UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

| |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20162018 |

| |

| | OR |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the transition period from _________ to __________ |

Commission file numbers: 001-35263 and 333-197780

|

|

| VEREIT, Inc. |

| VEREIT Operating Partnership, L.P. |

| (Exact name of registrant as specified in its charter) |

|

| | |

| Maryland (VEREIT, Inc.) | | 45-2482685 |

| Delaware (VEREIT Operating Partnership, L.P.) | | 45-1255683 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | | |

| 2325 E. Camelback Road, Suite 1100, Phoenix, AZ | | 85016 |

| (Address of principal executive offices) | | (Zip Code) |

|

|

| (800) 606-3610 |

| (Registrant’s telephone number, including area code) |

|

| | |

| Securities registered pursuant to Section 12(b) of the Securities Exchange Act of 1934: |

| Title of each class: | Name of each exchange on which registered: |

| Common Stock, $0.01 par value per share (VEREIT, Inc.) | New York Stock Exchange |

| 6.70% Series F Cumulative Redeemable Preferred Stock, $0.01 par value per share (VEREIT, Inc.) | New York Stock Exchange |

| | | |

| Securities registered pursuant to Section 12(g) of the Securities Exchange Act of 1934: |

| None | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act of 1933.

VEREIT, Inc. Yes x No o VEREIT Operating Partnership, L.P. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act of 1934.

VEREIT, Inc. Yes o No x VEREIT Operating Partnership, L.P. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. VEREIT, Inc. Yes x No oVEREIT Operating Partnership, L.P. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web Site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). VEREIT, Inc. Yes x No o VEREIT Operating Partnership, L.P. Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ox

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company or an emerging growth company. See definitionthe definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

| | | | | | | | |

| VEREIT, Inc. | Large accelerated filer | x | | Accelerated filer | o | | Non-accelerated filer | o |

| | | | | | | |

| Smaller reporting company | o | | Emerging growth company | o | | |

|

| | | |

VEREIT, Inc. | Large accelerated filer x

| | Accelerated filer o

|

| Non-accelerated filer o

| (Do not check if a smaller reporting company) | Smaller reporting company o

|

|

| | | |

| VEREIT Operating Partnership, L.P. | Large accelerated filer | o | | Accelerated filer | o | | Non-accelerated filer | x |

| | Non-accelerated filer x

| (Do not check if a smaller reporting company) | | | | | |

| Smaller reporting company | o | | Emerging growth company | o | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards pursuant to Section 13(a) of the Exchange Act. VEREIT, Inc. ¨ VEREIT Operating Partnership, L.P. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

VEREIT, Inc. Yes o No x VEREIT Operating Partnership, L.P. Yes o No x

The aggregate market value of voting and non-voting common stock held by non-affiliates of VEREIT, Inc. as of June 30, 201629, 2018 was approximately $9.2$7.2 billion based on the closing sale price for VEREIT, Inc.’s common stock on that day as reported by the New York Stock Exchange. Such value excludes common stock held by executive officers and directors.

There were 974,109,378967,784,153 shares of common stock of VEREIT, Inc. outstanding as of February 22, 2017.19, 2019.

There is no public trading market for the common units of VEREIT Operating Partnership, L.P. As a result, the aggregate market value of the common units held by non-affiliates of VEREIT Operating Partnership, L.P. cannot be determined.

DOCUMENTS INCORPORATED BY REFERENCE

Certain portions of VEREIT, Inc.’s Definitive Proxy Statement for its 20172019 Annual Meeting of Stockholders (the “Proxy Statement”) to be filed pursuant to Rule 14a-6 of the Securities Exchange Act of 1934, as amended, are incorporated by reference into this Annual Report on Form 10-K. Other than those portions of the Proxy Statement specifically incorporated by reference pursuant to Items 10 through 14 of Part III hereof, no other portions of the Proxy Statement shall be deemed so incorporated.

EXPLANATORY NOTE

This report combines the Annual Reports on Form 10-K for the year ended December 31, 20162018 of VEREIT, Inc., a Maryland corporation, and VEREIT Operating Partnership, L.P., a Delaware limited partnership, of which VEREIT, Inc. is the sole general partner. Unless otherwise indicated or unless the context requires otherwise, all references in this report to “we,” “us,” “our,” “VEREIT,” the “Company” or the “Company”“General Partner” mean VEREIT, Inc., which we sometimes refer to as the “General Partner”, together with its consolidated subsidiaries, including VEREIT Operating Partnership, L.P., and all references to the “Operating Partnership” or “OP” mean VEREIT Operating Partnership, L.P. together with its consolidated subsidiaries.

As the sole general partner of VEREIT Operating Partnership, L.P., VEREIT, Inc. has the full, exclusive and complete responsibility for the Operating Partnership’s day-to-day management and control.

We believe combining the Annual Reports on Form 10-K of VEREIT, Inc. and VEREIT Operating Partnership, L.P. into this single report results in the following benefits:

enhancing investors’ understanding of the Company and the Operating Partnership by enabling investors to view the business as a whole in the same manner as management views and operates the business;

eliminating duplicative disclosure and providing a more streamlined and readable presentation since a substantial portion of the disclosure applies to both the Company and the Operating Partnership; and

creating time and cost efficiencies through the preparation of one combined report instead of two separate reports.

There are a few differences between the Company and the Operating Partnership, which are reflected in the disclosure in this report. We believe it is important to understand the differences between the Company and the Operating Partnership in the context of how we operate as an interrelated consolidated company. VEREIT, Inc. is a real estate investment trust whose only material asset is its ownership of partnership interests of the Operating Partnership. As a result, VEREIT, Inc. does not conduct business itself, other than acting as the sole general partner of the Operating Partnership, issuing public equity or debt from time to time and guaranteeing certain unsecured debt of the Operating Partnership and certain of its subsidiaries. The Operating Partnership holds substantially all of the assets of the Company and holds the ownership interests in the Company’s joint ventures. The Operating Partnership conducts the operations of the business and is structured as a partnership with no publicly traded equity. Except for net proceeds from public equity or debt issuances by VEREIT, Inc., which are generally contributed to the Operating Partnership in exchange for partnership units, the Operating Partnership generates the capital required by the Company’s business through the Operating Partnership’s operations, by the Operating Partnership’s direct or indirect incurrence of indebtedness or through the issuance of partnership units. To help investors understand the significant differences between VEREIT, Inc. and the Operating Partnership, there are separate sections in this report that separately discuss VEREIT, Inc. and the Operating Partnership, including the consolidated financial statements and certain notes to the consolidated financial statements as well as separate disclosures in Item 9A. Controls and Procedures and Exhibit 31 and Exhibit 32 certifications. As general partner with control of the Operating Partnership, VEREIT, Inc. consolidates the Operating Partnership for financial reporting purposes. Therefore, the assets and liabilities of VEREIT, Inc. and VEREIT Operating Partnership, L.P. are the same on their respective consolidated financial statements. The separate discussions of VEREIT, Inc. and VEREIT Operating Partnership, L.P. in this report should be read in conjunction with each other to understand the results of the Company on a consolidated basis and how management operates the Company.

VEREIT, INC. and VEREIT OPERATING PARTNERSHIP, L.P.

For the fiscal year ended December 31, 20162018

Forward-Looking Statements

This Annual Report on Form 10-K includes “forward-looking statements” (within the meaning of the federal securities laws, Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Exchange Act)Act of 1934, as amended (the “Exchange Act”)) that reflect our expectations and projections about our future results, performance, prospects and opportunities. We have attempted to identify these forward-looking statements by the use of words such as “may,” “will,” “seek,” “expects,” “anticipates,” “believes,” “targets,” “intends,” “should,” “estimates,” “could,” “continue,” “assume,” “projects,” “plans” or similar expressions. These forward-looking statements are based on information currently available to us and are subject to a number of known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by these forward-looking statements. These factors include, among other things, those discussed below. We intend for all such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in Section 27A of the Securities Act and Section 21E of the Exchange Act, as applicable by law. We do not undertake publicly to update or revise any forward-looking statements, whether as a result of changes in underlying assumptions or new information, future events or otherwise, except as may be required to satisfy our obligations under federal securities law.

The following are some, but not all, of the assumptions, risks, uncertainties and other factors that could cause our actual results to differ materially from those presented in our forward-looking statements:

We may be unable to renew leases, lease vacant space or re-lease space as leases expire on favorable terms or at all.

We are subject to risks associated with tenant, geographic and industry concentrations with respect to our properties.

Our properties, goodwill and intangible assets and other assets may be subject to impairment charges.

We could be subject to unexpected costs or unexpected liabilities that may arise from potential dispositions.dispositions, including related to limited partnership, tenant-in-common and Delaware statutory trust real estate programs (“1031 real estate programs”) and VEREIT’s management with respect to such programs.

We are subject to competition in the acquisition and disposition of properties and in the leasing of our properties and we may be unable to acquire, dispose of, or lease properties on advantageous terms.

We could be subject to risks associated with bankruptcies or insolvencies of tenants, or from tenant defaults generally.generally or from the unpredictability of the business plans and financial condition of our tenants.

We may be affected byare subject to risks associated with pending government investigations relating to the findings of the previously-announced investigation conducted in 2014 by the audit committee (the “Audit Committee”) of the General Partner’s boardBoard of directorsDirectors (the “Audit Committee Investigation”) and related litigation.litigation, including the expense of such investigations and litigation and any additional potential payments upon resolution.

We have substantial indebtedness, which may affect our ability to pay dividends, and expose us to interest rate fluctuation risk and the risk of default under our debt obligations.

Our overall borrowing and operating flexibility may be adversely affected by the terms and restrictions within the indenture governing the Senior Notes (as defined in Note 11 –Debtsenior unsecured notes (the “Senior Notes”), and the Credit Agreement governing the terms of the Credit Facility (as both terms are defined in Note 11 –DebtItem 1. Business).

Our access to capital and terms of future financings may be affected by adverse changes to our credit rating.

We may be affected by the incurrence of additional secured or unsecured debt.

We may not be able to achieve and maintain profitability.

We may not generate cash flows sufficient to pay our dividends to stockholders or meet our debt service obligations.

We may be affected by risks resulting from losses in excess of insured limits.

We may fail to remain qualified as a real estate investment trust (“REIT”) for U.S. federal income tax purposes.

Compliance with the REIT annual distribution requirements may limit our operating flexibility.

| |

• | We may be unable to fully reestablish the financial network which previously supported Cole Capital® and its Cole REITs (defined below) and/or regain the prior level of transaction and capital raising volume of Cole Capital.

|

Our Cole Capital operations are subject to extensive governmental regulation.

We are subject to conflicts of interest relating to Cole Capital’s investment management business.

We may be unable to retain or hire key personnel.

All forward-looking statements should be read in light of the risks identified in Part I, Item 1A. Risk Factors within thisour Annual Report on Form 10-K.10-K for the year ended December 31, 2018.

We use certain defined terms throughout this Annual Report on Form 10-K that have the following meanings:

When we refer to “annualized rental income,” we mean the rental revenue under our leases on operating properties owned at the respective reporting date on a straight-line basis, which includes the effect of rent escalations and any tenant concessions, such as free rent, and excludes any bad debt allowances and any contingent rent, such as percentage rent. Management uses annualized rental income as a basis for tenant, industry and geographic concentrations and other metrics within the portfolio. Annualized rental income is not indicative of future performance.

When we refer to a “creditworthy tenant,” we mean a tenant that has entered into a lease that we determine is creditworthy and may include tenants with an investment grade or below investment grade credit rating, as determined by major credit rating agencies, or unrated tenants. To the extent we determine that a tenant is a “creditworthy tenant” even though it does not have an investment grade credit rating, we do so based on our management’s determination that a tenant should have the financial wherewithal to honor its obligations under its lease with us. As explained further below, this determination is based on our management’s substantial experience performing credit analysis and is made after evaluating all of a tenant’s due diligence materials that are made available to us, including financial statements and operating data.

When we refer to a “direct financing lease,” we mean a lease that requires specific treatment due to the significance of the lease payments from the inception of the lease compared to the fair value of the property, term of the lease, a transfer of ownership, or a bargain purchase option. These leases are recorded as a net asset on the balance sheet. The amount recorded is calculated as the fair value of the remaining lease payments on the leases and the estimated fair value of any expected residual property value at the end of the lease term.

When we refer to properties that are net leased on a “long term basis,” we mean properties with remaining primary lease terms of generally seven to 10 years or longer on average, depending on property type.

Under a “net lease,” the tenant occupying the leased property (usually as a single tenant) does so in much the same manner as if the tenant were the owner of the property. There are various forms of net leases, most typically classified as triple net or double net. Triple net leases typically require that the tenant pay all expenses associated with the property (e.g., real estate taxes, insurance, maintenance and repairs). Double net leases typically require that the tenant pay all operating expenses associated with the property (e.g., real estate taxes, insurance and maintenance), but excludes some or all major repairs (e.g., roof, structure and parking lot). Accordingly, the owner receives the rent “net” of these expenses, rendering the cash flow associated with the lease predictable for the term of the lease. Under a net lease, the tenant generally agrees to lease the property for a significant term and agrees that it will either have no ability or only limited ability to terminate the lease or abate rent prior to the expiration of the term of the lease as a result of real estate driven events such as casualty, condemnation or failure by the landlord to fulfill its obligations under the lease.

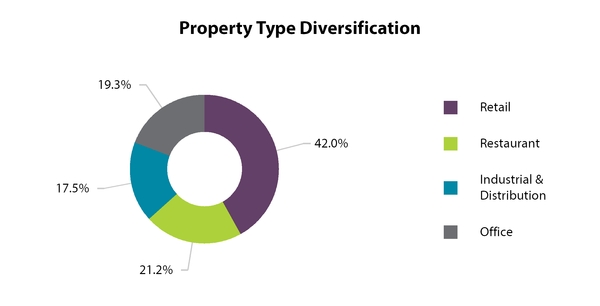

When we refer to “operating properties” we mean properties owned by the Company and beginning in 2017, omitting Excluded Properties. “Excluded Properties” are defined as properties for which (i) the related mortgage loan is in default, and (ii) management decides to transfer the properties to the lender in connection with settling the mortgage note obligation. As of December 31, 2018, our portfolio was comprised of 3,994 retail, restaurant, office and industrial real estate properties with an aggregate of 95.0 million square feet, of which 98.8% was leased, with a weighted-average remaining lease term of 8.9 years. As of December 31, 2018, there were no Excluded Properties. During the year ended December 31, 2018, one vacant industrial property was considered an Excluded Property. The Company entered into a deed-in-lieu of foreclosure agreement and conveyed its interest in this property to the lender in April 2018.

PART I

Item 1. Business.

Overview

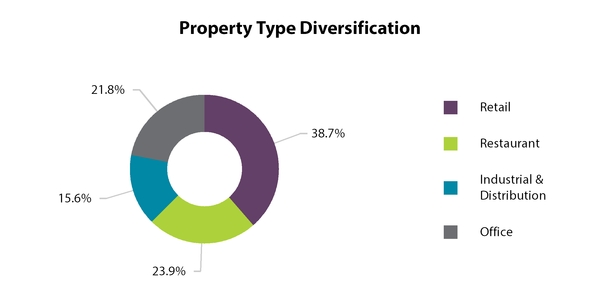

We areVEREIT is a full-service real estate operating company that operates through two business segments, our real estate investment (“REI”) segmentwhich owns and our investment management segment, Cole Capital, as further discussedmanages one of the largest portfolios of single-tenant commercial properties in “Note 3 – Segment Reporting” to our consolidated financial statements. Through our REI segment, we own and actively manage a diversified portfolio of 4,142the U.S. The Company has 3,994 retail, restaurant, office and industrial real estateoperating properties with an aggregate of 93.395.0 million square feet, of which 98.3%98.8% was leased as of December 31, 2016,2018, with a weighted-average remaining lease term of 9.98.9 years. Through our Cole Capital segment, we are responsibleVEREIT’s business model provides equity capital to creditworthy corporations in return for raising capital for and managing the affairs of certain non-listed real estate investment trusts (the “Cole REITs”)long-term leases on a day-to-day basis, identifying and making acquisitions and investments on behalf of the Cole REITs, and recommending to the respective board of directors of each of the Cole REITs an approach for providing investors with liquidity. Cole Capital receives compensation and reimbursement for performing these services.their properties.

Substantially all of the REI segment’sour real estate operations are conducted through the Operating Partnership. VEREIT, Inc. is the sole general partner and holder of 97.6% of the common partnership interests in the Operating Partnership (the “OP Units”) as of December 31, 20162018 with the remaining 2.4% of the OP Units owned by certain non-affiliated investors and certain former directors, officers and employees of the Former Manager (defined below)(as defined in Item 1A. Risk Factors).

Prior to the fourth quarter of 2017, the Company operated through two business segments, the real estate investment segment and the investment management segment, Cole Capital. The Company completed the sale of Cole Capital on February 1, 2018. SubstantiallyThe assets, liabilities and related financial results of substantially all of the Cole Capital segment’s operationssegment are conducted through Cole Capital Advisors, Inc. (“CCA”), an Arizona corporation and a wholly owned subsidiary ofreflected in the Operating Partnership. CCA is treated as a taxable REIT subsidiary (“TRS”) under Section 856 of the Internal Revenue Code of 1986, as amended (the “Internal Revenue Code”). Prior to January 8, 2014, we were externally managed by ARC Properties Advisors, LLC (the “Former Manager”) on a day-to-day basis, with the exception of certain acquisition, accounting and portfolio management activities which were performed by our employees. In August 2013, our board of directors (the “Board of Directors” or the “Board”) determined that it was in our best interests to become self-managed, and we completed our transition to self-management on January 8, 2014. Through strategic mergers and acquisitions discussed in “Note 6 – Mergers with Real Estate Businesses” to our consolidated financial statements the Company has grown significantly since incorporation.as discontinued operations.

VEREIT, Inc. was incorporated in the State of Maryland on December 2, 2010 and has elected to be treated as a REIT for U.S. federal income tax purposes. The Operating Partnership was incorporatedformed in the State of Delaware on January 13, 2011. We operate our business in a manner that permits us to maintain our exemption from registration under the Investment Company Act of 1940, as amended (the “Investment Company Act”).amended. VEREIT, Inc.’s shares of common stock (“Common Stock”) and 6.70% Series F Cumulative Redeemable Preferred Stock (“Series F Preferred Stock”) trade on the New York Stock Exchange (the “NYSE”) under the trading symbols “VER” and “VER PRF,” respectively.

20162018 Developments

Real Estate Acquisitions

During the year ended December 31, 2016,2018, the Company acquired controlling financial interests in eight52 commercial properties, including one land parcel for build-to-suit development, for an aggregate purchase price of $100.2 million.$502.7 million, which includes $2.6 million of external acquisition-related expenses that were capitalized.

Real Estate Dispositions

During the year ended December 31, 2016,2018, the Company disposed of 301 149 properties, including one property conveyed to a lender in a deed-in-lieu of foreclosure transaction, the Excluded Property, and one property owned by an unconsolidated joint venture for an aggregate sales price of $1.20 billion,$560.5 million, of which the Company’s share was $1.14 billion,$521.4 million, resulting in consolidated proceeds of $1.00 billion$502.3 million after closing costs, $55.0 millionrepayment of debt assumptions and $57.0 million of debt repayments by the unconsolidated joint venture.venture’s mortgage loan and closing costs. The Company recorded a gain of $96.9 million related to the dispositions.

Balance Sheet and Liquidity

2016 Bond OfferingLitigation Settlements

During the year ended December 31, 2018, the Company entered into settlement agreements with various plaintiffs in connection with litigation filed as a result of the findings of the Audit Committee Investigation for $217.5 million. The Company also entered into a settlement agreement for $15.7 million subsequent to December 31, 2018, which was accrued as of December 31, 2018 and $300.0 million 2016 Term Loanincluded in litigation, merger and other non-routine costs, net of insurance recoveries in the consolidated statements of operations for the year ended December 31, 2018. See Note 10 – Commitments and Contingencies for additional information.

Credit Agreement

On June 2, 2016,May 23, 2018, the Operating Partnership closed its senior note offeringGeneral Partner, as guarantor, and the OP, as borrower, entered into a credit agreement with Wells Fargo Bank, National Association, as administrative agent and the other lenders party thereto (the “2016 Bond Offering”“Credit Agreement”),. The Credit Agreement allows for maximum borrowings of $2.9 billion, consisting of (i) $0.4a $2.0 billion aggregate principal amount of 4.125% Senior Notes due June 1, 2021unsecured revolving credit facility (the “Revolving Credit Facility”) and (ii) $0.6 billion aggregate principal amount of 4.875% Senior Notes due June 1, 2026 and entereda $900.0 million unsecured term loan facility (the “Credit Facility Term Loan,” together with the Revolving Credit Facility, the “Credit Facility”). In connection with entering into the $300.0 million 2016 Term Loan, as defined in Note 11 –Debt. On July 5, 2016,Credit Agreement, the Company redeemedOP repaid all of the $1.3 billion aggregateoutstanding obligations under the Amended and Restated Credit Agreement dated as of June 30, 2014 (as amended, the “2014 Credit Agreement”) and the 2014 Credit Agreement was terminated.

2018 Convertible Notes

The Company’s convertible senior notes due August 1, 2018 (the “2018 Convertible Notes”) matured and the principal amountoutstanding balance of our outstanding 2.000% Senior Notes due February 2017,$597.5 million, plus accrued and unpaid interest thereon, andwas repaid with proceeds from the required make-whole premium.Revolving Credit Facility.

Common Stock Offering2025 Senior Notes

On August 10, 2016, VEREIT, Inc. issued 69.0October 16, 2018, the Company closed a senior note offering, consisting of $550.0 million sharesaggregate principal amount of common stock in a public offering forthe OP’s 4.625% Senior Notes due 2025 (the “2025 Senior Notes”). The OP used the net proceeds after underwriting discounts andfrom the offering costs, of $702.5 million, which were usedthe notes to repay the entire $300.0 million 2016 Term Loan and in part to repay amountsborrowings under theits Revolving Credit Facility.

Common Stock Continuous Offering ProgramDebt Activity

On September 19, 2016, the Company registered a continuous equity offering program (the “Program”) pursuant to which the Company can offer and sell, from time to time through September 19, 2019 in “at-the-market” offerings or certain other transactions, shares of common stock with an aggregate gross sales price of up to $750.0 million, through its sales agents. There were no shares of common stock issued under the Program duringDuring the year ended December 31, 2016.

Debt Repayments

As a result2018, the Company’s total debt increased by $14.5 million, from $6.07 billion to $6.09 billion, partially due to the issuance of the reduction in mortgage debt due to property dispositions2025 Senior Notes, and other measures taken by management,net borrowings on the Company decreased total debt by $1.7 billion, from $8.1 billion to $6.4 billion, comprised of unsecured bonds of $0.3 billion, unsecured2014 Credit Agreement and Credit Facility of $1.0 billion,$218.0 million. These borrowings were partially offset by the repayment of $597.5 million of the 2018 Convertible Notes and a reduction of $153.9 million in secured debtdebt.

Share Repurchase Programs

On May 12, 2017, the Company’s Board of $0.4 billion.Directors authorized the repurchase of up to $200.0 million of the Company’s outstanding Common Stock over the subsequent 12 months, as market conditions warranted (the “2017 Share Repurchase Program”). On May 3, 2018, the Company’s Board of Directors terminated the 2017 Share Repurchase Program and authorized a new program (the “2018 Share Repurchase Program,” and collectively with the 2017 Share Repurchase Program, the “Share Repurchase Programs”) that permits the Company to repurchase up to $200.0 million of its outstanding Common Stock through May 3, 2019, as market conditions warrant. During the year ended December 31, 2018, the Company repurchased approximately 6.4 million shares of Common Stock in multiple open market transactions, at a weighted average share price of $6.94, for an aggregate purchase price of $44.6 million, as part of the 2017 Share Repurchase Program and 0.8 million shares of Common Stock in multiple open market transactions, at a weighted average share price of $6.95 for an aggregate purchase price of $5.6 million as part of the 2018 Share Repurchase Program.

Cole Capital Sale

On February 1, 2018, we sold all of the issued and outstanding shares of common stock of Cole Capital Advisors, Inc. (“CCA”), our subsidiary that sponsored and managed non-listed real estate investment trusts, and certain of CCA’s subsidiaries, to CCA Acquisition, LLC (the “Cole Purchaser”), an affiliate of CIM Group, LLC for total consideration of approximately $120.0 million in cash.

On February 1, 2018, we entered into a services agreement (the “Services Agreement”) with Cole Capital, pursuant to which we will continue to provide certain services to Cole Capital and its subsidiaries and to Cole Credit Property Trust IV, Inc. (“CCPT IV”), CIM Income NAV, Inc. (formerly known as Cole Real Estate Income Strategy (Daily NAV), Inc.) (“INAV”), Cole Office & Industrial REIT (CCIT II), Inc. (“CCIT II”), Cole Office & Industrial REIT (CCIT III), Inc. (“CCIT III”), and Cole Credit Property Trust V, Inc. (“CCPT V” and collectively with CCPT IV, INAV, CCIT II and CCIT III, the “Cole REITs”) including operational real estate support. Under the terms of the Services Agreement, we are entitled to receive reimbursement for certain of the services provided and fees based on the future revenues of Cole Capital above a specified dollar threshold (the “Net Revenue Payments”), up to an aggregate of $80.0 million in Net Revenue Payments. There were no Net Revenue Payments received or earned for 2018.

Primary Investment Focus

We own and actively manage a diversified portfolio of single-tenant retail, restaurant, office and industrial real estate assets subject to long-term net leases with creditworthy tenants. Our focus is on single-tenant, net-leased properties that are strategically located and essential to the business operations of the tenant, as well as retail properties that offer necessity and value-oriented products or services. We actively manage the portfolio by considering several metrics including property type, tenant concentration, geography, credit and key economic factors for appropriate balance and diversity. We believe that actively managing our portfolio allows us to attain the best operating results for each asset and the overall portfolio through strategic planning, implementation of these plans and responding proactively to changes and challenges in the marketplace.

Additionally, we employ a shared services model for Cole Capital’s portfolios by providing transactional and operational real estate functions. The shared services model allows our strong and experienced real estate team to be active in the markets at all times and manage complimentary portfolios.

Investment Policies

When evaluating prospective investments in or dispositions of real property, our management considers relevant real estate and financial factors, including the location of the property, the leases and other agreements affecting the property and business operations of the tenant, the creditworthiness of major tenants, its income-producing capacity, its physical condition, its prospects for appreciation, its prospects for liquidity, tax considerations and other factors. In this regard, our management will have substantial discretion with respect to the selection of specific investments, subject in certain instances to the approval of the Board of Directors.

As part of our overall portfolio strategy, we seek to lease space and/or acquire properties leased to creditworthy tenants that meet our underwriting and operating guidelines. Prior to entering into any transaction, our corporate credit analysis and underwriting professionals conduct a review of a tenant’s credit quality. In addition, we consistently monitor the credit quality of our portfolio by actively reviewing the creditworthiness of certain tenants, focusing primarily on those tenants representing the greatest concentration of our portfolio. This review primarily includes an analysis of the tenant’s financial statements either quarterly, or as frequently as the lease permits. We also consider tenant credit quality when assessing our portfolio for strategic dispositions. When we assess tenant credit quality, we, among other factors that we may deem relevant: (i) review relevant financial information,

including financial ratios, net worth, revenue, cash flows, leverage and liquidity; (ii) evaluate the depth and experience of the tenant’s management team; and (iii) assess the strength/growth of the tenant’s industry. On an on-going basis, we evaluate the need for an allowance for doubtful accounts arising from estimated losses that could result from the tenant’s inability to make required current rent payments and an allowance against accrued rental incomerevenue for future potential losses that we deem to be unrecoverable over the term of the lease. The factors considered in determining the credit risk of our tenants include, but are not limited to: payment history; credit status and change in status (credit ratings for public companies are used as a primary metric); change in tenant space needs (i.e., expansion/downsize); tenant financial performance; economic conditions in a specific geographic region; and industry specific credit considerations. We are of the opinion that the credit risk of our portfolio is reduced by the high quality of our existing tenant base, reviews of prospective tenants’ risk profiles prior to lease execution and consistent monitoring of our portfolio to identify potential problem tenants.

tenants and mitigation options.

Real Estate Investments

As of December 31, 2016,2018, the Company owned 4,1423,994 operating properties comprising 93.395.0 million square feet of retail and commercial space located in 49 states and Puerto Rico, and Canada, which includes properties owned through consolidated joint ventures. The rentable space at these properties was 98.3%98.8% leased with a weighted-average remaining lease term of 9.98.9 years. There were no tenants exceeding 10% of our consolidated annualized rental income as of December 31, 20162018, 2017 or 2015.2016. As of December 31, 2014, leases with Red Lobster® restaurants2018, 2017 and 2016, properties located in Texas represented 11.6%12.5%, 12.8% and 13.5%, respectively, of our consolidated annualized rental income. As of December 31, 2016, 20152018, tenants in the casual dining restaurant and 2014, properties locatedmanufacturing industries accounted for 12.8% and 10.1%, respectively, of our consolidated annualized rental income. As of December 31, 2017, tenants in Texas represented 13.5%, 13.1%the casual dining restaurant and 12.7%manufacturing industries accounted for 13.8% and 10.1%, respectively, of our consolidated annualized rental income. As of December 31, 2016, tenants in the casual dining restaurant and manufacturing industries accounted for 15.6% and 10.1%, respectively, of our consolidated annualized rental income. As of December 31, 2015, tenants in the casual dining restaurant and manufacturing industries accounted for 16.6% and 10.1%, respectively, of our consolidated annualized rental income. As of December 31, 2014, tenants in the casual dining restaurant industry accounted for 18.4% of our consolidated annualized rental income.

Cole Capital®

Cole Capital sponsors and manages direct investment real estate programs, which primarily include five publicly registered, non-listed REITs, as discussed in “Note 2 – Summary of Significant Accounting Policies” to our consolidated financial statements. Cole Capital is responsible for raising capital for and managing the day-to-day affairs of the Cole REITs, identifying and making acquisitions and investments on behalf of the Cole REITs, and recommending to each of the Cole REIT’s respective board of directors an approach for providing investors with liquidity. Cole Capital serves as the dealer manager and distributes shares of common stock for certain Cole REITs and advises them regarding offerings, manages relationships with participating broker-dealers and financial advisors, and provides assistance in connection with compliance matters relating to the offerings. Cole Capital receives compensation and reimbursement for services relating to the Cole REITs’ offerings and the investment, management, financing and disposition of their respective assets, as applicable. Cole Capital also develops new REIT offerings, including obtaining regulatory approvals from the U.S. Securities and Exchange Commission (the “SEC”), the Financial Industry Regulatory Authority, Inc. (“FINRA”) and various blue sky jurisdictions for such offerings.

Financing Policies

We rely on leverage to allow us to invest in a greater number of assets and enhance our asset returns. We expect our leverage metrics to improve over time.

We intend to finance future acquisitions with the most advantageous source of capital available to us at the time of the transaction, which may include a combination of public and private offerings of our equity and debt securities, secured and unsecured corporate-level debt, property-level debt and mortgage financing and other public, private or bank debt. In addition, we may acquire properties in exchange for the issuance of common stockCommon Stock or OP Units and in many cases we may acquire properties subject to existing mortgage indebtedness.

We also may obtain secured or unsecured debt to acquire properties, and we expect that our financing sources will include the public debt market, banks and institutional investment firms, including asset managers and life insurance companies. Although we intend to maintain a conservative capital structure, our charter does not contain a specific limitation on the amount of debt we may incur and the Board of Directors may implement or change target debt levels at any time without the approval of our stockholders.

Competition

In our REI segment, weWe are subject to competition in the acquisition and disposition of properties and in the leasing of our properties. We compete with a number of developers, owners and operators of retail, restaurant, office and industrial real estate, many of which own properties similar to ours in the same markets in which our properties are located. We also may face new competitors and, due to our focus on single-tenant properties located throughout the United States, and because many of our competitors are locally or regionally focused, we do not expect to encounter the same competitors in each region of the United States. Many of our competitors have greater financial and other resources than us and may have other advantages over us. Our competitors may be willing to accept lower returns on their investments and may succeed in buying the properties that we have targeted for acquisition. We may also incur costs in connection with unsuccessful acquisitions that we will not be able to recover. Foreign investors may view the U.S. real estate market as being more stable than other international markets and may increase investments in high-quality single-tenant properties, especially in gateway cities.

In our Cole Capital segment, We may also incur costs in connection with unsuccessful acquisitions that we also face competition in raising funds for the Cole REITs from other entities with similar investment objectives such as other non-listed REITs, publicly traded REITs and private funds, including hedge funds.will not be able to recover.

Regulations

Our investments are subject to various federal, state, local and foreign laws, ordinances and regulations, including, among other things, health, safety and zoning regulations, land use controls, environmental controls relating to air and water quality, noise pollution and indirect environmental impacts such as increased motor vehicle activity. We believe that we have all material permits and approvals necessary under current law to operate our investments.

Our properties are also subject to laws such as the Americans with Disabilities Act of 1990 (“ADA”), which require that all public accommodations must meet federal requirements related to access and use by disabled persons. Some of our properties may currently not be in compliance with the ADA. If one or more of the properties in our portfolio is not in compliance with the ADA or any other regulatory requirements, we may be required to incur additional costs to bring the property into compliance.

Environmental Matters

Under various federal, state and local environmental laws, a current owner of real estate may be required to investigate and clean up contaminated property. Under these laws, courts and government agencies have the authority to impose cleanup responsibility and liability even if the owner did not know of and was not responsible for the contamination. For example, liability can be imposed upon us based on the activities of our tenants or a prior owner. In addition to the cost of the cleanup, environmental contamination on a property may adversely affect the value of the property and our ability to sell, rent or finance the property, and may adversely impact our investment in that property.

Prior to acquisition of a property, we will obtain Phase I environmental reports, or will rely on recent Phase I environmental reports. These reports will be prepared in accordance with an appropriate level of due diligence based on our standards and generally include a physical site inspection, a review of relevant federal, state and local environmental and health agency database records, one or more interviews with appropriate site-related personnel, review of the property’s chain of title and review of historic aerial photographs and other information on past uses of the property and nearby or adjoining properties. We may also obtain a Phase II investigation which may include limited subsurface investigations and tests for substances of concern where the results of the Phase I environmental reports or other information indicates possible contamination or where our consultants recommend such procedures.

Employees

As of December 31, 2016,2018, we had approximately 350180 employees.

Available Information

We electronically file Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports, and proxy statements, with the SEC.U.S. Securities and Exchange Commission (the “SEC”). You may read and copyaccess any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, D.C. 20549, or you may access them through the EDGAR database at the SEC’s website at http://www.sec.gov. In addition, copies of our filings with the SEC may be obtained from theour website maintained for us at www.ir.vereit.com. We are providing our website address solely for the information of investors. We do not intend for the information contained on our website to be incorporated into this Annual Report on Form 10-K or other filings with the SEC.

Supplemental Federal Income Tax Considerations

This summary is for general information purposes only and is not tax advice. This discussion does not address all aspects of taxation that may be relevant to particular holders of our securities in light of their personal investment or tax circumstances.

Recent Legislation

Tax Cuts and Jobs Act

On December 22, 2017, H.R. 1, informally titled the Tax Cuts and Jobs Act (the “TCJA”), was enacted. The TCJA made major changes to the Internal Revenue Code of 1986, as amended (the “Internal Revenue Code”), including a number of provisions of the Internal Revenue Code that affect the taxation of REITs and their stockholders. The long-term effect of the significant changes made by the TCJA remains uncertain, and additional administrative guidance will be required in order to fully evaluate the effect of many provisions. The effect of any technical corrections with respect to the TCJA could have an adverse effect on us or our stockholders or holders of our debt securities.

Item 1A. Risk Factors.

Investors should carefully consider the following factors, together with all the other information included in this Annual Report on Form 10-K, in evaluating the Company and our business. If any of the following risks actually occur, our business, financial condition and results of operations could be materially and adversely affected, the trading price of the General Partner'sVEREIT's securities could decline and its stockholders and/or the Operating Partnership's unitholders may lose all or part of their investment. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may impair our business operations. This “Risk Factors” section contains references to our “capital stock” and to our “stockholders” and “unitholders.” Unless expressly stated otherwise, references to our “capital stock” represent the General Partner’s common stockVEREIT’s Common Stock and any class or series of its preferred stock, references to our “stockholders” represent holders of the General Partner’s common stockVEREIT’s Common Stock and any class or series of its preferred stock, and references to our “unitholders” represent holders of the OP unitsUnits and any class of series of the Operating Partnership’s preferred units.

Risks Related to Our Business

We are primarily dependent on single-tenant leases for our revenue and, accordingly, if we are unable to renew leases, lease vacant space, including vacant space resulting from tenant defaults, or re-lease space as leases expire, on favorable terms or at all, our financial condition could be adversely affected.

We focus our investment activities on ownership of freestanding, single-tenant commercial properties that are net leased to a single tenant. Therefore, the financial failure of, or other default by, a significant tenant or multiple tenants could cause a material reduction in our revenues and operating cash flows. In addition, this risk is increased where we lease multiple properties to the extent that we enter intoa single tenant under a master lease withlease. In such an instance, a default specific to a particular tenant, theproperty could result in a termination of such master lease could affect each property subject to the entire master lease, resulting in the loss of revenue from all such properties.properties under the master lease.

We cannot assure you that our leases will be renewed or that we will be able to lease or re-lease the properties on favorable terms, or at all, or that lease terminations will not cause us to sell the properties at a loss. Any of our properties that become vacant could be difficult to sell or re-lease at similar or sell.favorable rental rates or at all. We have and may continue to experience vacancies either by the continued default of a tenant under its lease or the expiration of one of our leases. We typically must incur all of the costs of ownership for a property that is vacant. Upon or pending the expiration of leases at our properties, we may be required to make rent or other concessions to tenants, or accommodate requests for renovations,lower rents, remodeling and other improvements, in order to retain and attract tenants. Certain of our properties may be specifically suited to the particular needs of a tenant (e.g., a retail bank branch or distribution warehouse) and major renovations and expenditures may be required in order for us to re-lease the space for other uses. If the vacancies continue for a long period of time, we may suffer reduced revenues, resulting in less cash available for distribution to our stockholders and unitholders. If we are unable to renew leases, lease vacant space, including vacant space resulting from tenant defaults, or re-lease space as leases expire, on favorable terms or at all, our financial condition could be adversely affected.

We are subject to tenant, geographic and industry concentrations that make us more susceptible to adverse events with respect to certain tenants, geographic areas or industries.

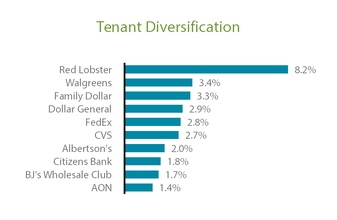

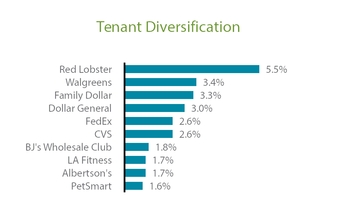

As of December 31, 2016,2018, we had derived approximately:

$96.763.7 million, or 8.2%5.5%, of our annualized rental income from Red Lobster®, a wholly owned subsidiary of Golden Gate Capital;

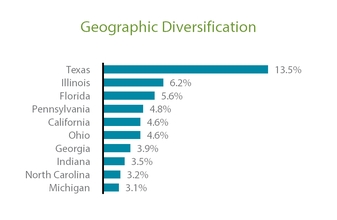

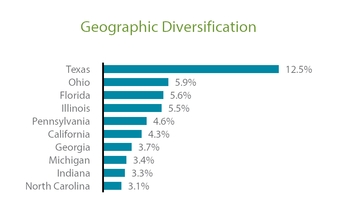

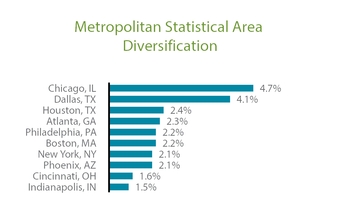

$297.7339.2 million, or 25.3%29.5%, of our annualized rental income from properties located in the following threefour states: Texas (13.5%(12.5%), Illinois (6.2%Ohio (5.9%), Florida (5.6%), and Florida (5.6%Illinois (5.5%); and

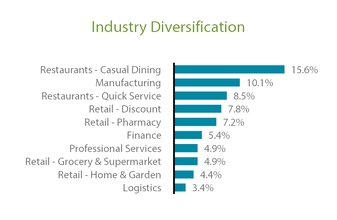

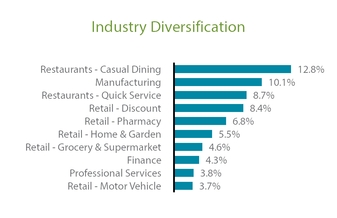

$642.0600.9 million, or 54.6%52.3%, of our annualized rental income from tenants in the following six industries: the casual dining restaurant industry (15.6%(12.8%), the manufacturing industry (10.1%), the quick service restaurant industry (8.5%(8.7%), the discount retail industry (7.8%(8.4%), the pharmacy retail industry (7.2%(6.8%) and the financehome and garden retail industry (5.4%(5.5%).

As we continue to acquire properties, our portfolio may become more concentrated by tenant, geographic area or industry. Any adverse change in the financial condition of a tenant with whom we may have a significant credit concentration now or in the future, or any downturn of the economy in any state or industry in which we may have a significant credit concentration now or in the future, could result in a material reduction of our cash flows or material losses to us. These concentrations may also strengthen tenant bargaining power and make us more susceptible to adverse regulatory changes, natural disasters or other unexpected events that may impact a particular tenant, geographic location or industry which could negatively affect our operations or result in a material reduction of our cash flows or material losses to us.

Our net leases may require us to pay property-related expenses that are not the obligations of our tenants.

Under the terms of the majority of our net leases, in addition to satisfying their rent obligations, our tenants are responsible for the payment or reimbursement of property expenses such as real estate taxes, insurance and ordinary maintenance and repairs. However, under the provisions of certain existing leases and leases that we may enter into in the future with our tenants, we may be required to pay some or all of the expenses of the property, such as the costs of environmental liabilities, roof and structural repairs, real estate taxes, insurance, certain non-structural repairs and maintenance. If our properties incur significant expenses that must be paid by us under the terms of our leases, our business, financial condition and results of operations may be adversely affected and the amount of cash available to meet expenses and to make distributions to our stockholders and unitholders may be reduced.

Our properties may be subject to impairment charges.

We routinely evaluate our real estate investments for impairment indicators. The judgment regarding the existence of impairment indicators is based on factors such as market conditions and tenant performance. For example, the early termination of, or default under, a lease by a tenant may lead to an impairment charge. Since our investment focus is on properties net leased

to a single tenant, the financial failure of, or other default by, a single tenant under its leaselease(s) may result in a significant impairment loss. If we determine that an impairment has occurred, we would be required to make a downward adjustment to the net carrying value of the property, which could have a material adverse effect on our results of operations in the period in which the impairment charge is recorded. Management has recorded impairment charges related to certain properties in the year ended December 31, 2016,2018, and may record future impairments based on actual results and changes in circumstances. Negative developments in the real estate market may cause management to reevaluate the business and macro-economic assumptions used in its impairment

analysis. Changes in management’s assumptions based on actual results may have a material impact on the Company’s financial statements. See “Note 10 Note 6 – Fair Value Measures”Measures to our consolidated financial statements for a discussion of real estate impairment charges.

Our ownership of certain properties and other facilities are subject to ground leases or other similar agreements which limit our uses of these properties and may restrict our ability to sell or otherwise transfer such properties.

As of December 31, 2016,2018, we held interests in properties and other facilities through leasehold interests in the land on which the buildings are located and we may acquire additional properties in the future that are subject to ground leases or other similar agreements. As of December 31, 2016,2018, the costs associated with these ground leases represented 2.0% of annualized rental revenue. ManyThe terms of the ground leases may be different than the related operating lease for the property and many of our ground leases and other similar agreements limit our uses of these properties and may restrict our ability to sell or otherwise transfer such properties without the ground landlord’s consent, all of which may impair their value.

Real estate investments are relatively illiquid and therefore we may not be able to dispose of properties when appropriate or on favorable terms.

Real estate investments are, in general, relatively illiquid and may become even more illiquid during periods of economic downturn. As a result, we may not be able to sell our properties quickly or on favorable terms in response to changes in the economy or other conditions when it otherwise may be prudent to do so. In addition, certain significant expenditures generally do not change in response to economic or other conditions, including debt service obligations, real estate taxes, and operating and maintenance costs. This combination of variable revenue and relatively fixed expenditures may result, under certain market conditions, in reduced earnings. Further, as a result of the 100% prohibited transactions tax applicable to REITs, we intend to hold our properties for investment, rather than primarily for sale in the ordinary course of business, which may cause us to forgo or defer sales of properties that otherwise would be favorable. Therefore, we may be unable to adjust our portfolio promptly in response to economic, market or other conditions, which could adversely affect our business, financial condition, liquidity and results of operations.

Our investments inA substantial portion of our properties where the underlying tenant hasare leased to tenants with a below investment grade credit rating, as determined by major credit rating agencies, or has an unrated tenantare leased to tenants that are not rated, and may have a greater risk of default.

As of December 31, 2016,2018, approximately 58.8%58.1% of our tenants were not rated or did not have an investment grade credit rating from a major ratings agency or were not affiliates of companies having an investment grade credit rating. Our investments in properties leased to such tenants may have a greater risk of default and bankruptcy than investments in properties leased exclusively to investment grade tenants. When we invest in properties where the tenant does not have a publicly available credit rating, we will use certain credit assessmentcredit-assessment tools as well as rely on our own estimatesunderwriting and analysis of the tenant’s credit rating which includes, among other things, reviewing the tenant’s financial information (e.g., financial ratios, net worth, revenue, cash flows, leverage and liquidity, if applicable). If our ratings estimates are inaccurate, the default or bankruptcy risk for the subject tenant may be greater than anticipated. If our lender or a credit rating agency disagrees with our ratings estimates, we may not be able to obtain our desired level of leverage or our financing costs may exceed those that we projected. This outcome could have an adverse impact on our returns on that asset and hence our operating results.

We may be unable to sell a property if or when we decide to do so, including as a result of uncertain market conditions, which could adversely impact our ability to make cash distributions to our stockholders and unitholders.

We expect to hold the various real properties in which we invest until such time as we decide that a sale or other disposition is appropriate given our investment business objectives.objectives and REIT limitations. We generally intend to hold properties for an extended time, but our management or Board of Directors may exercise their discretion as to whether and when to sell a property to achieve investment or portfolio objectives. Our ability to dispose of properties on advantageous terms or at all depends on certain factors beyond our control, including competition from other sellers, and the availability of attractive financing for potential buyers of our properties.properties and the quality of the underlying tenant. In addition, if our competitors sell assets similar to assets we intend to divest and/or at valuations below our valuations for comparable assets, we may be unable to divest our assets at all or at favorable pricing or terms. We cannot predict the various market conditions affecting real estate investments which will exist at any particular time in the future. Due to the uncertainty of market conditions which may affect the disposition of our properties, we cannot assure you that we will be able to sell such properties at a profit or at all in the future. Accordingly, the extent to which our stockholders and unitholders will receive cash distributions and realize potential appreciation on our real estate investments will depend upon

fluctuating market conditions. Furthermore, we may be required to seek modifications of an underlying lease or expend funds to correct defects or to make improvements before a property can be sold.

Dividends paid from sources other than our cash flow from operations could affect our profitability, restrict our ability to generate sufficient cash flow from operations, and dilute stockholders’ and unitholders’ interests in us.

We may not generate sufficient cash flow from operations to pay dividends and we may in the future pay dividends from sources other than from our cash flow from operations, such as from the proceeds of property or other asset dispositions, borrowings (including on our existing line of credit), cash and cash equivalents balances, and/or the saleofferings of assets debt and/or the proceeds from offerings ofequity securities. We have not established any limit on the amount of borrowings and/or the sale of property or other assets or the proceeds from an

offering of debt or equity securities that may be used to fund dividends, except that, in accordance with our organizational documents and Maryland law, we may not make dividend distributions that would: (1) cause us to be unable to pay our debts as they become due in the usual course of business; (2) cause our total assets to be less than the sum of our total liabilities plus senior liquidation preferences; or (3) jeopardize our ability to qualify as a REIT.

Funding dividends from borrowings could restrict the amount we can borrow for investments, which may affect our profitability. Funding dividends with the sale of property or other assets or the proceeds of offerings of debt or equity securities may affect our ability to generate cash flows. In addition, funding dividends from the sale of additional securities could dilute your interest in us if we sell shares of our common stock or securities that are convertible or exercisable into shares of our common stock to third party investors. As a result, the return you realize on your investment may be reduced. Payment of dividends from these sources could affect our profitability, restrict our ability to generate sufficient cash flow from operations, and dilute stockholders’ and unitholders’ interests in us, any or all of which may adversely affect your overall return. In addition, funding dividends from the sale of additional debt or equity securities could dilute your interest in us if we sell shares of our Common Stock or securities that are convertible or exercisable into shares of our Common Stock to third party investors. As a result, the return you realize on your investment may be reduced.

We could face potential adverse effects from the bankruptcies or insolvencies of tenants or from tenant defaults generally.

The bankruptcy or insolvency of our tenants may adversely affect the income produced by our properties. Under bankruptcy law, a tenant cannot be evicted solely because of its bankruptcy and has the option to assume or reject any unexpired lease. If the tenant rejects the lease, any resulting claim we have for breach of the lease (excluding collateral securing the claim) will be treated as a general unsecured claim. Our claim against the bankrupt tenant for unpaid and future rent will be subject to a statutory cap that might be substantially less than the remaining rent actually owed under the lease, and it is unlikely that a bankrupt tenant that rejects its lease would pay in full amounts it owes us under the lease. Even if a lease is assumed and brought current, we still run the risk that a tenant could condition lease assumption on a restructuring of certain terms, including rent, that would have an adverse impact on us. Any shortfall resulting from the bankruptcy of one or more of our tenants could adversely affect our cash flows and results of operations and could cause us to reduce the amount of distributions to our stockholders and unitholders.

In addition, the financial failure of, or other default by, one or more of the tenants to whom we have exposure could have an adverse effect on the results of our operations. While we evaluate the creditworthiness of our tenants by reviewing available financial and other pertinent information, there can be no assurance that any tenant will be able to make timely rental payments or avoid defaulting under its lease. If any of our tenants’ businesses experience significant adverse changes, they may fail to make rental payments when due, close a number of stores, exercise early termination rights (to the extent such rights are available to the tenant) or declare bankruptcy. A default by a significant tenant or multiple tenants could cause a material reduction in our revenues and operating cash flows. In addition, if a tenant defaults, we may incur substantial costs in protecting our investment.

If a sale-leaseback transaction is re-characterized in a tenant’s bankruptcy proceeding, our financial condition could be adversely affected.

We have entered and may continue to enter into sale-leaseback transactions. In a sale-leaseback transaction, we purchase a property and then lease it back to the third party from whom we purchased it. In the event of the bankruptcy of a tenant, a transaction structured as a sale-leaseback might possibly be re-characterized as either a financing or a joint venture, either of which outcomes could adversely affect our financial condition, cash flows and the amount available for distributionsdistribution to our stockholders and unitholders.

If thea sale-leaseback wereis re-characterized as a financing, we would not be considered the owner of the property and, as a result, would have the status of a creditor in relation to the tenant. In that event, we would no longer have the right to sell or encumber our ownership interest in the property. Instead, we would have a claim against the tenant for the amounts owed under the lease, with the claim arguably secured by the property. The tenant/debtor might have the ability to propose a plan restructuring the term, interest rate and amortization schedule of its outstanding balance. If confirmed by the bankruptcy court, we could be bound by the new terms and prevented from foreclosing our lien on the property. If the sale-leaseback wereis re-characterized as a joint venture, our lesseetenant and we could be treated as co-venturers with regard to the property. As a result, we could be held liable, under some circumstances, for debts incurred by the lesseetenant relating to the property.

We have a history of operating losses and cannot assure you that we will achieve or maintain profitability.

Since our inception in 2010, we have experienced net losses (calculated in accordance with generally accepted accounting principles in the United States (“U.S. GAAP) each fiscal yearGAAP”) and as of December 31, 2016,2018, had an accumulated deficit of $4.2$5.47 billion. The extent of our future operating losses and the timing of when we will achieve profitability are uncertain, and together depend on the demand for, and value of, our portfolio of properties. We may never achieve or sustain profitability.

We may be unable to enter into and consummate property acquisitions on advantageous terms or our property acquisitions may not perform as we expect due to competitive conditions and other factors.

We may acquire properties in the future. The acquisition of properties entails various risks, including the risks that our investments may not perform as we expect and that our cost estimates for bringing an acquired property up to market standards may prove inaccurate. Further, we expect to finance any future acquisitions through a combination of borrowings (including under our unsecured credit facility (the “Credit Facility”)Revolving Credit Facility), cash and cash equivalent balances, proceeds from equity and/or debt offerings by the General Partner,VEREIT, the Operating Partnership or their subsidiaries, fundscash flow from operations and proceeds from property contributions andor other asset dispositions which, if unavailable, could adversely affect our cash flows.

In addition, our ability to acquire properties in the future on satisfactory terms and successfully integrate and operate such properties is subject to the following significant risks:

we may be unable to acquire desired properties or the purchase price of a desired property may increase significantly because of competition from other real estate investors, including other real estate operating companies, REITs and investment funds, including the Cole REITs;funds;

we may acquire properties that are not accretive to our resultsearnings upon acquisition;

we may be unable to obtain the necessary debt or equity financing to consummate an acquisition or, if obtainable, financing may not be on satisfactory terms;

we may need to spend more than budgeted amounts to make necessary improvements or renovations to acquired properties;

agreements for the acquisition of properties are typically subject to customary conditions to closing, including satisfactory completion of due diligence investigations, and we may spend significant time and money on potential acquisitions that we do not consummate;

we may be unable to quickly and efficiently integrate new acquisitions, particularly acquisitions of portfolios of properties, into our existing operations; and

we may acquire properties without any recourse, or with only limited recourse, for liabilities, whether known or unknown, such as cleanup of environmental contamination, remediation of latent defects, claims by tenants, vendors or other persons against the former owners of the properties and claims for indemnification by general partners, directors, officers and others indemnified by the former owners of the properties.

Any of the above risks could adversely affect our business, financial condition, liquidity and results of operations.

We have assumed, and may in the future assume, liabilities in connection with our property acquisitions, including unknown liabilities.

We have assumed, and may in the future assume, existing liabilities in connection with property acquisitions, some of which may have been unknown or unquantifiable at the time of the transaction or the magnitude of which may have increased since the time of the transaction. UnknownSuch liabilities might include liabilities for cleanup or remediation of undisclosed or disclosed environmental conditions, claims of tenants or other persons dealing with prior owners of the properties, tax liabilities, employment-related issues, and accrued but unpaid liabilities whether incurred in the ordinary course of business or otherwise. If the magnitude of such unknown liabilities is high,material or higher than anticipated, either singly or in the aggregate, it could adversely affect our business, financial condition, liquidity and results of operations.

We face intense competition, which may decrease or prevent increases in the occupancy and rental rates of our properties.

We are subject to competition in the leasing of our properties. We compete with numerous developers, owners and operators of retail, restaurant, industrial and office real estate, many of which have greater financial and other resources than us. Many of our competitors own properties similar to ours in the same markets in which our properties are located. If one of our properties is nearing the end of the lease term or becomes vacant and our competitors (which could include funds sponsored by us) offer space at rental rates below current market rates or below the rental rates we currently charge our tenants, we may lose existing or potential tenants and we may be pressured to reduce our rental rates below those we currently charge or to offer substantial rent concessions in order to retain tenants when such tenants’ lease

leases expire or to attract new tenants. In addition, if our competitors sell assets similar to assets we intend to divest in the same markets and/or at valuations below our valuations for comparable assets, we may be unable to divest our assets at all or at favorable pricing or on favorable terms. As a result of these actions by our competitors, our business, financial condition, liquidity and results of operations may be adversely affected.

The value of our real estate investments is subject to risks associated with our real estate assets and with the real estate industry.

Our real estate investments are subject to various risks, fluctuations and cycles in value and demand, many of which are beyond our control. Certain events may decrease our cash available for distribution to our stockholders and unitholders, as well as the value of our properties. These events include, but are not limited to:

adverse changes in international, national or local economic and demographic conditions;

vacancies or our inability to lease space on favorable terms, including possible market pressures to offer tenants rent abatements, tenant improvements, early termination rights or tenant-favorable renewal options;

adverse changes in financial conditions of buyers, sellers and tenants of properties;

inability to collect rent from tenants, or other failures by tenants to perform the obligations under their leases;

competition from other real estate investors, including other real estate operating companies, REITs and institutional investment funds;

reductions in the level of demand for commercial space generally, and freestanding net leased properties specifically, and changes in the relative popularity of our tenants and/or properties;

increases in the supply of freestanding single-tenant properties;

fluctuations in interest rates, which could adversely affect our ability, or the ability of buyers and tenants of our properties, to obtain financing on favorable terms or at all;

increases in expenses, including, but not limited to, insurance costs, labor costs, energy prices, real estate assessments and other taxes and costs of compliance with laws, regulations and governmental policies, all of which have an adverse impact on the rent a tenant may be willing to pay us in order to lease one or more of our properties;

loss of property rights, adverse impacts on our tenants’ business operations and/or increases in tenant vacancies resulting from eminent domain proceedings;

civil unrest, acts of God, including earthquakes, floods, hurricanes and other natural disasters, including extreme weather events from possible future climate change, which may result in uninsured losses, and acts of war or terrorism; and

changes in, and changes in enforcement of, laws, regulations and governmental policies, including, without limitation, health, safety, environmental, zoning and tax laws, governmental fiscal policies and the ADA.

In addition, our properties are subject to the ADA and while our tenants are obligated to comply with the ADA and may be obligated under our leases to pay for the costs associated with compliance with the ADA, if compliance involves expenditures that are greater than anticipated or if tenants fail or are unable to comply, we may be required to incur expenses to bring a property into compliance.

Any or all of these factors could materially adversely affect our results of operations through decreased revenues or increased costs.

Uninsured losses or losses in excess of our insurance coverage could materially adversely affect our financial condition and cash flows, and there can be no assurance as to future costs and the scope of coverage that may be available under insurance policies.

We carry comprehensivecommercial general liability, fire, extended coverage,flood, earthquake, and property and rental loss insurance covering all of the properties in our portfolio under one or more blanket insurance policies with policy specifications, limits and deductibles customarily carried for similar properties. In addition, we carry professional liability and directors’ and officers’ insurance, and cyber liability insurance. We select policy specifications and insured limits that we believe are appropriate and adequate given the relative risk of loss, insurance coverages provided by tenants, the cost of the coverage and industry practice. There can be no assurance, however, that the insured limits on any particular policy will adequately cover an insured loss if one occurs. If any such loss is insured, we may be required to pay a significant deductible on any claim for recovery of such a loss prior to our insurer being obligated to reimburse us for the loss, or the amount of the loss may exceed our coverage for the loss. In addition, we may reduce or discontinue terrorism, earthquake, flood or other insurancecertain coverages on some or all of our properties in the future if the cost of premiums for any of these policies exceeds, in our judgment, the value of the coverage discounted for the risk of loss. Our title insurance policies may not insure for the current aggregate market value of our portfolio, and we do not intend to increase our title insurance coverage as the market value of our portfolio increases.

Further, we do not carry insurance for certain losses, including, but not limited to, losses caused by riots, war or war.nuclear explosions. Certain types of losses may be either uninsurable or not economically insurable, such as losses due to earthquakes,nuclear explosions, riots or acts of war. If we experience a loss that is uninsured or which exceeds policy limits, we could lose the capital invested in

the damaged properties as well as the anticipated future cash flows from those properties. In addition, if the damaged properties are subject to recourse indebtedness, we would continue to be liable for the indebtedness, even if these properties were irreparably damaged. In addition, we carry several different lines of insurance, placed with several large insurance carriers. If any one of these large insurance carriers were to become insolvent, we would be forced to replace the existing insurance coverage with another suitable carrier, and any outstanding claims would be at risk for collection. In such an event, we cannot be certain that we would be able to replace the coverage at similar or otherwise favorable terms. As a result of any of the situations described above, our financial condition and cash flows may be materially and adversely affected.

Our participation in joint ventures creates additional risks as compared to direct real estate investments, and the actions of our joint venture partners could adversely affect our operations or performance.