smaller companies that have been able to develop strong local or regional customer bases. In certain countries, some of our competitors are more established, benefit from greater name recognition and have greater resources within those countries than we do.

Consolidation of our competitors in the markets in which we operate could place us at a competitive disadvantage and reduce our profitability.

We operate in an industry, which is highly fragmented on a global scale, but in which there has been a trend toward consolidation in recent years. ConsolidationsConsolidation of our competitors may also further enhance their financial position, provide them with the ability to offer more competitive prices to customers for whom we compete, and allow them to achieve increased efficiencies in their consolidated operations that enable them to more effectively compete for customers. This may jeopardize the strength of our positions in one or more of the markets in which we operate and any advantages we currently enjoy due to the comparative scale of our operations. Losing some of those advantages could adversely affect our business, financial condition and results of operations, as well as our growth potential.

We purchase and sell a wide variety of chemicals, the price and availability of which may fluctuate, and may be subject to large and significant price increases. Many of our contracts with producers include chemical prices that are not fixed or are tied to an index, which allows our producers to change the prices of the chemicals we purchase as the price of the chemicals fluctuates in the market. Changes in chemical prices affect our net sales and cost of goods sold, as well as our working capital requirements, levels of debt and financing costs. We might not always be able to reflect increases in our chemical costs, transportation costs and other costs in our own pricing. Any inability to pass cost increases onto customers may adversely affect our business, financial condition and results of operations.

10

In order to meet customer demand, we typically maintain significant inventories, and we are therefore subject to a number of risks associated with our inventory levels, including the following:

•declines in the prices of chemicals that are held by us;

•the need to maintain a significant inventory of chemicals that may be in limited supply and therefore difficult to procure;

•buying chemicals in bulk for the best pricing and thereby holding excess inventory;

•responding to the fluctuating demand for chemicals;

•cancellation of customer orders; and

•responding to customer requests for rapid delivery.

In order to manage our inventories successfully, we must estimate demand from our customers and purchase chemicals that substantially correspond to that demand. If we overestimate demand and purchase too much of a particular chemical, we face a risk that the price of that chemical will fall, leaving us with inventory that we cannot sell profitably or have to write down such inventory from its recorded value. If we underestimate demand and purchase insufficient quantities of a particular chemical and prices of that chemical rise, we could be forced to purchase that chemical at a higher price and forego profitability in order to meet customer demand. Our business, financial condition and results of operations could suffer a material adverse effect if either or both of these risks without substantial expense, delaysituations occur frequently or in large volumes.

Our indebtedness may adversely affect our business, financial condition and operating results.

As of December 31, 2019, we had $2,713.8 million of total debt. Our indebtedness may have material adverse effects on our business, financial condition and operating results. The amount of our debt, as well as any additional debt or other operational or financial problems.

•our ability to satisfy obligations to lenders or note holders may be impaired, resulting in possible defaults on and acceleration of management attention;our indebtedness;

•our assets that currently serve as collateral for regulatory reasons to dispose of a portion of our existingdebt may be insufficient, or acquired businesses); and

•a substantial portion of our cash flow from operations could be used to repay the principal and interest on acceptable termsour debt;

•we may be increasingly vulnerable to economic downturns and increases in interest rates;

•our flexibility in planning for and reacting to changes in our business and the markets in which we operate may be limited; and

•we may be placed at a competitive disadvantage relative to other companies in our industry with less debt or comparable debt at more favorable interest rates.

The agreements governing our indebtedness contain operating covenants and restrictions that limit our operations and could lead to adverse consequences if we fail to comply with them.

The agreements governing our indebtedness contain certain operating covenants and when required, particularly becauseother restrictions relating to, among other things, limitations on indebtedness (including guarantees of additional indebtedness) and liens, mergers, consolidations and dissolutions, sales of assets, investments and acquisitions, dividends and other restricted payments, repurchase of shares of capital stock and options to purchase shares of capital stock and certain transactions with affiliates. In addition, our current high leverageNorth American ABL Facility and Euro ABL Facility include certain financial covenants.

Failure to comply with these financial and operating covenants could result from, among other things, changes in our results of operations, the incurrence of additional indebtedness, the pricing of our products, our success at implementing cost reduction initiatives, our ability to successfully implement our overall business strategy or changes in general economic conditions, which may make it difficultbe beyond our control. The breach of any of these covenants or impossible for us to secure additional financing for acquisitions.

11

As a result of our current and past operations, we may becomeare subject to liabilities.

Previous operations, including those of acquired companies, have resulted in contamination at a number of current and former sites, which must be investigated and remediated. We have ongoing investigations and remediation activities, or are contributing to cleanup costs, at approximately 107 currently or formerly owned, operated or used sites or other sites impacted by CVC.our operations. We have spent substantial sums on such investigation and remediation and we expect to continue to incur such expenditures in the future. We may also recognize additional goodwill and intangible assetsincur losses in connection with future business acquisitions. Goodwillinvestigation and remediation obligations that exceed our environmental reserve. There is not amortized for book purposes. We test for impairment annually using a fair value based approach. We also test goodwill for impairment if an event occurs or circumstances changeno guarantee that indicateour estimates will be accurate, that the fair value of a reporting unit has more likely than not declined below its carrying value. The identification and measurement of impairment involves the estimation of the fair value of reporting units, which requires judgment and involves the use of significant estimates and assumptions by management. The estimates of fair value of reporting units are based on the best information available as of the date of the assessment and incorporate management assumptions about expected future cash flows and contemplate other valuation techniques. Our estimates of future cash flows may differ from actual cash flows that are subsequently realized due to many factors, including future worldwide economic conditions and the expected benefits of our initiatives, among other things. Intangible assets are amortized for book purposes over their respective useful lives and are tested for impairment if any event occurs or circumstances change that indicates that carrying value maynew contamination will not be recoverable. Although we currently do not expectdiscovered or that our goodwill and intangible assets will be further impaired, we cannot guarantee that a material impairmentnew environmental laws or regulations will not occur, particularly inrequire us to incur additional costs. Any such inaccuracies, discoveries or new laws or regulations, or the eventinterpretation of a substantial deterioration in our future prospects either in total or in a particular reporting unit. See “Note 13: Goodwillexisting laws and intangible assets” in Item 8 of this Annual Report on Form 10-K for a discussion of our 2018 impairment review. If our goodwill and intangible assets become impaired, itregulations, could have a material adverse effect on our business, financial condition and results of operations.

We could be held liable for the costs to investigate, remediate or otherwise address contamination at any real property we have ever owned, leased, operated or used or other sites impacted by our operations. Some environmental laws could impose on us the entire cost of cleanup of contamination present at a site even though we did not cause all of the contamination. These laws often identify parties who can be strictly and jointly and severally liable for remediation. The discovery of previously unknown contamination at current or former sites or the imposition of other environmental liabilities or obligations in the future, including additional investigation or remediation obligations with respect to contamination that has impacted other properties, could lead to additional costs or the need for additional reserves that have a material adverse effect on our business, financial condition and results of operations. In addition, we may be required to pay damages or civil judgments related to third party claims, including those relating to personal injury (including exposure to hazardous materials or chemicals we blend, handle, store, sell, transport or dispose of), product quality issues, property damage or contribution to remedial obligations. We have been identified as a potentially responsible party at certain third party sites at which we have arranged for the disposal of our hazardous wastes. We may be identified as a potentially responsible party at additional sites beyond those for which we currently have financial obligations. Such developments could have a material adverse effect on our business, financial condition and results of operations.

Societal concerns regarding the safety of chemicals in commerce and their potential impact on the environment have resulted in a growing trend towards increasing levels of product safety and environmental protection regulations. These concerns could influence public perceptions, impact the commercial viability of the products we sell and increase the costs to comply with increasingly complex regulations, which could have a negative impact on our business, financial condition and results of operations. Additional findings by government agencies that chemicals pose significant environmental, health or safety risks may lead to their prohibition in some or all of the jurisdictions in which we operate.

We may be unable to integrate the business of Nexeo successfully or realize the anticipated benefits of the acquisition.

We are required to devote significant management attention and resources to integrating the business practices and operations of Nexeo and the Company. Potential difficulties that we may encounter as part of the integration process include the following:

•the inability to successfully combine Nexeo and manage the combined business in a manner that permits us to achieve, on a timely basis, or at all, the enhanced revenue opportunities and cost savings and other benefits anticipated to result from the Nexeo acquisition; and

•complexities associated with managing the combined businesses, including difficulty addressing possible differences in corporate cultures and management philosophies and the challenge of integrating complex systems, technology, networks and other assets of each of the companies in a seamless manner that minimizes any adverse impact on customers, suppliers, employees and other constituencies.

12

These issues could adversely affect our ability to maintain relationships with customers, suppliers, employees and other constituencies or achieve the anticipated benefits of the acquisition, or could reduce our earnings or otherwise adversely affect our business and financial results following the acquisition.

Our business could be seriously impacted by business disruptions and security breaches, including cybersecurity incidents.

Business and/or supply chain disruptions, plant downtime, and/or power outages, and information technology system and/or network disruptions, regardless of cause, including acts of sabotage, employee error or other actions, geo-political activity, military actions, terrorism (including cyber-attacks), weather events, and natural disasters could seriously harm our operations as well as the operations of our customers and suppliers. Any such event could have a negative impact on our business, results of operations, financial condition, and cash flows.

Cyber-attacks or security breaches could compromise confidential, business critical information, cause a disruption in the Company’s operations or harm the Company’s reputation. While the Company has a comprehensive cyber-security program that is continuously reviewed, maintained and upgraded, there can be no assurance that such procedures, controls, and intelligence will be sufficient to prevent security breaches from occurring. If any security breaches were to occur, they could lead to losses of sensitive information, critical infrastructure or capabilities essential to our operations and could have a material adverse effect on our reputation, financial position, results of operations or cash flows, and could result in claims being brought against us.

We require significant working capital, and we expect our working capital needs to increase in the future, which could result in having lower cash available for, among other things, capital expenditures and acquisition financing.

We require significant working capital to purchase chemicals from chemical producers and distributors and sell those chemicals efficiently and profitably to our customers. Our working capital needs may increase if the price of products we purchase and inventory increase. Our working capital needs also increase at certain times of the year, as our customers’ requirements for chemicals increase. For example, our customers in the agricultural sector require significant deliveries of chemicals within a growing season that can be very short and depend on weather patterns in a given year. We need inventory on hand to have product available to ensure timely delivery to our customers. If our working capital requirements increase and we are unable to finance our working capital on terms and conditions acceptable to us, we may not be able to obtain chemicals to respond to customer demand, which could result in a loss of sales.

In addition, the amount of working capital we require to run our business is expected to increase in the future due to expansions in our business activities. If our working capital needs increase, the amount of free cash we have at our disposal to devote to other uses will decrease. A decrease in free cash could, among other things, limit our flexibility, including our ability to make capital expenditures and to acquire suitable acquisition targets that we have identified. If increases in our working capital occur and have the effect of decreasing our free cash, it could have a material adverse effect on our business, financial condition and results of operations.

We have a history of net losses and may not sustain profitability in the future.

Although we maintain a significant portfolio of owned and leased transportation assets, including trucks, trailers and railcars,rail cars, we also rely on transportation and warehousing provided by third parties (including common carriers and rail companies) to deliver products to our customers. Our access to third party transportation is not guaranteed, and we may be unable to transport chemicals at economically attractive rates in certain circumstances, particularly in cases of adverse market conditions or disruptions to transportation infrastructure. We are also subject to increased costs that we may not always be able to recover from our customers, including fuel prices, as well as charges imposed by common carriers, leasing companies and other third parties involved in transportation. In particular, our US operations rely to a significant extent on rail shipments, and we are therefore required to pay rail companies’ network access fees. We can also experience the availability of trucks and drivers tighten. We are also subject to the risks normally associated with product delivery, including inclement weather, disruptions in the transportation infrastructure, disruptions in our lease arrangements and the availability of fuel, as well as liabilities arising from accidents to the extent we are not adequately covered by insurance or misdelivery of products. Our failure to deliver products in a timely and accurate manner could harm our reputation and brand, which could adversely affect our business, financial condition and results of operations.

Accidents, safety failures, environmental damage, product quality issues, major or systemic delivery failures involving our distribution network or the products we carry, or adverse health effects or other harm related to hazardous materials we blend, manage, handle, store, sell, transport or dispose of could damage our reputation and result in substantial damages or remedial obligations.

Our business depends to a significant extent on our customers’ and producers’ trust in our reputation for reliability, quality, safety and environmental responsibility. Actual or alleged instances of safety deficiencies, mistaken or incorrect deliveries, inferior product quality, exposure to hazardous materials resulting in illness, injury or other harm to persons, property or natural resources, or of damage caused by us or our products, could damage our reputation and lead to customers and producers curtailing the volume of business they do with us. Also, there may be safety, personal injury or other environmental risks related to our products which are not known today. Any of these events, outcomes or allegations could also subject us to substantial legal claims, and we could incur substantial expenses, including legal fees and other costs, in defending such legal claims, which could materially impact our financial position and results of operations.

13

Actual or alleged accidents or other incidents at our facilities or that otherwise involve our personnel or operations could also subject us to claims for damages by third parties. Because many of the chemicals that we handle are dangerous, we are subject to the ongoing risk of hazards, including leaks, spills, releases, explosions and fires, which may cause property damage, illness, physical injury or death. We sell products used in hydraulic fracturing, a process that involves injecting water, sand and chemicals

into subsurface rock formations to release and capture oil and natural gas. The use of such hydraulic fracturing fluids by our customers may result in releases that could impact the environment and third parties. Several of our distribution facilities including our Los Angeles facility, one of our largest, are located near high-density population centers. If any such events occur, whether through our own fault, through preexisting conditions at our facilities, through the fault of a third party or through a natural disaster, terrorist incident or other event outside our control, our reputation could be damaged significantly. We could also become responsible, as a result of environmental or other laws or by court order, for substantial monetary damages or expensive investigative or remedial obligations related to such events, including but not limited to those resulting from third party lawsuits or environmental investigation and cleanup obligations on and off-site. The amount of any costs, including fines, damages and/or investigative and remedial obligations, that we may become obligated to pay under such circumstances could substantially exceed any insurance we have to cover such losses.

Any of these risks, if they materialize, could significantly harm our reputation, expose us to substantial liabilities and have a material adverse effect on our business, financial condition and results of operations.

Our business exposes us to potential product liability claims and recalls, which could adversely affect our financial condition and performance.

The repackaging, blending, mixing, manufacture, sale and distribution of chemical products by us, including products used in hydraulic fracturing operations and products produced with food ingredients or with pharmaceutical and nutritional supplement applications, involve an inherent risk of exposure to product liability claims, product recalls, product seizures and related adverse publicity, including, without limitation, claims for exposure to our products, spills or escape of our products, personal injuries, food related claims and property damage or environmental claims. A product liability claim, judgment or recall against our customers could also result in substantial and unexpected expenditures for us, affect consumer confidence in our products and divert management’s attention from other responsibilities. Although we maintain product liability insurance, there can be no assurance that the type or level of coverage is adequate or that we will be able to continue to maintain our existing insurance or obtain comparable insurance at a reasonable cost, if at all. A product recall or a partially or completely uninsured judgment against us could have a material adverse effect on our business, financial condition and results of operation.

Our business is subject to additional general regulatory requirements and tax requirements, which increase our cost of doing business, could result in regulatory, unclaimed property or tax claims and enforcement actions, and could restrict our business in the future.

Our general business operations are subject to a broad spectrum of general regulatory requirements,international, federal, state, and local laws and regulations, including, without limitation, those relating to antitrust, regulations, food and drug, regulations,labor and human resources, regulations, tax, regulations, unclaimed property, transportation, anti-bribery, banking and treasury, regulations,privacy and data protection (including the European Union's General Data Protection Regulation), hydraulic fracturing or other oil and gas production activities, among others. These laws and regulations add cost to our conduct of business and could, in some instances, result in claims or enforcement actions or could reduce our ability to pursue business opportunities. FutureAny changes could result in additional coststhe laws and restrictions to our business activities. We are currently undergoing a multi-state unclaimed property audit, the timing and outcome of which cannot be predicted; we will incur significant professional fees in connection with the audit and if we are found not to be in compliance the auditing states may seek significant remittances and other penalties and interest.

14

We are exposed to risks including, but not limited to, accidents, contamination and environmental damage, safety claims, natural disasters, terrorism, acts of war and civil unrest and other events that could potentially interrupt our business operations and/or result in significant costs. Although we attempt to cover these risks with insurance to the extent that we consider appropriate, we may incur losses that are not covered by insurance or exceed the maximum amounts covered by our insurance policies. Even if our insurance coverage is appropriate, our insurers may contest, and prevail in litigation regarding, and claims. We have incurred environmental risks and losses, often from our historic activities, for which we have no available or remaining insurance.

We are subject to the risk of litigation, other legal claims and proceedings, and regulatory enforcement actions in the ordinary course of our business. Also, there may be safety or personal injury risks related to our products which are not known today. The results of legal proceedings cannot be predicted with certainty. We cannot guarantee that the results of current or future legal proceedings against McKesson and a few claims asserted directly against Univar USA Inc. will not materially harm our business, reputation or brand, nor can we guarantee that we will not incur losses in connection with current or future legal proceedings that exceed any provisions we may have set aside in respect of such proceedings or that exceed any applicable insurance coverage. We also cannot guarantee that any tax assessment previously made against us by the Canada Revenue Agency will not result in a material tax liability or that the issues raised by Customs and Border Patrol will not result in a material liability. The occurrence of any of these events could have a material adverse effect on our business, financial condition or results of operations. See “Business—Legal Proceedings” in Item 1 of this Annual Report on Form 10-K.

Many of the products we sell have “long-tail” exposures, giving rise to liabilities many years after their sale and use. Insurance purchased at the time of sale may not be available when costs arise in the future and producers may no longer be available to provide indemnification.

In June 2016 the U.K. electorate voted in a referendum to voluntarily depart from the E.U., known as Brexit and in December 2019, the U.K. approved the Withdrawal Agreement and left the European Union (“Brexit”) on January 31, 2020.

The potential impact on our results of operations and liquidity resulting from Brexit remains unclear. The actual effects of Brexit will depend upon many factors and significant uncertainty remains with respect to the terms of the ultimate resolution of the Brexit negotiations. The final terms of the withdrawal may impact certain of our commercial and general business operations in the U.K. and the E.U. In addition, Brexit could lead to legal uncertainty and potentially divergent national laws and regulations, including tax and free trade agreements, supply chain logistics, environmental, health and safety laws and regulations and employment laws, as the U.K. determines which E.U. laws to replace or replicate. We cannot predict the direction Brexit-related developments will take nor the impact of those developments on our European operations and the economies of the markets where we operate. This may cause us to adjust our strategy in order to compete effectively in global markets and could adversely affect our business, financial condition, operating results and cash flows.

Our results of operations could suffer if we are unable to expand into new geographic markets or manage the various risks related to our international activities.

Our profitability and longer-term success may be adversely affected if we fail to continue to expand our penetration in certain foreign markets and to enter new and emerging foreign markets. The profitability of our international operations will largely depend on our continued success in the following areas:

•securing key producer relationships to help establish our presence in international markets;

•hiring and training personnel capable of supporting producers and our customers and managing operations in foreign countries;

•localizing our business processes to meet the specific needs and preferences of foreign producers and customers;

•building our reputation and awareness of our services among foreign producers and customers; and

•implementing new financial, management information and operational systems, procedures and controls to monitor our operations in new markets effectively, without causing undue disruptions to our operations and customer and producer relationships.

In addition, we are subject to risks associated with operating in foreign countries, including:

•varying and often unclear legal and regulatory requirements that may be subject to inconsistent or disparate enforcement, particularly regarding environmental, health and safety issues and security or other certification requirements, as well as other laws and business practices that favor local competitors, such as exposure to possible expropriation, nationalization, restrictions on investments by foreign companies or other governmental actions;

•less stable supply sources;

•competition from existing market participants that may have a longer history in and greater familiarity with the foreign markets where we operate;

•tariffs, export duties, quotas and other barriers to trade; as well as possible limitations on the conversion of foreign currencies into US dollars or remittance of dividends and other payments by our foreign subsidiaries;

•divergent labor regulations and cultural expectations regarding employment and agency;

•different cultural expectations regarding industrialization, international business and business relationships;

•foreign taxes and related regulations, including foreign taxes that we may not be able to offset against taxes imposed upon us in the United States, and foreign tax and other laws limiting our ability to repatriate earnings to the United States;

15

•extended payment terms and challenges in our ability to collect accounts receivable;

•changes in a specific country’s or region’s political or economic conditions;

•compliance with anti-bribery laws such as the US Foreign Corrupt Practices Act, the UK Bribery Act and similar anti-bribery laws in other jurisdictions, the violation of which could expose us to severe criminal or civil sanctions; and

•compliance with anti-boycott, privacy, economic sanctions, anti-dumping, antitrust, import and export laws and regulations by our employees or intermediaries acting on our behalf, the violation of which could expose us to significant fines, penalties or other sanctions.

Increases in interest rates would increase the cost of servicing our debt and could reduce our profitability.

Certain of our outstanding debt bears interest at variable rates. As a result, increases in interest rates would increase the cost of servicing our debt and could materially reduce our profitability and cash flows. Approximately $1.8 billion, or 67 percent of our debt is indexed to LIBOR as a benchmark for establishing the rate and we may hold other operational contracts, including leases, that are also indexed to LIBOR. The U.K. Financial Conduct Authority, which regulates LIBOR, has announced that it intends to phase out LIBOR by the end of 2021. If LIBOR ceases to exist, we may need to amend our debt and other certain agreements that use LIBOR as a benchmark and we cannot predict what alternative index or other amendments may be negotiated with our counterparties. As a result, our interest or operating expense could increase and our available cash flow for general corporate requirements may be adversely affected. For additional information on our indebtedness, debt service obligations and sensitivity to interest rate fluctuations, see “Qualitative and Quantitative Disclosures About Market Risk” in Item 7A of this Annual Report on Form 10-K.

We may have future capital needs and may not be able to obtain additional financing on acceptable terms, or at all.

We have historically relied on debt financing to fund our operations, capital expenditures and expansion. The macroeconomic conditions that affect the markets in which we operate and our credit ratings could have a material adverse effect on our ability to secure financing on acceptable terms, if at all. The terms of additional financing may limit our financial and operating flexibility, and if financing is not available when needed, or is not available on acceptable terms, we may be unable to take advantage of business opportunities or respond to competitive pressures, any of which could have a material adverse effect on our business, financial condition and results of operations.

If we raise additional funds through further issuances of equity, convertible debt securities or other securities convertible into equity, our existing stockholders could suffer significant dilution in their percentage ownership of our company, and any new securities we issue could have rights, preferences and privileges senior to those of holders of our common stock.

Fluctuations in currency exchange rates may adversely affect our results of operations.

We have sizable sales and operations in Canada, Europe, Middle East, Africa, Asia, and Latin America. We report our consolidated results in US dollars and the results of operations and the financial position of our local operations are generally reported in the relevant local currencies and then translated into US dollars at the applicable exchange rates. As a result, our financial performance is impacted by currency fluctuations. For additional details on our currency exposure and risk management practices, see “Quantitative and Qualitative Disclosures About Market Risk” in Item 7A of this Annual Report on Form 10-K.

The integration of our business systems may negatively impact our operations.

We are currently in the process of integrating our legacy business systems into the legacy Nexeo business systems (the “Systems Integration”). The Systems Integration is anticipated to be completed at the end of 2021. Since we will process and reconcile our information from multiple systems until the Systems Integration is complete, the chance of errors is greater. Inconsistencies in the information from multiple systems could adversely impact our ability to manage our business efficiently and may result in heightened risk to our ability to maintain our books and records and comply with regulatory requirements. Any disruptions, delays or deficiencies in the Systems Integration could adversely affect our ability to process orders, track inventory, ship products in a timely manner, prepare invoices to our customers, maintain regulatory compliance and otherwise carry on our business in the ordinary course. The Systems Integration involves numerous risks, including:

•diversion of management’s attention away from normal daily business operations;

•loss of, or delays in accessing, data;

•increased demand on our operations support personnel;

•initial dependence on unfamiliar systems while training personnel to use new systems; and

•increased operating expenses resulting from training, conversion and transition support activities.

Any of the foregoing or if we are unable to implement the Systems Integration successfully, could result in a material increase in information technology compliance or other related costs, and could have a negative impact on our business, financial condition and results of operations.

16

Our balance sheet includes significant goodwill and intangible assets, the impairment of which could affect our future operating results.

We carry significant goodwill and intangible assets on our balance sheet. As of December 31, 2019, our goodwill and intangible assets totaled approximately $2.3 billion and $0.3 billion, respectively. At least annually, the Company assesses goodwill for impairment. If testing indicates that goodwill is impaired, the carrying value is written down based on fair value with a charge against earnings. Where the Company utilizes a discounted cash flow methodology in determining fair value, weakened demand for a specific product line or business could result in an impairment. Intangible assets are amortized for book purposes over their respective useful lives and are tested for impairment if any event occurs or circumstances change that indicates that carrying value may not be recoverable. Accordingly, any determination requiring the write-off of a significant portion of goodwill or intangible assets could negatively impact the Company's financial condition and results of operations. See “Note 15: Goodwill and intangible assets” in Item 8 of this Annual Report on Form 10-K for a discussion of our 2019 impairment review.

We have in the past and may in the future make acquisitions, ventures and strategic investments, some of which may be significant in size and scope, which have involved in the past and will likely involve in the future numerous risks. We may not be able to address these risks without substantial expense, delay or other operational or financial problems.

Acquisitions or investments have involved in the past and will likely involve in the future various risks, such as:

•integrating the technologies, operations and personnel of any acquired business;

•the potential disruption of our ongoing business, including the diversion of management attention;

•the possible inability to obtain the desired financial and strategic benefits from the acquisition or investment;

•customer attrition arising from preferences to maintain redundant sources of supply;

•producer attrition arising from overlapping or competitive products;

•assumption of contingent or unanticipated liabilities or regulatory liabilities;

•dependence on the retention and performance of existing management and work force of acquired businesses for the future performance of these businesses;

•regulatory risks associated with acquired businesses (including the risk that we may be required for regulatory reasons to dispose of a portion of our existing or acquired businesses); and

•the risks inherent in entering geographic or product markets in which we have limited prior experience.

Future acquisitions and investments may need to be financed in part through additional financing from banks, through public offerings or private placements of debt or equity securities or through other arrangements, and could result in substantial cash expenditures. The necessary acquisition financing may not be available to us on acceptable terms if and when required, particularly if our debt leverage levels make it difficult or impossible for us to secure additional financing for acquisitions.

Negative developments affecting our pension and multi-employer pension plans in which we participate may occur.

We operate a number of pension and post-retirement plans for our employees and have obligations with respect to several multi-employer pension plans sponsored by labor unions in the United States. The terms of these plans vary from country to country. The recognition of costs and liabilities associated with the pension and postretirement plans is affected by assumptions made by management and used by actuaries engaged by us to calculate the benefit obligations and the expenses recognized for these plans. The inputs used in developing the required estimates are calculated using a number of assumptions, which represent management’s best estimate of the future. The assumptions that have the most significant impact on costs and liabilities are the discount rate, the estimated long-term return on plan assets for the funded plans, retirement rates, and mortality rates. Changes to the funded status of our pension plans as a result of updates to actuarial assumptions and actual experience that differs from our estimates are recognized as gains or losses in the period incurred under our “mark to market” accounting policy, and could result in a requirement for additional funding.

As of December 31, 2019, our pension plans were underfunded by $234.4 million and our unfunded postretirement plan liabilities were approximately $1.4 million. In recent years, declining interest rates have negatively impacted the funded status of our pension and postretirement plans. If the interest rates continue to decline, funding requirements for our pension plans may become more significant. If our cash flows and capital resources are insufficient to fund our obligations under these pension and postretirement plans, we could be forced to reduce or delay investments and capital expenditures, seek additional capital, or incur indebtedness.

The union sponsored multi-employer pension plans in which we participate are also underfunded, including the substantially underfunded New England Teamsters and Trucking Industry Pension Fund and Central States, Southeast and Southwest Areas Pension Plan, Riskwhich have liabilities that exceed its assets. Often, this requires us to make substantial withdrawal liability payments when we close a facility covered by one of these plans, which could hinder our ability to make otherwise appropriate management decisions to operate as efficiently as possible.

17

A portion of our workforce is unionized and labor disruptions could decrease our profitability.

As of December 31, 2019, approximately 22% of our labor force is covered by a collective bargaining agreement, including approximately 11%, 20%, and 46% of our labor force in the USA, Canada and Europe, respectively. Approximately 3% of our labor force is covered by a collective bargaining agreement that will expire within one year. These arrangements grant certain protections to employees and subject us to employment terms that are similar to collective bargaining agreements. We cannot guarantee that we will be able to negotiate these or other collective bargaining agreements or arrangements with works councils on the same or more favorable terms as the current agreements or arrangements, or at all, and without interruptions, including labor stoppages at the facility or facilities subject to any particular agreement or arrangement. A prolonged labor dispute, which could include a work stoppage, could have a material adverse effect on our business, financial condition and results of operations.

We depend on a limited number of key personnel who would be difficult to replace. If we lose the services of these individuals, or are unable to attract new talent, our business will be adversely affected.

We depend upon the ability and experience of a number of our executive management and other key personnel who have substantial experience with our operations, the chemicals and chemical distribution industries and the selected markets in which we operate. The loss of the services of one or a combination of our senior executives or key employees could have a material adverse effect on our results of operations. We also might suffer an additional impact on our business if one of our senior executives or key employees is hired by a competitor. Our success also depends on our ability to continue to attract, manage and retain other qualified management and technical and clerical personnel as we grow. We may not be able to continue to attract or retain such personnel in the future.

Anti-takeover provisions in our charter documents and Delaware law could discourage, delay or prevent a change in control of our company and may affect the trading price of our common stock.

Our Certificate of Incorporation and By-laws include a number of provisions that may discourage, delay or prevent a change in our management or control over us that stockholders may consider favorable. For example, our Certificate of Incorporation and By-laws currently:

•authorize the issuance of “blank check” preferred stock that could be issued by our Board of Directors to thwart a takeover attempt;

•limit the ability of stockholders to remove directors; and

•establish advance notice requirements for nominations for election to our Board of Directors or for proposing matters that can be acted upon by stockholders at stockholder meetings.

These provisions may prevent our stockholders from receiving the benefit from any premium to the market price of our common stock offered by a bidder in a takeover context. Even in the absence of a takeover attempt or before our Board becomes fully declassified, the existence of these provisions may adversely affect the prevailing market price of our common stock if the provisions are viewed as discouraging takeover attempts in the future. See “Description of Capital Stock—Anti-Takeover Effects of our Certificate of Incorporation and By-laws.” Our Certificate of Incorporation and By-laws may also make it difficult for stockholders to replace or remove our management. These provisions may facilitate management entrenchment that may delay, deter, render more difficult or prevent a change in our control, which may not be in the best interests of our stockholders.

ITEM 1B. UNRESOLVED STAFF COMMENTS.COMMENTS

None.

ITEM 2. PROPERTIES

Our principal executive office is located in Downers Grove, Illinois under a lease expiring in June 2024. As of December 31, 2018,2019, we had 278354 locations in the United States in 47 states. Of thesestates and 336 locations approximately 265 are warehouse facilities responsible for storing and shippingoutside of products and 13 are dedicated office space.the United States in 30 countries. Our warehouse facilities are nearly equally comprised of owned, leased and third party warehouses and our office space is generally leased. Our facilities focus on the storing, repackaging and blending of chemicals and ingredients for distribution. Such facilities do not require substantial investments in equipment, can be opened fairly quickly and replaced with little disruption. As such, we believe that none of our facilities on an individual basis is principalmaterial to the operation of our business. We select locations for our warehouses based on proximity to producers and our customers to maintain efficient distribution networks. We believe that our facilities are adequate and suitable for our current operations. We hold a relatively small number of surplus sites for potential disposition. In some instances, our larger owned sites have been mortgaged under our secured credit facilities.

ITEM 3. LEGAL PROCEEDINGS

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

18

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information for Common Stock

Our common stock is listed on the New York Stock Exchange under the symbol “UNVR”.UNVR.

Holders of Record

As of December 31, 2018,2019, there were 2 stockholders of record12 holders of our common stock,Common Stock, as determined by counting our record holders and the closing pricenumber of participants reflected in a security position listing provided to us by the Equiniti Trust Company (EQ). Because such EQ participants are brokers and other institutions holding shares of our common stock was $17.74 per share as reportedCommon Stock on behalf of their customers, we do not know the New York Stock Exchange.actual number of unique shareholders represented by these record holders.

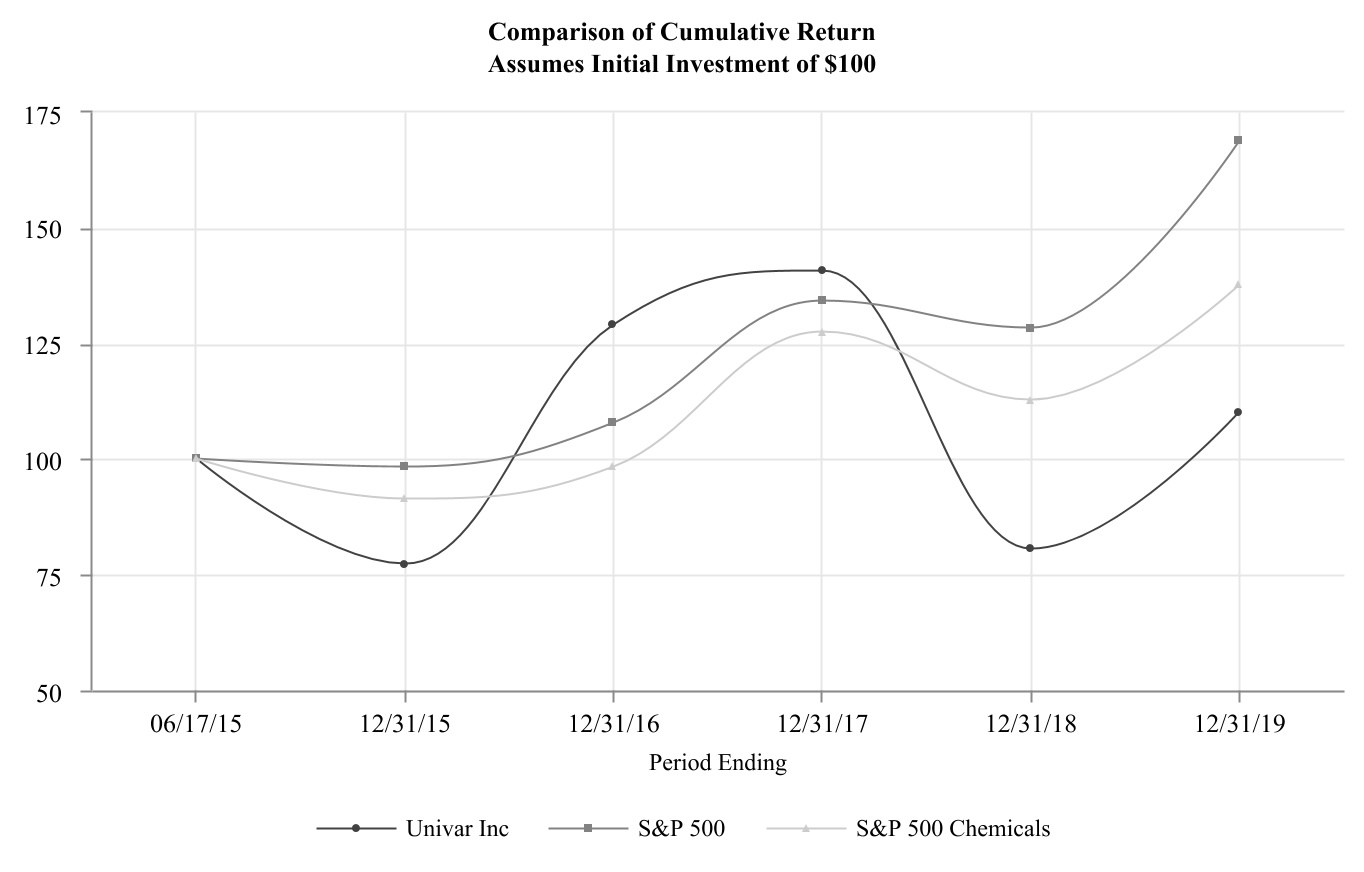

Stock Performance

The following graph shows a comparison of cumulative total shareholder return, calculated on a dividend reinvested basis, for the Company, the S&P 500 and the S&P 500 Chemical Index for the period beginning on June 17, 2015 through year ended December 31, 2018.2019. The graph assumes $100 was invested in each of the Company's common stock, the S&P 500 and S&P 500 Chemical Index as of the market close on June 17, 2015. Note that historic stock price performance is not necessarily indicative of future stock price performance.

Dividend Policy

We have never declared or paid any cash dividend on our common stock. We currently intend to retain any future earnings and we have no current plans to pay dividends in future periods.the near future. In addition, our credit facilities contain restrictionslimitations on our ability to pay dividends.

19

ITEM 6. SELECTED FINANCIAL DATA

This “Selected Financial Data” should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7 of this Annual Report on Form 10-K and our audited consolidated financial statements and related notes included in Item 8 of this Annual Report on Form 10-K.

| Year ended December 31, | |||||||||||||||||||||||||||||||||||||||||||||||||||||

2019 (1) | 2018 | 2017 | 2016 | 2015 | |||||||||||||||||||||||||||||||||||||||||||||||||

| (in millions, except per share data) | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Consolidated Statements of Operations | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net sales | $ | 9,286.9 | $ | 8,632.5 | $ | 8,253.7 | $ | 8,073.7 | $ | 8,981.8 | |||||||||||||||||||||||||||||||||||||||||||

Operating income (2) | 187.3 | 387.4 | 338.0 | 138.4 | 259.3 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Net (loss) income from continuing operations | (105.6) | 172.3 | 119.8 | (68.4) | 16.5 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Net (loss) income | (100.2) | 172.3 | 119.8 | (68.4) | 16.5 | ||||||||||||||||||||||||||||||||||||||||||||||||

| (Loss) income per common share from continuing operations– diluted | (0.64) | 1.21 | 0.85 | (0.50) | 0.14 | ||||||||||||||||||||||||||||||||||||||||||||||||

| (Loss) income per common share – diluted | (0.61) | 1.21 | 0.85 | (0.50) | 0.14 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Consolidated Balance Sheet | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash and cash equivalents | $ | 330.3 | $ | 121.6 | $ | 467.0 | $ | 336.4 | $ | 188.1 | |||||||||||||||||||||||||||||||||||||||||||

| Total assets | 6,494.8 | 5,272.4 | 5,732.7 | 5,389.9 | 5,612.4 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Long-term liabilities | 3,312.6 | 2,746.1 | 3,223.2 | 3,240.5 | 3,502.2 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Stockholders’ equity | 1,732.8 | 1,191.7 | 1,090.1 | 809.9 | 816.7 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Other Financial Data | |||||||||||||||||||||||||||||||||||||||||||||||||||||

Cash provided by operating activities (3) | $ | 363.9 | $ | 289.9 | $ | 282.6 | $ | 450.0 | $ | 356.0 | |||||||||||||||||||||||||||||||||||||||||||

| Cash used by investing activities | (433.1) | (99.0) | (79.1) | (136.0) | (294.4) | ||||||||||||||||||||||||||||||||||||||||||||||||

Cash provided (used) by financing activities (3) | 295.2 | (518.3) | (112.4) | (166.5) | (19.8) | ||||||||||||||||||||||||||||||||||||||||||||||||

| Capital expenditures | 122.5 | 94.6 | 82.7 | 90.1 | 145.0 | ||||||||||||||||||||||||||||||||||||||||||||||||

Adjusted EBITDA (2)(4) | 704.2 | 640.4 | 593.8 | 547.4 | 573.3 | ||||||||||||||||||||||||||||||||||||||||||||||||

Adjusted EBITDA margin (2)(4) | 7.6 | % | 7.4 | % | 7.2 | % | 6.8 | % | 6.4 | % | |||||||||||||||||||||||||||||||||||||||||||

| Fiscal year ended December 31, | |||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | |||||||||||||||

| (in millions, except per share data) | |||||||||||||||||||

| Consolidated Statements of Operations | |||||||||||||||||||

| Net sales | $ | 8,632.5 | $ | 8,253.7 | $ | 8,073.7 | $ | 8,981.8 | $ | 10,373.9 | |||||||||

| Operating income | 387.4 | 338.0 | 138.4 | 259.3 | 315.7 | ||||||||||||||

| Net income (loss) | 172.3 | 119.8 | (68.4 | ) | 16.5 | (20.1 | ) | ||||||||||||

| Income (loss) per common share – diluted | 1.21 | 0.85 | (0.50 | ) | 0.14 | (0.20 | ) | ||||||||||||

| Consolidated Balance Sheet | |||||||||||||||||||

| Cash and cash equivalents | $ | 121.6 | $ | 467.0 | $ | 336.4 | $ | 188.1 | $ | 206.0 | |||||||||

| Total assets | 5,272.4 | 5,732.7 | 5,389.9 | 5,612.4 | 6,067.7 | ||||||||||||||

| Long-term liabilities | 2,746.1 | 3,223.2 | 3,240.5 | 3,502.2 | 4,300.7 | ||||||||||||||

| Stockholders’ equity | 1,191.7 | 1,090.1 | 809.9 | 816.7 | 248.1 | ||||||||||||||

| Other Financial Data | |||||||||||||||||||

| Cash provided by operating activities | $ | 289.9 | $ | 282.6 | $ | 450.0 | $ | 356.0 | $ | 126.3 | |||||||||

| Cash used by investing activities | (99.0 | ) | (79.1 | ) | (136.0 | ) | (294.4 | ) | (148.2 | ) | |||||||||

| Cash (used) provided by financing activities | (518.3 | ) | (112.4 | ) | (166.5 | ) | (19.8 | ) | 84.1 | ||||||||||

| Capital expenditures | 94.6 | 82.7 | 90.1 | 145.0 | 113.9 | ||||||||||||||

Adjusted EBITDA (1) | 640.4 | 593.8 | 547.4 | 573.3 | 624.8 | ||||||||||||||

Adjusted EBITDA margin (1) | 7.4 | % | 7.2 | % | 6.8 | % | 6.4 | % | 6.0 | % | |||||||||

(1)Effective January 1, 2019, the Company adopted new guidance on lease accounting. Prior year amounts have not been adjusted. Refer to “Note 2: Significant accounting policies” for more information. On February 28, 2019, the Company completed the Nexeo acquisition. See “Note 3: Business combinations.”